April 9, 2019 Shree Cement Ltd. Catalysts in place for further growth… CMP INR 18,846 Initiating Coverage – Neutral SKP Securities Ltd www.skpsecurities.com Page 1 of 33 Key Share Data Face Value (INR) 10.0 Equity Capital (INR Mn) 348.4 Market Cap (INR Mn) 656,615.5 52 Week High/Low (INR) 19260/13125 6 months Avg. Daily Volume (NSE) 24,491 BSE Code 500387 NSE Code SHREECEM Reuters Code SHCM.NS Bloomberg Code SRCM:IN Shareholding Pattern (as on Dec 2018) Source: Company 64.8% 5.8% 13.1% 16.3% Promoter MFs FIIs Puiblic & Other Particulars FY18 FY19E FY20E FY21E Net Sales 98,331.0 120,935.7 149,915.6 169,874.2 Growth (%) 14.4% 23.0% 24.0% 13.3% EBITDA 24,727.5 27,331.5 36,729.3 42,638.4 PAT 13,841.5 12,059.4 16,138.6 19,641.6 Growth (%) 3.4% -12.9% 33.8% 21.7% EPS (INR) 397.3 346.1 463.2 563.8 BVPS (INR) 2553.6 2851.7 3230.9 3674.7 Key Financials (INR Million) Particulars FY18 FY19E FY20E FY21E P/E (x) 41.9 54.4 40.7 33.4 P/BVPS (x) 6.5 6.6 5.8 5.1 Mcap/Sales (x) 5.9 5.4 4.4 3.9 EV/EBITDA (x) 23.9 24.3 17.9 15.2 ROCE (%) 12.8% 10.5% 14.4% 15.5% ROE (%) 15.6% 12.1% 14.3% 15.3% EBITDA Mar (%) 25.1% 22.6% 24.5% 25.1% PAT Mar (%) 14.1% 10.0% 10.8% 11.6% Debt - Equity (x) 0.4 0.3 0.3 0.3 Key Financials Ratios Source: Company, SKP Research 1 Yr price performance Shree; vis-à-vis BSE SENSEX -20% -10% 0% 10% 20% 2-Apr-18 23-Apr-18 14-May-18 4-Jun-18 25-Jun-18 16-Jul-18 6-Aug-18 27-Aug-18 17-Sep-18 8-Oct-18 29-Oct-18 19-Nov-18 10-Dec-18 31-Dec-18 21-Jan-19 11-Feb-19 4-Mar-19 25-Mar-19 Shree BSE SENSEX Company Background Shree Cement Ltd (Shree), promoted by Mr. H M Bangur, Managing Director, is India's fourth largest cement manufacturer, with ~8% market share, sold under “Shree Jung Rodhak, Bangur, Rockstrong and Roofon” brands. It has total cement manufacturing capacity of 41.9 mn tpa (MTPA) spread across North (~58%), East (~13%), Central (~12%) and South (~7%) India and UAE (10%) and co-generation power capacity of 639.7 MW including 126 MW from waste heat recovery system (WHRS). Shree is the largest cement producer in North India, with a capacity of 24.3 MTPA, enjoying ~24% market share. The Company also started commercial sale of power in FY09, contributing ~5% to sales in FY18. Investment Rationale New capacities and geographies to aid above-industry volume growth Shree demonstrated a differentiated expansion strategy, with regular capacity additions at higher frequency but of smaller magnitude. This enabled it to (1) expand systematically as per market demand, (2) achieve faster project turnaround and quick stabilization, and (3) drive growth with minimum pressure on balance sheet. Over the last few years, Shree has strengthened its market presence by entering into eastern and southern markets, thus, diversifying away from vagaries of regional demands. Recently, the Company has commissioned 3 MTPA cement grinding unit in Karnataka (south) and has planned to add 5.5 MTPA in east by H1FY20, which will reduce its capacity concentration in the north to less than 50%. The eastern and southern region is expected to witness sustained demand recovery driven by rejuvenated housing and infrastructure development, thereby, resulting in better volumes and realization. Consequently, Shree is expected to grow volumes at ~1.4-1.5x industry growth. Supply concerns receding; increasing entry barriers limit fragmentation and consolidation of capacities to support prices In zeal to gain market share, aggressive manufacturers added robust capacity, leading to overcapacity, and utilisations collapsing to 65% in 2018 from peak of 83% in 2008. Off-late, country’s cement sector is passing through a phase of aggressive consolidation, resulting in top 5 groups controlling ~52% of the industry capacity, aiding reduced competition and better pricing power. Also, indirect entry barriers like land acquisition, high capital cost, securing raw materials like lime stones and increasing gestation period due to regulatory clearances may slow the pace of fresh capacity additions. This will result into better utilisation and improved realization. The growth in cement demand has always had a positive correlation to the GDP growth with long‐term average correlation of 0.9-1.2x of GDP. Shree has substantial limestone reserve which is critical to address the Company’s expansion plan, particularly under the dynamic regulatory environment. Cost leadership to provide competitive advantage Shree is among lowest cost, cement producer, and enjoys superior profitability due to (a) best energy efficiency on account of early adoption of pet coke, WHRS, alternate fuel & raw material (AFR’s) and a 100% captive power plant, (b) economies of scale due to large scale operations and single location largest kiln in the north, and (c) pioneer status in split grinding strategy, thereby, saving logistics cost. The operating efficiency gives the Company a significant cost advantage vs. peers in the environment of subdued demand, lower utilisations and rising costs. Therefore, Shree’s strong focus on operating efficiencies has led to production cost which are almost at ~15-20% discount to tier-I players. Balance sheet strength and positive cash flow to fund future capex Due to smaller periodic expansions, Shree’s balance sheet strength was not diluted in the past. We believe this will continue going forward too. Capex cost for Shree continues to be ~20% lower than the industry average given (a) the Company’s organic model of growth without additional debt, (b) scope for higher brownfield expansions, (c) ability to garner critical resources (land, limestone) by overcoming regulatory hurdles (d) securing equipment at competitive rates with quick utilization ramp-up, and (e) replicating capacity designs by in-house team. Thus, Shree’s cost competence and balance sheet strength make it favorably placed for growth, going forward. Shree is expected to generate cash flow from operations of ~88 bn over FY19E-21E vs. its capex need of only ~Rs 30 bn, thereby, driving growth without impacting balance sheet strength. It is expected to maintain its debt/equity low at ~0.3x, going forward. Valuation With Government’s thrust on infrastructure development, leadership in North with hi gh entry barriers, strong brand pull coupled with robust distribution network, retail-centric business model, raw material security with cost leadership, diversifying growth in eastern and southern market and enhancing return ratios, augurs well for Shree. Therefore, we believe, its premium multiple is expected to sustain, which can be supported by thin liquidity and meagre non-institutional holdings. We have valued the stock on the basis of 15x of FY21E EBITDA (equivalent to replacement cost of ~USD 180/tn). Currently at Rs 18,846, we feel that the stock is adequately priced, based on current fundamentals. Pending triggers for a fresh re-rating or a stronger conviction, we are Neutral on the stock. Analysts: Anik Das Tel No: +91-33-40077020 E-mail: [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

April 9, 2019

Shree Cement Ltd.

Catalysts in place for further growth…

CMP INR 18,846 Initiating Coverage – Neutral

SKP Securities Ltd www.skpsecurities.com Page 1 of 33

Key Share Data

Face Value (INR) 10.0

Equity Capital (INR Mn) 348.4

Market Cap (INR Mn) 656,615.5

52 Week High/Low (INR) 19260/13125

6 months Avg. Daily Volume (NSE) 24,491

BSE Code 500387

NSE Code SHREECEM

Reuters Code SHCM.NS

Bloomberg Code SRCM:IN Shareholding Pattern (as on Dec 2018)

Source: Company

64.8%

5.8%

13.1%

16.3%Promoter

MFs

FIIs

Puiblic & Other

Particulars FY18 FY19E FY20E FY21E

Net Sales 98,331.0 120,935.7 149,915.6 169,874.2

Growth (%) 14.4% 23.0% 24.0% 13.3%

EBITDA 24,727.5 27,331.5 36,729.3 42,638.4

PAT 13,841.5 12,059.4 16,138.6 19,641.6

Growth (%) 3.4% -12.9% 33.8% 21.7%

EPS (INR) 397.3 346.1 463.2 563.8

BVPS (INR) 2553.6 2851.7 3230.9 3674.7

Key Financials (INR Million)

Particulars FY18 FY19E FY20E FY21E

P/E (x) 41.9 54.4 40.7 33.4

P/BVPS (x) 6.5 6.6 5.8 5.1

Mcap/Sales (x) 5.9 5.4 4.4 3.9

EV/EBITDA (x) 23.9 24.3 17.9 15.2

ROCE (%) 12.8% 10.5% 14.4% 15.5%

ROE (%) 15.6% 12.1% 14.3% 15.3%

EBITDA Mar (%) 25.1% 22.6% 24.5% 25.1%

PAT Mar (%) 14.1% 10.0% 10.8% 11.6%

Debt - Equity (x) 0.4 0.3 0.3 0.3

Key Financials Ratios

Source: Company, SKP Research

1 Yr price performance Shree; vis-à-vis BSE SENSEX

-20%

-10%

0%

10%

20%

2-A

pr-

18

23-A

pr-

18

14-M

ay-1

8

4-J

un

-18

25-J

un-1

8

16-J

ul-1

8

6-A

ug-1

8

27-A

ug

-18

17-S

ep

-18

8-O

ct-

18

29-O

ct-

18

19-N

ov-1

8

10-D

ec-1

8

31-D

ec-1

8

21-J

an-1

9

11-F

eb-1

9

4-M

ar-

19

25-M

ar-

19

Shree BSE SENSEX

Company Background

Shree Cement Ltd (Shree), promoted by Mr. H M Bangur, Managing Director, is India's fourth largest cement manufacturer, with ~8% market share, sold under “Shree Jung Rodhak, Bangur, Rockstrong and Roofon” brands. It has total cement manufacturing capacity of 41.9 mn tpa (MTPA) spread across North (~58%), East (~13%), Central (~12%) and South (~7%) India and UAE (10%) and co-generation power capacity of 639.7 MW including 126 MW from waste heat recovery system (WHRS). Shree is the largest cement producer in North India, with a capacity of 24.3 MTPA, enjoying ~24% market share. The Company also started commercial sale of power in FY09, contributing ~5% to sales in FY18.

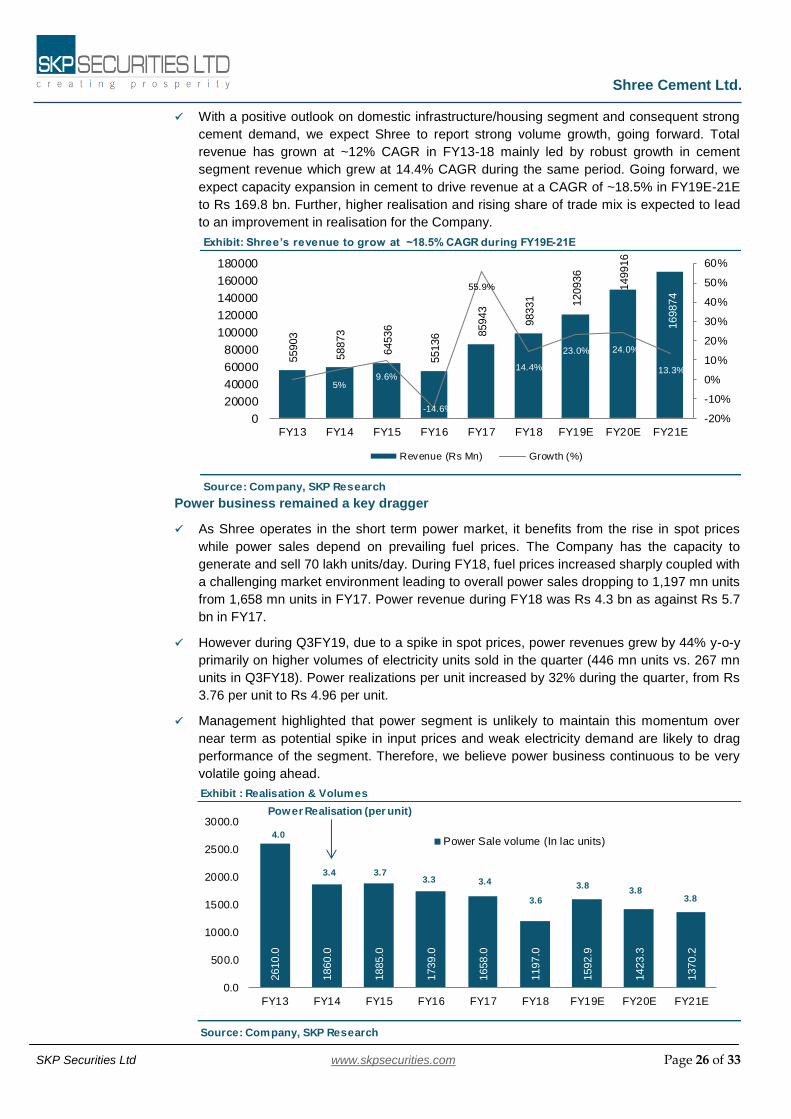

Investment Rationale New capacities and geographies to aid above-industry volume growth

Shree demonstrated a differentiated expansion strategy, with regular capacity additions at higher frequency but of smaller magnitude. This enabled it to (1) expand systematically as per market demand, (2) achieve faster project turnaround and quick stabilization, and (3) drive growth with minimum pressure on balance sheet.

Over the last few years, Shree has strengthened its market presence by entering into eastern and southern markets, thus, diversifying away from vagaries of regional demands. Recently, the Company has commissioned 3 MTPA cement grinding unit in Karnataka (south) and has planned to add 5.5 MTPA in east by H1FY20, which will reduce its capacity concentration in the north to less than 50%. The eastern and southern region is expected to witness sustained demand recovery driven by rejuvenated housing and infrastructure development, thereby, resulting in better volumes and realization. Consequently, Shree is expected to grow volumes at ~1.4-1.5x industry growth.

Supply concerns receding; increasing entry barriers limit fragmentation and consolidation of capacities to support prices

In zeal to gain market share, aggressive manufacturers added robust capacity, leading to overcapacity, and utilisations collapsing to 65% in 2018 from peak of 83% in 2008. Off-late, country’s cement sector is passing through a phase of aggressive consolidation, resulting in top 5 groups controlling ~52% of the industry capacity, aiding reduced competition and better pricing power. Also, indirect entry barriers like land acquisition, high capital cost, securing raw materials like lime stones and increasing gestation period due to regulatory clearances may slow the pace of fresh capacity additions. This will result into better utilisation and improved realization.

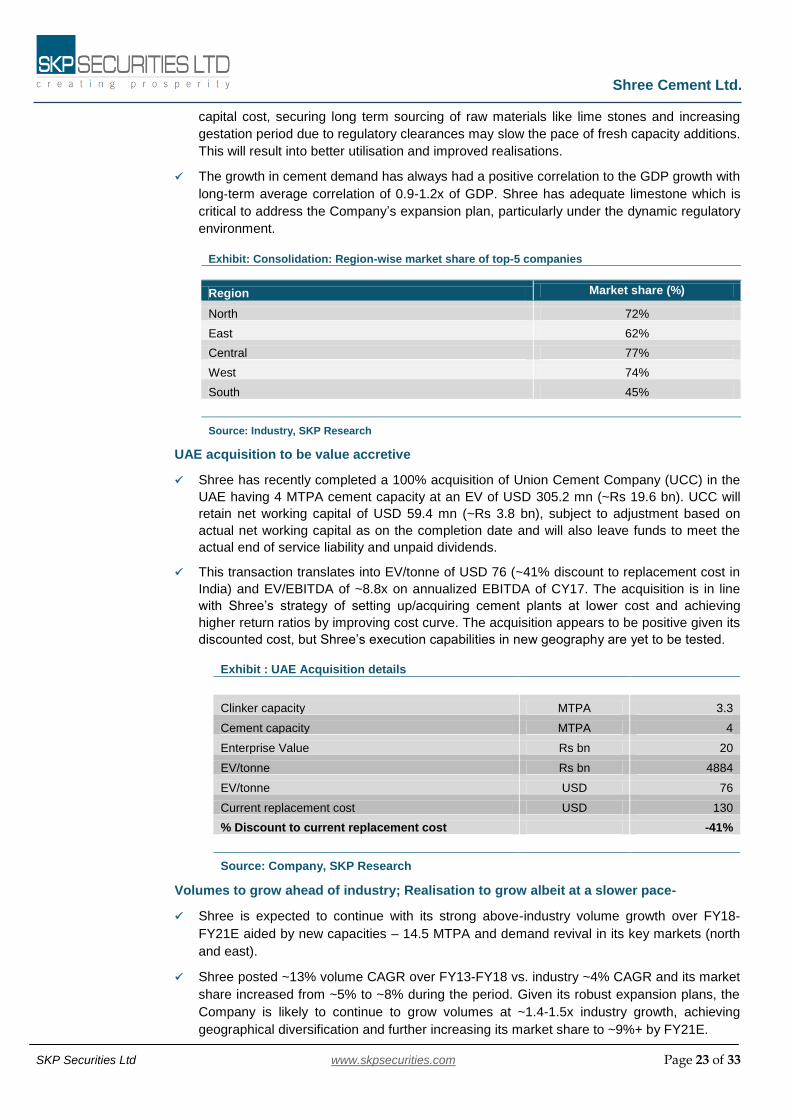

The growth in cement demand has always had a positive correlation to the GDP growth with long‐term average correlation of 0.9-1.2x of GDP. Shree has substantial limestone reserve which is critical to address the Company’s expansion plan, particularly under the dynamic regulatory environment.

Cost leadership to provide competitive advantage

Shree is among lowest cost, cement producer, and enjoys superior profitability due to (a) best energy efficiency on account of early adoption of pet coke, WHRS, alternate fuel & raw material (AFR’s) and a 100% captive power plant, (b) economies of scale due to large scale operations and single location largest kiln in the north, and (c) pioneer status in split grinding strategy, thereby, saving logistics cost. The operating efficiency gives the Company a significant cost advantage vs. peers in the environment of subdued demand, lower utilisations and rising costs. Therefore, Shree’s strong focus on operating efficiencies has led to production cost which are almost at ~15-20% discount to tier-I players.

Balance sheet strength and positive cash flow to fund future capex

Due to smaller periodic expansions, Shree’s balance sheet strength was not diluted in the past. We believe this will continue going forward too. Capex cost for Shree continues to be ~20% lower than the industry average given (a) the Company’s organic model of growth without additional debt, (b) scope for higher brownfield expansions, (c) ability to garner critical resources (land, limestone) by overcoming regulatory hurdles (d) securing equipment at competitive rates with quick utilization ramp-up, and (e) replicating capacity designs by in-house team. Thus, Shree’s cost competence and balance sheet strength make it favorably placed for growth, going forward.

Shree is expected to generate cash flow from operations of ~88 bn over FY19E-21E vs. its capex need of only ~Rs 30 bn, thereby, driving growth without impacting balance sheet

strength. It is expected to maintain its debt/equity low at ~0.3x, going forward. Valuation

With Government’s thrust on infrastructure development, leadership in North with high entry barriers, strong brand pull coupled with robust distribution network, retail-centric business model, raw material security with cost leadership, diversifying growth in eastern and southern market and enhancing return ratios, augurs well for Shree. Therefore, we believe, its premium multiple is expected to sustain, which can be supported by thin liquidity and meagre non-institutional holdings.

We have valued the stock on the basis of 15x of FY21E EBITDA (equivalent to replacement cost of ~USD 180/tn). Currently at Rs 18,846, we feel that the stock is adequately priced, based on current fundamentals. Pending triggers for a fresh re-rating or a stronger conviction, we are Neutral on the stock.

Analysts: Anik Das

Tel No: +91-33-40077020

E-mail: [email protected]

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 2 of 33

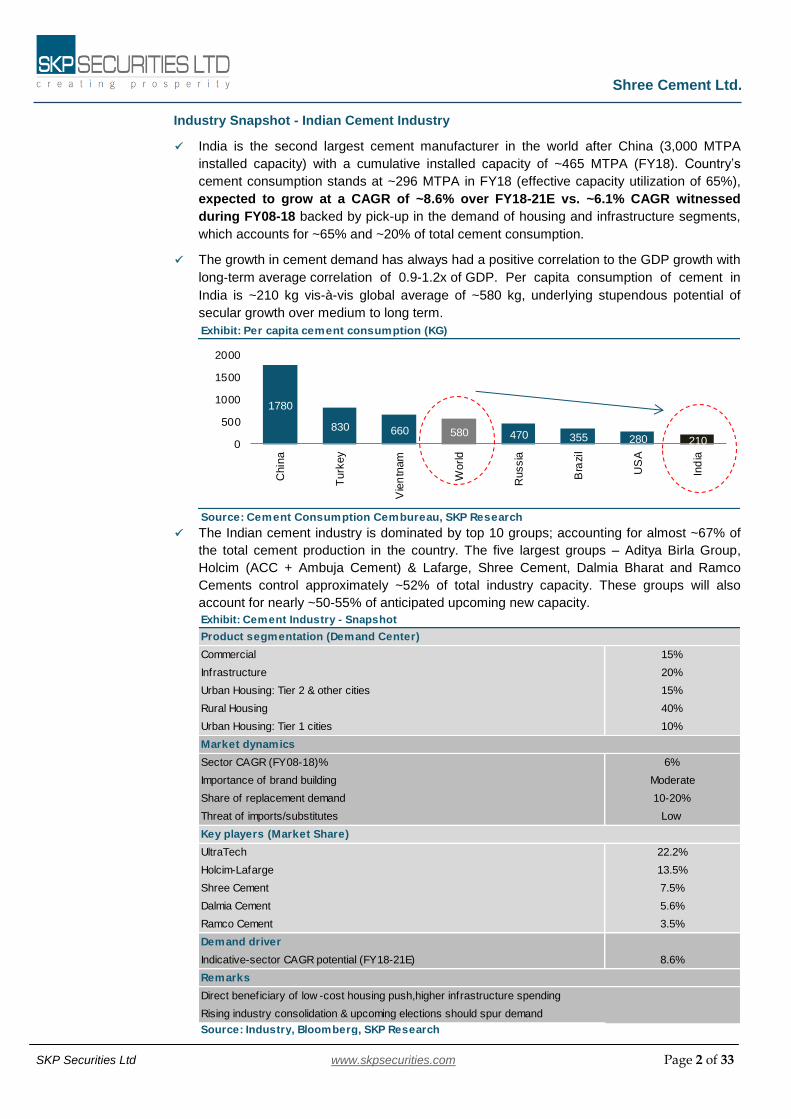

Exhibit: Per capita cement consumption (KG)

Source: Cement Consumption Cembureau, SKP Research

1780

830 660 580 470 355 280 2100

500

1000

1500

2000

Chin

a

Turk

ey

Vie

ntn

am

World

Russia

Bra

zil

US

A

Ind

ia

Exhibit: Cement Industry - Snapshot

Commercial 15%

Infrastructure 20%

Urban Housing: Tier 2 & other cities 15%

Rural Housing 40%

Urban Housing: Tier 1 cities 10%

Sector CAGR (FY08-18)% 6%

Importance of brand building Moderate

Share of replacement demand 10-20%

Threat of imports/substitutes Low

UltraTech 22.2%

Holcim-Lafarge 13.5%

Shree Cement 7.5%

Dalmia Cement 5.6%

Ramco Cement 3.5%

Demand driver

Indicative-sector CAGR potential (FY18-21E) 8.6%

Source: Industry, Bloomberg, SKP Research

Product segmentation (Demand Center)

Direct beneficiary of low -cost housing push,higher infrastructure spending

Rising industry consolidation & upcoming elections should spur demand

Market dynamics

Key players (Market Share)

Remarks

Industry Snapshot - Indian Cement Industry

India is the second largest cement manufacturer in the world after China (3,000 MTPA

installed capacity) with a cumulative installed capacity of ~465 MTPA (FY18). Country’s

cement consumption stands at ~296 MTPA in FY18 (effective capacity utilization of 65%),

expected to grow at a CAGR of ~8.6% over FY18-21E vs. ~6.1% CAGR witnessed

during FY08-18 backed by pick-up in the demand of housing and infrastructure segments,

which accounts for ~65% and ~20% of total cement consumption.

The growth in cement demand has always had a positive correlation to the GDP growth with

long‐term average correlation of 0.9-1.2x of GDP. Per capita consumption of cement in

India is ~210 kg vis-à-vis global average of ~580 kg, underlying stupendous potential of

secular growth over medium to long term.

The Indian cement industry is dominated by top 10 groups; accounting for almost ~67% of

the total cement production in the country. The five largest groups – Aditya Birla Group,

Holcim (ACC + Ambuja Cement) & Lafarge, Shree Cement, Dalmia Bharat and Ramco

Cements control approximately ~52% of total industry capacity. These groups will also

account for nearly ~50-55% of anticipated upcoming new capacity.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 3 of 33

(MTPA) FY18 FY19E FY20E FY21E Company FY18 FY19E FY20E FY21E

Installed capacity 102 102 104 108 Asian Cement 1.5

Effective capacity 101 101 103 106 JK Cement 2.0

y-o-y (%) 6 0 2 3 JK Lakshmi

Volumes 72 75 79 80 Shree Cement

Utilisation (%) 71 74 77 75 Shree Cement 3.6

y-o-y change (%) -6 4 3 -2 Ultratech Cement 3.5

Total 5.1 2.0 3.5

Source: Industry,SKP Research Source: Industry,SKP Research

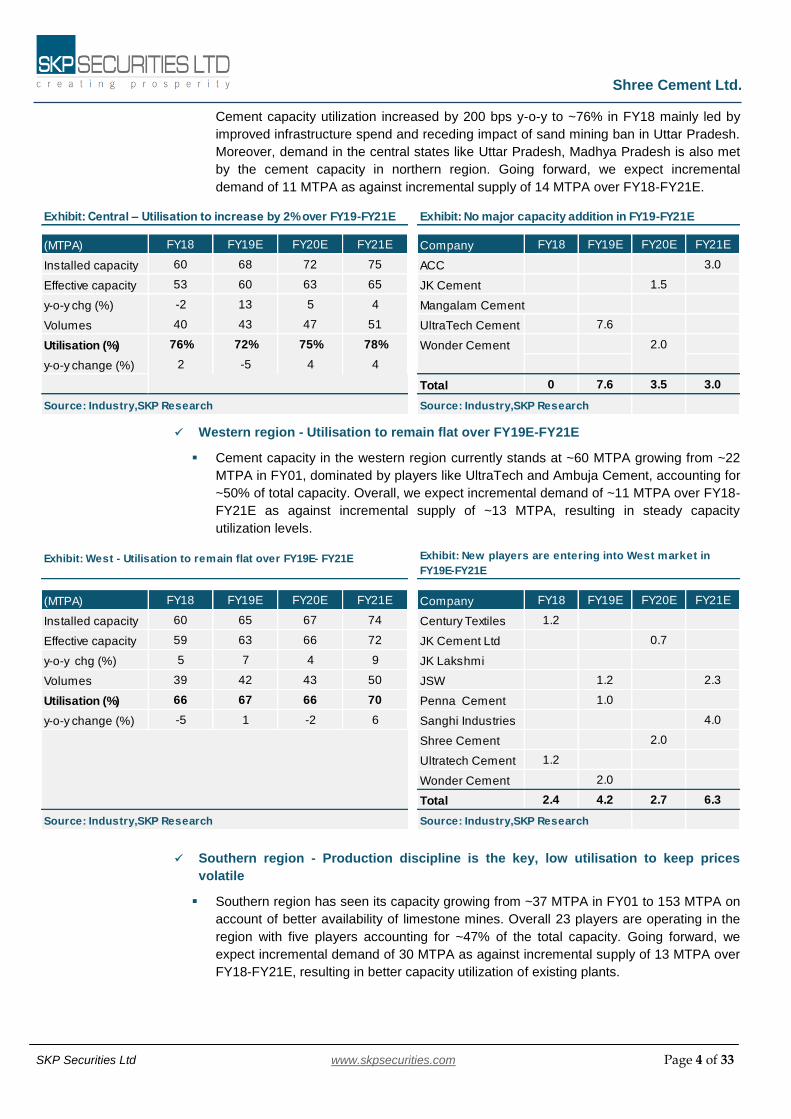

Exhibit: North – Cement utilisation to rise to 75% by FY21E Exhibit: No major capacity addition in FY19-FY21E

Exhibit: Geographical distribution of cement manufacturers

Source: Industry, UltraTech investor presentation, SKP Research,*Based on capacity

Cem

ent

Industr

y

SOUTH 153 MTPATamil Nadu, Andhra Pradesh & Karnataka

33%

NORTH 102 MTPARajasthan, Punjab, Haryana & the NCR 22%

EAST & North East 88 MTPAWest Bengal,

Chhattisgarh, Orissa & Jharkhand

19%

WEST 60 MTPA Maharashtra, Gujarat 13%

CENTRAL 60 MTPAUttar Pradesh, Madhya

Pradesh 13%

Installed Capacity Key Markets *Market Composition

Cement Industry - Geographical distribution

Considering the bulky nature of cement, the industry is influenced by regional rather than

national demand-supply dynamics. Due to varying levels of infrastructure/real

estate/industrial development in different regions, companies operating in developing

states/regions are better placed. To some extent, there is also inter-regional movement of

cement. Andhra Pradesh is the leading state with 40 large cement plants, followed by Tamil

Nadu and Rajasthan having 21 and 20 plants, respectively.

Northern region - Cement capacity utilisation to improve by 400 bps over FY18-21E

Cement capacity in North region stands at ~102 MTPA in FY18 from ~22 MTPA in FY01

with Rajasthan alone accounting for ~65-70% of total capacity due to better availability of

limestone mines (Rajasthan accounts for ~12% of the country’s limestone reserves). The

market is currently dominated by Shree Cement and UltraTech, both collectively

accounting for ~48% of the total capacity. Going forward, we estimate incremental

demand of 8 MTPA as against incremental supply of 5.5 MTPA over FY18-FY21E.

Central region - utilisation to increase over FY18-FY21E

Cement capacity in central region has increased from ~19 MTPA in FY01 to ~60 MTPA

in FY18. Overall 10 players are operating in the region with five players accounting for

~81% of the total capacity. Post expansion of UltraTech’s capacity in the central region,

the Company will have a mammoth share of ~36.7% by FY21E from ~29% in FY18.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 4 of 33

(MTPA) FY18 FY19E FY20E FY21E Company FY18 FY19E FY20E FY21E

Installed capacity 60 68 72 75 ACC 3.0

Effective capacity 53 60 63 65 JK Cement 1.5

y-o-y chg (%) -2 13 5 4 Mangalam Cement

Volumes 40 43 47 51 UltraTech Cement 7.6

Utilisation (%) 76% 72% 75% 78% Wonder Cement 2.0

y-o-y change (%) 2 -5 4 4

Total 0 7.6 3.5 3.0

Source: Industry,SKP Research Source: Industry,SKP Research

Exhibit: Central – Utilisation to increase by 2% over FY19-FY21E Exhibit: No major capacity addition in FY19-FY21E

(MTPA) FY18 FY19E FY20E FY21E Company FY18 FY19E FY20E FY21E

Installed capacity 60 65 67 74 Century Textiles 1.2

Effective capacity 59 63 66 72 JK Cement Ltd 0.7

y-o-y chg (%) 5 7 4 9 JK Lakshmi

Volumes 39 42 43 50 JSW 1.2 2.3

Utilisation (%) 66 67 66 70 Penna Cement 1.0

y-o-y change (%) -5 1 -2 6 Sanghi Industries 4.0

Shree Cement 2.0

Ultratech Cement 1.2

Wonder Cement 2.0

Total 2.4 4.2 2.7 6.3

Source: Industry,SKP Research Source: Industry,SKP Research

Exhibit: New players are entering into West market in

FY19E-FY21E Exhibit: West - Utilisation to remain flat over FY19E- FY21E

Cement capacity utilization increased by 200 bps y-o-y to ~76% in FY18 mainly led by

improved infrastructure spend and receding impact of sand mining ban in Uttar Pradesh.

Moreover, demand in the central states like Uttar Pradesh, Madhya Pradesh is also met

by the cement capacity in northern region. Going forward, we expect incremental

demand of 11 MTPA as against incremental supply of 14 MTPA over FY18-FY21E.

Western region - Utilisation to remain flat over FY19E-FY21E

Cement capacity in the western region currently stands at ~60 MTPA growing from ~22

MTPA in FY01, dominated by players like UltraTech and Ambuja Cement, accounting for

~50% of total capacity. Overall, we expect incremental demand of ~11 MTPA over FY18-

FY21E as against incremental supply of ~13 MTPA, resulting in steady capacity

utilization levels.

Southern region - Production discipline is the key, low utilisation to keep prices

volatile

Southern region has seen its capacity growing from ~37 MTPA in FY01 to 153 MTPA on

account of better availability of limestone mines. Overall 23 players are operating in the

region with five players accounting for ~47% of the total capacity. Going forward, we

expect incremental demand of 30 MTPA as against incremental supply of 13 MTPA over

FY18-FY21E, resulting in better capacity utilization of existing plants.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 5 of 33

(MTPA) FY18 FY19E FY20E FY21E Company FY18 FY19E FY20E FY21E

Installed capacity 153 162 166 166 Chettinad 2.5

Effective capacity 150 159 163 163 JSW 3.0

YoY chg (%) -4 6 3 0 KCP 1.5

Volumes 88 103 112 118 My Home

Utilisation (%) 59% 65% 69% 73% Nagarjuna Cement 0.8

y-o-y change (%) 7 11 6 5 Penna Cement 2

Ramco Cements 0.2 1.1

SGC 1.3 0.5

Shree Cement 3.0

Tamilnadu Cements 1.0

Total 4.0 8.8 4.1

Source: Industry,SKP Research Source: Industry,SKP Research

Exhibit: South – Utilisation to see uptick Exhibit: Few capacity additions expected over FY19E-FY21E

(MTPA) FY18 FY19E FY20E FY21E Company FY18 FY19E FY20E FY21E

Installed capacity 88 93 99 106 ACC 0 0 0 0

Effective capacity 83 88 93 100 Dalmia Bharat 0 0 0 2.6

y-o-y chg (%) 14 5 6 7 EMAMI Cement 0 3.8 0 0

Volumes 57 62 70 80 Shree Cement 2 0.9 2 2

Utilisation (%) 68 71 75 80 JK Lakshmi Cement 1 0 0.8 0

y-o-y change (%) -6 3 6 7 JSW 2.4 0 1.2 1.2

STAR 0 0 0 1

Ramco Cement 0 0 2 0

Ultratech Cement 0.3 0 0 0

Total 5.7 4.7 6.0 6.8

Source: Industry,SKP Research Source: Industry,SKP Research

Exhibit: East & North East - Utilisation to increase over FY19-

FY21E

Exhibit: More grinding unit additions expected in FY19E-

FY21E

Eastern & North Eastern region – Higher capacity utilization to improve prices

Over the next two years the region is expected to witness capacity addition of ~18 MTPA

from ~88 MTPA to ~106 MTPA. UltraTech, Dalmia Bharat, ACC, Nirma Cement and

Shree accounts for ~70% of the market. Post expansion of Dalmia Bharat in the East, the

Company will become the market leader with ~21% capacity share by FY21E. Despite

huge capacity expansion in pipeline, utilization levels in East is bound to remain on a

higher side due to better housing demand, higher infrastructure spends and receding

impact of sand mining issues in Bihar. Going forward, we expect incremental demand of

23 MTPA as against incremental supply of ~18 MTPA over FY18-FY21E.

Industry - Cost drivers

The cost structure for cement sector is skewed towards variable cost with only 20%

being fixed. Of the variable cost, raw material (limestone, gypsum and fly ash) cost

accounts for just ~15-18% while, power and fuel along with freight cost comprises ~50%-

55%. Hence, efficiencies in terms of energy consumption and freight optimization are

very important to maintain costs.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 6 of 33

Source: The Indian Bureau of Mines,SKP Research Source: The Indian Bureau of Mines,SKP Research

Exhibit: Limestone resource positioning Exhibit: Production of Limestone (By Region)

25%

36%

14%12% 12%

0%

5%

10%

15%

20%

25%

30%

35%

40%

North South East andNorth East

West Central

Exhibit: Output of different raw material to cement

Items OPC PPC PSC

Clinker 95% 65% 45%

Gypsum 5% 5% 5%

Flyash - 30% -

Slag - - 50%

Margin for Manufacturer Lowest Higher Highest

Source: Industry, SKP Research

Limestone availability remains a key

Limestone is the primary raw material in cement manufacturing. Other raw material includes flyash, gypsum and slag. Raw material costs could vary by the mix of cement sold. Shree and Ambuja stand out on raw material costs owing to adequate access to limestone and fly ash.

India has limestone reserves of ~203 bn tonnes which is expected to last for 35-40 years.

Within the Country, reserves are concentrated in seven major clusters – Satna (M.P.),

Chanderria (Rajasthan), Nalagonda (Telangana), Gulbarga (Karnataka), Yerraguntla

(Andhra Pradesh), Chandrapur (Maharashtra), and Bilaspur (Chhattisgarh) and the top 5

states contribute to ~64% of limestone production. While there are concerns about the

limited availability of limestone, some large and mid-tier Companies have acquired

additional limestone reserves to aid their cement capacity additions in future. Shree has

substantial limestone reserves which is critical to address the Company’s

expansion plan, particularly under the dynamic regulatory environment.

However, limestone can be substituted with other materials namely Flyash or Slag, which

will still provide the strength but to a lesser extent. The threshold limit of mixing Flyash is

maximum 35%.

Fly ash/slag is sourced from steel or power companies at relatively low price, hence cost

mainly includes transport cost which in turn depends on the lead distance to the plant. To

maintain sufficient and timely supply of fly ash/slag, cement companies are looking at

JVs with power/steel companies.

There are various varieties of Cement depending on the composition of materials,

namely OPC (ordinary portland cement), PPC (portland pozzolana cement) and PSC

(portland slag cement). At this juncture, PPC comprises 56% while OPC comprises 34%

and PSC adds up the residual.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 7 of 33

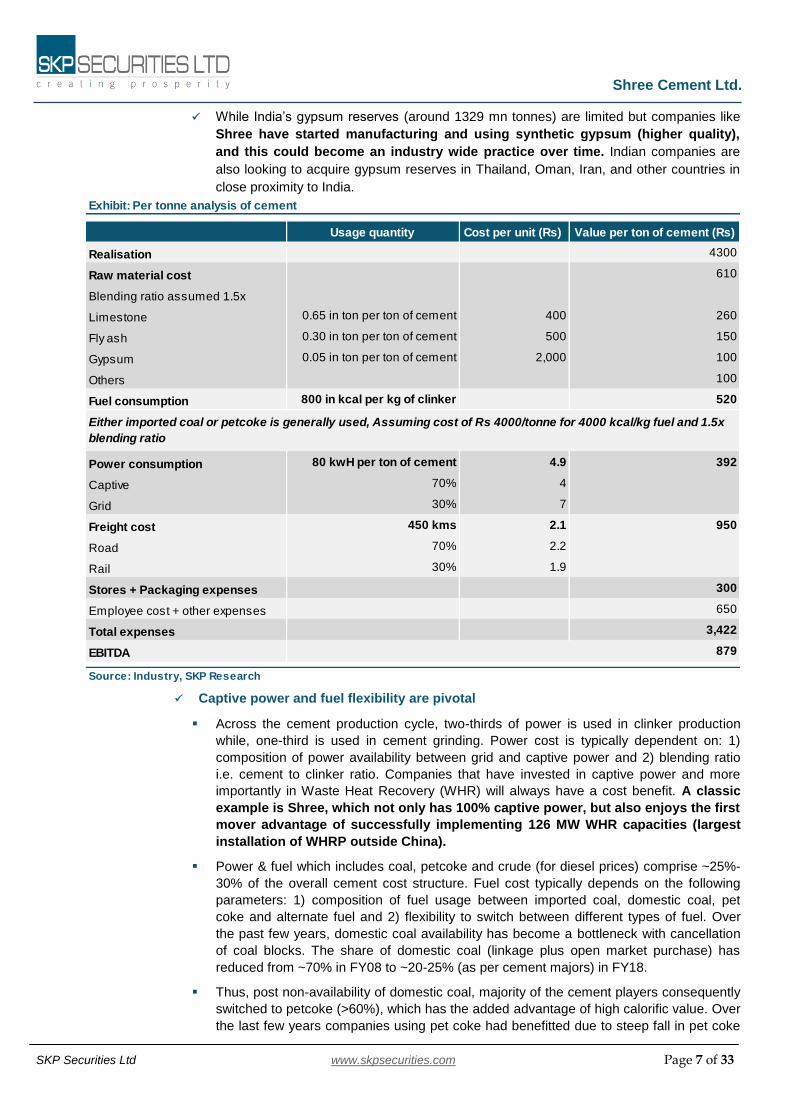

Exhibit: Per tonne analysis of cement

Usage quantity Cost per unit (Rs) Value per ton of cement (Rs)

Realisation 4300

Raw material cost 610

Blending ratio assumed 1.5x

Limestone 0.65 in ton per ton of cement 400 260

Fly ash 0.30 in ton per ton of cement 500 150

Gypsum 0.05 in ton per ton of cement 2,000 100

Others 100

Fuel consumption 800 in kcal per kg of clinker 520

Power consumption 80 kwH per ton of cement 4.9 392

Captive 70% 4

Grid 30% 7

Freight cost 450 kms 2.1 950

Road 70% 2.2

Rail 30% 1.9

Stores + Packaging expenses 300

Employee cost + other expenses 650

Total expenses 3,422

EBITDA 879

Source: Industry, SKP Research

Either imported coal or petcoke is generally used, Assuming cost of Rs 4000/tonne for 4000 kcal/kg fuel and 1.5x

blending ratio

While India’s gypsum reserves (around 1329 mn tonnes) are limited but companies like

Shree have started manufacturing and using synthetic gypsum (higher quality),

and this could become an industry wide practice over time. Indian companies are

also looking to acquire gypsum reserves in Thailand, Oman, Iran, and other countries in

close proximity to India.

Captive power and fuel flexibility are pivotal

Across the cement production cycle, two-thirds of power is used in clinker production

while, one-third is used in cement grinding. Power cost is typically dependent on: 1)

composition of power availability between grid and captive power and 2) blending ratio

i.e. cement to clinker ratio. Companies that have invested in captive power and more

importantly in Waste Heat Recovery (WHR) will always have a cost benefit. A classic

example is Shree, which not only has 100% captive power, but also enjoys the first

mover advantage of successfully implementing 126 MW WHR capacities (largest

installation of WHRP outside China).

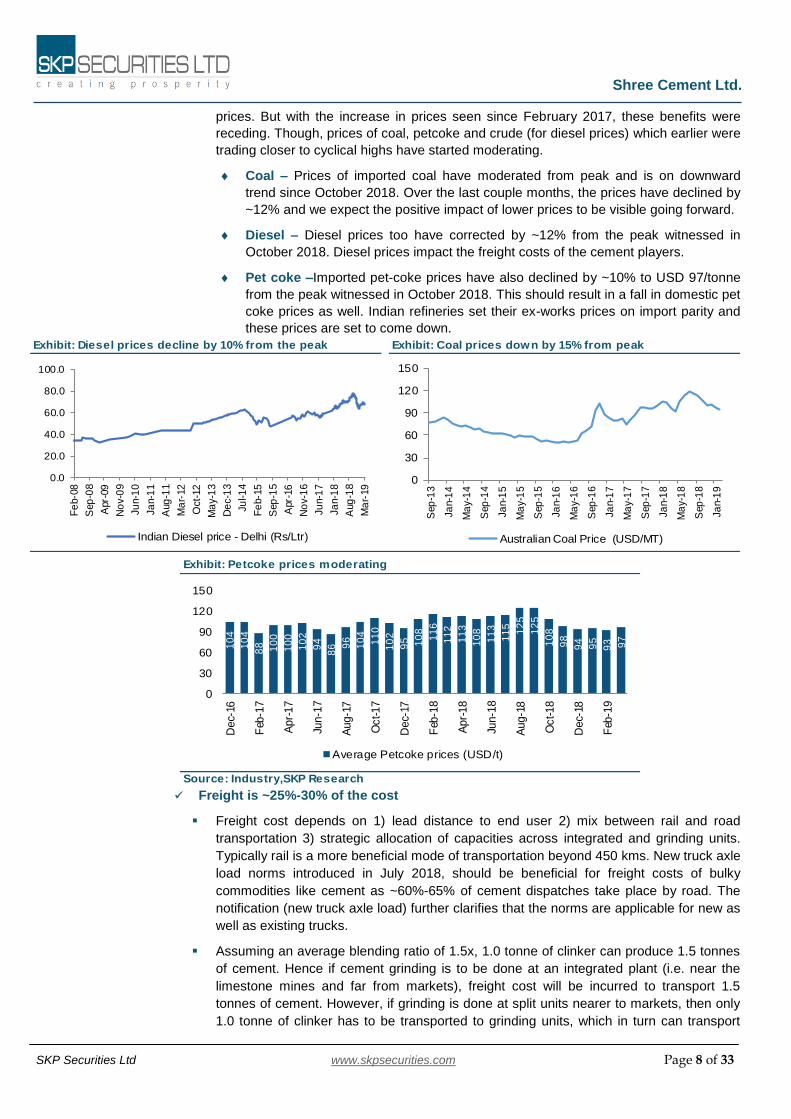

Power & fuel which includes coal, petcoke and crude (for diesel prices) comprise ~25%-

30% of the overall cement cost structure. Fuel cost typically depends on the following

parameters: 1) composition of fuel usage between imported coal, domestic coal, pet

coke and alternate fuel and 2) flexibility to switch between different types of fuel. Over

the past few years, domestic coal availability has become a bottleneck with cancellation

of coal blocks. The share of domestic coal (linkage plus open market purchase) has

reduced from ~70% in FY08 to ~20-25% (as per cement majors) in FY18.

Thus, post non-availability of domestic coal, majority of the cement players consequently

switched to petcoke (>60%), which has the added advantage of high calorific value. Over

the last few years companies using pet coke had benefitted due to steep fall in pet coke

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 8 of 33

Exhibit: Diesel prices decline by 10% from the peak Exhibit: Coal prices down by 15% from peak

Exhibit: Petcoke prices moderating

Source: Industry,SKP Research

0

30

60

90

120

150

Sep

-13

Ja

n-1

4

Ma

y-1

4

Sep

-14

Ja

n-1

5

Ma

y-1

5

Sep

-15

Ja

n-1

6

Ma

y-1

6

Sep

-16

Ja

n-1

7

Ma

y-1

7

Sep

-17

Ja

n-1

8

Ma

y-1

8

Sep

-18

Ja

n-1

9

Australian Coal Price (USD/MT)

10

4

10

4

88 10

0

10

0

10

2

94

86 9

6

10

4

11

0

10

2

95 10

8

11

6

11

2

11

3

10

8

11

3

11

5

12

5

12

5

10

8

98

94

95

93 97

0

30

60

90

120

150

Dec-

16

Feb

-17

Apr-

17

Jun-1

7

Aug-1

7

Oct-17

Dec-

17

Feb

-18

Apr-

18

Jun-1

8

Aug-1

8

Oct-18

Dec-

18

Feb

-19

Average Petcoke prices (USD/t)

0.0

20.0

40.0

60.0

80.0

100.0

Fe

b-0

8

Sep

-08

Apr-

09

No

v-0

9

Ju

n-1

0

Ja

n-1

1

Aug

-11

Ma

r-12

Oct-

12

Ma

y-1

3

De

c-1

3

Ju

l-1

4

Fe

b-1

5

Sep

-15

Apr-

16

No

v-1

6

Ju

n-1

7

Ja

n-1

8

Aug

-18

Ma

r-19

Indian Diesel price - Delhi (Rs/Ltr)

prices. But with the increase in prices seen since February 2017, these benefits were

receding. Though, prices of coal, petcoke and crude (for diesel prices) which earlier were

trading closer to cyclical highs have started moderating.

Coal – Prices of imported coal have moderated from peak and is on downward

trend since October 2018. Over the last couple months, the prices have declined by

~12% and we expect the positive impact of lower prices to be visible going forward.

Diesel – Diesel prices too have corrected by ~12% from the peak witnessed in

October 2018. Diesel prices impact the freight costs of the cement players.

Pet coke –Imported pet-coke prices have also declined by ~10% to USD 97/tonne

from the peak witnessed in October 2018. This should result in a fall in domestic pet

coke prices as well. Indian refineries set their ex-works prices on import parity and

these prices are set to come down.

Freight is ~25%-30% of the cost

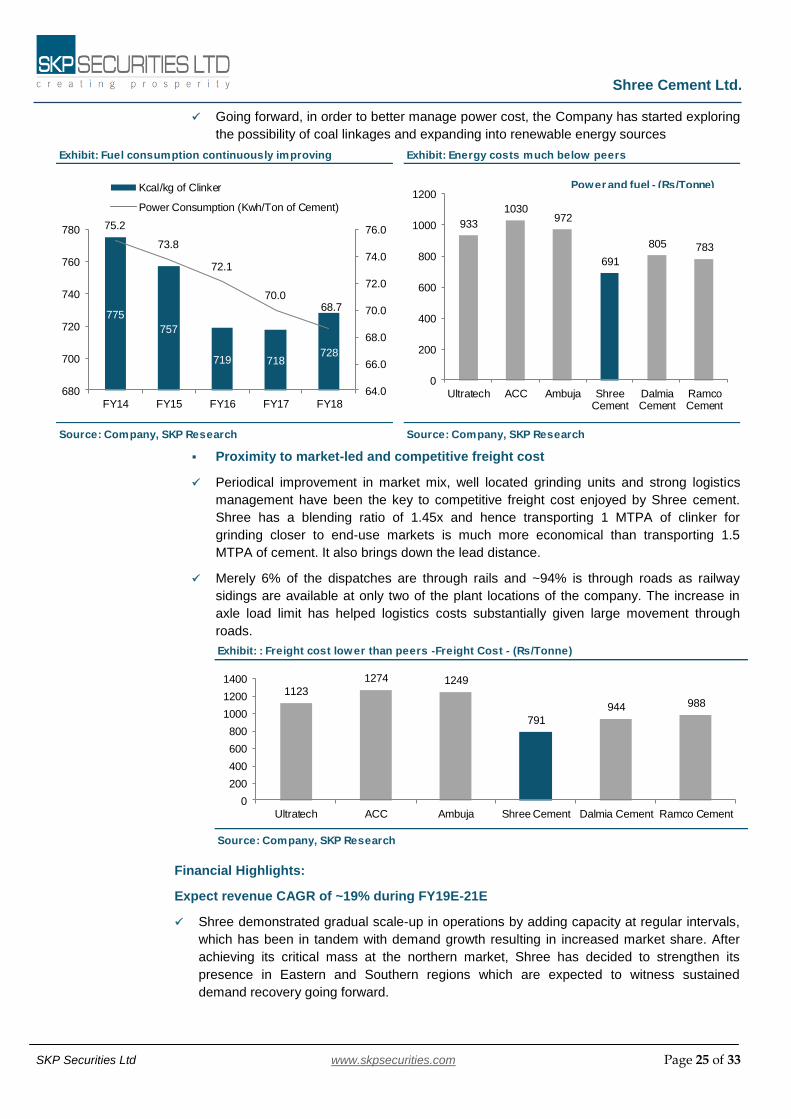

Freight cost depends on 1) lead distance to end user 2) mix between rail and road

transportation 3) strategic allocation of capacities across integrated and grinding units.

Typically rail is a more beneficial mode of transportation beyond 450 kms. New truck axle

load norms introduced in July 2018, should be beneficial for freight costs of bulky

commodities like cement as ~60%-65% of cement dispatches take place by road. The

notification (new truck axle load) further clarifies that the norms are applicable for new as

well as existing trucks.

Assuming an average blending ratio of 1.5x, 1.0 tonne of clinker can produce 1.5 tonnes

of cement. Hence if cement grinding is to be done at an integrated plant (i.e. near the

limestone mines and far from markets), freight cost will be incurred to transport 1.5

tonnes of cement. However, if grinding is done at split units nearer to markets, then only

1.0 tonne of clinker has to be transported to grinding units, which in turn can transport

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 9 of 33

Exhibit: Demand/supply model over FY08-FY21E

NorthCentralWesternSouthEast

Source: Ultratech Presentation, SKP Research

198 216

276 3

10 328 3

63

376 402

417

428 456

473 492

507

164

178 203

214

230

243

249

257

269

272 296 325 351 379

34 38

73 9

6

98 1

20

127 145

148

156

160

148

141

128

83% 82%

74%69% 70%

67% 66%64% 65% 64%

65%69%

71%75%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

100

200

300

400

500

600

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Actual- effective capacity (MTPA) Demand (MTPA) Surplus capacity (MTPA) Utilisations (%)

Incremental Supply ‐ 258 MTPA> Demand ‐ 132 MTPA Supply ‐51 MTPA> Demand ‐84 MTPA

Industry capacity more than doubled in last decade.Around 55 million tons capacity added in last 3 y ears Demand picked up in FY18.

Surplus capacity in the sector ~ 160 million tonnes

1.5 tonnes of cement to the markets. Shree is the leader here as well, since they have

strategically placed smaller split grinding units across all their addressable

markets and hence have the lowest freight cost per ton across the players.

Demand - supply mismatch to moderate

India’s cement sector is favourably placed to benefit from the multiple tailwinds: rising

demand, improving utilisations and subsiding cost inflation. After a spurt in capacity

additions (over FY11-18, India's cement industry saw ~138 MTPA of capacity additions - at

an average of ~19 MTPA/year, significantly above incremental cumulative demand of ~83

MTPA) witnessed during the last decade; during which the industry capacity has almost

doubled to ~465 MTPA, the pace of new capacity addition has considerably slowed down

on account of volatile earnings, stretched balance sheets of certain players and higher costs

of funding.

As a result, we believe ~40%-45% of the FY19-21E pipeline capacity (~35-40 MTPA) will be

delayed, thus, improving the demand-supply dynamics. We estimate demand could record

~8% CAGR over the same period (~54 MTPA in absolute demand), translating to an

improvement in utilization rates – from ~65% in FY18 to ~75% in FY21E.

Industry’s clinker capacity addition a better parameter to gauge actual cement production

Clinker capacity addition in FY18 has been the lowest in the past decade. We believe

clinker utilization would be a better parameter to gauge actual cement production rather

than cement utilization as few of the capacities may be just grinding units to optimise logistic

costs, to enter new markets etc. While there was hardly any gap between cement and

clinker utilization till FY17, the hiatus increased in FY18-19E and is likely to widen by FY21E

and even higher going ahead. This is mainly due to the fact that while 42 MTPA capacities

are being added over FY18-FY19E, clinker capacity additions are likely to be around 9

MTPA.

Moreover, one can safely conclude, anchored by slim capacity addition pipeline over the

next two years as announced by companies and orders placed with equipment

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 10 of 33

(MTPA) FY16 FY17 FY18 FY19E FY20E FY21E

Clinker capacity- effective 296 305 314 319 327 340

Blending ratio 1.4 1.4 1.4 1.4 1.4 1.4

Maximum cement production capacity- effective 420 434 448 456 467 486

Clinker utilisation- effective capacity (%) 67 67 71 77 80 81

Cement utilisation- effective capacity (%) 65 64 65 69 71 75

Source: Industry, SKP Research

All-India

Exhibit: Clinker utilisation likely to be higher

Exhibit: Cement plant construction costs inching up Exhibit: Time required to set up a cement plant

Source: Industry, FL Smidth, SKP Research Source: Industry, FL Smidth, SKP Research

Equipment, 45%

Land and mining

rights, 19%

Captiv e power , 10%

Others, 7%

Erection , 8%

Civ il works, 10%

0

10

20

30

40

50

60

70

80

Greenfield Brownfield Greenfield Brownfield

5 years ago Current

Land EPC Construction

Months

manufacturers, that the industry’s clinker utilization will rise from ~71% in FY18 to 81% by

FY21E.

Entry barrier - High initial capital outlay & long gestation periods have elongated the duration of a cement project

The cost of setting up a cement plant has nearly doubled over the past seven years.

Furthermore, the lead time for establishing a cement plant in India has increased from three

to four years to approx six years due to challenges in acquiring land and delays in

regulatory clearances. In the recent past, companies have announced projects at an

average cost of USD 110-130/tonne for a Greenfield integrated project, while for a

brownfield grinding project the average cost announced was USD 50/tonne.

The industry has also witnessed some escalation in the costs of equipment and land. A

cement plant with 1 MTPA of capacity/annum requires ~ 200 hectares of land. Assuming an

80% capacity utilization rate and a price of Rs 300 per bag, a cement plant would barely

earn its cost of capital. Therefore, this will curtail new supply plans in the long term.

Furthermore, with substantial capacity additions over the last five years, many mid-tier

Indian cement companies have stretched their balance sheets. Hence, we believe they are

unlikely to undertake incremental capacity additions in the coming years unless they start to

see growing returns for their existing plants.

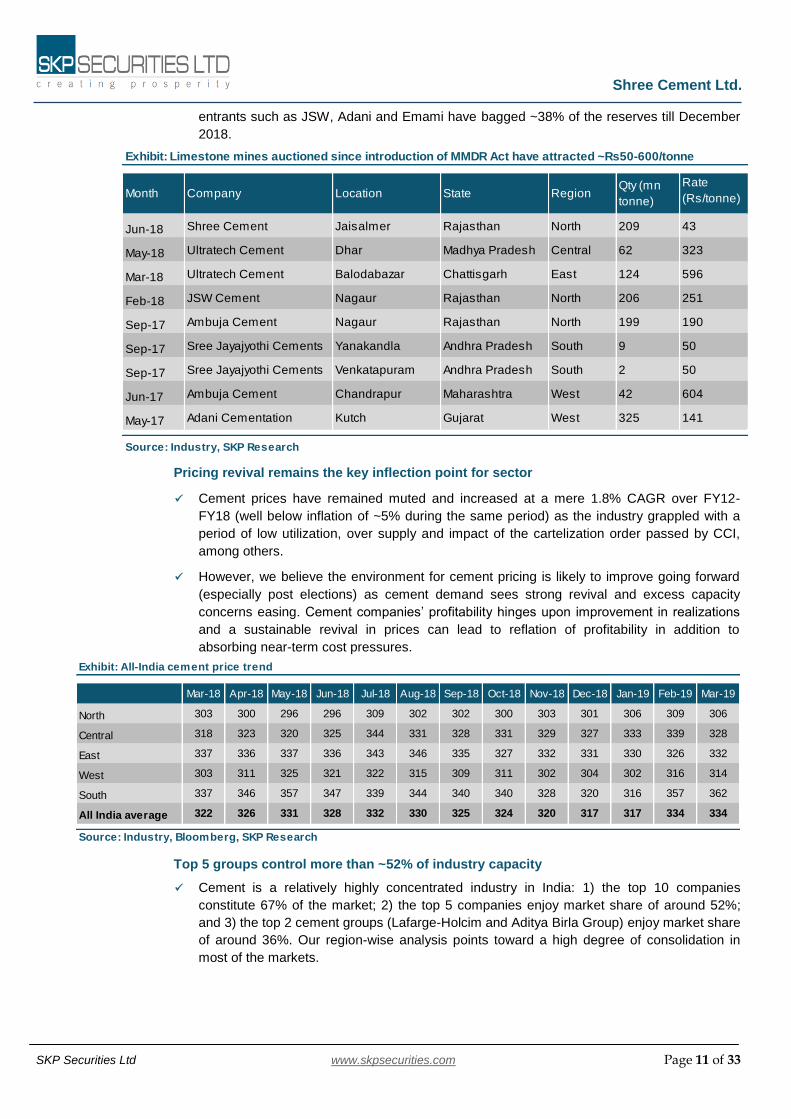

Increase in limestone costs as mines auctioned at material premium

The process of acquiring limestone mines, which is the key raw material in cement

production, has undergone a significant change post MMDR (Amendment) Act, 2015. As

limestone is one among the ‘notified’ minerals under the act, licensing of mines has to go

through a compulsory bidding process, which creates a level playing field for all cement

players. It also creates an additional cost burden, which shaves away profitability.

Players have been aggressively bidding in limestone block auctions, with winning bids at

recent auctions going as high as 125% of the value of the mineral. The top five players in

the industry have won over ~50% of the 2.80 bn tonnes of limestone reserves, while new

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 11 of 33

Exhibit: Limestone mines auctioned since introduction of MMDR Act have attracted ~Rs50-600/tonne

Jun-18 Shree Cement Jaisalmer Rajasthan North 209 43

May-18 Ultratech Cement Dhar Madhya Pradesh Central 62 323

Mar-18 Ultratech Cement Balodabazar Chattisgarh East 124 596

Feb-18 JSW Cement Nagaur Rajasthan North 206 251

Sep-17 Ambuja Cement Nagaur Rajasthan North 199 190

Sep-17 Sree Jayajyothi Cements Yanakandla Andhra Pradesh South 9 50

Sep-17 Sree Jayajyothi Cements Venkatapuram Andhra Pradesh South 2 50

Jun-17 Ambuja Cement Chandrapur Maharashtra West 42 604

May-17 Adani Cementation Kutch Gujarat West 325 141

Source: Industry, SKP Research

MonthQty (mn

tonne)

Rate

(Rs/tonne)Company Location State Region

Exhibit: All-India cement price trend

Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19

North 303 300 296 296 309 302 302 300 303 301 306 309 306

Central 318 323 320 325 344 331 328 331 329 327 333 339 328

East 337 336 337 336 343 346 335 327 332 331 330 326 332

West 303 311 325 321 322 315 309 311 302 304 302 316 314

South 337 346 357 347 339 344 340 340 328 320 316 357 362

All India average 322 326 331 328 332 330 325 324 320 317 317 334 334

Source: Industry, Bloomberg, SKP Research

entrants such as JSW, Adani and Emami have bagged ~38% of the reserves till December

2018.

Pricing revival remains the key inflection point for sector

Cement prices have remained muted and increased at a mere 1.8% CAGR over FY12-

FY18 (well below inflation of ~5% during the same period) as the industry grappled with a

period of low utilization, over supply and impact of the cartelization order passed by CCI,

among others.

However, we believe the environment for cement pricing is likely to improve going forward

(especially post elections) as cement demand sees strong revival and excess capacity

concerns easing. Cement companies’ profitability hinges upon improvement in realizations

and a sustainable revival in prices can lead to reflation of profitability in addition to

absorbing near-term cost pressures.

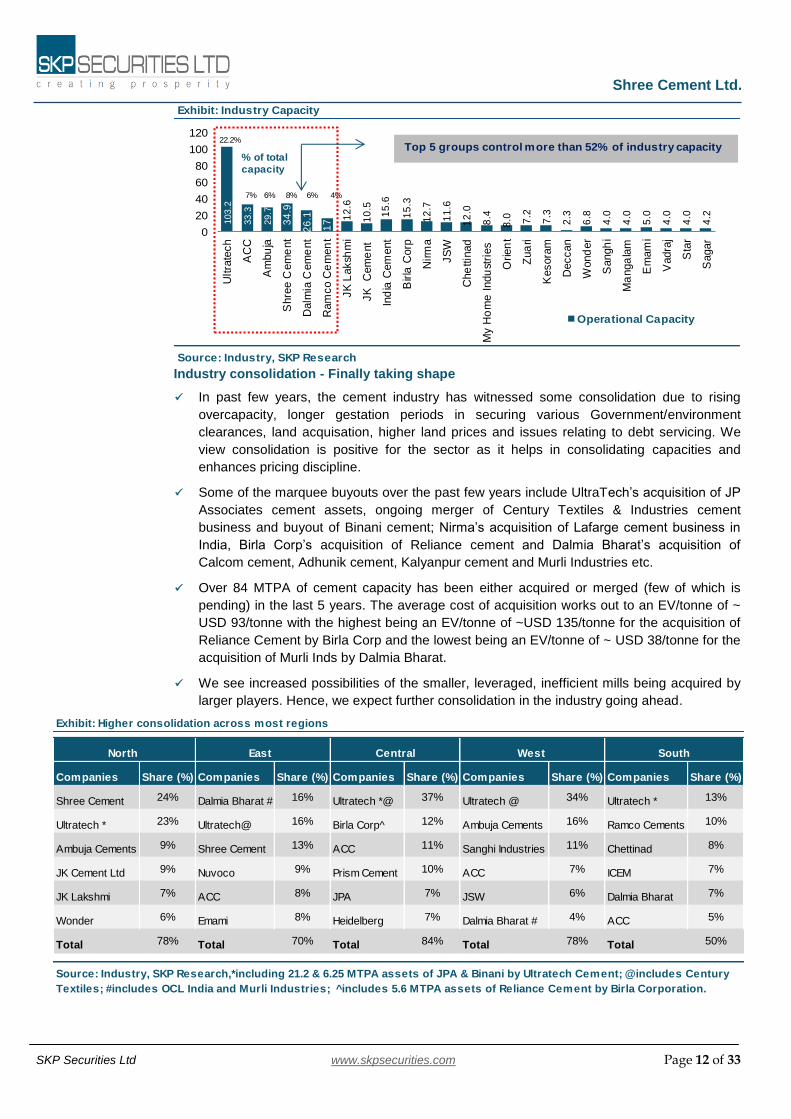

Top 5 groups control more than ~52% of industry capacity

Cement is a relatively highly concentrated industry in India: 1) the top 10 companies

constitute 67% of the market; 2) the top 5 companies enjoy market share of around 52%;

and 3) the top 2 cement groups (Lafarge-Holcim and Aditya Birla Group) enjoy market share

of around 36%. Our region-wise analysis points toward a high degree of consolidation in

most of the markets.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 12 of 33

Exhibit: Higher consolidation across most regions

Companies Share (%) Companies Share (%) Companies Share (%) Companies Share (%) Companies Share (%)

Shree Cement 24% Dalmia Bharat # 16% Ultratech *@ 37% Ultratech @ 34% Ultratech * 13%

Ultratech * 23% Ultratech@ 16% Birla Corp^ 12% Ambuja Cements 16% Ramco Cements 10%

Ambuja Cements 9% Shree Cement 13% ACC 11% Sanghi Industries 11% Chettinad 8%

JK Cement Ltd 9% Nuvoco 9% Prism Cement 10% ACC 7% ICEM 7%

JK Lakshmi 7% ACC 8% JPA 7% JSW 6% Dalmia Bharat 7%

Wonder 6% Emami 8% Heidelberg 7% Dalmia Bharat # 4% ACC 5%

Total 78% Total 70% Total 84% Total 78% Total 50%

Source: Industry, SKP Research,*including 21.2 & 6.25 MTPA assets of JPA & Binani by Ultratech Cement; @includes Century

Textiles; #includes OCL India and Murli Industries; ^includes 5.6 MTPA assets of Reliance Cement by Birla Corporation.

North East Central West South

Exhibit: Industry Capacity

Source: Industry, SKP Research

10

3.2

33.3

29.7

34

.9

26

.1

17 1

2.6

10

.5

15

.6

15

.3

12

.7

11

.6

12

.0

8.4

8.0 7.2

7.3

2.3

6.8

4.0

4.0

5.0

4.0

4.0

4.2

0

20

40

60

80

100

120

Ultra

tech

AC

C

Am

bu

ja

Shre

e C

em

ent

Dalm

ia C

em

ent

Ram

co C

em

en

t

JK

Laksh

mi

JK

C

em

ent

Ind

ia C

em

ent

Birla

Corp

Nirm

a

JS

W

Che

ttin

ad

My H

om

e I

ndu

stri

es

Orien

t

Zua

ri

Kesora

m

Deccan

Wond

er

Sangh

i

Ma

nga

lam

Em

am

i

Vadra

j

Sta

r

Sagar

Operational Capacity

22.2%

7% 6% 8% 6% 4%

% of total

capacity

Top 5 groups control more than 52% of industry capacity

Industry consolidation - Finally taking shape

In past few years, the cement industry has witnessed some consolidation due to rising

overcapacity, longer gestation periods in securing various Government/environment

clearances, land acquisation, higher land prices and issues relating to debt servicing. We

view consolidation is positive for the sector as it helps in consolidating capacities and

enhances pricing discipline.

Some of the marquee buyouts over the past few years include UltraTech’s acquisition of JP

Associates cement assets, ongoing merger of Century Textiles & Industries cement

business and buyout of Binani cement; Nirma’s acquisition of Lafarge cement business in

India, Birla Corp’s acquisition of Reliance cement and Dalmia Bharat’s acquisition of

Calcom cement, Adhunik cement, Kalyanpur cement and Murli Industries etc.

Over 84 MTPA of cement capacity has been either acquired or merged (few of which is

pending) in the last 5 years. The average cost of acquisition works out to an EV/tonne of ~

USD 93/tonne with the highest being an EV/tonne of ~USD 135/tonne for the acquisition of

Reliance Cement by Birla Corp and the lowest being an EV/tonne of ~ USD 38/tonne for the

acquisition of Murli Inds by Dalmia Bharat.

We see increased possibilities of the smaller, leveraged, inefficient mills being acquired by

larger players. Hence, we expect further consolidation in the industry going ahead.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 13 of 33

Exhibit: Mergers and acquisitions (M&A) activities have picked up in the last 5 years

Date Buyer Seller Capacity

(MTPA)

EV/Tn

(USD)Remarks

Jul '13 Ambuja Cements Holcim India 30.7 115 Acquired 50.01% equity stake in ACC

Sept '13 UltraTech Cement *JAL 4.8 125 Gujarat assets of JAL, EV/EBITDA of 11x

Mar '14 Dalmia Bharat *JAL 2.1 90Acquired JAL's 74% stake in 2.1 MT grinding unit w ith a 30-year clinker / slag

supply agreement.

Aug'14 Shree Cement *JAL 1.5 40 Grinding unit only in Haryana

Sept '14 Sagar Cement BMM Cement 1.3 90Integrated plant in Andhra Pradesh w ith 25MW capacity, 174.7 MTPA of

limestone reserve

Feb '15 Dalmia Bharat OCL India 6.8 110Increases its stake from 48.23% to 74.93% consolidating OCL India w ith its

operations

Feb '16 Birla Corp Reliance Cement 5.5 135 One integrated plant and tw o grinding units

Feb '16 UltraTech Cement *JAL 22.4 110 Assets spread across Central, North and South

Jul '16 Nirma Lafarge 11.0 117 Assets spread across East and North region.

Dec '17 Dalmia Bharat Murli Industries 3.0 38 Capex of Rs 3 billion required to make the plant operational

Jan '18 Dalmia Bharat Kalyanpur Cement 1.1 50Dalmia Bharat w ill pay a total consideration of Rs. 3.53 billion to acquire and

an additional Rs. 1 billion in capex to make the plant operational

May '18 UltraTech Cement Century Textile 13.4 106 It includes 2 MTPA grinding units. Ultratech received CCI approval in Aug’18

Jan '18 UltraTech Cement Binani Cement 11.0 100It includes good quality of limestone reserves, and has potential for further

brow nfield expansion.

Source: Industry, SKP Research, USD rate on the date of transaction,*JAL-Jaiprakash Associates Ltd.

Demand Drivers Cement demand – at a cusp of turnaround

The cement demand cycle is at an inflexion point and is on the cusp of turnaround. India’s

cement industry has remained a largely structural growth story with consumption growth

averaging ~6.1% over the last 10 years. However, in the last 5 years (FY14-FY18) the trend

has reversed from the long-term growth average, including one year of marginal growth

(1%) during the demonetization period. This is largely due to: 1) India’s GDP growth rate

has slowed in recent years and 2) cement demand growth has dipped to <1.0x GDP growth.

The low base for demand recovery, coupled with infrastructure related spending (primarily

housing and infrastructure) in FY20E sets the stage for a potentially sharp cyclical demand

recovery in the sector.

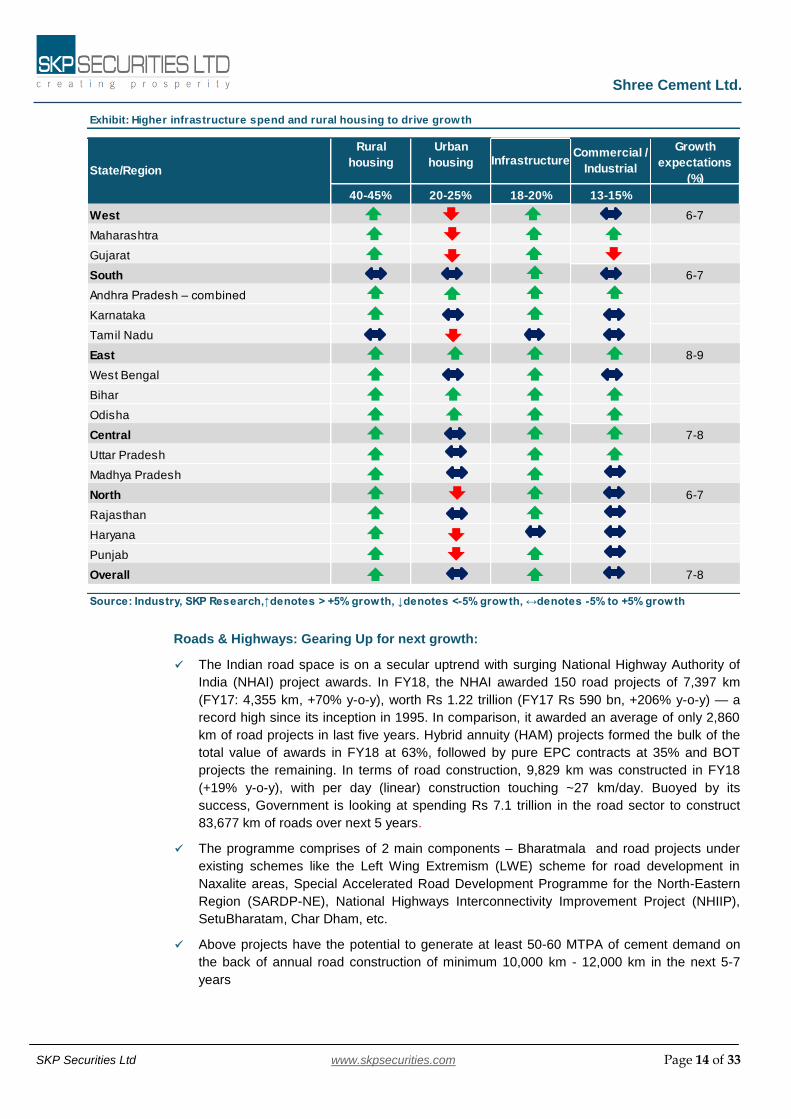

Higher infrastructure spending to drive growth

East, Central and South regions are leading growth in demand backed by higher

Government infrastructure spends like roads and irrigation, pick-up in construction of

affordable houses and rural housing demand. The share of infrastructure in overall cement

demand is expected to increase from the current ~18%-20% to ~22%-24% over the next

five years led by increased public spending. Over the past few years, weak macroeconomic

environment and several regulatory issues impacted infrastructure sector. However,

increase in project announcements and pick-up in execution suggests a signs of revival. In

addition, with general elections approaching in the next ~5-6 months, we expect project

execution pace to further improve.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 14 of 33

West

Maharashtra

Gujarat

South

Andhra Pradesh – combined

Karnataka

Tamil Nadu

East

West Bengal

Bihar

Odisha

Central

Uttar Pradesh

Madhya Pradesh

North

Rajasthan

Haryana

Punjab

Overall

Source: Industry, SKP Research,↑denotes > +5% growth, ↓denotes <-5% growth, ↔denotes -5% to +5% growth

6-7

6-7

8-9

7-8

6-7

7-8

Exhibit: Higher infrastructure spend and rural housing to drive growth

State/Region

Rural

housing

Urban

housing InfrastructureCommercial /

Industrial

Growth

expectations

(%)

40-45% 20-25% 18-20% 13-15%

Roads & Highways: Gearing Up for next growth:

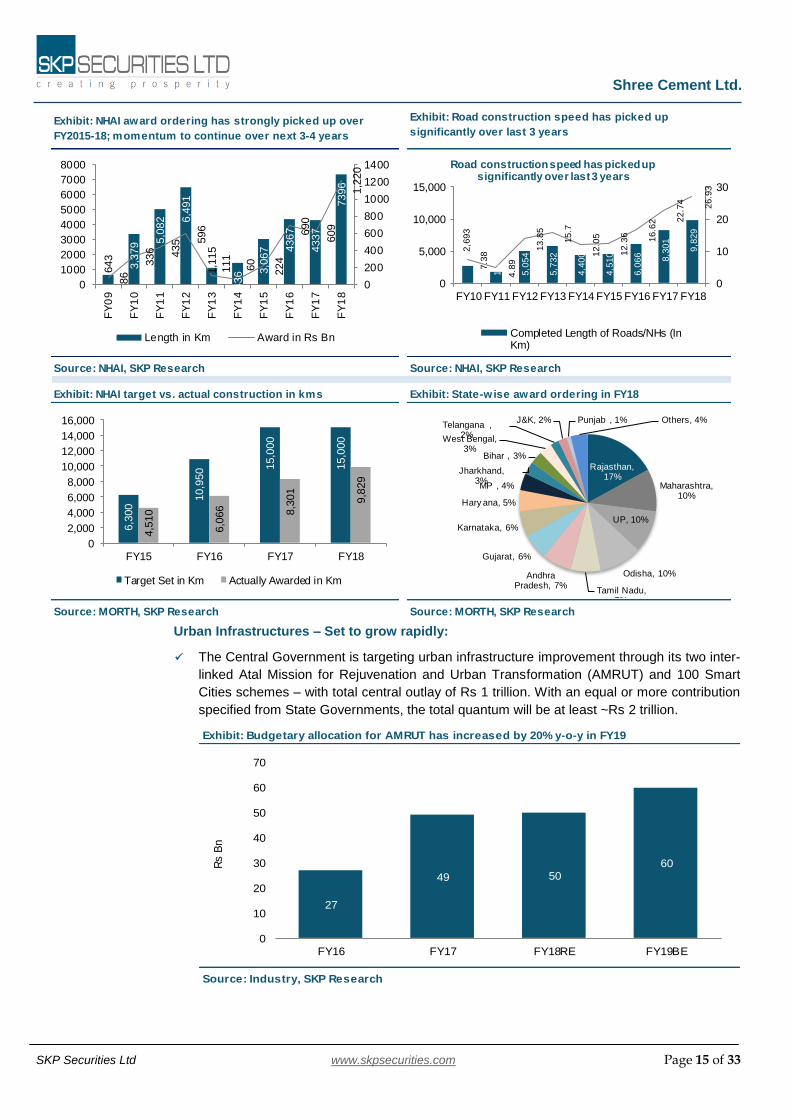

The Indian road space is on a secular uptrend with surging National Highway Authority of

India (NHAI) project awards. In FY18, the NHAI awarded 150 road projects of 7,397 km

(FY17: 4,355 km, +70% y-o-y), worth Rs 1.22 trillion (FY17 Rs 590 bn, +206% y-o-y) — a

record high since its inception in 1995. In comparison, it awarded an average of only 2,860

km of road projects in last five years. Hybrid annuity (HAM) projects formed the bulk of the

total value of awards in FY18 at 63%, followed by pure EPC contracts at 35% and BOT

projects the remaining. In terms of road construction, 9,829 km was constructed in FY18

(+19% y-o-y), with per day (linear) construction touching ~27 km/day. Buoyed by its

success, Government is looking at spending Rs 7.1 trillion in the road sector to construct

83,677 km of roads over next 5 years.

The programme comprises of 2 main components – Bharatmala and road projects under

existing schemes like the Left Wing Extremism (LWE) scheme for road development in

Naxalite areas, Special Accelerated Road Development Programme for the North-Eastern

Region (SARDP-NE), National Highways Interconnectivity Improvement Project (NHIIP),

SetuBharatam, Char Dham, etc.

Above projects have the potential to generate at least 50-60 MTPA of cement demand on

the back of annual road construction of minimum 10,000 km - 12,000 km in the next 5-7

years

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 15 of 33

Source: NHAI, SKP Research Source: NHAI, SKP Research

Exhibit: NHAI target vs. actual construction in kms Exhibit: State-wise award ordering in FY18

Source: MORTH, SKP Research Source: MORTH, SKP Research

Exhibit: NHAI award ordering has strongly picked up over

FY2015-18; momentum to continue over next 3-4 years

Exhibit: Road construction speed has picked up

significantly over last 3 years

643

3,3

79 5

,082 6,4

91

1,1

15

1,4

36 3

,067 4

367

4337

7396

86

336 435 5

96

111

60

224

690

609

1,2

20

0

200

400

600

800

1000

1200

1400

0

1000

2000

3000

4000

5000

6000

7000

8000

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

Length in Km Award in Rs Bn

2,6

93

1,7

86

5,0

54

5,7

32

4,4

00

4,5

10

6,0

66 8,3

01

9,8

29

7.3

8

4.8

9

13.8

5

15.7

12.0

5

12.3

6

16.6

2 22.7

4

26.9

3

0

10

20

30

0

5,000

10,000

15,000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Road construction speed has picked up significantly over last 3 years

Completed Length of Roads/NHs (InKm)

6,3

00

10,9

50 1

5,0

00

15,0

00

4,5

10

6,0

66 8,3

01

9,8

29

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY15 FY16 FY17 FY18

Target Set in Km Actually Awarded in Km

Rajasthan, 17%

Maharashtra, 10%

UP, 10%

Odisha, 10%

Tamil Nadu, 7%

Andhra Pradesh, 7%

Gujarat, 6%

Karnataka, 6%

Hary ana, 5%

MP , 4%

Jharkhand, 3%

Bihar , 3%

West Bengal, 3%

Telangana , 2%

J&K, 2% Punjab , 1% Others, 4%

Source: Industry, SKP Research

Exhibit: Budgetary allocation for AMRUT has increased by 20% y-o-y in FY19

27

49 5060

0

10

20

30

40

50

60

70

FY16 FY17 FY18RE FY19BE

Rs B

n

Urban Infrastructures – Set to grow rapidly:

The Central Government is targeting urban infrastructure improvement through its two inter-

linked Atal Mission for Rejuvenation and Urban Transformation (AMRUT) and 100 Smart

Cities schemes – with total central outlay of Rs 1 trillion. With an equal or more contribution

specified from State Governments, the total quantum will be at least ~Rs 2 trillion.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 16 of 33

Source: Ministry of Rural Development, SKP Research Source: Union Budget, SKP Research

Exhibit: Budgetary allocation under PMAY-G increased by

43% y-o-y in FY19

Exhibit: Construction of rural houses increased by 39%

YoY in FY18

1.1 1.21.8

3.2

4.5

0

1

2

3

4

5

FY14 FY15 FY16 FY17 FY18

(Mn Houses)

110

100 1

60

230

330

111

101 1

61

0

50

100

150

200

250

300

350

FY15 FY16 FY17 FY18RE FY19BE

Budgeted Actual

Exhibit: ~30 MTPA of cement demand from PMAY-G by FY22

Key project

Total no. of houses to targeted be constructed (in mn) 29.5

Houses already constructed 4.8

No. of (mn) houses yet to be constructed (govt.) 24.7

Target achieved (%) assumed 25%

No. of houses to be constructed 6.2

Average size of house (sqft) 270.0

Cement required (kg/sqft) 18.0

Total cement demand 30.0

Source: Industry, SKP Research

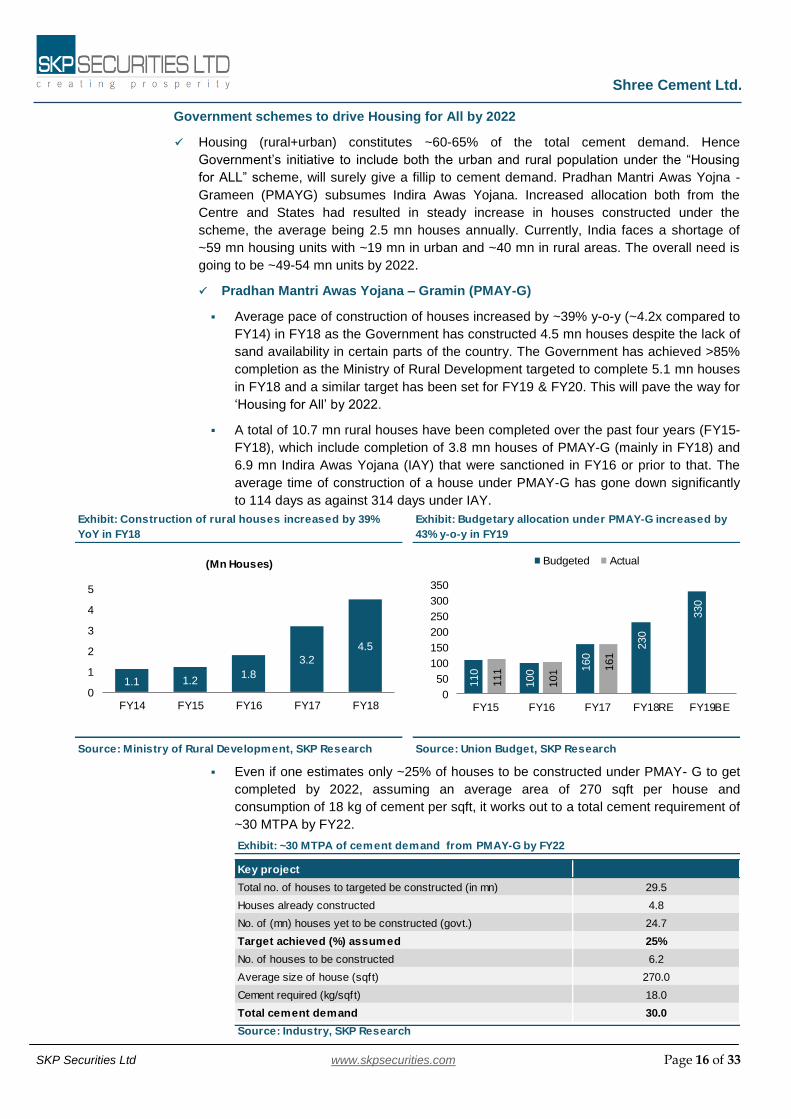

Government schemes to drive Housing for All by 2022

Housing (rural+urban) constitutes ~60-65% of the total cement demand. Hence

Government’s initiative to include both the urban and rural population under the “Housing

for ALL” scheme, will surely give a fillip to cement demand. Pradhan Mantri Awas Yojna -

Grameen (PMAYG) subsumes Indira Awas Yojana. Increased allocation both from the

Centre and States had resulted in steady increase in houses constructed under the

scheme, the average being 2.5 mn houses annually. Currently, India faces a shortage of

~59 mn housing units with ~19 mn in urban and ~40 mn in rural areas. The overall need is

going to be ~49-54 mn units by 2022.

Pradhan Mantri Awas Yojana – Gramin (PMAY-G)

Average pace of construction of houses increased by ~39% y-o-y (~4.2x compared to

FY14) in FY18 as the Government has constructed 4.5 mn houses despite the lack of

sand availability in certain parts of the country. The Government has achieved >85%

completion as the Ministry of Rural Development targeted to complete 5.1 mn houses

in FY18 and a similar target has been set for FY19 & FY20. This will pave the way for

‘Housing for All’ by 2022.

A total of 10.7 mn rural houses have been completed over the past four years (FY15-

FY18), which include completion of 3.8 mn houses of PMAY-G (mainly in FY18) and

6.9 mn Indira Awas Yojana (IAY) that were sanctioned in FY16 or prior to that. The

average time of construction of a house under PMAY-G has gone down significantly

to 114 days as against 314 days under IAY.

Even if one estimates only ~25% of houses to be constructed under PMAY- G to get

completed by 2022, assuming an average area of 270 sqft per house and

consumption of 18 kg of cement per sqft, it works out to a total cement requirement of

~30 MTPA by FY22.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 17 of 33

Exhibit: ~14 MTPA of cement demand from PMAY-U by FY22

Key project

Total no. of houses to targeted be constructed (in mn) 10.0

Houses already constructed 0.8

No. of (mn) houses yet to be constructed (govt.) 9.2

Target achieved (%) assumed 25%

No. of houses to be constructed 2.3

Average size of house (sqft) 350.0

Cement required (kg/sqft) 18.0

Total cement demand 14.0

Source: Industry, SKP Research

Exhibit: States going for elections by FY21E

State Region Election scheduled % of annual cement demand

Odisha East Jun-19 4%

Andhra Pradesh* South Jun-19 7%

Haryana North Nov-19 4%

Maharashtra West Nov-19 10%

Jharkhand Region Nov-19 2%

NCT Delhi North Feb-20 3%

Jammu and Kashmir South Feb-21 1%

Total 31%

Source: Industry, SKP Research, Andhra Pradesh and Telangana – combined

Pradhan Mantri Awas Yojana – Urban (PMAY- U)

Under this scheme, the Government aims to construct 10 mn affordable houses by 2022 in urban areas for slum dwellers and people from economically weaker sections and low income groups. Track record of sanctions under the PMAY-U scheme is comparatively much better as it sanctioned 5.4 mn houses in the past three years, ~4.3x more houses sanctioned over previous decade. Central Government assistance approved for release to states and Union Territories has increased to Rs 820 bn in past three years vs. just Rs 188 bn in the previous decade.

Overall, budgetary allocation for PMAY-U has increased by ~5.2x y-o-y to Rs 315 bn in FY19 including Rs 250 bn under EBR. Additionally, a National Urban Housing Fund for Rs 600 bn has been set up for raising EBR in phases, for the speedy execution of the scheme. The significant increase in the budget for urban housing is expected to accelerate the completion of houses and revival in urban housing demand.

Even if one estimates only ~25% of houses to be constructed under PMAY- U get completed by 2022, assuming an average area of 350 sqft per house and consumption of 18 kg of cement per sqft, it works out to a total cement requirement of ~14 MTPA by FY22.

Upcoming state elections should spur demand

Demand for cement picks up during the election time, as incumbent Government tries to

meet some of the infrastructure related commitments. Over the next two to three years,

besides general election at the Centre, many key cement consuming states like

Maharashtra, Andhra Pradesh, Odisha, Haryana etc are scheduled for elections. It is

expected that there would be a greater thrust by all agencies to marquee projects such as

Bharatmala, the Smart Cities Project and the Housing for All by 2022 scheme. These

electoral developments will keep demand buoyant till FY21E.

Outlook

We anticipate a revival in cement demand driven by 1) sustained focus on individual/rural

housing and infra, 2) lessening demand - supply mismatch 3) rising consolidation with top 5

groups account for ~52% of current production, leading to increasing concentration in

cement supply 4) difficulty in greenfield capacity expansions with tighter regulations

(MMDR, environmental norms, etc.) and muted return on investment and 5) softening raw

material prices especially pet-coke price and stable freight cost (lower crude prices).

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 18 of 33

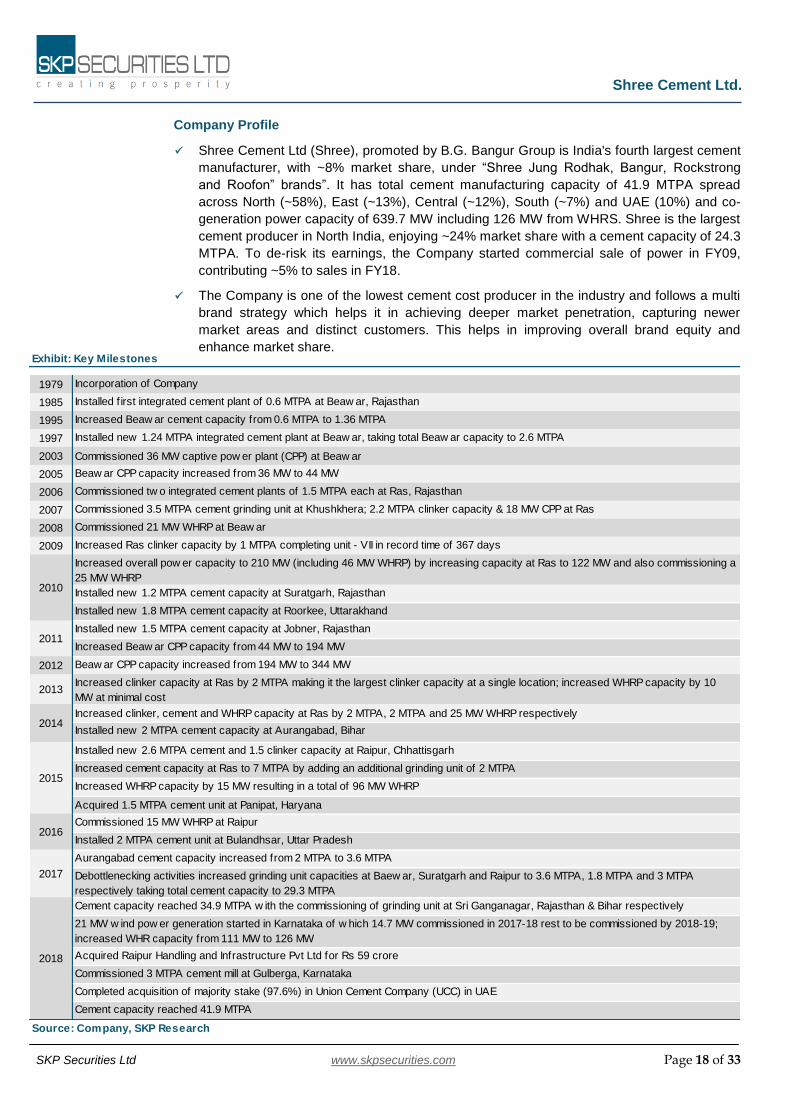

Exhibit: Key Milestones

1979 Incorporation of Company

1985 Installed f irst integrated cement plant of 0.6 MTPA at Beaw ar, Rajasthan

1995 Increased Beaw ar cement capacity from 0.6 MTPA to 1.36 MTPA

1997 Installed new 1.24 MTPA integrated cement plant at Beaw ar, taking total Beaw ar capacity to 2.6 MTPA

2003 Commissioned 36 MW captive pow er plant (CPP) at Beaw ar

2005 Beaw ar CPP capacity increased from 36 MW to 44 MW

2006 Commissioned tw o integrated cement plants of 1.5 MTPA each at Ras, Rajasthan

2007 Commissioned 3.5 MTPA cement grinding unit at Khushkhera; 2.2 MTPA clinker capacity & 18 MW CPP at Ras

2008 Commissioned 21 MW WHRP at Beaw ar

2009 Increased Ras clinker capacity by 1 MTPA completing unit - VII in record time of 367 days

Increased overall pow er capacity to 210 MW (including 46 MW WHRP) by increasing capacity at Ras to 122 MW and also commissioning a

25 MW WHRP

Installed new 1.2 MTPA cement capacity at Suratgarh, Rajasthan

Installed new 1.8 MTPA cement capacity at Roorkee, Uttarakhand

Installed new 1.5 MTPA cement capacity at Jobner, Rajasthan

Increased Beaw ar CPP capacity from 44 MW to 194 MW

2012 Beaw ar CPP capacity increased from 194 MW to 344 MW

2013Increased clinker capacity at Ras by 2 MTPA making it the largest clinker capacity at a single location; increased WHRP capacity by 10

MW at minimal cost

Increased clinker, cement and WHRP capacity at Ras by 2 MTPA, 2 MTPA and 25 MW WHRP respectively

Installed new 2 MTPA cement capacity at Aurangabad, Bihar

Installed new 2.6 MTPA cement and 1.5 clinker capacity at Raipur, Chhattisgarh

Increased cement capacity at Ras to 7 MTPA by adding an additional grinding unit of 2 MTPA

Increased WHRP capacity by 15 MW resulting in a total of 96 MW WHRP

Acquired 1.5 MTPA cement unit at Panipat, Haryana

Commissioned 15 MW WHRP at Raipur

Installed 2 MTPA cement unit at Bulandhsar, Uttar Pradesh

Aurangabad cement capacity increased from 2 MTPA to 3.6 MTPA

Debottlenecking activities increased grinding unit capacities at Baew ar, Suratgarh and Raipur to 3.6 MTPA, 1.8 MTPA and 3 MTPA

respectively taking total cement capacity to 29.3 MTPA

Cement capacity reached 34.9 MTPA w ith the commissioning of grinding unit at Sri Ganganagar, Rajasthan & Bihar respectively

21 MW w ind pow er generation started in Karnataka of w hich 14.7 MW commissioned in 2017-18 rest to be commissioned by 2018-19;

increased WHR capacity from 111 MW to 126 MW

Acquired Raipur Handling and Infrastructure Pvt Ltd for Rs 59 crore

Commissioned 3 MTPA cement mill at Gulberga, Karnataka

Completed acquisition of majority stake (97.6%) in Union Cement Company (UCC) in UAE

Cement capacity reached 41.9 MTPA

Source: Company, SKP Research

2017

2018

2010

2011

2014

2016

2015

Company Profile

Shree Cement Ltd (Shree), promoted by B.G. Bangur Group is India's fourth largest cement

manufacturer, with ~8% market share, under “Shree Jung Rodhak, Bangur, Rockstrong

and Roofon” brands”. It has total cement manufacturing capacity of 41.9 MTPA spread

across North (~58%), East (~13%), Central (~12%), South (~7%) and UAE (10%) and co-

generation power capacity of 639.7 MW including 126 MW from WHRS. Shree is the largest

cement producer in North India, enjoying ~24% market share with a cement capacity of 24.3

MTPA. To de-risk its earnings, the Company started commercial sale of power in FY09,

contributing ~5% to sales in FY18.

The Company is one of the lowest cement cost producer in the industry and follows a multi

brand strategy which helps it in achieving deeper market penetration, capturing newer

market areas and distinct customers. This helps in improving overall brand equity and

enhance market share.

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 19 of 33

Source: Company, SKP Research,*Includes UAE capacity of 4 MTPA

Exhibit : Capacity Over the Last 5 years

Year- 2014Installed capacity: 17.5 MTPA

Year- 2019E*Installed capacity: 41.9 MTPA

#7 plants in #3 states #11 plants in #7 states

Capacity has doubled in last 4 years

Over the years, Shree has transformed itself from being a regional player (north India) to

currently having presence in east, central and now south India by following small but regular

organic and inorganic expansions. From FY14 till date, the Company has multiplied its

capacity by 2.4x from 17.5 MTPA to currently 41.9 MTPA by adding 10.8 MTPA capacity in

north and central, followed by 6.6 mtpa capacity in east and 3 mtpa capacity in south.

Lately, Shree has established its footprint in UAE with acquisition of Union Cement

Company (UCC) having 4 MTPA cement capacity at an enterprise value (EV) of Rs 19.5 bn.

The Company has a track record of completing projects within time periods, much lower

than the industry standards, thereby optimizing on both cost and time. Though, incremental

capacity additions especially Greenfield will come at a higher cost due to challenges in

acquiring land coupled with higher land prices and securing long term availability of

limestone, particularly under the dynamic regulatory environment.

Revenue Mix

Shree has three business segments viz. cement, clinker and Power. Cement vertical

contributes ~90%+ of total sales whereas clinker and power vertical contributes ~8-10% of

total sales.

Exhibit: Revenue Mix - (%)

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Cement 89.5% 88.6% 90.4% 92.4% 94% 93.0% 94.3% 94.9%

Clinker 0.7% 1.7% 0.2% 1.6% 2% 1.9% 1.9% 1.9%

Power Sales 9.8% 9.8% 9.4% 6.0% 4% 5.1% 3.7% 3.2%

Source: Company, SKP Research

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 20 of 33

Parameter Cement Power Clinker

Key competitors

Demand drivers

Credit Rating

Source: Company, SKP Research

Key risks

2%

2%

Exhibit : Shree Cement Limited - Business Mix

Geographic presence

Sales grow th (FY14-FY18 – 4-yr CAGR)

Sales forecast (FY18-FY21 – 3-yr CAGR)

4%

3%

Revenue contribution (FY18) 94%

(14%) (12% grow th in volume and 2% grow th in realization CAGR).

(20%) (17% grow th in volume and 3% grow th in realization CAGR).

Capital Allocation

North (~58%), East (~13%), Central (~12%), South (~7%) and UAE (10%).

Shree is India's fourth largest cement manufacturer, w ith ~8% market share, and a total

manufacturing capacity of 41.9 MTPA. It is also the largest cement producer in North India,

enjoying ~24% market share w ith a cement capacity of 24.3 MTPA. The north plant is strategically

located in central Rajasthan from w here it caters to entire Rajastha, NCR and Haryana at

economical logistic cost. Off late, the Company has forayed into eastern markets by setting up an

integrated unit at Chattisgarh and grinding unit at Bihar. It is also venturing into South markets

through a green filed expansion at Gulbarga, Karnataka.

Shree has been prudent in capital allocation. Unlike majority cement players, w herein capital

deployment is for servicing debt/equity, Shree cement’s capital allocation is for putting cement

capacities—w here cash ROCE >30%. Shree is enhanced capacity over FY14-18, more than 2x at

capital cost of $60-90/tonne (peers take anyw here betw een $100 and $160/tonne and 2x Shree’s

delivery time). A shorter payback compounds cash flow s faster, w hich is again deployed in

business to enhance market share w ithout dilution.

Revenue contribution (FY21E)

Market position

Aditya Birla Group, Holcim-Lafarge, Dalmia Bharat and Ramco Cements.

Direct beneficiary of low -cost housing push, higher infrastructure spending, rising industry

consolidation & upcoming elections should spur demand.

Government’s failure to revive infrastructure projects.

A substantial increase in operating cost.

95%

CARE Ratings assigned CARE A1+ rating in view of long and satisfactory track record of the

company.

Clinker capacity

Shree total clinker capacity stands at 23.4 MTPA spread across north (15.4 MTPA), east

(5.2 MTPA) and south (2.8 MTPA). The Company has no plans of adding another clinker

capacity for new grinding units. Though, 5.2 MTPA east clinker capacity with some

debottlenecking will cater to 14 MTPA of grinding capacity.

Overall cement-to-clinker ratio for Shree is at 1.45x while, in the east the ratio is at 2x due to

higher sales of blended cement. The new grinding unit in Pune of 2 mtpa will likely source

clinker from Karnataka plant.

Exhibit: Clinker capacity

Source: Company, SKP Research

15.4

5.2

2.8

23.4

North East South Total Capacity

MTPA

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 21 of 33

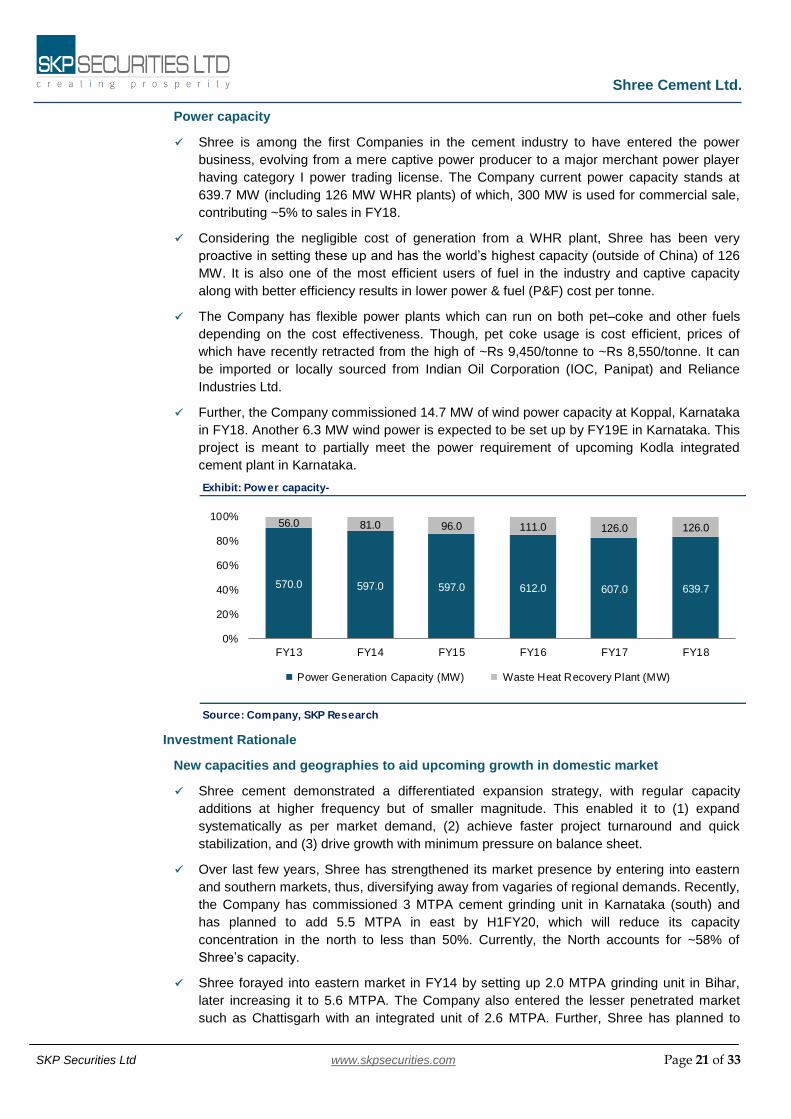

Exhibit: Power capacity-

Source: Company, SKP Research

570.0 597.0 597.0 612.0 607.0 639.7

56.0 81.0 96.0 111.0 126.0 126.0

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16 FY17 FY18

Power Generation Capacity (MW) Waste Heat Recovery Plant (MW)

Power capacity

Shree is among the first Companies in the cement industry to have entered the power

business, evolving from a mere captive power producer to a major merchant power player

having category I power trading license. The Company current power capacity stands at

639.7 MW (including 126 MW WHR plants) of which, 300 MW is used for commercial sale,

contributing ~5% to sales in FY18.

Considering the negligible cost of generation from a WHR plant, Shree has been very

proactive in setting these up and has the world’s highest capacity (outside of China) of 126

MW. It is also one of the most efficient users of fuel in the industry and captive capacity

along with better efficiency results in lower power & fuel (P&F) cost per tonne.

The Company has flexible power plants which can run on both pet–coke and other fuels

depending on the cost effectiveness. Though, pet coke usage is cost efficient, prices of

which have recently retracted from the high of ~Rs 9,450/tonne to ~Rs 8,550/tonne. It can

be imported or locally sourced from Indian Oil Corporation (IOC, Panipat) and Reliance

Industries Ltd.

Further, the Company commissioned 14.7 MW of wind power capacity at Koppal, Karnataka

in FY18. Another 6.3 MW wind power is expected to be set up by FY19E in Karnataka. This

project is meant to partially meet the power requirement of upcoming Kodla integrated

cement plant in Karnataka.

Investment Rationale

New capacities and geographies to aid upcoming growth in domestic market

Shree cement demonstrated a differentiated expansion strategy, with regular capacity

additions at higher frequency but of smaller magnitude. This enabled it to (1) expand

systematically as per market demand, (2) achieve faster project turnaround and quick

stabilization, and (3) drive growth with minimum pressure on balance sheet.

Over last few years, Shree has strengthened its market presence by entering into eastern

and southern markets, thus, diversifying away from vagaries of regional demands. Recently,

the Company has commissioned 3 MTPA cement grinding unit in Karnataka (south) and

has planned to add 5.5 MTPA in east by H1FY20, which will reduce its capacity

concentration in the north to less than 50%. Currently, the North accounts for ~58% of

Shree’s capacity.

Shree forayed into eastern market in FY14 by setting up 2.0 MTPA grinding unit in Bihar,

later increasing it to 5.6 MTPA. The Company also entered the lesser penetrated market

such as Chattisgarh with an integrated unit of 2.6 MTPA. Further, Shree has planned to

Shree Cement Ltd.

SKP Securities Ltd www.skpsecurities.com Page 22 of 33

setup 3 MTPA cement grinding unit in Odisha and 2.5 MTPA cement grinding unit in

Jharkhand at a capex of Rs 4.23 bn and Rs 4.8 bn respectively which is expected to come

on stream by H1FY20. Post expansion, Shree capacity in eastern region will increase from

8.6 MTPA to 14.1 MTPA, and total capacity will stand at 49.4 MTPA including overseas

capacity of 4 MTPA.

Exhibit : Cement capacity at various locations-

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Beawar, Rajasthan 3.0 3.0 3.0 3.6 3.6 3.6 3.6 3.6

Ras, Rajasthan 5.0 7.0 7.0 7.0 7.0 7.0 7.0 7.0

Khushkhera, Rajasthan 3.0 3.0 3.0 3.5 3.5 3.5 3.5 3.5

Suratgarh, Rajasthan 1.2 1.2 1.2 1.8 5.4 5.4 5.4 5.4

Laksar, Uttarakhand 1.8 1.8 1.8 1.8 1.8 1.8 1.8 1.8

Jobner, Rajasthan (Jaipur) 1.5 1.5 1.5 1.5 1.5 1.5 1.5 1.5

Panipat, Haryana — 1.5 1.5 1.5 1.5 1.5 1.5 1.5

North 15.5 19.0 19.0 20.7 24.3 24.3 24.3 24.3

Bulandsahar, Uttar Pradesh — — 2.0 2.0 2.0 2.0 2.0 2.0

Central 0.0 0 2.0 2.0 2.0 2.0 2.0 2.0

Raipur, Chhattisgarh — 2.6 2.6 3.0 3.0 3.0 3.0 3.0

Aurangabad, Bihar 2.0 2.0 2.0 3.6 5.6 5.6 5.6 5.6

Cuttack, Odisha — — — — — — 3.0 3.0

Jharkhand — — — — — — 2.5 2.5

East 2.0 4.6 4.6 6.6 8.6 8.6 14.1 14.1

Karnataka — — — — — 3.0 3.0 3.0

South 0.0 0.0 0.0 0.0 0.0 3.0 3 3

Pune — — — — — — — 2

West 0.0 0.0 0.0 0.0 0.0 0.0 0.0 2.0

UAE 4.0 4.0 4.0

Cement capacity (MTPA) 17.5 23.6 25.6 29.3 34.9 41.9 47.4 49.4

Source: Company, SKP Research

The eastern and southern region is expected to witness sustained demand recovery driven

by rejuvenated housing and infrastructure development, thereby, resulting in better volumes

and realisations, partially absorbing the rising cost pressures. Further, eastern market is