Page 1 of 55 BAYERO UNIVERSITY, KANO FACULTY OF SOCIAL AND MANAGEMENT SCIENCES DEPARTMENT OF BUSINESS ADMINSTRATION & ENTERPRENUERSHIP 15th December, 2014 COURSE: MBA 8237 (Public Finance) CLASS: Masters in Business Administration (MBA) Finance and Investment Option (Full Time Regular, Full Time Special, Part Time II Regular and Part Time III Special) SESSION/SEMESTER: 2013/2014 Session — Second Semester LECTURER: Kabir Tahir Hamid, PhD., FCIFC, FIDRP CONSULTATION: Strictly by Appointment OFFICE: A8, Department of Accounting, Aminu Alhassan Dantata School of Business, New Campus, Bayero University, Kano A. COURSE DESCRIPTION This course is designed to introduce students to the basic aspects of public finance that would enhance their preparation as public administrators. B. COURSE OBJECTIVES On completion of this course, it is expected that the students will be able to understand: (i) the meaning of public finance management; (ii) the sources of government revenue and expenditure and issues related to them; (iii) expenditure and revenue framework of public sector; (iv) the policy issues surrounding public finance and fiscal policy; (v) the theory of Public Finance, public expenditure, revenue allocation, reasons for increase in Government expenditure, price stability, full employment; (vi) the principles of taxation and provide detailed causes of internal (domestic) and external (foreign) debts and external debt management strategies; (vii) the purpose of the Fiscal Responsibility Act and the functions and powers of the Fiscal Responsibility Commission; (viii) the importance of revenue control techniques and those of Fund Accounting, in the Public Sector; C. COURSE CONTENTS 1. Introduction to Public Finance 1.1 Meaning of Public Finance 1.2 Nature and Scope of Public Finance 1.3 Functions of Public Finance 1.4 The Role of Taxation in Public Finance 2 Government Revenue 2.1 Meaning of Revenue 2.2 Sources and Classification of Government Revenue 2.3 Taxation as a Source of Government Revenue 3 Public Expenditure 3.1 Meaning of Public Expenditure 3.2 Basic Functions of Government Expenditure 3.3 Purposes of Government Expenditure

Welcome message from author

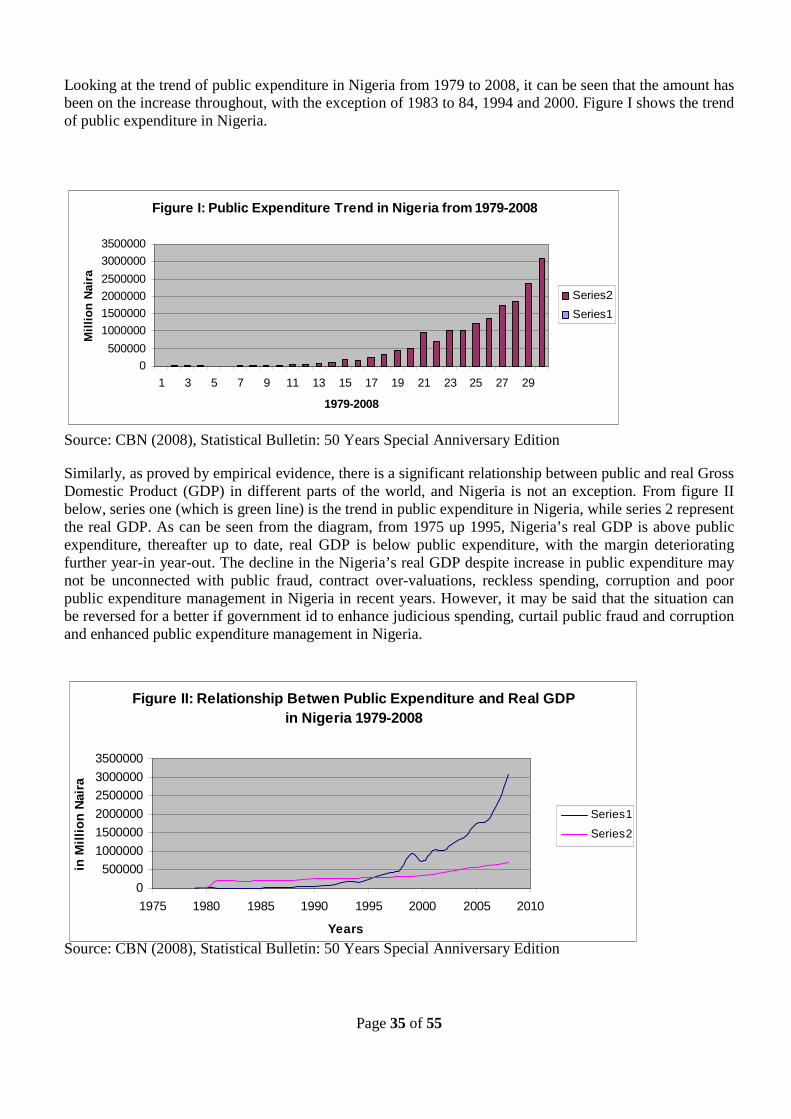

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Page 1 of 55

BAYERO UNIVERSITY, KANO FACULTY OF SOCIAL AND MANAGEMENT SCIENCES

DEPARTMENT OF BUSINESS ADMINSTRATION & ENTERPRENUER SHIP

15th December, 2014 COURSE: MBA 8237 (Public Finance) CLASS: Masters in Business Administration (MBA) Finance and Investment Option (Full Time

Regular, Full Time Special, Part Time II Regular and Part Time III Special) SESSION/SEMESTER: 2013/2014 Session — Second Semester LECTURER : Kabir Tahir Hamid, PhD., FCIFC, FIDRP CONSULTATION : Strictly by Appointment OFFICE: A8, Department of Accounting, Aminu Alhassan Dantata School of Business, New Campus, Bayero University, Kano A. COURSE DESCRIPTION This course is designed to introduce students to the basic aspects of public finance that would enhance their preparation as public administrators. B. COURSE OBJECTIVES On completion of this course, it is expected that the students will be able to understand: (i) the meaning of public finance management; (ii) the sources of government revenue and expenditure and issues related to them; (iii) expenditure and revenue framework of public sector; (iv) the policy issues surrounding public finance and fiscal policy; (v) the theory of Public Finance, public expenditure, revenue allocation, reasons for increase in

Government expenditure, price stability, full employment; (vi) the principles of taxation and provide detailed causes of internal (domestic) and external

(foreign) debts and external debt management strategies; (vii) the purpose of the Fiscal Responsibility Act and the functions and powers of the Fiscal

Responsibility Commission; (viii) the importance of revenue control techniques and those of Fund Accounting, in the Public

Sector; C. COURSE CONTENTS 1. Introduction to Public Finance 1.1 Meaning of Public Finance 1.2 Nature and Scope of Public Finance 1.3 Functions of Public Finance 1.4 The Role of Taxation in Public Finance 2 Government Revenue 2.1 Meaning of Revenue 2.2 Sources and Classification of Government Revenue 2.3 Taxation as a Source of Government Revenue 3 Public Expenditure 3.1 Meaning of Public Expenditure 3.2 Basic Functions of Government Expenditure 3.3 Purposes of Government Expenditure

Page 2 of 55

3.4 Guiding Principles of Public Expenditure 3.5 Financing Public Expenditure 3.6 The Impact of Government Expenditure 4 Fiscal Policy 4.1 Meaning of Fiscal Policy 4.2 Objectives of Fiscal policy 4.3 Instruments of Fiscal Policy 4.4 Compensatory Fiscal Policy 4.5 Incidence and Effects of Taxes 4.6 Incidence of Commodity Taxation 4.7 Factors Determining the Incidence of Commodity Tax under Perfect Competition 4.8 Effectiveness of Fiscal Policies in Nigeria 5 Government Activity and Economic Development 6 Tax System and Value Added Tax 7 Monetary Policies 8 The Federation Account 9 Monitoring Government Allocation and Expenditures

D. RECOMMENDED TEXT BOOKS (i) Public Finance in Theory and Practice by Musgrave, R.A & Musgrave, P.B. (ii) Principles of Public Sector Accounting and Finance by Jimoh, B. (iii) Public Sector Accounting and Finance by Adams, R.A. (iv) Public Sector Accounting and Finance for Decision-Making by Banmeke, S.A. (v) Public Sector Accounting and Finance by ICAN (vi) Public Sector Accounting by Daniel, G.I. (vii) Theory and Practice of Public Sector Accounting and Finance by Tiku, G.J.D. (viii) Introduction to Public Finance (NOUN) by Anthony I. Ehiagwina (ix) Introduction to Public Sector Accounting and Finance ICAN Pack (x) Monetary Economics, 2nd Edition by Jagdish Handa (xi) Public Financial Management (NOUN) by Mr. E. U. Abianga (xii) Monetary Economics: Theory, Policy and Institutions by Anyanwu, J. C. (xiii) Economic Development in Nigeria (NOUN) by Onyemaechi J. Onwe E. COURSE REQUIREMENTS Every student is required to attend the class regularly and participate actively in group discussions and study group activities. Attendance at lecture is compulsory and at least 75% attendance record is mandatory for a student to qualify to sit for the end of semester examination. F. COURSE DELIVERY STRATEGIES/METHODOLOGY Face to face lectures, multi-media presentation class discussion, group work. The course outline along with the complete lecture notes would be made available to the class and would be posted onto the internet. Students are expected to photocopy (and or download) and read the notes before each lecture for better understanding and effective participation during class discussion.

Page 3 of 55

G. BREAK-DOWN OF GRADING S/No. Type

Scores (%) 1 Assignments 20 2 Continuous Assessment

(Tests) 20

3 Final Examination 60 Total Score 100 The continuous assessment marks are to be absorbed through snap test (s) to be given without notice, scheduled test (s) and/or paper presentation.

Page 4 of 55

INTRODUCTION TO PUBLIC FINANCE 1.1 Meaning of Public Finance Finance is a discipline concerned with the acquisition and disbursement of funds in an optimum way for effective operations and attainment of desired objectives of an organization. Finance is a function in business (private/public) that acquires funds for the organisation and manages those funds within the organisation. These activities include preparing of budgets; doing cash flow analysis; and planning for the expenditure of funds assets. Public finance is the field of economics that deals with budgeting the revenues and expenditures of the public, taxes, public debt and public financial administration. Public Finance, therefore, deals with methods used to finance government expenditure, the characters of such expenditures and the keeping of adequate record for money raised and spent. Essentially, Public Finance deals with acquiring, spending and accounting for revenue and other receipts of the government with a view to ensuring efficiency of the state and the general well-being of the people. It is the study of the role of the government in the economy. In recent years, Public Finance has tended to shift from the traditional taxation and expenditure approach to that of stabilisation and general application of macro-economic models. Economists such as Musgrave and Prese focused on resource allocation, income distribution and stabilisation aspects. In respect of resource allocation, Government plays a paramount role in the economy because of market failure. The stabilization aspect of Public Finance is concerned with achieving macro-economic objectives such as: (a) Economic growth and development. (b) Price stability. (c) Balance of payment equilibrium (d) Equitable distribution of income. (e) Full employment.

The principles of public finance were developed as far back as the period of the classical economists. Most of the early writers on the subject focused on different areas. Adam Smith focused on taxation. David Richard and J. S. Mill laid emphasis on revenue, expenditure and public debt. A.C. Pigou in his own contribution dealt with taxation principles which are based on the theory of 'economic welfare'. He stated that taxes are levied in such a way that the overall marginal sacrifice of taxation is equal to the overall marginal benefit of public expenditure.

Public finance encompasses both positive and normative analysis. Positive analysis deals with issues of cause and effect, for example, “If the government cuts the tax rate on gasoline, what will be the effect on gasoline consumption?” Normative analysis deals with ethical issues, for example, “Is it fairer to tax income or consumption?” Modern public finance focuses on the microeconomic functions of government, how the government does and should affect the allocation of resources and the distribution of income. Public financial management is defined by the Chartered Institute of Public Finance and Accountancy (CIPFA) as “the system by which financial management resources are planned, directed and controlled to enable and influence the efficient and effective delivery of public service goals.”

1.2 Nature and Scope of Public Finance The scope of public finance is cover four basic issues, namely (i) government expenditure, (ii) government revenue, (iii) public debt, and (iv) financial management.

(i) Public Revenues: Every government has to make a number of expenditures, both recurrent and capital. For this purpose it has to raise revenues with a view to finance the expenditures and the major share of public revenues is obtained through taxes. Again, government also raises revenue through non-tax sources like fees and penalties. Thus in the science of public finance, different

Page 5 of 55

types of taxes are studied, as well as, the principles of taxation, the burden of taxes, and the system of taxes.

(ii) Public Expenditures: The revenues which a government raises have to be spent on different items. Thus in public finance, the principles of making government expenditures are studied, and the major items of government expenditures. Again, whether the expenditures are diverted to productive fields or non-productive fields, and the effects of public expenditures on the level of income distribution and level of output.

(iii) Public Debt: The government revenues are at times far less than the government expenditures, thus leading to deficit which could necessitates borrowing. The government has to make the traditional as well as the welfare expenditures. In some circumstances, the government expenditures may exceed government revenues, thus necessitating government to depend on public debt. In Public finance, therefore types of public debt that are available to the government are studied; the rate of interest against each source available; the type of bonds the government can issue; and how the government will repay the debt, among others.

(iv) Financial Administration : Financial management is studied in public finance. Financial management deals with how the government prepares budgets, how the budgets are executed, budgetary control process, prudence, transparency and accountability in budget execution and public sector financial management.

A.C. Pigou and Hugh Dalton, in their own contribution to the development of the subject matter of public Finance, proposed taxation principles, which are based on the theory of economic welfare. Essentially, these principles of taxation required the government at the centre to levy taxes in such a way that the overall marginal sacrifices of taxation would be equal to the overall marginal benefits of public expenditure (OMST=OMBPE). The assumption behind this is that welfare would be maximized when expenditure and taxation are carried out in a way such that the benefit obtained from an additional unit of expenditure, is equal to the sacrifice that has to be made when an additional unit of tax is levied.

1.3 Functions of Public Finance The scope of public finance is logically concerned with the operations of the public treasury. It deals with how the public treasury operates as well as the repercussions of the various policies, which the treasury might adopt. Public tax and expenditure measures, affects the economy in a number of ways and may be designed to serve many purposes. The policy objectives which are set forth may be categorized into four, namely: (i) Allocation of resources: The resource allocation aspect in public finance deals with the role of

government in the allocation of resources as a result of market failure. It is a known fact that externalities arise in the economy. Externalities arise because of action by one economic unit which causes a gain or loss in either consumption or production by other non-involved economic units. Clearly, the initiator of the action will not pay the external costs or receive the external benefits unless “there is some form of coercive body” (such as a Government) to allocate either the costs or the benefits. Public Finance is concerned with how Government allocates costs or benefits when externalities arise.

(ii) Adjustment in the distribution of income and wealth: The income distribution aspect of public Finance is concerned with how income is distributed in the economy. Factors of production such as land, labour, capital and entrepreneurship are priced in the market place depending on competitive circumstance and the value of the marginal product. Hence, an individual’s income depends on demand and supply of the factors he has available, plus in some cases, inherited wealth. The resulting income distribution based purely on market pricing may or may not be in line with society’s desires. In this regard, society must determine somehow, the “just” state of income distribution. Some economists have suggested that in order for justice to prevail in the society, income distribution in the economy should

Page 6 of 55

be such that a person should receive the fruits derived from his endowments, others argued that income distribution should be such that total happiness should be maximized. Yet others argued that the aim of income distribution should be egalitarianism, while still others feel that ‘‘justice’’ would be obtained, when the income of the least well off individual in the society is maximized. Public Finance in this regard, is concern with tras1ating these ‘‘rules of justice’’ into a set of policies to distribute income.

(iii) Stabilization of prices and employment: The stabilization aspect in public finance is concerned with how to achieve desirable levels of price stability as well as desirable levels of employment. Without government involvement through fiscal and monetary policies, a typical capitalist economy tends to be subjected to substantial fluctuations. Thus, the economy may be in equilibrium at a level of employment far below what the government desires. When this happens, Government may use fiscal and monetary policies to adjust the economy to the desired levels. Public Finance is concerned with how Government does this.

(iv) Attaining balance of payment equilibrium: Balance of payment is the relationship between visible and invisible import and export of a country over a considerable period of time usually one year. However, when export (which is considered as a + because of the injection of foreign exchange into the economy) is greater than import (which is considered as a- because of letting some part of the economy to go as leakage due to deflation in foreign reserve) balance of a payment is said to be unfavorable. This can be corrected through public finance by embarking on activities which can stimulate export and discourage import to reverse the trend.

1.4 The Role of Taxation in Public Finance The Government of almost every country engages in a number of activities which require the expenditure of funds. In order for the Government to be able to undertake most of these activities, it raises funds through a number of sources taxation. But, taxes are the most important reliable sources of revenue to the government. In every country, there are certain services which the government must provide to the citizens because of their essential nature. The services are essential that, even where individuals are allowed to provide them, they are not allowed to monopolize their supplies or production, so as to ensure their even supply and distribution. The contributions made by individuals and corporate entities in form of taxes, fees and levies therefore serve as the main source of revenue to the government for the supply of such essential services. In this vein, Musgrave and Musgrave (1989) argued that taxation plays three major functions of allocation; stabilization and distribution within an economy. By Allocative function, as spelt out in part 1, section 4 of the Second Schedule of the 1999 constitution of the Federal Republic of Nigeria, provides for the provision of social goods; ensure adequate sharing of resources between social and private goods and creating proper mix of social goods provision. stabilization function is about maintaining price stability; high level of employment; high and sustainable economic growth as well as the attainment of favorable balance of payments. The 1999 constitution of the Federal Republic of Nigeria has outlined the procedure for disbursing the ‘Distributable Pool Account to the three levels of government as per section 162, subsection 1 and 2. So, distribution function promotes equity in income and wealth distribution thereby attaining of a “just” or “fair” state of distribution. To achieve these goals there is a need to adequately address the incidences of revenue leakages, excesses, abuses and fraud by improving various revenues generating capacities and cash flows thereby minimizing operating expenses. T 1.4.2 Theory of Taxation and Incidence of Taxation Taxes are the most important source of revenue for modern economies. The theory of taxation explores how taxes should be levied to enhance economic efficiency and to promote a “fair” distribution of income. Similarly, policy debates about taxation are usually dominated by the question of whether it burden is

Page 7 of 55

distributed fairly. Suppose that the government levies a tax of one dollar on the sellers of a certain commodity. Suppose that prior to the tax, the price of the commodity is N 20, and that after the tax is levied, the price increases to N21. Clearly, the sellers receive as much per unit sold as he did before. The tax has not made them worse off. Consumers pay the entire tax in the form of higher prices. Suppose that instead, the price increases to N 20.25. In this case, sellers are worse off by 75 cents per unit sold; consumers are worse off by 25 cents per unit sold. The burden of the tax is shared between the two groups. Yet another possibility is that after the tax is imposed, the price stays at N 20. If so, the consumer is no worse off, while the seller bears the full burden of the tax. The statutory incidence of a tax indicates who is legally responsible for the tax. All three cases above have exactly the same statutory incidence. But the situations differ drastically with respect to who really bears the burden. The economic incidence of a tax is the change in the distribution of private real income induced by the tax. The example above suggests that the economic incidence problem is fundamentally one of determining how taxes change prices. In the conventional supply and demand model of price determination, the economic incidence of a tax depends on how responsive supply and demand are to prices.

1.4.2 Definition of Tax Tax may therefore be defined as a compulsory contribution made by individuals and corporate entities for the purpose of financing the expenditure of the government. Taxation is therefore the process of levying and collection of tax from taxable persons. A Tax is a fee charged or levied by a government on a product, income, or activity. If it is levied directly on personal or corporate income, it is called a direct tax. If it is levied on the price of a good or service, then it is called an indirect tax. The main reason for taxation is to finance government expenditure and to redistribute income for economic development of a country 1.4.3 Classification of Taxes There are several bases used in the classification of taxes. However, we shall recognize three broad classifications as follows: (i) Classification based on Tax base; (ii) Classification based on Incidence; and (iii) Classification based on Tax rate. 1.4.3.1 Classification Based on Tax Base A Tax base is the object or item on which tax is collected. This could be income, capital, consumption etc. Within the context of the Nigerian Tax Laws, three (3) bases are identifiable. These are:

(i) Income: These are taxes levied on the income of Individual and companies. In Nigeria, the common classifications are: Personal Income Tax, Companies Income Tax and Petroleum Profit Tax.

(ii) Capital: These are taxes levied on asset. The asset could be human or other forms of assets. The Nigerian Tax Law recognizes two forms of Capital taxation i.e. Capital Gains Tax and Capital Transfer Tax. However, the Federal Government of Nigeria has through the 1996 budget abrogated the Capital Transfer Tax.

(iii) Consumption: These are taxes levied on goods and services. The most common forms of consumption tax in Nigeria are the Value Added Tax, Excise Duties and Customs duties.

1.4.3.2 Classification Based on Incidence of Tax An incidence of tax is the impact of tax on the person who pays tax to the Government. Under this classification of tax, two forms of taxes are evident.

Page 8 of 55

(i) Direct Taxes: These are taxes collected directly from the income of individuals and companies whose incidence and burden is on the individuals or the companies that paid the tax to the Government. Examples are Personal Income Tax, Company Income Tax, Petroleum Profit Tax, Capital Gains Tax, etc.

(ii) Indirect Taxes: These are taxes imposed on the value of goods and services, produced and consumed within the country, imported into the country or exported to other countries, whose burden can be shifted in part or in full by the taxpayer who has paid the tax to the government to the final consumers who do not even know either when they pay the tax or the exact amount of the tax they pay. Examples are Value Added Tax, entertainment tax, import duties, export duties, excise duties, etc. Indirect taxes paid by a company usually reflect in the selling price of the goods and Services to be payable by the consumers, depending on the nature of elasticity of demand of the product and other factors.

1.4.3.3 Classification Based on Tax Rate A Tax rate is the portion of tax base paid as tax. Under this classification, the following can be identified.

(i) Progressive Tax: This is a tax which increases as the tax base (i.e. income or stock of wealth being tax) increases. It is commonly found in income taxation and the aim is to achieve equitable distribution of tax burden. For example Mr. A earns N20,000 taxable income and pays 10% as tax (i.e. N,2000) and Mr. B earns a taxable income of N80,000 and pays 20% as tax (i.e. 16,000). In this situation, income tax is progressive, as the tax rate has direct relationship with the tax base (i.e. they change in the same direction).

(ii) Proportional Tax : This is a tax that remains fixed regardless of change in the tax base. In proportional tax, all tax payers, both the rich and the poor are made to pay the same percentage of their income as tax. For example Mr. A earns N20,000 taxable income and pays 10% as tax (i.e. N,2000) and Mr. B earns a taxable income of N80,000 and pays 10% as tax (i.e. 8,000). In this case, the rich pays more than the poor in absolute terms, even thought the tax rate is fixed percentage of the tax base.

(iii)Regressive Tax: This is the tax which decreases as the tax base (i.e. income or stock of wealth being tax) increases. For example Mr. A earns N20,000 taxable income and pays 10% as tax (i.e. N,2000) and Mr. B earns a taxable income of N15,000 and pays 20% as tax (i.e. 3,000). This tax system is usually imposed as punishment for non-performance in situation where the government created an enabling business environment but the citizens are inherently lazy.

1.4.4 Distinction between Tax and Other Levies There are other payments which resemble tax but are not tax. These payments are:

1. Fees: This is a levy imposed with the aim of reducing the cost of each recurrent service undertaken by the Government in public interest but conferring a significant advantage on the fee payer. E.g. registration fees, court fees, school fees, etc.

2. Licenses: This is a charge by Government to grant permission to a person for the performance of a service. E.g. motor vehicle license fees, broadcasting license fees, business registration fees, etc.

3. Fines: This is a levy imposed as a punishment for breach of law with a view to ensuring future adherence.

However, all these levies above are similar to tax because they are compulsory payments and they also serve as a source of income to the Government, but differ from tax in the sense that taxes are not levied in return for any specific service rendered by the Government to the taxpayer. 1.4.5 Purposes of Taxation Government imposes tax for a number of reasons, which include but not limited to the following:

1. Revenue Generation: Government imposed tax to serve as a source of income which can be used in order to finance the construction of schools, building of roads, bridges, hospitals and markets,

Page 9 of 55

provision of pipe-borne water, provision of social, health and educational facilities, provision for defense and protection of lives and properties and provision of funds for the day-to-day running of government (namely salaries and wages, insurance premium, fueling of cars and generators, maintenance of buildings, electricity and telephone charges, etc).

2. Income Re-Distribution: Tax is an important instrument used by the government income re-distribution. Tax is normally charged at a progressive rate to take resources away from those who have more than they need for good living to provide for those who need more than they have for minimum sustenance. Through the income generated by the government, most of which come from the rich, is used to finance the supply of social, health and educational facilities and services, just to mention but a few, most of which is enjoyed more by the poor than the rich.

3. Economic Stabilization: In periods of cyclical trend in economic activities, tax serves as a means of reducing or increasing the disposable income of the consumer, payment of unemployment benefits, supporting ailing industries, changing the pattern of aggregate demand, aggregate supply, national income and mopping-up excess liquidly to check inflation.

4. Discourage the Consumption of harmful goods and services: Tax is used to discourage the consumption of harmful goods and services. In doing this, a higher rate of tax is imposed on such goods as tobacco and alcohol.

5. Protect Infant Industries: The Government imposes tax on imported goods in the form of customs duties, in order to make their prices higher than locally produced items, with a view to protecting infant industries which are not matured enough to favourably compete with their foreign counterparts.

6. Prevent Dumping: Tariffs are usually imposed by the Government on imported goods in order to prevent deliberate attempt by foreign firms to kill local infant industries with a view to possessing monopoly power in the supply of certain goods.

7. Correct Unfavourable Balance of Payment: Taxes are imposed on imported items with a view to discouraging import and encouraging export so as to correct unfavourable balance of payment. For balance of payment to be favourable it thus demands that visible and invisible exports of a country should exceed her visible and invisible import over a period of time, usually one year.

1.4.6 Principles of Taxation These are the rules, qualities, conditions, standards or yardsticks by which the goodness of a tax system is measured and by which a good tax policy can be formulated. Adams Smith was noted to have been the first person to mention the principles of taxation, but he called them cannons of taxation in his book “The Wealth of Nations” in 1776. Although Adams Smith mentioned only four principles, scholars that came after him made some generally accepted additions. Some of these principles include the following:

1. Principle of Equity : This principle states that a good tax system should be as just as possible by ensuring that all persons who ought to pay the tax are covered by the tax and that each taxpayer pays exactly what is just and equitable considering his circumstance and ability. There are two types of equity i.e. vertical and horizontal equity. Vertical equity is the unequal treatment of taxable persons with varied taxable income. While horizontal equity is the equal treatment of tax payers with the same taxable income.

2. Principle of Economy: This principle states that the cost of collecting tax should not be too high so as to outweigh the benefits derivable from the imposition of tax. For example if it costs a government N9milliom to collect tax revenue of N10million, the tax system is said to lack economy.

3. Principle of Certainty : This principle states that the amount to collect as tax, the time of payment, the mode of payment and the place of payment must be made clear to the tax payer, so that the tax payer is not left at the whims and caprice of the tax authorities. In other words, the taxpayer should be fully informed about taxes to be able to arrive at a conclusion as to the amount of tax payable by him with reference to the provision of the tax law, as well as, to

Page 10 of 55

preventing him from being subjected to cheating by unwanted people and dishonest tax officials.

4. Principle of Convenience: This principle states that tax should be imposed at a time, in a manner and at a place that the taxpayer is in position to pay, so that collection of tax would be easy for the tax administrators. E.g. salary earner should be asked to pay tax when he receive his salary and not at the middle or the end of the month when the salary may have been exhausted. This is why the PAYE (Pay-As-You-Earn) is deducted at source, because it is more convenient than requiring the taxpayer to pay after collection of salary and a farmer should be asked to pay tax when he harvest his crops and not when he is doing the planting or clearing the farm.

5. Principle of Simplicity : This principle states that a good tax system and the tax law should be as simple as possible, both in interpretation and application. This requirement is particularly important in developing economy where the rate of illiteracy is high and where the culture of record keeping has not been imbibed by most small scale entrepreneurs.

6. Principle of Neutrality : This principle states that a good tax system should neither distort the consumption habit nor the production decision of a tax payer. In other words, a good tax system should not interfere with people’s willingness to work, produce, consume, save and invest.

7. Principle of Efficiency: This principle states that a good tax system should make it difficult for tax evasion (i.e. should make it difficult for nonpayment of tax or illegal reduction of one’s tax liability).

8. Flexibility : This principle states that a good tax system and tax law should be such that it can be easily amended when the need arises, without unnecessary protocol.

1.4.7 Tax Laws These are the various legal instruments put in place to ensure the realization of the tax policy objectives of the Governments. The notable ones are:

1. Personal Income Tax Act (PITA) CAP P8 LFN 2004 (as Amended in 2011): This law imposes tax on the income of individual, a partner in partnerships, an executor, a trustee, village or community throughout the Federation.

2. Companies Income Tax Act (CITA) CAP C21 LFN 2004: This law applies in relation to companies throughout the Federation.

3. Petroleum Profits Tax Act (PPTA) CAP P13 LFN 2004: This law applies to companies that engage in petroleum exploration and production throughout the Federation.

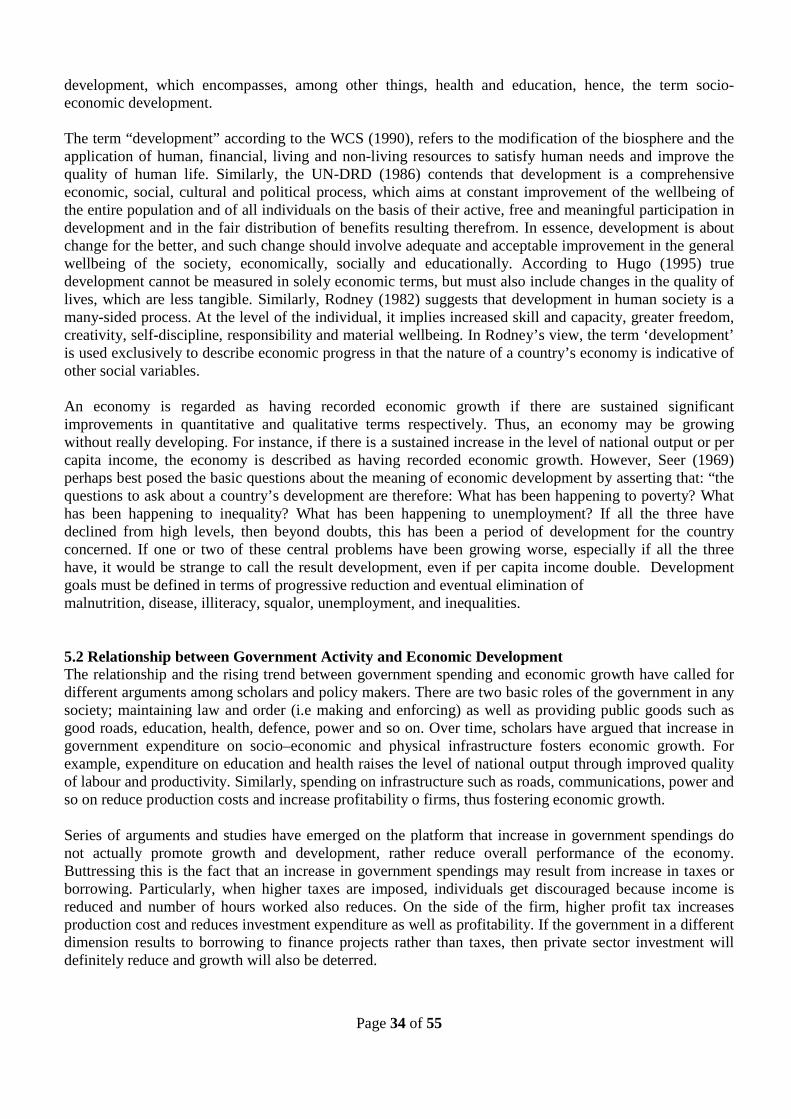

4. Capital Gains Tax Act (CGTA) CAP C1 LFN 2004: This law imposes capital gains tax on any capital gains i.e. gains resulting from the disposal of chargeable assets, by both chargeable individuals and corporate entities throughout the Federation.

5. Value Added Tax Act (VATA) CAP V1 LFN 2004: This is a multi stage tax levied on the value of some selected goods and services that are consumed within the country.

6. Education Tax Act (ETA) CAP E4 LFN 2004: This law imposes tax on the assessable profit of all registered companies throughout Nigeria in order to raise funds for the educational sector.

7. Stamp Duties Act (SDA) CAP S8 LFN 2004: The law imposes tax on documents throughout Nigeria.

2. Government Revenue 2.1 Introduction Government generates revenue from various sources to run its administration machinery and to provide the development projects in all sectors of the economy. Such revenues are generated by the revenue generation agencies and organizations through effective machinery, and allocated through the budgetary system to the spending organizations for their operations. A good system of revenue generation is paramount to ensure that government mobilizes enough financial resources to meet its expenditure programs.

Page 11 of 55

2.2 Meaning of Public Revenue Public revenue could be defined as the funds required by the government to finance its activities. Such funds are generally obtained from various sources, such as taxes, borrowing, fees, fines, income from public undertakings, sales of government assets, rents, mining and royalties, etc. It may be useful, however, to make a distinction between public revenue and public receipts. While public receipt include all sources of income available to the government, public revenue is of much narrower part and does not include borrowing, sale of government assets or income from “printing press” (printing of more money by the CBN). Revenues accruing to an economy, such as Nigeria, can be divided into two main categories, namely oil revenue (which include petroleum profit tax, rent, royalties, and Nigerian National Petroleum Company earnings) and non-oil revenue( include trade income, company income tax, customs and excise duties, and independent revenue sources which consists of fees, licenses, rent on government property, among others). For most of the 1960s, federally-collected revenue was largely revenue from non-oil sources, accounting for an average of 92 percent of the total receipts while revenue from the oil sources accounted for the balance. As can be deduced from the narration of the oil disposition from the 1970s to this day, the non-oil sector revenue accounted for the balance of about 20 to 30 percent receipts annually, to complement the oil sector receipts which form the mainstay of the sources receipts of Federal Republic of Nigeria. Since the 1970s oil revenue became the dominant source of government revenue, contributing over 70 per cent of federally- collected revenue. For most of the 1960s, federally-collected revenue from oil sources accounted for an average of 8 percent of total receipts. The oil boom of the 1970s propelled the sector to become dominant, accounting for most of the foreign exchange earnings as well as federally-collected revenue. The contribution of the oil sector to total receipts increased from average of about 46 percent between 1970 and 1973 to about 77 percent between 1974 and 1980. Through-out the 1980s and 1990s, the contribution of the oil sector to total revenue maintained its dominant position and contributed between 70 and 76 percent of the federally-collected revenue. In addition to the above, Oshisami (1994) categorized revenue accruing to the Government into internally generated revenue and revenue allocation from the Federation Account. There are two main sources via which revenue accruing to the Federation gets to the States and Local governments. These are statutory allocation and non-statutory allocation. The later takes the form of grants as may be deemed fit by the Federal Government to help pursue a policy which in the opinion of the Federal Government should be to the benefit of the country as a whole. Statutory allocation on the other hand is prescribed by law, specifying the basis for distribution of the revenue amongst the three tiers of government, the formulae for distribution and modes of distribution. 2.3 Sources and Classification of Federal/State and Local Government Revenue 2.3.1 Sources of Federal/State Government Revenue Sources of federal/ state government revenue in Nigeria are as follows: (i) Taxes: These refer to the levy collected by the government mostly in the form of company income tax,

petroleum profit tax, value-added tax, education tax (applies to companies), capital gains tax (individuals are under states while corporate bodies and Abuja residents under federal), stamp duties (instruments executed by individuals are states and corporate bodies under federal), withholding tax (individuals under states and companies under federal), personal income tax (residents of the state are under states while personnel of the armed forces, police, external affairs ministry, and residents of Abuja are under the federal), taxes on pool bets, lottery and casino wins, and customs and excise duties (i.e., import and export duties). According to the principles of public finance, tax revenue should be the main source of finance for the public sector. Citizens should be the main contributors of finance for the development of the Nation.

Page 12 of 55

(ii) Non-Tax Revenue: This is made up of all revenues, other than taxes, that are generated by government to finance its expenditures. These include fines, fees and rates, licenses, earnings from sales, rent from government properties, interest payment and repayment of loans, re-imbursement, statutory grant and miscellaneous revenue. a) Fines, Fees and Rates: This include fines imposed on individual, school fees collected from

students, water rate collected from consumers, etc. b) Licenses: These cover amount received for issuance of licenses of various types by the government,

e.g. vehicle licenses, business premises and registration fees in urban and rural areas. c) Earnings from Sales: These cover money realized from the sale of government properties e.g. sale

of government vehicles, houses, earnings from oil sales, etc. d) Rent of Government Properties: These include rent of government houses / quarters and land etc. e) Interest Payment and Repayment of Loan: These are interest payments by government

employees and government companies, on loans granted by the government, e.g. payment of interest on motor vehicle loan and the repayment of the loan itself.

f) Re-imbursements: These are refunds for services rendered to another tier of Government, public corporations and other statutory bodies by the Government.

g) Statutory Grant : This is the share received from the Federation Account and value added tax. h) Miscellaneous: These are sources other than the sources mentioned above, e.g. dividend from

investment, stamp duties, business premises and registration fees, streets name registration fees and fees for right of occupancy on urban land, mining, rents and royalties.

2.3.3 Sources of Local Government Revenue These are other revenues that central government makes available to the local government or district assembly apart from the Common Fund. Examples of these revenues are: (i) Statutory and Non-Statutory Allocation: Revenue accruing to Local Governments from the Federal

government can be categorized into two, namely statutory and non-statutory allocation. The later takes the form of grants as may be deemed fit by the Federal Government to help pursue a policy which in the opinion of the Federal Government should be to the benefit of the country as a whole. Statutory allocation on the other hand is prescribed by law, specifying the basis for distribution of the revenue amongst the three tiers of government, the formulae for distribution and modes of distribution.

(ii) Grants-in-aid: These are donations received from foreign governments through the central government.

(iii) Transfers: These are monies that the central government gives to meet other expenses and pensions of district assemblies’ staff

(iv) Ceded Revenues: These are sources of revenues which the federal government has given over to district assemblies by the virtue of Decree No. 21 of 1998. These include tenancy rates, shops and kiosk rates, fees for on-off liquor licenses, fees for butcher slabs, fees for marriage, birth and death registrations, fees for street name registration (except in the state capital) motor park fees, market taxes and levies (except in any market where state finance is involved), fees for domestic animal licenses, fees for bicycles, trucks, canoes, wheelbarrows, carts and canoes, fees for right of occupancy on land in rural areas (except those of federal and state governments) and cattle tax (applies to cattle farmers only). Others are entertainment and road closure levy, fees for radio and television licenses, vehicle parking and radio license fees, charges for wrongful parking, fees for public convenience, sewage and refuse disposal, customary ground permit fees, fees for permits for religious establishments and fees for permits for signboards, bill boards and advertisements.

2.3 Taxation as a Source of Government Revenue in Nigeria The history of taxation in Nigeria goes back to the pre-colonial rule. There was a system of taxation in existence in the form of contribution of compulsory service, money, farm produce, goods and labour, which were essentially meant to support the various monarchies that existed in the present day Nigeria.

Page 13 of 55

Mainly, these taxes were levied in the form of ground rent, palm fruit tax, farm produce tax, cattle ownership tax, etc. However, history has it that modern tax system as we have today in Nigeria was first introduced in the year 1904 by the late Lord Lugard as community tax in the then Northern Nigeria. He later made changes which resulted to Native Revenue Ordinance of 1917 in Northern Nigeria and a provision for extension to western Nigeria was made in 1918 and 1928. The ordinance was extended to the eastern part of Nigeria in 1929. During the colonial rule taxes were imposed on individuals and corporate entities through a series of promulgations by the Colonial power. In 1940 two major legislations were passed, these were the Direct Taxation Ordinance No. 4 of 1940 and the Income Tax Ordinance No. 3 of 1940. The Direct Taxation Ordinance of 1940 applied to all citizens except those in Lagos Township. The Income Tax Ordinance No. 3 of 1940 applied to expatriates and to Nigerians living in Lagos. Income Tax Ordinance was passed in 1943 repealing the 1940 Ordinance. The 1943 Ordinance together with Direct Taxation (Amendment) Ordinance, 1943 continued to apply until 1956. In 1956 Eastern Region passed the Finance Law No. l of 1956. The basis of computation of tax provided in the Finance Law No. 1 of 1956 was basically the same as in the Ordinance of 1943. In 1956 tax allowances were provided for married taxpayers, and additional allowances for families with children up to a maximum of three children. It also introduced the Pay-As-Your-Earn (PAYE) system of taxation. The Eastern Region Finance Law number 1 became operative in the Region on April 1 1956, thus ceasing the application of Direct Taxation Ordinance in the Region. Another Law was passed in 1962 repealing the 1956 Law. The Western Region departed with the Direct Taxation Ordinance by passing the Income Tax Law in 1957. The Pay-As- You-Earn system was introduced in the Region by the Income Tax (Amendment) Law 1961. To ensure uniformity in both the application and incidence of taxation on individuals throughout Nigeria, the Income Tax Management Act (ITMA) was enacted in 1961, thus repelling all previous laws applicable to individuals, and making main provisions applicable to all individuals throughout Nigeria. In the same vein the Companies Income Tax Act (CITA) of 1961 was also promulgated. Subsequently, ITMA 1961 was repelled and replaced by Personal Income Tax Act (PITA) 1993, which came into being through Decree No. 104 of 1993, while the Companies Income Tax Act (CITA) of 1961 was repelled by the enactment of Companies Income Tax Act (CITA) of 1979. The tax Acts which suffered series of amendments, reassessment and review, are now included in the Laws of the Federation of Nigeria, 2004. Thus, codifying them as Personal Income Tax Act (PITA) CAP P8 LFN 2004 and Companies Income Tax Act (CITA) CAP C21 LFN 2004. Revenue from taxation include direct and indirect taxes. Direct taxes are taxes on individual and companies e.g. companies’ income tax, petroleum profit tax, capital gain tax, bark duty assessment, personnel income tax, surcharge on pioneer companies, with holding tax capital transfer tax, etc. Indirect taxes are taxes raised from goods and commodities in the form of customs and excise duties e.g. import duties export duties excise duty tariffs forfeiture penalty, VAT, etc. Taxation has been an important source of revenue in Nigeria since its introduction in Northern Nigeria by Lord Lugard in 1904.

Page 14 of 55

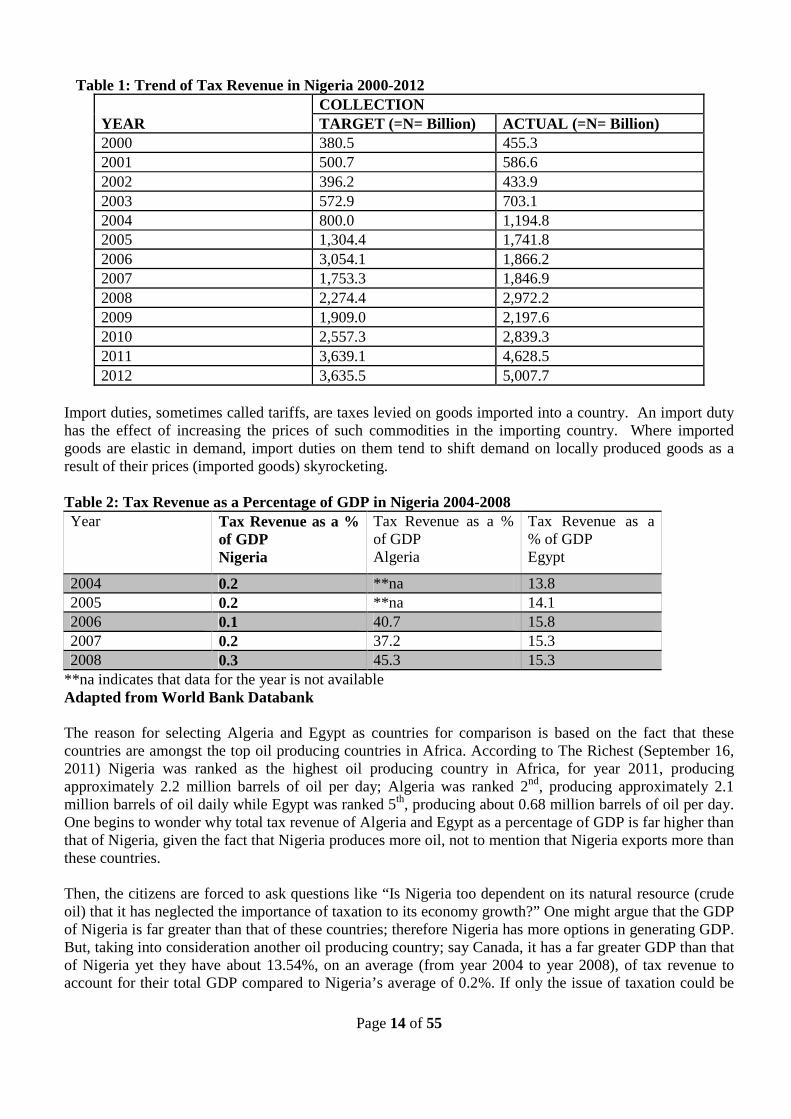

Table 1: Trend of Tax Revenue in Nigeria 2000-2012

YEAR COLLECTION TARGET (=N= Billion) ACTUAL (=N= Billion)

2000 380.5 455.3 2001 500.7 586.6 2002 396.2 433.9 2003 572.9 703.1 2004 800.0 1,194.8 2005 1,304.4 1,741.8 2006 3,054.1 1,866.2 2007 1,753.3 1,846.9 2008 2,274.4 2,972.2 2009 1,909.0 2,197.6 2010 2,557.3 2,839.3 2011 3,639.1 4,628.5 2012 3,635.5 5,007.7

Import duties, sometimes called tariffs, are taxes levied on goods imported into a country. An import duty has the effect of increasing the prices of such commodities in the importing country. Where imported goods are elastic in demand, import duties on them tend to shift demand on locally produced goods as a result of their prices (imported goods) skyrocketing. Table 2: Tax Revenue as a Percentage of GDP in Nigeria 2004-2008 Year Tax Revenue as a %

of GDP Nigeria

Tax Revenue as a % of GDP Algeria

Tax Revenue as a % of GDP Egypt

2004 0.2 **na 13.8 2005 0.2 **na 14.1 2006 0.1 40.7 15.8 2007 0.2 37.2 15.3 2008 0.3 45.3 15.3

**na indicates that data for the year is not available Adapted from World Bank Databank The reason for selecting Algeria and Egypt as countries for comparison is based on the fact that these countries are amongst the top oil producing countries in Africa. According to The Richest (September 16, 2011) Nigeria was ranked as the highest oil producing country in Africa, for year 2011, producing approximately 2.2 million barrels of oil per day; Algeria was ranked 2nd, producing approximately 2.1 million barrels of oil daily while Egypt was ranked 5th, producing about 0.68 million barrels of oil per day. One begins to wonder why total tax revenue of Algeria and Egypt as a percentage of GDP is far higher than that of Nigeria, given the fact that Nigeria produces more oil, not to mention that Nigeria exports more than these countries. Then, the citizens are forced to ask questions like “Is Nigeria too dependent on its natural resource (crude oil) that it has neglected the importance of taxation to its economy growth?” One might argue that the GDP of Nigeria is far greater than that of these countries; therefore Nigeria has more options in generating GDP. But, taking into consideration another oil producing country; say Canada, it has a far greater GDP than that of Nigeria yet they have about 13.54%, on an average (from year 2004 to year 2008), of tax revenue to account for their total GDP compared to Nigeria’s average of 0.2%. If only the issue of taxation could be

Page 15 of 55

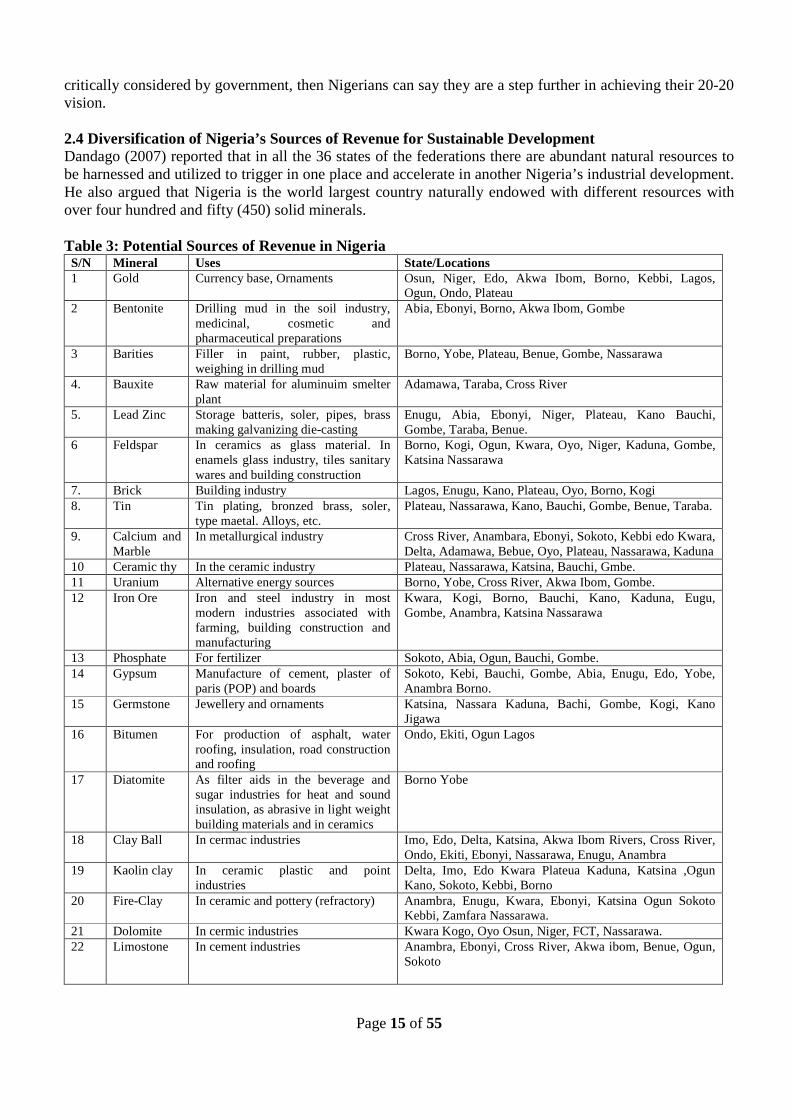

critically considered by government, then Nigerians can say they are a step further in achieving their 20-20 vision. 2.4 Diversification of Nigeria’s Sources of Revenue for Sustainable Development Dandago (2007) reported that in all the 36 states of the federations there are abundant natural resources to be harnessed and utilized to trigger in one place and accelerate in another Nigeria’s industrial development. He also argued that Nigeria is the world largest country naturally endowed with different resources with over four hundred and fifty (450) solid minerals. Table 3: Potential Sources of Revenue in Nigeria S/N Mineral Uses State/Locations 1 Gold Currency base, Ornaments Osun, Niger, Edo, Akwa Ibom, Borno, Kebbi, Lagos,

Ogun, Ondo, Plateau 2 Bentonite Drilling mud in the soil industry,

medicinal, cosmetic and pharmaceutical preparations

Abia, Ebonyi, Borno, Akwa Ibom, Gombe

3 Barities Filler in paint, rubber, plastic, weighing in drilling mud

Borno, Yobe, Plateau, Benue, Gombe, Nassarawa

4. Bauxite Raw material for aluminuim smelter plant

Adamawa, Taraba, Cross River

5. Lead Zinc Storage batteris, soler, pipes, brass making galvanizing die-casting

Enugu, Abia, Ebonyi, Niger, Plateau, Kano Bauchi, Gombe, Taraba, Benue.

6 Feldspar In ceramics as glass material. In enamels glass industry, tiles sanitary wares and building construction

Borno, Kogi, Ogun, Kwara, Oyo, Niger, Kaduna, Gombe, Katsina Nassarawa

7. Brick Building industry Lagos, Enugu, Kano, Plateau, Oyo, Borno, Kogi 8. Tin Tin plating, bronzed brass, soler,

type maetal. Alloys, etc. Plateau, Nassarawa, Kano, Bauchi, Gombe, Benue, Taraba.

9. Calcium and Marble

In metallurgical industry Cross River, Anambara, Ebonyi, Sokoto, Kebbi edo Kwara, Delta, Adamawa, Bebue, Oyo, Plateau, Nassarawa, Kaduna

10 Ceramic thy In the ceramic industry Plateau, Nassarawa, Katsina, Bauchi, Gmbe. 11 Uranium Alternative energy sources Borno, Yobe, Cross River, Akwa Ibom, Gombe. 12 Iron Ore Iron and steel industry in most

modern industries associated with farming, building construction and manufacturing

Kwara, Kogi, Borno, Bauchi, Kano, Kaduna, Eugu, Gombe, Anambra, Katsina Nassarawa

13 Phosphate For fertilizer Sokoto, Abia, Ogun, Bauchi, Gombe. 14 Gypsum Manufacture of cement, plaster of

paris (POP) and boards Sokoto, Kebi, Bauchi, Gombe, Abia, Enugu, Edo, Yobe, Anambra Borno.

15 Germstone Jewellery and ornaments Katsina, Nassara Kaduna, Bachi, Gombe, Kogi, Kano Jigawa

16 Bitumen For production of asphalt, water roofing, insulation, road construction and roofing

Ondo, Ekiti, Ogun Lagos

17 Diatomite As filter aids in the beverage and sugar industries for heat and sound insulation, as abrasive in light weight building materials and in ceramics

Borno Yobe

18 Clay Ball In cermac industries Imo, Edo, Delta, Katsina, Akwa Ibom Rivers, Cross River, Ondo, Ekiti, Ebonyi, Nassarawa, Enugu, Anambra

19 Kaolin clay In ceramic plastic and point industries

Delta, Imo, Edo Kwara Plateua Kaduna, Katsina ,Ogun Kano, Sokoto, Kebbi, Borno

20 Fire-Clay In ceramic and pottery (refractory) Anambra, Enugu, Kwara, Ebonyi, Katsina Ogun Sokoto Kebbi, Zamfara Nassarawa.

21 Dolomite In cermic industries Kwara Kogo, Oyo Osun, Niger, FCT, Nassarawa. 22 Limostone In cement industries Anambra, Ebonyi, Cross River, Akwa ibom, Benue, Ogun,

Sokoto

Page 16 of 55

S/N Mineral Uses State/Locations 23 Sand (Glass

sand) In glass industries Edo, Delta, Ondo, Ekiti, Rivers, Bayelsa, Anambra, Enugu,

Ebonyi, Imo, Abia Kogi, Lagos, Nassarawa 24 Salt For nutritional purposes Ebonyi, Benue, Imo Abia Enugu, Anambra, Cross River,

Plateau, Nassarawa Akwa Ibom, Kebbi. 25 Soda Ash For various purposes Borno, Yobe, Kano, Jigawa. 26 Talc In paint and cosmetic industries Oyo, Osun, Ondo, Ekiti, Niger, Kog, FCT, Kwara

Nassarawa Source: Dandago (2007:106-111) The analysis of Table 3 reveals that there are twenty six (26) mineral deposits endowed in virtually all 36 states of the Federal Republic of Nigeria that could be mined for various forms of utilization. These mineral resources could be used as agents of industrializing Nigeria, accelerating the level of employment by increasing the earning propensity of the citizenry which in the long term will trigger high level of national output. The exploration of these resources will immensely contribute to credits of the Federation Account by improving the revenue generation capacity of the states of their domain by the 13% share. From the table it is reported that, for example, Anambra, Ebonyi, Benue, Cross River, Akwa ibom, Benue, Ogun, Sokoto have deposited in their areas Limostone used in producing cement. In another revelation, the table shows Delta, Imo, Edo Kwara Plateua Kaduna, Katsina ,Ogun Kano, Sokoto, Kebbi, Borno with adundant deposits of Kaolin clay for ceramic, plastic and point industries. Katsina, Nassara Kaduna, Bachi, Gombe, Kogi, Kano Jigawa states have Germstone for Jewellery and ornaments. Furthermore, there is large gold endowment in Osun, Niger, Edo, Akwa Ibom, Borno, Kebbi, Lagos, Ogun, Ondo, Plateau states. Evidently, surveys reported that such resources are in large quantities could be explored for quite a long period. Central Bank of Nigeria (CBN, 2012) reported that oil revenue accounted for up to 80% of the composition federation account with contribution to the country’s Gross Domestic Product (GDP) of 25.9%, 12.9%, 15.9%, 23.7% and 19.8% in 2008, 2009, 2010, 2011 and 2012 respectively. The report also showed that non-oil revenue accounted for the average of 6.06 contributions to GDP over the period under review. This is not plausible enough to rely on oil alone as the major source for Nigeria’s revenue even without the associated challenges. There is an urgent need for the government to identify and explore other potential revenue generating avenues dominant within the jurisdiction of Nigeria. For instance, there are abundant natural resources endowed in various locations across the 36 states of the federation untapped. It is evidently established that if these resources were to be tapped could not only generate sufficient revenue for the country to facilitate the realization of vision 20:20:20, the project could launch Nigeria among the most industrialized countries. In addition to the mineral exploration, the country is blessed with large wealth of agricultural products both for food and cash crops as well as animal products. These products could make Nigeria self sufficient in its own food production and self reliant in the provision of the necessary raw material for industrial consumption. For example, Dandago (2007) argued that if Nigeria adequately harness its agricultural potentials in food cultivation could favorably compete with Thailand in Rice Production from 17 states alone ( Akwa ibom, Benue, Gombe, Kano, Kogi, Ebonyi states among others). In Cotton could compete with Indonesia, Malaysia for raw material provision to Textile and milling industries of the country from only 10 states. In Palm produce Nigeria could enjoy competitive advantage over even Malaysia from 21 states of South-south, South-east and west including some states from the North. Nigeria has edge in tourism industry. Much a lot of revenue can be generated from tourism. Revenue centers can be created in various states’ tourist sites. For example, in Akwa Ibom, Wildlife park, Oron National Meseum etc, Anambra: Nkisi stream Onitsha, Ofala Festival, igbo ukure, palace of Oba, Cross River: Ogbudu Cattle Ranch, Ekpe Masquerade. With all abundant tourist attractions Nigeria is endowed, yet revenue generation and exchange earning are insignificant in the aggregate revenue of the country. It is

Page 17 of 55

on record that there are other countries of the world that relied on tourism as a major source of revenue and that it accounts significantly in their national income. For example Egypt, United States of America, Kenya, South Africa and the rest. Even in the area of taxation a lot is desired to be done to develop other forms of taxes to improve the complexion from taxation. Jimoh (2007) argued that some reasons are against proper generation of revenue from taxation in Nigeria. Some of the reasons, according to him, include subsistent nature of the economy; Tax avoidance and evasion; level of income; tax revenue leakages among others. 3. Public Expenditure Public expenditure refers to the expenses which Government incurs in the performance of its operations. With increasing State activities, it may be difficult to judge what portion of public expenditure can be ascribed to the maintenance of Government itself and what portion to the benefit of the society and the economy as a whole. 3.1 The Theory of Public Expenditure Two notable theories of public expenditure are examined, viz: (a) "The Law of Increasing State Activities": A German Economist- Adolph Wagner in 1890 postulated this theory. According to him, there are inherent tendencies for the activities of Government to grow, both intensively and extensively. He added that there exists a functional relationship between the growth of an economy and that of Government activities, and that the Governmental sector grows faster than the economy. All categories of Governments, irrespective of their levels, intentions and sizes, had exhibited the same kind of tendencies of increased expenditure. (b) "The Displacement Theory": Jack Wiseman and Allan T. Peacock put forth the theory in 1961. Their main argument was that public expenditure does not increase in a straight or continuous manner, but in "Jack or Stepwise" fashion. At times, some social or other disturbances occur which show the need for increase in public expenditure, which the existing level of revenue cannot meet. Therefore, public expenditure increases will make the inadequacy of the existing level of revenue clear to everyone. The movement from the initial and low level of expenditure and taxation to a new and higher level is known as the "displacement effect," while the inadequacy of the revenue as compared with the required expenditure creates the "inspection effect." Both Government and the people would attain a new level of "tax tolerance" by reviewing the revenue position and finding solution to the problem of inadequate finance. Since each major disturbance always leads Government to assume a larger proportion of the national economic activities, the net result is the 'concentration effect'. Therefore, 'concentration effect' is the tendency for Government activities to grow faster than the economy. 3.2 Types of Expenditures Public expenditure may be classified on the following basis:

(i) Nature of Expenditure Incurred: Under this basis Government expenditure is broadly divided in to two (2) main categories, namely recurrent expenditure and capital expenditure: (a) Recurrent/revenue expenditures: Recurrent expenditure is the type of expenditure that happens

repeatedly on daily, weekly or even monthly basis. This includes for example payment of pensions and salaries, administrative overheads, maintenance of official vehicles, payment of electricity and telephone bills, water rate and insurance premiums etc.

(b) Capital or development expenditures: Capital expenditure on the other hand refers to expenditure on capital projects. This includes construction of houses, roads, schools and hospitals, human capital development (expenditures on education and health), purchase of official vehicles, construction of boreholes and electrification projects, etc.

(ii) Economic Purpose for Expenditure: Under this basis we have three classes, namely: (a) Government consumption: Government purchases of goods and services for current use. (b) Government Investment: Purchases of goods intended to create future benefits e.g. infrastructure,

education and research and development.

Page 18 of 55

(c) Transfer payments: Transfers that do not involve purchase of any good or service, eg. unemployment benefits, scholarships, social welfare support, interest on public debt, etc.

(iii) Unit of government involved: Under this basis we have: (a) Federal government and its MDAs (b) State government and its MDAs (c) Local government (d) Separate Government bodies

(iv) Basis of function at which expenditure is directed: a) justice and public order; b) infrastructure (roads, railways, etc); c) military; d) Education; e) health care; f) support for the poor, the old, the disadvantaged; g) support for firms, export and production in general; h) special policy expenditure (e.g. foreign aid, fight against drugs, etc). –

(v) Kinds of goods and services purchased. This gives rise to three sub-classifications: a) capital goods; b) consumption goods; c) personnel expenditure. (In national accounts, public expenditure does not include transfers among social groups, such as pensions, and interest payments of public debt).

3.3 Models of a State

The starting point is to understand that public spending nearly corresponds to three general models of state to which a government may subscribe. In other words, how much a government spends, overall, depends on which of these political frameworks it has chosen as the foundation for running its affairs. These models are: 1) The minimal state: where justice , public order, foreign policy and some basic functions should be carried out by the state; relaying on private sector for the rest. The minimal state is currently the trend and is manifested in the drive towards less- government and greater privatization in what advocates call public sector reforms; 2) The welfare state: where the state cares about the people’s well being directly, also through expenditure in education, health, and support for the poor, the old, and the disadvantaged; 3) The developmental state: where the state takes the responsibility of promoting economic development; also through expenditure in infrastructure, support for firms, export and production in general. Items of the minimal state are found in both welfare and developmental states. However, military and special spending is common to all three models, even though in different proportions. Government expenditure virtually depends on the model of state chosen. 3.4 Determinants and Types of Public Expenditure Determinants-Public expenditure is determined, generally, by:

(a) The political will of those at the helm of affairs of the government; (b) their priorities, (c) chosen state-model (d) interpretation of current economic and political trend.

Page 19 of 55

(e) other factors: Urbanization; Population; Economic growth; Depreciation; Technological change; and Reduction in inequality.

3.5 Reasons for Increase in Government Expenditure A number of factors have been identified as causing increasing in public expenditure in various countries over time. Some of these are general, having relevance to all countries, while others are specific to certain countries. These factors include the following:

(i) The traditional functions of government such as defense, maintenance of law and order, etc. are becoming extensive and cumbersome. Defense is becoming expensive more than ever. Within the country administrative set up is increasing both in coverage and intensity, that is, government machinery has to be manned by experts in their respective fields. In addition, various complexities of economic and social measures develop which make an efficient administration complex and expensive as well.

(ii) Besides the traditional functions of the state, there is growing awareness of additional responsibilities. The government is expanding its activities in the area of various welfare measures which include measures to enrich the cultural life of the society and those designed to provide social securities to the people such as pensions, old peoples’ home etc.

(iii) Increasing population may also be a determinant of public expenditure growth. The share scale of various public goods and services has to rise in conformity with the growth of population. The need for more schools, hospitals and such likes cannot be over-emphasized is the light of increasing population.

(iv) It has been suggested that urbanization and the resulting congestion has increased the need for more infrastructure and public goods and services. Also quite a number of incidental services like those connected with traffic, roads, pedestrian bridge etc. has to be provided.

(v) The tendency for prices to go up has equally contributed to the growth of public expenditure. The increase in prices of input and other goods purchased by public sector has resulted in an increase in public expenditure. It is the responsibility of the government to protect the citizenry against the evils of price mechanism. Consequently, anti-cyclical and other regulatory measures are put in place. Efforts are made to reduce income and wealth inequalities and bring about social and economic justice.

(vi) Increasing public expenditure can also he explained in terms of increasing cost of debt servicing. Since states are related to one another through various economic transactions, there are tendencies to run into debts, which must be settled.

3.6 Purposes/Functions of Public Expenditure The effects of public expenditure include the following:

1. Economic Stabilization: The philosophy of laisser faire leaves much to be desired in terms of economic results. The more advanced and free the market mechanism, the more prone the economy is to the vagaries of income, employment and price fluctuations. Public expenditure as an anti-cyclical tool can be devised in such a manner as to create effective demand thereby stimulating investment activities. It may be emphasized that the total demand need he regulated so that the demand flows match the supply flows otherwise the stimulating effect would result in inflationary pressure.

2. Production: Public expenditure can help the economy to attain a higher level of production. Through stimulation of investment, it can create conditions favourable for market forces to push up production.

Page 20 of 55

It can be used to create human skills through education and training and maintenance of social overheads. Public sector investment can be specifically directed towards creation of particular supplies and facilities, which may form an important and necessary input for other industries. Through research and development, new and effective methods of production can be found whereby local resources are used.

3. Economic Growth: Economic growth can be defined as an increase in a country’s physical output over a long period of time. A country is said to have experiment economic growth, when the real output of goods and services is increasing at a faster rate than the rate of growth of its population. Countries pursue economic growth in order to enjoy the benefit of a greater output, hence improve their standard of living. In a developed economy, through economic stabilization, stimulation of investment activities and so on, public expenditure helps to maintain a smooth growth rate. In an under-developed economy. Public expenditure has important role to play in reducing regional disparities, developing social overheads, creation of infrastructure for economic growth in terms of communication and transportation facilities, education and training, growth of capita] goods industries, research and development etc. When expenditure is incurred, it may be directed towards a particular investment or it may be used to bring about re-allocation of investible resources in the private sector of the economy. An important way in which expenditure can accelerate the rate of economic activities is by reducing the divergence between the social and marginal productivity of certain investment.

4. Economic Development: Economic development cat be defined as the elimination or reduction in poverty, inequality and unemployment within the context of a growing economy, there may be growth without economic development.

5. Distribution: An important evil of the market mechanism is the inequalities of income and wealth, which arise on account of it and get widened through the institution of private property and inheritance Furthermore, such income and wealth disparities not only result in social and economic injustice but also distort production and employment patterns. Suffice to say that lesser income and wealth inequalities contribute towards economic stability. Welfare consideration favours an equitable distribution of income and wealth since the purpose of economic policy is to attain the maximum level of social benefits possible. A shift towards equality may be achieved through various forms of public expenditure especially those that are meant to help the poorer sector of the society. Items of common consumption may be subsidized and production of those, which are in short supply, can be taken up by Public Sector. Left for the market mechanism the supply of merit goods tiny in be possible. Public Expenditure through direct purchase production or subsidies can ensure that their supply is augmented to the desired level and can reduce unemployment and improve income and wealth distribution.

6. Price Stability: Price stability refers to a situation where the general level of process of goods and services changes very little or no changes at all. Price level stability exists when the annual rate of increases in prices measured by appropriate indexes is less than 2%. Common measures of price stability are: (i) Consumer price index (measure of level of prices of all new domestically produced goods and service); (ii) Wholesale price index; and (iii) National product deflator (an economic metric that accounts for the effect of inflation in the current year’s GNP by converting its output to a level relative to a base period).

7. Full Employment: Full employment is a concept that cannot be precisely defined. Full employment does not mean that everyone has a job. This is because there shall always be people, such as babies, under-aged kids, very old people who cannot work even if they are willing to do so. This situation makes every government to define its full employment level e.g. in US full employment level is 97%. In Canada it is 96%, then the balance being the unemployment rate. In Nigeria, however, full employment policy has not been given a place of prominence and specific

Page 21 of 55

target has not been mentioned, Unemployment is a welfare loss to the society in terms of total output that is being forgone. It is equally a welfare burden borne by individuals.

8. Balance of Payment (BOP) Equilibrium: Balance of Payment (BOP) equilibrium is a record of a country’s transaction with the rest of the world over a period of time in respect of visible and invisible items. The balance of payment provides an indicator of a country’s international economic position. Because of the importance of the above, balance of payment equilibrium becomes an important objective of economic stabilization policy.

9. Equitable Distribution of Incomes: This has to do with how income is being distributed in the economy in a fair and equitable manner. Unfortunately in less developed countries, the income distribution pattern is an asymmetrical one, i.e. it is not evenly distributed. This accounted for the widespread poverty in these countries. The policy investment usually used to achieve the above macro-economic objective are: (i) Monetary Policies (cost, allocation and distribution of credit to change the level of money supply); (ii) Fiscal Policies (government spending and levying taxes to achieve macroeconomic objectives); (iii) Incomes Policy (regulation of reward to factors of production, minimum and maximum prices, minimum wages, rent and interest). The monetary policy is a measure designed to influence cost, allocation and is tribulation of credit in order to change the level of money supply in the economy. This fiscal policy refers to the deliberate action, which the government of a country takes in areas spending money and/or levying taxes with the objective of achieving macro-economic variable. The income policy on the other hand relates to the regulation of the rewards that go to the factors of production such as labour (minimum wage legislation). It equally includes the registration of product prices (minimum and maximum price legislation).

3.8 Standard Expenditure Decisions Expenditure decisions should be guided by the following standards, among others: a) Economy: The nation's resources are scarce, compared with the needs of the society. It is therefore important that no wastage is allowed in public expenditure. The process of public spending should not involve the use of more resources than are actually necessary wasteful usage of public fund must be avoided. Scientific approach towards assessment of required expenditure must be adopted. Budgeting techniques such as Planning and Programming Budgeting System and Zero-Base Budgeting System could be adopted. (b) Benefit: Every public expenditure should be viewed against the benefits that will accrue there from. It should be incurred only if it is beneficial to the society. (c) Surplus: Government should avoid persistent deficit budgeting. It should be consistently prudent and aim at meeting its current expenditure needs out of current revenue. Government should not over- spend and eventually run into debt. Moderate surpluses over some years will take care of any unavoidable deficit during any other year. (d) Sanction: All public expenditure should be subjected to legal appropriations and authorisations. Any contravention of expenditure procedure and due process should be sanctioned. As required by law all unspent appropriations should be returned to the Treasury at the financial year end.

3.9 Public Expenditure Management and Control: The management and control of public expenditure is a responsibility that falls on government institutions and individual public servants. As an institutional duty, both executive and parliamentary arms of government have constitutional roles aimed at ensuring the proper disbursement of public fluids. Individually, all civil servants who handle government funds and properties are required to observe certain rules and guidelines in ensuring appropriate custody and spending of public monies. For clarity, expenditure management and control are discussed separately, although they are inter-related.

Page 22 of 55

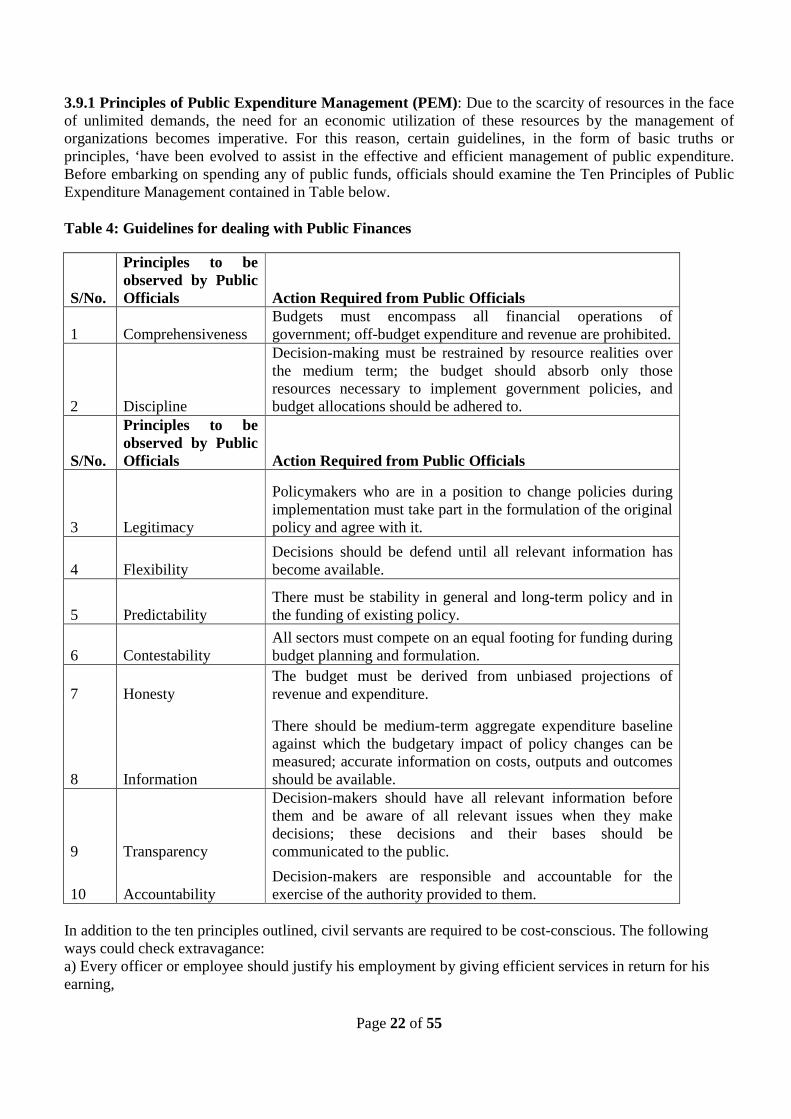

3.9.1 Principles of Public Expenditure Management (PEM): Due to the scarcity of resources in the face of unlimited demands, the need for an economic utilization of these resources by the management of organizations becomes imperative. For this reason, certain guidelines, in the form of basic truths or principles, ‘have been evolved to assist in the effective and efficient management of public expenditure. Before embarking on spending any of public funds, officials should examine the Ten Principles of Public Expenditure Management contained in Table below.

Table 4: Guidelines for dealing with Public Finances

S/No.

Principles to be observed by Public Officials Action Required from Public Officials

1 Comprehensiveness Budgets must encompass all financial operations of government; off-budget expenditure and revenue are prohibited.

2 Discipline

Decision-making must be restrained by resource realities over the medium term; the budget should absorb only those resources necessary to implement government policies, and budget allocations should be adhered to.

S/No.

Principles to be observed by Public Officials Action Required from Public Officials

3 Legitimacy

Policymakers who are in a position to change policies during implementation must take part in the formulation of the original policy and agree with it.

4 Flexibility Decisions should be defend until all relevant information has become available.

5 Predictability There must be stability in general and long-term policy and in the funding of existing policy.

6 Contestability All sectors must compete on an equal footing for funding during budget planning and formulation.

7 Honesty The budget must be derived from unbiased projections of revenue and expenditure.

8 Information

There should be medium-term aggregate expenditure baseline against which the budgetary impact of policy changes can be measured; accurate information on costs, outputs and outcomes should be available.

9 Transparency

Decision-makers should have all relevant information before them and be aware of all relevant issues when they make decisions; these decisions and their bases should be communicated to the public.

10 Accountability Decision-makers are responsible and accountable for the exercise of the authority provided to them.

In addition to the ten principles outlined, civil servants are required to be cost-conscious. The following ways could check extravagance: a) Every officer or employee should justify his employment by giving efficient services in return for his earning,

Page 23 of 55