SEE APPENDIX I FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS Company Update 9 July 2013 PP16832/01/2013 (031128) Malaysia Padini Holdings Not The Time To Shop Yet Maintain SELL. Padini’s share price has retreated from its peak of MYR2.17, but we believe that a better opportunity would be to accumulate the shares after the upcoming 4QFY6/13 results (typically annou nced towards end-Aug), which we expect to be weaker YoY. Our net profit forecasts for FY6/13-15 are adjusted by -6%/-3%/+2%. Maintain SELL with a marginally lower TP of MYR1.75 (-5sen), based on 12x FY6/14 PER (unchanged). Another weak quarter. The upcoming 4QFY6/13 results will likely be weak due to the absence of festivals in the quarter as well as cautious sentiment ahead of the 13 th General Election on 5 May. Shopping activities had apparently slowed down before the election as voters were busy attending campaign rallies nationwide and did not recover much after the election. On that note, we have trimmed our FY6/13 net profit forecast to MYR80.8m (from MYR85.8m), expecting the group to report a subdued net profit of MYR11.1m in 4QFY6/13 (-26% YoY). Additional 90,000 sq ft in 1HFY6/14. The group will open 7 large stores in 1HFY6/14, comprising 3 Padini Concept Stores (+50,000 sq ft) in Penang, Miri and Seremban and 4 Brands Outlets (+40,000 sq ft) in Penang, Miri, Seremban and Langkawi. There could be a few more new outlets in 2HFY6/14, depending on the completion of upcoming retail space in Sunway Velocity, Sunway Putra Place, etc. We increase our new retail space assumption to 110,000 sq ft (80,000 sq ft previously). To move out from Gurney Plaza. At the end of its tenancy agreement in Dec 2014, Padini will close down its stores in Gurney Pl aza, Penang, given the close proximity and cheaper rentals in Gurney Paragon, which is to open in July 2013. We are neutral on this as it depends on Gurney Paragon’s abil ity to attract footfall from Gurney Plaza. Higher dividend payout. We expect a 10sen DPS (2.5sen/quarter) for FY6/14 which translates to a 69% net profit payout. Dividend yields of 4-5% may provide some support to the share price, but PER valuations at this stage (12x CY14) are already >1 SD abo ve mean of 10.7x. Padini Holdings – Summary Earnings Table Source: Maybank KE FYE Jun (MYR m) 2011A 2012A 2 013F 2014F 2015F Revenue 568.5 725.2 746.8 837.2 978.6 EBITDA 126.9 150.9 134.9 155.8 177.8 Recurring Net Profit 75.7 96.0 80.8 95.8 109.8 Recurring Basic EPS (sen) 11.5 14.6 12.3 14.6 16.7 EPS growth (%) 24.1% 26.8% (15.9%) 18.6% 14.7% DPS (sen) 4.0 6.0 8.0 10.0 11.0 BVPS (MYR) 0.43 0.52 0.56 0.61 0.67 PER 16.1 12.7 15.1 12.7 11.1 EV/EBITDA (x) 8.9 7.5 8.2 7.0 6.1 Div Yield (%) 2.2 3.2 4.3 5.4 5.9 P/BV(x) 4.3 3.6 3.3 3.0 2.8 Net Gearing (%) Cash Cash Cash Cash Cash ROE (%) 29.3% 30.8% 22.8% 24.9% 26.2% ROA (%) 18.9% 20.7% 15.9% 17.2% 17.9% Consensus Net Profit (MYR m) na na 90.7 102.9 114.2 Earnings Revision (%) na na -6% -3% +2% Sell (unchanged) Share price: MYR1.85 Target price: MYR1.75 (from MYR1.80) Kang Chun Ee [email protected] (603) 2297 8675 Stock Information Description: Retail garments, shoes and accessories. Ticker: PAD MK Shares Issued (m): 657.9 Market Cap (MYR m): 1,217.1 3-mth Avg Daily Turnover (US$ m): 0.92 KLCI: 1,762.87 Free float (%): 50.1 Major Shareholders: % PANG CHAUN YONG 44.0 SKIM AMANAH SAHAM 5.0 Key Indicators Net cash / (debt) (MYR m): 91.9 NTA/shr (MYR): 0.43 Net Gearing (x): (0.3) Historical Chart 0.4 0.9 1.4 1.9 2.4 2.9 Jul-11 Nov-11 Mar-12 Jul-12 Nov-12 Mar-13 PAD MK Equity Performance: 52-week High/Low MYR2.37/MYR1.69 1-mth 3-mth 6-mth 1-yr YTD Absolute (%) (11.5) (5.1) (2.1) (0.5) - Relative (%) (10.8) (9.5) (6.2) (9.3) (4.4)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 1/8

SEE APPENDIX I FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

Company Update 9 July 2013

PP16832/01/2013 (031128) Malaysia

Padini HoldingsNot The Time To Shop Yet

Maintain SELL. Padini’s share price has retreated from its peak of

MYR2.17, but we believe that a better opportunity would be to

accumulate the shares after the upcoming 4QFY6/13 results (typically

announced towards end-Aug), which we expect to be weaker YoY. Our

net profit forecasts for FY6/13-15 are adjusted by -6%/-3%/+2%.

Maintain SELL with a marginally lower TP of MYR1.75 (-5sen), based

on 12x FY6/14 PER (unchanged).

Another weak quarter. The upcoming 4QFY6/13 results will likely beweak due to the absence of festivals in the quarter as well as cautious

sentiment ahead of the 13th

General Election on 5 May. Shopping

activities had apparently slowed down before the election as voters

were busy attending campaign rallies nationwide and did not recover

much after the election. On that note, we have trimmed our FY6/13 net

profit forecast to MYR80.8m (from MYR85.8m), expecting the group to

report a subdued net profit of MYR11.1m in 4QFY6/13 (-26% YoY).

Additional 90,000 sq ft in 1HFY6/14. The group will open 7 large

stores in 1HFY6/14, comprising 3 Padini Concept Stores (+50,000 sq ft)

in Penang, Miri and Seremban and 4 Brands Outlets (+40,000 sq ft) in

Penang, Miri, Seremban and Langkawi. There could be a few more newoutlets in 2HFY6/14, depending on the completion of upcoming retail

space in Sunway Velocity, Sunway Putra Place, etc. We increase our

new retail space assumption to 110,000 sq ft (80,000 sq ft previously).

To move out from Gurney Plaza. At the end of its tenancy agreement

in Dec 2014, Padini will close down its stores in Gurney Plaza, Penang,

given the close proximity and cheaper rentals in Gurney Paragon,

which is to open in July 2013. We are neutral on this as it depends on

Gurney Paragon’s ability to attract footfall from Gurney Plaza.

Higher dividend payout. We expect a 10sen DPS (2.5sen/quarter) for

FY6/14 which translates to a 69% net profit payout. Dividend yields of

4-5% may provide some support to the share price, but PER valuations

at this stage (12x CY14) are already >1 SD above mean of 10.7x.

Padini Holdings – Summary Earnings Table Source: Maybank KE

FYE Jun (MYR m) 2011A 2012A 2013F 2014F 2015FRevenue 568.5 725.2 746.8 837.2 978.6EBITDA 126.9 150.9 134.9 155.8 177.8Recurring Net Profit 75.7 96.0 80.8 95.8 109.8Recurring Basic EPS (sen) 11.5 14.6 12.3 14.6 16.7EPS growth (%) 24.1% 26.8% (15.9%) 18.6% 14.7%DPS (sen) 4.0 6.0 8.0 10.0 11.0BVPS (MYR) 0.43 0.52 0.56 0.61 0.67

PER 16.1 12.7 15.1 12.7 11.1EV/EBITDA (x) 8.9 7.5 8.2 7.0 6.1Div Yield (%) 2.2 3.2 4.3 5.4 5.9

P/BV(x) 4.3 3.6 3.3 3.0 2.8Net Gearing (%) Cash Cash Cash Cash CashROE (%) 29.3% 30.8% 22.8% 24.9% 26.2%ROA (%) 18.9% 20.7% 15.9% 17.2% 17.9%Consensus Net Profit (MYR m) na na 90.7 102.9 114.2 Earnings Revision (%) na na -6% -3% +2%

Sell (unchanged)

Share price: MYR1.85Target price: MYR1.75 (from MYR1.80)

Kang Chun [email protected](603) 2297 8675

Stock Information

Description: Retail garments, shoes and accessories.

Ticker: PAD MKShares Issued (m): 657.9Market Cap (MYR m): 1,217.13-mth Avg Daily Turnover (US$ m): 0.92KLCI: 1,762.87Free float (%): 50.1

Major Shareholders: %PANG CHAUN YONG 44.0SKIM AMANAH SAHAM 5.0

Key Indicators

Net cash / (debt) (MYR m): 91.9NTA/shr (MYR): 0.43Net Gearing (x): (0.3)

Historical Chart

0.4

0.9

1.4

1.9

2.4

2.9

Jul-11 Nov-11 Mar-12 Jul-12 Nov-12 Mar-13

PAD MK Equity

Performance:

52-week High/Low MYR2.37/MYR1.69

1-mth 3-mth 6-mth 1-yr YTD

Absolute (%) (11.5) (5.1) (2.1) (0.5) -

Relative (%) (10.8) (9.5) (6.2) (9.3) (4.4)

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 2/89 July 2013 Page 2 of 8

Padini Holdings Other updates

Sourcing for new suppliers. The group now sources its finished

goods from manufacturers in China (70%), Bangladesh (30%) and the

rest is sourced locally. With China and Bangladesh having their own

labour issues, Padini has set up a new team to look for new suppliers inthe other countries, probably in Sri Lanka and Vietnam. Possible

limitations besides pricing include (i) size of factory (ii) quality and

reliability and (iii) the language barrier.

Leaner inventory. The inventory level for the group has fallen to 0.44x

against cost of goods sold in 9MFY6/13, far below the peak of more

than 0.6x in FY6/08 and FY6/11. At the latest levels, we think the

inventory level is manageable, though Padini will eventually have to top

up, for with seven new stores in the pipeline contributing to total

additional space of approximately 90,000 sq ft, inventories are expected

to deplete faster.

Chart 1: Inventory / COGS coming down from the peak

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.0

50.0

100.0

150.0

200.0

250.0

FY06 FY07 FY08 FY09 FY10 FY11 FY12 9MFY13

(X)(MYR m) Inventories (LHS) Inventories / COGS (RHS)

Source: Company, Maybank KE

H&M in Penang soon. Swedish retail, H&M will open another two

outlets in 2013 in Gurney Paragon (c. 19,000 sq ft) in Penang and

Avenue K in KL CBD, opposite KLCC Mall. This will further heat up the

competition in the domestic apparel market, which is already inundated

with many local and foreign brands. We understand that Padini has

lowered the prices for certain products in the past 9 months to make it

more affordable for the mass. Coupled with increasing preference for its

cheaper Brands Outlet’s clothing, gross margins are likely to remain

under pressure, in our view. Our forecasts impute lower average gross

profit margins of 46% in FY6/14-15 versus 48% in FY6/12.

Chart 2: Margins trend

42%

43%44%

45%

46%

47%

48%

49%

50%

51%

52%

0

50100

150

200

250

300

350

400

450

500

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13F FY14F FY15F

MYR m Gross Profit (LHS) GP Margin (RHS)

Source: Company, Maybank KE

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 3/89 July 2013 Page 3 of 8

Padini Holdings Financials and valuation

Assumptions

FY6/12A FY6/13F FY6/14F FY6/15F

Revenue (MYR m)

Vincci 227.8 197.2 216.9 223.4Padini 225.7 211.6 236.1 271.2

Seed 87.9 77.9 82.5 84.2

Yee Fong Hung 148.3 226.7 266.6 363.1

Mikihouse 25.1 24.8 26.0 27.3

Others 8.6 8.7 9.0 9.4

Total 723.4 746.8 837.2 978.6

Revenue (%)

Vincci 31.5% 26.4% 25.9% 22.8%

Padini 31.2% 28.3% 28.2% 27.7%

Seed 12.2% 10.4% 9.9% 8.6%

Yee Fong Hung 20.5% 30.4% 31.8% 37.1%

Mikihouse 3.5% 3.3% 3.1% 2.8%

Others 1.2% 1.2% 1.1% 1.0%

Number of large stores

Brands Outlet 19 20 25 26

Padini Concept Store 26 26 30 31

Total retail space (sq ft) 699,136 719,544 829,544 859,544

Source: Maybank KE

Stores expansion to resume in FY6/14. Brands Outlet in Fahrenheit

88 measuring c. 20,000 sq ft (opposite Pavilion Mall in KL CBD) is the

only new store for FY6/13. The group will open 7 new stores (+90,000

sq ft in total) in 1HFY6/14, comprising 3 Padini Concept Stores (in Miri,

Seremban and Penang) and 4 Brands Outlets (in Miri, Seremban,

Penang and Langkawi). Our new retail space assumption for FY6/14 is

raised to +110,000 sq ft from +80,000 sq ft previously. Brands Outlet

(under Yee Fong Hung) is expected to be the biggest revenue

contributor to the group from FY6/13 onwards.

Still trading above +1 SD of mean. Padini current trades at 12.7x

FY14 earnings and 12x on a calendarized CY14 basis, which is higher

than the +1 SD above its historical mean, of 10.7x. On the flip side,

Padini has been paying good dividends on a quarterly basis and we

expect the company to pay a DPS of 10sen (+25% YoY) for FY6/14.

This equates a dividend payout ratio of 69% in FY6/14, compared to

65% and 40% in FY6/13 and FY6/12 respectively.

Chart 2: One-year forward PER Chart 3: Increasing dividend payout ratio

0

5

10

15

20

25

J a n -

0 0

J a n -

0 1

J a n -

0 2

J a n -

0 3

J a n -

0 4

J a n -

0 5

J a n -

0 6

J a n -

0 7

J a n -

0 8

J a n -

0 9

J a n -

1 0

J a n -

1 1

J a n -

1 2

J a n -

1 3

PE (x)

-1sd: 5.7

+1sd: 10.7

mean: 8.2

0%

10%

20%

30%

40%

50%

60%

70%

80%

F Y 0 7

F Y 0 8

F Y 0 9

F Y 1 0

F Y 1 1

F Y 1 2

F Y 1 3 F

F Y 1 4 F

F Y 1 5 F

Source: Maybank KE Source: Company, Maybank KE

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 4/89 July 2013 Page 4 of 8

Padini Holdings

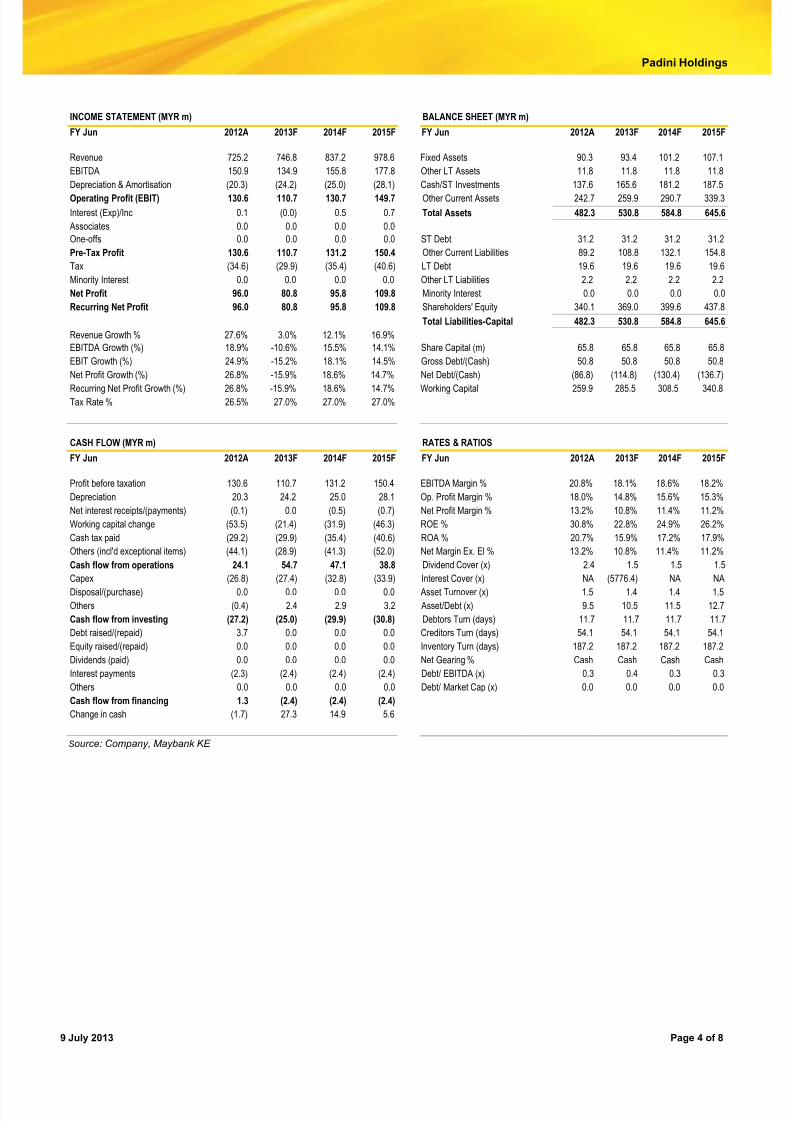

INCOME STATEMENT (MYR m) BALANCE SHEET (MYR m)

FY Jun 2012A 2013F 2014F 2015F FY Jun 2012A 2013F 2014F 2015F

Revenue 725.2 746.8 837.2 978.6 Fixed Assets 90.3 93.4 101.2 107.1

EBITDA 150.9 134.9 155.8 177.8 Other LT Assets 11.8 11.8 11.8 11.8

Depreciation & Amortisation (20.3) (24.2) (25.0) (28.1) Cash/ST Investments 137.6 165.6 181.2 187.5Operating Profit (EBIT) 130.6 110.7 130.7 149.7 Other Current Assets 242.7 259.9 290.7 339.3

Interest (Exp)/Inc 0.1 (0.0) 0.5 0.7 Total Assets 482.3 530.8 584.8 645.6

Associates 0.0 0.0 0.0 0.0

One-offs 0.0 0.0 0.0 0.0 ST Debt 31.2 31.2 31.2 31.2

Pre-Tax Profit 130.6 110.7 131.2 150.4 Other Current Liabilities 89.2 108.8 132.1 154.8

Tax (34.6) (29.9) (35.4) (40.6) LT Debt 19.6 19.6 19.6 19.6

Minority Interest 0.0 0.0 0.0 0.0 Other LT Liabilities 2.2 2.2 2.2 2.2

Net Profit 96.0 80.8 95.8 109.8 Minority Interest 0.0 0.0 0.0 0.0

Recurring Net Profit 96.0 80.8 95.8 109.8 Shareholders' Equity 340.1 369.0 399.6 437.8

Total Liabilities-Capital 482.3 530.8 584.8 645.6

Revenue Growth % 27.6% 3.0% 12.1% 16.9%

EBITDA Growth (%) 18.9% -10.6% 15.5% 14.1% Share Capital (m) 65.8 65.8 65.8 65.8

EBIT Growth (%) 24.9% -15.2% 18.1% 14.5% Gross Debt/(Cash) 50.8 50.8 50.8 50.8

Net Profit Growth (%) 26.8% -15.9% 18.6% 14.7% Net Debt/(Cash) (86.8) (114.8) (130.4) (136.7)Recurring Net Profit Growth (%) 26.8% -15.9% 18.6% 14.7% Working Capital 259.9 285.5 308.5 340.8

Tax Rate % 26.5% 27.0% 27.0% 27.0%

CASH FLOW (MYR m) RATES & RATIOS

FY Jun 2012A 2013F 2014F 2015F FY Jun 2012A 2013F 2014F 2015F

Profit before taxation 130.6 110.7 131.2 150.4 EBITDA Margin % 20.8% 18.1% 18.6% 18.2%

Depreciation 20.3 24.2 25.0 28.1 Op. Profit Margin % 18.0% 14.8% 15.6% 15.3%

Net interest receipts/(payments) (0.1) 0.0 (0.5) (0.7) Net Profit Margin % 13.2% 10.8% 11.4% 11.2%

Working capital change (53.5) (21.4) (31.9) (46.3) ROE % 30.8% 22.8% 24.9% 26.2%

Cash tax paid (29.2) (29.9) (35.4) (40.6) ROA % 20.7% 15.9% 17.2% 17.9%

Others (incl'd exceptional items) (44.1) (28.9) (41.3) (52.0) Net Margin Ex. El % 13.2% 10.8% 11.4% 11.2%

Cash flow from operations 24.1 54.7 47.1 38.8 Dividend Cover (x) 2.4 1.5 1.5 1.5

Capex (26.8) (27.4) (32.8) (33.9) Interest Cover (x) NA (5776.4) NA NA

Disposal/(purchase) 0.0 0.0 0.0 0.0 Asset Turnover (x) 1.5 1.4 1.4 1.5

Others (0.4) 2.4 2.9 3.2 Asset/Debt (x) 9.5 10.5 11.5 12.7

Cash flow from investing (27.2) (25.0) (29.9) (30.8) Debtors Turn (days) 11.7 11.7 11.7 11.7

Debt raised/(repaid) 3.7 0.0 0.0 0.0 Creditors Turn (days) 54.1 54.1 54.1 54.1

Equity raised/(repaid) 0.0 0.0 0.0 0.0 Inventory Turn (days) 187.2 187.2 187.2 187.2

Dividends (paid) 0.0 0.0 0.0 0.0 Net Gearing % Cash Cash Cash Cash

Interest payments (2.3) (2.4) (2.4) (2.4) Debt/ EBITDA (x) 0.3 0.4 0.3 0.3

Others 0.0 0.0 0.0 0.0 Debt/ Market Cap (x) 0.0 0.0 0.0 0.0

Cash flow from financing 1.3 (2.4) (2.4) (2.4)

Change in cash (1.7) 27.3 14.9 5.6

Source: Company, Maybank KE

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 5/89 July 2013 Page 5 of 8

Padini Holdings

RESEARCH OFFICES REGIONAL

P K BASU Regional Head, Research & Economics

(65) 6432 1821 [email protected]

WONG Chew Hann, CA Acting Regional Head of Institutional Research

(603) 2297 8686 [email protected]

ONG Seng YeowRegional Products & Planning (65) 6432 1453 [email protected]

ECONOMICSSuhaimi ILIAS Chief Economist

Singapore | Malaysia(603) 2297 8682 [email protected]

Luz LORENZO

Philippines(63) 2 849 8836 [email protected]

Tim LEELAHAPHAN

Thailand (662) 658 1420 [email protected]

JUNIMAN Chief Economist, BII

Indonesia(62) 21 29228888 ext 29682 [email protected]

Josua PARDEDE Economist / Industry Analyst, BII

Indonesia(62) 21 29228888 ext 29695 [email protected]

MALAYSIAWONG Chew Hann, CA Head of Research (603) 2297 8686 [email protected] Strategy

Construction & InfrastructureDesmond CH’NG, ACA(603) 2297 8680 [email protected] Banking - Regional LIAW Thong Jung(603) 2297 8688 [email protected]

Oil & Gas Automotive

ShippingONG Chee Ting, CA(603) 2297 8678 [email protected] Plantations- Regional

Mohshin AZIZ (603) 2297 8692 [email protected]

Aviation Petrochem

YIN Shao Yang, CPA(603) 2297 8916 [email protected] Gaming – Regional

Media TAN CHI WEI, CFA(603) 2297 8690 [email protected] Power

TelcosWONG Wei Sum, CFA(603) 2297 8679 [email protected] Property & REITsLEE Yen Ling

(603) 2297 8691 [email protected] Building Materials Manufacturing

Technology

LEE Cheng Hooi Head of Retail [email protected] Technicals

HONG KONG / CHINAIvan CHEUNG, CFA(852) 2268 0634 [email protected] HK Property

IndustrialJacqueline KO, CFA(852) 2268 0633 [email protected]

Consumer Andy POON (852) 2268 0645 [email protected]

Telecom & equipmentAlex YEUNG (852) 2268 0636 [email protected]

IndustrialKaren KWAN (852) 2268 0640 [email protected]

China PropertyJeremy TAN (852) 2268 0635 [email protected] GamingWarren LAU (852) 2268 0644 [email protected] Technology – Regional

INDIAJigar SHAH Head of Research

(91) 22 6623 2601 [email protected] Oil & Gas Automobile

CementAnubhav GUPTA (91) 22 6623 2605 [email protected]

Metal & Mining Capital goods PropertyUrmil SHAH (91) 22 6623 2606 [email protected] Technology

MediaVarun VARMA (91) 226623 2611 [email protected] n

Banking

SINGAPOREGregory YAP Head of Research (65) 6432 1450 [email protected] Technology & Manufacturing Telcos - Regional Wilson LIEW (65) 6432 1454 [email protected]

Property & REITsJames KOH (65) 6432 1431 [email protected]

Logistics Resources

Consumer Small & Mid Caps

YEAK Chee Keong, CFA(65) 6432 1460 [email protected]

Offshore & MarineAlison FOK

(65) 6432 1447 [email protected] Services S-chipsONG Kian Lin(65) 6432 1470 [email protected] REITs / PropertyWei Bin(65) 6432 1455 [email protected] S-chips

Small & Mid Caps

INDONESIALucky ARIESANDI, CFA (62) 21 2557 1127 [email protected]

Base metals Mining Oil & Gas

WholesaleRahmi MARINA (62) 21 2557 1128 [email protected]

Banking Multifinance

Pandu ANUGRAH (62) 21 2557 1137 [email protected] Automotive

Heavy equipment Plantation Toll road

Adi N. WICAKSONO (62) 21 2557 1128 [email protected] GeneralistAnthony YUNUS (62) 21 2557 1139 [email protected] Cement

Infrastructure Property

PHILIPPINESLuz LORENZO Head of Research

(63) 2 849 8836 [email protected] StrategyLaura D Y-LIACCO (63) 2 849 8840 [email protected] Utilities Conglomerates

Telcos

Lovell SARREAL (63) 2 849 8841 [email protected] Consumer Media

CementLuz LORENZO / Mark RACE (63) 2 849 8844 [email protected]

Conglomerates Property Ports/ Logistics

GamingKatherine TAN (63) 2 849 8843 [email protected]

Banks ConstructionRamon ADVIENTO (63) 2 849 8845 [email protected] Mining

TH ILANDSukit UDOMSIRIKUL Head of Research (66) 2658 6300 ext [email protected]

Maria LAPIZ Head of Institutional Research Dir (66) 2257 0250 | (66) 2658 6300 ext [email protected]

Consumer/ Big Caps

Andrew STOTZ Strategist (66) 2658 6300 ext 5091

Mayuree CHOWVIKRAN (66) 2658 6300 ext 1440 [email protected] StrategyPadon Vannarat(66) 2658 6300 ext 1450 [email protected] Strategy

Surachai PRAMUALCHAROENKIT (66) 2658 6300 ext 1470 [email protected] Auto Conmat Contractor SteelSuttatip PEERASUB (66) 2658 6300 ext 1430 [email protected]

Media CommerceSutthichai KUMWORACHAI (66) 2658 6300 ext 1400 [email protected] Energy PetrochemTermporn TANTIVIVAT (66) 2658 6300 ext 1520 [email protected] PropertyWoraphon WIROONSRI (66) 2658 6300 ext 1560 [email protected]

Banking & FinanceJaroonpan WATTANAWONG

(66) 2658 6300 ext 1404 [email protected] Transportation Small cap.Chatchai JINDARAT

(66) 2658 6300 ext 1401 [email protected] ElectronicsPongrat RATANATAVANANANDA (66) 2658 6300 ext 1398 [email protected] Services/ Small Caps

VIETNAMMichael KOKALARI, CFA Head of Research

(84) 838 38 66 47 [email protected]

StrategyNguyen Thi Ngan Tuyen(84) 844 55 58 88 x 8081 [email protected]

Food and Beverage Oil and GasNgo Bich Van(84) 844 55 58 88 x 8084 [email protected] BankingTrinh Thi Ngoc Diep(84) 844 55 58 88 x 8242 [email protected] Technology Utilities

ConstructionDang Thi Kim Thoa(84) 844 55 58 88 x 8083 [email protected] Consumer Nguyen Trung Hoa+84 844 55 58 88 x 8088 [email protected] Steel Sugar

Resources

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 6/89 July 2013 Page 6 of 8

Padini Holdings APPENDIX I: TERMS FOR PROVISION OF REPORT, DISCLAIMERS AND DISCLOSURES

DISCLAIMERS

This research report is prepared for general circulation and for information purposes only and under no circumstances should it be considered or intended as anoffer to sell or a solicitation of an offer to buy the securities referred to herein. Investors should note that values of such securities, if any, may fluctuate and thateach security’s price or value may rise or fall. Opinions or recommendations contained herein are in form of technical rating s and fundamental ratings.

Technical ratings may differ from fundamental ratings as technical valuations apply different methodologies and are purely based on price and volume-relatedinformation extracted from the relevant jurisdiction’s stock exchange in the equity analysis. Accordingly, investors’ returns may be l ess than the original suminvested. Past performance is not necessarily a guide to future performance. This report is not intended to provide personal investment advice and does nottake into account the specific investment objectives, the financial situation and the particular needs of persons who may receive or read this report. Investorsshould therefore seek financial, legal and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

The information contained herein has been obtained from sources believed to be reliable but such sources have not been independently veri fied by MaybankInvestment Bank Berhad, its subsidiary and affiliates (collectively, “MKE”) and consequently no representation is m ade as to the accuracy or completeness of this report by MKE and it should not be relied upon as such. Accordingly, MKE and its officers, directors, associates, connec ted parties and/or employees(collectively, “Representatives”) shall not be liable for any direct, indirect or consequential losses or damages that may arise from the use or reliance of thisreport. Any information, opinions or recommendations contained herein are subject to change at any time, without prior notice.

This report may contain for ward looking statements which are often but not always identified by the use of words such as “anticipate”, “believe”, “estimate”,“intend”, “plan”, “expect”, “forecast”, “predict” and “project” and statements that an event or result “may”, “will”, “can”, “should”, “could” or “might” occur or beachieved and other similar expressions. Such forward looking statements are based on assumptions made and information currently available to us and aresubject to certain risks and uncertainties that could cause the actual results to differ materially from those expressed in any forward looking statements.Readers are cautioned not to place undue relevance on these forward-looking statements. MKE expressly disclaims any obligation to update or revise any suchforward looking statements to reflect new information, events or circumstances after the date of this publication or to reflect the occurrence of unanticipated

events.

MKE and its officers, directors and employees, including persons involved in the preparation or issuance of this report, may, to the extent permitted by law, fromtime to time participate or invest in financing transactions with the issuer(s) of the securities mentioned in this report, perform services for or solicit businessfrom such issuers, and/or have a position or holding, or other material interest, or effect transactions, in such securities or options thereon, or other investmentsrelated thereto. In addition, it may make markets in the securities mentioned in the material presented in this report. MKE may, to the extent permitted by law,act upon or use the information presented herein, or the research or analysis on which they are based, before the material is published. One or more directors,officers and/or employees of MKE may be a director of the issuers of the securities mentioned in this report.

This report is prepared for the use of MKE’s clients and may not be reproduced, altered in any way, transmitted to, copied or distributed to any other party inwhole or in part in any form or manner without the prior express written consent of MKE and MKE and its Representatives accepts no liability whatsoever for theactions of third parties in this respect.

This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This rep ort is for distribution only under suchcircumstances as may be permitted by applicable law. The securities described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. Without prejudice to the foregoing, the reader is to note that additional disclaimers, warnings or qualifications may apply based on geographicallocation of the person or entity receiving this report.

Malaysia

Opinions or recommendations contained herein are in the form of technical ratings and fundamental ratings. Technical ratings may differ from fundamentalratings as technical valuations apply different methodologies and are purely based on price and volume-related information extracted from Bursa MalaysiaSecurities Berhad in the equity analysis.

Singapore

This report has been produced as of the date hereof and the information herein may be subject to change. Maybank Kim Eng Research Pte. Ltd. (“MaybankKERPL”) in Singapore has no obligation to update such information for any recipient. For distribution in Singapore, recipient s of this report are to contactMaybank KERPL in Singapore in respect of any matters arising from, or in connection with, this report. If the recipient of this report is not an accredited investor,expert investor or institutional investor (as defined under Section 4A of the Singapore Securities and Futures Act), Maybank KERPL shall be legally liable for thecontents of this report, with such liability being limited to the extent (if any) as permitted by law.

Thailand

The disclosure of the survey result of the Thai Institute of Directors Association (“IOD”) regarding corporate governance is made pursuant to the policy of theOffice of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailandand the market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from theperspective of a third party. It is not an evaluation of operation and is not based on inside information.The survey result is as of the date appearing in the

Corporate Governance Report of Thai Listed Companies. As a result, the survey may be changed after that date. Maybank Kim Eng Securities (Thailand)Public Company Limited (“MBKET”) does not confirm nor certify the accuracy of such survey result.

Except as specifically permitted, no part of this presentation may be reproduced or distributed in any manner without the pri or written permission of MBKET.MBKET accepts no liability whatsoever for the actions of third parties in this respect.

US

This research report prepared by MKE is distributed in the United States (“US”) to Major US Institutional Investors (as defin ed in Rule 15a-6 under theSecurities Exchange Act of 1934, as amended) only by Maybank Kim Eng Securities USA Inc (“Maybank KESUSA”), a broker -dealer registered in the US(registered under Section 15 of the Securities Exchange Act of 1934, as amended). All responsibility for the distribution of this report by Maybank KESUSA inthe US shall be borne by Maybank KESUSA. All resulting transactions by a US person or entity should be effected through a registered broker-dealer in theUS. This report is not directed at you if MKE is prohibited or restricted by any legislation or regulati on in any jurisdiction from making it available to you. Youshould satisfy yourself before reading it that Maybank KESUSA is permitted to provide research material concerning investments to you under relevantlegislation and regulations.

UK

This document is being distributed by Maybank Kim Eng Securities (London) Ltd (“Maybank KESL”) which is authorized and regulated, by the Fi nancialServices Authority and is for Informational Purposes only. This document is not intended for distribution to anyone defined as a Retail Client under the Financial

Services and Markets Act 2000 within the UK. Any inclusion of a third party link is for the recipients convenience only, and that the firm does not take anyresponsibility for its comments or accuracy, and that access to such links is at the individuals own risk. Nothing in this report should be considered asconstituting legal, accounting or tax advice, and that for accurate guidance recipients should consult with their own independent tax advisers.

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 7/89 July 2013 Page 7 of 8

Padini Holdings DISCLOSURES

Legal Entities Disclosures

Malaysia: This report is issued and distributed in Malaysia by Maybank Investment Bank Berhad (15938-H) which is a Participating Organization of BursaMalaysia Berhad and a holder of Capital Markets and Services License issued by the Securities Commission in Malaysia. Singapore: This material is issuedand distributed in Singapore by Maybank KERPL (Co. Reg No 197201256N) which is regulated by the Monetary Authority of Singapore. Indonesia: PT KimEng Securities (“PTKES”) (Reg. No. KEP-251/PM/1992) is a member of the Indonesia Stock Exchange and is regulated by the BAPEPAM LK. Thailand: MBKET (Reg. No.0107545000314) is a member of the Stock Exchange of Thailand and is regulated by the Ministry of Finance and the Securities andExchange Commission. Philippines: Maybank ATRKES (Reg. No.01-2004-00019) is a member of the Philippines Stock Exchange and is regulated by theSecurities and Exchange Commission. Vietnam: Maybank Kim Eng Securities JSC (License Number: 71/UBCK-GP) is licensed under the State SecuritiesCommission of Vietnam.Hong Kong: KESHK (Central Entity No AAD284) is regulated by the Securities and Futures Commission. India: Kim Eng SecuritiesIndia Private Limited (“KESI”) is a participant of the National Stock Exchange of Ind ia Limited (Reg No: INF/INB 231452435) and the Bombay Stock Exchange(Reg. No. INF/INB 011452431) and is regulated by Securities and Exchange Board of India. KESI is also registered with SEBI as Category 1 Merchant Banker (Reg. No. INM 000011708) US: Maybank KESUSA is a member of/ and is authorized and regulated by the FINRA – Broker ID 27861. UK: Maybank KESL(Reg No 2377538) is authorized and regulated by the Financial Services Authority.

Disclosure of Interest

Malaysia: MKE and its Representatives may from time to time have positions or be materially interested in the securities referred to herein and may further actas market maker or may have assumed an underwriting commitment or deal with such securities and may also perform or seek to perform investment bankingservices, advisory and other services for or relating to those companies.

Singapore: As of 9 July 2013, Maybank KERPL and the covering analyst do not have any interest in any companies recommended in this research report.

Thailand: MBKET may have a business relationship with or may possibly be an issuer of derivative warrants on the securities /companies mentioned in theresearch report. Therefore, Investors should exercise their own judgment before making any investment decisions. MBKET, its associates, directors, connectedparties and/or employees may from time to time have interests and/or underwriting commitments in the securities mentioned in this report.

Hong Kong: KESHK may have financial interests in relation to an issuer or a new listing applicant referred to as defined by the requirements under Paragraph16.5(a) of the Hong Kong Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission.

As of 9 July 2013, KESHK and the authoring analyst do not have any interest in any companies recommended in this research report.

MKE may have, within the last three years, served as manager or co-manager of a public offering of securities for, or currently may make a primary market inissues of, any or all of the entities mentioned in this report or may be providing, or have provided within the previous 12 months, significant advice or investmentservices in relation to the investment concerned or a related investment and may receive compensation for the services provided from the companies coveredin this report.

OTHERS

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research analyst’s compensation was, is or will be, directly or indirectly, related to th e specific recommendations or views expressed in the report.

Reminder

Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable

of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and politicalfactors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility and the credit quality of anyissuer or reference issuer. Any investor interested in purchasing a structured product should conduct its own analysis of the product and consult with its ownprofessional advisers as to the risks involved in making such a purchase.

No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior consent of MKE.

Definition of Ratings

Maybank Kim Eng Research uses the following rating system:

BUY Return is expected to be above 10% in the next 12 months (excluding dividends)

HOLD Return is expected to be between - 10% to +10% in the next 12 months (excluding dividends)

SELL Return is expected to be below -10% in the next 12 months (excluding dividends)

Applicability of Ratings

The respective analyst maintains a coverage universe of stocks, the list of which may be adjusted according to needs. Investm ent ratings are only

applicable to the stocks which form part of the coverage universe. Reports on companies which are not part of the coverage do not carry investment ratings

as we do not actively follow developments in these companies.

Some common terms abbreviated in this report (where they appear):

Adex = Advertising Expenditure FCF = Free Cashflow PE = Price Earnings

BV = Book Value FV = Fair Value PEG = PE Ratio To Growth

CAGR = Compounded Annual Growth Rate FY = Financial Year PER = PE Ratio

Capex = Capital Expenditure FYE = Financial Year End QoQ = Quarter-On-Quarter

CY = Calendar Year MoM = Month-On-Month ROA = Return On Asset

DCF = Discounted Cashflow NAV = Net Asset Value ROE = Return On EquityDPS = Dividend Per Share NTA = Net Tangible Asset ROSF = Return On Shareholders’ Funds

EBIT = Earnings Before Interest And Tax P = Price WACC = Weighted Average Cost Of Capital

EBITDA = EBIT, Depreciation And Amortisation P.A. = Per Annum YoY = Year-On-Year

EPS = Earnings Per Share PAT = Profit After Tax YTD = Year-To-DateEV = Enterprise Value PBT = Profit Before Tax

7/27/2019 MayBank Research

http://slidepdf.com/reader/full/maybank-research 8/89 J l 2013 P 8 f 8

Padini Holdings Malaysia

Maybank Investment Bank Berhad(A Participating Organisation of Bursa Malaysia Securities Berhad)33rd Floor, Menara Maybank,100 Jalan Tun Perak,50050 Kuala Lumpur

Tel: (603) 2059 1888;Fax: (603) 2078 4194

Singapore

Maybank Kim Eng Securities Pte Ltd Maybank Kim Eng Research Pte Ltd9 Temasek Boulevard#39-00 Suntec Tower 2Singapore 038989

Tel: (65) 6336 9090Fax: (65) 6339 6003

London

Maybank Kim Eng Securities(London) Ltd 6/F, 20 St. Dunstan’s Hill London EC3R 8HY, UK

Tel: (44) 20 7621 9298

Dealers’ Tel: (44) 20 7626 2828 Fax: (44) 20 7283 6674

New York

Maybank Kim Eng SecuritiesUSA Inc 777 Third Avenue, 21st Floor New York, NY 10017, U.S.A.

Tel: (212) 688 8886

Fax: (212) 688 3500

Stockbroking Business:Level 8, Tower C, Dataran Maybank,No.1, Jalan Maarof 59000 Kuala Lumpur Tel: (603) 2297 8888Fax: (603) 2282 5136

Hong Kong

Kim Eng Securities (HK) Ltd Level 30,Three Pacific Place,1 Queen’s Road East, Hong Kong

Tel: (852) 2268 0800Fax: (852) 2877 0104

Indonesia

PT Kim Eng Securities Plaza BapindoCitibank Tower 17th Floor Jl Jend. Sudirman Kav. 54-55Jakarta 12190, Indonesia

Tel: (62) 21 2557 1188Fax: (62) 21 2557 1189

India

Kim Eng Securities India Pvt Ltd2nd Floor, The International 16,Maharishi Karve Road,Churchgate Station,Mumbai City - 400 020, India

Tel: (91).22.6623.2600Fax: (91).22.6623.2604

Philippines

Maybank ATR Kim Eng SecuritiesInc.

17/F, Tower One & Exchange Plaza Ayala Triangle, Ayala AvenueMakati City, Philippines 1200

Tel: (63) 2 849 8888Fax: (63) 2 848 5738

Thailand

Maybank Kim Eng Securities(Thailand) Public Company

Limited 999/9 The Offices at Central World,20th - 21st Floor,Rama 1 Road Pathumwan,Bangkok 10330, Thailand

Tel: (66) 2 658 6817 (sales)Tel: (66) 2 658 6801 (research)

VietnamIn association with

Maybank Kim Eng Securities JSC1st Floor, 255 Tran Hung Dao St.

District 1Ho Chi Minh City, Vietnam

Tel : (84) 844 555 888Fax : (84) 838 38 66 39

Saudi ArabiaIn association with

Anfaal CapitalVilla 47, Tujjar Jeddah

Prince Mohammed bin AbdulazizStreet P.O. Box 126575Jeddah 21352

Tel: (966) 2 6068686Fax: (966) 26068787

South Asia Sales Trading

Kevin [email protected]: (65) 6336-5157US Toll Free: 1-866-406-7447

North Asia Sales Trading

Eddie [email protected]: (852) 2268 0800US Toll Free: 1 866 598 2267

www.maybank-ke.com | www.maybank-keresearch.com

Related Documents