1 A Market for Lemons in Mutual Fund Management Michael J. Gibbs 1 Andrew A. Lynch 2 Khaled Obaid 1* Kuntara Pukthuanthong 1 Abstract We use mutual fund manager hiring decisions as laboratory for examining a “lemons” failure in the market for agents (Akerlof, 1970). In a functioning market, managers with skill should move to funds where they can capitalize on that skill. However, constraints placed on managers by mutual funds induce noise into the skill signal sent by returns. We find that prior performance is only an important component of the hiring decision when managers earned them at funds with low constraints (high tracking error). Managers at funds with high constraints (low tracking error) have to substantially outperform managers at low constraint funds to be hired by a low constraint fund. We interpret this as evidence consistent with a lemons failure in the market for mutual fund managers. 1 Robert J. Trulaske, Sr. College of Business, University of Missouri, Columbia, MO 65211 2 College of Business Administration, University of Mississippi, University, MS 38677 * Corresponding author: [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

A Market for Lemons in Mutual Fund Management

Michael J. Gibbs1

Andrew A. Lynch2

Khaled Obaid1*

Kuntara Pukthuanthong1

Abstract We use mutual fund manager hiring decisions as laboratory for examining a “lemons” failure in the market for agents (Akerlof, 1970). In a functioning market, managers with skill should move to funds where they can capitalize on that skill. However, constraints placed on managers by mutual funds induce noise into the skill signal sent by returns. We find that prior performance is only an important component of the hiring decision when managers earned them at funds with low constraints (high tracking error). Managers at funds with high constraints (low tracking error) have to substantially outperform managers at low constraint funds to be hired by a low constraint fund. We interpret this as evidence consistent with a lemons failure in the market for mutual fund managers.

1 Robert J. Trulaske, Sr. College of Business, University of Missouri, Columbia, MO 65211 2College of Business Administration, University of Mississippi, University, MS 38677 * Corresponding author: [email protected]

2

I. Introduction

The identification and mitigation of agency costs has been an important component

of the finance literature for over four decades. To reduce these costs, principles can either

monitor and incentivize their chosen agents or hire agents with sufficient ability to perform.1

The problem faced by principles is that both methods are costly, with costs proportional to

the level of information asymmetry around measuring agent performance. Corporate boards

face uncertainty when estimating a CEO’s ability both before and after hiring them while

investors receive noisy signals of portfolio managers’ skill through returns.

If the information asymmetry around measuring agent ability is high enough the

market for hiring agents could fail. Labeled a ‘lemons’ problem by Akerlof (1970), such

failure occurs when the signal of the quality of goods becomes sufficiently noisy that the

trading of higher quality goods slows or ceases. Applied to the market for agents, a lemons

problem would see decreased movement in high ability agents to the principles who need

that ability. The market for lemons has been studied in numerous settings.2 However, due to

the inherent difficulty in quantifying the ability of managers, it has yet to be examined in the

agent hiring decision. While there is considerable uncertainty in measuring the ability of

corporate managers (Pan, Wang, and Weisbach, 2015), there is general consensus that the

ability of portfolio managers should manifest, to some extent, in returns.3 What is unknown

1 For monitoring and incentivizing see e.g., Ross (1973), Jensen and Meckling (1976), Harris and Raviv (1979), Holstrom (1979), and Jensen and Murphy (1990). For hiring agents with ability see e.g.,Brennan (1994), Almazan, Brown, Carlson, and Chapman (2004), and Carlin and Gervais (2014). We note that principles may both monitor and hire skilled agents, however monitoring costs are inversely related to agent skill. 2 See e.g., Bond (1982), Gibbons and Katz (1991), Rosenman and Wilson (1991), and Downing, Jaffee, and Wallace (2009). 3 See e.g., Chevalier and Ellison (1997), Sirri and Tufano (1998), Edelen (1999), Berk and Green (2004), Kacperczyk, Sialm, and Zheng (2008), and Barras, Scaillet, and Wermers (2010).

3

is whether the signal conveyed through returns is clear enough to produce a separating

equilibrium in hiring, accurately matching managers and investors based on ability.

In this paper we use mutual fund managers as a natural laboratory to test for a lemons

failure in the market for agents. Mutual funds are an ideal setting for this test for two distinct

reasons. First, though returns are accepted as a measure of ability, they are a noisy signal.4

Second, there is cross-sectional dispersion in the demand for fund manager ability. Many

funds explicitly or implicitly index a large portion of their assets (Cremers and Petijisto,

2009; Cremers, Ferreira, Matos, and Starks, 2016) or place restrictions on investments,

which constrain active management (Almazan et al., 2004; Renneboog, Horst, and Chang,

2011), reducing funds’ need for managerial skill. We exploit these two features of the mutual

fund market to examine the movement of managers between high constraint (low ability

need) and low constraint (high ability need) funds.

Jensen and Meckling (1976) formalize the problem of divergent interests between

principals and agents and the externalities, which emerge from restrictions designed to align

agent’s incentives with principle interests. Applied to investment management, investors

(principal) delegate their money to mutual fund managers (agent) for professional

management, diversification, and liquidity purposes. Given incentives to shirk or risk-shift

(Stoughton, 1993; Chevalier and Ellison, 1997), investors contract to minimize those agency

costs (Almazan et al., 2004). Additionally, investors may restrict the magnitude of active

management as a way to mitigate agency costs. Active funds allow discretion for managers

to deviate from the market portfolio to trade on mispricing. Activism requires skill and is

4Hence the literature on distinguishing between luck and skill (see e.g., Kosowski, Timmerman, Wermers, and White, 2006; Fama and French, 2010).

4

more risky than passive management. Therefore, according to optimal contracting theory,

investors should allow more discretion (less constraint) to managers who are skilled and

less (more constraint) to those who are unskilled.

Not all agency conflicts are intentional. Sometimes agents have a false sense of skill.

For instance, overconfidence among mutual fund managers leads to increased turnover

(Puetz and Ruenzi, 2011) and lower returns (Eshraghi and Taffler, 2012). These behavioral

biases necessitate a clear signal of skill to low constraint funds when hiring, as placing a low

skill manager in a low constraint environment could lead to abnormally low returns.

Conversely, funds with high constraints have less downside risk in hiring. The potential

losses to low skill managers are less than in their low constraint counterparts.

It is difficult to signal skill in high constraint funds. True skill is unknown to investors

and potentially unknown to managers themselves. Thus, investors are forced to infer skill

through the past performance of managers. While past performance is not a perfect proxy

for skill, it is the most observable characteristic to the investor. High constraint funds have

returns mechanically closer to their objective benchmark than low constraint funds,

meaning their returns convey less information about manager skill. Conversely, since there

is more flexibility to deviate from benchmarks in low constraint funds, it is easier for their

managers to reveal skill (both positive and negative) to themselves and investors. The

consequence is that, holding all else constant, given two managers with identical skill and

performance a low constraint fund is more likely to hire the manager already managing a

low constraint fund than the manager at a high constraint fund. It becomes more difficult for

skilled managers to leave the high constraint funds for low constraint funds than it is for

5

skilled managers to stay in the low constraint funds because of limited availability to signal

skill in the high constraint funds.

There are strong incentives for skilled managers to leave high constraint funds. Sirri

and Tufano (1998) show a convex relationship between fund flow and performance,

revealing that inflows are more sensitive to high returns than outflows are to low returns. A

skilled manager at a low constraint fund will be able to earn higher returns than at high

constraint fund and, attracting inflows, will increase their compensation (Berk and Green,

2004). Additionally, investors, seeking active management, choose to allocate assets to

managers with high skill signal. In a fully functioning agent market, investors and managers

perfectly match on skill.

However, the noise in the return signal created by fund constraints could reduce the

quality of the market for fund managers. Akerlof (1970) explains how, when quality is not

easily discernible, externalities drive down the quality of an entire market. When rational

consumers are unable to discern the quality of two competing products, they must assume

that they both have the low quality and as such are only willing to pay for the low quality

product. As a result, suppliers of high quality products are driven out of the market. Applied

to fund managers, we expect that investors will view all managers of high constraint funds

as unskilled when making hiring decisions. Only through an extraordinarily large signal (i.e.

extremely high returns) will skilled high constraint manager be able distinguish themselves

from their low skilled competitors.

A lemons failure in the market for managers would have several consequences. First,

skilled managers who should be managing low constraint funds are essentially stuck in high

constraint funds. Second, low or negatively skilled managers who should be removed from

6

their positions in the high constraint funds remain. While investors of high constraint funds

may be amenable to retaining skilled managers they otherwise would lose, both of these

consequences create a deadweight loss in the investment community.

We examine 3,537 employment changes across US Equity Mutual Funds between

1980 and 2014 and find evidence consistent with a lemons failure in the market for

managers. On average, we find a significant inverse relationship between performance and

constraint when managers move between funds. In other words, when managers move,

those with higher returns move to funds with lower constraints. However, this result is

driven entirely by low constraint managers. Returns appear to be an important signal of skill

only when a manager runs a low constraint fund. Additionally, we examine the probability

of a low constraint fund hiring from either another low constraint fund or a high constraint

fund. High constraint managers have to substantially outperform relative to low constraint

managers to be hired by a low constraint fund. The apparent noisiness of the return signal

extends outside the hiring decision. Examining cash flows to all equity funds, we find the

flows to high constraint funds are less sensitive to performance than the flows to low

constraint funds. Overall, we conclude that the noisiness of the return signal is dependent on

the constraint level of the fund and impacts both hiring and cash flows.

This paper makes several contributions to the agency and mutual fund literatures. We

are, to our knowledge, the first paper to examine how information asymmetry causes a

failure in the market for agents. Though we use mutual funds for our empirical tests, we

consider our results applicable across numerous agent hiring settings. Concerning the

mutual fund literature, we make two distinct contributions. First, we add to the

understanding of the career concerns of fund managers (see e.g., Chevalier and Ellison, 1999)

7

and how the importance of past performance is conditional on where it was generated.

Second, we present evidence that the asymmetric cash flow and performance relation found

in the literature (see e.g., Sirri and Tufano, 1998) is conditional on the constraints placed on

the fund. High constraint funds have a significantly different relation between flows and

performance than low constraint funds.

II. Literature Review

A. The Market for Lemons

A considerable literature has empirically examined the existence of an Akerlof (1970)

lemons failure in a wide variety of markets. A lemons failure can become evident in

potentially two different ways: price and quality. Genesove (1993) and Fabel and Lehmann

(2000) find price differentials across different types of sellers in the used car market.

Rosenmann and Wilson (1991) find such differentials across heterogeneous and

homogeneous cherry lots and Gibbons and Katz (1991) find wage differentials across

workers hired following plants closing verses those laid-off.

However, our study is more related to the quality implications of a lemons failure.

Greenwald and Glasspiegel (1983) find fewer skilled slaves being auctioned in Pre-Civil War

New Orleans than exist in the overall slave population. Injured baseball players are more

likely to move to a different team at the end of their contract than healthy players (Len,

1984). And information asymmetry appears to have nearly completely eliminated Chinese

IPOs in the US in recent years (Beatty, Lu, Lou, 2014).

The presence of adverse selection and information asymmetry does not necessitate a

lemons market failure. Spence (1973) suggest sufficient external signal validation can

8

partially or entirely mitigate a lemons problem. For instance, Rosemann and Wilson (1991)

find that in the repeated game environment of the cherries market, firms which repeatedly

sell higher quality heterogeneous lots are able to command higher prices in the future

without separating out high and low quality cherries. Concerning quality, Bond (1982) finds

no higher maintenance costs among used truck purchases than comparable new truck

purchases, suggesting car dealers are able to accurately signal used vehicle quality to buyers.

B. Career Concerns of Mutual Fund Managers

Managers, concerned with ex post settling up, are incentivized to exert effort and

strive to meet principle objectives (Fama, 1980). However, this also means their incentives

are tied to the probability they either keep their job or can acquire a different, higher paying

job. Avery and Chevalier (1999) argue that young managers, insecurity in their jobs and

future prospects, will forgo idiosyncratic risk and are more likely to herd while older

managers, more secure in their jobs, will take more risk. The empirical literature since then

has been largely consistent with this claim (see e.g., Chevalier and Ellison, 1999; Hong, Kubik,

and Solomon, 2000; Lamont, 2002).

The current literature suggests managers are allocated by skill to jobs where that skill

can be utilized most effectively. Fang, Kempf, and Trapp (2014) find fund families move

skilled managers to funds which invest in more inefficient asset markets (i.e. high yield fixed

income). The best performing mutual fund managers are often hired to hedge funds

concurrently (Deuskar, Pollet, Wang, and Zheng, 2011). Additionally, funds appear to

attempt to remove unskilled managers by firing managers following periods of poor

performance (Khorana, 1996; Chevalier and Ellison, 1999).

C. Tracking Error as a Proxy for Constraints

9

In this paper we use tracking error as a proxy of fund constraints placed on managers.

Traditionally, tracking error has been used in the mutual fund literature as a measure of

active management (see e.g., Chan, Chen, and Lakonishok, 2002). We use it here in a very

similar way, except we add the assumption that managers are incentivized to be as active as

possible up to the point they encounter binding constraints. Managers face considerable

upside to taking risk (Chevalier and Ellison, 1997; Sirri and Tufano, 1998) while at the same

time being exposed to downside risk only in limited circumstances (see e.g., Chevalier and

Ellison, 1999). Managers, taking as much risk as is allowed by either the fund or their own

risk tolerance, will naturally deviate from their benchmark as much as possible until

constraints limit their risk-taking.

There are three ways in which a manager could be constrained. First, a fund could

place explicit constraints on asset classes or trading strategies (Almazan et al., 2004). Such

constraints would, to some extent, mechanically limit a manager’s ability to deviate from

their fund’s underlying benchmark. Second, funds could place implicit constraints on

managers. For instance, there may be informal limits on the systematic risk of the portfolio

or trading strategies (i.e. short selling, leverage) which are technically allowed but are

discouraged.5 Such constraints, while not evident in fund filings, would also result in less

deviation from the underlying benchmark.

Finally, managers could constrain themselves. There is substantial evidence in the

mutual fund literature of “closet indexing” funds (see e.g., Cremers and Petajisto, 2009; Elton,

Gruber, and Blake, 2012; Cremers et al., 2013). These funds are categorized as active, yet for

5 For instance, Chen, Desai, and Krishnamurthy (2013) find that while 63% of actively managed equity mutual funds were allowed to short in 2009, only 7 percent chose to utilize short selling.

10

reasons not explained by explicit constraints, have returns which closely match their

benchmarks. Given the previously discussed incentives to take risk, the only reason a

manager would closet index would be implicit constraints placed by the fund or personally

imposed constraints due to a lack of skill. Given low skilled managers may be fired (Khorana,

1996) or may expect to, over time, lose money due to outflows (Berk and Green, 2004) they

are actually incentivized to obfuscate the signaling of their skill by reducing their return’s

deviation from their benchmark.6

Empirically disentangling implicit from self-imposed constraints is difficult, if not

impossible. This difficulty creates an adverse selection problem for funds when they hire. If

funds could identify explicit and implicit constraints, they could limit their hiring problem to

an information asymmetry problem by refusing to hire managers with self-imposed

constraints.7 However, low skill managers can self-select into the high constraint subsample,

effectively masking their ability. As these implicit and self-imposed constraints are a vital

part of the potential lemons failure, we require a measure which captures all three

constraints.8 We believe tracking error meets this requirement.

III. Data and Empirical Method

A. Manager Employment History

We obtain manager employment history data from Morningstar Direct. For funds in

Morningstar Direct, we have a list of current and former managers and tenure dates for those

6 Such incentives are consistent with the window dressing literature (see e.g., Lakonishok, Shleifer, Thaler, and Vishny, 1991; Brown, Harlow, and Starks, 1996). 7 Such a strategy could still create a lemons failure, but would require substantially more information asymmetry to impact the quality of the market. 8 As Almazan et al. (2004) measures only explicit constraints, its use of N-SAR filings as a constrain measure are not appropriate for this study.

11

managers. This gives us a time series of each manager’s employment at each fund, including

overlap if multiple funds are managed simultaneously.

B. Mutual Fund Returns

We collect fund characteristics, returns, and expense ratio data from the CRSP

Survivor-Bias-Free US Mutual Fund database. We filter funds in our sample by using the fund

style database from CRSP. We use the Lipper, Strategic Insight, and Wiesenberger

classification codes to select funds that are classified as domestic equity. If the fund is

unclassified or is missing a classification from CRSP, we keep funds with at least 80% of

assets invested in common stock (Kacperczyk, Sialm, and Zheng, 2008). If percentage of

common stock is not available, we keep unclassified or missing classification funds in our

sample as long as they use one of the 19 equity benchmarks (see "Benchmarks" section). We

start with returns net of total expenses and add back expenses to get raw returns that include

dividends and capital gains. In case of multiple share classes, we value-weight raw returns

and expense ratios for the different share classes using one period lagged total net assets

(TNA) to compute fund-level values.

C. Benchmarks

In order to compute tracking error and risk-adjust returns, we obtain returns of

benchmarks used by the funds in our sample. For each of the funds in our sample, we collect

information about the self-designated benchmark from Morningstar. 9 Primary and

secondary benchmark variables are provided by Morningstar. However, since data for the

secondary benchmark is not well populated, we use the primary benchmark. One concern

9 Some studies (see e.g., Cremers and Petajisto, 2009) optimally identify benchmarks using the lowest tracking error or active share instead of the stated benchmark. Given our use of tracking error as a proxy for constraints, we believe the stated benchmark is more appropriate.

12

with the benchmark data from Morningstar is that it is cross-sectional. However, this is not

a problem because benchmark changes are rare (Sensoy, 2009).

We keep funds that use one of 19 major equity indexes from S&P/Barra, Russell, and

Wilshire.10 These benchmarks cover many equity investing styles and sizes. Of funds that are

identified as actively managed, diversified domestic equity mutual funds according to

Morningstar, 91.6% are covered by 12 of the 19 benchmarks in our list (Sensoy, 2009). We

obtain those benchmark returns, including dividends, from Thomson Reuters Datastream.

We collect benchmark returns from 1980 till 2014.

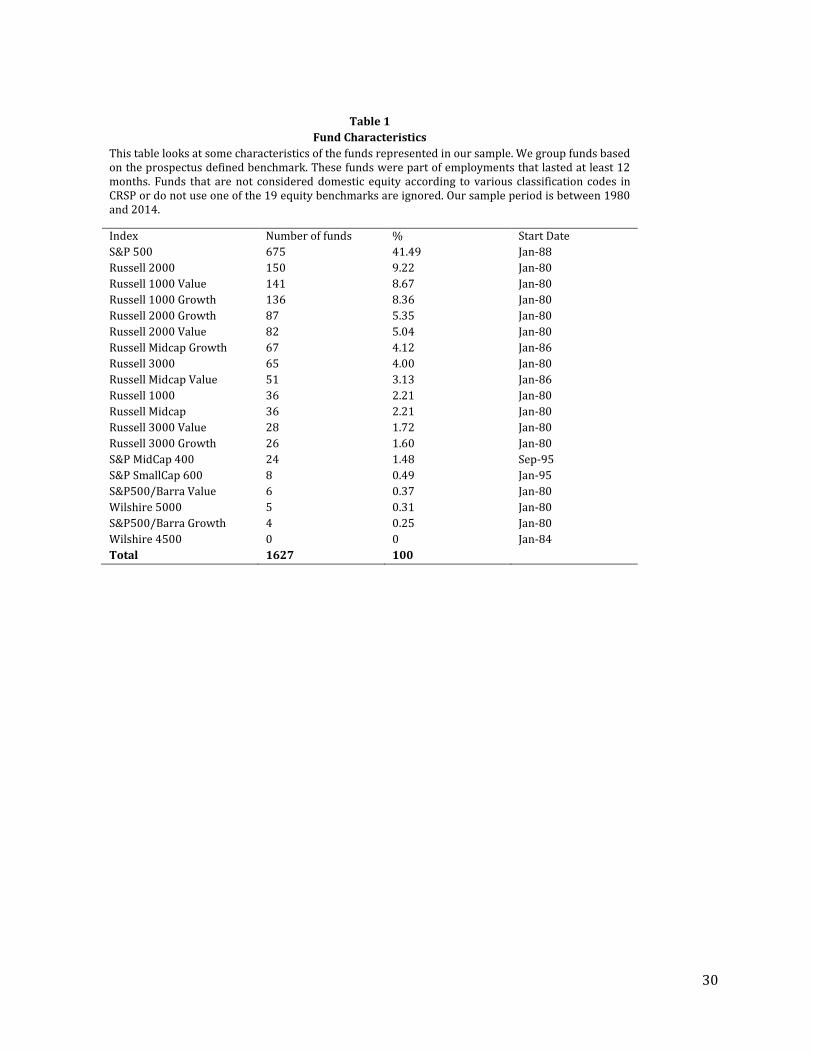

Our sample includes 1,627 distinct mutual funds. According to Table 1, most funds in

our sample use the S&P 500 (41.49%) as a benchmark, followed by Russell 2000 (9.22%),

Russell 1000 Value (8.67%), and Russell 1000 Growth (8.36%). 11 . Overall, our sample

includes funds from all the major equity caps and styles. Most indexes in our study start

reporting in 1980. However, some indexes such as the S&P MidCap 400 and S&P SmallCap

600 start reporting in 1995. Sensoy (2009) uses a sample of 1,815 actively managed,

diversified domestic equity mutual funds from Morningstar that use one of 12 benchmarks,

all of which we include in our study. His sample period is 1994–2004. Of the funds in their

sample, 44.4% use the S& P500, 13.3% use the Russell 2000, 5.9% use the Russell 1000

Growth, and 5.6% use the Russell 1000 Value. Our sample has fewer funds likely because we

require that the fund has employment history data available and that it has at least one

employment that lasts at least 12 months. Also, we require funds to have returns in CRSP

10This is the same list used by Cremers and Petajisto (2009). 11 While we include the Wilshire 4500 as in Cremers and Petajisto (2009), once we screen for employment changes none of the remaining funds in our sample use it as their benchmark.

13

and we identify funds using classification codes in CRSP while Sensoy (2009) uses returns

and fund classifications from Morningstar.

D. Identifying Employments

We create an employment identifier that changes anytime a manager drops or adds a

fund. When the employment identifier changes for a given manager, we create a one year

window pre- and post-employment change. We require all employments to last at least 12

months in order to ensure that we have a long enough sample to accurately measure fund

level constraints but short enough time period that we are not biasing our results to

survivors.12 We end up with 3,537 employment changes. In some cases, there is a gap from

when a manager terminates current employment and transitions to a new employment. One

of the ways in which managers have a gap between employments in our sample is when

managers change employment from equity to non-equity funds. In such cases, they exit our

sample but come back later when they re-enter the equity mutual fund market. As an

additional robustness check, we evaluate employments for which managers may not re-

enter after leaving domestic equity. For the no-gap sample, we have 2,223 employment

changes. We run our main tests using the sample of employment changes with gaps allowed;

however, we also use the sample with no-gaps for robustness.

According to Panel A of Table 2, the average number of employment changes per

manager is 2.96 with a standard deviation of 1.29. We have 1,803 managers that have more

than one employment, while the majority of managers in our sample, 3,361, only have a

single employment. In total we have 5,164 managers represented in our sample. In Panel B,

12 In unreported tables we rerun our analyses across both shorter and longer time periods pre- and post-

employment change and find qualitatively similar results.

14

the length of employments for managers that have a single employment is 66.68 months. For

managers with multiple employments, the average length of each of their employments is

42.56 months. To compute the career length of managers, we assume the career of the

manager started when they entered our sample. To provide an intuitive understanding of

the rate at which managers change employments, we divide the number of employment

changes per manager by the length of the career for each manager in months. In Panel C, we

see that those managers with the longest careers (top quintile) change employment on

average every 8.91 years. While managers with the shortest career (bottom quintile) change

employment on average every 1.7 years.

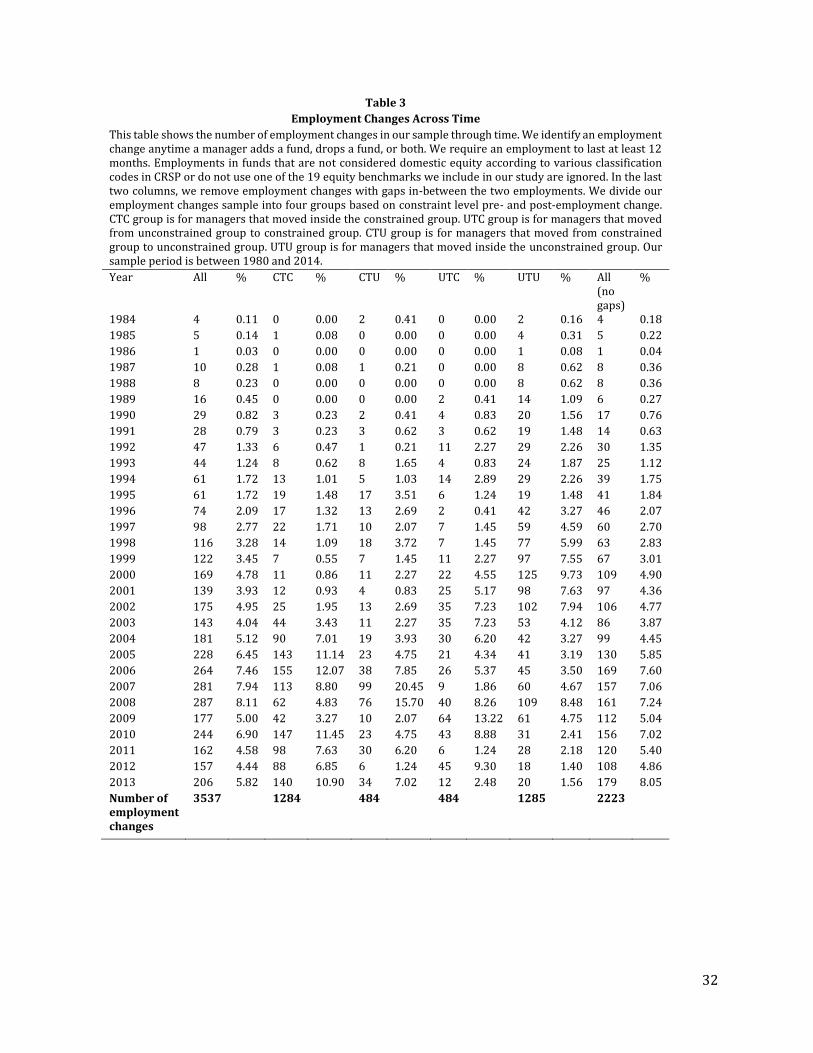

In Table 3, we look at the number of employment changes over time. Consistent with

the large growth in number of funds over our sample period, we find increased fund hiring

over time. There is a noticeable spike in the number of employment changes around the

financial crisis (2007-2008), which is expected as managers are likely laid-off or shift their

portfolios to better match the market demand. For example, during volatile markets we often

see flight to quality. Managers likely leave equity funds for money market funds to better

meet the demand of investors.

Although our time period of our study covers 1980 through 2014, we only report

employment changes from 1984 through 2013 because our first and last employment

change happen in 1984and 2013, respectively. The average number of employment changes

per year for our entire sample (excluding employments with gaps) is 118 and the standard

deviation is 90.8.

E. Key Variables

Constraint

15

We use tracking error as our proxy for fund constraint. Tracking error is calculated

as the standard deviation of the difference between fund returns (Rfund,t) and fund's

benchmark index returns (Rindex,t) over time:

Tracking error = Stdev[Rfund,t− Rindex,t]

As an example, the manager of an S&P 500 index fund is obligated to mimic the S&P 500

index with very little room to deviate from it in search for mispriced securities (high-

constraints create low-tracking error). An aggressive growth fund that allows the manager

discretion to select any stock in the Russell 1000 allows more opportunities for the manager

to deviate from the benchmark in search of mispriced securities (low-constraints create

high-tracking error).

There are two alternate ways which, on face value, could measure constraints.

Cremers and Petajist (2009) measure tracking error as the standard deviation of the residual

from the index model, capturing only idiosyncratic deviation from benchmark returns.

However, limiting managers ability to take systematic risk is a constraint investors could

place on managers. Additionally, one could propose using the R2 from the index model to

measure constraints. This method suffers from the same problem as the residual standard

deviation, capturing only idiosyncratic deviation from the benchmark. Our measure of

tracking error captures both systematic and idiosyncratic constraints placed on fund

managers.

Another method of measuring activism is Active Share, which focuses on deviation

from index holdings (Cremers and Petajisto, 2009). Although Active Share helps better

capture different dimensions of activism, the data requirement of calculating Active Share

(quarterly holdings data) drastically shrinks our sample. Almazan et al. (2004) use mutual

16

fund SEC filings (N-SAR) to measure financial constraints of mutual funds. However, financial

constraints are only one dimension of constraints on mutual fund managers.

The first step to computing employment-level tracking error is to compute an

employment-level returns net of benchmark returns by taking the value-weighted average

of returns net of benchmark returns using monthly TNA for all the funds in the same

employment each month. Second, we take the time-series standard deviation of

employment-level returns net benchmark returns over 12 months pre- and post-

employment change and this is employment-level tracking error pre- and post-employment

change, respectively. The difference between employment-level tracking error pre- and

post-employment change is our main dependent variable, diff_tracking.

For some of our tests we divide employment changes based on the constraint level of

pre- and post-employment change. For each employment change, we use pre- and post-

employment change tracking error windows as our proxy for constraint. We rank all pre-

employment change tracking error windows into constrained (low tracking error or high

constraint) and unconstrained (high tracking error or low constraint) groups based on the

median pre-employment tracking error window. We do the same procedure for the post-

employment change tracking error windows. We classify employments into four groups:

employment changes that resulted in a manager moving within unconstrained group (UTU);

within constrained group (CTC); from unconstrained to constrained employment (UTC); and

from constrained to unconstrained employment (CTU).

Performance

To compute employment-level returns, we first risk-adjust monthly fund returns by

ranking the returns into quintiles each month against their peers in the same benchmark

17

group. We then take the value-weighted average of the ranked returns across funds in the

same employment each month using monthly TNA. 13 Our key independent variable is

returns and is defined as the geometric mean of the employment-level ranked returns for the

12 months pre-employment change. diff_returns is the difference between the geometric

mean of the ranked returns pre- and post-employment using a 12 month window.

Size

To compute an employment-level monthly TNA, we sum the TNA of the funds based

on the employment identifier to get monthly employment-level values. The difference

between pre- and post-employment change average of monthly employment-level TNA over

12 month windows is diff_mtna.

IV. Results

A. Returns and Constraint after an Employment Change

In Table 4 we report the results of change in manager constraint and returns when

an employment change takes place. Change is calculated as the post-employment value

minus the pre-employment value. We evaluate changes in returns and constraint pre- and

post-employment change in order to determine broadly whether manager characteristics

are affected by employment change. We proxy for constraint using the change in 12 month

tracking error measured across net benchmark returns. Panel A reports results based on the

sample that allows gaps in manager employments, and Panel B reports results when

employment gaps are not allowed.

13 In untabulated results, we equal-weight returns and find qualitatively similar results.

18

The first three rows of each panel in Table 4 report results of differences in means of

benchmark ranked returns (diff_returns), raw returns (diff_returns_raw), and tracking error

(diff_tracking)pre-and post-employment change. The fourth through sixth rows of each

panel report the results of differences of the absolute values of means of benchmark ranked

returns, raw returns, and tracking error pre-and post-employment change. We find that the

change in benchmark ranked returns and raw returns of the manager is insignificant

following an employment change; however the constraint level of a manager does change.

When a manager alters their employment (from a more constrained to less constrained or

vice versa) the post-employment change constraint decreases on average. Rows four

through six show that the absolute value of benchmark ranked returns and raw returns does

change when a manager changes employment. This, when interpreted in conjunction with

the results from the first three columns, may imply that when managers underperform they

underperform by more after a change in employment and that when they over perform pre-

employment change they over perform by more post-employment change, but that they

cancel each other out. For robustness, we show the same test using the employment change

sample with no-gaps. Our results do not change.

B. Skill Signal and Hiring Decisions

In Table 5, we evaluate the relationship between performance and future constraints

in order to examine whether over performing managers transition to less constrained

employments, while underperforming managers transition to more constrained

employments. The motivation lies in the belief that if a manager feels over-employed, he or

she will attempt to hide his or her skill level by moving to a more constrained fund in the

future where skill signal is more noisy, while a manager who feels under-employed will

19

attempt to showcase his or her skill in the future by moving to less constrained fund where

skill signal is less noisy.

To empirically evaluate this prediction we regress change in tracking error

(diff_tracking) on past benchmark ranked returns at every employment change. In Panel A

we include all employment changes and in Panel B we include only employments that have

no gaps. Model 1 regresses change in tracking error on pre-employment ranked returns. In

order to remove the effects that growth in assets arise from outperformance (Berk and

Green, 2004) we include the control variable for change in total net assets in Model 2. Models

3 and 4 additionally include year and manager fixed effects respectively. We use year fixed

affects to control for changes in trends as well as trends in the availability of data and

manager fixed effects to control for unobservable manager characteristics.

The results across all four models (across both Panel A and Panel B) show that there

is a statistically significant relationship between pre-employment change returns and pre-

to post- employment change tracking error. The relationship is positive, implying that, on

average, when a manager outperforms relative to peers he or she will transition to lower

constraint employment and when they underperform relative to peers they will transition

to more constrained employments. This follows our theory that managers will self-select

into constraint areas that showcase or hide their skill based on how well they have

performed in the past. Additionally, change in total net assets shows up across all models as

negative and significant. This is as is expected given Berk and Green (2004); as a firm's (or

manager's) assets under management increases they are forced to engage in less activism.

C. Nosiness of Skill Signal

20

In Panels C and D of Table 5, we evaluate whether a manager's skill signal is less noisy

in unconstrained funds than constrained funds. In constrained funds, information

asymmetry gets in the way of observing skill of managers, making it difficult to detect and

reward talent of managers. We predict that managers in unconstrained funds will have a

better gauge of their skill than managers in constrained funds and so we should find that the

relationship between skill and constraint level in hiring is much stronger. However, we

should find that managers in constrained funds are less aware of their skill than managers

in unconstrained funds because of higher information asymmetry and so the relationship

between skill and constraint level in hiring is weaker.

This is what we find in Panels D and C of Table 5. We break employment changes into

two groups; unconstrained (low tracking error) and constrained (high tracking error)

groups based on pre-employment change tracking error over 12 months. We find that for

managers that change employment from constrained employments, the relationship

between returns prior to employment change and change in tracking error is not significant.

However, for managers in the unconstrained employments, we find that relationship

between returns prior to employment change and change in tracking error is significantly

positive.

In Table 6 we examine whether higher returns are required to leave constrained

funds to unconstrained funds because of the noisy signal of returns compared to returns to

remain in unconstrained group. We have speculated that over performance needs to be

higher for managers in constrained funds because the market treats their performance as

being affected by higher information asymmetry. To test this idea we reduce our sample of

employment changes to only those where the managers go from constrained funds to

21

unconstrained funds and those that stay in unconstrained funds. We run logistic regressions

to develop an intuitive understanding of how the probability of a move changes given your

pre-employment change performance.

Panel A of Table 6 shows results from the logistic regressions on the sample that

allows employment gaps and Panel B eliminates employments changes that have gaps.

Model 1, of each panel, is the basic logistic regression of the binary dependent variable of

moving from unconstrained to constrained (binary=1) and unconstrained to unconstrained

(binary=0) on the continuous variable of benchmark ranked returns (returns). Model 2

includes year fixed affects to control for changes in trends as well as trends in the availability

of data.

The results from both Panel A and B of Table 6, as well as Models 1 and 2 show that a

manager is significantly more likely to move from a constrained fund to an unconstrained

fund when the pre-employment change returns are higher than otherwise.

D. Cash Flow Sensitivity

Up to this point, we have examined the return signal only in the context of

employment changes. However, if the noisiness of the signal is driving our results we should

expect to see consistent evidence return signal noisiness outside of hiring. Fund investors

rely on return signals when allocating capital (Berk and Green, 2004; Sirri and Tufano, 1998).

If constrained fund returns are noisier signals of skill we should expect their cash flows to

be less sensitive to performance.

Table 7 reports the results of regressing annual fund net cash flows on the prior year’s

performance. Model (1) reports results without tracking error. As in Sirri and Tufano (1998),

we find an asymmetric relation between flows and performance. Performance, when in the

22

20th percentile or lower (LowRank), has a statistically significant but economically small

0.3057 relation with flows. That relation increases in magnitude for middle performance

(20th through 80th percentile, MidRank) to 0.4058. When funds have returns in the 80th or

higher percentile (HighRank) the relation increases to 1.7011. While the funds in our sample

are punished for poor performance, they are proportionally more greatly rewarded for high

performance.

That relationship changes substantially when we add in tracking error. For easier

interpretation of results, we rank tracking error into deciles annually across all equity funds.

Model (2) includes ranked tracking error both as an independent variable and interacted

with the three performance rank variables. There are three important results from including

tracking error. First, for funds with middle performance (MidRank), flow sensitivity

increases with tracking error. A highly constrained fund, with a tracking error rank of 0, has

a relatively small 0.2549 flow to performance relation. That coefficient increases by 0.0342

for each tracking error rank increase, meaning the least constrained funds (rank 9) have a

0.5627 flow to performance relation. This suggests investors find high constraint fund

returns less informative, just as funds themselves do when hiring.

The second important result out of Model (2) is that high constraint funds have flows

that are more sensitive to extreme performance than low constraint funds. The highest

constrained funds have a flow performance relation of 0.9494 (2.4505) to low (high)

performance, which declines by -0.1237 (-0.1351) for each increase in tracking error rank.

In the extreme, the lowest constrained funds have a flow performance relation of -0.1639 to

low performance and 1.2346 to high performance. It may appear counter intuitive for high

constraint funds to have flows more sensitive to performance. However, this is in fact

23

consistent with a noisier return signal. The only way for a noisy signal to convey information

is for it to be strong. The coefficient on MidRank, representing normal returns (the middle

60% of ranked returns), reveals that on average flows to high constraint funds are less

sensitive to performance. When returns become large enough in absolute terms to clear the

noise (LowRank and HighRank, the top and bottom 20%) investors are responsive to the

signal.

The third important result out of Model (2) is that the traditional asymmetric flow

performance sensitivity found in the literature appears to not be true for high constraint

funds. The highest constraint funds see greater sensitivity to returns when they are low

(LowRank coefficient of 0.9494) than when they are in the middle (MidRank coefficient of

0.2549). The accepted position in the mutual fund literature has long been that funds are

rewarded for high performance with inflows, but see small or zero outflows following poor

performance (see e.g., Chevalier and Ellison, 1997). This appears to only be true for low

constraint funds.

Overall, we interpret these cash flow sensitivity results as consistent with the returns

of high constraint funds being a noisier signal of managerial skill than the returns of low

constraint funds.

V. Conclusion

The role of information asymmetry in the market for agents is difficult to measure but

vital for understanding and mitigating agency costs. We use the market for mutual fund

managers as a natural laboratory for examining the effect signal noise has on the quality of

the hiring process. Returns are an important, but noisy, signal of fund manager ability. The

24

noisiness of that signal is also dependent on the constraints placed on managers, either by

their funds or by themselves. We exploit this cross-sectional dispersion in signal noise to

examine the role of past performance in hiring.

We find that while past performance is an important factor in the manager hiring

decision, past returns appear to only matter when earned at funds with low constraints. In

fact, managers at high constraint funds have to substantially outperform managers at low

constraint funds to be hired by low constraint funds. Additionally, we find that investors are,

on average, more sensitive to returns of low constraint funds than high constraint funds

when allocating capital. This suggests both funds and their investors find the skill signal

present in returns to be noisy. Overall, these findings suggest a misallocation of manager

skill, resulting in skilled managers not moving to funds which need skill and unskilled

managers not being fired when they underperform.

25

References

Akerlof, G. A., 1970, The Market for" Lemons": Quality Uncertainty and the Market

Mechanism. The Quarterly Journal of Economics, 84(3), pp.488-500.

Almazan, A., Brown, K. C., Carlson, M., & Chapman, D. A., 2004, Why Constrain Your Mutual

Fund Manager?, Journal of Financial Economics, 73(2), 289–321.

Avery, C. N., & Chevalier, J. A., 1999, Herding Over the Career, Economic Letters 53, 327-333.

Barras, L., Scaillet, O., & Wermers, R., 2010, False Discoveries in Mutual Fund Performance,

The Journal of Finance 65, 179-216.

Beatty, R., Lu, H., & Luo, W., 2014, The Market for Lemons: A Study of Quality Uncertainty and

the Market Mechanism for Chinese Firms Listed in the US, Working Paper, University

of Southern California.

Berk, J. B., & Green, R. C., 2004, Mutual Fund Flows and Performance in Rational Markets,

Journal of Political Economy, 112(6), 1269-1295.

Bond, E. W., 1982, A Direct Test of the “Lemons” Model: The Market for Used Pickup Trucks,

The American Economic Review 72, 836-840.

Brown, K.C., Harlow, W.V., & Starks L.T., 1996, Of Tournaments and Temptations: An Analysis

of Managerial Incentives in the Mutual Fund Industry, The Journal of Finance 51, 85-

110.

Carlin, Ian, B., & Gervais, S., 2014, Work Ethic, Employment Contracts, and Firm Value, The

Journal of Finance 64, 785-821.

26

Chan, L. K. C., Chen, H., & Lakonishok, J., 2002, On Mutual Fund Investment Styles, Review of

Financial Studies 15, 1407-1437.

Chen, H., Desai, H., & Krishnamurthy, S., 2013, A First Look at Mutual Funds that use Short

Sales, Journal of Financial and Quantitative Analysis 48, 761-787.

Chevalier, J., Ellison, G., 1997, Risk Taking by Mutual Funds as a Response to Incentives,

Journal of Political Economy 105, 1167–1200.

Chevalier, J., Ellison, G., 1999, Career Concerns of Mutual Fund Managers, The Quarterly

Journal of Economics 114, no. 2 (1999): 389-432.

Cremers, M., Ferreira, M. A., Matos, P., and Starks, L., 2016, The Mutual Fund Industry

Worldwide: Explicit and Closet Indexing, Fees, and Performance, forthcoming Journal

of Financial Economics.

Cremers, K. M., & Petajisto, A., 2009, How Active is Your Fund Manager? A New Measure That

Predicts Performance. Review of Financial Studies, hhp057.

Deuskar, P., Pollet, J.M., Wang, J., & Zheng, L., 2011, The Good or the Bad? Which Mutual Fund

Managers Join Hedge Funds?, Review of Financial Studies 24, 3008-3024.

Downing, C., Jaffee, D., & Wallace, N., 2009, Is the Market for Mortgage-Backed Securities a

Market for Lemons?, Review of Financial Studies 22, 2457-2494.

Edelen, R. M., 1999, Investor Flows and the Assessed Performance of Open-End Mutual

Funds, Journal of Financial Economics 53, 439-466.

Elton, E. J., Gruber, M. J., & Blake, C. R., 2012, Does Mutual Fund Size Matter? The Relationship

Between Size and Performance, Review of Asset Pricing Studies 2, 31-55.

27

Eshraghi, A., & Taffler, R., 2012, Fund Manager Overconfidence and Investment Performance:

Evidence from Mutual Funds, Working paper.

Fabel, O., & Lehmann, E., 2000, Adverse Selection and the Economic Limits of Market

Substitution, Working Paper, University of Konstanz.

Fama, E. F., 1980, Agency Problems and the Theory of the Firm, Journal of Political Economy

88, 288-307.

Fama , E. F., & French, K. R., 2010, Luck versus Skill in the Cross-Section of Mutual Fund

Returns, The Journal of Finance 65, 1915-1947.

Fang, J., Kempf, A., & Trapp, M., 2014, Fund Manager Allocation, Journal of Financial

Economics 111, 661-674.

Genesove, D., 1993, Adverse Selection in the Wholesale Used Car Market, Journal of Political

Economy 101, 644-665.

Gibbons, R., and Katz, L. F., 1991, Layoffs and Lemons, Journal of Labor Economics 9, 351-380.

Greenwald B., & Glasspigel, R., 1983, Adverse Selection in the Market for Slaves: New Orleans

1830-1860, Quarterly Journal of Economics 98, 479-499.

Harris, M., & Raviv, A., 1979, Optimal Incentive Contracts with Imperfect Information, Journal

of Economic Theory 20, 231-259.

Holmstrom, B., 1979, Moral Hazard and Observability, The Bell Journal of Economics 10, 74-

91.

Hong, H., Kubik, J. D., & Solomon, A., 2000, Security Analyst’s Career Concerns and Herding

of Earnings Forecasts, RAND Journal of Economics 31, 121-144.

Jensen, M. C., & Meckling, W. H., 1976, Theory of the Firm: Managerial Behavior, Agency Costs

and Ownership Structure, Journal of Financial Economics 3, 305-360.

28

Jensen, M. C., & Murphy, K. J., 1990, Performance Pay and Top-Management Incentives,

Journal of Political Economy 98, 225-264.

Kacperczyk, M., Sialm, C., and Zheng, L., 2008, Unobserved Actions of Mutual Funds, Review

of Financial Studies 21, 2379-2416.

Khorana, A., 1996, Top Management Turnover: An Empirical Investigation of Mutual Fund

Managers, Journal of Financial Economics 40, 403-427.

Kosowski, R., Timmerman, A., Wermers, R., & White, H., 2006, Can Mutual Fund “Starts”

Really Pick Stocks? New Evidence from a Bootstrap Analysis, The Journal of Finance

61, 2551-2595.

Lakonishok, J., Shleifer, A., Thaler, R.H., & Vishny, R., 1991, Window Dressing by Pension Fund

Managers, The American Economic Review 81, 227-231.

Lamont, O., 2002, Macroeconomic Forecasts and Microeconomic Forecasters, Journal of

Economic Behavior and Organization 48, 265-280.

Lehn, K., 1984, Information Asymmetries in Baseball’s Free Agent Market, Economic Inquiry

22, 37-44.

Pan, Y., Wang, T. Y., & Weisbach, M. S., 2015, Learning about CEO Ability and Stock Return

Volatility, Review of Financial Studies28, 1623-1666.

Puetz, A., & Ruenzi, S., 2011, Overconfidence among Professional Investors: Evidence from

Mutual Fund Managers, Journal of Business Finance and Accounting 38, 684-712.

Renneboog, Luc, Jenke Ter Hosrt, and Chendi Zhang, 20011, Is ethical money financially

smart?, Journal of Financial Intermediation 20, 562-588.

29

Rosenman, R .E. & Wilson, W.W., 1991, Quality Differentials and Prices: are Cherries Lemons?

The Journal of Industrial Economics, pp.649-658.

Ross, S.A., 1973, The Economic Theory of Agency: The Principal's Problem. The American

Economic Review, 63(2), pp.134-139.

Sensoy, B.A., 2009, Performance Evaluation and Self-Designated Benchmark Indexes in the

Mutual Fund Industry. Journal of Financial Economics, 92(1), pp.25-39.

Sirri, E. R., & Tufano, P., 1998, Costly Search and Mutual Fund Flows. The Journal of Finance,

53(5), 1589-1622.

Spence, M., 1973, Job Market Signaling, The Quarterly Journal of Economics 87, 355-374.

Stoughton, N. M., 1993, Moral Hazard and the Portfolio Management Problem, The Journal of

Finance, 48(5), pp.2009-2028.

30

Table 1

Fund Characteristics

This table looks at some characteristics of the funds represented in our sample. We group funds based on the prospectus defined benchmark. These funds were part of employments that lasted at least 12 months. Funds that are not considered domestic equity according to various classification codes in CRSP or do not use one of the 19 equity benchmarks are ignored. Our sample period is between 1980 and 2014.

Index Number of funds % Start Date

S&P 500 675 41.49 Jan-88

Russell 2000 150 9.22 Jan-80

Russell 1000 Value 141 8.67 Jan-80

Russell 1000 Growth 136 8.36 Jan-80

Russell 2000 Growth 87 5.35 Jan-80

Russell 2000 Value 82 5.04 Jan-80

Russell Midcap Growth 67 4.12 Jan-86

Russell 3000 65 4.00 Jan-80

Russell Midcap Value 51 3.13 Jan-86

Russell 1000 36 2.21 Jan-80

Russell Midcap 36 2.21 Jan-80

Russell 3000 Value 28 1.72 Jan-80

Russell 3000 Growth 26 1.60 Jan-80

S&P MidCap 400 24 1.48 Sep-95

S&P SmallCap 600 8 0.49 Jan-95

S&P500/Barra Value 6 0.37 Jan-80

Wilshire 5000 5 0.31 Jan-80

S&P500/Barra Growth 4 0.25 Jan-80

Wilshire 4500 0 0 Jan-84

Total 1627 100

31

Table 2

Descriptive Statistics for Employments

This table shows basic statistics about employments of managers in our sample. Number of employment changes is calculated by counting the number of times a manager adds or drops a fund, or both to their portfolio of funds. We require an employment to last at least 12 months. Employments in funds that are not considered domestic equity according to various classification codes in CRSP or do not use one of the 19 equity benchmarks we include in our study are ignored. Length of employment is calculated by counting the number of months since the new employment began until a change of employment. Career length rank is calculated by counting the number of months in the career of each manager and ranking into quantiles. Number of years before an employment change is calculated by dividing the length of the career of the manager in months by the number of employment changes and multiplying by 12. Our sample period is between 1980 and 2014.

Panel A: Number of employment changes throughout the career of managers

Key variable: Number of employment changes per manager

Single employment indicator

N Mean StdDev Minimum Maximum

0 1803 2.96 1.29 2 10

1 3361 1 0 1 1

Number of Managers

5164

Panel B: Number of years at each employment

Key variable: Length of each employment (months)

Single employment Indicator

N Mean StdDev Minimum Maximum

0 5340 42.56 32.74 12 239

1 3361 66.68 52.88 12 244

Total number of employments

8701

Panel C: Number of employment changes and length of career for each manager

Key variable: Number of years before an employment change

Career length rank

N Mean StdDev Minimum Maximum

Shortest Career

1027 1.70 0.45 1.00 2.50

2 1039 3.12 0.84 1.13 4.50

3 1027 4.61 1.73 1.21 7.25

4 1041 6.22 2.99 1.43 11.50

Longest Career

1030 8.91 5.42 1.74 20.33

Number of Managers

5164

32

Table 3

Employment Changes Across Time

This table shows the number of employment changes in our sample through time. We identify an employment change anytime a manager adds a fund, drops a fund, or both. We require an employment to last at least 12 months. Employments in funds that are not considered domestic equity according to various classification codes in CRSP or do not use one of the 19 equity benchmarks we include in our study are ignored. In the last two columns, we remove employment changes with gaps in-between the two employments. We divide our employment changes sample into four groups based on constraint level pre- and post-employment change. CTC group is for managers that moved inside the constrained group. UTC group is for managers that moved from unconstrained group to constrained group. CTU group is for managers that moved from constrained group to unconstrained group. UTU group is for managers that moved inside the unconstrained group. Our sample period is between 1980 and 2014.

Year All % CTC % CTU % UTC % UTU % All (no gaps)

%

1984 4 0.11 0 0.00 2 0.41 0 0.00 2 0.16 4 0.18

1985 5 0.14 1 0.08 0 0.00 0 0.00 4 0.31 5 0.22

1986 1 0.03 0 0.00 0 0.00 0 0.00 1 0.08 1 0.04

1987 10 0.28 1 0.08 1 0.21 0 0.00 8 0.62 8 0.36

1988 8 0.23 0 0.00 0 0.00 0 0.00 8 0.62 8 0.36

1989 16 0.45 0 0.00 0 0.00 2 0.41 14 1.09 6 0.27

1990 29 0.82 3 0.23 2 0.41 4 0.83 20 1.56 17 0.76

1991 28 0.79 3 0.23 3 0.62 3 0.62 19 1.48 14 0.63

1992 47 1.33 6 0.47 1 0.21 11 2.27 29 2.26 30 1.35

1993 44 1.24 8 0.62 8 1.65 4 0.83 24 1.87 25 1.12

1994 61 1.72 13 1.01 5 1.03 14 2.89 29 2.26 39 1.75

1995 61 1.72 19 1.48 17 3.51 6 1.24 19 1.48 41 1.84

1996 74 2.09 17 1.32 13 2.69 2 0.41 42 3.27 46 2.07

1997 98 2.77 22 1.71 10 2.07 7 1.45 59 4.59 60 2.70

1998 116 3.28 14 1.09 18 3.72 7 1.45 77 5.99 63 2.83

1999 122 3.45 7 0.55 7 1.45 11 2.27 97 7.55 67 3.01

2000 169 4.78 11 0.86 11 2.27 22 4.55 125 9.73 109 4.90

2001 139 3.93 12 0.93 4 0.83 25 5.17 98 7.63 97 4.36

2002 175 4.95 25 1.95 13 2.69 35 7.23 102 7.94 106 4.77

2003 143 4.04 44 3.43 11 2.27 35 7.23 53 4.12 86 3.87

2004 181 5.12 90 7.01 19 3.93 30 6.20 42 3.27 99 4.45

2005 228 6.45 143 11.14 23 4.75 21 4.34 41 3.19 130 5.85

2006 264 7.46 155 12.07 38 7.85 26 5.37 45 3.50 169 7.60

2007 281 7.94 113 8.80 99 20.45 9 1.86 60 4.67 157 7.06

2008 287 8.11 62 4.83 76 15.70 40 8.26 109 8.48 161 7.24

2009 177 5.00 42 3.27 10 2.07 64 13.22 61 4.75 112 5.04

2010 244 6.90 147 11.45 23 4.75 43 8.88 31 2.41 156 7.02

2011 162 4.58 98 7.63 30 6.20 6 1.24 28 2.18 120 5.40

2012 157 4.44 88 6.85 6 1.24 45 9.30 18 1.40 108 4.86

2013 206 5.82 140 10.90 34 7.02 12 2.48 20 1.56 179 8.05

Number of employment changes

3537 1284 484 484 1285 2223

33

Table 4

Returns and Constraint Post-Employment Change

This tables looks at how employment-level returns and tracking error change after a change in employment. We require an employment to last at least 12 months. Employments in funds that are not considered domestic equity according to various classification codes in CRSP or do not use one of the 19 equity benchmarks we include in our study are ignored. We risk-adjust fund-level returns by grouping returns based on their prospective defined benchmarks and ranking them against their peers each month. We take the value-weighted average using monthly total net assets of the ranked returns each month in case a manager is managing more than one fund at one point in time to get employment-level risk-adjusted ranked returns for each manager monthly. diff_returns is calculated for each employment change by taking the difference between geometric mean of the pre- and post-employment change employment-level ranked returns using 12 month window. Return variables followed by "raw" indicate that the employment returns have not been risk adjusted. Tracking error is calculated by taking the standard deviation of fund returns less benchmark returns every month. In case of multiple employments, we value-weight the fund returns less benchmark returns to obtain employment-level values. We then take the standard deviation of the employment-level returns net of benchmark returns. diff_tracking is the difference between post-and pre-employment change tracking error using 12 month window. Variables proceeded by "abs" signify that we took the absolute value. For this analysis we ignored managers with a single employment because there is no employment change. For Panel B, we remove employment changes with gaps in-between the two employments. Number of employment changes is calculated by counting the number of times a manager adds or drops a fund, or both to their portfolio of funds. Our sample period is between 1980 and 2014. *, **, *** signify that the mean is significantly different from zero at 10%, 5% and 1% respectively

Panel A: Employments with gaps allowed

Variable Number of employment changes Mean StdDev

diff_returns 3537 0.0025 0.6081

diff_returns_raw 3537 -0.0003 0.0255

diff_tracking 3537 -0.0017*** 0.0133

abs_diff_returns 3537 0.4746*** 0.3802

abs_diff_returns_raw 3537 0.0184*** 0.0177

abs_diff_tracking 3537 0.00781*** 0.0109

Panel B: Employments with gaps not allowed

diff_returns 2223 -0.0093 0.5941

diff_returns_raw 2223 -0.0007 0.0245

diff_tracking 2223 -0.0013*** 0.0102

abs_diff_returns 2223 0.4597*** 0.3763

abs_diff_returns_raw 2223 0.0170*** 0.0176

abs_diff_tracking 2223 0.0064*** 0.0080

34

Table 5

Skill Signal and Hiring Decisions

We regress the change of tracking error after an employment change on returns pre-employment change. We identify an employment change anytime a manager adds a fund, drops a fund, or both. We require an employment to last at least 12 months. Employments in funds that are not considered domestic equity according to various classification codes in CRSP or do not use one of the 19 equity benchmarks we include in our study are ignored. We risk-adjust fund-level returns by grouping returns based on their prospectus defined benchmarks and ranking them against their peers each month. We take the value-weighted average of the ranked returns each month using monthly total net assets (mtna) in case a manager is managing more than one fund at one point in time to get employment-level ranked returns for each manager monthly. returns is calculated for each manager by taking the geometric mean of the pre-employment change employment-level ranked returns using 12 month window. Tracking error is calculated by taking the standard deviation of fund returns less benchmark returns each month. In case of multiple employments, we value-weight the returns less benchmark returns to obtain employment-level values. We then take the standard deviation of the employment-level returns net of benchmark returns. diff_tracking is the difference between post-and pre-employment change tracking error using 12 month window. diff_mtna is calculated by first summing the mtna of all funds under same employment every month in case of multiple funds in a single employment. We then take the difference between the average of mtna pre- and post-employment change using 12 month window. For this analysis we ignored managers with a single employment because there is no employment change. For panel B, we remove employment changes with gaps in-between the two employments. In panel C and D, we divide our original employment changes sample into two groups; constrained and unconstrained employments based on the median of the tracking error pre-employment change using 12 month window. We then run the same regression as in panel A. Our sample period is between 1980 and 2014. *, **, *** signify significance at 10%, 5% and 1%, respectively

Panel A: Employment gaps allowed Panel B: Employment gaps not allowed

DV diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking

(1) (2) (3) (4) (1) (2) (3) (4)

Intercept -0.0097 -0.010 -0.0083 -0.0083

returns 0.0029*** 0.0030*** 0.0031*** 0.0034*** 0.0026*** 0.0026*** 0.0027*** 0.0027***

diff_mtna (x106) -0.1019*** -0.0958*** -0.0952*** -0.0439** -0.0341* -0.0675**

AdjR-Sq 0.0096 0.0147 0.1349 0.5712 0.0123 0.0139 0.1665 0.6051

Year FE 0 0 1 0 0 0 1 0

Manager FE 0 0 0 1 0 0 0 1

N 3537 3537 3537 3537 2223 2223 2223 2223

Panel C: Constrained group (CTU and CTC) Panel D: Unconstrained group (UTC and UTU)

DV diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking diff_tracking

(1) (2) (3) (4) (1) (2) (3) (4)

Intercept 0.0027 0.003 -0.0137 -0.0139

returns -0.0002 -0.0002 -0.0004 0.0009 0.0031*** 0.0032*** 0.0041*** 0.0044***

diff_mtna(x106) -0.0437*** -0.0286** -0.0253*** -0.3012*** -0.3197*** -0.2422*

AdjR-Sq -0.0003 0.0059 0.1277 0.7034 0.0075 0.0186 0.1409 0.6409

Year FE 0 0 1 0 0 0 1 0

Manager FE 0 0 0 1 0 0 0 1

N 1768 1768 1768 1768 1769 1769 1769 1769

35

Table 6

Noisiness of Skill Signal

This table shows the results from our logistic regression. We look for employment changes where the manager moved from constrained group to the unconstrained group (CTU) or remained in the unconstrained group (UTU). We rank employments based on tracking error pre- and post- employment change using 12 month window. We identify an employment change anytime a manager adds a fund, drops a fund, or both. We require an employment to last at least 12 months. Employments in funds that are not considered domestic equity according to various classification codes in CRSP or do not use one of the 19 equity benchmarks we include in our study are ignored. We risk-adjust fund-level returns by grouping returns based on their prospectus defined benchmarks and ranking them against their peers each month. We take the value-weighted average of the ranked returns each month using monthly total net assets (mtna) in case a manager is managing more than one fund at one point in time to get employment-level ranked returns for each employment monthly. returns is calculated for each manager by taking the geometric mean of the pre-employment change employment-level ranked returns using 12 month window. Tracking error is calculated by taking the standard deviation of fund returns less benchmark returns each month. In case of multiple employments, we value-weight the returns less benchmark returns to obtain employment-level values. We then take the standard deviation of the employment-level returns net of benchmark returns. diff_tracking is the difference between post-and pre-employment change tracking error using 12 month window. diff_mtna is calculated by first summing the mtna of all funds under management every month in case of multiple funds. We then take the difference between the average of mtna pre- and post-employment change using 12 month window. For this analysis we ignored managers with single employment because there is no employment change. For panel B, we remove employment changes with gaps in-between the two employments. Our sample period is between 1980 and 2014. *, **, *** signify significance at 10%, 5% and 1%, respectively

Panel A: Employment gaps allowed Panel B: Employment gaps not allowed

DV 1=CTU 0=UTU

1=CTU 0=UTU

1=CTU 0=UTU

1=CTU 0=UTU

(1) (2) (1) (2)

Intercept -1.832 -4.0433 -2.0244 -5.2820

returns 0.3141*** 0.4794*** 0.3136** 0.6113***

diff_mtna (x106) -20.0000** -20.0000* -20.0000* -20.0000***

Year FE 0 1 0 1

N (CTU) 484 484 266 266

N(UTU) 1285 1285 846 846

N 1769 1769 1022 1022

Wald (Pr>ChiSq) 0.0011 <.0001 0.0155 <.0001

36

Table 7

Cash Flow Sensitivity

This table shows the results from annual net cash flows regressed on fund characteristics and performance. Flows in year t are defined as (TNAt – (1+Rett)TNAt-1) / TNAt-1. Objective flow is TNA-weighted mean flows in year t of all funds in the same investment objective, grouped into Growth, Growth and Income, Small Capitalization, and Aggressive Growth by Lipper Objective Code. TNA, Expense Ratios, and Loads are as reported in CRSP. Max Load is the largest of the front and rear loads. Return Stdev is the annual standard deviation of monthly returns. Tracking Error is the tracking error of monthly fund returns (as defined in Table 4) over the 12 months of year t. Returns are ranked into percentiles annually by investment objective and converted into three piece-wise variables as in Sirri and Tufano (1998). LowRank is returns in the lowest 20th percentile, MidRank is returns between the 20th and 80th percentiles, and HighRank is returns in the 80th percentile. Regression use pooled OLS with standard errors clustered by year. T-statistics are reported in parentheses. Our sample period is between 1980 and 2012.

Model (1) Model (2)

Intercept 0.4670 6.56 0.4031 4.33

Log(TNAt-1) -0.0719 -11.12 -0.0737 -11.04

Objective Flowt 1.1362 14.02 1.1963 15.41

Expense Ratiot-1 2.9927 1.21 1.7640 0.69

Max Loadt-1 -0.2349 -0.87 -0.0754 -0.27

Return Stdevt-1 -0.5578 -1.09 -0.4553 -0.81

Tracking Errort-1 0.0147 1.71

LowRank t-1 0.3057 2.16 0.9494 3.21

MidRank t-1 0.4058 6.26 0.2549 3.59

HighRank t-1 1.7011 4.38 2.4505 4.41

LowRank t-1*TE t-1 -0.1237 -2.69

MidRank t-1*TE t-1 0.0342 3.02

HighRank t-1*TE t-1 -0.1351 -1.59

N 19,258 18,698

R2 0.1095 0.1099

Related Documents

![Reputation & Regulations: Evidence from eBay1 Introduction Asymmetric information can lead to adverse selection, moral hazard, market ine ciency, or even market failure (Akerlof[1970]).](https://static.cupdf.com/doc/110x72/5fde385cd2ccbd0951181025/reputation-regulations-evidence-from-1-introduction-asymmetric-information.jpg)