393 ECONOMIC ANALYSIS & POLICY, VOL. 40 NO. 3, DECEMBER 2010 Labor Market Institutions and Wage and Inflation Dynamics Fatih Macit * Department of Economics Beykent University Istanbul, Turkey 34396 (Email: [email protected]) Abstract: This paper develops a New Keynesian (NK) model that incorporates standard search and matching structure with firing costs. I analyze how labor market institutions affect the macroeconomic dynamics, in particular, wage and inflation dynamics. I particularly look at two important labor market institutions namely unemployment benefits and firing costs. I find that in countries where unemployment benefits are higher and there are more strict employment protection legislations, inflation and wages become less volatile and more persistent. I also find that the level of these labor market institutions affect how wages and inflation respond to exogenous shocks, in particular, to productivity and monetary policy shocks. I first present some empirical evidence that shows a cross- country link between labor market institutions and wages and inflation. Then I build a dynamic stochastic general equilibrium model which provides theoretical support for this empirical evidence. I. INTroducTIoN The recent development of models that combine the traditional New Keynesian models and standard search and matching models have been quite successful in replicating the main business cycle dynamics that standard models fail to achieve. For instance, these models are able to obtain large and persistent responses of output to exogenous shocks and relatively smooth behavior of wages over the cycle. Gertler, Sala, and Trigari (2008) find that these models accompanied by staggered wage contracting fit the data roughly well. In a related paper Macit (2010) shows that incorporating on-the-job search does the job of staggered wage contracting and achieves the same results with fully flexible wages. Trigari (2006), Krause and Lubik (2006), and christoffel, Kuester, and Linzert (2006) are some recent examples of this modelling literature and they have been quite successful in matching important business cycle facts. Besides matching the business cycle dynamics there have also been papers that attempt to look at optimal monetary policy in these models. Faia (2006), Thomas (2008), and Arseneau and chugh (2007) are some 1 I would like to thank my advisor Professor Behzad diba for his guidance and support in the preparation of this paper. I would also like to thank Professor James Albrecht and Professor Susan Vroman for their very valuable suggestions and comments. All errors are my own.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

393

Economic AnAlysis & Policy, Vol. 40 no. 3, DEcEmBER 2010

Labor Market Institutions and Wage and Inflation Dynamics

Fatih Macit*

Department of Economics Beykent University

Istanbul, Turkey 34396 (Email: [email protected])

Abstract: ThispaperdevelopsaNewKeynesian(NK)modelthatincorporatesstandardsearchandmatchingstructurewithfiringcosts.Ianalyzehowlabormarketinstitutionsaffectthemacroeconomicdynamics,inparticular,wageandinflationdynamics.Iparticularlylookattwoimportantlabormarketinstitutionsnamelyunemploymentbenefitsandfiringcosts.Ifindthatincountrieswhereunemploymentbenefitsarehigherandtherearemorestrictemploymentprotectionlegislations,inflationandwagesbecomelessvolatileandmorepersistent.Ialsofindthattheleveloftheselabormarketinstitutionsaffecthowwagesandinflationrespondtoexogenousshocks, inparticular, toproductivityandmonetarypolicyshocks.Ifirstpresentsomeempiricalevidencethatshowsacross-countrylinkbetweenlabormarketinstitutionsandwagesandinflation.ThenIbuildadynamicstochasticgeneralequilibriummodelwhichprovidestheoreticalsupportforthisempiricalevidence.

I.INTroducTIoN

TherecentdevelopmentofmodelsthatcombinethetraditionalNewKeynesianmodelsandstandardsearchandmatchingmodelshavebeenquitesuccessfulinreplicatingthemainbusinesscycledynamicsthatstandardmodelsfailtoachieve.Forinstance,thesemodelsareabletoobtainlargeandpersistentresponsesofoutputtoexogenousshocksandrelativelysmoothbehaviorofwagesoverthecycle.Gertler,Sala,andTrigari(2008)findthatthesemodelsaccompaniedbystaggeredwagecontractingfitthedataroughlywell.InarelatedpaperMacit(2010)showsthatincorporatingon-the-jobsearchdoesthejobofstaggeredwagecontractingandachievesthesameresultswithfullyflexiblewages.Trigari(2006),KrauseandLubik(2006),andchristoffel,Kuester,andLinzert(2006)aresomerecentexamplesofthismodellingliteratureandtheyhavebeenquitesuccessfulinmatchingimportantbusinesscyclefacts.Besidesmatchingthebusinesscycledynamicstherehavealsobeenpapersthatattempttolookatoptimalmonetarypolicyinthesemodels.Faia(2006),Thomas(2008),andArseneauandchugh(2007)aresome

1 IwouldliketothankmyadvisorProfessorBehzaddibaforhisguidanceandsupportinthepreparationofthispaper.IwouldalsoliketothankProfessorJamesAlbrechtandProfessorSusanVromanfortheirveryvaluablesuggestionsandcomments.Allerrorsaremyown.

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

394

recentexamplesthatlookatoptimalmonetarypolicywithsearchandmatchingfrictionsinthelabormarketinanotherwisestandardNKmodel.

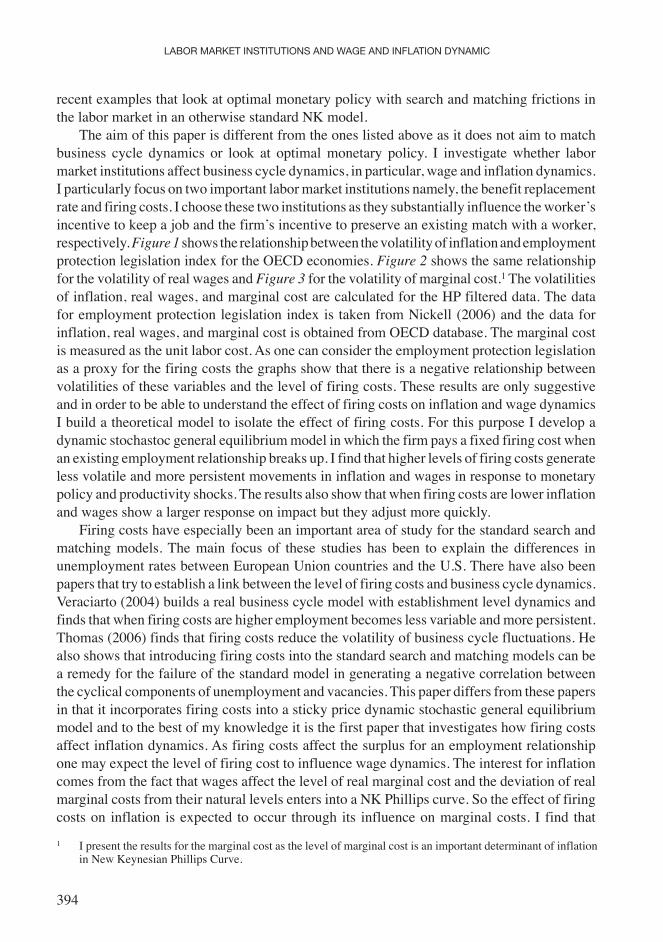

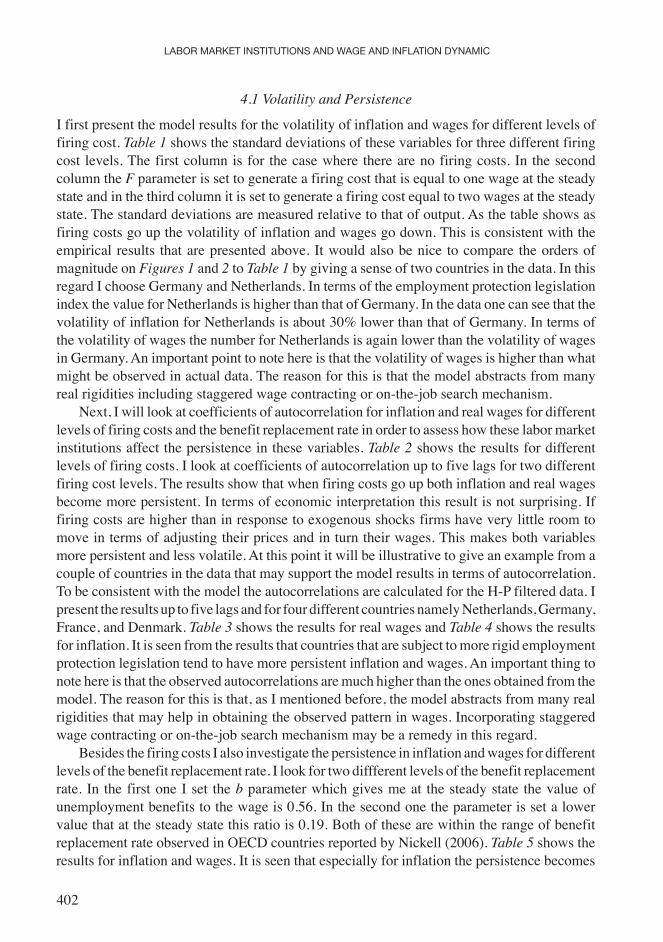

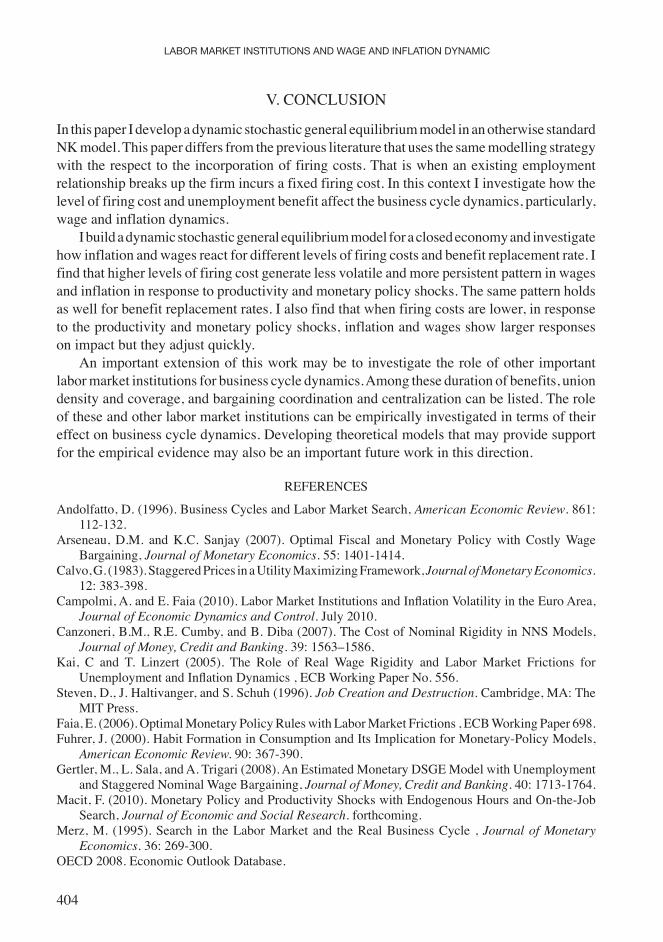

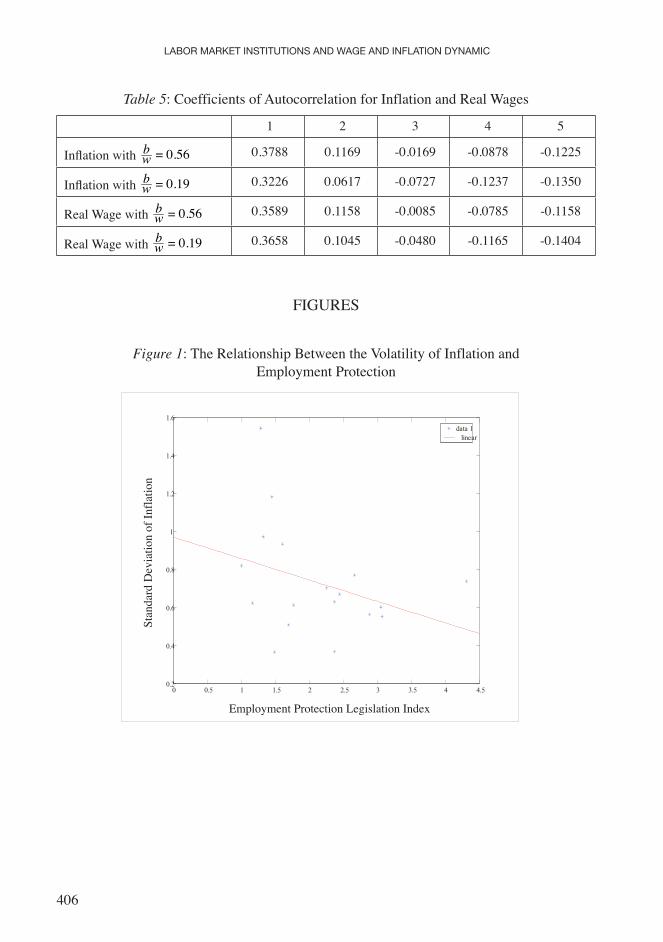

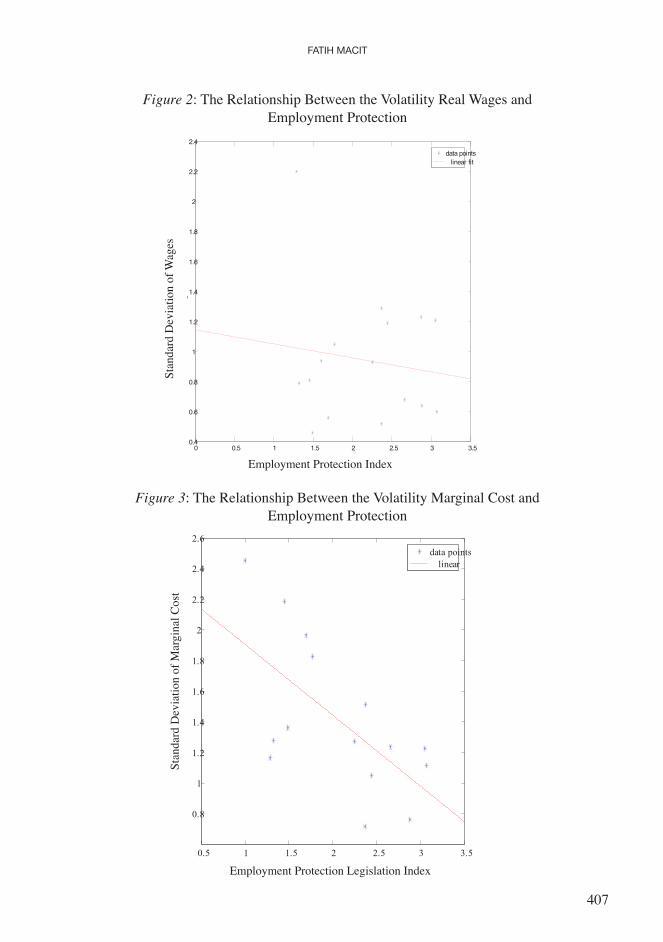

Theaimofthispaperisdifferentfromtheoneslistedaboveasitdoesnotaimtomatchbusiness cycle dynamics or look at optimalmonetary policy. I investigatewhether labormarketinstitutionsaffectbusinesscycledynamics,inparticular,wageandinflationdynamics.Iparticularlyfocusontwoimportantlabormarketinstitutionsnamely,thebenefitreplacementrateandfiringcosts.Ichoosethesetwoinstitutionsastheysubstantiallyinfluencetheworker’sincentivetokeepajobandthefirm’sincentivetopreserveanexistingmatchwithaworker,respectively.Figure 1showstherelationshipbetweenthevolatilityofinflationandemploymentprotectionlegislationindexfortheoEcdeconomies.Figure 2showsthesamerelationshipforthevolatilityofrealwagesandFigure 3forthevolatilityofmarginalcost.1Thevolatilitiesofinflation,realwages,andmarginalcostarecalculatedfortheHPfiltereddata.ThedataforemploymentprotectionlegislationindexistakenfromNickell(2006)andthedataforinflation,realwages,andmarginalcostisobtainedfromoEcddatabase.Themarginalcostismeasuredastheunitlaborcost.Asonecanconsidertheemploymentprotectionlegislationasaproxyforthefiringcoststhegraphsshowthatthereisanegativerelationshipbetweenvolatilitiesofthesevariablesandtheleveloffiringcosts.TheseresultsareonlysuggestiveandinordertobeabletounderstandtheeffectoffiringcostsoninflationandwagedynamicsIbuildatheoreticalmodeltoisolatetheeffectoffiringcosts.ForthispurposeIdevelopadynamicstochastocgeneralequilibriummodelinwhichthefirmpaysafixedfiringcostwhenanexistingemploymentrelationshipbreaksup.Ifindthathigherlevelsoffiringcostsgeneratelessvolatileandmorepersistentmovementsininflationandwagesinresponsetomonetarypolicyandproductivityshocks.Theresultsalsoshowthatwhenfiringcostsarelowerinflationandwagesshowalargerresponseonimpactbuttheyadjustmorequickly.

Firingcostshaveespeciallybeenanimportantareaofstudyforthestandardsearchandmatchingmodels.Themain focus of these studies has been to explain thedifferences inunemploymentratesbetweenEuropeanunioncountriesandtheu.S.Therehavealsobeenpapersthattrytoestablishalinkbetweentheleveloffiringcostsandbusinesscycledynamics.Veraciarto(2004)buildsarealbusinesscyclemodelwithestablishmentleveldynamicsandfindsthatwhenfiringcostsarehigheremploymentbecomeslessvariableandmorepersistent.Thomas(2006)findsthatfiringcostsreducethevolatilityofbusinesscyclefluctuations.Healsoshowsthatintroducingfiringcostsintothestandardsearchandmatchingmodelscanbearemedyforthefailureofthestandardmodelingeneratinganegativecorrelationbetweenthecyclicalcomponentsofunemploymentandvacancies.Thispaperdiffersfromthesepapersinthatitincorporatesfiringcostsintoastickypricedynamicstochasticgeneralequilibriummodelandtothebestofmyknowledgeitisthefirstpaperthatinvestigateshowfiringcostsaffectinflationdynamics.Asfiringcostsaffectthesurplusforanemploymentrelationshiponemayexpecttheleveloffiringcosttoinfluencewagedynamics.TheinterestforinflationcomesfromthefactthatwagesaffectthelevelofrealmarginalcostandthedeviationofrealmarginalcostsfromtheirnaturallevelsentersintoaNKPhillipscurve.Sotheeffectoffiringcostson inflation isexpected tooccur through its influenceonmarginalcosts. I find that

1 IpresenttheresultsforthemarginalcostasthelevelofmarginalcostisanimportantdeterminantofinflationinNewKeynesianPhillipscurve.

fAtih mAcit

395

higherfiringcostsmakeinflationlessvolatileandmorepersistent.Theleveloffiringcostalsoaffectsthepatternthatinflationshowsinresponsetoexogenousshocks,inparticular,toproductivityandmonetarypolicyshocks.

BesidestheeffectoffiringcostsonwagesandinflationdynamicsIalsoinvestigatehowthesevariablesareaffectedbythelevelofunemploymentbenefits.InthisregardanimportantpreviousstudyhasbeendonebycampolmiandFaia(2010).Theybuildadynamicstochasticgeneralequilibriumopeneconomymodelforamonetaryunion.TheythenaskthequestionwhethertheinflationdifferentialsbetweenEuropeanunioncountriescanbeexplainedbythedifferencesinlabormarketinstitutions.Theyparticularlylookatthelevelofunemploymentbenefits inEuropeanunioncountriesmeasuredbybenefit replacement rateand find thathigherlevelsofunemploymentbenefitsareassociatedwithlowervolatiliesofinflation,wages,andrealmarginalcost.InthecurrentmodelIlookattheeffectofunemploymentbenefitsonwagesandinflationfromtheperspectiveofaclosedeconomyasopposedtotheopeneconomymodelofcampolmiandFaia(2007)andIalsoinvestigatehowthesevariablesrespondtoproductivityandmonetarypolicyshocks.

Therestofthepaperisorganizedasfollows.Inthenextsection,Ibuildacloseddynamicstochasticgeneralequilibriummodelinordertobeabletoisolatetheeffectoffiringcostoninflationandwagedynamics.SectionIIIdealswiththecalibrationofthemodelandSectionIVpresentstheresults.SectionVconcludes.

II.ModEL

ThemodelthatIadoptisveryclosetothatdevelopedbyTrigari(2006).ThedifferencebetweenthismodelandtheoneproposedbyTrigari(2006)isthatfirmsincurfiringcostswhenanexistingemploymentrelationshipbreaksup.Therearefouragentsintheeconomy:workers,intermediategoodfirms,retailfirms,andamonetaryauthority.Ifirstcharacterizetheproblemoftherepresentativehouseholdandthenthelaborandproductmarkets.

2.1 Households

Eachhouseholdconsistsofacontinuumofmemberswithnamesontheunitinterval.Eachmemberhasthefollowingutilityfunction:

€

u(ct ,ct−1) − g(ht ) = log(ct −ξct−1) −Ψh

ht1+φ

1+φ (1)

wherectistheconsumptionofthefinalgood,htisthehoursworkedandIallowforhabitpersistence.2Therepresentativehouseholdmaximizeslifetimeutilitybychoosingconsumption,ct,andbondholdings,Bt,subjecttothebudgetconstraint.Thelifetimeutilityofthehouseholdisgivenby:

€

Et

s=0

∞

∑β s[u(c

t+s,ct+s−1) −Gt+s] (2)

whereβε(0,1)istheintertemporaldiscountfactorandthevariableGt isthefamily’sdisutility

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

396

fromsupplyinghoursofwork.3Idonotwritethisfunctionexplicitlyashoursworkedisnotachoicevariableforthehousehold.Ineachperiodhouseholdsaresubjecttothefollowingbudgetconstraint:

€

ct +Bt

ptrt= dt +

Bt−1

pt (3)

wherept is theaggregatepricelevelandrt is thegrossnominal interestrateonthebond.FollowingMerz(1995)andAndolfatto(1996),Iassumethatthereisperfectconsumptionrisksharingbetweenemployedandunemployedfamilymembers.Thevariabledtincludeswageincomeearnedbyemployedmembers,unemploymentbenefitsearnedbyunemployedmembers,theshareofprofitsfromretailers,netofagovernmentlump-sumtaxusedtofinanceunemploymentbenefits.

Therepresentativehouseholdmaximizes(2)subjecttotheperiodbudgetconstraintbychoosingconsumptionandbondholdings.Thefirstorderconditionsforaninteriorsolutionareasfollows:

€

λt=

1

ct−ξc

t−1

−Etβξ

1

ct+1 −ξct

(4)

€

λt= E

t[βr

t

λt+1

πt+1

] (5)

whereλtistheLagrangemultiplierassociatedwiththebudgetconstraintandπt+1isthegrossinflationrate.

2.2 Firms and the Labor Market

Therearetwotypesoffirmsinthemodel:intermediategoodsfirmsandretailfirms.Intermediategoodsfirmscarryouttheactualproductionusinglaborastheonlyfactorofproduction.Thesefirmsaresubjecttosearchandmatchingfrictionsinthelabormarketandselltheiroutputinaperfectlycompetitivemarket.retailfirmsfacemonopolisticcompetitionandaresubjecttonominalrigiditiesinthepricesettingdecision.

2.2.1TheLaborMarket

Thematchingprocessbetweentheworkersandthefirmsischaracterizedbyamatchingfunctionwhichgivesthenumberofmatchesinagivenperiodbetweenjobseekersandvacancies.Thetotalnumberofperperiodnewmatchesisgivenbythefollowingfunction:

€

mt=Mu

t

µvt

1−µ (6)

wherevtisthemeasureofvacanciespostedbyfirmsandutisthemeasureofunemployedworkerssearchingforajob.Iassumeaconstantreturntoscalematchingfunctionwhichischaracterizedby

€

mt = Mutµvt

1−µ .TheconstantMreflectstheefficiencyofthematchingprocess.

3 Assumingthatthereisperfectconsumptionrisksharingbetweenemployedandunemployedfamilymembersallowsonetoaggregatetheutilityfunctionforthefamily.

fAtih mAcit

397

Icanderivetheprobabilitiesofmakingamatchforfirmsandsearchingworkersusingthematchingfunction.Idefine

€

θt = vt /ut asthemeasureoflabormarkettightnessinthematchingmarket.Afirmfillsavacancywithprobabilityqt ≡ mt /vt andaworkersearchingforajobmakesamatchwithprobabilityst ≡ mt/ut.Theseprobabilitiesaregivenby:

€

qt =Mθt−µ (7)

€

st=Mθ

t

1−µ (8)

Iassumethatmatchesbreakupexogenouslywithprobabilityρ.Giventhistheevolutionofemploymentisasfollows:

€

nt+1 = (1− ρ)(nt +m

t) (9)

wherent isthenumberofpeopleemployedinperiodt.Thisequationimpliesthatnewmatchedcannotenter into theproductionfunctionif therelationshipisbrokenuprightafterbeingnegotiated.Asthemeasureoflaborisequaltoone,thenumberofunemployedpeople,ut,isgivenby:

ut =1– nt (10)

2.2.2ValueFunctions

TheproblemoftheworkersandthefirmsischaracterizedbyBellmanequations.Ifirststartwiththevaluefunctionsforthefirms.ThevalueofacontinuingemploymentrelationshipforafirmisdenotedasJt andthethevalueofanewemplomentrelationshipdenotedas

€

Jtn

andaregivenby:

€

Jt = xtat f (ht ) −wtht +Etβt,t+1[(1− ρ)Jt+1 + ρ(Vt −F)] (11)

€

Jtn = xtat f (ht ) − wt

nht + Etβt,t +1[(1− ρ)Jt +1 + ρ(Vt − F)] (12)

wherewt isthewagepaidforanexistingemploymentrelationshipand

€

wtn istheonefora

newemploymentrelationship,xt isthepriceoftheintermediategoodandatistheproductivityshock.Thevalueof a continuingmatch is equal to the current profitswhich is givenby

€

xtat f (ht ) − wtht plusthecontinuationvalue.4Withprobabilityl–ρthematchcontinuesandthefirmenjoystheexpectedvalueofthejob.Withprobabilityρ thematchbreaksupnextperiod.InthiscasethefirmenjoysthevalueofavacancybutatthesametimeincursthefixedfiringcostgivenbyF.5Thefuturevalueofthejobisdiscountedbythediscountfactorβt+1whichisgivenbyβλt + 1 / λt.

Thevalueofavacancy,Vt,isasfollows:

€

Vt =−κ +Etβt,t+1[qt (1− ρ)Jt+1 + (1− qt )Vt+1] (13)

4 Theproductionfunctionf(h)isassumedtobeadecreasingreturnstoscaleproductionfunction.5 Firingcostsarenotmodelledintheformofseverancepayment.

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

398

whereκistheflowcostofpostingavacancy.Withprobability

€

qt (1− ρ) avacancywillbefillednextperiodandwillactuallybeproducing.Assumingfreeentryofvacancieswilldrivethevalueofavacancytozeroinordertoeliminateanyarbitrageopportunity.Thiswillgivethefollowingequilibriumcondition:

€

κ

qt= Etβt,t+1[(1− ρ)Jt+1]

(14)

Themeaningofthisequilibriumconditionisthattheexpectedcostofavacancyisequaltotheexpectedbenefitreceivedfromfillingthatvacancy.

NowletWt andUt bethevalueofemploymentandunemploymentrespectivelyfromtheperspectiveofaworker.Valueofemploymentforaworkerisgivenby:

€

Wt = wtht −g(ht )

λt+Etβt,t+1[(1− ρ)Wt+1 + ρUt+1]

(15)

Theterm

€

g(ht )λt

isthedisutilityfromsupplyinghoursofworkanditisexpressedintermsof current consumption inorder topreserveconsistencybetween the terms.Thevalueofunemploymentisgivenbythefollowingvaluefunction:

€

Ut= b+E

tβt,t+1[st (1− ρ)Wt+1 + (1− s

t(1− ρ))U

t+1] (16)

whereb isthevalueofunemploymentbenefitsreceivedbytheworkerwhichisfinancedbyalump-sumgovernmenttax.

2.2.3WageBargaining

Iassumethatwagesaredeterminedbysurplussplittingassumption.However,thepresenceoffiringcostscreatesdifferencebetweenthesurplusforanewemploymentrelationshipandthesurplusforanexistingemploymentrelationshipfromtheperspectiveofafirm.Whenaworkerandafirmmeetforthefirsttimeforawagebargainthefirmdoesnotneedtopayafiringcostifthematchisnotsuccessful.ontheotherhand,foranexistingemploymentrelationshipifthematchbreaksupthefirmincursafixedfiringcost.Sowhencalculatingthesurplusforafirmthathasanexistingmatchoneneedstotakeintoaccountthefiringcoststhatareavoidedifthematchcontinues.Foranewmatchtheoutcomeofthesurplussplittingassumptionmaximizestheproduct:

€

(Wt−U

t)η(J

t

n −Vt)1−η (17)

wherethefirsttermisthesurplusfortheworkerandthesecondtermisthesurplusforthefirm.Theparameterη reflectsthebargainingpoweroftheworker.Firmsandworkersmaximizethejointsurplusofthematch.Thewagethatmaximizesthejointsurplusgivesthefollowingfirstordercondition:

€

ηJt

n= (1−η)(W

t−U

t) (18)

fAtih mAcit

399

AsImentionedabovethesurplusforafirmfromanexistingemploymentrelationshipwilldifferfromtheoneforanewmatchduetothefiringcostthatthefirmincurswhenthematchbreaks up. For an existing employment relationship the outcome of the surplus splittingassumptionmaximizesthefollowingproduct:

€

(Wt−U

t)η(J

t− (V

t−F))1−η (19)

ThesecondtermreflectsthefactthatwhenthematchendsupthefirmendsupwiththevalueofvacancyandpaysthefixedfiringcostsF.Thewagethatmaximizesthejointsurplusgivesthefollowingoptimalitycondition:

€

η(Jt+F) = (1−η)(W

t−U

t) (20)

usingthesebargainingequationsandthejobcreationconditiongivesusthewageforanewmatchandthewageforanexistingemploymentrelationship:

€

wt =ηxtat f (ht )

ht+κθtht

+(1− βρ)F

ht]+ (1−η)[

g(ht )

htλt+b

ht] (21)

€

wtn=η

xtat f (ht )

ht+κθtht

−βρF

ht]+ (1−η)[

g(ht )

htλt+b

ht] (22)

where

€

wtn referstothewageforaworkerthathasmadeanewmatchwiththefirm.Thewage

equationsshowthatworkersthatalreadyhaveajobbenefitfromahigherfiringcostwhereasworkersthatdonothaveajobareharmed.ThisisalsoconsistentwiththeempiricalevidencereportedbyoEcdmentioningthatworkersthatalreadyhaveajobarefavoredbyhigherfiringcostswhereasthehigherfiringcostsmakeitmoredifficultforoutsiderstofindajobandreducestheirwages.

ForthedeterminationofhoursworkedIassumethatworkersandfirmsjointlydeterminehours.Trigari(2006)definesthisbargainingprocedureasefficientbargaining.Theoptimalityconditionforthedeterminationofhoursworkedisgivenby:

€

xtat fh (ht ) =g'(ht )

λt (23)

where

€

at fh (ht ) referstomarginalproductofhoursworkedand

€

g' (ht )λ

denotesmarginalrateofsubstitution.

2.3 Retail Firms

There is a continuum of retails firms on the unit interval indexed by j operating in amonopolisticallycompetitivemarket.retailfirmstransformtheintermediategoodswithatechnologyandresellthemtothehouseholdsasafinalconsumptiongood.definingyjt astheoutputproducedbyretailfirmj,finalgoods,denotedbyyt, aregivenbythefollowingcombinationofindividualretailgoods:

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

400

€

yt = 0

1

∫ y jtε−1

ε dj

ε

ε−1

(24)

whereεistheelasticityofsubstitutionacrossthedifferentiatedretailgoods.usingthisconditioneachretailfirmhasthefollowingdemandfunctiongivenby:

€

y jt = (p jt

pt)−εyt (25)

wherepjt isthepricechargedbyretailfirmj andpt istheaggregatepriceindexgivenby:

€

pt = 0

1

∫ p jt1−εdj[ ]

1

1−ε (26)

retailfirmsaresubjecttocalvo(1983)typenominalpricerigidity.Eachperiodaretailfirmisallowedtoadjustitspricewithprobability1–ϕ andthisprobabilityisindependentofhistoryofpriceadjustments.Theretailfirmsthathavethechancetosettheirpricewillchoosetheirpriceinordertomaximizetheirexpectedfuturediscountedprofitssubjecttothedemandfortheirgoodandtotheconditionthatthepricethattheysetatdatet prevailsatdatet + k withprobabilityϕt + k.Thefirstorderconditionfortheretailfirm’sprofitmaximizationproblemisgivenby:

€

p jt = ςEtk=0

∞

∑ψ t,t +kmct +kn (27)

where

€

ς = εε −1istheflexiblepricemarkupandtheterm

€

mctn = ptmct isthenominalmarginal

costatdatet. Therelevantweights

€

ψ t,t +k arewrittenas:

€

ψ t,t+k =ϕ kβt,t+kRjt,t+k

Etk=0

∞

∑ϕ kβt,t+kRjt,t+k

(28)

whereRjt, t + k istherevenueattimet + k giventhatthelastpriceadjustmentisdoneinperiodt

2.4 Monetary Authority

Iassumethattheshort-terminterestrateisthepolicyinstrumentofthemonetarypolicyandthemoneysupplyisadjustedaccordingly.IsetaTaylortyperuleforthenominalinterestratergivenby:

€

rt = β−(1−τ )

(rt−1)τEt (π t+1)

απ(1−τ )

(yt − y)αy(1−τ )

eεtr

(29)

wheretheparameterτmeasuresthedegreeofinterestratesmoothing.Thenominalinterestraterespondstoinflationandthedeviationofoutputfromitssteadystatevalue.Theresponsecoefficientsare

€

απ and

€

αy respectively.Thelastterminthepolicyfunction,

€

εtr ,isthei.i.d

monetarypolicyshock.

fAtih mAcit

401

Iclosethemodelbywritinganaggregateresourceconstraint.Thatisgivenby:

€

yt = ct +κvt + ρFnt−1 (30)

Thisshowsthatoutputgoestoconsumptionorvacancypostingcostorfiringcost.

III.cALIBrATIoN

InordertoinvestigatethebusinesscyclepropertiesofthetheoreticalmodelIassignnumericalvaluestothestructuralparameters.Isetthediscountfactor,β,to0.99whichimpliesa4%annualinterestrate.Thevalueofthehabitpersistenceparameterissetas0.6.Isetthelaborsupplyelasticityas1/3whichisconsistentwiththemicroeconomicstudiesthatestimatethelaborsupplyelasticitycloseto0andnothigherthan0.5.

FollowingtheliteratureIchooseacobb-douglasformforthematchingfunction.Thematchingfunctionisgivenby

€

m = Mv1−µuµ .FollowingKrauseandLubik(2006)Isetthelevelparameter,M, as0.6.InaccordancewithTrigari(2006)Isettheelasticityparameter,μ, equalto0.5.6Theparameterfortheseparationrateissetas0.1.Therearesomeempiricalestimatesintheliteraturefortheu.S.separationrate.Hall(1995)reportsthisratetobebetween8to10percent.davis,Haltiwanger,andSchuh(1996)estimatestheu.S.separationrateas8%.ThevaluethatIsetisconsistentwiththeempiricalestimates.Forthevacancypostingcost,followingKrauseandLubik(2006)Icalibrateitas0.16.Thatimpliesthatatthesteadystateabout4%oftheoutputgoestovacancypostingcost.FollowingKrauseandLubik(2006)thevaluefromunemploymentgivenbyz issetas0.4andtherelativebargainingpoweroftheworkerissetas0.5.ThisvalueisthesameastheelasticityparameterofthematchingfunctionandsosatisfiestheHosios(1990)condition.

Inowcalibratethestructuralparametersfortheretailsector.Isettheprobabilitythatafirmisnotallowedtochangeitspriceinagivenperiodequalto0.67whichimpliespricesonaveragearefixedbythreequarters.Isettheflexiblepricemarkupas10%whichimplies�

Lastly,Icalibratetheparametersfortheexogenousshocksandthemonetarypolicyrule.IassumethatthelogarithmoftheaggregateproductivityshockfollowsanAr(1)processwithacoefficient0.923whichisusedbycanzoneri,cumby,anddiba(2007).Againfollowingcanzoneri,cumby,anddiba(2007)theinterestratesmoothingparameterissetas0.824andthecoefficientsoninflationandoutputaresetequalto2.02and0.184respectively.

IV.rESuLTS

InthissectionIpresentthemodelresultsintermsofinvestigatinghowthelevelofthebenefitreplacementrateandfiringcostsaffectthewageandinflationdynamics.

6 Fortheestimationofthematchingfunction,PetrongoloandPissarides(2001)reportthisparametertobebetween0.5and0.7intheirsurveyoftheliterature.

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

402

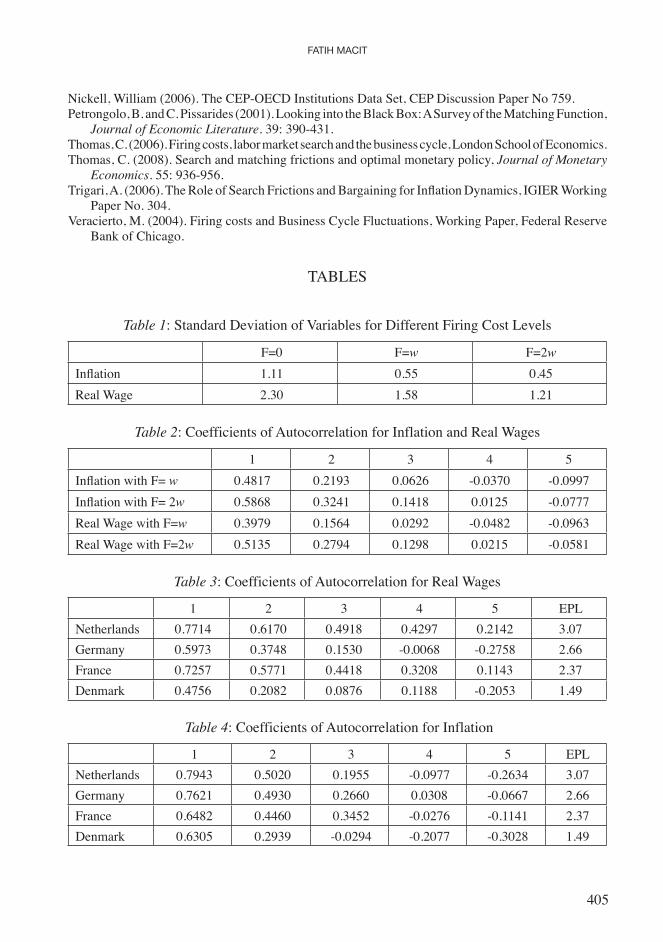

4.1 Volatility and Persistence

Ifirstpresentthemodelresultsforthevolatilityofinflationandwagesfordifferentlevelsoffiringcost.Table 1showsthestandarddeviationsofthesevariablesforthreedifferentfiringcost levels.Thefirstcolumnisfor thecasewheretherearenofiringcosts.InthesecondcolumntheF parameterissettogenerateafiringcostthatisequaltoonewageatthesteadystateandinthethirdcolumnitissettogenerateafiringcostequaltotwowagesatthesteadystate.Thestandarddeviationsaremeasuredrelativetothatofoutput.Asthetableshowsasfiringcostsgoupthevolatilityofinflationandwagesgodown.Thisisconsistentwiththeempiricalresults thatarepresentedabove.Itwouldalsobenice tocompare theordersofmagnitudeonFigures 1and2toTable 1bygivingasenseoftwocountriesinthedata.InthisregardIchooseGermanyandNetherlands.IntermsoftheemploymentprotectionlegislationindexthevalueforNetherlandsishigherthanthatofGermany.InthedataonecanseethatthevolatilityofinflationforNetherlandsisabout30%lowerthanthatofGermany.IntermsofthevolatilityofwagesthenumberforNetherlandsisagainlowerthanthevolatilityofwagesinGermany.Animportantpointtonotehereisthatthevolatilityofwagesishigherthanwhatmightbeobservedinactualdata.Thereasonforthisisthatthemodelabstractsfrommanyrealrigiditiesincludingstaggeredwagecontractingoron-the-jobsearchmechanism.

Next,Iwilllookatcoefficientsofautocorrelationforinflationandrealwagesfordifferentlevelsoffiringcostsandthebenefitreplacementrateinordertoassesshowtheselabormarketinstitutionsaffectthepersistenceinthesevariables.Table 2showstheresultsfordifferentlevelsoffiringcosts.Ilookatcoefficientsofautocorrelationuptofivelagsfortwodifferentfiringcostlevels.Theresultsshowthatwhenfiringcostsgoupbothinflationandrealwagesbecomemorepersistent.Intermsofeconomicinterpretationthisresultisnotsurprising.Iffiringcostsarehigherthaninresponsetoexogenousshocksfirmshaveverylittleroomtomoveintermsofadjustingtheirpricesandinturntheirwages.Thismakesbothvariablesmorepersistentandlessvolatile.Atthispointitwillbeillustrativetogiveanexamplefromacoupleofcountriesinthedatathatmaysupportthemodelresultsintermsofautocorrelation.TobeconsistentwiththemodeltheautocorrelationsarecalculatedfortheH-Pfiltereddata.IpresenttheresultsuptofivelagsandforfourdifferentcountriesnamelyNetherlands,Germany,France,anddenmark.Table 3showstheresultsforrealwagesandTable 4showstheresultsforinflation.Itisseenfromtheresultsthatcountriesthataresubjecttomorerigidemploymentprotectionlegislationtendtohavemorepersistentinflationandwages.Animportantthingtonotehereisthattheobservedautocorrelationsaremuchhigherthantheonesobtainedfromthemodel.Thereasonforthisisthat,asImentionedbefore,themodelabstractsfrommanyrealrigiditiesthatmayhelpinobtainingtheobservedpatterninwages.Incorporatingstaggeredwagecontractingoron-the-jobsearchmechanismmaybearemedyinthisregard.

BesidesthefiringcostsIalsoinvestigatethepersistenceininflationandwagesfordifferentlevelsofthebenefitreplacementrate.Ilookfortwodiffferentlevelsofthebenefitreplacementrate.In thefirstoneIset theb parameterwhichgivesmeat thesteadystate thevalueofunemploymentbenefitstothewageis0.56.Inthesecondonetheparameterissetalowervaluethatatthesteadystatethisratiois0.19.BothofthesearewithintherangeofbenefitreplacementrateobservedinoEcdcountriesreportedbyNickell(2006).Table 5showstheresultsforinflationandwages.Itisseenthatespeciallyforinflationthepersistencebecomes

fAtih mAcit

403

moreobviouswhenthebenefitreplacementrategoesup.Whenthebenefitreplacementrateishigherworkersarenotwillingtotakelargewagecutsinresponsetoexogenousshocks.Thismakesbothwagesandinflationmorepersistentinresponsetotheseshocks.

4.2 Impulse Responses

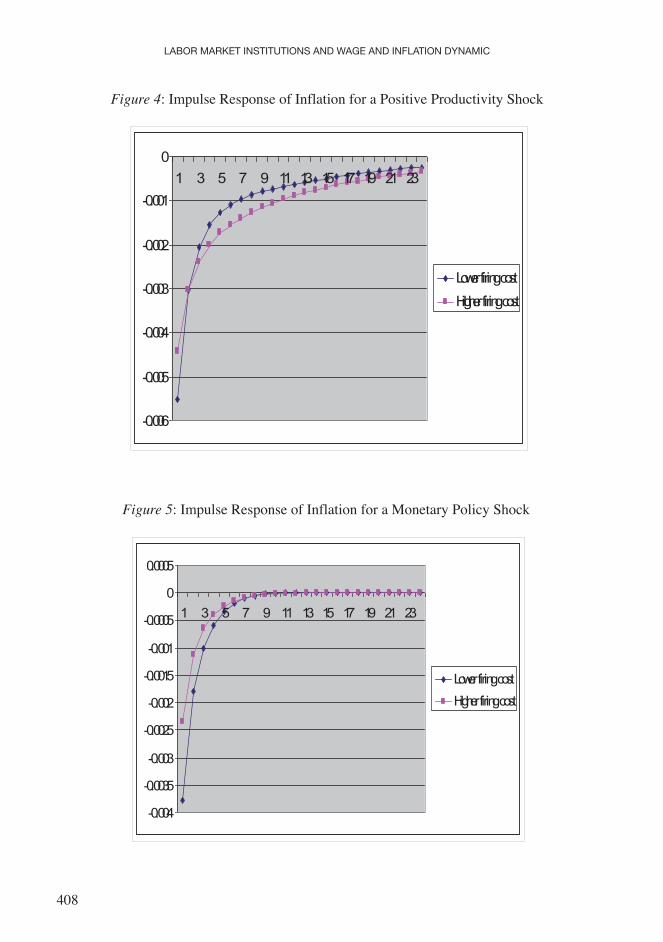

Anotherimportantissueaboutthelabormarketinstitutionsiswhetherdifferencesintheseaffecthowmacrovariablesrespondtoexogenousshocks.InthissectionIinvestigatehowtheleveloffiringcostsandthebenefitreplacementrateaffectthepatternthatinflationandwages show in response toexogenous shocks inparticular toproductivityandmonetarypolicyshock.Figure 4showstheresponseofinflationtoapositiveproductivityshockfortwodifferentfiringcostlevels.onecanseethatwhenfiringcostsarelower,onimpactinflationshowsalargerresponse.Inthiscaseonimpactinflationgoesdownby0.55%whereasinthecasewherefiringcostsarehigherinflationgoesdownbyabout0.45%.However,itisseenthatwhenfiringcostsarelowerinflationadjustsmorequicklyinresponsetotheproductivityshock.Thisisactuallyconsistentwiththepreviousresultsthatarepresented.Thatiswhenfiringcostsarehigher,inresponsetotheexogenousshocksinflationbecomesmorepersistent.Figure 5showsthesameresultsforamonetarypolicyshockthatraisestheinterestrates.onecanseethesamepatternintheresponseofinflationthatisseeninproductivityshock.oncetheeconomyishitbyamonetarypolicyshockonimpactinflationgoesdownbyabout0.4%whenthefiringcostsareloweranditgoesdownby0.25%whenfiringcostsarehigher.However,again,inflationdoesnotshowapersistentresponsewhenfiringcostsareloweranditadjustsmorequicklycomparedtothecasewherefiringcostsarehigher.

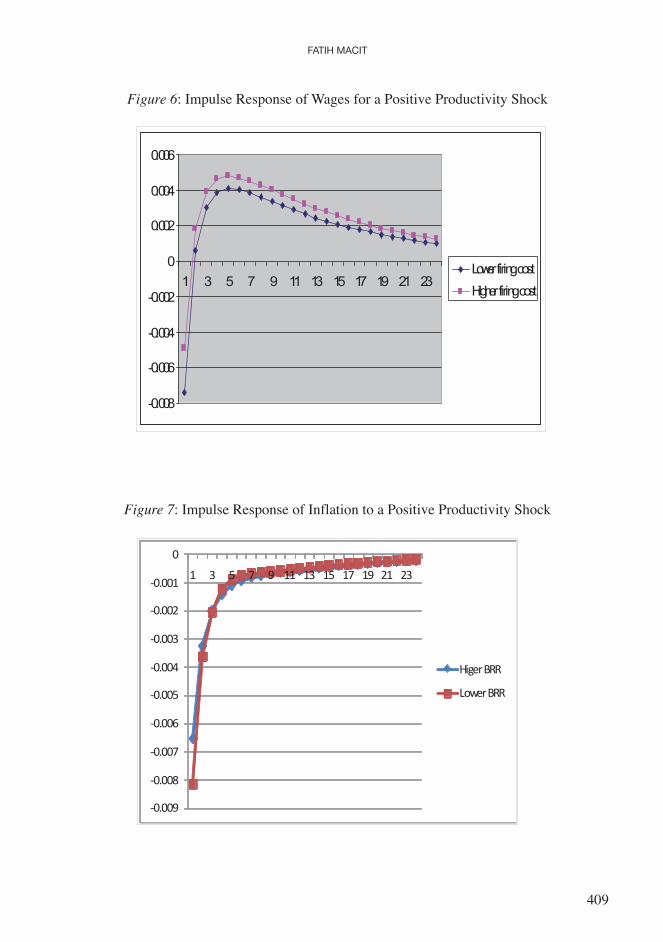

Thepatternthatisseenininflationcanalsobeseenintheresponseofwages.Figure 6shows the response ofwages in response to a positive productivity shock.one can seethatonimpactlowerfiringcostscreatealargerresponse.However,thispatterndoesnotpersistandadjustveryquickly.Lowerfiringcostsgeneratemoreflexibilityforthefirmsinadjustingtheirwagesandcreateslargerandquickeradjustmentsinwagesinresponsetotheproductivityshock.

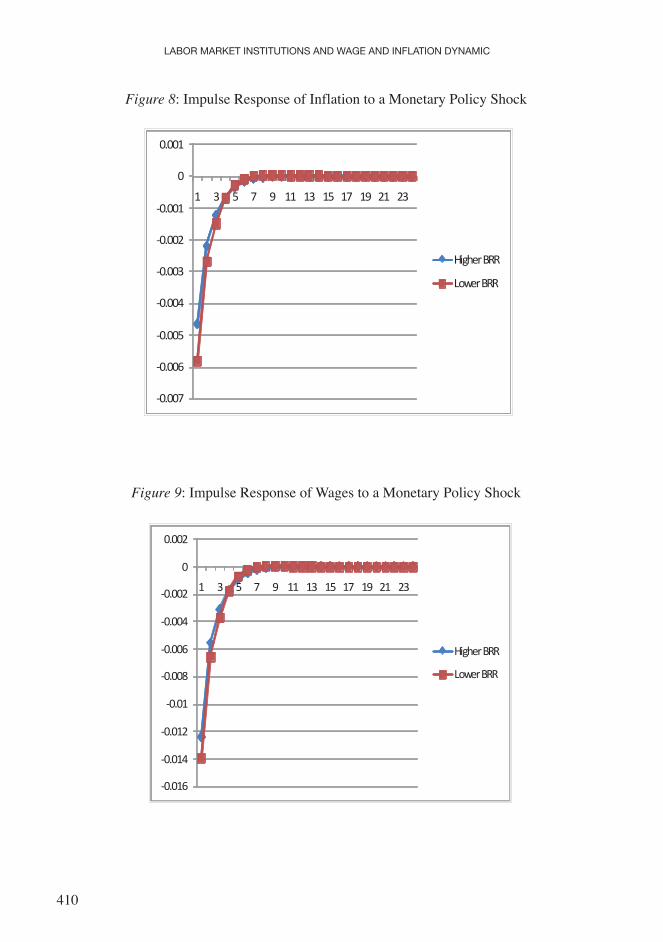

Besidestheleveloffiringcostthelevelofbenefitreplacementrateisalsoeffectivefortheresponseofinflationandwagestoproductivityandmonetarypolicyshocks.Figure 7showstheresponseofinflationtoapositiveproductivityshockfortwodifferentbenefitreplacementratesthathavebeenusedinprevioussection.Thesamepatternisobservedthathasbeenseenforfiringcosts.Whentherearelessgenerousunemploymentbenefitsonimpact,inflationshowsa larger response to thepositiveproductivityshockbut itadjusts faster than is thecasewhentherearemoregenerousunemploymentbenefits.Figure 8showsthesameresultsnowforamonetarypolicyshockandexactlythesamepatternisobserved.Lowerbenefitreplacementratesmakeinflationlesspersistentandthiscanbeobservedintheresponseofinflationtoaproductivityandmonetarypolicyshock.Figure 9showstheresponseofwagestoamonetarypolicyshockagainfortwodifferentbenefitreplacementratelevels.Whenthebenefitreplacementrateislower,wagesshowaslightlylargerresponseatthebeginningbutthenadjustveryquickly.Itisimportanttonotethattheleveloffiringcostsseemstoberelativelymoreinfluentialonimpulseresponsescomparedtotheeffectofthebenefitreplacementrate.

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

404

V.coNcLuSIoN

InthispaperIdevelopadynamicstochasticgeneralequilibriummodelinanotherwisestandardNKmodel.Thispaperdiffersfromthepreviousliteraturethatusesthesamemodellingstrategywiththerespecttotheincorporationoffiringcosts.Thatiswhenanexistingemploymentrelationshipbreaksupthefirmincursafixedfiringcost.InthiscontextIinvestigatehowtheleveloffiringcostandunemploymentbenefitaffectthebusinesscycledynamics,particularly,wageandinflationdynamics.

Ibuildadynamicstochasticgeneralequilibriummodelforaclosedeconomyandinvestigatehowinflationandwagesreactfordifferentlevelsoffiringcostsandbenefitreplacementrate.Ifindthathigherlevelsoffiringcostgeneratelessvolatileandmorepersistentpatterninwagesandinflationinresponsetoproductivityandmonetarypolicyshocks.Thesamepatternholdsaswellforbenefitreplacementrates.Ialsofindthatwhenfiringcostsarelower,inresponsetotheproductivityandmonetarypolicyshocks,inflationandwagesshowlargerresponsesonimpactbuttheyadjustquickly.

Animportantextensionofthisworkmaybetoinvestigatetheroleofotherimportantlabormarketinstitutionsforbusinesscycledynamics.Amongthesedurationofbenefits,uniondensityandcoverage,andbargainingcoordinationandcentralizationcanbelisted.Theroleoftheseandotherlabormarketinstitutionscanbeempiricallyinvestigatedintermsoftheireffectonbusinesscycledynamics.developingtheoreticalmodelsthatmayprovidesupportfortheempiricalevidencemayalsobeanimportantfutureworkinthisdirection.

rEFErENcES

Andolfatto,d.(1996).BusinesscyclesandLaborMarketSearch,American Economic Review.861:112-132.

Arseneau,d.M. andK.c. Sanjay (2007). optimal Fiscal andMonetary Policywith costlyWageBargaining,Journal of Monetary Economics.55:1401-1414.

calvo,G.(1983).StaggeredPricesinautilityMaximizingFramework,Journal of Monetary Economics.12:383-398.

campolmi,A.andE.Faia(2010).LaborMarketInstitutionsandInflationVolatilityintheEuroArea,Journal of Economic Dynamics and Control.July2010.

canzoneri,B.M.,r,E.cumby,andB.diba(2007).ThecostofNominalrigidityinNNSModels,Journal of Money, Credit and Banking.39:1563–1586.

Kai, c and T. Linzert (2005). The role of realWage rigidity and Labor Market Frictions forunemploymentandInflationdynamics,EcBWorkingPaperNo.556.

Steven,d.,J.Haltivanger,andS.Schuh(1996).Job Creation and Destruction.cambridge,MA:TheMITPress.

Faia,E.(2006).optimalMonetaryPolicyruleswithLaborMarketFrictions,EcBWorkingPaper698.Fuhrer,J.(2000).HabitFormationinconsumptionandItsImplicationforMonetary-PolicyModels,

American Economic Review. 90:367-390.Gertler,M.,L.Sala,andA.Trigari(2008).AnEstimatedMonetarydSGEModelwithunemployment

andStaggeredNominalWageBargaining,Journal of Money, Credit and Banking.40:1713-1764.Macit,F.(2010).MonetaryPolicyandProductivityShockswithEndogenousHoursandon-the-Job

Search,Journal of Economic and Social Research.forthcoming.Merz,M. (1995).Search in theLaborMarketand therealBusinesscycle ,Journal of Monetary

Economics. 36:269-300.oEcd2008.Economicoutlookdatabase.

fAtih mAcit

405

Nickell,William(2006).ThecEP-oEcdInstitutionsdataSet,cEPdiscussionPaperNo759.Petrongolo,B.andc.Pissarides(2001).LookingintotheBlackBox:ASurveyoftheMatchingFunction,

Journal of Economic Literature.39:390-431.Thomas,c.(2006).Firingcosts,labormarketsearchandthebusinesscycle,LondonSchoolofEconomics.Thomas,c.(2008).Searchandmatchingfrictionsandoptimalmonetarypolicy,Journal of Monetary

Economics.55:936-956.Trigari,A.(2006).TheroleofSearchFrictionsandBargainingforInflationdynamics,IGIErWorking

PaperNo.304.Veracierto,M.(2004).FiringcostsandBusinesscycleFluctuations,WorkingPaper,Federalreserve

Bankofchicago.

TABLES

Table 1:StandarddeviationofVariablesfordifferentFiringcostLevels

F=0 F=w F=2wInflation 1.11 0.55 0.45realWage 2.30 1.58 1.21

Table 2:coefficientsofAutocorrelationforInflationandrealWages

1 2 3 4 5InflationwithF=w 0.4817 0.2193 0.0626 -0.0370 -0.0997InflationwithF=2w 0.5868 0.3241 0.1418 0.0125 -0.0777realWagewithF=w 0.3979 0.1564 0.0292 -0.0482 -0.0963realWagewithF=2w 0.5135 0.2794 0.1298 0.0215 -0.0581

Table 3:coefficientsofAutocorrelationforrealWages

1 2 3 4 5 EPLNetherlands 0.7714 0.6170 0.4918 0.4297 0.2142 3.07Germany 0.5973 0.3748 0.1530 -0.0068 -0.2758 2.66France 0.7257 0.5771 0.4418 0.3208 0.1143 2.37denmark 0.4756 0.2082 0.0876 0.1188 -0.2053 1.49

Table 4:coefficientsofAutocorrelationforInflation

1 2 3 4 5 EPLNetherlands 0.7943 0.5020 0.1955 -0.0977 -0.2634 3.07Germany 0.7621 0.4930 0.2660 0.0308 -0.0667 2.66France 0.6482 0.4460 0.3452 -0.0276 -0.1141 2.37denmark 0.6305 0.2939 -0.0294 -0.2077 -0.3028 1.49

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

406

Table 5:coefficientsofAutocorrelationforInflationandrealWages

1 2 3 4 5

Inflationwith

bw = 0.56 0.3788 0.1169 -0.0169 -0.0878 -0.1225

Inflationwith

bw = 0.19 0.3226 0.0617 -0.0727 -0.1237 -0.1350

realWagewith

bw = 0.56 0.3589 0.1158 -0.0085 -0.0785 -0.1158

realWagewith

bw = 0.19 0.3658 0.1045 -0.0480 -0.1165 -0.1404

FIGurES

Figure 1:TherelationshipBetweentheVolatilityofInflationandEmploymentProtection

Inflation with

0.56=wb

0.3788 0.1169 -0.0169 -0.0878 -0.1225

Inflation with

0.19=wb

0.3226 0.0617 -0.0727 -0.1237 -0.1350

Real Wage with

0.56=wb

0.3589 0.1158 -0.0085 -0.0785 -0.1158

Real Wage with

0.19=wb

0.3658 0.1045 -0.0480 -0.1165 -0.1404

0 0.5 1 1.5 2 2.5 3 3.5 4 4.50.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Employment Protection Legislation Index

The S

tandar

d Devi

ation o

f Infla

tion

data 1 linear

Figure 1: The relationship between the volatility of inflation and employment

StandarddeviationofInflation

EmploymentProtectionLegislationIndex

fAtih mAcit

407

Figure 2:TherelationshipBetweentheVolatilityrealWagesandEmploymentProtection

Figure 3:TherelationshipBetweentheVolatilityMarginalcostandEmploymentProtection

0 0.5 1 1.5 2 2.5 3 3.50.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2.2

2.4

Employment Protection Index

Standa

rd Devia

tion of W

ages

data points linear fit

Figure 2: The relationship between the volatility real wages and

0.5 1 1.5 2 2.5 3 3.5

0.8

1

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

Employment Protection Legislation Index

Standa

rd Devi

ation o

f Marg

inal C

ost

data points linear

Figure 3: The relationship between the volatility marginal cost and employment protection

-0.006

-0.005

-0.004

-0.003

-0.002

-0.001

01 3 5 7 9 11 13 15 17 19 21 23

Lower firing costHigher firing cost

Figure 4: Impulse response of inflation for a positive productivity shock

StandarddeviationofWages

StandarddeviationofM

arginalc

ost

EmploymentProtectionIndex

EmploymentProtectionLegislationIndex

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

408

Figure 5:ImpulseresponseofInflationforaMonetaryPolicyShock

Figure 4:ImpulseresponseofInflationforaPositiveProductivityShock

0.5 1 1.5 2 2.5 3 3.5

0.8

1

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

Employment Protection Legislation Index

Standa

rd Devi

ation o

f Marg

inal C

ost

data points linear

Figure 3: The relationship between the volatility marginal cost and employment protection

-0.006

-0.005

-0.004

-0.003

-0.002

-0.001

01 3 5 7 9 11 13 15 17 19 21 23

Lower firing costHigher firing cost

Figure 4: Impulse response of inflation for a positive productivity shock

-0.004

-0.0035

-0.003

-0.0025

-0.002

-0.0015

-0.001

-0.0005

0

0.0005

1 3 5 7 9 11 13 15 17 19 21 23

Lower firing costHigher firing cost

Figure 5: Impulse response of inflation for a monetary policy shock

-0.008

-0.006

-0.004

-0.002

0

0.002

0.004

0.006

1 3 5 7 9 11 13 15 17 19 21 23Lower firing costHigher firing cost

Figure 6: Impulse response of wages for a positive productivity shock

fAtih mAcit

409

Figure 6:ImpulseresponseofWagesforaPositiveProductivityShock

Figure 7:ImpulseresponseofInflationtoaPositiveProductivityShock

-0.004

-0.0035

-0.003

-0.0025

-0.002

-0.0015

-0.001

-0.0005

0

0.0005

1 3 5 7 9 11 13 15 17 19 21 23

Lower firing costHigher firing cost

Figure 5: Impulse response of inflation for a monetary policy shock

-0.008

-0.006

-0.004

-0.002

0

0.002

0.004

0.006

1 3 5 7 9 11 13 15 17 19 21 23Lower firing costHigher firing cost

Figure 6: Impulse response of wages for a positive productivity shock

-0.009

-0.008

-0.007

-0.006

-0.005

-0.004

-0.003

-0.002

-0.001

0

1 3 5 7 9 11 13 15 17 19 21 23

Higer BRR

Lower BRR

Figure 7: Impulse response of inflation to a positive productivity shock

-0.007

-0.006

-0.005

-0.004

-0.003

-0.002

-0.001

0

0.001

1 3 5 7 9 11 13 15 17 19 21 23

Higher BRR

Lower BRR

Figure 8: Impulse response of inflation to a monetary policy shock

lABoR mARkEt institutions AnD WAgE AnD inflAtion DynAmic

410

Figure 8:ImpulseresponseofInflationtoaMonetaryPolicyShock

Figure 9:ImpulseresponseofWagestoaMonetaryPolicyShock

-0.009

-0.008

-0.007

-0.006

-0.005

-0.004

-0.003

-0.002

-0.001

0

1 3 5 7 9 11 13 15 17 19 21 23

Higer BRR

Lower BRR

Figure 7: Impulse response of inflation to a positive productivity shock

-0.007

-0.006

-0.005

-0.004

-0.003

-0.002

-0.001

0

0.001

1 3 5 7 9 11 13 15 17 19 21 23

Higher BRR

Lower BRR

Figure 8: Impulse response of inflation to a monetary policy shock

-0.016

-0.014

-0.012

-0.01

-0.008

-0.006

-0.004

-0.002

0

0.002

1 3 5 7 9 11 13 15 17 19 21 23

Higher BRR

Lower BRR

Figure 9: Impulse response of wages to a monetary policy shock

Related Documents