ORDINANCE NO. 1506 ORDINANCE APPROVING THE ILLINOIS MUNICIPAL LEAGUE RISK MANAGEMENT ASSOCIATION INSURANCE AGREEMENT FOR THE PERIOD OF J ANUARY 1, 2022 TO JANUARY 1, 2023 WHEREAS, the City of Le banon, St. Clair County, Illino is {hereinafter "City"}, is a non-home rule municipality duly establi shed, existing and operating in accordance with the provisions of the Illinois Municipal Code (Section 5/ 1-1-1 et se q. of Chapter 65 of th e Illinois Compiled Statutes); and WHEREAS , City is a memb er in good standing of the Illinois Municipal Le ague Ri sk Management Association (hereinafter "IMLRMA") and a party to the IMLRM A Inte rgove rnme ntal Coo perat ion Contract; and WHEREAS, City Council has been ful ly apprised of the IMLR MA Agreement fo r the period from January 1.2022 to J an uary 1, 2023 an d WHEREAS, City Council find s it to be in th e best interest of City to approve th e IMLRMA Agreement attached he reto as Exhibit A; and WHEREAS, City Council finds th at the Mayor an d/or Trea surer shou ld be authorize d an d directed to execute any docum en t s necessary to enter the IMLRM A Agreement (Exhibit A). NOW, THEREFORE, BE IT ORDAINED, by the City Council of the City of Lebanon as follows : Section 1. Th e foregoing recitals are incorporated herein as findings of the C ity Cou nci l of the City of Lebanon, Illi noi s. Section 2. The IMLRM A Agree ment is approved. See Exhibit A. Section 3. the Mayor and/ or Treasurer is authorized and directed to execute any docum ents necessa ry to enter the IMLRMA Agreeme nt . See Exhibits A. Section 4. acco rd ance with law. Thi s ordinance shall t ake effect imm ed iately upon its passage and approval in Passe d by the City Council of the City of Leb anon, Illinoi s, approved by the Mayor, an d deposited and fil e d in the Office of th e City Cler k, on th e 13th day of December, 2021, the vote being taken by ayes and noes, an d entere d upon the legislative records, as follows: ATIEST: Lu ann e Ha lper, Cit City of L eba non St. Clair County, Illinois

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ORDINANCE NO. 1506

ORDINANCE APPROVING THE ILLINOIS MUNICIPAL LEAGUE RISK MANAGEMENT ASSOCIATION INSURANCE AGREEMENT FOR THE PERIOD OF

J ANUARY 1, 2022 TO JANUARY 1, 2023

WHEREAS, the City of Le banon, St. Clair County, Illino is {hereinafter "City"}, is a non-home rule municipality duly establi shed, existing and operating in accordance with the provisions of the Illinois Municipal Code (Section 5/ 1-1-1 et se q. of Chapter 65 of th e Illinois Compiled Statutes); and

WHEREAS , City is a memb er in good standing of the Illinoi s Municipal Le ague Ri sk Management Association (hereinafter "IMLRMA") and a party to the IMLRM A Inte rgove rnme ntal Coo perat ion Contract; and

WHEREAS, City Council has been ful ly apprised of the IMLR MA Agreement fo r the period from January 1.2022 to Jan uary 1, 2023 an d

WHEREAS, City Council find s it to be in th e best interest of City to approve th e IMLRMA Agreement attached he reto as Exhibit A; and

WHEREAS, City Council finds th at the Mayor an d/or Trea surer shou ld be authorize d an d directed to execute any docum en t s necessary to enter the IMLRM A Agreement (Exhibit A).

NOW, THEREFORE, BE IT ORDAINED, by the City Council of the City of Lebanon as follows :

Section 1. Th e foregoing recitals are incorporated herein as findings of the City Cou nci l of the City of Lebanon, Illi noi s.

Section 2. The IMLRM A Agree ment is approved. See Exhibit A.

Section 3. the Mayor and/ or Treasurer is authorized and directed to execute any docum ents necessa ry to enter the IMLRMA Agreeme nt . See Exhibits A.

Section 4. acco rd ance with law.

Thi s ordinance shall t ake effect imm ed iately upon its passage and approval in

Passe d by the City Council of the City of Leb anon, Illinoi s, approved by the Mayor, an d deposited and fil e d in the Office of th e City Cler k, on th e 13th day of December, 2021, the vote being taken by ayes and noes, an d entere d upon the legislative records, as follows:

ATIEST:

Lu ann e Ha lper, Cit City of Leba non St. Clair County, Illinois

Exhibit A

Illinois Municipal League Risk 1\1anagement Association

Agreement

and

Proposal for coverage and Risk Management Services

111111ols Murilcipal League

RMA Risk Management Association .

soo East capitol Avenue I PO Box 5180 J Sprlngfteld; !L 62705·5180 Phone#: 217·52S·t220 I Fax#: 217~525·7438 I www.Jmlrma.org

Michelle Davis, RMC Oty of Lebanon 312 W Sathtlouls st Lebanon IL 62254·1561

Customer #312

AGREEMENT

Desctlptloo llilte

11/29/21 2022 annual ccntrlbutlon Invoice 1/1/2022. 1/1/2023 1 % Installment fee 2022 !ML membership dues

November 29, 2021

Amilllnt

$85,811.00

$858.11

$0.00

Send a slg ed copy of this agreement with 1st payment and

INSTALLMENTS

Due Dates 12/17/2021 3/18/2022 6/17/2022 9/16/2022

also a copy of the contribution Invoice with 1st payment.

PAYMENT

Total amount due $86,669,11 · --~~--'!

Quarterly amount due_-"'$=o21"'.;""',66"'7'-''"'28"'--1

#of p<;yments _____ 4"-l Make checks payable to

IML Risk Management Association Payment amount __ -"'$2"'1"',6"'6.:.c7 '"'28=i

Please contact us If you have any questions. Phone: (217) 525·1220

Email .address: lndulrv@tmtrma,org

Illinois Munidpal League

RMA November 29, 202 l

Ms. MfohelleDavis City ofLeha11on

Risk Management Association

312 W8ai11t Louis St Lebanon, IL 62254· 1561

Dear Ms. !:la vis:

The City of Lebanon has requested· and been approved for an installment payment plan for fue 2022 Hlinois Municipal. Leab>ue Risk Mmwgemetlt Association (RMA) annual oonttibutim1, totaling $86,669. 11.

The payment due dates and scheduled amounts for your selected plan are as follows:

12/17/2021 3/lS/2022 6/17/2022 9/16/2022

$21,667.28 $21,667.28 $21,667.28 $21,667.27

Y mt will also receive invoices according to the selected payment plan.

Please sign a copy oftltis letter and send it back to me acknowledging your agreernent to the payments associated wtth your municipality's selected payment plan. Please feel welcome to contact me with a11y questions. Thanks.

fkfiiliji_ City of Leban:: .

Managing Director

500 Ens! Copllol Avenue I r:o. Box 51 ao I Springfield, IL 62705-5180 l Phone: 217.525.1220 ! Fnx: 217 .525.7438 I www.im!rmo.wg

PRIOR ACTS COVERAGE FOR

EMPLOYMENT PRACTICES LIABILITY and EMPLOYEE

BENEFITS LIABILITY

.if\~_:_,_,

*'.;;·''~ The Clty of Lebanon ls. ·requesting Prior Acts protection in the amol;\Jl;~ •. pf $5'0~ OOOl1~ach occurrence/$1,000,000 all occurrences for possible claims that are uo't\ye'~t,:k,P,o.~&\ifor. the continuous time period innnediately prior to the effective date ot11,s?vei~,'rw!;\vltiif!r;1MLRMA during which coverage was provided on a "claims-made basis." "'''''·· '\'.h

;~~~~:~>~· Name of Curreut Carrier: ICRMT

Current Limits: $ 1.000.000 -.:.

·]:.~~' '"4;:.:~ ,/,,:i.;o·

·;\;:!.\ .. ·:.;:;o

The undersigned states there are no KN,,Ci,f,WN'?itiqi'ct~trr~ .. dfili~g this period of prior "Claims Mad.e" coverage that could result in a t)~jm and tha,t I1iive not already been timely filed with the previous Insurance Carrier. ''".(!, f.

·:·. ,:;·. ··:;''

PRlOR ACTS COVERAGE FOR

PUBLIC OFFICIALS LlABlLITY

The City of Lebanon is requesting Prior Acts protection i!J the amount of $1,000,000 each wrongful act!$ tQOQ,000 aggregate for a)! wrongful acts for possible en-ors or o~issions that are not yet known. for the continuous time period immediately prior to the effective:'i:l'4,t~ ofcoverage with IMLRMAduring which coverage was provided on a "claims-made b~J~, 1 '.' ·:,c\i:,, /.('

'{o:\ '"< l'.r., 1;;"'· ,c ,_ ·F

,,,~;;'}'t' ')[:· . .;?

Name of Current Carrier: ICRMT

Curtent Limits; $ 1,000.000

.~j~-•.• ·:.·,'.·,·,.·.y . -. .:~+;:'!-> . '~ :·"· . - ";·;,~;_:: ;;!:;.,~' ~ ~;-~%~1

,,.:-1: ' .• /:>- .fh'> '-; ~:,:\_

Note: The undersigned states there are no ~~~n<ih~lden~··~tring this period ofplior "Claims Made" coverage that could result in a c!~nf'dnc\,th~\,j1ay,,1f1ot already been timely filed with the previous insurance canier. <~,\ · :(;, ··

~f··i'.~-(-. '. ~~ ·-'.,

111.• • ·""'' • • . I L , , ino1s 1v:i.un1c1pa . . eag ue

,,

Mill

R,. ·.k JS,.

Manag.eme,nt Assoclation

Proposal for Coverage

and Risk Management Services*

City of Lebanon

* This proposal of coverage is intended to facilitate an understanding of the coverage provided by RMA. It is not intended to replace or supersede the actual coverage grants. A sample copy of the RMA coverage grants are available upon request.

TABLE OF CONTENTS

Executive Letter ............. : ................................................................................ ; ............. 2

About RMA ..................................................... .' ............................................................. 3

Members ....................................................................................................................... 5

SUMMARY OF COVERAGE

Property ................................................ : .......................... : ................................ 6

Equipment Breakdown ......................... : .................................................................... 7

Portable Equipment .......................................................................................... 8

Crime ............................................................................... ,. ................................. 9

General Liability .............................................................................................. 10

Public Officials Liability ................................................................................... 11

Cyber Liability ................................................................................................. 12

Automobiles ................................................................................................... 13

Workers' Compensation ................................................................................. 14

Public Officials Bonds ...................................................................................... 15

Membership Services Team ...................................................................................... 16

loss Control Team ...................................................................................................... 17

Risk Management & Loss Control Services ................................................................ 18

Claims Information ..................................................................................................... 21

Testimonials ................................................................................................................ 22

Definitions and Exclusions .......................................................................................... 23

Coverage Overview ......................................................................................... ; ........... 24

RMA Pricing Overview ................................................................................................ 25

Notes ........................................................................................................................ 26

' "' '''"''

R MA : ... ,,. . . """' "'"'" """ '" . ~ ' '" "

About the IJ\1L JUsl;. 1'11mrngeiucnt A~sociatlon

~·"~"'"IW .. <'P''~"''"'°"'"'"' ""'a"'""''""'"of«""dm""""''''"m~"'· "'"""-"''l"""S''"'"' """"'~~mo""'""'"°" '""' " ' .M,<C<O ll\0 """'°l' by ""'""" 10 '"'""'' '"' '°"'"''''·'"' """"~°' ,,f1'1< !"ff"' '"" ""'""'"''~ ""'"'" '""~°"

imlrm·a.org

·.-·.- .-~ --~·. :

.-;;-<-:-.-·.-·

The entire staff at the Illinois Municipalleague Risk Management Association (RMA) would liketo·thankthecC:ityof

leb·anon for the bpportunify to- present our history, qualifications and the benefits of our self-insurance pool and risk

management resources ..

The City of Lebanon will direi:tly benefit from the knowledge and experience of our dedicated team. Both the Illinois

Municipal League (IML) and /ML Risk Management Association are the leading experts on Illinois municipal

government and strive to ensure that all munidpalities have access to the information that we-learn from our

members and partners: Weare confident that our proposal will demon.strate how much we care about our members

and the communities they live in, and what we can provide through superior programs and services.

Again, thank you for the opportunity to be of service to your community. Please do not hesitate to contact our office

in Springfield at any time with questions about the pool or general questions that you have about your daily work.

We are here to help our members as often as needed. Thanks.

Managing bi rector ' ...

. ·-:·

:--:'. ;·.,· /.'-i:;--.;,-, .. , ..

. . oisef;itneftt:ke !fdiie$e2r&tcommercii1/ and Jiii'rintlal infdtmatioricontaln~d in'the documents hereby provided are pfopf)etriry, pf(vll~ged and2o.tift~entiarJMLRMA/.&Msiredords. Distribution df;uchtrarfe secret, commercla/or financ/a/ . lnfoffuadh~ is'~~~'hJ~ited anll~dUfd~aJse'cdmp~tirlv~h";.,im to IMLRMA/CCMsl. · · · · · · ·

,_ ·':>': -F .- ,.-·;_ :· ·.-,-;,:

ABOUl"-RMA

In 1981, the Illinois Municipal League (IML) governing board formed the Illinois Municipal League Risk

Management Association (RMA) to stabilize costs and provide liability, property and workers'

compensation coverage needed specifically for municipalities.

Our primary goahis to help city, village and town officials to safeguard their physical, human and

financial assets.

Now in our 40tb year of operation, we have a proven track record of success. We have developed a very

specialized body of knowledge to assist llliilois municipalities in ways not otherwise available through

commercial insurance carriers.

RMA has loyal and long-standing partnerships with our members who value our role in enabling them to

achieve their long-term goals. RMA members recognize the value of our wide-ranging coverage and

services and understand that their contribution is an investment in municip_al protection and service.

RMA BOARD OF DIRECTORS

• MayorTrevor Clatfelter, Sherman; Chair

• Mayor Steve Frattini, Herrin; Vice Chair

• VillagePresidenf'[\(lark A. Hodge, Hopkins Park

• MayorGregiJ1.iry, Loves Park . ' - ·- ' - . :: , .. _,,: ': -_;·-' ._:_ - ... ~

• VIllagePces'identBean Widener, Mahomet

• .;giflage';l'tesident:'.GleJ1n Ryback, Wadsworth

: Vil;fa'.g~'Presi'dent ~h~·en Phipps, Wayne

· .ABOUJ-RMA

• Brad Cole, IML Executive Directo.r; Ex Officio Member

[4

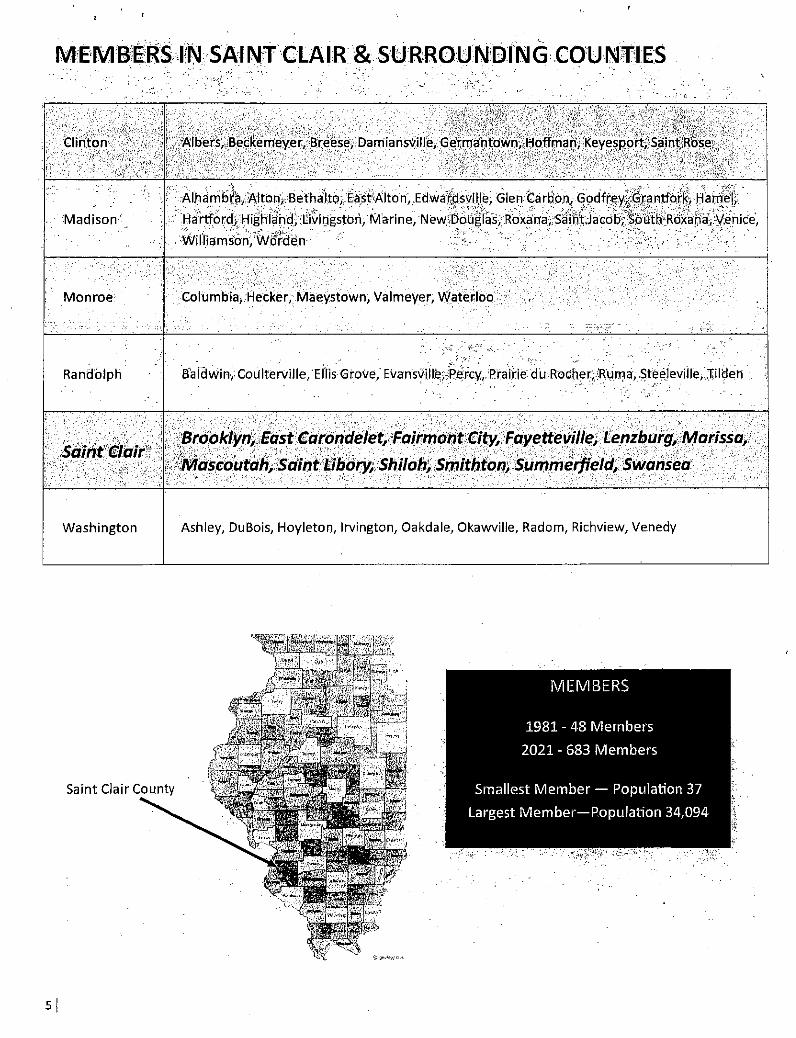

l\ll'EM'B'.E.RS. JN> SAi NT CLAIR & StJRROUN·DfN G .. co·u NtflES ' .. : - ·- . . ' . : :···! ._'. .

,·,,·: .·

· Madison

;· ... ::~_ - ._ - - ·. 'i - • . _:: .•. : ·_. . . . .. .: __ ._ - . , ,,_ - ., __ . ·- -- :.,-,)·-·· ·.:· r::~ '.;, .. ··:,·,~;~;· -• Al.tiamb[a,Alton/Bethalto;. 'Ei(st«Alto n;.:EdwatdSYil,le, Glen.Carboni qo.dfr~yi;GrantfO,r~i Haooe1;: ··

-: • .. : ., ._ ''.'_: .... _· _ -_:~:: _:' .. -'·_: .. ·_ ----~:-: •. , _ ·· •. _ . ··:·':-··:~·:--';_'~·: _ · - ---·. - 0 ·- : ;·- =-. ;·," .. ::~··-:-: ;<:··.:::-;.-:'':_~_}'.''·,:, .. ,'. ·-:·-~'YF. :,\ -_-, . .:~~-\ .. · ···· Rartford;;Highl~[ic))'illviogston; ·Marine, New\Doilglas;.Roxami;:saili~:Jatobi·'.sohth'Rdxai:\a';Y:enke',

. v\iilriam~o~;'wlrd~n ·· ·:: '·'

~-··.

,. i

Monroe C~lumbia, Hecker, Maeystown, Valmeyer, ~ateiloo

Randolph Ba id win, Coulterville, ·Eins Grove, Evansvili~;;F'eicy, Nafrie du .Rocher/Ruma, ~teeJeviile,,Jiltlen ' '-· . ' - · .. · .• . ..... .

... , . -.

Washington Ashley, DuBois, Hoyleton, Irvington, Oakdale, Okawville, Radom, Richview, Venedy

sl

.. -,_·:.

··• Storrli"·sirens

~Memorials

UMITS <--:·

Prope;ty;_;'Auto Pliy:Slcal oaniage -Portable Equipment (c6nibin'edi $30 ·~iinoh :~~Y lo:t~tion, e~ch.·o~cu.r"r~~~e; $2SO'milllon. each occurrence all members

Flood and Earthquake (combined) $76.5.million annual aggregate all members

Business Income/Extra Expense $250,000 annual aggregate (higher limits available upon request)

Valuable Papers/Records and Electronic Media/Records $'50,000 each occurrence

K-9 Officers (police dogs) $15,000 each dog injured or killed In the line of duty

Unmanned aircraft (drones') $2 1 500 each item

Outdoor Trees, Shrubs and Plants $1 1 000 per item/$10,000 per occurrence

DEDUCTIBllES

$500 each occurrence for property claims

$25,000 each occurrence for flood and earthquake claims

FEATURIES • Bullding evaluations -with a few exceptions for unique municipal property, RMA will provide our members with the appropriate values for

their municipal property .. This is a free service we provide to our members.

• RMA does not have any co-Insurance requirements.

• RMA does not exclude coverage for properties that are ln Flood Zone A. Many commercial carrlers exclude items in Flood Zone A which ls

considered to be a higher risk by the Federal Emergency Management Agency (FEMA),

• To suit your munlclpa llty's Individual needs, RMA offers three property coverage valUation options.

Replacement Cost (RC)- cost to repair or replace with like kind and quality,

Please be aware that for a unique pr~perty RMA may not be able_to value it for replacement cost, the member will ~e

asked to provide a value and the replacement cost will be limited to 130% of the value scheduled with RMA.

Actual Cash Value (ACV)- replacement cost less depreciation.

Functional Replacement (FR) - a value between RC and ACV, for example: If a member has an older building that was donated to the

municipality and Is useable, but if a fire destroyed the building, the municipality would replace it with something that niay be of more

practical use.

• Optional endorsements a member may request: (separate limits may apply)

Mine Subsidence Gas or Electric Utility Property Property In the Course of Construction Ordinance or Law Coverage

[6

COVE RAG IE

RMA equipmenfbreakdown cove~age·(alsoknownas boiler & mach:inerY) is for lossesciueto mechanical or

electrical breakdown of equipment. It covers th~ piece ofequipmenta~d any other.damage caused by the

breakdown. Coverage is automatically included for members with property values of less than.$10 million,

unless the member cannot meet all the reinsurance requirements. Members with greater than $10 million

in property values or ifthe member does not meet reinsurance requirements, will be provided an optional

proposal.

UM!TS

Spoilage

Expediting Expenses

Data and Media

Fungus, Wet Rot and Dry Rot

Hazardous Substance

Off Premises Equipment

Extra Expense

Water Damage

Electrical Risk Improvements

DEIJUCTHSLIES

$500 on direct damage claims

$100,000 each occurrence, annual aggregate

$100,000 each occurrence, annual aggregate .

$100,000 each occurrence, annual aggregate

$15,000 per location, annual aggregate •

$100,000 each occurrence, annual aggregate

$500,000 each occurrence, annual aggregate·

$1 million each occurrence, annual aggregate

$100,000 each occurrence, annual aggregate

10% of paid loss not to exceed $10,000 each occurrence

Various other deductibles apply based on the type and size of equipment covered.

FIEATURIE

• This coverage will provide the necessary boiler inspections required by Illinois statute.

7[

COVERAGE RMA portable equipment coverage (also known as inland marine) applies to damage to mobile property (machinery or

equipment not licensed for use on roads or equipment that is easily moved from one location to another) caused by a

covered peril. Covered perils may include: fire, vandalism, flood or earthquake. Examples of portable equipment:

• Street sweepers • Backhoes • Lawnmowers

• Police vehicle equipment - light bars or radios

U!VllTS Property-Auto Physical Damage - Portable Equipment (combined)

Flood and Earthquake (combined)

DEDUCf!BLES $500 each occurrence for portable equipment claims

$25,000 each occurrence forflood and earthquake claims

FEATU!U.:S

• Drones • Tractors

•Fire department turnout gear

$30 million any location, each occurrence;

$250 million each occurrence, all members

$76.5 million annual aggregate, all members

• The member has up to 60 days to report newly acquired portable equipment to'RMA: There.is no additional.·

contribution. for adding-new equipment duting the year.

• Members are. asked to list all portal;ife.equipmentvalued over $J,o'oo. ·All equipment valued''for less than $1,000 is

at.fromatica'ily covered for 10% of the total sch'~c:f~led)ortable eqtiipfnentvaluem up to $150,000. .. .

• RMA.offersthree types of valuations thatirnr members may. choose from:: .

· Replacement Cost (RC) - costto repair orrePi~i;ewithlike kind and quality.dttwillbeHmit~d to ~30%,offhe value on file with RMA.

Actual Cash Value (ACV) - replacement cost less depreciation.

Functional Replacement (FR) - a value between RC and ACV.

[8

SU MM.AR¥ OF.COVERAGE: CR'l'.M.E ·

··~ .-

l!M!T 'CF!rne $500;000 pe(otcurrence

---'f15i:1'1Ji;TIB!.f>-:_ ---------- ---- _ .. __ _

$500 each occurrence for crime claims

H:O.ATURE

• RMA offers comprehensive crime coverage including computer frau_d and funds tra.nsfer fraud:

Computer fraud is the unlawful taking of money, securities or other property through unauthorized

entry into 6r deletion of data from a computer system committed byathir<l-party.

Funds transfer fraud is a fraudulent written or electronic instruction issued to a financial institution

by a third-party <lirecting the financial institution totransfer, pay or deliver money from an account

maintained by a member, without the member's knowledge or consent.

SUM.MA 1 RY OF.COVERAGE: GENERAL LIABILITY

COVERAGE ··,; ''. RM~· g~ ri ~.·t~I) i.a.P.i! ity::a:r.!f:~.o_~-Rr~_tl~ n.~ iV~;_g~ ~7r·a_1~.U~_,~f ]i~\·~.6f i:f-~'~~]~ c:i·8-ae;~~b_q:cHl~Y-' i_ b }~.r.Y~?JJp ~-~rty_:d a~-a ge.1 p ~rs Cina I rnJ u ry a n d a dve rti sing i n jury

caus0~'fz~ru~;~;c,Jg~t~~~{':~1 ~:~,:fir.~1~~(':o~,~i.,~g;·tn1f a~e~r~ orithe'm,Nnihp;~\'~'.!~t~ii~11{;·· ··• · · . · · . . .. · · . ·

TypeS:-.o_f:;g~~ne;t~J'.~iJ'.~,:~gmpr~,hclH'S:!v~-ge_nera,_l?l,ia·bl.i_if(~~,~}'..fil_ed: · .. ,·:·:i ·;, .. {. .. -_~:~.:,·' ..' ) /,:;-. .;;~:- , ; ; _<i;.·;/_'.:.- -.,,,, · -:· ... - ·:·-.:- _ .. · · ·· - .. ..-, , .. , ;'·>:-· · :: - .. >-;-<::]:·.: ,_;'.\":f;'.:,~i·~. _ · ··.;: ·_.:;:_,-. ::·:.,;_ ·-_ r ;·~'.:;::-: -.. ::.<·'. .. >c'.:i''. ;_' _ :- · . .: _ -· · .

: •!faw1~~f8rc~rti~~~Jiabllity · • 1ntentiorial·bulldingferiiov'a'J, ' '"tiq)J'i:>rli~bilitVc-speclal events and host

.. • ~kiifiiiritingliabiiftY • ln~lde~~a[\~~c~iiJ\\~~·1~1~~~~<·' ~:· ~ ~~~i~~d~rit benefit pr~gram administration .. •' ... -,,;·;·'·'·"·" " ' ..

LIMITS General. and Cbmpreh<insive General Liability . $gi·m/Uion each occli'rre'.nce, $16 million ·annu~-J a·g~,~~g~f~· _

Law ER!Orcement and Fire~ghting Liability ·:,.>

EmP.loVme.ni:Practices._,, ..... ____ ..~ -----===~-~=--=::-:·:::-.::":"_~:

· · '$8\liilli~n each .occurren-~e, $15 million annu.al aggregate

-_,.~-~=$:8-:~;i.llion-each~oc~~~-r~n~e;-~-$16:milllon:arinUal:agg(egate:- __

Uquor.Ll~billty-'-speclal eveht; and host

Fire Legal Liability.

Polite Impound Liability

Premises Medic~·! PaVrrie~~-

Limited.POllution Co~~~~~~ ·· ·?· _ .

- ihci\Jdes p0110tf6'~~-caused_by.~~hicle~ or porta.ble equipm~nt, r·aad-_tre~t_me-nt;··~w'rmmrrig_ pa Or t_reat~e~t,: herb.i_cicte and peistid~e app"lica'tiori:and ·water_arfd ·sew_er D""):ieratlonS·

Unmanned Ai~craft (Drone) Liability

Non-Monetary Legal Defense Only

COVID-19 Organic Pathogen Defense Only

DEDUCTIBlE

., . . .. -·. $~ ni)llJ?n each ·actt.irferiCe;.$1 n)ll!ion ann"ua! aggregate

$'1.0o,ooo each6Ccurrenc~,;,$1oo";ooa·.-ann~-a-I aggregate .·~.·._ ,_. . -·- . - . . ' .

:$100 1 0b.o_~-~aCh o~Cur.rence fdr'autom~bli~S ~~d wate.fcraft;

$:so)loO·eaC:h occurrence for any ~C?ther'propei;ty

'$_3 1 000._eaCh'person 1 $1 million each occurrence . .

· $_561 000 each·occurrence, $50,0bo ann~al a"ggr~gate

. . .

$50 1 000 ea.ch occurrence, $50,000 annual aggregate

$25,000 annual aggregate

$50,000 each occurrence/$50,000 annual aggregate

$0 for general liability claims other than liquor liability; $5,000 each loss for all liquor liability claims

FEATURES • RMA offers only occurrence based coverage to our members. Occurrence policies protect members from any covered lncident that

11 occurs" during the coverage period, regardless of when a claim is filed. An occurrence policy will respond to claims that come in - even

after the policy has been canceled - so long as the incident occurred during the period in which coverage was Jn force. In effect, an occurrence po!lcy offers permanent coverage for incidents that occur during the policy period.

• Most other commercial carriers only offer claims-made coverage which pr.ovides for clafms only when both the alleged Incident and the

resulting claim happen di.iring the petiod the coverage is in force. Clalms made to the commercial carrier after the coverage i:erlod ends

will not be covered 1 even If the alleged Incident occurred whl!e the policy was In force. A claims~made policy will cover claims after the

coverage period only if the member purchases extended reporting period or 11 tail 11 coverage.

• Optional endorsements a member may request; (separate limits may apply)

Urban Bus or Van Coverage

Electric Utility Liability

Fireworks General Liability Coverage Liquor Liabi.lity-regular selling of alcohol

[ 10

RMA public officials liability coverage protects the elected, appointed, paid and unpaid employees (other than

professional employees) for their:wrongfulacts, errors and omissions while ·acting on be.half of the member

municipality.

UM ff

Public Officials Liability. $8 million each occurrence, $16 million annual aggregate

Non-Monetary Legal Defense Only $25,000 ann~al aggregate

COVID-.19•0rganic Pathogen·oefenseOnly $50,000 each occUrrence/$50,000 a nnua'laggregate

DEDUCTH3U:;

$0 for public official claims

FE.trn.11u: • Just like our general liability coverage, RMA offers only occurrence based coverage for public officials liability.

COVERAGE

RMA offers coverage for liability associated with cyber losses. The coverage will respond to incidents that involve

breaches of a municipal computer system from either inside or outside the system. RMA will also cover Payment Card

lndu~tl"Y Data SecuriWStand_ard .(PCI or PCI D_SSJpenaltieso[_finesassociated withviolatioos_ofthe_ruJ,es for credit card __ _

compliance.

Ll!VllTS

Cyber Liability Coverage

Included coverages:

$250,000 each occurrence, each member, all applicable coverages

$5 million annual aggregate all members

Privacy and Security Liability and Regulatory (claims-made)

Security Breach Response Coverage (claims-made}

PCI DSS Assessments Coverage (claims-made)

Cyber Extortion Threats (claims-made)

Business Income Loss and Digital Access Restoration (claims-made}-Waiting Period 8 hours

*Claim preparation costs applicable to Business Income Loss - $10,000 each loss

Multimedia Liability (claims-made}

DEDUCTIBLE $5,000 each loss for cyber liability claims

FEATURES

• We understand. that' our members' computer systems may be open to·a wide range of exposures. RMA coverage offers

basic protections that our members need for today's world.

• Highe·r limits (up to $1 million) available upon request.

• Access-to:exclusiveBrit DataSafe·online risk management resources:

> Training· resources - online training courses spedfic in HI.PAA-and-PC!.

> Knowledge center- over 500 online sample policies, guidance on vendor risks and.laws.

> Cyber fitness check - assess your organiza·tions -cyber posture.

> 24/7 breach hotline - experienced professionals available during crucial hours after a breach.

112

su IVir.f/i'ARV" 'GlF';tt>VEttA<i1 E': :~liJtfoMe'alLES _·:,. · : -' ,,:_ - ·~---:::·.,_ 1 • ,., •. ·::·_ '!" ·'::. ::::':·. ·- ~- _ .. ,, :(: ··,.<~::"\'_'<Yn.·1·,, _. - ... ---~·· _.'j __ '.-'-.'\. ·' ·.-.':'··;".':-::::-'~ ·:c:/ >~;_:·''.'.(-~-\.':·:~_,:.'Jo·,,_·

': ·::: -:{ .:;· . .

COVERAGE _:_:_)_i~ -· .. :··.c·_ .. ·: .. st:~f -; -· ._:··:·:./ ... :--·. - · _ . · _ · :;._:.~ -.:.r_·:::}. _ -<~-· :·-:·--,- ::· ·· _. __ ,_ - ._,_: :·;-·· . .

R~'i'\',O.ffers·:two types· oftove rage for. rti~Jiici pal. autortiobi les. ·.~<:;:·.:.'~p·:':f~_:.;_:_,">" ::· •_ :~_:;•'_-'.'·_-:-·''. _ _. ._ __ :_:· ._'.;·:-;" .. ::'<-:··~.'.:;: __ , __ >'· :··.:·: ._ · ___ · ··_-::.:_; _ ........ _, _·.· ._ · : ___ ,.:o:·:-,·; -._ . ·· .. , _ '_ .. ".._ ;,,,_·,,.:':.,.,_,··,. .. _:·· .. _. ... ·_' · .. . ·.·:

1 .. A~tbrilqp)leiliability, ~·covers, al l)iapi)i~;i;frorti owned and non-own.edye ~i.cl~s as w~Jl ~s;hired. a tltbni:qolles 011.fil e .with RM/( cb\ler~g~ is for bodilyinjur;y, prBber'\y cta:in~ge,[iiedical.paymentS ~rldJJnirisured/(Jnderihsuied accidents .• ' .

. - . ' ._. _- - - ., .- ' . ::_ ;,_ ;·.y.;; ·_ '·'·-: - -_, __ · .- . '. ·: _. . :·: -, _. ':- - - '-_ -- . - '. ·:-- -' ·. ;·':"\'~ ---.- '-· . .. ... ,. ' ,_· - . :' - . _- .. - .' . - ·- -: . '·. _.. . - .

2. .·A4tarl1obUe· pbysical dartiage - cover§f~hQi~PrtiPrehen~i~~'or cbllisior\;~la.im~rf'or autam~bil~s'.involved .in accid~nK.The ,. -··- · - - - .. ::!\!.~ ... :-:'. .: ·. _.'· - ._, : _ · _ :,_ .__ . _,;. . ,.;--;,;:.~·,:;;):i,<;·, ._:,:,\if:it;'--~'$~. -- i),;:'.· __ ,_'; ·,·!,\'.: ;:y.-:/•--~,1{:':_ - ,-.,:.'(:·.;·;:\'~;· .<;.::.C-./'-~-, .. :- . : --,_~·:: , .·- _. . - >-. ·; ,_· .. -_ - -. ·. . _'

· · auto mdqjles (nust.be;on a sched u le;.witli RMA:!Alla yt'ornol:Jil."-s:~·r~ v~lu~g,afact4~lc.as.foval~ e (ACV), fir.efightjhg · · ... , . automoblles nfay be valued at replacementcost (RC) or.functional repl~cement(FR). · . . . . .

U~VUllTS - -----

Automobile Liability

Automobile Medical Payments

Uninsured/Und.erinsuted Motorist

:::.::-- -

$8. million each occurrence

$10,000 each person, $1 million each occurrence . . .

$10b;ooo each person, $300~000 each accident

Auto Physical Damage-Property-Portable Equipment (combined) $3Dinillioli any location, each occurrence;

$250 million each occurrence all'membe·rs

$0 for automobile liability claims

$500 each occurrence for automobile physical damage claims

• Members should report the acquisition of new vehicles within 90 days of receipt: There is no additional charge for adding vehicles to coverage lists.

• RMA offers three types of valuations for firefighting vehicles: Replacement Cost (RC)- cost to repair or replace with like kind and quality.

Please be aware that each member will be required to provide a replacement cost value for their

firefighting vehicles which will be limited to 130% of the value scheduled with RMA.

Actual Cash Value (ACV) - replacement cost less depreciation.

Functional Replacement (FR)- a value between RC and ACV:;For example: lfa member has a 1996 fire truck that is

lost in an accident, the member may wish.to replac.e.it with a 2009 fire truck ..

• RMA offers rental reimbursement for affcovered vehitles, The numbernf days allowed for the rental wrn be the lesser

of the number of days to reasonably repair, replace or in case of theft return the vehicle or up to a.maximum of 30 days. RMA will reimburse the lesser of any necessary and actual expenses incurred up to a maximum of $75 per day.

' '

SUMMARY OF COVERAGE: WORKERS' COMPENSATION

COVERAGE····.· · W6.~k_e.rs' comp~h iation·coiterage: wit.h• RMA. includes p rotectio h'Jor·a I I Wo rk-related•i nj tir,iesor diseases, al I

.... :!, .'-"~':\": ···>,:''.'\f;- ... "·\.'"_: .'"·''.· ,,,.-··:·:·,:-·.: ·_. -:.:.-_ .. ··: -----· .-··:::·. _: --. ·.·.,>_·-_--·,'.· . ___ ··_:··_ ... > ~.

compehsationand•.othetcbe,neffts£reggired bythelllihbis.Workers'.ConipensatiptrAct,Jhe .c0Ver9geaJso provides·

~mplOyers iiabifity0hich protects ~mdidye~s from negligence dajms'hroughtby ihjUl'ed•employees cir spouses.

uM1rs. Workers' Compensaii'oh

Employers Lia.bility

Statutory lim'its as provided iii the IL Workers' Compehsation Act(.820 llCS 305) ·

$3 miillon each accident

-----------------------' .. --~---·- ·"-------~-------------------------~-------- --$0 for workers' compensation cla.ims.

FEATURE • .RMA will.ask for.estimated and actual.payroll values from each member, but you will not receive a payroll audit

bill for the difference between the estimated and actual payroll after the coverage year starts.

• RMA medical bill review process provides a 57% savings.

• Nurse case. managers assist your injured employees throughout the medical process, from.answering questions to

guidance through: their treatment plan.

• Access·.to a Workers" Comp Kit® - on line self-evaluation that will .help assess how your loss control program aligns

with best practices and benchmarks losses against your peers. After your evaluation, you can access

presentations, forms and worksheets to help reduce the cost of claims after they have occurred.

[ 14

.s··11 " 1'1\'11•1\·11tA;'0 ""'it,;\'F ···co· t•(1E;RyA·1~··e·· ·p· ·u· 'B'L'I c. '~'F,1:·1 r.1·A· ·L ·B·o·M "'·S' · .v~1,v·l:-IV;l/";\E)f-l:::·U, ·-: - ' .· .. v.~: ' .: ~\3\ •, •. : ·: '• . " .. V.< ··P-: .\..r .- . - J-"~LI .. . ·

COVER.AGE

Illinois statutes (65 ILCS 5/3.1-10-30) require some municipal officials to have a bond to· hold theirposition,

conditioned on the faithful performance of the duties of the office. RMA offers bonds forvarious positions that are

required by statute and the member may add po.sitions that may be required by local c:irdinance,_This coverage is

offered upon request.

UMiTS

Bonds are available for these positions at no additional charge:

Mayor/Village President/Town President

Clerk

Administrator/Manager·

Treasurer

Finance officer/comptroller ··).

:·., -- ;

DEDUCTl'BEE ·~ . ·---- -, . - ' ·-'--« •. f•' ·-- •· - . •

$0 for publfC'bfftd'alho~d•claims .· ·~ .

$50,000 annual aggregate

$50,000 annual agwegate

$50,000 annual aggregate

Greater of$5o,ooo arinual aggregate;orthre~.times:·popufation

$5b;Ooo:annua1·aggtegate .

·_:., ...

·-·'

. , ... :·· .. . ,;· ,.,:

• Our·membersm~·y.add mot<;i m0nicip·al.pqsltio~s tO'the ·above llsi::as required'by:!pcalatilinance;·~i;.;;its.lif up to

$1 million annual·a·ggregate are also:•ail~ilaliile.upon· requestand .for a-modest-additional contribution.·

15 [

Eric Little West Central

Membership Specialist

. ,.;,• .. _.

Chris Korte South & Southeast

Membership Specialist

Aaron Golden North & Northeast

Membership Specialist

MEMBERSHIP SERVICES TEAM

Eric has been an RMA Membership Specialist since 2006.

Eric serves RMA·men:ibers located-In.west central lllinois.

Er.Jc attended .Butler Un iversin' .before: rece·ivi ng,hls .Bachel'Or'.$/.d'e.gre'eJn ·Busl ness-_.Admin istration

from· fi°ffr1oiS-·Cb!lege· ih Jackso.nvHie;,_H~ also has His Illinois .Pr<Yp_e:i±y_ 8i c·asua·1fy-pr~d~c~ris_;llcense as well as Life & Health andVariable·Contra·cts. He· became a·Certinecf Playground Safety Inspector

(CPSI) in•2010,

Prior tO RMA;- Eric·worked for several carriers in the. Insurance ·industry.

Er.ic's governmental experience Includes servlng·as an elected Dffici_al during ·a slX year term·as a

county commissioner in Scott County, Illinois .. He also served on v.3r'ious other loca1 economic

development .and. advisory boards.

·Eric was··born an'd-ra·ised in Winchester, Illinois, where he still liV.~s today with h.is'wlfe, Abbe and

=-=ttleir-=;twcraa ugtlterS; lfftliS· spa re time 1 .-Er1c-=e-rijoys:-oa sRetDal!?Diking.,fisl'li'rl!f"1HYd=s·penarng0 ti me with

family and friends.

Eric can be reached at [email protected] or {217) 836-6569 .

Chris joined the RMA Membership Services Team in July 2017.

Chris selves RMA members located in south and southeastern Illinois.

Chris acquired his Bachelors of Science degree In finance with an Insurance and risk management

concentration from the University of 1111nois.

With 30 years of. Insurance experience, Chris has a varied background in managing risk, marketing,

field underwriting, management, consulting and sales.

Chris grew up in Tuscola, llllnois and moved back home after living and working in different parts of

the country. He enjoys playing go!f and attending ILUNI games in his spare time.

Chris can be reached at [email protected] or (217) 836-6612.

Aaron joined the RMA Membership services Team in February 2017.

Aaron serves north and northeastern llllnois RMA members.

Aaron attended Illinois State.University and has Bachelor's degre.es in·polititaLsC.ieh_ce and

insurance. He has ·also" obtained the CPCU, AIC, and AINS profes.SiOii8'1 insura·nce designations and

holds'an Illinois Property & Casualty Producers license.

Prior to working for RMA, Aaron spent nine years workingJor State,Farm lnsur~nce,as a customer

· service specialist, a quote and bind producer, and a cata~ttOPhe. clai'ms.adjUster.

Aaron grew. up In Danville, Illinois and has moved back h~l)1e .. after. spending the last: Several years in

Okla ho.ma .. In his spare time) Aaron enjoys kayaking, .. worklhg,out/a·rtd'·tollowing.sports.

Aaron can be reached at [email protected] or (217) 474-2919.

[ 16

RISK' M'ANAGEMENT &LOSS CONTROL TEAM

17/

Blaine l<urth Northern Region

loss Control Specialist

.: ,. ' .

·;>." :· ·· ...:>:· ,'. -<-~:/.·: ·. •' Blaihe 'Ii ai'beeri ~roviding·loss'eontroi,~er\iii:es fa;flrYlA m e!ri\~e~s;si'b'Je ,199G.

·· Aftergraduatingfroin.UlinoisState·Un iversity in 199•hvith a:Bacli~lbf'sdeg~ee in occupa'tibnal safety and he.alth, Hlainewo'rked with• conimercia 1 ·and 'r~sidential ccinstrudion and focused on ergonomics.

Blaine's d~ties i ndu de providing·safety ·inspections .and assess'i ng. haz~'rds for

members, providing o 0 -site·safety training, reviewing or assisting'ih'cr~atingwritten safety policies and procedures, conducting park and:playground.in\fp~qtibns;

=;co_3ia_~b111g~wJ1rkczenecsafety•an·d,.Gertifie.MlaggerceE>Urses;,indceonductingcerg9nomic ass_essments.

· In his spare time, Blaine enjoys music and spending ti.me outdoors with.his wife and two daughters.

Blaine can be reached at [email protected] or (217) 841-2445.

Jim has been providing-loss control services to RMA niembers since 2002.

Jim assists members with hazard identification, employee'training$, safety com

mittee development, public liability inspection of parks and sidewalks and devel

opment of workers' compensation cost-savings programs (early return to work).

Jim teaches the Illinois Department of Transportation(IDOT) flag.ger class, assists members with Illinois Department of Labor (IDOL) comPl.iance regarding required trainings. In 2015, Jim implemented a•pollc~ focus· group made lip·Ofsouthern

RMA members, which meets to assist with law enforce:ment rislflna'tfag~ment issues. Jim is also a former risk management coordiMfdr'withtne•Cit,y:of

Mattoon.

Jim .is a graduate of Eastern llli.nois University, is married wlth·fo~r·2~ilaren and lives.in Mattoon. In his spare tiCTle, Jim enjoys officiaifrjghighschooi¥t!ptball

games. .. {· . .

Jim can be reached at [email protected] or (217) 254-9038'

' '

RISK MANAGEIVl'ENT &··LOSS CONTROL SERVICES

RMA PROVIDES PROFESSIONAL R!St< i\llA.NAGEfVIENT AND LOSS

CONTROL SERVICES AT NO ADDITIONAL COST TO YOU

We don't just pay claims.

We.help you prevent claims, reduce costs and keep your employees safe, healthy and productive all while

keeping yciur·community and residents ·Safe.

RMA loss cbhtrol sped a lists bave a combined total ofmore than 40 years ofexperience providiqg loss.

cci.ntrol se~i'~es'for .RMA members. They are·corhmittedto deliveril)g tjualityand eff~ctive.services by

.. workibg clbsely'vvith' your municipalofficials,departinent heads and supervisors"throughoutthe safety

tr~ihing.process:.

' I I I

!j

I :

il l!

i'

:,:

• Accident Investigation and .Prevention. .• Eye Safety

... · ~:~~f~trn j;~,~tno;~;,ps \, .t::,0·t:;1~;[ .J: . . •· 'Co'[lfined;spaceEcitt,y:•.and:;f'!eS:c(ie .. , .

.~: '·· 6~·r1tr,aJ·ot;Haia'rd6u{!~n~r,gylL~~~o:u:it<f~g~ut ··~.· ·o.e:fl;ritfv;ibriVing · ' · · ·· .· , ·•

:;;

. ~·· --.. ' ·.,;< -·.

ONflN'E TRA:iNtNG AVAll.ABlE.ATYOUR EM~lOYEES' CQN~'ENlEl:\fCE . :; .' · 7 ~- . -~/· , _ , '" .. _._ _ , ·, ;. _, _· -:·· · , :• ·-'·:· '· , 1 ::,tJ~~~ .. ,;'.~.::..~;, ..c,:_'.:--:-'.-~~~~;~;; .. : .. , , .:."- ••--==~~.:='~~;-~:cc~r;::f:7.,.:.;.CC•0·: ····--~ .-.:, " •• ----~:::_:.,.~ • __ r;---:_--·-·:-;:_=-::::=:;:~ -

··-~==S'elff,rae~d''offflf:le'tra1ningon·rrn:ire'thai:nfS'O'titlesTree of ci,-~rge and available'24/7from 1 anyJocation.

The:s;~.~durse~ ~iH·also,h el~yqu stayii11Con1~Jia11ce with I ffirrafi,Oe,p•art~e~tof Labor(.fDOt}.regulatory .

req~iFen\ ~n t~)fdr.tb;r?iis like'' B~ck' 1[1Jury P ~e~ention,•~i oodlJorh eiP:~fti oge ~s, Confined s pac.es ;. Excavation/

tre~~fo~'i;sH6ri~g/;~,a1'1 Protection,cHazardiCohimuni.c'atiol),)bb's~fetyAha~Jysis,Lockout/lagout, PPE;·

Respi?atory P~6foc:tfon, SexuaTHa radiment aila:wbrkplace:\lidleiic,i'i'. .

SAMPlE ~l\ll~tOYEE HAND~OOI< This samplehandbqokcanserVe·asa r~source.toassist in creati~g:~rup'd<itingyour current;~mpi(Jymeritrelatedi$6Jiciesand:pr6ceou r~s. AdoPfiogan employee h andboCJlca~d re[at'ed policies hel~~::r;fr'btecvb()th the muniCipalityarid' its employees,

CONTRACf REVIEW Our staff will review contracts before you sign them to point out problematic Jia'bility language that could

put your municipality at risk.

SPECIAL EVENT REV!EV\! Special event reviews will help you recognize and prevent hazards to participants and spectators. Contact our

stafffor.he,Jpful che.cklists and advice.before your next event

;)

',' 19 I

RISK MANAGEMENT & LOSS CONTROL SERVICES

BUl.LDING EVALUATIONS Building evaluation services ensure your municipal properties are adequately covered. RMA has the ability to

evaluate some of your buildings and provide you with proper values.

VOLUNTEER COVERAGE

RMA has partnered with EPIC Insurance Midwest and AIG to provide members with a program to help

provide accident coverage for volunteers if they are injured while performing municipal volunteer work.

-===C:oyernggj11cludes,il<;~Lde[1Jal=mec!ic_al=e.><Jlef'.1$~~,enefi~s~ci_eJl1,1ered=oJJ=either-a-primary,or-excess-basis,_,-----

atcidenfaJdeath and dismembernierit behefits,.we·ekiy accident indemnity benefits and a catastrophic cash . . ··~- ' - . . benefit for paralysis or coma. Coverage is subject to a $500 minimum premium.

PROGRAM DEVELOPtv'lENT ASS.!STAMCIE

RMA loss control specialists are able to help develop inspection programs for facilities, sidewalks, sign age,

water meter lids and .other liability exposures.

TULIP

Access to the Tenant User Liability Insurance Program (TULIP) allows resident users of your municipal

facilities to purchase affordable liability coverage that protects your municipality from their negligent acts.

SERVICE ACTIVITIES

RMA has been covering Illinois municipalities since 1981.

Below are some of the vvays we actively serve our members.

You will not find any other carrier that can match RMA's

service.

19 Conducted on-site member service and loss control visits

• Conducted loss control-specific trainings for thousands of

municipal employees and supervisors on important topics

ranging from accident investigations to IDOL/OSHA

required topics like bloodborne pathogens and PPE, to

defensive driving and public liability issues.

• Covered 2,500+ firefighters, 3,000+ law enforcement and

13,200+ other municipal employees

• Reviewed contracts for risk management and public

liability issues

e Provided access to online loss control training

• Conducted on-site building evaluations

e Conducted several special event reviews

•

•

•

Inspected recreational facilities including parks and

playgrounds

Participated in safety committee meetings

Conducted safety policy reviews

• Participated in safety program development

] 20

· ... >·-.. .. \

m'.ft~~'·'~~~mlt4il~~~~~-~~~ZW'Jf1'i>~4Mft&1~~£W~-Mfl?~~~[t

'COSS NOTICE REPORT' .A4cLAtr.ls.oi;~~!.:wKWo~i1~11s;cor;;•~NsAiioN

.:-,~r~·~t~~;~_::r:·;;'· :::/\)':/= ·:;.:-::-~-;~: .. :.:_ ... :·~,;-- ->-···. ~ M_t,1H!c1PA1Jrt; .

ILLINOIS FORM 4Sf E.MPLOYER'S FiRST REPORT OF INJURY

Date of report · . l Case or file #

. Doing buslness as

Nature of Business or Service SIC Code

P!ets. typ& or print.

Is this a lost workday "'R?

YestJ NoC

Employer's email addl'KS

Coverages in the RMA program are designed to· protect municipal employees, assets and property. We hope you

ne.ver have to use your coverage protection, but accidents and unexpected events do happen. When they do, RMA.

and our claims service professionals are here to help you recover as quickly as possible. We have highly experienced

claims staff and defense atto'rneys who workfor our members to bring aboutpositive solutions.

All RMA members are encouraged to submit claims via the Internet Claims Edge ( iCE~); iCE'" is a state-of-the-art

online reporting tool that allows RMA members to submit claims quickly. By using iCE~, you are able to:

• Report claims immediately and securely through the Internet.

• Use "form filler" to quickly print out any additional forms you will need to complete, such as the IL Form 45.

• Receive an immediate notification of receipt of your claim,

• View, edit or delete initial report forms.

Print a "transaction ~egister" that shows what payments have been ma.de.on behalf of your municipality . .·· . - . . - . :' . ·-· - . ._ '. ;. - .. ' . .,. . .. . ' -._- -. . __ · -- ' -- _;- .. .• .• > . ;

Se~~ch.~ornpleted initiai reporti tiy ~faimai:itJast name, d9t,e.~f loss, repo~.typeor,ih~Utdate.: •

• . . ,., : - _.-. . ··--.· '-.·.:·> ' .. --. .. -.,. . --_ - ---,-,, ·' ,_,;_ - . ' . . • .. _- . - ·•·· .. , ' .

. • . .chmih Un icate\.Vlth'iheEl~ihl adj u;ter: ~rta ~ p~clfid cialhi·arid ~tfai:h'~Hctltiona ( i rifO:ntratfoif; . . - \'~ - . - . - - - >_ ' . ·- .. ,, . '· ' - .. ,·· ' .

. - \ .. ,

21 j

,~ft~~i,~::wv1.s tSf ~ICE ' '. : · ,· , ;Jl\i\t;:RlskMai:iageiTienfAssodaticih

''.'.,'~~.,~~~~~~~::1~>···· . ' ii6lln~:·1866)9ti8-9i36. ·

·., .... ··. f:~,lc'i13$2'f~ss~6~77· ...

_! ,,

TESTIMONIALS

RMAJS THE BEST RISK MANA.GEMENT PROGHAM AVAILABLE FOR IUJNOIS

l\;jtJNldiPA11Tl~~;· . . . '." ·. --.... '• .

But don'i]ust take our wordfbr it-here are some of the things our members have said:

"We have enjoyed tremendous support from the

Illinois Municipal League Risk Management

Association (RMA), and we have always been

impressed with their pricing, administrative support

and proactive risk management practices. But the

frffectesfijf any ihsDTafice'is~nawclaims a re ·h-ahalea:''' '

The RMA team was here immediately to help us assess

the damage and they processed payments for the

repairs quickly and fairly. RMA was a great help."

J. Drew Hoel, City Administrator, City of Tuscola

(Douglas County) population 4,480

"Risk management is most effective when proactive.

RMA loss control partners with us to educate and

train employees, evaluate all city locations and

provide customized safety suggestions. Our RMA loss

control specialist is the city's default risk

management coordinator."

Hal Patton, Mayor, City of Edwardsville

(Madison County) population 26,631

"While the health and safety of our employees is one of

our most important priorities in the Village of Beach Park, sound·fin·ancial management is mission critical. Last

year we tested the market for risk management services and reaffirmed that'the Illinois Municipal League Risk

,Managernent,Associationc(RMA)-willcrnmain,our,fisk- -

management partner. The excellent customer service

provided in the areas of claims processing, training, and

general questions about coverage is essential for the

administration, management and prevention of potential loss to the village. We are pleased to have a relationship

with RMA that is built on trust, transparent

communication and the common goal of excellent public financial stewardship."

John Hucker, Village President, Village of Beach Park

(Lake County), population 13,638

"When it comes to professionals, you need to look no

further than RMA. It is a pleasure to work with such a

reputable organization as yours."

Ricky J. Gattman, Mayor, City of Vandalia

(Fayette County) population 7,042

122

I

I . 1 I'; 'I I I! I I

I!! I .. I j i

I· ·; I !

'' ! '

: i :

. I

I

'

DEFl·NJJilClNS & EXCL.USIONS ,:'

' .,.,

The follbWiilg defiifrtiOh~ applyto't/\e'i:iescription of covered risks set forth in this proposal:

..C,l~ii((~~a!J rnerg .. writj:etj, or.o.tar q0,tiq~fr9m.~11Y p~r:ty 'l,lithfhe int~ntjon of such partyto h~ld the - ··:.(•y",; , ... ,. : .. -,' :· ;<- ···.-. ';.;-... ·, -.,_.:' - •.. --.. ', . ' .'-··-.---_ ·' '· --. • : ,_, - .. ·" ' •· • -' •---' -_ .

· in'ferri,ber responsible for a wrongful act to a person or.p,roperty. . . . · . ·'·- :. ' ~. - . . . - .

2. l'h'et~rm "occurr.ence" means an accident which results in bodily injury or propeftY damage that was not intende

'wtietitnultipleinjuries occur due to t~e same conditions, there is only one occurrence. ''

EXCLUSIONS

•Public transit systems; urbanjlus Ql".llanc(aqv;vehieleJhat•piGl(SCUp;,ffansports'affa oiscna~ges p;~~~~e~~·~t.fegular . ---antlfrequenTl~~;i=-;1;ps-al-;ng~-pfescribed route). Some coveragellVendorsement. ' .·.· ., ' . •' •'

• Me~hanical amus~m~nt devices; autombbiie or motorc\!cle racing ~r rodeos

• Professional liability; unless the professional is an employee of the municipality

• Hospitals, nursing homes, clinics, infirmaries or sanitariums, including nurses' and physidans' medical malpractice

• Pension boards, their trustees, commissioners and public officials

• Electric or gas utility operations and airport operations (electric utility liability available by endorsement)

• Pollution-related damage, including sudden and accidental

• Condemnation or inverse condemnation

• War liability; bodily injury or property damage

• Nuclear liability

• Housing authorities

• Landfills (premises liability is covered)

•Bridges across a navigable body of water- excluded for liability coverage {premises liability is covered)

• Bridges - excluded for property coverage, unless specifically reported by the member and accepted for coverage by

RMA; co~erage is limited to the stated'value and in no event more.than $500,000 per bridge . - . . ' . .,·-' - \ -. .. '"' .. --_ .. , __ .. ,.,, .

. '· .

23 [

. ! )~

COVERAG'E·OVERVIEW .. . . .

MUNICJP,All!V:.City of Lebanon .·:_, .• _· ·. '"::·,~~;· .;:··:.~ ._, .. ~'-,:.-.... ·:, ·. ·, ··.;.- <:., '.

PRESENTED BY: Chris Korte, Membership Specialist

:::~· !~-;.,;,~,~-·~ c~:RR'.::'17 V/1LU:::S/'_ ;«/;·:·s ;-{~\'1.~i '\/,\l~~.}:.:S/L:t\ll:Ts

'

Property

Employee Benefits Lia.bility

(incllJdihg umbrella)

?ciif°;Enfbrcer.Jent&iabilitv·.

1(f~&1uar&~i!i~1Yr,~li~t··. ··•· .· Public Officials Liability

(including umbrella)

.• Empioyment Practic~'s Liabilit;•.

\(iR'dcidi~g·Unibrella} •. .J> ~- ·:> < . ·,'

Automobile Liability

(including umbrella)

.workers' Compensation

(estimated payroll)

\ 11if!Wll:i9~ri liability · ; .,. ~". ~ .. ..... ..~,

Publio Official Bonds

Cyber Liability

1 ... : · ·.s10'·03s'3B5· ' _I •. I

$2,500 deductibie ·

.~,., .. $24;372,026

$500 deductible $50,000 flood/earthquake $25,000 flood/earthquake deductible

deductible

., .. ,., · ..

$383;999

$1,000 deductiole .

$500;000

. $610,9611

$500 deductible

$500,000

$8milli6il/$10million · $8 mllli6n/$16million

$1,000 deductible.. $0 deductible ··-.-·- '

$8 million/$8 million

$2,500 deductible

Claims made

$8million/$16.millldh '

. .. $2,500 decihttiliie

$8 million/$8 million

$2,500 deductible

Claims Made

$8rililli6n/$'8 rtiillio"!"]., · ..

.·•s2,soociJtiu.dtM1~' Claims rviac:le

$8 million per occurrence

$0 deductible

$807,535 (rated on costnew)

• ~;$'1JOOO'ttedtrctibJe: •

$1,610,582

Included under Crime up to the statutory limit or policy.limit,.

whichever is less

$1 mi.Ilion

$5,000 deductible

$8 million/$15 million

$0 deductible

Occurrence

· · ·· $8 ni'illiOn/$16 milffiln 1

. . $O:deductible ;· . - ~ !

$8 million/$16 million'

$0 deductible

Occurrence

'$8·m illion/$16 mil lion· .

·.·· $Odeductihle

occ~·rren~e $8 million per occurrence

$0 deductible

· §.:rno;732 (rated on:AC\I) ·

· :$soo·.d~d uctibl'e

$1,610,582

···, ·$3 .. million .. ' ,_ . ~· . . ~

$50,000 each Village President,

Clerk and Treasurer

·• $24'-372025 : . ~ .· ··:I . . .I . -

$500 deduc):ible

$250,000 i

$5,000 deductible

j 24

•;·' : !"

.. / ~ (

.;:

i '.·1 'i ii ~I I 'I i !

I I

'

CITY OF LEBANON RMA PRICING OVERVIEW:''· .. ···

COV:ERAGE,EF-FEC11tVE:.oeceniber1;:ZD2l .. , ··

t7';'-'-:;'.\if-~;:;,,.::;:!,:,~';'' '\"'] 0 ..,f'-1'<ki ~-c, /c!~-"yc<''" '~~' ;~•;;.'·"~:--"1,'\':~•~,~~~' ',~

!!Nor;i:ilal Guatanfeed Cost RMll:Armu'al. ednti:ibution . ·:·.,'.c:- J,., .•. _., ',_ .>,:·; ' -

i MJ!l'!AM~i·~i~k&har;Jng Price;Optibk i·•.C .· . ' -· ' . .· 1:-··,,

:· >,x,; .. ;, .-·. '":.· .. :·.,· -·," . -.

.. ·· M::lximu:nY'.Confributibn:

' (/~~iod)hgiJiifie S~b;id~hce and Ordinance or Law) .

. Portahl~ Equipment

·(~i1ntreas~d'timit·otssoo,ooo)

Genera!Uability (Including .Law.Enforcement & Public Officials Liability)

A:utbmo'~;fe l::ia'bility

Automobile Physical Damage --~, ····-'/'.

··w.arckers'Compensation '. . ·,/":'.'"!."-: .• .. , ... - ' . -~--~, ... ,. ;,

·'''.'':1:··-

Public Official BOnds ,__ ;; ~-;-,: ' '_",~, "

,E,qdipmentBreakdown.· c.<-··- ., ,_. . . . '-"-' ·-·'- ... ,

*increased Cyber Limits to $1,000,000 (12/1/21-1/1/22)

*subject.to reinsurance approval

· .•. , -·-'·- .

•\

... ,.

.. -,'

· RMA C'ONTRIBIJTION· _ ... ·-. ~ - - ' .

$36;1dl

.$762'

$3,750 '

'$27,649

$1,041 . ~··' - ;., --. - .

. ssc?.;~14,1

lncJlicted .

' $'4~509 ' •• • • •. ;.- ·~ '• I ~,-,- C . • "-,.{ ··;'~ _;, - ' •

Included .

1 Ate~s~'note'that.•we·do not.have a.quoteforthe .. increadedcyber/imits pasf.1;A1fQ'Qito 1 shareat ,thJ~·tirfJe:,rJn?e:r:eceived,.we. willpro~idethjsadditional,quote•tq~ou,. · .. ·· ... · . . .

*Norrnai Gu~rariteed Cost RMA Annual·Corttdhlition . ' ....

I fQ/Jqte.subjecFt6·reinsuranceacceptance ' . -,_ ' - .

./ >

• i _(1

Option to participate in the RMA's MIN/MAX risk-sharing program. The Min/Max program

enables a member municipality to share in the .financial results (success or failure) of their

individual claim experience.

- - - ----"--··---·. ---- ---

- - ....

By. accepting the Min/Max prbpbs·~ 1j·the'·Cit~ ~fteba'hohag,re,es to pay tli"e;mihltnum

contribution. amou ntof $12'4;s2s. 1f paidJo§~Js,exceetftne ~lhirnu rn:loss furfd of$84, 772, . - ,. - ' -.' .. - _,. - . ' .. -·- . - -·- -· -- . ~ - -· - " _. ' - .

'the dty oflebahon·agre~sto pay alf losses 1 '.ff6liarf6r'doH<lr,up'tothe'rfi~xi~~m ·

~::~t.~:t;~~~t!~~~~~~~:~t~:M~~~d::~:~~l:i~~~:,. ,·Mbt~.a~taikonthi~]Cipfton.andfth~·Joter'itiat~handal benefits wil I be proitideif~poh request. · -- : .. . .· .. ·'- __ _._ ,_ . . .

#2) Optional Prior Acts Coverage for Public Officials Liability,

Employment Practices Liability, and Employee Benefits

Liability

#3) 1% Early Pay Renewal Discount

.;/.:.

By paying your renewal contribution approximately 30 days

prior to the annual due date, you receive an additional .savings

of 1% off your annual contribution. (Contribution must be

paid in full to receive the discount.)

9/17/2021

$7,174

. -$1,394.85

l.lllnois Municipi>f L~a.gue

RMA Risk Management Asso¢iiltkm

5 Prooertv losses of $5,000 each

5 General Liabil~v losses of $10,000 each

2 Public Officials' Liability losses of $25,000 each

2 Workers' Comoensation losses of $200,000 each

Total additional amount you will incur above your initial contributlonfpremium for the coverage period

I

FAQs , DEDUCTIBLES AND C~INSURANCE

$2,500 $5 000 $5,000

$2,500 $5,000 $25,000

$0 $5,000 $25,000

$0 $2,000 $10,000

$0 $2,000 $10,000

$5,000 $19,000 $75,000

'i !i

$5,obo i

$25,000 I I

$50,000

$20,000 ;i

$20,000 I

$120,opo

$5,000 $5,000

$25,000 $25,000

$50,000 $50,000

$50,000 $50,000

$50,000 I $100.000 I

$180,000 I $230,000 I

Amount: The higher the deductible, the less you may pay up-front, but the more you will incur for the losses. you have.

$5,000

$25,000

$50,000

$50,000

$200,000

$330,000

Lines of coverage: RMA's deductibles apply to property, inland marine, and auto physical damage coverage~. Some carrier$ include or require deductibles for other lines of coverage, such ai; g1meral liability, employment practices liability, law enforcement liability, auto liability, and Workers' Compensation, umbrella and excess. For purposes of this comparison. we are using RMA deductibles and a~suming that the comparing carrier has deductibles for all lines and has deductibles availaple for all amounts shown.

Expected number of losses: It's tempting to acc;:ept high deduc;:tibles when you se<;> what your up-front savings can be. However, you should estimat<;> the number of fosses you're likely to have and bUdQet for the deductible amounts you will incur and add tho~+ amounts to the UP.-front Costs to get a true picture of what you could ultimately pay throughout the year. Keep in mind that you can't predict the null]ber of claims you have. If you actually have fewer claims than you thought, thafs great But if you under.estimate the number of claims, you will incur additional deductible costs later.

Your loss control efforts: If you choose higher deductibles, you should mak.e sure that the carrier offers you quality loss eontrol services to help you reduce the number of claims you'll have and minimize their severity. Check to see if the costs for the loss co~trol services are included in the quote and budget accordingly. Also ask about the quality of the loss control services.

RMA's $500 deductibles are !!Oother way that we help you achieve budg~t stability.

Form ri;vised 1012018 FAQs-Deductibles and Coinsurance f Page 1 of 2

Ullrto1$ Mu!\l~ipal L~t'!~ue FAQs RMA Risk

Ml!nag~m~nt As$Ottiatfurr DEDUCTIBLES AND C(i)INSURANCE

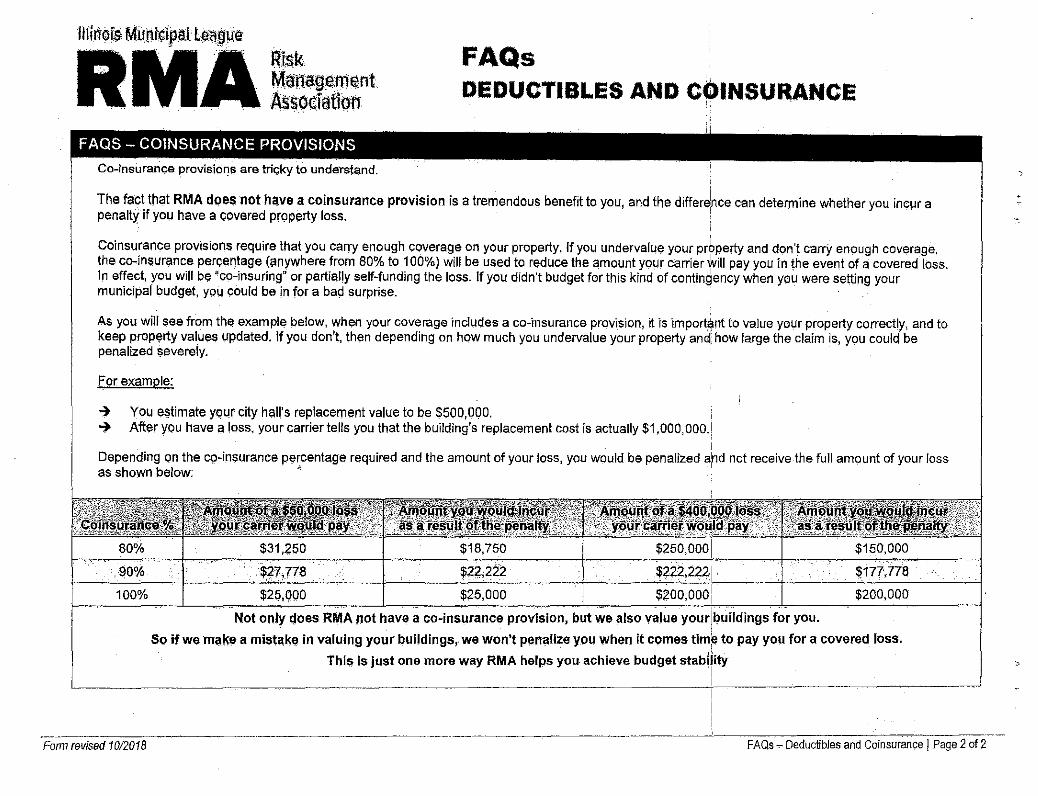

Co-insuran~e provisiol'}~ are tric;-ky to understand.

The fact tnat RMA does not have a coinsurance provision is a tremendous benefit to you, and the differ~nce can determine whether you incµr a penalty if you have a covered property loss. ·

Coinsurance provisions require that you carry enough coverage on your property. If you undervalu<;i your prbperty and don't carry enough coverage, the co-insurance percentage (anywhere from 80% to 100%) will be used to r11duce the amount your carrier Will pay you in the event of a covered loss. In effec~ you will b<;i 'co-insuring' or partially self-funding the loss. If you didn't budget for this kind of contlnijency when you were setting your municipal budget, you could be in for a bap surprise. ·

As you will see from thE! example below, when your coverage includes a co-insurance provision, tt is important to value your property correctly, and to keep property valu~ updated. If you don't, then depending on how much you undervalue your property an di how large the claim is, you coulq be penalized severely.

For example:

~ You estimate your city hall's replacement value to l)e $500,000. ~ After you have a loss, your carrier tells you that the building's replacement cost is actually $1,000,000.i

i

Depending on the co-in$Urance percentage required and the amount of your loss, you would be penalized aind not receive the full amount of your loss as shown below '

~(f\tSi~~~iJll~J~~\~?~~'.ltlf~ltW~"·'~ 80% $31,zso $18,750 $250,oool $150,000

. 90% •· .. •· . .... . .. $27,778 $2f,222 $?2f,222l 1)177,778

100% I $25,ooo I $25,ooo I $20o,ooq I I $200,000

Not only ooes RMA not have a co-insurance provision, but ~e also va.lue you~]tmildings for you. ' i

So if we m<1~e a mist11ke in valuing your buildings, we won't pen;dize you when it comes tin\~ to pay you for a covered loss. ,, This is just one more way RMA helps you achieve budget stabliity

. I

I

--------------··-----Form revised 1012018 FAQs~ Deductibles and Coinsural1ce I Page 2 of 2

.,

llli110~.Muni~ipal·1;¢~~µe

•R.. · .. •.·.M .. ·· .. ·.· · .. ·... .A' .. · .. ~~~agement As •. f > . sa<::1a 1011

Claims-made vs. Occurrence-based Liability Coverages

As public officials, it is important to understand both claims-made coverage and occurrence-based coverage when considering quotes from other insurance providers. Don't assume that coverage under claims-made coverage is the same as coverage under an occurrence-based coverage, even if the limits are identical. The decision to accept claims-made coverage is a gamble your municipality may not want to take.

OCCURRENCE-BASED COVERAGE

The Illinois Municipal League Risk Management Association (RMA) provid·es occurrence-based liability

coverage for public officials. Some features of occurrence-based coverage include:

a. Coverage continues even after the policy has ended. In other words, an occurrence-based policy pays

for claims that happen during the policy period- regardless of when the claim/suit is filed. For

example, if a covered incident occurred during your RMA 2020 coverage year, but the claim/suit

wasn't filed until several years later, the occurrence-based coverage would allow for coverage of that

claim/suit.

b. There are no hidden costs. Occurrence-based coverage is a fixed cost. For example, when you pay the

2020 contribution for RMA's occurrence-based coverages, you won't have to pay more if a claim is

discovered later.

c. You can file a claim on coverages years after they expire for an incident that occurred when they were

active-.

ClAIMS·MADE COVERAGE

Other insurance providers write liability coverages on a claims-made basis. Some features of claims-made

coverage include:·

a. Coverage is available only during the policy period. There is only coverage for claims filed and

reported during the policy period. If you have an incident in 2020 but the claim/lawsuit Isn't filed until

2022, there is no coverage for the claim/suit under the 2020 policy.

b. There is no guaranteed continued insurability. With claims-made coverage, once the policy ends

and you stop paying prem.iums, your coverage ends. You nm the risk of not being covered for a

potential claim because it was not discovered until after the policy expired.

Fonn revised 1112019 Claims-made vs Occurrence-based Liability Coverage I Page 1 of 2

, \ , .. .f• '

c. Coverage gaps may occur. It's difficult to cancel a claims-made policy without having possible

coverage gaps unless you have an unlimite<f or full extended reporting period .. Unfortunately; a 90-

day, 1-yea·r or even 5-year extended reporting period is simply not enough on public officials' liability

incidents. In addition, you must make sure that the language of the extended reporting period

doesn't limit you to claims that were reported during the policy period or within 60- or 90-days of its

expiration.

d. Quotes that include claims-made coverages generally cost less up front because claims-made

coverages provide less protection and are therefore less expensive. The cost increases over a period

of several· years because the chance for reporting a claim increases.

e. There are hidden costs that aren't explained in the initial quote. If your municipality changes providers,

if the provider doesn't renew your coverage or if the provider stops writing municipal policies, you -,;.;-u1a n;;e'dt~buv an e](tend~d reporting p~riod endors~~~~t. u~t;,t;,;~ate!Y:-extended r;porti~~ periods are often limited, and the cost to purchase unlimited or full extended reporting period

coverage can be 200% to 300% of your annual premium. Another option is to purchase "prior acts

coverage" from a new provider with a retroactive date to the day you first started the claims-made

coverage policy; RMA offers "prior acts coverage" as an option to new members.

COMPARING TllE COSTS OF Cl.AIMS-MADE VS. OCCURRENCE-BASED COVERAGE

It's very difficult to adequately compare the value of two quotes when one insurance provider offers claims

made coverage and the other offers occurrence-based coverage.

In order to be as protected as possible, you should require all quotes to be submitted using occurrence-based

coverage only.

However, if a provider can't or won't quote occurrence-based coverage, ask for the cosf of an unlimited or full

extended reporting period. However, doing so will not provide the same kind of protection as occurrence

based coverage.

In summary, claims-made policies. provide far less coverage than occurrence-based policies. Public officials

should always insist that any carrier provide them with occurrence-based liability coverage; RMA offers

occurrence-based liability coverage on all policies.

Form revised 1112019 Claims-made vs Occurrence-based Liability Coverage I Page 2 of 2

'"

Related Documents