1 Corporate Presentation PT GARUDA INDONESIA (PERSERO) Tbk. Maybank Insight Gathering 19th January 2016 Sentral Senayan 3, 28th Floor Jakarta

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Corporate Presentation PT GARUDA INDONESIA (PERSERO) Tbk.

Maybank Insight Gathering19th January 2016

Sentral Senayan 3, 28th Floor Jakarta

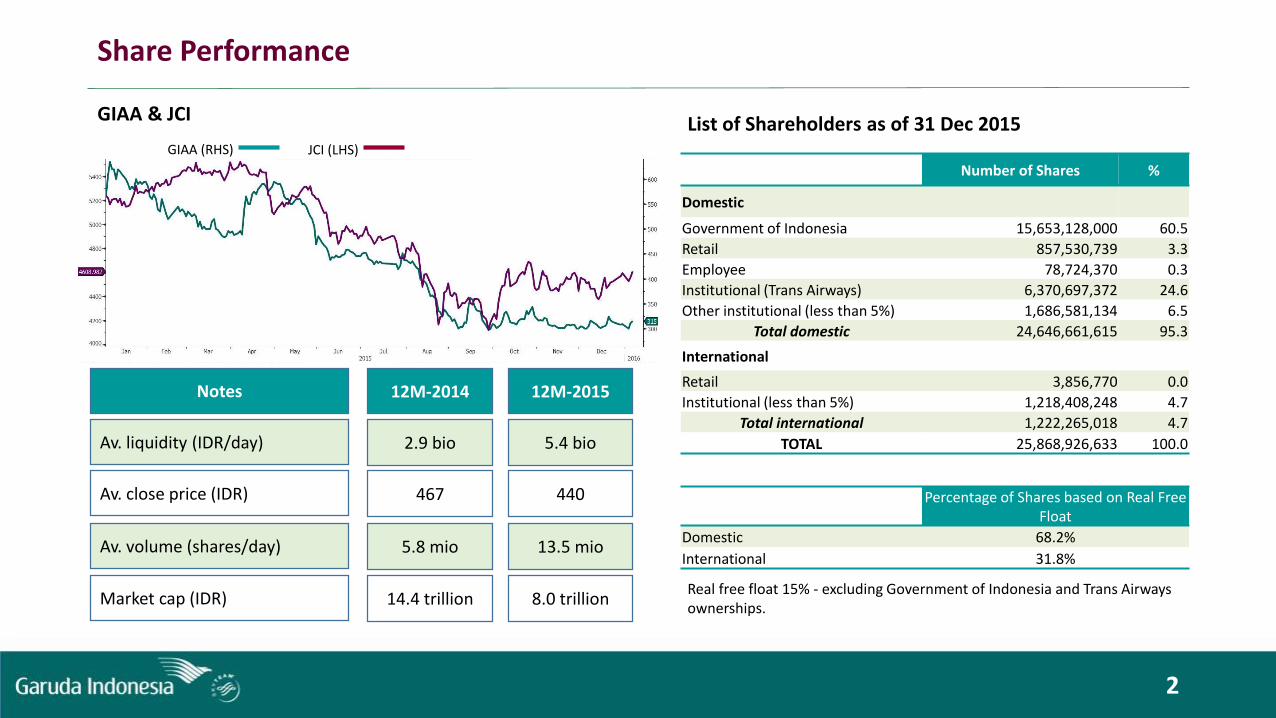

List of Shareholders as of 31 Dec 2015GIAA & JCI

Notes

Av. liquidity (IDR/day)

12M-2014

2.9 bio

12M-2015

5.4 bio

Av. close price (IDR) 467 440

Av. volume (shares/day) 5.8 mio 13.5 mio

Market cap (IDR) 14.4 trillion 8.0 trillionReal free float 15% - excluding Government of Indonesia and Trans Airways ownerships.

Share Performance

GIAA (RHS) JCI (LHS)

2

Number of Shares %

Domestic

Government of Indonesia 15,653,128,000 60.5

Retail 857,530,739 3.3

Employee 78,724,370 0.3

Institutional (Trans Airways) 6,370,697,372 24.6

Other institutional (less than 5%) 1,686,581,134 6.5

Total domestic 24,646,661,615 95.3

International

Retail 3,856,770 0.0

Institutional (less than 5%) 1,218,408,248 4.7

Total international 1,222,265,018 4.7

TOTAL 25,868,926,633 100.0

Percentage of Shares based on Real Free Float

Domestic 68.2%

International 31.8%

Sustained GDP growth in 2015 and 2016F

Global GDP Growth Forecast

3

Source: Bloomberg

Source: IRU BI Presentation

Air

Rail

Sea

23

150

13

FY 2004

111

278

13

+ 17.2%

+ 6.3%

+ 0.4%

Indonesia: Transportation profile (Passengers in million)

FY 2014 CAGR

Archipelago Country

Air

Rail

Highway

121

1.073

16.289

FY 2004

352

2.357

39.342

+ 12.5%

+ 8.2%

+ 9.2%

China:Transportation profile (Passengers in million)

FY 2014 CAGR

Sea 181 2.75 + 4.3%

Massive Land Country

Strong Economic Fundamental and Demand

7.0% 7.0% 6.9% 6.9% 6.9%6.5%

4.7% 4.7% 4.7% 4.8% 4.7%5.2%

2.9% 2.7%2.1% 2.2%

2.5% 2.5%1.3%

2.3%

3.3%

4.3%

5.3%

6.3%

7.3%

Q1 Q2 Q3 Q4 FY15 FY16

GDP Growth in 2016

CN ID US

5.4%

4.2%3.4% 3.3% 3.4% 3.1% 3.6% 3.8% 3.9% 4.0% 4.0%

3.1%

1.7%1.2% 1.1%

1.8% 2.0% 2.2% 2.2% 2.2% 2.0% 1.9%

7.5%

6.3%

5.2% 5.0%4.6%

4.0%4.5%

4.9% 5.1% 5.2% 5.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2010 2011 2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Global growth Developed countries Developing countries

Population Air Traffic

34.2 (476%)

Numbers are in million 46.3 (156%)

Sources: Data Internal, Bloomberg, IMF, and www.worldbank.org, Full Year 2014

4

7.3

Hongkong

30.3

Malaysia

68.7

Thailand

40.7 (61%)

251.5

Indonesia

111.0 (44%)

30.6 (566%)

Singapore

5.5

Airline Business Penetration

Population

(Population, in Million persons)

2012 2013 2014 2015 2016F

Indonesia 244.5 248.0 251.5 255.1 258.7

Phillippines 95.8 97.5 99.4 101.4 103.5

Vietnam 88.8 89.7 90.6 91.6 92.5

Thailand 68.0 68.3 68.7 68.8 69.0

Myanmar 50.5 51.0 51.4 51.8 52.3

Malaysia 29.5 29.9 30.3 30.8 31.3

Cambodia 14.9 15.1 15.3 15.5 15.8

Singapore 5.3 5.4 5.5 5.5 5.6

Brunei Darussalam 0.4 0.4 0.4 0.4 0.4

5

Business Strategy - Short Time Strategy - Quick Wins 2015

Revenue generator

Optimizingcapital

structure

Cost

efficiency

Revenue generator• Restructuring flights by cutting unprofit routes

(Brisbane, Taipei, and Narita) • Developing new routes to China and Middle East

(especially expanding to Umrah market) through non scheduled and chartered services

• The 4th hangar to be completed in 2015• Improve seat load factor by managing RPK growth

higher compared to ASK growth.

Cost efficiency• Early termination of operating leases• Identified non-fuel cost savings of US$200m for 2015• Simplify fleet

Optimizing capital structure• US$500m bridge facility used to re-profile existing

commercial term loans• Proposed USD Sukuk to refinance bridge loan to extend

maturity profile

6

V I S I O N 2 0 2 0“ T O B E A S U S TA I N A B L E A I R L I N E C O M P A N Y T H R O U G H G R O W T H I N P R O F I T ”

M I S S I O N 2 0 1 6 - 2 0 2 0B E C O M E T H E L E A D I N G A I R L I N E C O M PA N Y W H I C H V A L U E S C U S T O M E R T I M E A N D E X P E R I E N C E

T H R O U G H H U M A N - T O - H U M A N C A R I N G S E R V I C E , C O S T L E A D E R S H I P I N O P E R AT I O N A N D S Y N E R G Y U N D E R O N E G R O U P

SKY BEYONDMAKE EVERY MOMENT COUNTSThe strategy emphasizes on appreciation of customer time.

7

Business Strategy: Long Term Strategy – Sky Beyond 2016 - 2020

Group

synergy

Cost

leadership

Caring

service

Established an IT based airline

Optimize network & alliances

Strengthen medium haul & expand

selected long haul routes

Develope high performance

people

Deliver new airline experience

Build GA Brand as world’s most caring

airline

Indonesian hospitality

Dominate domestic market through GA

and Citilink

Set up holding company

Assumptions - 2016

• USDIDR – 15K/USD

• Fuel Price – USc70/L (Into Plane Price)

• Inflation rate – 4.7%

• Interest rate – 5.5%

• GDP – 5.5%

8

Government Policy And Strategy Amidst The Challenging Environment

Free visa to Indonesia

Tax incentives forassets revaluation

Acceleration of infrastructure development

Supportthe export Minded

Scrap import tax on plane parts

Global ChallengesFiscal stimulus

Special economic zones

9

Awards

• Service: 22 awards• Commercial: 13 awards• Business: 7 awards• Corporate: Transformation: 7 awards• Human Capital: 4 awards• People Management: 5 awards• GCG: 5 Awards• Financial: 2 awards

65 awards 2015:Domestic: 50 awards

International: 15 awards

• SKYTRAX Awards 2015 “The World’s Best Cabin Crew”• SKYTRAX Awards 2015 “World’s Best Airline” 8th Rank• Finance Asia Awards 2015 “Asia’s Best Companies 2015”• Schipol Aviation Awards “Passenger Airline of the Year Award 2014-Intercontinental”• Indonesia Human Capital Award 2015 “1st in Human Resources Technology”• Indonesia Good Corporate Governance Award 2015 “Score A (Excellent)”• Pacific Asia Travel Association (PATA) “Gold Awards 2015 for Inflight Magazine”

Picture’s source: www.google.com

Milestones

10

First Quarter 2015• Garuda Indonesia implemented hedging cooperation through Cross Currency Swap (CCS) transactions with banks.

The first and the biggest CCS transaction, exercised by SOE in Indonesia.• Garuda Indonesia, BII-Maybank, and NBAD/DIB carried signing of bridging loan facility with the principles of Sharia

facility of $ 500 million.

Second Quarter 2015• Garuda Indonesia launched the "New Mobile Apps“• Garuda Indonesia and Cardig Air signed a cooperation of air cargo management and business development• Garuda Indonesia exercised “Reprofiling Debt” of “Quick Wins” strategy by issuing sukuk amounted $500 mio with

4 times booking order.

Third Quarter 2015• Garuda Indonesia ends the Hajj Flights 2015 with 92.38% On-Time Performance Rates.• The Inaugurations of Garuda Maintenance Facilities AeroAsia (GMF-AA) 4th Hangar • President & CEO of Garuda Indonesia appointed as President of Indonesia Marketing Association (IMA) for the

period 2015-2017

Picture’s source: www.google.com

Fourth Quarter 2015• Hajj flight Operational Phase II has finished with OTP 83.34%• Develop the Chinese market by opening Direct Flights Denpasar - Guangzhou vv.• Garuda Indonesia got ISO 9001: 2015 for delay management from Ministry of Transportation

11

Garuda Indonesia Group Market Share – YTD October 2015

2014 2015

14%16%

44%38%

42%46%

Others

GA Group

Lion Group

Garuda domestic market share group (including Citilink)These market share were calculated based on all Garuda Indonesia’s routesSource: Company Data

Domestic Market Share

2014 2015

73%77%

27%23%

Others

GA Main Brand

International Market Share

Garuda main brand international market shareThese market share were calculated based on all Garuda Indonesia’s routesSource: Company Data

Picture’s source: www.google.com

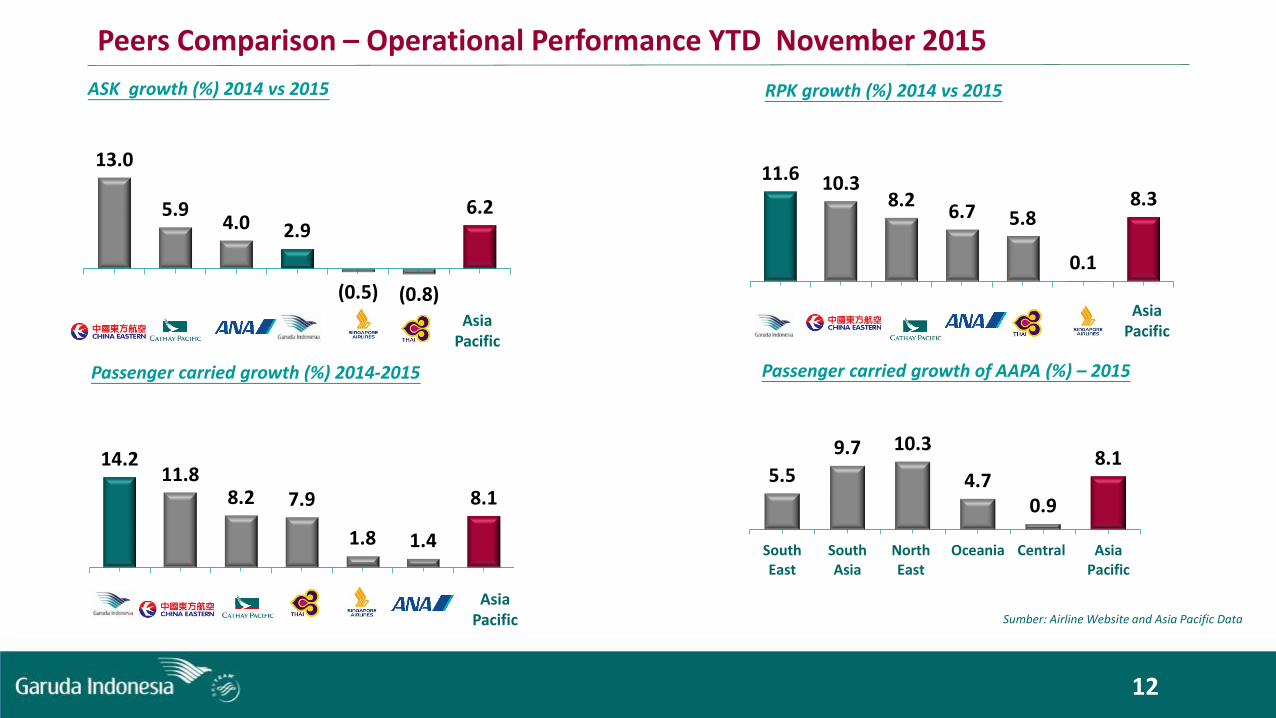

Passenger carried growth (%) 2014-2015

ASK growth (%) 2014 vs 2015 RPK growth (%) 2014 vs 2015

Asia Pacific

Passenger carried growth of AAPA (%) – 2015

Asia Pacific

Asia Pacific

12

Peers Comparison – Operational Performance YTD November 2015

Sumber: Airline Website and Asia Pacific Data

14.2 11.8

8.2 7.9

1.8 1.4

8.1

-

5.00

10.00

15.00

20.00

25.00

13.0

5.9 4.0 2.9

(0.5) (0.8)

6.2

(5.00)

-

5.00

10.00

15.00

20.00

25.00

11.6 10.3 8.2

6.7 5.8

0.1

8.3

-

5.00

10.00

15.00

20.00

25.00

5.5

9.7 10.3

4.7 0.9

8.1

-

5.0

10.0

15.0

20.0

25.0

SouthEast

SouthAsia

NorthEast

Oceania Central AsiaPacific

13

Operational Performance

Number of Fleets

5.85.0 4.5 4.3 4.5

2012 2013 2014 2015 2016E

Average Age (year)

14

Fleets per Dec 2014 169In

* B737-800NG 7

* CRJ - 1000 3

* ATR 72-600 3

* B777-300 ER 3

* A330-300 2* A320-200 4

Total 22

Out

* A330-200 2

* B737-800 1

* B737-500 1

Total 4Fleets per Nov 2015 187

14-Dec Dec15 Ops.lease Fin lease/

Dec16owned

Narrow body

• B737-500 4 - - - -• B737-800 NG 75 81 81 - 75• CRJ - 1000 15 18 12 6 18• ATR 72-600 8 11 11 - 15Total narrow body 102 110 104 6 108Wide Body

• B747-400 2 2 - 2 2

• B777-300 ER 6 9 9 - 10

• A330-200 11 9 9 - 7

• A330-300 11 13 7 6 17Total wide body 30 33 25 8 36Garuda main brand 132 143 129 14 144Citilink • B737-300 5 5 - 5 5• B737-500 - 3 - 3 3•A320-200 32 36 36 - 45Total Citilink 37 44 36 8 53Total fleets 169 187 165 22 197

15

Operational Performance Garuda Group

Operational

Efficiency

Passenger & Cargo

Financial

9M-2014 9M-2015 ∆ %

Aircraft Utilization (Hours) 9:53 9:11 -0:42

Frequencies 165,642 186,105 12.4

On Time Performance - OTP (%) 89.6 88.2 (1.4)

ASK ('000) 36,902,810 38,748,407 5.0

Average Fuel Price (USD/L) 0.9 0.5 (37.9)

Fuel Burn/Blockhours 3,699 3,590 (2.9)

Passenger Carried 20,893,654 24,551,594 17.5

RPK ('000) 26,086,291 29,951,212 14.8

Seat Load Factor (%) 70.7 77.3 6.6

Passenger Yield (USc) 8.6 7.5 (13.7)

Cargo/Mail Uplifted (Ton) 292,888 257,304 (12.1)

CASK (Usc) 7.6 6.4 (15.3)

CASK-excl Fuel (Usc) 4.5 4.5 0.0

• The passenger yield decreased 13.7% due to IDR depreciation ±12.1% and lower international fares amidst unstable economic.

Yield decreased

• The utilization was going down to be 9:11 hours due to route restructuring of Quick Wins program, especially in international market.

Utilization decreased

• OTP decrease due to Mount Raung eruption and fire incident in SHIA Terminal 2

• Cargo capacity decrease due to the increase of passenger carried as Garuda Cargo is ‘belly cargo’ on Garuda Group.

Others

Operational Performance Domestic & International

Domestic

International

16

9M-2014 9M-2015 ∆ %

Passenger Carried 12,666,172 14,508,965 14.5

Frequency 106,581 118,607 11.3

ASK ('000) 14,779,378 16,448,716 11.3

RPK ('000) 10,915,976 12,675,797 16.1

Seat Load Factor (%) 73.9 77.1 3.20

Passenger Yield (Usc) 10.1 8.6 (14.5)

CASK (Usc) 8.6 7.1 (17.1)

CASK-excl Fuel (Usc) 5.3 5.0 (4.4)

Passenger Carried 2,897,051 3,176,986 9.7

Frequency 21,549 20,835 (3.3)

ASK ('000) 16,963,144 15,742,812 (7.2)

RPK ('000) 11,101,472 11,953,539 7.7

Seat Load Factor (%) 65.4 75.9 10.49

Passenger Yield (Usc) 8.0 6.9 (13.6)

CASK (Usc) 7.3 6.3 (13.6)

CASK-excl Fuel (Usc) 4.4 4.5 3.0

Garuda Indonesia main brand has 58 domestic destinations

17 international destinations

Picture’s source: www.google.com

Operational Performance Main Brand & Citilink

Main Brand

Citilink

17

9M-2014 9M-2015 ∆ %

Passenger Carried 15,563,223 17,685,951 13.6

Frequency 128,130 139,442 8.8

ASK ('000) 31,742,521 32,191,527 1.4

RPK ('000) 22,017,448 24,629,336 11.9

Seat Load Factor (%) 69.4 76.5 7.15

Passenger Yield (Usc) 9.1 7.8 (13.7)

CASK (Usc) 7.9 6.7 (14.9)

CASK-excl Fuel (Usc) 4.8 4.8 (0.2)

Passenger Carried 5,330,431 6,865,643 28.8

Frequency 37,512 46,663 24.4

ASK ('000) 5,160,289 6,556,880 27.1

RPK ('000) 4,068,844 5,321,876 30.8

Seat Load Factor (%) 78.9 81.2 2.31

Passenger Yield (Usc) 6.5 5.8 (10.7)

CASK (Usc) 5.7 5.0 (13.4)

CASK-excl Fuel (Usc) 2.9 3.2 11.2

18

Financial Performance

Summary of Consolidated Income Statement

Garuda GroupTop Line (USD, Bio)

Operating Revenue

Operating Expenses

Income

EBITDAR Margin 14.4% 32.3%

Garuda GroupNet Income (USD, Mio)

19

In USD Mio 9M14 9M15 ∆ % YoY

EBITDAR 406.3 918.4 126.0

Total revenues 2,831.3 2,845.7 0.5

Fuel 1,175.7 806.5 (31.4)

Aircraft rental and charter 530.1 659.9 24.5

Others 1,374.8 1,251.3 (9.0)

Total expenses 3,080.6 2,717.6 (11.8)

EBIT (249.3) 128.1 151.4

EBT (298.3) 81.3 127.3

Net income (220.1) 51.4 123.4

0.9 0.9

1.0

Q1 Q2 Q3

12.4 16.9

22.1

Q1 Q2 Q3

Operating Revenue

2,831.3

2,845.7

(2.4%)

2.4%0.5%

9M14 9M15

Schedule airline

Non Schedule Airline

Others

Operating Revenue Operating Revenue

• Lower yield due to IDR depreciation and unstable economic condition in regional

• Losing revenue potency due to challenging conditions such as mount eruption, SHIA fire incident, and hazardous haze in Indonesia surroundings

Scheduled airline decrease

• Sustainable increase of charter revenue to China market and Umrah (Middle East).

• Additional revenue from Hajj season

Non schedule airline increase

• Others revenue increased due to green performance of subsidiaries.

Others increase

In USD mio% Change

*PoT : Percentage of total

20

Operating Revenue *PoT

Schedule airline 84.60%

Non schedule airline 6.20%

Others 9.20%

Operating Expenses

2,717.6

3,080.6

(12.0%)

4.7% (1.6%)(0.3%)

(2.6%)

9M14 9M15Operating Expenses Operating Expenses

Fuel Fligh Ops + Maintenance +

User charge

Tickets + Passenger

Service

G&AOthers

In USD mio% change

*PoT : Percentage of total

• Fuel expenses decreased 31.4% to be USD 806.5miocompared to same period last year of USD 1.2bio due to fuel price declining 37.9% compare last year.

• Total operating expenses decreased 11.8% to be USD 2.7 bio compared to the same period last year USD 3.1bio.

• Fuel efficiency YTD 9M15 USD 369.3mio as impact of fuel price declining and fuel efficiency program

• Non fuel efficiency YTD 9M15 USD ±115.3mio

Decreasing expenses

• The rental cost increased 24.5% to be USD 659.9mio compared to the same period last year of USD 530.1 mio in line with the additional fleets.

• The maintenance cost increased by 9.5% to be USD 210.2mio compared to the same period last yearUSD 192.0mio in line with the additional fleets.

Increasing expenses

21

Operating Expenses PoT*

Fuel 28.97%

Flight ops + Rental + Maintenance + User charge 47.96%

Ticketing + Passenger Service 15.62%

G & A 5.89%

Others 1.55%

Summary of Consolidated Balance Sheet

Asset

Liability

Equity

Lease Adj. Net Debt/EBITDAR 10.1x 7.5x

22

FY14 9M15 ∆ % YoY

Current assets 810.5 843.5 4.1

Non current assets 2,302.6 2,238.5 (2.8)

Total Assets 3,113.1 3,082.0 (1.0)

Current liabilities 1,219.4 1,103.7 (9.5)

Non current liabilities 1,014.2 1,107.2 9.2

Total liabilities 2,233.6 2,210.9 (1.0)

Total equities 879.5 871.1 (0.9)

Total liabilities & Equities 3,113.1 3,082.0 (1.0)

Summary of Consolidated Cash Flow

Operating

Cash receipts from customers USD 2.8bio

Cash payments to suppliers USD 2.4bio

Payments of interest and financial expenses USD 45.2mio

Investing

Payments PDP & Maintenance Reserve Fund: USD 303.4mio

Security Deposit payment: USD 11.1mio Refund of PDP and Maintenance Reserve

Fund: USD 216.2mio Receipts of security Deposit : USD 9.0mio

Financing

Proceed of long term loan, bank loan, & financial institution and sukuk USD 1,4bio

Payment of long term loan, bank loan & financial institution: USD 1.3bio

23

Min 5% of Cash Ratio

Picture’s source: www.google.com

9M14 9M15 ∆ % YoY

Beginning cash 480.4 434.3 (9.6)

Cash from operating activities (180.9) 56.0 130.9

Cash from investing activities (189.6) (104.1) (45.1)

Cash from financing activities 271.2 44.8 (83.5)

Net increase (decrease) in cash (99.3) (3.1) n.a.

Ending cash 396.6 409.5 3.2

Cash and Net Gearing

24

464.9 464.0 409.5 1,313.2 1,305.8 1,212.7 856.6 864.4 853.4

0.99

0.97

0.94

0.90

0.92

0.94

0.96

0.98

1.00

1.02

1.04

1.06

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

3M15 6M15 9M15

Cash Debt Equity Net Gearing

In USD Mio

31%

60%

9%

Debt Structure 9M2015

Short term loan Long term loan Lease

Max 2.5x of Debt to Equity Ratio

Min capital USD 800mio

Picture’s source: www.google.com

25

Main Brand Financial Performance YTD November 2015

in USD mio

Monthly 2015 Year to Date Growth

Jan-15Actual

Feb-15Actual

Mar-15Actual

Apr-15Actual

May-15Actual

Jun-15Actual

Jul-15Actual

Aug-15Actual

Sept-15Actual

Oct-15Actual

Nov-15Actual

YTD Nov-14Actual

YTD Nov-15Actual

∆ %YoY

Scheduled Airline 253.3 213.9 242.5 228.4 239.7 229.4 241.3 239.3 198.2 208.8 208.9 2,705.5 2,503.7 (7.5)

Non-Scheduled Airline 9.8 13.2 7.4 4.5 4.8 2.6 7.9 42.4 62.0 85.5 (4.1) 195.3 235.9 20.8

Others 6.8 6.6 8.4 7.5 6.9 8.1 6.4 6.7 5.8 6.6 6.7 63.1 76.6 21.3

Total Operating Revenue 269.8 233.8 258.3 240.3 251.4 240.0 255.7 288.4 266.0 301.0 211.4 2,963.9 2,816.1 (5.0)

Fuel Expense 83.5 67.8 74.7 73.0 78.1 74.4 79.6 80.0 72.0 78.1 55.2 1,258.7 816.4 (35.1)

Other Operating Expense 186.2 162.4 169.7 163.3 166.3 155.4 178.2 202.8 174.1 210.2 170.3 2,076.5 1,939.0 (6.6)

Total Operating Expense 269.7 230.3 244.4 236.3 244.4 229.8 257.8 282.8 246.1 288.4 225.5 3,335.2 2,755.5 (17.4)

Income / Loss from Operation 0.1 3.5 13.9 4.0 7.0 10.3 (2.1) 5.5 19.9 12.6 (14.1) (371.3) 60.7 116.3

Net Income (2.8) 2.0 12.2 1.3 4.3 10.7 2.7 6.7 14.5 4.8 0.8 (349.2) 57.2 116.4

EBITDAR 73.3 74.6 92.4 76.5 79.5 86.1 73.7 89.2 104.8 101.3 68.7 376.0 919.9 144.6

USDIDR 12,540 12,697 13,053 12,946 12,946 13,258 13,346 13,675 14,403 14,157 13,679 11,883 13,336 12.2

26

Operational Performance YTD November 2015

Jan15 Feb15 Mar15 April15 May15 June15 July15 Aug15 Sep15 Oct15 Nov15 YTD Nov14 YTD Nov15 ∆%

GA Group

Pax Carried 2,530,719 2,352,514 2,718,162 2,617,933 2,844,598 2,837,035 3,131,599 2,997,062 2,521,972 2,654,890 2,703,168 26,185,823 29,909,652 14.2

ASK (000) 4,579,484 3,969,185 4,379,174 4,382,420 4,525,879 4,246,134 4,490,507 4,311,873 3,863,669 3,967,296 3,931,849 45,350,834 46,647,470 2.9

RPK (000) 3,384,857 2,981,210 3,353,161 3,227,157 3,428,019 3,387,562 3,630,462 3,544,254 3,014,528 3,107,323 3,024,192 32,335,038 36,082,726 11.6

SLF (%) 73.9 75.1 76.6 73.6 75.7 79.8 80.9 82.2 78.0 78.3 76.9 71.3 77.4 6.1

Passanger Yield (Usc) 7.8 7.5 7.4 7.5 7.5 7.2 7.6 7.4 7.0 7.1 7.3 8.6 7.4 -14.0

CASK (Usc) 6.6 6.5 6.3 6.3 6.4 6.5 6.6 6.4 6.4 6.5 6.5 7.6 6.4 -15.8

CASK-excl Fuel (Usc) 4.6 4.7 4.3 4.4 4.4 4.4 4.4 4.5 4.7 4.7 4.8 4.6 4.5 -2.2

Fuel Price (USD/Liter) 0.57 0.51 0.55 0.55 0.56 0.58 0.59 0.51 0.47 0.49 0.48 0.85 0.53 -37.6

USDIDR 12,540 12,697 13,053 12,946 12,946 13,258 13,346 13,657 14,403 14,157 13,679 11,883 13,336 12.2

Domestic

Pax Carried 1,478,488 1,395,139 1,606,296 1,557,859 1,691,570 1,702,988 1,834,235 1,748,335 1,494,055 1,595,898 1,593,807 15,859,790 17,698,670 11.59

ASK (000) 1,814,370 1,652,182 1,867,850 1,855,800 1,916,993 1,812,428 1,913,557 1,915,803 1,699,649 1,769,055 1,780,271 18,440,677 19,998,041 8.45

RPK (000) 1,307,505 1,221,731 1,415,898 1,363,281 1,476,052 1,481,925 1,573,470 1,530,538 1,305,396 1,412,568 1,403,522 13,699,666 15,491,886 13.08

SLF (%) 72.1 74.0 75.8 73.5 77.0 81.8 82.2 79.9 76.8 79.9 78.8 74.29 77.5 3.2

International

Pax Carried 393,304 321,390 349,884 343,704 357,420 357,277 376,012 362,762 315,233 313,972 283,760 3,574,867 3,774,718 5.59

ASK (000) 2,120,078 1,705,563 1,785,559 1,834,306 1,835,190 1,685,657 1,705,301 1,600,580 1,470,577 1,437,313 1,289,719 20,406,769 18,469,843 -9.49

RPK (000) 1,579,310 1,275,576 1,339,302 1,302,737 1,330,834 1,294,929 1,340,011 1,325,174 1,165,664 1,116,598 964,549 13,487,581 14,034,687 4.06

SLF (%) 74.5 74.8 75.0 71.0 72.5 76.8 78.6 82.8 79.3 77.7 74.8 66.09 76.0 9.9

Citilink

Pax Carried 658,927 635,985 761,982 716,370 795,608 776,770 921,352 885,965 712,684 745,020 825,601 6,751,166 8,436,264 24.96

ASK (000) 645,035 611,439 725,764 692,314 773,696 748,049 871,649 795,489 693,443 760,929 861,859 6,503,388 8,179,667 25.78

RPK (000) 498,042 483,901 597,961 561,138 621,134 610,709 716,981 688,541 543,469 578,157 656,121 5,147,790 6,556,154 27.36

SLF (%) 77.2 79.1 82.4 81.1 80.3 81.6 82.3 86.6 78.4 76.0 76.1 79.2 80.2 1.0

27

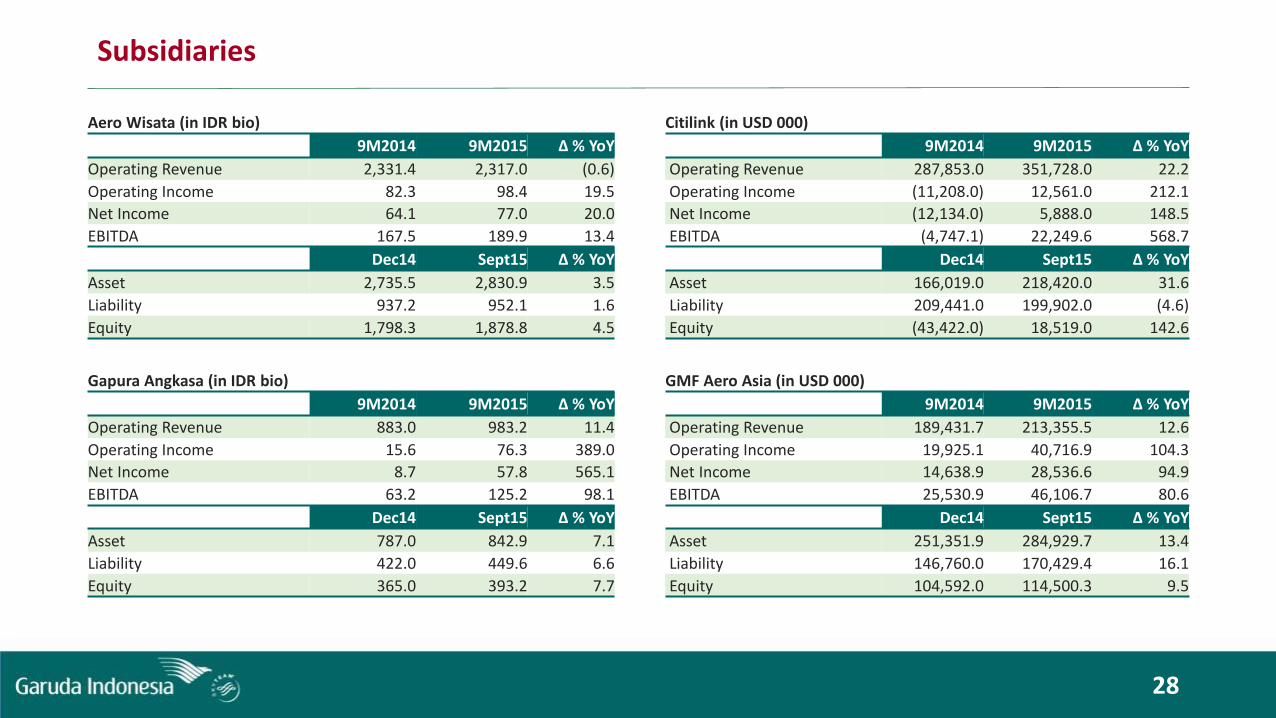

Subsidiaries

Subsidiaries

28

Aero Wisata (in IDR bio) Citilink (in USD 000)

9M2014 9M2015 ∆ % YoY 9M2014 9M2015 ∆ % YoY

Operating Revenue 2,331.4 2,317.0 (0.6) Operating Revenue 287,853.0 351,728.0 22.2

Operating Income 82.3 98.4 19.5 Operating Income (11,208.0) 12,561.0 212.1

Net Income 64.1 77.0 20.0 Net Income (12,134.0) 5,888.0 148.5

EBITDA 167.5 189.9 13.4 EBITDA (4,747.1) 22,249.6 568.7

Dec14 Sept15 ∆ % YoY Dec14 Sept15 ∆ % YoY

Asset 2,735.5 2,830.9 3.5 Asset 166,019.0 218,420.0 31.6

Liability 937.2 952.1 1.6 Liability 209,441.0 199,902.0 (4.6)

Equity 1,798.3 1,878.8 4.5 Equity (43,422.0) 18,519.0 142.6

Gapura Angkasa (in IDR bio) GMF Aero Asia (in USD 000)

9M2014 9M2015 ∆ % YoY 9M2014 9M2015 ∆ % YoY

Operating Revenue 883.0 983.2 11.4 Operating Revenue 189,431.7 213,355.5 12.6

Operating Income 15.6 76.3 389.0 Operating Income 19,925.1 40,716.9 104.3

Net Income 8.7 57.8 565.1 Net Income 14,638.9 28,536.6 94.9

EBITDA 63.2 125.2 98.1 EBITDA 25,530.9 46,106.7 80.6

Dec14 Sept15 ∆ % YoY Dec14 Sept15 ∆ % YoY

Asset 787.0 842.9 7.1 Asset 251,351.9 284,929.7 13.4

Liability 422.0 449.6 6.6 Liability 146,760.0 170,429.4 16.1

Equity 365.0 393.2 7.7 Equity 104,592.0 114,500.3 9.5

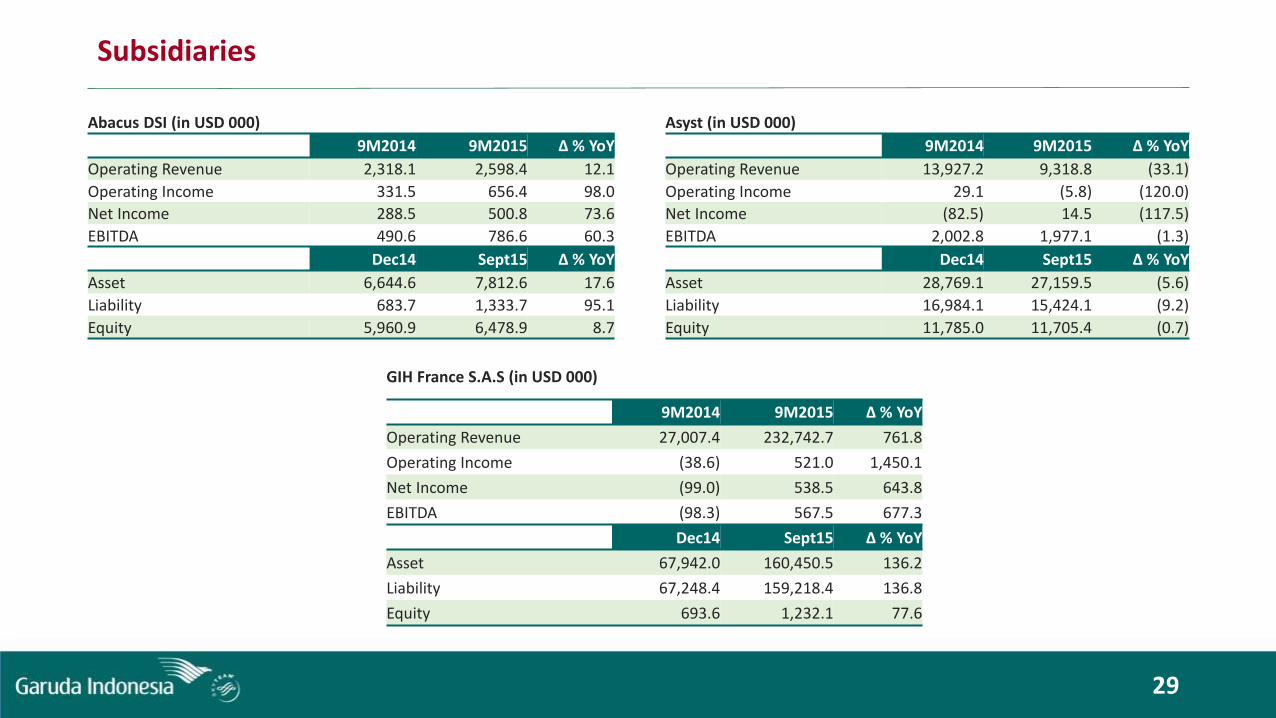

Subsidiaries

29

Abacus DSI (in USD 000) Asyst (in USD 000)

9M2014 9M2015 ∆ % YoY 9M2014 9M2015 ∆ % YoY

Operating Revenue 2,318.1 2,598.4 12.1 Operating Revenue 13,927.2 9,318.8 (33.1)

Operating Income 331.5 656.4 98.0 Operating Income 29.1 (5.8) (120.0)

Net Income 288.5 500.8 73.6 Net Income (82.5) 14.5 (117.5)

EBITDA 490.6 786.6 60.3 EBITDA 2,002.8 1,977.1 (1.3)

Dec14 Sept15 ∆ % YoY Dec14 Sept15 ∆ % YoY

Asset 6,644.6 7,812.6 17.6 Asset 28,769.1 27,159.5 (5.6)

Liability 683.7 1,333.7 95.1 Liability 16,984.1 15,424.1 (9.2)

Equity 5,960.9 6,478.9 8.7 Equity 11,785.0 11,705.4 (0.7)

GIH France S.A.S (in USD 000)

9M2014 9M2015 ∆ % YoY

Operating Revenue 27,007.4 232,742.7 761.8

Operating Income (38.6) 521.0 1,450.1

Net Income (99.0) 538.5 643.8

EBITDA (98.3) 567.5 677.3

Dec14 Sept15 ∆ % YoY

Asset 67,942.0 160,450.5 136.2

Liability 67,248.4 159,218.4 136.8

Equity 693.6 1,232.1 77.6

30

Notes

31

Notes

32

PT Garuda Indonesia (Persero) Tbk.Investor Relations Department

2nd Floor Management BuildingGaruda CitySoekarno-Hatta International AirportPhone: 62-21-2560 1201Email: [email protected]

Related Documents