Mllma Research Repor Prepared by: Adra Allo Crsa Aom Paul Eres Beaa Golembecka Marc Krzkosk Aa Mazera Olexader Ou January 2010 Prae Peso Ssems Ceral ad Easer Europe

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 1/68

M ll ma Research Repor

Prepared by:

Adr a AlloCr s a A omPaul Er esBea a Golemb eckaMarc Krz ko skA a MazeraOlexa der O u

January 2010

Pr a e Pe s o S s ems Ce ral a d Eas er Europe

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 2/68

Milliman, whose corporate offices arein Seattle, serves the full spectrum ofbusiness, financial, government, andunion organizations. Founded in 1947 asMilliman & Robertson, the company has52 offices in principal cities in the UnitedStates and worldwide. Milliman employsmore than 2,400 people, including aprofessional staff of more than 1,100qualified consultants and actuaries. Thefirm has consulting practices in employeebenefits, healthcare, life insurance/financial services, and property andcasualty insurance. Milliman’s employeebenefits practice is a member of AbelicaGlobal, an international organization of

independent consulting firms servingclients around the globe. For furtherinformation visit www.milliman.com.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 3/68

M ll ma Research Repor

Table of ConTenTs

SCOPE 2

OvERviEw Of PRivAtE PEnSiOn SyStEMS 3Ma da or Pe s o s 3

Scheme Me r cs 3Charg g S ruc ures 4i es me Op o s 6Prude al Super s o 7Compe e La dscape 8Co r bu o Ra es 9

volu ar Pe s o s 9Scheme Me r cs 9O her fea ures 10

PRivAtE PEnSiOn SyStEMS in SPECifiC MARKEtS 11

Pola d 11Summar o he S s em 11Ma da or Pe s o s 11volu ar Pe s o s 15Pe s o Compa es 17

Roma a 24Summar o he S s em 24Ma da or Pe s o s 24

volu ar Pe s o s 28Pe s o Compa es 30

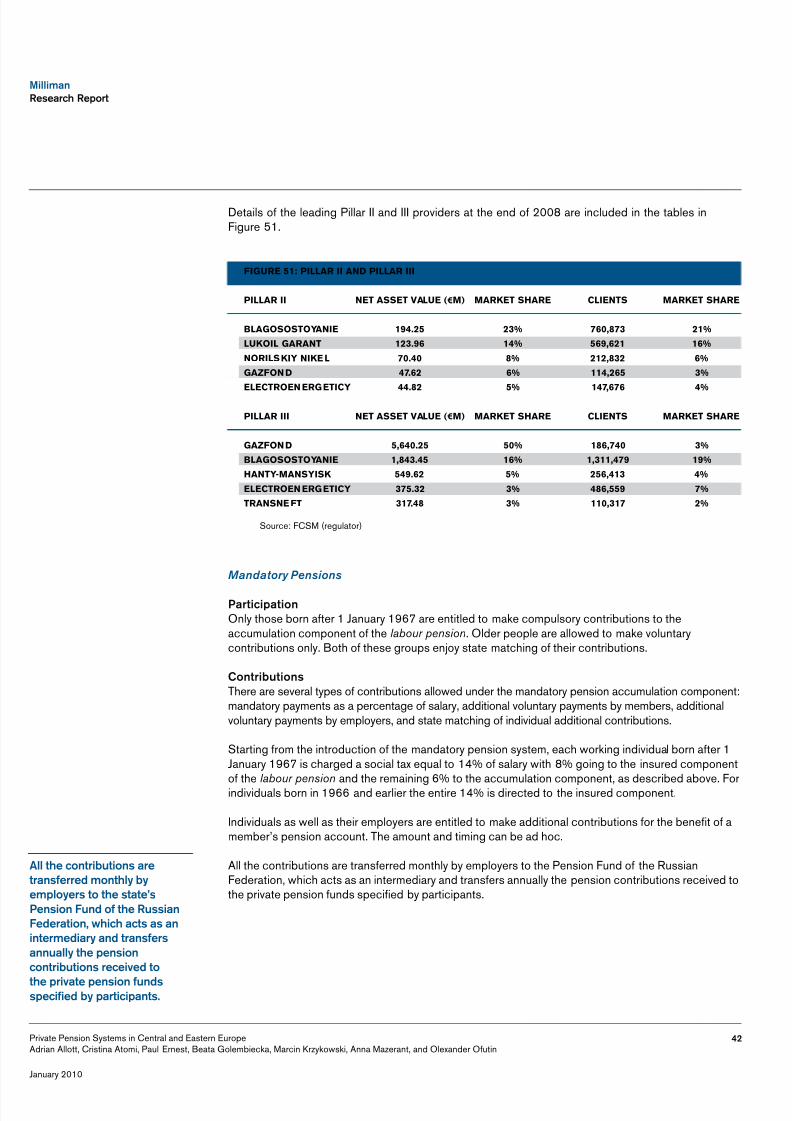

Russ a 41Summar o he S s em 41Ma da or Pe s o s 42volu ar Pe s o s 45

Hu gar 48Summar o he S s em 48Ma da or Pe s o s 48volu ar Pe s o s 52

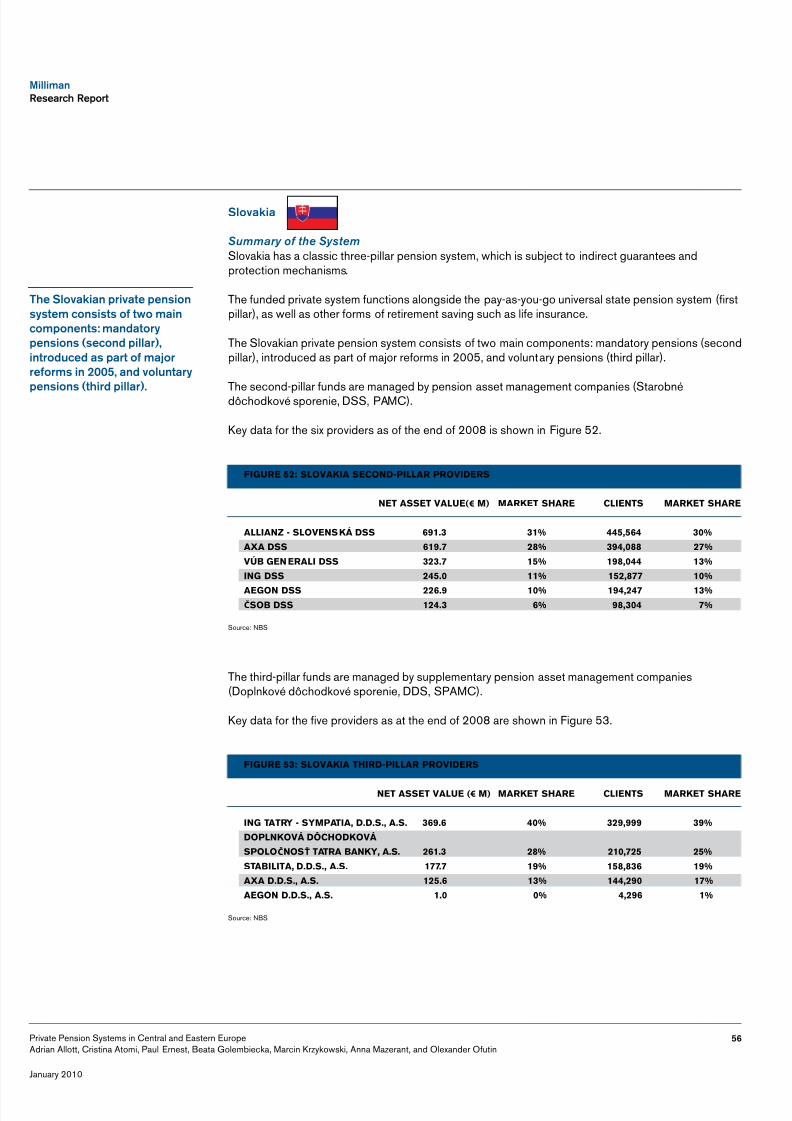

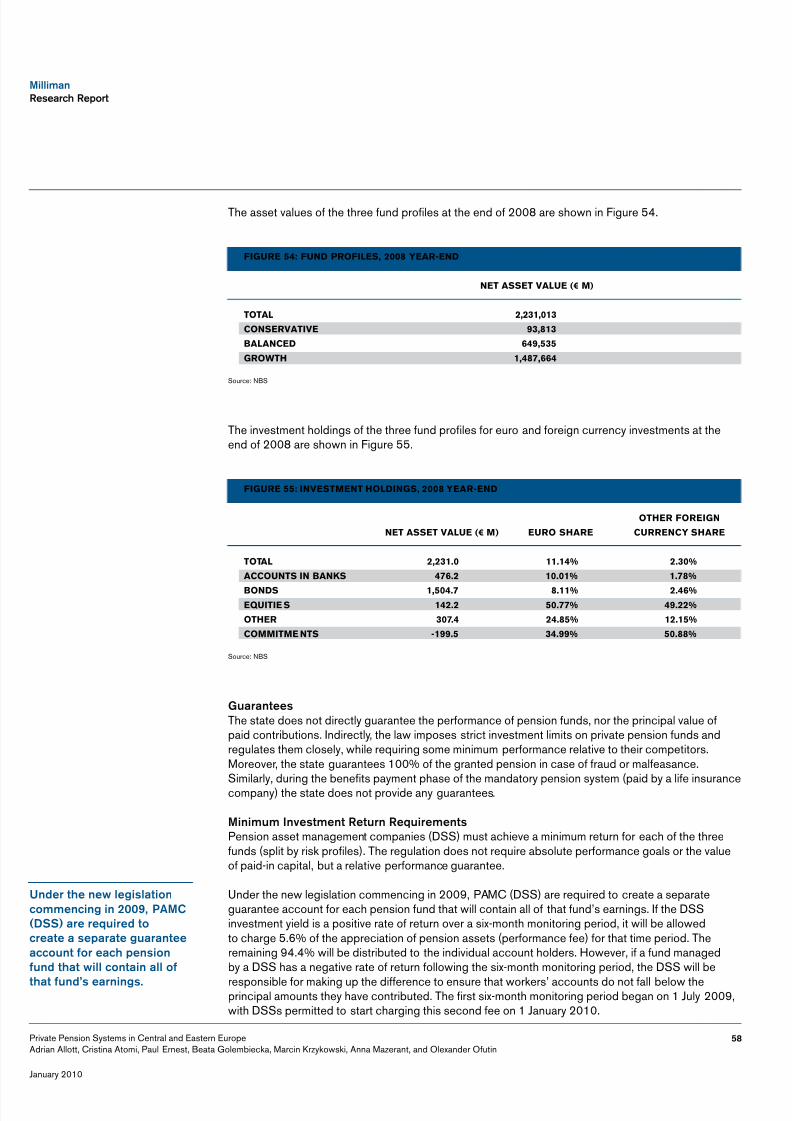

Slo ak a 56Summar o he S s em 56Ma da or Pe s o s 57volu ar Pe s o s 60

OvERviEw Of PRivAtE PEnSiOn SyStEMS in OtHER MARKEtS 62Czech Republ c 62Slo e a 62Croa a 62Serb a 63Bulgar a 63Es o a 63La a 64L hua a 64

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 4/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

2

January 2010

sCope

For more than two decades, the World Bank has been active in promoting a move away from totalreliance on pay-as-you-go public pension provision.

The Bank’s preferred model is a three-pillar pension environment in which a state pension (typicallyuniversal, pay-as-you-go) is supplemented by two defined contribution pension arrangements, onefunded by mandatory contributions from workers, and the other voluntary but tax-advantaged.

The original template for the funded pillars was the pension systems of Chile and other Latin Americancountries; however, the bank considered that their introduction would also be appropriate in theCentral and Eastern European region, given that state pension provision in those countries was

particularly weak and that they faced similar demographic changes to developed countries.Tentative reforms commenced in the mid 1990s in Hungary and the Czech Republic.

In 1998, Poland became the first country in the region to implement the full World Bank model; it hassubsequently been followed by a number of others.

Private pensions have grown strongly in most countries in Central and Eastern Europe (CEE)in recent years. Although the pension systems in the region face important challenges from thecurrent economic downturn, they continue to represent a significant growth opportunity for financialservices providers.

The purpose of this report is to help Milliman’s clients and partners gain a better understanding of thevariety and current state of funded pension systems in the region, a decade on from the Polish launch,and the opportunities and challenges facing pension providers in these countries.

We have restricted our study to five markets. These have been chosen to provide a representation ofthe diversity in the region. An overview of the private pension systems in the other major markets isincluded for comparison.

the purpose o h s repors o help M ll ma ’s cl e s

a d par ers ga a be eru ders a d g o he ar ea d curre s a e o u dedpe s o s s ems he reg o ,a decade o rom he Pol shlau ch, a d he oppor u esa d challe ges ac g pe s opro ders hese cou r es.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 5/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

3

overview of privaTe pension sysTems

Ma da or Pe s o s

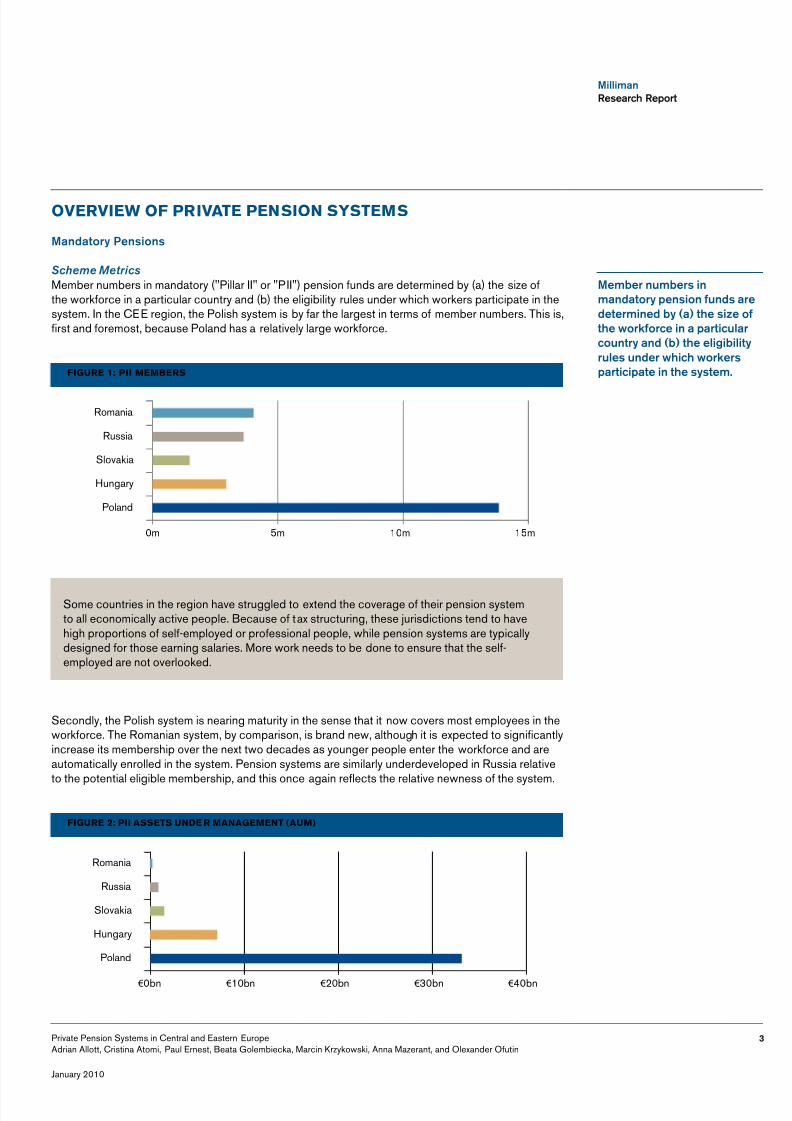

Scheme MetricsMember numbers in mandatory ("Pillar II" or "PII") pension funds are determined by (a) the size ofthe workforce in a particular country and (b) the eligibility rules under which workers participate in thesystem. In the CEE region, the Polish system is by far the largest in terms of member numbers. This is,first and foremost, because Poland has a relatively large workforce.

: pii membersfigure 1

0m 5m 10m 15m

Poland

Hungary

Slovakia

Russia

Romania

Secondly, the Polish system is nearing maturity in the sense that it now covers most employees in theworkforce. The Romanian system, by comparison, is brand new, although it is expected to significantlyincrease its membership over the next two decades as younger people enter the workforce and areautomatically enrolled in the system. Pension systems are similarly underdeveloped in Russia relative

to the potential eligible membership, and this once again reflects the relative newness of the system.

: pii asseTs unDe r managemenT (aum)figure 2

€ 0bn € 10bn € 20bn € 30bn € 40bn

Poland

Hungary

Slovakia

Russia

Romania

Some countries in the region have struggled to extend the coverage of their pension systemto all economically active people. Because of tax structuring, these jurisdictions tend to havehigh proportions of self-employed or professional people, while pension systems are typicallydesigned for those earning salaries. More work needs to be done to ensure that the self-employed are not overlooked.

Member umbers ma da or pe s o u ds arede erm ed b (a) he s ze o

he ork orce a par cularcou r a d (b) he el g b lrules u der h ch orkerspar c pa e he s s em.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 6/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

4

January 2010

Assets under management (AUM) are a function of (a) member numbers, (b) contribution rates, (c)charge rates, (d) investment returns, and (e) the age of the system. Once again, Poland is by far thelargest market in the region, benefitting from 10 years of accumulated contributions, high participantnumbers, and a relatively high contribution rate.

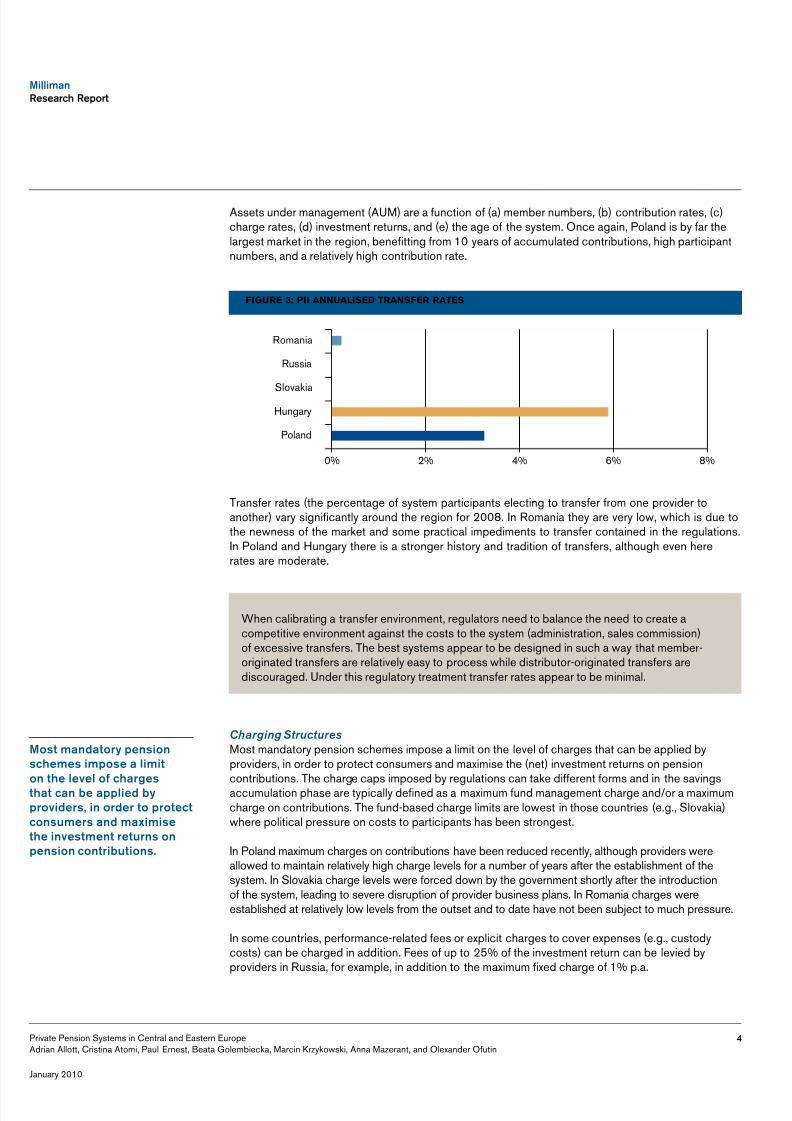

: pii annualiseD Transfer raTesfigure 3

0% 2% 4% 6% 8%

Poland

HungarySlovakia

Russia

Romania

Transfer rates (the percentage of system participants electing to transfer from one provider toanother) vary significantly around the region for 2008. In Romania they are very low, which is due tothe newness of the market and some practical impediments to transfer contained in the regulations.In Poland and Hungary there is a stronger history and tradition of transfers, although even hererates are moderate.

Charging StructuresMost mandatory pension schemes impose a limit on the level of charges that can be applied byproviders, in order to protect consumers and maximise the (net) investment returns on pension

contributions. The charge caps imposed by regulations can take different forms and in the savingsaccumulation phase are typically defined as a maximum fund management charge and/or a maximumcharge on contributions. The fund-based charge limits are lowest in those countries (e.g., Slovakia)where political pressure on costs to participants has been strongest.

In Poland maximum charges on contributions have been reduced recently, although providers wereallowed to maintain relatively high charge levels for a number of years after the establishment of thesystem. In Slovakia charge levels were forced down by the government shortly after the introductionof the system, leading to severe disruption of provider business plans. In Romania charges wereestablished at relatively low levels from the outset and to date have not been subject to much pressure.

In some countries, performance-related fees or explicit charges to cover expenses (e.g., custodycosts) can be charged in addition. Fees of up to 25% of the investment return can be levied byproviders in Russia, for example, in addition to the maximum fixed charge of 1% p.a.

When calibrating a transfer environment, regulators need to balance the need to create acompetitive environment against the costs to the system (administration, sales commission)of excessive transfers. The best systems appear to be designed in such a way that member-originated transfers are relatively easy to process while distributor-originated transfers arediscouraged. Under this regulatory treatment transfer rates appear to be minimal.

Mos ma da or pe s oschemes mpose a l m

o he le el o chargesha ca be appl ed bpro ders, order o pro ecco sumers a d max m se

he es me re ur s ope s o co r bu o s.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 7/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

5

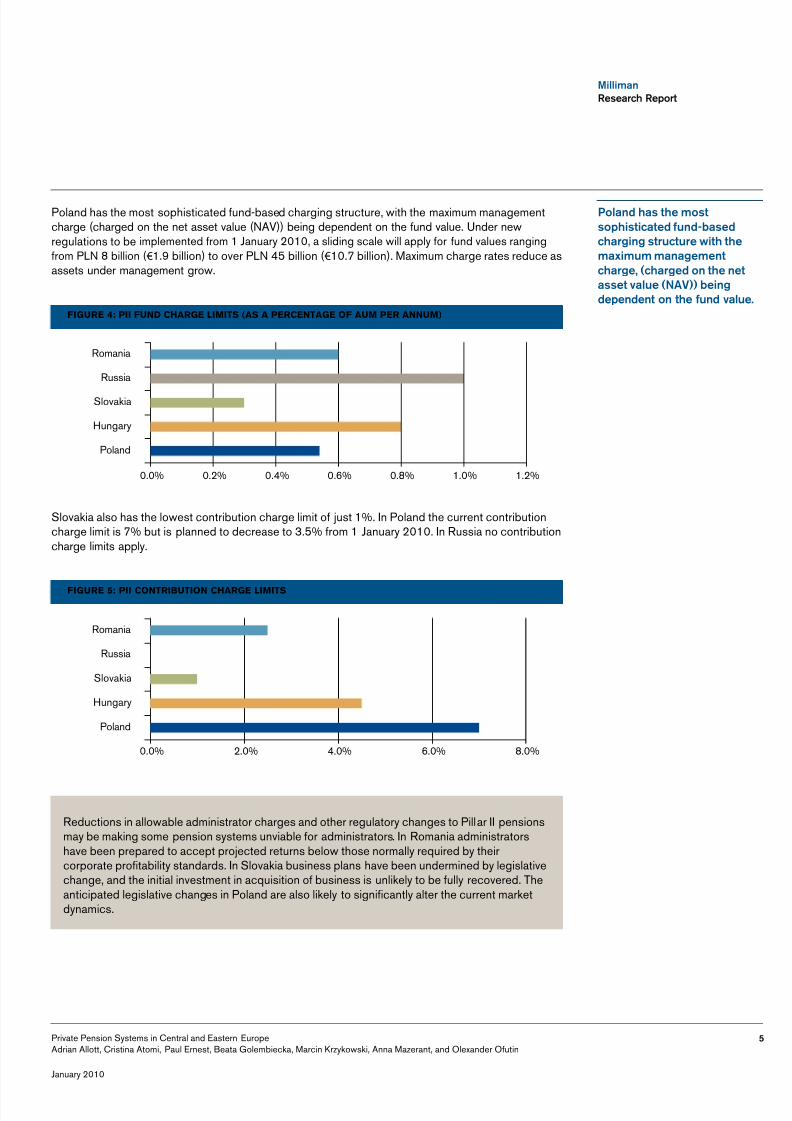

Poland has the most sophisticated fund-based charging structure, with the maximum managementcharge (charged on the net asset value (NAV)) being dependent on the fund value. Under newregulations to be implemented from 1 January 2010, a sliding scale will apply for fund values rangingfrom PLN 8 billion (€ 1.9 billion) to over PLN 45 billion (€ 10.7 billion). Maximum charge rates reduce asassets under management grow.

: pii funD Charge limiTs (as a perCenTage of aum per annum)figure 4

0.0% 0.2% 0.4% 0.6% 0.8% 1.0% 1.2%

Poland

Hungary

Slovakia

Russia

Romania

Slovakia also has the lowest contribution charge limit of just 1%. In Poland the current contributioncharge limit is 7% but is planned to decrease to 3.5% from 1 January 2010. In Russia no contributioncharge limits apply.

: pii ConTribuTion Charge limiTsfigure 5

0.0% 2.0% 4.0% 6.0% 8.0%

Poland

Hungary

Slovakia

Russia

Romania

Reductions in allowable administrator charges and other regulatory changes to Pillar II pensionsmay be making some pension systems unviable for administrators. In Romania administratorshave been prepared to accept projected returns below those normally required by theircorporate profitability standards. In Slovakia business plans have been undermined by legislativechange, and the initial investment in acquisition of business is unlikely to be fully recovered. Theanticipated legislative changes in Poland are also likely to significantly alter the current marketdynamics.

Pola d has he mossoph s ca ed u d-basedcharg g s ruc ure h hemax mum ma agemecharge, (charged o he easse alue (nAv)) be gdepe de o he u d alue.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 8/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

6

January 2010

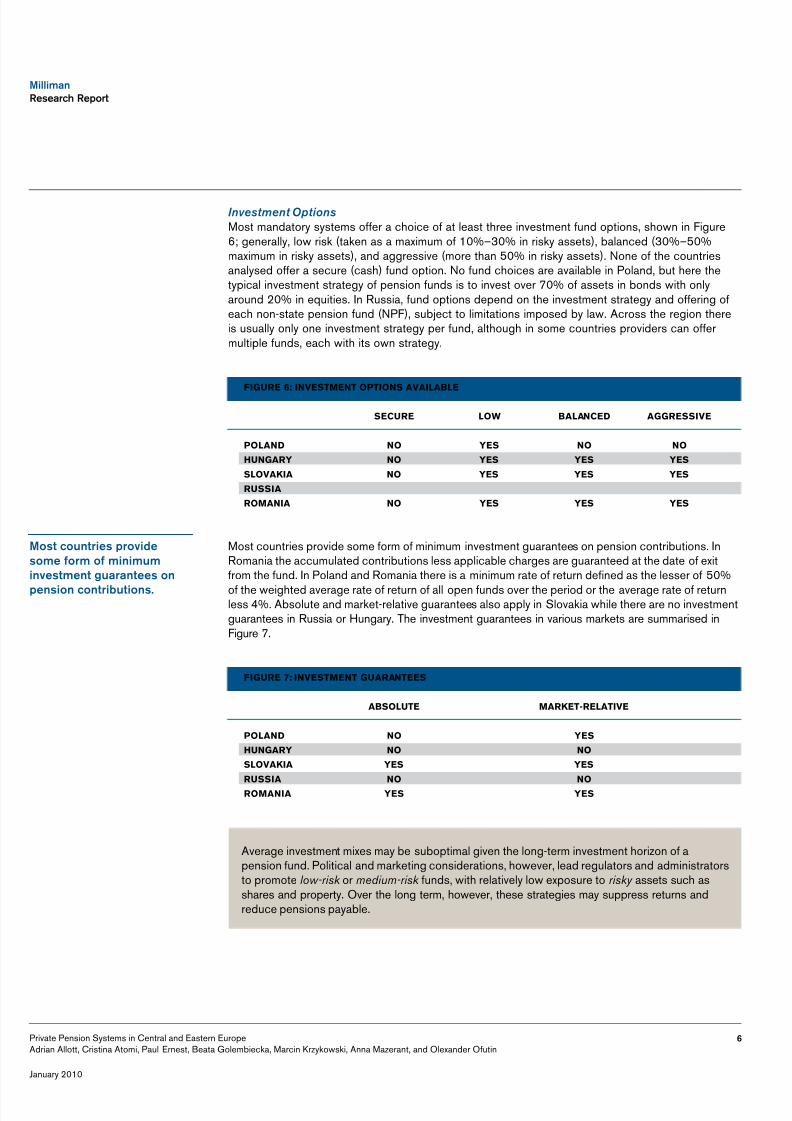

Investment OptionsMost mandatory systems offer a choice of at least three investment fund options, shown in Figure6; generally, low risk (taken as a maximum of 10%–30% in risky assets), balanced (30%–50%maximum in risky assets), and aggressive (more than 50% in risky assets). None of the countriesanalysed offer a secure (cash) fund option. No fund choices are available in Poland, but here thetypical investment strategy of pension funds is to invest over 70% of assets in bonds with onlyaround 20% in equities. In Russia, fund options depend on the investment strategy and offering ofeach non-state pension fund (NPF), subject to limitations imposed by law. Across the region thereis usually only one investment strategy per fund, although in some countries providers can offermultiple funds, each with its own strategy.

: invesTmenT opTions availablefigure 6

seCure low balanCeD aggressive

polanD no yes no nohungary no yes yes yesslovakia no yes yes yesrussiaromania no yes yes yes

Most countries provide some form of minimum investment guarantees on pension contributions. InRomania the accumulated contributions less applicable charges are guaranteed at the date of exitfrom the fund. In Poland and Romania there is a minimum rate of return defined as the lesser of 50%of the weighted average rate of return of all open funds over the period or the average rate of returnless 4%. Absolute and market-relative guarantees also apply in Slovakia while there are no investmentguarantees in Russia or Hungary. The investment guarantees in various markets are summarised inFigure 7.

: invesTmenT guaranTeesfigure 7

absoluTe markeT-relaTive

polanD no yeshungary no noslovakia yes yesrussia no noromania yes yes

Mos cou r es pro desome orm o m mum

es me guara ees o

pe s o co r bu o s.

Average investment mixes may be suboptimal given the long-term investment horizon of apension fund. Political and marketing considerations, however, lead regulators and administratorsto promote low-risk or medium-risk funds, with relatively low exposure to risky assets such asshares and property. Over the long term, however, these strategies may suppress returns andreduce pensions payable.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 9/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

7

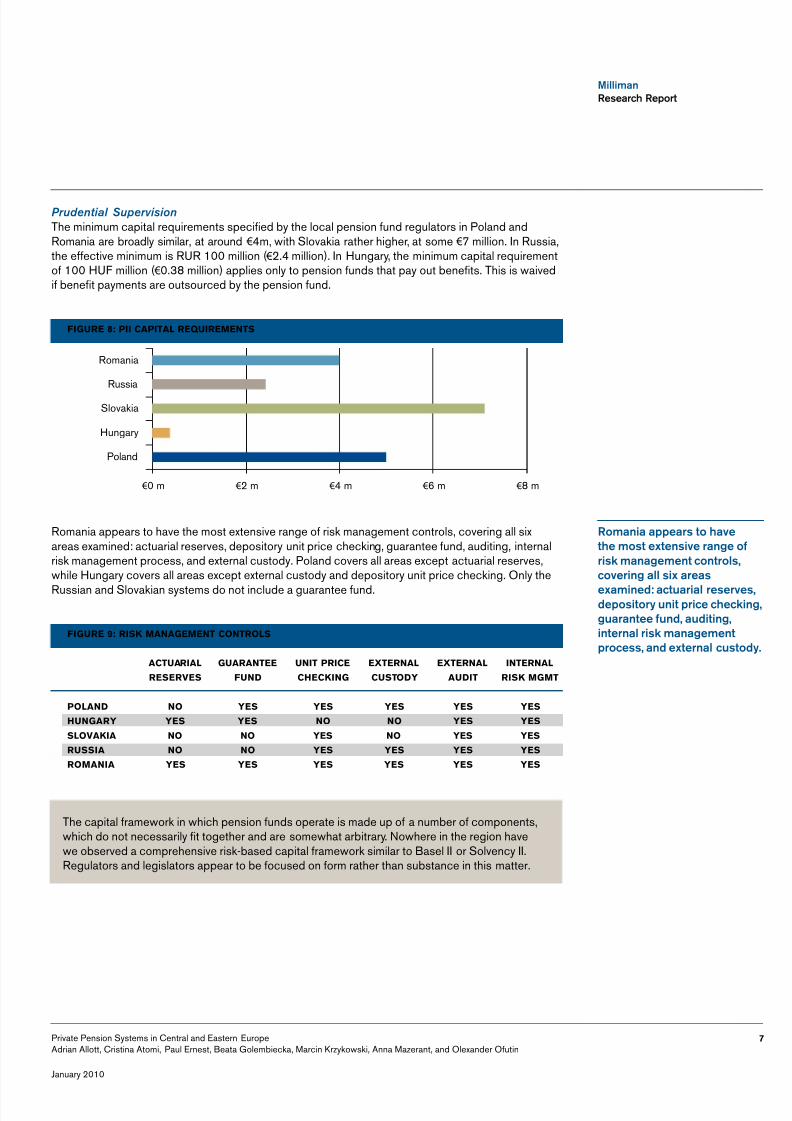

Prudential SupervisionThe minimum capital requirements specified by the local pension fund regulators in Poland andRomania are broadly similar, at around € 4m, with Slovakia rather higher, at some € 7 million. In Russia,the effective minimum is RUR 100 million ( € 2.4 million). In Hungary, the minimum capital requirementof 100 HUF million (€ 0.38 million) applies only to pension funds that pay out benefits. This is waivedif benefit payments are outsourced by the pension fund.

: pii CapiTal requiremenTsfigure 8

€ 0 m € 2 m € 4 m € 6 m € 8 m

Poland

Hungary

Slovakia

Russia

Romania

Romania appears to have the most extensive range of risk management controls, covering all sixareas examined: actuarial reserves, depository unit price checking, guarantee fund, auditing, internalrisk management process, and external custody. Poland covers all areas except actuarial reserves,while Hungary covers all areas except external custody and depository unit price checking. Only theRussian and Slovakian systems do not include a guarantee fund.

: risk managemenT ConTrolsfigure 9

aCTuarial guaranTee uniT priCe eXTernal eXTernal inTernalreserves funD CheCking CusToDy auDiT risk mgmT

polanD no yes yes yes yes yeshungary yes yes no no yes yesslovakia no no yes no yes yesrussia no no yes yes yes yesromania yes yes yes yes yes yes

Roma a appears o ha ehe mos ex e s e ra ge o

r sk ma ageme co rols,co er g all s x areas

exam ed: ac uar al reser es,depos or u pr ce check g,guara ee u d, aud g,

er al r sk ma agemeprocess, a d ex er al cus od .

The capital framework in which pension funds operate is made up of a number of components,which do not necessarily fit together and are somewhat arbitrary. Nowhere in the region havewe observed a comprehensive risk-based capital framework similar to Basel II or Solvency II.Regulators and legislators appear to be focused on form rather than substance in this matter.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 10/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

8

January 2010

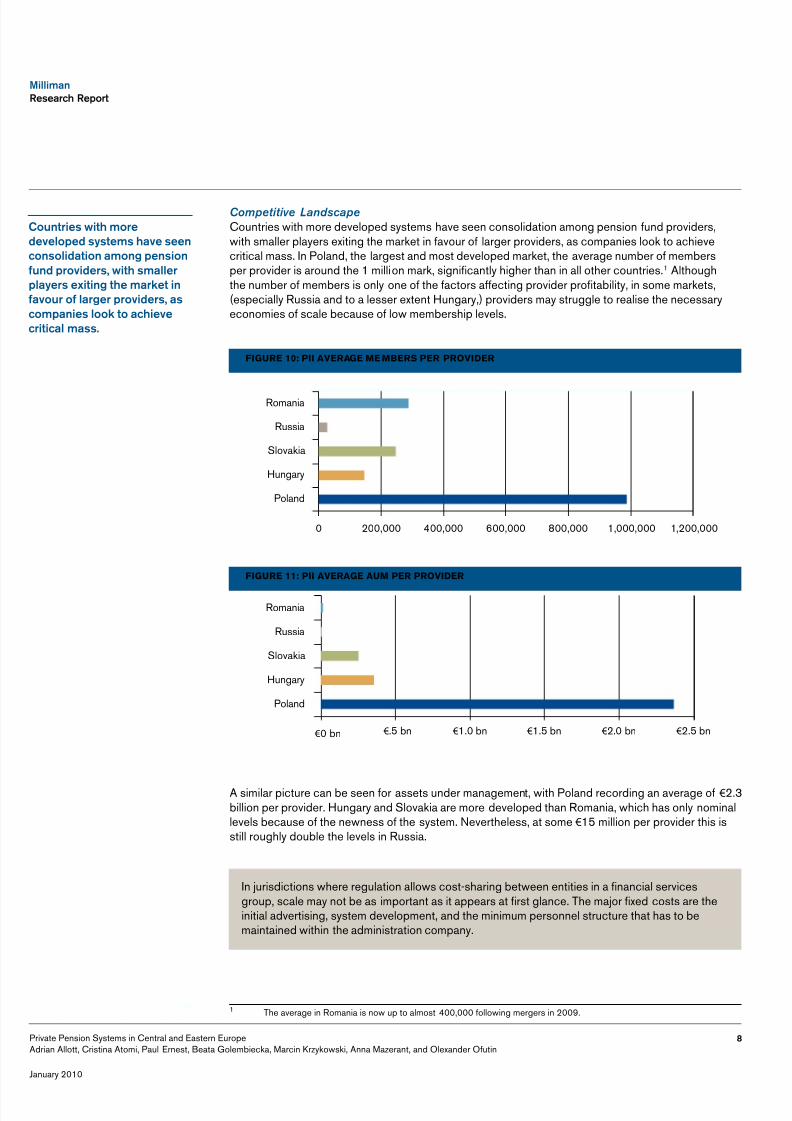

Competitive LandscapeCountries with more developed systems have seen consolidation among pension fund providers,with smaller players exiting the market in favour of larger providers, as companies look to achievecritical mass. In Poland, the largest and most developed market, the average number of membersper provider is around the 1 million mark, significantly higher than in all other countries. 1 Althoughthe number of members is only one of the factors affecting provider profitability, in some markets,(especially Russia and to a lesser extent Hungary,) providers may struggle to realise the necessaryeconomies of scale because of low membership levels.

: pii average me mbers per proviDerfigure 10

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000

Poland

Hungary

Slovakia

Russia

Romania

: pii average aum per proviDerfigure 11

€ 0 bn € .5 bn € 1.0 bn € 1.5 bn € 2.0 bn € 2.5 bn

Poland

Hungary

Slovakia

Russia

Romania

A similar picture can be seen for assets under management, with Poland recording an average of € 2.3billion per provider. Hungary and Slovakia are more developed than Romania, which has only nominallevels because of the newness of the system. Nevertheless, at some € 15 million per provider this isstill roughly double the levels in Russia.

1 The average in Romania is now up to almost 400,000 following mergers in 2009.

In jurisdictions where regulation allows cost-sharing between entities in a financial servicesgroup, scale may not be as important as it appears at first glance. The major fixed costs are theinitial advertising, system development, and the minimum personnel structure that has to bemaintained within the administration company.

Cou r es h morede eloped s s ems ha e seeco sol da o amo g pe s o

u d pro ders, h smallerpla ers ex g he marke

a our o larger pro ders, ascompa es look o ach e ecr cal mass.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 11/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

9

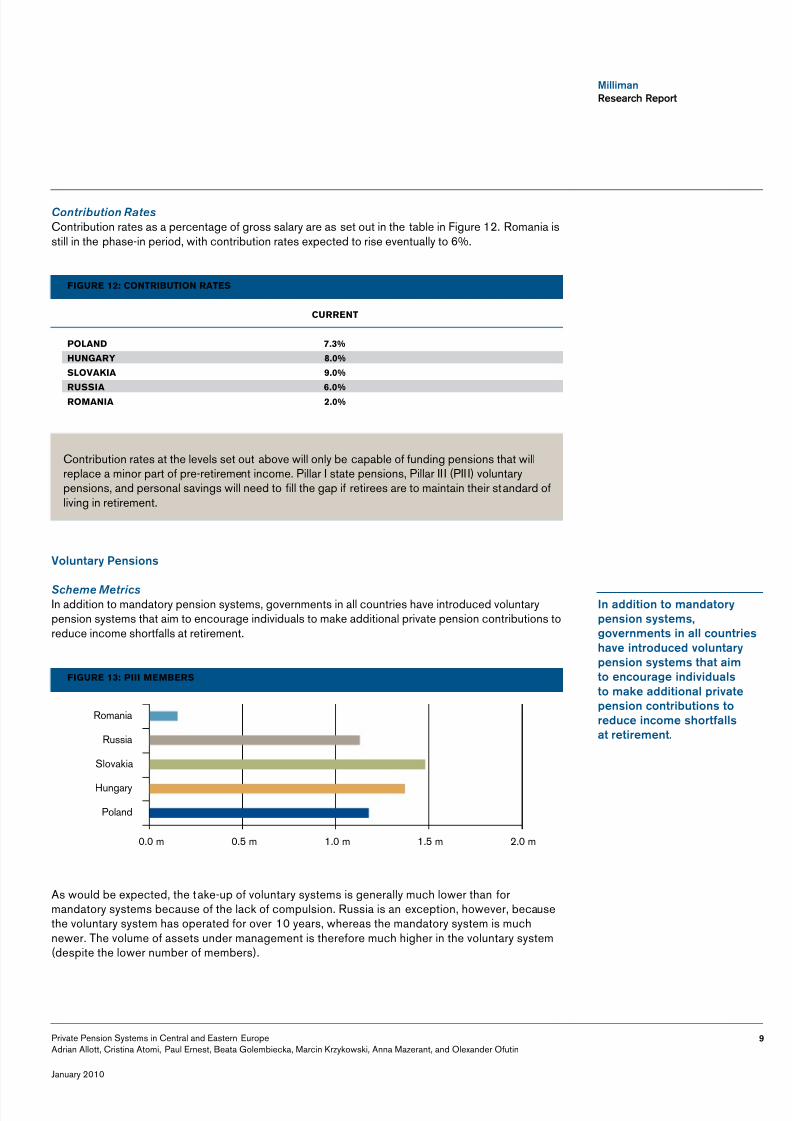

Contribution RatesContribution rates as a percentage of gross salary are as set out in the table in Figure 12. Romania isstill in the phase-in period, with contribution rates expected to rise eventually to 6%.

: ConTribuTion raTesfigure 12

CurrenT

polanD 7.3%hungary 8.0%slovakia 9.0%russia 6.0%romania 2.0%

volu ar Pe s o s

Scheme MetricsIn addition to mandatory pension systems, governments in all countries have introduced voluntarypension systems that aim to encourage individuals to make additional private pension contributions toreduce income shortfalls at retirement.

: piii membersfigure 13

0.0 m 0.5 m 1.0 m 1.5 m 2.0 m

Poland

Hungary

Slovakia

Russia

Romania

As would be expected, the take-up of voluntary systems is generally much lower than formandatory systems because of the lack of compulsion. Russia is an exception, however, becausethe voluntary system has operated for over 10 years, whereas the mandatory system is muchnewer. The volume of assets under management is therefore much higher in the voluntary system(despite the lower number of members).

Contribution rates at the levels set out above will only be capable of funding pensions that willreplace a minor part of pre-retirement income. Pillar I state pensions, Pillar III (PIII) voluntarypensions, and personal savings will need to fill the gap if retirees are to maintain their standard ofliving in retirement.

i add o o ma da orpe s o s s ems,go er me s all cou r esha e roduced olu arpe s o s s ems ha a m

o e courage d dualso make add o al pr a e

pe s o co r bu o s oreduce come shor allsa re reme .

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 12/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

10

January 2010

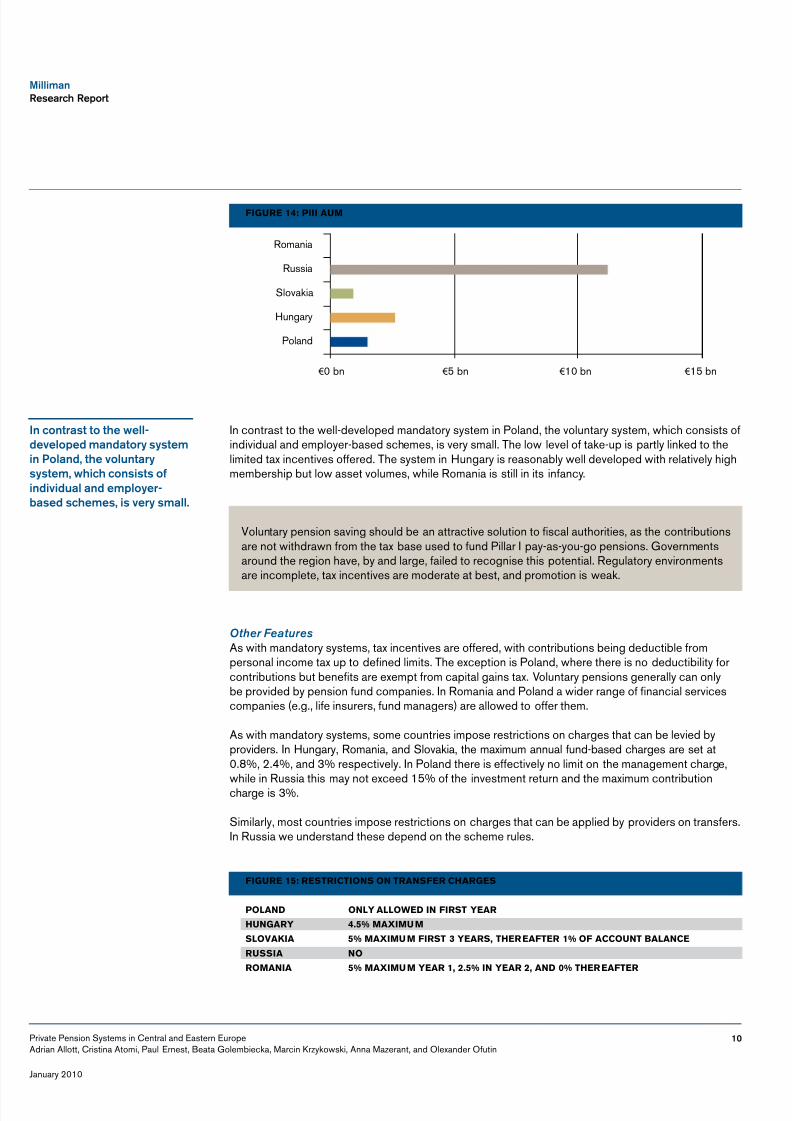

: piii aumfigure 14

€ 0 bn € 5 bn € 10 bn € 15 bn

Poland

Hungary

Slovakia

Russia

Romania

In contrast to the well-developed mandatory system in Poland, the voluntary system, which consists ofindividual and employer-based schemes, is very small. The low level of take-up is partly linked to thelimited tax incentives offered. The system in Hungary is reasonably well developed with relatively highmembership but low asset volumes, while Romania is still in its infancy.

Other FeaturesAs with mandatory systems, tax incentives are offered, with contributions being deductible frompersonal income tax up to defined limits. The exception is Poland, where there is no deductibility forcontributions but benefits are exempt from capital gains tax. Voluntary pensions generally can onlybe provided by pension fund companies. In Romania and Poland a wider range of financial servicescompanies (e.g., life insurers, fund managers) are allowed to offer them.

As with mandatory systems, some countries impose restrictions on charges that can be levied byproviders. In Hungary, Romania, and Slovakia, the maximum annual fund-based charges are set at0.8%, 2.4%, and 3% respectively. In Poland there is effectively no limit on the management charge,

while in Russia this may not exceed 15% of the investment return and the maximum contributioncharge is 3%.

Similarly, most countries impose restrictions on charges that can be applied by providers on transfers.In Russia we understand these depend on the scheme rules.

: resTriCTions on Transfer Chargesfigure 15 polanD only alloweD in firsT yearhungary 4.5% maXimumslovakia 5% maXimum firsT 3 years, ThereafTer 1% of aCCounT balanCerussia noromania 5% maXimum year 1, 2.5% in year 2, anD 0% ThereafTer

Voluntary pension saving should be an attractive solution to fiscal authorities, as the contributionsare not withdrawn from the tax base used to fund Pillar I pay-as-you-go pensions. Governmentsaround the region have, by and large, failed to recognise this potential. Regulatory environmentsare incomplete, tax incentives are moderate at best, and promotion is weak.

i co ras o he ell-de eloped ma da or s s em

Pola d, he olu ars s em, h ch co s s s o

d dual a d emplo er-based schemes, s er small.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 13/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

11

privaTe pension sysTems in speCifiC markeTs

Pola d

Summary of the SystemWith effect from 1 January 1999, a new pension system was introduced in Poland. The aim of thereform was to change the pension system in order to provide its participants with an adequate level ofincome after retirement. In the new system for people born after 1948 the pension depends only onthe capital accumulated throughout the life of a person. The pension system introduced is based on aso-called three-pillar framework.

The first pillar is represented by the individual account of the insured person at the Social Insurance

Institution (Zakład Ubezpieczeń

Społecznych, ZUS). The deposited capital is value-adjusted by thefactor announced by the Minister of Labour and Social Policy, based on the consumer price index (CPI).The pension from the first pillar is funded on a pay-as-you-go basis. This means that pensions paid outcurrently are financed by contributions from current employees. In return for mandatory contributionspaid to ZUS amounting to 19.52% of gross salary (12.22% if an insured is a member of a second-pillarfund), individuals acquire pension rights, which cannot be transferred away by inheritance.

The second pillar of the pension system is based on Open Pension Funds (pension funds, OFE),which are managed by dedicated pension fund management companies (PTE). The activity of pensionfunds and management companies is regulated by the 'Act on Organization and Functioning ofPension Funds from 28 August 1997', with the subsequent 'Amendment to the Act on Organizationand Functioning of Pension Funds and other Acts from 27 August 2003' (the Act).

The essential activity of mandatory pension funds is to collect and invest the contributions of pensionfund members with the purpose of paying out benefits to the members of the fund when they reachretirement age. Member contributions (7.3% of the gross salary) are transferred to pension fundsthrough ZUS as part of overall pension contributions. At the moment of contribution the second-pillarpremiums are exempt from income tax. While the first pillar is mandatory, the second one is mandatoryonly for those born after 31 December 1968.

The third pillar of the system is voluntary and includes employee pension schemes (PracowniczePlany Emerytalne, PPE) and individual pension accounts (Indywidualne Konta Emerytalne, IKE).Because the third pillar is less strictly regulated, other forms of pension savings (e.g., ordinary lifeinsurance or mutual funds) are often also referred to as third pillar .

Mandatory Pensions

Re e ues o Pe s o fu dsRevenues of PTEs consist of asset management charges and charges from contributions/premiumspaid by pension fund members.

Upper limits for both types of the charges are specified in the Act.

Upper limits on management charges as a percentage of Net Asset Value (NAV) are presented in thetable in Figure 16.

S ar g rom 1 Ja uar 1999,a e pe s o s s em as

roduced Pola d. the a mo he re orm as o cha ge

he pe s o s s em ordero pro de s par c pa s

a adequa e le el o come

a er re reme .

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 14/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

12

January 2010

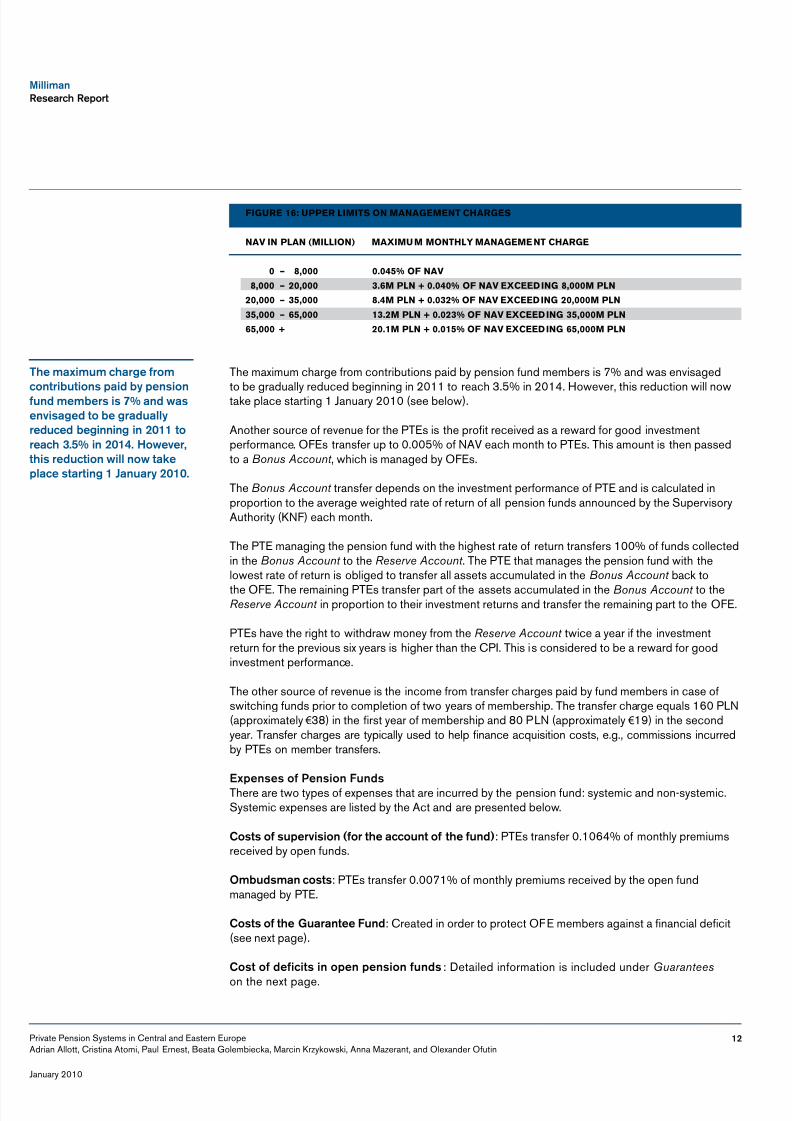

: upper limiTs on managemenT Chargesfigure 16

nav in plan (million) maXimum monThly manageme nT Charge

0 – 8,000 0.045% of nav8,000 – 20,000 3.6m pln + 0.040% of nav eXCeeDing 8,000m pln

20,000 – 35,000 8.4m pln + 0.032% of nav eXCeeDing 20,000m pln 35,000 – 65,000 13.2m pln + 0.023% of nav eXCeeDing 35,000m pln 65,000 + 20.1m pln + 0.015% of nav eXCeeDing 65,000m pln

The maximum charge from contributions paid by pension fund members is 7% and was envisaged

to be gradually reduced beginning in 2011 to reach 3.5% in 2014. However, this reduction will nowtake place starting 1 January 2010 (see below).

Another source of revenue for the PTEs is the profit received as a reward for good investmentperformance. OFEs transfer up to 0.005% of NAV each month to PTEs. This amount is then passedto a Bonus Account , which is managed by OFEs.

The Bonus Account transfer depends on the investment performance of PTE and is calculated inproportion to the average weighted rate of return of all pension funds announced by the SupervisoryAuthority (KNF) each month.

The PTE managing the pension fund with the highest rate of return transfers 100% of funds collectedin the Bonus Account to the Reserve Account . The PTE that manages the pension fund with thelowest rate of return is obliged to transfer all assets accumulated in the Bonus Account back tothe OFE. The remaining PTEs transfer part of the assets accumulated in the Bonus Account to theReserve Account in proportion to their investment returns and transfer the remaining part to the OFE.

PTEs have the right to withdraw money from the Reserve Account twice a year if the investmentreturn for the previous six years is higher than the CPI. This is considered to be a reward for goodinvestment performance.

The other source of revenue is the income from transfer charges paid by fund members in case ofswitching funds prior to completion of two years of membership. The transfer charge equals 160 PLN(approximately € 38) in the first year of membership and 80 PLN (approximately € 19) in the secondyear. Transfer charges are typically used to help finance acquisition costs, e.g., commissions incurredby PTEs on member transfers.

Expe ses o Pe s o fu dsThere are two types of expenses that are incurred by the pension fund: systemic and non-systemic.Systemic expenses are listed by the Act and are presented below.

Cos s o super s o ( or he accou o he u d) : PTEs transfer 0.1064% of monthly premiumsreceived by open funds.

Ombudsma cos s : PTEs transfer 0.0071% of monthly premiums received by the open fundmanaged by PTE.

Cos s o he Guara ee fu d : Created in order to protect OFE members against a financial deficit(see next page).

Cos o de c s ope pe s o u ds: Detailed information is included under Guarantees on the next page.

the max mum charge rom

co r bu o s pa d b pe s ou d members s 7% a d ase saged o be graduallreduced beg g 2011 oreach 3.5% 2014. Ho e er,

h s reduc o ll o akeplace s ar g 1 Ja uar 2010.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 15/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

13

fees pa d o ZUS rom co r bu o s pa d b u ds members : According to the law, ZUS isentitled to receive not more than 0.8% of contributions for social insurance. The level of the ZUS fee(to cover its operating costs) is determined annually in the state budget.

tra s er ee pa d o bo h ZUS a d he na o al Depos or or Secur es (KDPw) : Accordingto the Act, the transfer charge paid to ZUS equals 1% of the minimum monthly wage for each newmembership agreement resulting from incoming transfer, whereas the charge paid to the KDPWequals 1% of the minimum monthly wage for transfers between OFEs.

Cos s o acqu s o /d sposal o asse s ( .e., deal g cos s) o ope pe s o u ds.

Cos o depos or ba k.

The Guarantee Fund consists of basic and additional parts. The basic part of the Guarantee Fund isadministered by the National Depository for Securities (KDPW S.A). PTEs make contributions to thebasic part of the Guarantee Fund and the total value of the basic part of the Guarantee Fund cannotbe higher than 0.1% of the net asset value (NAV) of all OFEs operating in the market.

PTEs also make payments to the additional part of the Guarantee Fund administered by their OFE.The total value of the additional part is between 0.3% and 0.4% of the NAV of the OFE managed bythe PTE (see below).

Expe ses o Pe s o fu d Adm s ra orsThe costs not regulated by the law are called non-systemic costs and involve all other expensesincurred in the operation of a PTE such as:

Acquisition costs, including costs of marketingGeneral management costs including salariesMinimum required rate of return and elimination of deficits

Guara eesThe law guarantees a minimum rate of return to the fund participants. In cases where the rate of returnon the fund drops below the minimum required rate of return, a deficit appears.

In cases where the current rate of return on the fund for the last 36 months is lower than minimumrequired rate of return, then the amount of the deficit is determined by multiplying the number of unitsof account in the pension fund on the last working day of the period of 36 months by the differencebetween the value of the unit of account that would ensure achievement of minimum rate of return andthe actual value of the unit of account on the last working day of the period of 36 months.

The minimum rate of return is defined as the lower of 50% of the weighted average rate of return of allopen funds during the period or the weighted average rate of return less 4%.

Open pension funds are obliged to redeem the fund units kept in the reserve account in order tocover any deficit. The income from the redeemed units increases the value of remaining units of thefund. In the case where the deficiency cannot be fully offset by the reserve account, the fund redeemsunits from the additional part of the Guarantee Fund. If the deficit is still not offset, the PTE has tocompensate the shortfall from its own assets. If the above sources are not sufficient to cover thedeficit, the remaining amount is compensated from the basic portion of the Guarantee Fund. In casethe basic portion of the Guaranteed Fund is insufficient to cover the deficit, the remaining amount isguaranteed by the state.

Ope pe s o u ds areobl ged o redeem he u du s kep he reser eaccou order o co er ade c . the come rom heredeemed u s creases

he alue o rema g u so he u d.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 16/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

14

January 2010

i her a ceAssets managed by OFEs may be inherited, subject to some restrictions.

In case of the death of an OFE member, 50% of the account value is transferred to the spouse’s OFEaccount. The remaining 50% is inherited according to the rules given in the law. The OFE membermay, however, choose the beneficiaries and override the inheritance law.

D s r bu o S ra eg a d Age /Broker Remu era oAs the system has been in operation since 1999, the market is already saturated and has stabilised.Currently the new entrants to the fund are mostly new young employees entering the workforce forthe first time.

It is obligatory to choose a pension fund on taking the first job. If an employee fails to do so in aspecified period, a fund will be allocated to him or her by lottery. The allocation is made twice a yearwith the exclusion of funds that have excessive market share.

Membership of OFE funds is offered directly by the PTEs through call centres and the Internet andby insurance agents (including multi-level networks). The market is estimated at around 600,000–700,000 new members annually. Several times a year there are massive sales campaigns by PTEs(especially on TV).

Insurance agents typically receive commissions of between 200 PLN and 500 PLN. Commission ishigher for transfers with high assets under management (and may exceed 500 PLN). For the careerstarters the commissions tend to be at the lower end of the above range and are independent of theexpected contribution level.

There were 156,000 new members allocated by the lottery in 2008 (down one third from 2007),which is 20%-25% of all new OFE members. Only funds that have higher investment returns than themarket average and a share of AUM lower than 10% may take part in the lottery.

Because of widespread criticism of inappropriate selling in recent years, in particular in the transfermarket, the newest legal amendment is expected to introduce a ban on the acquisition of OFEmembers by insurance agents. Agents would be replaced entirely by direct channels (call centres,Internet, and direct mail).

i es me S ra eg esThe law stipulates investment limits for the PTEs. The most important limitation is that up to 40% ofassets may be invested in shares listed on the Warsaw Stock Exchange.

PTEs are not allowed to invest in derivatives of any kind.Foreign investment may total up to 5% of a fund’s assets. This regulation was recently questioned bythe European Commission, which considers the investment restrictions imposed by law on OFEs tobe contrary to the principle of free movement of capital. This dispute has not yet been resolved.

taxa o o Co r bu o s a d Be e sContributions paid to the OFE are deducted from gross salary and are not subject to income taxes orsocial security charges.

Regular benefit payments paid out by the OFE in the future are expected to be subject to the generalrules of personal income tax (e.g., growth in value may be subject to capital gains tax).

Expec ed Cha ges Leg sla o

Since the beginning of 2009 a number of changes in the legislation regarding pension funds wereproposed by the Ministry of Labour and Social Policy. They mainly concern decreasing the level ofcontribution charges, management fees, the detailed rules of operation of the Bonus Account , and

the la s pula es es mel m s or he PtEs. the mos

mpor a l m a o s haup o 40% o asse s ma be

es ed shares l s ed ohe warsa S ock Excha ge.

S ce he beg g o 2009a umber o cha ges heleg sla o regard g pe s o

u ds ere proposed bhe M s r o Labour a d

Soc al Pol c . the ma lco cer decreas g he le elo co r bu o charges,ma ageme ees, he

de a led rules o opera o ohe Bonus Account , a d he

Guara ee fu d.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 17/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

15

the Guarantee Fund. The other proposed change was the introduction of a multi-fund structure thatwould allow for lower investment risk for older members of the system (Type A and Type B sub-funds).

Two of the changes proposed above are being introduced through new legislation. On June 26,the Polish Parliament adopted an amendment to the Act on Organization and Functioning ofPension Funds that set the maximum level of acquisition charges from the premiums paid to 3.5%.The amendment also decreases the maximum management charges paid by open funds to themanagement funds. The proposed table of maximum management charges (as a proportion of NAV)is shown in Figure 17. :

: proposeD maXimum managemenT Chargesfigure 17

nav in plan (million) maXimum monThly managemenT Charge

0 – 8,000 0.045% of nav8,000 – 20,000 3.6m pln + 0.040% of nav eXCeeDi ng 8,000m pln

20,000 – 35,000 8.4m pln + 0.032% of nav eXCeeDing 20,000m pln 35,000 – 45,000 13.2m pln + 0.023% of nav eXCeeDing 35,000m pln 45,000 + 15.5m pln

This amendment was accepted by the Polish Senate in mid-July and has been approved by thepresident. The law is expected to be in force starting from 1 January 2010.

The temporary law regarding the payout phase of first pensions from OFE was passed in 2008.Several thousand women born before 1949 are entitled to pensions from OFEs starting from thebeginning of 2009. Because the retirement age for men is higher it is expected that they will start toreceive their first pension benefits in 2014.

In accordance with the (transitory) law, the new pensions will be paid in two forms: fixed-termannuities and life annuities. Lump-sum payments are not allowed. Current OFE members (practicallyonly women) will be entitled to a guaranteed five-year annuity upon attaining the age of 60 years. After65, the member of OFE will be entitled to a life annuity under a new, permanent law.

The total pension paid will be the sum of the Pillar I and Pillar I I pensions. In the case of life annuities,an OFE member will be able to choose among offers of the life annuities available in the market.Funds accumulated in an OFE account will be transferred via ZUS to the chosen life annuity funds(Fundusz Do żywotnich Emerytur Kapitałowych, DEK fund), which will be managed by a pensioncompany (Zakład Emerytalny).

Annuities cannot be inherited. However, if the retiree dies within three years of the first annuitypayment, a guaranteed lump sum will be paid to the beneficiaries.

The payout phase system for the fixed five-year term annuity was adopted as a temporary law at theend of 2008. However, the law that stipulates the creation, organization, and operation of DEK fundshas been vetoed by the president and is expected to be rewritten before 2014.

Voluntary Pensions

i d dual e Ko o Emer al e (i d dual Pe s o Accou )The law provides tax incentives for additional savings through individual pension accounts. AnIndywidualne Konto Emerytalne (IKE) account holder may choose a combination of different forms ofsaving, including bank deposits, unit-linked insurance products, mutual investment funds, and directstock exchange investments. IKE accounts are offered by almost all mutual fund companies, mostbanks, some insurance companies, and stock exchange brokers. In case of survival up to the age of60 (or premature retirement), investment returns from the IKE are exempt from capital gains tax.

the la pro des axce es or add o al

sa gs hrough d dualpe s o accou s. Ai d dual e Ko oEmer al e (iKE) accouholder ma choose acomb a o o d ere

orms o sa g, clud gba k depos s, u -l ked

sura ce produc s, mu uales me u ds, a d d rec

s ock excha ge es me s.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 18/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

16

January 2010

There is effectively no limit imposed on providers with respect to the level of fund managementcharges. Additional costs such as dealing charges have to be charged by insurers at the actual costlevied by third parties.

A limit is imposed on charges applied on transfers. A charge can only be applied in the first year andthereafter no charge is permitted.

In case of surrender, the account holder will be taxed with a capital gains tax of 19% and is notallowed to participate in the IKE program in the future.

Take-up of IKEs has been weak because of low levels of sales commission and the low interest ratesbeing paid on traditional pension savings.

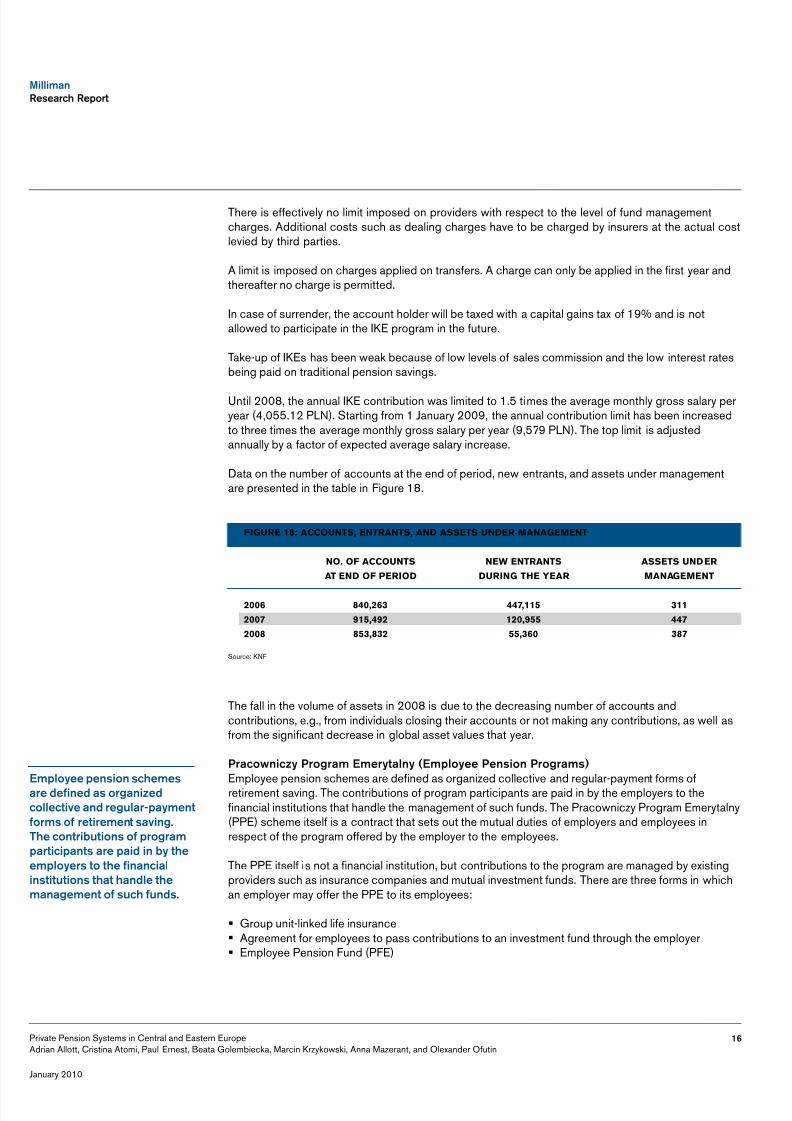

Until 2008, the annual IKE contribution was limited to 1.5 times the average monthly gross salary peryear (4,055.12 PLN). Starting from 1 January 2009, the annual contribution limit has been increasedto three times the average monthly gross salary per year (9,579 PLN). The top limit is adjustedannually by a factor of expected average salary increase.

Data on the number of accounts at the end of period, new entrants, and assets under managementare presented in the table in Figure 18.

: aCCounTs, enTranTs, anD asseTs unDer managemenTfigure 18

no. of aCCounTs new enTranTs asseTs unDeraT enD of perioD During The year managemenT

2006 840,263 447,115 3112007 915,492 120,955 4472008 853,832 55,360 387

Source: KNF

The fall in the volume of assets in 2008 is due to the decreasing number of accounts andcontributions, e.g., from individuals closing their accounts or not making any contributions, as well asfrom the significant decrease in global asset values that year.

Praco cz Program Emer al (Emplo ee Pe s o Programs)

Employee pension schemes are defined as organized collective and regular-payment forms ofretirement saving. The contributions of program participants are paid in by the employers to thefinancial institutions that handle the management of such funds. The Pracowniczy Program Emerytalny(PPE) scheme itself is a contract that sets out the mutual duties of employers and employees inrespect of the program offered by the employer to the employees.

The PPE itself is not a financial institution, but contributions to the program are managed by existingproviders such as insurance companies and mutual investment funds. There are three forms in whichan employer may offer the PPE to its employees:

Group unit-linked life insuranceAgreement for employees to pass contributions to an investment fund through the employerEmployee Pension Fund (PFE)

Emplo ee pe s o schemesare de ed as orga zedcollec e a d regular-pa me

orms o re reme sa g.the co r bu o s o programpar c pa s are pa d b heemplo ers o he a c al

s u o s ha ha dle hema ageme o such u ds.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 19/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

17

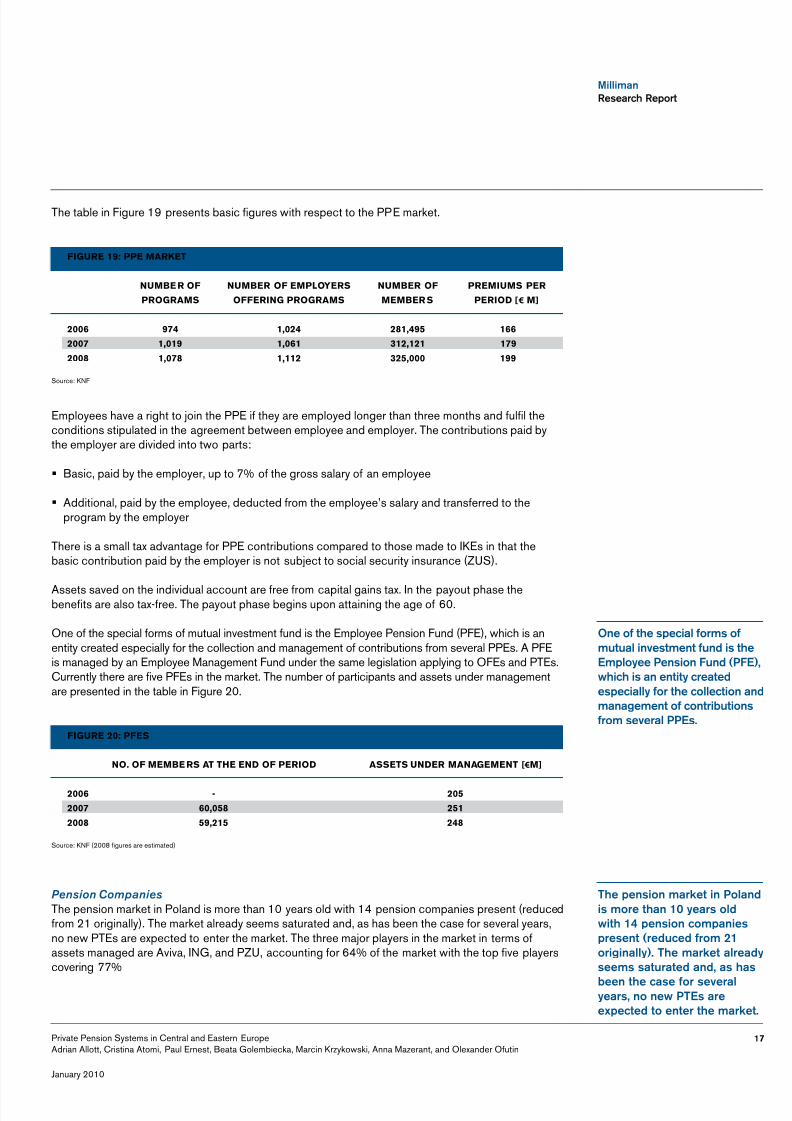

The table in Figure 19 presents basic figures with respect to the PPE market.

: ppe markeTfigure 19

numbe r of number of employers number of premiums perprograms offering programs member s perioD [ € m]

2006 974 1,024 281,495 1662007 1,019 1,061 312,121 1792008 1,078 1,112 325,000 199

Source: KNF

Employees have a right to join the PPE if they are employed longer than three months and fulfil theconditions stipulated in the agreement between employee and employer. The contributions paid bythe employer are divided into two parts:

Basic, paid by the employer, up to 7% of the gross salary of an employee

Additional, paid by the employee, deducted from the employee’s salary and transferred to theprogram by the employer

There is a small tax advantage for PPE contributions compared to those made to IKEs in that thebasic contribution paid by the employer is not subject to social security insurance (ZUS).

Assets saved on the individual account are free from capital gains tax. In the payout phase thebenefits are also tax-free. The payout phase begins upon attaining the age of 60.

One of the special forms of mutual investment fund is the Employee Pension Fund (PFE), which is anentity created especially for the collection and management of contributions from several PPEs. A PFEis managed by an Employee Management Fund under the same legislation applying to OFEs and PTEs.Currently there are five PFEs in the market. The number of participants and assets under managementare presented in the table in Figure 20.

: pfesfigure 20

no. of membe rs aT The enD of perioD asseTs unDer managemenT [ € m]

2006 - 2052007 60,058 2512008 59,215 248

Source: KNF (2008 figures are estimated)

Pension CompaniesThe pension market in Poland is more than 10 years old with 14 pension companies present (reducedfrom 21 originally). The market already seems saturated and, as has been the case for several years,no new PTEs are expected to enter the market. The three major players in the market in terms ofassets managed are Aviva, ING, and PZU, accounting for 64% of the market with the top five playerscovering 77%

O e o he spec al orms omu ual es me u d s heEmplo ee Pe s o fu d (PfE),

h ch s a e crea edespec all or he collec o a dma ageme o co r bu o s

rom se eral PPEs.

the pe s o marke Pola ds more ha 10 ears old

h 14 pe s o compa esprese (reduced rom 21or g all ). the marke alreadseems sa ura ed a d, as has

bee he case or se eralears, o e PtEs are

expec ed o e er he marke .

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 20/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

18

January 2010

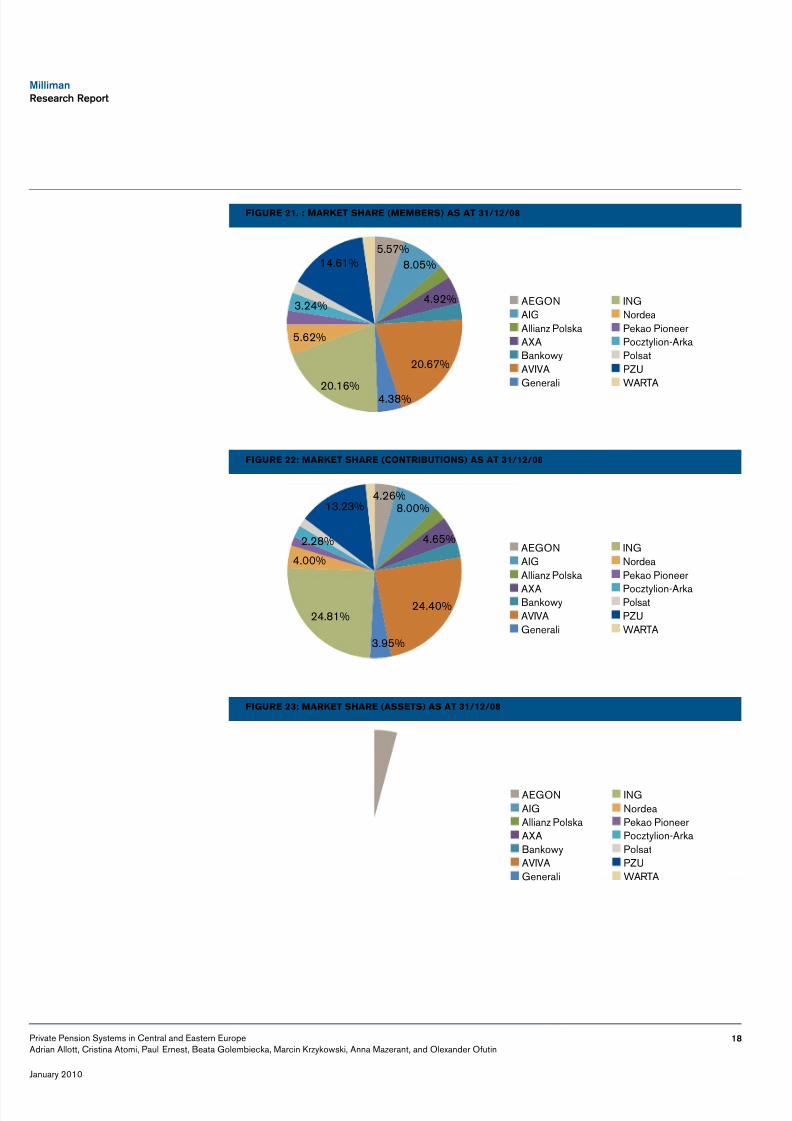

. : markeT share (members) as aT 31/12/08figure 21

5.57%8.05%

4.92%

20.67%

4.38%20.16%

5.62%

3.24%

14.61%

AEGONAIGAllianz PolskaAXABankowyAVIVAGenerali

INGNordeaPekao PioneerPocztylion-ArkaPolsatPZUWARTA

: markeT share (ConTribuTions) as aT 31/12/08figure 22

AEGONAIGAllianz Polska

AXABankowyAVIVAGenerali

INGNordeaPekao Pioneer

Pocztylion-ArkaPolsatPZUWARTA

4.26%8.00%

4.65%

24.40%

3.95%

24.81%

4.00%

2.28%

13.23%

: markeT share (asseTs) as aT 31/12/08figure 23

AEGONAIGAllianz PolskaAXABankowyAVIVAGenerali

INGNordeaPekao PioneerPocztylion-ArkaPolsatPZUWARTA

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 21/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

19

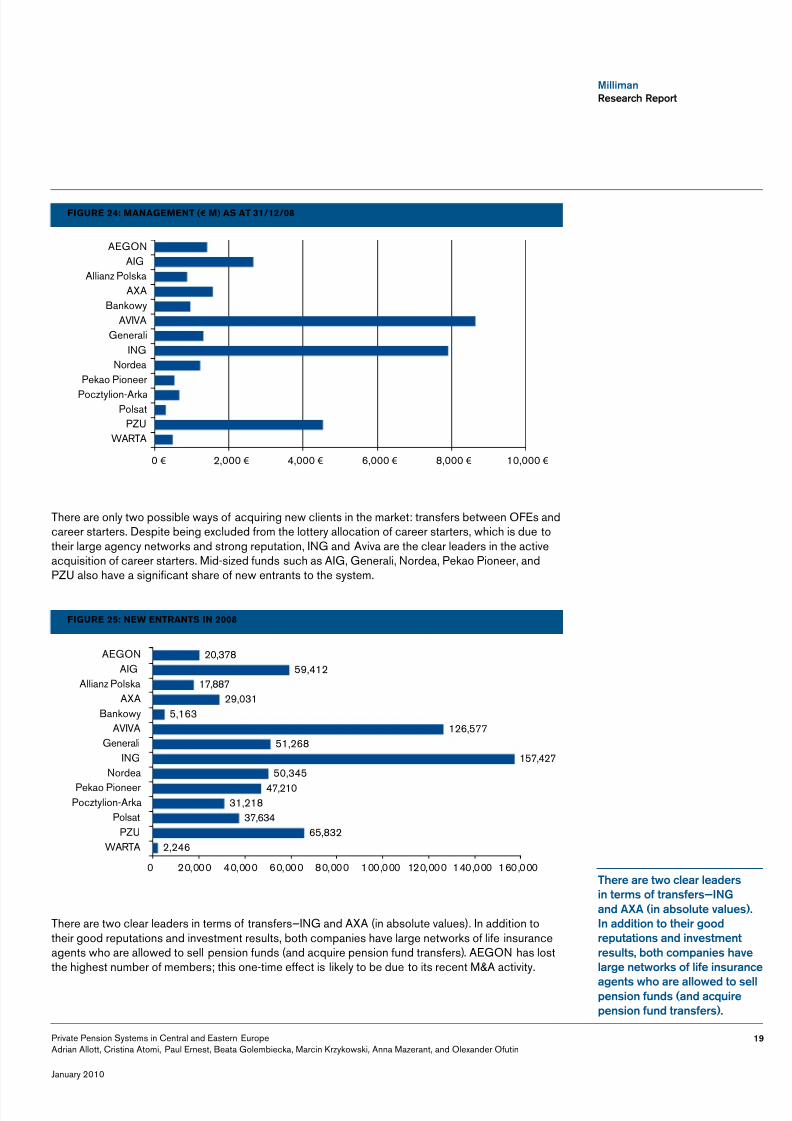

: managemenT (figure 24 € m) as aT 31/12/08

0 € 2,000 € 4,000 € 6,000 € 8,000 € 10,000 €

AEGONAIG

Allianz PolskaAXA

BankowyAVIVA

GeneraliING

NordeaPekao Pioneer

Pocztylion-ArkaPolsat

PZUWARTA

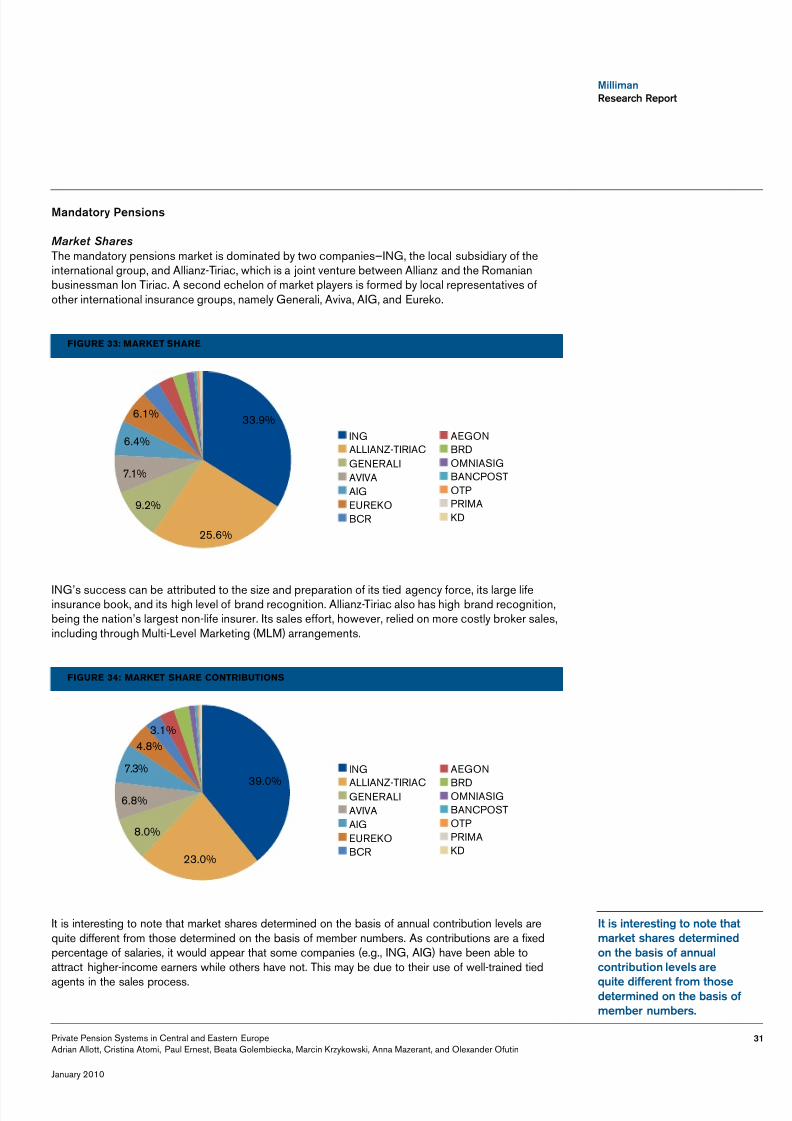

There are only two possible ways of acquiring new clients in the market: transfers between OFEs andcareer starters. Despite being excluded from the lottery allocation of career starters, which is due totheir large agency networks and strong reputation, ING and Aviva are the clear leaders in the activeacquisition of career starters. Mid-sized funds such as AIG, Generali, Nordea, Pekao Pioneer, andPZU also have a significant share of new entrants to the system.

: new enTranTs in 2008figure 25

20,37859,412

17,88729,031

5,163126,577

51,268157,427

50,34547,210

31,21837,634

65,8322,246

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000

AEGONAIG

Allianz PolskaAXA

BankowyAVIVA

GeneraliING

NordeaPekao Pioneer

Pocztylion-ArkaPolsat

PZUWARTA

There are two clear leaders in terms of transfers—ING and AXA (in absolute values). In addition totheir good reputations and investment results, both companies have large networks of life insuranceagents who are allowed to sell pension funds (and acquire pension fund transfers). AEGON has lostthe highest number of members; this one-time effect is likely to be due to its recent M&A activity.

there are o clear leaders erms o ra s ers—inG

a d AXA ( absolu e alues).i add o o he r goodrepu a o s a d es meresul s, bo h compa es ha elarge e orks o l e sura ce

age s ho are allo ed o sellpe s o u ds (a d acqu repe s o u d ra s ers).

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 22/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

20

January 2010

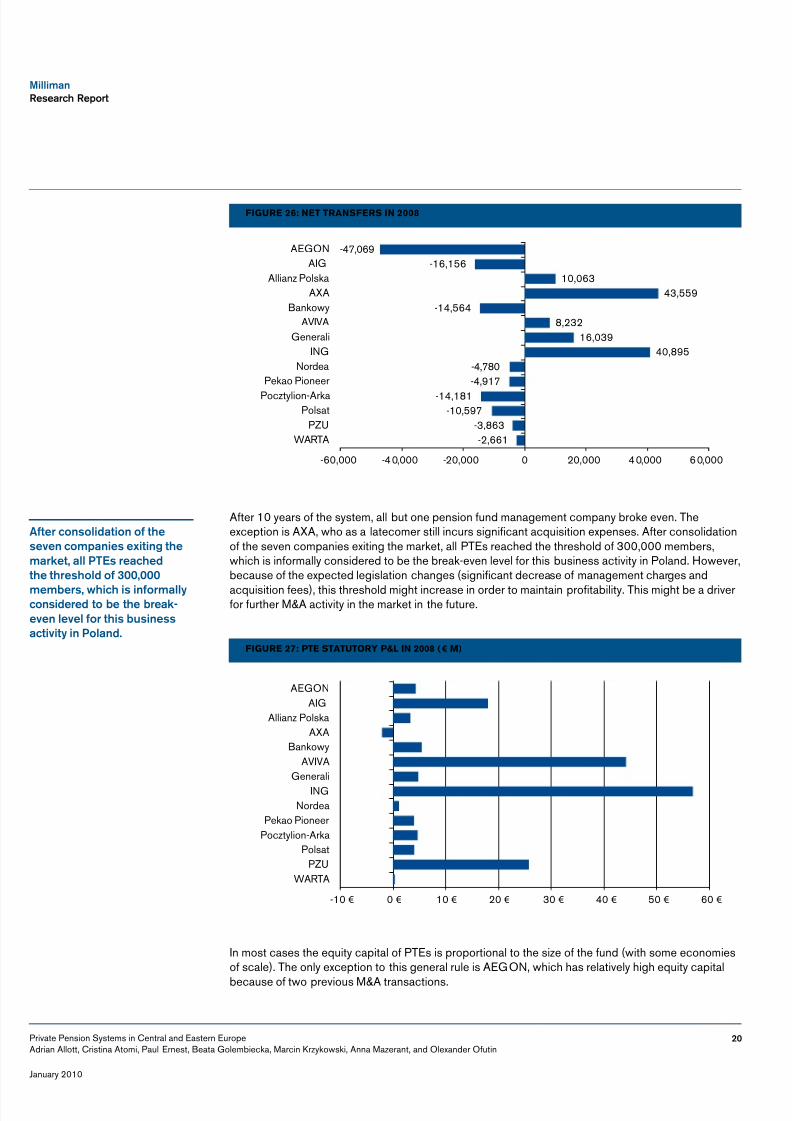

: neT Transfers in 2008figure 26

-47,069-16,156

10,06343,559

-14,5648,232

16,03940,895

-4,780-4,917

-14,181-10,597

-3,863-2,661

-60,000 -40,000 -20,000 0 20,000 40,000 60,000

AEGONAIG

Allianz PolskaAXA

BankowyAVIVA

GeneraliING

NordeaPekao Pioneer

Pocztylion-ArkaPolsat

PZUWARTA

After 10 years of the system, all but one pension fund management company broke even. Theexception is AXA, who as a latecomer still incurs significant acquisition expenses. After consolidationof the seven companies exiting the market, all PTEs reached the threshold of 300,000 members,which is informally considered to be the break-even level for this business activity in Poland. However,because of the expected legislation changes (significant decrease of management charges andacquisition fees), this threshold might increase in order to maintain profitability. This might be a driverfor further M&A activity in the market in the future.

: pTe sTaTuTory p&l in 2008 (figure 27 € m)

-10 € 0 € 10 € 20 € 30 € 40 € 50 € 60 €

AEGONAIG

Allianz PolskaAXA

BankowyAVIVA

GeneraliING

NordeaPekao Pioneer

Pocztylion-ArkaPolsat

PZUWARTA

In most cases the equity capital of PTEs is proportional to the size of the fund (with some economiesof scale). The only exception to this general rule is AEGON, which has relatively high equity capitalbecause of two previous M&A transactions.

A er co sol da o o hese e compa es ex g hemarke , all PtEs reached

he hreshold o 300,000

members, h ch s ormallco s dered o be he break-e e le el or h s bus essac Pola d.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 23/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

21

: pTe's own CapiTal, 31/12/2008 (figure 28 € m)

0 € 20 € 40 € 60 € 80 € 100 € 120 € 140 € 160 €

AEGONAIG

Allianz PolskaAXA

BankowyAVIVA

GeneraliING

NordeaPekao Pioneer

Pocztylion-ArkaPolsat

PZUWARTA

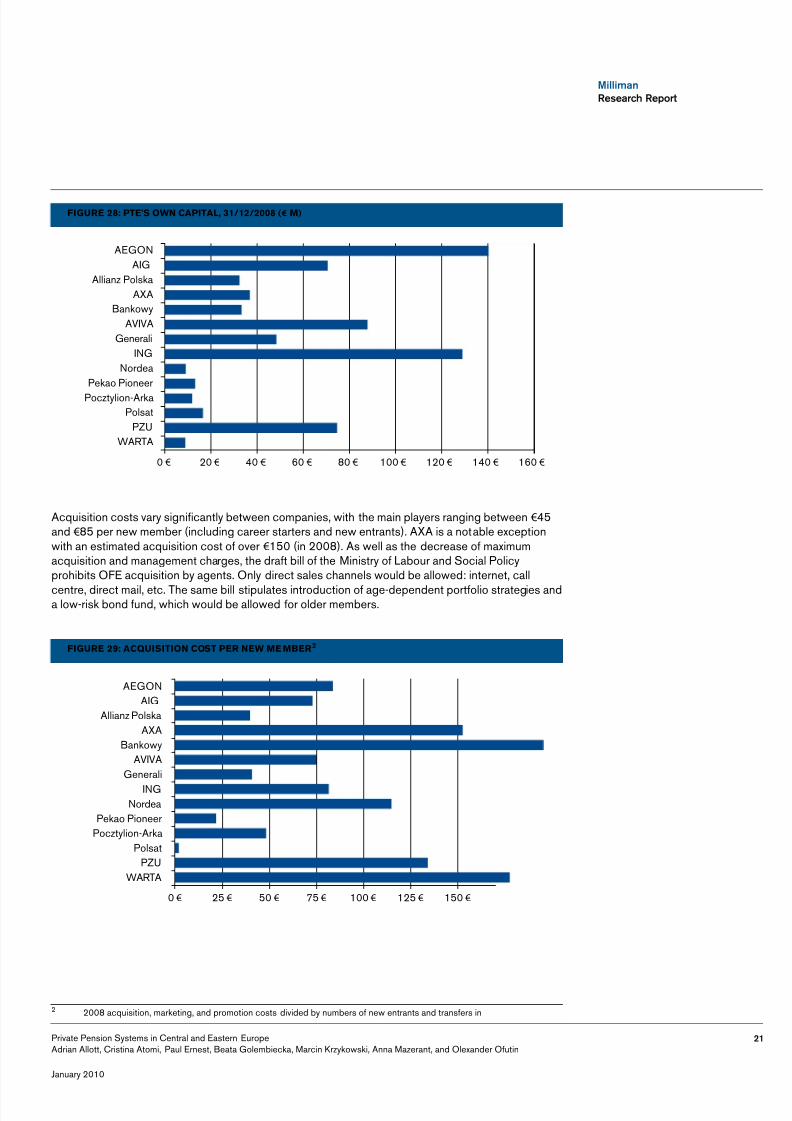

Acquisition costs vary significantly between companies, with the main players ranging between € 45and € 85 per new member (including career starters and new entrants). AXA is a notable exceptionwith an estimated acquisition cost of over € 150 (in 2008). As well as the decrease of maximumacquisition and management charges, the draft bill of the Ministry of Labour and Social Policyprohibits OFE acquisition by agents. Only direct sales channels would be allowed: internet, callcentre, direct mail, etc. The same bill stipulates introduction of age-dependent portfolio strategies anda low-risk bond fund, which would be allowed for older members.

: aCquisiTion CosT per new me mberfigure 29 2

0 € 25 € 50 € 75 € 100 € 125 € 150 €

AEGONAIG

Allianz PolskaAXA

BankowyAVIVA

GeneraliING

NordeaPekao Pioneer

Pocztylion-ArkaPolsat

PZUWARTA

2 2008 acquisition, marketing, and promotion costs divided by numbers of new entrants and transfers in

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 24/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

22

January 2010

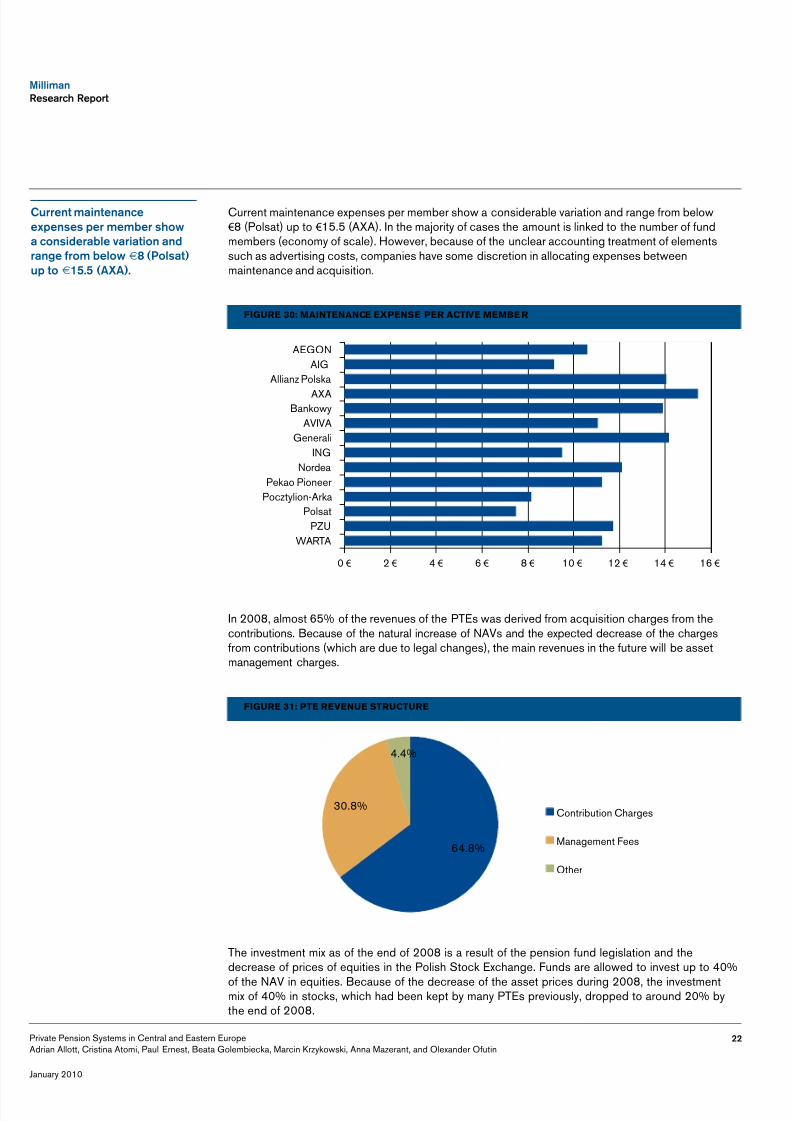

Current maintenance expenses per member show a considerable variation and range from below€ 8 (Polsat) up to € 15.5 (AXA). In the majority of cases the amount is linked to the number of fundmembers (economy of scale). However, because of the unclear accounting treatment of elementssuch as advertising costs, companies have some discretion in allocating expenses betweenmaintenance and acquisition.

: mainTenanCe eXpense per aCTive membe rfigure 30

0 € 2 € 4 € 6 € 8 € 10 € 12 € 14 € 16 €

AEGONAIG

Allianz Polska

AXABankowy

AVIVAGenerali

INGNordea

Pekao PioneerPocztylion-Arka

PolsatPZU

WARTA

In 2008, almost 65% of the revenues of the PTEs was derived from acquisition charges from thecontributions. Because of the natural increase of NAVs and the expected decrease of the chargesfrom contributions (which are due to legal changes), the main revenues in the future will be assetmanagement charges.

: pTe revenue sTruCTurefigure 31

64.8%

30.8%

4.4%

Contribution Charges

Management Fees

Other

The investment mix as of the end of 2008 is a result of the pension fund legislation and thedecrease of prices of equities in the Polish Stock Exchange. Funds are allowed to invest up to 40%of the NAV in equities. Because of the decrease of the asset prices during 2008, the investmentmix of 40% in stocks, which had been kept by many PTEs previously, dropped to around 20% bythe end of 2008.

Curre ma e a ceexpe ses per member shoa co s derable ar a o a dra ge rom belo € 8 (Polsa )up o € 15.5 (AXA).

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 25/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

23

: invesTmenT porTfolio sTruCTurefigure 32

0.83%

75.10%

2.21%

0.43%

21.44%

Equities

Treasury bills

Securities and deposits

Bonds

Other

After the presidential veto at the beginning of 2009, PTEs are waiting for new legislation regarding thebenefit payout phase. The main issues to be decided include 'fairness', the choice of the entitiesresponsible for the payments, and the factors contributing to the expected profitability of the business.Any changes are likely to impact on designated pension providers rather than PTEs, however.

A er he pres de al e o he beg g o 2009,

PtEs are a g or eleg sla o regard g hebe e pa ou phase.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 26/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

24

January 2010

Roma a

Summary of the SystemRomania has a classic three-pillar pensions system, the mechanics of which are functioning wellfollowing the commencement of contributions in May 2007 (facultative) and May 2008 (mandatory).

The private system functions alongside the pay-as-you-go universal state pension system as well asother forms of retirement saving such as life insurance. Outcomes for the participants are limited bythe relatively low levels of contributions going into the two private pillars.

The profitability of pension administrators in the mandatory system is marginal because of the lowlevels of fees that can be charged.

The system is subject to a range of guarantees and protection mechanisms, but capitalrequirements are somewhat incoherent.

There is little sales activity underway for mandatory pensions. Voluntary pensions are typically soldby tied agents and multi-level marketing (MLM) brokers as part of a life insurance offer.

Investment strategies are quite conservative because of guarantee requirements.

Mandatory Pensions

Par c pa oParticipation in a mandatory pension fund is obligatory for all employees born after 31 December1972; 65% of members come from this category. Employees born between 1 January 1963 and 31December 1972 have the option to and account for the remaining 35% of fund members.

Participants choose which fund they want to belong to, and are free to transfer their moneybetween funds.

Currently there are nine funds, four smaller funds having merged with larger rivals. Eachadministrator may manage only one fund.

Co r bu o sContributions are mandatory and are collected through the income tax system alongsidecontributions to the state pension system. The contributions are collected by the National Pensionsand Social Insurance authority, and then distributed to the privately administered funds.

The contribution rate is currently 2% of gross salary, but it will gradually rise to 6% by 2016.In December 2008, 24% of fund participants failed to pay the scheduled contribution. By 31December 2008, however, only 11% of participants had failed to make any contribution whatsoever.

i es meContributions received are converted into fund units, with the moneys being invested in a diversifiedportfolio of assets.

The unit price is dependent on the market value of the assets and the number of units on issue.

Roma a has a class chree-p llar pe s o s s s em,he mecha cs o h ch

are u c o g ell ollo ghe comme ceme o

co r bu o s Ma2007 ( acul a e) a d Ma2008 (ma da or ).

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 27/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

25

Be e sThe value of the units is paid out to the participant in the event of reaching the state retirement age oron becoming totally and permanently disabled.

In the event of the participant’s death prior to retirement, the participant’s account is paid out to theparticipant’s legal heirs.

In some cases the benefit payment is required to be paid as an annuity, but enabling legislation is yetto be enacted.

Insured benefits may be available, if offered in the fund’s prospectus by the administrator.

Approaches o Ac uar al R sks a d Guara ees, Reser g, a d Sol e cGuaranteesAs in Poland, the mandatory pension system requires administrators to ensure that their returns arebroadly in line with market averages. If, over a two-year period, the investment return is more than 4%below the average or less than 50% of the average, the administrator’s licence will be withdrawn.

The mandatory system's account balance paid on transfer, death, disablement, or retirement issubject to a minimum of contributions paid to date minus fees. In some interpretations of the law andregulations, the amount guaranteed ratchets up annually with investment income credited through theunit price, and the guarantee also applies to transfers.

Prudential ReservesNo solvency margin is required to be set up.

Administrators are required to establish actuarial reserves to provide for the ' return of contributions less fees ' guarantee in the mandatory system. The reserve is essentially the amount required tobe held now to fund at date of exit any currently existing gap between account balances andguaranteed values.

No reserves are formally required for the market-relative guarantees, insured benefits, or any otherrisks faced by the funds and administrators.

A guarantee fund is to be established as a separate legal entity. Administrators will be required tocontribute around 0.3% p.a. of assets under management (which is hefty in relation to the allowedadministrator commissions) from their own resources. The purpose of the guarantee fund is to protectparticipants when administrators are unable to fulfil their obligations.

O her Sa e Mecha smsThe system has a dedicated regulator and supervisor, in the form of the Commission for theSupervision of the Private Pensions System (CSSPP).

A depository bank must be appointed to have custody over the fund’s assets and to check theadministrator’s unit price calculations.

Every fund is subject to an annual audit requirement.

Every administrator must retain an actuary, who must complete a simple financial conditionreport annually.

€ 4m of initial paid-up capital is required for mandatory pension administrators, although there isapparently no requirement that a particular level of capital be maintained in the long term.

the s s em has a ded ca edregula or a d super sor, he

orm o he Comm ss o orhe Super s o o he Pr a e

Pe s o s S s em (CSSPP).

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 28/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

26

January 2010

Role o i surers a d O her f a c al Ser ces Compa esPension administration companies are typically owned by large multinational financial services groups.Mandatory pension funds may only be managed by dedicated administration companies, which arenot allowed to undertake any other form of business activity.

In most cases, however, the operations of the administration company complement and are tightlywoven in with the other financial services operations of the group in question, in order to minimisecosts and maximise revenue synergies.

Dr ers o Pro ab lThe key driver of profitability is the asset management fee charged by the administrators, as over thelong term this is expected to be the most significant item of revenue. The fee on contributions has a

useful role in covering initial costs but is not a major contributor to profitability.Another key driver is the contribution rate, as this determines the volume of assets undermanagement and hence the amount of asset management fees collected. The contribution ratewas supposed to rise to 2.5% in 2009 but was held down at 2.0% by the government in a move torestrict its budget deficit.

Expenses also play a critical role. Low charge levels render profitability very sensitive to small changesin expenses incurred. Information from 2008 indicates maintenance expenses in the vicinity of € 5 perparticipant for companies tightly integrated within a financial services group and € 8 per participant forcompanies operating more independently.

Investment guarantees represent a significant hidden cost. These are not properly charged orreserved for at the current time, and hence are not well understood.

Pr c g a d Res r c o s o ChargesAdministrator fees levied on mandatory pension contributions are restricted to 2.5% ofcontributions paid.

Asset management fees are limited to 0.05% of assets per month.

Fees of up to 5% of account value are chargeable on transfer out of a fund during the first two yearsof membership.

Most administrators have established pricing at the maximum allowable level. This is understood to bebecause profitability is marginal, even at this level.

The only discounts offered on the maximum fee levels in the mandatory system have come in the formof a one- or two-year holiday from the asset management fee.

Adm s ra o S s emsRomanian private pension funds are akin to mutual funds in their operations, hence client accountmanagement systems designed for the mutual fund industry may be reused.

A further option is to utilise administration systems designed for life insurance unit-linked products,although these need to be adapted to reflect the restricted benefit design and off-balance-sheet nature of the client’s accounts.

Some administrators have chosen to reuse systems already in use by a sister company (i.e., lifeinsurer or mutual fund operation). Others have installed new systems designed for the purpose,typically by Romanian software houses.

the ke dr er o pro ab ls he asse ma ageme ee

charged b he adm s ra ors,as o er he lo g erm h s sb ar he mos s g ca

em o re e ue.

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 29/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

27

For cost-minimisation purposes, some administrative processes are tied as closely as possible tothose of a sister company, while preserving any necessary legal separation of functions.

D s r bu o S ra eg a d Age /Broker Remu era oThe initial adhesion campaign lasted four months, running from 17 September 2007 to 17 January2008. During the course of the campaign, 4.4 million prospective participants were signed up.

During the initial adhesion campaign the following distribution methods were used:

Tied agency forcesMulti-level agency forces operated by brokersBank branches

Union organisationsThe sales results produced by union organisations were extremely poor, while the passive approachof sales through bank branches delivered only moderate volumes of business (albeit at a lowacquisition cost—less than € 25 per case).

The most successful channels were those using active sales approaches—tied agents and MLMbrokers. Total commission costs per case for the former were in the range € 24– € 34, while for MLMbrokers commission costs per case ranged from € 50– € 90 per case. 3

Agent commissions were typically structured as a fixed amount of RON or euros per case, as it wasimpossible to tell how large a participant’s contributions would be. Overrides were paid to the salesmanagement structures in proportion to the underlying sales.

Deals between administrators and brokers were struck on the basis of fixed amounts per case plusbonuses for achieving predetermined levels of sales.

Commission levels changed frequently throughout the course of the adhesion campaign ascompanies adapted their strategies in response to (a) their performance relative to budget, (b) theactivities of competitors, (c) agent responsiveness, and (d) shareholder imperatives.

Because of the way in which cases were validated, commissions were paid on all adhesions submitted,but many were never validated and many others have become erratic payers of contributions.

Subsequent to the initial campaign, sales activity has been limited and is targeted at new entrants tothe workforce, a market of perhaps 100,000–150,000 per annum.

Theoretically, bank distribution should have an advantage in capturing new entrants to the workforce,given that these are typically students finishing their studies, setting up bank accounts, and takingconsumer and housing loans.

In practice, however, over 90% of new entrants to the workforce are failing to make an election withinthe allotted time period. The result is that they are allocated by lottery to funds in proportion to thecurrent member numbers of each fund.

i es me S ra eg esThe CSSPP classifies investment strategies according to levels of investment risk, and sets strictguidelines on allowable holdings by asset class for each classification. Low-risk funds are essentiallybond funds while medium-risk funds have a small degree of exposure to risky assets such as shares.High-risk funds can have up to 50% of their holdings in risky assets .

3 Source: http: //www.pensiileprivate.ro.

the CSSPP class eses me s ra eg es

accord g o le els oes me r sk, a d se s

s r c gu del es o allo able

hold gs b asse class oreach class ca o .

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 30/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

28

January 2010

In the mandatory pension market, because of the one fund per administrator restriction, mostadministrators have decided to follow a medium-risk strategy in the hope that this will provide bothcomfort and a moderately enhanced long-term return to their clients. Only one administrator hasopted for a high-risk strategy.

Average holdings across the mandatory pensions market as of 30 June 2009 4 were: 7.6% bankdeposits, 54.8% government bonds, 3.6% municipal bonds, 26.6% corporate bonds, 6.7% bondsissued by multinational organisations such as the World Bank, and 3.7% shares.

Holdings of shares have been kept artificially low under a dispensation from the CSSPP in relation torecent economic volatility; fund prospectuses actually require higher levels of investment than 3.7%.

Risks related to the holding of corporate bonds do not appear to be well-appreciated by the market.taxa o o Co r bu o s a d Be e sIn the mandatory pension system, all contributions are deductible and are also not subject to socialsecurity levies.

Pension benefits are currently tax-free up to an amount of 1,000 lei per month, but this provision ofthe tax code was written with state pensions in mind and could be adapted for private pensions oncethey commence the payout phase.

Investment returns are generally not taxed.

Voluntary Pensions

Par c pa oParticipation in a voluntary pension fund is possible for all employees who have at least 90 monthsremaining before they turn 55.

Participants choose which fund they want to belong to, and are free to transfer their moneybetween funds.

Currently there are 14 funds offered by 10 administration companies.

Co r bu o sContributions are voluntary and are collected directly from employers.

There is no fixed contribution rate; some participants set their contributions as a percentage of salary,

while others use a fixed amount per annum (typically, this is the level of maximum deductibility). Bylaw, a maximum of 15% of salary may be contributed to such a fund.

i es meInvestment structures are the same as for the mandatory system.

Be e sThe value of the units is paid out to the participant upon reaching age 55 or in the event of becomingtotally and permanently disabled.

In other respects, benefit structures and payments are similar to the mandatory system.

4 Source: CSSPP half-yearly report. Note: Figures do not add up to 100%.

there s o xedco r bu o ra e; somepar c pa s se he r

co r bu o s as a perce ageo salar , h le o hers usea xed amou per a um( p call , h s s he le el omax mum deduc b l ).

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 31/68

M ll ma Research Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

January 2010

29

Approaches o Ac uar al R sks a d Guara ees, Reser g a d Sol e c

GuaranteesThe voluntary pension system requires administrators to ensure that their returns are broadly in linewith market averages. If, over a two-year period, the investment return is more than 4% below theaverage or less than 50% of the average, the administrator’s licence will be withdrawn.

Prudential ReservesPrudential reserves are largely the same as for the mandatory system.

O her Sa e Mecha sms€ 1.5m of initial paid-up capital is required for voluntary pension administrators, although there is no

requirement that a particular level of capital be maintained in the long term.In other respects, safety mechanisms are as per the mandatory system.

Role o i surers a d O her f a c al Ser ces Compa es

General As with the mandatory sector, pension administration companies are typically owned by largemultinational financial services groups.

In a most cases, the operations of the administration company complement and are tightly woven inwith the other financial services operations of the group in question, to minimise costs and maximiserevenue synergies.

Voluntary pension funds may be administered either by a dedicated company or by another financialservices entity (i.e., a life insurer, asset manager, or bank). In the latter case, the financial servicesentity is required to separately hold and account for assets, liabilities, capital, incomes, and expensesrelating to its voluntary pensions.

Dr ers o Pro ab lDrivers of profitability are the same as for the mandatory system.

Pr c g a d Res r c o s o ChargesAdministrator fees are restricted to 5% of contributions paid.

Asset management fees are limited to 0.2% of assets per month.

Fees of up to 5% of account value are chargeable on transfer out of a fund during the first two yearsof membership.

For voluntary pension funds, administrators have established pricing in a range just below themaximum allowable level.

The higher caps and greater flexibility in the voluntary system have resulted in a wider range ofproduct designs and charging structures.

Some voluntary pension products include insured benefits, while others offer fee structures targetedat particular groups of participants (e.g., corporate clients).

8/8/2019 Milliman Private Pensions in CEE 01-2010

http://slidepdf.com/reader/full/milliman-private-pensions-in-cee-01-2010 32/68

M ll maResearch Repor

Private Pension Systems in Central and Eastern EuropeAdrian Allott, Cristina Atomi, Paul Ernest, Beata Golembiecka, Marcin Krzykowski, Anna Mazerant, and Olexander Ofutin

30

January 2010

Adm s ra o S s emsAdministration systems are the same as for the mandatory system.