Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group 1 2009 Q4 LI & FUNG RESEARCH CENTRE CHINA CHAIN STORE & FRANCHISE ASSOCIATION KPI report for retail chain stores in China Foreword About the KPI report The China Chain Store & Franchise Association and the Li & Fung Research Centre have collaborated and established the Key Performance Index System (hereafter the “KPI system”) for retail chain operators in China since 2007 and published reports on a quarterly basis. The system aims to collect key performance indices of different format retail stores in China. In 2009, the data collection system are further upgraded and revised, and more store samples have been added. The revised KPI report covers over 100 retail stores in China of 5 major formats, including convenience stores, supermarkets, hypermarkets, department stores and home electronics appliance chains, of which supermarkets and hypermarkets are further divided into several categories by operating area for easier references. We hope this report can shed some light on the key development trends of China's retail chain stores. About the indicators Data of the following is collected in the KPI system – 1. Monthly sales ( ) – Pre-tax monthly sales value 2. Total operating area ( ) – Including self-operating area and leasing area 3. Leasing area ( ) – Area leased to other operators 4. Total staff number ( ) – Total number of staff including dispatched employees hired by labor agents ( ) 5. Total number of contract staff ( ) – Total number of staff hired directly by the retailers 6. Total operating cost ( ) 7. Total salaries and wages ( ) 8. Total number of SKUs ( ) 9. Number of SKUs distributing directly through the distribution centre ( ) 10. Average daily number of transactions ( ) 11. Inventory turnover days ( ) 12. Non-operating income ( ) – Income derived from activities other than sales of goods

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

1

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

KPI report for retail chain stores in China

Foreword

About the KPI report

The China Chain Store & Franchise Association and the Li & Fung Research Centre have collaborated and established

the Key Performance Index System (hereafter the “KPI system”) for retail chain operators in China since 2007 and

published reports on a quarterly basis. The system aims to collect key performance indices of different format retail

stores in China.

In 2009, the data collection system are further upgraded and revised, and more store samples have been added. The

revised KPI report covers over 100 retail stores in China of 5 major formats, including convenience stores, supermarkets,

hypermarkets, department stores and home electronics appliance chains, of which supermarkets and hypermarkets are

further divided into several categories by operating area for easier references. We hope this report can shed some light

on the key development trends of China's retail chain stores.

About the indicators

Data of the following is collected in the KPI system –

1. Monthly sales (月度銷售額) – Pre-tax monthly sales value

2. Total operating area (總營業面積) – Including self-operating area and leasing area

3. Leasing area (對外租賃面積) – Area leased to other operators

4. Total staff number (員工總數) – Total number of staff including dispatched employees hired by labor agents (勞務派遣人員)

5. Total number of contract staff (正式員工數) – Total number of staff hired directly by the retailers

6. Total operating cost (成本及費用總額)

7. Total salaries and wages (工資總額)

8. Total number of SKUs (單品總數)

9. Number of SKUs distributing directly through the distribution centre (統一配送單品數)

10. Average daily number of transactions (平均日交易數)

11. Inventory turnover days (庫存周轉天數)

12. Non-operating income (營業外收入) – Income derived from activities other than sales of goods

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

2

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Survey results by retail formats

Format Monthly sales (million yuan)

Average sales per m

2

(yuan/ m2/day)

Average sales per staff

(yuan/person/day)

Average customer spending

(yuan/visit)

Gross margin (%)

Convenience stores 0.30 92 1,301 14 18.74

Supermarkets (300-999 m2) 1.10 68 1,500 30.35 14.7

Supermarkets (1,000-1,999 m2) 2.85 68 1,301 44.73 15.42

Supermarkets (2,000-3,999 m2) 6.13 73 1,475 47.57 14.07

Supermarkets (4,000-5,999 m2) 10.99 77 1,668 45.67 12.6

Hypermarkets (6,000-9,999 m2) 12.76 54 1,431 57.4 12.45

Hypermarket (10,000-14,999 m2) 13.62 42 1,409 67.22 14.11

Hypermarket (over 15,000 m2) 22.85 40 1,485 81.12 11.49

Department stores 102.99 110 2,184 471.45 16.85

Home electronics appliance chains 61.25 131 5,435 1,572.67 n.a.

Format Cashier efficiency 1 (yuan/machine/day)

Cashier efficiency 2 (number of transaction/

machine /day)

% of damaged

goods

Inventory turnover (Days)

Average operating area per employee (m

2/employee)

Convenience stores 9,810 683 0.14 10 13.25

Supermarkets (300-999 m2) 9,001 344 0.2 20 21

Supermarkets (1,000-1,999 m2) 11,624 297 0.22 19 19.16

Supermarkets (2,000-3,999 m2) 14,139 307 0.2 34 20.3

Supermarkets (4,000-5,999 m2) 15,351 253 0.15 30 21.6

Hypermarkets (6,000-9,999 m2) 11,635 149 0.23 23 26.5

Hypermarket (10,000-14,999 m2) 14,857 252 0.25 n.a. 33.9

Hypermarket (over 15,000 m2) 15,425 200 0.23 23 36.8

Department stores 52,235 118 0.13 63 19.8

Home electronics appliance chains 116,896 75 n.a. n.a. 41.58

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

3

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

I. Convenience stores Average operating area: 106m

2

Average number of cash registers: 1 (i.e. 1 cash register for every 106 m2)

Monthly sales

0.250.28 0.29

0.33

0.22

0.23

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

7885 90

102

72

66

0

20

40

60

80

100

120

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

1,0691,206 1,263

1,433

910

989

0

500

1,000

1,500

2,000

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

12.54

16.9

12.23 12.81

11.61

16.05

0

5

10

15

20

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

600

650

700

750

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

0

5,000

10,000

15,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

19.31

18.8518.77

18.62

19.5

19.51

18

18.2

18.4

18.6

18.8

19

19.2

19.4

19.6

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

4

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 0.28 0.29 0.33 0.30 29.80%

2. Average sales per m2

(yuan/ m2/day)

85 90 102 92 28.00%

3. Average sales per staff

(yuan/person/day)

1,206 1,263 1,433 1,301 31.50%

4. Average customer spending

(yuan/visit)

16.9 12.23 12.81 14 4.30%

5. Cashier efficiency 1

(yuan/machine/day)

9,098 9,527 10,804 9,810 31.20%

Cashier efficiency 2

(number of transaction/

machine /day)

681 685 682 683 -0.30%

6. Gross margin (%) 18.85 18.77 18.62 18.74 -3.60%

7) % of damaged goods: 0.14%

8) Inventory turnover days: 10 days

8) Average operating area per employee (員工配置): 13.25 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

5

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

II. Supermarkets (divided into 4 groups according to operating area)

1. Supermarkets (300-999 m2)

Average operating area: 526 m2

Average number of cash registers: 4 (i.e. 1 for every 132 m2)

Monthly sales

1.141.07 1.03

1.211.11

0.99

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

72

6665

74

63

68

55

60

65

70

75

Jul Aug Sep Oct Nov Dec

(yuan/ m

2/d

ay)

Average sales per staff

1,579

1,443 1,429

1,629

1,495

1,376

1,200

1,300

1,400

1,500

1,600

1,700

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

33.49

27.3429.78

33.92

32.12

34.67

0

5

10

15

20

25

30

35

40

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

300

350

400

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

7,000

8,000

9,000

10,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

13.36

14.24

15.0614.81

13.89

14.05

12.5

13

13.5

14

14.5

15

15.5

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

6

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 1.07 1.03 1.21 1.10 2.30%

2. Average sales per m2

(yuan/ m2/day)

66 65 74 68 1.30%

3. Average sales per staff

(yuan/person/day)

1,443 1,429 1,629 1,500 1.10%

4. Average customer spending

(yuan/visit)

27.34 29.78 33.92 30.35 -9.20%

5. Cashier efficiency 1

(yuan/machine/day)

8,658 8,573 9,772 9,001 1.10%

Cashier efficiency 2

(number of transaction/

machine /day)

355 339 338 344 -7.90%

6. Gross margin (%) 14.24 15.06 14.81 14.7 6.80%

7) % of damaged goods: 0.2%

8) Inventory turnover days: 20 days

9) Average operating area per employee (員工配置): 21 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

7

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

2. Supermarkets (1,000-1,999 m2)

Average operating area: 1,370 m2

Average number of cash registers: 8 (i.e. 1 for every 171 m2)

Monthly sales

2.81 2.842.79

2.93

2.56

2.5

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

3

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

69

6768

69

61

61

56

58

60

62

64

66

68

70

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

1,1301,281 1,300 1,320

996

1,002

0

200

400

600

800

1,000

1,200

1,400

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

55.91

40.96 42.7

50.5351.5939.83

0

10

20

30

40

50

60

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

260

280

300

320

340

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

9,000

10,000

11,000

12,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

15.3815.47

15.78

15.0315.01 15.29

14.6

14.8

15

15.2

15.4

15.6

15.8

16

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

8

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 2.84 2.79 2.93 2.85 8.70%

2. Average sales per m2

(yuan/ m2/day)

67 68 69 68 7.10%

3. Average sales per staff

(yuan/person/day)

1,281 1,300 1,320 1,301 24.80%

4. Average customer spending

(yuan/visit)

40.96 42.7 50.53 44.73 -8.90%

5. Cashier efficiency 1

(yuan/machine/day)

11,450 11,623 11,799 11,624 7.50%

Cashier efficiency 2

(number of transaction/

machine /day)

306 302 283 297 -4.20%

6. Gross margin (%) 15.47 15.78 15.03 15.42 1.30%

7) % of damaged goods: 0.22%

8) Inventory turnover days: 19 days

9) Average operating area per employee (員工配置): 19.16 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

9

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

3. Supermarkets (2,000-3,999 m2)

Average operating area: 2,738 m2

Average number of cash registers: 14 (i.e. 1 for every 196 m2)

Monthly sales

6.26.62

5.696.065.33

5.69

0

1

2

3

4

5

6

7

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

75 7869 71

69

63

0

20

40

60

80

100

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

1,526 1,5781,402 1,4441,269

1,402

0

500

1,000

1,500

2,000

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

48.97

51.01

44.66

47.03

44.0342.73

38

40

42

44

46

48

50

52

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

0

100

200

300

400

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

0

5,000

10,000

15,000

20,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

13.45 13.53

14.5214.17

13.05 13.57

12

12.5

13

13.5

14

14.5

15

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

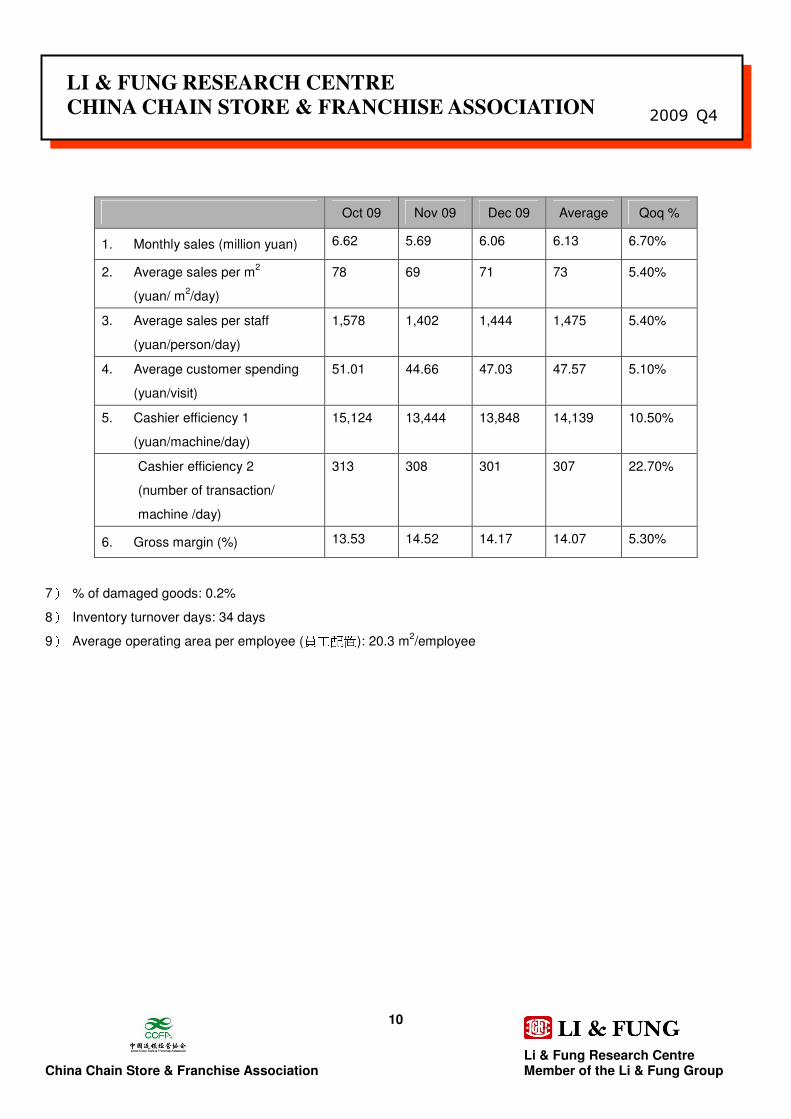

10

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 6.62 5.69 6.06 6.13 6.70%

2. Average sales per m2

(yuan/ m2/day)

78 69 71 73 5.40%

3. Average sales per staff

(yuan/person/day)

1,578 1,402 1,444 1,475 5.40%

4. Average customer spending

(yuan/visit)

51.01 44.66 47.03 47.57 5.10%

5. Cashier efficiency 1

(yuan/machine/day)

15,124 13,444 13,848 14,139 10.50%

Cashier efficiency 2

(number of transaction/

machine /day)

313 308 301 307 22.70%

6. Gross margin (%) 13.53 14.52 14.17 14.07 5.30%

7) % of damaged goods: 0.2%

8) Inventory turnover days: 34 days

9) Average operating area per employee (員工配置): 20.3 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

11

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

4. Supermarkets (4,000-5,999 m2)

Average operating area: 4,640 m2

Average number of cash registers: 23 (i.e: 1 for every 202 m2)

Monthly sales

13.04

10.33 9.98

12.6510.73

10.63

0

2

4

6

8

10

12

14

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

94

72 72

88

77

75

0

20

40

60

80

100

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

1,7931,553 1,550

1,901

1,429

1,463

0

500

1,000

1,500

2,000

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

58.44

47.11 45.96 43.9346.44

46.9

0

10

20

30

40

50

60

70

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

230240250260270280

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

0

10,000

20,000

30,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

12.96 12.95

12.69

12.15

12.37

12.41

11.6

11.8

12

12.2

12.4

12.6

12.8

13

13.2

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

12

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 10.33 9.98 12.65 10.99 -4.20%

2. Average sales per m2

(yuan/ m2/day)

72 72 88 77 -5.60%

3. Average sales per staff

(yuan/person/day)

1,553 1,550 1,901 1,668 6.80%

4. Average customer spending

(yuan/visit)

47.11 45.96 43.93 45.67 -9.70%

5. Cashier efficiency 1

(yuan/machine/day)

14,293 14,265 17,494 15,351 -10.10%

Cashier efficiency 2

(number of transaction/

machine /day)

253 257 249 253 -5.00%

6. Gross margin (%) 12.95 12.69 12.15 12.6 0.20%

7) % of damaged goods: 0.15%

8) Inventory turnover days: 30 days

9) Average operating area per employee (員工配置): 21.6 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

13

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

III. Hypermarkets (divided into 3 groups by operating areas)

1. Hypermarkets (6,000-9,999 m2)

Average operating area: 7,703 m2

Average number of cash registers: 36 (i.e. 1 for every 214 m2)

Monthly sales

9.91

13.1112.08

13.08

8.72

8.75

0

2

4

6

8

10

12

14

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

43

5552

55

38

36

0

10

20

30

40

50

60

Jul Aug Sep Oct Nov Dec

(yuan/ m

2/d

ay)

Average sales per staff

1,143

1,455 1,385 1,451

974

1,009

0

500

1,000

1,500

2,000

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

60.55

57.8956.84 57.46

52.87

54.49

48

50

52

54

56

58

60

62

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

130140150160170180

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

0

5,000

10,000

15,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

12.12

12.36

12.64

12.36

12.43

12.11

11.8

12

12.2

12.4

12.6

12.8

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

14

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 13.11 12.08 13.08 12.76 39.80%

2. Average sales per m2

(yuan/m2/day)

55 52 55 54 38.60%

3. Average sales per staff

(yuan/person/day)

1,455 1,385 1,451 1,431 37.30%

4. Average customer spending

(yuan/visit)

57.89 56.84 57.46 57.4 2.50%

5. Cashier efficiency 1

(yuan/machine/day)

11,834 11,268 11,802 11,635 28.90%

Cashier efficiency 2

(number of transaction/

machine /day)

157 146 144 149 -6.60%

6. Gross margin (%) 12.36 12.64 12.36 12.45 1.90%

7) % of damaged goods: 0.23%

8) Inventory turnover days: 23 days

9) Average operating area per employee (員工配置): 26.5 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

15

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

2. Hypermarket (10,000-14,999 m2)

Average operating area: 10,676 m2

Average number of cash registers: 30 (i.e. 1 for every 356 m2)

Monthly sales

13.2115.74

12.36 12.7612.83

11.41

0

5

10

15

20

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

4148

39 3940

34

0

10

20

30

40

50

60

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

1,4341,612

1,308 1,3061,1991,393

0

500

1,000

1,500

2,000

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

59.39

72.4

58.48

70.78

53.22

51.75

0

10

20

30

40

50

60

70

80

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

0

100

200

300

400

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

0

5,000

10,000

15,000

20,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

13.94

14.09

14.18

14.06

14.23

14.09

13.7

13.8

13.9

14

14.1

14.2

14.3

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

16

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 15.74 12.36 12.76 13.62 9.10%

2. Average sales per m2

(yuan/ m2/day)

48 39 39 42 7.70%

3. Average sales per staff

(yuan/person/day)

1,612 1,308 1,306 1,409 5.00%

4. Average customer spending

(yuan/visit)

72.4 58.48 70.78 67.22 22.70%

5. Cashier efficiency 1

(yuan/machine/day)

16,999 13,794 13,779 14,857 -2.30%

Cashier efficiency 2

(number of transaction/

machine /day)

278 242 237 252 -8.50%

6. Gross margin (%) 14.09 14.18 14.06 14.11 0.20%

7) % of damaged goods: 0.25%

8) Inventory turnover days: n.a.

9) Average operating area per employee (員工配置): 33.9 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

17

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

3. Hypermarket (over 15,000 m2)

Average operating area: 18,431 m2

Average number of cash registers: 48 (i.e. 1 for every 384 m2)

Monthly sales

23.29

23.75

21.31

23.49

22.1823.26

20

20.5

21

21.5

22

22.5

23

23.5

24

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

42 42

39

4142

39

37

38

39

40

41

42

43

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

1,528 1,528

1,417

1,511

1,408

1,526

1,300

1,350

1,400

1,450

1,500

1,550

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

82.39

80.17 80.3

82.88

76.49

78.01

72

74

76

78

80

82

84

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

180

190

200

210

220

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

13,000

14,000

15,000

16,000

17,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

10.98

11.27

11.63 11.58

10.82

10.68

10.2

10.4

10.6

10.8

11

11.2

11.4

11.6

11.8

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

18

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 23.75 21.31 23.49 22.85 -0.30%

2. Average sales per m2

(yuan/m2/day)

42 39 41 40 -1.40%

3. Average sales per staff

(yuan/person/day)

1,528 1,417 1,511 1,485 -0.10%

4. Average customer spending

(yuan/visit)

80.17 80.3 82.88 81.12 2.70%

5. Cashier efficiency 1

(yuan/machine/day)

15,869 14,714 15,693 15,425 -3.60%

Cashier efficiency 2

(number of transaction/

machine /day)

192 200 208 200 -3.40%

6. Gross margin (%) 11.27 11.63 11.58 11.49 6.20%

7) % of damaged goods: 0.23%

8) Inventory turnover days: 23 days

9) Average operating area per employee (員工配置): 36.8 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

19

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

IV. Department stores Average operating area: 30,824 m

2

Average number of cash registers: 51 (i.e. 1 for every 604 m2)

Monthly sales

90.13101.07 97.01

110.9

66.37

73.87

0

20

40

60

80

100

120

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

99106 105

120

8170

0

20

40

60

80

100

120

140

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

1,9032,097 2,080

2,377

1,3561,560

0

500

1,000

1,500

2,000

2,500

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

451.23

310.73

542.49561.14

392.78

423.33

0

100

200

300

400

500

600

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

100

110

120

130

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

0

20,000

40,000

60,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Gross margin

16.97

16.18

17.44

16.94

17.52

17.64

15

15.5

16

16.5

17

17.5

18

Jul Aug Sep Oct Nov Dec

(%)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

20

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 101.07 97.01 110.90 102.99 34.10%

2. Average sales per m2

(yuan/ m2/day)

106 105 120 110 32.30%

3. Average sales per staff

(yuan/person/day)

2,097 2,080 2,377 2,184 36.00%

4. Average customer spending

(yuan/visit)

310.73 542.49 561.14 471.45 11.60%

5. Cashier efficiency 1

(yuan/machine/day)

50,133 49,725 56,847 52,235 27.30%

Cashier efficiency 2

(number of transaction/

machine /day)

125 109 120 118 5.00%

6. Gross margin (%) 16.18 17.44 16.94 16.85 -3.00%

7) % of damaged goods: 0.13%

8) Inventory turnover days: 63 days

9) Average operating area per employee (員工配置): 19.8 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

21

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

V. Home electronics appliance chains Average operating area: 15,221 m

2

Average number of cash registers: 17 (i.e. 1 for every 895 m2)

Monthly sales

39.06

60.08

32.1

91.56

28.91

26.85

0

20

40

60

80

100

Jul Aug Sep Oct Nov Dec

(mill

ion y

uan)

Average sales per m 2

93

127

70

194

64

66

0

50

100

150

200

250

Jul Aug Sep Oct Nov Dec(y

uan/ m

2/d

ay)

Average sales per staff

4,4045,300

2,926

8,077

3,154

3,027

0

2,000

4,000

6,000

8,000

10,000

Jul Aug Sep Oct Nov Dec

(yuan/p

ers

on/d

ay)

Average customer spending

1,461

1,669

1,5531,497

1,4401,400

1,200

1,300

1,400

1,500

1,600

1,700

Jul Aug Sep Oct Nov Dec

(yuan/v

isit)

Cashier efficiency

0

50

100

150

Jul Aug Sep Oct Nov Dec

(num

ber

of

transaction/

machin

e /

day)

0

50,000

100,000

150,000

200,000

(yuan/

machin

e/d

ay)

Efficiency 2 (number of transaction/ machine /day)

Efficiency 1 (yuan/machine/day)

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

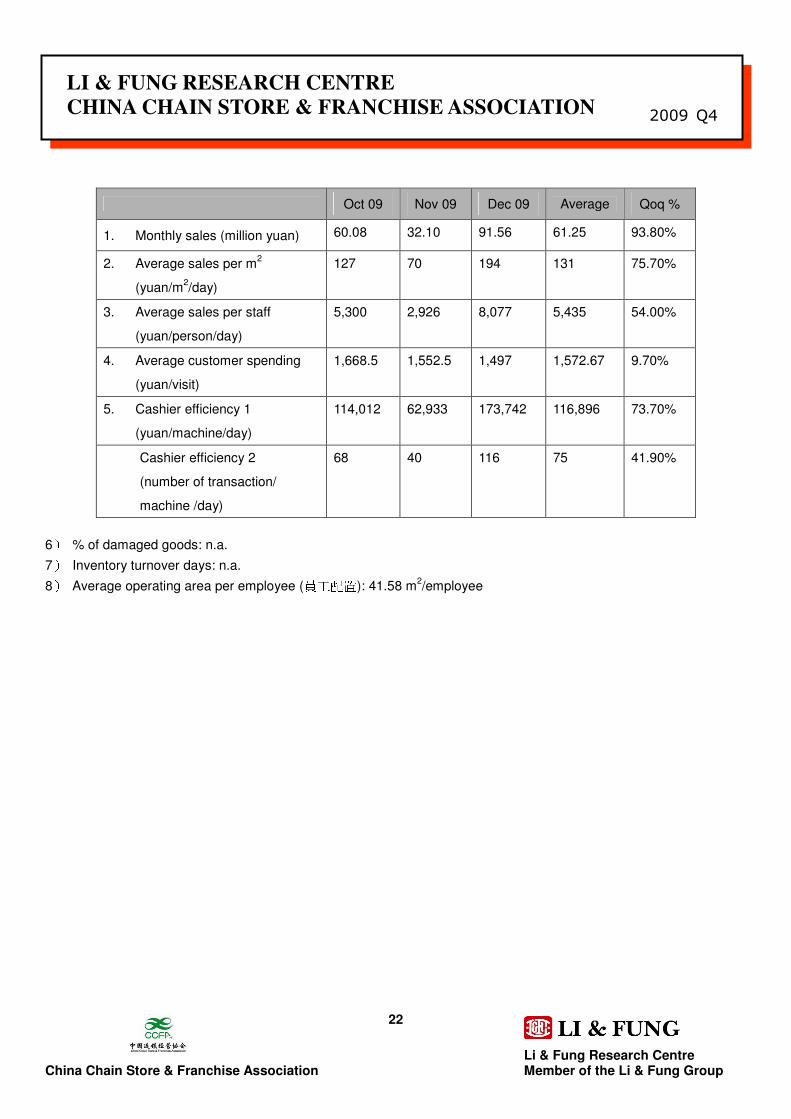

22

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Oct 09 Nov 09 Dec 09 Average Qoq %

1. Monthly sales (million yuan) 60.08 32.10 91.56 61.25 93.80%

2. Average sales per m2

(yuan/m2/day)

127 70 194 131 75.70%

3. Average sales per staff

(yuan/person/day)

5,300 2,926 8,077 5,435 54.00%

4. Average customer spending

(yuan/visit)

1,668.5 1,552.5 1,497 1,572.67 9.70%

5. Cashier efficiency 1

(yuan/machine/day)

114,012 62,933 173,742 116,896 73.70%

Cashier efficiency 2

(number of transaction/

machine /day)

68 40 116 75 41.90%

6) % of damaged goods: n.a.

7) Inventory turnover days: n.a.

8) Average operating area per employee (員工配置): 41.58 m2/employee

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

23

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

Recent highlights of the retail chain operators (Brief notes from the speech of Ms Guo Ge-ping, Chairperson of the China Chain Store & Franchise Association during

the 11th China Retail Industry Convention)

After years of rapid developments, more retailers in China now pay increasing attention to achieving sustainable growth.

Improving efficiency, instead of solely pursuing scale, is high on many players’ agenda.

1. Growing calls to change retailers’ profit structure

In recent years, the profit structure of many retailers in China has changed significantly. Many retailers no longer derive

their profits from direct merchandise sales. Instead, cumbersome charges laid on suppliers, rental income and other

investment income become predominant source of income. This profit model may help retailers reduce initial outlays

and risks; in the long run, however, it would bring about problems such as lack of differentiation, strained relationship

between retailers and suppliers, and even corruption. These undermine retailers’ capability to effectively address to

consumers’ needs and retailers have to rely on price competition to stimulate sales. More and more retailers now are

trying to change the picture. And we see major changes in sourcing models in the fresh food category. Growing number

of retailers now embark on direct-farm sourcing to improve operating performance. .

2. Improving capability in merchandise management

The current profit structure of retailers in China has weakened their capability in merchandise management. To build

demand-driven supply chains, retailers in China must improve their capability in sourcing and merchandising – retailers

now recognize that more efforts should be paid on areas such as customer research and analyses, supplier

management, inventory control, and sales and marketing. By adding new value to customers, retailers can improve their

profit margin and speed up inventory turnover.

3. Launching private labels

Private labels are relatively new in China, accounting for only 3% of the total retail sales compared with more than 20%

in developed markets such as Europe or the United States. Many Chinese consumers are unfamiliar with or do not trust

private label products. And developing successful private labels requires retailers a lot of professional knowledge in

design, product development and quality control, etc. Nonetheless, as a possible lucrative profit source and a tool to

differentiate from competitors, many retailers are keen to try launching their private labels. It can also help build

customer loyalty and save customers’ money.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

24

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

4. Managing supply chains

Many retailers have been squeezing suppliers for favorable terms; supply chain relationship is viewed as a zero-some

game. Supply chain management is gaining attention. More retailers now hope to collaborate with their supply chain

partners to lower costs and build win-win relationships with both customers and suppliers. Some ways to enhance

supply chain collaborations include improving logistics and information system, building strategic relationships with

suppliers etc.

5. Improving corporate social responsibility

In recent years, some established retailers in China have been taking key initiatives to improve corporate social

responsibility. Adopting green measures and charitable donations are some examples; and there are growing calls that

socially-responsible retailers must handle well relationships with suppliers as well. Indeed, more players now see a

socially-responsible image help them build their retailing brands and improve customer loyalty.

Li & Fung Research Centre China Chain Store & Franchise Association Member of the Li & Fung Group

25

2009 Q4

LI & FUNG RESEARCH CENTRE

CHINA CHAIN STORE & FRANCHISE ASSOCIATION

About the Organizations

The China Chain Store & Franchise Association

中國連鎖經營協會中國連鎖經營協會中國連鎖經營協會中國連鎖經營協會

Founded in 1997, the China Chain Store & Franchise Association (CCFA) is an official representative of the retailing and

franchise industry in China. Currently, there are 800 enterprise members with 160,000 outlets, including domestic &

overseas retailers, franchisers, suppliers, and relevant organizations. The total sales of China’s “Top 100 retail chain

operators”, which are part of the members of the CCFA, exceeded RMB 1.2 trillion in 2008, with more than 12,000

stores in total.

CCFA participates in policymaking and coordination, safeguards the interests of industry and members, provides a

series of professional trainings and industry information and data for its members and establishes platforms for

exchange and cooperation.

Li & Fung Group

利豐集團利豐集團利豐集團利豐集團

The Li & Fung Group is a Hong Kong-based multinational company with three distinct core businesses: export sourcing,

distribution and logistics, and retailing. Founded in Guangzhou in 1906, the Li & Fung Group achieved an annual

turnover of around US$16.7 billion in 2008. Today, the Li & Fung Group operates in some 40 countries and regions and

employs over 35,000 people worldwide. One of its core competencies is “Supply Chain Management” (SCM).

Li & Fung Research Centre

利豐研究中心利豐研究中心利豐研究中心利豐研究中心

Li & Fung Research Centre is the research institute of the Li & Fung Group. It serves as a knowledge bank on China's

economy, industries, logistics and distribution sector, with its research scope covering the whole spectrum of the entire

supply chain, from ideas, production, distribution, retailing to consumers. It also offers research analyses and consulting

services to colleagues and clients to assist them in their day-to-day decision-making.

© Copyright 2010 Li & Fung Research Centre and the China Chain Store & Franchise Association (CCFA). All rights reserved.

Though Li & Fung Research Centre and CCFA endeavor to have information presented in this document as accurate and updated as possible, it accepts no responsibility for any error, omission or misrepresentation. Li & Fung Research Centre, CCFA and/or their associates accept no responsibility for any direct, indirect or consequential loss that may arise from the use of information contained in this document. Reproduction or redistribution of this material without Li & Fung Research Centre and CCFA’s prior written consent is prohibited.

Related Documents