MANAGERIAL COMPETENCIES, ACCESS TO CREDIT AND BUSINESS SUCCESS BY JAMIYA NAKIYINGI 2007/HD10/11266U A DRAFT DISSERTATION SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OF THE DEGREE OF MASTER OF SCIENCE IN ACCOUNTING AND FINANCE OF MAKERERE UNIVERSITY NOVEMBER, 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MANAGERIAL COMPETENCIES, ACCESS TO CREDIT

AND BUSINESS SUCCESS

BY

JAMIYA NAKIYINGI

2007/HD10/11266U

A DRAFT DISSERTATION SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OF

THE DEGREE OF MASTER OF SCIENCE IN ACCOUNTING AND

FINANCE OF MAKERERE UNIVERSITY

NOVEMBER, 2010

ii

DECLARATION I, the undersigned, Jamiya Nakiyingi declare that, to the best of my knowledge, the work

presented in this dissertation is truly my original work and has never been submitted for

the requirement of the award of a degree in this or any other university of learning.

Where work of others has been used, due acknowledgement has been made.

Signed: ……………………………… JAMIYA NAKIYINGI Date: ………………………………..

iii

APPROVAL

This is to certify that this dissertation has been submitted in partial fulfillment of the

requirement for the award of a Master of Science degree in Accounting and Finance of

Makerere University with my approval as University Supervisor.

Signed: …………………… Date: ………………… DR. ARTHUR SSERWANGA

MAKERERE UNIVERSITY

Signed: ................................. Date: …………………. DR. JOSEPH NTAYI

MAKERERE UNIVERSITY

iv

DEDICATION I would like to dedicate this study to my lovely parents, Al-Hajji & Al-Hajati Lutalo and

the entire family who have supported me in every way. Your belief in me has propelled

me to heights.

v

ACKNOWLEDGEMENTS

I wish to thank my supervisors, Dr. Arthur Sserwanga and Dr. Joseph Ntayi for their

support and continued guidance during this research study. My sincere gratitude goes to

the management of MUBS for the financial support you forwarded to help me

accomplish this study. MUBS, I highly commend you.

I am indebted to the owners and / or mangers of the SMEs in Kampala who accepted and

responded to the Questionnaire(s) of this survey. Finally to the Almighty ALLAH be the

glory for his faithfulness to me and without whom I would never have come this far.

I owe all of you this achievement and to you I will remain sincerely indebted.

vi

TABLE OF CONTENTS Declaration………………………………………………………………………………..ii

Approval………………………………………………………………………………….iii

Dedication………………………………………………………………………………...iv

Acknowledgements...………………………………………………………………..........v

Table of Contents…………………………………………………………………………vi

List of Abbreviations……………………………………………………………………..ix

List of Tables……………………………………………………………………………...x

List of Figures...…………………………………………………………………………..xi

Abstract…………………………………………………………………………………..xii Chapter One...................................................................................................................1

1.1 Introduction………………………………………………………………………..1

1.2 Background to the Study ...................................................................................... 1

1.3 Statement of the Problem ..................................................................................... 3

1.4 Purpose of the Study ............................................................................................ 4

1.5 Objectives of the Study ........................................................................................ 4

1.6 Research Questions .............................................................................................. 4

1.7 Scope of the Study ................................................................................................ 5

1.7.1 Subject Scope................................................................................................ 5

1.7.2 Geographical Scope ...................................................................................... 5

1.8 Significance of the Study ....................................................................................... 5

1.9 Conceptual Framework .......................................................................................... 6

1.10 Organization of the report…………………………………………………………6

vii

Chapter Two ……...…………………………………………………………………...7

2.1 Introduction………………………………………………………………………..7 2.1 Small and Medium size Enterprises (SMEs) ........................................................ 9

2.2 Managerial Competencies .................................................................................. 10

2.3 Credit Accessibility ........................................................................................... 14

2.4 Business Success ............................................................................................... 15

2.5 Managerial Competencies and Business Success................................................ 16

2.6 Access to Credit and Business Success .............................................................. 17

2.7 Managerial Competencies, Access to Credit and Business Success .................... 18

2.8 Conclusion......................................................................................................... 19

Chapter Three.……………………………………………………………………….20

3.1 Introduction .......................................................................................................... 20

3.2 Research Design ................................................................................................... 20

3.3 Area and Study Population ................................................................................... 20

3.4 Sample size and Sampling Procedure .................................................................... 20

3.5 Sources of Data .................................................................................................... 21

3.6 Data Collection Instruments .................................................................................. 21

3.7 Measurement of Research Variables ..................................................................... 22

3.8 Validity and Reliability of the Instruments ............................................................ 22

3.9 Data Processing and Analysis ............................................................................... 23

3.10 Limitations to the Study ........................................................................................ 24

Chapter Four….……………………………………………………………………...25

4.1 Introduction ........................................................................................................... 25

viii

4.2 Demographic Features ........................................................................................... 25

4.3 Rotated Component Factor Analysis ...................................................................... 28

4.4 Correlations…………………………………………………………………………33

Pearson Correlation………...…………………………………………………………….34

4.4.1 Relationship between Managerial Competencies and Business Success……….35

4.4.2 Relationship between Credit Accessibility and Business Success……………...35

4.4.3 Relationship between Managerial Competencies and Credit Accessibility…….35

4.5 Regression Analysis .............................................................................................. 38

4.6 Combined Regression Analysis ............................................................................. 39

4.7 Other Findings ....................................................................................................... 40

Chapter Five…..…………………………………………………………………...…45

5.0 Introduction ........................................................................................................... 45

5.1 Discussions…………………………………………………………………………45

5.2 Conclusion ............................................................................................................ 48

5.3 Recommendations ................................................................................................. 50

5.4 Areas for further research ...................................................................................... 51

REFERENCES…………………………………………………………………….……52

APPENDIX 1……………………………………………………………………………58

APPENDIX 2……………………………………………………………………………61

ix

LIST OF ABBREVIATIONS

ANOVA - Analysis of Variance BUDs - Business Uganda Development Scheme GEM - Global Entrepreneurship Monitor MFPED - Ministry of Finance, Planning & Economic Development MHRM - Masters in Human Resource Management MUBS - Makerere University Business School PSFU - Private Sector Foundation Uganda SME - Small and Medium-sized Enterprises SPSS - Statistical Package for Social Scientists UBOS - Uganda Bureau of Statistics UMA - Uganda Manufacturers Association URA - Uganda Revenue Authority USSIA - Uganda Small Scale Industries Association

x

LIST OF TABLES

Table 1: Reliability Coefficients………………………………………………………..22

Table 2: Gender of respondents ................................................................................... 25

Table 3: Category of the positions held by the respondents in the SMEs ...................... 26

Table 4: Education Levels of the respondents .............................................................. 27

Table 5: Existence in the business ............................................................................... 27

Table 6: Kind of business the firm is engaged in ......................................................... 28

Table 7: Factor Analysis for managerial competencies ............................................... 29

Table 8: Pearson correlation moment .......................................................................... 35

Table 9: Regression Analysis ....................................................................................... 38

Table 10: Combined Regression Analysis..................................................................... 39

Table 11: ANOVA between Gender and the Study ...................................................... 40

Table 12: ANOVA between Legal Status and the Study .............................................. 41

Table 13: ANOVA between Education Levels and the Study....................................... 42

Table 14: ANOVA between Study Variables and Duration ……………………………43

xi

LIST OF FIGURES

Figure 1: Conceptual Model………………………………………………………..7

Figure 2: Legal status of the enterprise …………………………………….……26

xii

ABSTRACT

The purpose of the study was to investigate the relationship between Managerial

Competencies, Access to credit and Business success of selected SMEs in Kampala. The

research was guided by three objectives; to establish the relationship between managerial

competencies and business success, to investigate the relationship between credit

accessibility and business success and to examine the relationship between managerial

competencies, access to credit and success of selected SMEs’.

The research followed a cross sectional design. Primary data was collected using self

administered questionnaires issued to the respondents. Data was collected and analyzed

using a sample size of 381 SMEs randomly selected from a population of 45,832 SMEs.

Data analysis was done with help of SPSS and with the use of pearson’s correlation

coefficient which was used to measure the strength and direction between managerial

competencies, access to credit and business success.

The findings disclose a positive and significant relationship between managerial

competencies, credit accessibility and business success. Managerial competencies and

access to credit explain about 27.7% of the variance in business success. This implies that

in order to achieve business success SMEs should improve managerial competencies and

put in place better mechanisms for accessing credit. This survey recommends that in the

quest for solutions for the business success, other factors should also be emphasized that

have an effect on firm performance.

xiii

1

CHAPTER ONE

1.1 Introduction

This chapter presents an overview of the research starting with the background to the study,

statement of the problem, purpose of the study, objectives of the study, research questions,

scope of the study, significance of the study, conceptual framework and the organization of

the study.

1.2 Background to the Study Small and medium-sized enterprises (SMEs) represent over 90% of enterprises in Uganda.

According to Hatega (2007), it is estimated that the number of SMEs is more than

1,069,848 which constitutes ninety percent (90%) of Uganda’s private sector. Its

composition is more of the informal sector than the formal sector and mainly deals in agro-

processing, trade, small and medium manufacturing. Eighty percent (80%) of these SMEs

are located in the urban areas and they contribute seventy five (75%) of the Gross Domestic

Product (GDP).

In Uganda, a number of SMEs, which for the purpose of this study are defined as those

resident business units that are a seedbed for entrepreneurship development, usually

operate in the informal sector of the economy, employ mainly wage-earning workers, and

participate more fully in organized markets (Torgler, 2002). These Small and micro-

enterprises do not have a standard definition in Uganda. According to the Uganda Ministry

of Finance, Planning and Economic Development (2000), there is a distinction between

small and micro businesses. In the Ugandan context, micro businesses are defined as those

enterprises which employ less than five people, with value of assets, excluding land and

buildings, of not more than Uganda Shs.2.5m and an annual turnover of below Uganda

2

Shs.10 million. Furthermore, as the Ministry points out, micro-enterprises are

predominantly family businesses which are usually not registered and primarily operate in

the informal sector. Small enterprises are defined as businesses that employ up to 50 people

with value of assets, excluding land and buildings, of not more than Uganda Shillings 50

million, an annual turnover of between Uganda Shs.10 million and Shs.50 million and an

investment in plant and machinery not exceeding Uganda shillings 40 million. Most small

enterprises operate in the formal sector and are duly registered for taxation purposes.

Traditionally, SMEs’ in Uganda do not have requisite managerial

competencies to run certain activities / tasks in their firms (Balunywa, 2003). Such

managerial competencies are a set of skills, related knowledge, traits and attitudes that

allow an individual to perform a task or an activity within a specific function or job

(Raynard, 2001). Although the competencies that are required of the members are known,

there is evidence that some of the entrepreneurs that run these SMEs’ are usually poorly

educated, lack experience, are unimaginative and lack business skills and knowledge to

perform their work which in turn affects business performance (Senge, 2002).

More so, in order to ensure continuity and realized success, SMEs’ need to

acquire the necessary financial resources / credit that could allow them to invest now

drawing on expected future income (Audretsch, 2002). Acquisition of such credit is

difficult for the SMEs’ due to the high lending rates and this has constrained the private

sector demand for the credit which limits their progress (Kikonyogo, 2000). On the other

hand, the banking sector in Uganda has a history of high default rates which has

3

discouraged them from lending to SMEs’ since they are regarded as very risky ventures.

There is therefore a gap to be filled between the potential borrowers who are the SMEs’ to

access credit and the lenders who are the commercial banks (BOU Report, 2004).

Such difficulties faced in accessing credit by the SMEs’ from the lenders may

impact on the SMEs’ success. Chakraborty, 2006 attributes success of SMEs’ to easy credit

access, other ethinic resources (finance from within) and opportunities provided by the

emergence of niche markets to satisfy the demands. Some researchers however argue that it

is the management teams’ motivation to continue the business activities when faced with a

dynamic business performance environment like managing those periods of transition

between the readily identifiable phases of growth that will ultimately determine the

businesses success (Cangemi, 1998). This therefore sets the basis for the researcher to

further investigate the case within SMEs’ in Kampala.

1.3 Statement of the Problem

SMEs’ low success may be attributed to lack of reliable managerial competencies to run

certain activities and credit accessibility (Bhattacharya, 1998). Such SMEs that would

utilize the funds from the money lending institutions find it hard due to their inaccurate,

untimely, incomplete records as forwarded from their management who have ignored their

key competencies like; ability to network, assimilate experience, set goals, monitor

resources, build entrepreneurial teams, solve problems and cope with uncertainties

(Atanasova and Wilson, 2004). This may be responsible for affecting business success and

hence needed to be investigated.

4

1.4 Purpose of the Study

The study sought to ascertain a relationship between managerial competencies, access to

credit and business success of SMEs’ in Uganda.

1.5 Objectives of the Study

The main objectives of the study were: i.) To establish the relationship between managerial competencies and

business success of SMEs’ in Uganda.

ii.) To investigate the relationship between credit accessibility and business

success of SMEs’ in Uganda.

iii.) To examine the relationship between managerial competencies, access to

credit and success of the SMEs’ in Uganda.

1.6 Research Questions

The study was guided by the following research questions:

i.) What is the relationship between the managerial competencies and the

business success of SMEs’ in Uganda?

ii.) What is the relationship between credit accessibility and business

success of SMEs’ in Uganda?

iii.) What is the relationship between managerial competencies, credit

accessibility and success of SMEs’ in Uganda?

5

1.7 Scope of the Study

1.7.1 Subject Scope

The study focused on the managerial competencies in respect to the skills, knowledge,

Attitude and access to credit in respect to the amounts received and the frequency of credit

accessibility and business success of the SMEs’ in Uganda.

1.7.2 Geographical Scope The study confined to a few selected SMEs’ in Uganda within the chosen divisions. This

was so because of the money and time constraint.

1.8 Significance of the Study

The study sought to make the following contributions:

a) The results of this study will help the banks and other lending institutions to

establish which decision variables have the greatest impact on the access to credit

by the SMEs’ in Uganda.

b) The findings of this study could contribute to the existing information on SMEs’ to

enable these firms model themselves into credit worthy businesses which are

plausible to money lenders when seeking for loan facilities.

c) The findings will be of use to the owners of these enterprises themselves as they

will be able to adopt some of the recommendations advanced in the study.

d) Finally, it will be an academic resource providing solutions to the identified

problem and highlighting areas for further research.

6

1.9 Conceptual Framework The following Conceptual framework was developed after review of existing literature to

investigate the research questions at hand. The framework shows Managerial competencies

and access to credit as the independent variables used to explain business success as the

dependent variable. In order to facilitate the study, the researcher developed a conceptual

framework drawn from the works Berger (2002) where business success was described in

terms of sales, profitability and survival. The model has adopted underlying characteristics

of entrepreneurs such as skills, knowledge and experiences to represent managers’

innovativeness, networking, capacity building, competitiveness, persistence among others

which in turn explains managerial competencies as stated by Karns (1998) that could lead

to business success. For the purpose of this research, access to credit may be determined in

respect to amounts borrowed (shillings) from money lending institutions with their turnover

(number of times) as described by Chakraborty (2006). This is because other variables

were not catered for in the data sets that were used for the study.

7

Figure 1: Conceptual Model

9.0 Literature Revie

1.10 Organisation of the Study

The study is organized in five broad chapters. Chapter one laid the foundation of the

research. It is the introductory chapter and this covers the background to the study, the

problem statement, the purpose of the study, research objectives, the research questions,

scope of the study, significance of the study and the conceptual framework on which the

study is based. Chapter two covers a review of the related literature on managerial

competencies, access to credit and business success and this brings out information that has

already been written on the subject by other scholars. Chapter three stipulates the

methodology adapted by the researcher and covers the research design, area and study

population, sample size, sources of data, data collection instruments, measurement of the

Managerial Competencies

Capacity building Networking Competitiveness Innovativeness Motivation

Access to credit Amount received

- Volume (Shillings)

Frequency of access (Number of times)

Business success of SMEs’

Growth Profitability Increased

Productivity & Sales

Survival

8

research variables, data processing and analysis and limitations that were encountered.

Chapter four is where data collected was presented, analyzed and findings discussed and

Chapter five is the final chapter where conclusions on the findings as laid down in chapter

four were made, recommendations made by the researcher and areas for further research.

9

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter examines available literature on the relationship between the different

variables used in this study namely; managerial competencies, access to credit and business

success.

2.2 Small and Medium size Enterprises (SMEs) Small and medium-sized enterprises (SMEs) represent over 90% of enterprises in Uganda

and they contribute about 75% of the Gross Domestic Product, (Hatega 2007). SMEs play a

significant role in the economies (Narain, 2001). They influence their growth and

development, income generation through employment of the citizens among others,

(MFPED, 2000). Despite their contribution to national economy, SMEs have been bogged

down by performance issues which have influenced their success. The literature mainly

attributes challenges of success among SMEs to lack of financing, marketing problems,

poor record keeping and incompetencies of their managers among others (Stevenson,

2005).

SMEs’ are very important for a developing economy because they provide

employment opportunities up to approximately 2.5 million and are a basis for developing

new ideas as well as contributing to economic growth and sustainable development (UMA

consultancy and information services, 2007). They are the driving force behind a large

number of innovations and contribute to the growth of the national economy through

investments, exports and generate a large share of new jobs in the economy (Badagawa,

2002).

10

The Small and Medium size business sector is of interest to policymakers not only

because of the important role it plays in the Ugandan economy, but also because of the

avenue to advancement that the SME business ownership represents, in particular for ethnic

minorities (Raynard, 2002). Critical to SME businesses' success is the availability of

financing for both capital acquisition and working capital purposes. Much of this financing

takes the form of credit extended by commercial banks and non bank lenders (Berger,

1995).

SMEs need to have access to adequate financial support and reliable management to

enhance productivity and in turn facilitate market access (Sebstad, 1995). The

establishment of an active SMEs sector and the effective utilization of quality business

information and credit have been identified as crucial in attaining long term and sustainable

business success and better performance for developed and developing countries (

McMahon, 2007).

2.3 Managerial Competencies

Henderson (2000) defines competency as a combination of knowledge and skills required

to successfully perform an assignment. Its attainment is evidenced by the ability of an

individual to gather data, process it into useful information, access it and arrive at an

appropriate and useful decision in order to initiate the actions necessary to accomplish the

assignment in an acceptable manner.

Managerial competencies are a cluster of similar knowledge, skills and attributes

that are essential to effective job performance (Karns, 1998). For this study, managerial

competencies did cover employee training and development, leadership skills, knowledge

and professional experience (Stoner et al., 1995). These competencies are the result of

11

behavioural research to identify superior performance and are applied horizontally across

the organization (Nyhan, 1995).

On the other hand Boyatzis (2000) describes managerial competencies as

underlying characteristics of a person that he or she uses to solve problems that arise at a

work place. Some of the underlying characteristics of the Executive Directors include the

ability to speak and perform in public, express the desire to persuade others of their point of

view, motivate others to action, make decisions and amend those decisions to fit in with the

organizational vision or current realities (Hagberg Consulting Group 2005). Boyatzis

(2000) as well as Munene (1998), have identified different types of competences, which

they have referred to as operant competences and emotional competences respectively.

According to Kayes et al (2005), managerial competencies involve internally and

externally managing the host people and other expatriates in the organization. This internal

management skill serves to resolve conflicts between local employees and expatriates and

maintain a close relationship between them.

Managerial Competences are important because they are forward looking, describe

the skills and attitudes the staff need to meet future challenges, help clarify expectations

and provide a sound basis for consistent and objective performance standards by creating a

shared language about what is needed and expected in an organization (United Nation’s

Report, 2004).

According to Shippmann et al. (2000) the notion of managerial competences is

relational. It brings together disparate things-abilities of managers (deriving from

combinations of attributes) and the tasks that need to be performed in a particular situation.

Thus managerial competences are conceived of as a complex structuring of attributes

12

needed for intelligent performance in specific situations. Such competences need to be

operationalised through activities, outcomes and criteria in order to be a basis for

meaningful reflection.

Managerial competencies are further reflected through Leadership Skills which are

an occurrence when one group member modifies the motivation or competencies of others

in a given group (Boam, 1992). In order for managers to be both effective and efficient in

their managerial functions, they must possess exemplary leadership skills (Cangemi et al.,

1998)

For leaders to allow employees to take risks, they must also trust them a great deal.

Trust is an important element of good leadership. It is something that is very hard to earn

and very easy to loose. Such skills are ways in which trust is built between employees and

the leaders, (Bartlett, 2007).

Leaders must make sure the team has clearly defined goals and that those goals

align with the overall vision, goals and objectives of the company. So knowing the

company’s vision, objectives and goals would allow the managerial leader and the team to

develop strategies that could differentiate their product or service from others and provide

them with a competitive advantage (Cangemi et al., 1998). Related to the above is the

argument that selection of employees will impact on job performance because it relies on

clear definition of critical managerial competencies which must be derived from the

requirements of an organization (Thompson, 1999).

Hence given the size of their firms, managers of SMEs are expected to be a window

to the outside world. They need to be innovative, figurehead; that is having a greater degree

of power and influence. The manager is the nerve centre and turbulent handler for they

13

either make or break their organizations. In a survey carried out on the high mortality rate

of SMEs that were failing in the USA; of the 1200 respondents, 41 percent said the major

culprit was lack of reliable managerial competencies that in turn influenced business

success (Penrose, E.T.; 1995).

Education and training of managers through educational policies and curricular

content emphasize practical business skills such as; technical skills, engineering,

accounting and finance, marketing and human resource management do contribute to

providing potential entrepreneurs with the needed managerial skills, (Stoner et al, 1995).

Education and training policies and programmes are most supportive of SMEs

when they lead to the development of skills and attitudes that are consistent with and

relevant to the opportunities present in the environment. Innovation provides the firm with

the capability to generate new products and services faster than the competitors. For

example; several studies suggest that the increase in the level of education and business

skills in the United States increased entrepreneurship and new firms, (Calderon & Nickel,

1998 and Audretsch & Thurik, 2000).

Managers with autonomy are motivated to act and make decisions independently

(Frese et al, 2002). Autonomy leads to the desire to express ones individuality in the work

place and also disliking superior orders. There are many tasks for which business managers

don’t receive explicit training in developing a business plan, book-keeping and marketing.

Therefore they depend on learning from experience and must develop their knowledge base

independently in order to succeed (Minniti & Bygrave, 2001).

14

2.4 Credit Accessibility Credit arises from the lending activities between individuals, business enterprises, financial

institutions and the government. Credit is simply the right of the lender to receive money in

future, in return for his obligations to transfer the use of his funds to the borrower (Levine,

1997).

Credit is a claim on the incomes and assets of the borrower. It is an asset to the

lender. Credit plays a vital role in the functioning of a free market economy. This market is

based on credit and sustained by credit. The development of modern SMEs’ would hardly

be possible without developed credit systems (Ondiege, 1998).

SMEs’ borrow loans to meet their working capital needs. Such enterprises that

desire to acquire machines and equipment for the expansion of their production facilities

need additional funds, either from financial intermediaries like banking institutions or even

individuals, Castelli (2006). The lending activities in the commercial banks today tend to

concentrate on less risky and higher short term lending. This was caused as a result of the

banks experience of non-performing assets; which led to risk aversion tendencies that were

tight resulting to exceptionally high real lending rates (Kikonyogo C.N, 2000).

Prior studies revealed that the ability of several SMEs to exploit highly profitable

opportunities would be enhanced if external financing were more accessible. High rates of

application for loans among the firms and their willingness to pay above market rates of

interest indicate a strong and excess demand (Kasekende & Opondo, 2003; Kayser, 1990;

Miller, 1999; UNCTAD, 2002).

The flows of credit between the various sectors of the economy are just like the

flow of blood through the organs of the human body. So long as it flows smoothly and

expands at rates as required for a steady growth of output, it would make possible for the

15

raising of incomes, employment, production and sales. Therefore the failure of specialized

financial institutions to meet the credit needs of SMEs’ underlines the importance of a

needs oriented financial system in order to achieve rural development (Atieno R, 2001).

Further more, Pandey (1996) asserts that the Credit Limit, which is the minimum

amount of credit set to be accessed by the borrower at a certain point in time, has a positive

impact it plays on the business success. Such loan amounts offered by the banks encourage

more SMEs’ to access credit in various forms from the commercial banks and hence better

performance.

Torgler (2007) further argue that the type of financial institution and its policies will

often determine the access to credit problem by the Small and Medium sized Enterprises.

Where the credit duration, terms of payment, required security and the provision of

supplementary services do not fit the needs of the target group, potential borrowers will not

apply for the credit even when it exists and when they do, they will be denied access hence

hindering the success of their businesses.

2.5 Business Success Castelli (2006) defines Business success as a subject to individual interpretation based on

upbringing, past experiences, role models, competitive forces, personal motivations and

goals. For some, merely staying in business can be considered success, while for others it

could be achieving a certain level of sales or an IPO thus core values of the business

(Castelli, 2006).

Timmons (1999) asserts that as you achieve business success, it is sometimes

measurable and sometimes not. Accumulating a certain volume in sales is certainly one

way to measure success, but it is not the only way; earning a prestigious award, earning the

16

respect of your peers, or providing livelihood to your employees may be far more

meaningful to you.

Very few people achieve success in business accidentally. Most people who

achieve business success first defined it, then planned for it, and pursued it diligently; they

set goals to achieve it. Once you have defined what it means to achieve business success,

your next step is to set goals that will lead you to your definition of success. You must

create realistic, viable plans to achieve those goals. Follow your plans, be flexible, and

enjoy the process (Timmons, 1999).

2.6 Managerial Competencies and Business Success From a sociological perspective, managerial competencies can fully be enhanced through

various employee developments in businesses for the firm success in the long run.

According to Karns (1998), promotion of employees in firms is a means of examining the

managers’ competencies that are essential for effective job performance / business success.

Managerial competencies can be improved through promotion of employees which

is less expensive than transferring or hiring which in turn has a positive effect on business

success. In so doing, the firm institutes a culture among the work team that promotable

insiders are also proven resources (Stoner, 1995). This also has a positive motivational

impact on their competencies that will also boost the business success. Experience has

shown that people tend to work harder when they believe there is a possibility of being

promoted which limits social in-breeding and creates a better positive feedback at work

(Drejer, 2000).

According to Karns (1998), what should not be negotiable between the manager and

the team are the firms goals and objectives. Management should strive not to completely

17

give up control of the organizational goals and objectives because they must make sure the

team members’ goals too align with those of the business to enhance the firms’ success

(Balunywa, 2003).

To help empower the team, managerial competencies must become a resource of

the team to enhance business success. A pivotal skill that allows a leader to do this is good

communication (Blake, 1996). The more the team and management communicate, the more

interdependence there will be and this in turn creates a participative relationship between

the two. The upward communication allows employees to gain more information and solve

problems easier. They would also be motivated to work knowing that they have an

influence or say on what goes on above them in the organization which would also help

them to take chances with minimal risk (Blake, 1996).

2.7 Access to Credit and Business Success According to Kashyap (1996), lack of access to credit is a critical constraint to the success

of firms. Such business enterprises in both developed and developing economies have

difficulties in obtaining assistance from banks and other money lending / financial

institutions. Studies show that most SMEs’ start their lives without institutional help.

However, such enterprises find it difficult to grow and succeed in business without the

opportunity to borrow from these lending institutions (Berger, 2002).

Levitsky and Ranga, (1994) advanced reasons for limited access to institutional

finance by these SMEs’ which further deeply affects their performance in business. For

instance; lending to SMEs’ is considered to be a risky venture. The uncertainties facing

such firms, the high mortality rate of such enterprises, the nature of the interest rates to be

charged, the vulnerability to market and economic changes make banks reluctant to deal

18

with them. This further reflects the parallel reluctance on the part of SMEs’ to borrow from

those money lending Institutions and in turn limiting their business success (Atanasova,

2004).

The availability of credit for SMEs’ depends significantly on the nation’s financial

structure and its accompanying lending infrastructure and technologies. Through these

mechanisms, government policies and financial structures do influence the level of credit

availability and inturn the business success (Berger and Udell, 2006). The lending

infrastructure ranges from the information, tax, legal, judicial and bankruptcy environments

to the social regulatory environments. Lending technologies include information on which

financial institutions rely upon to determine the supply of debt finance to SMEs while

simultaneously addressing the opacity problems (Berger and Udell, 2006).

2.8 Managerial Competencies, Access to Credit and Business Success Empirical evidence from several prior research works through decades up to date provide

strong support for the proposition that as businesses progress through their growth stages,

the financial dimensions of their operations under the management team running them tend

to become more challenging (Vozikis,1999). In the eighties, the same preposition was

further confirmed that there was a greater need for careful attention to management if the

expanding businesses were to succeed in survival and performance terms (Ray, 1980a,

1980b; Hutchinson et al., 1981; Ray & Hutchinson, 1983; Kazanjian & Drazin, 1989).

In light of O’Farrell & Hitchens’, (1990) work, it was justifiable to include the

managerial competencies amongst the new abilities referred to by Penrose (1995). O,Farrell

and Hitchens (1990) claim that there are both theoretical and empirical reasons for

believing that the Penrose effect is a major determinant of the business success. More so,

19

the businesses will have to sustain in nature with their ability to access credit from lenders.

Both case studies and econometric analyses support this view. Thus, there could be

managerial diseconomies in SMEs’ related to the availability and abilities of senior

managers (including owner managers) who could under take financial management.

Improved credit accessibility terms and managerial competencies are intended to

permit a business to handle more effectively and efficiently the progress and in the long run

the business success (Bhattacharya, 1998). The presumption is that the more challenging

the financial circumstances of the business with an unreliable management, the more

sophisticated would need to be financial management practices employed to deal with such

difficulties hence having a great effect on the firms’ performance (McMahon, 1998).

2.9 Conclusion The purpose of this research was to thoroughly examine the relationship between

managerial Competencies, access to credit and business success. Hence SMEs which

recognize the need to adapt financial expertise practices to changing circumstances are

more likely to succeed in performance terms. That is when need arises for external

financing, firms would use their finance expertise to negotiate with the lending banks on

the cost of external financing such as the interest rates before they would also accept or

decline these money lending institutions offer.

20

CHAPTER THREE

METHODOLOGY

3.1 Introduction This section presents the research methods that were used to carry out the study. It covers

the research design, survey population, sample size, sampling procedures, sources of data,

data collection methods, measurement of variables, data analysis and limitations of the

study.

3.2 Research Design A cross sectional design was used together with the explanatory research design to answer

the research questions. In order to obtain reliable and representative study results within the

limited time, this study was conducted as quantitative in nature. It employed a survey

design mainly having owner – managers of SMEs as the primary respondents.

3.3 Area and Study Population The population consisted of SMEs operating in Kampala estimated to be 48,300 as in the

Uganda Bureau of Statistics 2003. Their real number cannot be established. Kampala town

chosen is further sub-divided into various zones and these formed the strata.

3.4 Sample Size and Sampling Procedure The sample size used for the study was 381 SMEs. This was based on Krejcie & Morgan

(1970) table for determining the sample size where they contend that a sample size of 379

is appropriate for a population of 30,000, 380 is appropriate for a population of 40,000

SMEs and 381 is appropriate for the population of 50,000. Therefore given the population

21

of 48,300 SMEs in Kampala, a sample size of 381 was recommended for this study. Simple

random sampling was used to select a representative sample of the SMEs.

3.5 Sources of Data The researcher used both the primary and secondary sources to collect data for the study.

3.5.1 Primary Data

The primary data was obtained from respondents using self administered

questionnaires and interviews.

3.5.2 Secondary Data Secondary data was also heavily relied upon because of the nature of analysis that

was undertaken. Secondary data was collected from previous studies on SMEs,

documents and journals from UMA, URA, libraries of MFPED, MUBS and World

Bank. Other sources consisted of Electronic Journals, Government Publications,

Periodicals, Internet searched material and other published literature.

3.6 Data Collection Instruments Questionnaire

A self – administered, structured questionnaire was used. The questions in the

questionnaires were close-ended. These were rated using a 5 – point Likert Scale of

strongly agree(5), agree(4), uncertain(3), disagree(2) and strongly disagree(1). The

questionnaire was divided into major sections to address specifically every variable in the

model. These included; Background Information, Managerial Competencies, Credit

Accessibility and Business Success.

22

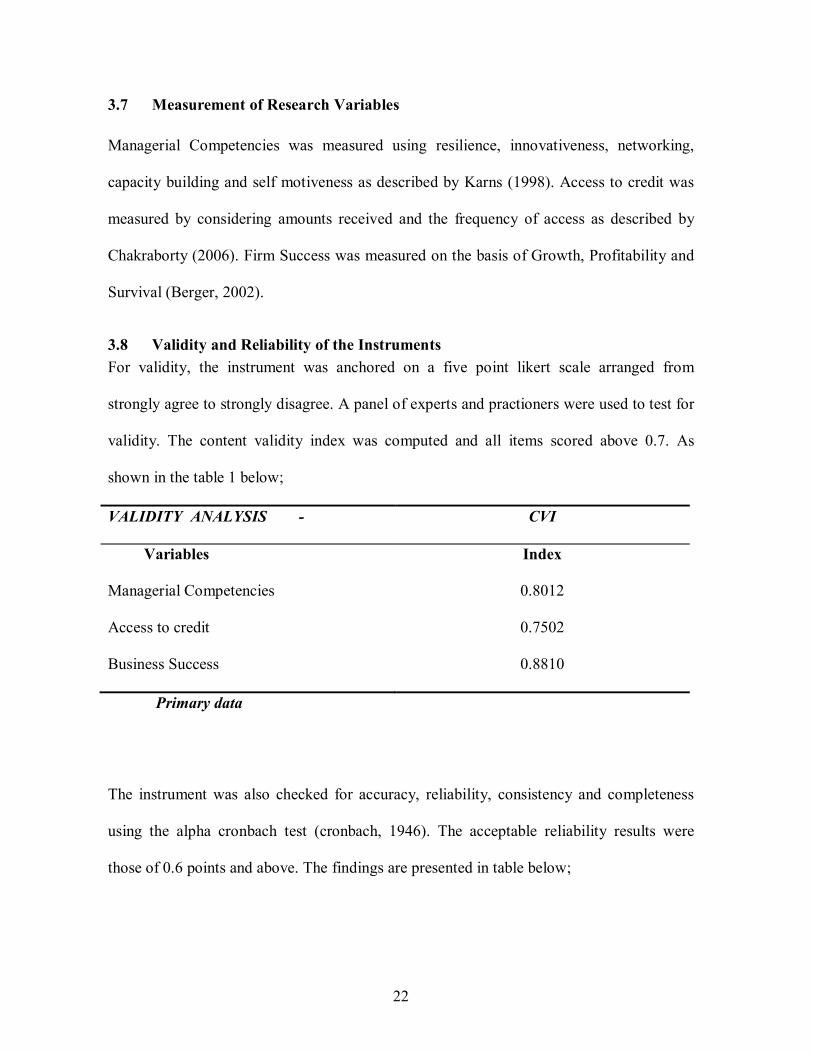

3.7 Measurement of Research Variables Managerial Competencies was measured using resilience, innovativeness, networking,

capacity building and self motiveness as described by Karns (1998). Access to credit was

measured by considering amounts received and the frequency of access as described by

Chakraborty (2006). Firm Success was measured on the basis of Growth, Profitability and

Survival (Berger, 2002).

3.8 Validity and Reliability of the Instruments For validity, the instrument was anchored on a five point likert scale arranged from

strongly agree to strongly disagree. A panel of experts and practioners were used to test for

validity. The content validity index was computed and all items scored above 0.7. As

shown in the table 1 below;

VALIDITY ANALYSIS - CVI

Variables Index

Managerial Competencies 0.8012

Access to credit 0.7502

Business Success 0.8810

Primary data

The instrument was also checked for accuracy, reliability, consistency and completeness

using the alpha cronbach test (cronbach, 1946). The acceptable reliability results were

those of 0.6 points and above. The findings are presented in table below;

23

Table 1: Reliability Coefficients RELIABILITY ANALYSIS - SCALE ( ALPHA )

Variables Alpha

Managerial Competencies 0.8021

Access to credit 0.7611

Business Success 0.8710

Primary Data

Since the Alpha coefficients for all the study variables were above 0.60 as indicated

in table 1 above, this implied that the scales used to measure the study variables were

consistent and therefore reliable. Hence meeting acceptance standards for the research and

reflecting a similarity in the research as sighted by Kanyerezi Kenneth (2006) – MHRM –

Makerere University and Nunnally (1978).

3.9 Data Processing and Analysis Data collected in the field was computerized, sorted, edited, classified and coded.

The cleaned data was summarized and converted into frequencies and percentages us. The

data collected was analyzed to examine the managerial competencies, access to credit and

business success using the Statistical Package for Social Scientists (SPSS).

Pearson’s Correlation Coefficients were run to examine the relationship among the

study variables which were set out in the objectives of this study while the relationship

between managerial competencies, access to credit and business success was determined

using multiple regressions.

24

3.10 Limitations to the Study The researcher did encounter the following constraints:

a) The study was affected by non – response from some of the Small and

Medium Enterprises contacted. Respondents here did view the required

information as private.

b) Constrained resources in terms of funds and time were encountered. These

were compressed by utilizing the only available resources at hand.

c) In some instances, respondents did demand for money before they could

respond. This was overcome by convincing the affected respondents that the

study was purely academic and not for economic purposes whatsoever.

d) Some employees posed themselves as the managers and / or owners whereas

not and as such they did not readily provide all data asked in the

questionnaire. The researcher made effort to have post survey tests

especially towards the SMEs’ where earlier data was suspected.

Despite these limitations, the researcher believes that the findings of this

study will be useful in filling the knowledge gap that the study set out to fill.

25

CHAPTER FOUR

DATA PRESENTATION AND ANALYSIS OF FINDINGS

4.1 Introduction

This chapter presents results relating to sample characteristics, the factor structure of

managerial competencies, relationships between study variables and the prediction model

of business success.

4.2 Demographic Features

The demographic features of the respondents / general information in the study included

the gender, the age, the level of education and how long their businesses had been in

existence. This information is vital to the study since such education levels, registration of

the businesses, number of employees in the business and the business existences are related

to entrepreneurship (GEM Report, 2004).

4.2.1 Gender of the Respondents The findings as reflected in table 2 showed that most of the respondents were male

representing 73.6% and the female representing 26.4%. This implies that there was a

greater positive male response rate representation of respondents in terms of gender

compared to the female. Details are presented in Table 2;

Table 2: Gender of respondents Frequency Percent ( % ) Male 109 73.6

Female 39 26.4 Total 148 100.0

26

4.2.2 Legal status of the enterprise

Figure 2 shows that 48% of the enterprises were limited liabilities while 46% were sole

proprietorship. The remaining 7% were partnerships.

Figure 2 : Legal status of the enterprise 4.2.3 Positions held by the Respondents.

Table 3 shows that as regards ownership of the SMEs, 33.1% were owner managers while

66.9% were mere employees of the firms. Inclusive in the general managers, 11.5% were

part of the owner management team while 88.5% were just employed by the firm. Other

respondents who were employed by these SMEs included accountants 25.7%, operations

managers 7.4% and 3.4% were other categories.

Table 3: Category of the positions held by the respondents in the SMEs

Frequency Percent ( % ) General Manager 30 20.3 Owner mangers 49 33.1 Accountant 38 25.7 Operations Manager 11 7.4 Chief Administrators 15 10.1 Others 5 3.4 Total 148 100

Partnership7%

Limited Liability48%

Sole Proprietorship45%

Partnership

Limited LiabilitySole Proprietorship

27

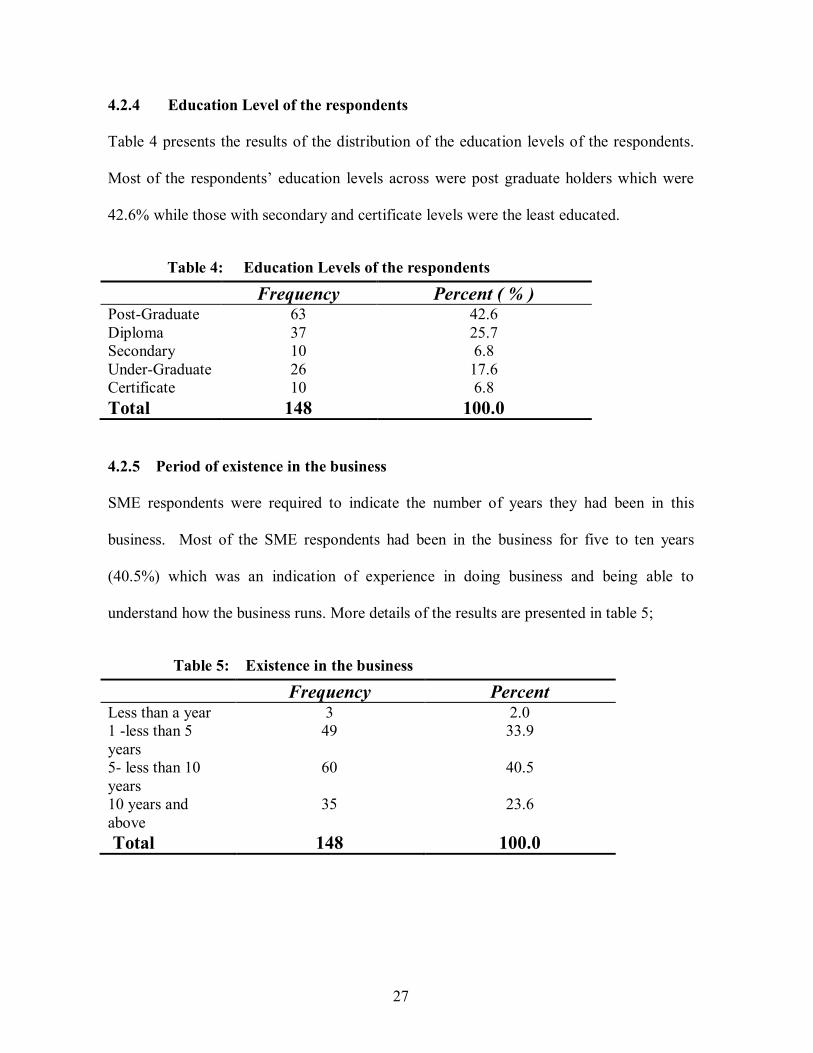

4.2.4 Education Level of the respondents

Table 4 presents the results of the distribution of the education levels of the respondents.

Most of the respondents’ education levels across were post graduate holders which were

42.6% while those with secondary and certificate levels were the least educated.

Table 4: Education Levels of the respondents

Frequency Percent ( % ) Post-Graduate 63 42.6 Diploma 37 25.7 Secondary 10 6.8 Under-Graduate 26 17.6 Certificate 10 6.8 Total 148 100.0

4.2.5 Period of existence in the business

SME respondents were required to indicate the number of years they had been in this

business. Most of the SME respondents had been in the business for five to ten years

(40.5%) which was an indication of experience in doing business and being able to

understand how the business runs. More details of the results are presented in table 5;

Table 5: Existence in the business

Frequency Percent Less than a year 3 2.0 1 -less than 5 years

49 33.9

5- less than 10 years

60 40.5

10 years and above

35 23.6

Total 148 100.0

28

4.2.6 The kind of business the firm is engaged in

Table 6 presents results of the kind of businesses the various SMEs are engaged in. Nearly

half of the businesses were dealing in general trading (52.7%) while the least were engaged

in bakery products (1.4%).

Table 6: Kind of business the firm is engaged in

Frequency Percent ( % ) General Trading 78 52.7 Agriculture Trading 7 4.7 Metal Fabrication 10 6.8 Carpentry 7 4.7 Bakery products 2 1.4 Others 44 29.1 Total 148 100.0

4.3 Rotated Component Factor Analysis The rotated factor analysis was run to examine the factor structure of managerial

competencies and to validate the item scales used to measure the construct. The unraveled

underlying dimensions were used as input variables for Pearson correlation analysis and

Regression analysis. The study used principal component analysis with varimax rotation.

The rotation converged in 15 iterations producing 10 factors explaining 43% of the

variance in managerial competencies. The factor analysis results are summarized in table 7

below;

29

Table 7: Factor Analysis for managerial competencies

Item Component Capacity

building

Independence

Networkin

g

Enterprisin

g

Innovative/ creative

Commitment

Resilience

Transparence

Monitoring and control

Self motivated

Provides mutual support and a mentoring environment to his/her employees

.67

Is in a position of training his employees in skill development

.65

S(he) looks after his employees by paying them their salaries and providing for them essential commodities

.63

S(he) trains his/her employees to acquire the necessary skills needed to perform their duties

.62

S(he) is honest and treats his employees well .61 S(he) pays the salaries of his/her employees promptly

.59

Services his loans promptly .58 S(he) does not fear to take financial risks by acquiring bank loans

.56

Holds regular shop-floor meetings .48 S(he) should be in position of paying his workers well

.46

S(he) establishes and maintains good working relationships with his customers and bankers

.44

S(he) often advertises his products to the public

.42

Be able to conduct a market research related to the business

.34

S(he) likes depending on his own ideas and rarely consults others in business

.74

S(he) has a strong desire to be independent and to take his own decision without consulting

.71

Offers his products at a cheap price compared to other competitors in the same field

.64

S(he) produces quality goods at a cheap price .62 Rewards his customers every end of the month

.61

Gives back to his customers in terms of gifts and lotteries

.58

Consults and gets external information from suppliers, buyers and competitors

.26

Possesses computer skills .52 S(he) is creative and likes sharing ideas with his fellow managers. Uses various techniques of out competing his rivals

.52

Listens to customer complaints in his business .50 S(he) has contacts with other managers .49 Is trustworthy in his/her dealings with the customers

.42

S(he) possesses management skills and these have enables his business to survive

.39

Is always in position to organize and deliver business initiatives leading to business success

.37

S(he) knows which labour to use, either human beings or machinery, after conducting

.62

30

a feasibility study of his business S(he) believes in competing with other similar businesses

.55

S(he) allows good ideas to work for him and improve his business

.55

Has the capacity of accessing monetory and financial resources

.44

Appreciates customers whenever they buy from him

.35

Keeps himself up-to-date with the knowledge required to perform his duties

.60

Keeps records of all the transactions made in the business

.58

Demonstrates self confidence by getting involved in the areas he is good at

.53

Possesses skills to enable him/her perform at high capacity

.47

S(he) knows whether his business is growing or stagnant by focusing on the amount of stock available and profits made

.45

Maintains sufficient materials and skills to perform his duties

.44

S(he) is organized; utilizes his time as efficiently as possible

.60

S(he) knows what he is good at and what his weaknesses are

.53

S(he) is self motivated and committed to his business

.50

Gives customers enough attention .40 S(he) should be growth oriented .34 S(he) always invents new ways of doing his business

.22

Has the ability to persevere in good and bad times

.58

Maintains a close relationship with his employees and customers

.51

S(he) knows the available markets and their conditions; he identifies the most competitive market

.49

S(he) has a positive attitude towards his work; he enjoys his work and has interest in it

.39

S(he) comes early for work and leaves very late after accomplishing all the tasks

.37

Is a persistent person who is able to take on challenging work

-.36

Explains to the employees the budget performance

.52

Take corrective action where there is evidence of deviation

.51

Determines stock levels of inputs .49 Honors his business commitments and appointments

-.45

S(he) comes up with a unique idea and his creativity transforms an existing product into a better product

.60

Establishes performance standards .48 S(he) displays leadership qualities such as the ability to guide people in achieving the set goals

.40

Has a high desire to achieve business success by using available funds to make more profits and increased production

.39

31

Takes corrective action where there is evidence of deviation

.55

S(he) knows the information necessary to up-date production technologies

-.53

S(he) raises enough funds to provide working equipment for his employees

.40

Eigen Values 7.2 3.6 2.8 2.4 2.1 2.1 2.0 1.8 1.8 1.7 Percentage of Variance explained 7.9 6.4 4.0 3.9 3.6 3.6 3.5 3.4 3.3 3.0 Cumulative percentage of variance 8 14 18 22 26 29 33 36 40 43 Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization

a. Rotation converged in 15 iterations.

Table 7 indicates the underlying managerial competencies according to the data

obtained from the respondents, which are grouped into ten sub – components with

percentage of variance explained on each one of them. These are: capacity building,

independence, networking, enterprising, innovative/creative, commitment, resilience, open

minded, monitoring and control and self motivation. These explained 43% of the variance

in managerial competencies implying that managerial competencies in SMEs were below

average. The 57% could be attributed to other factors which are outside the scope of the

study.

The first component referred to as capacity building specifically focuses at

investing in new ways of doing things in the business, maintaining close relationship with

employees and customers, identifying most competitive markets and demonstrating interest

in the job. This explained 7.9% of the variance in managerial competencies.

This was followed by the second component of Independence which explained

6.4% of the variance. This component brings together items that indicate capacity to make

independent decisions that are key to managerial competence. This competence suggests

that a manager may need to depend on his ideas, take his own decisions with out consulting

and always take decisions to make quality products.

32

The third component was networking which explained 4.0% of the variance. This

component indicates that a manager should have capacity to network with others. This is

manifested in sharing ideas with his fellow managers, using various techniques of out

competing his rivals, listing to customer complaints, wide networks, and capacity to

organize and deliver business initiatives

The fourth component is about enterprising. This indicates that a good manager

must know which model of operations to use; labour intensive or capital intensive, belief in

competing with others, allowing good ideas to work with him and improve his business,

capacity to access monetary and financial resources, good management skills, and

appreciation of customers. This explained 3.9% of the variance in managerial

competencies.

The Fifth component brings items that suggest that innovative/creativeness is the

key competence for management. This is manifested through activities like, Keeps himself

up-to-date with the knowledge required to perform his duties, Keeps records of all the

transactions made in the business, Demonstrates self confidence by getting involved in the

areas he is good at, Possesses skills to enable him/her perform at high capacity, knows

whether his business is growing or stagnant by focusing on the amount of stock available

and profits made and Maintains sufficient materials and skills to perform his duties. This

explained 3.6% of the variance in managerial competencies.

Next in line was the component of commitment that explained 3.6% of the variance.

This component indicates that a manager must be committed to the objectives and goals of

the organization. This is manifested through items like utilizing all his time as efficiently as

33

possible, self motivation and commitment to the business, giving attention to customers,

focusing on growth orientation of the business and investing in new ways of doing things

The seventh component was resilience which explained 3.5% of the variance in

managerial competencies. Resilience which is the ability to bounce back from undesirable

situations was portrayed by the items like ability to persevere in good and bad times,

surviving in competitive market, having positive attitude towards work; coming early for

work and leaves very late after accomplishing all the tasks and persistence in all activities

and able to take on challenging work

Lastly; components eight, nine and ten suggest that transparence, monitoring and

control and self drive respectively are key competencies of competent Managers. These

components explained 3.4%, 3.3% and 3.0% of the variance in managerial competencies

respectively. Transparence was defined by items like explaining to the employees the

budget performance, taking corrective action where there was evidence of deviation,

determining stock levels of inputs and honoring business commitments and appointments.

Monitoring and control was defined with behaviors like establishing performance

standards, displaying leadership qualities such as the ability to guide people in achieving

the set goals and desire to achieve business success by using available funds to make more

profits and increased production coupled with keeping to promises at all the time and self

drive was defined by behaviors like taking actions where there is evidence of deviation,

searching for relevant information and design strategies to raise enough funds to provide

working equipments for his employees .

34

4.4 Correlations

Correlation analysis measures the degree of relationship between two or more

variables. Correlation analysis was done to determine the relationship between each of the

independent variables that is; managerial competencies and access to credit and the

dependent variable; business success.

Pearson Correlation Analysis

The Pearson’s correlation coefficient was computed to measure the degree of

relationships between the study variables as per the objectives. The study objectives were:

I. To establish the relationship between managerial competencies and business

success of SMEs’ in Uganda

II. To investigate the relationship between credit accessibility and business success of

SMEs in Uganda

III. To examine the relationship between managerial competencies, access to credit and

success of the SMEs’ in Uganda.

Below are the results of the pearson correlation moment;

35

Table 8: Results of the Pearson Correlation Moment

Variables 1 2 3 4 5 6 7 8 9 10 11 12 13 Independency 1.00 Capacity Building .22** 1.00

Networking 0.06 0.15 1.00

Enterprising 0.12 0.07 0.11 1.00

Innovative/creative 0.11 .246**

0.12 0.11 1.00

Commitment 0.02 .171*

.183*

0.14 -0.1 1.00

Resilience .162* .300**

.215**

0.13 0.058 0.06 1.00

Open minded .260*

* .387

** 0.14 0.11 0.128 0.14 0.15 1.00

Monitoring & control 0.15 .287**

0.14 0.15 0.042 0.09 0.04 0.09 1.00

Self motivated 0.14 0.09 .179*

.241**

0.057 0.1 0.1 .264*

* 0.04 1.00

Managerial competence .53** .64*

* .481

** .412

** .331

** .340*

* .453*

* .607*

* .452*

* .448*

* 1.00

Access to credit -0.07 .440**

0.1 0.15 0.12 0.11 0.07 0.14 0.03 0.06 .233*

* 1.0

0 Business success .271*

* .383

** .276

** .237

** 0.142 .221*

* .17* .26** 0.15 0.16 .48** .34

** 1.00

**. Correlation is significant at the 0.01 level (2-tailed). *. Correlation is significant at the 0.05 level (2-tailed).

36

4.4.1 Relationship between managerial competencies and business success

Table 8 shows that there was a significant positive relationship between managerial

competencies and business success (r = .48, p <.01). This implies that existence of

managerial competencies in the business will result into business success and lack of

managerial competencies results into failure of the business. Table 8 further indicates that

seven of the components of the managerial competencies relate positively with business

success although three of the components in the relationship were not significant. These

insignificant components were: monitoring & control (r = .15, p > 0.05), creativeness (r =

.14, p > 0.05) and self motivated (r = .16, p > 0.05). The other components that relate

positively with business success were: Independence; (r = .27, p < 0.01), Capacity building

(r = .38, p < 0.01), net working (r = .28, p < 0.01), enterprising (r = .24, p < 0.01),

commitment (r = .22, p < 0.01), resilience (r = .17, p < 0.05) and transparence (r = .26, p <

0.01). This implies that possession of the above competencies improves business success.

4.4.2 Relationship between credit accessibility and business success

Table 8 indicates a significant positive relationship between credit accessibility and

business success (r =.34; p < 0.01). This implies that credit accessibility influences business

success with companies that can easily access credit from money lending institutions hence

succeeding more than those that can not get access to credit.

4.4.3 Relationship between Managerial Competencies and Access to Credit

Table 8 further shows that there was a positive significant relationship between managerial

competencies and Access to credit (r =.23; p < 0.01). This implies that more competent

37

managers can easily access credit than less competent managers. It is further revealed that

only one component of the managerial competence that is; capacity building is positively

related with access to credit (r =.44; p < 0.01). This implies that increase in capacity

building results into increase in access to credit. Independence component relates

negatively to access to credit (r =.-0.07; p > 0.05). This finding tends to suggest that

independent minded managers may find it difficult to access credit from money lending

institutions. These managerial competencies relate insignificantly positive to access to

credit. These include: Net working (r = .12; p > 0.05), enterprising (r = .15; p > 0.05),

innovative/creativeness (r = .12; p > 0.05), commitment (r = .11; p > 0. 05), resilience (r =

.07; p > 0.05), transparence (r = .14; p > 0.05), monitoring and control (r = .03; p < 0. 01)

and self motivated (r = .06; p < 0.01).

38

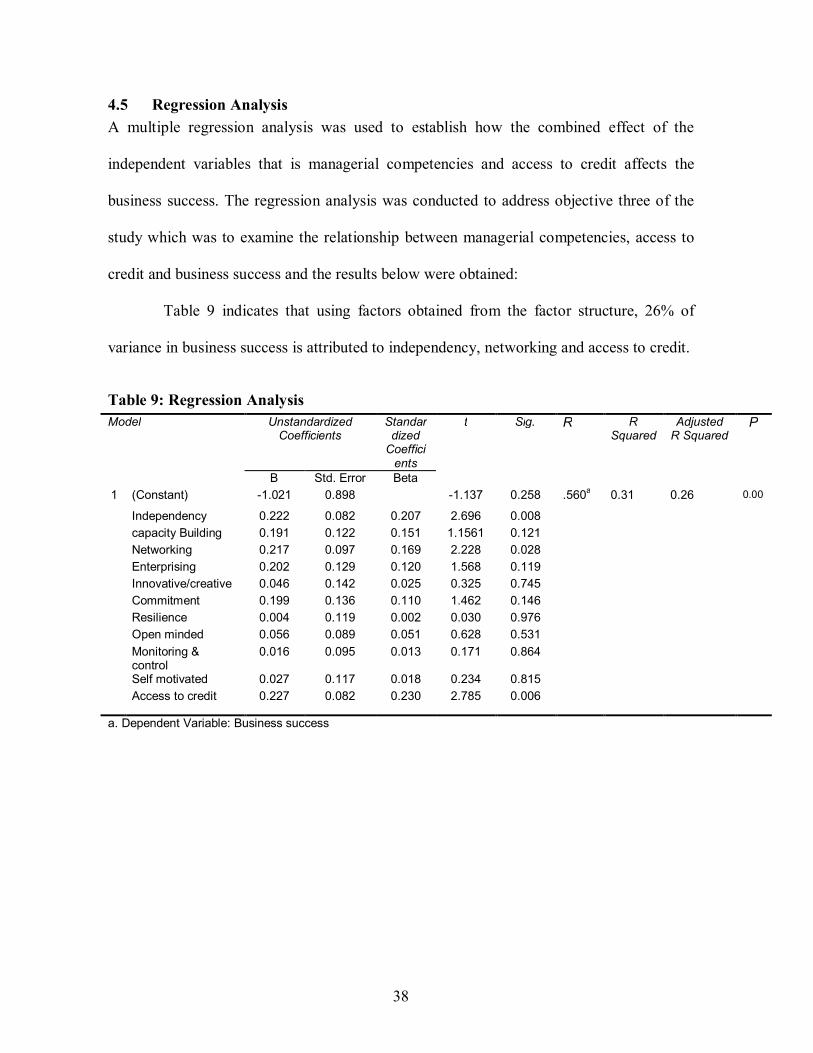

4.5 Regression Analysis A multiple regression analysis was used to establish how the combined effect of the

independent variables that is managerial competencies and access to credit affects the

business success. The regression analysis was conducted to address objective three of the

study which was to examine the relationship between managerial competencies, access to

credit and business success and the results below were obtained:

Table 9 indicates that using factors obtained from the factor structure, 26% of

variance in business success is attributed to independency, networking and access to credit.

Table 9: Regression Analysis Model Unstandardized

Coefficients Standardized

Coefficients

t Sig. R R Squared

Adjusted R Squared

P

B Std. Error Beta 1 (Constant) -1.021 0.898 -1.137 0.258 .560a 0.31 0.26 0.00

Independency 0.222 0.082 0.207 2.696 0.008 capacity Building 0.191 0.122 0.151 1.1561 0.121 Networking 0.217 0.097 0.169 2.228 0.028 Enterprising 0.202 0.129 0.120 1.568 0.119 Innovative/creative 0.046 0.142 0.025 0.325 0.745 Commitment 0.199 0.136 0.110 1.462 0.146 Resilience 0.004 0.119 0.002 0.030 0.976 Open minded 0.056 0.089 0.051 0.628 0.531 Monitoring & control

0.016 0.095 0.013 0.171 0.864

Self motivated 0.027 0.117 0.018 0.234 0.815 Access to credit 0.227 0.082 0.230 2.785 0.006

a. Dependent Variable: Business success

39

4.6 Combined Regression Analysis The combined regression analysis in table 10 below shows that managerial competencies

(Beta = 0.425, P < 0.01) and access to credit (Beta = 0.242, P < 0.01) are significant

predictors of business success accounting for 27.7% of the variance.

Table 10: Combined Regression Analysis Model Unstandardized

Coefficients Standardiz

ed Coefficients

t Sig. R R- Squared

Adjusted R

Squared

P

1 (Constant) -1.28 0.696 -1.84 0.07 .536a 0.287 0.277 0.00

Managerial competencies

1.219 0.207 0.425 5.90 0.00

Access to credit

0.239 0.071 0.242 3.36 0.00

a. Dependent Variable: Business success

40

4.7 Other Findings

Analysis of Variance (ANOVA) We used ANOVA to establish the relationship between the study variables and the demographic

characteristics of the study sample. The demographic characteristics included: Gender, Education

qualification, position, legal status and kind of business.

Below we present the findings for each;

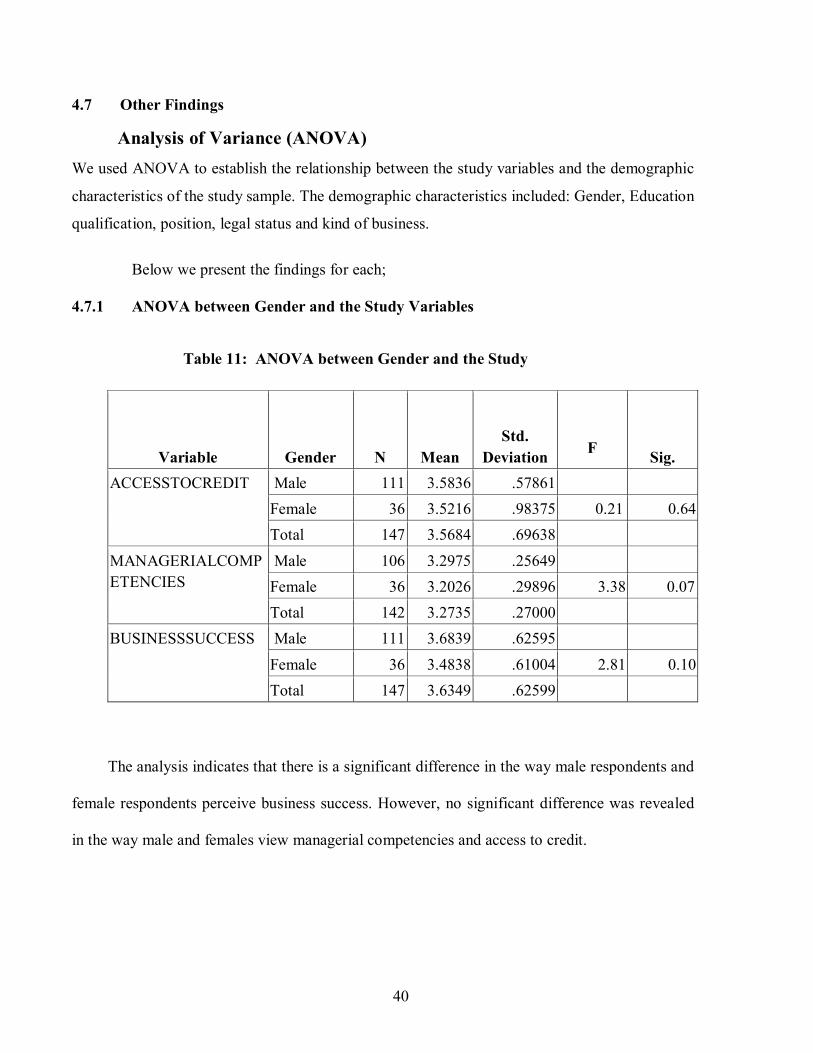

4.7.1 ANOVA between Gender and the Study Variables

Table 11: ANOVA between Gender and the Study

Variable

Gender N Mean Std.

Deviation

F Sig. ACCESSTOCREDIT Male 111 3.5836 .57861

Female 36 3.5216 .98375 0.21 0.64 Total 147 3.5684 .69638

MANAGERIALCOMPETENCIES

Male 106 3.2975 .25649 Female 36 3.2026 .29896 3.38 0.07 Total 142 3.2735 .27000

BUSINESSSUCCESS Male 111 3.6839 .62595 Female 36 3.4838 .61004 2.81 0.10 Total 147 3.6349 .62599

The analysis indicates that there is a significant difference in the way male respondents and

female respondents perceive business success. However, no significant difference was revealed

in the way male and females view managerial competencies and access to credit.

41

4.7.2 ANOVA between Legal Status and the Study Variables

Table 12: ANOVA between Legal Status and the Study

N Mean Std.

Deviation F

Variable Legal Status Sig.

ACCESSTOCREDIT Partnership 13 3.7009 .53168

Limited Liability 62 3.6738 .65468 1.95 0.15

Sole Proprietorship

72 3.4537 .74495

Total 147 3.5684 .69638

MANAGERIALCOMPETENCIES

Partnership 13 3.3503 .22410

Limited Liability 59 3.2970 .25927 1.32 0.27

Sole Proprietorship

70 3.2393 .28453

Total 142 3.2735 .27000

BUSINESSSUCCESS Partnership 13 3.8718 .74661

Limited Liability 62 3.7151 .57943 2.65 0.07

Sole Proprietorship

72 3.5231 .62818

Total 147 3.6349 .62599

The analysis revealed a significant difference in the way respondents from businesses with

different legal status perceived business success and access to credit. Respondents from

partnership enterprises indicated that it was easier to access the credit, followed by limited

liability enterprises and then sole proprietorships. The results also indicate that Partnership

businesses succeed more in the field than the limited liability businesses and then the sole

proprietorship.

42

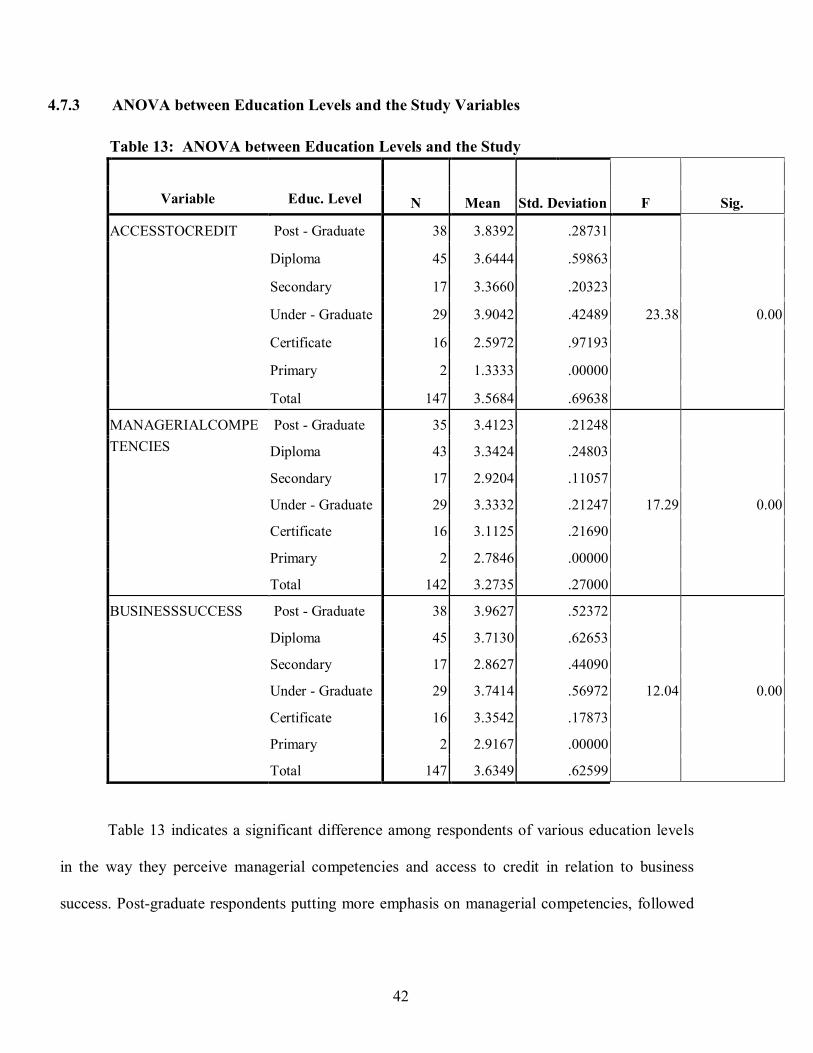

4.7.3 ANOVA between Education Levels and the Study Variables

Table 13: ANOVA between Education Levels and the Study

N Mean Std. Deviation F

Variable Educ. Level Sig.

ACCESSTOCREDIT Post - Graduate 38 3.8392 .28731

Diploma 45 3.6444 .59863

Secondary 17 3.3660 .20323

Under - Graduate 29 3.9042 .42489 23.38 0.00

Certificate 16 2.5972 .97193

Primary 2 1.3333 .00000

Total 147 3.5684 .69638

MANAGERIALCOMPETENCIES

Post - Graduate 35 3.4123 .21248

Diploma 43 3.3424 .24803

Secondary 17 2.9204 .11057

Under - Graduate 29 3.3332 .21247 17.29 0.00

Certificate 16 3.1125 .21690

Primary 2 2.7846 .00000

Total 142 3.2735 .27000

BUSINESSSUCCESS Post - Graduate 38 3.9627 .52372

Diploma 45 3.7130 .62653

Secondary 17 2.8627 .44090

Under - Graduate 29 3.7414 .56972 12.04 0.00

Certificate 16 3.3542 .17873

Primary 2 2.9167 .00000

Total 147 3.6349 .62599

Table 13 indicates a significant difference among respondents of various education levels

in the way they perceive managerial competencies and access to credit in relation to business

success. Post-graduate respondents putting more emphasis on managerial competencies, followed

43

by the diplomas, under-graduates, certificate holders, secondary and the primary graduates come

last.

On the other hand, Undergraduates put more emphasis on access to credit, followed by post

graduate, diploma, secondary, certificate and primary come last. The study further showed post

graduates as more successful in business, followed by undergraduates, diploma holders,

certificates, primary and the secondary holders come last.

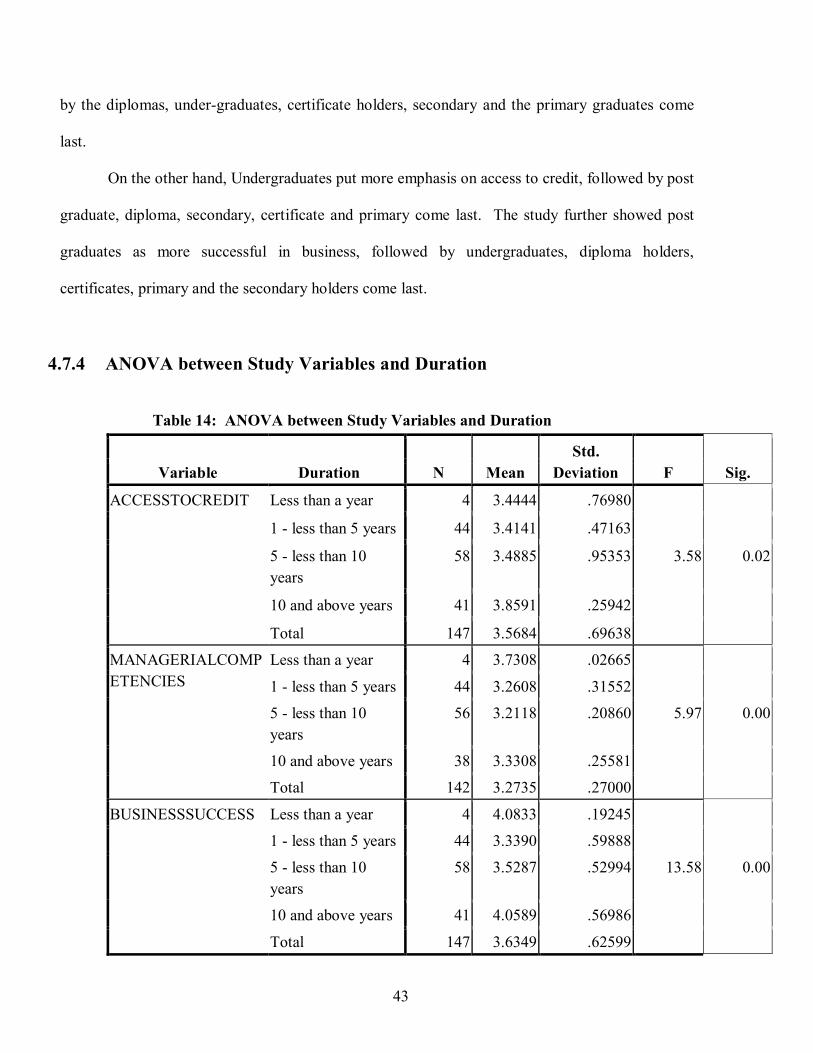

4.7.4 ANOVA between Study Variables and Duration

Table 14: ANOVA between Study Variables and Duration

N Mean

Std. Deviation F Sig. Variable Duration

ACCESSTOCREDIT Less than a year 4 3.4444 .76980

1 - less than 5 years 44 3.4141 .47163

5 - less than 10 years

58 3.4885 .95353 3.58 0.02

10 and above years 41 3.8591 .25942

Total 147 3.5684 .69638 MANAGERIALCOMPETENCIES

Less than a year 4 3.7308 .02665 1 - less than 5 years 44 3.2608 .31552 5 - less than 10 years

56 3.2118 .20860 5.97 0.00

10 and above years 38 3.3308 .25581 Total 142 3.2735 .27000

BUSINESSSUCCESS Less than a year 4 4.0833 .19245 1 - less than 5 years 44 3.3390 .59888 5 - less than 10 years

58 3.5287 .52994 13.58 0.00

10 and above years 41 4.0589 .56986 Total 147 3.6349 .62599

44

Table 14 indicates a significant difference in the way period of existence affects

the business success with businesses that have been in existence for less than a year and 10

years and above registering a higher mean, followed by 5 years but less than 10 years and

those between 1 and 5 years registering the lowest mean.

45

CHAPTER FIVE

DISCUSSION, RECOMMENDATIONS AND CONCLUSION

5.0 Introduction This chapter presents the discussions on the findings in chapter four. This is followed

by conclusions and further recommendations. The presentation of the discussion is in

line with the objectives of the study. The first part examines the relationship between

managerial competencies and business success. Second is the investigation of the

relationship between credit accessibility and business success. Third is the investigation

into the relationship between managerial competencies, access to credit and business