Page 1 MNCS COMPANY UPDATE MNC Sekuritas Research Division September 8, 2017 Please see important disclaimer at the back of this report Key Financial Highlight In billion IDR 2014FY 2015FY 2016FY 2017E 2018F Revenues 641.93 2,644.32 4,717.15 7,111.82 9,438.52 Gross Profit 146.71 419.43 1,050.06 1,719.09 2,252.83 Gross Profit Margin 22.85% 15.86% 22.26% 24.17% 23.87% Net Income 140.30 334.37 634.82 1,052.21 1,348.99 Net Profit Margin 21.86% 12.64% 13.46% 14.80% 14.29% ROA 11.67% 7.72% 4.62% 6.20% 6.66% ROE 19.98% 25.12% 8.57% 12.33% 13.52% Financial Performance 1H17 & August 17: Supported by Toll Road Development PT Waskita Beton Precast Tbk (WSBP) booked revenues of Rp2.67 trillion, for an increase of 42.75%, compared to 1H17. This achievement is equivalent to 37.52% of the MNCS estimate, in line with earnings projections from MNCS. The largest contribution to revenue is precast sales, at Rp1.16 trillion, with a contribution of 43.40% to the total, readymix sales of Rp652 billion with contribution of 24.40%, the remainder contributed by construction services, amounting to Rp859 billion and 32.20%. Up until August 2017, WSBP booked new contracts of Rp7 trillion, or 56.63% from total target this year. WSBP booked net profit of Rp436.46 billion, increased by 27.98% compared to same period last year. This achievement is equivalent to 40.62% of the MNCS estimate, in line with net profit projection from MNCS. Robust Financial Performance with Synergy & Efficiency, Undervalued Stock Price, and Corporate Action WSBP is predicted to continue to increase financial performance and positive stock price movement, driven by: 1) Solid synergy with the parent company; 2) Potential increase in new contracts, offset by higher production capacity; 3) Growth of positive financial performance through efficiency measures; 4) Undervalued share price; 5) Corporate action: share buyback amounting to Rp1 trillion. Focus on Developing Toll Roads & Land Acquisition Issue With a large portion of projects derived from the parent company, we see that WSBP is still focused on toll road development. In addition, there are concerns over potential obstacles to the realization of infrastructure development ahead of the political year of 2019. The issue of land acquisition remains one of the classic challenges for WSBP that could hamper business development in the future. Valuation & Recommendation: BUY with TP: Rp690 We maintain a positive outlook on the positive growth prospects of WSBP financial performance, along with a positive growth industry sector in the future. In addition, support from stock buyback action can also be a catalyst that can drive the stock price. We also believe that this moment is a good momentum for investors to be able to accumulate WSBP shares. We thus recommend BUY for WSBP at a target price / TP: Rp690. It implies PE17E/FY18F of 16.91x - 11.60x PBV17E / PBV18F of 2.26x - 1.99x. PT Waskita Beton Precast Tbk (WSBP) Basic Industry and Chemicals Time to Rise Up BUY Stock Data Target Price : Rp690 Current Price : Rp422 52wk Range : Rp645-416 Share Outstanding : 26.361,2 mn Free Float (%) : 10,5% Mkt Capitalization (IDR bn) : 11.282,6 Major Shareholders Research Analyst Gilang Anindito [email protected] (021) 2980 3111 ext. 52235 Sorce : Company Public : 40% PT Waskita Karya Tbk : 59,99% www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Page 1

MNCS COMPANY UPDATE

MNC Sekuritas Research Division September 8, 2017

Please see important disclaimer at the back of this report

Key Financial Highlight

In billion IDR 2014FY 2015FY 2016FY 2017E 2018F Revenues 641.93 2,644.32 4,717.15 7,111.82 9,438.52 Gross Profit 146.71 419.43 1,050.06 1,719.09 2,252.83 Gross Profit Margin 22.85% 15.86% 22.26% 24.17% 23.87% Net Income 140.30 334.37 634.82 1,052.21 1,348.99 Net Profit Margin 21.86% 12.64% 13.46% 14.80% 14.29% ROA 11.67% 7.72% 4.62% 6.20% 6.66% ROE 19.98% 25.12% 8.57% 12.33% 13.52%

Financial Performance 1H17 & August 17: Supported by Toll Road Development PT Waskita Beton Precast Tbk (WSBP) booked revenues of Rp2.67 trillion, for an increase of 42.75%, compared to 1H17. This achievement is equivalent to 37.52% of the MNCS estimate, in line with earnings projections from MNCS. The largest contribution to revenue is precast sales, at Rp1.16 trillion, with a contribution of 43.40% to the total, readymix sales of Rp652 billion with contribution of 24.40%, the remainder contributed by construction services, amounting to Rp859 billion and 32.20%. Up until August 2017, WSBP booked new contracts of Rp7 trillion, or 56.63% from total target this year. WSBP booked net profit of Rp436.46 billion, increased by 27.98% compared to same period last year. This achievement is equivalent to 40.62% of the MNCS estimate, in line with net profit projection from MNCS. Robust Financial Performance with Synergy & Efficiency, Undervalued Stock Price, and Corporate Action WSBP is predicted to continue to increase financial performance and positive stock price movement, driven by: 1) Solid synergy with the parent company; 2) Potential increase in new contracts, offset by higher production capacity; 3) Growth of positive financial performance through efficiency measures; 4) Undervalued share price; 5) Corporate action: share buyback amounting to Rp1 trillion. Focus on Developing Toll Roads & Land Acquisition Issue With a large portion of projects derived from the parent company, we see that WSBP is still focused on toll road development. In addition, there are concerns over potential obstacles to the realization of infrastructure development ahead of the political year of 2019. The issue of land acquisition remains one of the classic challenges for WSBP that could hamper business development in the future. Valuation & Recommendation: BUY with TP: Rp690 We maintain a positive outlook on the positive growth prospects of WSBP financial performance, along with a positive growth industry sector in the future. In addition, support from stock buyback action can also be a catalyst that can drive the stock price. We also believe that this moment is a good momentum for investors to be able to accumulate WSBP shares. We thus recommend BUY for WSBP at a target price / TP: Rp690. It implies PE17E/FY18F of 16.91x - 11.60x PBV17E / PBV18F of 2.26x - 1.99x.

PT Waskita Beton Precast Tbk (WSBP) Basic Industry and Chemicals

Time to Rise Up

BUY

Stock Data

Target Price : Rp690

Current Price : Rp422

52wk Range : Rp645-416

Share Outstanding : 26.361,2 mn

Free Float (%) : 10,5%

Mkt Capitalization (IDR bn)

: 11.282,6

Major Shareholders

Research Analyst Gilang Anindito [email protected] (021) 2980 3111 ext. 52235

Sorce : Company

Public : 40%

PT Waskita Karya Tbk : 59,99%

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

Company Update Report | MNC Sekuritas Research Division

Page 2

Please see important disclaimer at the back of this report

WSBP booked revenues of Rp2.67 trillion, or increased by 42.75%, compared to 1H17. The largest contribution to revenue is Rp1.16 trillion in precast sales, marking 43.40% of the total, readymix sales of Rp652 billion with a contribution of 24.40% and construction services at Rp859 billion with a contribution of 32.20%. In addition, WSBP booked net profit of Rp436.46 billion, for an increase of 27.98% compared to same period last year. New contracts earned up to 1H17 amounted to Rp5.57 trillion, equivalent to 45.06% of the total target of WSBP. The total of contracts managed by WSBP up to 1H17 amounted to Rp15.75 trillion, exceeding the realization of 2016 of Rp15.01 trillion. Until August 2017, WSBP booked new contracts of Rp7 trillion, or 56.63% of total target this year. To pursue new contracts, WSBP needs Rp5.36 trillion. Toll road projects to be pursued are Cibitung-Cilincing (Rp2 trillion), Kualanamu-Prapat (Rp500 billion), Legundi-Bunder (Rp1.2 trillion), Probolinggo-Banyuwangi (Rp2.5 trillion), and Penajam-Balikpapan (Rp750 billion – Rp1 trillion). WSBP’s revenue growth of 1H17 is equivalent to 37.52% of the MNCS estimate, in line with earnings projections from MNCS. Meanwhile, WSBP’s net profit of 1H17 is equivalent to 40.62%, in line with net profit projection from MNCS.

Financial Performance 1H17 & August 17: Supported by Toll Road

Exhibit 01. New Contracts (Rp Trillion)

Source : WSBP

WSBP’s FY17E Targets: Optimistic Growth Still Continues

Revenue is targeted at Rp7.75 trillion, or 64.3% higher in FY17E. Meanwhile, net profit is targeted at Rp1.13 trillion, for an increase of 78% from the realization of net income in FY16. As for new contracts, WSBP targets Rp12.36 trillion, or 1.3% of the actual acquisition of new contracts last year. WSBP allocated Rp1.99 trillion for capital expenditures: Rp1.17 trillion for capital expenditure, readymix at Rp67 billion, Rp500 billion for quarries and Rp256 billion for equipment.

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

4,01 2,66

12,22 12,36

14,95

-33.67%

359.40%

1.15% 20.95%

FY14 FY15 FY16 FY17E FY18F

CAGR FY14-FY18F 30.11%

New Contract Growth

Company Update Report | MNC Sekuritas Research Division

Page 3

Please see important disclaimer at the back of this report

Exhibit 02. Precast and Ready Mix Plant

Source : WSBP

WSBP is one of the subsidiaries of PT Waskita Karya (Persero) Tbk (WSKT), one of the largest state-owned construction companies in Indonesia. WSBP main focus is on the production of precast and readymix concrete. The precast segment is a molded concrete piece of a size already custom-made for construction work. Advantage of precast concrete for construction work is that it can save time and cost. Meanwhile, readymix segment is ready-made bulk concrete casts, used in medium-to-upper scale projects. Currently, WSBP has 10 precast factories, with a capacity of 3.25 million tons and 56 readymix batching plants, with an hourly production capacity of 90 cubic meters, spread across several regions. We believe that the factories scattered across several areas can enable WSBP to reach projects to be undertaken. This can improve the efficiency of the Company and lower costs.

With WSKT's projects growing every year, there will be a very positive impact. It is predicted that in 2017 WSBP will work on around 80% of the total projects from the parent company, and 20% from private projects %. The focus of the projects undertaken by the parent company is toll road development. Thus, the majority of contracts managed by WSBP for this year are within the Java trans-toll project. This synergy not only enhances the growth of WSBP performance, but also has a positive impact on the parent company.

Subsidiary of PT Waskita Karya (Persero) Tbk with Focus on Precast and Ready Mix

Solid Synergy with WSKT

Exhibit 03. Synergy with WSKT

Source : WSBP

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

Year 2014 2015 2016 2017F

Contract Value(IDR)

● Bekasi-Cawang-Kp.Melayu (Becakayu Seksi 1-2) ● Pejagan Pemalang (Seksi 3) ● Pejagan Pemalang (Seksi 4) ● Cibitung - Cilincing● Pejagan Pemalang (Seksi 1-2) ● Kuala Tanjung Port ● Cimanggis Cibitung Paket 2 ● Cinere -Serpong● Depok - Antasari Tollroad ● MKTT ● Pemalang Batang ● Manado - Bitung

● Solo - Ngawi (Seksi 1-2) ● Batang Semarang ● Terbanggi Besar – Kayu Agung● Ngawi Kertosono ● Bogor Ciawi 2 – 4 ● Tol Kunciran – Bandara● Cimanggis Cibitung Paket 1 ● LRT – Palembang ● Terbanggi Besar – Mesuji

● Legundi – Bunde ● Tol Kediri – Kertosono● Kayu Agung- Palembang – Betung ● Japanan Mojosari – Mojokerto● Pasuruan – Probolinggo ● Dermaga Kijing● Boyolali – Salatiga ● Penajam – Balikpapan

● Tol Probolinggo - Banyuwangi● Tol Cinere – Serpong Jaya

Projects

3.3 T 2.2 T 12.2 T Potentials

Company Update | MNC Sekuritas Research Division

Page 4

Please see important disclaimer at the back of this report

New Contract Enhancement is Offset by Increased Production Capacity

According to the Draft State Budget (RAPBN) 2018, the amount of budget for infrastructure projects amounts to Rp409 trillion, or increased by 7.63% from the APBN 2017 infrastructure budget Rp106 trillion or 25.92% of the total infrastructure budget is to be allocated to the Ministry of Public Works and Public Housing (PUPR). The funds will be used by the Ministry of PUPR for 46,000 km of national roads, 856 km of new road builders, 8,761 meters of bridges, and 25 km of toll roads. In addition, if it refers to the government's strategic plan 2015-2019, it is estimated that there are 1,060 km of new toll roads. However, based on the Toll Road Regulatory Agency (BPJT) in a study predicted to be completed by 2019 there will be approximately 1,850 km of new toll roads, with an estimated investment value of between Rp220 trillion and RP230 trillion. We consider this to be a positive catalyst for WSBP, since the synergy with the parent company is the construction of toll roads. With this potential, it provides wide space for WSBP to improve its financial performance more positively.

Exhibit 04. Toll Road Projects until 2019

Source : BPJT

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

No Toll Road lenght (Km)Investment Value

Estimation1 Pasuruan - Probolinggo 31 42 Probolinggo - Banyuwangi 170 183 Krian-Legundi-Bunder-Manyar 39 74 Jakarta - Cikampek II (elevated) 36 145 Jakarta - Cikampek II sisi selatan (Jatiasih-Cipularang-Sadang) 64 186 Yogyakarta - Solo 40 27 Semarang - Demak 24 38 Sukabumi - Ciranjang - Padalarang 61 59 Sigli - Banda Aceh 75 13

10 Binjai - Langsa 110 1911 Tebing Tinggi - Pematang Siantar - Parapat - Tarutung - Sibolga 200 2012 Bukit Tinggi - Padang Ginjang - Lubuk Alung - Padang 55 813 Rantau Prapat - Kisaran 100 1714 Langsa - Lhokseumawe 135 2215 Lhokseumawe - Sigli 135 2216 Pekanbaru - Bangkinang - Payakumbuh - Bukit Tinggi 185 2917 Yogyakarta - Bawen 72 1218 Pekanbaru-Dumai 13119 Terbanggi Besar-Kayu Agung 185

Total 1,850 232

Company Update | MNC Sekuritas Research Division

Page 5

Please see important disclaimer at the back of this report

As the new contracts continue to grow, WSBP sees that there is great potential for project work every year. Thus, WSBP anticipates increasing its production capacity so as to be able to meet the needs of these projects. Currently, WSBP is estimated to be able to reach production capacity of up to 3.25 million tons in FY17E. This will continue as a consequence of the increase in WSBP’s new contracts. Predicted to FY18E, WSBP is able to achieve production capacity of up to 3.55 million tons. This is underpinned by the construction of a new 200,000 ton plant located in Medan, Panajam of 300,000 tons, and increasing capacity plant in Gassing up to 200,000 tons by 2018. We consider that WSBP move to continue to increase its production capacity to anticipate increased project work will continue to grow in some areas. This step is correct, considering WSBP is predicted to not only focus development on the island of Java, but to expand outside Java.

Exhibit 06. Precast Capacity (Thousand Tons)

Source : WSBP, MNCS Estimate

800

1.800

2.650

3.250

3.750

FY14 FY15 FY16 FY17E FY18F

CAGR FY14-FY18F 32.20%

Production Capacity

125%

47.22%

22.64%

15.38%Growth

Exhibit 05. New Contracts (Rp Trilion)

Source : WSBP, MNCS Estimate

4,01 2,66

12,22 12,36

14,95

-33.67%

359.40%

1.15% 20.95%

FY14 FY15 FY16 FY17E FY18F

CAGR FY14-FY18F 30.11%

New Contract Growth

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

The impact of the growth of toll road development is predicted to affect the increase of new contracts to be obtained by WSBP. Despite the increase in FY17E new contracts, increased by 1.15% or Rp12.36 trillion, we assess that up to FY18F there will be a new contract increase of 20.98% of Rp14.95 trillion. This is supported by the increase in toll road projects and other private projects that are predicted to continue to grow.

Company Update | MNC Sekuritas Research Division

Page 6

Please see important disclaimer at the back of this report

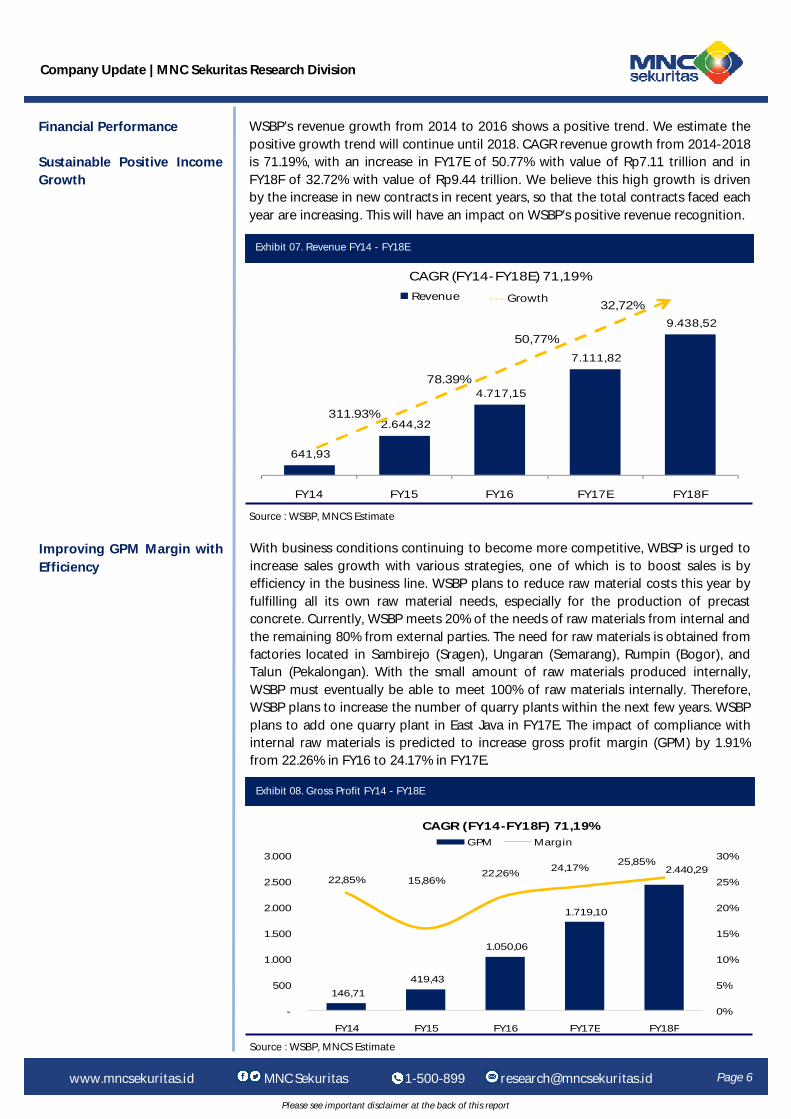

Financial Performance Sustainable Positive Income Growth

WSBP’s revenue growth from 2014 to 2016 shows a positive trend. We estimate the positive growth trend will continue until 2018. CAGR revenue growth from 2014-2018 is 71.19%, with an increase in FY17E of 50.77% with value of Rp7.11 trillion and in FY18F of 32.72% with value of Rp9.44 trillion. We believe this high growth is driven by the increase in new contracts in recent years, so that the total contracts faced each year are increasing. This will have an impact on WSBP’s positive revenue recognition.

Improving GPM Margin with Efficiency

With business conditions continuing to become more competitive, WBSP is urged to increase sales growth with various strategies, one of which is to boost sales is by efficiency in the business line. WSBP plans to reduce raw material costs this year by fulfilling all its own raw material needs, especially for the production of precast concrete. Currently, WSBP meets 20% of the needs of raw materials from internal and the remaining 80% from external parties. The need for raw materials is obtained from factories located in Sambirejo (Sragen), Ungaran (Semarang), Rumpin (Bogor), and Talun (Pekalongan). With the small amount of raw materials produced internally, WSBP must eventually be able to meet 100% of raw materials internally. Therefore, WSBP plans to increase the number of quarry plants within the next few years. WSBP plans to add one quarry plant in East Java in FY17E. The impact of compliance with internal raw materials is predicted to increase gross profit margin (GPM) by 1.91% from 22.26% in FY16 to 24.17% in FY17E.

Exhibit 07. Revenue FY14 - FY18E

Source : WSBP, MNCS Estimate

Exhibit 08. Gross Profit FY14 - FY18E

Source : WSBP, MNCS Estimate

641,93

2.644,32

4.717,15

7.111,82

9.438,52

FY14 FY15 FY16 FY17E FY18F

CAGR (FY14-FY18E) 71,19%Revenue --- Growth

311.93%

78.39%

50,77%

32,72%

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

146,71 419,43

1.050,06

1.719,10

2.440,29 22,85% 15,86%

22,26% 24,17% 25,85%

0%

5%

10%

15%

20%

25%

30%

-

500

1.000

1.500

2.000

2.500

3.000

FY14 FY15 FY16 FY17E FY18F

CAGR (FY14-FY18F) 71,19%GPM Margin

Company Update | MNC Sekuritas Research Division

Page 7

Please see important disclaimer at the back of this report

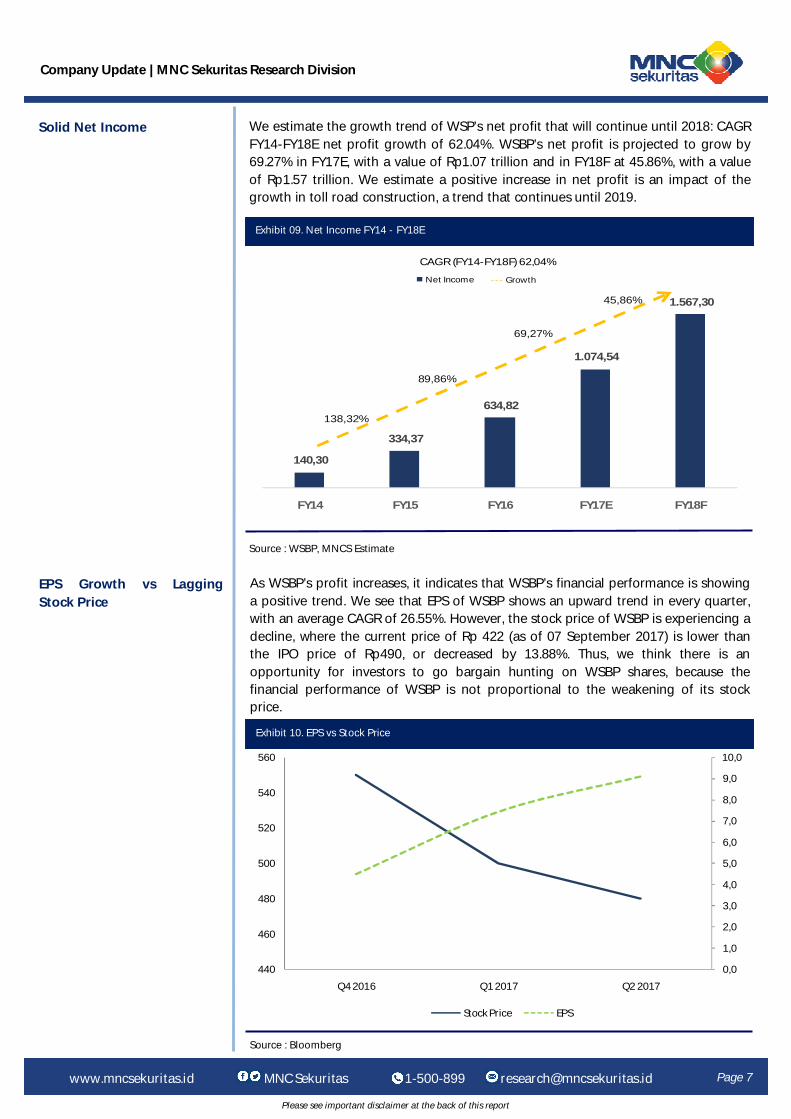

Solid Net Income We estimate the growth trend of WSP’s net profit that will continue until 2018: CAGR FY14-FY18E net profit growth of 62.04%. WSBP’s net profit is projected to grow by 69.27% in FY17E, with a value of Rp1.07 trillion and in FY18F at 45.86%, with a value of Rp1.57 trillion. We estimate a positive increase in net profit is an impact of the growth in toll road construction, a trend that continues until 2019.

EPS Growth vs Lagging Stock Price

As WSBP’s profit increases, it indicates that WSBP’s financial performance is showing a positive trend. We see that EPS of WSBP shows an upward trend in every quarter, with an average CAGR of 26.55%. However, the stock price of WSBP is experiencing a decline, where the current price of Rp 422 (as of 07 September 2017) is lower than the IPO price of Rp490, or decreased by 13.88%. Thus, we think there is an opportunity for investors to go bargain hunting on WSBP shares, because the financial performance of WSBP is not proportional to the weakening of its stock price.

Exhibit 09. Net Income FY14 - FY18E

Source : WSBP, MNCS Estimate

Exhibit 10. EPS vs Stock Price

Source : Bloomberg

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

10,0

440

460

480

500

520

540

560

Q4 2016 Q1 2017 Q2 2017

Stock Price EPS

140,30

334,37

634,82

1.074,54

1.567,30

FY14 FY15 FY16 FY17E FY18F

Net Income

CAGR (FY14-FY18F) 62,04%

--- Growth

138,32%

89,86%

69,27%

45,86%

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

Company Update | MNC Sekuritas Research Division

Page 8

Please see important disclaimer at the back of this report

Corporate Action Through Share Buyback, Worth Rp1 trillion

WSBP plans to buy back shares, starting in 2017. The number to be repurchased is up to 7% of the total, or about 1.84 billion shares. The schedule for the share buyback process of WSBP starts from July 27, 2017 and goes to January 27, 2019. The company plans to set aside Rp1 trillion to conduct share buyback. Funds to conduct the share buyback were obtained from the cash receipts from WSBP receivables from the parent company, which reached Rp1.4 trillion. Later, WSBP will keep the shares of the share buyback process as treasury stock. The purpose of the stock buyback is because WSBP considers that the current stock price does not reflect the positive trend of WSBP’s performance. Currently, WSBP’s average share performance is below the IPO price of Rp490. We believe that this corporate action will impart a positive sentiment to WSBP stock performance. With the stock buyback, it is estimated stock price can reach Rp540 for a short time.

Investment Risk: What is next after Developing Toll Road Projects ?

Currently, the projects obtained by WSBP are mostly from government infrastructure projects. If the government focus is no longer on infrastructure development, it will potentially increase the risk for WSBP’s business growth in the future. The projects undertaken by WSBP are largely derived from the development of toll roads. If the number of toll road projects is reduced as a result of the decline of infrastructure projects from the government, it will have a negative impact on the financial performance of WSBP, which is predicted to take a larger portion of its work from the private sector in the future. We positively assess the strategic steps taken by WSBP to diversify the type of project work and reduce the dominant contribution of the parent company. Along with the upgrading of projects in the future, WSBP will continue to increase factory capacity to balance major projects to be secured in the future. Synergy with other BUMN companies can be undertaken to improve projects and funding to support the realization of project work.

Land Acquisition is One Big Issue

With the focus of toll road development, WSBP will face challenges for land acquisition. For national strategic projects, government has cleared 53% of land. Currently, the government has set up a special agency to manage land acquisition called Lembaga Managemen Aset Negara (LMAN), as of the end of 2016. Later, LMAN will take care of funding and land use planning and land compensation payments. For toll road land acquisition in 2017, Rp13.26 trillion is needed. As for the land acquisition for all strategic projects in 2018 Rp46.8 trillion will be required. Later, these funds require the approval of Dewan Perwakilan Rakyat (DPR). Now, we see if these funds are not distributed, it will impact some projects which cannot run because of incomplete land acquisition. We conclude that if all the land for national strategic projects (especially toll road development) has not been released by 2018, then many toll road projects will not completed by 2019. This may increase the risk for WSBP.

Valuation

and Recommendation :

BUY with TP of Rp690

We maintain a positive outlook on the growth prospects of WSBP financial performance, along with a positive industry sector growth in the future. In addition, support from stock buyback action can be a catalyst that can drive the growth of WSBP stock price. We also believe that this moment represents good momentum for investors to be able to accumulate WSBP shares. We recommend BUY for WSBP with target price / TP: Rp690. It implies PE17E/FY18F of 16.91x/11.60x, PBV17E/PBV18F of 2.26x/1.99x.

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

Company Update | MNC Sekuritas Research Division

Please see important disclaimer at the back of this report

Exhibit 11. Financial Estimate

Source : Company, MNCS Estimate

Page 9 www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

Income Statement Balance Sheet

Cash Flow Ratios

IDR Billion 2014FY 2015FY 2016FY 2017E 2018F

Revenues 641.93 2,644.32 4,717.15 7,111.82 9,438.52

Precast 523.65 2,171.90 3,011.44 5,394.30 6,978.99

Readymix 118.28 472.42 1,705.71 1,717.52 2,459.53

COGS Before Depreciation - 2,140.02 3,553.37 5,392.46 7,185.35

COGS After Depreciation 495.23 2,224.89 3,667.09 5,392.73 7,185.69

Gross Profit Before Depre-ciation

641.93 504.30 1,163.78 1,719.36 2,253.17

Gross Profit After Deprecia-tion

146.71 419.43 1,050.06 1,719.09 2,252.83

Total Expenses 4.01 58.58 100.42 128.77 200.48

Selling - 2.32 4.28 6.71 9.10

General & administration - 53.75 92.73 113.95 181.18

Depreciation - 2.51 3.41 8.10 10.20

Operating Profit (EBIT) 142.70 360.85 949.65 1,590.32 2,052.35

EBITDA 641.93 448.23 1,066.77 1,598.70 2,062.89

Other Income/Expenses - 15.30 17.70 (187.37) (194.37)

Earning Before Tax 142.70 345.55 967.34 1,402.95 1,857.97

Tax Expenses 2.39 11.18 332.53 350.74 508.99

Net Income 140.30 334.37 634.82 1,052.21 1,348.99

EPS (full amount) 5.32 12.68 24.08 39.92 51.17

IDR Billion 2014FY 2015FY 2016FY 2017E 2018F

CFO Total (85.00) (686.14) (3,034.91) 306.08 779.09

Net Income 140.30 334.37 634.82 1,052.21 1,348.99

Depreciation 7.30 87.38 117.13 280.33 351.64

Change in Working Capital (530.48) 694.15 (1,899.90) (785.41) (695.74)

Change in others 297.88 (1,802.04) (1,886.95) (241.06) (225.80)

CFI Total (21.62) (123.56) (833.32) (2,540.95) (2,161.29)

Change in ST Investment - - - - -

Change in LT Investment - (2,320.14) (1,307.51) (580.42) (589.13)

Capex - (755.48) (2,069.21) (1,997.27) (1,607.86)

Change in Others (21.62) 2,952.06 2,543.39 36.74 35.70

CFF Total 378.84 635.66 7,975.86 1,624.49 1,170.04

Change in ST debt - 301.78 1,605.28 968.12 940.64

Change in LT debt - 459.26 989.67 576.71 134.09

Equity financing 617.57 217.48 1,801.06 - -

Dividend payment - - (379.74) (420.89) (404.70)

Others (238.73) (342.87) 3,959.59 500.55 500.00

Net Cash Increase 272.22 (174.04) 4,107.63 (610.39) (212.16)

Closing Balance 272.22 98.19 4,205.82 3,595.44 3,383.27

IDR Billion 2014FY 2015FY 2016FY 2017E 2018F

Revenue Growth 311.93% 78.39% 50.77% 32.72%

Operating Profit Growth 152.88% 163.17% 67.46% 29.05%

EBITDA Growth -30.18% 138.00% 49.86% 29.04%

Net Profit Growth 138.32% 89.86% 65.75% 28.20%

Current Ratio 196.01% 41.27% 170.63% 145.06% 132.70%

Quick Ratio 182.38% 25.09% 152.15% 123.82% 111.14%

Assset/ Liabilities 240.31% 144.34% 217.01% 201.12% 197.03%

Liabilities/Equity 71.27% 225.54% 85.46% 98.90% 103.06%

Net Debt to Equity 0.00% 57.19% 45.32% 57.41% 59.87%

Gross Profit Margin 22.85% 15.86% 22.26% 24.17% 23.87%

Operating Profit Margin 22.23% 13.65% 20.13% 22.36% 21.74%

Ebitda Margin 23.24% 16.95% 22.61% 22.48% 21.86%

Net Profit Margin 21.86% 12.64% 13.46% 14.80% 14.29%

ROA 11.67% 7.72% 4.62% 6.20% 6.66%

ROE 19.98% 25.12% 8.57% 12.33% 13.52%

IDR Billion 2014FY 2015FY 2016FY 2017E 2018F

Current Assets 980.93 1,003.67 8,132.62 9,059.61 10,482.60

Cash and Cash Equivalents 272.22 98.19 4,205.82 3,595.44 3,383.27

Account Receivable 640.47 511.95 3,046.13 4,137.52 5,396.33

Inventories 21.18 54.55 231.95 348.61 404.97

Others current Assets 47.06 338.98 648.72 978.04 1,298.02

Non-Current Assets 221.68 3,328.74 5,601.65 7,918.90 9,784.55

Fix Asset - net 221.68 987.35 1,932.85 3,648.80 4,905.02

Other Non-Current Assets - 2,341.39 3,668.79 4,270.11 4,879.53

TOTAL ASSETS 1,202.61 4,332.41 13,734.27 16,978.51 20,267.14

Current Liabilities 500.44 2,432.18 4,766.32 6,245.35 7,899.61

Short-term Bank Loans - 301.78 1,907.06 2,875.18 3,815.83

Account payable 131.17 730.17 1,541.85 1,964.49 2,583.93

Other current liabilities 369.27 1,400.23 1,317.40 1,405.67 1,499.85

Non-Current Liabilities - 569.40 1,562.45 2,196.79 2,386.87

Long-term Liabilities - Net - 459.26 1,448.92 2,025.63 2,159.72

Other Liabilities - 110.15 113.52 171.16 227.15

TOTAL EQUITY 702.17 1,330.82 7,405.50 8,536.37 9,980.66

TOTAL LIABILITIES & EQ-UITY

1,202.61 4,332.41 13,734.26 16,978.51 20,267.14

MNC SEKURITAS RESEARCH TEAM

Edwin J. Sebayang Head of Retail Research, Technical, Auto, Mining [email protected] (021) 2980 3111 ext. 52233

I Made Adi Saputra Head of Fixed Income Research [email protected] (021) 2980 3111 ext. 52117

Disclaimer This research report has been issued by PT MNC Sekuritas, It may not be reproduced or further distributed or published, in whole or in part, for any purpose. PT MNC Sekuritas has based this document on information obtained from sources it believes to be reliable but which it has not independently verified; PT MNC Sekuritas makes no guarantee, representation or warranty and accepts no responsibility to liability as to its accuracy or completeness. Expression of opinion herein are those of the research department only and are subject to change without notice. This document is not and should not be construed as an offer or the solicitation of an offer to purchase or subscribe or sell any investment. PT MNC Sekuritas and its affiliates and/or their offices, director and employees may own or have positions in any investment mentioned herein or any investment related thereto and may from time to time add to or dispose of any such investment. PT MNC Sekuritas and its affiliates may act as market maker or have assumed an underwriting position in the securities of companies discusses herein (or investment related thereto) and may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or underwriting services for or relating to those companies.

Page 10

Victoria Venny Telco, Infrastructure, Logistics [email protected] (021) 2980 3111 ext. 52236

Rr. Nurulita Harwaningrum Banking [email protected] (021) 2980 3111 ext. 52237

Krestanti Nugrahane Widhi Research Associate [email protected] (021) 2980 3111 ext. 52166

Sukisnawati Puspitasari Research Associate [email protected] (021) 2980 3111 ext. 52307

Thendra Crisnanda Head of Institutional Research, Strategy [email protected] (021) 2980 3111 ext. 52162

Gilang Anindito Property, Construction [email protected] (021) 2980 3111 ext. 52235

Rheza Dewangga Nugraha Junior Analyst of Fixed Income [email protected] (021) 2980 3111 ext. 52294

MNC Research Investment Ratings Guidance BUY : Share price may exceed 10% over the next 12 months

HOLD : Share price may fall within the range of +/- 10% of the next 12 months SELL : Share price may fall by more than 10% over the next 12 months

Not Rated : Stock is not within regular research coverage

PT MNC SEKURITAS MNC Financial Center Lt. 14 – 16

Jl. Kebon Sirih No. 21 - 27, Jakarta Pusat 10340 Telp : (021) 2980 3111 Fax : (021) 3983 6899 Call Center : 1500 899

Benny Narendro Head of Institutional Client [email protected] (021) 2980 3111 ext. 52198

Nesya Kharismawati Equity Sales Manager [email protected] (021) 2980 3111 ext. 52182

Okhy Ibrahim Manager Equity Trader [email protected] (021) 2980 3111 ext. 52180

Harun Nurrosyid Manager Equity Trader [email protected] (021) 2980 3111 ext. 52187

Anastasia Pratiwi Manager Equity Institution [email protected] (021) 2980 3111 ext. 52181

Agus Eko Santoso Manager Equity Trader [email protected] (021) 2980 3111 ext. 52185

Gilang Ramadhan Manager Equity Trader [email protected] (021) 2980 3111 ext. 52178

Iman Hadimulya, ST Manager Equity Institution [email protected] (021) 2980 3111 ext. 52174

MNC SEKURITAS EQUITY SALES TEAM

www.mncsekuritas.id MNC Sekuritas 1-500-899 [email protected]

Company Update | MNC Sekuritas Research Division

Related Documents