Humanising Financial Services Disclaimer: The contents of this document/information remain the intellectual property of Maybank and no part of this is to be reproduced or transmitted in any form or by any means, including electronically, photocopying, recording or in any information storage and retrieval system without the permission in writing from Maybank. The contents of this document/information are confidential and its circulation and use are restricted. Financial Results Fourth Quarter and Full Year FY2021 ended 31 December 2021 24 February 2022 Investor Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Humanising Financial Services

Disclaimer: The contents of this document/information remain the intellectual property of Maybank and no part of thisis to be reproduced or transmitted in any form or by any means, including electronically, photocopying, recording or in

any information storage and retrieval system without the permission in writing from Maybank. The contents of this

document/information are confidential and its circulation and use are restricted.

Financial ResultsFourth Quarter and Full Year FY2021 ended 31 December 202124 February 2022

Investor Presentation

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

Table of Contents

2

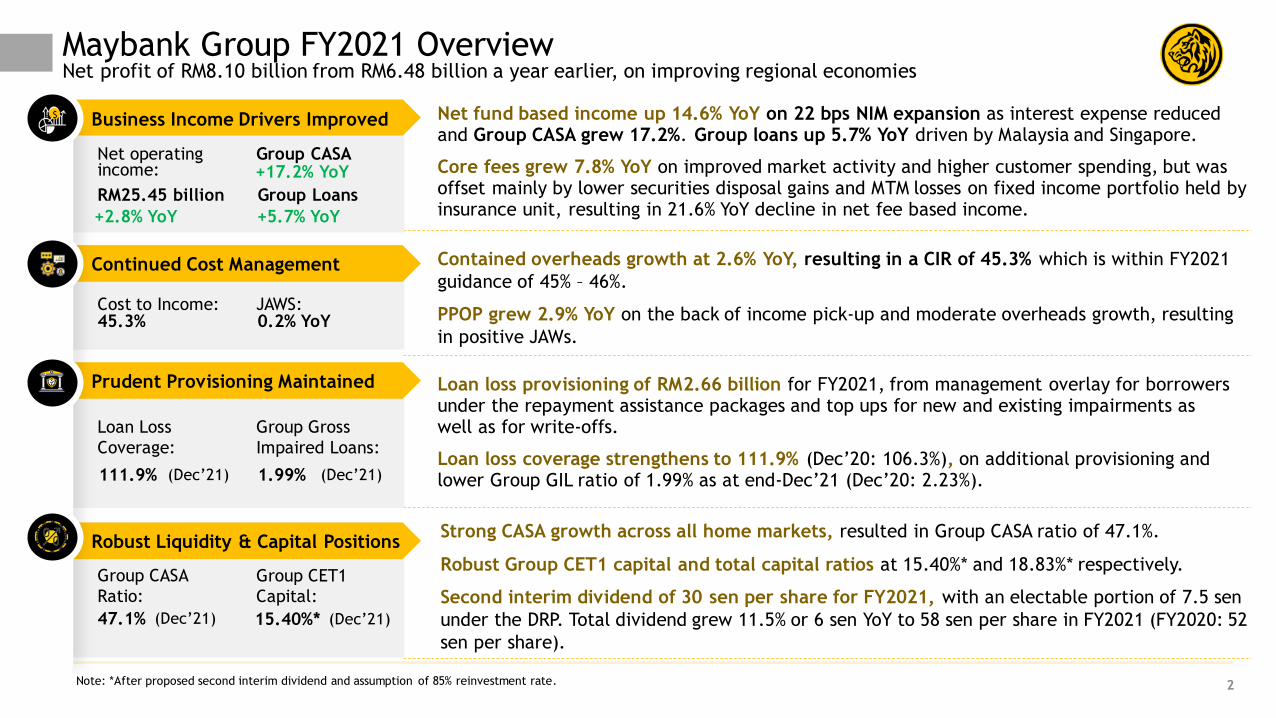

Net operating income:

RM25.45 billion

+2.8% YoY

Net fund based income up 14.6% YoY on 22 bps NIM expansion as interest expense reduced and Group CASA grew 17.2%. Group loans up 5.7% YoY driven by Malaysia and Singapore.

Core fees grew 7.8% YoY on improved market activity and higher customer spending, but was offset mainly by lower securities disposal gains and MTM losses on fixed income portfolio held by insurance unit, resulting in 21.6% YoY decline in net fee based income.

Contained overheads growth at 2.6% YoY, resulting in a CIR of 45.3% which is within FY2021

guidance of 45% – 46%.

PPOP grew 2.9% YoY on the back of income pick-up and moderate overheads growth, resulting

in positive JAWs.

Cost to Income: JAWS: 45.3% 0.2% YoY

111.9%

Loan Loss

Coverage:

Group Gross

Impaired Loans:

1.99% (Dec’21)

Loan loss provisioning of RM2.66 billion for FY2021, from management overlay for borrowers under the repayment assistance packages and top ups for new and existing impairments as well as for write-offs.

Loan loss coverage strengthens to 111.9% (Dec’20: 106.3%), on additional provisioning and lower Group GIL ratio of 1.99% as at end-Dec’21 (Dec’20: 2.23%).

Strong CASA growth across all home markets, resulted in Group CASA ratio of 47.1%.

Robust Group CET1 capital and total capital ratios at 15.40%* and 18.83%* respectively.

Second interim dividend of 30 sen per share for FY2021, with an electable portion of 7.5 sen

under the DRP. Total dividend grew 11.5% or 6 sen YoY to 58 sen per share in FY2021 (FY2020: 52

sen per share).

Group CASA

Ratio:

47.1%

Group CET1

Capital:

15.40%*

Note: *After proposed second interim dividend and assumption of 85% reinvestment rate.

(Dec’21)

Group CASA

Group Loans

+5.7% YoY

(Dec’21)

$ Business Income Drivers Improved

Continued Cost Management

Prudent Provisioning Maintained

Robust Liquidity & Capital Positions

(Dec’21)

Maybank Group FY2021 OverviewNet profit of RM8.10 billion from RM6.48 billion a year earlier, on improving regional economies

+17.2% YoY

3

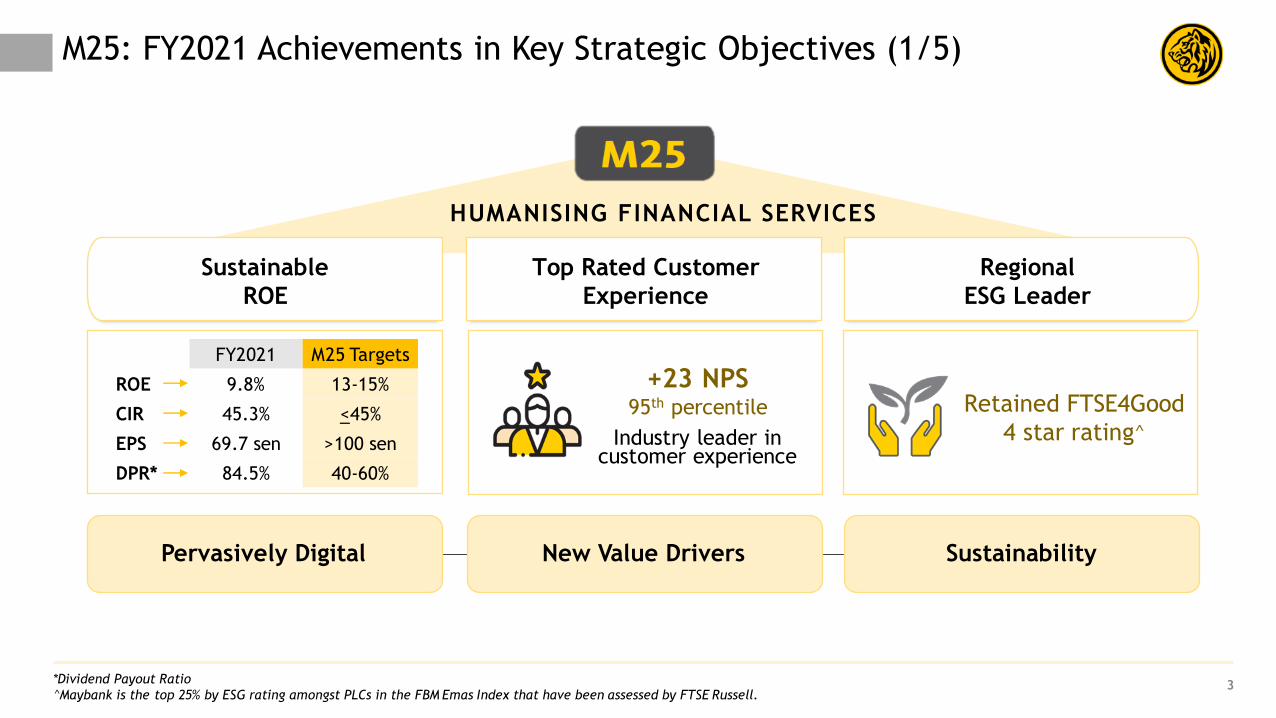

M25: FY2021 Achievements in Key Strategic Objectives (1/5)

FY2021 M25 Targets

ROE 9.8% 13-15%

CIR 45.3% <45%

EPS 69.7 sen >100 sen

DPR* 84.5% 40-60%

Retained

MSCI ESG AA rating

Pervasively Digital

HUMANISING FINANCIAL SERVICES

+23 NPS

Industry leader in customer experience

95th percentile

Sustainable

ROE

Top Rated Customer

Experience

Regional

ESG Leader

Retained FTSE4Good

4 star rating^

New Value Drivers Sustainability

*Dividend Payout Ratio

^Maybank is the top 25% by ESG rating amongst PLCs in the FBM Emas Index that have been assessed by FTSE Russell.

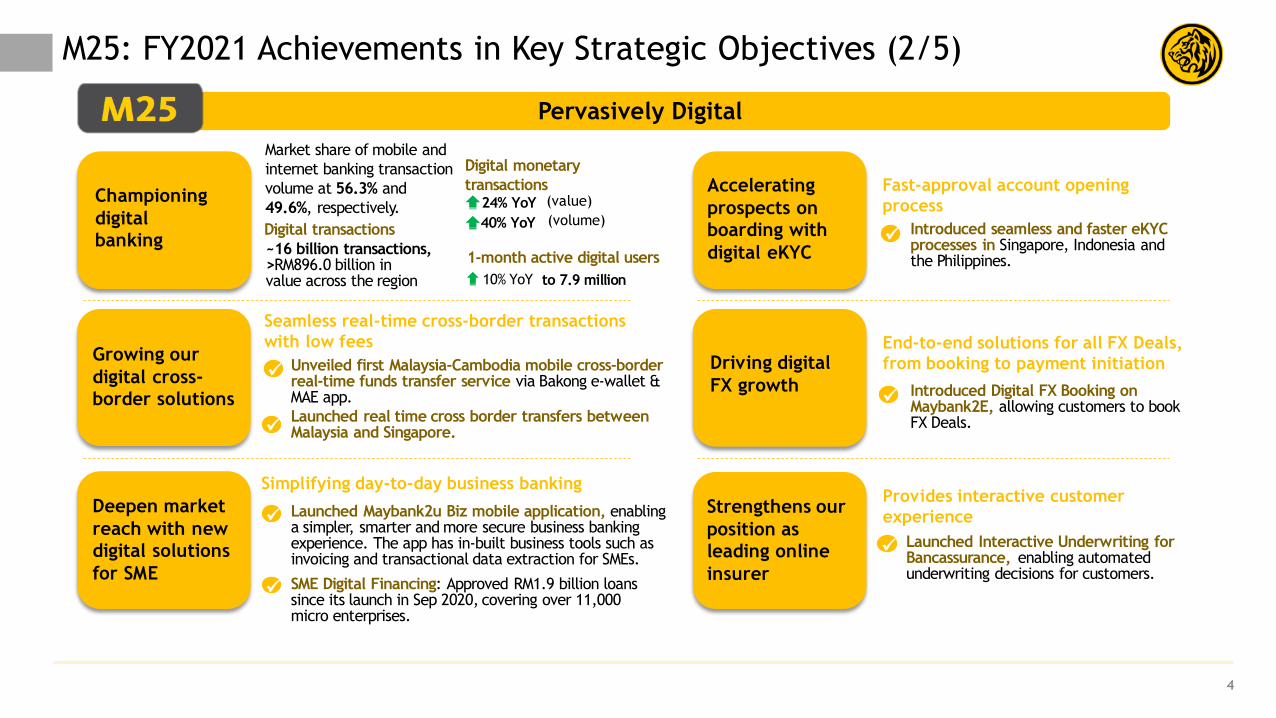

Pervasively Digital

4

Unveiled first Malaysia-Cambodia mobile cross-border real-time funds transfer service via Bakong e-wallet & MAE app.

Growing our

digital cross-

border solutionsLaunched real time cross border transfers between Malaysia and Singapore.

Championing

digital

banking

Market share of mobile and

internet banking transaction

volume at 56.3% and

49.6%, respectively.

~16 billion transactions, >RM896.0 billion in value across the region

Digital monetary

transactions24% YoY

40% YoY

(value)

(volume)Digital transactions

1-month active digital users

to 7.9 million10% YoY

Deepen market

reach with new

digital solutions

for SME

Launched Maybank2u Biz mobile application, enabling a simpler, smarter and more secure business banking experience. The app has in-built business tools such as invoicing and transactional data extraction for SMEs.

Accelerating

prospects on

boarding with

digital eKYC

Launched Interactive Underwriting for Bancassurance, enabling automated underwriting decisions for customers.

Introduced seamless and faster eKYCprocesses in Singapore, Indonesia and the Philippines.

Driving digital

FX growth Introduced Digital FX Booking on Maybank2E, allowing customers to book FX Deals.

Strengthens our

position as

leading online

insurer

M25: FY2021 Achievements in Key Strategic Objectives (2/5)

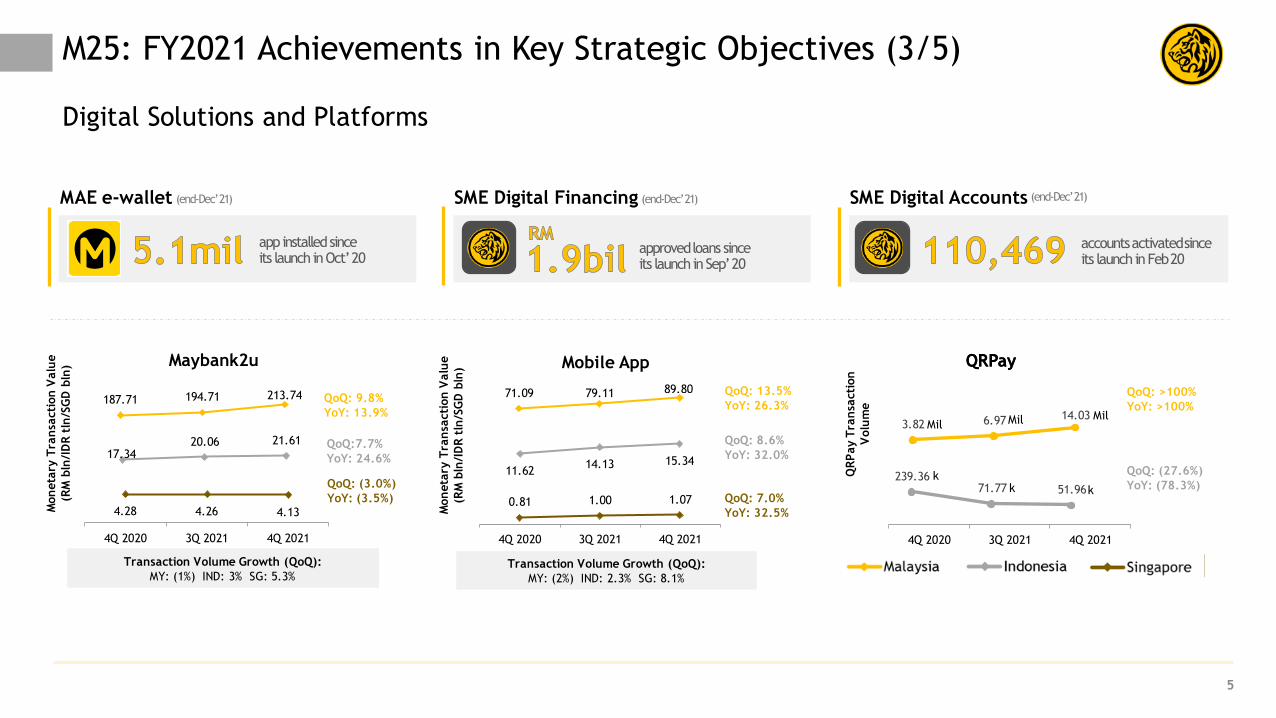

SME Digital Financing: Approved RM1.9 billion loans since its launch in Sep 2020, covering over 11,000 micro enterprises.

Seamless real-time cross-border transactions

with low fees

Simplifying day-to-day business banking

Fast-approval account opening

process

End-to-end solutions for all FX Deals,

from booking to payment initiation

Provides interactive customer

experience

5

(end-Dec’ 21)

app installed since its launch in Oct’ 20

MAE e-wallet SME Digital Financing

approved loans since its launch in Sep’ 20

SME Digital Accounts

accounts activated since its launch in Feb 20

(end-Dec’ 21) (end-Dec’ 21)

Digital Solutions and Platforms

4Q 2020 3Q 2021 4Q 2021

3.82 6.97 14.03

239.3671.77 51.96

QRPay

QR

Pay T

ran

sacti

on

Volu

me

QRPay

QoQ: >100%

YoY: >100%

QoQ: (27.6%)

YoY: (78.3%)

Mil Mil Mil

kk k

4.28 4.26 4.13

4Q 2020 3Q 2021 4Q 2021

Maybank2u

Mon

eta

ry T

ran

sacti

on

Valu

e

(RM

bln

/ID

R t

ln/S

GD

bln

)

187.71 194.71 213.74

17.3420.06 21.61

QoQ: 9.8%

YoY: 13.9%

QoQ:7.7%

YoY: 24.6%

QoQ: (3.0%)

YoY: (3.5%)

Transaction Volume Growth (QoQ):

MY: (1%) IND: 3% SG: 5.3%

71.09 79.11 89.80

0.81 1.00 1.07

4Q 2020 3Q 2021 4Q 2021

Mobile App

QoQ: 13.5%

YoY: 26.3%

QoQ: 8.6%

YoY: 32.0%

Transaction Volume Growth (QoQ):

MY: (2%) IND: 2.3% SG: 8.1%

Mon

eta

ry T

ran

sacti

on

Valu

e

(RM

bln

/ID

R t

ln/S

GD

bln

)11.62

14.13 15.34

QoQ: 7.0%

YoY: 32.5%

M25: FY2021 Achievements in Key Strategic Objectives (3/5)

New Value Drivers

6

Enhance

customer insights

and cross-sell

capabilities

Growing SME

financing

segments

Expansion of

ESG solutions

Enhance Auto

Insurance

services

Fortifying our

leading position

in Bancassurance

Islamic Banking

expansion of

Wealth

Management

solutions

M25: FY2021 Achievements in Key Strategic Objectives (4/5)

Launched the platform in July 2021 to

provide comprehensive financial solutions

that will drive Islamic fee-based income.

Launched several ESG-centric funds,

expanding our ESG-related AUM to RM13.5

billion.

Established Regional Client Solutions Group

covering the retail, mid-market and wholesale

segments. No.1 Bancassurance/ Bancatakaful player in Regular Premium and Total Life APE with 27.1% and 24.1% market share respectively in Malaysia

Achieved greater SME borrowing penetration

SME customers grew +2.4% YoY in Singapore,

Indonesia, the Philippines and Cambodia.

7.15% (2021)6.55% (2020)Malaysia:

Launched the first Shariah-Compliant

Autocallable-i product in the region.

Participated in several sustainability-linked

transactions such as SME Bank Berhad’s and Bank

Pembangunan Malaysia Berhad’s inaugural

sustainability Sukuks.

Developing All Things Auto (ATA) system to create an ecosystem that will benefit customers to make better decisions on all auto needs including choice of service provider for breakdown/accident services.

Etiqa Virtual Insurance Advisor (EVIA) will enable our intermediaries to provide better advice to customers based on data analytics.

Differentiated investment management

advisory and solutions

Supporting our customer’s sustainability

aspirations

Fast and Easy Auto Assistance

Better recommendations for protection needs

Launched Islamic Wealth Management

total solutions

No. of customers

Sustainability

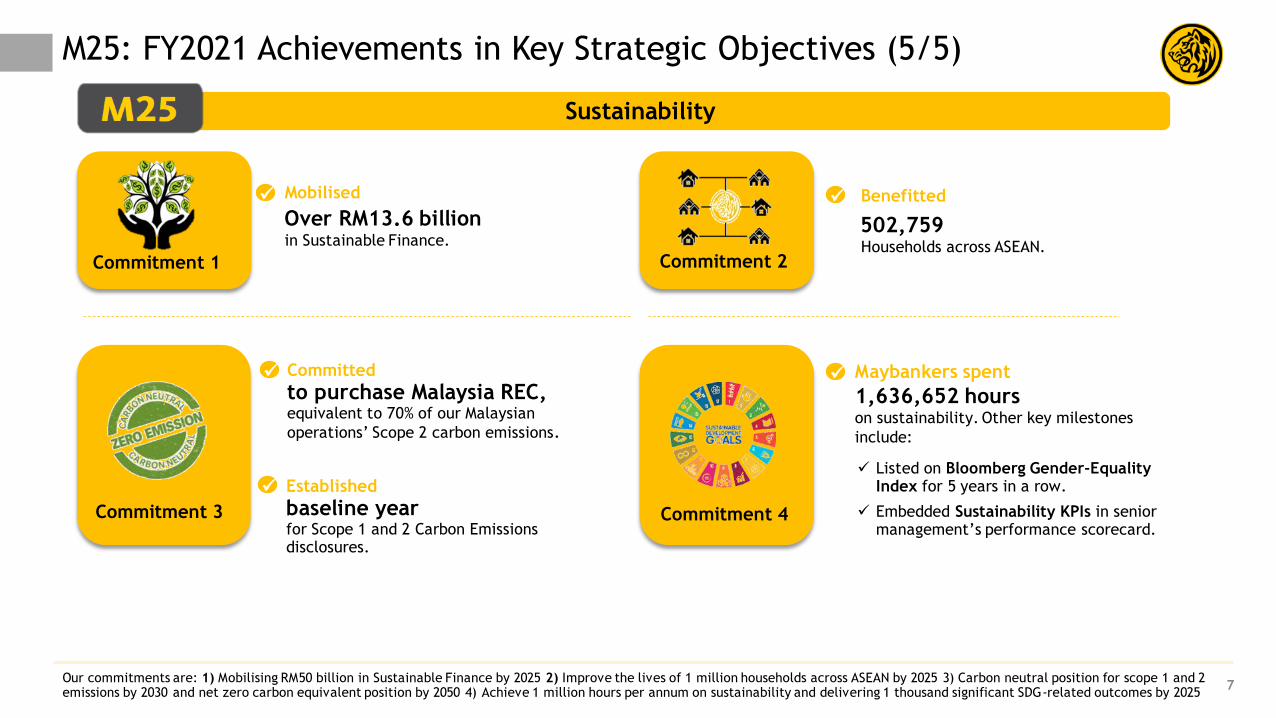

7Our commitments are: 1) Mobilising RM50 billion in Sustainable Finance by 2025 2) Improve the lives of 1 million households across ASEAN by 2025 3) Carbon neutral position for scope 1 and 2 emissions by 2030 and net zero carbon equivalent position by 2050 4) Achieve 1 million hours per annum on sustainability and delivering 1 thousand significant SDG-related outcomes by 2025

Commitment 3

Commitment 1 Commitment 2

Commitment 4

M25: FY2021 Achievements in Key Strategic Objectives (5/5)

Over RM13.6 billionin Sustainable Finance. Households across ASEAN.

502,759

Committed

to purchase Malaysia REC, equivalent to 70% of our Malaysian

operations’ Scope 2 carbon emissions.

Established

baseline year for Scope 1 and 2 Carbon Emissions disclosures.

Mobilised Benefitted

Listed on Bloomberg Gender-Equality Index for 5 years in a row.

Embedded Sustainability KPIs in senior management’s performance scorecard.

Maybankers spent

1,636,652 hours on sustainability. Other key milestones

include:

16.9%

27.1%30.6%

20.6%

6.7% 6.1% 3.9% 3.4%

13.4%15.3% 15.2%

12.4%

May'21 Aug'21 Nov'21 Feb'22

Malaysia

Singapore

Indonesia

Financing Support for Customers

% of OutstandingLoan Balance^

As at 12/11/21

As at 11/02/22

Mortgage 32.7% 15.6%

Auto Finance 29.2% 9.6%

Unit Trust 24.4% 12.0%

Other Retail Loans 4.7% 5.2%

SME 39.8% 39.1%1

Business Banking 30.1% 29.4%1

Total CFS 30.4% 17.3%

Global Banking 31.6% 31.8%

Total Malaysia 30.6% 20.6%

% of Loans Under Repayment Assistance, Relief and R&R Programmes

Against Respective Total Home Market Loans

^ Against o/s total gross loans by each country’s respective segments @ 31 Oct 2021 & 31 Jan 20221 Includes Special Relief Facility loans disbursed (RM1.77 billion as at Feb 2022)2 Bank-only, not including subsidiaries i.e., WOM and Maybank Finance.

3 Includes Government relief loans. 4 ESG is the MAS SGD Facility that provides low-cost funding for banks to grant loans under Enterprise Singapore’s Temporary

Bridging Loan Programme and Enterprise Financing Scheme – SME Working Capital Loan

% of OutstandingLoan Balance^

As at 12/11/21

As at 11/02/22

Mortgage 0.9% 0.0%

Auto Finance 0.0% 0.0%

Credit Cards & Personal Loans

4.4% 4.0%

Other Retail Loans 1.8% 0.0%

SME 40.0%3 40.6%3

Business Banking 22.3%3 21.2%3

Total CFS 6.8% 5.8%

Global Banking 0.3% 0.3%

Total Singapore 3.9% 3.4%

% of OutstandingLoan Balance^

As at 12/11/21

As at 14/02/22

Mortgage 14.8% 14.5%

Auto Finance 2.9%2 1.8%2

Credit Cards & Personal Loans

10.8% 2.9%

RSME 20.0% 18.3%

SME+ 20.3% 18.9%

Business Banking 17.8% 16.9%

Total CFS 15.9% 14.4%

Global Banking 14.2% 9.6%

Total Indonesia 15.2% 12.4%

• 17.3% of total CFS loans outstanding (o/s)

is under relief programmes:

o Deferred instalment is 53%

o Reduced instalment is 8%

o Customised/hybrid packages is 39%

• Missed payments is 6% of loans under

relief.

• Of total CFS loans under relief:

o B40: 14%

o M40: 16%

o T20: 31%

o Retail SME: 21%

o Business Banking: 18%

Malaysia

• 31.8% of total GB loans o/s is under relief

programmes:

o Missed payments is 1.0%.

Indonesia

• 14.4% of total CFS loans o/s is under

relief programmes:

o Principal-only deferment option is 19%

o Other relief packages is 81%

• 81% prompt payments.

• 9.6% of total GB loans o/s is under relief

programmes:

o Principal-only deferment option is 54%

o Reduced instalments is 15%

o Conversion of working capital to term

loan instalments and facility

extensions is 31%

• 84% prompt payments.

Singapore

• 5.8% of total CFS loans o/s is under

relief programmes:

o Partial deferment options and

other types of schemes is 6%

o ESG4 is 94%

• 95% prompt payments.

• 0.3% of total GB loans o/s is under

relief programmes:

o Moratorium schemes is 1%

o ESG4 is 99%

• 100% prompt payments.

8

Including URUS and Flood Relief Assistance Programmes, Malaysia’s % of loans under relief increases by 0.2% to 20.8%

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

Table of Contents

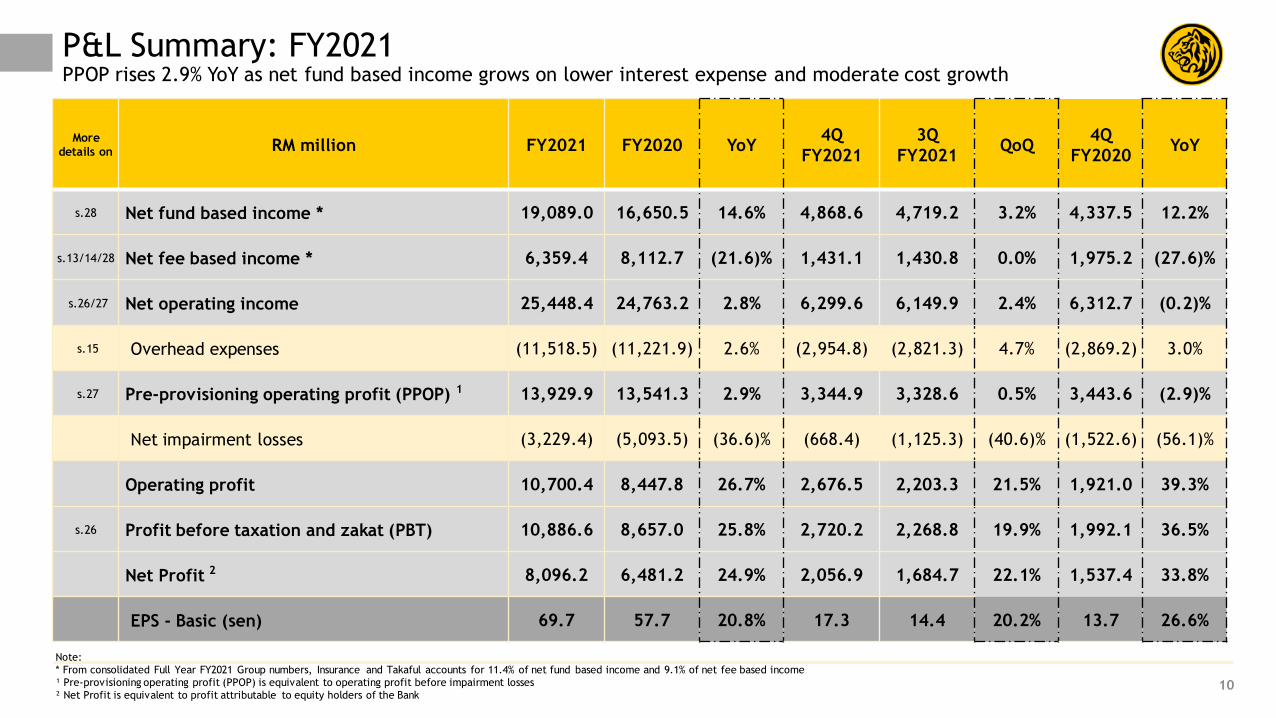

P&L Summary: FY2021PPOP rises 2.9% YoY as net fund based income grows on lower interest expense and moderate cost growth

10

Note:

* From consolidated Full Year FY2021 Group numbers, Insurance and Takaful accounts for 11.4% of net fund based income and 9.1% of net fee based income

¹ Pre-provisioning operating profit (PPOP) is equivalent to operating profit before impairment losses

² Net Profit is equivalent to profit attributable to equity holders of the Bank

More details on RM million FY2021 FY2020 YoY

4Q

FY2021

3Q

FY2021QoQ

4Q

FY2020YoY

s.28 Net fund based income * 19,089.0 16,650.5 14.6% 4,868.6 4,719.2 3.2% 4,337.5 12.2%

s.13/14/28 Net fee based income * 6,359.4 8,112.7 (21.6)% 1,431.1 1,430.8 0.0% 1,975.2 (27.6)%

s.26/27 Net operating income 25,448.4 24,763.2 2.8% 6,299.6 6,149.9 2.4% 6,312.7 (0.2)%

s.15 Overhead expenses (11,518.5) (11,221.9) 2.6% (2,954.8) (2,821.3) 4.7% (2,869.2) 3.0%

s.27 Pre-provisioning operating profit (PPOP) 1 13,929.9 13,541.3 2.9% 3,344.9 3,328.6 0.5% 3,443.6 (2.9)%

Net impairment losses (3,229.4) (5,093.5) (36.6)% (668.4) (1,125.3) (40.6)% (1,522.6) (56.1)%

Operating profit 10,700.4 8,447.8 26.7% 2,676.5 2,203.3 21.5% 1,921.0 39.3%

s.26 Profit before taxation and zakat (PBT) 10,886.6 8,657.0 25.8% 2,720.2 2,268.8 19.9% 1,992.1 36.5%

Net Profit 2 8,096.2 6,481.2 24.9% 2,056.9 1,684.7 22.1% 1,537.4 33.8%

EPS - Basic (sen) 69.7 57.7 20.8% 17.3 14.4 20.2% 13.7 26.6%

19.3 23.5

32.3 24.6

Dec 20 Dec 21

CASA FD Others

248.0 290.8

259.3244.1

72.9 82.8

Dec 20 Dec 21

22.6 24.6

16.3 17.9

Dec 20 Dec 21

Community Financial Services Global Banking

71.5 67.6

36.4 37.1

Dec 20 Dec 21

IDR

tri

llio

n

+2.0%+9.5%

166.4 193.1

116.3 116.772.9

82.1

Dec 20 Dec 21

+12.7%

+13.5%

+8.5%

45.7 53.9

69.4 60.7

Dec 20 Dec 21

(12.6)%+17.2%

247.0 259.7

79.6 80.4

Dec 20 Dec 21

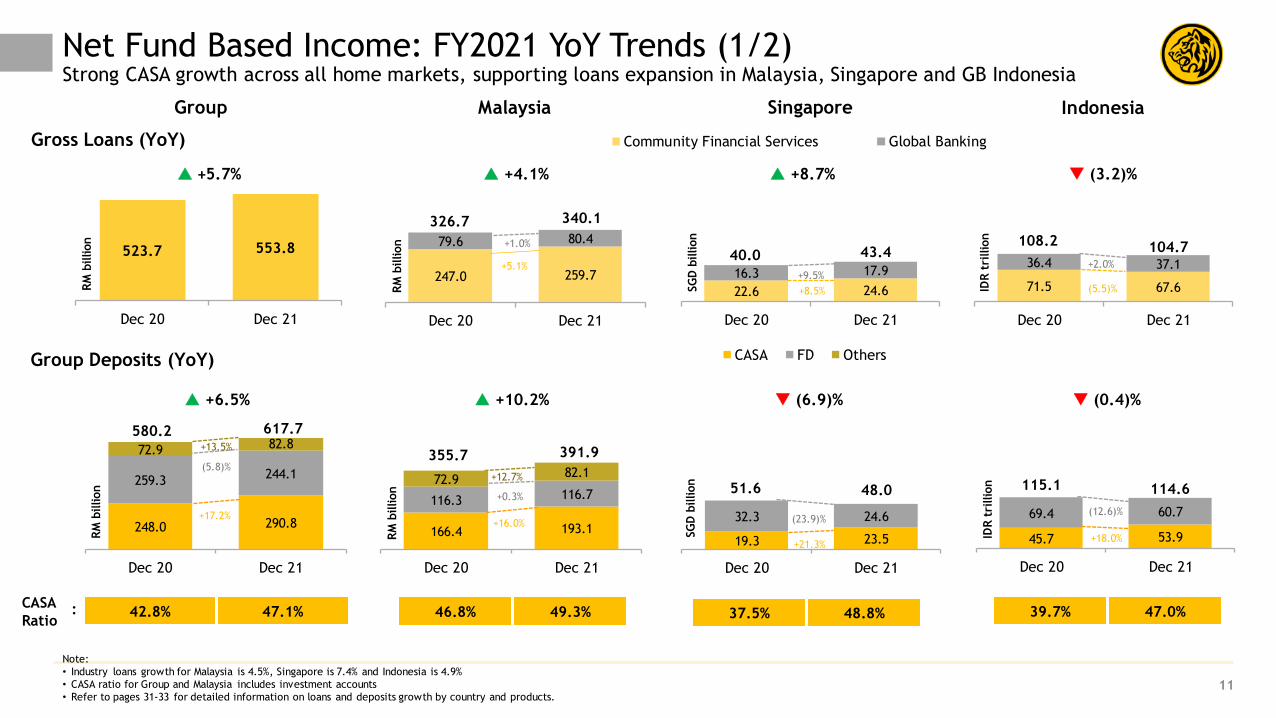

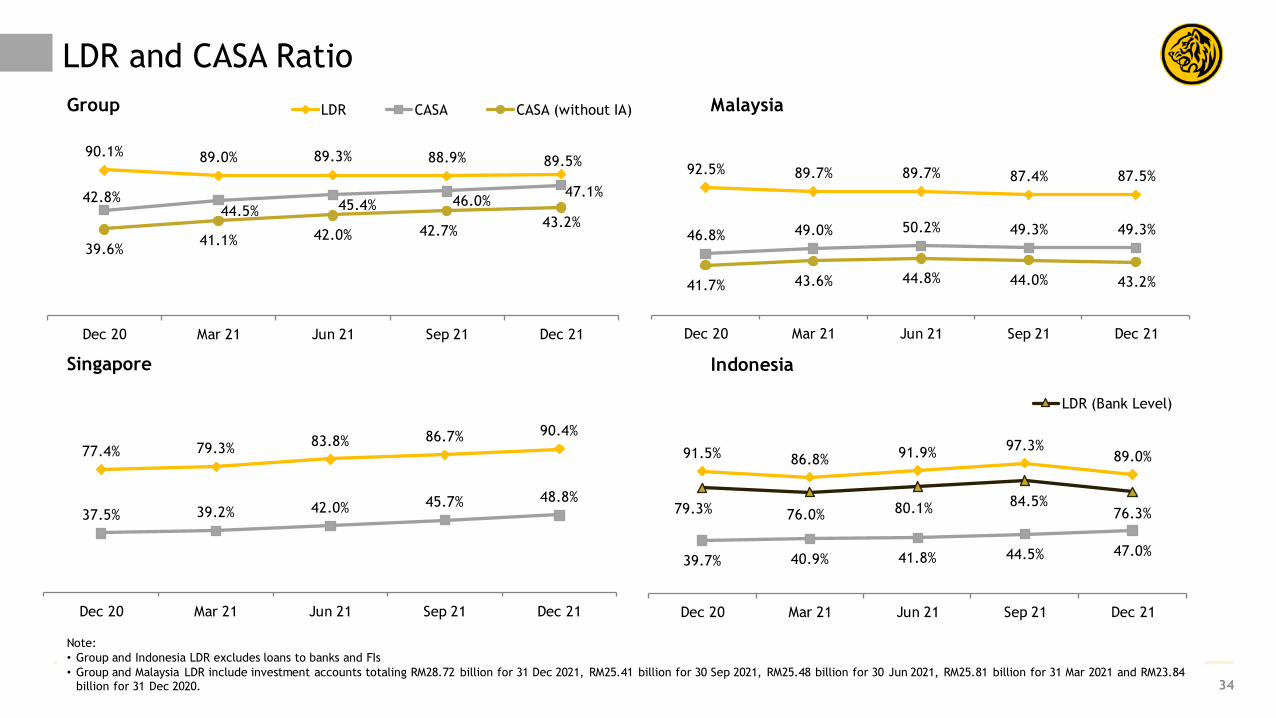

Net Fund Based Income: FY2021 YoY Trends (1/2)Strong CASA growth across all home markets, supporting loans expansion in Malaysia, Singapore and GB Indonesia

11

(5.5)%

+5.1%

391.9(5.8)%

104.7523.7 553.8

Dec 20 Dec 21

326.7

43.4108.2

RM

billion

SG

D b

illion

Gross Loans (YoY)

+4.1% (3.2)% +5.7%

40.0

340.1

RM

billion

RM

billion

SG

D b

illion

IDR

tri

llio

n

Group Deposits (YoY)

37.5% 48.8%46.8% 49.3%42.8% 47.1% 39.7% 47.0%CASA

Ratio:

+0.3%

(23.9)%

580.2 617.7

355.7

51.6 48.0 115.1 114.6

+10.2% (6.9)% (0.4)% +6.5%

+18.0%

RM

billion +1.0%

Note:

• Industry loans growth for Malaysia is 4.5%, Singapore is 7.4% and Indonesia is 4.9%

• CASA ratio for Group and Malaysia includes investment accounts

• Refer to pages 31-33 for detailed information on loans and deposits growth by country and products.

+16.0%

+21.3%

Group Malaysia Singapore Indonesia

+8.7%

2.36 2.33

2.27

2.10

2.32

FY2017 FY2018 FY2019 FY2020 FY2021

12

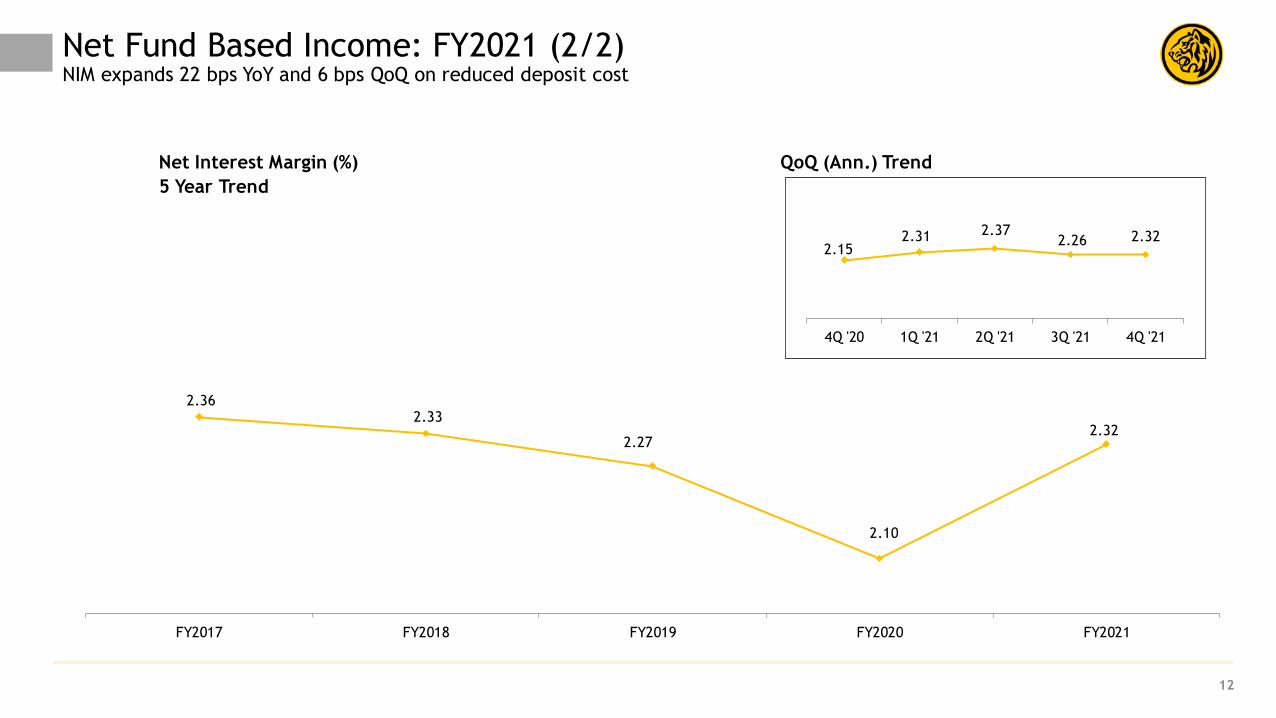

Net Fund Based Income: FY2021 (2/2)NIM expands 22 bps YoY and 6 bps QoQ on reduced deposit cost

5 Year Trend

Net Interest Margin (%) QoQ (Ann.) Trend

2.15 2.31 2.37

2.26 2.32

4Q '20 1Q '21 2Q '21 3Q '21 4Q '21

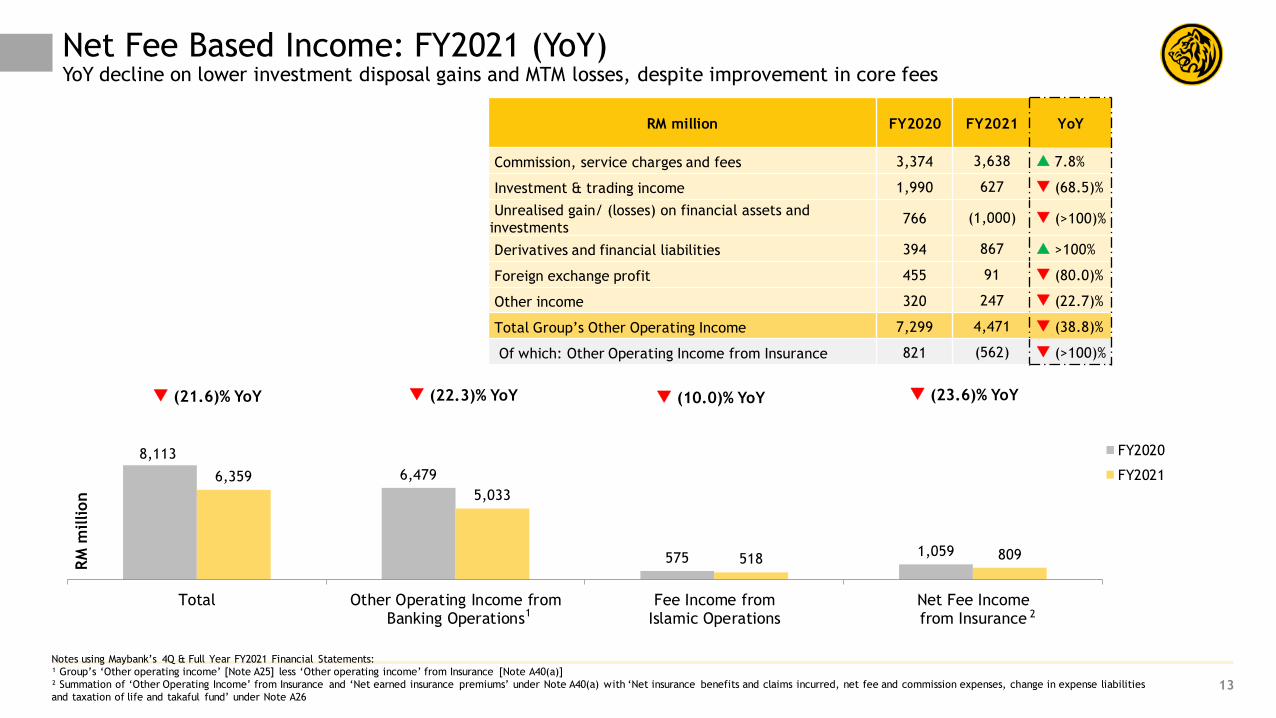

8,113

6,479

575 1,059

6,359

5,033

518 809

Total Other Operating Income fromBanking Operations

Fee Income fromIslamic Operations

Net Fee Incomefrom Insurance

FY2020

FY2021

(23.6)% YoY

13

Net Fee Based Income: FY2021 (YoY)YoY decline on lower investment disposal gains and MTM losses, despite improvement in core fees

RM million FY2020 FY2021 YoY

Commission, service charges and fees 3,374 3,638 7.8%

Investment & trading income 1,990 627 (68.5)%

Unrealised gain/ (losses) on financial assets and

investments766 (1,000) (>100)%

Derivatives and financial liabilities 394 867 >100%

Foreign exchange profit 455 91 (80.0)%

Other income 320 247 (22.7)%

Total Group’s Other Operating Income 7,299 4,471 (38.8)%

Of which: Other Operating Income from Insurance 821 (562) (>100)%

RM

million

1 2

Notes using Maybank’s 4Q & Full Year FY2021 Financial Statements:

¹ Group’s ‘Other operating income’ [Note A25] less ‘Other operating income’ from Insurance [Note A40(a)]

² Summation of ‘Other Operating Income’ from Insurance and ‘Net earned insurance premiums’ under Note A40(a) with ‘Net insurance benefits and claims incurred, net fee and commission expenses, change in expense liabilities

and taxation of life and takaful fund’ under Note A26

(10.0)% YoY (22.3)% YoY (21.6)% YoY

14

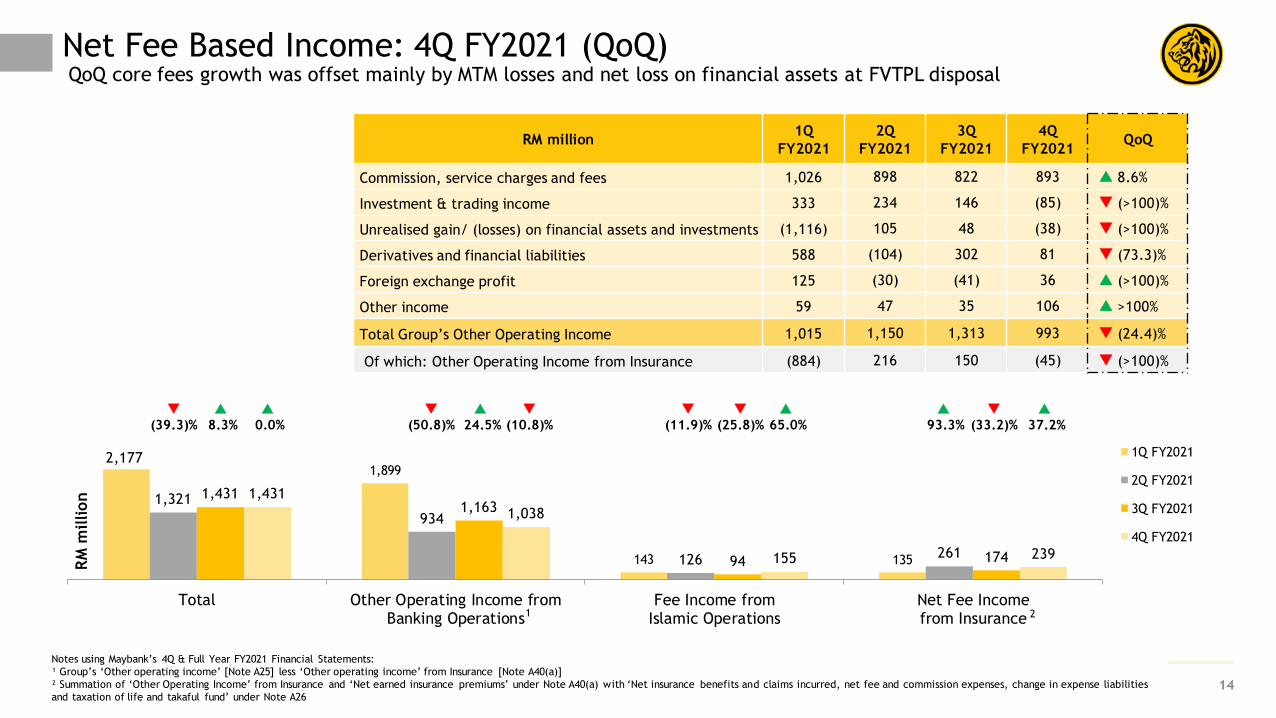

Net Fee Based Income: 4Q FY2021 (QoQ)QoQ core fees growth was offset mainly by MTM losses and net loss on financial assets at FVTPL disposal

2,177 1,899

143 135

1,321

934

126 261

1,431 1,163

94 174

1,431

1,038

155 239

Total Other Operating Income fromBanking Operations

Fee Income fromIslamic Operations

Net Fee Incomefrom Insurance

1Q FY2021

2Q FY2021

3Q FY2021

4Q FY2021

RM million1Q

FY2021

2Q

FY2021

3Q

FY2021

4Q

FY2021QoQ

Commission, service charges and fees 1,026 898 822 893 8.6%

Investment & trading income 333 234 146 (85) (>100)%

Unrealised gain/ (losses) on financial assets and investments (1,116) 105 48 (38) (>100)%

Derivatives and financial liabilities 588 (104) 302 81 (73.3)%

Foreign exchange profit 125 (30) (41) 36 (>100)%

Other income 59 47 35 106 >100%

Total Group’s Other Operating Income 1,015 1,150 1,313 993 (24.4)%

Of which: Other Operating Income from Insurance (884) 216 150 (45) (>100)%

65.0%

(25.8)%

(11.9)%

(50.8)%

24.5%

(10.8)%

(33.2)%

37.2%

93.3%

0.0%

8.3%

(39.3)%

RM

million

1 2

Notes using Maybank’s 4Q & Full Year FY2021 Financial Statements:

¹ Group’s ‘Other operating income’ [Note A25] less ‘Other operating income’ from Insurance [Note A40(a)]

² Summation of ‘Other Operating Income’ from Insurance and ‘Net earned insurance premiums’ under Note A40(a) with ‘Net insurance benefits and claims incurred, net fee and commission expenses, change in expense liabilities

and taxation of life and takaful fund’ under Note A26

15

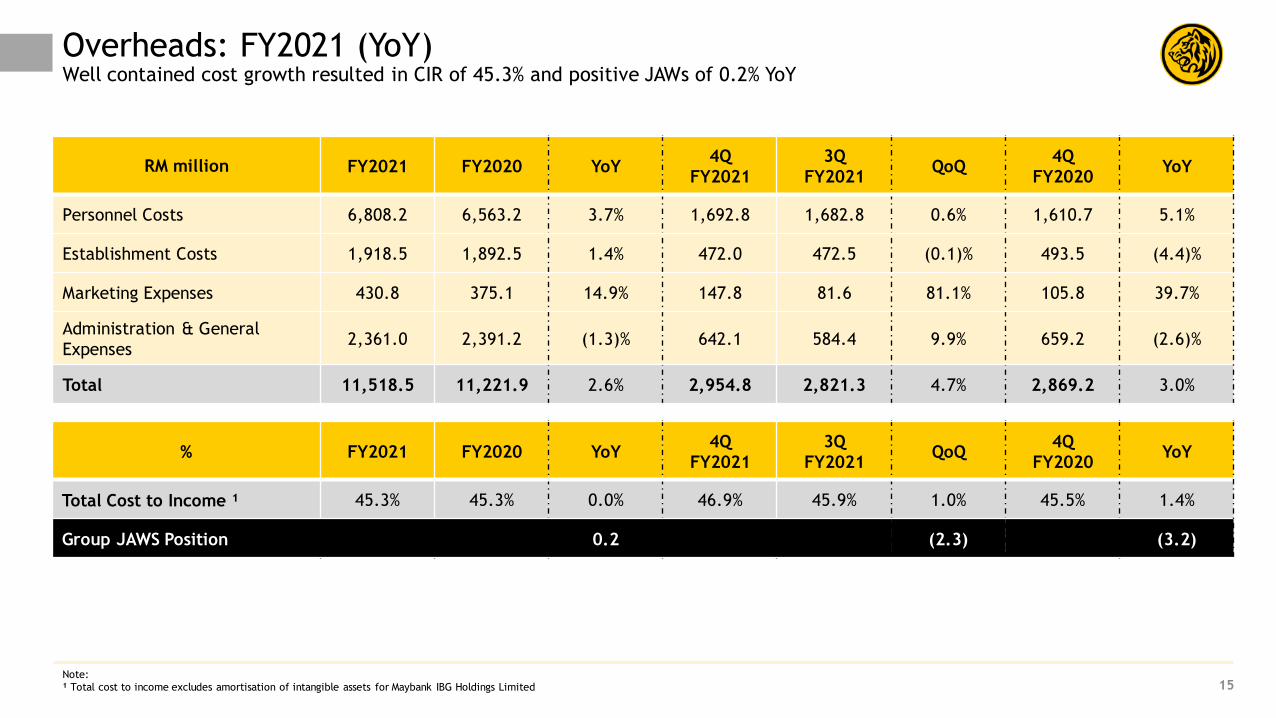

Overheads: FY2021 (YoY)Well contained cost growth resulted in CIR of 45.3% and positive JAWs of 0.2% YoY

Note:

¹ Total cost to income excludes amortisation of intangible assets for Maybank IBG Holdings Limited

RM million FY2021 FY2020 YoY4Q

FY2021

3Q

FY2021QoQ

4Q

FY2020YoY

Personnel Costs 6,808.2 6,563.2 3.7% 1,692.8 1,682.8 0.6% 1,610.7 5.1%

Establishment Costs 1,918.5 1,892.5 1.4% 472.0 472.5 (0.1)% 493.5 (4.4)%

Marketing Expenses 430.8 375.1 14.9% 147.8 81.6 81.1% 105.8 39.7%

Administration & General

Expenses 2,361.0 2,391.2 (1.3)% 642.1 584.4 9.9% 659.2 (2.6)%

Total 11,518.5 11,221.9 2.6% 2,954.8 2,821.3 4.7% 2,869.2 3.0%

% FY2021 FY2020 YoY4Q

FY2021

3Q

FY2021QoQ

4Q

FY2020YoY

Total Cost to Income ¹ 45.3% 45.3% 0.0% 46.9% 45.9% 1.0% 45.5% 1.4%

Group JAWS Position 0.2 (2.3) (3.2)

16

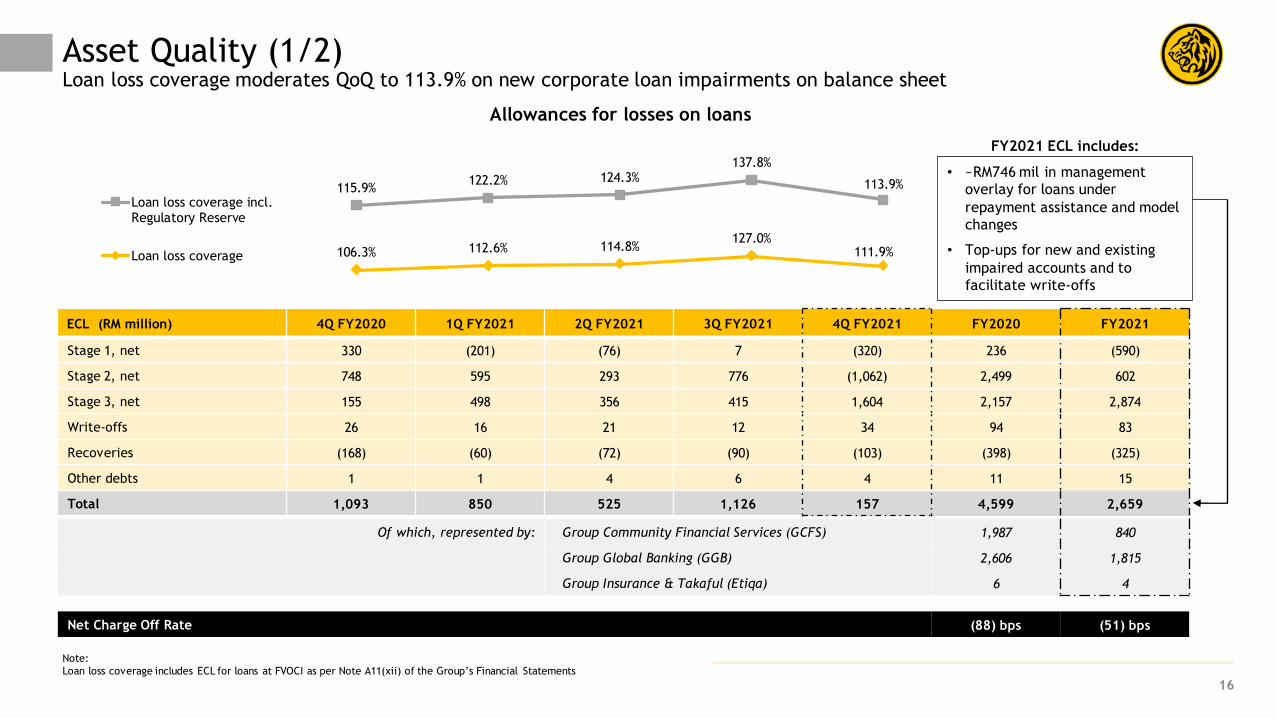

Asset Quality (1/2)Loan loss coverage moderates QoQ to 113.9% on new corporate loan impairments on balance sheet

Allowances for losses on loans

Note:

Loan loss coverage includes ECL for loans at FVOCI as per Note A11(xii) of the Group’s Financial Statements

FY2021 ECL includes:

• ~RM746 mil in management

overlay for loans under

repayment assistance and model

changes

• Top-ups for new and existing

impaired accounts and to

facilitate write-offs

ECL (RM million) 4Q FY2020 1Q FY2021 2Q FY2021 3Q FY2021 4Q FY2021 FY2020 FY2021

Stage 1, net 330 (201) (76) 7 (320) 236 (590)

Stage 2, net 748 595 293 776 (1,062) 2,499 602

Stage 3, net 155 498 356 415 1,604 2,157 2,874

Write-offs 26 16 21 12 34 94 83

Recoveries (168) (60) (72) (90) (103) (398) (325)

Other debts 1 1 4 6 4 11 15

Total 1,093 850 525 1,126 157 4,599 2,659

Of which, represented by: Group Community Financial Services (GCFS) 1,987 840

Group Global Banking (GGB) 2,606 1,815

Group Insurance & Takaful (Etiqa) 6 4

Net Charge Off Rate (88) bps (51) bps

106.3% 112.6% 114.8%127.0%

111.9%

115.9%122.2% 124.3%

137.8%

113.9%

Loan loss coverage incl.Regulatory Reserve

Loan loss coverage

17

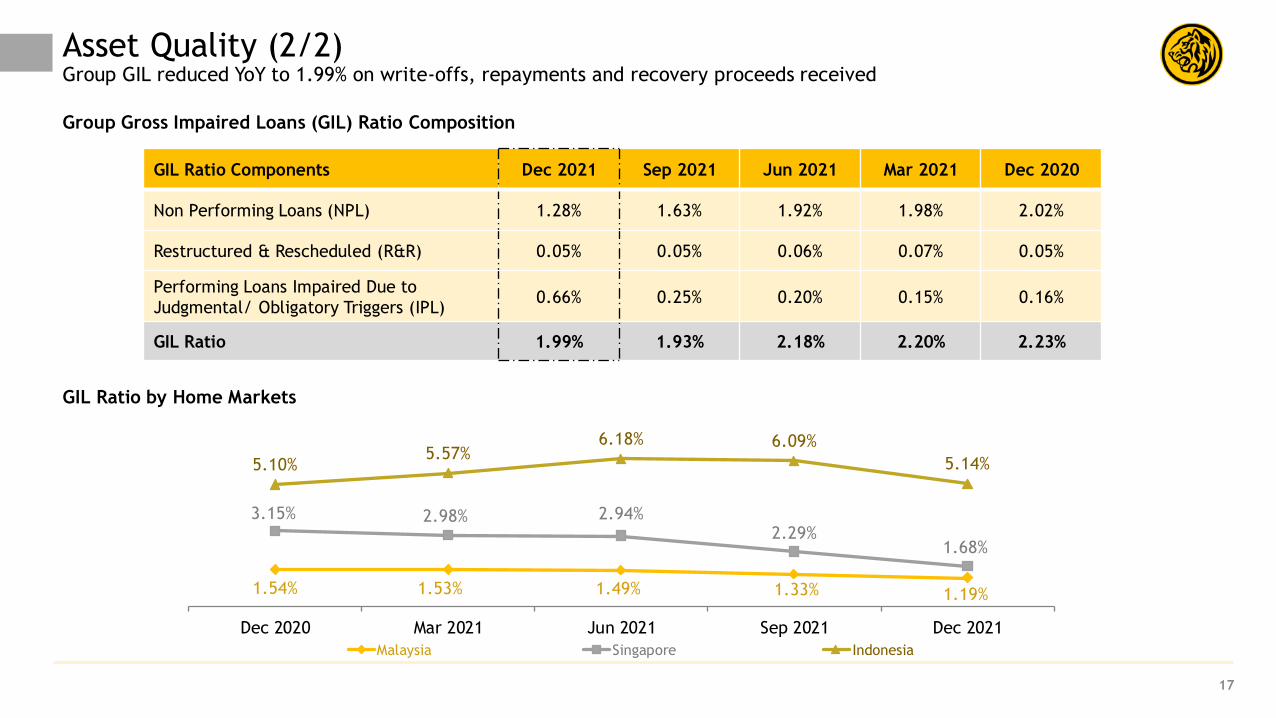

Asset Quality (2/2)Group GIL reduced YoY to 1.99% on write-offs, repayments and recovery proceeds received

1.54% 1.53% 1.49% 1.33% 1.19%

3.15% 2.98% 2.94%2.29%

1.68%

5.10%5.57%

6.18% 6.09%

5.14%

Dec 2020 Mar 2021 Jun 2021 Sep 2021 Dec 2021

Malaysia Singapore Indonesia

GIL Ratio Components Dec 2021 Sep 2021 Jun 2021 Mar 2021 Dec 2020

Non Performing Loans (NPL) 1.28% 1.63% 1.92% 1.98% 2.02%

Restructured & Rescheduled (R&R) 0.05% 0.05% 0.06% 0.07% 0.05%

Performing Loans Impaired Due to

Judgmental/ Obligatory Triggers (IPL)0.66% 0.25% 0.20% 0.15% 0.16%

GIL Ratio 1.99% 1.93% 2.18% 2.20% 2.23%

Group Gross Impaired Loans (GIL) Ratio Composition

GIL Ratio by Home Markets

18

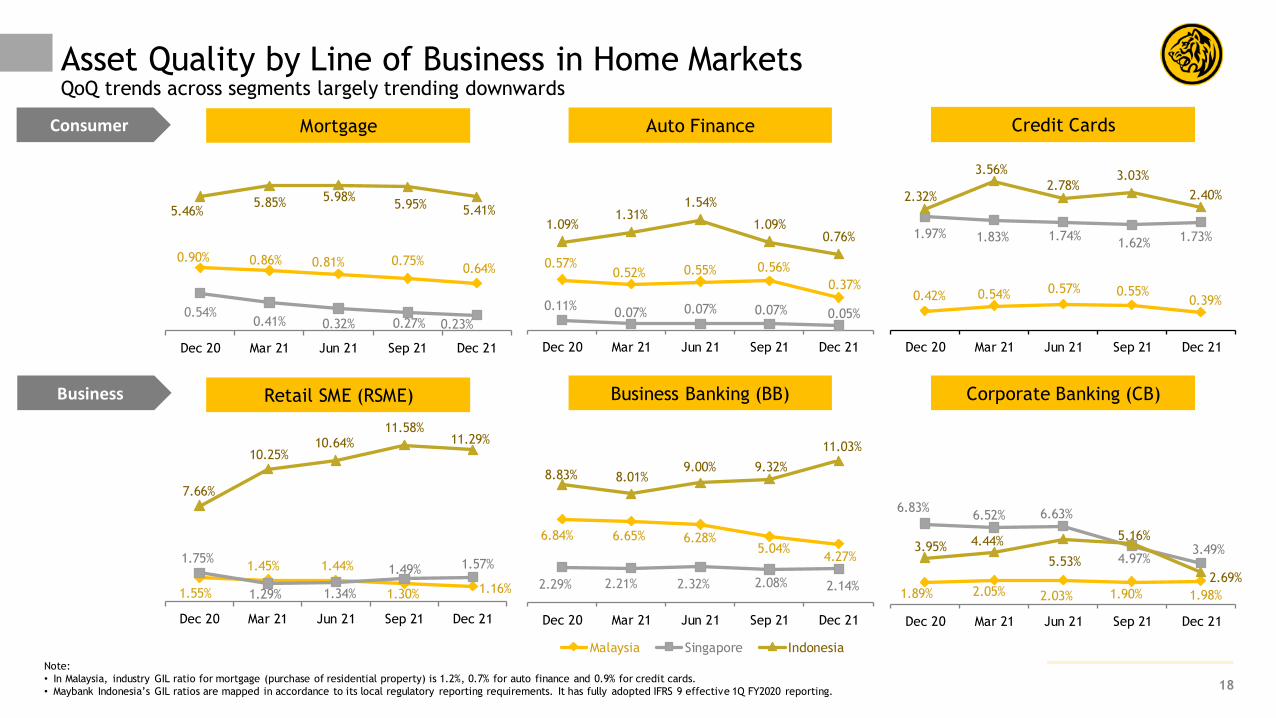

Asset Quality by Line of Business in Home MarketsQoQ trends across segments largely trending downwards

Note:

• In Malaysia, industry GIL ratio for mortgage (purchase of residential property) is 1.2%, 0.7% for auto finance and 0.9% for credit cards.

• Maybank Indonesia’s GIL ratios are mapped in accordance to its local regulatory reporting requirements. It has fully adopted IFRS 9 effective 1Q FY2020 reporting.

0.42% 0.54% 0.57% 0.55%0.39%

1.97% 1.83% 1.74%1.62%

1.73%

2.32%

3.56%

2.78%3.03%

2.40%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

6.84% 6.65% 6.28%5.04%

4.27%

2.29% 2.21% 2.32% 2.08% 2.14%

8.83% 8.01%9.00% 9.32%

11.03%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

Malaysia Singapore Indonesia

Mortgage Auto Finance Credit Cards

Retail SME (RSME) Business Banking (BB) Corporate Banking (CB)

Consumer

Business

0.90% 0.86% 0.81% 0.75%0.64%

0.54%0.41% 0.32% 0.27% 0.23%

5.46%5.85% 5.98%

5.95% 5.41%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

0.57%0.52% 0.55% 0.56%

0.37%

0.11%0.07% 0.07% 0.07% 0.05%

1.09%1.31%

1.54%

1.09%0.76%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

1.89% 2.05% 2.03% 1.90% 1.98%

6.83%6.52% 6.63%

4.97%3.49%3.95% 4.44%

5.53%

5.16%

2.69%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

1.55%

1.45% 1.44%

1.30% 1.16%

1.75%

1.29% 1.34%

1.49% 1.57%

7.66%

10.25%10.64%

11.58%11.29%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

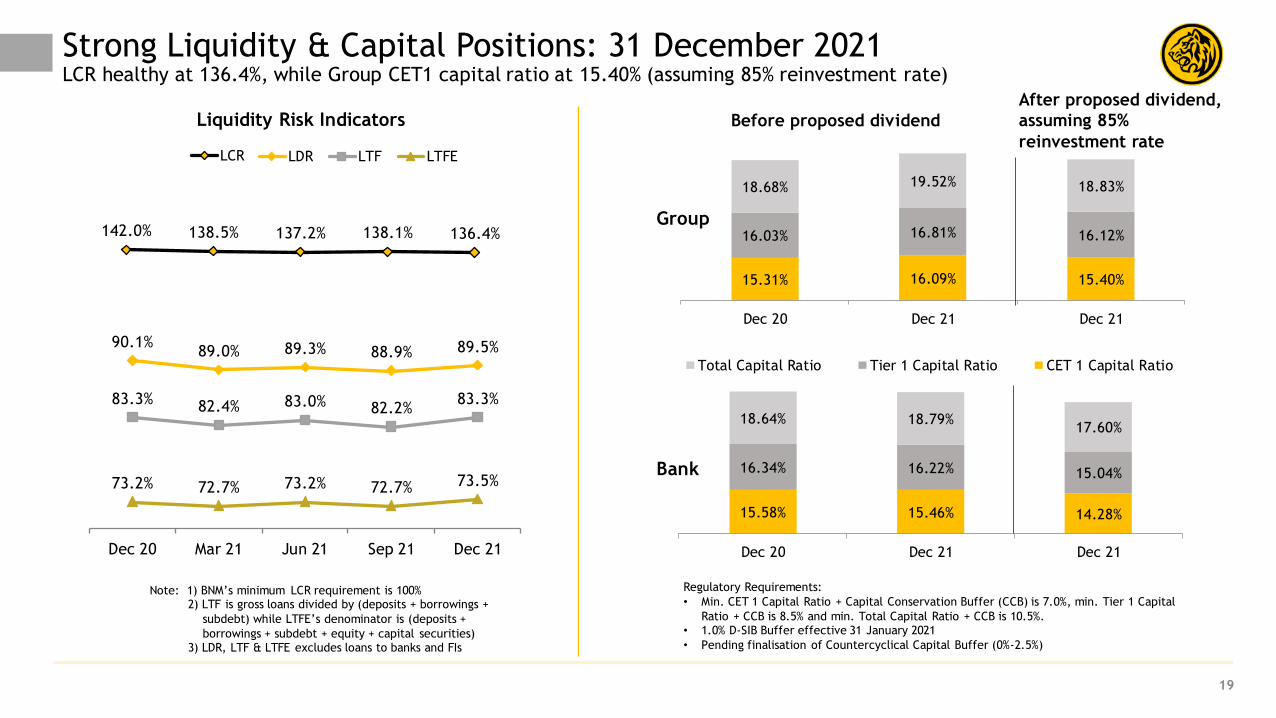

90.1%89.0% 89.3% 88.9% 89.5%

83.3% 82.4% 83.0% 82.2%83.3%

73.2% 72.7% 73.2% 72.7% 73.5%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

LDR LTF LTFE

142.0% 138.5% 137.2% 138.1% 136.4%

LCR

15.58% 15.46% 14.28%

16.34% 16.22% 15.04%

18.64% 18.79%17.60%

Dec 20 Dec 21 Dec 21

15.31% 16.09% 15.40%

16.03% 16.81% 16.12%

18.68% 19.52% 18.83%

Dec 20 Dec 21 Dec 21

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

After proposed dividend,

assuming 85%

reinvestment rate

Before proposed dividendLiquidity Risk Indicators

19

Strong Liquidity & Capital Positions: 31 December 2021LCR healthy at 136.4%, while Group CET1 capital ratio at 15.40% (assuming 85% reinvestment rate)

Regulatory Requirements:

• Min. CET 1 Capital Ratio + Capital Conservation Buffer (CCB) is 7.0%, min. Tier 1 Capital

Ratio + CCB is 8.5% and min. Total Capital Ratio + CCB is 10.5%.• 1.0% D-SIB Buffer effective 31 January 2021

• Pending finalisation of Countercyclical Capital Buffer (0%-2.5%)

Note: 1) BNM’s minimum LCR requirement is 100%2) LTF is gross loans divided by (deposits + borrowings +

subdebt) while LTFE’s denominator is (deposits +

borrowings + subdebt + equity + capital securities)3) LDR, LTF & LTFE excludes loans to banks and FIs

Group

Bank

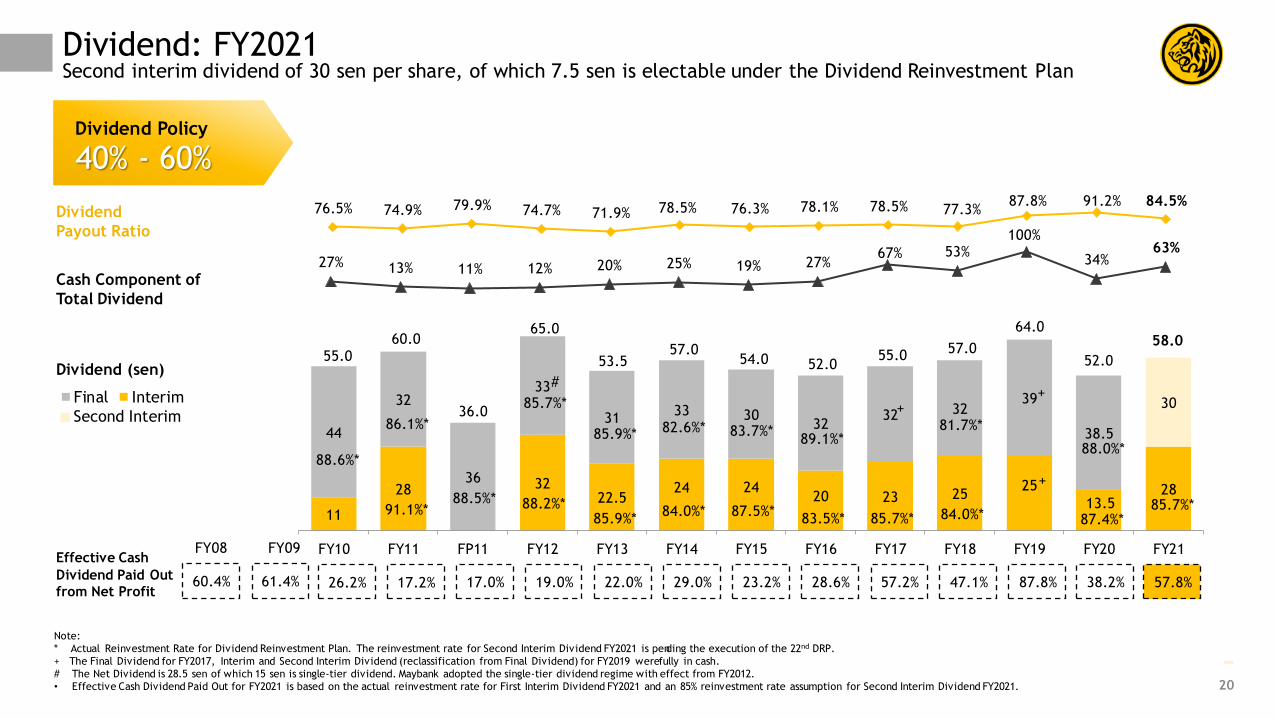

40% - 60%Dividend Policy

11

28 3222.5

24 2420 23 25

25

13.528

44

32

36

33

3133 30

3232 32

39

38.5

30

FY10 FY11 FP11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21

Final Interim

76.5% 74.9% 79.9% 74.7% 71.9% 78.5% 76.3% 78.1% 78.5% 77.3%87.8% 91.2% 84.5%

Dividend

Payout Ratio

Cash Component of

Total Dividend

Effective Cash

Dividend Paid Out

from Net Profit

27% 13% 11% 12% 20% 25% 19% 27%67% 53%

100%

34%63%

26.2% 17.2% 17.0% 19.0% 22.0% 29.0% 23.2% 28.6% 57.2% 47.1% 87.8% 38.2% 57.8%

65.0 64.0

85.9%*

85.7%*

88.2%*85.9%*

88.5%*91.1%*

86.1%*

88.6%*

82.6%*

84.0%*

83.7%*

87.5%*

89.1%*

83.5%* 85.7%* 84.0%*

+81.7%*

+

+

#

55.060.0

36.0

53.557.0

54.0 52.055.0 57.0

88.0%*

52.0

58.0

FY08 FY09

60.4% 61.4%

Dividend (sen)

Note:

* Actual Reinvestment Rate for Dividend Reinvestment Plan. The reinvestment rate for Second Interim Dividend FY2021 is pending the execution of the 22nd DRP.

+ The Final Dividend for FY2017, Interim and Second Interim Dividend (reclassification from Final Dividend) for FY2019 werefully in cash.

# The Net Dividend is 28.5 sen of which 15 sen is single-tier dividend. Maybank adopted the single-tier dividend regime with effect from FY2012.

• Effective Cash Dividend Paid Out for FY2021 is based on the actual reinvestment rate for First Interim Dividend FY2021 and an 85% reinvestment rate assumption for Second Interim Dividend FY2021. 20

Dividend: FY2021Second interim dividend of 30 sen per share, of which 7.5 sen is electable under the Dividend Reinvestment Plan

Second Interim

85.7%*87.4%*

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

Table of Contents

>>>>>

>>>>>

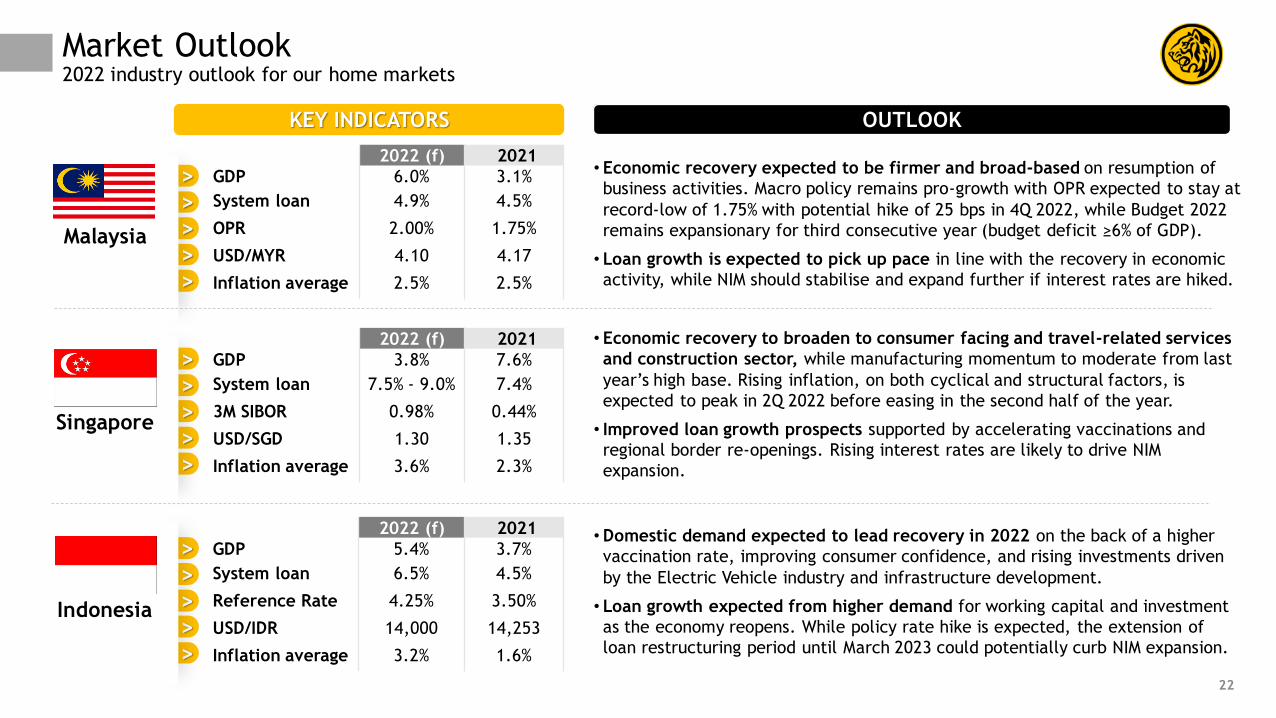

2022 (f) 2021

GDP 3.8% 7.6%

System loan 7.5% - 9.0% 7.4%

3M SIBOR 0.98% 0.44%

USD/SGD 1.30 1.35

Inflation average 3.6% 2.3%

22

Market Outlook2022 industry outlook for our home markets

>>>>>

Malaysia

Indonesia

Singapore

KEY INDICATORS OUTLOOK

• Economic recovery expected to be firmer and broad-based on resumption of

business activities. Macro policy remains pro-growth with OPR expected to stay at

record-low of 1.75% with potential hike of 25 bps in 4Q 2022, while Budget 2022

remains expansionary for third consecutive year (budget deficit ≥6% of GDP).

• Loan growth is expected to pick up pace in line with the recovery in economic

activity, while NIM should stabilise and expand further if interest rates are hiked.

• Economic recovery to broaden to consumer facing and travel-related services

and construction sector, while manufacturing momentum to moderate from last

year’s high base. Rising inflation, on both cyclical and structural factors, is

expected to peak in 2Q 2022 before easing in the second half of the year.

• Improved loan growth prospects supported by accelerating vaccinations and

regional border re-openings. Rising interest rates are likely to drive NIM

expansion.

•Domestic demand expected to lead recovery in 2022 on the back of a higher

vaccination rate, improving consumer confidence, and rising investments driven

by the Electric Vehicle industry and infrastructure development.

• Loan growth expected from higher demand for working capital and investment

as the economy reopens. While policy rate hike is expected, the extension of

loan restructuring period until March 2023 could potentially curb NIM expansion.

2022 (f) 2021

GDP 6.0% 3.1%

System loan 4.9% 4.5%

OPR 2.00% 1.75%

USD/MYR 4.10 4.17

Inflation average 2.5% 2.5%

2022 (f) 2021

GDP 5.4% 3.7%

System loan 6.5% 4.5%

Reference Rate 4.25% 3.50%

USD/IDR 14,000 14,253

Inflation average 3.2% 1.6%

23

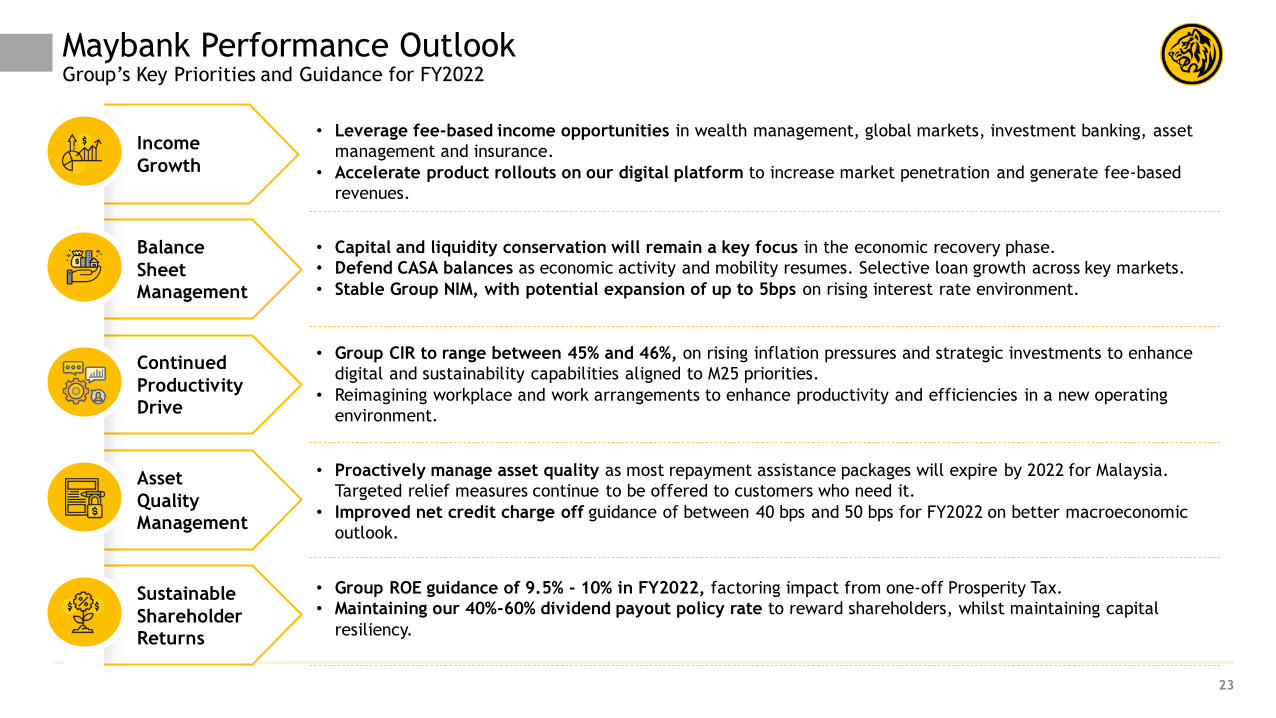

Income

Growth

• Leverage fee-based income opportunities in wealth management, global markets, investment banking, asset

management and insurance.

• Accelerate product rollouts on our digital platform to increase market penetration and generate fee-based

revenues.

Maybank Performance OutlookGroup’s Key Priorities and Guidance for FY2022

Balance

Sheet

Management

Continued

Productivity

Drive

Asset

Quality

Management

Sustainable

Shareholder

Returns

• Capital and liquidity conservation will remain a key focus in the economic recovery phase.

• Defend CASA balances as economic activity and mobility resumes. Selective loan growth across key markets.

• Stable Group NIM, with potential expansion of up to 5bps on rising interest rate environment.

• Group CIR to range between 45% and 46%, on rising inflation pressures and strategic investments to enhance

digital and sustainability capabilities aligned to M25 priorities.

• Reimagining workplace and work arrangements to enhance productivity and efficiencies in a new operating

environment.

• Proactively manage asset quality as most repayment assistance packages will expire by 2022 for Malaysia.

Targeted relief measures continue to be offered to customers who need it.

• Improved net credit charge off guidance of between 40 bps and 50 bps for FY2022 on better macroeconomic

outlook.

• Group ROE guidance of 9.5% - 10% in FY2022, factoring impact from one-off Prosperity Tax.

• Maintaining our 40%-60% dividend payout policy rate to reward shareholders, whilst maintaining capital

resiliency.

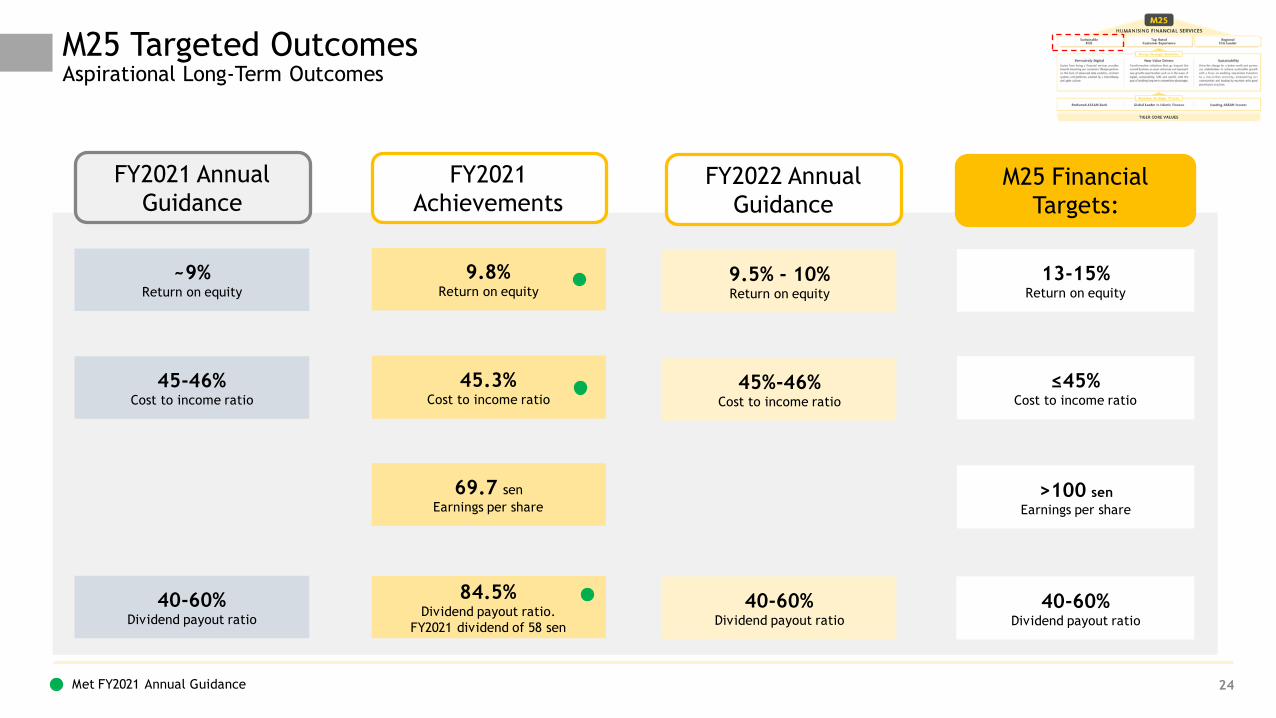

M25 Targeted OutcomesAspirational Long-Term Outcomes

24

M25 Financial

Targets:

13-15% Return on equity

≤45%Cost to income ratio

>100 sen

Earnings per share

40-60%Dividend payout ratio

FY2021 Annual

Guidance

FY2021

Achievements

~9% Return on equity

45-46% Cost to income ratio

40-60%Dividend payout ratio

9.8% Return on equity

45.3% Cost to income ratio

69.7 sen

Earnings per share

84.5%Dividend payout ratio.

FY2021 dividend of 58 sen

Met FY2021 Annual Guidance

FY2022 Annual

Guidance

9.5% - 10% Return on equity

45%-46% Cost to income ratio

40-60%Dividend payout ratio

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

Table of Contents

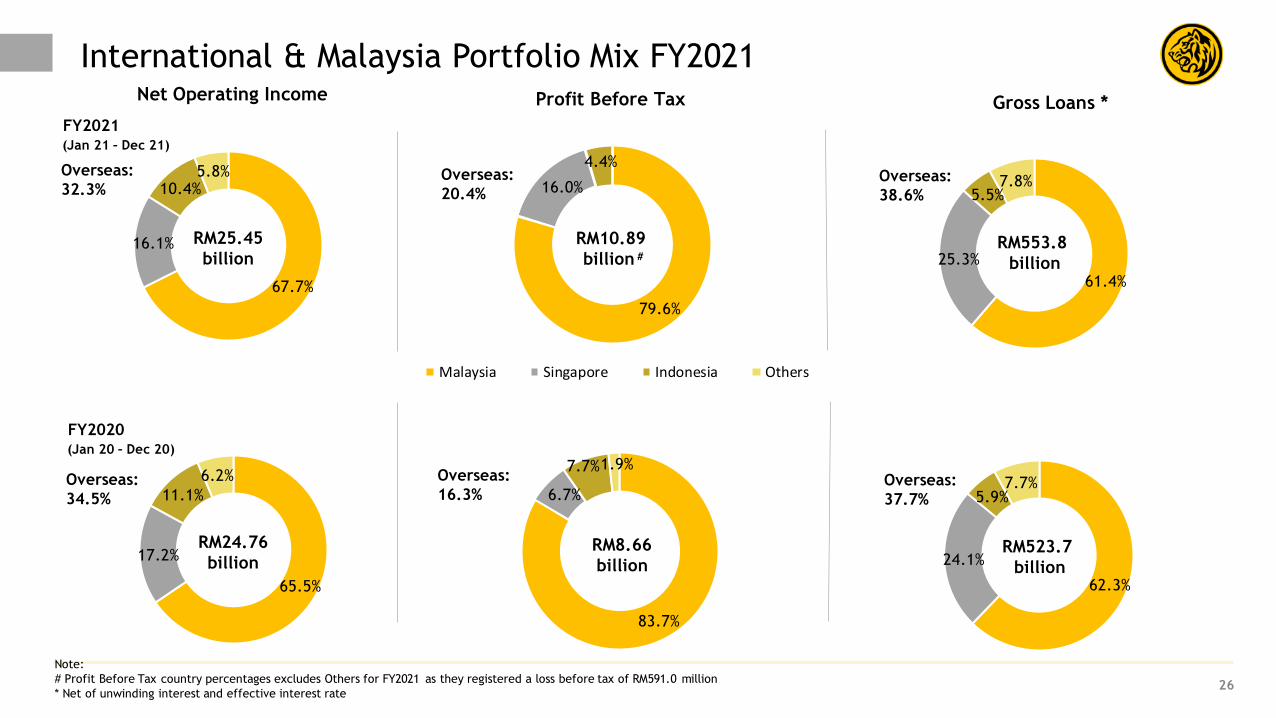

83.7%

6.7%

7.7%1.9%

79.6%

16.0%

4.4%

Malaysia Singapore Indonesia Others

Overseas:

20.4%

Overseas:

16.3%

61.4%

25.3%

5.5%7.8%

International & Malaysia Portfolio Mix FY2021

26

Overseas:

38.6%

67.7%

16.1%

10.4%5.8%

Net Operating Income Profit Before Tax

FY2021

Gross Loans *

Overseas:

32.3%

(Jan 21 – Dec 21)

RM10.89

billion #RM553.8

billion

RM25.45

billion

62.3%

24.1%

5.9%7.7%Overseas:

37.7%

65.5%

17.2%

11.1%

6.2%

FY2020

Overseas:

34.5%

(Jan 20 – Dec 20)

RM8.66

billionRM523.7

billion

RM24.76

billion

Note:

# Profit Before Tax country percentages excludes Others for FY2021 as they registered a loss before tax of RM591.0 million

* Net of unwinding interest and effective interest rate

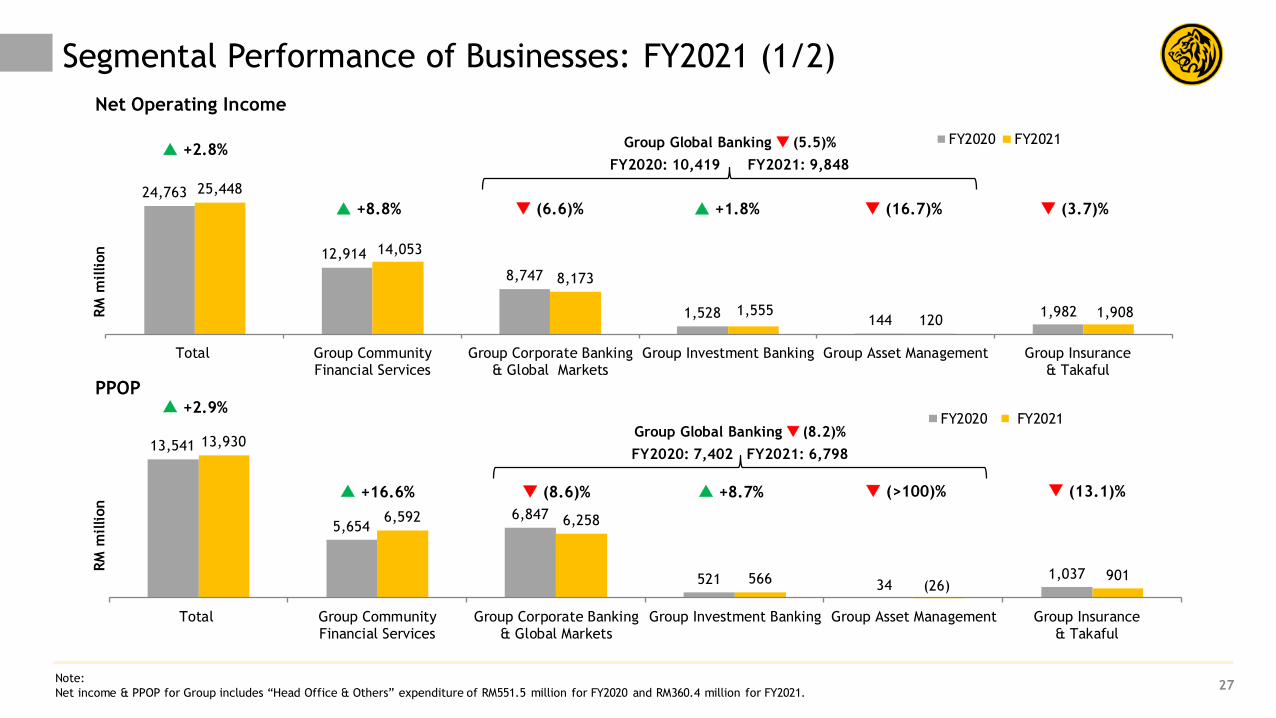

Segmental Performance of Businesses: FY2021 (1/2)

27

13,541

5,654 6,847

521 34 1,037

13,930

6,592 6,258

566 (26)

901

Total Group CommunityFinancial Services

Group Corporate Banking& Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2020 FY2021

24,763

12,914

8,747

1,528 144

1,982

25,448

14,053

8,173

1,555 120

1,908

Total Group CommunityFinancial Services

Group Corporate Banking& Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2020 FY2021

Net Operating Income

+2.8%

RM

million

PPOP

+8.8% (6.6)%

Group Global Banking (8.2)%

Group Global Banking (5.5)%

FY2020: 10,419 FY2021: 9,848

FY2020: 7,402 FY2021: 6,798

RM

million

(8.6)% +16.6%

+1.8% (16.7)% (3.7)%

+2.9%

+8.7% (>100)% (13.1)%

Note:

Net income & PPOP for Group includes “Head Office & Others” expenditure of RM551.5 million for FY2020 and RM360.4 million for FY2021.

16,651

9,900

5,409

243 2 1,260

19,089

10,866

5,703

306 2 1,376

Total Group CommunityFinancial Services

Group Corporate Banking & Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2020 FY2021

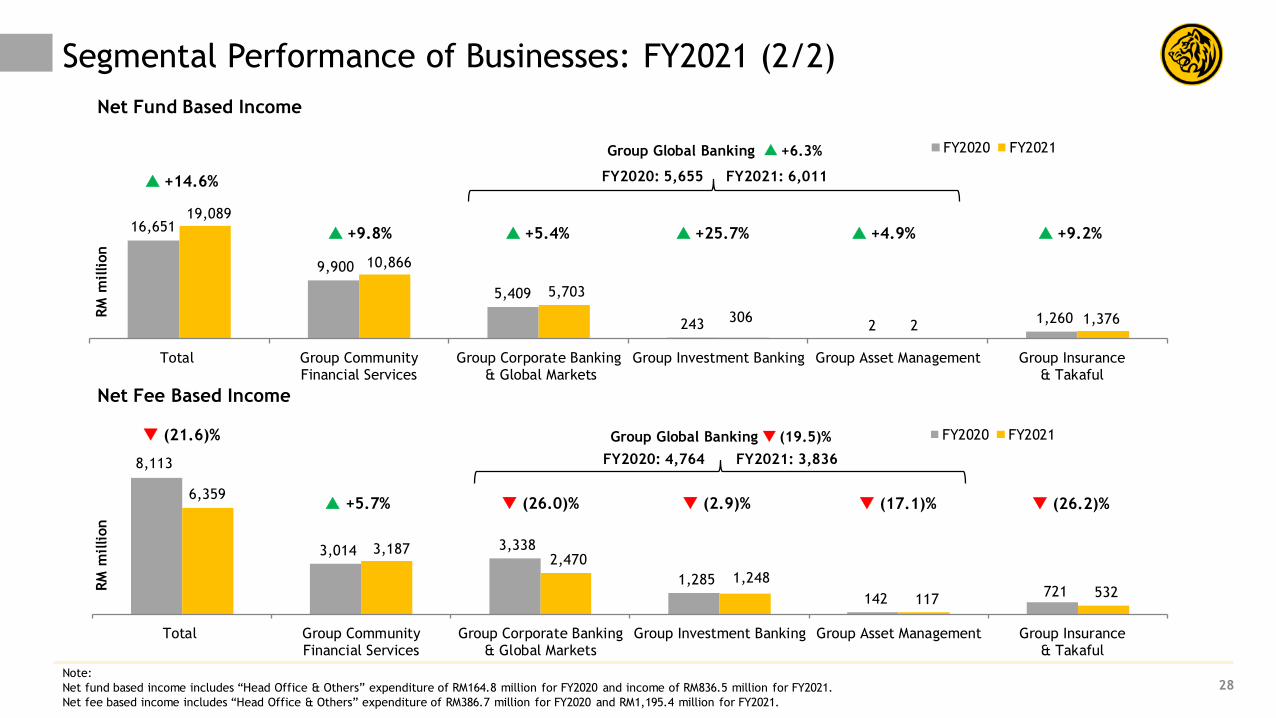

Segmental Performance of Businesses: FY2021 (2/2)

28

8,113

3,014 3,338

1,285

142 721

6,359

3,187 2,470

1,248

117 532

Total Group CommunityFinancial Services

Group Corporate Banking& Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2020 FY2021

Net Fund Based Income

Group Global Banking +6.3%

Net Fee Based Income

+25.7% +4.9% +9.8% +5.4% +9.2%

FY2020: 5,655 FY2021: 6,011

Group Global Banking (19.5)%

FY2020: 4,764 FY2021: 3,836

(26.0)% +5.7%

(21.6)%

+14.6%

(2.9)% (17.1)% (26.2)%

Note:

Net fund based income includes “Head Office & Others” expenditure of RM164.8 million for FY2020 and income of RM836.5 million for FY2021.

Net fee based income includes “Head Office & Others” expenditure of RM386.7 million for FY2020 and RM1,195.4 million for FY2021.

RM

million

RM

million

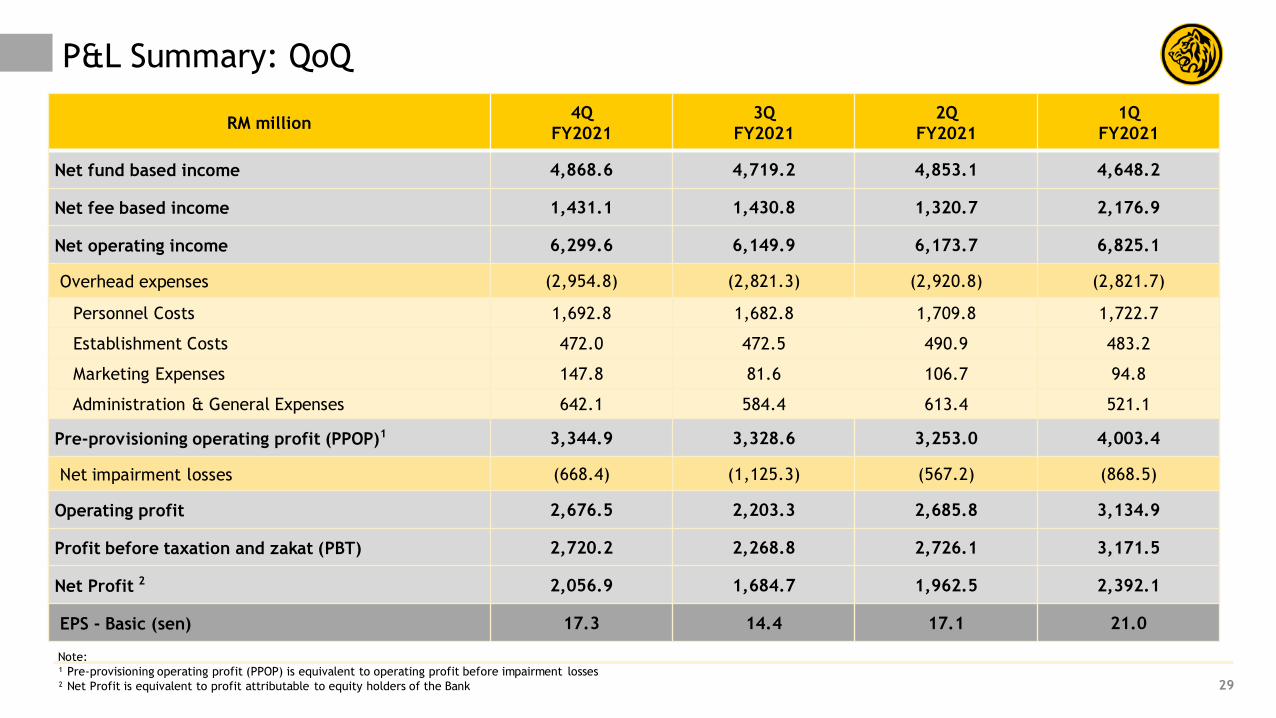

P&L Summary: QoQ

29

RM million4Q

FY2021

3Q

FY2021

2Q

FY2021

1Q

FY2021

Net fund based income 4,868.6 4,719.2 4,853.1 4,648.2

Net fee based income 1,431.1 1,430.8 1,320.7 2,176.9

Net operating income 6,299.6 6,149.9 6,173.7 6,825.1

Overhead expenses (2,954.8) (2,821.3) (2,920.8) (2,821.7)

Personnel Costs 1,692.8 1,682.8 1,709.8 1,722.7

Establishment Costs 472.0 472.5 490.9 483.2

Marketing Expenses 147.8 81.6 106.7 94.8

Administration & General Expenses 642.1 584.4 613.4 521.1

Pre-provisioning operating profit (PPOP)1 3,344.9 3,328.6 3,253.0 4,003.4

Net impairment losses (668.4) (1,125.3) (567.2) (868.5)

Operating profit 2,676.5 2,203.3 2,685.8 3,134.9

Profit before taxation and zakat (PBT) 2,720.2 2,268.8 2,726.1 3,171.5

Net Profit 2 2,056.9 1,684.7 1,962.5 2,392.1

EPS - Basic (sen) 17.3 14.4 17.1 21.0

Note:

¹ Pre-provisioning operating profit (PPOP) is equivalent to operating profit before impairment losses

² Net Profit is equivalent to profit attributable to equity holders of the Bank

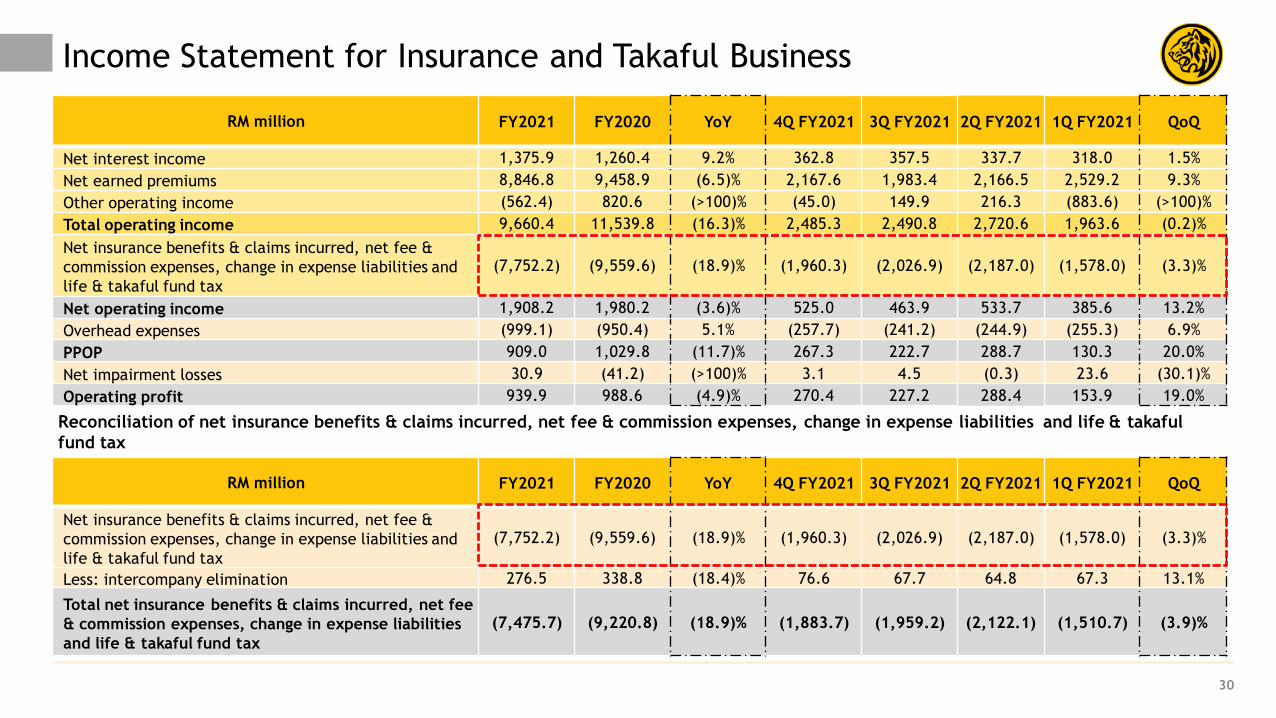

Income Statement for Insurance and Takaful Business

30

RM million FY2021 FY2020 YoY 4Q FY2021 3Q FY2021 2Q FY2021 1Q FY2021 QoQ

Net interest income 1,375.9 1,260.4 9.2% 362.8 357.5 337.7 318.0 1.5%

Net earned premiums 8,846.8 9,458.9 (6.5)% 2,167.6 1,983.4 2,166.5 2,529.2 9.3%

Other operating income (562.4) 820.6 (>100)% (45.0) 149.9 216.3 (883.6) (>100)%

Total operating income 9,660.4 11,539.8 (16.3)% 2,485.3 2,490.8 2,720.6 1,963.6 (0.2)%

Net insurance benefits & claims incurred, net fee &

commission expenses, change in expense liabilities and

life & takaful fund tax

(7,752.2) (9,559.6) (18.9)% (1,960.3) (2,026.9) (2,187.0) (1,578.0) (3.3)%

Net operating income 1,908.2 1,980.2 (3.6)% 525.0 463.9 533.7 385.6 13.2%

Overhead expenses (999.1) (950.4) 5.1% (257.7) (241.2) (244.9) (255.3) 6.9%

PPOP 909.0 1,029.8 (11.7)% 267.3 222.7 288.7 130.3 20.0%

Net impairment losses 30.9 (41.2) (>100)% 3.1 4.5 (0.3) 23.6 (30.1)%

Operating profit 939.9 988.6 (4.9)% 270.4 227.2 288.4 153.9 19.0%

RM million FY2021 FY2020 YoY 4Q FY2021 3Q FY2021 2Q FY2021 1Q FY2021 QoQ

Net insurance benefits & claims incurred, net fee &

commission expenses, change in expense liabilities and

life & takaful fund tax

(7,752.2) (9,559.6) (18.9)% (1,960.3) (2,026.9) (2,187.0) (1,578.0) (3.3)%

Less: intercompany elimination 276.5 338.8 (18.4)% 76.6 67.7 64.8 67.3 13.1%

Total net insurance benefits & claims incurred, net fee

& commission expenses, change in expense liabilities

and life & takaful fund tax

(7,475.7) (9,220.8) (18.9)% (1,883.7) (1,959.2) (2,122.1) (1,510.7) (3.9)%

Reconciliation of net insurance benefits & claims incurred, net fee & commission expenses, change in expense liabilities and life & takaful

fund tax

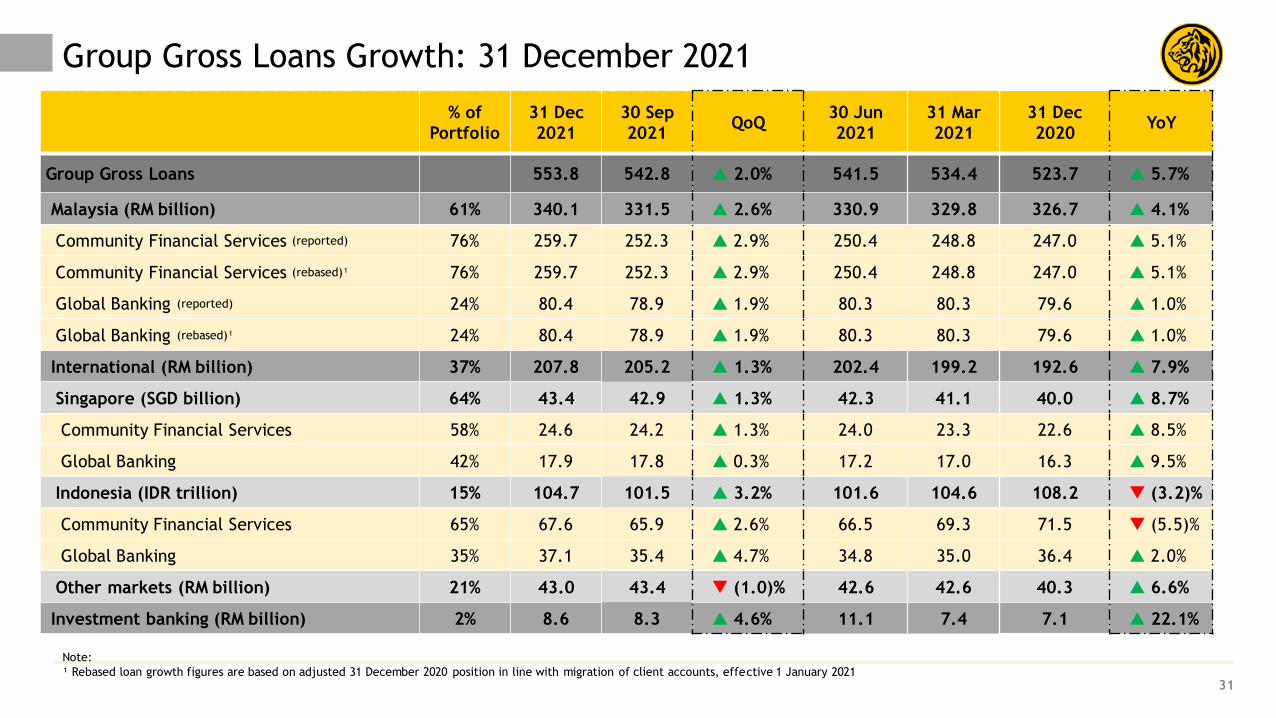

Group Gross Loans Growth: 31 December 2021

31

% of

Portfolio

31 Dec

2021

30 Sep

2021QoQ

30 Jun

2021

31 Mar

2021

31 Dec

2020YoY

Group Gross Loans 553.8 542.8 2.0% 541.5 534.4 523.7 5.7%

Malaysia (RM billion) 61% 340.1 331.5 2.6% 330.9 329.8 326.7 4.1%

Community Financial Services (reported) 76% 259.7 252.3 2.9% 250.4 248.8 247.0 5.1%

Community Financial Services (rebased)¹ 76% 259.7 252.3 2.9% 250.4 248.8 247.0 5.1%

Global Banking (reported) 24% 80.4 78.9 1.9% 80.3 80.3 79.6 1.0%

Global Banking (rebased)¹ 24% 80.4 78.9 1.9% 80.3 80.3 79.6 1.0%

International (RM billion) 37% 207.8 205.2 1.3% 202.4 199.2 192.6 7.9%

Singapore (SGD billion) 64% 43.4 42.9 1.3% 42.3 41.1 40.0 8.7%

Community Financial Services 58% 24.6 24.2 1.3% 24.0 23.3 22.6 8.5%

Global Banking 42% 17.9 17.8 0.3% 17.2 17.0 16.3 9.5%

Indonesia (IDR trillion) 15% 104.7 101.5 3.2% 101.6 104.6 108.2 (3.2)%

Community Financial Services 65% 67.6 65.9 2.6% 66.5 69.3 71.5 (5.5)%

Global Banking 35% 37.1 35.4 4.7% 34.8 35.0 36.4 2.0%

Other markets (RM billion) 21% 43.0 43.4 (1.0)% 42.6 42.6 40.3 6.6%

Investment banking (RM billion) 2% 8.6 8.3 4.6% 11.1 7.4 7.1 22.1%

Note:

¹ Rebased loan growth figures are based on adjusted 31 December 2020 position in line with migration of client accounts, effective 1 January 2021

Malaysia Loans Growth: 31 December 2021

32

RM billion% of

Portfolio

31 Dec

2021

30 Sep

2021QoQ

30 Jun

2021

31 Mar

2021

31 Dec

2020YoY

Community Financial Services (reported) 76% 259.7 252.3 2.9% 250.4 248.8 247.0 5.1%

Community Financial Services (rebased)¹ 76% 259.7 252.3 2.9% 250.4 248.8 247.0 5.1%

Consumer 61% 207.9 202.0 3.0% 200.9 200.2 199.2 4.4%

Total Mortgage 34% 115.2 112.7 2.2% 111.5 110.0 108.1 6.6%

Auto Finance 16% 53.9 52.0 3.7% 52.8 53.0 52.8 2.0%

Credit Cards 2% 7.4 6.7 9.8% 6.5 6.9 7.1 4.5%

Unit Trust 8% 29.1 28.3 2.9% 28.0 28.2 29.2 (0.2)%

Other Retail Loans 1% 2.3 2.2 3.4% 2.2 2.1 2.1 11.7%

Business Banking + SME (reported) 15% 51.7 50.4 2.7% 49.5 48.7 47.8 8.3%

Business Banking + SME (rebased)¹ 15% 51.7 50.4 2.7% 49.5 48.7 47.8 8.3%

SME (reported) 7% 24.1 23.3 3.2% 22.6 22.1 21.7 10.7%

SME (rebased)¹ 7% 24.1 23.3 3.2% 22.6 22.1 21.5 11.9%

Business Banking (reported) 8% 27.7 27.1 2.2% 26.9 26.6 26.0 6.3%

Business Banking (rebased)¹ 8% 27.7 27.1 2.2% 26.9 26.6 26.3 5.3%

Global Banking (Corporate) (reported) 24% 80.4 78.9 1.9% 80.3 80.3 79.6 1.0%

Global Banking (Corporate) (rebased)¹ 24% 80.4 78.9 1.9% 80.3 80.3 79.6 1.0%

Total Malaysia 340.1 331.5 2.6% 330.9 329.8 326.7 4.1%

Note:

¹ Rebased loan growth figures are based on adjusted 31 December 2020 position in line with migration of client accounts, effective 1 January 2021

Group Deposits Growth: 31 December 2021

33

% of

Portfolio

31 Dec

2021

30 Sep

2021QoQ

30 Jun

2021

31 Mar

2021

31 Dec

2020YoY

Group Gross Deposits 617.7 609.6 1.3% 605.0 599.6 580.2 6.5%

Malaysia (RM billion) 63% 391.9 382.7 2.4% 372.2 370.3 355.7 10.2%

Savings Deposits 17% 67.4 67.1 0.4% 64.9 62.5 56.8 18.5%

Current Accounts 32% 125.7 121.6 3.4% 122.0 118.9 109.6 14.7%

Fixed Deposits 30% 116.7 121.6 (4.1)% 120.5 118.1 116.3 0.3%

Others 21% 82.1 72.4 13.4% 64.8 70.8 72.9 12.7%

International 37% 227.4 228.2 (0.4)% 233.9 230.7 225.6 0.8%

Singapore (SGD billion) 65% 48.0 49.5 (2.9)% 50.6 51.8 51.6 (6.9)%

Savings Deposits 19% 9.2 9.3 (0.5)% 9.1 9.0 8.6 7.1%

Current Accounts 30% 14.2 13.3 6.7% 12.1 11.4 10.7 32.9%

Fixed Deposits 51% 24.6 26.8 (8.5)% 29.4 31.5 32.3 (23.9)%

Indonesia (IDR trillion) 15% 114.6 101.6 12.7% 107.5 117.2 115.1 (0.4)%

Savings Deposits 19% 21.9 21.3 2.8% 21.3 21.1 21.2 3.4%

Current Accounts 28% 32.0 23.9 33.8% 23.7 26.8 24.5 30.6%

Fixed Deposits 53% 60.7 56.4 7.6% 62.5 69.3 69.4 (12.6)%

90.1% 89.0% 89.3% 88.9% 89.5%

42.8%44.5% 45.4% 46.0%

47.1%

39.6%41.1% 42.0% 42.7%

43.2%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

LDR CASA CASA (without IA)

77.4% 79.3%83.8% 86.7% 90.4%

37.5% 39.2% 42.0% 45.7% 48.8%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

LDR and CASA Ratio

34

Indonesia

Malaysia

92.5% 89.7% 89.7% 87.4% 87.5%

46.8% 49.0% 50.2% 49.3% 49.3%

41.7% 43.6% 44.8% 44.0% 43.2%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

Singapore

Group

91.5% 86.8% 91.9%97.3%

89.0%

39.7% 40.9% 41.8% 44.5% 47.0%

79.3% 76.0% 80.1%84.5%

76.3%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

LDR (Bank Level)

Note:

• Group and Indonesia LDR excludes loans to banks and FIs

• Group and Malaysia LDR include investment accounts totaling RM28.72 billion for 31 Dec 2021, RM25.41 billion for 30 Sep 2021, RM25.48 billion for 30 Jun 2021, RM25.81 billion for 31 Mar 2021 and RM23.84 billion for 31 Dec 2020.

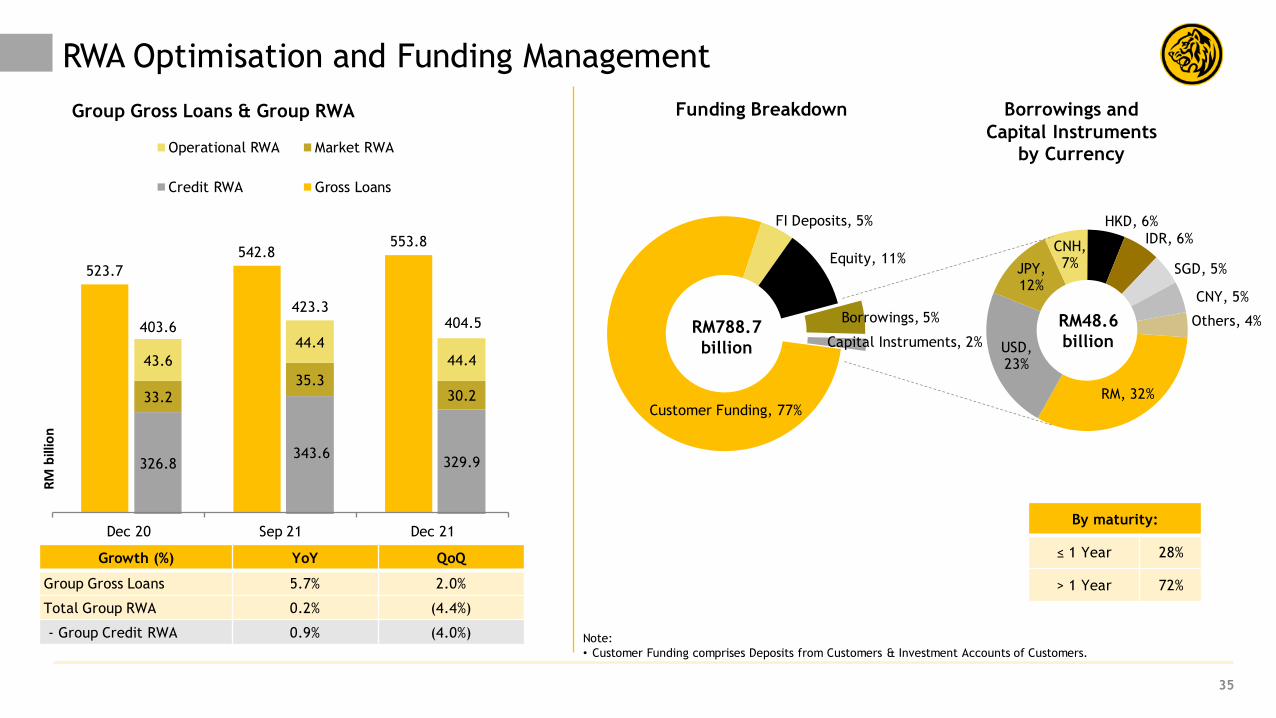

326.8343.6

329.9

33.235.3

30.2

43.6

44.4

44.4

Operational RWA Market RWA

Credit RWA Gross Loans

523.7

542.8553.8

Dec 20 Sep 21 Dec 21

404.5 Borrowings, 5%

Capital Instruments, 2%

Customer Funding, 77%

FI Deposits, 5%

Equity, 11%

RWA Optimisation and Funding Management

35

RM, 32%

USD, 23%

JPY, 12%

CNH, 7%

HKD, 6%

IDR, 6%

SGD, 5%

CNY, 5%

Others, 4%

Funding Breakdown

Note:

• Customer Funding comprises Deposits from Customers & Investment Accounts of Customers.

By maturity:

≤ 1 Year 28%

> 1 Year 72%

Borrowings and

Capital Instruments

by Currency

Group Gross Loans & Group RWA

RM

bill

ion

Growth (%) YoY QoQ

Group Gross Loans 5.7% 2.0%

Total Group RWA 0.2% (4.4%)

- Group Credit RWA 0.9% (4.0%)

403.6

423.3

RM788.7

billion

RM48.6

billion

Specific Loan Exposure as at 31 December 2021

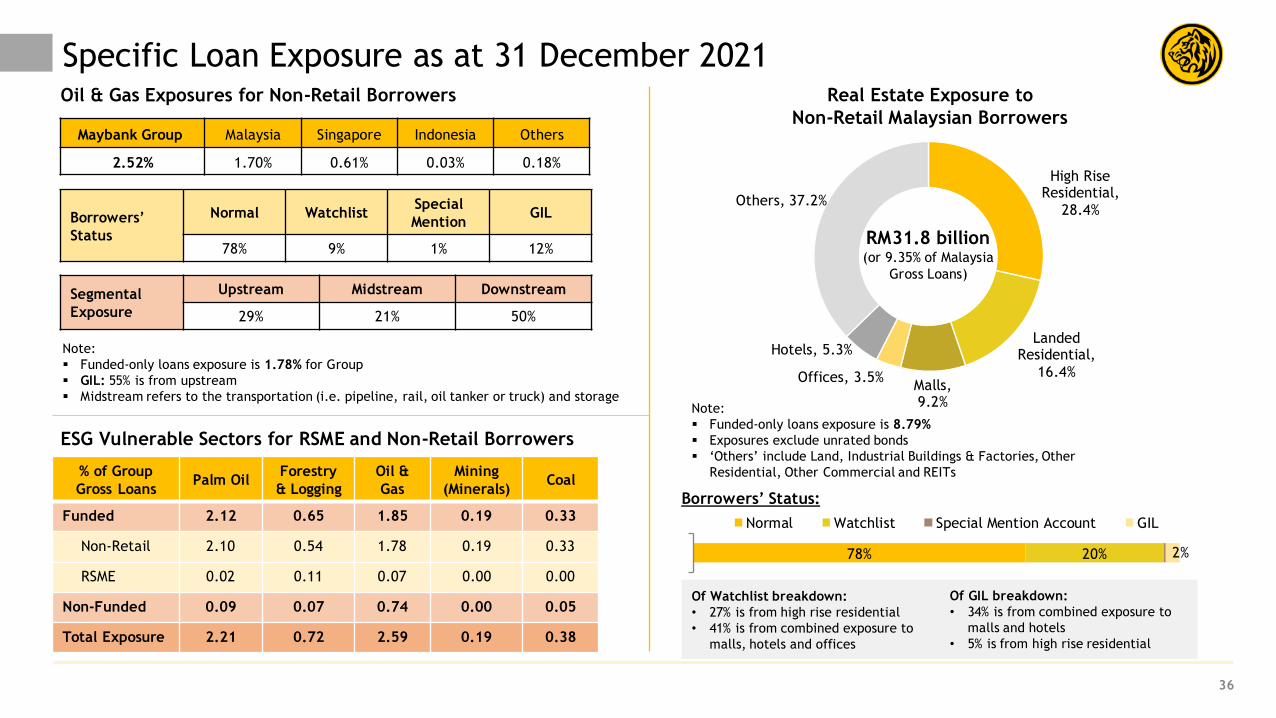

36

% of Group

Gross LoansPalm Oil

Forestry

& Logging

Oil &

Gas

Mining

(Minerals)Coal

Funded 2.12 0.65 1.85 0.19 0.33

Non-Retail 2.10 0.54 1.78 0.19 0.33

RSME 0.02 0.11 0.07 0.00 0.00

Non-Funded 0.09 0.07 0.74 0.00 0.05

Total Exposure 2.21 0.72 2.59 0.19 0.38

Maybank Group Malaysia Singapore Indonesia Others

2.52% 1.70% 0.61% 0.03% 0.18%

Note:

Funded-only loans exposure is 1.78% for Group

GIL: 55% is from upstream

Midstream refers to the transportation (i.e. pipeline, rail, oil tanker or truck) and storage

Borrowers’

Status

Normal WatchlistSpecial

MentionGIL

78% 9% 1% 12%

Segmental

Exposure

Upstream Midstream Downstream

29% 21% 50%

Real Estate Exposure to

Non-Retail Malaysian Borrowers

Note:

Funded-only loans exposure is 8.79%

Exposures exclude unrated bonds

‘Others’ include Land, Industrial Buildings & Factories, Other

Residential, Other Commercial and REITs

78% 20% 2%

Normal Watchlist Special Mention Account GIL

Borrowers’ Status:

Of GIL breakdown:

• 34% is from combined exposure to

malls and hotels

• 5% is from high rise residential

Of Watchlist breakdown:

• 27% is from high rise residential

• 41% is from combined exposure to

malls, hotels and offices

High Rise Residential,

28.4%

Landed Residential,

16.4%Malls, 9.2%

Offices, 3.5%

Hotels, 5.3%

Others, 37.2%

Oil & Gas Exposures for Non-Retail Borrowers

ESG Vulnerable Sectors for RSME and Non-Retail Borrowers

RM31.8 billion(or 9.35% of Malaysia

Gross Loans)

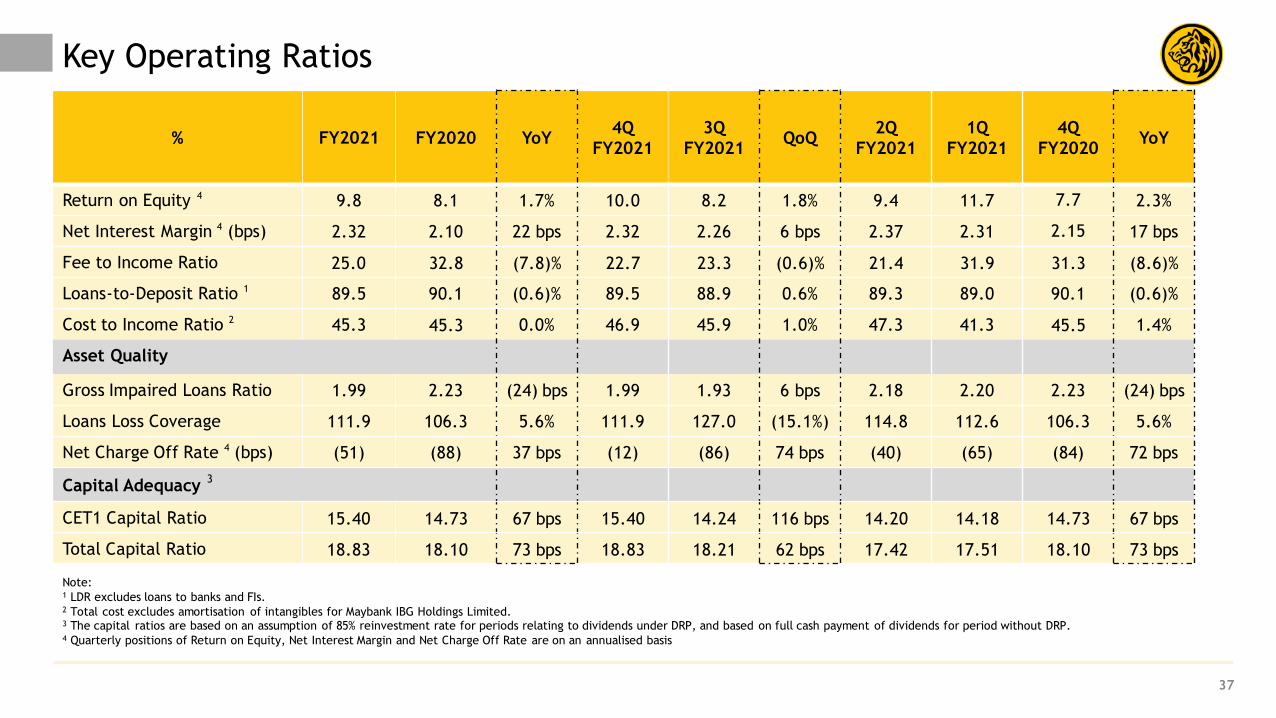

Key Operating Ratios

37

% FY2021 FY2020 YoY4Q

FY2021

3Q

FY2021QoQ

2Q

FY2021

1Q

FY2021

4Q

FY2020YoY

Return on Equity 4 9.8 8.1 1.7% 10.0 8.2 1.8% 9.4 11.7 7.7 2.3%

Net Interest Margin 4 (bps) 2.32 2.10 22 bps 2.32 2.26 6 bps 2.37 2.31 2.15 17 bps

Fee to Income Ratio 25.0 32.8 (7.8)% 22.7 23.3 (0.6)% 21.4 31.9 31.3 (8.6)%

Loans-to-Deposit Ratio 1 89.5 90.1 (0.6)% 89.5 88.9 0.6% 89.3 89.0 90.1 (0.6)%

Cost to Income Ratio 2 45.3 45.3 0.0% 46.9 45.9 1.0% 47.3 41.3 45.5 1.4%

Asset Quality

Gross Impaired Loans Ratio 1.99 2.23 (24) bps 1.99 1.93 6 bps 2.18 2.20 2.23 (24) bps

Loans Loss Coverage 111.9 106.3 5.6% 111.9 127.0 (15.1%) 114.8 112.6 106.3 5.6%

Net Charge Off Rate 4 (bps) (51) (88) 37 bps (12) (86) 74 bps (40) (65) (84) 72 bps

Capital Adequacy 3

CET1 Capital Ratio 15.40 14.73 67 bps 15.40 14.24 116 bps 14.20 14.18 14.73 67 bps

Total Capital Ratio 18.83 18.10 73 bps 18.83 18.21 62 bps 17.42 17.51 18.10 73 bps

Note:1 LDR excludes loans to banks and FIs.2 Total cost excludes amortisation of intangibles for Maybank IBG Holdings Limited.3 The capital ratios are based on an assumption of 85% reinvestment rate for periods relating to dividends under DRP, and based on full cash payment of dividends for period without DRP.4 Quarterly positions of Return on Equity, Net Interest Margin and Net Charge Off Rate are on an annualised basis

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

Table of Contents

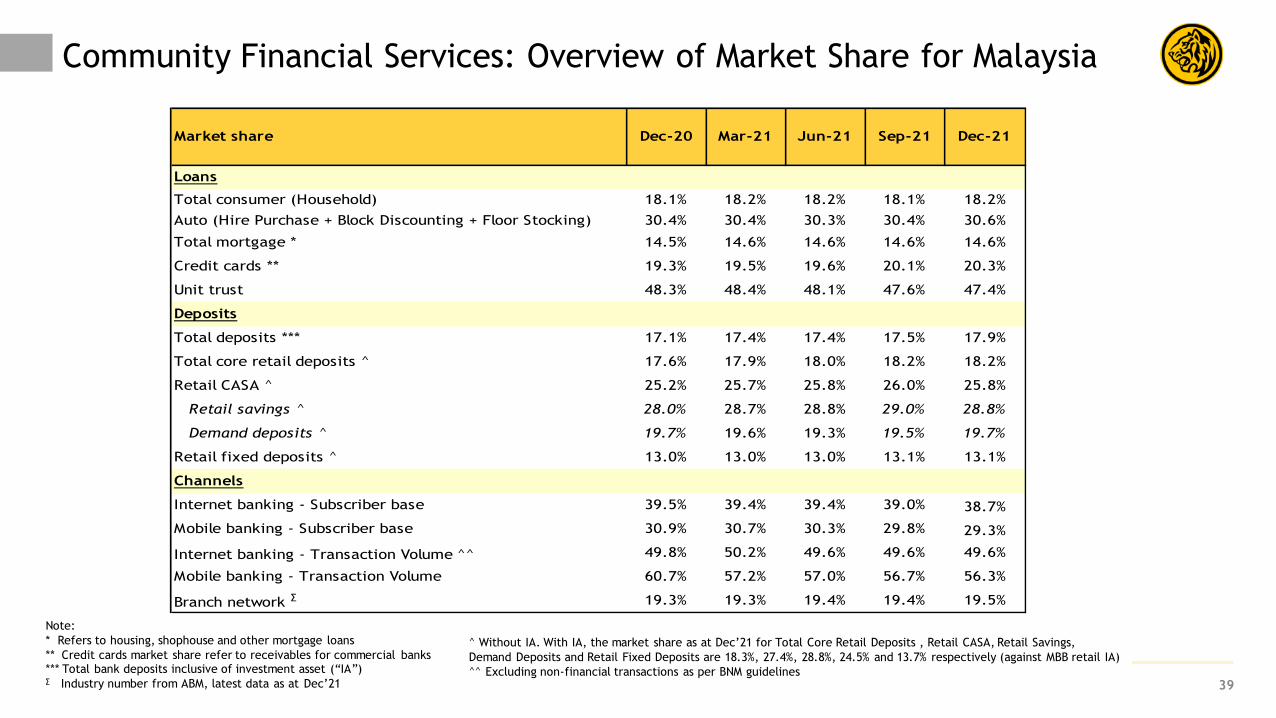

39

Community Financial Services: Overview of Market Share for Malaysia

Note:

* Refers to housing, shophouse and other mortgage loans

** Credit cards market share refer to receivables for commercial banks*** Total bank deposits inclusive of investment asset (“IA”)∑ Industry number from ABM, latest data as at Dec’21

Loans

Total consumer (Household) 18.1% 18.2% 18.2% 18.1% 18.2%

Auto (Hire Purchase + Block Discounting + Floor Stocking) 30.4% 30.4% 30.3% 30.4% 30.6%

Total mortgage * 14.5% 14.6% 14.6% 14.6% 14.6%

Credit cards ** 19.3% 19.5% 19.6% 20.1% 20.3%

Unit trust 48.3% 48.4% 48.1% 47.6% 47.4%

Deposits

Total deposits *** 17.1% 17.4% 17.4% 17.5% 17.9%

Total core retail deposits ^ 17.6% 17.9% 18.0% 18.2% 18.2%

Retail CASA ^ 25.2% 25.7% 25.8% 26.0% 25.8%

Retail savings ^ 28.0% 28.7% 28.8% 29.0% 28.8%

Demand deposits ^ 19.7% 19.6% 19.3% 19.5% 19.7%

Retail fixed deposits ^ 13.0% 13.0% 13.0% 13.1% 13.1%

Channels

Internet banking - Subscriber base 39.5% 39.4% 39.4% 39.0% 38.7%

Mobile banking - Subscriber base 30.9% 30.7% 30.3% 29.8% 29.3%

Internet banking - Transaction Volume ^^ 49.8% 50.2% 49.6% 49.6% 49.6%

Mobile banking - Transaction Volume 60.7% 57.2% 57.0% 56.7% 56.3%

Branch network ∑ 19.3% 19.3% 19.4% 19.4% 19.5%

Dec-20Market share Dec-21Sep-21Jun-21Mar-21

^ Without IA. With IA, the market share as at Dec’21 for Total Core Retail Deposits , Retail CASA, Retail Savings,

Demand Deposits and Retail Fixed Deposits are 18.3%, 27.4%, 28.8%, 24.5% and 13.7% respectively (against MBB retail IA)

^^ Excluding non-financial transactions as per BNM guidelines

3.10 3.55

1.101.26

FY2020 FY2021

Fund Fee

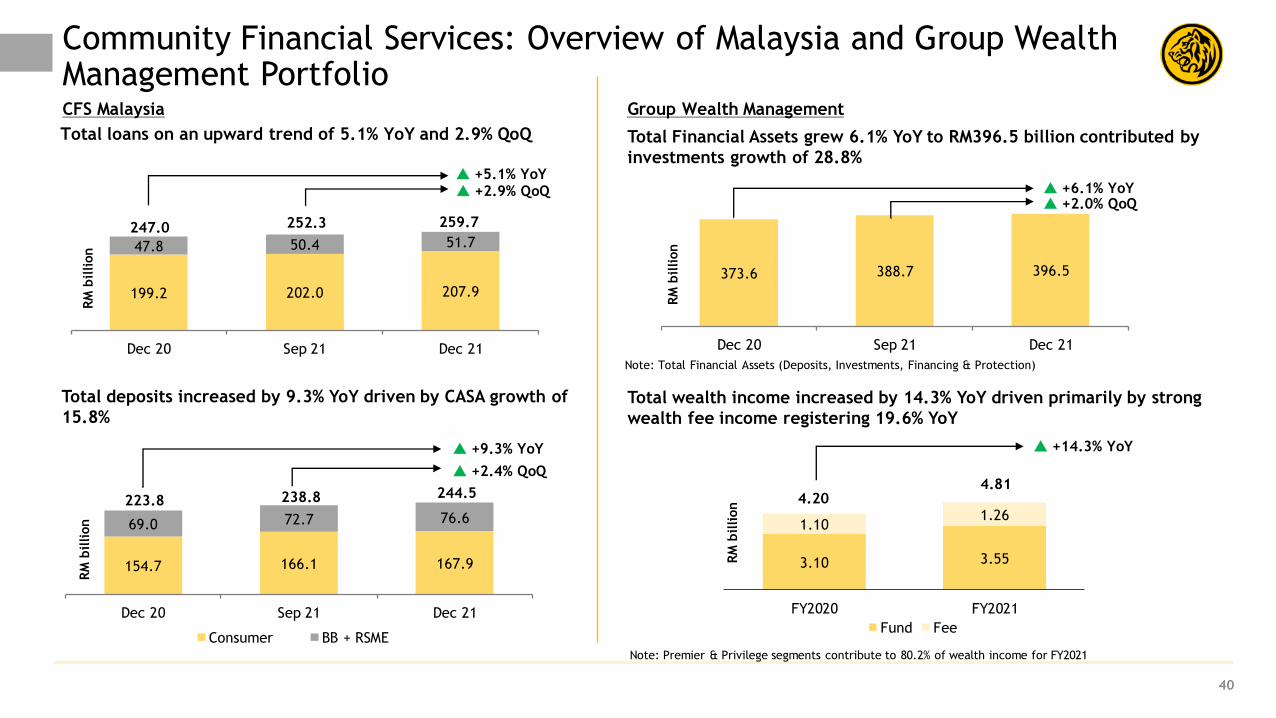

Community Financial Services: Overview of Malaysia and Group Wealth Management Portfolio

40

154.7 166.1 167.9

69.0 72.7 76.6

Dec 20 Sep 21 Dec 21

Consumer BB + RSME

223.8 238.8

Total loans on an upward trend of 5.1% YoY and 2.9% QoQ

+2.4% QoQ

Total deposits increased by 9.3% YoY driven by CASA growth of

15.8%

+9.3% YoY

199.2 202.0 207.9

47.8 50.4 51.7

Dec 20 Sep 21 Dec 21

259.7

+2.9% QoQ +5.1% YoY

247.0 252.3

244.5

RM

billion

RM

billion

Total Financial Assets grew 6.1% YoY to RM396.5 billion contributed by

investments growth of 28.8%

CFS Malaysia Group Wealth Management

Total wealth income increased by 14.3% YoY driven primarily by strong

wealth fee income registering 19.6% YoY

+14.3% YoY

RM

billion

4.204.81

Note: Premier & Privilege segments contribute to 80.2% of wealth income for FY2021

Note: Total Financial Assets (Deposits, Investments, Financing & Protection)

373.6 388.7 396.5

Dec 20 Sep 21 Dec 21

+6.1% YoY

RM

billion

+2.0% QoQ

Table of Contents

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

9.9

21.2

48.4

11.2

19.5

48.2

11.6

20.4

48.3

Dec 21 Sep 21 Dec 20

65.2 60.7 60.1 65.7 65.8

54.0 62.1 53.659.2 58.8

60.6 60.161.3

63.8 65.6

28.0 26.625.2

23.6 24.07.4 8.0

8.89.7 9.7

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

Govt. Securities - Domestic

Govt. Securities - Foreign

PDS/Corp Bonds - Domestic

PDS/Corp Bonds - Foreign

Others

222.0

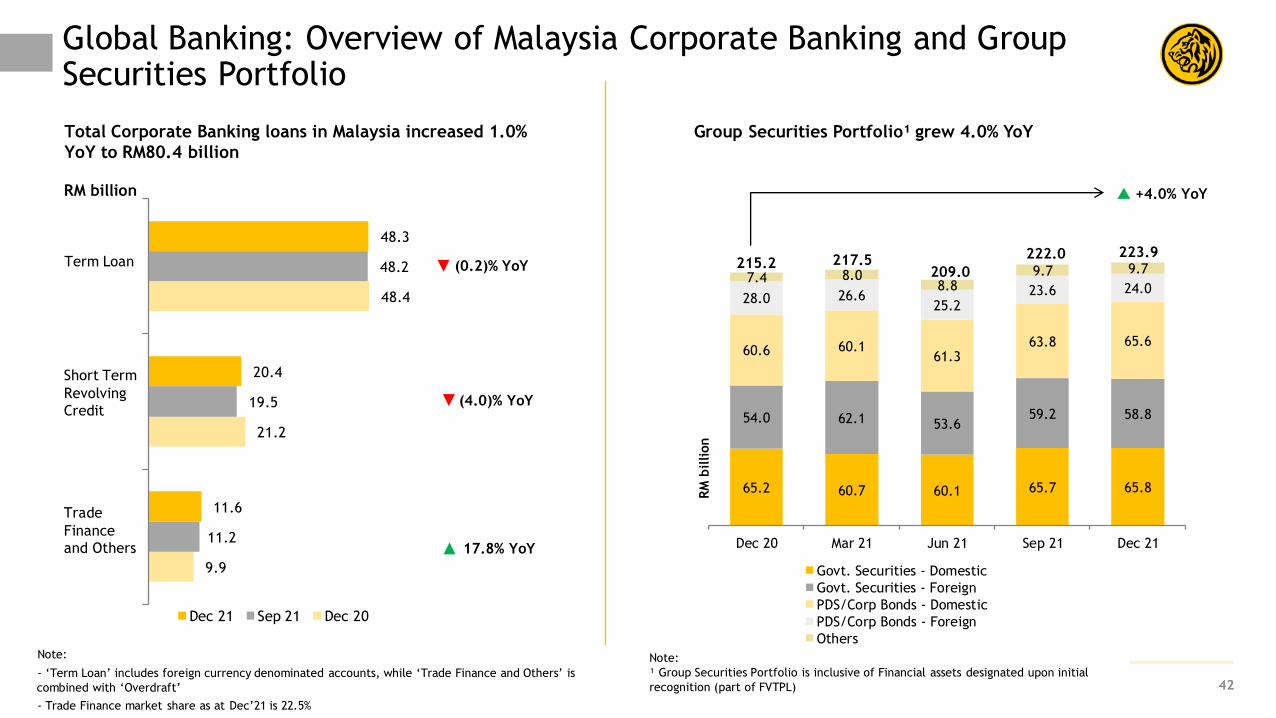

Global Banking: Overview of Malaysia Corporate Banking and Group Securities Portfolio

42

Note:

- ‘Term Loan’ includes foreign currency denominated accounts, while ‘Trade Finance and Others’ is

combined with ‘Overdraft’

- Trade Finance market share as at Dec’21 is 22.5%

Total Corporate Banking loans in Malaysia increased 1.0%

YoY to RM80.4 billion

RM billion

Term Loan

Short Term

Revolving

Credit

Trade

Finance

and Others 17.8% YoY

Group Securities Portfolio¹ grew 4.0% YoY

Note:

¹ Group Securities Portfolio is inclusive of Financial assets designated upon initial

recognition (part of FVTPL)

+4.0% YoY

215.2 217.5209.0

RM

billion

(4.0)% YoY

(0.2)% YoY223.9

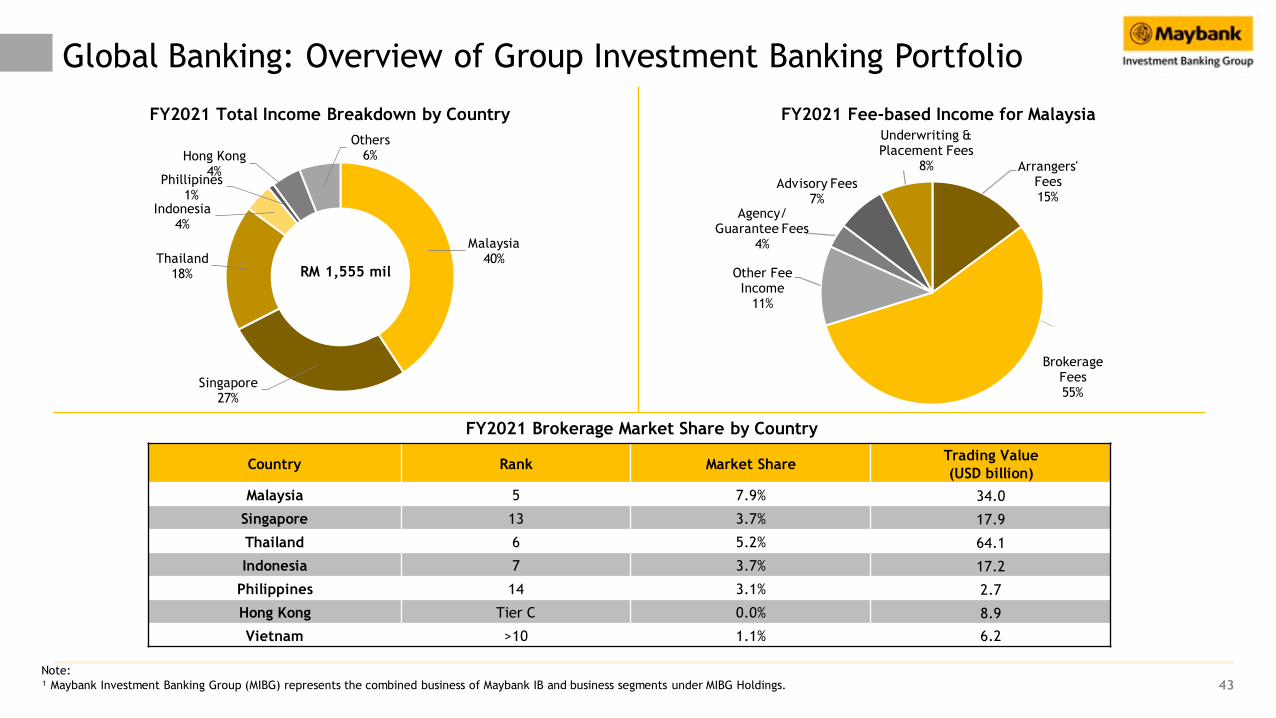

Global Banking: Overview of Group Investment Banking Portfolio

43

FY2021 Fee-based Income for MalaysiaFY2021 Total Income Breakdown by Country

Note:

¹ Maybank Investment Banking Group (MIBG) represents the combined business of Maybank IB and business segments under MIBG Holdings.

Country Rank Market ShareTrading Value

(USD billion)

Malaysia 5 7.9% 34.0

Singapore 13 3.7% 17.9

Thailand 6 5.2% 64.1

Indonesia 7 3.7% 17.2

Philippines 14 3.1% 2.7

Hong Kong Tier C 0.0% 8.9

Vietnam >10 1.1% 6.2

FY2021 Brokerage Market Share by Country

Arrangers' Fees15%

Brokerage Fees55%

Other Fee Income

11%

Agency/ Guarantee Fees

4%

Advisory Fees7%

Underwriting &Placement Fees

8%

Malaysia40%

Singapore27%

Thailand18%

Indonesia4%

Phillipines1%

Hong Kong4%

Others6%

RM 1,555 mil

Table of Contents

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

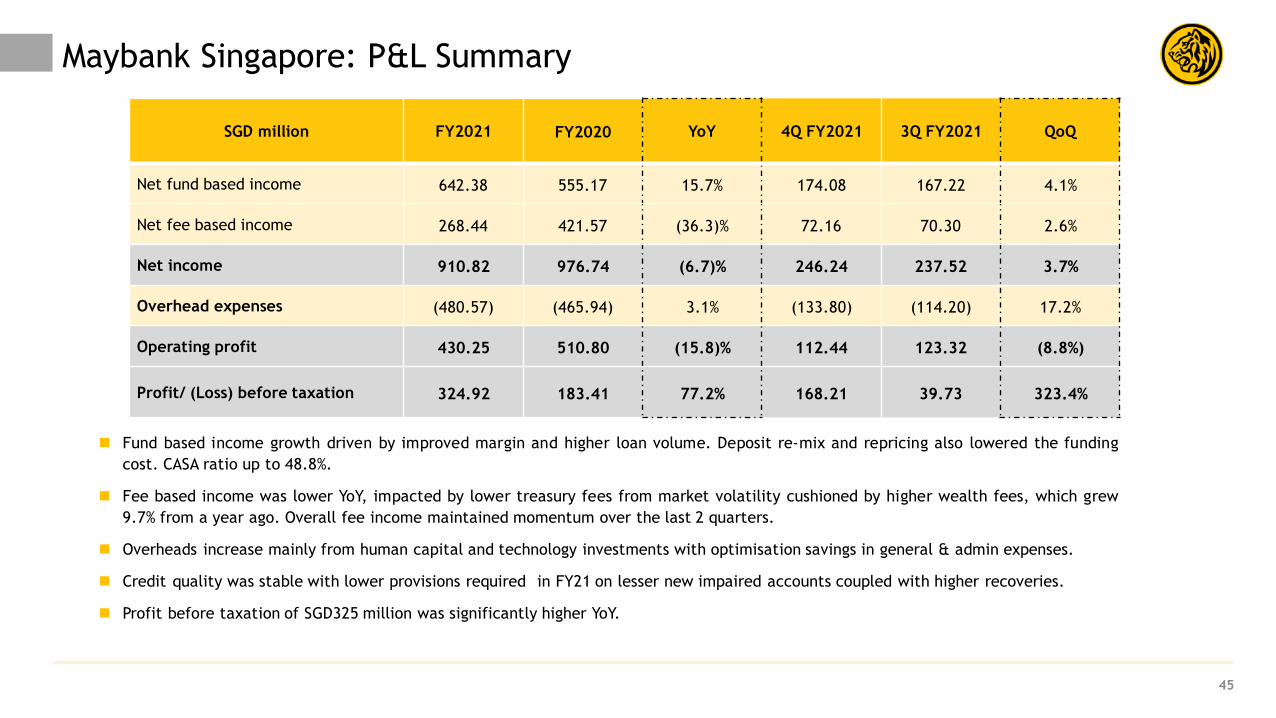

Maybank Singapore: P&L Summary

Fund based income growth driven by improved margin and higher loan volume. Deposit re-mix and repricing also lowered the funding

cost. CASA ratio up to 48.8%.

Fee based income was lower YoY, impacted by lower treasury fees from market volatility cushioned by higher wealth fees, which grew

9.7% from a year ago. Overall fee income maintained momentum over the last 2 quarters.

Overheads increase mainly from human capital and technology investments with optimisation savings in general & admin expenses.

Credit quality was stable with lower provisions required in FY21 on lesser new impaired accounts coupled with higher recoveries.

Profit before taxation of SGD325 million was significantly higher YoY.

SGD million FY2021 FY2020 YoY 4Q FY2021 3Q FY2021 QoQ

Net fund based income 642.38 555.17 15.7% 174.08 167.22 4.1%

Net fee based income 268.44 421.57 (36.3)% 72.16 70.30 2.6%

Net income 910.82 976.74 (6.7)% 246.24 237.52 3.7%

Overhead expenses (480.57) (465.94) 3.1% (133.80) (114.20) 17.2%

Operating profit 430.25 510.80 (15.8)% 112.44 123.32 (8.8%)

Profit/ (Loss) before taxation 324.92 183.41 77.2% 168.21 39.73 323.4%

45

8.6 9.3 9.2

10.713.3 14.2

32.3 26.8 24.6

Dec 20 Sep 21 Dec 21

Time Deposits

Demand Deposits

Savings

37.5%45.7%

46

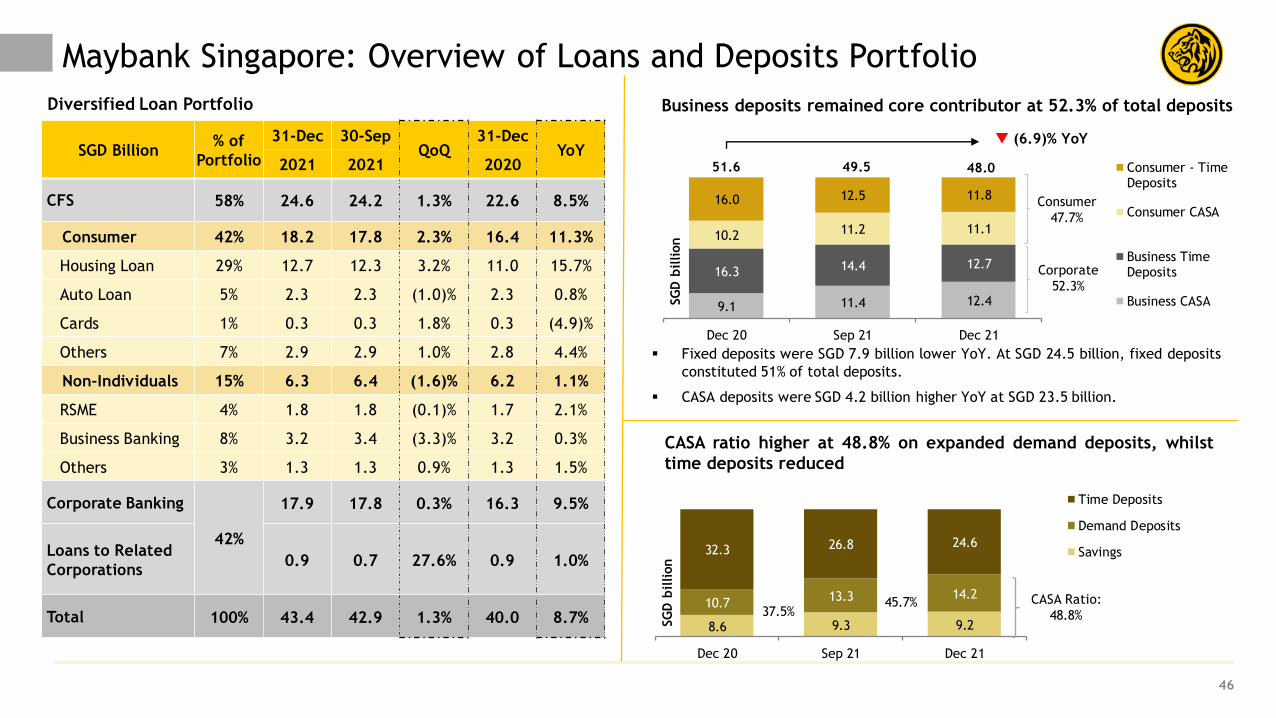

Maybank Singapore: Overview of Loans and Deposits Portfolio

9.1 11.4 12.4

16.3 14.4 12.7

10.2 11.2 11.1

16.0 12.5 11.8

Dec 20 Sep 21 Dec 21

Consumer - TimeDeposits

Consumer CASA

Business TimeDeposits

Business CASA

48.049.5

Diversified Loan Portfolio

Consumer

47.7%

Corporate

52.3%

Business deposits remained core contributor at 52.3% of total deposits

CASA Ratio:

48.8%

SG

D b

illion

CASA ratio higher at 48.8% on expanded demand deposits, whilst

time deposits reduced

Fixed deposits were SGD 7.9 billion lower YoY. At SGD 24.5 billion, fixed deposits

constituted 51% of total deposits.

CASA deposits were SGD 4.2 billion higher YoY at SGD 23.5 billion.

51.6

(6.9)% YoY

SG

D b

illion

SGD Billion% of

Portfolio

31-Dec 30-SepQoQ

31-DecYoY

2021 2021 2020

CFS 58% 24.6 24.2 1.3% 22.6 8.5%

Consumer 42% 18.2 17.8 2.3% 16.4 11.3%

Housing Loan 29% 12.7 12.3 3.2% 11.0 15.7%

Auto Loan 5% 2.3 2.3 (1.0)% 2.3 0.8%

Cards 1% 0.3 0.3 1.8% 0.3 (4.9)%

Others 7% 2.9 2.9 1.0% 2.8 4.4%

Non-Individuals 15% 6.3 6.4 (1.6)% 6.2 1.1%

RSME 4% 1.8 1.8 (0.1)% 1.7 2.1%

Business Banking 8% 3.2 3.4 (3.3)% 3.2 0.3%

Others 3% 1.3 1.3 0.9% 1.3 1.5%

Corporate Banking

42%

17.9 17.8 0.3% 16.3 9.5%

Loans to Related

Corporations0.9 0.7 27.6% 0.9 1.0%

Total 100% 43.4 42.9 1.3% 40.0 8.7%

Table of Contents

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

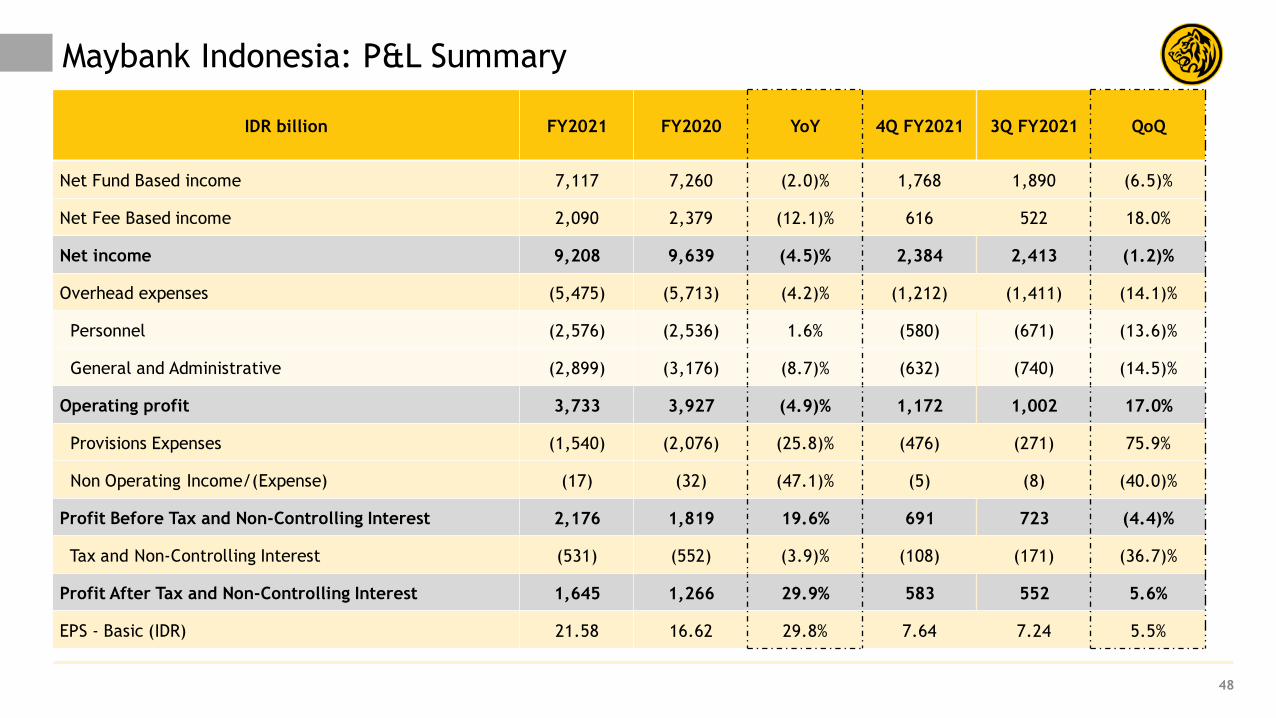

Maybank Indonesia: P&L Summary

48

IDR billion FY2021 FY2020 YoY 4Q FY2021 3Q FY2021 QoQ

Net Fund Based income 7,117 7,260 (2.0)% 1,768 1,890 (6.5)%

Net Fee Based income 2,090 2,379 (12.1)% 616 522 18.0%

Net income 9,208 9,639 (4.5)% 2,384 2,413 (1.2)%

Overhead expenses (5,475) (5,713) (4.2)% (1,212) (1,411) (14.1)%

Personnel (2,576) (2,536) 1.6% (580) (671) (13.6)%

General and Administrative (2,899) (3,176) (8.7)% (632) (740) (14.5)%

Operating profit 3,733 3,927 (4.9)% 1,172 1,002 17.0%

Provisions Expenses (1,540) (2,076) (25.8)% (476) (271) 75.9%

Non Operating Income/(Expense) (17) (32) (47.1)% (5) (8) (40.0)%

Profit Before Tax and Non-Controlling Interest 2,176 1,819 19.6% 691 723 (4.4)%

Tax and Non-Controlling Interest (531) (552) (3.9)% (108) (171) (36.7)%

Profit After Tax and Non-Controlling Interest 1,645 1,266 29.9% 583 552 5.6%

EPS - Basic (IDR) 21.58 16.62 29.8% 7.64 7.24 5.5%

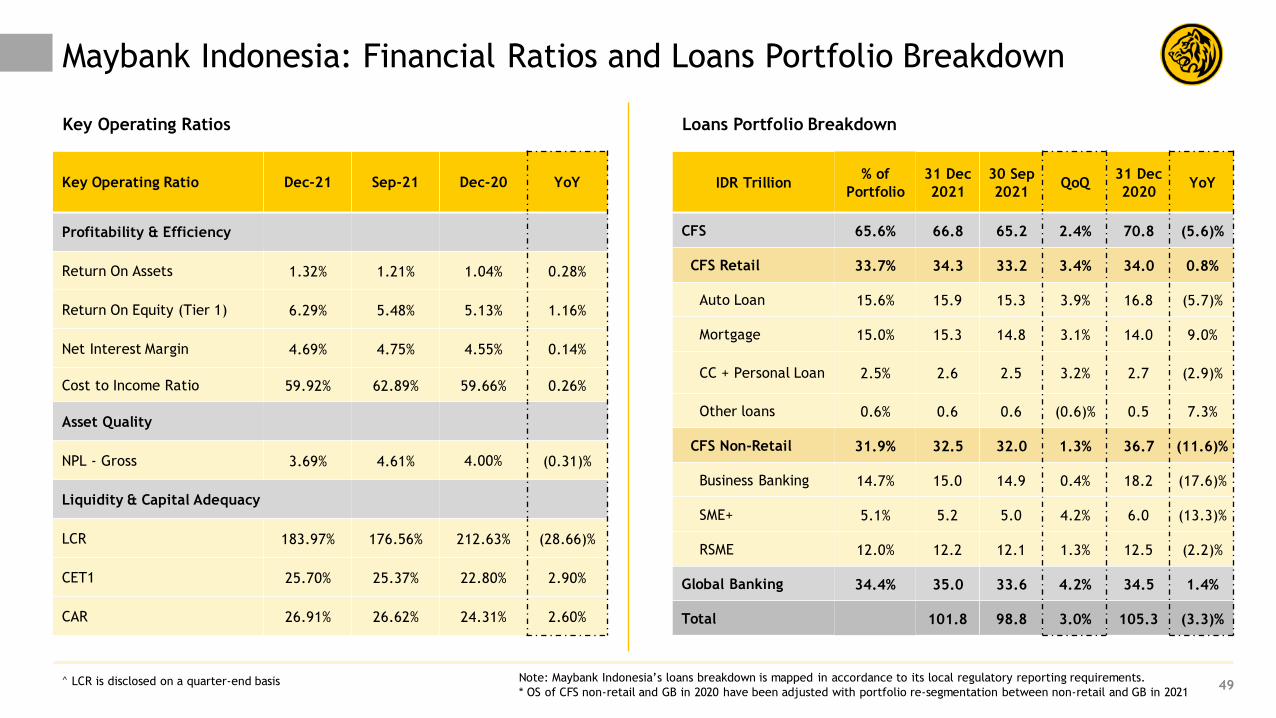

Maybank Indonesia: Financial Ratios and Loans Portfolio Breakdown

49

Key Operating Ratios Loans Portfolio Breakdown

Key Operating Ratio Dec-21 Sep-21 Dec-20 YoY

Profitability & Efficiency

Return On Assets 1.32% 1.21% 1.04% 0.28%

Return On Equity (Tier 1) 6.29% 5.48% 5.13% 1.16%

Net Interest Margin 4.69% 4.75% 4.55% 0.14%

Cost to Income Ratio 59.92% 62.89% 59.66% 0.26%

Asset Quality

NPL - Gross 3.69% 4.61% 4.00% (0.31)%

Liquidity & Capital Adequacy

LCR 183.97% 176.56% 212.63% (28.66)%

CET1 25.70% 25.37% 22.80% 2.90%

CAR 26.91% 26.62% 24.31% 2.60%

IDR Trillion% of

Portfolio

31 Dec

2021

30 Sep

2021QoQ

31 Dec

2020YoY

CFS 65.6% 66.8 65.2 2.4% 70.8 (5.6)%

CFS Retail 33.7% 34.3 33.2 3.4% 34.0 0.8%

Auto Loan 15.6% 15.9 15.3 3.9% 16.8 (5.7)%

Mortgage 15.0% 15.3 14.8 3.1% 14.0 9.0%

CC + Personal Loan 2.5% 2.6 2.5 3.2% 2.7 (2.9)%

Other loans 0.6% 0.6 0.6 (0.6)% 0.5 7.3%

CFS Non-Retail 31.9% 32.5 32.0 1.3% 36.7 (11.6)%

Business Banking 14.7% 15.0 14.9 0.4% 18.2 (17.6)%

SME+ 5.1% 5.2 5.0 4.2% 6.0 (13.3)%

RSME 12.0% 12.2 12.1 1.3% 12.5 (2.2)%

Global Banking 34.4% 35.0 33.6 4.2% 34.5 1.4%

Total 101.8 98.8 3.0% 105.3 (3.3)%

Note: Maybank Indonesia’s loans breakdown is mapped in accordance to its local regulatory reporting requirements.

* OS of CFS non-retail and GB in 2020 have been adjusted with portfolio re-segmentation between non-retail and GB in 2021^ LCR is disclosed on a quarter-end basis

Table of Contents

Executive Summary 2-8

4Q & Full Year FY2021 Financial Performance 10-20

Prospects & Outlook 22-24

Appendix:

1. Financial Performance 26-37

2. Community Financial Services 39-40

3. Global Banking 42-43

4. Maybank Singapore 45-46

5. Maybank Indonesia 48-49

6. Other Segments 51-53

Maybank Islamic, 64.9%

Maybank Conventional,

Malaysia, 35.1%

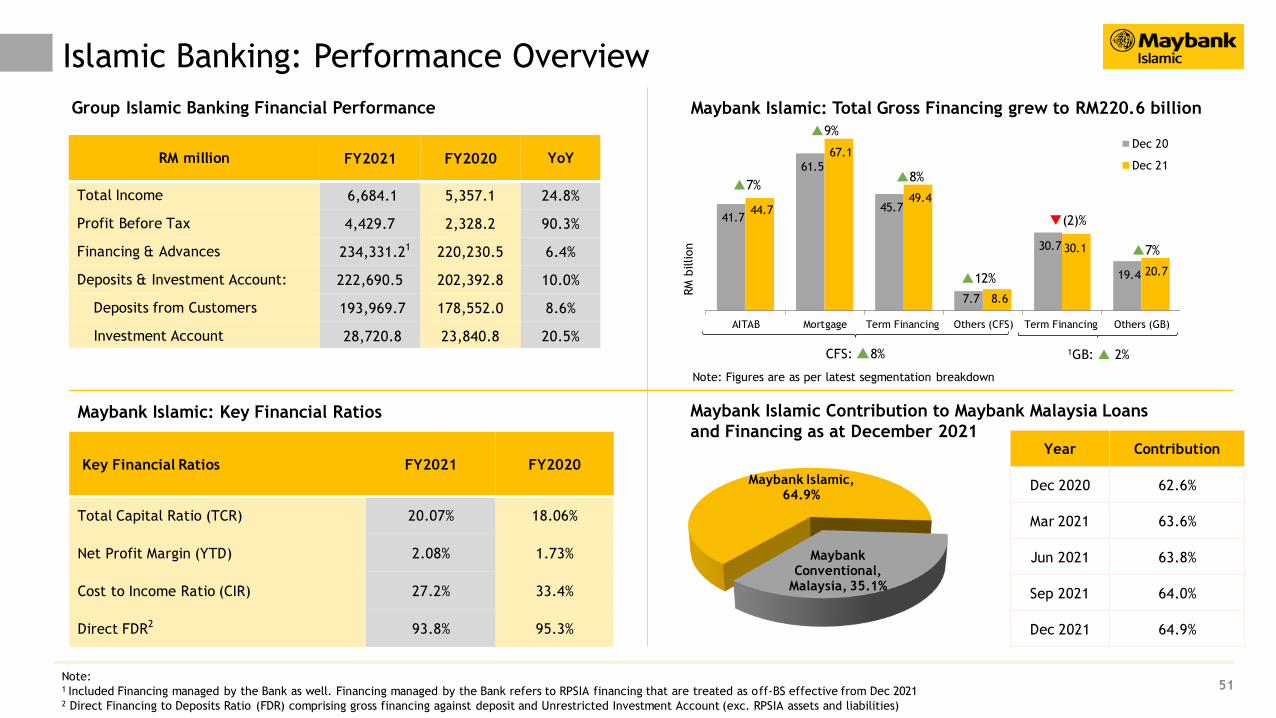

RM million FY2021 FY2020 YoY

Total Income 6,684.1 5,357.1 24.8%

Profit Before Tax 4,429.7 2,328.2 90.3%

Financing & Advances 234,331.21 220,230.5 6.4%

Deposits & Investment Account: 222,690.5 202,392.8 10.0%

Deposits from Customers 193,969.7 178,552.0 8.6%

Investment Account 28,720.8 23,840.8 20.5%

Islamic Banking: Performance Overview

51

Group Islamic Banking Financial Performance

Maybank Islamic: Key Financial Ratios

Key Financial Ratios FY2021 FY2020

Total Capital Ratio (TCR) 20.07% 18.06%

Net Profit Margin (YTD) 2.08% 1.73%

Cost to Income Ratio (CIR) 27.2% 33.4%

Direct FDR2 93.8% 95.3%

Note:1 Included Financing managed by the Bank as well. Financing managed by the Bank refers to RPSIA financing that are treated as off-BS effective from Dec 20212 Direct Financing to Deposits Ratio (FDR) comprising gross financing against deposit and Unrestricted Investment Account (exc. RPSIA assets and liabilities)

Maybank Islamic: Total Gross Financing grew to RM220.6 billion

Note: Figures are as per latest segmentation breakdown

Year Contribution

Dec 2020 62.6%

Mar 2021 63.6%

Jun 2021 63.8%

Sep 2021 64.0%

Dec 2021 64.9%

Maybank Islamic Contribution to Maybank Malaysia Loans

and Financing as at December 2021

41.7

61.5

45.7

7.7

30.7

19.4

44.7

67.1

49.4

8.6

30.1

20.7

AITAB Mortgage Term Financing Others (CFS) Term Financing Others (GB)

Dec 20

Dec 218%

7%

RM

billion

(2)%

CFS: 8% 1GB: 2%

12%

9%

7%

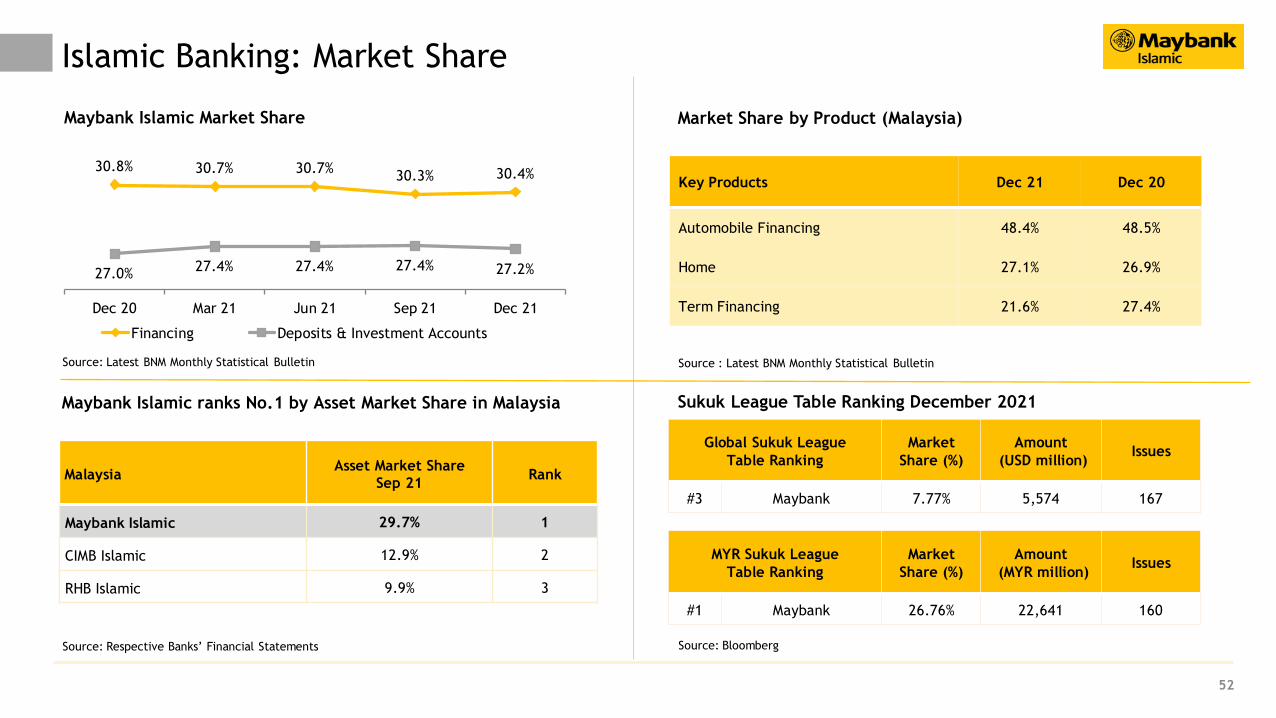

Islamic Banking: Market Share

52

Key Products Dec 21 Dec 20

Automobile Financing 48.4% 48.5%

Home 27.1% 26.9%

Term Financing 21.6% 27.4%

Maybank Islamic ranks No.1 by Asset Market Share in Malaysia

Market Share by Product (Malaysia) Maybank Islamic Market Share

30.8% 30.7% 30.7%30.3% 30.4%

27.0%27.4% 27.4% 27.4% 27.2%

Dec 20 Mar 21 Jun 21 Sep 21 Dec 21

Financing Deposits & Investment Accounts

MalaysiaAsset Market Share

Sep 21Rank

Maybank Islamic 29.7% 1

CIMB Islamic 12.9% 2

RHB Islamic 9.9% 3

Source: Latest BNM Monthly Statistical Bulletin

Sukuk League Table Ranking December 2021

Source : Latest BNM Monthly Statistical Bulletin

Source: BloombergSource: Respective Banks’ Financial Statements

Global Sukuk League

Table Ranking

Market

Share (%)

Amount

(USD million)Issues

#3 Maybank 7.77% 5,574 167

MYR Sukuk League

Table Ranking

Market

Share (%)

Amount

(MYR million)Issues

#1 Maybank 26.76% 22,641 160

Profit Before Tax

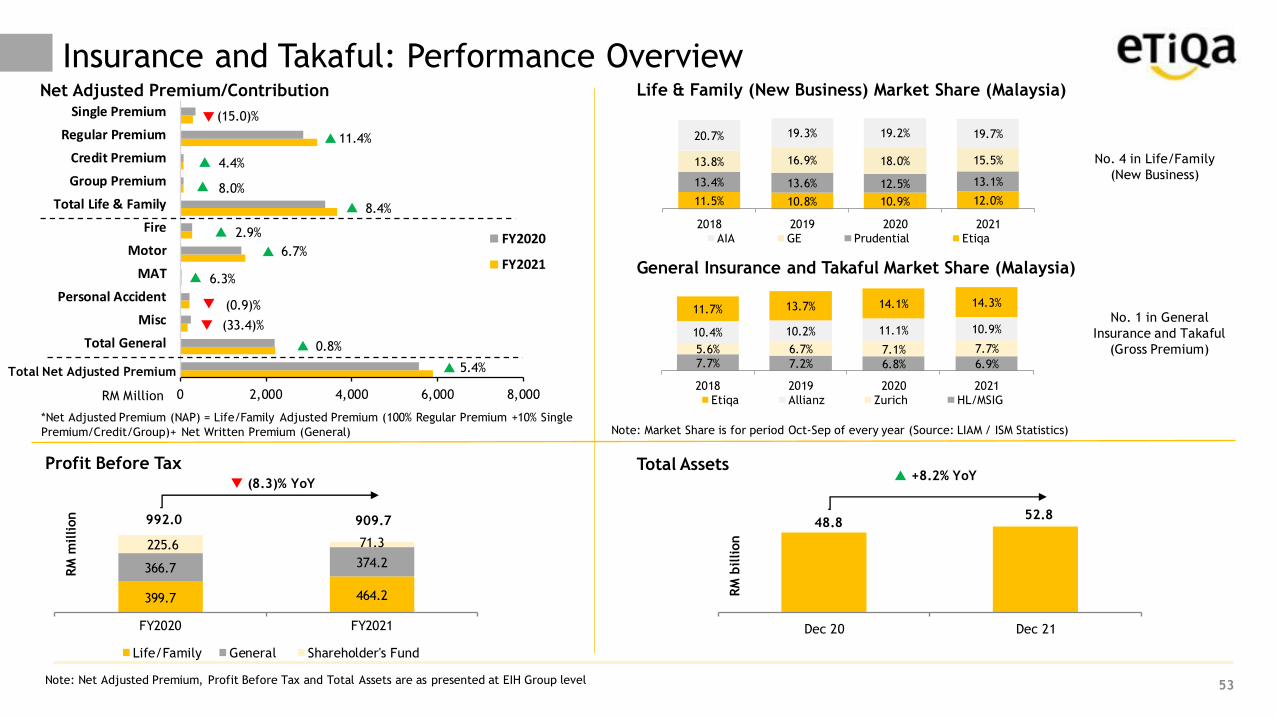

Insurance and Takaful: Performance Overview

53

Total Assets

Net Adjusted Premium/Contribution Life & Family (New Business) Market Share (Malaysia)

No. 1 in General

Insurance and Takaful

(Gross Premium)

General Insurance and Takaful Market Share (Malaysia)

Note: Market Share is for period Oct-Sep of every year (Source: LIAM / ISM Statistics)

No. 4 in Life/Family

(New Business)

*Net Adjusted Premium (NAP) = Life/Family Adjusted Premium (100% Regular Premium +10% Single

Premium/Credit/Group)+ Net Written Premium (General)

Note: Net Adjusted Premium, Profit Before Tax and Total Assets are as presented at EIH Group level

399.7 464.2

366.7 374.2

225.6 71.3

FY2020 FY2021

Life/Family General Shareholder's Fund

(8.3)% YoY

992.0 909.7

RM

million

48.8 52.8

Dec 20 Dec 21

+8.2% YoY

RM

billion

0 2,000 4,000 6,000 8,000

Total General

Misc

Personal Accident

MAT

Motor

Fire

Total Life & Family

Group Premium

Credit Premium

Regular Premium

Single Premium

RM Million

FY2020

FY2021

(15.0)%

11.4%

4.4%

8.0%

8.4%

2.9%

6.7%

(0.9)%

6.3%

(33.4)%

0.8%

5.4%

Total Net Adjusted Premium7.7% 7.2% 6.8% 6.9%

5.6% 6.7% 7.1% 7.7%

10.4% 10.2% 11.1% 10.9%

11.7% 13.7% 14.1% 14.3%

2018 2019 2020 2021

Etiqa Allianz Zurich HL/MSIG

11.5% 10.8% 10.9% 12.0%

13.4% 13.6% 12.5% 13.1%

13.8% 16.9% 18.0% 15.5%

20.7% 19.3% 19.2% 19.7%

2018 2019 2020 2021

AIA GE Prudential Etiqa

Humanising Financial Services

MALAYAN BANKING BERHAD14th Floor, Menara Maybank100, Jalan Tun Perak50050 Kuala Lumpur, MalaysiaTel : (6)03-2070 8833

www.maybank.com

Disclaimer. This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the information that

may be required to evaluate the Company or its financial position. No representation or warranty, express or implied, is given by or on behalf of the Company as to the accuracy or

completeness of the information or opinions contained in this presentation.

The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of it form the basis

of, or be relied in any connection with, any contract, investment decision or commitment whatsoever.

The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in connection therewith.

Related Documents