1 Milk value chain analysis: industry competitiveness and the dairy policy environment in Pakistan S. S. Godfrey A, C , G. C. Ramsay A , K. Behrendt A T.L. Nordblom A, B and P. C. Wynn A A Graham Centre for Agricultural Innovation (alliance between Charles Sturt University and NSW Department of Primary Industries), Wagga Wagga, NSW 2650, Australia. B Strategic Policy and Economics Branch, NSW Trade and Investment, Wagga Wagga, NSW 2650, Australia. C Corresponding Author: Sosheel Godfrey E-mail: [email protected] / [email protected] 1. Introduction This paper develops and uses value chain analysis framework as a lens to examine the Pakistani dairy industry. It explains the functioning of a rural-urban milk value chain case study with a particular focus on the poor and disadvantaged. The literature review initially focuses on Pakistan and its dairy industry to understand the challenges that it faces. The later section then dwells deeper into the value chain theory, which has been used as a framework to design the questionnaires needed for this research. Effective value chains are essential in meeting the evolving needs of the poor. These typically represent small-scale production and marketing systems, which offer the means to increase access to animal sourced foods for poor consumers, and present opportunities for poor producers and marketers: thus they have a pro-poor value chain focus (Echeverría, Solh, Seré, & Hall, 2011. Urbanization also provides economies of scale for markets closer to home and opportunities for a local production base from farmers whose livelihoods depend on related food systems {Food and Agriculture Organization, 2013 #309). Policies and development strategies in many countries,

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Milk value chain analysis: industry competitiveness and the dairy policy

environment in Pakistan

S. S. GodfreyA, C, G. C. RamsayA, K. BehrendtA T.L. NordblomA, B and P. C. WynnA

AGraham Centre for Agricultural Innovation (alliance between Charles Sturt University and NSW

Department of Primary Industries), Wagga Wagga, NSW 2650, Australia.

BStrategic Policy and Economics Branch, NSW Trade and Investment, Wagga Wagga, NSW 2650,

Australia.

CCorresponding Author: Sosheel Godfrey E-mail: [email protected] /

1. Introduction

This paper develops and uses value chain analysis framework as a lens to examine the Pakistani dairy

industry. It explains the functioning of a rural-urban milk value chain case study with a particular

focus on the poor and disadvantaged. The literature review initially focuses on Pakistan and its dairy

industry to understand the challenges that it faces. The later section then dwells deeper into the value

chain theory, which has been used as a framework to design the questionnaires needed for this

research.

Effective value chains are essential in meeting the evolving needs of the poor. These typically

represent small-scale production and marketing systems, which offer the means to increase access to

animal sourced foods for poor consumers, and present opportunities for poor producers and

marketers: thus they have a pro-poor value chain focus (Echeverría, Solh, Seré, & Hall, 2011.

Urbanization also provides economies of scale for markets closer to home and opportunities for a

local production base from farmers whose livelihoods depend on related food systems {Food and

Agriculture Organization, 2013 #309). Policies and development strategies in many countries,

2

however, often fail to recognize and provide adequate support to smallholder production systems and

value chain development, focusing instead on higher‐profile industrial production (Echeverría et al.,

2011).

Pakistan faces numerous domestic and external challenges. The country’s economic performance, in

the last several years, has continuously been affected adversely by devastating floods, internal

security hazards, and a severely crippling energy crisis that has led to large-scale power outages and

depressed output (Ahmad, 2013; International Monetary Fund, 2013a, 2013b). Agriculture has a 21

percent share of GDP in 2012-13 and is important to the country’s economy with livestock making

up a 56% share of the agricultural economy (Ahmad, 2013). The agriculture sector is the major

employer absorbing 45% of the total labour force (Mazhar, 2013). Agriculture engages half the

country’s households and 59% of those households are in Punjab (Government of Pakistan, 2010).

The sector is though categorized as non-wage employment. The value added to the economy per

worker in the primary sector stands quite low at $US 1,187 (World Bank, 2012).

Pakistan’s 184 million people is growing at two percent per annum. The country is projected to be

world’s fifth most populous nation by 2050 (Mazhar, 2013; United Nations, 2012; World Bank,

2014). Thirty-six percent of country’s population is urban. Punjab is population wise country’s large

with 53% of the total population (Mazhar, 2013; United Nations, 2012; World Bank, 2014).

The research focused on milk supply chains from irrigated rural districts to the urban Lahore city,

second most populous city of Pakistan with and population of nine million plus(Government of

Pakistan, 2011; Government of the Punjab, 2012; Mazhar, 2013).

According to a 2008 survey, 21% of the country’s population was below the extreme income poverty

measure of $1.25 a day, while 60% have incomes of less than $2 a day (World Bank, 2013).

The Multidimensional Poverty Index (MPI) provides an index of overlapping deprivations in health,

education and standard of living. Using this criterion, Pakistan ranks as the second highest in South

Asia with 49% of the population living in multidimensional poverty (Malik, 2013). Poverty is closely

3

linked with undernourishment assessed by energy intake (Food and Agriculture Organization,

2013b). Pakistan’s annual development plan 2013-14, disclosed that 33% of the country’s children

under five years of age and 18% of mothers are underweight (Planning Commission, 2013). These

facts highlight the issue of under nutrition in Pakistan and studying the diets of average Pakistanis.

Milk and particularly fresh milk is important in the diet of an average Pakistani household that which

spends almost eleven percent of the household budget on milk and milk based products1 (Government

of Pakistan, 2013). Milk2 provides 10.6% of the 1700 calories and 18.7% of the 45 grams of protein

consumed per capita per day (Pakistan Bureau of Statistics, 2011; Wynn et al., 2006). Despite, the

significant importance of fresh milk in human diet and high production base, consumption per capita

has shown a decreasing trend in the last ten years. The fresh per capita milk consumption has gone

down by about 5% since 2007 (Government of Pakistan, 2011, 2013).

This pattern can be linked directly to inflation and food price escalation in particular. Pakistan has

experienced double-digit inflation for five consecutive from the fiscal year 2007 to 2012 (Khan,

2012). Food inflation in the same period averaged 14%, which has resulted in phenomenal food price

increases. This steep rise in prices is an enormous challenge in particular as real household incomes

have been stagnant since FY 2000 (Asian Development Bank, 2011; Siddique, 2011). Average own

price elasticity of demand for dairy products in Pakistan is inelastic (-0.571)3 (United States

Department of Agriculture [USDA], 2005).Income elasticity of demand for dairy products is 0.779,

which means their consumption is less sensitive to incomes, a common occurrence with basic

necessities (Andrew, Seale, Meade, & Regmi, 2013; United States Department of Agriculture

[USDA], 2005).

Livestock is a crucial component of country’s mixed crop-livestock farming system. Pakistan ranks

as the second and eleventh largest country for whole fresh buffalo and cow milk production

1 From HEIS 2011-12, average household spends 45.01% on food. Of that 20.59% goes to fresh milk and 25.21% to all dairy products combined. This makes the share of fresh milk as 9.3%=45.01÷100×20.59 and milk and milk based products as 11.3%=45.01÷100×25.21, in the total consumption

expenditure. 2 unpackaged fresh, packaged and powdered 3 1% increase in the prices will decrease demand by only -0.571

4

respectively (FAOSTAT 2011). Overall, the country is ranked the third largest milk producer in the

world (Hemme, 2010).

Milk production in Pakistan has grown at 3.3 % per annum in the last decade (Food and Agriculture

Organization, 2013a). The country raises buffalo and cattle for milk and meat remains a by-product

of these animals (Wynn et al., 2006). FAO data for 2011 suggest milk from buffalo and cattle is the

most valuable of all the agricultural commodities produced in the country (Food and Agriculture

Organization, 2013a). Punjab has a 63% share of milk production (Fakhar, Fakhar Law International,

& Walker, 2006).

Small dairy holders dominate the sector. Milk is crucial to meet the nutrient needs of dairying

communities and to maintain regular cash flows. Livestock also acts as a buffer to mitigate risk from

damage to crops (Afzal, 2010; Fakhar et al., 2006; Farooq, 2012; Teufel & Gall, 1999).

Approximately 80 percent of milk is produced in rural areas with urban and peri-urban areas

accounting for 20% of the total production. Approximately 60% of the milk produced in rural farms

is consumed at the household level and the rest is sold (Zia, Mahmood, & Ali, 2011). Despite decades

of livestock rearing the productivity remains low at 1290 kg per annum per animal whereas it is 5773

kg per cow per annum in Australia (Fakhar et al., 2006) (Wynn et al., 2006).

Domestic milk supply is seasonal and inversely related to demand. Milk demand peaks in summer

due to increased usage of milk based drinks and yogurt, whereas supply declines with decreased

production in winter (Figure 1).

5

Figure 1: Seasonal changes in milk production and the related practices

Data Source: Adopted from Anjum, Lodhi, Raza, Walters, and Krause (1989)

Production of milk falls to 55% of peak production at its lowest point in mid-June, while the demand

increases 60% during this time compared to December when the milk supply is ample. The supply of

buffalo milk decreases in the summer months of May-June and increases by an estimated 88 % in

winter during January-February. For buffalo, winter is widely recognized as the period of flush

production whereas heat stress is linked to the decline in summer.

Cows, on the other hand, are more productive during the summer with high milk production in May-

June and low production in November-December. This offsets the buffalo yield pattern to maintain a

more constant milk supply in addition to the wide use of reconstituted powdered milk by the formal

sector. During the lean season, when the availability of the milk is very limited, the prices increase

(Anjum et al., 1989; Fakhar et al., 2006).

Modern processing plants were introduced as early as the 1960s, to meet the growing urban demand

for milk. The 23 milk pasteurization plants were located around the major cities of Islamabad, Lahore

and Karachi. These plants have all closed which signaled poor acceptance of reconstituted milk by

consumers. In 1977, ultra heat treated (UHT) milk was introduced by a local packaging company and

later taken over by Nestlé Pakistan. Currently, there are twelve large-scale dairy processing plants in

50

60

70

80

90

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ind

ex o

f p

rod

uct

ion

&

con

sum

pti

on

Seasonal change in milk supply and demand

Supply

Water

Demand

Excess demand met by recostituted, powder and diluted milk

Excess supply that is converted to powder and other processed products

Milk supply

Dilution

(milk + water)

Demand

6

Pakistan that on average operate at 50 percent of their capacity. The operational capacity goes down

particularly in summer when production is low and demand is high (Anjum et al., 1989; Zia et al.,

2011).

Although the country’s formal processing industry segment has negligible (less than five percent)

market share, there has been a strong overall industry growth (Staal, Pratt, & Jabbar, 2008, p. x). Milk

is supplied to the consumers by two main types of chains that can be defined as informal and formal

chains. The main differences between the two are cool chain infrastructure and logistics, hygiene and

handling practices and packaging (Zia et al., 2011).

Quality remains a continuous concern in these informal chains. Milk adulteration is associated with

dilution by up to 60% with poor quality water as well as the use of penicillin, formalin, hydrogen

peroxide, milk productivity hormones and many other potentially harmful preservatives and residues

(Staal et al., 2008). Informal milk value chains operate with minimal technology and infrastructure

but remain a dominant link between millions of urban consumers and predominantly smallholder

dairy producers. The function of milk collection, transport, and distribution is performed by different

tiers of small, medium and large vendors, colloquially known as dodhis. The milk is sold by

specialized retail milk shops to final consumers (Figure 2) (Burki & Khan, 2007; Burki, Khan, &

Bari, 2004).

Domestic milk

production

• 80% rural (60%

consumed at source)

• 20% urban & peri-

urban

40% of rural production

• 85% procured by small, medium

and large dhodhis

• 10% goes to dairy processors

• 5% to bakers or confectioner

Urban fresh

unpackaged milk

consumption (39.5%

of total production)

• Specialized retail

milk shops

• Home delivery by

retail shops and

dhodhis

• Self pick up by

consumers from peri

urban dairies

Whole urban & peri-urban production

• 85% sold directly to urban

consumers

• 15% sold to specialized retail milk

shops

Supply Chains

52% of total

production

Total production

(0.8% imports and 0.02%

exports)

44.5% of total

production

Urban & rural total

packaged fresh milk

consumption is (4.75% of

total production)

7

Figure 2: Fresh raw milk flows from rural and peri-urban producers to urban consumer

Source: Author’s own depiction based on various FAO reports and dairy industry research papers

The World Bank’s analysis of the milk-processing sector revealed that Pakistan has an internationally

competitive cost of production of milk at the farm. Losses in the collection, however, due to a large

number of geographically dispersed small-scale farmers and rudimentary chilling methods reduces

its competitiveness by the time the milk has been delivered to the processors. Also for the Pakistani

dairy industry, the terms of trade heavily favour subsidized dairy products imported from the EU, US,

and Canada. This means any production increases are more likely to be absorbed by the domestic

fresh milk market rather than being exported (Shah, 2006). An important issue that is an impediment

to industry’s competitiveness and export penetration for processed dairy products is the inadequate

system for quality assurance and health safety standards. The practice of combining imported milk

from the formal sector with milk from the informal sector makes quality control and traceability even

more complex (World Bank, 2006).

The fragmented food safety laws that exist are not aligned with international quality standards. These

laws are inadequate for meeting market demands and are poorly enforced. Lack of hygiene, poor

handling practices, and almost non-existent cold chains lead to an inferior quality product. Existing

regulations do not prohibit or limit the use of harmful preservatives, including bacteria inhibitors such

as penicillin and formalin as well as other substances such as urea, sugar, and glucose (Zia et al.,

2011). The Punjab Government’s ‘Pure Food Laws’ (Government of the Punjab, 2011) stipulate that

milk from dairy animals is allowed to undergo standardization and reconstitution. For cow and buffalo

milk the standard is set at 12% milk solids (3.5% fat and 8.5% Solids not fat: SNF) and 14% milk

solids (5.0% fat and 9.0% SNF) respectively. Overall, the law requires milk to have no less than 34%

of milk protein and 46% of lactose in milk solids other than SNF.

Government by-laws also control and fix retail prices of fresh milk under the pretense of protecting

the public interest. The District Coordination Officer (DCO), a senior bureaucrat sets up a District

8

Price Review Committee comprising representatives from the livestock department, dairy farmers,

milk retailers, consumers and various stakeholders in the milk trade. This price review committee,

under the overall leadership of the DCO, reviews and sets the price of milk and thus plays a significant

role in the fresh milk market (Zia, 2007). These prices are not based on the cost of production but

favour urban consumers. Although not strictly enforced yet, these prices act as a disincentive to

investors to improve and invest in the production of better quality milk (Ministry of Food, 2007).

The livestock sector has long been identified by the government as being of crucial importance to

support the pro-poor growth (Amjad, 2010). There exists an unapproved national livestock

development policy initiated in 2007 that recommends rationalization of milk and meat prices. It also

raises the need for easy access to credit for small livestock farmers, who fail to meet the collateral

requirement for financial institutions and a liberal credit regime from production, processing through

to marketing. Another important point that the policy raises is the provision of a level playing field

for the local dairy industry by imposing duty and taxes on imported milk powder and other dairy

products equivalent to the production and export subsidies provided by the exporting countries

(Ministry of Food, 2007).

Despite the importance of fresh unpackaged milk supply chains, very little is known about them and

how and why have they been operating so successfully over so many decades. The work done on

these chains so far, very broadly identifies traditional milk marketing channels and role of chain actors

(Ali, 2006; Anjum et al., 1989; Fakhar et al., 2006; Raja, 2001; Sharif & Farooq, 2004; Zia, 2007;

Zia et al., 2011). Therefore, this research project aims to look at these chains from a developing

country’s pro-poor value chain perspective.

9

Competition and the role of firms in a market economy, competitive advantage, and the

value chain

The section aims to set the scene for studying the competitiveness of an industry and where value

chains impact on industry efficiency in a developing country.

Bain (1968) developed the industry structure-conduct and performance (S-C-P) model to examine the

efficiency of the industry. The model suggests classification of industries according to their

characteristics that provide a framework to test the influence of market structure on market conduct

and performance. Bain describes market economies, as a multitude of privately owned enterprises

that produce goods and services. These enterprises determine what and how much of each commodity

is produced and how they distribute it to the end users. The Government’s role is as referee and rule

maker to put in place certain minimal restraints in the public interest otherwise a laissez-faire4

approach would be the rule.

Porter (1998) built on the industrial organization theory and brought firm at the centre of focus to

understand competitiveness that is the ability of a firm to develop and maintain an edge over rivals in

an industry. To diagnose competitive advantage, it is necessary to define a firm’s value chain in

relation to a particular industry. A value chain is a basic tool that examines all the activities performed

by a firm and their interactions help establish their competitive advantage. The structure of an industry

both shapes the value chain of a firm and is a reflection of the collective value chains of competitors.

Structure determines the bargaining relationships with buyers and suppliers that are reflected in both

configuration of a firm’s value chain and how the margins are divided (Porter, 1998).

This S-C-P model and the value chain theory are the genesis of this research’s analysis framework.

From here onwards, the review will dwell deeper into the value chain theory to develop a basis for

the analysis.

4 French, literally "let (people) do (as they think best),"

10

Value chains approach and analysis framework

In value chain approach, the competition or rivalry debate shifts from that among the firms and

industry to value chains and firms within those chains competing against each other in order to get a

larger share of the final consumers’ expenditure on food (Boehlje, 1999). The competitiveness is

influenced by inter-firm interactions (Collins, 2009) with competition in many instances, evaluated

as a network of co-operating firms competing with other firms along the entire chain (Spekman,

Kamauff Jr, & Myhr, 1998). The chain starts from the production system of the raw materials and

will move along the linkages with other enterprises engaged in trading, assembling, processing and

marketing the product(Purcell, Gniel, & van Gent, 2008). Customers are businesses that are the next

links in the chain to which the product is sold while consumers are the final users of the finished

product (Fearne, 2009).

For developing countries, value chains and the way they are governed have important development

implications and therefore need to be understood. The chains have different patterns of organization

and it is important to recognize these differences to identify the inherent risks and opportunities

arising from these patterns, especially for poor people. This is required to form policies that optimize

social inclusiveness without sacrificing long-term competitiveness (Altenburg, 2006c). How different

forms of industrial organization impact on the availability, quality and price of products is, therefore,

a development issue, especially if the goods concerned make up a substantial share of the poor

households’ consumption basket (Altenburg, 2006b) and affect the prospects for economic growth

and poverty reduction in the development of less demanding local markets (Humphrey, 2006).

The basic principle of value creation is to produce or provide a product or services that will create

sufficient value for customers and end users (Boehlje, 1999), as customer value is a single major

source of competitive advantage (Woodruff, 1997). The term value from a chain’s perception refers

to those attributes that are valued by the next customer downstream or the final consumers who use

11

the finished product supplied by a specific chain (Collins, 2009) with the consumer as the ultimate

target of the activities of a chain (Collins, 2006).

A few key definitions of value chains that will guide this value chain analysis framework are as

follows:

Collins (2009) defines “Food value chains as systems driven by the interaction of their technical

(production, processing, transport etc.), economic (profitability), information-related

(communication) and governance (human relationships) systems”.

Boehlje (1999), makes a case for the structural realignments in agricultural industries that relate to

transactions between various tiers of firms, require an understanding of relationships and information

flows as well as physical and financial flows, best described by taking a value chain approach

(Boehlje, 1999). He thus advocates using VCA as an industry wide tool. Boehlje suggested that the

conceptual framework to study the structural changes in an agricultural industry would come from

various fields or disciplines. The challenge is to integrate the appropriate concepts into a

comprehensive analytical framework (Boehlje, 1999).

Altenburg (2006a) linked VCA to industry analysis that focuses on the impediments to growth,

studying upstream and downstream operations as a relevant framework influencing an industry’s core

competitiveness.

At the heart of chain mapping is the wider industry and key linkages (Purcell et al., 2008). VCA plays

a key role in understanding the need and scope for systemic competitiveness and is useful analytical

tool in understanding the policy environment (Kaplinsky & Morris, 2001).

This research will draw on VCM literature to identify key building blocks for a VCA framework to

carry out this research and its analysis, focusing on the following four key areas (Figure 3):

1. Actors and their core roles along the chain, which includes buying and selling; technology used

and physical functions of production, storage and cooling, processing and transport and the time

associated with these physical functions; risks associated with handling a perishable product.

12

2. Physical flows based on consumer value; product volumes handled; quantity and quality

standards and financial flows linked to the chain standards associated with price, costs and

margins.

3. Information flows both micro or internal to the chain and macro or industry level with a focus

on price

4. Governance both micro or chain level and macro or industry level and closely linked to

information flows: focusing on price information flow only:

For macro level, governance we study industry wide price setting associated with product

demand and supply and who holds the power to set the farm gate and retail prices and though

along each chain studied.

For chain level micro level governance we study; financing in the absence of formal

contracts; relationships; conflict resolution and problem solving

Figure 3: Value Chain Analysis Framework

Source: Authors own depiction based on Boehlje (1999), Kohls et al. (2002), Schaffner et al. (2003) and Collins (2009)

4. Governance (micro i.e. chain level and macro i.e. industry level)

& Information Flows (both chain and industry level)

Farmer Middlemen Processor Retailer Consumer

2. Physical Flows (quantity, quality and standardization)

3. Financial Flows (economics: profits & margins)

Exchange Functions: buying & selling, time, risk bearing

1. Value chain actor and their roles

Physical Functions: collection & transport, storage & cooling, processing

13

Value chains actors and their core roles, technology and infrastructure and physical

spoilage risks

Food systems have various business structures and contributors that have various roles (Tansey &

Worsley, 1995). A range of physical activities are performed in the food chains that create value for

the final consumer. Transport is required to move products from where they are produced to

consumption centres. Storage and cooling is required to buffer day-to-day variations in supply and

demand, which are seldom in balance. Fresh produce, in particular, is highly perishable and ideally

requires cool chain infrastructure to maintain a certain temperature, which is often quite a costly

endeavour.

Processing of fresh produce adds value and is essentially a form changing activity. Risk bearing is

another component of a fresh produce supply chain. Product deterioration or spoilage is a major risk,

which can result in substantial losses to the firm holding the product title (Gunderson, Wysocki, &

Stern, 2009; Kohls & Uhl 2002; Schaffner et al., 2003). Mapping the product flow along the chain

identifies the product transformation from raw material to final product and creates a clear picture of

what forms of products are handled, transformed and transported at each stage of the value chain

(Purcell et al., 2008). Smart firms customize logistics according to the requirement and profitability

of the customer segment (Anderson, Britt, & Favre, 2007).

Physical and financial flows and capital invested along the chain

In the contemporary production systems, the primacy is the product characteristics pulled by the final

market (Kaplinsky & Morris, 2001). Commercial product standards should be set by the government

or else the private systems of coordination within a chain implement their own standards. VCA

identifies how information about applicable rules and standards are transmitted through the value

chain and its impacts, both at the industry level and internally through the lead firm via its

coordination system. Quantity or product volume flows can be estimated at different stages of the

14

chain (Purcell et al., 2008). Quality is driven by attributes valued by the final consumer. At the retail

or final consumption point, fresh food products have specific attributes such as taste, freshness and

overall sensory experience that consumer loosely integrates into what is termed quality. The final

consumer weighs price and quality to determine whether the product is good value for money or not.

The challenge for the chain is, therefore, to understand and deliver this value profitably (Collins,

2009). Consumer value links marketing strategy back to the biological production process. In terms

of the dairy industry, this means, the milk composition that meets specific needs of the market. With

respect to attributes, price structures can give economic signals to appropriate parties leading to the

development of a system that rewards those who meet these specific component contents (Boehlje &

Schiek, 1998).

15

Product seasonality, price determination, pricing dynamics and information flows

The biological production processes are associated with variability. For the dairy industry, seasonality

of milk production and associated utilization, is the biggest challenge (Boehlje & Schiek, 1998).

Changes in demand or supply of a commodity are reflected by a change in price. Price is a highly

effective communication signal capable of inducing change. Both consumers and producers respond

independently to price changes in order to maximize utility and profitability (Williamson, 1991).

Along the chain, the response at each stage can be initiated only after price signals the need for change

in quantity or quality. The ability to respond quickly to economic changes is critical to maintaining

profit margins. Quick recognition of erroneous decisions, followed by appropriate adjustments and

corrections, are essential to survival and success (Boehlje & Schiek, 1998).

Information mapping in the value chain involves showing the flow of information between actors at

each tier of the chain (Purcell et al., 2008). An integrated value chain requires continuous information

flows that help makes best product flows possible with the final consumer being the primary focus of

all the chain activities. The kind of information passed among chain members and its frequency has

a strong influence on a chain’s efficiency (Lambert & Cooper, 2000). Information is a significant

force in industries characterized by negotiated or personal linkages. The firms or individuals with

unique and accurate information and knowledge exercise increasing power and control in the

agricultural production system that garners better profits from and transfers risk to others with less

power (Boehlje & Schiek, 1998).

16

Governance along the value chains

Governance conceptualizes complex value chain structures with a range of patterns of industrial

organization that occurs between the two extremes of spot markets or arm’s length trade and vertical

integration (Altenburg, 2006c ; Williamson, 1971).

Governance refers to both the official rules that directly relate to management of the commercial

environment to ensure the preservation of competition between firms: it involves unofficial

instruments that range from contracts between chain actors to unwritten norms or understandings.

There are potential key actors within and outside the value chain that influence the governance

structure and they may establish their own set of wider rules which have broader implications for the

wider industry (Purcell et al., 2008). VCA highlights the role of governance, which can be internal or

external to the chain (Kaplinsky & Morris, 2001).

External governance is important from a policy perspective and identifies the institutional

arrangements that may need to be targeted to improve wider capabilities of value chains operating in

the industry. These may be very specific commercial rules including the association of quality grades

with pricing of the product (Kaplinsky & Morris, 2001; Purcell et al., 2008).

There are dominant firms in the industry promulgating practices that constrain economic and social

development. These firms may choose to impede competition or abuse market power to squeeze the

margins of other firms upstream and/or downstream in the value chain. These dominant firm(s) have

common interests with their suppliers as far as the overall efficiency of the supply chain is concerned,

but pursue different policies, which favour their commercial profitability when it comes to negotiating

purchasing prices and quality standards. These leaders try to gain monopsonistic market power by

creating competition among suppliers in order to enhance their own bargaining power (Altenburg,

2006b). These dominant firms set the parameters of industrial organization and engage in quasi-

hierarchical relationships with firms upstream and downstream in the value chain that are legally

independent but nevertheless to a high degree reliant on their decisions (Kaplinsky, 2001). Rogers

17

and Sexton (1994) highlighted the need to consider the monopsony/oligopsony issues in the policy

debate particularly in the agricultural markets to promote competition.

In the formal sector, processors have to maintain adequate processing capacity to handle milk during

the peak supply season, but plants are often idle during the off-season. This excess capacity adds

substantial system costs for processors (Boehlje & Schiek, 1998). Demand and supply conditions in

agricultural chains vary with seasons, and influence the governance and power of different chain

actors (Purcell et al., 2008). Price fluctuation is a risk associated with variation in supply and demand,

which can lead to changes in the governing rules. The risk associated with pricing volatility is borne

by the product title owners and the ability to manage this risk associated with changes in supply and

demand is a key factor in the sustainability of chain function (Gunderson et al., 2009; Kohls & Uhl

2002).

Internal value chain governance is process control through non-market mechanisms to coordinate

economic activities along the chain. It refers to the structure of relationships and coordination

mechanisms that exist between actors along the value chain to monitor the activities of supplier firms.

The management of risk across the chain is important to ensure that no one essential contributor fails

financially thereby leading to major disruption to the marketing of product. Governance takes various

forms and differs significantly with respect to how strongly governance is exercised, how much it is

concentrated in the hands of a single firm, and how many lead firms exercise governance over chain

members (Gereffi, Humphrey, Kaplinsky, & Sturgeon, 2001; Kaplinsky & Morris, 2001). Effective

chain governance minimizes transaction costs and enhances efficiency (Dyer & Singh, 1998).

Relationships between sellers and buyers are important, defined as a social connection between two

parties, where trust provides social capital that enables efficient linkages through the reduction of

transaction costs (Purcell et al., 2008). The relationships a lead firm has with suppliers can either be

helpful to improve the competitiveness of the industry based on long term commitments or can be

predatory with a focus on realizing a quick profit in the short-term (USAID Microlinks, n.d.). Firms

18

reduce price risks using coordination and control mechanisms, which are different to the open market

pricing system. A common business strategy is to reduce the risk of high input prices by contracting

for supplies combined with contracting product sales (Boehlje & Schiek, 1998).

The success of a business, in a competitive environment, depends on its ability to manage its intricate

network of business relationships with multiple firms (Lambert & Cooper, 2000). Dyer and Singh

(1998) link relationships in which a firm is committed to a source of competitive advantage. Effective

inter-firm relationships are crucial to the performance of value chains and enhancing industry

competitiveness over time (Campbell, 2008).

2. Methods

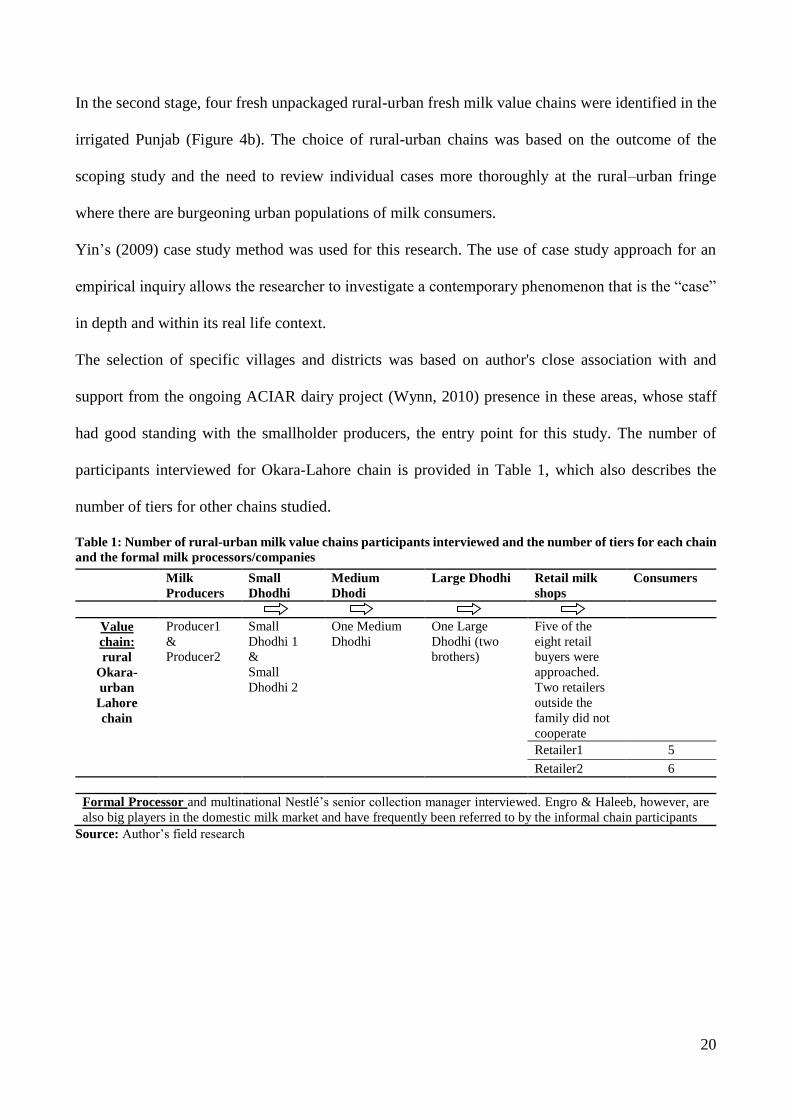

The study originated from the irrigated Okara and arid Bhakkar districts of Punjab (Figure 4 a & b).

The choice of the districts studied was based on the availability of farm economic analysis data from

a two-year longitudinal survey (Wynn, Unpublished) for these two districts.

The study involved two stages. The first stage involved a scoping study which used a purposive

sampling method (Patton, 2002) to identify and sample fresh unpackaged milk informal and formal

chains in both districts. Twenty-seven producers, 11 small, 8 medium and 5 large dhodhis, 22

retailers, 2 formal processors and 11 consumers were interviewed personally, using four different

questionnaires. In total twenty-five informal chains and two formal processor chains were studied.

The questionnaires were developed using a simple value chain analysis framework to identify key

functions being performed along the chain. The initial rural participants were identified with the help

of the Australian Centre for International Agricultural Research (ACIAR) project team (Wynn, 2010)

and their buyers were then tracked and subsequently interviewed. Some middlemen colloquially

known as “dhodhis” and retailers were also randomly surveyed to provide greater cross-sectional

perspectives. During the course of this research, the Okara-Lahore chain model stood out because of

its complexity and author did some preliminary analysis of the chain.

19

Figure 4a. Map of Pakistan highlighting the Punjab province; b. Map of Punjab showing Kasur district and Lahore city

Source: City and border data spatial from 2012 ESRI data & maps

20

In the second stage, four fresh unpackaged rural-urban fresh milk value chains were identified in the

irrigated Punjab (Figure 4b). The choice of rural-urban chains was based on the outcome of the

scoping study and the need to review individual cases more thoroughly at the rural–urban fringe

where there are burgeoning urban populations of milk consumers.

Yin’s (2009) case study method was used for this research. The use of case study approach for an

empirical inquiry allows the researcher to investigate a contemporary phenomenon that is the “case”

in depth and within its real life context.

The selection of specific villages and districts was based on author's close association with and

support from the ongoing ACIAR dairy project (Wynn, 2010) presence in these areas, whose staff

had good standing with the smallholder producers, the entry point for this study. The number of

participants interviewed for Okara-Lahore chain is provided in Table 1, which also describes the

number of tiers for other chains studied.

Table 1: Number of rural-urban milk value chains participants interviewed and the number of tiers for each chain

and the formal milk processors/companies

Milk

Producers

Small

Dhodhi

Medium

Dhodi

Large Dhodhi Retail milk

shops

Consumers

Value

chain:

rural

Okara-

urban

Lahore

chain

Producer1

&

Producer2

Small

Dhodhi 1

&

Small

Dhodhi 2

One Medium

Dhodhi

One Large

Dhodhi (two

brothers)

Five of the

eight retail

buyers were

approached.

Two retailers

outside the

family did not

cooperate

Retailer1 5

Retailer2 6

Formal Processor and multinational Nestlé’s senior collection manager interviewed. Engro & Haleeb, however, are

also big players in the domestic milk market and have frequently been referred to by the informal chain participants

Source: Author’s field research

21

The research was underpinned by mixed methods that are qualitative and quantitative techniques to

collect and analyze data. The method combines the use of both quantitative and qualitative

methodologies within the same study in order to address a single research question. The integration

of these two approaches to collect data helps develop a complete understanding of the research

problems than what either one by itself would net. These studies can later be brought together and

integrated, by casting them within a larger theoretical framework (Bergman, 2008; Creswell, 2010;

Creswell & Plano Clark, 2011; Jupp, 2006).

The quantitative data collected for each value chain case study will give a clear picture of

a) Physical flows including product quantity, quality and time to transfer product along the chain

b) Financial flows represented by costs and margins and value creation and distribution

c) Technology and infrastructure used in transport, storage, cooling and processing and its

economic value

The qualitative data collected for each value chain case study identified

a) Value chain participants and their functions (who?), roles (what?) and rules (how / why?)

b) Governance internal to the chain that is relationships, power dynamics, conflict and problem

solving. External governance in terms of government and dominant market players and their

influence on price, quality and price information flows

c) Information flows with a particular focus on price to understand the type, direction, timing,

completeness, accuracy and distortion if any in these flows

d) Consumers and what they value

For this research field observations were made and face-to-face in-depth interviews were carried with

milk value chain participants using four questionaries that included fixed-choice and open-ended

questions. The questionnaires from the first stage were further refined to go deeper using the

framework developed in the literature review to both collect and analyze the data. The purpose of the

research was explained to each respondent to gain the trust.

22

Patton (2002) and Yin (2009) point towards the use of interviews and personal observations as the key

tools for data collection in the qualitative case study research. Clarke (1999), describes interviews as a

conversation with a purpose. He describes that in a structured interview, questions are asked in a

systematic and consistent order while semi-structured interviews follow a less rigid format and

include open-ended questions.

For this research, structured questions were asked to get the numbers. Both Likert scale and ranking

scale were used to determine the priorities of respondents. The semi-structured questions were used

to understand how and why the chain participants do what they do. The semi-structured questions

generated more in-depth responses although often the structured questions also lead to further

discussions and insight. USAID (2005) qualitative interview manual was also used as a guide for

doing the research in a developing country setting. The author tested the questions with a colleague

with several years of fieldwork experience in the dairy sector of Pakistan. The sequence of questions

was refined several times after each case study.

The practices and understanding of two keys aspects of milk quality and quantity varied for chain

participants and across the milk value chains. Evidence related to these practices was gathered

through direct observation of their participation and practices at various tiers of the chain. Apart from

taking occasional field notes outside the formally designed questionnaires, pictures and voice

recording were extremely valuable tools for the analysis of data collected later on.

In this research, validity aspect was addressed by collecting data from multiple sources. This approach

to construct validity is consistent with Patton (2002) and Yin (2009) who recommend multiple

sources of evidence in case studies.

The primary data sources were milk producers, dhodhis at different tiers, retailers and final consumers

of milk whose statements were cross-examined. Various government reports and local research

publications on the dairy industry of Pakistan also helped make better sense of the local industry

although it was somewhat generic and biased against the local milk chains.

23

The most important advantage presented by using multiple sources of evidence is the development of

converging lines of inquiry or triangulation, a technique to ensure that an account is rich, comprehensive

and well developed (Patton, 2002; Yin, 2009). The author relied on the triangulation through matching

and cross-examining the response of chain participants about the same thing to check the consistency.

Finally, the milk quality collected by Aslam (2015) at each tier of the milk value chain case study

identified by the author was a key source of validation and has been used to develop an even deeper

understanding of the chains studied and the dairy industry of Pakistan.

24

3. Results:

The informal fresh unpackaged milk chain outlined in Figure 5 has five tiers before the product

reaches the final consumer. In addition, the formal processing sector operates parallel and at times

integrates with the informal chain. It originates from rural Okara district 135km southwest of Lahore

city, to which the milk is being supplied. The district in the southern irrigated plains of Punjab lies

between the rivers Ravi and Sutlej (Figure 5). It is famous for rearing local Nili-Ravi water buffalo

and Sahiwal cattle breeds.

Figure 5: Okara-Lahore chain5 model and product physical flows

5 Producer household estimates as large dhodhi collects 2350L milk ÷ 35small dhodhis = 52L as each of the 3 medium dhodhis have approx. 10 small

dhodhi suppliers & large dhodhi has 15 direct small dhodhi suppliers. Now 52L ÷ 10Ps =5.2L therefore 2350L ÷ 5.2LperP = 452 Ps approx. & Consumer

household estimates are based on 2011-12 Household Income Economic Survey (HEIS). Average per capita household size → 6.36L per month÷30day = 0.212Lper day× 6.41 member per household=1.4L → 2350L ÷ 1.4 = 1679 households approx.

Producer1 + Producer2

+ approx. 450 milk producers

Small Dhodhi1+Small Dhodhi2

+28 small dhodhis

3 family owned specialized

retail milk shops

including Retailer1 & Retailer2

+ 5 other retailers

1679 consumer households

1 Large Dhodhi

Formal

Processors

1 Medium Dhodhi

+2medium dhodhis

15 small

dhodhis

Mega

Contractors

Estimated 10 million consumers given a

5% market share

25

Introduction of value chain actors, product physical flows and spoilage risks

Rural milk Producers1 and 2 sell milk to Small Dhodhis 1&2. Medium Dhodhi buys milk from

these and ten other small dhodhis. He operates from a small shop at a bus stand called “adda6”, which

is a midpoint between rural village roads and is quite near to the main highway. Large Dhodhi is

from a powerful Gujjar clan that dominates the urban Lahore milk market. He buys milk from three

medium and directly from fifteen small dhodhis and then supplies to eight retail shops in Lahore city

of which four belong to his close relatives. He is also vertically integrating at the retail end, as his

close family members own fresh milk retail shops in urban Lahore. Two specialized milk retailers 1

and 2 who are close relatives of an buy milk from the same large dhodhi were interviewed in Lahore

city. Data from ten consumers interviewed at these two-retail shop will be used in the later sections.

Formal Processors operate outside but are linked to the informal Okara chain as illustrated in Figure

5. There is are no incentives for higher fat content offered by the formal processors whereas the Large

Dhodhi gives a relatively better price for higher fat content buffalo milk to the farmers. Large Dhodhi

sells any unsold milk and excess winter production to the formal processors and said, “[winter months

when] there is plenty of milk at the back [rural suppliers] and less demand [in urban Lahore market]

and we then sell to companies at a loss...[we sell to] any company where we find a relatively better

rate” (Figure 5).

Milk collection and distribution, using transport is the key function carried out by the dhodhis, though

this transport is not refrigerated. The two retailers perform overnight storage using refrigerators and

retailer1 does some processing. The chain also generates 979 employment7 opportunities. The milk

producers, Large Dhodhi and retailers work for a substantially large number of hours in their

enterprises. The chain works every day of the week with only exception being the holiday of

6 Bus stop in Urdu language or the centre of some activity. Central collection point of informal chains in this case. 7 Average 904 at farms as an estimated 452 farms household with 2workers taking care of livestock + 45small dhodhis + 3medium dhodhi and their 3 record keeper + large dhodhi brothers their 3 loaders and 2 drivers +8 retail shop owners & 2 workers on average at each shop

26

Gyarwee8 Sharif each month; a day in Islamic calendar when producers are said to give away their

milk to the needy for free.

Producers do not face the risk of physical spoilage but the level of risk varies from small dhodhi to

the retailer. In summer, Small Dhodhis do not use ice since Large Dhodhi pays a premium for higher

fat content, suggesting small dhodhis are prepared to accept the risk in order to gain the higher price.

Large Dhodhi manages risk by collecting milk and carrying it to Lahore in relatively small 128 L and

160 L blue plastic cans9. Large Dhodhi said, “No it [spoilage] is rare, only if we get late [on our way

to the city] or ice [used to dilute milk] is not [of] good [quality] but not the whole quantity [spoiled],

just a matti10”. Retailer2 said, “Yes [milk does get spoiled] several times...just recently a whole matti

was spoiled”, which illustrates that the spoilage risk increases downstream.

Consumer value, quality determination; grading and quantity measurements along the

chain and gross margins

Higher fat content associated with buffalo milk followed by the sweeter taste of milk are of prime

importance in this chain. Figure 6 portrays the units of volume and various pots used to handle milk

and the mechanism for quality assessment along the chain. In brief, more volume is obtained from

producers. According to the Large Dhodhi, the higher fat content milk11 is standardized to 4.5% fat

by diluting with ice, and finally, lesser quantities are sold to the consumers. This mechanism will be

discussed in detail later in the section.

8 11th in Urdu language 9 Not in a tanker where all the milk has to be mixed up

10 Recycled 128 L and 160 L plastic cans (Figure 6) that have previously been used for holding chemicals 11 Dhodhi collect both cow and buffalo cow milk. Buffalo milk has 7.4% fat compared to 3.7% in cow’s milk (Fellows & Hampton, 1992).

27

Figure 6: Quantity and quality

along the Okara-Lahore chain

Data Source: Author’s field research

Producer Small Dhodhi Large Dhodhi Retailer

Retailer Quantity

At retail

Retailer1 & Retailer2 sell

1litre = 925ml

i.e. 75 ml less per litre

Large Dhodhi’s 46 litres Lahori panda or maund

=

Retailer’s 48 litres

i.e. 46 ÷ 0.925 = 49.7 litres

SD’s seer or gadvi

for producer

Medium Dhodhi /

Large Dhodhi’s

measure used to convert SD’s gadvi to litres

Large Dhodhi uses 128 and 160 litre plastic drums

to collect milk from Small Dhodhi

Gadvi OR litre

for consumer

Medium Dhodhi

Weight

Lahori 46 litrepanda or 46kg

maund for retailers

Large Dhodhi’s urban Quality standard

Large Dhodhi then lowers the fat for retailers from the average of 6% to around 4.5% by diluting it with

ice

1ice : 8 milk

7.2 ice : 50.4 milk

Therefore easy for Large Dhodhi to make 46litre Lahori panda or maund

Large Dhodhi’s rural Quality standard

Large Dhodhi has set a 6% fat standard for Small Dhodhiswith

a reward and penalty system in place

Premium = (litres × actual fat) ÷ 6% fat standard

Assuming Small Dhodhis 46.5L milk had 6.2% fat

Premium Paid = (46.5L × 6.5) ÷ 6% = 50.4 litres i.e. Small Dhodhi gains another 3.5litres

This is only possible as Small Dhodhi given 0.7% extra for fat in summer and 0.5 % in winter

Producer Quantity

At farm gate

1 seer OR gadvi = 1073 ml i.e. Small Dhodhi gets 73ml

extra per litre

Producer1’ s 1 gadvi= Small Dhodhi’s

1.073litres

i.e. 1 × 1.073=1.073

Price between Producer & Small

Dhodhi is fixed however for a 40 kg or

litre maund

Small Dhodhi Quantity

With extra quantities from producers

40 gadvis becomes 43 litres

i.e. 40 × 1.073 = 43 approx.

So the same farm gate maund becomes 43litres & not 40kg or litre

Small Dhodhis gains some more volumes at Medium Dhodhi’s central collection point since Large Dhodhi gives him leverage

i.e. buys 0.925

therefore

43 ÷ 0.925 = 46.5 litres

i.e. a gain of 6.5 litres for Small Dhodhi in total

28

Value chains are driven by what the final consumer values. Comments by the final consumers

interviewed at the two milk retail shops highlight that butterfat or cream closely followed by taste are

attributes most valued by the final consumer. A consumer (C6) at retailer1 said, “taste [is

important]...to my wife quality means more cream after boiling milk”. The milk is used after boiling

and the amount of cream set on the top, associated with higher fat content buffalo milk is an indicator

of quality. The final consumers also have very little understanding of the units used by the retail shops

to sell milk.

At the farm gate, there is no precise mechanism for the quality assessment of milk. “[Small Dhodhi2]

doesn’t really check anything in milk [while buying] and takes it with his eyes closed”, said Producer2

and this is due to rural cultural norms. There is little clarity and no consistency on the use of measuring

units. Producer2 who is well-educated and understood units said, “We sell milk [to Small Dhodhi2]

in gadvi. Gadvi has 16 chatanks12. The Small Dhodhi nonetheless gets 17 chatank per gadvi”, which

means there is a social acceptance for this to happen. Small Dhodhi2 said, “We buy in gadvi and sell

in litres”. “We buy from the farmer chantank more and sell chantank less [to Large Dhodhi]” Small

Dhodhi1 further elaborated, “…in a maund13 we save 4 to 5 kg14 as the quantity has increased”.

Collection pots used to collect milk from producers, and utensils to measure this collection belong to

Medium Dhodhi. The small dhodhis trust these measurements. Medium Dhodhi clarified the

complicated unit conversion, explained as follows:

Small Dhodhi′s gadvi for producer is 1073 ml instead of actual 1000ml

Therefore small dhodhi obtains 73ml of extra milk per gadvi

Large Dhodhi gives leverage to small dhodhi i. e. 1073 ÷ 0.925

= 1160ml. Small Dhodhi has gained 148ml extra milk per gadvi in total

12 Producer2 is educated and knows the correct chatank in a kg 13 40kg or litre at which price is set between Producer & small dhodhi 14 These participants kept switching between various units

29

Producers consider the aggregate unit of maund, for which milk price is agreed between them and

small dhodhi, to be 40 L, also referred to as kg, which is contrary to the reality. This becomes evident

by applying the above conversions to a maund.

Small Dhodhi′s maund for producer → 40 × 1073 = 42.92L i. e. approx. 3L extra per maund

Large Dhodhi′s leverage given to small dhodhi → 43 ÷ 0.925 = 46.5L i. e approx. 6.5L gain in total

Small dhodhis unload their milk collection directly to Large Ddhodhi’s plastic cans (Figure 6). Prior

to that, however, Medium Dhodhi’s hired munshi15 takes a sample from each of the twelve small

dhodhi supplier’s milk to him to measure the butterfat percentage using the Gerber16 method. The fat

percentage is recorded for making payments later on to small dhodhis. At Medium Dhodhi’s central

collection point Large Dhodhi offers a premium for butterfat above 6% and penalizes small dhodhis

with lesser fat, using the following formula:

Premium Paid = [(Milk in 𝑙𝑖𝑡𝑟𝑒 × %actual fat) ÷ 6%base target fat content] × Base Price per 𝑙𝑖𝑡𝑟𝑒

In the chain, there is feedback from final consumer in place too to check quality. Medium Dhodhi

explained, “At times small dhodhis are able to deceive us and our tests fail. For example if cooking

oil is added to cow’s milk17, we can’t detect it but next day we may get some feedback after complaint

by consumers [at urban retail milk shops] who set yogurt [from the milk]. If this [complaints]

continues we can track the culprit and it would result in termination of purchase [from that small

dhodhi”. This demonstrates an efficient check and balance mechanism.

Large Dhodhi is quite careful, prior to purchase decision, and tests the milk once again. He said “We

first taste then check sample [fat] and finally measure the quantity [of small dhodhi’s milk].We check

fat, LR and temperature”. Large Dhodhi further added, “Both fat and LR [lactometer reading] are

important. Just the fat on its own can be increased by putting cream18 into water. Fat test tells

15 Record keeper and milk tester 16 Milk fat content test to determine the price to be paid. 10 ml of sulphuric acid followed by 11 ml milk and 1 ml of Amyl alcohol added to butyrometer, which is then placed in a hand-operated centrifuge machine and spined for a few minutes to get an estimated butterfat percentage in milk.

17 To increase fat and get an incentive for higher fat content buffalo milk given by large dhodhi 18 possibly cheap powdered milk

30

chicknai19 and LR tells the powder in the milk. LR and temperature have to go together, if fat is more

and LR is less or vice versa that means the milk is adulterated. If the temperature is higher, LR or

gravity will reduce and vice versa. For example at 20 °C temperature the LR has to be 27, LR will be

26 at 17 °C and so on i.e. LR will change by one [centigrade] with every three degrees of temperature

change”. These statements show that Large Dhodhi is the real master of this trade and knows the

product quality aspect really well.

Large Dhodhi dilutes the milk purchased from small dhodhis at central collection point with ice,

already present in his blue plastic cans (Figure 6). Ice is required to avoid milk spoilage, particularly

in hot summers and to gain volumes as Large Dhodhi said, “After buying ...for example 110 L of

milk and 18 kg of ice for a 128 L matti. We are supplying in summer at around 4.5 [%] fat and 22 to

23 LR”, which is Large Dhodhi’s standard at retail end of the chain.

Both retailers sell lesser quantities to the final consumer as Retailer2 said, “We buy in gadvi and sell

in litre...We sell 925 ml litre and that is how we make money”. He further said, “Lahori maund is 46

litres, I don’t know what happens in the rural market”. This is when he buys milk from Large Dhodhi

and before selling lesser quantities. Large Dhodhi, Retailer1 and Retailer3 later changed their

statement saying gadvi is same as litre.

Five retail buyers who are not part of Large Dhodhi’s extended family do check milk quality “by

making khoya20”, said Large Dhodhi. Retailer1 and Retailer2, who are large dhodhi’s close relatives,

are not performing any explicit quality tests for the milk supplied. Retailers are well aware of the

quality sought by the consumer as Retailer1 said, “[consumers seek] thickness [in milk] while

Retailer2 said “[Consumers want] better quality at cheap price”.

19 A word for fat in Urdu language 20 A traditional practice in Lahore market where around 2400ml of milk is boiled to get a certain amount of milk solids, based on which quality is determined

31

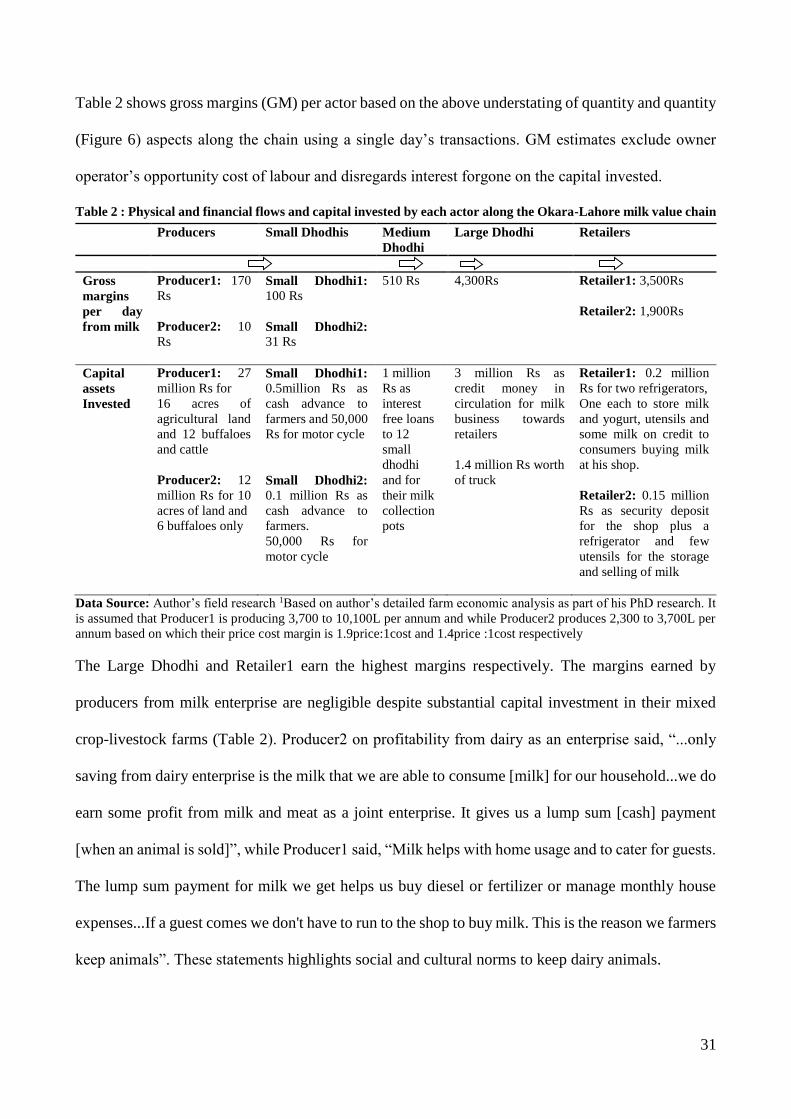

Table 2 shows gross margins (GM) per actor based on the above understating of quantity and quantity

(Figure 6) aspects along the chain using a single day’s transactions. GM estimates exclude owner

operator’s opportunity cost of labour and disregards interest forgone on the capital invested.

Table 2 : Physical and financial flows and capital invested by each actor along the Okara-Lahore milk value chain

Producers Small Dhodhis Medium

Dhodhi

Large Dhodhi Retailers

Gross

margins

per day

from milk

Producer1: 170

Rs

Producer2: 10

Rs

Small Dhodhi1:

100 Rs

Small Dhodhi2:

31 Rs

510 Rs 4,300Rs Retailer1: 3,500Rs

Retailer2: 1,900Rs

Capital

assets

Invested

Producer1: 27

million Rs for

16 acres of

agricultural land

and 12 buffaloes

and cattle

Producer2: 12

million Rs for 10

acres of land and

6 buffaloes only

Small Dhodhi1:

0.5million Rs as

cash advance to

farmers and 50,000

Rs for motor cycle

Small Dhodhi2:

0.1 million Rs as

cash advance to

farmers.

50,000 Rs for

motor cycle

1 million

Rs as

interest

free loans

to 12

small

dhodhi

and for

their milk

collection

pots

3 million Rs as

credit money in

circulation for milk

business towards

retailers

1.4 million Rs worth

of truck

Retailer1: 0.2 million

Rs for two refrigerators,

One each to store milk

and yogurt, utensils and

some milk on credit to

consumers buying milk

at his shop.

Retailer2: 0.15 million

Rs as security deposit

for the shop plus a

refrigerator and few

utensils for the storage

and selling of milk

Data Source: Author’s field research 1Based on author’s detailed farm economic analysis as part of his PhD research. It

is assumed that Producer1 is producing 3,700 to 10,100L per annum and while Producer2 produces 2,300 to 3,700L per

annum based on which their price cost margin is 1.9price:1cost and 1.4price :1cost respectively

The Large Dhodhi and Retailer1 earn the highest margins respectively. The margins earned by

producers from milk enterprise are negligible despite substantial capital investment in their mixed

crop-livestock farms (Table 2). Producer2 on profitability from dairy as an enterprise said, “...only

saving from dairy enterprise is the milk that we are able to consume [milk] for our household...we do

earn some profit from milk and meat as a joint enterprise. It gives us a lump sum [cash] payment

[when an animal is sold]”, while Producer1 said, “Milk helps with home usage and to cater for guests.

The lump sum payment for milk we get helps us buy diesel or fertilizer or manage monthly house

expenses...If a guest comes we don't have to run to the shop to buy milk. This is the reason we farmers

keep animals”. These statements highlights social and cultural norms to keep dairy animals.

32

Product seasonality, price determination and pricing power dynamics

On milk demand, Retailer1 said, “[in] May, June [and] July there is more demand and less supply but

abundant milk in winter”. On milk supply, both producers said that milk production peaks in winter

when there is an abundance of green fodders. The lactation cycle for the cow is said to be both same

and opposite to buffalo, depending on animal breed.

The retail price in urban markets is fixed on an annual basis by the city district Government (Figure

7). The price is generally fixed in mid-April to mid-May each year, a time when milk production

starts to decline. Retailer1 said, “Price changes ...after a year...the current price was fixed about two

months ago21...the rate will remain same in winter...this is Punjab government rate...the price will

only change after a year”.

The Large Dhodhi has an impact on the retail sale price of milk in this chain as he has advised his

price per gadvi to Retailer1 and Retailer2 which “is based on market rate” and has nothing to do with

quality said Retailer2. Retailer1 stated, “[Large Dhodhi] gives us [milk] at Rs 2000/maund22 and we

then fix the retail price accordingly [based on our expenses & margin]...the retail price23 was

suggested by Large Dhodhi”.

Large Dhodhi provided further insight on how benchmark retail prices are set in the city. He stated,

“20 to 30 shops in Lahore give a rate led by a key supplier...the magistrate raids that shop but then

others follow and that price is set...”. This statement describes how retailers influence the government

price. Most of these retailers are large dhodhis as well supplying milk to formal processors.

21 April 2012 22 43.5 Rs/L based on a Lahori maund of 46 litres 23 48 Rs / gadvi

33

Figure 7: Production and pricing mechanism in Okara - Lahore chain

Data Source: Author’s field research

Farm gate price for producers

changes with season

mainly in

increasing in summer

&

decreasing in winter

Price between Small Dhodhi & Large Dhodhi

fluctuates (up & down )

regularly with demand and supply.

Medium Dhodhi works on a fixed commission & is not affected by the

price changes

This price is based on the formal processors rural market buying

prices

Milk Producer

Small Dhodhi Large Dhodhi Retailers

Formal Processors

Rural Market Urban Market

Retail price between Large Dhodhi & retailers is fixed for whole year & worked around the price set by the

government

&

influenced by big market players. This price is a loose benchmark, not strictly followed by most retailers.

• Retailers get around the government price by altering units & Large Dhodhi by altering quality i.e. dilution

• Final consumer of informal chains is price sensitive

Medium Dhodhi

Governance (internal to the chain & external i.e. industry level)

34

The formal processors control farm gate milk prices. “[Rural market] price is determined on the basis

of company24 rate...we have to offer 1 or 2 Rupees higher than that offered by the company to be able

to procure milk [from medium dhodhis & small dhodhis]”, said Large Dhodhi. This statement

highlights the influence that formal processors have on rural pricing and the competition between the

informal and formal channels to procure milk.

Large Dhodhi’s statement was further consolidated by Medium Dhodhi who explained, “Different

dealers25 have an Adda26 rate and we are bound by it. We can’t pay less than that price [to small

dhodhis]...that is our minimum price...The oldest adda gives the rate”. Small Dhodhi1 verified what

Medium Dhodhi said, “Contractor’s [medium dhodhis] commission may vary with the loan extended

but the price offered by Lahori [Large Dhodhi] can’t be different and has to be same at each adda”.

This shows that the large dhodhi is bound to give a minimum price to his small dhodhi suppliers,

determined by the addas.

Medium Dhodhi explained that the add rate is dictated by the formal processors and he described,

“These days Adda “name” is giving the rate...the key price fixation though is based on factory27

rate...in this area dominated by Adam Cheese, CDL28, Nestlé and Engro”. These addas are also

Medium Dhodhi’s key source of price information as he said, “[We check price] from different

addas...there are 12 addas in this area”.

Medium Dhodhi further said “...in winter...production is high and lesser demand...the [farm gate]

price goes down from December to March and then increases with increase in demand from April to

almost November29 as [its] summer and [therefore] higher consumption of milk and other dairy

products. He further explained, “…the major price change is with these two seasons and prices are

relatively stable otherwise...It [price] varies with demand increase such as 1 to 2 Rupees will increase

24 formal processor 25 Milk traders like medium dhodhi and large dhodhi 26 Central rural collection points where a number of dhodhis bring their rural collection before it is transported to Lahore 27 Formal processors 28 Chaudhry Dairies Limited, one of the big national milk processor 29 Error! Reference source not found.

35

in the month of Ramadan30...political instability, less demand...imports of powdered milk by

factories31 will lead to lower prices in the market”.

On pricing mechanism between small dhodhi and producers, Small Dhodhi1 said, “Lahori [Large

Dhodhi] gives us the rate and we pass the same rate to our farmer...whenever the rate changes...it is

communicated to us”, which means that the price is generally passed on to the producer. There is an

annual fixed price arrangement, however, is place between Producer1 and Small dhodhi1. Producer1

said, “We have mutually fixed a price that will go on for both summer and winter. We have agreed

that it will not change. We have told the dhodhi [Small Dhodhi1] that milk is yours, whether cheaper

or expensive. Here all the houses are taking cash advance [but we haven’t and therefore able to fix a

price]”. This fixed price is rare.

Commonly the price changes with the season as Producer2 said, “The price only changes twice that

is summer and winter”. The producer explores local prevailing prices as Producer2 said, “We ask

other dhodhis, chiller [formal processors village collection centre] and tubwala32 [adda rate] to know

what they are paying the small dhodhi, we do investigate [price]”.

Facilitating functions of financing and relationships

There is an intricate set of facilitating functions in the chain that enable it to operate in the absence of

formal contracts illustrated in Figure 8.

Producers take cash advances from their small dhodhi buyers. The account between producer and

small dhodhis is settled once every month and the cash advance keeps rolling with producer owing

small dhodhi. The producer also borrows from small dhodhi whenever a need arises and it is then

deducted from the milk account. Producer1 said, “We get payment [i.e. cash from Small Dhodhi1]

30 Muslim holy month of fasting 31 Formal processors 32 Medium dhodhi has a huge unrefrigerated steel tank sitting at his shop, which is not used as milk is transferred directly from small dhodhi to large dhodhi. This steel tank is however called tub and wala means owner i.e. owner of tub

36

whenever a need arises...we get payment for our crops every six months but money from milk is

regular and helps meet our household needs”.

The conflicts if any are resolved by the involvement of people from the local village as Producer2

said, “...at times others [local village people] may get involved to sort out differences”. Small

Dhodhi2 said, “[conflicts with farmer sellers] are resolved but many times we lose our cash advance

[extended to secure milk purchase]...it is very difficult to find new chungan33 [suppliers] as they

demand more advance and higher rate”, which shows how important ready cash is for the trade to

occur.

The relationship between small dhodhis and Medium Dhodhi is bound through several means.

Medium Dhodhi has extended interest-free loans to small dhodhis without any written contract. The

Medium Dhodhi however, takes a bank cheque for the amount of cash advance extended from some

small dhodhi recipients as a guarantee. This security is a risk mitigating approach, particularly

applicable to those small dhodhis who are not from the same rural vicinity or those that he thinks

cannot be trusted, probably due to their bad repute in the market. The Medium Dhodhi’s commission

is based on the amount of advance the small dhodhi has borrowed. Small Dhodhi234 said, “Yes [we

can change buyer] but it is not easy to find another contractor [medium dhodhi] as the advance

[interest-free loan] has to be cleared”, so the switch is probably dependent on the reputation of small

dhodhi.

33 A local term use for milk producers / farmers 34 small dhodhi1 was said to be a drunkard, drinking local made alcohol, which is considered a real social evil in the Pakistani society

37

Figure 8: Financing, relationships and power dynamics along the Okara - Lahore chain

Data Source: Author’s Field research

• Almost all Ps take cash advance from Small Dhodhis to meet monthly household needs. They also borrow whenever a need arises

• Retailer 1&2 have an arrangement with Large Dhodhi where they don’t need to pay any cash advance to secure milk supply

•Retailer2 does home deliveries at a higher price

• Medium Dhodhiextends interest free loans to most Small Dhodhis enabling them to earn a livelihood and to pay cash advance to producers. This cash advance also makes Small Dhodhi’sfinancial hostages. Medium Dhodhi’scommission is based on the cash advance extended to Small Dhodhis

Milk Producers

Small Dhodhis Large Dhodhi Retailers ConsumersMedium Dhodhi

• Large Dhodhi has not extended cash advance to Medium Dhodhi but to those 15 Small Dhodhi’s from whom he procures milk directly

Cash Advance

Services

Regulatory of Payments

Nature or Relationship / Trust

• Small Dhodhis also provides services such as feed supplements to Ps

•Accounts settled once every month but the advance generally keeps rolling

•Relationship is based on kinships and time worked together is valued by both parties

• Cash advance & ready cash to meet needs followed by price are important

• Element of mistrust i.e. dilution

• Disputes if any are settled by involvement of locals

•Accounts are settled every eighth day but the Small Dhodhi can borrow more money from Medium Dhodhi if a need arises

• Trust in the sense that both parties are aware of the rules of game

• Price is a contentious issue between Small Dhodhis & Medium Dhodhi

•Smoother relationship and trust as both parties have clear rules of engagement i.e. quality and quantity arrangements

• Both parties are free to part ways as no capital involved but need each other

• Both parties have shared price information source that is rural central collection points (addas) linked to formal processors & market demand and supply

•Accounts are settled every eight day

•Family relationship and both parties need each other too

•Accounts settled on a daily basis and concession given by Large Dhodhi needed

• Cash sales at the shop but some customers buy on credit and pay after a month

Seller & Buyer relationships (chain level)

38

Medium Dhodhi and Large Dhodhi have more professional business dealings as both parties have

clear rules of engagement and are better informed than the other chain participants. Medium Dhodhi

has been supplying milk to Large Dhodhi for the last two years and gets paid every 2nd day. Medium