Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected]) https://mlebredefreitas.wordpress.com , 10/06/2018 1 National Accounts Index: National Accounts .......................................................................................................... 1 1.1 Introduction ........................................................................................ 3 1.2 Basic concepts.................................................................................... 3 1.3 Expenditure, production and income ................................................. 4 1.3.1 Gross National Expenditure (Final Domestic Demand) ............................ 4 1.3.2 Gross Domestic Product ............................................................................ 5 1.3.3 Gross National Income .............................................................................. 6 Box 1: Three approaches to measure economic activity........................................ 8 1.4 The Current Account ........................................................................ 10 1.4.1 From National Income to Disposable Income ......................................... 10 1.4.2 The Current Account................................................................................ 10 1.4.3 Savings and investment............................................................................ 11 1.5 The Balance of payments ................................................................. 12 1.5.1 The Capital Account ................................................................................ 13 1.5.2 The Financial Account ............................................................................. 14 1.5.3 The three components of the balance of payments .................................. 14 1.5.4 The Balance of payments identity............................................................ 15 1.5.5 Net errors and omissions.......................................................................... 15 1.6 The Net International Investment Position ...................................... 16 1.6.1 Changes in NIIP ....................................................................................... 16 Box 2: The Net International Financial Position in Portugal ............................... 17 1.6.2 Reserve Asset Transactions ..................................................................... 18 1.6.3 The analytical presentation of the Balance of Payments ......................... 19 Box 3 – The Balance of Payments of Angola ...................................................... 20 1.7 Budget constraints of institutional units .......................................... 21 1.7.1 Non-Financial Private sector.................................................................... 21 1.7.2 Government.............................................................................................. 23 1.7.3 Central bank ............................................................................................. 24

national accounts - SWEETsweet.ua.pt/afreitas/aulas/notas apoio/national accounts.pdf · Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected]) ,

Jun 05, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 1

National Accounts

Index:

National Accounts..........................................................................................................1

1.1 Introduction........................................................................................3

1.2 Basic concepts....................................................................................3

1.3 Expenditure, production and income .................................................4

1.3.1 Gross National Expenditure (Final Domestic Demand) ............................4

1.3.2 Gross Domestic Product ............................................................................5

1.3.3 Gross National Income ..............................................................................6

Box 1: Three approaches to measure economic activity........................................8

1.4 The Current Account........................................................................10

1.4.1 From National Income to Disposable Income .........................................10

1.4.2 The Current Account................................................................................10

1.4.3 Savings and investment............................................................................11

1.5 The Balance of payments.................................................................12

1.5.1 The Capital Account ................................................................................13

1.5.2 The Financial Account.............................................................................14

1.5.3 The three components of the balance of payments ..................................14

1.5.4 The Balance of payments identity............................................................15

1.5.5 Net errors and omissions..........................................................................15

1.6 The Net International Investment Position ......................................16

1.6.1 Changes in NIIP.......................................................................................16

Box 2: The Net International Financial Position in Portugal...............................17

1.6.2 Reserve Asset Transactions .....................................................................18

1.6.3 The analytical presentation of the Balance of Payments .........................19

Box 3 – The Balance of Payments of Angola......................................................20

1.7 Budget constraints of institutional units ..........................................21

1.7.1 Non-Financial Private sector....................................................................21

1.7.2 Government..............................................................................................23

1.7.3 Central bank .............................................................................................24

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 2

1.7.4 Commercial banks ...................................................................................25

1.7.5 Consolidated monetary sector..................................................................27

1.8 Aggregate relations ..........................................................................27

1.8.1 National wealth ........................................................................................27

1.8.2 National savings.......................................................................................28

Box 4: Savings and investment by institutional sector in Portugal .....................29

1.8.3 A consistency tool: the flow of funds map ..............................................31

1.8.4 Changes in national wealth ......................................................................32

Further reading.............................................................................................33

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 3

1.1 Introduction

The National Accounts system registers the economic activities in a country’ based on

a standardized accounting system. Economic variables, such as incomes, expenditures,

deficits and surpluses, are recorded in national income accounting. The national accounts

play therefore a central role in macroeconomic analysis. In this note, we introduce the main

variables, aggregates, and accounting identities, in order to frame our discussion in a single

notational setup.

1.2 Basic concepts

Flows versus stocks - Flows are variables that are measured along a period of time.

Stocks variables are measured in a moment in time. Changes of stocks are flows. For

instance, deficit is a flow, debt is a stock, a debt increase is a flow.

Gross Domestic Product - is the main aggregate in National Accounts. It measures the

total production taking place within a country’ borders (geographical criterion). It is a

flow variable, so it is defined over a time interval (usually, a quarter or a year).

The geographical criterion versus the residence criterion - Some national account

aggregates refer to an economy defined by its geographical borders, while some

others refer to an economy defined by its resident units. Aggregates referring to a

geographical area are labelled as “Domestic”; aggregates referring to an economy’

resident units are labelled as “National”.

Resident and non-resident units: A unit is considered resident when it engages for an

extended period of time (one year or more) in economic activities on this territory.

The resident institutional sectors include households, non-financial corporations,

financial corporations, and the general government. Citizenship is not the criterion for

residence. Resident units engage in transactions with non-resident units (that is, units

which are resident in other economies). These transactions are the external

transactions of the economy and are grouped in the “rest of the world” account. This

account is similar to that of resident institutional sectors, but with the point of view

being that of the rest of the world.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 4

Gross versus Net - Fixed capital (machines, buildings, transport equipment)

depreciates over time. In the national accounts, the estimated wear and tear of

produced means of production is labelled “depreciation” or “consumption of physical

Capital”. When depreciation is subtracted to an aggregate, the later is labelled as

“net”. Aggregates labelled as “Gross” are “inclusive of depreciation”.

Transactions with and without counterparts: Transactions involving two agents are of

two kinds: ‘something for something’, or ‘something for nothing’. The first type

includes the provision of goods, services or assets in return for a counterpart, e.g.

money. The second type includes the provision of cash, assets, goods and services

without counterpart. The later are called “transfers” and include, for instance,

unemployment benefits, investment grants, and personal donations. The National

Accounts distinguish two types of transfers: transfers of capital, when there is a

transfer of ownership of an asset other than currency; and current transfers, that

correspond to transfers in the form of money. The former are accounted for in the

capital account, while the later are accounted for in the current account.

1.3 Expenditure, production and income

1.3.1 Gross National Expenditure (Final Domestic Demand)

The national spending in final goods and services by resident institutional sectors

(government, households and corporations) is usually known as “Absorption”. In National

Accounts it is measured by the Gross National Expenditure. It is defined as1:

GICA (1)

where C denotes for Private Consumption, I for Gross investment, and G for Government

Consumption.

1 In this note, all variables are defined in nominal terms.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 5

Private Consumption are expenditures by the private sector on final goods, including

durable and nondurable goods, and services.

Government Consumption refers to purchases of goods and services by the

government and compensations of public sector workers. G does not include any transfer

payments, such as unemployment benefits and family allowances, because these do not

correspond to payments for goods or services.

Gross Investment consists in additions to the stock of capital by resident units.

Investment has two main components: The first is the acquisition of fixed assets (that are

used in production over more than one year). These, in turn, can be tangible assets, such as

buildings, equipment, and vehicles; or intangible assets such as R&D. The second component

of investment is the net increases in inventories2. Thus,

InvGFCFI

The Investment aggregate is labelled as “gross” because it refers to the total

expenditure in new capital, regardless as to whether it is destined to increase the productive

capacity or just to replace the depreciation of existing equipment. Subtracting depreciation

from Gross Investment, one obtains the Net Investment. Since the depreciation of physical

capital is hard to measure, a common procedure is to assume that it corresponds to some

proportion of the capital stock. In that case, the net investment, which measures the change

in the capital stock, K, becomes

qKIKq .

In this expression, the term q is the relative price of capital, that is, how many units of

output are necessary to acquire one unit of physical capital. Subtracting depreciation from

GNE, we obtain the Net National Expenditure.

1.3.2 Gross Domestic Product

2 Note that investment does not include the acquisition of existing real assets nor of financial assets. Investment refers to expenditures that increase a country’ productive capacity, only.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 6

GNE measures the total purchases of goods and services by home entities,

irrespectively as to whether these goods and services are produced internally or imported.

Because some spending by resident units involves goods and services that are produced

outside the country borders, spending and production by resident units are not, in general,

equal.

To compute a country’ production, we first need to subtract from Absorption the

domestic expenditure in goods and services that are produced abroad (imports). Then, we add

the value of domestic production sold abroad (exports). The value of domestic production,

GDP at market prices, is therefore:

TBGICQ (2)

Where TB refers to the sum of two balances: the Balance of Trade in Goods

(merchandise trade) and the Balance of Trade in Services (invisibles, such as transport and

travel, insurance, and royalties). The TB (Balance of Goods and Services) does not

distinguish weather imported and exported goods and services are destined for investment or

for consumption purposes. Whenever spending by residents (absorption) exceeds domestic

production (GDP), the TB is negative.

GDP measures the market value of all final goods and services produced within a

country’ geographical borders in a given period of time, and is the key measure of an

economy’ production. Equation (2) describes the measurement of a country GDP using the

expenditure approach. Since the expenditure in goods and services is determined at the

purchaser’s prices, GDP is defined at “market prices”, that is, inclusive of all taxes.

1.3.3 Gross National Income

Gross Domestic Product (GDP) is concerned with where production is taking place. It

therefore looks at a country as defined by its geographical borders. In doing so, it treats the

production achieved by non-residents within the country borders the same way as it treats

production by residents.

A different approach is to look at who generated the income. The income approach

measures the production achieved by residents only, regardless as to whether it was generated

inside or outside country borders. For instance, the profits generated by a foreign company

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 7

inside country borders correspond to domestic production, but not to production by resident

units.

In the National Accounts, adjustments from the country border criterion (Domestic) to

the factor residence criterion (National) are mediated by an item in the Current Account,

labelled “Primary Income Account”. The meaning of a primary income is that it is generated

completely in the production process.

The Primary Income Account registers the cross-border payments to factors of

production, the return to financial assets, and the rent of natural resources. Exports of primary

income include, for instance, wages paid by non-resident companies to workers residing in

the home country3. Reciprocally, the interest payments on external debt correspond to value

generated inside a country’ border by a factor owned by non-residents, and hence shall be

subtracted from GDP when the aim is to measure total income generated by resident units.

In the following, let’s use the label NFIA (Net Factor Incomes from Abroad, NFIA)

for the balance of Primary Income, that is, the difference between the value of factor services

exported minus the value of factor services imported. The Gross National Income (GNI) is

therefore computed as follows:

NFIATBGICGNI (3)

GNI (at market prices) measures the total income earned (or production by) by factors

owned by domestic resident units, irrespectively as to whether such income was generated

inside or outside the country borders. GNI looks at the ownership of production, rather than

to its location.

3 NFIA does not include migrant remittances because, by definition, migrants are residents in the host country. Hence, migrants contribute to both the domestic and the national income of the country where they reside.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 8

Box 1: Three approaches to measure economic activity

There are three main approaches to measure a country’ economic activity:

The first is the Production Approach. This consists in summing the value added of all

activities which produce goods and services (intermediate and final) on the territory of the

economy. A firm’ value added measures the value generated by its production and is

computed as the difference between the value of output and the acquisitions of all

intermediate goods and services consumed as inputs in the production process.

The value added approach avoids double counting by focusing on the contribution of

each firm to the economy’ production, regardless its stage in the production process (i.e, it

measures the contribution of the cheese-maker by the difference between sales of cheese and

purchases of milk and other inputs used in the production of cheese). The sum of all value

added generated by all firms in a given territory deliver the Gross Domestic Product at

production prices. To obtain the GDP at market prices, one must add indirect taxes and

subtract subsidies on products.

The second is the Final Expenditure Approach, This consists in summing the value of

all final expenditures made in either consuming the final output of the economy, or in

investment, plus exports less imports of goods and services. Purchases of intermediate goods

(e.g, the purchase of milk by a factory to produce cheese) are excluded, to avoid double

counting (the output value of the final good “cheese” already reflects the cost of the

intermediate input “milk”).

To see the relationship between the Production Approach and the Expenditure

approach, let’s start out with an equation stating that the value of output (total supply of

goods and services) must equal its total use (intermediate consumption, investment and final

consumption at home and abroad:

TBGCIConsIntTOutput i . .

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 9

In this equation, the item iT denotes for Indirect taxes minus subsidies4. This term is

necessary to mediate the value paid by the buyer (which is tax inclusive) and the value

received by the producer (without taxes). The difference between output and intermediate

consumption is Gross Value Added at basic prices:

ConsIntOutputGVA . .

Using equation (2) we see that iTGVAGDP . Hence, GDP is no more than an

economy’ Gross Value Added measured at market prices.

The third way to measure production is the Income Approach. The Income Account

approach describes how the value added generated by production in the territory is distributed

to labour, capital and government. In particular, GVA is obtained as the sum of three items:

compensation of employees (gross wages and salaries plus social contributions paid by

firms); production taxes (less subsidies) other than indirect taxes5; and Gross Operating

Surplus, ie, the surplus or deficit accruing from production activities before account has been

taken on the interest, rents, and depreciation (from another angle, the GOS consists in the

sum of rents, interest, depreciation and profits6).

Note that the calculation of GVA by the income approach covers only incomes

generated within the borders of a country. To obtain the total income generated by residents,

one must add the net primary income from the rest of the world (NFIA). Then, one can add

indirect taxes (less subsidies), iT , to obtain the GNI.

4 These are taxes on products, meaning that they are payable per unit of a given product or service produced.

5 These are taxes and subsidies incurred by firms as a result of engaging in production, but that are independent of the quantity produced. For instance, taxes on the ownership of land and buildings, and taxes paid for business and professional licenses.

6 In the case of self-employed, the income generated has characteristics of both wages and operating surplus. Instead of trying to disentangle the two categories, the national accounts consider a third category, labelled “Mixed Income”, which is added together with the Gross Operating Surplus and Compensations of employees to obtain the gross value added.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 10

1.4 The Current Account

1.4.1 From National Income to Disposable Income

Apart from what people produce, people may spend money that was received as gift.

Gifts are transactions of the type ‘something for nothing’: cash, goods or services that are

provided to a beneficiary without counterpart. In National Accounts, gifts are labelled

transfers. Examples of current international transfers are emigrants’ remittances, international

aid, personal donations, payments to retired citizens living abroad, and lottery winnings.

In the Balance of Payments accounts, there is an item measuring the current transfers

received by residents in one country minus the current transfers sent to residents abroad. This

is the so-called “Balance of Secondary Income”, or simply Net Unilateral Transfers (NUT)7.

Considering Net Unilateral Transfers, we move from a concept of income related to

factor returns (GNI) to a concept of income related to “resources available to spend”,

irrespectively as to whether these resources were generated by factors owned by residents or

non-residents. This new measure is labelled Gross National Disposable Income (GNDI), or

simply Y:

NUTNFIATBGICY (4)

GNDI (Y), at market prices, measures the total resources available for spending by

home entities, without the need to borrow from (or lend to) abroad.

1.4.2 The Current Account

The Current Account records a country’ international transactions in goods, services,

and income (primary and secondary). The Current Account Balance is defined as:

NUTNFIATBCA (5)

7 The label Secondary Income arises because it refers to the redistribution of primary income.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 11

From the definition of GNDI, we have:

CAAY (6)

The Current Account Balance measures the excess of income over spending. When

spending is less than income, the CA is positive (surplus). When spending exceeds income,

the CA is negative (deficit). When the CA is positive, it means that the country accumulates

assets relative to the rest of the World.

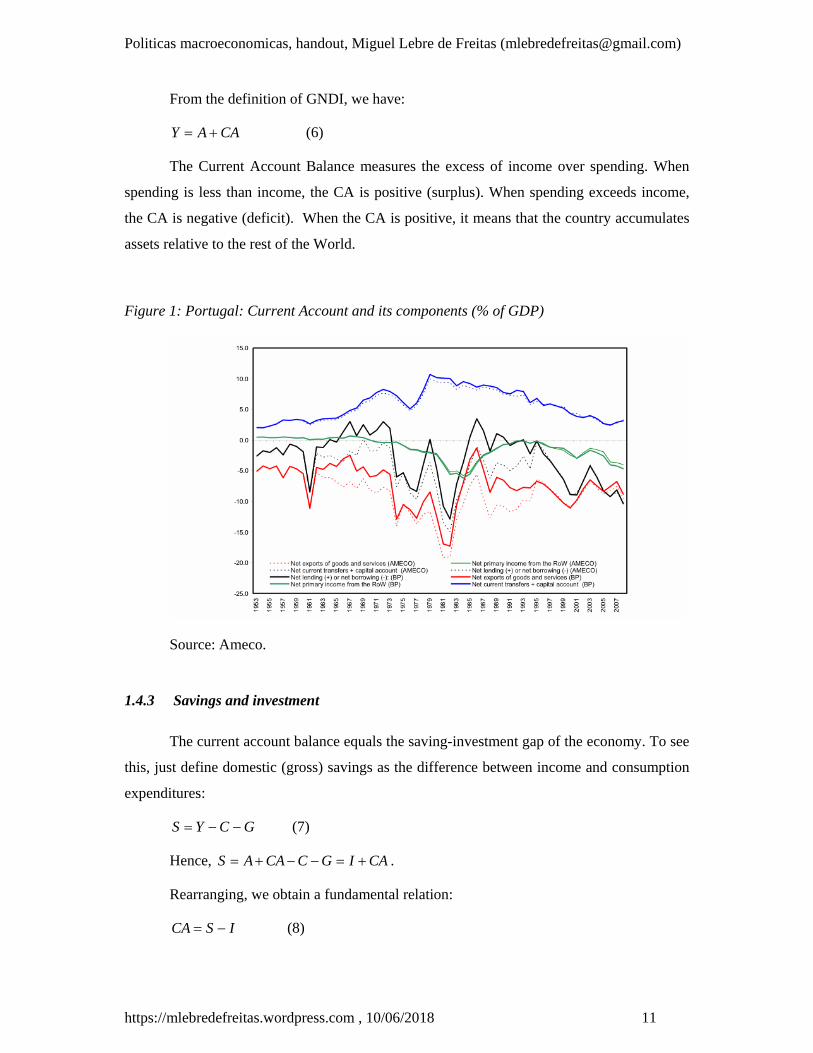

Figure 1: Portugal: Current Account and its components (% of GDP)

Source: Ameco.

1.4.3 Savings and investment

The current account balance equals the saving-investment gap of the economy. To see

this, just define domestic (gross) savings as the difference between income and consumption

expenditures:

GCYS (7)

Hence, CAIGCCAAS .

Rearranging, we obtain a fundamental relation:

ISCA (8)

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 12

Thus, the current account mirrors the saving and investment behaviour of the

economy. Note that this is an accountancy identity, something that must happen each moment

in time. When analyzing changes in the current account, one may use this identity to assess

the extent to which these changes are accounted for changes in national saving or in

investment. However, this accounting identity tell us nothing about causality: one cannot say

if a given improvement in the current account occurred because savings increased or, in

alternative, saving increased because the current account improved. Equation (8) merely

defines a relationship between variables that must hold each moment in time, and is silent in

respet to the behaviour of economic agents.

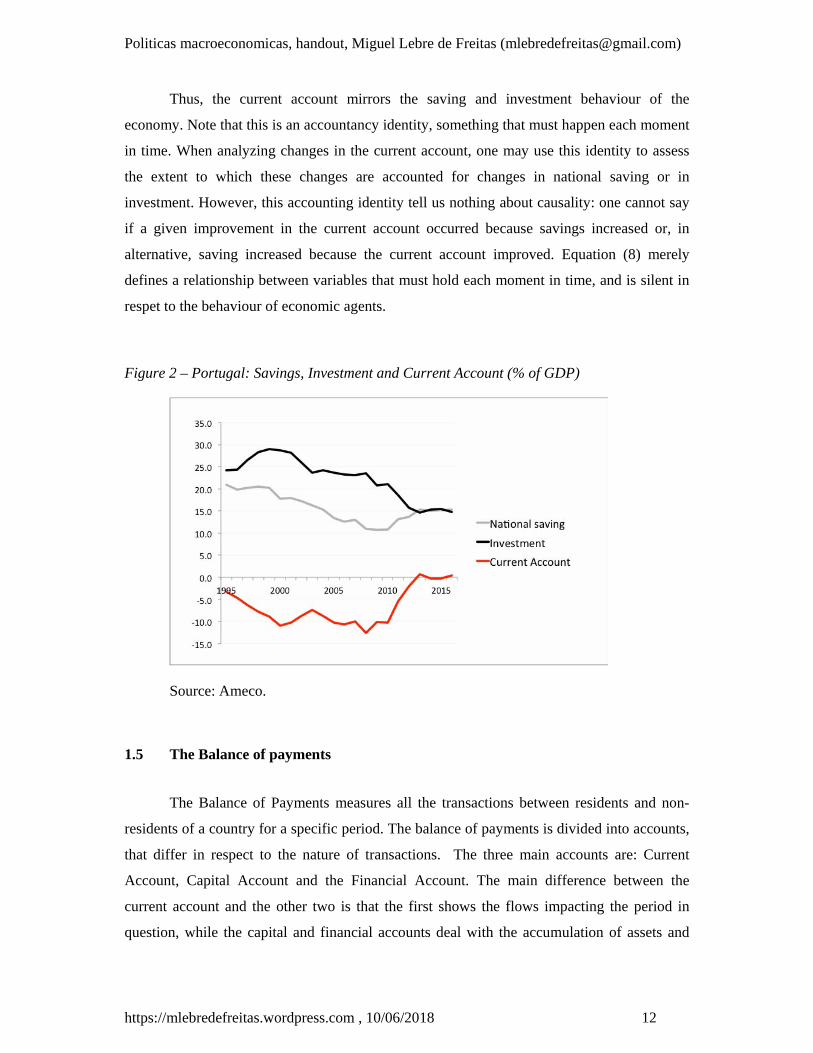

Figure 2 – Portugal: Savings, Investment and Current Account (% of GDP)

Source: Ameco.

1.5 The Balance of payments

The Balance of Payments measures all the transactions between residents and non-

residents of a country for a specific period. The balance of payments is divided into accounts,

that differ in respect to the nature of transactions. The three main accounts are: Current

Account, Capital Account and the Financial Account. The main difference between the

current account and the other two is that the first shows the flows impacting the period in

question, while the capital and financial accounts deal with the accumulation of assets and

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 13

liabilities in respect to the rest of the world. Thus, when an economy runs a surplus in the

Current Account, this means that it accumulates assets. In the National Accounts, this

accumulation is recorded in two different accounts, the Capital Account, and the Financial

Account8.

1.5.1 The Capital Account

The Capital Account (KA) is a minor component of the Balance of Payments

registering the “acquisitions or disposal of non-financial and non-produced assets”. By

exclusion, the financial assets are recorded in the Financial Account and the Produced Assets

(investment goods and services) are recorded in the Current Account.

The Capital Account is divided in two main categories: (a) acquisitions of non-

financial assets not accounted in the TB, such as permits to undertake specific activities (the

right to explore a natural resource), and marketing assets, such as brand names, trademarks,

and franchises9; and (b) capital transfers (i.e, transfers of assets) between residents and non-

residents: debt forgiveness, inheritance received, grants designed to finance capital formation,

such as those made by the European Agriculture Fund for Rural Development).

The sum of the balances on the current and capital accounts delivers the net lending

(surplus) or net borrowing (deficit) of the economy relative to the rest of the world. That is,

*BeKACA . (10)

8 The Capital Account and the Financial Account are labelled as “accumulation accounts”. Accumulation accounts cover international transactions of financial and non-financial assets. This differs from the current account, which deals with the production, redistribution, and use of income in the form of final expenditures.

9 These items are labelled “non-produced non-financial assets”. They are assets, because they can be bought and sold with resulting payment flows, but they differ from investment goods and valuables because they do not come into existence in result of any production processes. While international trade in produced non-financial assets (investment goods and valuables) is accounted for in the balance of goods and services (TB), this remaining category of non-financial assets is recorded in the capital account.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 14

Were *B denotes for the dollar value of the stock of net foreign assets owned by

residents, and e stands for the exchange rate. Whenever the right-hand side is positive, the

economy is accumulating financial assets relative to the rest of the world, in net terms.

1.5.2 The Financial Account

The current and capital accounts show the transactions that determines a country’

lending capacity. When the sum of the current and capital accounts is negative, this means

that the economy needs foreign financing. The financial account balance measures the net

debt accumulation of a country vis-à-vis the rest of the world. It registers the transactions

between residents and non-residents that involve financial assets and liabilities.

The financial account shows how net lending or borrowing is allocated or financed

across different types of assets or of financial transactions. It can be presented in terms of

type of assets (e.g, deposits, bonds, currency, etc) or in terms of functional categories (i.e,

what are the motives underlying these transactions).

In its manual for the Balance of Payments Statistics (BPM6), the IMF defines five

categories of financial transactions: (a) Direct Investment: cross-border asset transactions

(equity, loans, real state, reinvestment of profits) involving a resident in one economy having

influence on the management of an enterprise that is resident in another economy; (b)

Portfolio Investment: cross-border transactions of shares in business enterprises with no

influence in company management; purchases and issues of debt instruments not related to

Direct Investment; (c) Financial derivatives: international transactions of this separate group

of financial instruments. (d) Other investment: a very important item, as it corresponds to

operations of currency, deposits, trade, and credits – a foreign bank loan to a domestic

company, for instance, is registered here; (e) Reserve assets: Transactions involving foreign

assets owned by the monetary authority. The later include the purchase or sale, by the

monetary authorities, of gold, reserve positions at the IMF and foreign exchange reserves.

Since these assets belong to the central bank, they can be used to cover financial needs in the

balance of payments or to intervene in the foreign exchange markets. Note that when the

central bank swaps foreign money for domestic money, there is an impact in the domestic

money supply.

1.5.3 The three components of the balance of payments

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 15

The Balance of Payments is therefore composed by 3 main accounts:

- The Current Account (CA), that measures the international flows of goods and

services, and factor incomes; if positive, it means that the country accumulates

assets.

- The Capital Account (KA), a minor item that records international capital

transfers, as well as the acquisition and disposals of special (non-produced non-

financial) assets.

- The Financial Account (FA), that measures the net acquisition and disposal of

financial assets and liabilities. A surplus in the financial account (FA>0) means

that the country is a net exporter of financial assets (net borrower).

1.5.4 The Balance of payments identity

The financial account and the capital account are flows of funds that shall be added to

home GNDI to calculate the total resources available for expenditure by home residents. The

value of the total resources available for national expenditure is therefore

Y+KA+FA=A. (11)

Since, on the other hand, Y=A+CA, one obtains the Balance of Payments Identity:

0 FAKACA (12)

The Balance of Payments Identity states that any CA surplus must be matched by an

equal deficit in the other two accounts, meaning that the country is accumulating financial

and non-produced assets.

1.5.5 Net errors and omissions

The data on merchandise trade originate with the customs authorities, while the

remaining components of the Balance of Payments are collected by central banks. Because

these data come from different sources, and some transactions are not reported, equality (12)

will not in general hold. To account for statistical discrepancy, the Balance of Payments

Statistics include a component, called Net Errors and Omissions (EO), which is defined as

follows:

FAKACAEO (12a)

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 16

Because the EO captures hidden transactions, such as unreported capital movements,

it may occasionally be a meaningful indicator of financial stress, namely in economies under

capital controls.

1.6 The Net International Investment Position

A country’ Net International Investment Position is a measure that shows at a moment

in time the value of financial assets of residents of an economy that are claims on non-

residents minus the liabilities of residents to non-residents. This measure includes all types of

financial assets, namely, bonds, equity, gold, and financial derivatives, and is in general

measured in US dollar units.

In our framework, a country NIIP is summarised by the symbol *B . Because this

variable is defined in US dollars, the corresponding value in domestic currency is:

*eBNIIP (15)

Where e denotes for the exchange rate.

Whenever NIIP>0, external assets exceed external liabilities, so the country is a net

creditor relative to the rest of the World; when NIIP<0, external liabilities exceed external

assets, so the country is a net debtor relative to the rest of the World.

1.6.1 Changes in NIIP

The NIIP of a country is evaluated at market prices. Hence, changes in a country Net

International Investment Position may reflect both borrowing/lending (financial transactions)

and changes in the market value of the different assets that give rise to holding gains or losses

in the stock of assets held.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 17

For instance, a crash in the domestic stock market will increase the domestic country’

NIIP, through the losses faced by foreign investors at home; in turn, a crash in a stock market

abroad will reduce a country NIIP’ by the losses of domestic investors abroad. Thinking more

broadly, valuation changes can happen because of stock market fluctuations, because of

changes in bond yields, exchange rate movements, etc.

Abstracting from capital gains or losses other than those arising from movements in

the exchange rate, the change on NIIP will be10:

** eBBeNIIP (16)

The first component is related to a country’ net borrow and lending (-FA=CA+KA).

The second component captures eventual capital gains or losses due to changes in the value

of the assets comprising the NIIP (in equation 16, the valuation changes are attached to

exchange rate movements, only, for simplification).

Box 2: The Net International Financial Position in Portugal

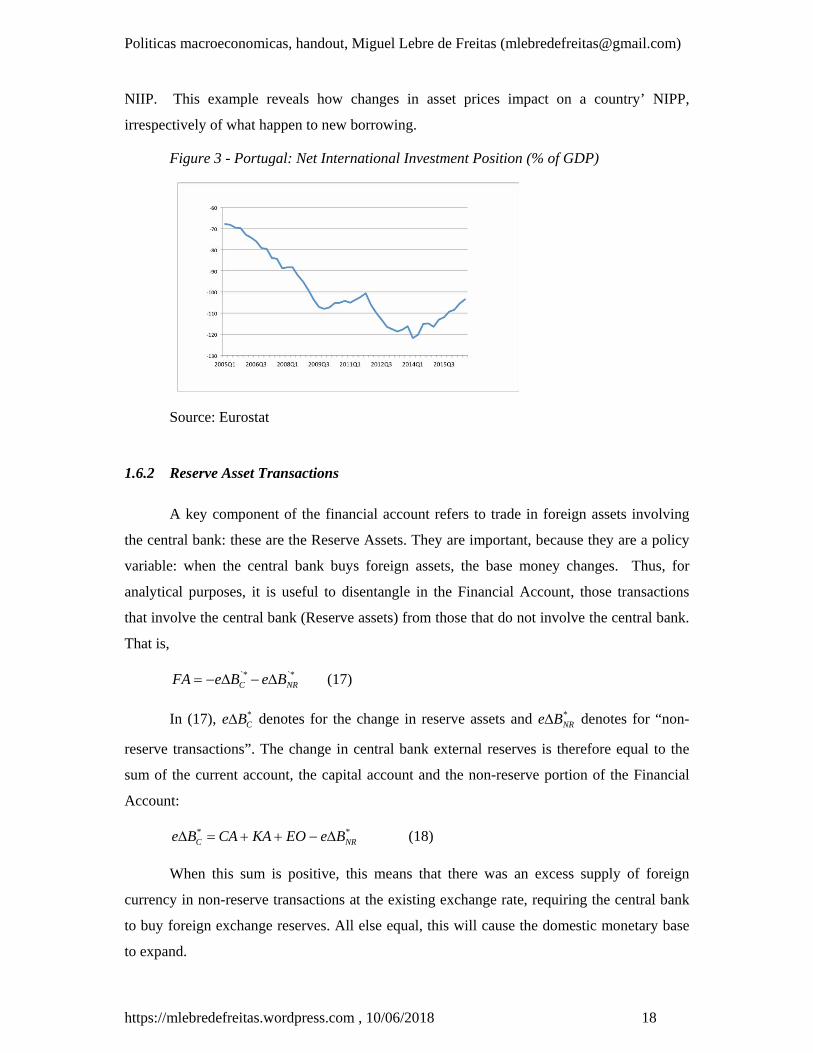

According to the Euroestat data, from 2010Q4 to 2011Q4, the NIIP of Portugal

improved from -104.3% of GDP to -100.7% (Figure 3). In 2011, however, the economy’ net

lending amounted to 4% of GDP. This means that an impressive valuation change more than

offset the large deficit in the current account.

Why was that? The reason is that the risk premium attached to liabilities issued by

Portuguese entities (bonds and other securities) increased sharply, causing the corresponding

secondary markets yields to increase and bond prices to fall. Thus, the net value or domestic

liabilities decreased.

Along 2011-2012 the reverse occurred: as the risk premia and the implied yields

declined back, the market value of bonds increased, implying a decline in the Portuguese

10 Obviously, the value of the net international investment position may change for reasons other than exchange rate movements. Stock market valuations, changes in interest rates impacting on the market value of bonds are among the factors that cause valuation changes. The decomposition above is only a simplification.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 18

NIIP. This example reveals how changes in asset prices impact on a country’ NIPP,

irrespectively of what happen to new borrowing.

Figure 3 - Portugal: Net International Investment Position (% of GDP)

Source: Eurostat

1.6.2 Reserve Asset Transactions

A key component of the financial account refers to trade in foreign assets involving

the central bank: these are the Reserve Assets. They are important, because they are a policy

variable: when the central bank buys foreign assets, the base money changes. Thus, for

analytical purposes, it is useful to disentangle in the Financial Account, those transactions

that involve the central bank (Reserve assets) from those that do not involve the central bank.

That is,

`*`*NRC BeBeFA (17)

In (17), *CBe denotes for the change in reserve assets and *

NRBe denotes for “non-

reserve transactions”. The change in central bank external reserves is therefore equal to the

sum of the current account, the capital account and the non-reserve portion of the Financial

Account:

**NRC BeEOKACABe (18)

When this sum is positive, this means that there was an excess supply of foreign

currency in non-reserve transactions at the existing exchange rate, requiring the central bank

to buy foreign exchange reserves. All else equal, this will cause the domestic monetary base

to expand.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 19

1.6.3 The analytical presentation of the Balance of Payments

The “standard” presentation of the Balance of Payments, as described in BPM6 and

ESA10, focuses on a major balancing item: the net lending/borrowing. Above this line, we

have the sum of the current account and capital account; below the line we have the financial

account. Thus, the main focus of the Balance of Payments presented that way is the impact of

international transactions in a country’ NIIP.

There are, however, other aspects one may want to emphasise when looking at the

balance of payments. One is the extent to which the central bank is intervening in the foreign

exchange market, buying and selling foreign exchange reserves, say, to influence the

exchange rate. The other is the extent to which the authorities in general (central bank and

government) are mobilizing international resources to fill a financing gap in the balance of

payments: when agents in an economy have sent more money abroad than they received

(through either trade of goods or trade in assets), the central bank can fill the gap, undertaking

“compensatory” operations, such as the mobilization of gold and reserves or the use of IMF

credit facilities. In plus, a country can use “exceptional financing” mechanisms, such as debt

forgiveness, debt restructuring, intergovernmental grants, and accumulation of arrears to

finance other “autonomous” international transactions.

In order to measure the extent to which these various “compensatory” instruments

have been used in a given period, a common practice by the IMF is to pull together these

items in a new account called “Reserves and Related Items”.

The analytical presentation of the Balance of Payments is therefore a reorganization

of the standard presentation to facilitate a basic distinction between (a) reserves and related

items; (b) other transactions. This presentation shows how reserves, along with other

exceptional financing mechanism are used to finance the autonomous international

transactions.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 20

When the Balance of Payments is presented that way, the sum of the items above the

line (CA, KA, FA, EO excluding Reserve and related items) is labelled “Overall balance”11.

Thus, while formally the total of the Balance of Payments should be zero, often by a Balance

of Payments surplus or deficit it is meant a surplus or a deficit in the “overall balance”.

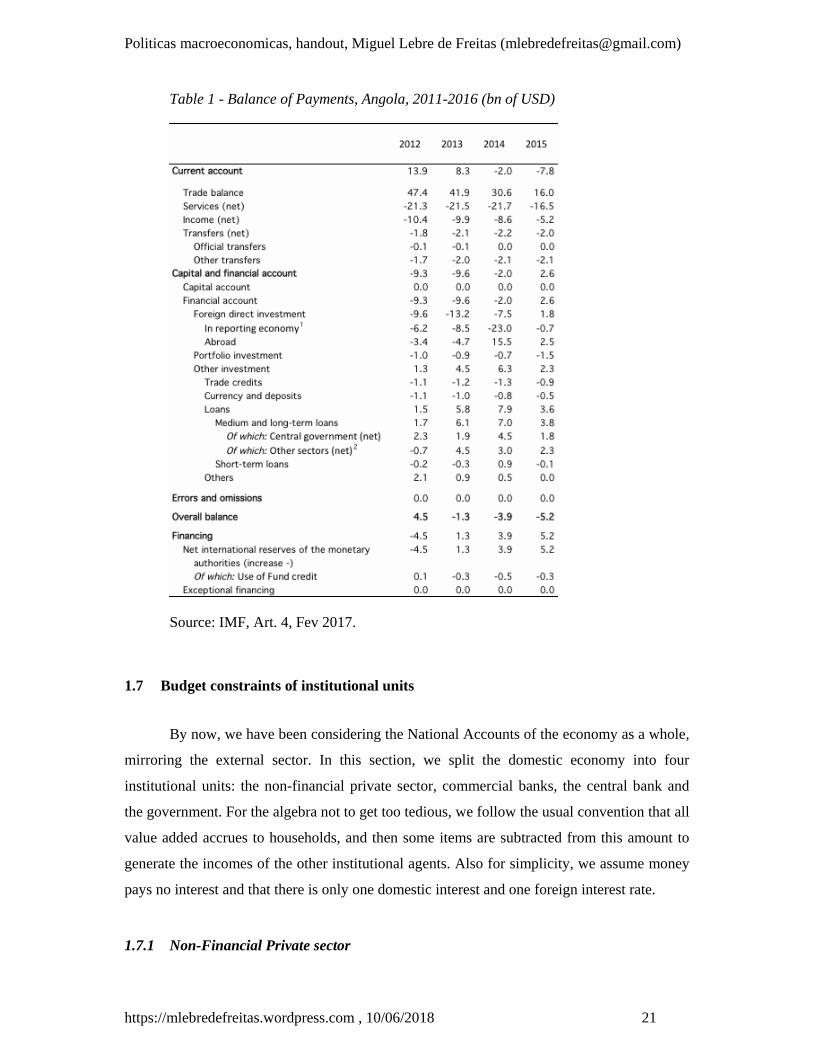

Box 3 – The Balance of Payments of Angola

Table 1 shows an “analytical” presentation of the Balance of Payments in Angola, as

reported in the 2006 IMF country review.

Thus, for instance, in 2012, there was a current account surplus amounting to 13.9bn

USD, that lead to a net acquisition of foreign assets by the non-monetary sector (the

“financial account has a deficit of 9.3bn). The difference was matched by an increase in

central bank reserves, by 4.5bn. Along 2013-2015, the fall in oil prices caused the current

account to deteriorate, and this was partially mitigated by a capital flow reversal (the

financial account turned positive in 2015, meaning that the country became a net borrower).

Still, the “overall balance” was negative, meaning that the central bank sold reserve assets.

This, in turn, implied a sharp contraction in the money base.

11 When this rearrangement is made, the items in the balance of payments from which transactions were taken are readjusted and marked with (n.i.e.): for instance, Capital Account (n.i.e.) does not include debt forgiveness; Financial Account (n.i.e.) does not include Reserve Assets.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 21

Table 1 - Balance of Payments, Angola, 2011-2016 (bn of USD)

Source: IMF, Art. 4, Fev 2017.

1.7 Budget constraints of institutional units

By now, we have been considering the National Accounts of the economy as a whole,

mirroring the external sector. In this section, we split the domestic economy into four

institutional units: the non-financial private sector, commercial banks, the central bank and

the government. For the algebra not to get too tedious, we follow the usual convention that all

value added accrues to households, and then some items are subtracted from this amount to

generate the incomes of the other institutional agents. Also for simplicity, we assume money

pays no interest and that there is only one domestic interest and one foreign interest rate.

1.7.1 Non-Financial Private sector

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 22

The non-financial private sector comprises households and non-financial

corporations. The balance sheet identity of the private sector is defined as follows12:

PPP BMqKNW , (19)

Where PNW denotes for the Net Worth of the private sector, PK for the stock of real

assets held by the private sector, q for the relative price of real assets, M for monetary assets

and PB for non-monetary non-financial assets (equity, bonds) net of liabilities. The later can

be decomposed into government bonds held by the private sector ( PGD ), external assets net of

external liabilities ( *PeB ), credit from commercial banks ( P

BL ), and (if any), liabilities to the

central bank ( PCL ). Thus,

PC

PB

PGPP LLDeBB * . (20)

The private sector disposable income is:

TNUTeBiLLDiQY PPPC

PB

PG

dP ** (21)

The term PNUT refers to the net secondary income received from abroad (emigrants

remittances, for instance). For simplicity, we use a single item, T, to describe all taxes minus

subsidies: more precisely, T refers to the sum of indirect taxes, direct taxes, and social

security contributions, minus government transfers (such as unemployment benefits) and

subsidies to production.

The current (gross) saving of the private sector is13:

CYS dPP (22)

12 Private agents rely on equity and on lending from each other as a source of finance, but these transactions cancel out in the private sector aggregate.

13 Because we are pooling together households and non-financial corporations, the model hides the fact that part of private savings consists in earnings retained by corporations to finance their investment (corporate savings). The disposable income of households is equal to the disposable income of the private sector minus retained earnings and accordingly; households savings are equal to private savings minus retained earnings.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 23

Just like in the balance of payment accounting, mediating current savings and the

accumulation of financial assets there is a capital account. The sum of current savings with

eventual capital transfers received by the private sector, PKA (grants from the government

and from abroad, net) gives the net accumulation of real, monetary and financial assets by the

private sector (first column in Table 1):

PB

PC

PGPPPP LLDBeMIKAS * (23)

By the definition, the balance-sheet of the private sector (19) gives the stocks of

assets, liabilities, and net worth of a sector at a moment in time. By taking the change in

stocks between two balance-sheets we get the net flows over the corresponding time spam,

which define the sources-and-use-of-funds statement:

PPPP BMqKKqNW

Using the fact that net investment is equal to gross investment minus depreciation

( PPP qKIKq ) and differentiating (20), we get:

PB

PC

PGPPPPP LLDeBBeMqKqKINW **

Using (23), we see that the net-worth of the private sector increases with net savings

(first-term), gifts, and valuation changes (last term):

*PPPPP BeqKKAqKSNW (24)

1.7.2 Government

The Net Worth of the government sector is defined as follows:

GGG DqKNW (25)

Where GK stands for the public capital stock, and

*G

CG

BG

PG

G eDDDDD (26)

With jGD denoting for government debt placed at the institutional sector j.

The government current gross saving is:

GGCG

BG

PGG NUTeDiDDDiGTS ** (27)

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 24

GNUT refers to the component of NUT that involves the government (official

transfers, like international assistance).

Denoting the net capital transfers received by the government by GKA (from abroad,

net, minus capital transfers paid to the private sector), the net borrowing of the general

government will be:

*G

CG

BG

PGGGG DeDDDIKAS (28)

The government sector sources-and-use-of-funds statement is:

GGGG DqKKqNW

Using **GG

CG

BG

PG

G eDDeDDDD , replacing in (27), and defining the

depreciation of capita as above, we get:

*GGGGGG eDKqKAqKSNW (29)

That is, the change in the new worth of the government sector is the sum of net

current savings, capital transfers received from abroad and capital gains or losses on physical

capital and foreign debt.

1.7.3 Central bank

The central bank balance sheet obeys to the following identity:

HBeBHLLDeBNW CCPC

BC

CGCC ** (30)

where, CNW denotes for the net worth of the central bank, *ceB for net foreign assets held by

the central bank expressed in domestic currency, CGD for government debt held by the CB,

BCL for loans to commercial banks, P

CL for loans to the private sector, and H for the Monetary

Base. The total amount of domestic assets held by the central bank is PC

BC

CGC LLDB .

The money base (H) is the most relevant liability of the central bank. It comprehends

notes and coins held by the public (X) and reserves held by commercial banks, R:

H=X+R (31)

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 25

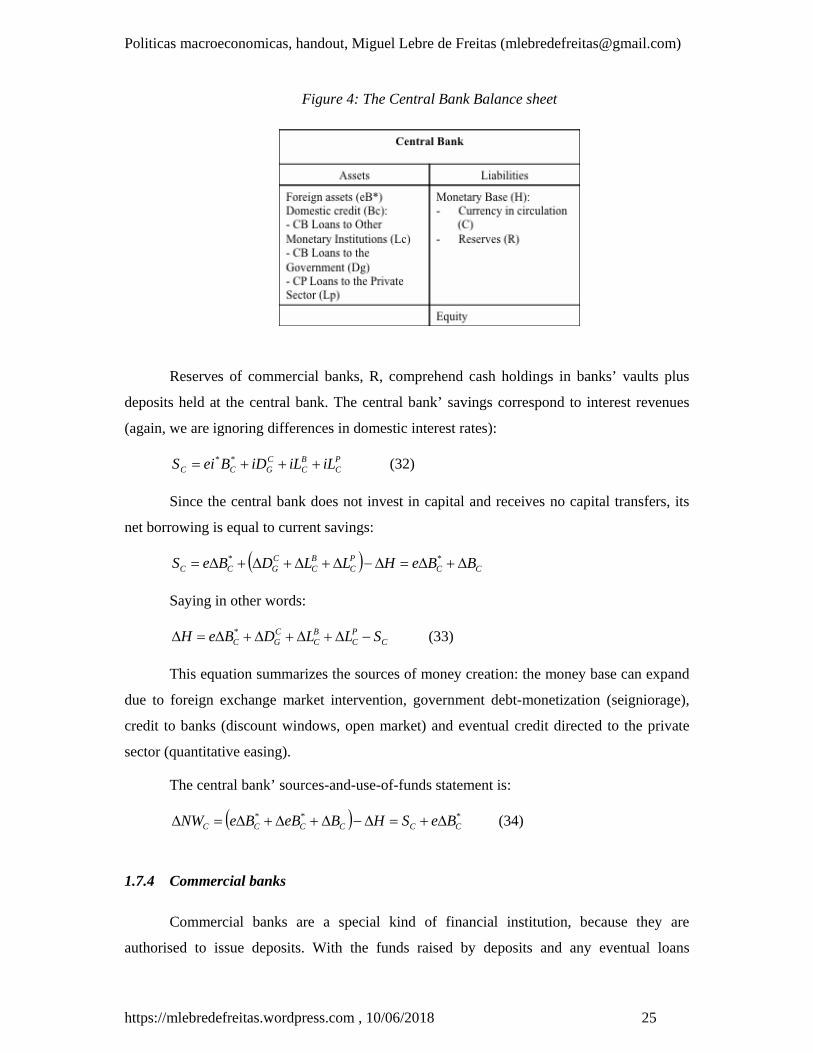

Figure 4: The Central Bank Balance sheet

Reserves of commercial banks, R, comprehend cash holdings in banks’ vaults plus

deposits held at the central bank. The central bank’ savings correspond to interest revenues

(again, we are ignoring differences in domestic interest rates):

PC

BC

CGCC iLiLiDBeiS ** (32)

Since the central bank does not invest in capital and receives no capital transfers, its

net borrowing is equal to current savings:

CCPC

BC

CGCC BBeHLLDBeS **

Saying in other words:

CPC

BC

CGC SLLDBeH * (33)

This equation summarizes the sources of money creation: the money base can expand

due to foreign exchange market intervention, government debt-monetization (seigniorage),

credit to banks (discount windows, open market) and eventual credit directed to the private

sector (quantitative easing).

The central bank’ sources-and-use-of-funds statement is:

*** CCCCCC BeSHBeBBeNW (34)

1.7.4 Commercial banks

Commercial banks are a special kind of financial institution, because they are

authorised to issue deposits. With the funds raised by deposits and any eventual loans

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 26

obtained from the central bank, BCL , commercial banks engage in their main activity, which is

granting credit to the non-financial sector. The balance sheet of the commercial banking

sector obeys to the following identity14:

DLDLRNW BC

BG

PBB (35)

where PBL denotes for banks’ loans to the private sector, G

CD for government securities, BNW

for the net worth of commercial banks, D for private deposits in the banking system, and the

remaining variables are defined as before.

Figure 5: The Balance sheet of Deposit banks

The banks savings are related to the interests they pay to the central bank and the

interest they charge on credit:

BC

PB

BGB iLiLiDS (36)

The corresponding sources-and-use-of-funds statement is:

DRLDLNW BC

BG

PBB (37)

14 For simplicity, we are ignoring funds raised by banks through the capital market, such as long term bonds. Note that individual banks also rely on lending from each other as a source of finance, but when considering the banking system as a whole, these inter-bank loans cancel out

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 27

1.7.5 Consolidated monetary sector

Taking together the central bank and the commercial banks balance sheets, one

obtains the consolidated balance sheet of the monetary sector:

DXDDLLeBNW CG

BG

PC

PBCCB

* (38)

The specific characteristic of bank deposits is that they are so liquid that they can

serve as means of payment. Because of this, bank deposits are part of what we call “money”,

together with currency in circulation (X). The money supply is, therefore: 15

DXM , (39)

equation (33) can be rearranged to:

CBGC

GB

PC

PBC NWDDLLeBM * (38a)

Equation (38a) reveals that the counterparts of money supply are foreign assets and

total domestic credit (government plus the private sector).

1.8 Aggregate relations

1.8.1 National wealth

Summing the newt worth of all national units, one gets the net worth of the economy

as a whole:

qKBDBeNWNWNWNWNW PGCBCGP *** (41)

The first component in the right hand side is the country’ International Investment

Position, because resident-to-resident claims net to zero in the national balance sheet:

15 In the real world, central banks monitor wider monetary aggregates, including short term securities held by the public (e.g, treasuries). For convenience, we ignore this complication.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 28

****PGC BDBB (42)

Hence:

qKeBNW * (41a)

A country total wealth is composed by the country stock of non-financial assets (K)

and the net holdings of financial assets (NIIP).

1.8.2 National savings

Summing the current savings across all agents (22, 27, 32, 36), we get national

savings:

* * * *P G C B C G PS S S S S Q C G NUT ei B D B

Rearranging, the sum of savings and consumption gives the Gross National

Disposable Income (GDNI):

YBeiNUTQGCS ** (43)

Note that the term **eBi corresponds to the Primary Income account of the Balance of

Payments (NFIA). The term NUT is, as we know, the Secondary Income Account. Then,

using the definition of CA and GDP by the spending approach, we are back to the main

identity of the national accounts:

CAIS (8)

Disentangling how savings and investment are split across institutional sectors, one

can learn on what is behind a current account deficit. In our framework:

GGPBCP ISISSSCA . (8a)

This identity shows that the budgetary balance of the government may be an

important factor influencing the current account balance. A situation in which a sustained

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 29

current account deficit is matched by a persistent government spending in excess of receipts

is labelled “twin deficit”16.

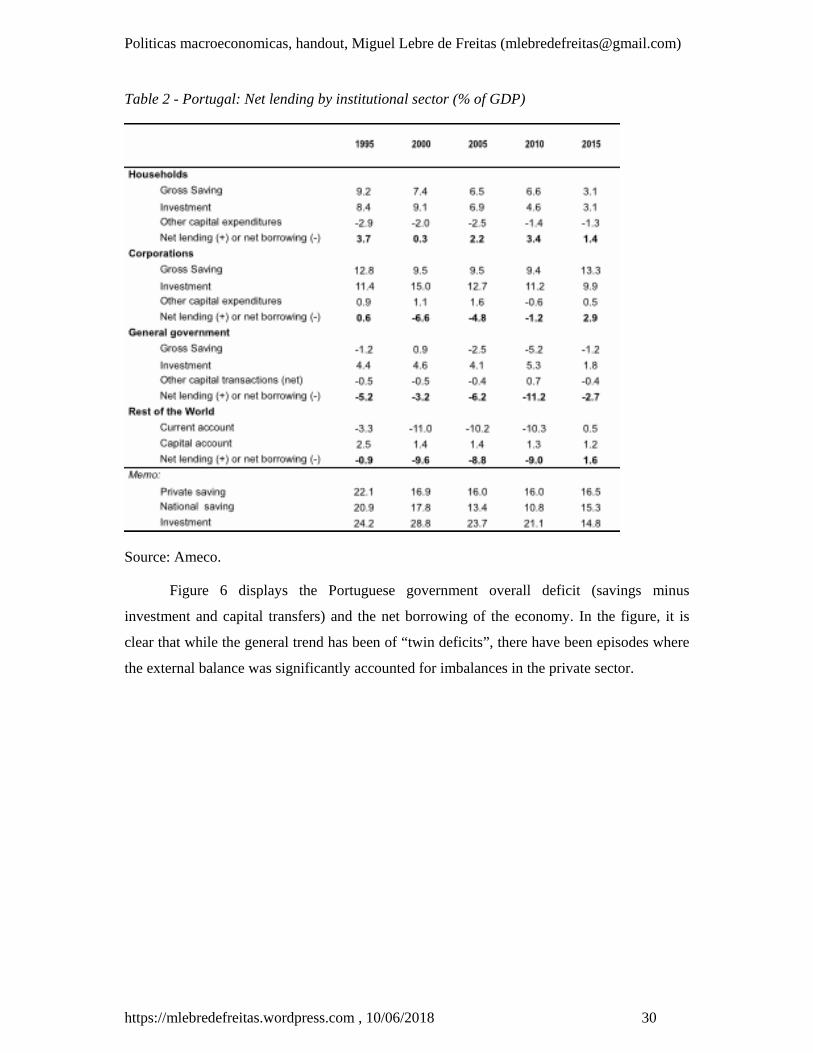

Box 4: Savings and investment by institutional sector in Portugal

Table 2 describes the net lending or borrowing by institutional sector in Portugal. In

the table, the private sector is split into households and corporations, only. For each resident

unit, under-spending or overspending on the acquisition of real assets (capital) relative to

savings and capital transfers, results in the balancing item “net lending or borrowing”. In the

case of the rest of the world, net lending is obtained as the difference between the

symmetrical of the current account corresponding savings (external saving), and the capital

account.

In the table, we see that 2010 can be categorized as a year of twin deficits: in that

year, the economy’ net borrowing (9% of GDP) was totally accounted for the government

sector deficit (-11.2% of GDP), while the private sector as a whole (i.e, the consolidation of

households with the firms that they own) exhibited a surplus (2.2% of GDP).

16 At the first sight this suggests that fiscal tightening could be used to achieve external balance. Note however that private savings are not independent of government savings: if taxes increase, for instance, it is possible that private savings decrease in response. This means that the accounting identity (8a) provides only a starting point for an analysis of the interaction between savings, investment and the current account. A more enlightened analysis must be supplemented with information regarding the behaviour of economic agents.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 30

Table 2 - Portugal: Net lending by institutional sector (% of GDP)

Source: Ameco.

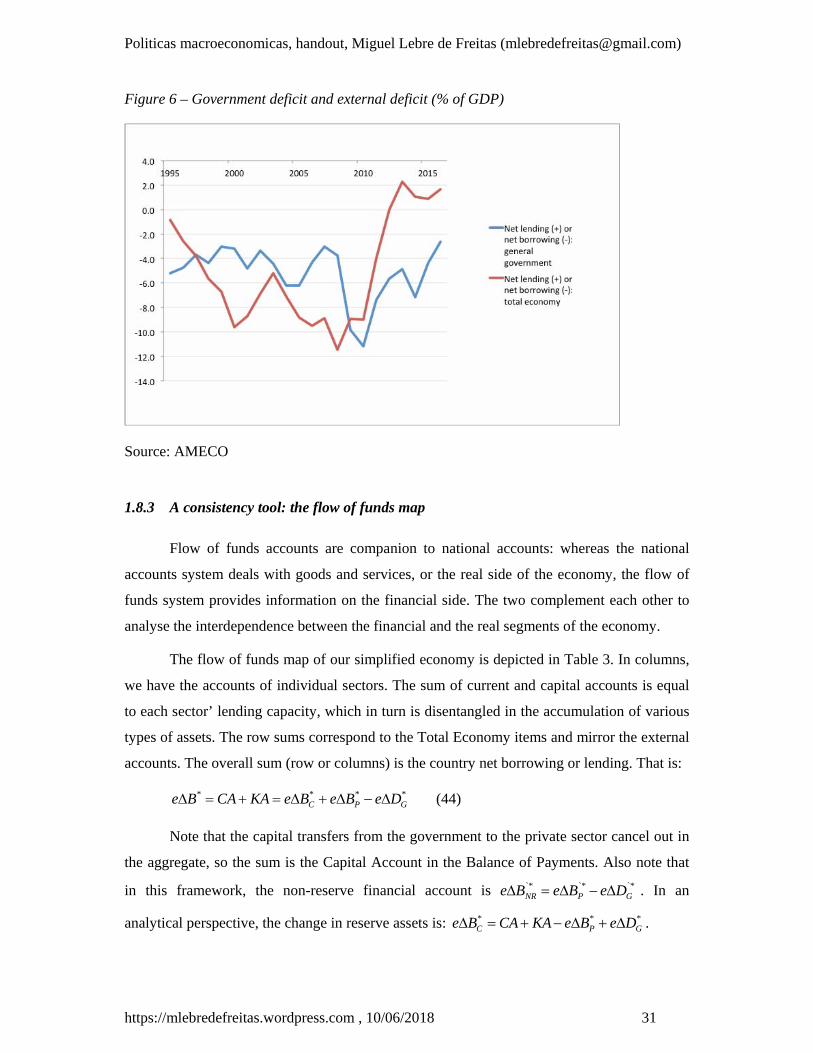

Figure 6 displays the Portuguese government overall deficit (savings minus

investment and capital transfers) and the net borrowing of the economy. In the figure, it is

clear that while the general trend has been of “twin deficits”, there have been episodes where

the external balance was significantly accounted for imbalances in the private sector.

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 31

Figure 6 – Government deficit and external deficit (% of GDP)

Source: AMECO

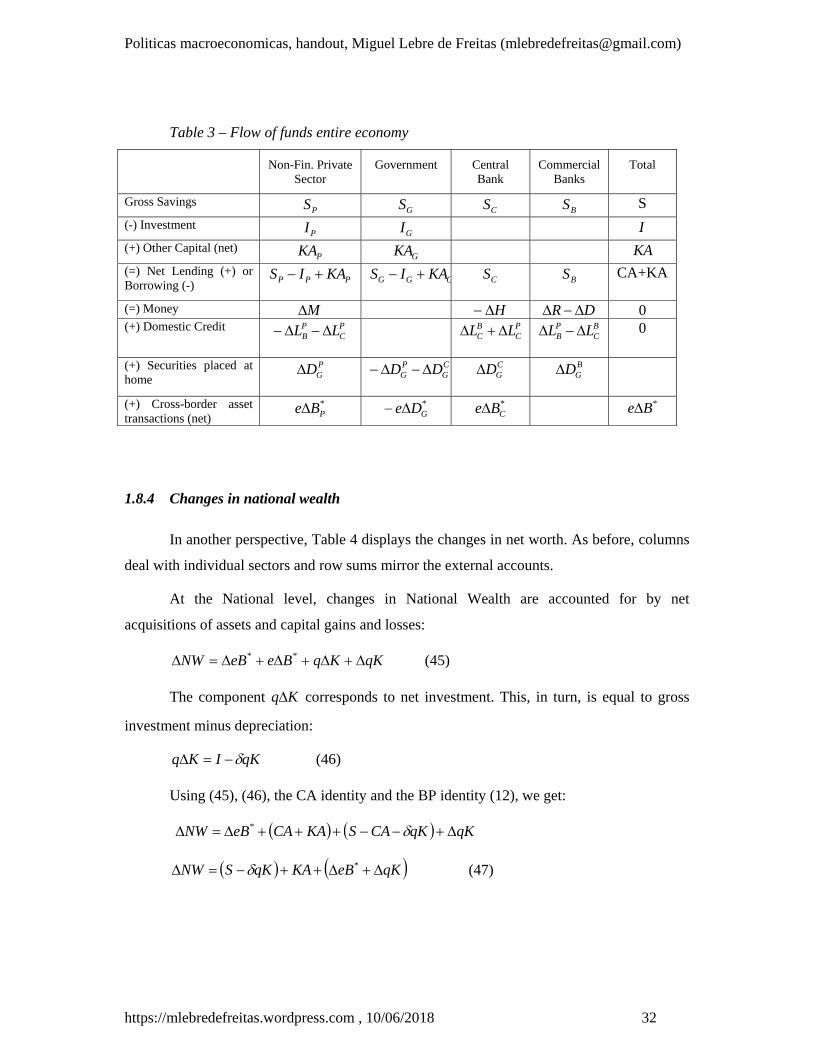

1.8.3 A consistency tool: the flow of funds map

Flow of funds accounts are companion to national accounts: whereas the national

accounts system deals with goods and services, or the real side of the economy, the flow of

funds system provides information on the financial side. The two complement each other to

analyse the interdependence between the financial and the real segments of the economy.

The flow of funds map of our simplified economy is depicted in Table 3. In columns,

we have the accounts of individual sectors. The sum of current and capital accounts is equal

to each sector’ lending capacity, which in turn is disentangled in the accumulation of various

types of assets. The row sums correspond to the Total Economy items and mirror the external

accounts. The overall sum (row or columns) is the country net borrowing or lending. That is:

****GPC DeBeBeKACABe (44)

Note that the capital transfers from the government to the private sector cancel out in

the aggregate, so the sum is the Capital Account in the Balance of Payments. Also note that

in this framework, the non-reserve financial account is `*`*`*GPNR DeBeBe . In an

analytical perspective, the change in reserve assets is: ***GPC DeBeKACABe .

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

https://mlebredefreitas.wordpress.com , 10/06/2018 32

Table 3 – Flow of funds entire economy

Non-Fin. Private Sector

Government Central Bank

Commercial Banks

Total

Gross Savings PS GS CS BS S

(-) Investment PI GI I

(+) Other Capital (net) PKA GKA KA

(=) Net Lending (+) or Borrowing (-)

PPP KAIS GGG KAIS

CS BS CA+KA

(=) Money M H DR 0 (+) Domestic Credit P

CPB LL P

CBC LL

BC

PB LL

0

(+) Securities placed at home

PGD C

GPG DD

CGD B

GD

(+) Cross-border asset transactions (net)

*PBe *

GDe *CBe *Be

1.8.4 Changes in national wealth

In another perspective, Table 4 displays the changes in net worth. As before, columns

deal with individual sectors and row sums mirror the external accounts.

At the National level, changes in National Wealth are accounted for by net

acquisitions of assets and capital gains and losses:

qKKqBeeBNW ** (45)

The component Kq corresponds to net investment. This, in turn, is equal to gross

investment minus depreciation:

qKIKq (46)

Using (45), (46), the CA identity and the BP identity (12), we get:

qKqKCASKACAeBNW *

qKeBKAqKSNW * (47)

Politicas macroeconomicas, handout, Miguel Lebre de Freitas ([email protected])

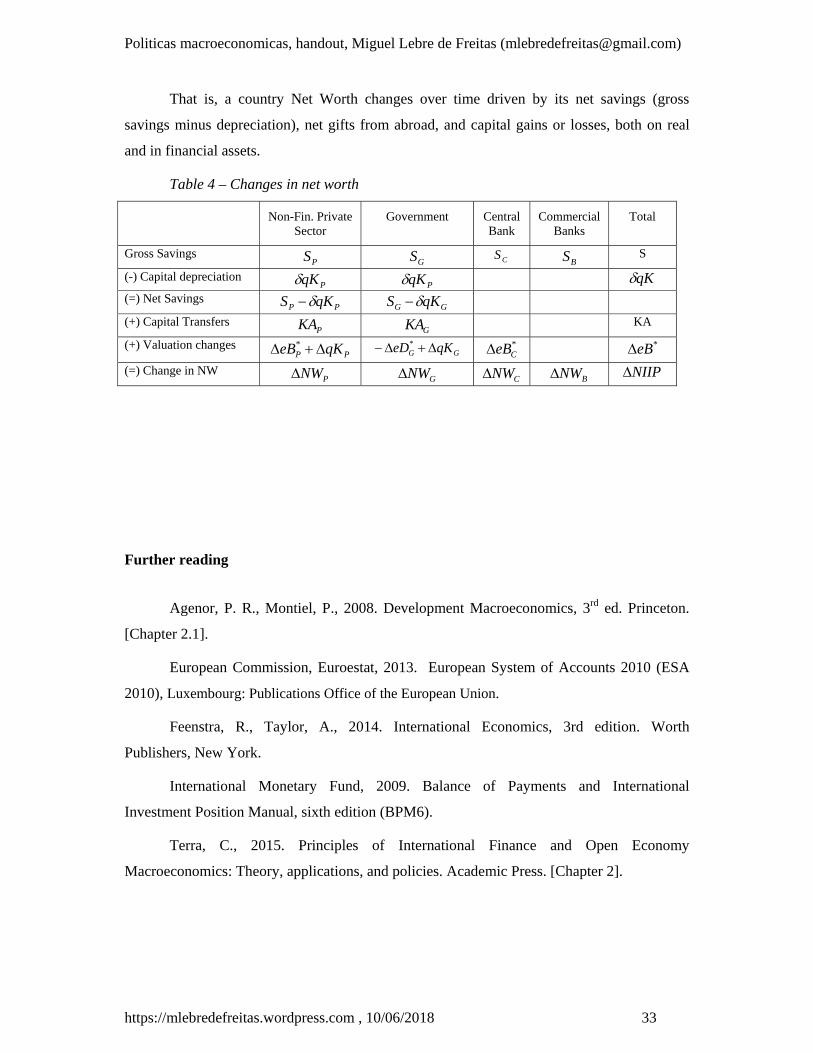

https://mlebredefreitas.wordpress.com , 10/06/2018 33

That is, a country Net Worth changes over time driven by its net savings (gross

savings minus depreciation), net gifts from abroad, and capital gains or losses, both on real

and in financial assets.

Table 4 – Changes in net worth

Non-Fin. Private Sector

Government Central Bank

Commercial Banks

Total

Gross Savings PS GS CS

BS S

(-) Capital depreciation PqK PqK qK

(=) Net Savings PP qKS GG qKS

(+) Capital Transfers PKA GKA KA

(+) Valuation changes PP qKeB * GG qKeD * *

CeB *eB

(=) Change in NW PNW GNW CNW BNW NIIP

Further reading

Agenor, P. R., Montiel, P., 2008. Development Macroeconomics, 3rd ed. Princeton.

[Chapter 2.1].

European Commission, Euroestat, 2013. European System of Accounts 2010 (ESA

2010), Luxembourg: Publications Office of the European Union.

Feenstra, R., Taylor, A., 2014. International Economics, 3rd edition. Worth

Publishers, New York.

International Monetary Fund, 2009. Balance of Payments and International

Investment Position Manual, sixth edition (BPM6).

Terra, C., 2015. Principles of International Finance and Open Economy

Macroeconomics: Theory, applications, and policies. Academic Press. [Chapter 2].

Related Documents