Nationwide Insurance Case Study: Integrated Marketing Communications by Jill Leigh Bullock [email protected] 919.424.8017 July 20, 2009 West Virginia University IMC 618 Introduction to Integrated Marketing Communications Professor William Nevin

Nationwide Insurance Marketing Case Study

Nov 16, 2014

Nationwide Insurance Case Study 2009. Nationwide Insurance practices Integrated Marketing Communications. The case study outlines Nationwide's illegal discriminatory practices of the 1990's that violated the 1968 Civil Rights Act and the 1988 Federal Fair Housing Act and how Nationwide rebuilt its reputation through IMC practices. Detailed marketing strategies tactics and future potential issues with social media are discussed.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Nationwide Insurance

Case Study: Integrated Marketing Communicationsby Jill Leigh Bullock

July 20, 2009

West Virginia UniversityIMC 618

Introduction to Integrated Marketing CommunicationsProfessor William Nevin

2 of 47

INTRODUCTION Assignment. Select a company that has a specific marketing challenge and write a case study including the following elements:

1. A real-life scenario

2. Supporting data and documents

3. Develop three open-ended business questions that should be answered in full.

Assumptions. For the purpose of this research, it is assumed that the audience has a good understanding of marketing communication concepts as well as technology and its role in marketing communications. Caveats. Where proprietary information is unavailable data may be substituted for illustration purposes. Substituted data will be noted and may or may not be viable for including but not limited to validating the success of recommended solutions, goals or objectives. Sweeping changes have affected the financial industry in the past year, with no clear signs of stabilization. Although the research presented in this case study is current, consideration should given where information is no longer relevant. Information that is known or suspect to be outdated will be noted at the time it is presented. Omissions. The focus of this case study will be directed towards Nationwide’s individual consumer segment; thus, detailed information regarding Nationwide’s other customer segments are beyond the scope of this study and while recognized are not researched nor documented in detail.

MARKETING CHALLANGES Nationwide Insurance implemented an Integrated Marketing Communications(IMC) program largely to overcome a negative image it had developed during the 1990’s for violating the Civil Rights Act of 1968 and the Federal Fair Housing Act of 1988. Nationwide utilized discriminatory underwriting practices until the United States Justice Department filed suit against Nationwide in 1997. Immediately thereafter, Nationwide quickly stepped forward and filed a consent decree offering corrective actions to repair its discriminatory practices. It has taken over a decade to overcome Nationwide’s reputation of illegal practices and turn its image and brand around. A large part of the turnaround success has been due to its IMC practices. However, as technology and the use of the Internet has increased and is more adopted by both corporate America and mainstream consumers, several issues may resurface for Nationwide in combating negative public opinion, specifically in regards to social media venues utilized in IMC practices. Although Nationwide ended its discriminatory practices, public opinion may be slower to accept Nationwide’s positive turn around. Negative press, Internet postings and future corporate missteps may affect Nationwide more harshly than corporations with an untarnished reputation. Navigating this potential public relations and branding challenge are the basis for two of my three marketing concerns. My third marketing concern addresses today’s economy and competing in a price sensitive market.

1. Nationwide Group has made a wise decision to leverage social media venues. However, the use of social media can mean losing control over public relation images. For example, Internet blogging and Comment Reviews. How does Nationwide Group combat negative blogs on social media websites where it does not have the ability to control communications, especially in light of fiduciary responsibility and broker/client confidentiality regulations?

2. How does Nationwide Group convey trust and dependability through its internal and external

communications and during a national meltdown of financial institutions, including the world’s largest insurer American Insurance Group(AIG), which was seized by the US government in September 2008?1

3. Several of Nationwide competitors are differentiating on price due to the recessionary economic times.

How does Nationwide Insurance add value, attract and retain customers and still remain profitable during difficult economic times?

3 of 47

SITUATION ANALYSIS Company

“Nationwide, based in Columbus, Ohio, is one of the largest and strongest diversified insurance and financial services organizations in the U.S. and is rated A+ by A.M. Best.” 2 It employs approximately 36,000 people3 and offers range of financial products including, “car insurance, motorcycle insurance, boat insurance, homeowners insurance, life, farm, commercial insurance, administrative services, annuities, mortgages, mutual funds, pensions, long-term savings plans and health and productivity services.”4 Nationwide Group is parent company of the Nationwide brand which is employed by its subsidiaries. Nationwide and its subsidiaries compete in 5 different financial segments including3:

1. Property and Casualty Insurance 2. Health Insurance 3. Life Insurance & Retirement Savings Plans 4. Banking & Mortgage 5. Asset Management

Management See Figure 1: Nationwide's Board of Directors and Office of the CEO Management Team3

Figure 1: Nationwide's Board of Directors and Office of the CEO Management Team

Source: 2007 Nationwide Annual Report for Shareholders

4 of 47

Nationwide Background Nationwide was founded in 1925, as a small mutual auto insurer, owned by policyholders and has grown to one of the largest insurance conglomerates today. Below is an excerpt taken directly from Nationwide’s website regarding its corporate history.5

“Over the last 80 years, Nationwide has grown from a small mutual auto insurer owned by policyholders to one of the largest insurance and financial services companies in the world, with more than $135 billion in statutory assets.

Early growth came from working together with Farm Bureaus that sponsored the company. Eight Farm Bureaus continue to promote Nationwide and provide discounts to members.

The Early Years

1925 − The Ohio Farm Bureau Federation incorporates the Farm Bureau Mutual Automobile Insurance Company with the goal of providing quality auto insurance at low rates for farmers in Ohio.

1926 − The first policy is sold, and The Ohio Farm Bureau Federation is open for business.

1928 − With help from locally based sponsoring organizations, Farm Bureau Mutual begins expanding into other states. These include West Virginia, Maryland, Delaware, Vermont and North Carolina.

1934 − The company starts insuring motorists in metropolitan areas and, through the purchase of a fire insurance company, begins writing property insurance policies.

1943 − Farm Bureau Mutual operates in 12 states and the District of Columbia.

Becoming Nationwide

1955 − From 1943 on, the Farm Bureau Mutual expanded operations until it became clear that they had far outgrown their original goals... and their name. So, with a western expansion that included 20 additional states, the company changed its name to Nationwide Insurance®.

1978 − Nationwide completes its international headquarters at One Nationwide Plaza. The 40-story structure is the largest single office building in Central Ohio.

1982 - Nationwide acquires Farmland Insurance, now Nationwide Agribusiness Insurance, a 100-year-old company and America's leading farm insurer.

1997 − Nationwide Financial® goes public.

2000 − With a ground breaking in 1997, the Nationwide Arena opens providing a home to a National Hockey League franchise, the Columbus Blue Jackets.

2007 − Nationwide Bank opens to the public.

5 of 47

Mission Statement Nationwide’s corporate mission is to:

“provide advice and products that help our customers protect and manage the most important assets in their lives: their homes, their cars, their families and their incomes after they retire. By focusing on three core businesses - the property/casualty insurance business, the life and retirement savings business, and the asset management business - we remain committed to increasing the value our customers have come to expect from us. Our shared values, and the investment we make to reinforce them, will move us to the great company we envision for tomorrow.”6

Guiding Principals “Nationwide Mutual Insurance Company's Board – in a spirit of continuous improvement – consistently assesses its performance against governance best practices and holds itself accountable for adhering to the highest standards of board professionalism and performance.”7 A corporate code of ethics is outlined by CEO Jurgensen in a professional, Nationwide communication brochure. The brochure is prefaced with the following letter addressed to Nationwiders by Jurgensen.

Figure 2: CEO Letter to Nationwiders regarding Code of Ethics & Conduct Dear Nationwiders, As one of the largest insurance and financial services organizations in the world, seldom a day goes by that Nationwide® is not confronted with making difficult decisions in an ever-changing marketplace. However, no matter how much things change, one factor will always remain constant – Nationwide’s commitment to integrity and ethical behavior. Whether you are new to Nationwide or have been a Nationwider for some time, it is your responsibility to read the important information in the Code. And know that each one of us – associates, officers and directors alike – will be held to the standards of business conduct and fair dealing contained within this Code. At Nationwide, honesty and integrity are the cornerstones of our foundation. These core values should never be compromised to meet a business plan or to make a profit. I am depending on all of you to adhere to the highest ethical standards. If you ever feel pressured to commit an act that conflicts with the Code or if you believe a colleague is violating the Code, please talk to your manager, Human Resources, or make a confidential call to the Office of Ethics and Business Practices (800-453-8442) immediately. Thank you for your support and for all you do for Nationwide and our customers every day. Sincerely, W. G. Jurgensen Chief Executive Officer8

6 of 47

As noted previously, Nationwide is a collective group of subsidiaries. To ensure adherence of its ethics policies between entities, Nationwide has a documented and broadly communicated an Ethics Guideline policy to ensure consistency in its ethic practices between subsidiaries.

Nationwide’s ethics policy addresses the areas of: The Board’s responsibilities, individual Board Member responsibilities, Board Member qualifications, Director compensation, Board committees, Board operations, annual performance review of the Boards, management succession, and Director representation of the companies.7

The goal of the Boards of Directors of Nationwide Mutual Insurance Company, Nationwide Mutual Fire Insurance Company and Nationwide Corporation (collectively, the "Companies") is to be a strategic asset of the Companies. The Boards must constantly ensure that they have the right people, addressing the right issues with the right information in a culture that stimulates teamwork.

To achieve this goal, the Boards must:

Be organized properly (board structure)

Conduct their business effectively and, when appropriate, confidentially (board process)

Have board competencies aligned with the company's strategy (people)

Have a culture that fosters open dialog and collaboration (culture)

The Boards of the Companies − in a spirit of continuous improvement − will consistently be assessing their performance against governance best practices and hold themselves accountable both as individuals and as Boards for adhering to the highest standards of board professionalism and performance.7

To learn more about Nationwide’s Ethic’s Policy and Guiding Principals, refer to Appendix A and B, attached to this case study submission.

Corporate Culture, Citizenship and Social Responsibility Nationwide clearly communicates its corporate culture, citizenship, and social responsibility. Its website states that:

“At Nationwide, we're working together to foster our inclusive culture where everyone feels challenged, appreciated, respected and engaged. We have developed a workplace where associates and leaders live our values and appreciate the similarities and differences in each other and our customers. It's at the heart of our On Your Side® promise.”9

“We're committed to recruiting, developing and retaining a diverse and talented workforce that reflects the communities and markets we serve…

… The importance of diversity and inclusion to our culture and our business is reflected in our values and every aspect of the company. Every core and performance value we have depends on our commitment to listening to every voice and to considering every point of view in our daily interactions with each other, our suppliers and our customers.

7 of 47

By weaving a diversity and inclusion mindset throughout Nationwide, we're free to express ourselves and to take full advantage of the broad experiences and talents we all bring. We have the opportunity to be better understood and to connect better with our co-workers. This leads to new opportunities to develop personally and professionally.

Our customers ultimately benefit as we work together to serve their needs and strengthen our ability to grow and extend our On Your Side® promise to more and more people.”10

Our Values

Trust, respect, honesty and integrity are much more than just words at Nationwide. These – along with focusing on customers and valuing people – are our core values and at the heart of who we are.

It’s living these values that brings Nationwide associates together. And the values provide the cornerstone for our culture. We seek creativity and new ways of thinking, knowing these come from people in all walks of life. We embrace inclusion because we understand that only through appreciating the richness of our diversity will we find the innovative ideas to set us apart from our competition.

Working together across boundaries, we share a bias for action and a passion for results. And, we think it’s important to have fun along the way. Nationwide challenges associates to deliver the On Your Side® promise to customers and rewards that high performance. We strongly support individual development and provide opportunities for associates to try different things, learn new skills and hone their talents through their careers with us. 11

Diversity and Inclusion are at the heart of our On Your Side® experience for our associates and customers. Each individual is unique. Recognizing this uniqueness and knowing how to work effectively across our differences are critical to our successes as a company and being able to deliver on our promise. The importance of diversity and inclusion to our culture and our business is reflected in our values and every aspect of the company. Every core and performance value we have depends on our commitment to listening to every voice and considering every point of view in our daily interactions with each other, our suppliers, and our customers.12

Nationwide goes beyond communicating its culture to customers, suppliers, and prospects. Nationwide has an active presence in the communities in which it represents. Nationwide is actively involved in contributing and giving back to the communities it serves through nonprofit sponsorships, the Nationwide Foundation and nonprofit partnerships.13

Nationwide’s Community Presence. “Saving, rebuilding and enriching lives is what Nationwide's Corporate Citizenship is all about. Every day, we turn critical moments into powerful possibilities. It's another way we're helping people when it matters most.

The Nationwide Foundation − We're positively impacting the quality of life in communities where our associates, agents and their families live and work. The highest priority for our grants is investing in nonprofit organizations whose services provide emergency and basic needs, or stabilize a crisis situation.

8 of 47

Nationwide Children's Hospital − In 2006, the Nationwide Foundation made its largest gift ever, granting $50 million to Columbus Children's Hospital, which was renamed to honor the gift.

On Your Side Volunteer Network® − Since 2005, our associates have volunteered with nearly 1,000 nonprofit organizations in 48 states through a network that helps connect them with nonprofit organizations that best match their interests and talents. The Nationwide Foundation supports these efforts by awarding a grant to qualifying organizations where associates spend at least 25 hours as volunteers.

United Way − We're proud of our long-standing commitment to United Way. In the past decade, our associates pledged more than $8 million to this national organization, an amount matched by the Nationwide Foundation. Associate pledges go directly to United Way agencies in their local communities.

Other organizations − Throughout the year, associates donate their time, skills and resources to other organizations such as the American Red Cross, Feeding America food banks and community organizations across the country. Through opportunities like these, everyone has a chance to get involved”14

Nationwide Marketing Strategy According to the American Productivity & Quality Center, Nationwide Insurance utilizes and has excelled in IMC as it defines, “Integrated marketing communications is a strategic business process used to plan, develop, execute and evaluate coordinated and measurable persuasive brand communication programs over time with consumers, customers, prospects and other targeted, relevant external and internal audiences."15

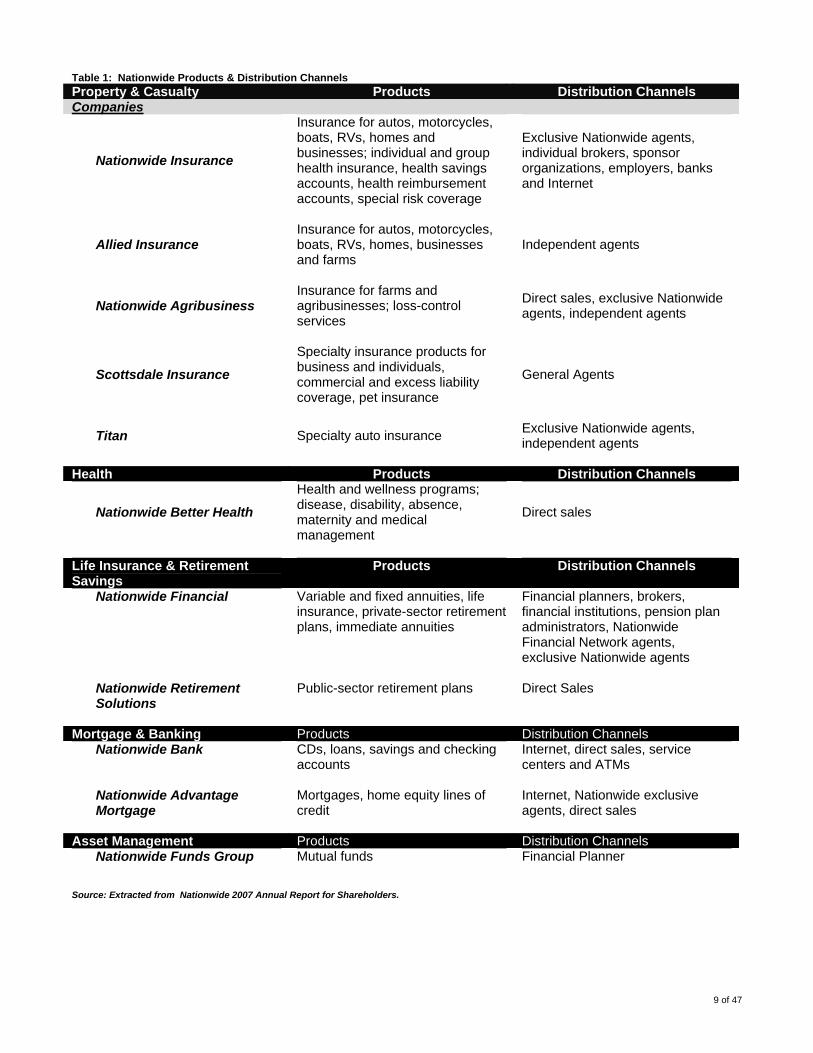

Product. Nationwide’s provides a variety of products within each of its five areas of expertise. See Table 1: Nationwide Products & Distribution Channels.3

9 of 47

Table 1: Nationwide Products & Distribution Channels Property & Casualty Products Distribution Channels Companies

Nationwide Insurance

Insurance for autos, motorcycles, boats, RVs, homes and businesses; individual and group health insurance, health savings accounts, health reimbursement accounts, special risk coverage

Exclusive Nationwide agents, individual brokers, sponsor organizations, employers, banks and Internet

Allied Insurance Insurance for autos, motorcycles, boats, RVs, homes, businesses and farms

Independent agents

Nationwide Agribusiness Insurance for farms and agribusinesses; loss-control services

Direct sales, exclusive Nationwide agents, independent agents

Scottsdale Insurance

Specialty insurance products for business and individuals, commercial and excess liability coverage, pet insurance

General Agents

Titan Specialty auto insurance Exclusive Nationwide agents, independent agents

Health Products Distribution Channels

Nationwide Better Health

Health and wellness programs; disease, disability, absence, maternity and medical management

Direct sales

Life Insurance & Retirement Savings

Products Distribution Channels

Nationwide Financial Variable and fixed annuities, life insurance, private-sector retirement plans, immediate annuities

Financial planners, brokers, financial institutions, pension plan administrators, Nationwide Financial Network agents, exclusive Nationwide agents

Nationwide Retirement Solutions

Public-sector retirement plans Direct Sales

Mortgage & Banking Products Distribution Channels

Nationwide Bank CDs, loans, savings and checking accounts

Internet, direct sales, service centers and ATMs

Nationwide Advantage Mortgage

Mortgages, home equity lines of credit

Internet, Nationwide exclusive agents, direct sales

Asset Management Products Distribution Channels

Nationwide Funds Group Mutual funds Financial Planner

Source: Extracted from Nationwide 2007 Annual Report for Shareholders.

10 of 47

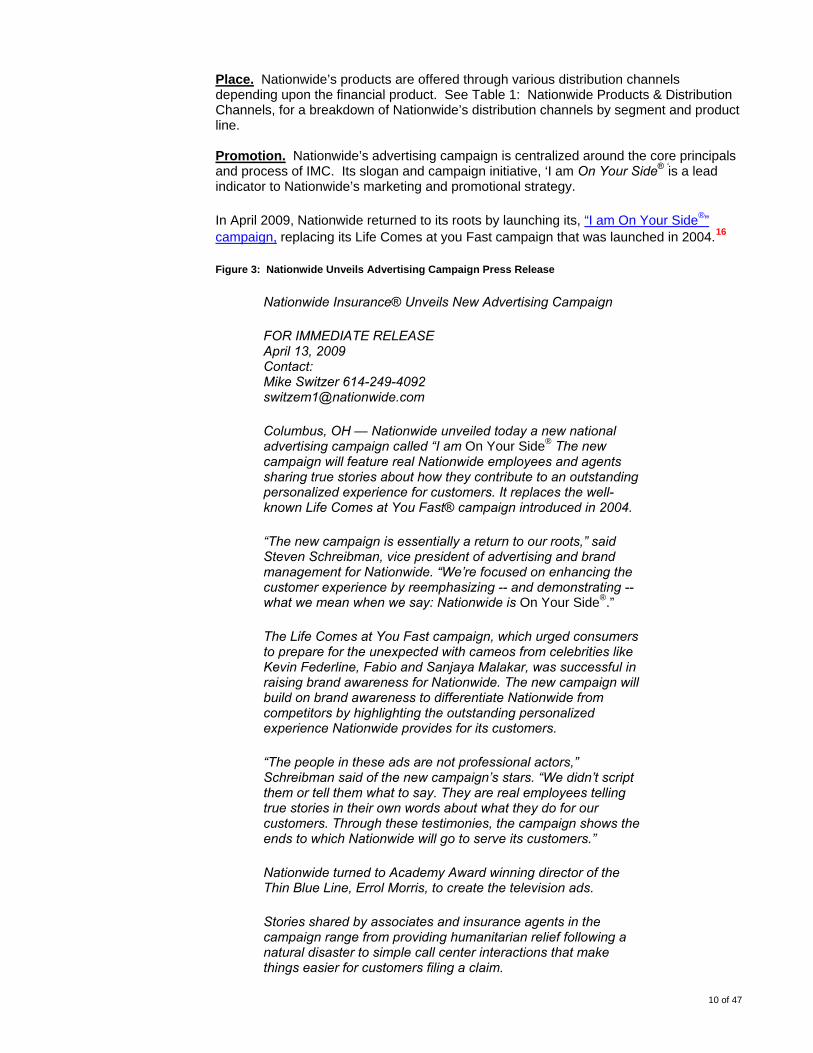

Place. Nationwide’s products are offered through various distribution channels depending upon the financial product. See Table 1: Nationwide Products & Distribution Channels, for a breakdown of Nationwide’s distribution channels by segment and product line. Promotion. Nationwide’s advertising campaign is centralized around the core principals and process of IMC. Its slogan and campaign initiative, ‘I am On Your Side® ‘is a lead indicator to Nationwide’s marketing and promotional strategy.

In April 2009, Nationwide returned to its roots by launching its, “I am On Your Side®” campaign, replacing its Life Comes at you Fast campaign that was launched in 2004.16

Figure 3: Nationwide Unveils Advertising Campaign Press Release

Nationwide Insurance® Unveils New Advertising Campaign

FOR IMMEDIATE RELEASE April 13, 2009 Contact: Mike Switzer 614-249-4092 [email protected]

Columbus, OH — Nationwide unveiled today a new national advertising campaign called “I am On Your Side® The new campaign will feature real Nationwide employees and agents sharing true stories about how they contribute to an outstanding personalized experience for customers. It replaces the well-known Life Comes at You Fast® campaign introduced in 2004.

“The new campaign is essentially a return to our roots,” said Steven Schreibman, vice president of advertising and brand management for Nationwide. “We’re focused on enhancing the customer experience by reemphasizing -- and demonstrating -- what we mean when we say: Nationwide is On Your Side®.”

The Life Comes at You Fast campaign, which urged consumers to prepare for the unexpected with cameos from celebrities like Kevin Federline, Fabio and Sanjaya Malakar, was successful in raising brand awareness for Nationwide. The new campaign will build on brand awareness to differentiate Nationwide from competitors by highlighting the outstanding personalized experience Nationwide provides for its customers.

“The people in these ads are not professional actors,” Schreibman said of the new campaign’s stars. “We didn’t script them or tell them what to say. They are real employees telling true stories in their own words about what they do for our customers. Through these testimonies, the campaign shows the ends to which Nationwide will go to serve its customers.”

Nationwide turned to Academy Award winning director of the Thin Blue Line, Errol Morris, to create the television ads.

Stories shared by associates and insurance agents in the campaign range from providing humanitarian relief following a natural disaster to simple call center interactions that make things easier for customers filing a claim.

11 of 47

The new campaign will include broadcast, cable, print, radio and online executions across the country. The new ads and related content, including behind the scenes footage is available at nationwide.com.

TM Advertising, based in Dallas, created the campaign.

Nationwide, based in Columbus, Ohio, is one of the largest and strongest diversified insurance and financial services organizations in the world and is rated A+ by A.M. Best. Nationwide ranks #108 on the Fortune 500 list. The company provides a full range of insurance and financial services, including auto insurance, motorcycle, boat, homeowners, life insurance, farm, commercial insurance, administrative services, annuities, mortgages, mutual funds, pensions, long-term savings plans and health and productivity services. For more information, visit www.nationwide.com.16

The ‘On Your Side®’ slogan and Nationwide logo is predominately displayed on most communication pieces, as a quick tour through the Nationwide website will quickly point out.

Figure 4: Nationwide Logo & Slogan17

Source: Nationwide website, www.nationwide.com

Nationwide’s “Watch My Story” , demonstrates Nationwide’s commitment to carry through the IMC, customer focused business process. The video and flashed based module presents unscripted Nationwide employees offering testimonials about its (and Nationwide’s) commitment to customers. The Watch My Story module extends creditability to Nationwide’s brand.18

As Figure 3: Nationwide Unveils Advertising Campaign Press Release indicates, Nationwide advertises through broadcast television/cable, web, print and radio to reach its target market. Nationwide also effectively utilizes Public Relations to promote branding. For example, “The “February through February”, 2009 campaign honoring National Black History month includes an interactive website where the public can publish significant moments of personal achievement within their African-American heritage. “ 19

In addition, Nationwide Insurance is the official sponsor of Auto, Home, and Life insurance for NASCAR. They have integrated the NASCAR sponsorship into is communication plan with a Nationwide NASCAR mico-website offering customers NASCAR schedules, a VIP sweepstakes opportunity to met Dale Earnhardt, Jr., NASCAR industry news articles and finally the opportunity to purchase Nationwide Auto insurance.20

Nationwide reaches its target base through personalized, seemingly tailored communications. For example, Nationwide offers a “RetireABILITY Check”, a personalized interactive tool that plays customized, pre-recorded seemingly tailored video clips from a database based on questionnaire responses. At the end of the “RetireABILITY Check” users receive and R-score, indicating retirement preparedness, and a summary of next steps to plan for retirement.21

12 of 47

Nationwide has recently begun to leverage social media venues like YouTube (35,722 channel views) 22 and Flicker.23 Mike Switzer, a spokesperson for Nationwide noted, “We [Nationwide] are now thinking holistically - using social media such as Facebook [1,650 fans], MySpace and Twitter [1270 followers], as well as mobile marketing through sports’ sponsorships, which we have done in the past, but which were probably not integrated into the broader campaign. Our strategy is not changing - it is still the ' On Your Side®' customer experience, but we are taking the strategy to the next level. Nationwide is outspent by our competitors, and we have to advertise and market 'smarter' to reach our target audience.”24

Figure 5: Nationwide Social Media Site Flicker

Source: Retrieved from http://www.flickr.com/photos/nationwide

Price. Nationwide does not compete on price; instead it competes on value add and creating new and innovative ideas, products and services. For instance, the newly released Nationwide iPhone application is new to the insurance industry.25 The iPhone application is open source, and allows customers to start a claims process when an accident occurs. Users can upload accident scene photos, call local authorities, and upload claims forms—directly from an iPhone. Since Nationwide has developed the application using open source code, not only can Nationwide’s customers use the application, consumers of competing insurance companies can utilize the application as well.26

Advertising Spend

In 2007 Nationwide, “spent nearly $185 million in major measured media, according to TNS Media Intelligence. Spending through the first nine months of 2008 exceeded $180 million.”27

13 of 47

Figure 6: Insurance Headlines, "Geico Advertising Spending Tops Among Auto Insurers In '06"

…[In 2006]The majority of advertising spending for the auto insurers was spent on television advertising, but there were some differences. Allstate spent the largest percentage of its ad budget on national television, while Geico had the most diversified mix, with more money spent on spot TV and radio than the others, with its spot market allocations very concentrated in the top 10 to 15 metropolitan areas. Progressive's spot broadcast advertising was more widely distributed, the study said.28

Figure 7: 2006 Auto Insurer Advertising Spend

GEICO $497 million subsidiary of Berkshire Hathaway

Progressive $257 million

Allstate $234 million

State Farm spent $152 million

Source: Retrieved from http://www.insuranceheadlines.com/Auto-Insurance/3882.html

Figure 8: InsuranceHits.com Press Release, “Marketing in the Insurance Industry”

Over the last ten years, advertizing spending [within the insurance industry] rose significantly but the spend slowly shifted from the traditional print and broadcast media, to niche marketing and the internet.

This general growth was fueled by competition for market share and, because the insurance industry was highly profitable, more money could be diverted to the marketing budget.

Today, the level of spending cannot be maintained. In fact, it has slowed quite significantly over the last eighteen months. There are two reasons for this. The market for insurance has peaked and is starting to contract in all segments as a looming recession forces policy holders to trim their budgets. Secondly, the price competition between the major insurers has reduced the level of profitability at a time of slowing revenue growth.

Despite this, the four leading insurers - Allstate, GEICO, Progressive and State Farm - have maintained brand awareness and their marketing activities pressure their smaller rivals to maintain their marketing momentum to avoid losing market share.

However, there is a potential problem. The growth of the internet has turned the standard policies of auto, health and homeowners into commodities. It has become easy for policy holders to obtain comparative quotes through sites like this. Policies can be written over the internet without the parties ever having to meet (whether directly or through an agent). So the advertising has to shift to differentiate the insurers and their policies. Price on its

14 of 47

own is not a key feature given the ease with which prices can be compared. That means a focus on other elements such as claims handling and customer service.

The internet is not passive. There are now customer sites which carry stories of poor service. The insurance industry is therefore having to spend less on marketing and more on actually delivering better service.

This has serious implications for media that have traditionally relied on advertising revenue from the advertising industry. Newspapers in particular have seen a dramatic drop in their insurance ad revenue. The new campaigns focus on market segments where growth is predicted.

More specialty products are being offered and Spanish language advertising to the Latino market has been growing. We can therefore expect to see a further reduction in marketing spend as the reality of a recession bites into consumer confidence.29

Figure 9: DMA Direct Marketing Facts and Figures in the Insurance Industry Press Release

DMA Releases 'Direct Marketing Facts and Figures in the Insurance Industry'

Direct Marketers in Insurance Field Saw $8.15 ROI for Every Dollar Spent New York, NY, January 23, 2008 — Insurance marketers last year spent $6.81 billion on direct marketing-related advertising expenditures, which in turn generated more than $55.53 billion in US sales. That is an impressive return on investment of $8.15 for every dollar spent. These are two of the top findings from the Direct Marketing Association’s (DMA) new report “Direct Marketing Facts and Figures in the Insurance Industry.” “DMA is releasing ‘Direct Marketing Facts and Figures in the Insurance Industry’ due to popular demand,” DMA Research Manager Michelle Tiletnick said. “Last year, we released the groundbreaking ‘Marketing Strategies for the Financial Services Industry,’ which was very successful. Based on feedback we received, customers wanted us to separate insurance from the rest of the financial services. They wanted a more focused, drilled-down report that looked exclusively at the insurance segment.” “This new report does that, shining DMA’s research spotlight on the employment of direct marketing to sell insurance products in the United States,” Tiletnick said. “Additionally, our report allows insurance companies to look at the current state of their multichannel direct marketing efforts and benchmark them against this report. Also, it gives them insight into what their near-term direct marketing future will hold.”

15 of 47

Other key findings from this report include: Direct marketing-driven sales are expected to grow at a rate

of 7.6 percent a year from 2007 to 2012. Direct marketing-driven employment is projected to rise

concurrently at a rate of 3.1 percent each year from 2007 to 2012.

Commercial email expenditures will skyrocket, seeing the

largest increase in direct marketing advertising spending in the insurance sector at 23.4 percent a year from 2007 to 2012.

The next largest advertising expenditure is projected to be in

Internet, at 18.7 percent each year from 2007 to 2012. Print advertising and telephone marketing spending will grow

the least, each increasing at 3.4 percent a year from 2007 to 2012.

Direct mail spending is expected to reach $2.2 billion in

2012, up from 2007’s $1.7 billion. Insert media advertising expenditures are expected to grow

7.4 percent each year from 2007 to 2012 Increases in broadcast advertising spending are expected to

reach 6.2 percent annually between 2007 and 2012.30

Market Position Nationwide Insurance is one of the largest national insurance companies in the United States, ranking 7 in total dollar volume in property and casualty direct premiums underwritten in 2007 and ranking 8 in property and casualty(P/C) annual revenues, according to the Insurance Information Institute.31 See Table 2: 2007 Top 10 Writer of P/C Insurance by Direct Premiums Written, Table 3: 2007 Top 20 US Property & Casualty Companies by Revenues and Table 4: Asset Capitalization of Top 20 P&C Companies by Revenues. Nationwide did not rank on the Insurance Information Institute’s 2007 top 20 health insurance providers ranking nor did Nationwide’s Annual Report reflect income from its health Insurance product segment in 2007.3 Nationwide did not enter the health care insurance segment until 2006 and thus was not in a position to be ranked among top health care providers in 2007. See Figure 10: Nationwide, 2007 Income Statement.

Other Nationwide significant rankings are as follows:

Property and Casualty Segment 3

4th-largest homeowners insurer 6th-largest auto insurer 9th-largest commercial insurer 6th-largest total property and casualty insurer

Life and Retirement Savings Segment 3

#1 provider of defined contribution plans #7 provider of variable life insurance #13 writer of individual variable annuities #18 U.S. life insurer based on premium #15 U.S. life insurer based on admitted assets

16 of 47

Table 2: 2007 Top 10 Writer of P/C Insurance by Direct Premiums Written

Source: Insurance Information Institute. Retrieved from http://www.iii.org/media/facts/statsbyissue/industry/

17 of 47

Table 3: 2007 Top 20 US Property & Casualty Companies by Revenues

Source: Insurance Information Institute. Retrieved from http://www.iii.org/media/facts/statsbyissue/industry/

18 of 47

Table 4: Asset Capitalization of Top 20 P&C Companies by Revenues

Source: Insurance Information Institute. Retrieved from http://www.iii.org/media/facts/statsbyissue/industry/

19 of 47

Figure 10: Nationwide, 2007 Income Statement

Source: Retrieved from http://www.nationwide.com/pdf/news-2007-annual-report.pdf

20 of 47

Nationwide Value Proposition The Nationwide value proposition is the ‘I am On Your Side® promise. Through this promise Nationwide reaches out to its customers and prospects to hear their needs, evaluate each person’s individual situation and deliver custom service. In addition, the On Your Side® promise includes being active in the communities in which it does business. For instance, Nationwide has sponsored three annual “Get Real” events where employee Lu Yardgrough conducted a hands on simulation to high school and college students. Students experienced buying a house, purchasing car insurance and making other economic decisions that are critical to making sound financial choices.32 Video casts further define the On Your Side® promise. Video cast topics include:

Doing things Better. Meet Michael Piccerello and find out how Nationwide's customers help us do things better. Nationwide is On Your Side.® Call 1-877-Nationwide today. Helping Your Community. Meet Ana Quevedo and find out how Nationwide Insurance is helping to make communities safer for families and children. Nationwide is On Your Side.® Call 1-877-Nationwide today. Prize Fight. Filing a claim with your insurance company doesn't have to be a prize fight. Meet Terry Medley, Nationwide Property Claims Representative. Nationwide is On Your Side. ® Call 1-877-Nationwide® today.

Second Chance. Need a second chance? With Nationwide Accident Forgiveness, your premium won't go up for your first accident. Call 1-877-Nationwide® to see if Accident Forgiveness is available in your area. Nationwide Mobile App. Nationwide is the first insurance company with a claims app for the iPhone. Meet Kathy Shear and find out how Nationwide Mobile can help you if you're in an accident. Nationwide is On Your Side.® Call 1-877-Nationwide today. Get the app.

In Times of Need. Meet Estrella Solorzano and find out how Nationwide helps customers in times of need. Nationwide is On Your Side.® Call 1-877-Nationwide today. Game of Life. Meet Lu Yarbrough and find out what Nationwide is doing to help improve financial literacy in our communities. Nationwide is On Your Side.® Call 1-877-Nationwide® today.32

The Nationwide Customer & Target Market Nationwide targets three types of customers and prospects: individual consumers, businesses, and farm/ranch owners. Nationwide does not target price sensitive customers and chooses to differentiate its products based on value add, not price.

The Individual Consumer Segment. Nationwide’s target market for individuals includes all ethnic backgrounds that have financial insurance, investment and banking needs including: property and casualty insurance, health insurance, life insurance, retirement plans, savings, banking and mortgages.

Further Segmentation

“By focusing on three core businesses - the property/casualty insurance business, the life and retirement savings business, and the asset management business - we remain committed to increasing the value our customers have come to expect from us.”6

21 of 47

Nationwide’s commitment to target diverse ethnicities can be evidenced by its 2008 campaign, “Life comes at you Fast”, which targeted the U.S. South Asian population.

Connecting with the rapidly growing South Asian population is very important to us,” said Tariq Khan, vice president of market development and diversity for Nationwide Financial Network, an affiliated retail distribution business of Nationwide Financial Services, Inc. (NYSE: NFS). “We wanted to create work that reflects scenarios and traditions that are relevant to them. This campaign is an example of our growing support of diverse markets.’

Five TV spots will appear on prominent South Asian networks, and a print campaign will run in major newspapers. There will also be online, in-theater and other out-of-home executions. The campaign will be national with a focus in key South Asian markets.

Additionally, Nationwide is sponsoring several South Asian events, including the India Independence Day Parade, Pakistan Parade and Diwali celebrations in November.

Nationwide is also reaching out to the U.S. Spanish speaking population as evidenced by its Spanish TV commercials.33

Individual Consumer Segment Psychographics & Behavior Nationwide consumers are typically employed, own personal property, have a family, drive a car, have a banking account(s)/financial needs, get sick, have accidents and thus have insurance protection needs. Individual Consumer Segment Demographics Typically, the Nationwide consumer is over 18-years of age. Nationwide customers generally live in the United States and may be of any nationality. Currently, Nationwide has specifically reached out to the African American community, Asians and the rapidly growing Spanish population.

The Business Segment. Nationwide targets corporations ranging from small business owners who have business insurance needs to larger corporations needing asset management plans, employee benefit plan administration.

The Farm & Ranch Segment. Nationwide’s third target market includes Farm and Ranch owners who need specific insurances related to farming and ranch tending, like equipment breakdown insurance, disruption of income insurance, or crop insurance.

Nationwide’s target segments are compared in Figure 11: 2007 Target Segment Revenues in Dollar Volume in terms of annual revenue generated by segment as noted by Nationwide’s 2007 Annual Report.

22 of 47

Figure 11: 2007 Target Segment Revenues in Dollar Volume

Source: Retrieved from http://www.nationwide.com/pdf/news-2007-annual-report.pdf

Customer Feedback Nationwide has done an excellent job of examining its organization from the customer’s point of view through surveys. For example, Nationwide examines its communications through ForeSee online customer satisfaction survey(s).34

Another example where Nationwide has reached out to customers and implemented a need is through its Nationwide Mobile App for the iPhone. Nationwide has developed the application for the iPhone allowing iPhone policy holders to file an accident report from their mobile phone including taking and uploading accident scene photographs and completing the accident form online, right from their mobile phone through the Nationwide application.25

Nationwide reaches out to suppliers by commutating Nationwide’s brand message through training and mentoring. Its Supplier Diversity Statement, points out this commitment, “At Nationwide® we're committed to identifying and establishing effective and positive business relationships with diverse suppliers. Nationwide recognizes the strong connection between our customers and the many relationships we have with diverse suppliers who help us meet our customer's needs. That is why we are committed to developing and implementing a process that promotes contracting with, educating, and mentoring diverse suppliers to improve their interactions with us and build their business.”12

Measuring & Implementing Feedback. Chris Cotton, Director of Marketing at Nationwide offered insight into the importance of and how Nationwide evaluates marketing analytics and customer feedback. Cotton was quoted during the Attribution Management Forum, hosted by ClearSaleing Inc. on Tuesday, October 28, 2008, “Now that we [Nationwide] have a robust advertising analytics platform in place that allows us to do cross-media profit tracking and identify and assemble all participating ads that contributed to a sale or conversion, the remaining challenge is to properly assign the value of the sale or conversion across the team of ads that contributed to it.” 35

23 of 47

Figure 12: Nationwide Marketing Research & Analytics Partnership with Ohio State University

The Nationwide Center for Advanced Customer Insights (NCACI) is a marketing research center developed as a partnership between the Nationwide Insurance Company and The Ohio State University. The center conducts insurance and financial product marketing research for Nationwide using state of the art predictive modeling, data mining and advanced analytical techniques that improve Nationwide's understanding of consumer behavior and purchasing patterns.

The center employs the best in class Ohio State faculty, staff and graduate students from across the university, including faculty and students from the Marketing, Statistics, Psychology, Economics and Computer Science Departments.

The center manages research projects involving the application of existing theory and methodologies to solve specific marketing problems as well as projects requiring the conduct of seminal research to develop new analytical methodologies. The center also offers Ohio State faculty and graduate students direct access to Nationwide customer and marketing data.36

Due to proprietary, inside information, further information was unavailable regarding Nationwide’s practices of measuring customer feedback and revising/implementing business plans based upon data collected.

Industry Overview & Background

“In the US, about 7,500 companies provide insurance coverage of various types and have combined annual revenue of $1 trillion. Large companies include AIG1, Aetna's Group Insurance division, MetLife, Allstate, State Farm, and GEICO. The industry is highly concentrated: the 50 largest companies hold more than 60 percent of the market. Within product segments, concentration is even higher.”37 Table 2, Table 3, and Table 4 presented under the Market Position heading, offer a good picture of the insurance industry competitive landscape, which includes:31

Allstate Insurance Group American Family Insurance Group American International Group (AIG) Assurant Auto-Owners Insurance Berkshire Hathaway Insurance Group Chubb Erie Insurance Group Fidelity National Financial First American Corp. Hartford Fire & Casualty Group Liberty Mutual Insurance Group Loews (CNA) Nationwide Group Progressive Group Safeco State Farm Group Travelers Group United Services Automobile Association (USAA) W.R. Berkley Zurich Insurance Group Notable mentions that did not appear in the list above are the following companies: GEICO Insurance and small regional insurance companies. GEICO is a wholly owned subsidiary of Berkshire Hathaway Insurance Group, which is included in the list above.

1 AIG, American Insurance Group is a recipient of the Troubled Asset Relief Program (TARP).

24 of 47

Demand [within the Insurance Industry] is driven by demographics and commercial transactions. Demand is also driven by legal or financial requirements. Consumers are usually required by states to buy auto insurance and by lenders to buy homeowners insurance, for example. The profitability of individual companies depends on effective marketing and on the ability to accurately estimate future payments. Large companies have big economies of scale in administration and in access to capital, as well as advertising and marketing. Small companies can compete successfully by specializing in particular products or industries. Average annual revenue per worker is around $400,000, so the industry is not labor-intensive. In the late 2000s recession, insurers saw revenues decline sharply when their investment portfolios lost value after the market fell. Insurance carriers rely heavily on their investment portfolios, which is where they invest premiums collected until they are needed to pay claims or benefits. In addition, deregulation of the insurance and financial services industries led to increased risk taking that hurt insurers' credit ratings. Insurance giant AIG was forced to accept $150 billion in government loans to stave off bankruptcy that was brought on by its overexposure to credit default swaps. Federal government bailouts have primarily targeted banks. Aside from AIG, insurance companies have not been as hard hit by the subprime mortgage meltdown. But some insurance companies are seeking relief from state regulators to allow them to operate with less capital. Other insurance companies are buying financial institutions to qualify for federal aid.3737

At a Glance

The insurance industry’s net premiums written totaled $1.1 trillion in 2007, with premiums recorded by life/health insurers accounting for 58 percent and premiums by property/casualty insurers accounting for 42 percent.

Property/casualty insurance consists mainly of auto, home and commercial insurance, as well as a small amount of health insurance. Net premiums written for the sector totaled $448 billion in 2007.

The life/health insurance sector consists of annuities and life insurance, along with some health insurance. Net premiums written for the sector totaled $617 billion in 2007.

Private health insurance is generally considered separately. It accounted for $331 billion in premiums in 2007, not including the health premiums written by L/H insurers ($155 billion in 2007) and P/C insurers ($7 billion in 2007).

There were 2,723 P/C insurance companies and 1,190 L/H insurance companies in the United States in 2007.

Insurance carriers and related activities accounted for $281 billion or 2.1 percent of U.S. gross domestic product in 2006 (latest data available).

The U.S. insurance industry employed 2.3 million people in 2008. Of those, 1.4 million worked for insurance companies, including life, health and medical insurers (804,200 workers) property/casualty insurers (569,200 workers) and reinsurers (28,400 workers). The

25 of 47

remaining 907,000 work for insurance agencies, brokers and other insurance related enterprises.

Total P/C cash and invested assets were $1.3 trillion in 2007. L/H cash and invested assets totaled $3 trillion in 2007.

In 2007, P/C insurers invested 66 percent of their assets in bonds, highly liquid securities which can be sold quickly to pay claims in the event of a major disaster. L/H insurers invested 73 percent of their assets in bonds.

Insurance companies, including P/C and L/H, paid $15.7 billion in premium taxes in 2008, or $52 for every person living in the United States.

P/C insurers paid out $25.2 billion to their policyholders for insured losses from catastrophes in 2008, including $10.7 billion caused by Hurricane Ike, $2.1 billion from Hurricane Gustav, and $3.6 billion from tornadoes and related damage.31

Nature of the Industry

Goods and services. The insurance industry provides protection against financial losses resulting from a variety of perils. By purchasing insurance policies, individuals and businesses can receive reimbursement for losses due to car accidents, theft of property, and fire and storm damage; medical expenses; and loss of income due to disability or death.

Industry organization. The insurance industry consists mainly of insurance carriers (or insurers) and insurance agencies and brokerages. In general, insurance carriers are large companies that provide insurance and assume the risks covered by the policy. Insurance agencies and brokerages sell insurance policies for the carriers. While some of these establishments are directly affiliated with a particular insurer and sell only that carrier’s policies, many are independent and are thus free to market the policies of a variety of insurance carriers. In addition to supporting these two primary components, the insurance industry includes establishments that provide other insurance-related services, such as claims adjustment or third-party administration of insurance and pension funds.

These other insurance industry establishments also include a number of independent organizations that provide a wide array of insurance-related services to carriers and their clients. One such service is the processing of claims forms for medical practitioners. Other services include loss prevention and risk management. Also, insurance companies sometimes hire independent claims adjusters to investigate accidents and claims for property damage and to assign a dollar estimate to the claim.

Insurance carriers assume the risk associated with annuities and insurance policies and assign premiums to be paid for the policies. In the policy, the carrier states the length and conditions of the agreement, exactly which losses it will provide compensation for, and how much will be awarded. The premium charged for the policy is based primarily on the amount to be awarded in case of loss, as well as the likelihood that the insurance carrier will actually have to pay. In order to be able to compensate policyholders for their losses, insurance companies invest the money they receive in premiums, building up a portfolio of financial assets and income-producing real estate which can then be used to pay

26 of 47

off any future claims that may be brought. There are two basic types of insurance carriers: primary and reinsurance. Primary carriers are responsible for the initial underwriting of insurance policies and annuities, while reinsurance carriers assume all or part of the risk associated with the existing insurance policies originally underwritten by other insurance carriers.

Primary insurance carriers offer a variety of insurance policies. Life insurance provides financial protection to beneficiaries—usually spouses and dependent children—upon the death of the insured. Disability insurance supplies a preset income to an insured person who is unable to work due to injury or illness, and health insurance pays the expenses resulting from accidents and illness. An annuity (a contract or a group of contracts that furnishes a periodic income at regular intervals for a specified period) provides a steady income during retirement for the remainder of one’s life. Property-casualty insurance protects against loss or damage to property resulting from hazards such as fire, theft, and natural disasters. Liability insurance shields policyholders from financial responsibility for injuries to others or for damage to other people’s property. Most policies, such as automobile and homeowner’s insurance, combine both property-casualty and liability coverage. Companies that underwrite this kind of insurance are called property-casualty carriers.

Some insurance policies cover groups of people, ranging from a few to thousands of individuals. These policies usually are issued to employers for the benefit of their employees or to unions, professional associations, or other membership organizations for the benefit of their members. Among the most common policies of this nature are group life and health plans. Insurance carriers also underwrite a variety of specialized types of insurance, such as real-estate title insurance, employee surety and fidelity bonding, and medical malpractice insurance.

Other organizations in the industry are formed by groups of insurance companies, to perform functions that would result in a duplication of effort if each company carried them out individually. For example, service organizations are supported by insurance companies to provide loss statistics, which the companies use to set their rates.38

Industry regulation. The insurance industry is regulated by the federal and state governments. Each state has an insurance commission(or department) that is mostly responsible for regulating insurance companies within its state. Depending upon what type of financial products an insurance company offers dictates the regulating body. Regulation bodies may include but are not limited to local State Insurance Commissions and the Securities and Exchange Commission.

Insurance agents must be licensed in every state in which they do business. Licenses are designated by the type such as life and health, property and casualty. If an agent sells variable annuities, they must also hold a securities license, which is governed by the Securities and Exchange Commission.

An example of the licensing and regulating body in Ohio is available at http://www.insurance.ohio.gov/Pages/default.aspx. Nationwide and its agents must also be licensed in every state in which it conducts business.39

27 of 47

Recent developments. Congressional legislation now allows insurance carriers and other financial institutions, such as banks and securities firms, to sell one another’s products. More insurance carriers now sell financial products such as securities, mutual funds, and various retirement plans. This approach is most common in life insurance companies that already sold annuities, but property and casualty companies also are increasingly selling a wider range of financial products. In order to expand into one another’s markets, insurance carriers, banks, and securities firms have engaged in numerous mergers, allowing the merging companies access to each other's client base and geographical markets.

Insurance carriers have discovered that the Internet can be a powerful tool for reaching potential and existing customers. Most carriers use the Internet simply to post company information, such as sales brochures and product information, financial statements, and a list of local agents. However, an increasing number of carriers are starting to expand their Web sites to enable customers to access online account and billing information, and some carriers even allow claims to be submitted online. Many carriers also provide insurance quotes online based on the information submitted by customers on their Internet sites. In fact, some carriers will allow customers to purchase policies through the Internet without ever speaking to a live agent.

In addition to individual carrier-sponsored Internet sites, several “lead-generating” sites have emerged. These sites allow potential customers to input information about their insurance policy needs. For a fee, the sites forward customer information to a number of insurance companies, which review the information and, if they decide to take on the policy, contact the customer with an offer. This practice gives consumers the freedom to accept the best rate.38

Game Changes. Over the last decade there has been a paradigm shift in personal lines insurance selling and promotion. The likes of Geico, Nationwide and Progressive have changed the game and the way in which it's played. Direct-to-consumer is what it's all about today. Why is it successful? Because direct-to-consumer means lower costs by eliminating the commissions the insurance agents enjoyed year after year. Today, Geico spends over $500 million reaching out to consumers. Direct-to-consumer is here to stay in this category. It's a whole new game.

This new battle is being played out in the digital world. New players are dominating the conversation. They've found new ways to reach out to customers, young and old, and get them to change the way they think about having to deal with insurance carriers. This is especially critical with older audiences who grew up with the bias that you bought your insurance through an insurance agent. That's a paradigm that no longer applies. The game has changed as we know it, especially for those of us who are over 50 years old.

The challenge is that as the Geico's, Progressive's and Nationwide's grow and evolve as brands, it is imperative that they find innovative ways to differentiate themselves. You can't compete on price alone. It's proven that if you compete on a price model, your margin will slowly erode year after year. They will have to find ways to maintain brand preference and, more importantly, get people to switch to their brand.

28 of 47

All of this leads to why I like Nationwide's newest product discriminator so much. Last month they introduced a new Nationwide iPhone application. It's a great product (and it's free, which makes it even better) that helps people who have been in an accident contact local authorities or emergency services, start the claims process and/or use the phone to take down information. It's essentially a checklist that helps you to think clearly at a time when you're distraught emotionally and, heaven forbid, hurt physically. The beauty is that Nationwide's new tool goes beyond being just a tool, and it does it whether or not you're a Nationwide customer - it's truly open. It's a brand differentiator and a category game changer in one. I'm sure that the Geico's and the Progressive's are going to offer an equivalent product, but Nationwide is in first. In the laws of the marketing jungle, he who is first in usually dominates. A game changer in the truest sense.26

Significant Industry Points

Job growth in this large industry will be limited by corporate downsizing, new technology, and increasing direct mail, telephone, and Internet sales, but numerous job openings will arise from the need to replace workers who leave or retire.

Growing areas of the insurance industry are medical services and health insurance, and its expansion into other financial services, such as securities and mutual funds.38

The Treasury Department recently announced that it has decided to extend federal bailout eligibility to struggling life insurance companies. Treasury officials are reviewing applications from about a dozen large insurance companies seeking a share of what is left of the Trouble Asset Relief Program (TARP) after the financial and auto industry bailouts.40See Figure 13: Excerpt from the New York Times, Tracking the $700 Billion Bailout.41

29 of 47

Figure 13: Excerpt from the New York Times, Tracking the $700 Billion Bailout

30 of 47

Economic Situation Current economic conditions are poor with high unemployment rates across the U.S. The banking and automotive industries have placed an enormous economic strain on the U.S. government and economy due to billion dollar bail-out packages. Consumer confidence and spending are also low. The United States Department of Labor reported, “Nonfarm payroll employment continued to decline in June (-467,000),and the unemployment rate was little changed at 9.5 percent”. Job losses were widespread across the major industry sectors, with large declines occurring in manufacturing, professional and business services, and construction.”42

The Consumer Confidence index stands at 49.3. “Says Lynn Franco, Director of The Conference Board Consumer Research Center: ‘After back-to-back months of strong gains, Consumer Confidence retreated in June. The decline in the Present Situation Index, caused by a less favorable assessment of business conditions and employment, continues to imply that economic conditions, while not as weak as earlier this year, are nonetheless weak. Looking ahead, Expectations continue to suggest less negative conditions in the months ahead, as opposed to strong growth.’”43

The Deloitte Consumer Spending Index declined again in May, driven downward primarily by the housing market. The Index attempts to track consumer cash flow as an indicator of future consumer spending.

“The year over year pace of decline in real consumer spending appears to have stabilized, however, recovery is being delayed by a sharp increase in consumer savings, which has risen to 5.7 percent from zero a year ago,” said Carl Steidtmann, chief economist with Deloitte Research, a subsidiary of Deloitte Services LP, and author of the monthly Index. “However, the weakness in the Index was driven almost entirely by falling home prices, which are down nearly 14 percent over the past year, undermining small gains in real wages, a declining tax burden and current stabilization in new unemployment claims.

The Index, comprising four components ― tax burden, initial unemployment claims, real wages and real home prices ― fell to 1.35 percent from an downwardly revised gain of 1.44 percent a month ago.

“The lack of improvement in the index suggests that consumers are still feeling the pressures of the economy,” said Stacy Janiak, vice chairman and U.S. Retail leader, Deloitte LLP. “Additionally, even when a recovery takes hold and spending strengthens, consumers will likely remain focused on value. Retailers should consider strategies that strike a connection with customers looking to keep expenditures down without trading down. That might mean expanding or reinventing a private label brand in a way that not only offers the right price point, but a certain amount of cache as well.”

Highlights of the Index include:

Tax burden: The tax burden continues to fall with the weakening of the economy. The tax burden is at a level only seen on a few occasions over the past 50 years during brief periods following tax rebates. Continued decline is expected.

Initial unemployment claims: Claims appear to have stabilized for the moment and in recent weeks have come down. While still at very elevated levels, the future direction of claims remains uncertain given sizable layoffs that are expected from the auto and auto dealer sectors of the economy.

31 of 47

Real wages: Real wage growth continues to post small gains due in large part to falling prices for energy. Real wages are up 4.3 percent from a year ago and on an annualized basis are up 8.0 percent over the last nine months as energy prices have given a big boost to consumer purchasing power.

Real home prices: Home prices continue to fall. Renewed efforts to forestall foreclosures coupled with a tax credit for home buyers may bring some stability to this market. The decline in home prices has made home buying much more affordable. What is lacking is mortgage financing and stable prices.”44

Legal During the 1990’s the public perception of Nationwide was dramatically different that Nationwide’s public image today. During the 1990’s Nationwide Insurance was involved in discriminatory practices violating the Civil Rights act of 1968 and the Fair Housing Act of 1988 in which the U.S Department of Justice outlined in Figure 14: U.S. Department of Justice vs Nationwide in Civil Action Suit.45

Figure 14: U.S. Department of Justice vs Nationwide in Civil Action Suit

CIVIL ACTION No. C2-97-291

UNITED STATES OF AMERICA, Plaintiff,

v

NATIONWIDE MUTUAL INSURANCE COMPANY; AND NATIONWIDE MUTUAL FIRE INSURANCE COMPANY, Defendants.

COMPLAINT

The United States of America alleges as follows:

1. The United States brings this action pursuant to the Fair Housing Act, Title VIII of the Civil Rights Act of 1968, as amended by the Fair Housing Act of 1988, 42 U.S.C. 3601, et seg.

2. This Court has jurisdiction of this action under the provisions of 28 U.S.C. 1345 and U.S.C. 3614(a).

3. The defendants (hereafter referred to jointly as "Nationwide") are affiliated domestic corporations which operate as one company under the Nationwide Mutual Insurance umbrella. Nationwide Mutual Insurance Company and Nationwide Mutual Fire Insurance Company are incorporated under the laws of the State of Ohio with their principal places of business in Columbus, Ohio, in the Southern District of Ohio. Nationwide Mutual Insurance Company, through its subsidiaries, operates insurance companies throughout the United States. Nationwide Mutual Fire Insurance Company is the entity which actually writes homeowners insurance.

4. Nationwide writes insurance, including homeowners insurance, in all fifty states in the country. Nationwide ranks fifth in the country in market share for homeowners insurance, with a total of 3,050,635 policies for all fire lines -- homeowners, inland marine, and property fire -- in effect as of. December, 1996. Nationwide's country-wide market share for homeowners insurance is 3.1% as of 1995.

5. The majority of Nationwide's business is in states east of the Mississippi River. Nationwide has the greatest number of its homeowners insurance policies in the states of Ohio, Pennsylvania, and North Carolina. Nationwide ranks second in the

32 of 47

homeowners insurance markets in the states of Ohio and North Carolina, with 358,997 policies comprising 10.3% market share in Ohio, and 344,491 policies comprising 16.1% market share in North Carolina. In Pennsylvania, Nationwide ranks third in the homeowners insurance market, with 289,300 policies in effect, and a market share of 9.7%.

6. The residential housing patterns in many of the cities where Nationwide does business are racially segregated. Readily identifiable neighborhoods exist in these cities which are predominantly minority in population. Nationwide has been aware of the racial and ethnic composition of these neighborhoods at all times relevant to this complaint.

7. As described below in paragraphs 9 through 11, Nationwide has established, implemented and maintained eligibility criteria for its homeowners insurance policies that discriminate against homeowners in minority neighborhoods in areas in which Nationwide does business and are not justified by legitimate business considerations.

8. Nationwide traditionally has offered two basic forms of homeowners insurance: repair cost coverage policies and replacement cost coverage policies. Replacement cost coverage policies are superior, for several reasons. In the case of damage constituting a total loss of a home, repair cost coverage provides the homeowner with compensation only up to the current market value of the home, even if the cost of replacing the home exceeds that market value. Replacement cost policies provide the full cost of replacement, even if the cost of replacing the home exceeds the market value. Additionally, replacement cost policies generally provide significantly better coverage at a lower premium cost per dollar of insurance coverage than do repair cost policies.

9. Nationwide has established, implemented and maintained minimum home market value criteria for the availability of homeowners insurance coverage and the availability of replacement cost coverage. Such minimum value criteria discriminate against homeowners in minority neighborhoods in areas in which Nationwide does business, as often properties in such neighborhoods sell for an amount that is less than these minimum values. For example, in Philadelphia, Nationwide does not offer replacement cost policies on homes with a value under $50,000, and does not offer even repair cost homeowners insurance on homes valued under $45,000. 1990 Census data shows that in Philadelphia County, 70.5% of houses in majority minority census tracts have values under $40,000, and 80.9% have values under $50,000. This compares with only 23.2% of houses valued under $40,000 and 33.5% under $50,000 in majority white census tracts in Philadelphia County. As a result of Nationwide's minimum home value criteria, many properties in minority neighborhoods in areas in which Nationwide does business may not be eligible for insurance coverage at all, or may only qualify for inferior repair cost coverage.

10. Nationwide has established, implemented and maintained eligibility criteria for its homeowners insurance policies which set maximum home ages for the availability of replacement cost coverage. Homes thirty years of age and older are ineligible for the Golden Blanket Policy, Nationwide's most comprehensive policy. Nationwide discourages writing any replacement cost policy on homes over thirty years old. This maximum age criteria discriminates against homeowners in minority communities in areas in which Nationwide does business.

11. Nationwide has established, implemented and maintained eligibility criteria for its homeowners insurance policies which require that the market value of a home be from 70% to 80% of the replacement cost in order to obtain replacement cost coverage. In many cities in this country in which Nationwide does business, residential properties in minority neighborhoods sell for an amount that is significantly less than the cost necessary to rebuild the dwellings. Accordingly, these criteria of Nationwide result in less access to homeowners insurance for homeowners in minority neighborhoods in areas in which Nationwide does business.

33 of 47

12. The eligibility criteria described in paragraphs 9 through 11 are not necessitated by considerations of risk, profit, or any other legitimate race-neutral business consideration. Alternative method's are available which would accomplish the business objectives forming the ostensible rationale for these practices without the substantial and disproportionate burden on residents of minority neighborhoods.

13. In large part because of the discriminatory policies described above and other policies, Nationwide has taken other actions described immediately below to limit the opportunities of minorities to obtain homeowners insurance.

14. Nationwide has imposed geographic restrictions on writing homeowners insurance in areas where minority persons are in the majority. In particular, Nationwide employees, including underwriters, district managers, and other management employees, have instructed sales agents that Nationwide did not desire homeowners insurance business from neighborhoods with substantial minority populations. Nationwide conveyed this information through the use of maps as well as oral and written instructions.

15. In order to avoid doing business with homeowners in minority neighborhoods, members of Nationwide's management have criticized agents for doing business in minority areas, have explicitly based decisions regarding the processing of insurance claims on the basis of race, and have pressured agents in minority areas to move their offices out of urban areas and into surrounding suburbs which are predominantly white.

16. Nationwide's marketing strategy identifies particular geographic areas as growth areas which managers and agents are directed to target in selling Nationwide Insurance. In the 1990s, one of the principal forms for this marketing analysis has been Local Area Marketing Plans or LAMP reports. The areas targeted pursuant to these marketing plans have been predominantly white in population.

17. The actions of Nationwide described in paragraphs 14 through 16 were intentional, willful, and taken with reckless disregard for the rights of persons aggrieved by such actions.

18. Nationwide's actions as alleged herein constitute:

a. A pattern or practice of resistance to the full enjoyment of rights secured by the Fair Housing Act, as amended, 42 U.S.C. 3601, et seg.; and

b. A denial of rights granted by the Fair Housing Act, as amended, 42 U.S.C. 3601, et seg., to a group of persons that raises an issue of general public importance.

19. The totality of Nationwide's standards, practices, and procedures, as described above, constitutes:

. Making unavailable or denying dwellings to persons, because of race, color, and national origin, in violation of Section 804(a) of the Fair Housing Act, 42 U.S.C. 3604(a);

a. Discriminating on the basis of race, color, and national origin, in the terms, conditions, or privileges of the provision of services or facilities in connection with the sale or rental of dwellings, in violation of Section 804(b) of the Fair Housing Act, 42 U.S.C. 3604(b); and

b. Making, printing, or publishing of a statement that indicates a preference, limitation, or discrimination based on race, color, and national origin, with respect to the sale or rental of a dwelling, in violation of Section 804(c) of the Fair Housing Act, 42 U.S.C. 3604(c).

20. Persons who have been victims of Nationwide's discriminatory policies and practices as described above, are aggrieved persons within the meaning of 42 U.S.C. 3602(i). These aggrieved persons have suffered damages as the result of Nationwide's conduct.

34 of 47

WHEREFORE, the United States prays that the Court enter a judgment:

1. Declaring that the actions of Nationwide described above constitute a violation of the Fair Housing Act, as amended, 42 U.S.C. 3601, et seg.;

2. Enjoining Nationwide, its agents, employees, successors, and all other persons in active concert or participation with it, from discriminating in any aspect of its homeowners insurance activities because of the predominant race, color, or national origin of an individual insured or prospective insured, or of the neighborhood in which a home may be located;

3. Requiring Nationwide to develop, and present for this Court's review, a detailed plan to ensure that Nationwide's homeowners insurance is available to all persons in cities in which it does business regardless of the racial and ethnic characteristics of the neighborhood in which their home is located, and to repair the harm done because of its discriminatory activity;

4. Requiring Nationwide to review applications for insurance coverage on homes located in predominantly minority areas under the same standards, and according to the same nondiscriminatory underwriting criteria, as applied to homes in majority white areas;

5. Requiring Nationwide to provide such monetary relief as necessary to remedy the harms caused by Nationwide's discriminatory practices;

6. Requiring Nationwide to pay punitive damages; and

7. Assessing a civil penalty against the defendants to vindicate the public interest.

The United States further prays for such additional relief as the interests of justice may require together with the costs and disbursements of this action.

JANET RENO Attorney General

ISABELLE KATZ PINZLER Acting Assistant Attorney General Civil Rights Division

PAUL F. HANCOCK Chief, Housing and Civil Enforcement Section Civil Rights Division

BRIAN F. HEFFERNAN SHARON BRADFORD FRANKLIN STEVEN J. MULROY Attorneys, Housing and Civil Enforcement Section Civil Rights Division U.S. Department of Justice P.O. Box 65998 Washington DC 20035 (202) 514-4736

DALE ANN GOLDBERG (0005054) United States Attorney Southern District of Ohio

JAMES E. RATTAN (0018632) Assistant U.S. Attorney 280 North High Street, 4th Fl. Columbus, OH 43215 (614) 469-5715

Source: U.S Justice Department. CIVIL ACTION No. C2-97-291

35 of 47