12/8/2017 Cannes, France http://www.miptv.com http://mipcom.com OTT & Pay TV: Forever Together? Simon Murray Principal Analyst Digital TV Research www.digitaltvresearch.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

12/8/2017Cannes, France

http://www.miptv.com http://mipcom.com

OTT & Pay TV: Forever Together?

Simon Murray

Principal Analyst

Digital TV Research

www.digitaltvresearch.com

Best of friends….for now

Just a couple of years ago, OTT platforms and

pay TV operators were seen as enemies. Now

they are partners.

Netflix is a prime example of this. It has

formed several global distribution

partnerships with some of the best known pay

TV operators.

Its partnerships are not restricted to these

operators, with many local deals in place. For

example, it also has deals with Vodafone in

several countries and Tigo in Latin America.

Digital TV Research estimates that Netflix has

about 150 platform partnerships worldwide.

By contrast, Amazon Prime Video only has

one partnership that we know of – with

Vodafone in India.

Netflix’s global partners

Why they work together

Distribution partnerships with pay TV

operators, retailers, mobile operators and

broadband operators give SVOD platforms

immediate and intimate access to their

subscriber bases.

It also removes billing concerns.

The operators benefit from adding well-

known brands.

Furthermore, they don’t have to negotiate

their own content deals.

The number of pay TV operators launching

their own platforms has fallen considerably in

the last year as more and more partnerships

are formed with SVOD platforms.

How do SVOD platforms succeed in

international markets?

• Supply content in the local language

• Provide locally-produced content

• Produce original content

• Demonstrate subscription fee sensitivity to each

local market

• Take payments in local currency

• Deliver a means of payment other than credit

card

• Form local distribution partnerships with pay TV

operators, retailers, ISPs, telcos and/or mobile

operators.

Stormy weather ahead

Always the best solution?

There are many good reasons for pay TV operators and SVOD platforms to work together. However, sometimes

this does not work and the two parties remain rivals.

Several high profile pay TV operators have their own SVOD platforms. Many of them started before the current

trend for SVOD and pay TV operators to work together.

In many cases, pay TV operators started these SVOD platforms to counter the anticipated rise of the SVOD

platforms. Many pay TV operators also control substantial content rights, so starting their own platforms is a

good way for them further exploit their assets.

However, some pay TV operators have gone even further by bundling their SVOD platforms into their pay TV

packages. So there is no added financial value from the SVOD platforms. Pay TV operators benefit from this as it

enhanced their offer. They soak up any content licensing fees. However, it usually means that they spend less on

original SVOD content.

Taking out the middleman

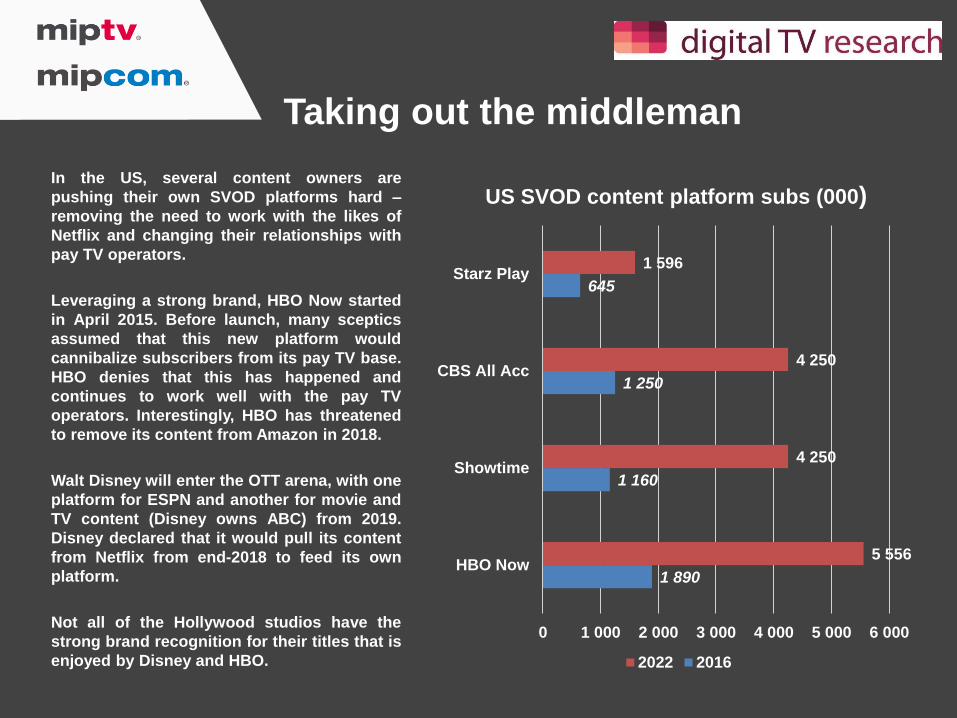

In the US, several content owners are

pushing their own SVOD platforms hard –

removing the need to work with the likes of

Netflix and changing their relationships with

pay TV operators.

Leveraging a strong brand, HBO Now started

in April 2015. Before launch, many sceptics

assumed that this new platform would

cannibalize subscribers from its pay TV base.

HBO denies that this has happened and

continues to work well with the pay TV

operators. Interestingly, HBO has threatened

to remove its content from Amazon in 2018.

Walt Disney will enter the OTT arena, with one

platform for ESPN and another for movie and

TV content (Disney owns ABC) from 2019.

Disney declared that it would pull its content

from Netflix from end-2018 to feed its own

platform.

Not all of the Hollywood studios have the

strong brand recognition for their titles that is

enjoyed by Disney and HBO.

1 890

1 160

1 250

645

5 556

4 250

4 250

1 596

0 1 000 2 000 3 000 4 000 5 000 6 000

HBO Now

Showtime

CBS All Acc

Starz Play

US SVOD content platform subs (000)

2022 2016

The linear channel SVOD threat

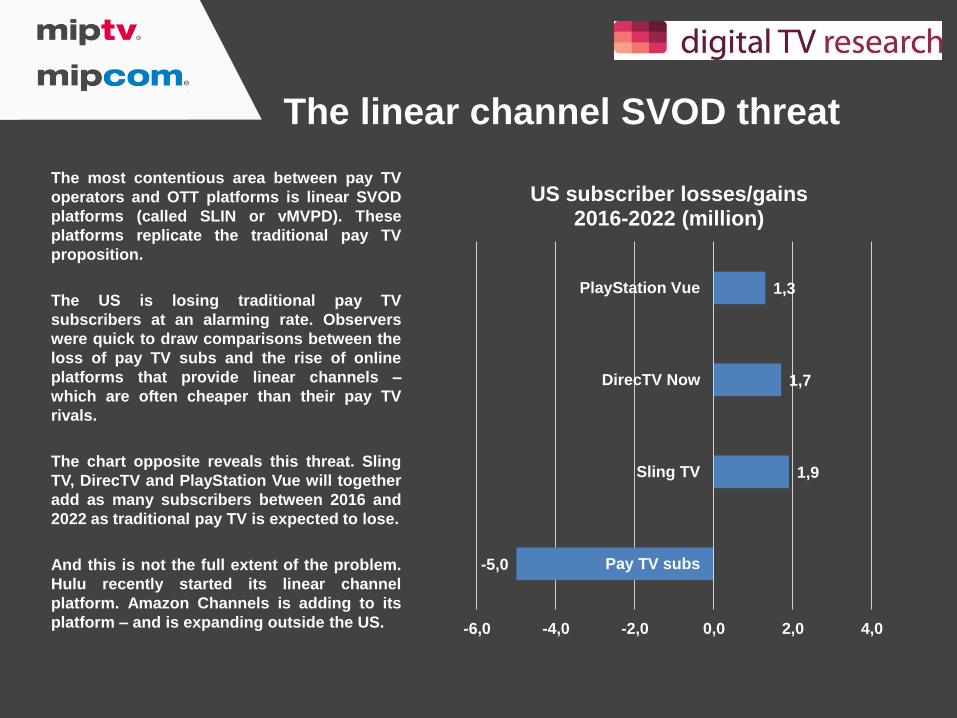

The most contentious area between pay TV

operators and OTT platforms is linear SVOD

platforms (called SLIN or vMVPD). These

platforms replicate the traditional pay TV

proposition.

The US is losing traditional pay TV

subscribers at an alarming rate. Observers

were quick to draw comparisons between the

loss of pay TV subs and the rise of online

platforms that provide linear channels –

which are often cheaper than their pay TV

rivals.

The chart opposite reveals this threat. Sling

TV, DirecTV and PlayStation Vue will together

add as many subscribers between 2016 and

2022 as traditional pay TV is expected to lose.

And this is not the full extent of the problem.

Hulu recently started its linear channel

platform. Amazon Channels is adding to its

platform – and is expanding outside the US.

-5,0

1,9

1,7

1,3

-6,0 -4,0 -2,0 0,0 2,0 4,0

Pay TV subs

Sling TV

DirecTV Now

PlayStation Vue

US subscriber losses/gains 2016-2022 (million)

US pay TV subscriber losses

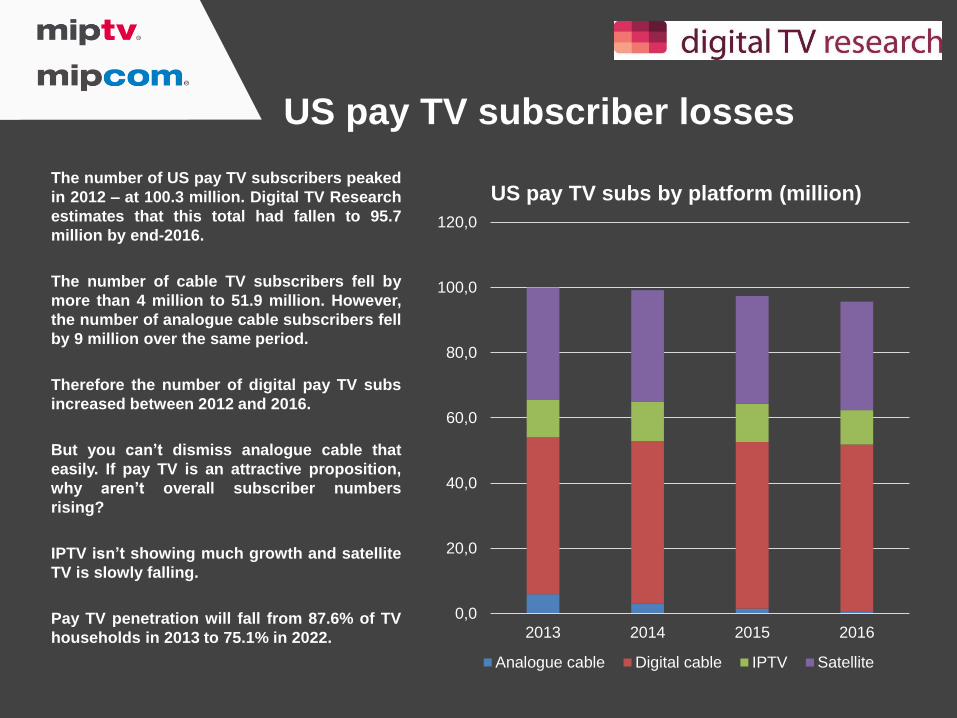

The number of US pay TV subscribers peaked

in 2012 – at 100.3 million. Digital TV Research

estimates that this total had fallen to 95.7

million by end-2016.

The number of cable TV subscribers fell by

more than 4 million to 51.9 million. However,

the number of analogue cable subscribers fell

by 9 million over the same period.

Therefore the number of digital pay TV subs

increased between 2012 and 2016.

But you can’t dismiss analogue cable that

easily. If pay TV is an attractive proposition,

why aren’t overall subscriber numbers

rising?

IPTV isn’t showing much growth and satellite

TV is slowly falling.

Pay TV penetration will fall from 87.6% of TV

households in 2013 to 75.1% in 2022.

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2013 2014 2015 2016

US pay TV subs by platform (million)

Analogue cable Digital cable IPTV Satellite

Amazon Channels: The

biggest threat to pay TV?

Amazon has been credited with disrupting several industries – from book publishing to advertising.

Despite being free to Prime members in 14 countries, Amazon Prime Video is yet to be held responsible

for disrupting the pay TV sector. It has not formed partnerships with local pay TV operators in a similar

way to Netflix. The only partnership announced so far is with Vodafone in India.

However, Amazon Channels could provide a major challenge to the traditional pay TV sector. Amazon

Channels provides Prime subscribers with an la carte option for monthly fees to linear channels, so

subscribers only pay for what they want.

Although some of the channels provided are niche, Amazon has attracted some major players, such as

HBO, Showtime, Starz and Cinemax in the US and Discovery, Eurosport and ITV Hub+ in the UK.

Amazon Channels started in the US as the Streaming Partners Program in late 2015. It expanded to the UK,

Germany and Austria in May 2017.

Online sports scares pay TV

Pay TV operators are also being challenged in one of their strongholds:

premium sports.

Sports streaming is already a big business in the US. MLB.TV was the streaming

pioneer, providing all out-of-market baseball games in its premium pack (from

$113/season) or subscribers can follow one team ($87/season).

Facebook moved into live sports streaming by signing a deal with Major League

Baseball to stream 20 games a season. Facebook also has a deal to screen

esports and Major League Soccer.

Twitter is also in on the act by adding 16 live streaming partners including MLB,

PGA Tour and WNBA.

Amazon screened the first of 11 live Thursday-night NFL games to its global

Prime base in September 2017.

And Disney has promised to launch its ESPN SVOD platform in the US from

2019.

Netflix has historically shied away from live sports – which could be one reason

why pay TV operators are willing to form partnerships with Netflix.

Coming up

roses

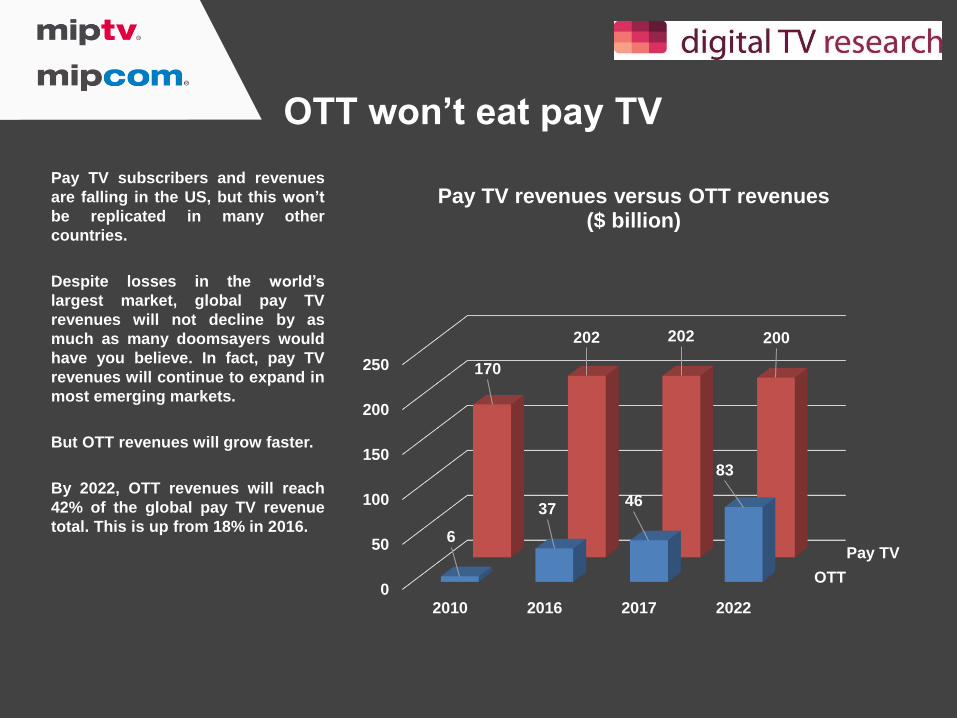

OTT won’t eat pay TV

Pay TV subscribers and revenues

are falling in the US, but this won’t

be replicated in many other

countries.

Despite losses in the world’s

largest market, global pay TV

revenues will not decline by as

much as many doomsayers would

have you believe. In fact, pay TV

revenues will continue to expand in

most emerging markets.

But OTT revenues will grow faster.

By 2022, OTT revenues will reach

42% of the global pay TV revenue

total. This is up from 18% in 2016.

OTT

Pay TV

0

50

100

150

200

250

2010 2016 2017 2022

6

3746

83

170

202 202 200

Pay TV revenues versus OTT revenues ($ billion)

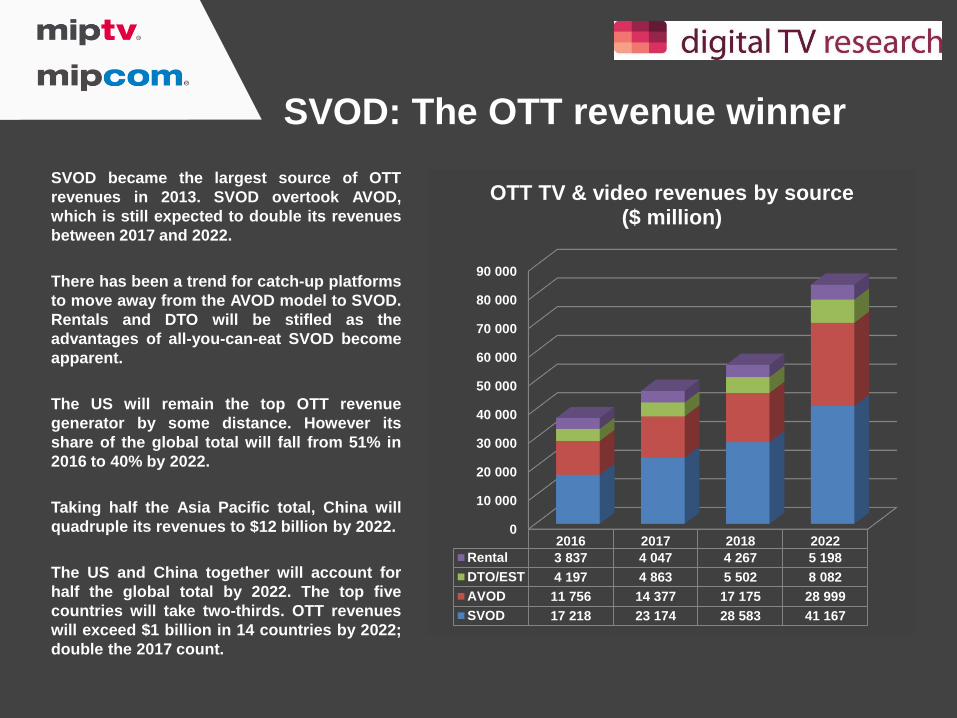

SVOD: The OTT revenue winner

SVOD became the largest source of OTT

revenues in 2013. SVOD overtook AVOD,

which is still expected to double its revenues

between 2017 and 2022.

There has been a trend for catch-up platforms

to move away from the AVOD model to SVOD.

Rentals and DTO will be stifled as the

advantages of all-you-can-eat SVOD become

apparent.

The US will remain the top OTT revenue

generator by some distance. However its

share of the global total will fall from 51% in

2016 to 40% by 2022.

Taking half the Asia Pacific total, China will

quadruple its revenues to $12 billion by 2022.

The US and China together will account for

half the global total by 2022. The top five

countries will take two-thirds. OTT revenues

will exceed $1 billion in 14 countries by 2022;

double the 2017 count.

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

2016 2017 2018 2022

Rental 3 837 4 047 4 267 5 198

DTO/EST 4 197 4 863 5 502 8 082

AVOD 11 756 14 377 17 175 28 999

SVOD 17 218 23 174 28 583 41 167

OTT TV & video revenues by source ($ million)

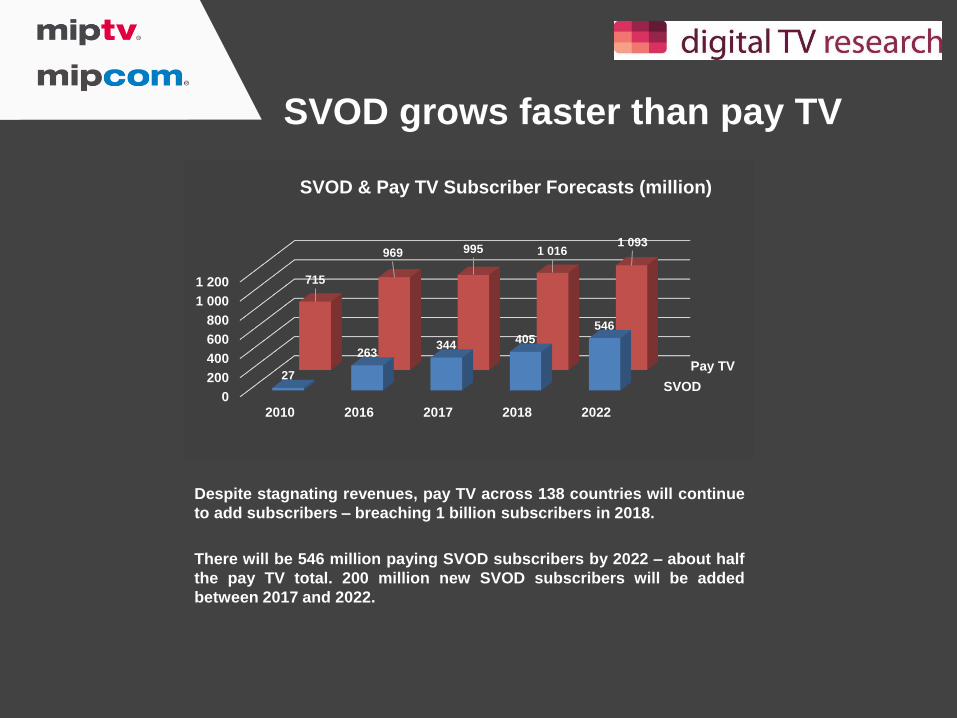

SVOD grows faster than pay TV

Despite stagnating revenues, pay TV across 138 countries will continue

to add subscribers – breaching 1 billion subscribers in 2018.

There will be 546 million paying SVOD subscribers by 2022 – about half

the pay TV total. 200 million new SVOD subscribers will be added

between 2017 and 2022.

SVOD

Pay TV

0

200

400

600

800

1 000

1 200

2010 2016 2017 2018 2022

27

263344

405546

715

969 995 1 0161 093

SVOD & Pay TV Subscriber Forecasts (million)

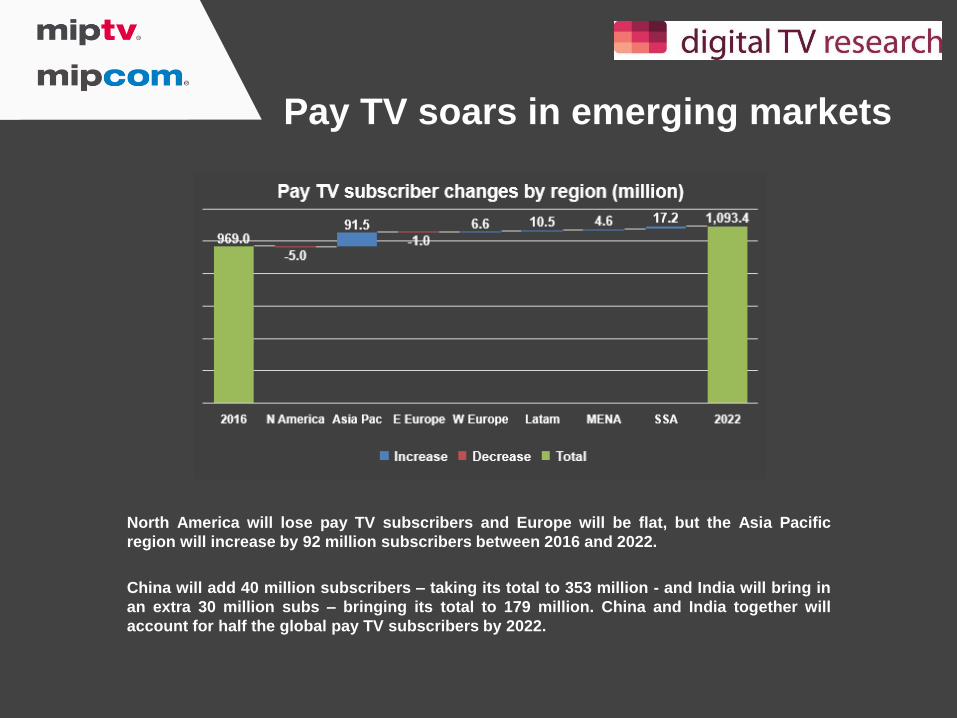

Pay TV soars in emerging markets

North America will lose pay TV subscribers and Europe will be flat, but the Asia Pacific

region will increase by 92 million subscribers between 2016 and 2022.

China will add 40 million subscribers – taking its total to 353 million - and India will bring in

an extra 30 million subs – bringing its total to 179 million. China and India together will

account for half the global pay TV subscribers by 2022.

SVOD: China to catch US soon

The US will still be SVOD subscriber market

leader by 2022, but China will be challenging

for its crown – despite the absence of Netflix

in China.

From the 203 million additions between 2017

and 2022, China will contribute 53 million, the

US 36 million and India 20 million. These

three countries will supply half the world’s

additional subscribers.

These figures are for paying SVOD

subscribers.

Some pay TV operators, especially in Latin

America, Spain and France, have bundled

their SVOD platforms in with their top pay TV

tiers, so these homes are not paying for

SVOD. 124160

86

1396

26

22

26

14

19

92

176

0

100

200

300

400

500

600

2017 2022

SVOD subs by country (million)

USA China India Japan UK Others

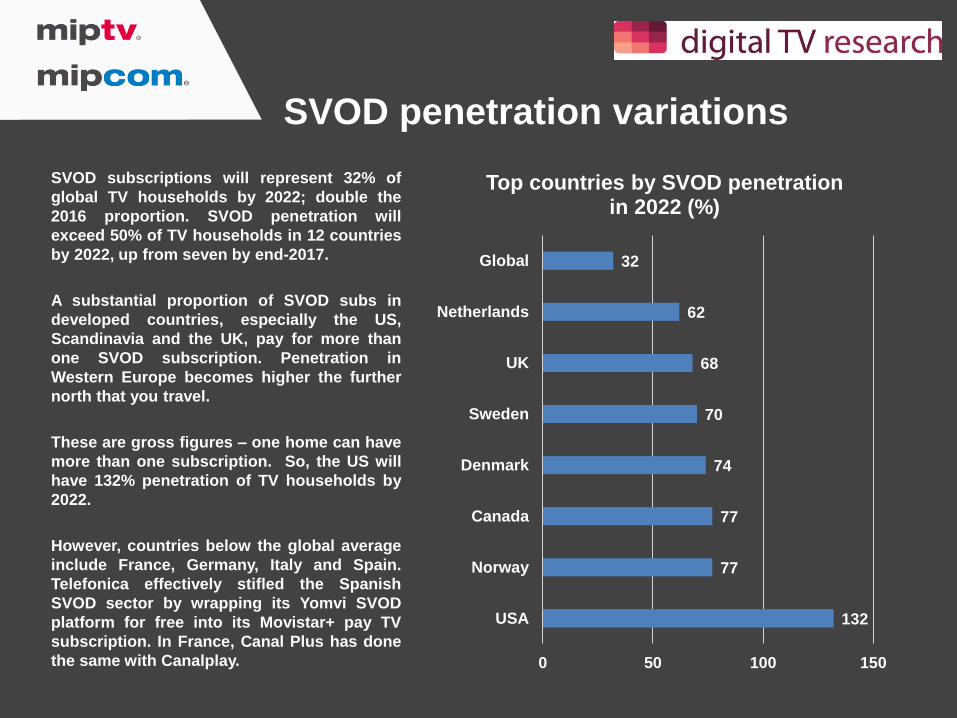

SVOD penetration variations

SVOD subscriptions will represent 32% of

global TV households by 2022; double the

2016 proportion. SVOD penetration will

exceed 50% of TV households in 12 countries

by 2022, up from seven by end-2017.

A substantial proportion of SVOD subs in

developed countries, especially the US,

Scandinavia and the UK, pay for more than

one SVOD subscription. Penetration in

Western Europe becomes higher the further

north that you travel.

These are gross figures – one home can have

more than one subscription. So, the US will

have 132% penetration of TV households by

2022.

However, countries below the global average

include France, Germany, Italy and Spain.

Telefonica effectively stifled the Spanish

SVOD sector by wrapping its Yomvi SVOD

platform for free into its Movistar+ pay TV

subscription. In France, Canal Plus has done

the same with Canalplay.

132

77

77

74

70

68

62

32

0 50 100 150

USA

Norway

Canada

Denmark

Sweden

UK

Netherlands

Global

Top countries by SVOD penetration in 2022 (%)

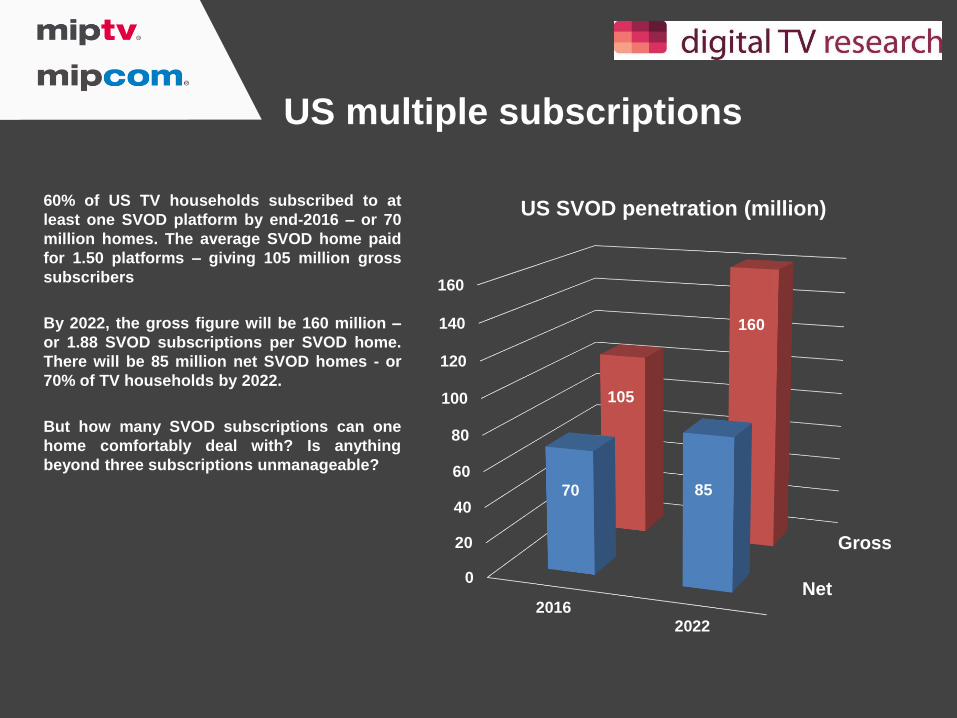

US multiple subscriptions

60% of US TV households subscribed to at

least one SVOD platform by end-2016 – or 70

million homes. The average SVOD home paid

for 1.50 platforms – giving 105 million gross

subscribers

By 2022, the gross figure will be 160 million –

or 1.88 SVOD subscriptions per SVOD home.

There will be 85 million net SVOD homes - or

70% of TV households by 2022.

But how many SVOD subscriptions can one

home comfortably deal with? Is anything

beyond three subscriptions unmanageable?

Net

Gross

0

20

40

60

80

100

120

140

160

20162022

70 85

105

160

US SVOD penetration (million)

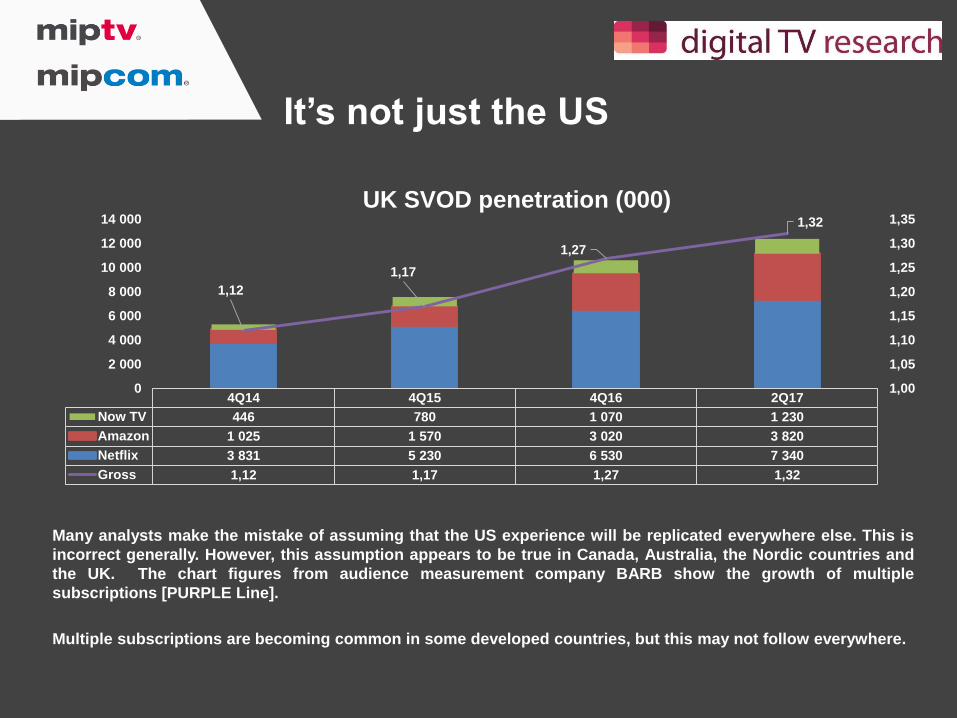

It’s not just the US

Many analysts make the mistake of assuming that the US experience will be replicated everywhere else. This is

incorrect generally. However, this assumption appears to be true in Canada, Australia, the Nordic countries and

the UK. The chart figures from audience measurement company BARB show the growth of multiple

subscriptions [PURPLE Line].

Multiple subscriptions are becoming common in some developed countries, but this may not follow everywhere.

4Q14 4Q15 4Q16 2Q17

Now TV 446 780 1 070 1 230

Amazon 1 025 1 570 3 020 3 820

Netflix 3 831 5 230 6 530 7 340

Gross 1,12 1,17 1,27 1,32

1,12

1,17

1,27

1,32

1,00

1,05

1,10

1,15

1,20

1,25

1,30

1,35

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

UK SVOD penetration (000)

About the Author

This report is brought to you by MIPTV-MIPCOM

MIPTV and MIPCOM are the world’s most important globalmarkets for the TV and digital media industry. They are thekey events for buying and selling, financing and distributingprogrammes in all genres, on all platforms.Together, every 6 months, they form the annual landmarkevents of the entertainment calendar, attracting key industryexecutives, thought-leaders and creative talent from theentire content spectrum to negotiate deals, network and gaininsight.

MIPTV and MIPCOM respectively take place every Apriland October in Cannes, France.

Our websites

http://feeds.feedburner.com/mipworld/ABNFhttp://twitter.com/mip

http://youtube.com/mipmarkets

http://facebook.com/mipmarkets http://linkd.in/mipmarkets

http://flickr.com/photos/mipmarkets

To download our MIPTV / MIPCOM app:

http://bit.ly/mymipapp

To follow us:

http://www.miptv.com http://www.mipcom.com

Simon Murray, Principal Analyst, Digital TV Research

Digital TV Research Limited was established by Simon Murray in January 2011. Simon’s

extensive international industry knowledge and contacts have been built up since he began

covering global media developments in 1988. Simon has authored in excess of 600 forecast

reports.

London-based Digital TV Research publishes more than 20 reports a year, which have been

purchased by over 350 clients. The forecasts and analysis in these reports covers more than 130

countries.

www.digitaltvresearch.com

Twitter @dtvresearch

https://www.linkedin.com/company/digital-tv-research/

Related Documents