University of South Carolina Scholar Commons eses and Dissertations 2018 Mitigating Advocacy Bias: e Effect Of e Reviewer Role On Tax Professional Judgment Mary E. Marshall University of South Carolina Follow this and additional works at: hps://scholarcommons.sc.edu/etd Part of the Business Administration, Management, and Operations Commons is Open Access Dissertation is brought to you by Scholar Commons. It has been accepted for inclusion in eses and Dissertations by an authorized administrator of Scholar Commons. For more information, please contact [email protected]. Recommended Citation Marshall, M. E.(2018). Mitigating Advocacy Bias: e Effect Of e Reviewer Role On Tax Professional Judgment. (Doctoral dissertation). Retrieved from hps://scholarcommons.sc.edu/etd/4665

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

University of South CarolinaScholar Commons

Theses and Dissertations

2018

Mitigating Advocacy Bias: The Effect Of TheReviewer Role On Tax Professional JudgmentMary E. MarshallUniversity of South Carolina

Follow this and additional works at: https://scholarcommons.sc.edu/etd

Part of the Business Administration, Management, and Operations Commons

This Open Access Dissertation is brought to you by Scholar Commons. It has been accepted for inclusion in Theses and Dissertations by an authorizedadministrator of Scholar Commons. For more information, please contact [email protected].

Recommended CitationMarshall, M. E.(2018). Mitigating Advocacy Bias: The Effect Of The Reviewer Role On Tax Professional Judgment. (Doctoral dissertation).Retrieved from https://scholarcommons.sc.edu/etd/4665

MITIGATING ADVOCACY BIAS: THE EFFECT OF THE REVIEWER ROLE ON TAX PROFESSIONAL JUDGMENT

by

Mary E. Marshall

Bachelor of Science in Business Administration Oklahoma State University, 2008

Bachelor of Science in Business Administration

Oklahoma State University, 2008

Master of Public Administration Wichita State University, 2012

Master of Accountancy

Wichita State University, 2013

Submitted in Partial Fulfillment of the Requirements

For the Degree of Doctor of Philosophy in

Business Administration

Darla Moore School of Business

University of South Carolina

2018

Accepted by:

Donna Bobek Schmitt, Major Professor

Amy Hageman, Committee Member

Jason Rasso, Committee Member

Chad Stefaniak, Committee Member

Cheryl L. Addy, Vice Provost and Dean of the Graduate School

ii

© Copyright by Mary E. Marshall, 2018 All Rights Reserved.

iii

DEDICATION

To my amazing husband, Mike, for tirelessly encouraging and supporting me in

all of my academic endeavors. Thank you for happily moving across the country for

me—at least twice. To my daughter, Madelyn, for teaching me that surprises are the best

part of life. I cannot imagine life, or finishing this degree, without you. To my parents,

for their support. To Kelli, who started as a fourth-year student willing to help a first year

and has become one of my most cherished friends, for cheering me on. Finally, to

Britton Gildersleeve, Mark Glaser, Don Herrmann, Bud Lacy, Maryanne Mowen, Jeff

Quirin, Andy Urich, and Melissa Walker, for inspiring me to be curious. I can only hope

to inspire others as you have inspired me.

iv

ACKNOWLEDGEMENTS

This dissertation would not have been possible without Donna Bobek Schmitt,

who selflessly agreed to mentor me before and during her transition to USC and has

continued to fill many roles. I had no idea how much she would change my life when I

joined her for breakfast four years ago but I cannot even imagine what my doctoral

program would have looked like without her. I am also thankful for the guidance of my

committee members: Amy Hageman, who continues to inspire me with her ability to

balance her very full life; Jason Rasso, who is an amazing example of the importance of

perseverance, determination, and positivity; and Chad Stefaniak, who has mentored me

since I first began considering pursuing a doctoral degree and is largely responsible for

the path my career has taken. I also thank Bryan Stikeleather for investing so heavily in

my success amid his own transition to faculty and Scott Jackson for his tireless support of

my growth as a scholar. In addition, my completion of the dissertation process and the

doctoral degree is largely due to the support of USC alumni. Your willingness to provide

feedback, read drafts, and help me appreciate the quirks of our doctoral program did not

go unnoticed. To my classmates, Erin Hawkins, Laura Feustel, Ethan LaMothe, Kun Liu,

and Nate Waddoups, I am thankful for your friendship and look forward to many projects

in the future. Finally, I appreciate the comments and suggestions from workshop

participants at Louisiana Tech University, Oklahoma State University, The University of

Mississippi, The University of North Texas, the University of South Carolina, and the

University of Tulsa.

v

ABSTRACT

Prior literature finds tax professionals exhibit advocacy bias, a threat to tax

professionals’ objectivity, which can expose accounting firms and their clients to

penalties for overly aggressive tax reporting decisions. Mitigating this bias has been the

topic of several prior studies; however, research thus far has focused on how reviewers

identify bias within tax research memorandums (e.g., stylized writing or other obvious

cues). In an experiment administered to seventy-five tax professionals, this study isolates

the effect of the reviewer role and compares professionals’ evidence evaluation and

conclusions by role (i.e., reviewer or preparer). I find professionals who occupy the

reviewer role are significantly less likely to exhibit advocacy bias than those who are in a

preparer role, which suggests the reviewer role changes how professionals approach

evidence evaluation. In addition, I examine the influence of accountability on tax

professionals’ judgments. I find initial evidence that accountability influences the

likelihood of professionals’ exhibiting advocacy bias.

vi

TABLE OF CONTENTS

DEDICATION ................................................................................................................... iii

ACKNOWLEDGEMENTS ............................................................................................... iv

ABSTRACT .........................................................................................................................v

LIST OF TABLES ............................................................................................................ vii

LIST OF FIGURES ......................................................................................................... viii

CHAPTER 1: INTRODUCTION ........................................................................................1 CHAPTER 2: THEORY AND HYPOTHESIS DEVELOPMENT ....................................7

CHAPTER 3: EXPERIMENTAL METHODS .................................................................20

CHAPTER 4: RESULTS ...................................................................................................32

CHAPTER 5: CONCLUSION ..........................................................................................48

REFERENCES ..................................................................................................................54

APPENDIX A: MEASUREMENT SCALES ...................................................................59

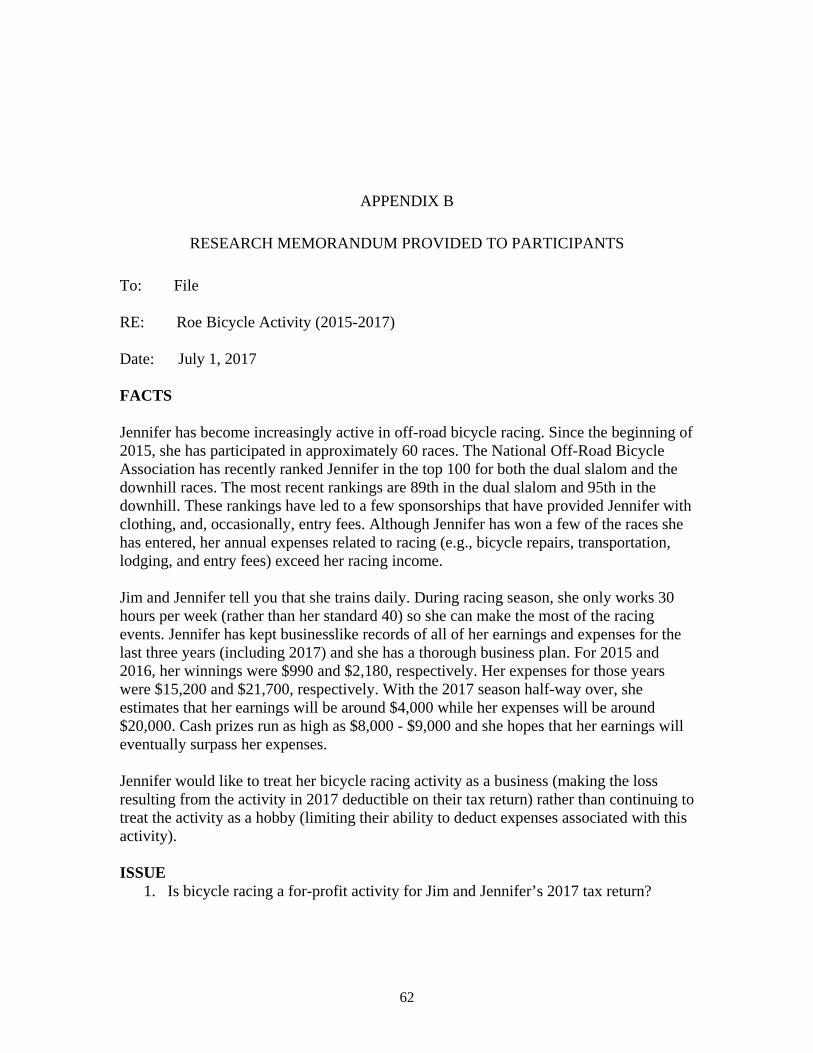

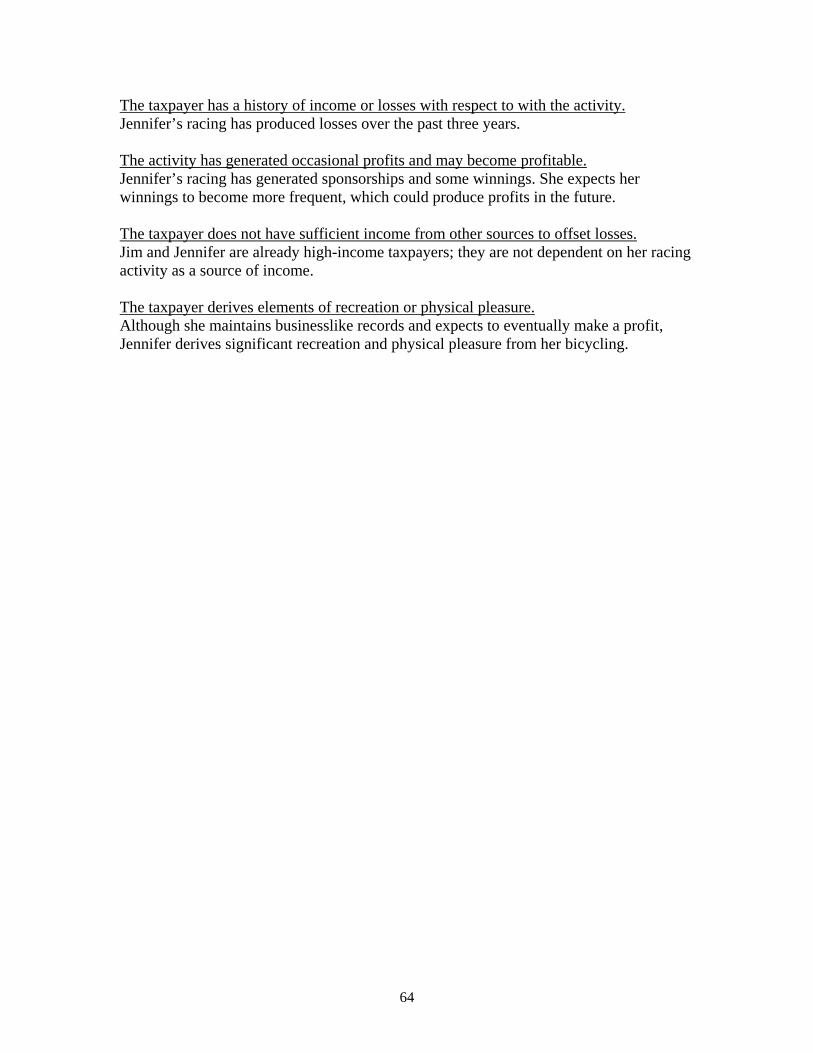

APPENDIX B: RESEARCH MEMORANDUM PROVIDED TO PARTICIPANTS .....62

vii

LIST OF TABLES

Table 3.1 Demographic Characteristics .............................................................................27

Table 3.2 Reg. 1.183-2 Factors to be considered ...............................................................28

Table 3.3 Accountability ....................................................................................................30

Table 4.1 Analysis of Advocacy Bias ................................................................................40

Table 4.2 Analysis of Accountability ................................................................................41

Table 4.3 Supplemental Analysis of Aggressiveness ........................................................43

Table 4.4 Supplemental Analysis of Partner Preference ...................................................44

Table 4.5 Supplemental Analysis of the Influence of FACTORS on LIKELY ................46

viii

LIST OF FIGURES

Figure 2.1 Predicted Effect of Client Advocacy on Evidence Evaluation .........................19

Figure 2.2 Predictions ........................................................................................................19

Figure 4.1 The Reviewer Role as a Moderator of Advocacy Bias ....................................47

1

CHAPTER 1

INTRODUCTION

Tax professionals are required to exhibit both objectivity in their analyses and

advocacy for their clients (Internal Revenue Service 2014; AICPA 2010). Importantly,

absent objectivity, tax professionals’ advocacy attitudes can cause them to

inappropriately assign greater weight to evidence supportive of their clients’ preferred

positions (Bobek, Hageman, and Hatfield 2010; Kahle and White 2004). This departure

from objectivity is referred to as advocacy bias, which occurs when “tax accountants’

advocacy attitudes produce confirmation bias when evaluating [evidence or] case law”

(Roberts 1998, 90). When present, advocacy bias affects multiple judgments of tax

professionals, including evidence search (Kadous, Magro, and Spilker 2008; Cloyd and

Spilker 1999), evidence evaluation (Kahle and White 2004; Johnson 1993), and bias

detection (Cuccia, Magro, and Whisenhunt 2017; Barrick, Cloyd, and Spilker 2004).

Advocacy bias can increase the likelihood of unexpected taxes, interest, and IRS

penalties for both the taxpayer and the tax professional signing the return (Hatfield 2000),

which is especially alarming because most clients expect tax professionals to focus on

accuracy rather than aggressiveness (Fleischman and Stephenson 2012; Collins, Milliron,

and Toy 1992).

Some argue advocacy bias is mitigated by the review process (Cuccia et al. 2017;

Hatfield 2001), which could happen if (1) reviewers exhibit individual characteristics

(e.g., experience, expertise) that decrease their susceptibility to bias or (2) elements of the

2

reviewer role (e.g., accountability or role expectations) facilitate more objective judgment

and decision making for those occupying the reviewer role. Tax reviewers may not be

aware of either their own or preparers’ advocacy bias because it is an unintentional (and

perhaps subconscious) bias that is stronger for those in higher ranks and with more

experience (Spilker, Stewart, Wilde, and Wood 2016; Bobek, Hageman, and Hatfield

2014; Bobek et al. 2010). Thus, reviewers may be just as susceptible to advocacy bias as

preparers despite increased experience. It is possible, however, that elements of the

reviewer role (e.g., accountability or role expectations) prompt professionals to focus

more on objectivity. Thus, the present study focuses on the effects of the reviewer role on

advocacy bias because individual characteristics are unlikely to mitigate bias and may

exacerbate bias.

Role theory (Biddle 1979) suggests elements of the reviewer role could mitigate

advocacy bias because individuals change how they make decisions based on the role

they occupy. According to Biddle (1979, 56), roles are a collection of “behaviors that are

characteristic of persons in a context.” My study examines how roles, and the

expectations associated with those roles, influence tax professional behavior. Barrick et

al. (2004) identify three expectations of tax professionals: accuracy, advocacy, and

feedback. Both preparers and reviewers are expected to achieve accuracy and advocacy,

but only those in the reviewer role are expected to provide feedback. I propose the

additional expectation of providing feedback may lead reviewers to approach evidence

evaluation differently than preparers. Specifically, this study predicts reviewers approach

engagements with a heightened focus on objectivity because they feel accountable for

meeting the expectations associated with reviewing (i.e., evaluation of preparer effort and

3

conclusion, assessment of evidence search and evaluation process, etc.). Prior literature

finds increased accountability leads to greater cognitive effort and reduced susceptibility

to cognitive biases (Tetlock 1999), thus I predict professionals occupying the reviewer

role are more likely to evaluate evidence objectively (e.g., with less bias) because of the

accountability associated with providing feedback to preparers.

Research has not yet examined whether the influence of advocacy bias changes

when tax professionals occupy the reviewer role (compared to when they occupy the

preparer role). Prior research suggests reviewers are unlikely to detect advocacy bias

without obvious cues (Cuccia, Magro, and Whisenhunt 2017; Barrick, Cloyd, and Spilker

2004; Hatfield 2000); however, past studies have focused on how reviewers

inappropriately evaluate biased preparer conclusions. Tax professionals, especially those

at the senior level, are often assigned to work as preparers on some engagements and as

reviewers on others, which suggests tax professionals can shift from one role to another.

The present study examines whether advocacy attitudes influence reviewer evaluation of

both the preparer’s conclusion and the associated evidence supporting the conclusions. In

addition, preparers in this study evaluate the same evidence and provide the same

judgments as reviewers, which allows me to compare the effects of advocacy attitudes on

the same evidence evaluation in both roles.

An online experiment was administered to 75 experienced tax professionals

recruited through a Qualtrics Panel. The study’s hypotheses are tested with a between-

participant experiment with three conditions. Participants act as either a reviewer or

preparer. In addition, the study manipulates whether participants assigned as reviewers

review a memo that (1) includes a preparer conclusion in favor of the client-preferred

4

treatment or (2) does not include a preparer conclusion. This additional manipulation

allows the study to fully isolate the effect of role by comparing reviewer judgments both

with and without the influence of a preparer conclusion.

Professionals determine the tax treatment (hobby or business) of a net loss

incurred in a bicycle racing activity, which the client prefers to treat as a business. In all

conditions, professionals are provided with partner instructions (indicating the partner has

no preferred outcome), client facts, a draft file memo documenting the preparer’s

research, and relevant tax authority. Professionals indicate whether the client facts

indicate business or hobby treatment based on the “hobby loss” rules of I.R.C. §183 and

Reg. Sec. 1.183-2. In addition, professionals in the reviewer (preparer) conditions are

asked the likelihood they would sign off on a conclusion (conclude) that the activity be

considered a business. Finally, they respond to items measuring client advocacy and

accountability.

Using ANOVA and regression analysis, I examine the effect of client advocacy,

role, and accountability on tax professionals’ evidence evaluation processes and

conclusions. Bias occurs when advocacy attitudes influence evidence search and/or

evaluation (e.g., if strong client advocacy attitudes lead a professional to inappropriately

assess evidence as supportive of the client’s preference). Results indicate that tax

professionals who occupy the reviewer role are less likely to exhibit advocacy bias than

those in a preparer role. Further, I find no evidence that reviewers’ evidence evaluation

processes are influenced by the preparer conclusion they view. However, I do find

evidence that accountability to the client influences preparers’ judgments. Specifically,

increasing accountability to the client decreases the likelihood of preparers exhibiting

5

advocacy bias, which provides initial evidence that firms may be able to mitigate

preparer advocacy bias by increasing felt accountability.

This study contributes to the literature in both theoretical and practical ways.

First, by examining the effect of the reviewer role on tax professional judgments, this

study adds to a growing literature (e.g., Cuccia et al. 2017; Barrick et al. 2004) studying

whether the review process mitigates advocacy bias. Whereas prior literature has

separately examined the effects of advocacy bias on both reviewer and preparer tasks,

this study isolates role by comparing how professionals in the role of reviewer evaluate

the same set of evidence as those in the role of preparer. Results provide initial evidence

that occupying the reviewer role mitigates advocacy bias.1 This study’s design examines

the effect of an existing firm mechanism (i.e., the review process) on the presence of

advocacy bias. The findings provide insight into the importance of the review process in

ensuring objective evidence evaluation as part of client recommendations.

Second, this study provides initial evidence of the effects of accountability on the

likelihood of tax preparers exhibiting advocacy bias. Specifically, preparers who feel

accountable to the client are less likely to exhibit advocacy bias, which provides insight

to firms regarding the importance of conveying the expectation that preparers are

accountable for their recommendations. Third, this study examines the effects of

accountability to multiple sources, including documenting different effects of

accountability to the client and firm. Interestingly, I find that accountability to the client

decreases the likelihood a preparer will exhibit advocacy bias but, surprisingly,

1 This study supports findings in prior audit studies which suggest occupying the reviewer role may improve objectivity in professional judgments (Reimers and Fennema 1999; Ricchute 1999; Libby and Trotman 1993).

6

accountability to the firm does not. Thus, I provide insights for future research about the

effect of accountability, especially when there are multiple accountability sources. For

example, auditors may also feel accountable to both the firm and the client (Gibbins and

Newton 1994). Future research could build on this study’s findings to disentangle the

effects of accountability to multiple sources on auditor and tax professional judgment.

Fourth, I find tax professionals are likely to assume the partner prefers to agree

with the client preference even when the partner explicitly specifies no preference. As a

result, professionals may feel pressure to find support for an outcome they

inappropriately assume the partner prefers, especially when in the preparer role. Thus,

firms can avoid unintentionally aggressive recommendations by explicitly and credibly

communicating information about preferences (or lack thereof). Finally, this study

empirically tests the effect of approval bias in professional judgment. Approval bias

occurs when professionals’ bias leads them to endorse other professionals’ potentially

biased judgments (Bazerman et al. 2002). Prior literature finds advocacy bias persists

across rank in the firm and experience levels; thus, the tax context provides one of the

most likely areas for approval bias to manifest. However, this study finds no evidence

that endorsing a preparer’s conclusion (e.g., signing off on a conclusion to support the

client’s preferred position) influences the likelihood of reviewer advocacy bias.

The remainder of this paper is organized as follows. Section 2 reviews the

literature on advocacy bias, role theory, and accountability, providing theoretical

development of the hypotheses. Sections 3 and 4 describe methods and results. Section 5

concludes.

7

CHAPTER 2

THEORY AND HYPOTHESIS DEVELOPMENT

2.1 Advocacy Bias

A tax professional has both the “right and the responsibility to be an advocate for

the taxpayer” (AICPA 2010); however, s/he also have a responsibility to “objectively

evaluate all relevant facts and tax authorities when preparing advice” (Kadous and Magro

2001, 453). Favoring a client’s preference supports a tax professional’s goal of being an

advocate but doing so without sufficient support of relevant authority may lead to

inappropriate recommendations. When advocacy attitudes “inhibit their abilities to

accurately assess authoritative support” (Cloyd and Spilker 1999, 1), tax professionals

may unintentionally interpret facts and/or evidence in a manner that inappropriately

supports the clients’ preferences. Prior tax literature has termed this “advocacy bias.”2

Advocacy bias can lead to the recommendation of aggressive tax positions;3

however, aggressiveness is not a direct indicator of advocacy bias. Rather, advocacy bias

occurs when professionals’ advocacy attitudes influence the judgments they make during

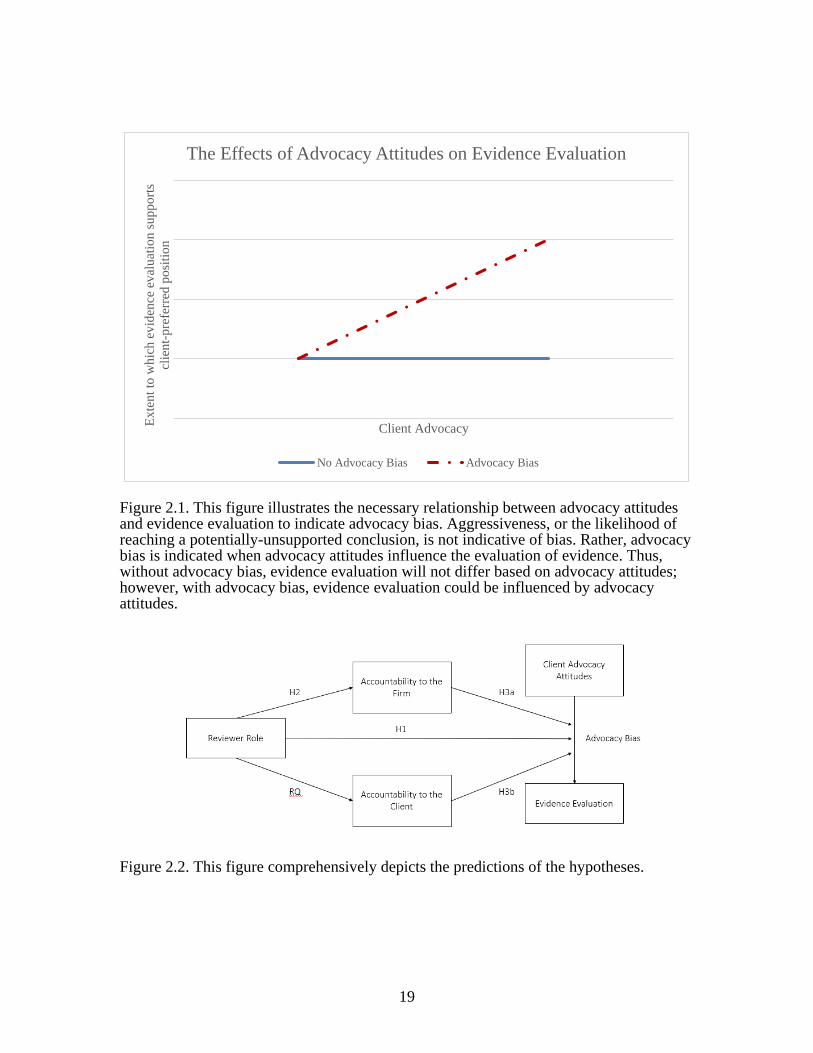

evidence search and/or evidence evaluation (see Figure 2.1). Because advocacy bias is

2 Advocacy bias is similar to confirmation bias because it leads to biased evaluation; however, advocacy bias refers to bias towards the client’s preference rather than the professional’s initial opinion or judgment. Tax professionals exhibiting advocacy bias attempt to confirm client preferences rather than objectively determine the appropriate tax treatment. See Bobek et al. (2010) for a synthesis of client advocacy research. 3 The present study uses the term “aggressive tax positions” to describe positions that could be overturned if challenged in Tax Court. Recommending an aggressive position is not necessarily illegal, but when such a recommendation is the result of biased evidence evaluation, the tax professional and the client are likely taking on more risk than they intend.

8

generally an unconscious bias, it is more difficult to detect and control than

aggressiveness. Prior studies establish that tax professionals acting as preparers exhibit

advocacy bias throughout the research process, including searching for evidence (Kadous

et al. 2008; Cloyd and Spilker 1999) and evaluating evidence (Kahle and White 2004;

Johnson 1993). For example, prior research has shown tax professionals assign greater

weight to court cases that support the client’s preferred treatment (Johnson 1993) and

focus primarily on evidence most consistent with the client’s preferences (Kadous et al.

2008; Hatfield 2001; Cloyd and Spilker 1999).

Research also shows reviewers may exhibit advocacy bias when determining

whether to rely on preparer research memorandums (Hatfield 2001) and when detecting

bias in others’ judgments (Cuccia et al. 2017; Barrick et al. 2004). Cuccia et al. (2017)

find reviewers are likely to detect preparer bias only when the memo is linguistically

stylized to emphasize the evidence supporting the client-preferred outcome. Barrick et al.

(2004) examine whether reviewers are subject to advocacy bias when the client preferred

position does not have a “realistic possibility” of being upheld in court. The authors find

reviewers are more likely to rely on biased memos that incorrectly support an

unsupportable client preference than on biased memos that correctly support an

alternative. That is, when both memos are biased, reviewers are more likely to rely on

and incorporate the memo that achieves the client preference. However, the authors also

find some evidence that reviewers can detect preparer bias. Specifically, they find

supervisors (e.g., reviewers) request more rework and are less persuaded when staff

submit clearly biased memos supporting a client preference that cannot be objectively

supported than when they support unbiased memos supporting the same unsupportable

9

client preference. That is, when both memos recommend an unsupportable position,

reviewers are more likely to rely on the unbiased memo.4 Thus, supervisors (reviewers)

appear likely to detect advocacy bias when that bias leads to obviously inappropriate

recommendations (Barrick et al. 2004) or highly stylized presentation (Cuccia et al.

2017). However, advocacy bias is generally considered to be unintentional (Bobek et al.

2010), which suggest it is likely judgments affected by advocacy bias are not always

accompanied by stylized writing, obviously unsupported recommendations, or other

obvious cues.

The abovementioned prior studies have established reviewer advocacy bias by

assessing whether reviewers sign off on (i.e., agree with) preparer recommendations to

support aggressive client preferences. Although advocacy bias can contribute to evidence

evaluation that supports aggressiveness, aggressiveness is not a direct indicator of

advocacy bias. As a result, an increase in aggressiveness is not a precise test of whether

advocacy bias influences judgment. Research has not yet identified whether reviewer

judgments are driven by (1) reviewers’ own advocacy biases, (2) over-reliance on

preparers’ biased recommendations, or (3) reviewers’ appetites for aggressiveness. This

study follows Bobek et al. (2010) and examines bias more directly by focusing on

whether advocacy attitudes influence evidence evaluation rather than focusing on the

aggressiveness of a conclusion.

4 Barrick, et al. (2004) examine a scenario where client preference is clearly unsupportable because it does not have a “realistic possibility” of being upheld if challenged in court. Thus, tax professionals are unable to support the client’s preference (advocacy expectation) because doing so would not be supported by relevant authority (accuracy expectation). Following Bobek, et al. (2010), my study incorporates sufficient ambiguity that biased professionals could determine meeting both expectations is possible.

10

2.2 Mitigating Advocacy Bias with the Review Process

Previous research has identified multiple antecedents and consequences of

advocacy bias; however, only a few studies have examined whether there are processes in

place to mitigate advocacy bias effectively. Some argue the review process can mitigate

advocacy bias (Cuccia et al. 2017). This argument is reasonable because the review

process serves as a quality control mechanism. Circular 230, which governs behavior of

tax professionals practicing before the IRS, requires a tax professional to use “reasonable

care in engaging, supervising, training, and evaluating” a subordinate (IRS 2014, 19).

Barrick et al. (2004) indicate all tax professionals have two expectations in a research

engagement: (1) accuracy, which requires that they evaluate the evidence and determine

the appropriate conclusion, and (2) advocacy, which requires that they “marshal

evidence” to support their client’s preferences. Reviewers have a third expectation of

“providing corrective feedback necessary for novice professionals to learn from their

experiences” (Barrick et al. 2004, 2).5 Given the differences between the two roles, the

review process could mitigate advocacy bias if (1) professionals acting as reviewers

possess individual characteristics (e.g., experience or expertise) that facilitate

identification of alternative explanations, omissions, or inconsistencies; or (2) elements of

the reviewer role (e.g., increased accountability) prompt professionals to approach a task

differently than when they are not in that role.

One way the review process could mitigate advocacy bias is if tax reviewers

possess individual characteristics that facilitate more objective judgments and decrease

5 The reviewer role has a similar focus in an audit environment. Yip-Ow and Tan (2000) describe an audit reviewer’s identification of alternative explanations, omissions, or inconsistences in the preparer’s work as one of the primary purposes of the review process.

11

susceptibility to advocacy bias when compared to preparers. Professionals serving as first

reviewers generally possess increased expertise and exposure to more complex tax issues

than preparers (AICPA 2016); thus, one might expect reviewers to be more objective than

preparers. However, prior research shows client advocacy attitudes are stronger for

professionals with more experience or higher rank (Spilker, Stewart, Wilde, and Wood

2016; Bobek et al. 2010). Although reviewers may have more experience and/or expertise

than preparers, they may also have increased propensity to exhibit advocacy bias given

their stronger advocacy attitudes. This study does not expect reviewers’ individual

characteristics (e.g., experience and/or expertise) to mitigate advocacy bias. Motivated by

role theory (Biddle 1979) and research in accountability (Lerner and Tetlock 1999;

Gibbins and Newton 1994; Tetlock 1985), I examine another way in which the review

process may mitigate advocacy bias: the effect of occupying the reviewer role.

2.3 Role Theory and Accountability

I am unaware of research directly comparing similar judgments of tax

professionals occupying the reviewer and preparer roles; however, the reviewer role has

been studied in an audit context. Specifically, audit reviewers are more focused on

inconsistent information, produce more plausible alternative hypotheses, and are more

sensitive to source objectivity than audit preparers (Ricchute 1999; Reimers and Fennema

1999; Ismail and Trotman 1995; Libby and Trotman 1993). These studies present two

potential explanations for differences in behavior across roles. First, Reimers and

Fennema (1999) and Libby and Trotman (1993) argue that the preparer (i.e., the “initial

decision maker”) is focused more on producing an initial judgment, which prompts a

focus on systematic decision making and on defending his/her conclusion(s). In contrast,

12

the authors describe the reviewers as entering the process after the initial decision has

already been made, which prompts a focus on counterarguments and alternative

explanations because “information that is novel or unexpected receives relatively more

attention” (Libby and Trotman 1993, 563) from those who are reviewing an existing

decision. Thus, prior studies suggest the reviewer can be more objective because s/he is

less focused on developing a conclusion and more focused on reviewing the accuracy and

appropriateness of an existing conclusion. Second, prior literature also suggests the high-

quality decision-making behaviors of audit reviewers could be associated with an

expectation of accountability, which is defined as the need to justify decisions and/or

actions to another (Lerner and Tetlock 1999; Tetlock 1985). This study argues the

reviewer role produces different evidence evaluation processes than does the preparer

role, whether by shifting from systematic to more holistic decision making or by

increasing accountability.6

According to role theory, individuals occupy multiple roles and each role is

accompanied by role expectations, which are learned over time through socialization

(Ammeter, Douglas, Ferris, and Goka 2004; Frink and Klimoski 1998; Biddle 1979).

Roles are not necessarily jobs; roles represent a collection of “behaviors that are

characteristic of persons in a context” (Biddle 1979, 56). Tax professionals occupy

multiple roles (e.g., preparer, reviewer, signer, etc.), often simultaneously, with multiple

role senders (e.g., partner, client, IRS, etc.) who have differing expectations. For

6 Tax professionals may respond to occupying the reviewer role differently than auditors. Prior findings in audit are informative of professional behavior, but tax professionals work in a different environment. Auditors are expected to operate with professional skepticism, which could enhance objectivity. In contrast, tax professionals are required to be advocates, which could reduce objectivity if tax professionals exhibit advocacy bias. By examining tax professional behavior, this study examines the effect of role in an environment without an expectation of professional skepticism.

13

example, both preparers and reviewers are expected to strive for accuracy and advocacy,

whereas only reviewers are expected to provide feedback to subordinates (Barrick et al.

2004). Further, although the review process is assumed to provide learning opportunities

for a preparer (Gibbins and Trotman 2002), those at the reviewer level are expected to

have the expertise necessary to facilitate that learning. Because providing feedback

requires reviewers to focus on the quality of both the workpapers and the conclusions, I

expect reviewers to be more focused on reaching objective conclusions than professionals

who are not expected to provide feedback. Formally stated below, this study predicts

reviewers are less likely to exhibit advocacy bias because of the expectations associated

with being a reviewer.

H1: Tax professionals occupying the reviewer role are less likely to exhibit advocacy bias than those occupying the preparer role.

2.4 Accountability and Advocacy Bias

In addition to examining the effect of occupying the reviewer role on the

likelihood of exhibiting advocacy bias, this study also examines (1) the effect of role on

accountability and (2) the effect of accountability on tax professionals’ likelihood of

exhibiting advocacy bias. Role theory suggests “role occupants” feel accountable for the

perceived role expectations sent by “role senders” (authoritative persons) (Biddle 1979).

These role expectations are developed both formally and informally and are largely based

on norms in a workplace environment or process (Frink and Klimoski 1998). Tax

professionals are expected to act as client advocates and to complete their work with due

diligence and objectivity. These expectations come from the firm, the client, and the IRS

(e.g., the “role senders”), so all tax professionals have the same role senders regardless of

the role they occupy. However, role senders may assign different expectations to

14

professionals based on role. As discussed by Barrick, et al. (2004), tax preparers are

expected to achieve accuracy and advocacy and tax reviewers are expected to achieve

accuracy, advocacy, and feedback. Ammeter, et al. (2004) explain that if professionals

perceived differences in expectations, this could lead to differences in felt accountability.

It is unclear whether reviewers are expected to exhibit stronger advocacy or increased

accuracy compared to preparers; however, only reviewers are required to provide

feedback. Hence, this paper expects professionals to perceive an additional expectation to

provide feedback, which role theory predicts will lead to increased accountability to the

firm (Ammeter et al. 2004; Hall, Blass, Ferris, and Massengale 2004; Biddle 1979).

Formally stated below, I predict tax professionals have higher accountability to the firm

when occupying the reviewer role than when occupying the preparer role.

H2: Occupying the reviewer role increases a tax professional’s perceived accountability to the firm. The effect of the reviewer role on accountability to the client is less clear.

Whereas firms have different expectations for professionals occupying the reviewer and

preparer roles, it is unclear whether clients’ expectations differ across roles. Further, even

if clients do have different expectations, it is difficult to predict whether professionals

perceive these differences. Nevertheless, it is possible that professionals feel different

levels of accountability to their clients as they move into different roles. For example,

professionals may feel more responsible for client retention as they gain experience.

When combined with the stronger client advocacy associated with higher ranks, an

increase in responsibility for client retention suggests reviewers may feel increased

accountability to the client. In contrast, they may also feel more pressure to protect the

firm from litigation, which may shift their focus away from client preferences and toward

15

the firm’s expectations. It is also possible that reviewers have the experience necessary to

more effectively manage the tradeoff between achieving client preferences and

minimizing firm exposure. Thus, I pose the following research question to further explore

the relationship between role and accountability to the client.

RQ: Does occupying the reviewer role influence a tax professionals’ perceived accountability to the client? Prior research finds accountability influences many accounting decisions

including: effort duration in tax research (Cloyd 1997), extent and breadth of audit testing

(Asare, Trompeter, and Wright 2000), level of consensus among audit team members

(Johnson and Kaplan 1991), conservativeness of audit fraud risk assessments (Hoffman

and Patton 1997), and amount of justification provided by auditors (Koonce, Anderson,

and Marchant 1995). Prior research generally manipulates accountability by requiring

justification of decisions or by informing participants their work will be reviewed by

superiors. In contrast, the present study examines whether occupying the reviewer role is

a naturally occurring prime which increases accountability. If occupying the reviewer

role affects decision makers similarly to being expected to justify ones’ decisions, then

the review process could mitigate bias by increasing the accountability felt by those

performing the reviews.

However, an increase in accountability may not always improve the likelihood of

the review process to mitigate advocacy bias and can lead to suboptimal decision making

in some cases (Siegel-Jacobs and Yates 1994). Specifically, accountability influences

judgment differently depending on (1) whether the accountability source’s (i.e., the

entity/person to which the individual feels accountable) preferences are known; (2)

whether there are multiple sources of accountability; and (3) the type of accountability

16

(i.e. outcome or process). If the accountability source’s preference is known, individuals

may engage in attitude shifting or defensive bolstering (Hatfield 2000; Gibbins and

Newton 1994; Tetlock 1985).7 In a tax context, examples of attitude shifting include (1)

ensuring research findings agree with the partner’s expected outcome and (2) following

the partner’s preferred research approach. Thus, attitude shifting leads tax professionals

to work towards the accountability source’s expectation. In contrast, when the

accountability source’s preferences are not known, accountability can lead to increased

cognitive effort, which may increase objectivity. For example, if a tax partner does not

express an opinion, there is no explicit target to shift towards. Accountability is most

likely to decrease bias when the source’s preferences are not known because development

of an objective, balanced argument to support a position (rather than engaging in attitude

shifting or defensive bolstering) is more likely to occur when source preferences are

unknown.

In addition, the direction of attitude shifting and/or defensive bolstering are

difficult to predict in a tax setting because public accounting professionals face multiple

sources of accountability (e.g., partner and client) who may have conflicting preferences

(Gibbins and Newton 1994). For example, tax professionals may feel accountable both to

their clients because of an advocacy relationship and to their firms because of career and

reputational concerns. Because the client’s preference is usually for tax minimization,

strong feelings of accountability to the client could lead a professional to align his or her

evidence evaluation process with tax minimization (e.g., a more aggressive position).

7 Attitude shifting occurs when decision makers match their decisions to those of the audience to which they feel accountable (the “accountability source”). Defensive bolstering occurs when decision makers increase justification of their conclusion because it conflicts with the source’s preferences.

17

Prior research shows tax professionals’ evidence evaluation is often biased to agree with

client preferences (Bobek et al.2010; Kahle and White 2004; Johnson 1993), so strong

feelings of accountability to the client could further exacerbate advocacy bias. A similar

outcome could occur if the professional assumes the firm wants to meet the client’s

preferences. However, it is more likely that the professional would assume the firm

prefers objective and defensible evaluations because firms are focused on long-term

outcomes such as client retention and avoiding penalties. Such a focus would prompt a

more thorough and unbiased process rather than attitude shifting or defensive bolstering.

Because advocacy bias limits objectivity, focusing on building an objective and thorough

analysis could mitigate advocacy bias by increasing the cognitive effort dedicated to the

task (Gibbins and Newton 1994).

The type of accountability (i.e., process or outcome) also influences whether

accountability improves decision making (Siegel-Jacobs and Yates 1996).8 Prior research

shows outcome accountability may lead to dysfunctional behavior while process

accountability improves decision quality (Siegel-Jacobs and Yates 1996). Because tax

professionals may perceive outcome expectations from both the client and the firm,

increased accountability could hinder objectivity and potentially increase bias. Advocacy

bias can be described as using a biased evidence evaluation (e.g., process) to support a

client’s preferred tax position (e.g., outcome). I expect (1) accountability to the firm to

reduce a tax professional’s advocacy bias by focusing him/her on the quality of the

evidence evaluation process and (2) accountability to the client to increase a tax

8 Process accountability relates to the steps taken to arrive at a final conclusion. An example in a tax context is whether the professional follows the appropriate workflow. Outcome accountability relates to the final conclusion, for example the professional’s recommendation to the client.

18

professional’s advocacy bias by focusing him/her on the client’s preferred outcome.9

Formally stated below, this paper expects perceived accountability to the firm and the

client to influence the likelihood tax professionals will exhibit advocacy bias.

H3a: Accountability to the firm decreases the likelihood tax professionals will exhibit advocacy bias. H3b: Accountability to the client increases the likelihood tax professionals will exhibit advocacy bias.

In summary, I study whether the reviewer role mitigates advocacy bias by

examining whether (1) professionals occupying the reviewer role are less likely to exhibit

advocacy bias, (2) the reviewer role increases accountability, and (3) accountability

mitigates the effect of advocacy attitudes on evidence evaluation (see Figure 2.2). I

expect the reviewer role to mitigate advocacy bias because of the expectations associated

with the reviewer role. In addition, I examine whether occupying the reviewer role

increases accountability to both the firm and the client, which could also influence the

likelihood of exhibiting advocacy bias.

9 Outcome accountability to the firm is held constant by informing participants the partner has no a priori preference related to outcome. This is a reasonable assumption because, although firm leadership is interested in client retention, they are likely more interested in providing quality service to their client. In addition, outcome accountability to the client is held constant by informing participants of the client’s preference.

19

Figure 2.1. This figure illustrates the necessary relationship between advocacy attitudes and evidence evaluation to indicate advocacy bias. Aggressiveness, or the likelihood of reaching a potentially-unsupported conclusion, is not indicative of bias. Rather, advocacy bias is indicated when advocacy attitudes influence the evaluation of evidence. Thus, without advocacy bias, evidence evaluation will not differ based on advocacy attitudes; however, with advocacy bias, evidence evaluation could be influenced by advocacy attitudes.

Figure 2.2. This figure comprehensively depicts the predictions of the hypotheses.

Exte

nt to

whi

ch e

vide

nce

eval

uatio

n su

ppor

ts

clie

nt-p

refe

rred

pos

ition

Client Advocacy

The Effects of Advocacy Attitudes on Evidence Evaluation

No Advocacy Bias Advocacy Bias

20

CHAPTER 3

EXPERIMENTAL METHODS

3.1 Participants

Seventy-five experienced tax professionals currently working in public

accounting were recruited through a Qualtrics panel. The effect of reviewer role is

isolated by randomly assigning participants of similar rank and experience to each role,

so only participants who have current or recent (e.g., within two years) experience in both

the preparer and reviewer roles were allowed to continue through the screening process.

In addition, participants must work (1) in a public accounting firm, (2) in tax, and (3) in

an office with at least 20 CPAs or CPA-eligible employees. Demographic information

about the participants is displayed in Table 1. Participants report an average age of 35

years, and 105 months (8.7 years) of experience. Forty-six (61 percent) participants are

female. Participants also reported education and experience common to professionals

working as tax professionals. Specifically, 16 percent work at Big 4 firms, seven percent

at international firms, 16 percent at national firms, 27 percent at regional firms, and 35

percent at local firms. Also, 68 percent of participants report they have researched hobby

loss issues (the issue in the experimental case) in the past. In addition, 71 participants

report either a bachelor’s or master’s degree in business, 55 are CPAs, six are either CIAs

or CMAs, and two are EAs. Demographic characteristics are not significantly different

21

across conditions (all p > 0.23) and do not significantly influence results (all p > 0.30).10

Thus, I conclude random assignment was achieved.

3.2 Design and Manipulations

The hypotheses are tested with a 3 x 1 between-participant experiment.

Participants determine whether Jim and Jennifer Roe can deduct expenses related to

Jennifer’s competitive bicycling activity as a for-profit business (rather than as a hobby),

which would allow the Roes to deduct a loss in the current year.11 Participants are

provided with a draft file memorandum and links to excerpts from IRC §183 and IRS

Regulation 1.183-2 for their reference. I manipulate role by randomly assigning

participants to act as a preparer completing a memorandum or as a reviewer evaluating a

memorandum. Random assignment controls for differences in experience or rank, which

have both been shown to influence advocacy attitudes (Spilker et al. 2016; Bobek et al.

2010).12

In addition to being influenced by the role they occupy, reviewers who view a

preparer’s conclusion in support of the client’s preference may perceive the

recommendation as additional information supporting the client’s preference. Such

additional information may lead to approval bias, which occurs when endorsing another’s

10 All p-values are two-tailed unless noted otherwise. 11 I.R.C. §183 requires taxpayers who engage in activities that might be viewed as hobbies to satisfy a “facts and circumstances” test based on nine identified factors (explained in IRS Regulation 1.183-2) to determine whether the activity is engaged in for profit (business treatment) or is a hobby. The factors are not explicitly weighted or ranked and there are few obvious trends in how the courts have applied the factors. If an activity does not meet the requirements of Reg. 1.183-2, the activity is considered a hobby and the expenses are only deductible as itemized deductions (subject to a floor) and the amount deducted is limited to the amount of income associated with the activity (i.e., no loss can be deducted); taxpayers prefer to treat activities as businesses to allow for the deduction of losses. The rules that apply beginning in 2018 make hobby treatment appear even less favorable because the deductibility of any expenses (rather than just expenses exceeding income) associated with hobbies is unclear. 12 Regression analysis indicates participants in this study exhibited similar trends, such that professionals’ client advocacy attitudes increased with higher rank (b = 0.187, p = 0.108) and increased experience (b = 0.176, p = 0.13).

22

judgment magnifies cognitive biases (Bazerman et al. 2002). To control for the potential

of approval bias, the experiment includes two reviewer conditions manipulating whether

the memo includes a preparer conclusion of business treatment or an explicitly omitted

preparer conclusion.13

3.3 Task and Procedure

The scenario is modified from Bobek et al. (2010), which was designed to be

ambiguous regarding whether the bicycling activity should be viewed as a hobby or

business. The scenario includes several factors that indicate business treatment

(businesslike records and likelihood of future profits) and only one that clearly indicates

hobby treatment (the taxpayer derives significant pleasure from the activity). The

magnitude of the losses in the present study is larger than that in Bobek et al. (2010),

which increases the likelihood the decision appears nontrivial to the Roes’ overall tax

liability. In addition, the Roes are presented as important clients with no clear indications

of high risk because advocacy bias is most likely to occur when client importance is high

and risk is low (Bobek et al. 2010; Kadous et al. 2008). Because the present study also

examines accountability, participants view instructions from the engagement partner that

emphasize the importance of the client and clearly state (1) the partner does not have a

specific outcome in mind and (2) the client prefers business treatment. Specifically, the

13 In practice, a reviewer is unlikely to review a memorandum with no preparer conclusion; however, I include the condition for experimental control. Approval bias suggests a preparer conclusion could exacerbate reviewer advocacy bias if the reviewer perceives the preparer conclusion as additional evidence in support of the client’s preference (i.e., the reviewer may be susceptible to approval bias). Thus, this study isolates the possible effect of approval bias on reviewer judgment by replacing the preparer’s recommendation (i.e., “The Roes’ activity should be treated as a business”) with a note indicating: “For this case study the preparer’s conclusion has been purposely omitted.” Untabulated results indicate the preparer conclusion did not influence (1) reviewers’ likelihood of exhibiting advocacy bias (p = 0.474) or (2) reviewers’ likelihood of assessing factors as supportive of business (p = 0.277). Thus, analysis and hypotheses testing include both reviewer conditions as one collapsed “reviewer” condition because there is no evidence of approval bias.

23

instrument states “Jennifer has become increasingly involved in bicycle racing and would

like to treat her bicycle racing as a business. I have not yet considered the

appropriateness of this decision and need to advise her soon.” This holds constant the

level of outcome accountability felt by participants.

Reviewers are informed they will be reviewing the memo completed by Sam, a

second-year staff at their firm. Preparers are informed the memo is almost complete and

their task is to develop a conclusion regarding the proper tax treatment of the bicycling

activity. The memo is near complete because the study is focused primarily on evidence

evaluation rather than on evidence search. Prior research finds advocacy bias affects both

the search for and evaluation of evidence (Bobek et al. 2010; Kadous et al. 2008; Cloyd

and Spilker 1999). Reviewers usually rely on preparers’ evidence search, but

professionals in both roles evaluate evidence. Thus, participants are presented with

evidence that has already been collected rather than conducting the entire search process,

which maintains similar presentation and cognitive load in all conditions while also

controlling for the effect of preparer stylization on reviewer judgment (Cuccia et al. 2017;

Tan and Trotman 2003).

3.4 Dependent Variable: Evidence Evaluation

The study’s primary analysis examines the relationship between advocacy

attitudes and evidence evaluation. After indicating their conclusion (preparer condition)

or sign-off (reviewer conditions) decisions, participants are asked to indicate whether

each of the nine factors included in Regulation 1.183-2 (see table 3.2) indicate business

or hobby treatment on 6-point scales (where 1 = definitely hobby and 6 = definitely

business). Because Reg. 1.183-2 requires that each determination be based on the facts

24

and circumstances of each case, not all nine factors are relevant to every case. Thus,

participants have the option to indicate that any of the nine factors are not applicable.

The primary dependent variable, FACTORS, is calculated by averaging each

participant’s responses regarding whether each factor indicates business/hobby. The

resulting variable forms a scale ranging from 1 (all factors definitely support hobby) to 6

(all factors definitely support business).14 Advocacy bias is indicated if advocacy

attitudes are related to evidence evaluation. Thus, if participants’ responses to the client

advocacy scale predicts FACTORS (i.e., evidence evaluation), this is evidence of

advocacy bias. As alternative dependent variables, the study also includes measures of

how aggressive the participants’ judgments are. Specifically, I measure participants’

likelihood of recommending business (LIKELY) and assessment of the likelihood the

Tax Court would uphold business treatment (TAXCOURT).

3.5 Accountability

Because tax professionals likely feel accountable to multiple sources, I develop a

scale measuring accountability to the client, firm, and IRS.15 The scale includes 12 items

modified from the scales of Frink and Ferris (1998) and Frink and Klimoski (1998), and

selected items from Donnelly (2017). Specifically, participants respond to items about

perceived accountability, perceived reputation effects, potential future consequences, and

pressure to agree with the client, the firm, and the IRS (See Table 3.3, Panel A for a list

of items). Factor analysis results indicate the items load onto three distinct factors. One

14 I use an average, rather than a sum or factor scores, because factors that are considered “not applicable” are excluded from the calculation of FACTORS for each participant. By averaging responses, the omission of factors for only some participants does not impede comparability. 15 The study’s formal hypotheses focus on accountability to the client and to the firm, but tax professionals may also feel accountable to the IRS. As shown in Table 3, Panel C, accountability to the IRS did not vary by role. However, participants did feel similarly accountable to the IRS as they did to the client and the firm. Accountability to the IRS did not influence their evidence evaluation or conclusions.

25

item, “I felt pressure to make a decision consistent with what the IRS would allow,”

cross-loaded with items related to both the Firm and the IRS. Another item, “I felt

pressure to make a decision consistent with the Roes’ preferences,” cross-loaded with

items related to all three accountability sources (e.g., firm, client, and IRS). Thus, I form

three scales with the remaining items. Accountability to the firm (ACCT_F) includes four

items with a Cronbach’s alpha of 0.775. Accountability to the client (ACCT_C) includes

three items with a Cronbach’s alpha of 0.739. Finally, accountability to the IRS

(ACCT_I) includes three items with a Cronbach’s alpha of 0.752. Mean responses to

each of the three scales are presented in Table 3.3, Panel B and construct correlations are

displayed in Table 3.3, Panel C. Construct correlations (e.g., correlations among the types

of accountability) were all below 0.48, which indicates discriminant validity because

construct correlation is < 0.85 (Klein 2005, 73). All participants, regardless of role, report

feelings of accountability that are not different from the midpoint of the scale (all p >

0.2), indicating participants felt similar levels of moderate accountability to all three

sources.

3.6 Additional Measures

Participants respond to a client advocacy (CA) scale (Bobek et al. 2010; Mason

and Levy 2000), which includes nine items measuring a professional’s attitude towards

his or her attitudes toward the client (See Appendix 1). Next, reviewers (preparers) rate

the hypothetical preparer’s (reviewer’s) competence and client advocacy. Preparers

received very little information about the reviewer, but I include these items to (1) control

26

for any differences in participants’ assumptions about the reviewer’s competence and/or

advocacy and (2) maintain similar time commitment across conditions.16

Next, participants answer three manipulation and attention check items about (1)

the client’s preferred outcome, (2) the role they held during the study (reviewer or

preparer), and (3) which outcome the preparer recommended (reviewers only). Finally,

participants respond to items about the perceived risk preferences of (1) the Roes (the

client) and (2) Oliver and Associates (the firm). Post-experimental questions include

demographic variables and measures of participants’ perceptions of the task. Specifically,

participants indicate which outcome they thought the partner expected, how hard they

worked to complete the task, and how motivated they were to do well. Finally,

participants respond to a scale measuring professional skepticism to control for

differences in participants’ natural levels of skeptical behavior. Bobek, Hageman, and

Radtke (2014) find the five-item questioning mind subscale has the highest correlation

with the full 30-item professional skepticism scale of Hurtt (2010). For brevity, I follow

Bobek et al. (2014) and use the subscale as a measure of professional skepticism.17

16 Preparers’ evidence evaluation (FACTORS) was not significantly influenced by their perceptions of the reviewers’ advocacy attitudes (p = 0.672). Further, time spent on the task did not vary by condition (p = 0.736) or role (p = 0.663). 17 Professional skepticism was not significantly different by ROLE (p = 0.445) and did not influence evaluation of evidence (FACTORS) (p = 0.742). However, professional skepticism did significantly influence likelihood of recommending business treatment (p = 0.054), such that increased professional skepticism led to increased likelihood of business treatment. However, this effect is moderated by role (p = 0.089), such that reviewers with increased professional skepticism were not more likely to indicate business treatment. In addition, professional skepticism is also significantly related to accountability to the client (p = 0.002), firm (p = 0.029), and IRS (p = 0.002), such that increased professional skepticism is related to increased accountability to all three sources. This suggests that the questioning mind construct measured by the professional skepticism subscale may influence both (1) aggressiveness and (2) accountability. Interestingly, this study does not find evidence that professional skepticism influences the effect of advocacy on evidence evaluation (p = 0.209). Future research should further examine the effect of professional skepticism on both aggressiveness and accountability among tax professionals.

27

Table 3.1: Demographic Characteristics

Average Age 35 Average Months of Work Experience 104.91 Gender Male. 37.33% Do not wish to respond. 1.33%

Education Bachelor's in Business (including Accounting or Finance) 78.67% Bachelor's in another area 8.00% Master's in Accounting, Taxation, or Business 41.33% Master’s in Another Area 9.3% Juris Doctorate 2.67% Certifications CPA 73.33% CMA OR CIA 10.67% EA 4.00% None 18.67% How would you classify your firm? Big 4 16.00% International (Other than the Big 4) 6.67% National 16.00% Regional 26.67% Local 34.67%

Current Title Partner/Director. 10.67% Manager/Senior Manager. 44.00% Senior. 26.67% Staff. 18.60%

How familiar are you with Section 183 hobby loss rules? Mean (where 1 = Very Unfamiliar and 7 = Very Familiar) 4.12 (Range 1-6,

Standard Deviation 1.139)

Have you ever researched a hobby loss issue for a client? Yes, many times. 24.00% Yes, once or twice. 44.00% No. 32.00%

Experience Reviewing Others Less than 1 year. 18.67% 1 - 2 years. 24.00% 3 years or more. 50.67% No experience. 6.67%

Currently act as preparer on some engagements Yes. 86.67% No. 13.33%

28

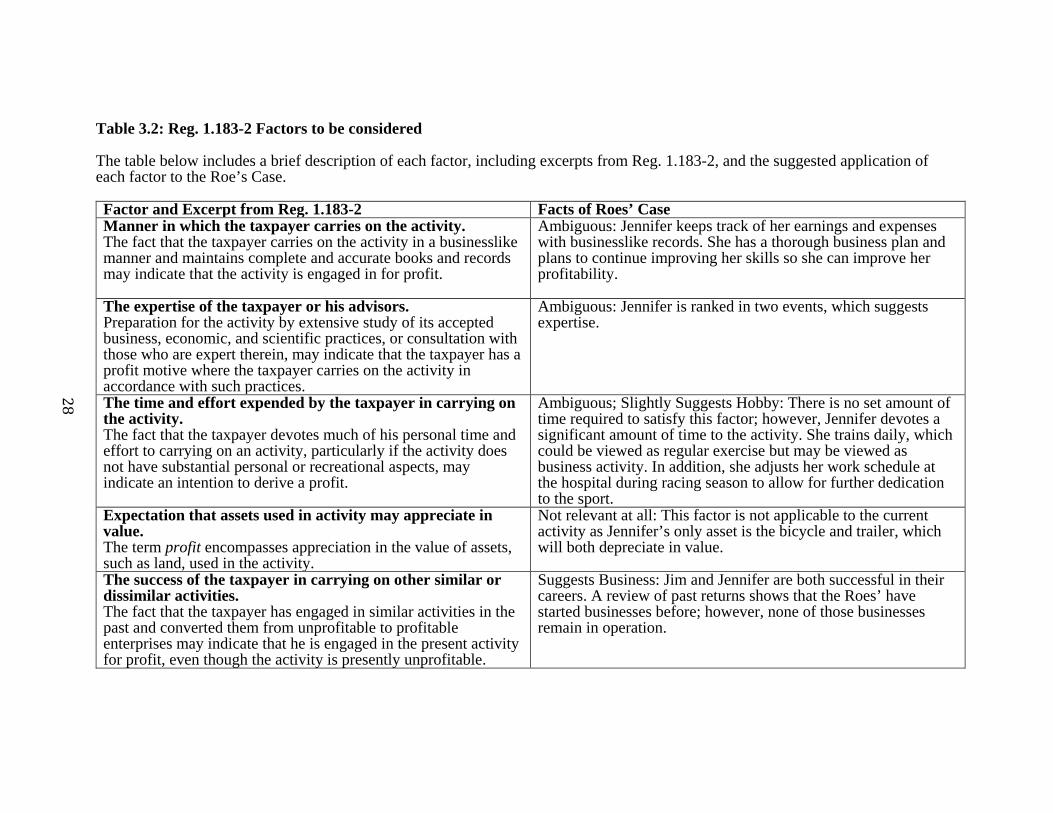

Table 3.2: Reg. 1.183-2 Factors to be considered The table below includes a brief description of each factor, including excerpts from Reg. 1.183-2, and the suggested application of each factor to the Roe’s Case.

Factor and Excerpt from Reg. 1.183-2 Facts of Roes’ Case Manner in which the taxpayer carries on the activity. The fact that the taxpayer carries on the activity in a businesslike manner and maintains complete and accurate books and records may indicate that the activity is engaged in for profit.

Ambiguous: Jennifer keeps track of her earnings and expenses with businesslike records. She has a thorough business plan and plans to continue improving her skills so she can improve her profitability.

The expertise of the taxpayer or his advisors. Preparation for the activity by extensive study of its accepted business, economic, and scientific practices, or consultation with those who are expert therein, may indicate that the taxpayer has a profit motive where the taxpayer carries on the activity in accordance with such practices.

Ambiguous: Jennifer is ranked in two events, which suggests expertise.

The time and effort expended by the taxpayer in carrying on the activity. The fact that the taxpayer devotes much of his personal time and effort to carrying on an activity, particularly if the activity does not have substantial personal or recreational aspects, may indicate an intention to derive a profit.

Ambiguous; Slightly Suggests Hobby: There is no set amount of time required to satisfy this factor; however, Jennifer devotes a significant amount of time to the activity. She trains daily, which could be viewed as regular exercise but may be viewed as business activity. In addition, she adjusts her work schedule at the hospital during racing season to allow for further dedication to the sport.

Expectation that assets used in activity may appreciate in value. The term profit encompasses appreciation in the value of assets, such as land, used in the activity.

Not relevant at all: This factor is not applicable to the current activity as Jennifer’s only asset is the bicycle and trailer, which will both depreciate in value.

The success of the taxpayer in carrying on other similar or dissimilar activities. The fact that the taxpayer has engaged in similar activities in the past and converted them from unprofitable to profitable enterprises may indicate that he is engaged in the present activity for profit, even though the activity is presently unprofitable.

Suggests Business: Jim and Jennifer are both successful in their careers. A review of past returns shows that the Roes’ have started businesses before; however, none of those businesses remain in operation.

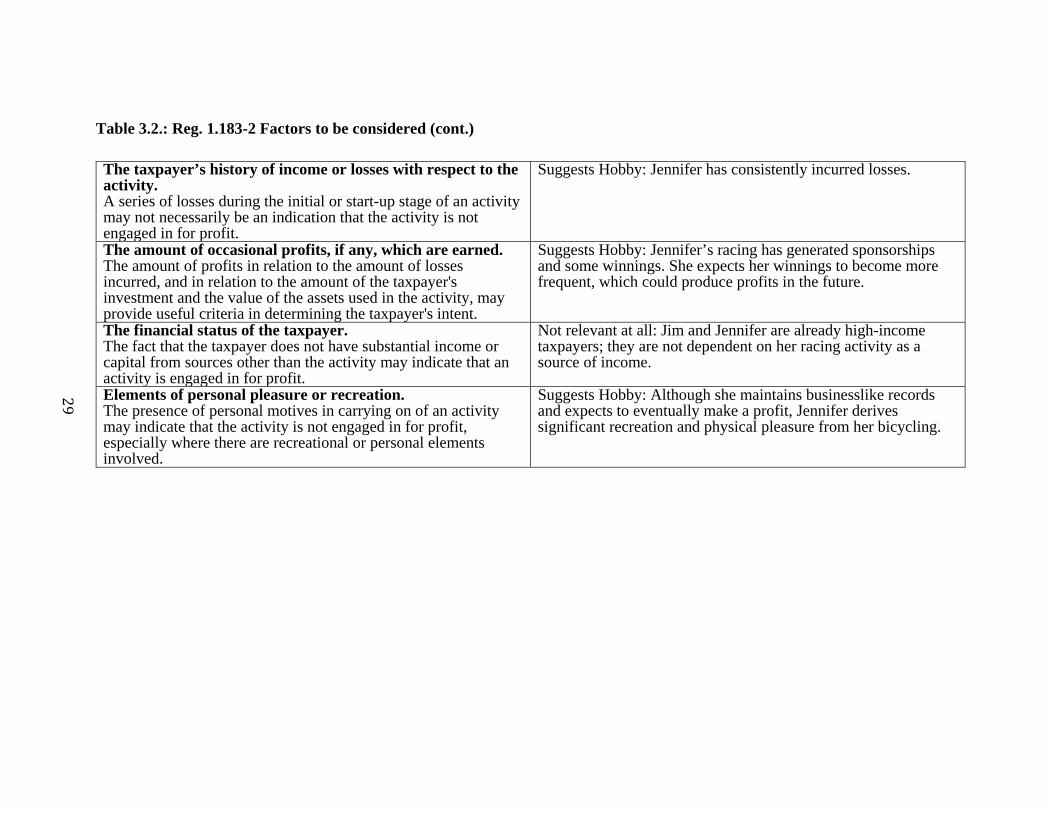

29

Table 3.2.: Reg. 1.183-2 Factors to be considered (cont.)

The taxpayer’s history of income or losses with respect to the activity. A series of losses during the initial or start-up stage of an activity may not necessarily be an indication that the activity is not engaged in for profit.

Suggests Hobby: Jennifer has consistently incurred losses.

The amount of occasional profits, if any, which are earned. The amount of profits in relation to the amount of losses incurred, and in relation to the amount of the taxpayer's investment and the value of the assets used in the activity, may provide useful criteria in determining the taxpayer's intent.

Suggests Hobby: Jennifer’s racing has generated sponsorships and some winnings. She expects her winnings to become more frequent, which could produce profits in the future.

The financial status of the taxpayer. The fact that the taxpayer does not have substantial income or capital from sources other than the activity may indicate that an activity is engaged in for profit.

Not relevant at all: Jim and Jennifer are already high-income taxpayers; they are not dependent on her racing activity as a source of income.

Elements of personal pleasure or recreation. The presence of personal motives in carrying on of an activity may indicate that the activity is not engaged in for profit, especially where there are recreational or personal elements involved.

Suggests Hobby: Although she maintains businesslike records and expects to eventually make a profit, Jennifer derives significant recreation and physical pleasure from her bicycling.

30

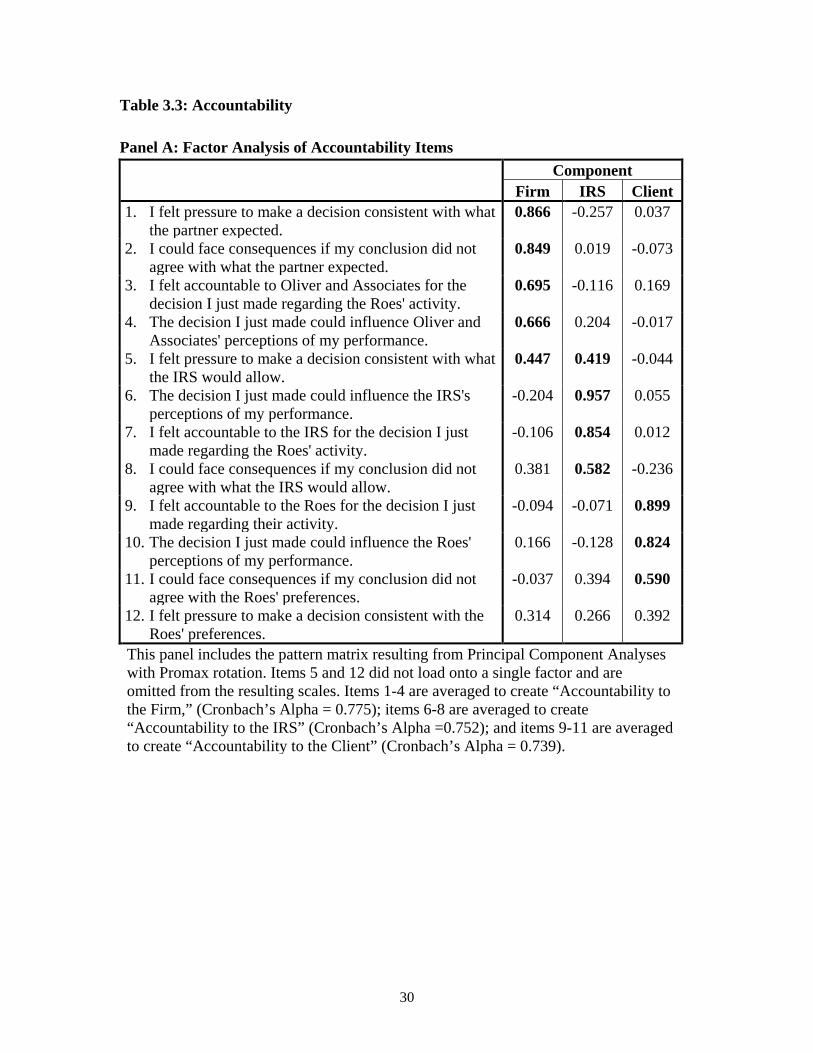

Table 3.3: Accountability

Panel A: Factor Analysis of Accountability Items

Component

Firm IRS Client 1. I felt pressure to make a decision consistent with what

the partner expected. 0.866 -0.257 0.037

2. I could face consequences if my conclusion did not agree with what the partner expected.

0.849 0.019 -0.073

3. I felt accountable to Oliver and Associates for the decision I just made regarding the Roes' activity.

0.695 -0.116 0.169

4. The decision I just made could influence Oliver and Associates' perceptions of my performance.

0.666 0.204 -0.017

5. I felt pressure to make a decision consistent with what the IRS would allow.

0.447 0.419 -0.044

6. The decision I just made could influence the IRS's perceptions of my performance.

-0.204 0.957 0.055

7. I felt accountable to the IRS for the decision I just made regarding the Roes' activity.

-0.106 0.854 0.012

8. I could face consequences if my conclusion did not agree with what the IRS would allow.

0.381 0.582 -0.236

9. I felt accountable to the Roes for the decision I just made regarding their activity.

-0.094 -0.071 0.899

10. The decision I just made could influence the Roes' perceptions of my performance.

0.166 -0.128 0.824

11. I could face consequences if my conclusion did not agree with the Roes' preferences.

-0.037 0.394 0.590

12. I felt pressure to make a decision consistent with the Roes' preferences.

0.314 0.266 0.392

This panel includes the pattern matrix resulting from Principal Component Analyses with Promax rotation. Items 5 and 12 did not load onto a single factor and are omitted from the resulting scales. Items 1-4 are averaged to create “Accountability to the Firm,” (Cronbach’s Alpha = 0.775); items 6-8 are averaged to create “Accountability to the IRS” (Cronbach’s Alpha =0.752); and items 9-11 are averaged to create “Accountability to the Client” (Cronbach’s Alpha = 0.739).

31

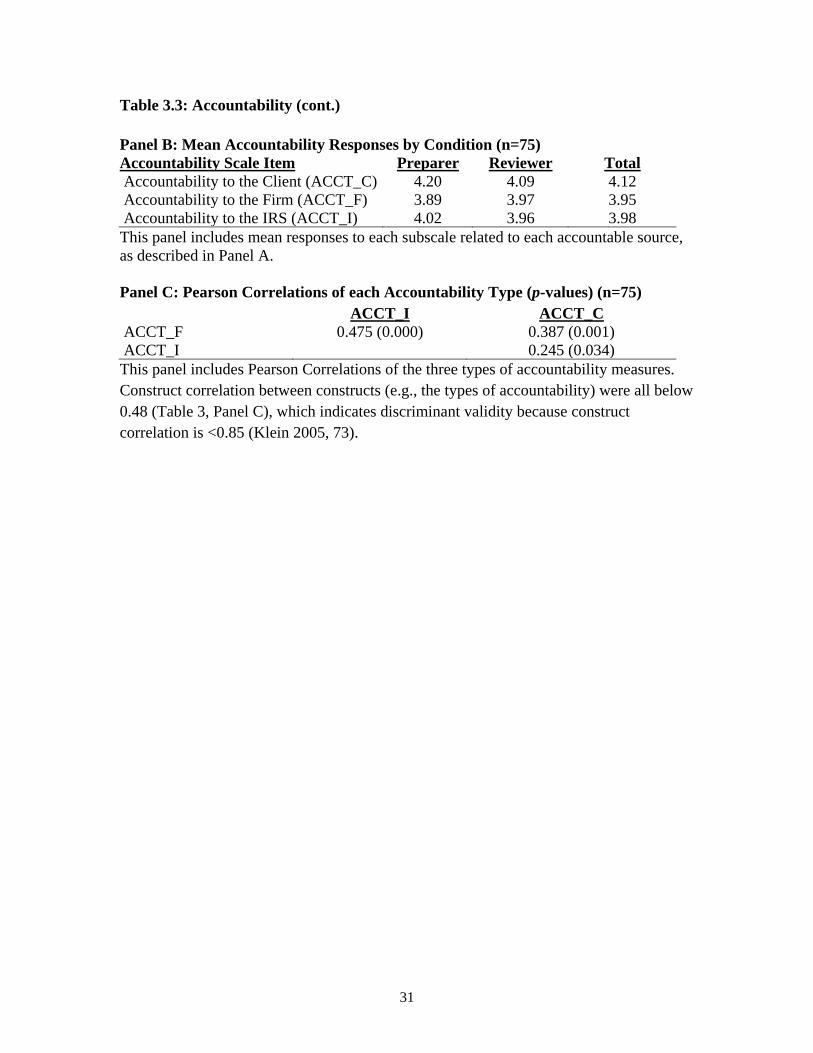

Table 3.3: Accountability (cont.) Panel B: Mean Accountability Responses by Condition (n=75) Accountability Scale Item Preparer Reviewer Total Accountability to the Client (ACCT_C) 4.20 4.09 4.12 Accountability to the Firm (ACCT_F) 3.89 3.97 3.95 Accountability to the IRS (ACCT_I) 4.02 3.96 3.98 This panel includes mean responses to each subscale related to each accountable source, as described in Panel A. Panel C: Pearson Correlations of each Accountability Type (p-values) (n=75)

ACCT_I ACCT_C ACCT_F 0.475 (0.000) 0.387 (0.001) ACCT_I 0.245 (0.034) This panel includes Pearson Correlations of the three types of accountability measures. Construct correlation between constructs (e.g., the types of accountability) were all below 0.48 (Table 3, Panel C), which indicates discriminant validity because construct correlation is <0.85 (Klein 2005, 73).

32

CHAPTER 4

RESULTS

4.1 Manipulation Checks

This study manipulates role by assigning participants to act as either a preparer or

reviewer on a tax research task. To confirm this manipulation, participants are asked

which role they were assigned in the study. All seventy-five participants correctly

responded to the manipulation check with the appropriate role. The study also

manipulates the presence of a preparer conclusion, which is confirmed by asking

participants in the reviewer conditions which preparer conclusion was included in the

memo. Participants assigned to the reviewer_business condition are expected to respond

“treatment as a for-profit business.” 84 percent (21/25) of participants assigned to

reviewer_business correctly responded. In contrast, participants assigned to the

reviewer_omitted condition are expected to respond “the memo did not include a

conclusion.” Surprisingly, 12 (one) of these participants incorrectly responded that the

preparer concluded business (hobby) treatment. Thus, only 48 percent of participants

correctly responded. Overall, 66 percent passed the manipulation check. This suggests

participants may have inferred a conclusion based on the information provided despite its

purposeful omission. Results are not affected by whether the 17 participants who

incorrectly responded to the preparer conclusion manipulation check are included in

analysis. Thus, analyses reported include all 75 participants.

33

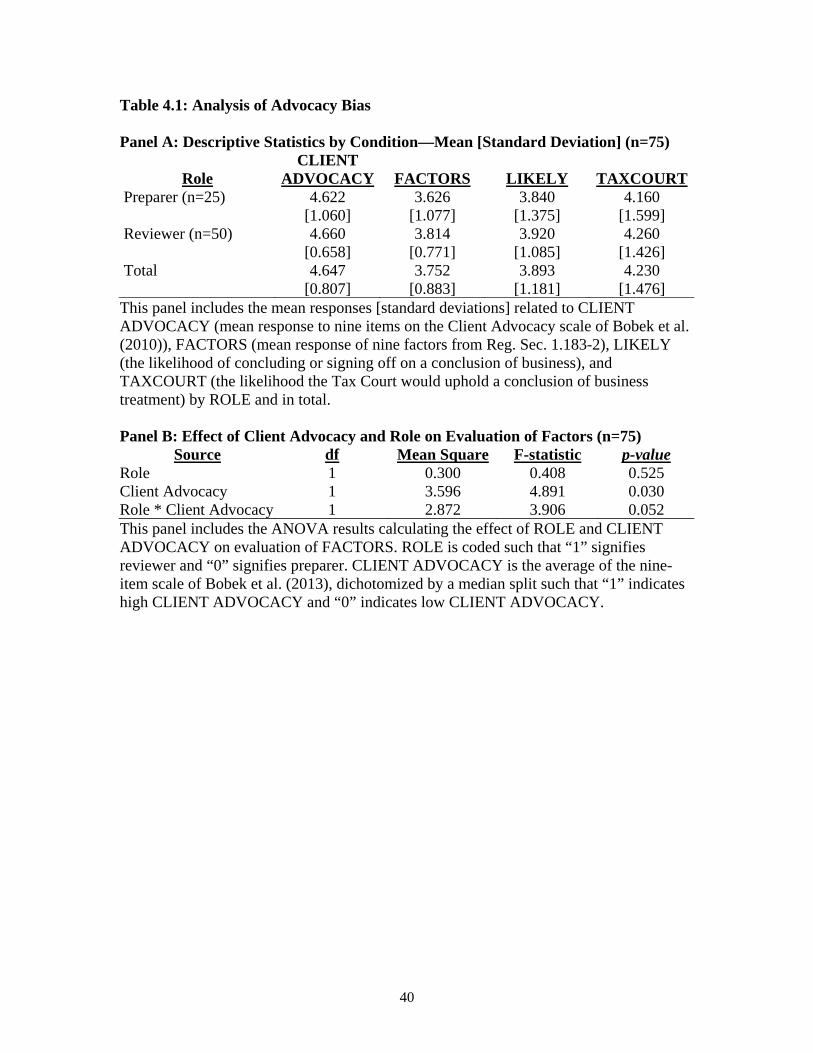

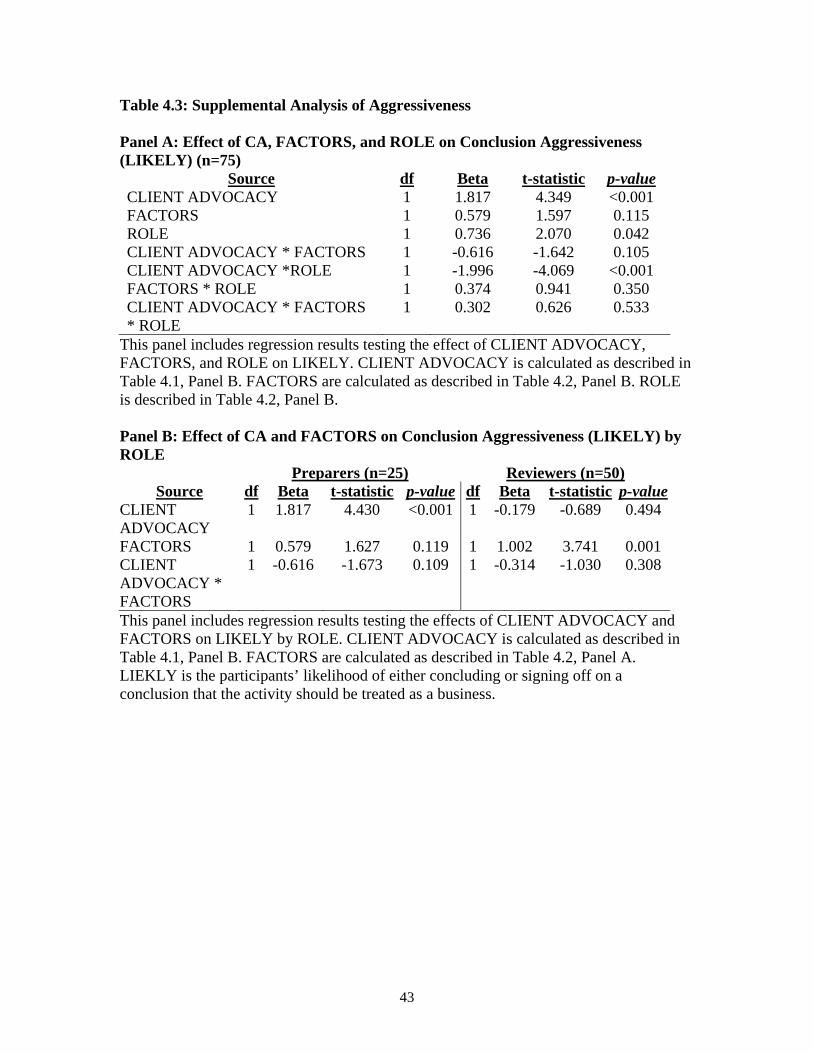

4.2 Analysis of Hypothesis 1

Hypothesis 1 predicts professionals occupying the reviewer role are less likely to

exhibit advocacy bias. To test H1, I first establish that participants exhibit advocacy bias

in their decisions which is indicated by a relationship between client advocacy (CA) and

evidence evaluation (FACTORS). Descriptive statistics of participants’ CA, FACTORS,

LIKELY, and TAXCOURT are included in Table 4.1, Panel A. None of the above-

mentioned variables are significantly different by role; however, results do indicate

advocacy bias. As shown in Table 4.1, Panel B, CA significantly influences FACTORS

(p = 0.03).18 In addition, the effect of CA on FACTORS is moderated by ROLE (p =

0.052). Additional untabulated analysis indicates the effect of CA on FACTORS is only

significant in the preparer condition, such that reviewers’ evidence evaluation is not

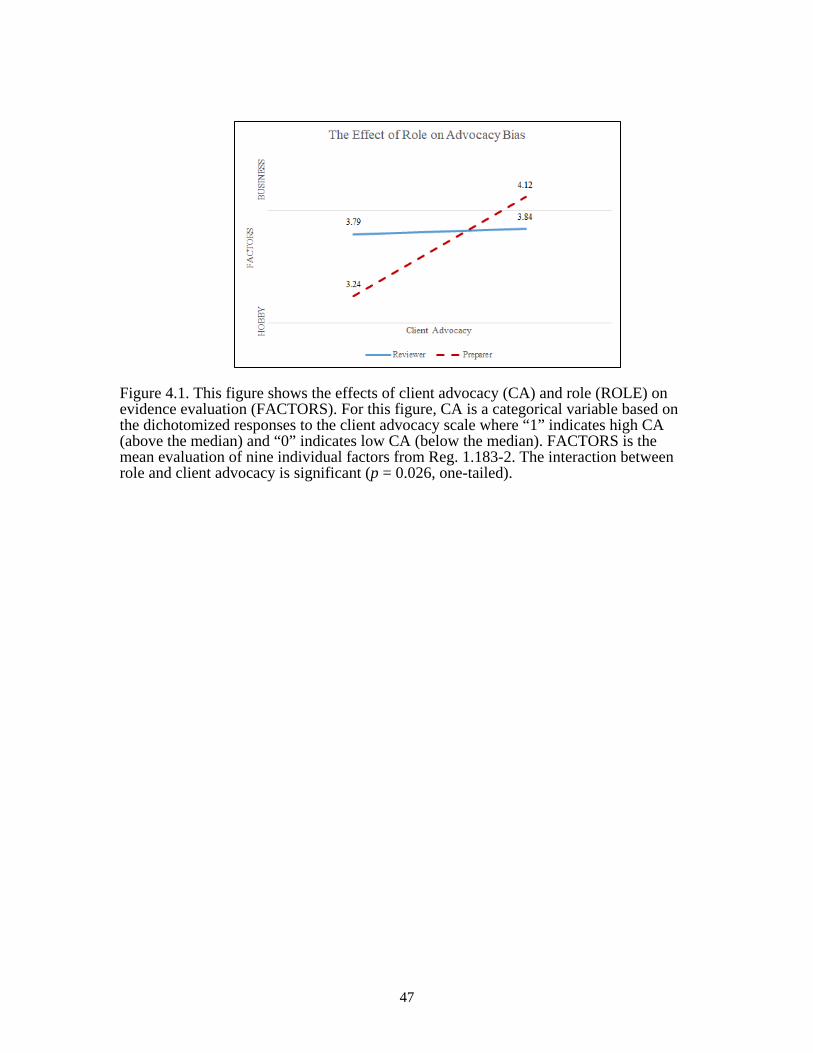

influenced by advocacy attitudes (p = 0.823). As illustrated in Figure 4.1, this finding

supports H1, providing initial evidence that occupying the reviewer role mitigates

advocacy bias.

4.3 Analysis of Hypothesis 2

Hypothesis two predicts occupying the reviewer role increases professionals’

accountability to the firm. I test H2 with a one-way ANOVA calculated on ACCT_F by

ROLE. As shown in Table 4.2, Panel A, results do not indicate ACCT_F is significantly

influenced by ROLE (p = 0.764).19 Thus, I conclude role did not influence perceived

accountability to the firm.

18 Due to low variance, results are not significant when using a continuous measure of CA. Thus, I perform a median split to classify participants into two groups where “1” indicates high advocacy attitudes (mean CA = 5.3025, std dev. = 0.42713) and “0” indicates low advocacy attitudes (mean CA = 4.0427, std dev. = 0.56519). All reported analyses use this dichotomous variable. 19 This is surprising, given the increased expectation of providing feedback identified by Barrick, et al. (2004); however, this result may be partly driven by the preparers’ unexpected perception of needing to provide “feedback to others on the engagement team regarding their work.” Additional analysis indicates

34

4.4 Analysis of Research Question

The research question investigates whether occupying the reviewer role

influences professionals’ accountability to the client. To test the RQ, I use a one-way

ANOVA calculated on ACCT_C by ROLE. Results indicate ROLE does not influence

ACCT_C (p = 0.634, Table 4.2, Panel A). Thus, I do not find evidence that occupying the

reviewer role affects professionals’ accountability to the client.

4.5 Analysis of H3a: Accountability to the Firm

H3a predicts ACCT_F reduces the likelihood of advocacy bias (the relationship

between CA and FACTORS). To test H3a, I regress ACCT_F and CA on FACTORS to

examine whether ACCT_F decreases the likelihood CA influences evidence evaluation.

Specifically, I examine whether the interaction of ACCT_F and CA is a significant

predictor of FACTORS in equation 1 below.

FACTORS = β1 ACCT_F + β2 CA + β3 ACCT_F * CA. (1) Regression results support a relationship between accountability and advocacy

bias if β3 is significant. As shown in Table 4.2, Panel B, the interaction between ACCT_F

and CA is not significant (p = 0.254), which indicates ACCT_F does not influence the

likelihood of advocacy bias. Thus, H3a is not supported and I find no evidence that

accountability to the firm, as measured in this study, influences the likelihood of

advocacy bias.

4.6 Analysis of H3b: Accountability to the Client

H3b predicts ACCT_C increases the likelihood of advocacy bias. To test H3b, I

regress ACCT_C and CA on FACTORS in equation 2 below to examine whether

participants’ perceptions of the importance of a feedback expectation did not differ by role (p = 0.505, untabulated).

35

accountability to the client increases the likelihood that advocacy attitudes influence

evidence evaluation.

FACTORS = β1 ACCT_C + β2 CA + β3 ACCT_C*CA. (2) Regression results support a relationship between accountability and advocacy

bias if β3 is significant. As shown in Table 4.2, Panel C, ACCT_C significantly influences

the effect of CA on FACTORS (b = -0.399, p = 0.064); thus, ACCT_C appears to

mitigate bias in the evaluation of evidence. Although an interesting finding, this does not

support H3b because H3b predicted ACCT_C would increase advocacy bias and findings

indicate a decrease in advocacy bias. Regardless, this finding suggests accountability to

the client leads professionals to be more objective and provides an unexpected initial

insight into the effect of accountability on tax professional advocacy bias.

4.7 The Interaction of Accountability and Role

Although not formally predicted, I expect accountability and role to jointly

influence the effects of advocacy attitudes on evidence evaluation (See Figure 2.1). H1

examines the effect of ROLE on the likelihood of advocacy bias; H2 examines the effect

of ROLE on accountability; and H3a and H3b examine the effect of accountability to the

firm and accountability to the client, respectively, on the likelihood of advocacy bias. As

supplemental analysis, I also examine the effects of ROLE and ACCT_F/ACCT_C on

likelihood of advocacy bias in a more comprehensive test of the model. Specifically, I

regress ACCT_F (ACCT_C), ROLE, and CA on FACTORS as shown in equations 3 (4),

below.

FACTORS = β1 ACCT_F + β2 CA + β3 Role + β4 ACCT_F*CA (3) + β5 ACCT_F*Role + β6 CA*Role + β7 ACCT_F*CA*Role.

36

FACTORS = β1 ACCT_C + β2 CA + β3 Role + β4 ACCT_C*CA (4) + β5 ACCT_C*Role + β6 CA*Role + β7 ACCT_C*CA*Role. As shown in Table 4.2, Panel D, I do not find evidence that ACCT_F influences

the likelihood of advocacy bias (p = 0.505). Given the findings in H1 that the reviewer

role reduces the likelihood of advocacy bias, I also test for a moderating effect of role. I

do not find that ROLE influences the relationship between ACCT_F and FACTORS.