• • • Variable Direction of risk 6 months Comment Cash rate Two factors will influence the RBA: labour market strength and whether the recent financial market volatility results in weaker global and domestic demand. The past two jobs numbers have been weak, although this followed an extended run of strength. The global data is mixed, but the domestic economy is doing Ok. Of more concern is that some forward-looking indicators (building approvals and capex) suggest weakness as we enter the second half of the year. Given the risks, we are expecting two 25bp rate cuts by year-end. 90-day bank bills Bill rates are currently about right given the near-term risks for the cash rate. As we progress through the year, bill yields are likely to decline as the cash rate is reduced. 3-year swap Three-year swap yields have declined in line with the increase in financial market volatility. A modest further fall is likely in the second half of the year as financial markets price in imminent rate cuts. 5-year swap There also remains some potential for longer-term swap yields to fall further in line with lower short-term yields and heightened global financial market volatility. AUS/USD The $A has stabilized in the early 70c range reflecting the recent rebound in commodity prices and an extended run of stronger economic data. Commodity prices are heading lower and domestic interest rates will likely decline further. This means a further fall in the $A is likely in 2016, most significantly against the Euro and the yen.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

•

•

•

Variable Direction

of risk 6

months

Comment

Cash rate Two factors will influence the RBA: labour market strength and

whether the recent financial market volatility results in weaker global

and domestic demand. The past two jobs numbers have been weak,

although this followed an extended run of strength. The global data is

mixed, but the domestic economy is doing Ok. Of more concern is

that some forward-looking indicators (building approvals and capex)

suggest weakness as we enter the second half of the year. Given

the risks, we are expecting two 25bp rate cuts by year-end.90-day bank bills Bill rates are currently about right given the near-term risks for the

cash rate. As we progress through the year, bill yields are likely to

decline as the cash rate is reduced.3-year swap Three-year swap yields have declined in line with the increase in

financial market volatility. A modest further fall is likely in the second

half of the year as financial markets price in imminent rate cuts. 5-year swap There also remains some potential for longer-term swap yields to fall

further in line with lower short-term yields and heightened global

financial market volatility. AUS/USD The $A has stabilized in the early 70c range reflecting the recent

rebound in commodity prices and an extended run of stronger

economic data. Commodity prices are heading lower and domestic

interest rates will likely decline further. This means a further fall in

the $A is likely in 2016, most significantly against the Euro and the

yen.

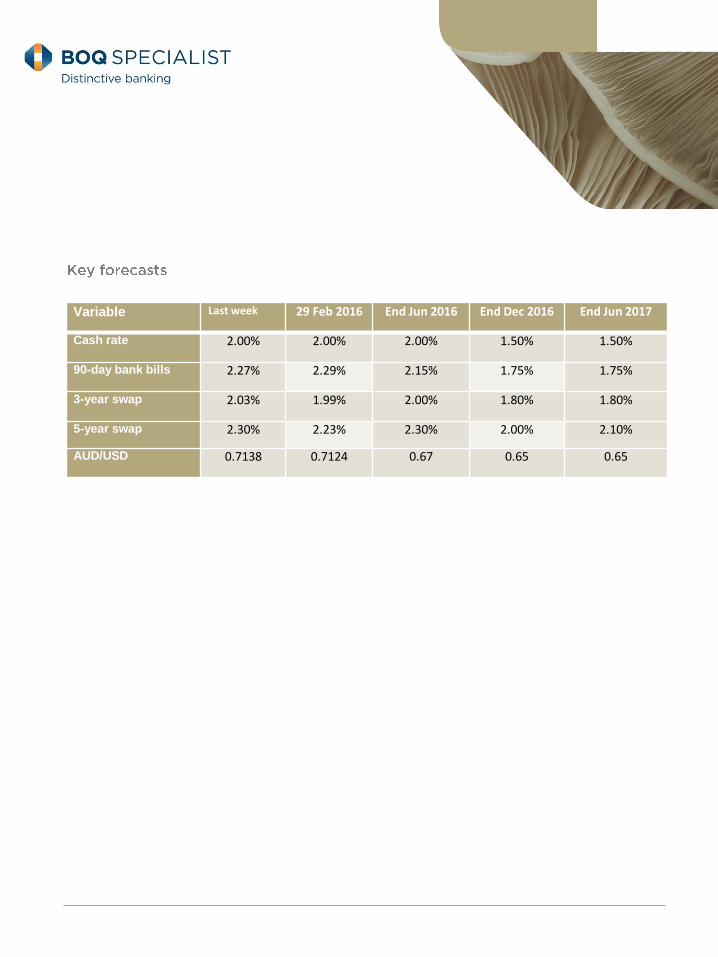

Variable Last week 29 Feb 2016 End Jun 2016 End Dec 2016 End Jun 2017

Cash rate 2.00% 2.00% 2.00% 1.50% 1.50%

90-day bank bills 2.27% 2.29% 2.15% 1.75% 1.75%

3-year swap 2.03% 1.99% 2.00% 1.80% 1.80%

5-year swap 2.30% 2.23% 2.30% 2.00% 2.10%

AUD/USD 0.7138 0.7124 0.67 0.65 0.65

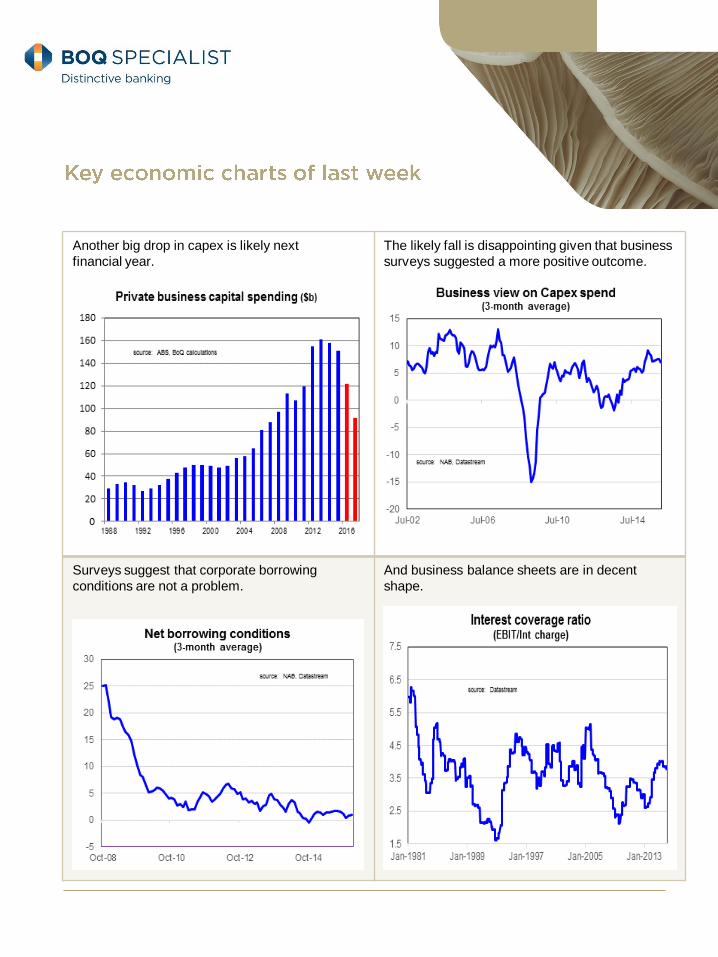

Another big drop in capex is likely next

financial year.

The likely fall is disappointing given that business

surveys suggested a more positive outcome.

Surveys suggest that corporate borrowing

conditions are not a problem.

And business balance sheets are in decent

shape.

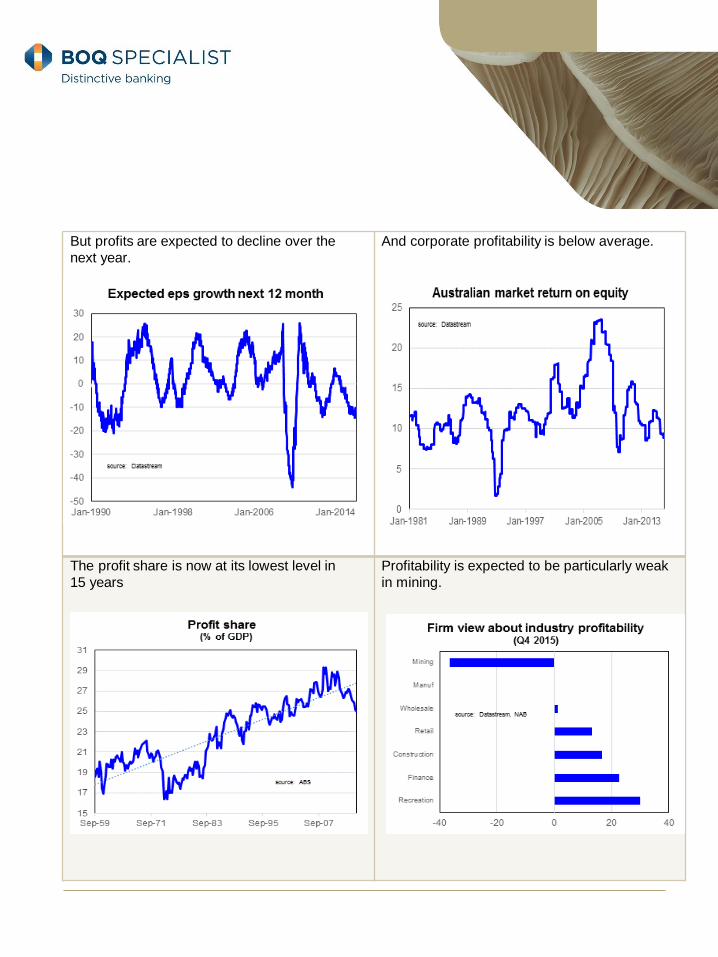

But profits are expected to decline over the

next year.

And corporate profitability is below average.

The profit share is now at its lowest level in

15 years

Profitability is expected to be particularly weak

in mining.

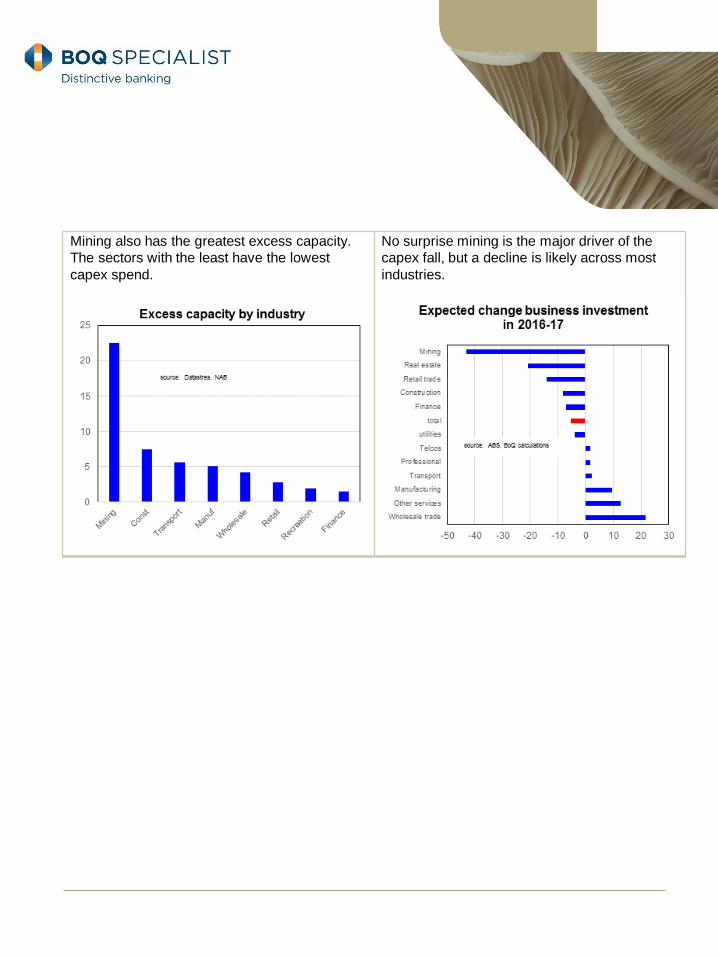

Mining also has the greatest excess capacity.

The sectors with the least have the lowest

capex spend.

No surprise mining is the major driver of the

capex fall, but a decline is likely across most

industries.

Economic and Market Analysis

NSW Peter Munckton 0439 310 837 [email protected]

Financial Markets

QLD / WA David Abbott 07 3212 3049 [email protected]

NSW/VIC Nigel Hodgson 0416 180 087 [email protected]

Trade Finance

QLD Steve Klinakis 0417 658 348 [email protected]

NSW Lloyd Guy 0467 798 132 [email protected]

VIC Ray Buxton 0427 049 430 [email protected]

WA Andrew Opie 0481 008 924 [email protected]

Corporate Banking

QLD Doug Snell 0414 887 659 [email protected]

NSW Jason Mares 0413 013 349 [email protected]

VIC Darryn Cahill 0411 080 985 [email protected]

WA Michael Storer 0438 456 834 [email protected]

Agribusiness

Tim Pryor 0407 754 535 [email protected]

Gerard (Ged) Thom 0477 341 424 [email protected]

Business Banking

QLD Leo Hawker 0418 228 071 [email protected]

Property

QLD Warren Bobbermien 07 3212 3510

NSW Glenn Hilleard 02 8222 8332

WA Louis de Klerk 0412 985 837

Private Bank

QLD Doug Snell 0414 887 659 [email protected]

Equipment and debtor finance

Qld Brendan Casey 0419 755 031 [email protected]

NSW Michael Campbell 0419 658 902 [email protected]

Vic Nick Stoneham 0422 157 781 [email protected]

Bank of Queensland Limited ABN 32 009 656 740 Australian

Credit Licence Number 244616 (BOQ). BOQ will not provide

you with advice in relation to the establishment, operation

and structure of your self-managed superannuation fund

(Super Fund). Nor will BOQ provide you with advice in

relation to the investment strategy of your Super Fund. You

should seek independent advice from a qualified

professional on these matters. Terms and conditions may

apply to individual products and services. The material in

this report may contain general advice. This material has

been prepared without taking account of your objectives,

financial situation or needs. The content of this report is for

information only and is not an offer by Bank of Queensland

Limited ABN 32 009 656 740 (BOQ) to provide any products

and services. BOQ makes no representations or warranties

about the accuracy or completeness of the content

contained in this report. BOQ recommends that you do not

rely on the contents of the report, that you consider the

appropriateness of any advice before acting on it and that

you obtain independent professional advice about your

particular circumstances. You should obtain and consider

the relevant terms and conditions or Product Disclosure

Statement (PDS) before making any decision about whether

to acquire or continue to hold any products. All other terms

and conditions or PDS and Financial Services Guide (FSG)

are available at any BOQ branch.

Related Documents