Mobile POS for Mobile Merchants A use case of Mobile Payment in Logistic & Transport Olivier Sery Country Manager & Head of EMV competence center www.tasgroup.eu

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Mobile POS for Mobile Merchants

A use case of Mobile Payment in Logistic & Transpor t

Olivier SeryOlivier SeryCountry Manager & Head of EMV competence center

www.tasgroup.eu

What is behind that “Little” m in mPOS

• How would you define it?A secure device linked to a connected smart device, enabling the processing of a payment with card holder authentication and online authorization in an EMV and PCI compliant manner.

• Does it replaces POS’ like we always known them?

Well, sometimes, but it mostly extends the reach of card Well, sometimes, but it mostly extends the reach of card payment acquiring to unequipped, to cope with high demand periods or to lower the cost of deploying card acceptance devices.

• What more can we do with it ?

Smart phone or PDA application interface. Bundled with a Payment gateway they offer continuity in the buying experience and an even deeper multichannel approach for merchants.

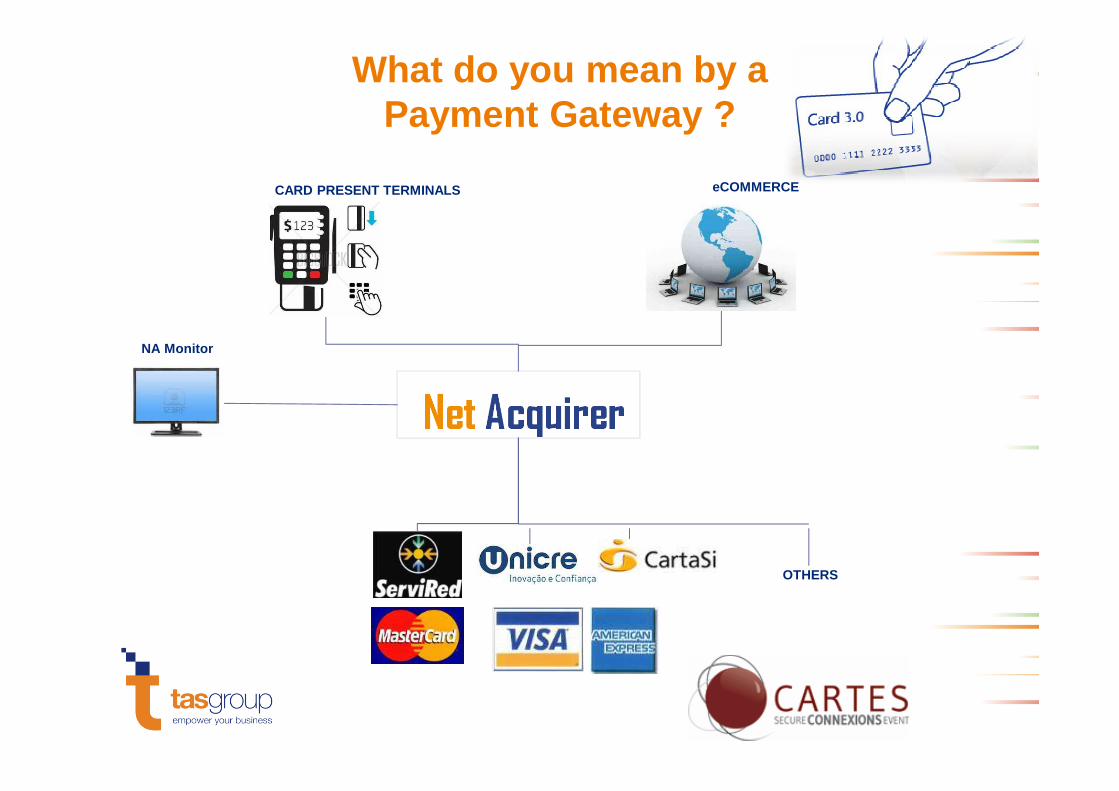

What do you mean by aPayment Gateway ?

eCOMMERCECARD PRESENT TERMINALS

NA Monitor

OTHERS

The values of a Payment Gateway

A Merchant centric solution• Dynamic switching:

– Within a given network (e.g. Least cost routing )– Between Networks/Acquirers, countries.

• Transactions Monitoring:– Multi channel.

– Real time.– Real time.

• Value adding services:– Dynamic Currency Change (DCC).– Tax free.– Wallet & Recurring payments (CNP).– Loyalty & Non financial information storage.– Closed loop cards (prepaid, gift).– Remote Terminal Management

The Values of aPayment Gateway

A dedicated resource focusing on achieving the transaction and integrated within the Acquiring ecosystem.

• One integration :

Direct integration with the management software via a library or app allowing:

– To capture the amount to be charged– To capture the amount to be charged

– Real time feed to the ERP of the payment result

– Same architecture and hardware for all the networks.

• Pin pad agnostic :

– Pin pad are managed by a software layer allowing hardware to be interchanged with no impact.

– The pin pad does not have to support the network protocol (the gateway manages the protocol).

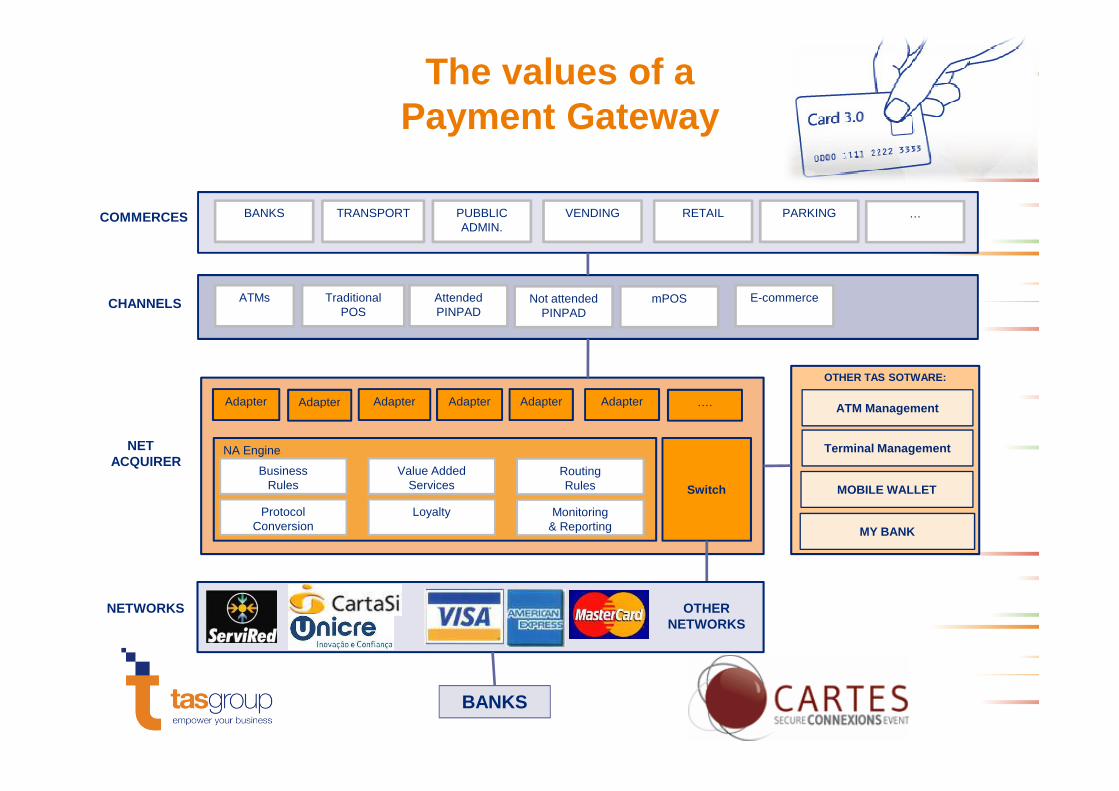

The values of a Payment Gateway

BANKS PUBBLIC ADMIN.

VENDING RETAILTRANSPORT PARKING

ATMs Traditional POS

Not attended PINPAD

mPOS E-commerce

COMMERCES

CHANNELS

…

Adapter AdapterAdapter Adapter Adapter Adapter

OTHER TAS SOTWARE:

….

Attended PINPAD

NETWORKS

NA Engine

Switch

BusinessRules

ProtocolConversion

RoutingRules

Value AddedServices

Loyalty Monitoring& Reporting

Adapter AdapterAdapter Adapter Adapter Adapter

NET ACQUIRER

ATM Management

Terminal Management

MOBILE WALLET

MY BANK

….

OTHER NETWORKS

BANKS

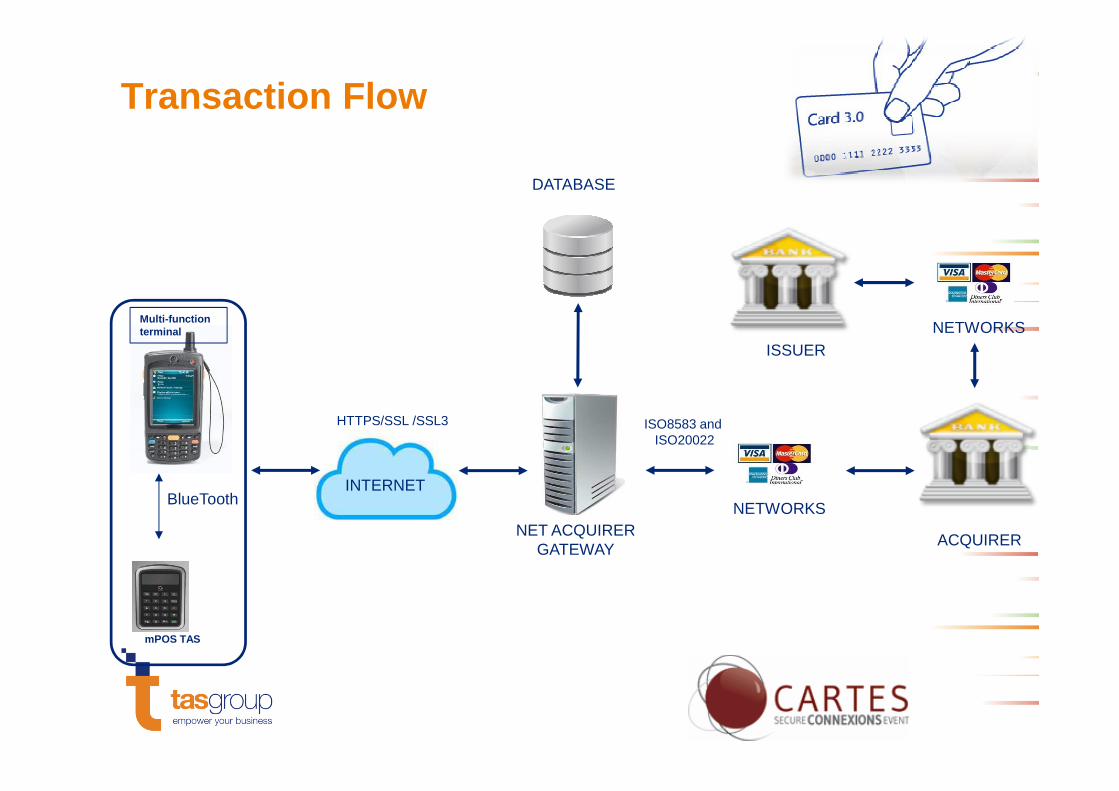

DATABASE

Transaction Flow

NETWORKSISSUER

Multi-function terminal

INTERNET

NET ACQUIRERGATEWAY

BlueTooth

HTTPS/SSL /SSL3

ACQUIRER

mPOS TAS

ISO8583 and ISO20022

NETWORKS

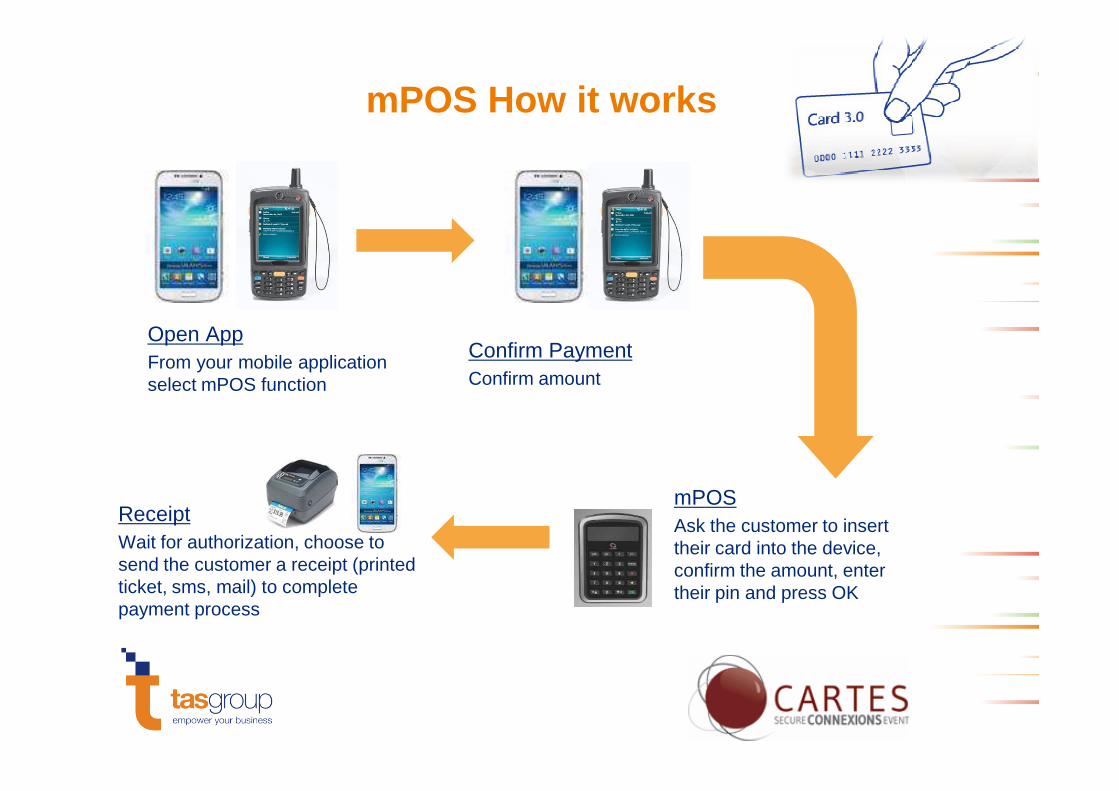

mPOS How it works

Open AppFrom your mobile applicationselect mPOS function

Confirm PaymentConfirm amount

mPOSAsk the customer to insert their card into the device, confirm the amount, enter their pin and press OK

ReceiptWait for authorization, choose to send the customer a receipt (printed ticket, sms, mail) to complete payment process

Enough technicalities … the market

• Our focus:– Merchants or Logistic companies with a “at your door

step” payment issue– People transport services with payment “at end of service”

(wherever that might be)• Some peculiarities

– Need to reduce exposure to cash management for risk and cost (multiple trips to the bank or dedicated service)

– Rugged environment and low technical expertise of users– Existing Dispatch, Route management, ERP integration

solutions to squeeze the payment process in– Existing Hardware and 3G connection

A focused solution

• Heavy duty fully integrated (no battery nor connection needs).

• Terminal agnostic mPOS (Windows Mobile, CE or Android). Mobile, CE or Android).

• SmartPhone based mPOS(Android or iOS) .

mPOS

• Chip&Pin or Magstripe cards.

• PCI PTS (PCI Pin Transaction Security).

• Secure PIN entry.

• Device hardened against physical & • Device hardened against physical & logical hacking.

• SRED module (encryption, Secure Read and Encryption of Data).

Some conclusions at this stageThe technology

Some positive… • EMV level 2 and PCI PTS

3.1 meant to last• Durable• Easy to replace the pin

pad/m-pos (decoupling)

… And some character building• Bluetooth is not a perfect

technology • ISO 8583 flavors and

domestic barriers still make SEPA cross border an • Easy update of the

application• Offering SMS or Email

receipts saves on the printer cost

SEPA cross border an attractive case

• SMS or Email receipts are OK for medium/high amounts but hard to justify and too slow for transport services

Some conclusions at this stageThe Business

Some positive…• New channel, new way to

communicate with your customers, new opportunities

• Cost effective vs a GPRS solution and …

… And some character building• It is hard to change an habit

(Low transaction volumes at start)

• Swap service, buffer stocks and phone supportsolution and …

• With volumes come lower costs on the device

• Savings on Dynamic switching and Acquirer selection easily compensate for the service fees

and phone support

Last but not least … Service continuity

via recurring payments

• Initial payment & enrollment – Card Present:– Payment at delivery or place of service via pin pad. – Enrollment on the spot or via web page. – Secure capture of card sensitive data (CP or secure web).– Secure storage (incl tokenization & PCI Certification).– Secure storage (incl tokenization & PCI Certification).

• Future deliveries – Card Not Present:– With just the proof of Delivery.– A new transaction is generated as Card Not Present.

“Direct Debit” on your card fulfilling PCI.

Empower your business

TAS Group is the strategic partner for business innovation in Payment Systems, Cards and Financial Markets

15

� 30 years experience� More than 500 experts� More than 150 customers

Listed in the Italian Stock Exchange, TAS Group operates globally and has direct presence in Europe USA and Latin America

� Software Applications� Software as a Service� Project Implementation� Professional Services� Housing & Hosting� Other IT Services

Expertise and Innovation

16

Payments Cards Mobile Solutions

Financial ValueChain

Financial Markets

CreditManagement

Treasury &Liquidity

Contact Information

Olivier SeryCountry Manager

& Head of EMV competence center

www.tasgroup.eu

17

Related Documents