Lecture IV Questions from last lecture Review questions: • What are economic problems posed by bankruptcy? • What are economic advantages/ benefits of bankruptcy laws? • What are short-comings of Paris and London Club? When do they arise? • What are problems with IMF’s SDRM approach?

Lecture IV Questions from last lecture Review questions: What are economic problems posed by bankruptcy? What are economic advantages/ benefits of bankruptcy.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lecture IV

Questions from last lecture

Review questions:• What are economic problems posed by bankruptcy?• What are economic advantages/ benefits of bankruptcy laws?• What are short-comings of Paris and London Club? When do they

arise?• What are problems with IMF’s SDRM approach?

Some types of flows are too persistent

Total foreign indebtedness in billions of US$

Foreign Debt

$0

$100

$200

$300

$400

$500

$600

$700

$800

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

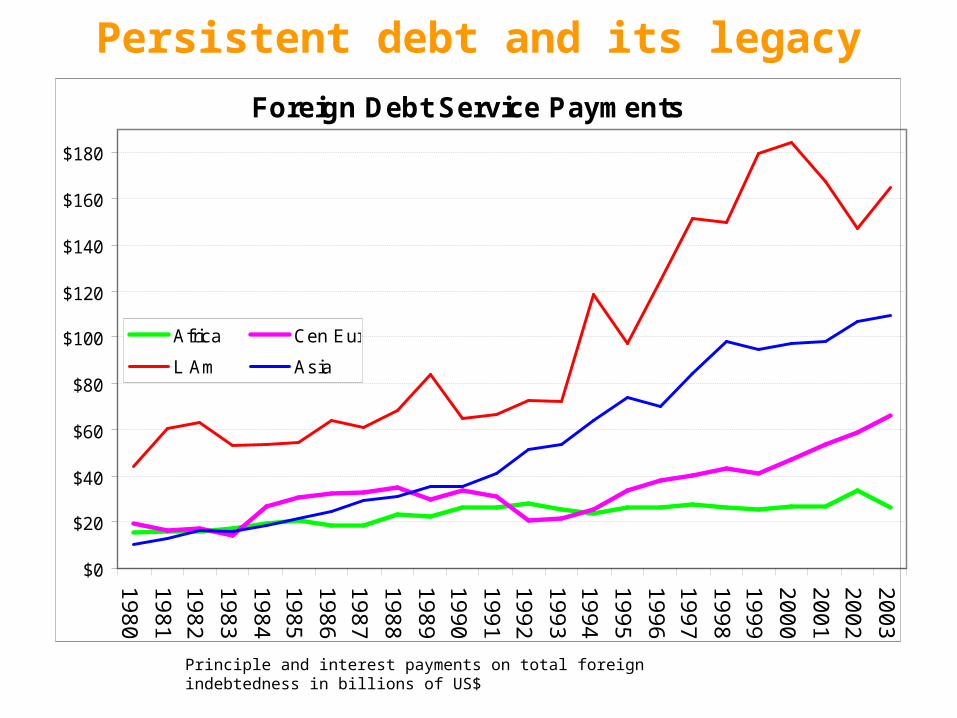

Africa Cen Eur

L Am Asia

Persistent debt and its legacy

Principle and interest payments on total foreign indebtedness in billions of US$

Foreign Debt Service Payments

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

Africa Cen Eur

L Am Asia

Lecture IVLocal Currency Debt

• Major part of problem as been dollar denomination of developing country debt.

• How did this come about?Dodd (1989) – banks and other lenders did not want currency risk – would not lend other terms that included local currency denomination.

• Hausmann, et al – due to Original SinNot the fault of LDCs, not a result of their errors

- not bad fiscal policy- not bad monetary policy- not foreign exchange volatility or inflation volatility- not history of default

Instead it is the result of a sort of “Original Sin”

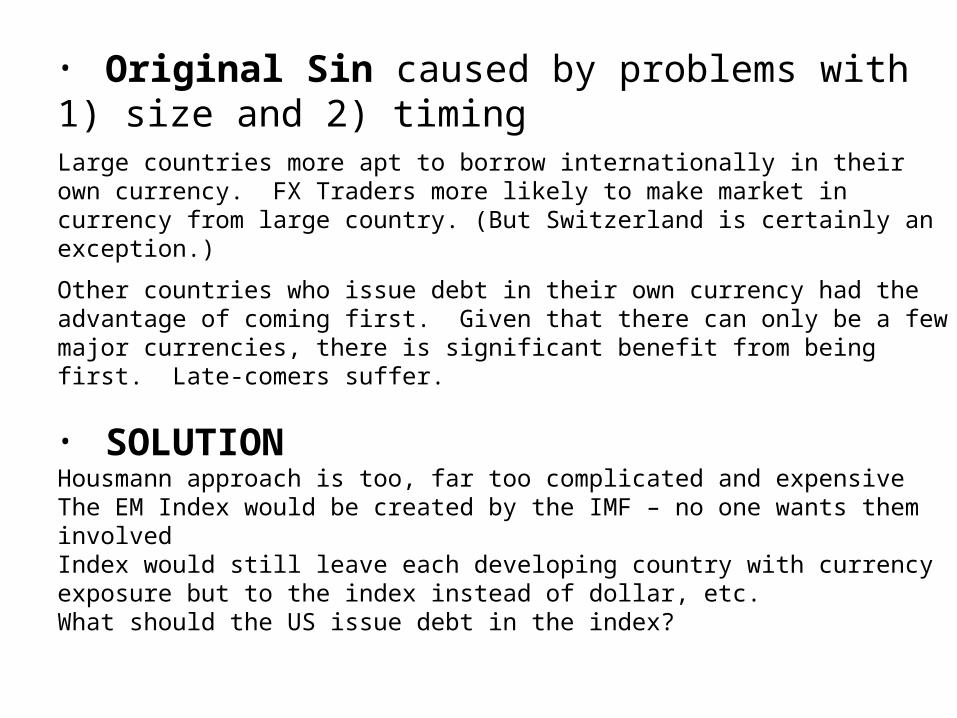

• Original Sin caused by problems with 1) size and 2) timingLarge countries more apt to borrow internationally in their own currency. FX Traders more likely to make market in currency from large country. (But Switzerland is certainly an exception.)

Other countries who issue debt in their own currency had the advantage of coming first. Given that there can only be a few major currencies, there is significant benefit from being first. Late-comers suffer.

• SOLUTIONHousmann approach is too, far too complicated and expensiveThe EM Index would be created by the IMF – no one wants them involvedIndex would still leave each developing country with currency exposure but to the index instead of dollar, etc.What should the US issue debt in the index?

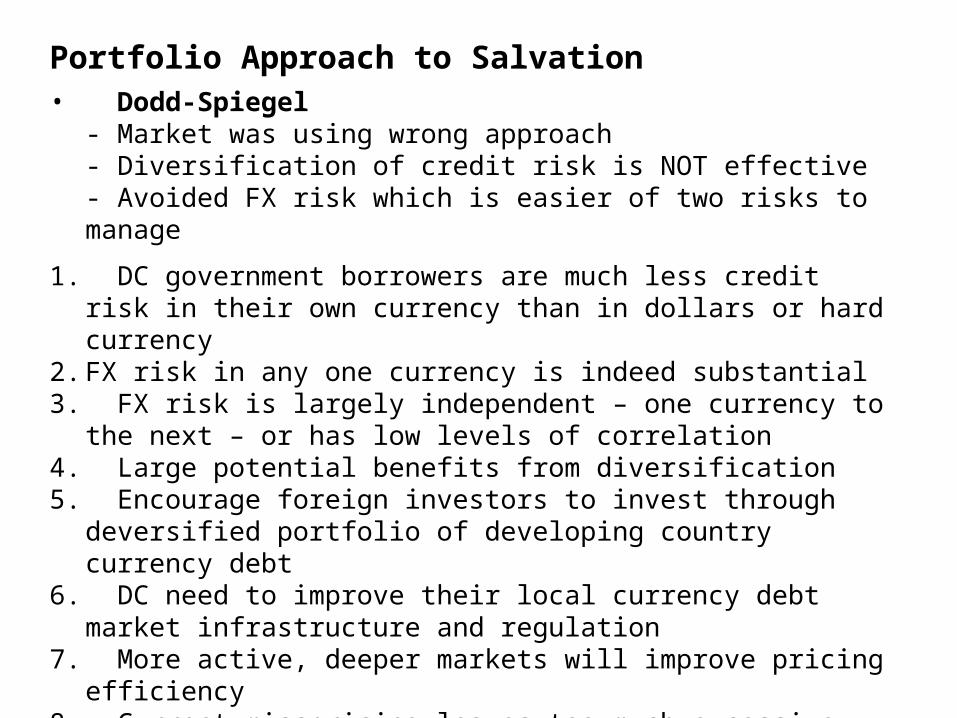

Portfolio Approach to Salvation• Dodd-Spiegel

- Market was using wrong approach- Diversification of credit risk is NOT effective- Avoided FX risk which is easier of two risks to manage

1. DC government borrowers are much less credit risk in their own currency than in dollars or hard currency

2. FX risk in any one currency is indeed substantial3. FX risk is largely independent – one currency to the next – or has

low levels of correlation4. Large potential benefits from diversification5. Encourage foreign investors to invest through deversified portfolio

of developing country currency debt6. DC need to improve their local currency debt market infrastructure

and regulation7. More active, deeper markets will improve pricing efficiency8. Current misspricing leaves too much excessive gains for foreign

investors, efficient pricing would allow DC to borrow more cheaply

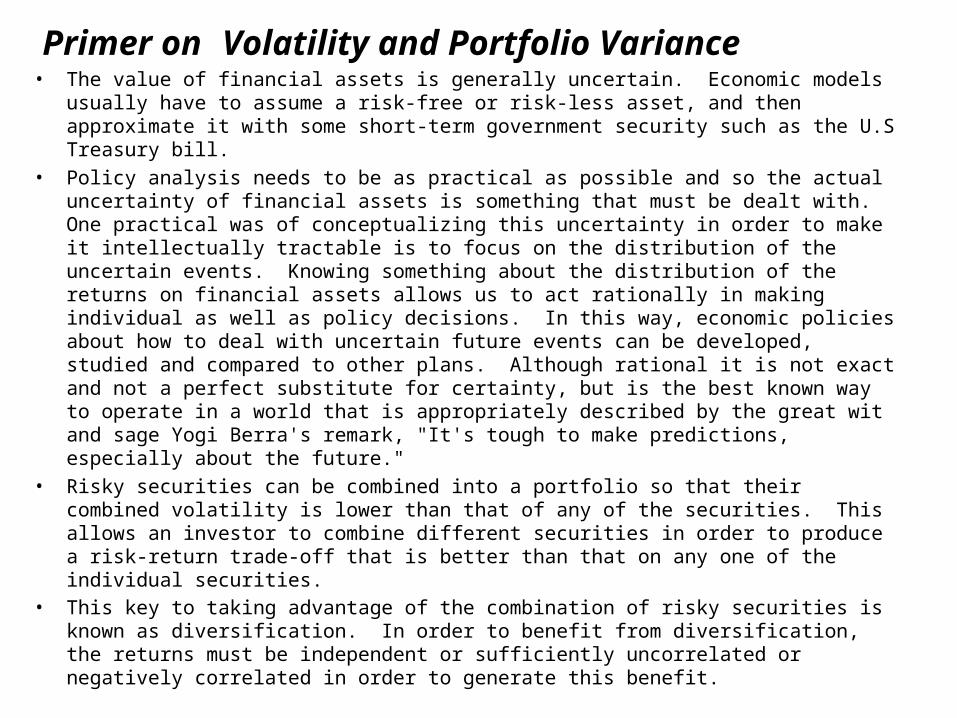

Primer on Volatility and Portfolio Variance• The value of financial assets is generally uncertain. Economic models usually have to

assume a risk-free or risk-less asset, and then approximate it with some short-term government security such as the U.S Treasury bill.

• Policy analysis needs to be as practical as possible and so the actual uncertainty of financial assets is something that must be dealt with. One practical was of conceptualizing this uncertainty in order to make it intellectually tractable is to focus on the distribution of the uncertain events. Knowing something about the distribution of the returns on financial assets allows us to act rationally in making individual as well as policy decisions. In this way, economic policies about how to deal with uncertain future events can be developed, studied and compared to other plans. Although rational it is not exact and not a perfect substitute for certainty, but is the best known way to operate in a world that is appropriately described by the great wit and sage Yogi Berra's remark, "It's tough to make predictions, especially about the future."

• Risky securities can be combined into a portfolio so that their combined volatility is lower than that of any of the securities. This allows an investor to combine different securities in order to produce a risk-return trade-off that is better than that on any one of the individual securities.

• This key to taking advantage of the combination of risky securities is known as diversification. In order to benefit from diversification, the returns must be independent or sufficiently uncorrelated or negatively correlated in order to generate this benefit.

Constant STDEV = 2.05

96

98

100

102

104

106

108

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

+/-2%

Grow th

Spike

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

5 Independently Distributed Random Series

Perfect Negative Correlation

0

5

10

15

20

25

1 5 9 13 17 21 25 29 33 37 41 45 49

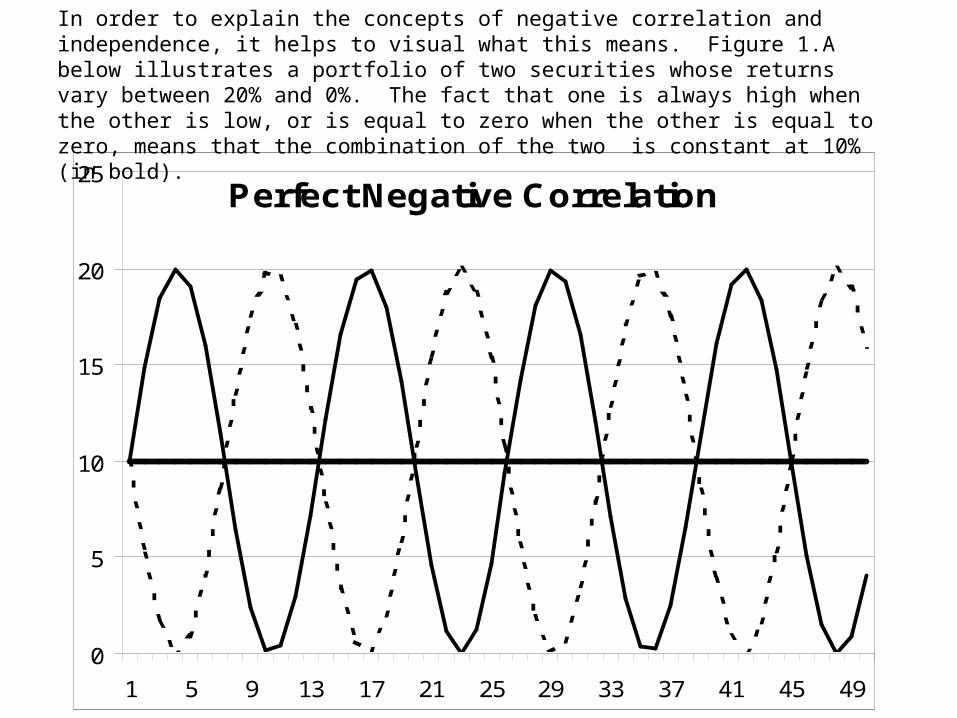

In order to explain the concepts of negative correlation and independence, it helps to visual what this means. Figure 1.A below illustrates a portfolio of two securities whose returns vary between 20% and 0%. The fact that one is always high when the other is low, or is equal to zero when the other is equal to zero, means that the combination of the two is constant at 10% (in bold).

Of course find two such perfectly and negatively correlated assets is unlikely (one exception would be short and long derivatives positions, but the combined return would be zero). Consider a slightly more complicated portfolio of four securities that are two pairs of perfectly negatively correlated securities but the two pairs are not perfectly correlated. This is illustrated by Figure 2.A below. Note that one pair has a greater volatility than the other pair (this is illustrated by the high amplitudes (both positive and negative) of the waves of returns).

Correlation & Variance

-5

0

5

10

15

20

25

1 5 9 13 17 21 25 29 33 37 41 45 49

Of course it is even more unlikely to find two pairs of perfectly negatively correlated securities. The point here is to illustrate the potential of combining different securities, and larger number of different securities, into a portfolio so as to reduce overall risk or volatility.

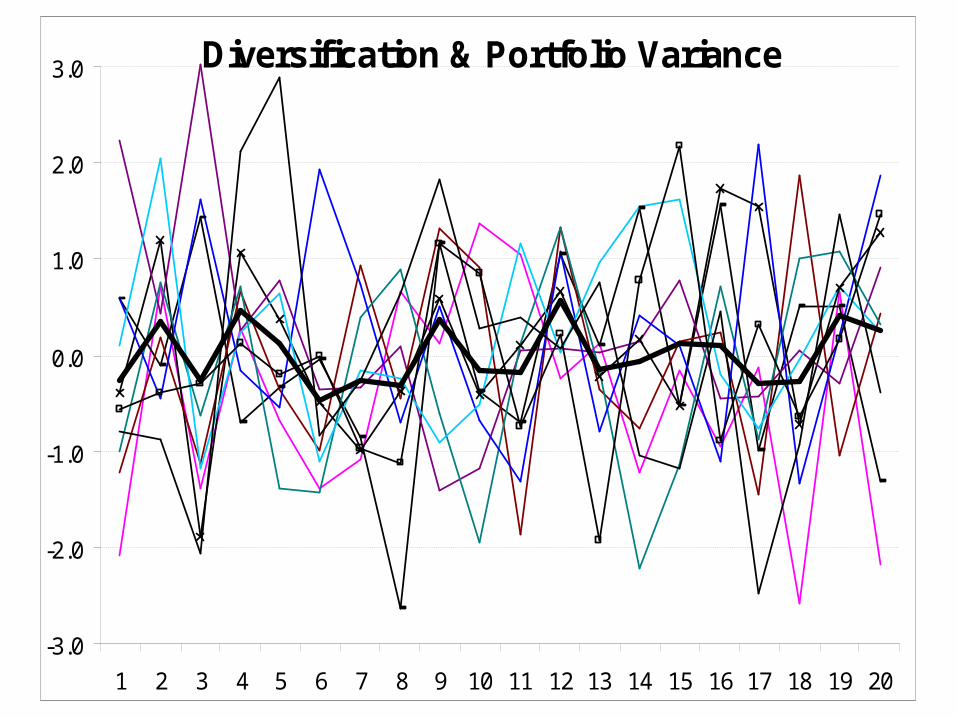

The next point to consider is independence. In order to illustrate this point, Figure 3.A below shows a portfolio of hypothetical returns created by a random number generator. Each security is not perfectly independent but is sufficiently independent that the portfolio variance, represented by the dark bold line, exhibits substantially less volatility than any of the individual securities.

Diversification & Portfolio Variance

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Figure above shows that a portfolio of securities that are each very volatile can be combined into a portfolio whose volatility is much less variable.

A concluding word of caution. The past distribution is not a guarantee of future distribution. The world, as Heraclitus pointed out some time ago, is constantly changing. And that applies also to the distribution of changing or uncertain things. This point was illustrated graphically but tragically when Long Term Capital Management collapsed when they investment strategy ran into uncharacteristic distribution of interest rates. Perhaps an easier way to remember this caveat is to recall again the words of the great wit and sage Yogi Berra who said, "The future is not what it used to be.“

Related Documents