Lecture 13

Lecture 13. Lecture overview Problem Question Job-Order Costing Document Flow Summary Job-Order System Cost Flows Overhead Application Example Overapplied.

Dec 31, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lecture 13

Lecture overview

• Problem Question• Job-Order Costing Document Flow Summary• Job-Order System Cost Flows• Overhead Application Example• Overapplied and Underapplied Manufacturing

Overhead• MCQs Test Questions

Cost Flows – Material Purchases

Raw material purchases are recorded in aninventory account.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Raw Materials XXXXX Accounts Payable XXXXX

Direct materials issued to a job increase Work in Process and decrease Raw Materials. Indirect materials used are

charged to Manufacturing Overhead and also decrease Raw Materials.

Cost Flows – Material Usage

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work in Process XXXXXManufacturing Overhead XXXXX Raw Materials XXXXX

Cost Flows – Labor

The cost of direct labor incurred increases Work in Process and the cost of indirect labor increases

Manufacturing Overhead.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work in Process XXXXXManufacturing Overhead XXXXX Salaries and Wages Payable XXXXX

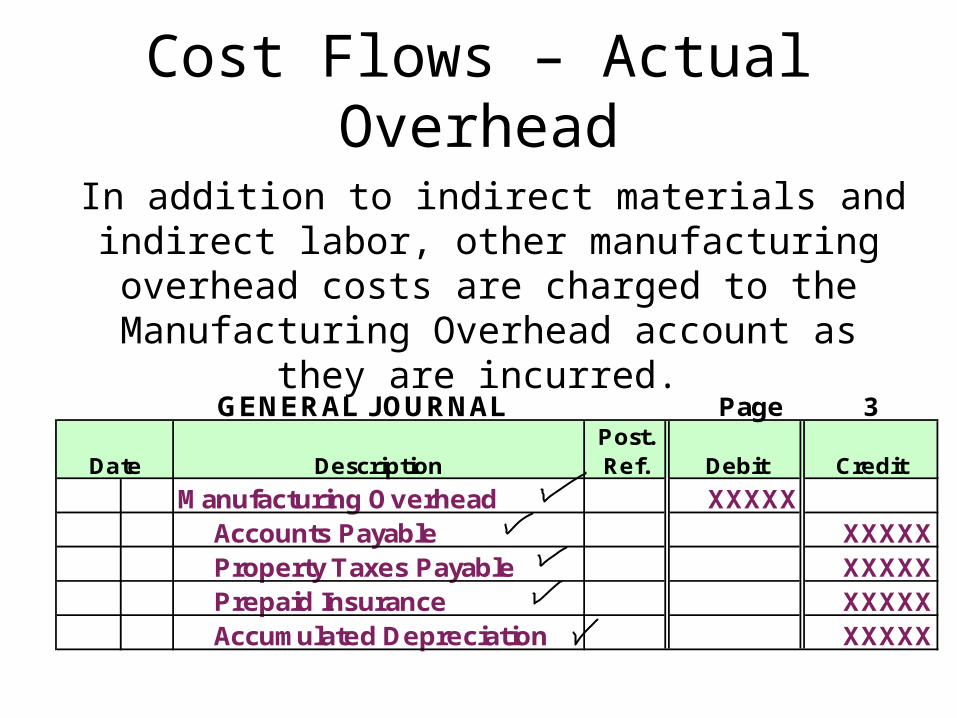

Cost Flows – Actual Overhead

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Manufacturing Overhead XXXXX Accounts Payable XXXXX Property Taxes Payable XXXXX Prepaid Insurance XXXXX Accumulated Depreciation XXXXX

In addition to indirect materials and indirect labor, other manufacturing overhead costs are charged to the

Manufacturing Overhead account as they are incurred.

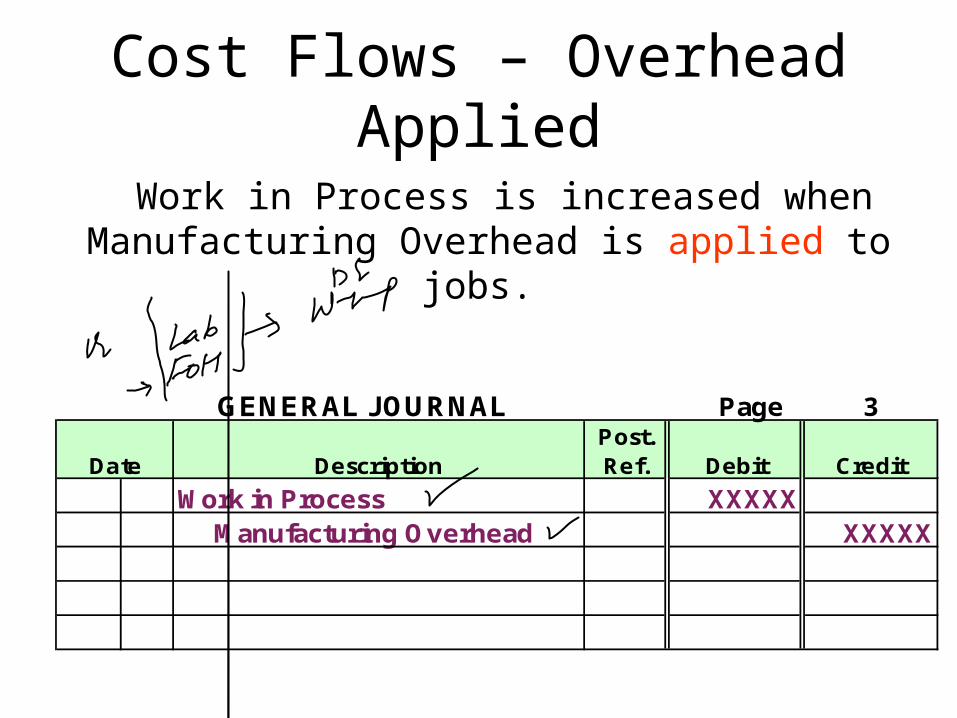

Cost Flows – Overhead Applied

Work in Process is increased when Manufacturing Overhead is applied to jobs.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work in Process XXXXX Manufacturing Overhead XXXXX

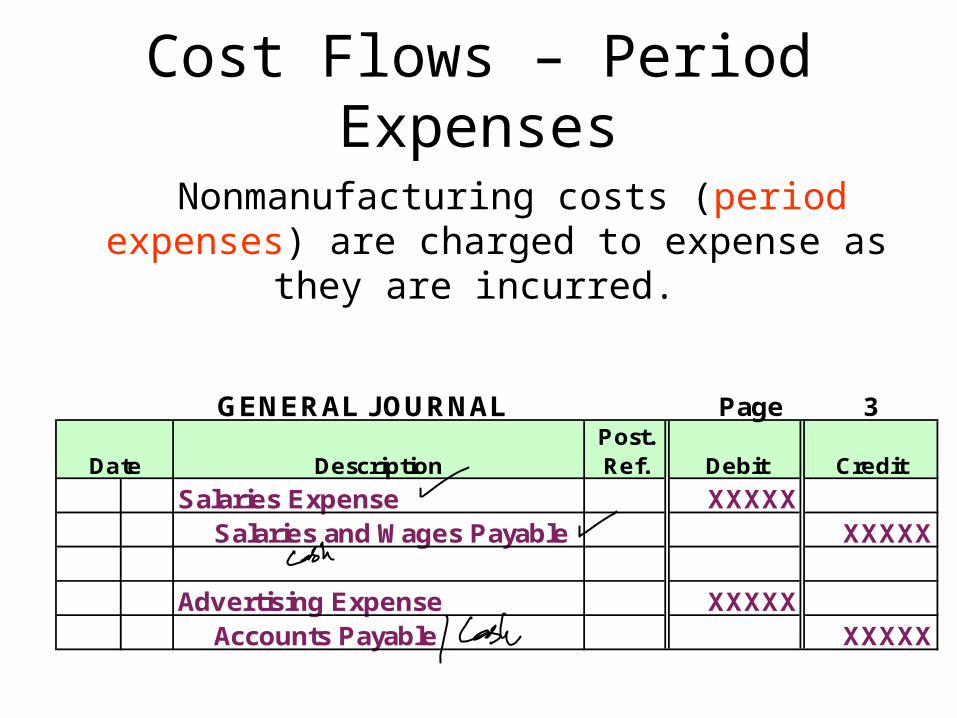

Cost Flows – Period Expenses

Nonmanufacturing costs (period expenses) are charged to expense as they are incurred.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Salaries Expense XXXXX Salaries and Wages Payable XXXXX

Advertising Expense XXXXX Accounts Payable XXXXX

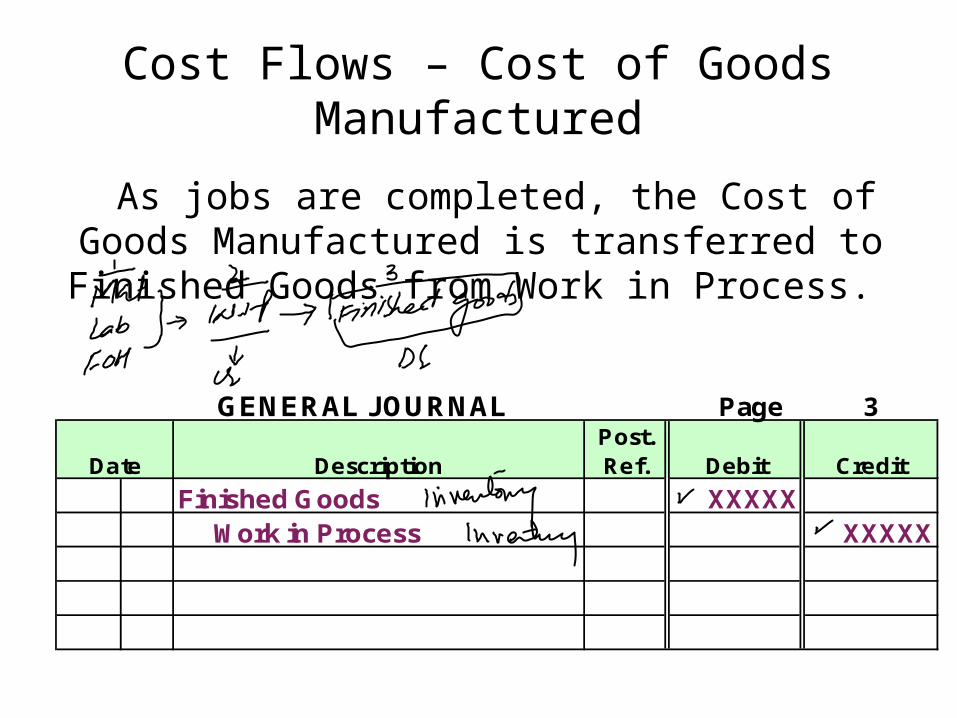

Cost Flows – Cost of Goods Manufactured

As jobs are completed, the Cost of Goods Manufactured is transferred to Finished Goods from Work in Process.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Finished Goods XXXXX Work in Process XXXXX

Cost Flows – Sales

When finished goods are sold, two entries are required: (1) to record the sale; and (2) to record Cost of Goods

Sold and reduce Finished Goods.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Accounts Receivable XXXXX Sales XXXXX

Cost of Goods Sold XXXXX Finished Goods XXXXX

Exercise Question

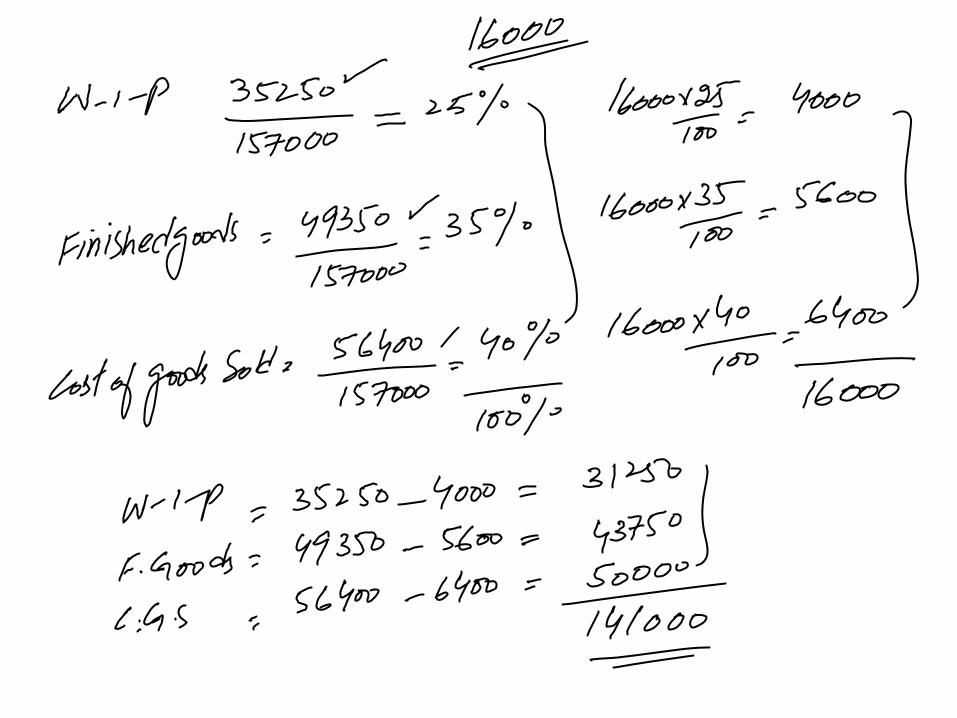

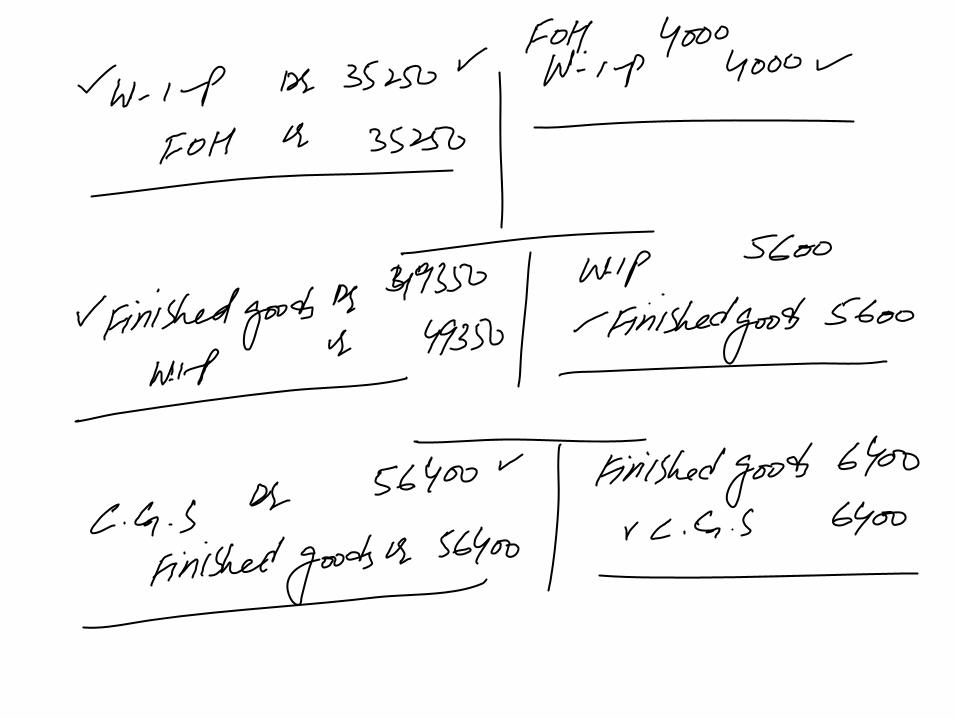

Unilever Company incurred $141000 of overhead during year just ended. However, $157000 of overhead was applied to production. At the conclusion of year, the following amounts of the year’s applied overhead remained in various manufacturing accounts.

Applied overhead remaining in account on December 31

Work in process $35250Finished Good Inventory 49350Cost of Goods Sold 72400

Required: Prepare a Journal Entry to close out the balance in the manufacturing overheadProrate the balance to the three manufacturing accounts

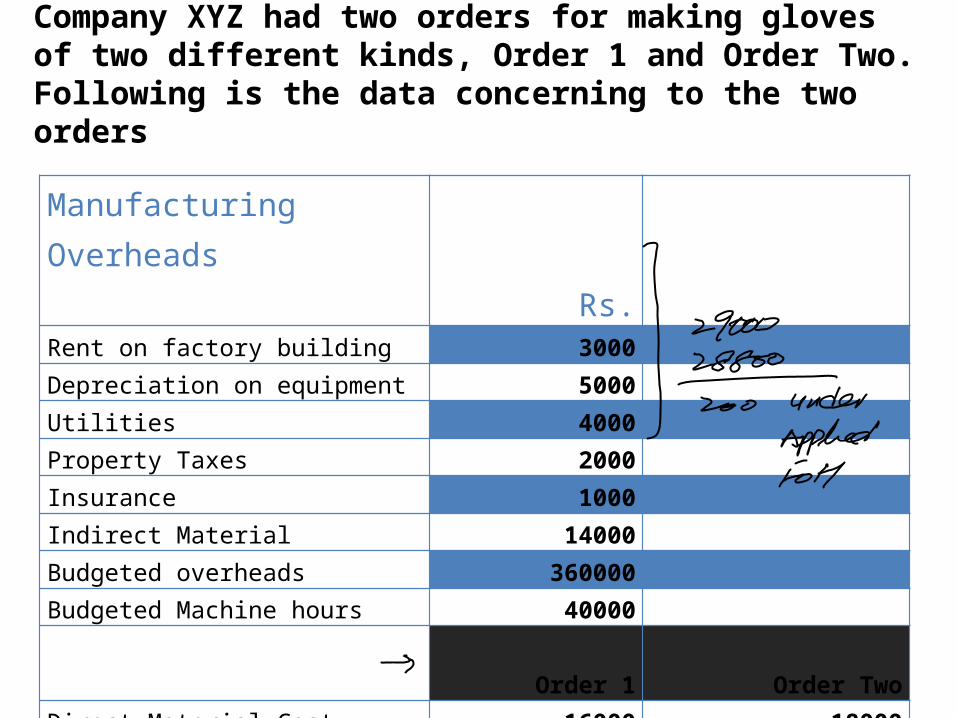

Company XYZ had two orders for making gloves of two different kinds, Order 1 and Order Two. Following is the data concerning to the two orders

Manufacturing Overheads Rs.Rent on factory building 3000Depreciation on equipment 5000Utilities 4000Property Taxes 2000Insurance 1000Indirect Material 14000Budgeted overheads 360000Budgeted Machine hours 40000

Order 1 Order TwoDirect Material Cost 16000 18000Direct Labor Cost 9000 12000Machine Hours 1200 2000Units 20000 10000

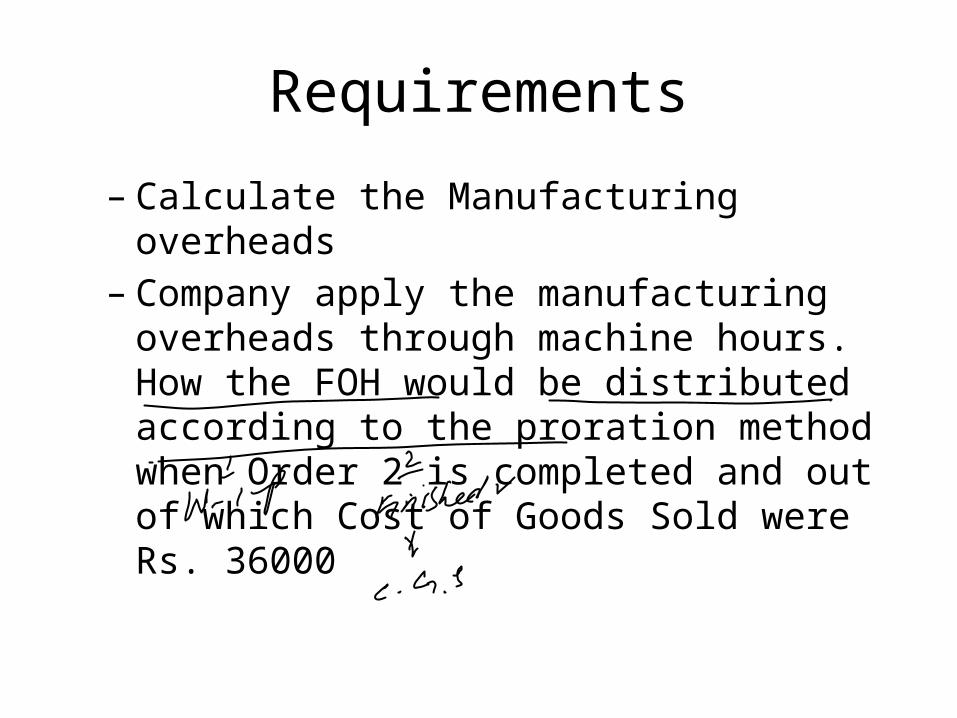

Requirements

– Calculate the Manufacturing overheads– Company apply the manufacturing overheads

through machine hours. How the FOH would be distributed according to the proration method when Order 2 is completed and out of which Cost of Goods Sold were Rs. 36000

Company XYZ had two orders for making gloves of two different kinds, Order 1 and Order Two. Following is the data concerning to the two orders

Manufacturing Overheads Rs.Rent on factory building 3000Depreciation on equipment 5000Utilities 4000Property Taxes 2000Insurance 1000Indirect Material 14000Budgeted overheads 360000Budgeted Machine hours 40000

Order 1 Order TwoDirect Material Cost 16000 18000Direct Labor Cost 9000 12000Machine Hours 1200 2000Units 20000 10000

Company XYZ had two orders for making gloves of two different kinds, Order 1 and Order Two. Following is the data concerning to the two orders

Manufacturing Overheads Rs.Rent on factory building 3000Depreciation on equipment 5000Utilities 4000Property Taxes 2000Insurance 1000Indirect Material 14000Budgeted overheads 360000Budgeted Machine hours 40000

Order 1 Order TwoDirect Material Cost 16000 18000Direct Labor Cost 9000 12000Machine Hours 1200 2000Units 20000 10000

End of Chapter 3

End of Lecture 13

Related Documents