Macroeconomic outlook and Food & Beverage Outlook 2016 15 October 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Macroeconomic outlook

and Food & Beverage Outlook 2016

15 October 2015

Agenda

• Macroeconomic outlook

• Food and Beverage outlook

2

Key determinants for business environment in 2016

3

1. Global economic recovery

2. China’s economic slowdown

3. Fed’s first rate hike

4. Low commodity prices

1. Export concerns

2. Consumption drag

3. Infra megaproject investment

4. Strong tourism growth

Global outlook Domestic outlook

Higher growth in 2016, except for China

4

Japan

China

Eurozone

Thailand U.S.

2.4 2.2 2.8

2014 2015F 2016F

0.9 1.5

2.0

2014 2015F 2016F

7.4 6.9 6.8

2014 2015F 2016F

0.9 2.2

3.0

2014 2015F 2016F

-0.1

0.9 1.6

2014 2015F 2016F

Source: EIC, IMF, Bloomberg and forecasts of major research houses (Goldman Sachs, J.P. Morgan, Deutsche Bank, Bank of America)

With slowdown in China’s investment, commodity prices will remain low

5

0

5

10

15

20

25

30

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Total

Real estate

Unit: %YOY of China’s fixed asset investment

Source: EIC analysis based on data from CEIC and EIA

20

40

60

80

100

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Crude oil

Sugar

Rubber

Rice

Unit: Index (June 2014=100)

The low commodity prices will continue to hold back Thailand’s households’ consumption spending

6

Source: EIC analysis based on data from Bank of Thailand, Office of Industrial Economics

50

60

70

80

90

100

110

120

Jan-1

3

Mar-

13

May-1

3

Jul-13

Sep-1

3

Nov-1

3

Jan-1

4

Mar-

14

May-1

4

Jul-14

Sep-1

4

Nov-1

4

Jan-1

5

Mar-

15

May-1

5

Jul-15

PCI PCI - nondurable PCI - durable

70

80

90

100

110

120

130

140

Jan-1

3

Mar-

13

May-1

3

Jul-13

Sep-1

3

Nov-1

3

Jan-1

4

Mar-

14

May-1

4

Jul-14

Sep-1

4

Nov-1

4

Jan-1

5

Mar-

15

May-1

5

Real non-farm wage Real farm income

Private Consumption Index (BOT) SA Index: Jan13 = 100 Unit: Index Jan 2013 = 100, 3MMA SA

Non-Farm Wage and Farm Income

Overall business environment for 2016 will be slightly better than this year

7

Private investment

Household consumption

• Public investment

• Sentiment

• Capacity utilization rate

• Farm income

• Household debt

Export

• External demand

• Commodity prices

• Exchange rate: THB/USD

Fails to pick up

Suppressed

Shrinking

Small recovery

No change

Stabilizing

• Shrinking

• Falling

• Weaker THB helps export

• Infra megaprojects to start

• Recovers

• Rising

• Falling commodities income amid severe drought

• High

• Stabilizing

• Stabilizing

• Weaker THB helps export

• Low commodities income with potential drought

• Remains high

• Delays in disbursement

• Deteriorates

• Remains low

Key economic factors 2015 2016

1

2

3

Source: EIC analysis

8

EIC’s baseline economic forecasts

1 %YOY except for policy rate (% per annum) and exchange rate (THB/USD). Source: EIC analysis as of September 2015 based on data from the MoC, the BoT, the NESDB, AIMC, Thai BMA and TFIIC

Comments and Outlook Estimates (%)1

Key drivers

GDP growth (%YOY)

Policy rate (end period)

Export growth (in USD)

THB/USD (end period)

2015F

2.0-2.5

1.50

-4.7 7MYOY

2014A

Weak domestic consumption and investment continue to hold down growth. Sentiment should improve as gov’t project s get going in 2016.

The main culprits are the depressed commodity prices and out-of-date technology products. Weaknesses from China also hurt exports.

BOT is likely to be very cautious against the prospect of volatile capital flows, making further aggressive move on rate unlikely.

With China and other regional players depreciating their currencies, THB will be allowed to weaken further.

2015A

1.50

36

0.9

-0.4

2.00

33.0

2016F

2.5-3.0

0-2

1.50

37

2.9 6MYOY

(-4.5)-(-5)

36

Agenda

• Macroeconomic outlook

• Food and Beverage outlook

9

10

4.7% 5.9%

3.2%

2016f

1.31

2015e

1.24

2014

1.18

2013

1.16

2012

1.13

+19%

+20%

2016f

399

72%

17%

11%

2015e

337

72%

17%

11%

2014

287

73%

17%

11%

2013

204

78%

10%

12%

2012

203

77%

11%

12%

2011

172

77%

11% 13%

2010

138

77%

11% 12%

Food +18%

Dairy +28%

Beverage +17% +6%

+5%

2016f

634

47%

33%

20%

2015e

597

46%

35%

19%

2014

562

45%

37%

18%

2013

533

45%

39%

16%

2012

568

42%

44%

15%

2011

534

41%

46%

13%

2010

464

39%

47%

13%

Other F&B +9% Meat +13%

Seafood -1%

Domestic F&B value

Unit: THB trillion

F&B import value

Unit: THB billion

F&B export value

Unit: THB billion

Domestic consumption, import and export will perform better than this year

Source: EIC analysis based on data from BMI and NFI

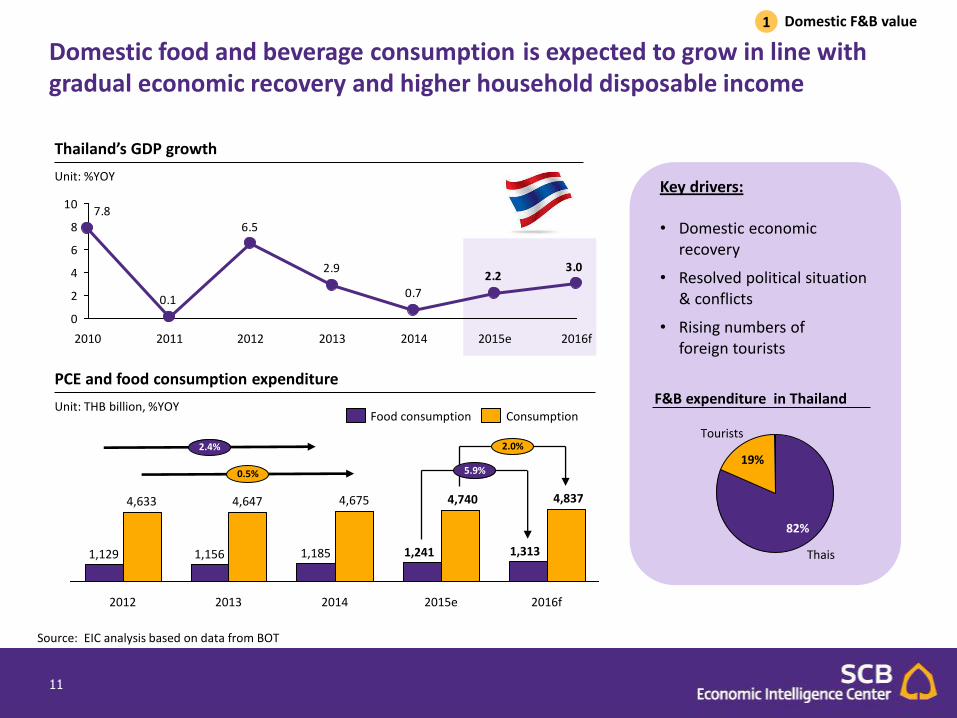

11

Thailand’s GDP growth

Unit: %YOY

Domestic food and beverage consumption is expected to grow in line with gradual economic recovery and higher household disposable income

0.7

2.9

6.5

0.1

7.8

3.02.2

0

2

4

6

8

10

2016f 2015e 2014 2013 2012 2011 2010

PCE and food consumption expenditure

Unit: THB billion, %YOY

2012

4,633

1,129

2014

4,675

1,185

2013

4,647

1,156

2.0%

5.9%

2.4%

0.5%

2016f

4,837

1,313

2015e

4,740

1,241

Consumption Food consumption

Domestic F&B value 1

Key drivers: • Domestic economic

recovery

• Resolved political situation & conflicts

• Rising numbers of foreign tourists

82%

19%

Tourists

Thais

F&B expenditure in Thailand

Source: EIC analysis based on data from BOT

12

Disposable income of Thai households is likely to move up the bracket in tandem with better economic growth

25%

75%

F&B spending

Others

Household spending by category

Number of households by disposable income bracket 2005, 2010, 2016

Unit: ‘000 households

Source: EIC analysis based on data from Euromonitor

Domestic F&B value 1

13

4.5

3.6

3.0

2.9

4.0

3.3

2.1

5.3

3.4

4.7

3.7

2.4

6.6

3.9

4.5

3.5

3.6

5.6

3.5

5.0

+24%

+12%

+14%

+19%

+21%

+13%

+16%

Snacks

+11%

Seasoning

Ready Meals

Pasta

Oils and Fats

Ice Cream

Dairy

Chilled Processed Food

Canned/Preserved Food

Bakery

2014-19 CAGR

2014-15

5.4

5.2

5.9

4.2

4.7

6.0

7.6

4.5+7%

Organic +15%

+29%

+15% Health & wellness

Functional

Naturally Healthy

2014-15

2014-19 CAGR

Rising urbanization and middle-income class will drive continued demand for processed food, RTE, RTD and health & wellness food in Thailand

Growth of packaged food sales in Thailand

Unit: %

Growth of health & wellness food sales in Thailand

Unit: %

Source: EIC analysis based on data from Euromonitor

Domestic F&B value 1

14

4%

Herb

2%

Meat

63% 15%

1%

Seasoning

0%

Seafood

1%

Fruit

Legumes

1%

Candy

Vegetable

Starchy products

8%

5%

Roots

Non-alcoholic beverage

2%

Hot drink 63%

Alcoholic beverage 35%

Source: EIC analysis based on data from NFI

Thailand’s food import value

Unit: billion THB

399

12%

72%

11%

337

17%

11%

2015e

17%

2016f

72%

17% 287

11%

2013

204

78%

10% 12%

2012

203

77%

11% 12%

2011

+19%

77%

11% 13%

2010

172

77%

11%

2014

73%

138

Dairy +28%

Food +18%

Beverage +17%

63% 15%

Vegetable

4%

1%

Herb

8%

Fruit

Legumes

5%

Seafood

1%

2%

Candy

Starchy products Meat

Seasoning

1%

0%

Roots

Non-alcoholic beverage

Alcoholic beverage

63%

35%

2%

Hot drink

Source: EIC analysis based on data from NFI

Import of F&B 2

Thailand’s key importing food items are seafood (tuna), diary products and beverages

15

Export of F&B 3

Thailand’s food export by main category

Unit: %

Other F&B export value

Unit: billion THB

12%

4%

Others

11%

Oceania

3%

US

Middle East

China

EU 12%

11% 12%

Africa

13%

22%

Japan

ASEAN

Other F&B

Seafood

45% 37%

18%

Meat

Thai food importer

Unit: %

21%

45%

19%

+8%

2013

10% 241

4%

41%

26%

19%

4%

11%

2012

237

44%

24%

251

2014

19%

25%

11% 3%

2010

46%

16%

44%

3%

15%

12%

26%

10%

182 3%

2011

219

Others

Dairy +17%

Fruit & Veg +9%

Starch +3%

Beverage +15%

ASEAN is our key destination for F&B products

Source: EIC analysis based on data from NFI

16

809

+6.9%

2020f

1,375

2012

2020f

7.7

25%

75%

2010

6.9

23%

77%

2000

6.1

21%

79%

Muslim +1.9% Non-muslim +1.0%

7.2 7.3

2017f 2010 2014 2011

6.9

2012 2015f

7.0 7.0

2016f

7.4 7.1

2013

7.4

+1%

2018f

7.5

Source: EIC analysis based on data from NFI, IMF, Trademap, UN and World Halal Summit Report

World population

Unit: Billion persons

Aging population

Unit: Million persons

Muslim population

Unit: Million persons

Export of F&B 3

Going forward, food and beverage serving Aging and Muslim population will have brighter prospects and bigger room to grow

17

-1

0

1

2

3

4

5

6

7

8

9

10

11

2014 2010 2018f

EU

EM

ASEAN-5

World MENA Japan

US China

46

77

52 49

78

54 52

79

56

DM EM World

+5%

+1%

+4%

2020f 2010 2015e

1317

31

2002 2011 2015e

-6%

* Poverty line = below USD 1.25 /day

EM and ASEAN-5 will become key potential markets for F&B consumption while urbanization trend will drive more demand for packaged and RTE food

GDP growth forecast

Unit: %YOY

Urban population

Unit: % of total

Population living below poverty line*

Unit: % of total

Source: EIC analysis based on data from IMF and UN

Export of F&B 3

18

51

118

2339

5

48

72

9

17

10

32

17

3

35

Milk Seafood Oil Sugar Starchy roots

Cereal exc. Beer

Meat Alcoholic beverages

Fruits Vegetables

2002 2014

844741

+3%

2018f 2013

442

336

+6%

2014 2019f

Growing protein intake will enhance global demand for meat, seafood and dairy products

Share of global dietary energy supply

Unit: % of total

Global meat and seafood market

Unit: USD billion

Global dairy market

Unit: USD billion

Source: EIC analysis based on data from Merrill Lynch

Meat consumption by type

Unit: Kilogram per capita

1.8

9.810.2

14.6

9.9

2.1

10.113.8

15.319.2

2.4

10.6

17.215.1

20.9

Fish* Pork Poultry Beef Lamb

1997/99

2030

2015

Export of F&B 3

19

84

43

2013 2018f

+15%

N. America Europe 43% 34%

4%

Others

66

34

2013

+14%

2018f

1,100

2019f

+3%

932

2014

Rising health awareness amongst consumers will contribute stronger sales for health and wellness F&B products, esp. in the developed economies

Global H&W food market

Unit: USD billion

Global organic F&B market

Unit: USD billion 2013: 80.4 USD billion

Export of F&B 3

Source: EIC analysis based on data from Merrill Lynch, Euromonitor, BCC Research and Agrarmarkt Austria Marketing

20

13%

2014

14%

1,516

10%

64%

11% 11%

2,580

2010

3%

+14%

67%

6%

2%

Others +1%

India +28% Viet Nam +13%

Thailand +15% Canada +16%

17% 4% 6%

Indonesia

Hong Kong

Others

30%

US

Viet Nam

21%

22% China

Source: EIC analysis based on data from Trademap

Chinese demand for Thai fresh and frozen fruits will continue to rise steadily over the forecasted period

Export of F&B 3

Major destination of Thai fruits export, 2014

Unit: % of total

China fruit imports, by supplying country

Unit: USD million

Thailand is the main supplier of fresh fruits in China

21

3%

5%

2%

20%

1,362

15%

72% 4%

65%

3% 3%

+22%

4%

5%

2014 2010

611

CLMV +25%

Philippines +11%

Indonesia +16%

Singapore +13%

Malaysia +24%

Others +14%

2010

36%

23%

64%

19

77%

2014

37 +18%

Non-alochoholic drinks +23%

Alcoholic drinks +4%

3

4

5

6

7

8

9

10

Vietnam

Laos

Myanmar

ASEAN-5

Cambodia

2018f

World

2010 2017f 2016f 2015f 2014 2013 2012 2011

Demand for Thai beverage, especially non-alcoholic beverages (tea and functional drinks), in CLMV is rising strongly in line with economic expansion

Export of F&B 3

Source: EIC analysis based on data from Trademap

Thai beverage export to CLMV market, by category

Unit: THB million

Major destination of Thai beverage export

Unit: THB million

GDP growth forecast

Unit: %YOY

22

Likewise, demand for Thai dairy products is also expected to grow steadily, particularly among the CLMV countries

Export of F&B 3

20%

1% 10%

4%

13%

13%

4%

189

8%

2010

5%

16%

13%

19%

12% 9%

8%

16%

9%

20%

+9%

2014

262

Germany +66%

Others +3%

US +16% Cambodia +7%

Hong Kong +17%

Singapore +4%

Laos +6%

Philippines +15%

Myanmar +5% Buttermilk & yogurt

31%

Sweetened milk

20%

Milk

12% Whey

6%

Others

31%

Import

Domestic

Production

2,602

57%

43%

Domestic

Export

2,602 7%

Consumption

93%

Source: EIC analysis based on data from Trademap

Major destination of Thai dairy export

Unit: USD million

Thai dairy export products, 2014

Unit: %

Thai dairy industry, 2014

Unit: ‘000 ton

23

In sum, EIC expects overall F&B industry to expand continuously in 2016 and over the forecasted period

Segment Key drivers 2016

Outlook MT

Outlook

Domestic & Import

• Population growth

• Economic recovery

• Higher disposable income

• Rising of middle-income class

• Rising urbanization

Export • Macro trend

Economic change

Demographic change

Demand change

• Demand for Thai fruits in China

• Demand for Thai beverage in CLMV

• Demand for Thai dairy products from Asian countries

Positive

G

Positive

G

Positive

G

Positive

G

Source: EIC analysis

End of document

24

Disclaimer Disclaimer Disclaimer Disclaimer

The information contained in this report

has been obtained from sources believed

to be reliable. However, neither we nor any

of our respective affiliates, employees or

representatives make any representation

or warranty, express or implied, as to the

accuracy or completeness of any of the

information contained in this report, and

we and our respective affiliates, employees

or representatives expressly disclaim any

and all liability relating to or resulting from

the use of this report or such information

by the recipient or other persons in

whatever manner.

Any opinions presented herein represent

our subjective views and our current

estimates and judgments based on various

assumptions that may be subject to

change without notice, and may not prove

to be correct.

This report is for the recipient’s

information only. It does not represent or

constitute any advice, offer,

recommendation, or solicitation by us and

should not be relied upon as such. We, or

any of our associates, may also have an

interest in the companies mentioned

herein.

26

Related Documents