Life Cycle Costing: an effective asset management tool “Applying LCC contributes to more cost-effective management control of the production facilities of small and medium enterprises (SMEs)” Master of Science in Asset Management Control International Masters School Student: Bas Kemps Supervisor: Ir. Peter van Gestel Date: 12-6-2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

�

Life Cycle Costing:

an effective

asset management tool

“Applying LCC contributes to more cost-effective

management control of the production

facilities of small and medium enterprises (SMEs)”

Master of Science in

Asset Management Control

International Masters School

Student: Bas Kemps

Supervisor: Ir. Peter van Gestel

Date: 12-6-2012

ACKNOWLEDGEMENTS

I would like to dedicate this dissertation to my wife and colleagues. Writing this master’s thesis has

been very time-consuming. This has certainly had various consequences at home as well as at work.

Thanks to the understanding of these people, it has nonetheless been possible to complete this

thesis.

For controlling the quality of this dissertation, I would also like to thank Niek van Nunen and Peter

van Gestel. To complete this phase, Niek van Nunen was designated company supervisor. Peter van

Gestel has been so good as to act as supervisor on behalf of the master’s program.

Dissertation document B. Kemps Page 3

Summary

This master’s thesis seeks to develop and accept the following hypothesis: applying LCC analysis

results in more cost-effective management control of production facilities of SMEs. Research on the

sub questions has demonstrated that there is a difference in Life Cycle Costing and Life Cycle Cost

Analysis. Life cycle costing takes into account all costs of an asset throughout its intended lifespan,

resulting in a total cost of ownership calculation. Life Cycle Cost Analysis can be described as a cost-

comparing method of possible alternatives, using the Life Cycle Costing approach. Because LCC

analysis compares alternatives, only the differences between the alternatives translated into costs

will have to be compared.

In relation to the purchasing process of assets, Veteka, the pilot company, can be seen as the user of

the installations. A customer perspective is therefore the most suitable one. In order to provide

evidence relevant to the hypothesis, four case studies are described. The purpose is to compare

alternatives for each case by means of an LCC analysis method. Because in each case the purpose is

to compare different alternatives, it is not necessary to implement a complete life cycle costing

model that would result in a total cost of ownership of the different alternatives. For the purposes of

this thesis, it is sufficient to implement an LLC analysis in which only the cost differences between

two or more alternatives are taken into account. Costs that are the same for two alternatives can be

eliminated from consideration.

One of the sub questions was to introduce a suitable model in order to make an objective

comparison. Dell'Isola and Kirk [2003] describe a model which meets the needs regarding this thesis.

The model has been developed in Excel and is therefore also very easy to use. It incorporates a

discount and escalation rate and calculates the present worth difference between two or more

alternatives. Although Dell’Isola and Kirk’s book [2003] describes the sensitivity and uncertainty in

input parameters, it is barely possible to implement their method in one simple model. As a result of

experience with the @Risk program, Dell'Isola & Kirk’s model has been adapted in order to

implement the @Risk program. The adapted model makes it possible to calculate discount rate,

escalation rate, sensitivity, and uncertainty, resulting in the present worth difference of two

alternatives at the same time. With the @Risk program it is possible to generate graphs to visualize

both the impact of the different input parameters and the likelihood of an outcome to be positive or

negative.

The results of the different cases dealt with provide sufficient evidence for the hypothesis to be

accepted. Conducting an LCC analysis creates transparancy among the different cost drivers. Through

LCC analysis, the management can gather a lot of information on the financial concequences of

different alternatives, and with relatively little effort. For instance, an LCC analysis will reflect the

impact of hidden costs. Creating transparancy about the different relevant costs results in the fact

that more balanced choices can and will be made. To refine the uncertainty and sensitivity in the

different costs it is strongly recommended that further investigation is carried out into reliability,

availability and maintainability.

Although this type of analysis helps the purchasing process of installations, it does not indicate the

total expected revenues over the intended life span. For this, an analysis which takes into account all

costs and profits should be conducted. The result is a net present value difference.

Dissertation document B. Kemps Page 4

Currently, at Veteka, the pilot company, the data needed to conduct this type of analysis are

insufficient. When further investigation is carried out into discount and escalation rates, and

maintainability, availability and reliability, this broader type of analysis will be useful for making

proper cost calculations.

Dissertation document B. Kemps Page 5

Index

Acknowledgements ................................................................................................................................. 2

Summary ................................................................................................................................................. 3

Index ........................................................................................................................................................ 5

1 Introduction ................................................................................................................................... 10

1.1 Life cycle costing and total cost of ownership ...................................................................... 10

1.2 Statement of the research problem ...................................................................................... 11

1.3 Research questions................................................................................................................ 12

1.4 Research method .................................................................................................................. 14

1.5 Relation between research questions and model ................................................................. 15

1.6 Definitions and Terms ........................................................................................................... 16

2 Scope of a Life Cycle and Life Cycle Costing .................................................................................. 18

2.1 General ....................................................................................................................................... 18

2.2 Life cycle ................................................................................................................................ 18

2.2.1 The life cycle of the market .................................................................................................. 18

2.2.2 The life cycle of the development/production process ....................................................... 19

2.3 Life cycle cost tree ................................................................................................................. 22

2.4 Difference between Life cycle costing and Life Cycle cost analysis ...................................... 23

2.5 Area of interest in LCC analysis ............................................................................................. 24

3 Models ........................................................................................................................................... 26

3.1 Introduction .......................................................................................................................... 26

3.2 Commonly used models ........................................................................................................ 26

3.3 Models relevant to this study ................................................................................................ 29

3.4 Cost breakdown structure ..................................................................................................... 29

3.5 Discount and Escalation rate ................................................................................................. 30

3.6 Uncertainty and sensitivity ................................................................................................... 31

4 The purchasing process ................................................................................................................. 32

Dissertation document B. Kemps Page 6

4.1 Introduction ................................................................................................................................ 32

4.2 Purchasing policy of SMEs ..................................................................................................... 32

4.3 Reliability, availability and maintainability of current installations ...................................... 33

4.4 Improvements expected from implementing LCC analysis .................................................. 35

5 Cases .............................................................................................................................................. 36

5.1 Description of the cases .............................................................................................................. 36

5.1.1 Weinig versus Leadermac .............................................................................................. 36

5.1.2 Moulding Cutter Head ................................................................................................... 36

5.1.3 Coating line .................................................................................................................... 37

5.1.4 Double vacuum box ....................................................................................................... 39

5.2 Input parameters ......................................................................................................................... 40

5.2.1 Starting points ............................................................................................................... 40

5.2.2 Manufacture parameters .............................................................................................. 40

5.3 Results ........................................................................................................................................ 41

5.3.1 Weinig versus Leadermac .............................................................................................. 42

5.3.2 Moulding Cutter Head ................................................................................................... 42

5.3.3 Coating line .................................................................................................................... 43

5.3.4 Double vacuum box ....................................................................................................... 43

5.4 Conclusions to separate cases ..................................................................................................... 44

6 Efforts involved in Life Cycle Costing ................................................................................................. 45

6.1 Human efforts ....................................................................................................................... 45

6.2 Cost of LCC analysis ............................................................................................................... 45

7 Conclusions ....................................................................................................................................... 47

8 Recommendations ............................................................................................................................. 50

9 Reflection on the impact of LCC on company and management ...................................................... 51

Literature ............................................................................................................................................... 52

Appendix ................................................................................................................................................ 54

Dissertation document B. Kemps Page 7

Appendix 1: Dell’Isola’s Model .......................................................................................................... 54

Appendix 2: Present worth (of annuity) factor ................................................................................. 55

Appendix 3: Effect of the discount rate ............................................................................................ 56

Appendix 4: Input parameters and calculation sheets...................................................................... 57

Appendix 4.1: input parameters Weinig versus Leadermac ......................................................... 57

Appendix 4.2: Calculation Weinig versus Leadermac ................................................................... 58

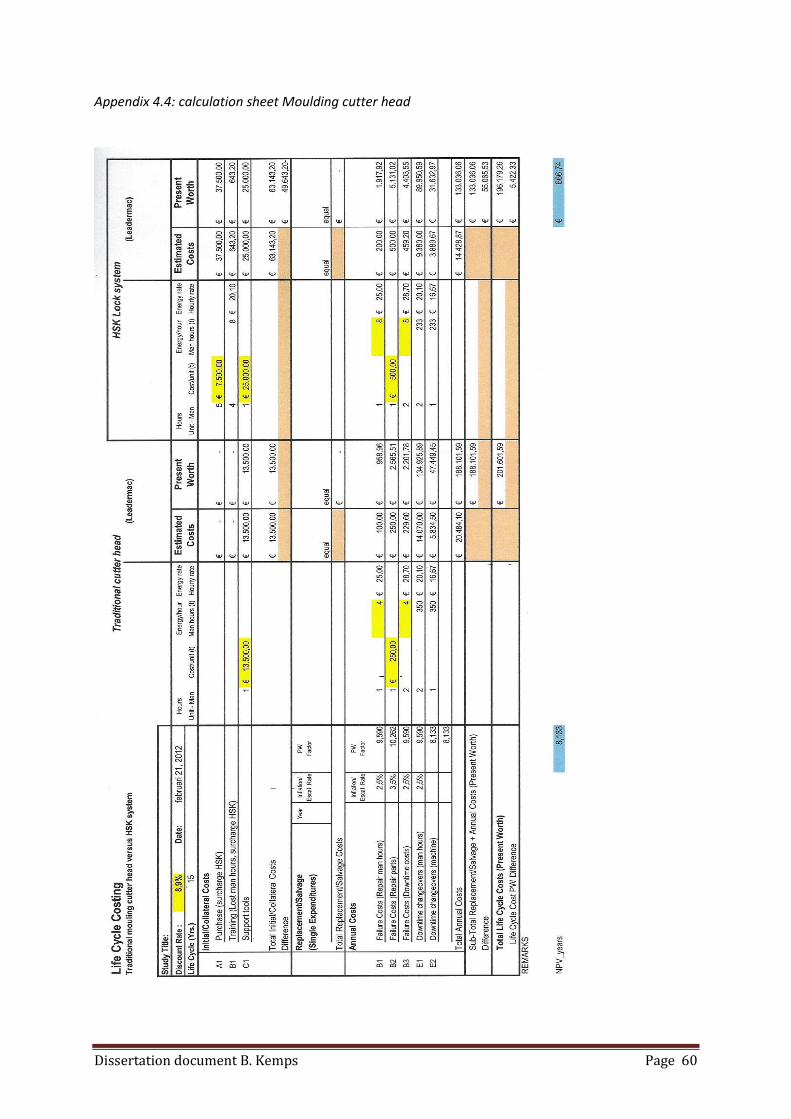

Appendix 4.4: calculation sheet Moulding cutter head ................................................................ 60

Appendix 4.5: Input parameters Coating line ............................................................................... 61

Appendix 4.6: Calculation sheet Coating line ................................................................................ 62

Appendix 4.7: Input parameters Double vacuum box .................................................................. 63

Appendix 4.8: Calculation sheet Double vacuum box ................................................................... 64

Appendix 5.1: Weinig versus Leadermac ...................................................................................... 66

Appendix 5.2: Moulding cutter head ............................................................................................ 69

Appendix 5.3: Coating line............................................................................................................. 72

Appendix 5.4: Double vacuum box ................................................................................................ 75

Appendix 6: Veteka, the pilot study .................................................................................................. 78

Dissertation document B. Kemps Page 8

Figure 1: Life cycle cost, consisting of acquisition costs and operations and maintenance 10

Figure 2: Exploratory-empirical research approach 14

Figure 3: different stages of a production life cycle 19

Figure 4: V-model 19

Figure 5: Life cycle assessment, design for environment approach 20

Figure 6: overall view of a life cycle 20

Figure 7: Area of interest in the life cycle from a customer point of view 21

Figure 8: Life cycle cost tree 22

Figure 9: Life cycle cost tree refined 23

Figure 10: Area of interest in LCC analysis for the pilot case 25

Figure 11: Life Cycle management domain 26

Figure 12: LCM, simplified for the purposes of this master thesis 27

Figure 13: Three layers of activity-based life cycle costing 28

Figure 14: Power lock system versus traditional moulding cutter head 37

Figure 15: Layout new coating line 38

Figure 16: Sophisticated transport system 39

Figure 17: Manufacture parameters 41

Figure 18: LCC analysis model 54

Table 1: Effect of the discount rate over the next 25 years 56

Table 2: Significant input parameters related to graph 1 66

Table 3: Significant input parameters related to graph 5 69

Table 4: Significant input parameters related to graph 9 72

Table 5: Significant parameters related to graph 13 75

Table 6: Essential characteristics of the replacement value of some used equipment 78

Dissertation document B. Kemps Page 9

Graph 1: Simple sensitivity analysis over the years, case 1 66

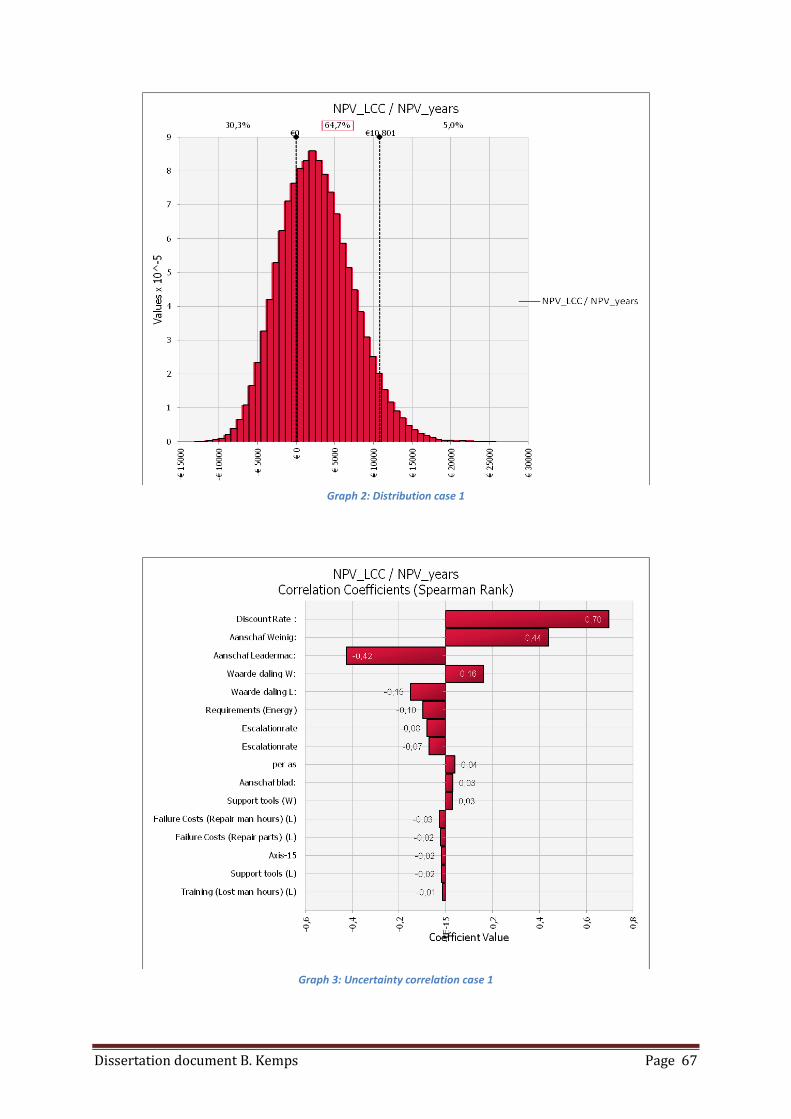

Graph 2: Distribution case 1 67

Graph 3: Uncertainty correlation case 1 67

Graph 4: sensitivity correlation case 1 68

Graph 5: Simple sensitivity analysis over the years, case 2 69

Graph 6: Distribution case 2 70

Graph 7: Uncertainty correlation case 2 70

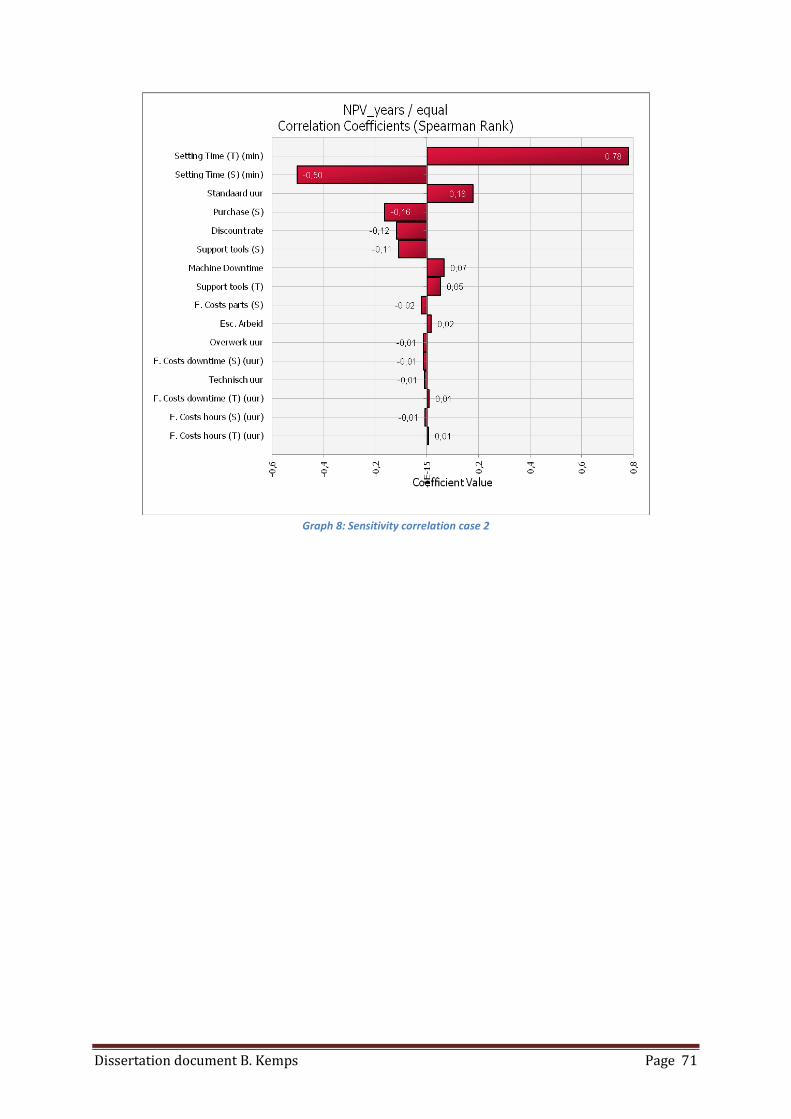

Graph 8: Sensitivity correlation case 2 71

Graph 9: Simple sensitivity analysis over the years, case 3 72

Graph 10: Distribution case 3 73

Graph 11: Uncertainty correlation case 3 73

Graph 12: sensitivity correlation case 3 74

Graph 13: Simple sensitivity analysis over the years, case 4 75

Graph 14: Distribution case 4 76

Graph 15: Uncertainty analysis case 4 76

Graph 16: sensitivity correlation case 4 77

Dissertation document B. Kemps Page 10

1 Introduction

1.1 Life cycle costing and total cost of ownership

Life cycle costing is an economic management tool designed to evaluate economic consequences of

an item, system or facility over its lifespan, expressed in terms of equivalent cost, using baselines

identical to those used for initial cost. Life cycle costing is used to compare various options by

identifying and assessing economic impacts over the life of each option. [Dell'Isola & Kirk, 2003]

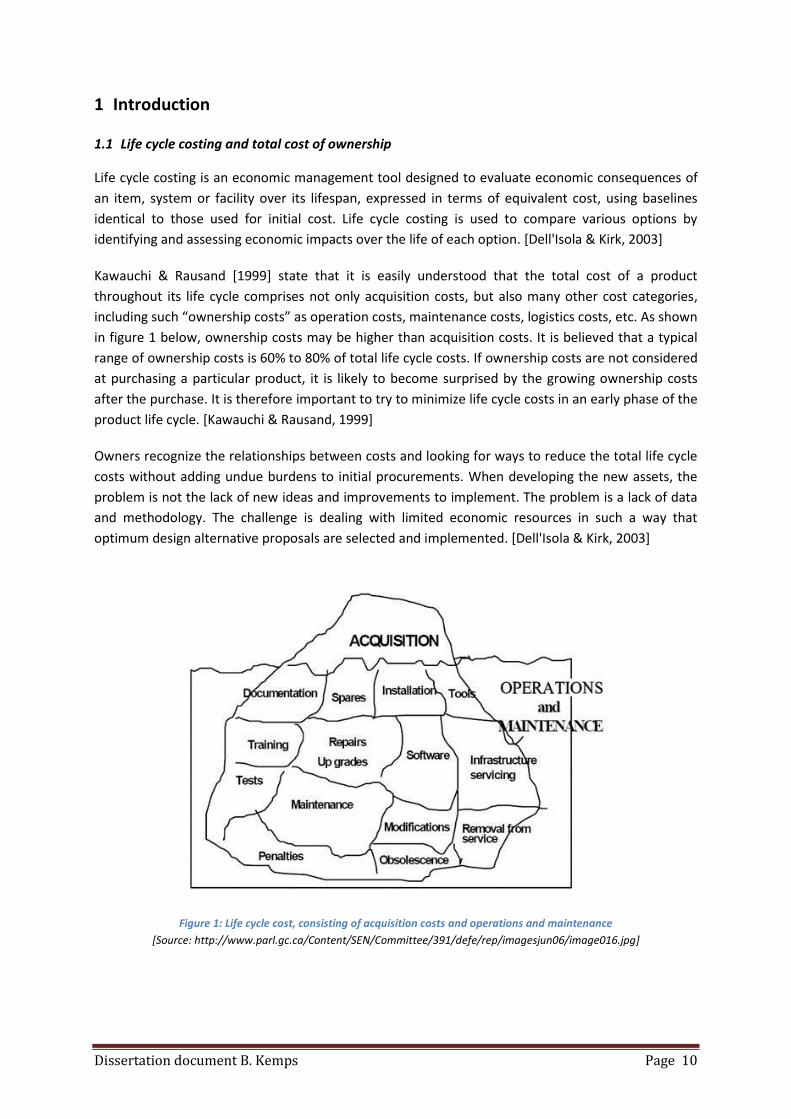

Kawauchi & Rausand [1999] state that it is easily understood that the total cost of a product

throughout its life cycle comprises not only acquisition costs, but also many other cost categories,

including such “ownership costs” as operation costs, maintenance costs, logistics costs, etc. As shown

in figure 1 below, ownership costs may be higher than acquisition costs. It is believed that a typical

range of ownership costs is 60% to 80% of total life cycle costs. If ownership costs are not considered

at purchasing a particular product, it is likely to become surprised by the growing ownership costs

after the purchase. It is therefore important to try to minimize life cycle costs in an early phase of the

product life cycle. [Kawauchi & Rausand, 1999]

Owners recognize the relationships between costs and looking for ways to reduce the total life cycle

costs without adding undue burdens to initial procurements. When developing the new assets, the

problem is not the lack of new ideas and improvements to implement. The problem is a lack of data

and methodology. The challenge is dealing with limited economic resources in such a way that

optimum design alternative proposals are selected and implemented. [Dell'Isola & Kirk, 2003]

Figure 1: Life cycle cost, consisting of acquisition costs and operations and maintenance

[Source: http://www.parl.gc.ca/Content/SEN/Committee/391/defe/rep/imagesjun06/image016.jpg]

Dissertation document B. Kemps Page 11

1.2 Statement of the research problem

Life cycle costing was originally designed for procurement purposes in the U.S. Department of

Defence [White & Ostwald, 1976] and is still most commonly used in the military sector and the

construction industry [Woodward, 1997]. Adoption of life cycle thinking has been very slow in other

industries [Lindholm & Suomala, 2005]. In a Finnish study, for instance, only 5% of large industrial

companies had used life cycle costing [Hyvönen, 2003]. These studies do not even mention the use of

life cycle costing in small and medium enterprises (SMEs).

Not much information is available regarding the use of life cycle costing within SMEs. Most decisions

are mainly based on experience, feelings and small basic calculations. For this reason there is only

little insight into the total cost of individual installations over their technical lifespan in SMEs.

To remain competitive and to maintain market position, SMEs have to continuously improve their

efficiency. As Emblemsvåg [2003] explains, the invention of the digital computer has created an

explosion in product variety at affordable prices because new manufacturing technologies enabled

mass production at an unprecedented scale. This development has resulted in a faster changing

environment in which techniques continuously change. As a result, companies have to secure the

purchasing policy of assets/installations in order to remain competitive. This study will concentrate

on the contribution of Life cycle cost analysis (LCC analysis) to the process of purchasing a new

production device in SMEs.

A small investigation among clients and suppliers has pointed out that SMEs rarely have a clear

insight into the total costs of individual installations over their technical lifespan. In order to make

cost-effective, well-founded decisions about new assets, it is essential to create transparency of all

costs over an asset’s technical lifespan (within a particular company). Life cycle cost calculations

could be a tool to gain insight in the total cost of ownership for different installations. Such

researchers as J. Emblemsvåg, B.S. Dhillon and H. Barringer have proved that life cycle cost

calculations contribute to a cost-effective management of assets. In the literature available, several

examples of life cycle costing models are provided. Although these examples are often about

complex “static” assets such as marine ships, (large) infrastructural projects, wind mill parks, power

plants, etc., there are also some examples which are similar in scale to assets in SMEs. [Barringer,

2003; Emblemsvåg, 2003; Korpi & Ala-Risku, post-2005; Dhillon, 2010] For instance, Barringer states

that life cycle cost calculations could be useful for investments starting between 10.000-25.000 US

dollars (in 2003). This statement will be discussed later in this thesis.

As mentioned before, the purchase policy of SMEs is often based on experience and general

knowledge. The question arises whether or not life cycle costing can help these companies to create

a more evidence-based purchase method. This is what this master’s thesis will be focused on. For this

particular case, the following hypothesis is developed:

“Applying LCC contributes to more cost-effective management control of production facilities of

SMEs.”

To test the hypothesis, the company Houtindustrie Veteka will serve as a pilot case. This company

was founded about 40 years ago. During these 40 years it has become one of the leading companies

Dissertation document B. Kemps Page 12

in supplying the Dutch construction market of houses with finished wooden mouldings. The company

is equipped with different production processes in order to profile and coat the wooden slats.

Within this company four individual cases will be discussed in order to find evidence to accept the

hypothesis.

1.3 Research questions

To provide a solution to the case described and to find evidence to prove the hypothesis, the

following research question is formulated:

“How can within a purchasing strategy life cycle cost analysis contribute to improve cost-effective

management control throughout SME’s?”

To find an answer to this question, different areas of interest have to be investigated and examined.

In order to perform a structured investigation seven sub questions are performed. Each sub question

contributes to the investigation on the different areas of interest to perform an answer on the

research question.

To provide an answer on the research question, first the research area has to be defined. For

example it is important to have insight in which cost parameters are of interest in the purchase

process of production installations and which are of minor importance? In this way the next sub

question is formulated:

1. What is the scope of life cycle cost analysis related to this case?

This question will be handled in chapter 2

Knowing the field of interest, first a literature study is done to create insight in the way LCC analysis

are conducted. It is believed that not all LCC calculations are performed in exactly the same way.

Investigation has to be carried out on which LCC model is suitable for this case and will it be possible

to extract a useful model for this study. This has led to perform the next sub questions:

2. Which commonly used models are available in the literature?

3. Which of the previously mentioned model(s) is/are suitable, and in what way is optimization

of one of these models (or a combination of models) possible, in order to develop a useful

model for production facilities within SMEs? These two questions will be handled in chapter

3

Dissertation document B. Kemps Page 13

In order to improve the purchasing strategy, it is important to have insight in the current purchasing

policy and all other relevant information available. With the knowledge gained from the previous

questions, necessary data to perform an LCC analysis can be derived. So besides the current

purchasing policy also data collection to fulfill the input parameters is needed. This has led to form

the next question:

4. How does the current purchasing process of installations take place, and what historical data

needed is at hand?

This question will be handled in chapter 4

Based on the previous questions some knowledge about LCC analysis and its boundaries is gained. In

order to stay focused on providing evidence to accept the hypothesis it becomes useful at this stage

to point out expected improvements. Therefore the next question is performed.

5. Which parts of the current purchasing process are expected to be improved with the

introduction of LCC?

This question will be handled in chapter 4

To provide evidence in order to accept the hypothesis four practical case studies within the pilot

company will be performed. These four cases are described in (section xx and xx). In these chapters

an experimental LCC analysis on each case is carried out, and the results will be presented. To

evaluate these outcomes the next sub questions are conducted.

6. What are the findings with the previously mentioned question when conducting an

experimental LCC analysis?

This question will be handled in chapter 5 (results and conclusions)

7. How are the efforts involved in conducting an LCC analysis related to the benefits of the LCC

analysis?

This question will be handled in chapter 6

With the total knowledge and insight gained on LCC analysis, and the answer on the last sub

questions it will be possible to derive conclusions on the stated hypothesis.

“Applying LCC contributes to more cost-effective management control of production facilities of

SMEs.”

Dissertation document B. Kemps Page 14

1.4 Research method

To guide this master’s thesis, the Exploratory-empirical research approach will be used. On initiation

of the project, a theoretical and practical investigation can be set up. This part of the research gains

insight in the available information and helps to clearly specify the problem definition. From this

theoretical basis and problem definition it is possible to design and expand an experimental model.

The empirical side of the research is mainly focused on deriving conclusions based on the

information of the experimental design and the theoretical and practical foundation. Purely empirical

research draws conclusions from results without any theoretical foundation. The figure below gives

an impression of the approach used. [Saunder, 2000]

Figure 2: Exploratory-empirical research approach

[Source: Saunder, 2000]

In this thesis, the hypothesis formulated forms the statement and foundation of the research. To

investigate the foundation, the problem definition will be defined by stating a central question and

sub questions. During the experimental system design, information will be gathered and structured.

The basis of a model will be designed. After this phase, the experimental model will be completed;

the practical results can be evaluated against the theoretical foundation and hypothesis.

Chapter 2,3 and 4 are mainly forming the exploratory research part of this thesis. In the fifth Chapter

four practical cases will be handled, this forms the empirical part of the research method. In chapter

5 and 7 the empirical research results will be discussed.

Dissertation document B. Kemps Page 15

1.5 Relation between research questions and model

To further define the relation of the investigation with the model used, the sub questions will be

assigned to a certain place in the model. Behind each block of the model, the appropriate sub

question(s) will be given.

Initiation

Theoretical &

practical foundation

Problem definition

Empirical

research results

Experimental

system design

In this specific part of the research the purpose of the research is pointed

out. This purpose can be clarified by the stated hypothesis which has to be

proven. In this part also general

A literature study will be performed to find out what theory is at hand

regarding this subject. With this knowledge an abstraction will be made to

distillate the scope and useful models of LCC related to this case (sub

question 2 & 1).

From the moment the scope and models are defined, the current purchase

process and available data needed has to be investigated. Expected

improvements also have to be pointed out.

(sub questions 1,4 & 5)

With the findings of the literature study and the problem definition a model

will be chosen and adjusted to make it suitable for this case. Four

experimental case studies will be performed by using this model (sub

question 3 & 6).

The results will be presented and a discussion will be started whether the

results correspond to the expectation. Moreover there will be discussed if

the efforts involved in conducting a LCC analysis will offset to the benefits

(sub question 6 & 7). A feedback to the theoretical & practical foundation

and the problem definition will be made.

The initiation of this research is caused by the development of new

constructors, the evolution of our own market and the need to gain more

precise insight into present and future costs of our installations

Dissertation document B. Kemps Page 16

1.6 Definitions and Terms

For reasons of clarity, some specific terms which will be used throughout this study will first be

explained.

Asset management: a management approach to manage all processes (specify, design,

produce, maintain and dispose) needed to achieve a capital asset capable to meet the

operational need in the most effective way for the customer/user. [Stavenuiter, 2002]

Asset Management Control: a management approach to manage and control, over the life

cycle, all processes (specify, design, produce, maintain and dispose) needed to achieve a

capital asset capable to meet the operational need in the most effective way for the

customer/user. [Stavenuiter, 2002]

Life cycle generaly: Life cycle definitions basically follow the same steps; these different steps

are:

o Development

o Introduction

o Growth

o Maturity

o Decline

When defining the life cycle of assets, the steps are different. The development/production

process approaches the life cycle from the conceptual stage till the phase of use,

maintenance and phase out. In section 2.2.2 this will be handled more detailed.

Life cycle cost: Emblemsvåg describes Life cycle costs as “the total costs that are incurred, or

may be incurred, in all stages of the product life cycle”. [Emblemsvåg, 2003]

Life cycle costing: Life cycle costing is an economic assessment of an item, area, system, or

facility that considers all significant costs of ownership over its lifespan, expressed in terms of

equivalent dollars. LCC is a technique that satisfies the requirements of owners for adequate

analyses of total costs. [Dell'Isola & Kirk, 2003] In extension, this technique/method can be

used to determine the total cost of ownership of an item.

Life cycle cost analysis: Life cycle cost analysis is an economic assessment of an item, system

or facility over its lifespan, expressed in terms of equivalent cost, using baselines identical to

those used for initial cost. Life cycle cost analysis is used to compare various options by

identifying and assessing economic impacts over the life of each option. [Dell'Isola & Kirk,

2003]

Life Cycle Analysis (LCA): LCA is an analytical tool of increasing importance for supply chain

management. It aims to provide the basis for decisions which will promote sustainable

development of our economies. Its strength is primarily related to the development of

cleaner production and products, in order to reduce material and energy use and emissions

harmful to the environment. [Stavenuiter, 2002]

Dissertation document B. Kemps Page 17

Life Cycle assessment: J. Stavenuiter [2002] explains in his book that life cycle assessment is

the same as life cycle analysis.

Discount Rate: a multiplicative number (calculated from a discount formula for a given

discount rate and interest period) that is used to convert costs and benefits occurring at

different times to a common time. Often, interest rate will be used as a synonym for discount

rate. Discount rate means the minimum attractive rate of return on an investment. [Dell'Isola

& Kirk, 2003]

Escalation rate: this rate has to be taken into account when price modifications of individual

items over time are greater than or less than the general discount/inflation rate.

Present worth (method): an economic method that requires conversion of costs and benefits

by discounting future cash flows to a baseline date. [Dell'Isola & Kirk, 2003]

The present worth can be defined for costs and benefits. When all discounted costs are

subtracted from all discounted benefits, one can determine the net present value.

Net present value: the standard criterion for deciding whether a program can be justified on

economic grounds is net present value. Net present value is computed by assigning monetary

values to benefits and costs, discounting future benefits and costs, using an appropriate

discount rate and subtracting the sum total of discounted costs from the sum total of

discounted benefits. [Dell'Isola & Kirk, 2003]

Cost-effectiveness: cost-effectiveness is defined as the value received for the resources

expended and is the ratio of cost to (system) effectiveness. [Stavenuiter, 2002; Juran, 1988]

Total cost of ownership: an estimate of all direct and indirect costs associated with an asset

or acquisition over its entire life cycle. [www.businessdictionary.com]

Uncertainty: applies to situations about which we do not even have reliable probability

information. Uncertainty is a superset of risk. [Emblemsvåg, 2003]

Capacity-related costs: costs associated with capacity-related resources. [Atkinson, Kaplan, &

Young, 2004]

Operational need: a statement of the capability, reliability and availability required for each

supplier-related operational function, including disposal. [Stavenuiter, 2002]

Operational function: a function with operational importance fulfilling (a part of) the

operational need for which the operator/customer is willing to pay. [Stavenuiter, 2002]

Risk: risk can be defined as chance of an event with undesired consequences. [Gestel, 2012]

Dissertation document B. Kemps Page 18

2 Scope of a Life Cycle and Life Cycle Costing

2.1 General

In literature LCC is mainly described in general. It is hard to find specific industry-related use of LCC

methods. It gives the impression that LCC as a decision tool is universally applicable. This seems to be

incorrect since there is a difference in, for example, standard products and client specific products.

There is also a difference in approach regarding LCC between a manufacturer and the client. [Bel &

Martin, 1993] As far as the pilot company is concerned, this subject needs to be clarified first.

2.2 Life cycle

Before starting to think about life cycle costing, a very basic concept must be clarified, namely the life

cycle. The interpretation of the term life cycle differs from decision maker to decision maker, as is

evident from the literature. [Emblemsvåg, 2003] In this matter for example, a manufacturer has a

point of view on a life cycle different from that of a customer, who will be the user of the

manufacturer’s product.

In practice, there are three different life cycle perspectives that have to be taken into account.

[Emblemsvåg, 2003] These are:

the life cycle of the market

the life cycle of the developing/production process

the life cycle of the product.

2.2.1 The life cycle of the market

Emblemsvåg [2003] describes the marketing perspective as consisting of at least four stages:

Introduction

Growth

Maturity

Decline

A marketing perspective follows the stages of the life cycle of the market and has nothing to do with

a life cycle of a product. For the purposes of this study, a marketing perspective is of minor interest,

since the focus is on the purchasing and use of production facility and not the marketing lifetime of a

product.

A possible way of visualizing these four stages is exemplified in figure 3.

Dissertation document B. Kemps Page 19

Figure 3: different stages of a production life cycle

[Source: http://www.maxi-pedia.com/product+life+cycle+plc]

2.2.2 The life cycle of the development/production process

The development/production process approaches the life cycle from the conceptual stage till the

phase of use, maintenance and phase out. Many models are developed to describe this approach of

the life cycle. While the marketing approach focuses on the revenues of a system or product over its

intended lifespan, the develop/production approach concentrates on the total cost during the

development process and use of a system.

As will be discussed in section 2.2.3, the development stage is of minor interest to this study. With

regard to this topic, reference will therefore be made to the literature, which is easily available.

Nevertheless two commonly used models will be visualized in figures 4 and 5 below:

Figure 4: V-model

[Source: http://ops.fhwa.dot.gov/publications/tptms/handbook/chapter_2.htm]

Dissertation document B. Kemps Page 20

Figure 5: Life cycle assessment, design for environment approach

[Source: Blanchard, 1994]

2.2.3 The life cycle of a product

Analysing the life cycle of a product, Emblemsvåg [2003] described the overall view provided in figure

6 below.

Figure 6: overall view of a life cycle

[Source: Emblemsvåg, 2003]

Dissertation document B. Kemps Page 21

In this overall view, everything starts with raw materials and, at the end of the lifespan, will end as

“dust”. Looking from the perspective of a manufacturer or a costumer, many of these stages can be

skipped.

For a manufacturer the left part of the circle is of minor interest. Notwithstanding the fact that, in

today’s society, the total cycle is becoming increasingly important, and companies are therefore

increasingly being forced to think in terms of “what will happen afterwards”, the main stages for the

manufacturer remain as follows: [Emblemsvåg, 2003]

Product conception

Design

Product and process development

Production

Logistics

Like the manufacturer, the costumer also has his own perspective, which consists of the following

stages: [Emblemsvåg, 2003]

Purchase

Operating

Support

Maintenance

Disposal

This can be visualized by means of figure 7 below:

Figure 7: Area of interest in the life cycle from a customer point of view

[Source: B. Kemps]

Dissertation document B. Kemps Page 22

Figure 7 shows that the yellow area is of primary interest to the customer. This overview of the

different stages of manufacturer and customer interest demonstrates that the customer’s

perspective follows the manufacturer’s.

For a production company with an established market, it is important to keep up with new

technologies. It is therefore important to maintain a cost-effective production layout. This study will

concentrate on a specific part of production, i.e. the purchasing of a new production device. So the

field of interest will be the purchasing process of a new asset. The most suitable perspective for this

aim has to be clarified. The stages which concern the research question most are those in the green

area: the purchase and use of an asset. This study will therefore focus on these stages and deal with

a customer perspective of a life cycle.

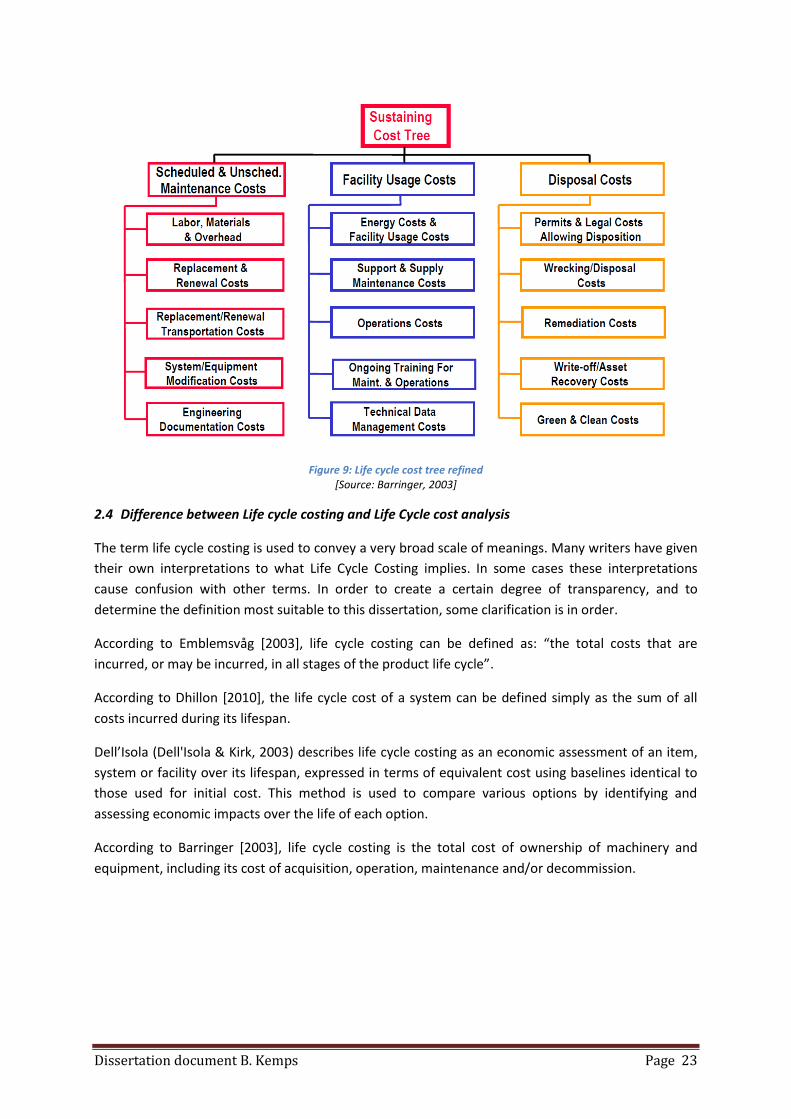

2.3 Life cycle cost tree

There are two major cost categories by which projects are to be evaluated in life cycle costing. They

are initial costs and future costs. Initial expenses are all costs incurred prior to purchasing the asset.

Future expenses are all costs incurred after commissioning the asset/facility. [Mearig, Coffee, &

Morgan, 1999] This is also specified by Barringer. He divides the life cycle cost tree into two major

parts: Acquisition Costs and Sustaining Costs.

Figure 8: Life cycle cost tree [Source: Barringer, 2003]

As can be seen in figure 8, Barringer defines the initial costs of building the installation as acquisition

costs. His figure shows that the cost tree can be divided into two parts: acquisition costs & sustaining

costs. Compared to the perspectives that Emblemsvåg describes, the setup of Barringer’s cost tree

suggests that his perspective on conducting a life cycle cost analysis is a customer perspective.

Emblemsvåg’s describes different perspectives. From the viewpoint of the constructor, sustaining

costs are not of prior concern related to the installation. From the customer’s viewpoint however, as

Barringer clearly states, sustaining costs are taken into account. Emblemsvåg in fact confirms that

Barringer visualizes a customer perspective.

Although acquisition costs can be very important for an LCC analysis, they can be seen as simple

input parameters resulting from a set of requirements which have to be met. A refined investigation

into the acquisition cost tree is therefore not of primary concern. Insight into the costs to keep the

installation in operating condition is more important. It is therefore crucial to be aware of the

differences in sustaining costs between possible alternatives. This is visualized by Barringer’s

sustaining cost tree, as provided in figure 9 below.

Dissertation document B. Kemps Page 23

Figure 9: Life cycle cost tree refined

[Source: Barringer, 2003]

2.4 Difference between Life cycle costing and Life Cycle cost analysis

The term life cycle costing is used to convey a very broad scale of meanings. Many writers have given

their own interpretations to what Life Cycle Costing implies. In some cases these interpretations

cause confusion with other terms. In order to create a certain degree of transparency, and to

determine the definition most suitable to this dissertation, some clarification is in order.

According to Emblemsvåg [2003], life cycle costing can be defined as: “the total costs that are

incurred, or may be incurred, in all stages of the product life cycle”.

According to Dhillon [2010], the life cycle cost of a system can be defined simply as the sum of all

costs incurred during its lifespan.

Dell’Isola (Dell'Isola & Kirk, 2003) describes life cycle costing as an economic assessment of an item,

system or facility over its lifespan, expressed in terms of equivalent cost using baselines identical to

those used for initial cost. This method is used to compare various options by identifying and

assessing economic impacts over the life of each option.

According to Barringer [2003], life cycle costing is the total cost of ownership of machinery and

equipment, including its cost of acquisition, operation, maintenance and/or decommission.

Dissertation document B. Kemps Page 24

When using life cycle costing to compare different alternatives, one should be aware that not all cost

categories are relevant to all projects. The preparer is responsible for the inclusion of the pertinent

cost categories that will produce a realistic life cycle costing comparison of project alternatives. If

costs in a particular cost category are equal in all project alternatives, they can be documented as

such and removed from consideration in the life cycle costing comparison. [Mearig, Coffee, &

Morgan, 1999] Dell’Isola and Kirk [2003] also mention that costs that are considered to be the same

for all alternatives can be eliminated from the life cycle cost analysis.

Thus, life cycle costing can be used as a method to compare and analyse different alternatives. When

comparing different alternatives it is possible to remove equal costs from consideration. If costs are

eliminated from consideration, one must be aware that the definitions of life cycle costing

mentioned above are no longer appropriate: when costs are eliminated from consideration it is more

suitable to use the term life cycle cost analysis (LCC analysis).

Life cycle cost analysis can be described as a cost-centered engineering economic method whose

objective is to systematically determine the costs attributable to each of one or more alternative

courses of action over a specified period of time. The key elements of such an analysis will be

examined, as will be the effectiveness of its results in a particular situation.

Before starting the process of cost calculation, it is important to clearly determine what exactly is to

be investigated.

Life cycle cost analysis can be used as a method to compare different alternatives.

Life cycle costing can be used to gain insight in the total cost of ownership of an asset.

It is important to keep this in mind when using a life cycle cost analysis model.

In addition, it is to be noted that when some equal costs are removed from the comparison, it is not

easy to reimplement these specific costs at a later stage. During the time that has lapsed, costs may

have changed, resulting in increasing inaccuracy of the outcome. It is also to keep in mind that

initiating and going through the process again is time-consuming. This can be of importance when,

for instance, a third or fourth alternative becomes possible. This problem also occurs when, at a later

stage, the management decides to investigate the possibility of investing in a complete new

installation. When costs are eliminated from consideration it will be hard to compare this

investigation with the life cycle cost analysis made earlier, because the latter is incomplete.

2.5 Area of interest in LCC analysis

For this particular case study, the pilot company can be seen as the purchaser and user of a new

asset/installation. This means that the customer perspective is most suitable for the pilot company.

Figure 10 below shows the area of interest for this business case. It visualizes the fact that the life

cycle cost analysis of the manufacturers is not taken into account. The different options available to

the manufacturers, and their specifications, are simply the input parameters of the analysis. For the

disposal of the installation it is important to know what the cost or perhaps residual value will be, as

expressed in euros.

Dissertation document B. Kemps Page 25

Figure 10: Area of interest in LCC analysis for the pilot case [Source: B. Kemps]

In this chapter, the scope of LCC analysis for the case study has been defined. A customer perspective

is most suitable, which implies that the development of installations is not of primary concern. The

purchase of the installation can therefore be seen as an input parameter. Further research has

pointed out that it is not necessary to conduct a complete LCC calculation. A life cycle cost analysis is

sufficient to investigate the case study.

Dissertation document B. Kemps Page 26

3 Models

3.1 Introduction

In this chapter, an impression of commonly used LCC models will be given. Directly linked to these

generally known models, a model suitable for this particular study will be presented. Shortcomings

will be pointed out; if possible, the model will be adapted with regard to these specific areas of

interest.

3.2 Commonly used models

In literature, life cycle cost models are described. Theories regarding these models are mainly

described in general. The models have become more and more elaborate and their complexity has

increased over the years. An abstract of the most important references relevant to this research will

be given below.

This thesis is part of the master’s program in “Asset Management Control” (AMC). The field of

interest within this AMC study is to improve cost-effective management of capital assets. Many

companies exploiting capital assets have to deal with identical problems related to the following

AMC objectives:

Specify system functionality

Acquire system functionality

Achieve cost-effectiveness

To meet these objectives, the AMC domain focuses on five specific areas of interest, viz.

management, engineering, education, information, and communication throughout the life cycle of

an asset. A Life cycle management (LCM) approach has been designed to meet these objectives.

In the figure below, the domain within this LCM approach is visualized.

Figure 11: Life Cycle management domain [Source: Stavenuiter, 2002]

Dissertation document B. Kemps Page 27

The Life cycle management domain mentioned above consists of different stages. In all of these

stages, different kinds of data are needed. All this data is collected, structured and provided by

Product Data Management (PDM). The total data needed to manage capital assets is called a life

cycle management (LCM) data set.

A considerable amount of parameters – including operating requirements, reliability, availability,

maintainability, energy, maintenance plans, etc. – is needed for an LCM data set and for life cycle

cost calculations. As such, a life cycle management data set can provide all data needed to make

proper cost calculations. Stavenuiter [2002] has developed a model to manage complex assets such

as marine ships. The model is able to visualize the effect of different installations and actors in terms

of performance of the total system. As Barringer [2003] points out, the purchase of the installation

can be seen as acquisition costs. Only slight specific adjustments of the installation are sometimes

possible. For this reason, the installation will usually be produced after an agreement on the

specifications. This is visualized in figure 12 below. Mainly relevant to this investigation are the

differences in costs of utilization and maintenance. As becomes clear, the LCM model deals with

many more aspects than is necessary for this thesis.

Figure 12: LCM, simplified for the purposes of this master thesis [Source: Stavenuiter, 2002]

However, the model itself will not be used, because it is too broad to be used directly for life cycle

cost calculations for SMEs. The general approach and insight gained into Life Cycle Management (and

AMC), however, has been very useful.

Fabrycky and Blanchard [1991] introduce three different ways to estimate costs:

Cost estimating by engineering procedures

Cost estimating by analogy

Cost estimating by parametric estimating methods.

Emblemsvåg [2003] also mentions these ways of cost estimating, describing them as models, and

adds a fourth way to estimate costs, viz. cost accounting models.

Cost estimating by procedures, (engineering cost models according to Emblemsvåg)

Costs are assigned to each element at the lowest level of design detail and then combined into a

total for the product or system. The main difficulties with this method are the need for detailed data

and the efforts involved in performing the calculations.

Dissertation document B. Kemps Page 28

The basic idea of Estimation by Analogy is to create accurate estimates for new projects by

comparing the new project to similar projects from the past. The most significant problem of this

type of estimating is the high level of judgment required. It is the cheapest way of cost estimating,

because not much data is needed.

Parametric estimation utilizes different statistical techniques and seeks for the factors on which the

life cycle cost depends. This type of estimating requires a lot of data. Emblemsvåg [2003] explains

that parametric models are in many ways more advanced analogy models.

The fourth cost estimating model, according to Emblemsvåg [2003], is what he calls cost accounting

models. He analyzed this way of cost estimating into three groups:

Volume based costing

Unconventional costing

Modern cost management systems

Cost management systems are frequently discussed in the literature. Emblemsvåg describes four of

them: Activity Based Costing (ABC), Just In Time (JIT) Costing, Target Costing (TC) and Strategic Cost

Management (SCM).

In addition to these models, he has developed an approach of his own in which he combines the

benefits of activity-based costing, life cycle costing and Monte Carlo methods. It results in a model

with a lot of advantages over the existing models.

Activity-Based life cycle costing handles both costs and cash flows

Activity-Based life cycle costing is process-oriented

Activity-Based life cycle costing relies on the establishment of cause and effect relationships

Activity-Based life cycle costing handles overhead costs

Activity-Based life cycle costing estimates the cost of all cost objects of a business unit

simultaneously

Figure 13: Three layers of activity-based life cycle costing [Source: Emblemsvåg, 2003]

Activity- Based Costing

•Overhead costs

•Relevant cost assigment

•Cause and effect

•Multiple cost objects

•Process-orientation

•Cost vs expense

•Cost vs cash flow

•Links to TQM, EP

Life-Cycle Costing

•Life-cycle perspective

•Total costs

•Cashflows

•Discountingfactors

Monte Carlo Methods

•Statistical sensitivity analysis

•Handle risk and uncertainty realistically

•Large models

•No limits

Dissertation document B. Kemps Page 29

3.3 Models relevant to this study

The question arises whether such complex approaches make sense for SME companies with an

established market and standard production equipment. As discussed before, the best way to

describe the life cycle of investments within these types of companies is the costumer perspective.

The key question for these companies will be “how to reduce costs” or, formulated in a slightly

different way, “what alternatives of an investment will be the one with the least incurred costs”.

With this in mind, all costs which are equal for the alternatives can be disregarded.

Dell’Isola [Dell'Isola & Kirk, 2003] describes a model disregarding all equal costs. Only costs that are

different for the alternatives will be included. For this reason, most life cycle costs can be

disregarded, which makes the model concise, clear and easy to understand. The advantage of less

input parameters is that it makes the relationship between outcome and input parameters much

easier to demonstrate.

The model provided by Dell’Isola [Dell'Isola & Kirk, 2003, cf. appendix 1] is based on an Excel

spreadsheet: this makes the model very accessible and, in addition, adaptable to specific cases. What

is more, this makes it possible to combine the model with other Excel based models. The latter

possibility will be drawn on in section 3.6, where the model will be extended through an uncertainty

and sensitivity analysis.

Dell’Isola distinguishes three types of costs (cf. appendix 1):

Initial/ collateral costs

Replacement/salvage costs

Annual costs

This classification is mainly based on the moment when and frequency with which the costs occur. As

a result, the classifications have their own ways of dealing with the value of money in time. This will

be discussed in section 3.5.

3.4 Cost breakdown structure

To make this model useful for this study, it is first of all necessary to examine the costs involved. An

inventory has therefore been made of all the costs of the life cycle of the assets. This is called a cost

breakdown structure. When grouping the major cost categories, it is useful to estimate all applicable

costs for each category. Besides the inventories and price level of the costs, it is also important to

investigate the frequency over its lifespan. With regard to this research, it is to be noted that not all

costs have to be investigated. Because, as stated before, this is an analysis of different alternatives,

costs that are similar in each alternative may be deleted from consideration. [Blanchard, 2004]

Dissertation document B. Kemps Page 30

For the purposes of this study, the following cost breakdown structure is used:

Initial/collateral cost

A. Purchase

B. Training

C. Support tools (tools exchangeable with other assets)

Replacement/salvage cost

A. Replacement costs hardware (technical lifespan)

B. Update software (including training)

C. Spare parts

D. Disposal/demolishing

Annual costs

A. Maintenance

B. Failure costs

Repair costs

Downtime costs

Disposal/residues

C. Requirements

Energy

Air

Extraction

Heating

D. Personnel

E. Downtime changeovers

3.5 Discount and Escalation rate

To make future costs comparable to today’s costs, it is necessary to incorporate both a discount rate

and an escalation rate. In the literature, much has been written on discount rates and methods

available for determining them. There is no universally accepted method or resulting rate. The

discount rate is often described as “the minimum attractive rate of return” on an investment. It is

generally the prerogative of the owner or policy maker to select the discount rate. The rate usually

includes the basic cost of borrowing money plus an increment that reflects the risk associated with

the investment. [Dell'Isola & Kirk, 2003] In appendix 2, formulas are given to calculate the present

worth factor and the present worth of annuity factor. These factors have to be used because today’s

euros will not necessarily have the same value tomorrow (appendix 3, effect of discount rate). Future

costs, such as operation and maintenance costs, have to be discounted to their present values before

they can be compared with such items as acquisition or procurement costs. On the other hand, some

costs will increase over time. Energy costs have become higher and higher, but labour costs are not

constant either. For that reason, an escalation rate should also be used. As opposed to the discount

rate, the escalation rate will be specific for the different types of costs. With the discount and

escalation rate, it is possible to determine the present worth factor (appendix 2).

Dissertation document B. Kemps Page 31

3.6 Uncertainty and sensitivity

The need for uncertainty assessments comes from the fact that input data for an LCC analysis are

based on estimates rather than known quantities. The data input is, therefore, uncertain.

Uncertainty exists in all situations when things are unknown, unpredictable, open-ended or complex.

Emblemsvåg [2003] defines uncertainty as a subset of unpredictability, which in turn is a subset of

the unknown. He states that an uncertain matter is not unknown or unpredictable. The problem is

the lack of information and knowledge about it. In addition, uncertainty is best described in relation

to complexity. This complexity often arises in open systems because they interact with their

environment to various degrees and evolve over time.

To identify high cost distributors, a sensitivity analysis can be conducted. A sensitivity analysis

examines the impact of changes in input parameters on the result. Varying the input parameters over

a range to see the impact on costs can help to highlight the major factors affecting costs. With a

sensitivity analysis it also becomes possible to visualize the effects on costs of different design

possibilities.

Different methods for conducting a sensitivity analysis have been developed. In this case the Monte

Carlo simulation will be used. This is a statistical method that involves the use of regression and

related partial correlation coefficients. It can be described as a statistical method that simulates what

happens in the model for a certain quantified number of points. The end result will not be exact, but

it will be good enough to give reliable indications. This simulation method can handle complicated

systems with many parameters. An advantage of this simulation is that it simultaneously combines

both a sensitivity analysis and uncertainty. The Monte Carlo simulation enables one to introduce

uncertainty in the model’s input variables in order to measure statistically the impact this uncertainty

has on the output’s variables.

The program @Risk will be used to perform this Monte Carlo simulation. In lectures on LCC as part of

this master’s program, the advantages of this tool became clear. It is a program/tool that uses

Microsoft Excel to perform this analysis. It can be completely integrated into the spreadsheet used.

The program is able to run Monte Carlo simulations; it recalculates the spreadsheet model thousands

of times. Based on the random values from the @RISK functions that are entered, it samples/changes

the input data, after which the program records the resulting outcomes. The resulting outcomes of

the simulations can be visualized by different graphs.

Dissertation document B. Kemps Page 32

4 The purchasing process

4.1 Introduction

In the previous chapters insight is gained on the scope of LCC analysis and what input parameters are

needed to perform a decent LCC analysis regarding this thesis. In order to improve the purchasing

process of assets it is necessary to have a correct impression on the current policy of purchasing

assets. There must also be clarified what data is at hand and how this data is provided. When this

information is known, it becomes possible to point out expected improvements with the contribution

of LCC analysis. So in this chapter sub questions 4 and 5 will be handled.

4.2 Purchasing policy of SMEs

SMEs often lack unambiguous or clearly stated policies for purchasing new installations. The demand

for an investigation into the possibilities of changing or expanding certain processes is usually caused

by:

Obsolescence of the current installation

Problems regarding capacity

Newer and improved production processes

Higher demands of regulatory rules stated by government or branch organizations

Exploration of new markets requiring new installations

These motives can/will lead to investigations into the most suitable alternative solution to meet the

requirements. The next section describes the purchasing process common to many SME companies.

It is based on Veteka (appendix 6). The case studies as described in section 5 are also based on this

company.

Generally the management team is responsible for the purchase of a new installation. When a

certain demand is signalized, they will start exploring the different possibilities.

When it concerns an existing installation they will investigate the possibilities for updates and a

complete overhaul. Usually this specific part of research is not very time-consuming, because of the

age of the asset concerned. The asset is usually outdated to such an extent that investing in a

complete overhaul and updates is simply too expensive. To come to this conclusion they mainly rely

on their own expertise. When there is some doubt about the feasibility of a certain overhaul or

update in relation to a complete new installation, they just make a phone call to one of their

suppliers for some indicative price settings. In those cases it is very easy to conclude whether or not

further investigation is advisable.

When the decision has been made to investigate the feasibility of a new installation, a list of

requirements will be set up. Every person who will become directly involved with the new

installation has the possibility to share his findings and recommendations. All items of this list will be

evaluated and they will be given a priority level. This list will be discussed with the board of directors

so all parties are aware of what is expected.

Dissertation document B. Kemps Page 33

Because the technical lifespan of installations often exceeds twenty years, the management typically

prefers a supplier that can be trusted and is consistent. For this reason the board of SMEs prefers to

choose well-known and recommended brands. So they make a first selection based on experience

and brand of potential suppliers which they contact for an appointment to discuss the plans and

requirements. They listen to their ideas and perspective on the situation.

Agreements for a first offer are made. These offers are collected. The management individually

studies and compares them. When all offers have been looked into, the management and all internal

parties involved sit together to discuss and compare the different alternatives.

Offers which are obviously unable to meet the requirements are dropped. In those cases, the

representative is informed. He often requests a final chance to review his proposal. When he is able

to convince the management that his company can meet the requirements, the management gives

him this last chance. Meanwhile, negotiations with other representatives continue.

In practice, negotiation is an ongoing process, in which comparisons are made and details discussed.

In some cases, but not always, the different options are compared in an overview made in Excel. To

investigate the revenues a small calculation is made on paper or in Excel. The purchasing process is

very flexible and based on expertise.

As should be clear from this description, there are no specific rules and guidelines. Decisions are

mainly based on feelings, trust, and experience. Because of the long term relationships between the

company and employees and employees and suppliers, a considerable amount of specific knowledge

is available. This can be seen as one of the company’s strengths.

During the last 15 years, however, there has been a revolution in the implementation and

combination of new technologies, including electronics and computers. [Emblemsvåg, 2003] This has

also affected the timber industries. In addition, the technological revolution in countries like China,

Korea and Taiwan has led to a new outlook on the purchasing process. Nowadays many “new”

constructors from foreign countries have proved their existence. Some of them have already existed

for more than 20 years and in most cases they are still growing every year. They have been able to

set up a dealer network, with a complete supporting service in Europe. A faster changing technical

environment and the emergence of new brands have led to a change in our familiar and safely

trusted environment. The existence of new makes and faster developing technologies can therefore

no longer be ignored. In future, these developments will have to be taken into account during the

purchasing process.

4.3 Reliability, availability and maintainability of current installations

Reliability can be defined simply as the probability that a system or product will perform in a

satisfactory manner for a given period of time when used under specified operating conditions.

There are four key elements which are extremely important when determining the reliability of a

product/system or asset:

Dissertation document B. Kemps Page 34

1. Probability: this is usually stated as a fraction or a percentage signifying the number of times

that an event occurs, divided by the number of trials.

2. Satisfactory performance: this is usually presented in the specification of a system that is

required. It concerns qualitative and quantitative factors.

3. Time: this is one of the most important elements when determining reliability. For a

particular function one must be able to predict the probability that an item will survive

(without failure) for a designated period of time. Often the reliability of a system is defined

as the Mean Time Between Failure (MTBF), Mean Time To Failure (MTTF) or Mean Time

Between Maintenance (MTBM).

4. Specified operating conditions: these are the conditions in which the system/product or asset

must be able to operate. These conditions include environmental factors, such as humidity,

temperature, vibration, etc.

Availability: within the context of systems engineering, availability can be defined as a measure of

system readiness. It can be expressed as a probability that an item or system is in an operable state.

In most cases, the probability is expressed as a percentage.

Maintainability: maintainability is the ability of an item to be maintained. It can be defined as a

characteristic in design that can be expressed in terms of maintenance frequency factors,

maintenance times and maintenance costs. Maintainability is a design parameter. A system should

be designed in such a way that it can be maintained without large investments of time, cost, or other

resources.

The maintenance itself includes all actions necessary for retaining a system or product in, or restoring

it into, a serviceable condition. Maintenance can be divided into two categories, viz. corrective

maintenance and preventive maintenance.

Reliability and maintainability have a huge impact on the success of the system in fulfilling its

intended purpose. When designing or implementing a new installation it is therefore important be

aware of the characteristics that affect reliability and maintainability.

An analysis of reliability, availability and maintainability together can be defined as a RAM-analysis. It

is typically used to predict the performance of processes and systems and to provide a basis for the

optimization of such systems. In such analyses the key performance indicator is availability, which is

the fraction of time that the system is fully functional. The purpose of this analysis is to investigate

and point out those items that have the greatest effect on availability. Afterwards it becomes

possible to carry out further investigation into those items in order to redesign certain aspects to

optimize the performance of the installation. [Blanchard, 2004]

In SMEs, data collection regarding availability and reliability of installations is scarce. Information can

only be derived from the maintenance that has been done on a certain installation in the past. Thus,

maintenance is assessed for each installation separately. In addition, these two aspects are evaluated

based on expertise and feelings. If an installation becomes unreliable or availability becomes critical,

the people in charge will determine what the exact problem is. Therefore, performing a reliable

RAM-analysis is often impossible.

Dissertation document B. Kemps Page 35

4.4 Improvements expected from implementing LCC analysis

One of the stated sub questions is to list expected improvements which will result from

implementing an LCC analysis. The current purchasing process has been described in paragraph 4.1;

with the theory which has been reviewed, the following outcomes are expected.

An LCC analysis is a data based decision making approach. When parameters are correctly fulfilled, it

generates hard decision making data. It makes it much more difficult for stakeholders and

management to doubt whether the right decision will be made. In addition, it also can help to

convince banks to lend money for the project at hand.

Because LCC implies that all cost drivers are taken into account, it is to be expected that a number of

hidden costs will emerge from the analysis.

With the program @risk, it is possible to determine the uncertainty and sensitivity of the different

input parameters. The outcomes on the uncertainties and sensitivities can result in new perspectives

and possibilities in order to reduce the uncertainty, sensitivity and the scale of the total costs.

It is to be expected that when, through the implementation of LCC, hidden costs emerge which have

to be taken into account during the purchasing process, more cost-effective alternatives will win out

on the traditional purchasing process.

Dissertation document B. Kemps Page 36

5 Cases

5.1 Description of the cases

In order to test the hypothesis, four life cycle analyses have been investigated. A description of the

cases will be given in this chapter. All these cases are practical examples from the company Veteka

(appendix 6). In the next chapter, the relevant analyses will be described and the results will be

discussed.

5.1.1 Weinig versus Leadermac

When different aspects of the pilot company, Veteka, are analyzed, it is clear that high standards are

applied throughout. Veteka’s policy has always demanded high quality installations. As described

earlier, some new makes have entered the world with relation to the purchasing process. These

makes are often a lot cheaper than the traditional, well-known brands. Because they have proved

their existence, the management can no longer ignore them. For this reason, this study will use LCC

to compare alternative moulders.

Traditional moulders at the pilot company have been made by two companies, Weinig and Waco.

About 7 years ago, Waco has been taken over by Weinig. The two brands still exist, but technologies

and price settings have been mutually adapted. The dealer for these brands is De Groot, located in

Rosmalen. An upcoming brand of moulders in Europe is “Leadermac”. The company is located in

Taiwan. The first time this brand crossed Veteka’s path was about 10 years ago at a trade fair in Italy.

On each fair the management visited, the expansion of the brand “Leadermac” was noted and, over

the years, the technical possibilities of its machinery have continuously grown. The dealer for

“Leadermac” in the Netherlands is VOS, located in Hendrik-Ido-Ambacht and not unfamiliar to

Veteka. VOS previously dealt for Waco but, due to the take-over of Waco by Weinig, lost his

dealership for the company.

In the first case a moulder from Weinig will be compared with a moulder from Leadermac. To

conduct this analysis information has been requested from the dealers.

5.1.2 Moulding Cutter Head

A few years ago a new moulder was purchased. De Groot in Rosmalen was contacted with a view to

purchasing a new Weinig. The requirements concerning possibilities, variations and options were

made clear. Weinig’s factory (located in Germany) was visited twice, with a view to clearly discussing

and looking into the different alternatives. This also applies to a new system used for the moulding