Case Study NESCAFÉ

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Case Study

NESCAFÉ

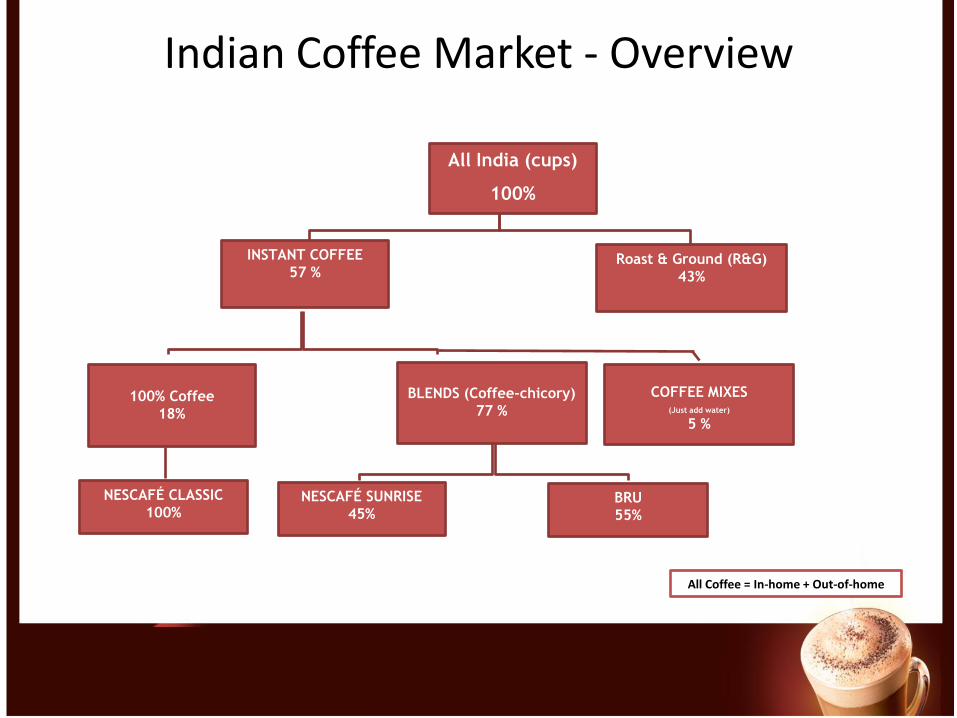

Indian Coffee Market - Overview

All India (cups)

100%

Roast & Ground (R&G)

43%

100% Coffee

18%

NESCAFÉ SUNRISE

45%BRU

55%

INSTANT COFFEE

57 %

BLENDS (Coffee-chicory)

77 %

NESCAFÉ CLASSIC

100%

COFFEE MIXES(Just add water)

5 %

All Coffee = In-home + Out-of-home

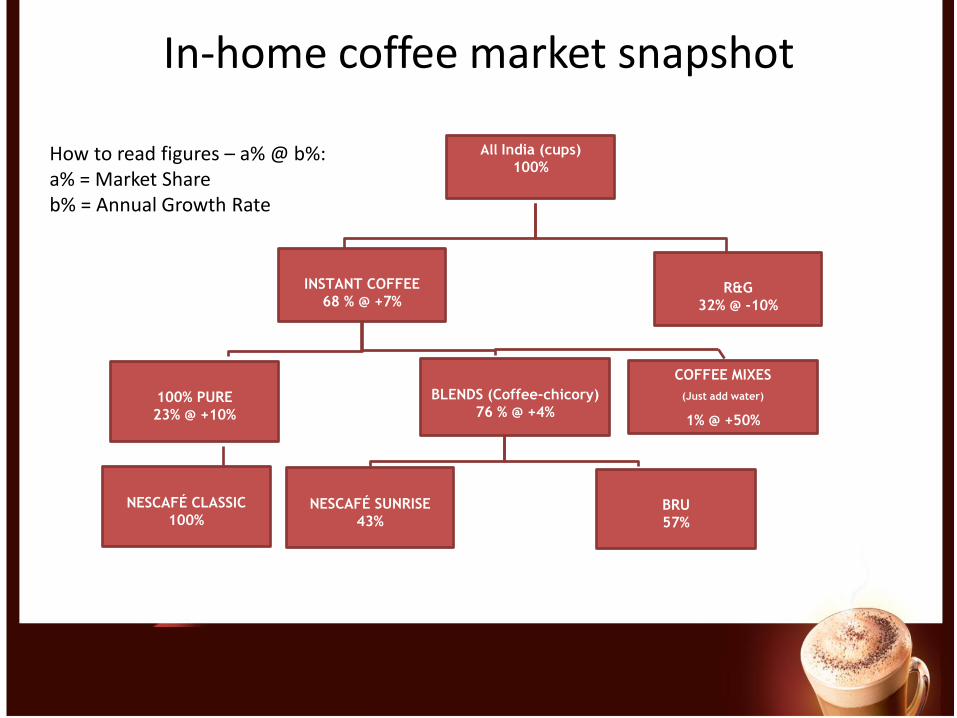

In-home coffee market snapshot

All India (cups)

100%

R&G

32% @ -10%

100% PURE

23% @ +10%

NESCAFÉ SUNRISE

43%BRU

57%

INSTANT COFFEE

68 % @ +7%

BLENDS (Coffee-chicory)

76 % @ +4%

NESCAFÉ CLASSIC

100%

COFFEE MIXES

(Just add water)

1% @ +50%

How to read figures – a% @ b%:a% = Market Shareb% = Annual Growth Rate

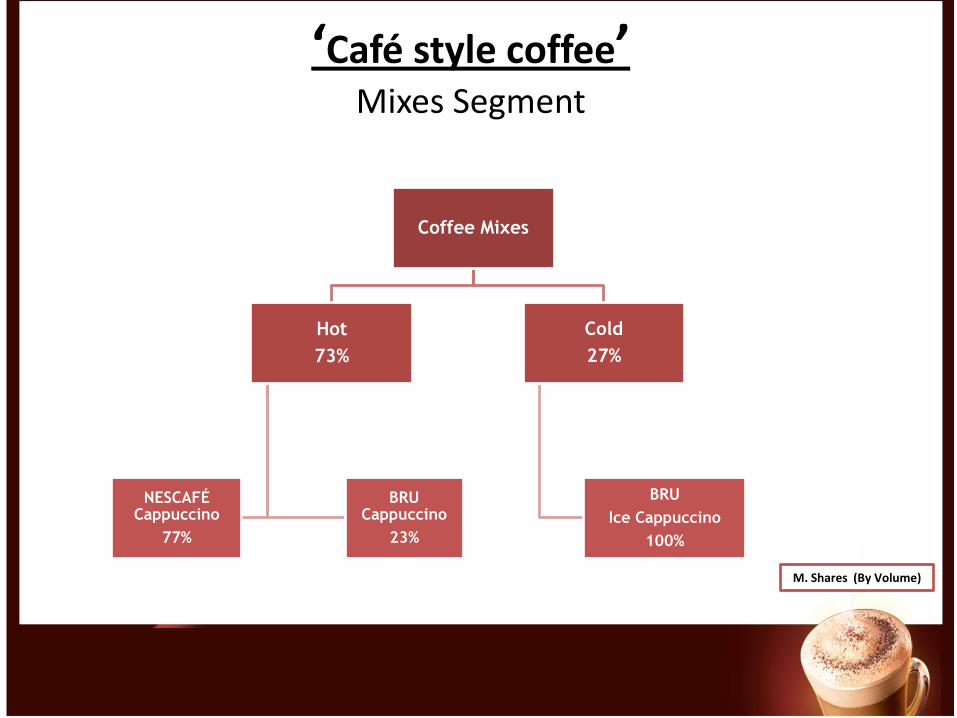

‘Café style coffee’ Mixes Segment

Coffee Mixes

Cold

27%

BRU

Ice Cappuccino

100%

Hot

73%

BRU Cappuccino

23%

NESCAFÉ Cappuccino

77%

M. Shares (By Volume)

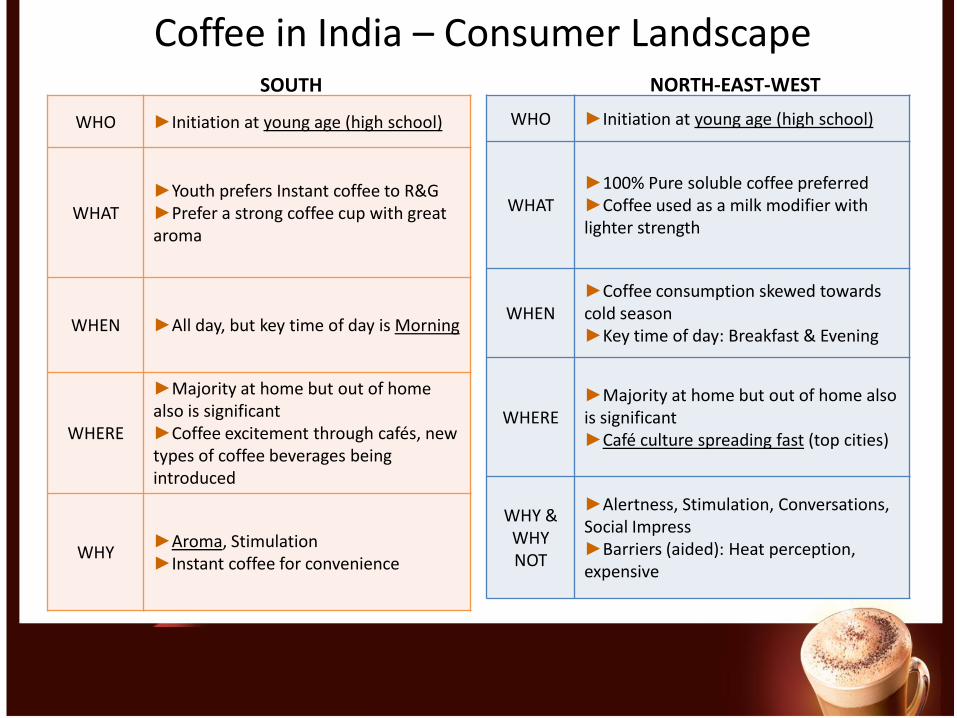

WHO ►Initiation at young age (high school)

WHAT►Youth prefers Instant coffee to R&G►Prefer a strong coffee cup with great aroma

WHEN ►All day, but key time of day is Morning

WHERE

►Majority at home but out of home also is significant►Coffee excitement through cafés, new types of coffee beverages being introduced

WHY►Aroma, Stimulation►Instant coffee for convenience

WHO ►Initiation at young age (high school)

WHAT►100% Pure soluble coffee preferred►Coffee used as a milk modifier with lighter strength

WHEN►Coffee consumption skewed towards cold season►Key time of day: Breakfast & Evening

WHERE►Majority at home but out of home also is significant►Café culture spreading fast (top cities)

WHY & WHY NOT

►Alertness, Stimulation, Conversations, Social Impress►Barriers (aided): Heat perception, expensive

Coffee in India – Consumer LandscapeSOUTH NORTH-EAST-WEST

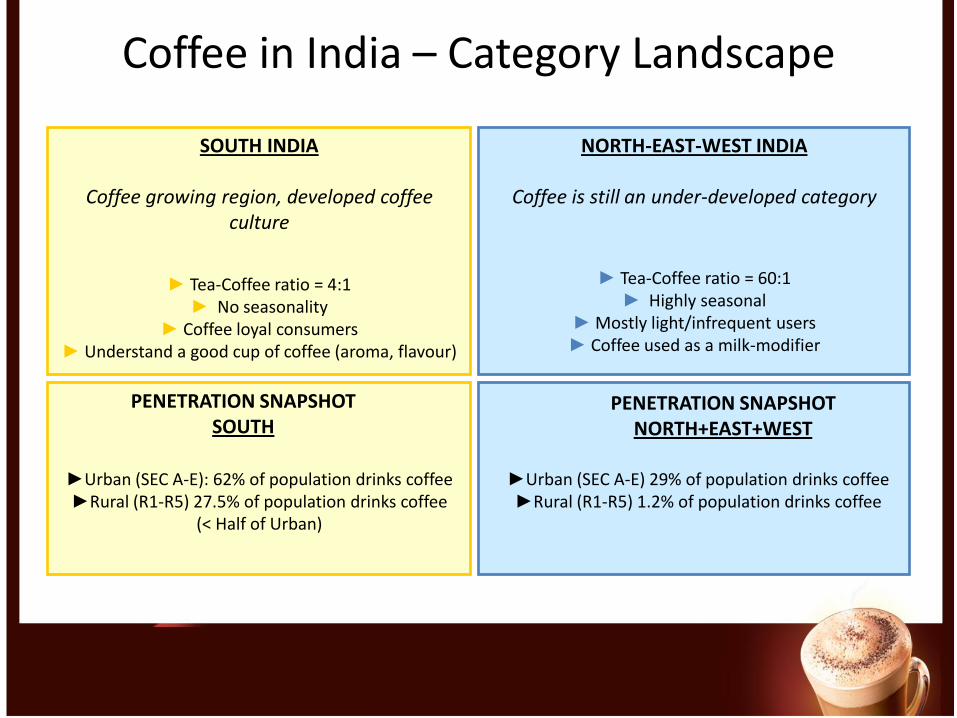

Coffee in India – Category Landscape

SOUTH INDIA

Coffee growing region, developed coffee culture

► Tea-Coffee ratio = 4:1► No seasonality

► Coffee loyal consumers► Understand a good cup of coffee (aroma, flavour)

NORTH-EAST-WEST INDIA

Coffee is still an under-developed category

► Tea-Coffee ratio = 60:1► Highly seasonal

► Mostly light/infrequent users► Coffee used as a milk-modifier

PENETRATION SNAPSHOT NORTH+EAST+WEST

►Urban (SEC A-E): 62% of population drinks coffee►Rural (R1-R5) 27.5% of population drinks coffee

(< Half of Urban)

►Urban (SEC A-E) 29% of population drinks coffee►Rural (R1-R5) 1.2% of population drinks coffee

PENETRATION SNAPSHOT SOUTH

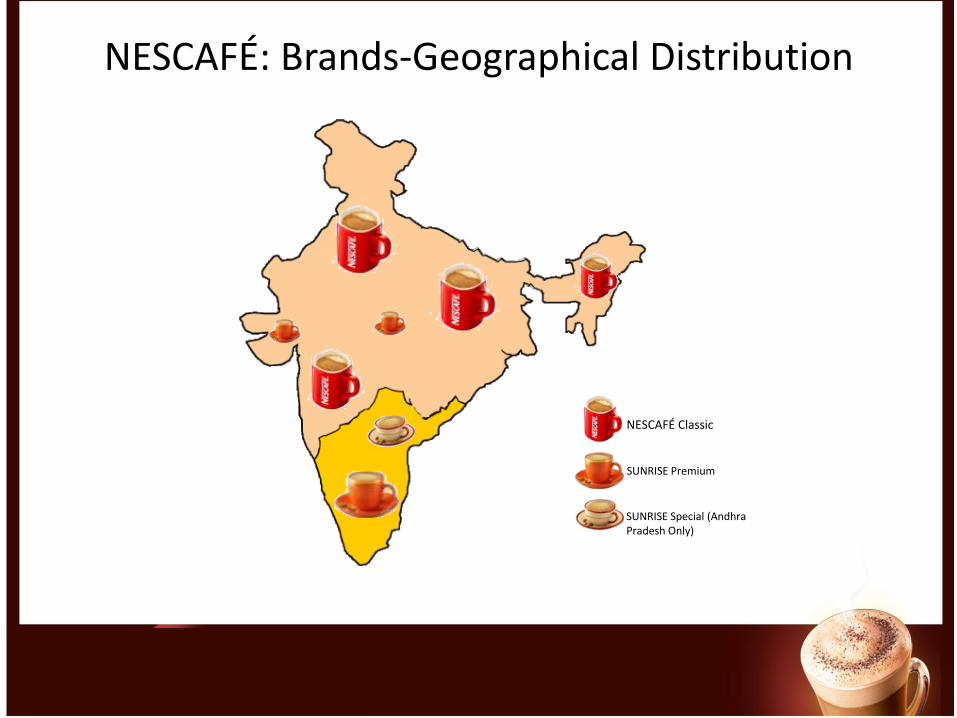

NESCAFÉ: Brands-Geographical Distribution

SUNRISE Premium

SUNRISE Special (Andhra Pradesh Only)

NESCAFÉ Classic

RegionNorth-East-West

Household Penetration (North-East-West)

Source :HHP 2007-2009, IMRB

28.5% 27.1% 29.5% 29.3% 28.2%

2005 2006 2007 2008 2009

Coffee Penet.% (Urban)

16.8%

8.8% 9.3%

16.7%18.0%

9.6% 9.5%

15.7%

15.9%

9.3% 9.2%

15.4%

Q1 Q2 Q3 Q4

Coffee Penet.% (Urban)

2007 2008 2009

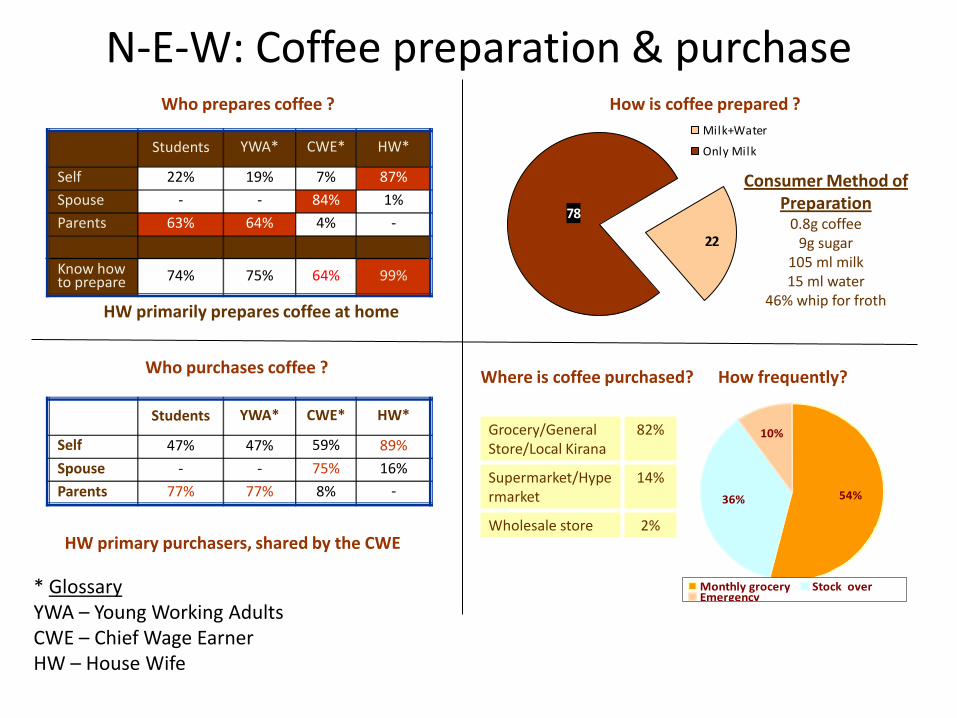

N-E-W: Coffee preparation & purchase

22

78

Milk+Water

Only Milk

How is coffee prepared ?

Consumer Method of Preparation

0.8g coffee9g sugar

105 ml milk15 ml water

46% whip for froth

Who prepares coffee ?

Students YWA* CWE* HW*

Self 22% 19% 7% 87%

Spouse - - 84% 1%

Parents 63% 64% 4% -

Know how to prepare 74% 75% 64% 99%

HW primarily prepares coffee at home

Who purchases coffee ?

Students YWA* CWE* HW*

Self 47% 47% 59% 89%

Spouse - - 75% 16%

Parents 77% 77% 8% -

HW primary purchasers, shared by the CWE

Where is coffee purchased? How frequently?

Grocery/General Store/Local Kirana

82%

Supermarket/Hypermarket

14%

Wholesale store 2%

54%36%

10%

Monthly grocery Stock overEmergency

* GlossaryYWA – Young Working AdultsCWE – Chief Wage EarnerHW – House Wife

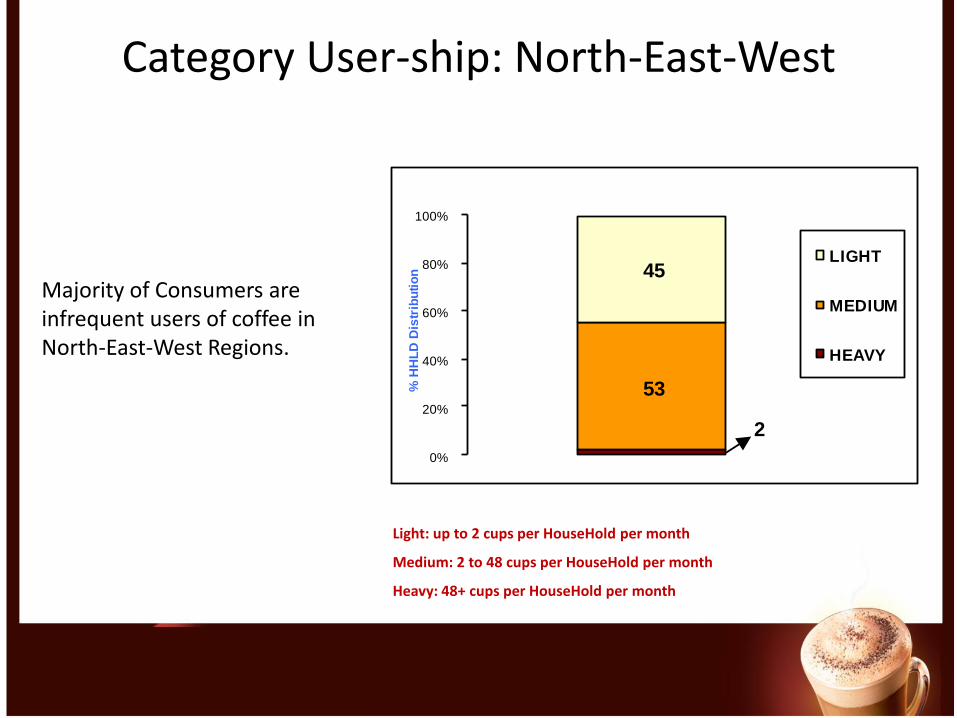

Category User-ship: North-East-West

2

53

45

0%

20%

40%

60%

80%

100%

% H

HL

D D

istr

ibu

tio

n

LIGHT

MEDIUM

HEAVY

Light: up to 2 cups per HouseHold per month

Medium: 2 to 48 cups per HouseHold per month

Heavy: 48+ cups per HouseHold per month

Majority of Consumers are infrequent users of coffee in North-East-West Regions.

RegionSouth

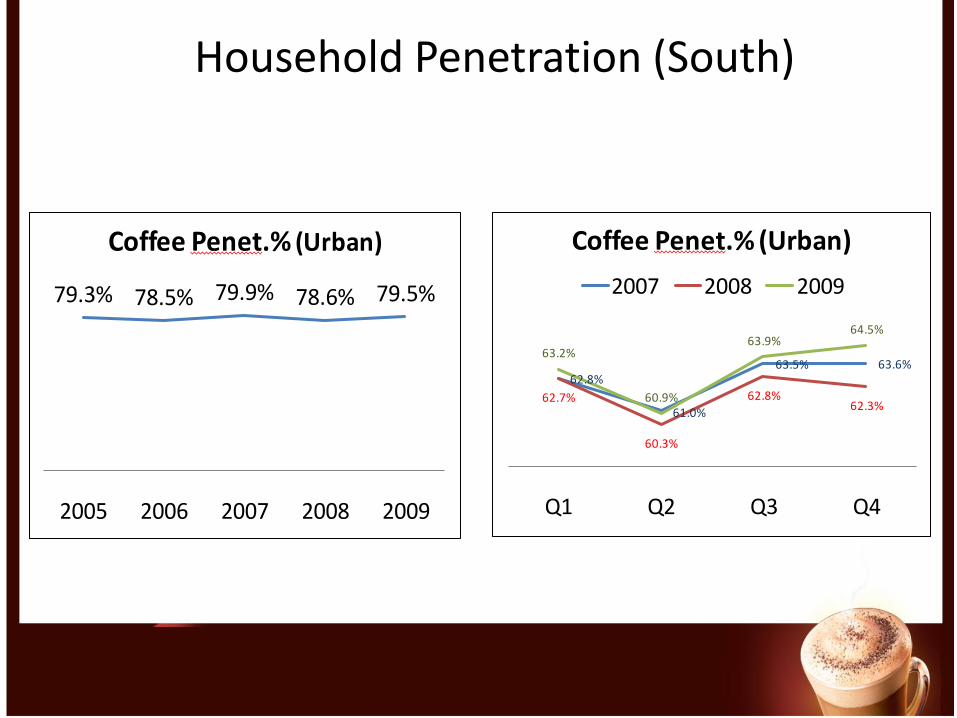

Household Penetration (South)

Source :HHP 2007-2009, IMRB

79.3% 78.5% 79.9% 78.6% 79.5%

2005 2006 2007 2008 2009

Coffee Penet.% (Urban)

62.8%

61.0%

63.5% 63.6%

62.7%

60.3%

62.8%62.3%

63.2%

60.9%

63.9%64.5%

Q1 Q2 Q3 Q4

Coffee Penet.% (Urban)

2007 2008 2009

Household Penetration (South)

South: Coffee preparation & purchase

< 13 years

School students

15

83

Black

Milk+Water

Only Milk

Cant say

How is coffee prepared ?

Consumer Method of Preparation

1.3g coffee9g sugar

120 ml milk40 ml water

Tumble for froth

Who prepares coffee ?

Students YWA* CWE* HW*

Self 11% 21% 15% 96%

Spouse - - 76% -

Parents 80% 74% 6% 1%

Know how to prepare 54% 47% 38% 99%

House wife primarily prepares coffee at home

Who purchases coffee ?

Students YWA* CWE* HW*

Self 19% 36% 35% 65%

Spouse - - 59% 34%

Parents 77% 59% 9% 3%

House wife is the primary purchaser

Where is coffee purchased? How frequently?

Grocery/General Store/Local Kirana

84%

Supermarket/Hypermarket

15%

Wholesale store 5%

54%37%

9%

Monthly grocery Stock overEmergency

Coffee is mostly prepared with a mix of milk and water

* GlossaryYWA – Young Working AdultsCWE – Chief Wage EarnerHW – House Wife

Café Culture

The Opportunity

50% of India’s population is below 30 years of age, making India the country with youngest population in the world

Young are earning high income at earlier stages of their career than compared to previous generations

High disposable income, a desire to spend on better things, and a desire for change

Increased relevance of Café culture

– Opened to different formats of coffee that can be consumed apart from the regular hot and cold

– Different variants, earlier not known at all are becoming familiar; such as Lattes, Cappuccinos, Espressos…

– Cafés becoming synonymous as meeting/hangout places where one can share great moments over a cup of coffee

Out of Home CCD, Barista, Mocha & Costa Coffee are the key players in the OOH

segment

– 2000 outlets across the country

– Huge expansion plans over the next 3-5 years; mainly in tier-II cities

– Also forayed into retailing of packaged coffees

New Entrant- Starbucks expected to open café’s in the Indian market soon

Nestlé’s presence in OOH segment

- Café NESCAFÉ’s

- NESCAFÉ Café Corners

- Vending points across educational institutions & corporate/commercial establishments

Coffee mixes (In-Home): A Brief History

First launched as a basic 3-in-1 coffee by NESCAFÉ in 1998, targeted at youth– Met with limited success, withdrawn next year

BRU launched the first foaming 3-in-1 coffee in 2005, targeted primarily at aspiring, trendy, upwardly mobile youth

BRU strategy : Focus in driving “Image”– Leverage Cappuccino imagery of “Trendy”, “Youthful”, “Modern” Beverage

– Growth in Volumes but base still low

– Significant investments behind Cappuccino (both ATL & BTL)- ‘Sip Lick mmmcampaign’

NESCAFÉ launched NESCAFÉ Cappuccino in 2008, with the proposition of ‘Bring home the café experience’– This was followed with launch of the variants: NESCAFÉ Choco Mocha &

NESCAFÉ Vanilla Latte

DELIVERABLES(STAGE 1)

Does ‘Café style’ coffee (in-home) have a role to play in developing the coffee category?

• If Yes – How?

• If No – Then what do you see as the way to grow Coffee Category?

• You may use graphs & charts to support the same

Limit: 1 slide

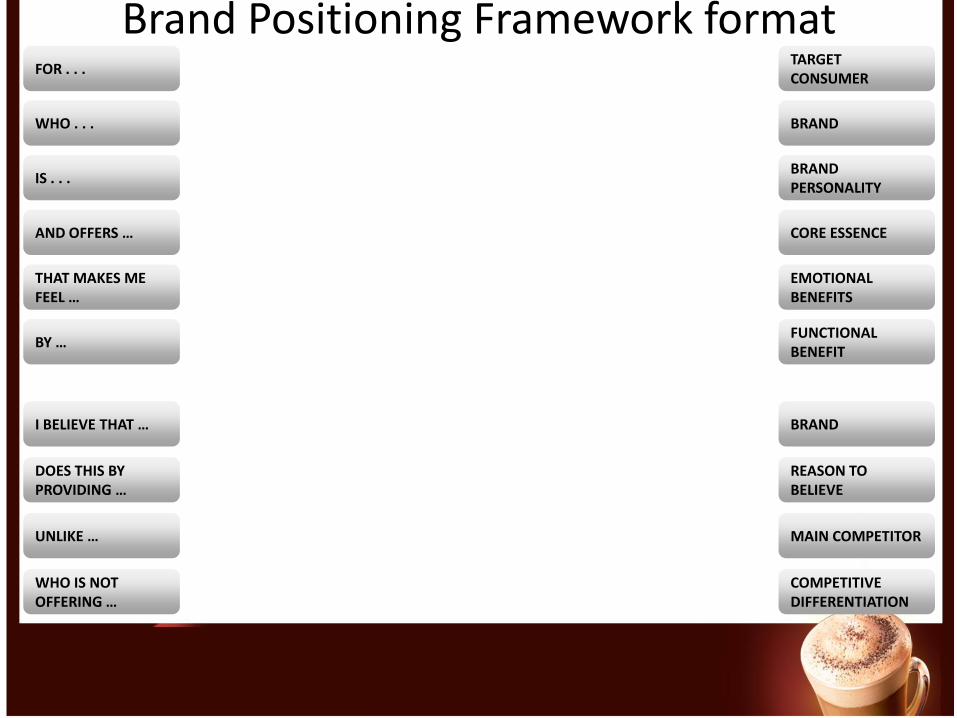

Give a Brand Positioning Framework for a Product (within the current portfolio or outside) that you will look to support/launch. Only one product may be selected. (Use the Brand Positioning Frame work given in the next two slides strictly – to provide your inputs)

Limit: 1 slide

Brand Positioning Framework formatFOR . . .

THAT MAKES ME FEEL …

IS . . .

AND OFFERS …

WHO . . .

BY …

I BELIEVE THAT …

DOES THIS BY PROVIDING …

UNLIKE …

WHO IS NOT OFFERING …

TARGET CONSUMER

EMOTIONAL BENEFITS

BRAND PERSONALITY

CORE ESSENCE

BRAND

FUNCTIONAL BENEFIT

BRAND

REASON TO BELIEVE

MAIN COMPETITOR

COMPETITIVE DIFFERENTIATION

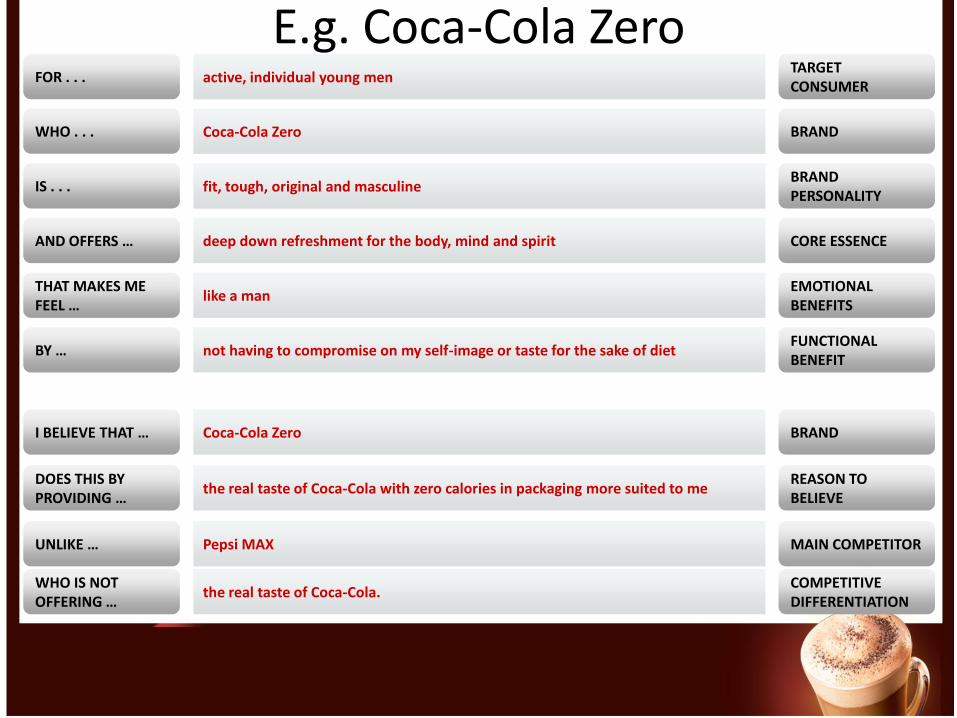

E.g. Coca-Cola ZeroFOR . . .

THAT MAKES ME FEEL …

IS . . .

AND OFFERS …

WHO . . .

BY …

I BELIEVE THAT …

DOES THIS BY PROVIDING …

UNLIKE …

WHO IS NOT OFFERING …

TARGET CONSUMER

EMOTIONAL BENEFITS

BRAND PERSONALITY

CORE ESSENCE

BRAND

FUNCTIONAL BENEFIT

BRAND

REASON TO BELIEVE

MAIN COMPETITOR

COMPETITIVE DIFFERENTIATION

active, individual young men

Coca-Cola Zero

fit, tough, original and masculine

deep down refreshment for the body, mind and spirit

like a man

not having to compromise on my self-image or taste for the sake of diet

Coca-Cola Zero

the real taste of Coca-Cola with zero calories in packaging more suited to me

Pepsi MAX

the real taste of Coca-Cola.

DELIVERABLES(Stage – II)

Instructions Complete Marketing Plan:

– Slide 1: 4Ps in detail

– Slide 2: Broad-level Sales & Distribution Strategy

– Slide 3: A Five-year development plan for the brand

• Targeted annual Volume Growth figures. Rationale (may be supported with statistical data).

• Marketing Inputs to be given, year-wise. Estimated spends.

• Assume a Marginal Contribution in the range of 30-35%. How long will the brand/portfolio take to break even?

Slide 4: Articulation of insight (from positioning framework)

Slide 5: Give the tagline for the Product. Any creative designed will be given brownie points!

Additional Data

Out of Home: Café Coffee Day

Background

Café Coffee Day is a division of India’s largest coffee conglomerate, the Amalgamated Bean Coffee Trading Company Limited (ABCTCL). Popularly known as Coffee Day, it’s a Rs. 750 crore, ISO 9002 certified company. With Asia’s second-largest network of coffee estates (10,500 acres) and 11,000 small growers, Coffee Day has a rich and abundant source of coffee. This coffee goes all over the world to clients across the USA, Europe and Japan, making it one of the top coffee exporters in the world.

ABCTCL’s retail division Café Coffee Day (CCD) pioneered the café concept in India in 1996 by opening its first café at Brigade Road in Bangalore. Café Coffee Day is now the largest organized retail café chain in India with cafes across top ninety cities in the country. It also has cafes in Vienna, Austria and Karachi

Operation in India

ABCTCL at present has 970 CCD outlets. The company plans to spend Rs 130-150 crore on expanding its store network and changing the look and feel of existing stores in this financial year. The Route To Market for Café’s is mainly through company owned, company operated Cafes.

The chain is also trying to capture a slice of spends on in home consumption of coffee by retailing its own coffee and related products through food and grocery chains.

Out of Home: Costa Coffee British coffee chain Costa Coffee has reworked its India strategy to turn

profitable and expand its footprint. The new strategy involves closing unprofitable locations, segmenting strategy for different locations, changing the look and feel of outlets and customising the menu to better suit the Indian palate.

The chain, which has a master franchisee agreement with DevyaniInternational, a subsidiary of Ravi Jaipuria owned RJ Corporation, is looking to expand only at metros. According to Santhosh Unni, the company went through its share of mistakes before setting the model right.

As part of the restructuring, Costa will have four key formats situated at airports, malls, high streets and IT parks. They have also introduced something called the off premise business where they are setting up kiosks in marriages, and seminars meetings.

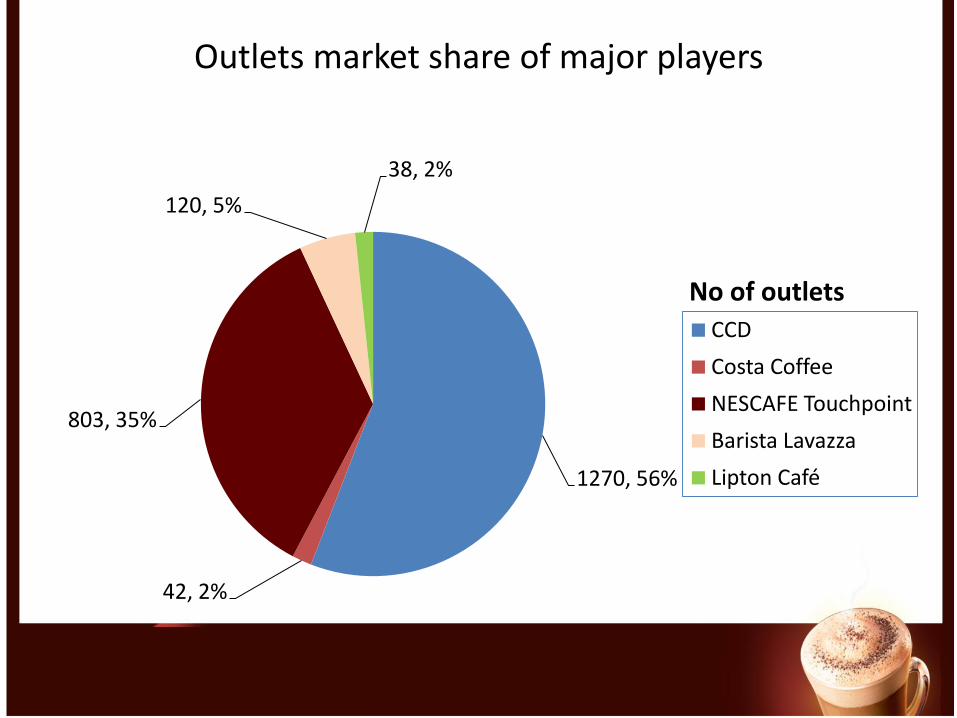

Outlets market share of major players

1270, 56%

42, 2%

803, 35%

120, 5%

38, 2%

No of outlets

CCD

Costa Coffee

NESCAFE Touchpoint

Barista Lavazza

Lipton Café

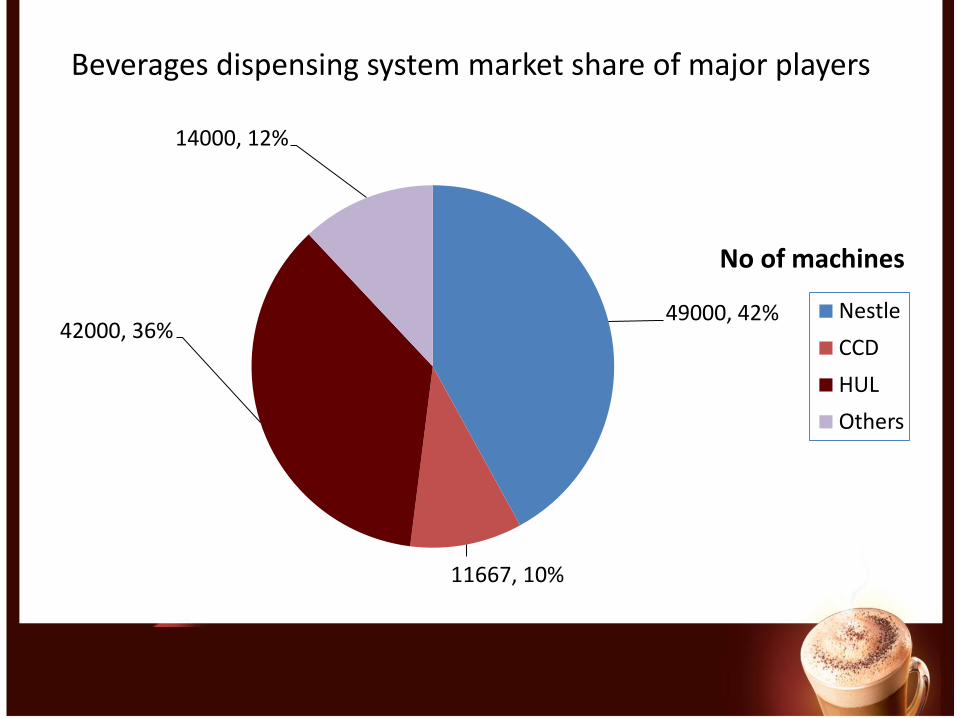

Beverages dispensing system market share of major players

49000, 42%

11667, 10%

42000, 36%

14000, 12%

No of machines

Nestle

CCD

HUL

Others

NESCAFÉ Cappuccino

Targeting youth (between 18-30) by offering a great alternative to expensive cappuccino’s available at Cafés

NESCAFÉ brand name lends credibility

Objectives

To become an image driver amongst the youth by establishing the versatility of NESCAFÉ as a brand

To provide an affordable café experience to those who aspire for it

Multi Pack(5X15g sachet)

Single Serve Pack15g Sachet

NESCAFÉ Cappuccino: New Variants

New variants were launched in October 2009:– NESCAFÉ Choco Mocha

– NESCAFÉ Vanilla Latte

Launched in select cities

Limited exclusive consumer communication done since launch.– Only In-Store communication through

Point of Sales

Related Documents