Master Limited P ar tner ship Pr imer Un derstanding an Emerging A sset Class SteelPath is a registered investment advisor that ma nages portolios ocused on midstream energy Master Limited Partnerships (MLPs) or a variety o institutional and individual clients. Te company ocuses on undamental analysis in this emerging asset class, combining a detailed, bottoms-up private equity philosophy with risk management programs designed to preserve capita l and mitig ate portolio volatility. SteelPath believes that this sector o the energy inrastructure space will continue to grow dramatically over the next decade and oers one o the most attractive risk-reward investment proles available to investors. SteelPath positions its portolios with a long-term investment horizon by ocusing on those companies with the strongest mana gement teams and most attractive investment opportunity sets in the midstream energy sector to provide downside protection with predictable distribution growth. McKinney Avenue Dallas, X steelpath.com Nothing in this document should be considered a solicitation to buy or an oer to sell shares o any SteelPath und. Tis report does not represent a recommendation to undertake transactions in MLPs, and is provided or inormational pur poses only, and may not be reproduced or redistributed. Tere is no representation that the inormation is accurate, complete or current, or that it reects the current opinion or all inormation known to SteelPath, its principals, or aliates. Past perormance is no gu arantee o uture results. Copyright; No Unauthorized Redistribution Tis research report was prepared by SteelPath in and is under protection o the copyright laws. Neither the whole nor any part o this materia l may be duplicated in any orm or by any means. Tis material may not be redistributed or disclosed to anyone without the prior SteelPath’s previous written consent.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 1/31

Master Limited

Partnership PrimerUnderstanding an Emerging Asset ClassSteelPath is a registered investment advisor that manages port olios ocused onmidstream energy Master Limited Partnerships (MLPs) or a variety o institutionaland individual clients.

Te company ocuses on undamental analysis in this emerging asset class,combining a detailed, bottoms-up private equity philosophy with risk managementprograms designed to preserve capital and mitigate port olio volatility. SteelPathbelieves that this sector o the energy in rastructure space will continue to growdramatically over the next decade and o ers one o the most attractive risk-rewardinvestment pro les available to investors.

SteelPath positions its port olios with a long-term investment horizon by ocusingon those companies with the strongest management teams and most attractiveinvestment opportunity sets in the midstream energy sector to provide downsideprotection with predictable distribution growth.

McKinney AvenueDallas, X

steelpath.com

Nothing in this document should be considered a solicitation to buy or an o er to sell shares o any SteelPath und. Tis report does not represent arecommendation to undertake transactions in MLPs, and is provided or in ormational purposes only, and may not be reproduced or redistributed. Tereis no representation that the in ormation is accurate, complete or current, or that it re ects the current opinion or all in ormation known to SteelPath, itsprincipals, or a liates. Past per ormance is no guarantee o uture results.

Copyright; No Unauthorized Redistribution

Tis research report was prepared by SteelPath in and is under protection o the copyright laws. Neither the whole nor any part o this materia l maybe duplicated in any orm or by any means. Tis material may not be redistributed or disclosed to anyone without the prior SteelPath’s previous written

consent.

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 2/31

SteelPath Fund AdvisorsMaster Limited Partnership Primer

able o ContentsExecut ive Summary.................................................................................................................................................................................................................................

Why own Master Limited Partne rships?..............................................................................................................................................................................................Tematic Investment in US Energy In ra struc ture Growth .............................................................................................................................................Hard Asset Play Provides angible Value in a Potentially In ationary Environment...................................................................................................Better Business Models........................................................................................................................................................................................................MLPs Exhibit Insigni cant Correl ation w ith the Broader Equit ies Market...................................................................................................................

An Emerging Asset Class........................................................................................................................................................................................................................Substantial Investment Required to Meet US In rastructure Demands........................................................................................................................Te Future o MLPs is Here oday.......................................................................................................................................................................................Structural Valuation Issues Create Substantial Long- erm Upside...............................................................................................................................Flying Under the Radar – L imited Institutional Ownership o MLPs...........................................................................................................................Te Emergence o Pure-Play Public ly raded GPs............................................................................................................................................................

Te Aler ian MLP Index Series ..............................................................................................................................................................................................................

What is a Midstream Asset?.................................................................................................................................................................................................................Crude Oil/Re ned Products ranspor tation....................................................................................................................................................................Marine ranspor tation.......................................................................................................................................................................................................Crude Oil/Re ned Products ermina ls............................................................................................................................................................................Midstream Natura l Gas Indust ry......................................................................................................................................................................................

ranspor tation....................................................................................................................................................................................................................Gathering.............................................................................................................................................................................................................................Dehydration.........................................................................................................................................................................................................................

reating................................................................................................................................................................................................................................Processing............................................................................................................................................................................................................................Fractionation.......................................................................................................................................................................................................................Storage..................................................................................................................................................................................................................................LNG ranspor tation............................................................................................................................................................................................................

Valuing Midstream Energy Businesses...............................................................................................................................................................................................Popular Misconcept ion: Relat ive Yield.............................................................................................................................................................................Stable, Growing Distributions – Te De ning Characteristic o the MLP Model........................................................................................................

Distr ibution Discount Model...............................................................................................................................................................................................................Investment/Acquisition Optiona lity.................................................................................................................................................................................

Other Relat ive Price Metrics................................................................................................................................................................................................................

Te Re-Bir th o the E&P MLP...............................................................................................................................................................................................................

Fundamental Risks ................................................................................................................................................................................................................................Regu latory Risk...................................................................................................................................................................................................................Demand-Side Troughput Risks........................................................................................................................................................................................Supply Asset -Speci c Risks................................................................................................................................................................................................Macro Supply Disruptions..................................................................................................................................................................................................Environmental Accidents...................................................................................................................................................................................................

errorism.............................................................................................................................................................................................................................ax Law Changes........................................................................................................................................... .....................................................................

Financial Risks.......................................................................................................................................................................................................................................Interest Rates.......................................................................................................................................................................................................................Equity Volatilit y and Correl ation......................................................................................................................................................................................Equity Crises........................................................................................................................................................................................................................

Appendix................................................................................................................................................................................................................................................A History o the Creation o MLPs.....................................................................................................................................................................................Genera l/Limited Partner Struc ture..................................................................................................................................................................................Income ax reatment........................................................................................................................................................................................................

Disclaimers.............................................................................................................................................................................................................................................

3

45677

899

101011

12

13131415151616171717171818

202020212122 22

2323242425252525

25262627

28282930

31

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 3/31

Executive SummaryMaster Limited Partnerships, or MLPs, are engaged in thetransportation, storage, processing, re ning, marketing,exploration, production, and mining o minerals or naturalresources. By con ning their operations to these speci c ac-tivities, their interests, or units, are able to trade on publicsecurities exchanges exactly like the shares o a corpora-tion, without entity level taxation. O the partnershipsthat SteelPath ollows closely, two-thirds trade on the New York Stock Exchange with nearly all o those remainingon the NASDAQ. MLPs must make public lings with theSecurities and Exchange Commission and must le -Ks,

-Qs, and notices o material changes like any publiclytraded corporation. MLPs are subject to the record keepingand disclosure requirements o the Sarbanes-Oxley Act.

Since , the Alerian MLP Index (NYSE: AMZ) has gener-ated compound annual total returns o . %, under theradar o the pro essional investment community. Tesestrong returns were generated through a combination o current yield and consistent distribution growth driven bythe uniquely attractive business models a orded by thesecompanies’ regional ranchise monopolies.

Tese partnerships generate predictable and growing cashows (and there ore distributions) predicated on the ol-

lowing:• Long-lived, high-value physical assets• Producer Price Index (PPI) revenue indexing, which

provides predictable growth and a built-in in ationhedge or port olios

• Substantial barriers to entry, which generate attractiveorganic investment opportunities

• Strong operating leverage through hard assets thatmagni y inelastic demand

Te energy in rastructure MLP sector, which includes com-panies that own and operate long-lived, high-value physi-

cal assets that engage in the transportation and storage o natural resources such as re ned petroleum products andnatural gas, today represents $ billion o public marketcapitalization out o a total $ billion in MLP marketcapitalization. MLPs have traditionally been owned byUnited States retail investors (institutional MLP owner-ship is less than %). Te market capitalization o the MLPsector has grown exponentially over the last decade, drivenby asset rationalization into MLPs, which have the operat-ing expertise and the organizational structure to optimize

their use, and by demand or new energy in rastructure. In, the sector market capitalization was a mere $ bil-

lion; this gure doubled by to $ billion and doubledyet again by to $ billion. SteelPath expects MLPmarket capitalization to continue to grow rom the current$ billion level as the demand or new energy in rastruc-ture continues to drive investment.

Tematically, an investment in an energy in rastructureMLP is an investment in the build-out o US energy in-

rastructure over the next decade. Unlike US or Canadianroyalty trusts, which own depleting resource pools, theseare toll-road business models on long-li e assets. Modernpipelines bene t rom rust coatings and cathodic protec-tion that will allow these pipelines to operate withoutmajor maintenance or years or more. In act, there arepipelines that were put in the ground prior to World War IIwhich had no rust coating o any kind that are still in usetoday. Tere is much speculation today about the uturetrajectory o oil prices, the appropriate levels o storage,and the outlook or the US re ning industry. However, onething that most “experts” agree on, regardless o whetherthey are predicting $ , $ , or $ per barrel o oil, ispredictable % annualized energy demand growth in the USover the next two decades, in spite o the current economicsituation. Demographic shi ts and population growthtrends increase the demand or energy goods. As a result,long-haul pipeline MLPs are agnostic to these commodityprice orecasts, and bene t rom simple throughput gainsin a xed-cost pipeline system.

Industry estimates indicate that the US needs $ billiono new natural gas in rastructure over the next decade anda nearly equivalent amount in crude oil and re ned petro-leum products processing, storage, and transportation in-

rastructure. Additionally, there are more than $ billiono US midstream assets currently owned in both private

and public corporate structures that are being rationalizedinto the asset class through acquisition and the creation o new MLPs. Te MLP structure is also ripe or billions morein new technology in rastructure once these assets are builtand generating cash, including lique ed natural gas (LNG)terminals, gas-to-liquids technology, and coal gasi cation.SteelPath believes that this emerging asset class representsan attractive value proposition given the low-risk businesspro les o most MLPs.

SteelPath Fund AdvisorsMaster Limited Partnership Primer

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 4/31

MLPs are attractive, not because o their tax treatment

or structure, but because o the type o assets that havemigrated into the asset class over the last decade. Energyin rastructure is an attractive business model – regionalmonopolies with transparent ederal regulation that trans-port commodities with inelastic demand. An investmentmanager cannot take this type o pure-play exposure intohis or her port olio through any other orm o public equi-ties. I o ce buildings are to be considered a stable invest-ment in real value, the pipelines that transport the naturalgas to run the air-conditioning in the summer and heat theproperty in the winter ought to have that same permanentvalue.

Many will note, however, that the asset class is not whatit used to be, and is moving away rom the type o assetswe have described above. Tis is partly true. With a surgein initial public o erings (more than in and combined), many new types o assets have entered thestructure, and many o them do not have the same mo-nopoly ootprints or supply diversity as their predecessors.Tere has been a very strong trend closer to the wellhead ascommodity-price-sensitive businesses dominated the IPOspace over the and period. Earnings volatility isnot synonymous with lower quality but nancial leverage,distribution levels, and hedging strategies must be appro-priately conservative given such volatility. Investors mustalso be cognizant o such risks in deciding the appropriateequity price. Tat being said, SteelPath has always beenand will remain ocused, as a rm, on traditional long-haulenergy in rastructure assets.

Te core thesis that SteelPath was ounded on in and maintains today is that MLPs are on a trajectory verysimilar to that experienced by the Real Estate Investment

rusts (REI s) in the late s. On average, in a normal-ized market environment, the rm expects - initialpublic o erings each year or the oreseeable uture. High-returning organic investment projects and acquisitions

will continue to create tremendous value and demand oradditional capital in ows. Te Jobs Creation Act con-tained a codicil that largely ailed in its attempt to broadenmutual und investment in MLPs. Although private “hedge”

und participation has increased, reaching a short-termpeak in , we do not expect to see a wholesale increasein institutional (mutual und, tax-exempt) participation inthe asset class as structural barriers to entry that e ective-ly preclude widespread mutual und ownership are unlikelyto be removed without a legislative rewrite. Until this eventoccurs, the space will likely remain ine cient with a high

dispersion o returns. However, liquidity and market capi-

talizations have reached the point where MLPs could com-prise a meaning ul portion o a large institutions port olio. As the sector continues to provide superior distributionyield and growth versus other yielding equities, moderategrowth in institutional participation will likely continue.Legislative progress and meaning ul mutual und and insti-tutional adaptation will likely take some time. When such aradical shi t in institutional participation occurs we expectthe sector to experience a substantial revaluation. However,in the meantime, we believe the sector simply o ers a veryattractive risk/return pro le.

In this uncertain environment, the undamentals are genu-inely in place or MLPs to generate attractive risk-adjustedreturns, without a broader market recovery. Combining anapproximate % group-average yield with consistent dis-tribution growth, we continue to expect low-to-mid-teensannualized total returns or the sector over the next veyears.

Why own MasterLimited Partnerships?Over the past years, midstream MLPs have outper-

ormed the S&P with a cumulative gain o over %,equal to a compound annual return o . %, versus %

or the broader market, equal to a compound annual returno . %. Many investors look at the historical returns wist-

ully believing they have missed out and that it must be toolate. Or, they look at the decline in MLP prices andwonder i the story really remains the same. Te unda-mental and structural underpinnings that led to decades o outper ormance remain solidly in place. Valuation remainsstructurally inexpensive relative to other yield-orientedequity classes. Demand or investment in new energy in-

rastructure has never been greater. Te structural encum-brances that restrict wholesale institutional investmentand create exploitable ine ciencies in the market are stillin place. Tis asset class is still in its in ancy and the oppor-tunity or superior returns over the next decade still exists.

Tere has only been one period in which MLP per ormancesigni cantly lagged the S&P . Tis occurred duringthe tech boom o - , when investors became excitedabout growth and were willing to pay extraordinary mul-tiples or high-growth companies.

SteelPath Fund AdvisorsMaster Limited Partnership Primer

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 5/31

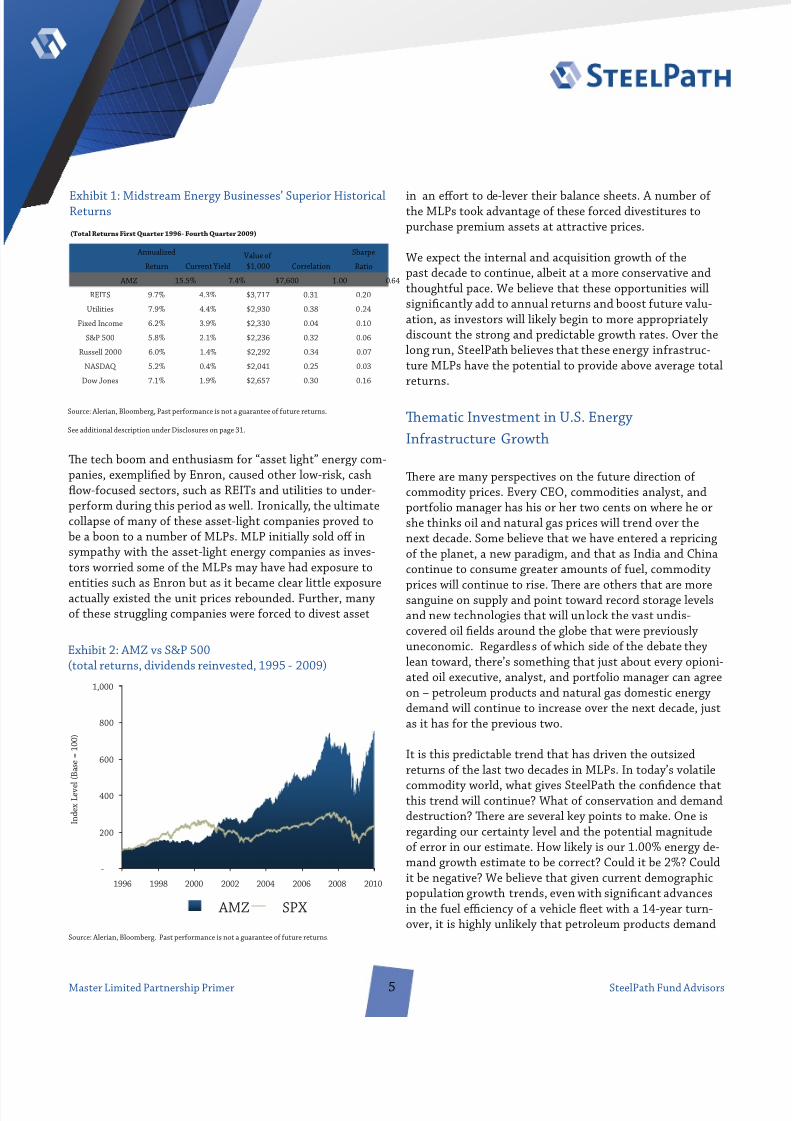

Te tech boom and enthusiasm or “asset light” energy com-panies, exempli ed by Enron, caused other low-risk, cash

ow- ocused sectors, such as REI s and utilities to under-per orm during this period as well. Ironically, the ultimatecollapse o many o these asset-light companies proved tobe a boon to a number o MLPs. MLP initially sold o insympathy with the asset-light energy companies as inves-tors worried some o the MLPs may have had exposure to

entities such as Enron but as it became clear little exposureactually existed the unit prices rebounded. Further, manyo these struggling companies were orced to divest asset

in an e ort to de-lever their balance sheets. A number o the MLPs took advantage o these orced divestitures topurchase premium assets at attractive prices.

We expect the internal and acquisition growth o thepast decade to continue, albeit at a more conservative andthought ul pace. We believe that these opportunities willsigni cantly add to annual returns and boost uture valu-ation, as investors will likely begin to more appropriatelydiscount the strong and predictable growth rates. Over thelong run, SteelPath believes that these energy in rastruc-ture MLPs have the potential to provide above average totalreturns.

Tematic Investment in U.S. EnergyIn rastructure Growth

Tere are many perspectives on the uture direction o commodity prices. Every CEO, commodities analyst, andport olio manager has his or her two cents on where he orshe thinks oil and natural gas prices will trend over thenext decade. Some believe that we have entered a repricingo the planet, a new paradigm, and that as India and Chinacontinue to consume greater amounts o uel, commodity

prices will continue to rise. Tere are others that are moresanguine on supply and point toward record storage levelsand new technologies that will unlock the vast undis-covered oil elds around the globe that were previouslyuneconomic. Regardless o which side o the debate theylean toward, there’s something that just about every opioni-ated oil executive, analyst, and port olio manager can agreeon – petroleum products and natural gas domestic energydemand will continue to increase over the next decade, justas it has or the previous two.

It is this predictable trend that has driven the outsizedreturns o the last two decades in MLPs. In today’s volatile

commodity world, what gives SteelPath the con dence thatthis trend will continue? What o conservation and demanddestruction? Tere are several key points to make. One isregarding our certainty level and the potential magnitudeo error in our estimate. How likely is our . % energy de-mand growth estimate to be correct? Could it be %? Couldit be negative? We believe that given current demographicpopulation growth trends, even with signi cant advancesin the uel e ciency o a vehicle eet with a -year turn-over, it is highly unlikely that petroleum products demand

SteelPath Fund AdvisorsMaster Limited Partnership Primer

-

200

400

600

800

1,000

1996 1998 2000 2002 2004 2006 2008 2010

I n d

e x

L e v e

l ( B

a s e =

1 0 0

)

AMZ SPX

Exhibit : AMZ vs S&P (total returns, dividends reinvested, - )

Source: Alerian, Bloomberg. Past per ormance is not a guarantee o uture returns.

Exhibit : Midstream Energy Businesses’ Superior HistoricalReturns

Annualized Sharpe

Return Ratio

AMZ 15.5% 7.4% $7,600 1.00 0.64

REITS 9.7% 4.3% $3,717 0.31 0.20

Utilities 7.9% 4.4% $2,930 0.38 0.24

Fixed Income 6.2% 3.9% $2,330 0.04 0.10

S&P 500 5.8% 2.1% $2,236 0.32 0.06

Russell 2000 6.0% 1.4% $2,292 0.34 0.07

NASDAQ 5.2% 0.4% $2,041 0.25 0.03

Dow Jones 7.1% 1.9% $2,657 0.30 0.16

(Total Returns First Quarter 1996- Fourth Quarter 2009)

Current Yield Value of $1,000 Correlation

Source: Alerian, Bloomberg, Past per ormance is not a guarantee o uture returns.

See additional description under Disclosures on page .

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 6/31

would not remain at least at with today, ve years, ten

years, or twenty years hence. Negative growth is certainlypossible or a period, perhaps or a ew quarters or years,but over the longer term, as the US population continuesto grow, spreads south and west, and the suburban sprawlcontinues to increase the number o drivers traveling longerdistances to reach their places o work, the rm believesthere is a very strong oor under today’s demand levels.We believe that as population growth and immigrationcontinue, overall demand will continue to grow, even i percapita growth is more muted. It is this creeping growth andthe shi ting o North America’s traditional supply sourcesthat necessitates new investment in energy in rastructure.Investors have not missed the boat on MLP per ormance

because the undamental macro actors that have driventhe asset class remain unchanged.

Te sources o North America’s energy commodities is on

the move. Natural gas is no longer primarily developed bywildcatters in exas. Te Rockies, new shale plays acrossthe country, and LNG hold our natural gas uture. Approxi-mately % o our petroleum products are oreign sourced;international gasoline arbitrage, Canadian oil sands andcoal-lique action technology now hold our petroleumproducts’ uture. As transportation dynamics change andthese trends continue to play out over the next decade,hundreds o billions o dollars o green eld investment willbe required. MLPs have been and will continue to be at the

ore ront o this value creation, and the need or invest-ment in US energy in rastructure has never been greater.

MLPs are typically toll-road business models. Tey ( ) re-

ceive a speci ed tari or hauling a product over a certain

distance; ( ) do not take title to the commodity; ( ) do nothave balance sheet exposure; ( ) are largely agnostic tothe level o commodity prices because these prices do notenter the revenue equation; and ( ) do not have signi cantcredit risk as commodity prices balloon. As the energy and

investment communities continue to argue over whether oilwill trade at $ per barrel or $ per barrel in , themore certain bet is on the growth trajectory o US energydemand and the high-return capital spending projects thatwill have to take place to support it.

Hard Asset Play Provides angible Value in a Po-tentially In ationary Environment

Modern pipelines bene t rom rust coatings and cathodicprotection that will allow these pipelines to operate with-out major maintenance or years or more. In act, thereare pipelines that were put in the ground prior to WorldWar II which had no rust coating o any kind that are still inuse today. Potentially, a ter we have exhausted this planet’ssupply o gaseous and liquid hydrocarbon energy resources,these conduits could be converted to alternative uels such

as hydrogen and ethanol. For the intervening generations,however, we believe these pipeline and other midstreamassets will provide real, long-term, and growing cash

ows. Further, many o the interstate petroleum pipelineshave annual rate adjustments that are equal to the PPI

or nished goods plus . %, which provides a direct andtimely cash ow adjustment to changes in the in ationaryenvironment.

SteelPath Fund AdvisorsMaster Limited Partnership Primer

0

5

10

15

20

25

1985 1990 1995 2000 2005 2010E 2015E 2020E

m i l l i o n s o f

b a r r e l s p e r

d a y

0.7% CAGR 1985 through 2020

Exhibit : Petroleum Products Consumption rend

Source: Energy In ormation Administration, SteelPath estimates

-

5.0

10.0

15.0

20.0

25.0

30.0

1985 1990 1995 2000 2005 2010E 2015E 2020

m i l l i o n

c u b i c

f e e t

0.9% CAGR 1985 through 2020

Exhibit : U.S. Natural Gas Consumption rend

Source: Energy In ormation Administration , SteelPath estimates

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 7/31

Better Business Models

MLPs generated . % annualized returns over the pastteen years, not because o any one-time event or change

in relative valuation, but by consistently growing theircash distributions over that period by - % per annum.Teir ability to continue to do this rests with their uniqueand superior business models. Midstream assets are typi-cally entrenched regional ranchises that in turn supportconsistent growth. Tese dominant and, in some instances,monopoly ranchises possess innate competitive advan-tages aided by regulation. Most MLP pipeline assets aregoverned by a ederal agency that protects their rights o way and provides or attractive rates o return to investors.Initial tari s are generally predicated on a cost basis andthen indexed to a measure o in ation, providing a built-inin ation hedge. Volumes have historically been and shouldcontinue to be highly predictable over the long run as theyare a unction o population growth and demographictrends.

MLPs have historically o ered more predictable earningsthan the broader market, in act, the S&P earningsvolatility is more than three times that o the MLPs that wecover. MLPs own assets with use ul lives o - years orlonger that provide consistent cash ows without the need

or substantial maintenance capital expenditures. Con-sistency is aided by airly inelastic demand as residentialand commercial consumers heat and cool their homes andbusinesses, and commuters drive to work even in the worsto times. Industrial customers can only take advantage o

uel-switching alternatives and capabilities to a certain ex-tent, and product throughput has risen over the past decadedespite the allout rom September th and the ensuing

, and indeed, the current recession. High barriers toentry exist because initial capital costs are prohibitive andthe ability to create new rights o way is very limited.

In summary, we expect midstream MLPs to generate supe-

rior risk-adjusted returns o to % or years to come,driven by the ollowing actors embedded in their businessmodel that have generated their returns in the past:

• op-line growth driven by energy demand growth andPPI indexed transportation tari s

• Mid-single digit cash ow growth as these xed-costbusiness models allow much o this predictable revenuegrowth to reach the bottom line

• Attractive organic investment opportunities resultingrom their ranchise-protected ootprint, generating

additional and o ten near-term accretion to the distri-

bution• Opportunities or additional asset acquisitions driven

by the macro trends described in detail below, creatingadditional immediate accretion to the distribution.

Importantly, these are the same actors that have allowedthese businesses to per orm well in the past and nothinghas changed in the macro environment that would suggestthat these same actors will not drive returns in the uture.

MLPs Exhibit Insigni cant Correlation with theBroader Equities Market

Te majority o equity asset classes and sectors tend to bestrongly positively correlated with the broader market.MLP returns have exhibited statistically insigni cantcorrelation with the market over nearly two decades. Tismakes undamental sense given that the demand or pe-troleum products and natural gas is highly inelastic in thenear term and is largely una ected by the vicissitudes o the economy.

For example, during , one o the sharpest recessions inUS history, petroleum products consumption remained at.In the current recession, as petroleum products prices have

stabilized, we have seen a similar inelasticity o demand.Swings in economic indicators and interest rates, which canroil the broader markets because they can both signi cantlyand rapidly a ect corporate America’s cash ows, do notmaterially impact the demographic trends underpinningthe long-term cash ow trajectory o MLPs.

Without physical product shortages, such as those experi-enced in the s, there will be very little consumptionimpact even over a period o years during times o highlyelevated prices. Tere ore, regardless o the direction o per ormance o the broader equity markets and the cyclicalstate o the economy, MLP cash ows should remain consis-

tent and ultimately provide or strong equity per ormancethat is relatively independent o these broader indicators.By adding an MLP allocation to a port olio, risk is signi -cantly reduced even as MLPs increase port olio returns.

SteelPath Fund AdvisorsMaster Limited Partnership Primer

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 8/31

An Emerging Asset Class

MLPs in their current orm were created by Congress in. Structured as partnerships, all income, losses, gains,

and deductions are passed on to limited partners andare only taxed at that level (i.e. no entity-level taxation),meaning that investors in MLPs avoid the double taxationo investing in corporations. Congress created this struc-ture to encourage investment in US natural resources andenergy in rastructure. Since then, as the MLP structure hasgained more widespread adoption, there has been a gradualyet quickly accelerating transition o MLP-quali ying assets

rom corporations to MLPs given the e ective tax arbitrage

o holding these assets in the partnership structure andthe value that highly specialized management teams canprovide.

Energy in rastructure assets held by oil majors, re ners,and utilities are o ten underutilized because they are notrun or pro t. In some cases, direct competitors would pre-

er not to risk divulging competitive in ormation. Exxon’sinvestors measure the company’s per ormance on explor-atory success, production growth, reserve replacement,and other ratios that do not reward the company’s stockprice or maintaining pipeline assets. Te potential pipelineearnings o such companies are dwar ed by their explora-

tion and production (E&P) cash ows. Consequently, largerenergy companies continue to ignore their midstreamassets and many remain undermanaged and underutilized.MLPs that hold these assets have the incentive, expertiseand reedom to maximize use and pro tability.

Corporations with MLP-quali y ing assets will o ten createMLPs in which they retain general partner (GP) ownershipinterests thus allowing these assets to be dropped downinto a more tax-e cient structure where stable cash owswill be ar more highly valued outside o the volatility o theparent company’s earnings stream. It makes little sense orhighly cyclical, low-P/E energy corporations to hold thesehigh-multiple assets on their balance sheets. E&P com-panies in particular are motivated to sell these businessesgiven the premium that is placed by their investors on mak-ing commodity price-sensitive investments that involveboth greater risk and greater potential reward.

We estimate that there are $ billion o such assets cur-rently held in structures subject to entity-level taxation,much o which should ultimately be rationalized into theMLP structure. Additionally, there are many groups o as-sets – including re neries, oil/gas wells, coal gasi cation,and LNG degasi cation acilities – that have begun to be in-cluded in this structure, potentially adding tens o billionso dollars to sector growth.

In , $ . billion o equity and $ billion o debt wasissued as companies aggressively nanced growth projectsand investments. Tis was on the heels o the previous

year’s $ billion record equity issuance. In , more than$ billion o equity issuance was spurred by initialpublic o erings. In , equity issuance reached $ bil-lion. Tough the rate o equity issuance abated somewhatin and due to the disruptions in the broadereconomy and capital markets, MLPs were still able to raisenearly $ billion in equity and an impressive $ billionin debt. Te ability o the MLPs to access capital over thisperiod is a testament to the stability o their underlyingbusinesses and the value that investors place on their stableand growing distributions. We believe MLP capital marketsactivity will only accelerate in . Te sector is in themidst o executing large scale pipeline and storage green-

eld projects and larger corporations will be increasinglyincentivized to divest their midstream port olios.

Since MLPs pay out a substantial portion o their cashows, they have to return to the equity capital markets tonance growth projects and acquisitions. Tis has instilled

a tremendous capital discipline in the sector. Unlike othersectors o the economy where a CEO can plough hundredso millions o dollars into a pet project or sel -servinginitiative, MLP management teams must have the vote o

SteelPath Fund AdvisorsMaster Limited Partnership Primer

Exhibit : MLP Market Capitalization

Source: SEC, SteelPath estimates

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

1995 2000 2005 2010E

( b i l l i o n

s )

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 9/31

con dence rom the public markets be ore they proceed.Further, due to the sectors ocus on distributions and cash

ows per unit, projects or acquisitions that are cash owdilutive or only minimally accretive are quickly exposed.Tere is no incentive or management teams to pursuequestionable transactions to simply boost GAAP earnings.

We believe that this is the reason cash returns on cashinvested in the MLP sector have dwar ed those o its energypeers including E&P, re ning, gas utilities, and electricutilities over the past two decades. Te typical investmentpursued by a midstream MLP will provide a - % IRR,carry relatively low risk and will provide substantial cash

ow accretion to unitholders.

Substantial Investment Required to Meet U.S.In rastructure Demands

We expect more than $ billion in natural gas in rastruc-ture investment over the next decade as production romnewer unconventional plays outpaces traditional sourceso US supply. We expect substantial investment in crudeand petroleum products in rastructure as demand contin-ues its relentless and steady pace and to accommodate oilsands production. Further in rastructure will be requiredas coal-lique action and gas-to-liquids technologies cometo widespread commercial ruition. Te opportunity set orhigh-returning, stable cash- ow generating energy in ra-structure investments continues to grow.

In an October letter to the Federal Energy RegulatoryCommission (FERC), the Department o ransportation(DO ), which oversees not only the traditional networko highways and waterways, but also pipelines, expressedconcern about the capacity o underlying petroleum prod-ucts pipelines to meet the growing demands placed on it.Te letter urged the FERC to seriously consider the neces-sary nancial commitments or operators to maintain andexpand pipeline system capacity. It also suggested thatthe FERC convene a workshop or technical con erence inorder to explore regulatory mechanisms that could exhortthis critical investment. MLPs have become an increasingportion o such expansion projects and we expect organicgrowth capital investment to continue to increase over thenext decade.

Te Future o MLPs

We have been speaking to this theme since the spring o ; the types o midstream logistics assets in the MLP

asset class is only going to continue to expand. We believethat in addition to the $ billion-plus stable o mid-stream assets currently housed in public corporate struc-tures and $ billion o “traditional” midstream newbuildnecessary to expand and maintain the United States’ en-

ergy in rastructure over the next decade, alternative energysources such as LNG, coal gasi cation, and gas-to-liquidstechnology, are very real and present hundreds o billionso dollars more in xed cost, hard asset, long-term contractenergy logistics assets

In act, Cheniere Energy (NYSE: LNG) completed an initialpublic o ering o subsidiary Cheniere Energy Partners(NYSE: CQP) on March , , orming an MLP that willown the corporate parent’s LNG regasi cation terminal.In , Calumet Specialty Products Partners (NASDAQ:CLM ), a re ner o uels and specialty products completedits initial public o ering. Also in , Exterran Partners

(NASDAQ: EXLP), an owner and operator o natural gascompression assets, completed its initial public o ering.Each o these o erings introduced new business types tothe MLP space and we expect to continue to see such newentrants. In addition, the legislation de ning allowedactivities or the structure was expanded in to includeindustrial sourced carbon dioxide as a natural resource. Also in , the transportation and storage o ethanol,biodiesel, and other alternative uels was added as an allow-able activity.

SteelPath Fund AdvisorsMaster Limited Partnership Primer

Exhibit : Number o Publicly raded MLPs

Source: SEC, SteelPath estimates

0

10

20

30

40

50

60

70

80

1995 2000 2005 2010E

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 10/31

Structural Valuation Issues Create SubstantialLong- erm Upside

We believe the lack o institutional participation in the as-set class has resulted in a structural under pricing o MLPsrelative to other asset classes. Institutional participationis limited due to some signi cant barriers to entry, includ-ing restrictions on mutual und ownership and UnrelatedBusiness axable Income (UB I) generation or tax-exemptinstitutions. UB I creates Unrelated Business Income ax(UBI ). Under the UBI rules, tax-exempt institutions andretirement accounts must pay tax on income rom a busi-

ness that is not related to their exempt purpose. Becauseo the pass-through nature o an MLP, or any partnership,unit holders are treated by the tax code as i they are di-rectly earning the MLP’s income. Tere ore, the tax is owedon the retirement account’s share o the MLP’s taxablebusiness income as reported on the K- . Tough there is adeduction that covers the rst $ , o unrelated businessincome rom all sources; a ter that, the retirement accountwill owe tax.

Te current growth trajectory o MLPs appears to stronglyresemble that o REI s during the s. Similar to MLPs,REI s were created as a tax-advantaged structure to en-

courage investment in that particular sector. We stronglybelieve there is a similar parallel between the emergence o REI s as a distinct asset class and the growth that we haveseen – and expect to continue to see – in MLPs. In ,there were approximately equity REI s with a combinedmarket capitalization o $ billion. oday, there are ap-proximately equity REI s representing $ billionin market capitalization (excluding hybrid and mortgageREI s). MLPs, while still in the early stages o development,have started to emerge.

During the rst years o their existence a ter Congresscreated the structure in , REI s traded at an average

basis-point premium to the -year reasury. Follow-ing the REI IPO boom o the late s and early sand the migration o institutional real estate allocationdollars rom the private to public markets, REI s havetraded on average at par with the -year reasury as inves-tors have been willing to trade o the business risk or thein ationary growth component o REI rents.

Since the creation o the modern MLP structure in ,MLPs have traded at an average basis point spread to

the -year reasury. Given the substantially similar asset

risk pro les o REI S and MLPs (we would argue MLPs havea substantially lower business risk pro le given their lowercash ow volatility, high degree o nancial transparencygiven real time ederal reporting requirements, and a con-structive ederal regulatory scheme), there is no compellingreason or this spread to exist. We believe the disparity hasbeen a unction o the restrictions that have been placed oninstitutional ownership o MLPs, and that as more sophis-ticated investors enter the space, this disparity will disap-pear. In the mean time, we believe this mispricing creates avery attractive relative risk/reward value proposition.

Flying Under the Radar – Limited InstitutionalOwnership o MLPs

Given the attractive historical per ormance track recordin the MLP sector, many investors wonder: How is it thatthere is so little institutional participation? What am Imissing? Isn’t this too good to be true i it hasn’t caught on?

o begin with, hindsight is always / . “Well o courseREI s make sense!” (Not a phrase that was said very o tenin the mid- s when there were publicly traded ve-hicles with an unimpressive $ billion o market capital-ization.) Now considered a staple o every institutional or

individual investor’s well-diversi ed port olio, REI s werenot on the institutional radar screen until the early s.REI s were created in , but it took some time be orethey were accepted.

In this case, however, there are very particular structuralreasons why MLPs have not become more popular with theinstitutional investor set. MLP distributions and income al-locations have historically been considered non-quali yingsources o income, which impedes regulated investmentcompanies (RICs) such as mutual unds rom investing. I Fidelity and Putnam cannot invest, then Goldman Sachs orMorgan Stanley can not earn a commission and, there ore,

there is no incentive or one o their salespeople to educateor pitch the investor on the asset class. In other words, WallStreet has never championed MLPs as an attractive invest-ment to their institutional customers because many o these customers were restricted rom purchasing. For thissame reason, the universe o expert analysts and port oliomanagers who understand the many nuances o the MLPspace is also limited. Tis product has always been solddirectly to retail through the private wealth managemento ces o the bulge-bracket investment banking rms.

SteelPath Fund AdvisorsMaster Limited Partnership Primer

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 11/31

Pursuant to Section o the American Jobs Creation Acto , MLP distributions and income allocations are nowconsidered quali ying sources as it relates to the special taxstatus o RICs. However, at least % o a RIC’s assets mustbe invested in investment vehicles that are not MLPs, and aRIC may not own more than % o any single MLP. Mutual

unds, and not their investors, will continue to receive

K- s, and will be required to le tax returns in the states inwhich the MLP operates.

As well meaning in spirit as the Jobs Act was, there arestill substantial practical hurdles to ull-scale mutual undinvestment in MLPs. First, the timing discrepancy betweenthe calculation o the RICs distributions and their s(typically November through January) and the issuance o K- s by MLPs (March) creates an administrative burden orRICs, which are orced to estimate their investors’ share o MLP income, losses, credits, and deductions without su -

cient in ormation. A mistake could result in substantialexcise taxes to the mutual und as well as a misstatement

o the s. When the K- s are ultimately issued, the undcould then be orced to adjust its s to account or thechanges. Because a restatement is such a rare event

or a mutual und, they are wary o taking on such a risk. Another administrative burden relates to state ling re-quirements. With some MLPs operating in multiple states,the mutual und itsel may consequently have to le taxreturns in each o those states. Furthermore, not all states(e.g. Massachusetts) recognize ederal statutes concern-ing quali y ing income, urther complicating the problem.

Retirement accounts and other tax-exempt investmentvehicles are also restricted in their ability to invest in thesector because MLPs generate UB I. I UB I exceeds $ ,

or a tax-exempt entity, investors may be liable to pay taxeson that income.

Another concern in the institutional investing communityis that the sector does not possess su cient liquidity orinvestment. However, this continues to improve. Te me-dian market capitalization in the space is now greater than$ . billion. Nonetheless, compared to gas utilities, whichattract substantial institutional attention, MLPs have vir-tually zero mutual und ownership. For example, Washing-ton Gas and Light (NYSE: WGL), a $ . billion gas utility,counts Barclays, American Century, Vanguard, and StateStreet among others in its top holders list. None o thesenames are present in the MLP space, which has companieswith signi cantly larger market capitalization and greatereconomic importance. Because institutional investors are

amiliar with gas utilities’ historical correlations, earningstrends, price behavior, and they are eligible or inclusion inmutual und and tax-exempt port olios, these institutionscontinue to devote substantial resources and capital invest-ment toward the gas utility sector while generally ignoringMLPs. However, as trading liquidity continues to increaseand distribution levels and growth continue to outpace

other dividend equities, we believe that institutional inter-est will continue to grow.

Te Emergence o Pure-Play Publicly raded GPs

MLPs are governed by their GPs, which are in turn alsosubject to Sarbanes-Oxley with respect to director indepen-dence. Some GPs are comprised o members o the execu-tive management team, some are nationally recognizedprivate equity groups, and still others are multinationalenergy companies. For many years, there have been publiclytraded GPs, and these have typically been corporationswhose cash ows were substantially derived rom otherenergy assets. Recently, there has been a trend toward thepure-play public GP entity and most utilize the MLP struc-ture themselves.

A ull explanation o the GP is provided in the “General/Limited Partner Structure” section below but in short thesestructures provide investors a leveraged play on the MLP’sgrowth. Trough the incentive distribution rights (IDRs)held by the GP, the GP receives an increasing share o totalcash distributed by the MLP as the distribution rate per

SteelPath Fund AdvisorsMaster Limited Partnership Primer

Exhibit : MLP Median Daily Dollar rading Volume

Source: Bloomberg, Alerian

0

100

200

300

400

500

600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

d o l l a r

t r a d i n g v o l u m e

( $ m

i l l i o n s )

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 12/31

unit is increased. For example, i the MLP were to make

an accretive acquisition and subsequently increased itsdistribution, the GP might receive an outsized portion o the total cash distributions associated with that distribu-tion increase. Further, i the MLP issued new units to undthe acquisition then total cash distributed would haveincreased even without a distribution rate increase due tothe additional units outstanding. Tere ore, the GP’s cashallocation would increase with the increase in total cashdistributed even though its share o that total would haveremained stagnate.

Although there is tremendous potential or distributiongrowth at the GP level due to the structure o the IDRs,that mechanism works similarly against GPs in scenarioswhere the distribution level at the LP must be reduced. O note, the IDR structure provides that i a certain minimumdistribution rate at the MLP is not achieved, then the GPreceives no cash through the IDRs. We believe this riskis o ten underappreciated by the investment communitywhich continues to accord GPs a %- % cost o equitycapital. With such a high degree o innate leverage, webelieve that GPs inherently demand a higher required rateo return. Te impacts o structural and nancial leverageand trading liquidity demand adjustments to the CAPMor any other model used to determine the cost o capital.Fundamentally, i the cost o equity capital or the underly-ing MLP were in the % to % range, the cost o capital

or the GP should be greater – substantially greater. We es-timate the appropriate required return somewhere between

- %. Under these cost o capital assumptions, a numbero the publicly traded GPs are overvalued today in all butthe most aggressive growth scenarios.

Tere is a belie that i an investor likes the LP, they mustlove the GP. We caution investors that the GP structurecarries signi cant risk and that risk must be appropriatelyweighed. In act, investors looking or leveraged exposureto a certain MLP’s cash ows might consider doing just that

by borrowing with debt and leveraging their position. Insome cases this could provide a better risk-adjusted returnthan purchasing the general partners at today’s valuations.

Te Alerian MLP Index SeriesTe Alerian MLP Index (NYSE: AMZ) measures the compos-ite per ormance o the most prominent energy masterlimited partnerships, and is calculated by real time using a

oat-adjusted, capitalization-weighted methodology. Tisindex is the industry standard benchmark or the energyMaster Limited Partnership asset class used by the compa-nies themselves in their internal corporate nance compar-isons and outside investor presentations, and by the equityresearch analyst community to track the per ormance o the asset class. Te corresponding total return index iscalculated on an end-o -day basis and will be disseminated

daily through its ticker symbol, “AMZX”.Te objective o the Alerian MLP Index is to provide inves-tors with an unbiased, comprehensive benchmark or theper ormance o the energy master limited partnershipuniverse. Using Standard & Poor’s proprietary calculationmethodology, the Alerian MLP Index was created to ll theneed or a reliable, transparent index to track this emergingasset class.

Te Alerian MLP In rastructure Index provides an en-hanced liquid subset o the Alerian MLP Index that includesonly midstream energy transportation and storage assets,

and selects those companies that are in rastructure hard-asset ocused. Te index provides greater diversi cationand speci c exposure to in rastructure investment.

New index constituents will be subject to the ollowingconditions:

. Market capitalization. Each constituent security musthave a market capitalization o at least $ million.Tis minimum requirement is reviewed rom time totime to ensure consistency with market conditions.

. Adequate trading liquidity. Each constituent securitymust maintain a ratio o annual dollar value tradedto market capitalization o . or greater. radingvolume o each component security is required to havebeen in excess o , units per month or each o the last six months.

. Public oat. Each constituent security must have apublic oat o at least % o the total outstandingunits.

. Financial viability. Each constituent security mustmaintain trailing months distributable cash owthat exceeds cash distributions paid to unitholders

SteelPath Fund AdvisorsMaster Limited Partnership Primer

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 13/31

Constituents o the Alerian MLP Index are oat-adjusted tore ect the number o units available to investors accordingto real time proprietary methodology. Te oat-adjustednumber o units or each stock is determined by assigningeach stock an availability actor. Tat actor represents thepercentage o units deemed available (i.e., tradable) on theopen market, and is developed by excluding certain types o holdings including: corporate cross-holdings, private con-trol block holdings, or government holdings. Subordinatedlimited partner units and any other holdings not readilyavailable to the public or investment are also excluded.

For a complete description o the Alerian MLP Indices visitthe Aler ian web site at http://alerian.com/.

What is a Midstream Asset?

raditional MLP operations can be broadly grouped intoour categories – pipelines, terminals/storage, marine

transportation and midstream services. Tese categoriescan urther be subdivided by product types, including am-monia, bulk products, carbon dioxide, coal, crude oil, heat-ing oil, re ned petroleum products, natural gas and naturalgas liquids, and propane.

Crude Oil/Re ned Products ransportation

Crude oil and re ned petroleum products are transported

by pipelines, marine transportation, railroads and trucks.Pipelines are the most e cient mode o transportation orlong-haul movement (accounting or roughly % o trans-portation), ollowed by tankers/barges (approximately %o transportation). Rail and truck usage is cost-e ectiveonly over short distances and, there ore, accounts or only asmall percentage o petroleum transportation.

Te US crude oil and petroleum products transportationsystem links oil wel ls and import terminals to re neries,which in turn are linked to end users o petroleum prod-ucts. Tis system is comprised o networks o pipelines,terminals, storage acilities, tankers, barges, rail cars,

and trucks. Generally speaking, pipelines are the lowest-cost alternative or transportation across long distances.Troughout the distribution system, terminals exist toprovide storage, distribution, blending, and other ancil-lary serv ices. Crude oil that is pumped to the sur ace romreservoir deposits is collected on gathering pipelines andbrought to longer-haul trunk pipelines to be transported tore neries, which then separate the eedstock into products.Product then originates on pipeline systems rom directconnections with re neries and interconnections withother interstate pipelines or transportation and ultimatedistribution.

Petroleum products transported, stored, and distributedthrough petroleum products pipelines and terminals in-clude:

• re ned petroleum products, which are the output romre neries and are primarily used as uels by consumers(gasoline, diesel, jet uel, kerosene, and heating oil)

• lique ed petroleum gases (LPGs), which are producedas byproducts o crude oil re ning and as part o natu-ral gas production (these include butane and propane)

SteelPath Fund AdvisorsMaster Limited Partnership Primer

Exhibit : Petroleum Products Content and Consumption( )

Source: Energy In ormation Administration

Industrial24%

Residential6%

Electric Power2%

Transport68%

Jet Fuel8%

Other22%

DistillateFuel20%

LiquefiedPetroleum

Gases9%

ResidualFuel3%

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 14/31

• blendstocks, which are blended with petroleum prod-ucts to enhance various speci cations, such as raising agasoline’s octane or oxygen content

• heavy oils and eedstock or urther processing byre neries and petrochemical acilities

• crude oil and condensate, which are used as eedstockby re neries

Fungible products shipped on such systems are typicallygeneric products. Tese products meet published standardspeci cations; shippers will receive equivalent product butmay not get back the actual product shipped. Segregatedproducts are branded products or speci c blendstock ma-terials. On segregated shipments, shippers will receive thesame product that they had injected into the system.

With pipeline transportation, crude oil and re ned petro-leum products travel at roughly three to ve miles per hourin long-haul trunkline pipelines. Te greater the volumebeing transported on a given day, the aster the productgenerally moves. It can take anywhere rom two to threeweeks or a batch o petroleum products to move rom are nery tailgate in Houston, exas, to the New York harbor.

Interstate pipelines carry crude oil and re ned productsacross state boundaries and are subject to FERC regulation

on the rates charged or their services, on the terms andconditions o the services they o er, and on the location,construction, and abandonment o their acilities. Intra-state pipelines transport within a particular state and arenot subject to regulation by the FERC, but rather individualstate agencies responsible or such oversight.

Petroleum pipelines bene t rom a benign overarchingederal regulatory ramework, which provides management

teams with a strong incentive to innovate and cut costs.Unlike traditional cost-o -service, authorized rate-o -return utility rate-making, petroleum products pipelines donot have to share cost improvements with their customers.

A ter an initial rate is set, as per the CongressionalEnergy Policy Act, the tari rate structure on the pipeline isincreased by the PPI or Finished Goods plus a . % marginevery July st.

ransportation tari s vary depending on where the prod-uct originates, where ultimate delivery occurs, and anyapplicable discounts. All interstate transportation ratesand discounts are in published tari s led with the FERC.

ari s are designed to ensure appropriate rates o return

or pipeline owners, with annual tari increases o PPI +. % unctioning as an embedded cost recovery mechanism

– thus providing a built-in in ation hedge or partnershipsthat own crude oil and re ned product interstate pipelines.Published tari s serve as contracts, and shippers nominatethe volume to be shipped up to a month in advance. Inaddition, supplemental agreements are entered into withshippers that typically result in volume and/or term com-mitments by shippers in exchange or reduced tari rates.Tese agreements have terms o one to years. Productservices such as ethanol loading, additive injection, andcustom blending are per ormed as needed under monthlyor long-term agreements. Pipeline operators generally donot take title to the product they are shipping, leaving littledirect commodity exposure (inelastic demand characteris-tics or re ned petroleum products urther supports this).Competition with other pipeline systems is based mainlyon transportation charges, quality o customer service,proximity to end users, and history o individual customerrelationships. However, given the di erent supply sourceson each pipeline, pricing at either the origin or terminalpoint on a pipeline may outweigh transportation costswhen customers choose which line to use.

Marine ransportation

Although pipelines are a key component in the distributionchain, they do not reach all markets and are not capableo transporting all re ned petroleum products or eco-nomically transporting most chemical products. Marinetransportation – primarily conducted by tankers and tugbarges – lls this gap. ankers and barges transport re nedpetroleum products rom re neries to terminals and acili-ties engaged in urther processing. Customer contractsgenerally have initial terms o one to three years. Similar topipeline transportation, marine transportation providersdo not assume ownership o any o the products that aretransported on their vessels.

Te US ag coastwise marine transportation industry isguided by the Merchant Marine Act o (commonlyre erred to as the Jones Act), a set o ederal statutes thatmandates that vessels engaged in trade between US portsmust operate under the US ag, be built in the US, beat least % owned and operated by US citizens, and besta ed by a US crew. One o the principle reasons or theJones Act is to maintain a eet o vessels available or char-ter to the US government to meet national de ense needs,but it also serves to insulate the market rom direct oreign

SteelPath Fund AdvisorsMaster Limited Partnership Primer

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 15/31

competition.

In , we saw the rst Jones Act marine transportationIPOs in the MLP sector: K-Sea ransportation Partners LPand US Shipping Partners LP. Te coastwise vessel eet ishighly ragmented and predominantly amily owned. Webelieve there will be additional IPOs and substantial op-portunity or consolidation in the sector as capital require-ments rise due to increasingly stringent environmentalrequirements. In many cases, we view these vessels as oat-ing pipelines; these ships o ten carry products that cannotbe carried in a competing pipeline, or they service areasthat are not currently serviced by pipelines and are unlikelyto be so in the uture.

Te domestic supply o vessels is decreasing due to theJones Act and the Oil Pollution Act o (OPA ), whichmandates the phase-out o certain non-double-hulledvessels by a series o deadlines through . Given theexpected decline in available vessels due to these require-ments, oil and chemical companies are increasingly in-terested in entering into long-term charter agreementsin order to ensure shipping capacity or their products.Further, major oil and chemical companies have becomeprogressively more selective in their choice o tanker andbarge operators. Tese companies place particular emphasis

on strong environmental and sa ety records as well as op-erating per ormance. Tis pre erence will likely acceleratethe scrapping o older, lower-quality vessels. Additionally,these companies continue to concentrate more on their coreoperations by divesting vessels and securing third-partytransportation.

Crude Oil/Re ned Products erminals

erminals are large storage and distribution acilities thathandle crude oil and re ned petroleum products. ermi-nals are typically located in close proximity to re neriesand can be classi ed as either inland or marine. Inlandterminals generally consist o multiple storage tanks thatare connected to a pipeline system. Products are loadedand unloaded rom the common carrier pipeline to storagetanks and directly rom storage tanks to a truck or rail carloading rack. Marine terminals primarily receive petroleumproducts by ship and barge, short-haul pipeline connections

rom neighboring re neries, and common carrier pipelines.

erminals generate ees primarily by providing short- andlong-term storage o crude oil and re ned petroleum prod-

ucts, as well as ancillary services. Revenue is generated bycharging customers a ee based on the amount o productthat is delivered through terminals. In addition to through-put ees, revenue is generated by charging customers a ee

or providing services such as blending and additive injec-tion. erminals are unregulated and rates are market-basedas a result. erminal contracts, which typically provide orstorage or anywhere rom a ew days to several months,generally last or one year with annual renewal provisions.Most o these contracts contain a minimum throughputprovision that obligates the customer to move a minimumamount o product through a terminal or pay or termi-nal capacity reserved but not used. In general, similar topipeline operators, terminal operators do not take title tothe products that are stored in or distributed rom theirterminals.

erminal demand is greatest in a contango market, inwhich uture petroleum prices represented by the orwardcurve are higher than prevailing spot prices. In thesecircumstances, customers tend to store more product toarbitrage the higher prices expected in the uture. Whenbackwardation (the opposite o contango, i.e. uture pricesare lower than spot prices) exists, customers tend to trans-port more product to end markets to take advantage o current higher prices in lieu o storing product.

Re ners and chemical companies wil l use third-partyterminals when their acilities are insu cient due to sizeconstraints, specialized product handling requirements, orgeographic considerations.

Midstream Natural Gas Industry

Natural gas is rapidly growing as a global energy source,accounting or approximately % o world energy con-sumption today. Tis growth has been driven by plenti ulreserves, the environmental bene ts o its clean-burningnature, and the broad range o its applications.

Once natural gas is produced rom wells in areas such as theGul o Mexico, producers then seek to deliver the naturalgas and its components to nal markets. Te midstreamnatural gas industry is the link between upstream E&Pand downstream end markets. Te midstream natural gasindustry generally consists o natural gas gathering, trans-portation, storage, and processing/ ractionation activities.Te midstream segment typically involves local competitionbased on the proximity o gathering systems and process-ing plants to natural gas-producing wells.

SteelPath Fund AdvisorsMaster Limited Partnership Primer

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 16/31

In May , the DC Circuit Court upheld the Federal Ener-gy Regulatory Commission’s policy regarding an implied taxcomponent in the cost o service or determining allowedpipeline rates o return. Tis ruiling marks the beginningo a signi cant shi t o interstate natural gas assets into theMLP structure with multiple initial public o erings o pureplay interstate natural gas pipeline companies, and continu-ing in what could amount to the divestiture o more than$ billion o assets could eventually ollow suit.

ransportation

Te US natural gas pipeline system transports natural gasrom producing regions to customers such as local distri-

bution companies (LDCs), industrial users, and electricgeneration acilities. Similar to crude oil and re ned prod-uct pipelines, interstate pipelines carry natural gas acrossstate boundaries and are subject to FERC regulation on therates charged or their services, terms and conditions o theservices they o er, and location, construction, and aban-donment o their acilities. Intrastate pipelines, likewise,provide transportation within a particular state and are notsubject to FERC regulation, but rather governance at thestate agency level.

Te US Gul Coast is the most proli c domestic naturalgas-producing region. otal US production is insu cientto meet US demand, however. Te majority o this supplyshort all is likely to be met through natural gas imports

rom Canada as well as through LNG imports, which areexpected to be delivered predominately through Gul Coast

terminals. According to the Energy In ormation Adminis-tration (EIA), LNG’s share o total US gas supply could be ashigh as % by , compared to less than % today. How-ever, the recent success US producers have had in accessingshale gas and other non-conventional sources might resultin a much reduced role or LNG versus even these relativelyrecent expectations. Nonetheless, given the extensive pipe-line in rastructure and available gas-processing capabilityin and around the region, the Gul Coast is the target ormost o the proposed onshore LNG terminals.

Gathering

Te natural gas-gathering process involves the connectiono producing wells to pipelines, called gathering systems,which provide short-haul takeaway capacity. Gatheringsystems generally consist o a network o small-diameterpipelines that collect natural gas rom producing wells andtransport it to trunkline pipelines or urther transmission.Gathering systems operate at design pressures that maxi-mize the throughput rom all connected wells. Some sys-tems are supported by a reserve dedication, which commitsthe producer to utilize the midstream service provider’ssystem or all current and uture production or a speci edperiod, o ten or the li e o the producer’s reservoir lease.

Since wells produce at progressively lower eld pressuresas they age, it becomes increasingly di cult to deliverthe remaining production in the ground against a higherpressure that exists in the connecting gathering system.Natural gas compression is a process in which a volume o gas at an existing pressure is compressed to a desired higherpressure, allowing gas that no longer naturally ows into ahigher-pressure downstream pipeline to be brought to mar-ket. Field compression is typically used to allow a gathering

SteelPath Fund AdvisorsMaster Limited Partnership Primer

Natural GasEnd Users

NGLEnd Users

Wellhead Gathering Dehydration,Treating,

Processing

Fractionation

NGL Transportation & Storage

Natural Gas Transportation & StorageExhibit : Natural Gas Chain

Source: SteelPath

8/6/2019 MLP Primer

http://slidepdf.com/reader/full/mlp-primer 17/31

system to operate at a lower pressure or provide su cientpressure to deliver gas into a higher-pressure downstreampipeline. I eld compression is not installed, then theremaining natural gas in the ground will not be producedbecause it cannot overcome the higher gathering systempressure. In contrast, i eld compression is installed, a wellcan continue delivering natural gas that otherwise wouldlikely not be produced.

Dehydration

Natural gas collected at the wellhead has a variety o com-ponents that typically render it unsuitable or long-haul

pipeline transportation. Produced natural gas can be satu-rated with water, which must be extracted given that natu-ral gas and water can combine to orm ice that can blockparts o the pipeline gathering and transportation system.Water can also cause corrosion when combined with carbondioxide (CO ) or hydrogen sul de (H S) in natural gas. Inaddition, condensed water in a pipeline can raise pipelinepressure. o meet downstream pipeline and end-user gasquality standards, natural gas is dehydrated to remove thesaturated water.

reating

In addition to water, natural gas collected through a gather-ing system may also contain impurities such as carbondioxide and hydrogen sul de, depending on the reservoir