Page 1 of 21 Kaset Thai International Sugar Corporation PCL 29 November 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Page 1 of 21

Kaset Thai International Sugar Corporation PCL

29 November 2016

Page 2 of 21

Agenda

9M-2016 Operating Results

Projects in Progress

Sugar & Bio Industrial Trends

Page 3 of 21

9M-2016 Operating Results

Page 4 of 21

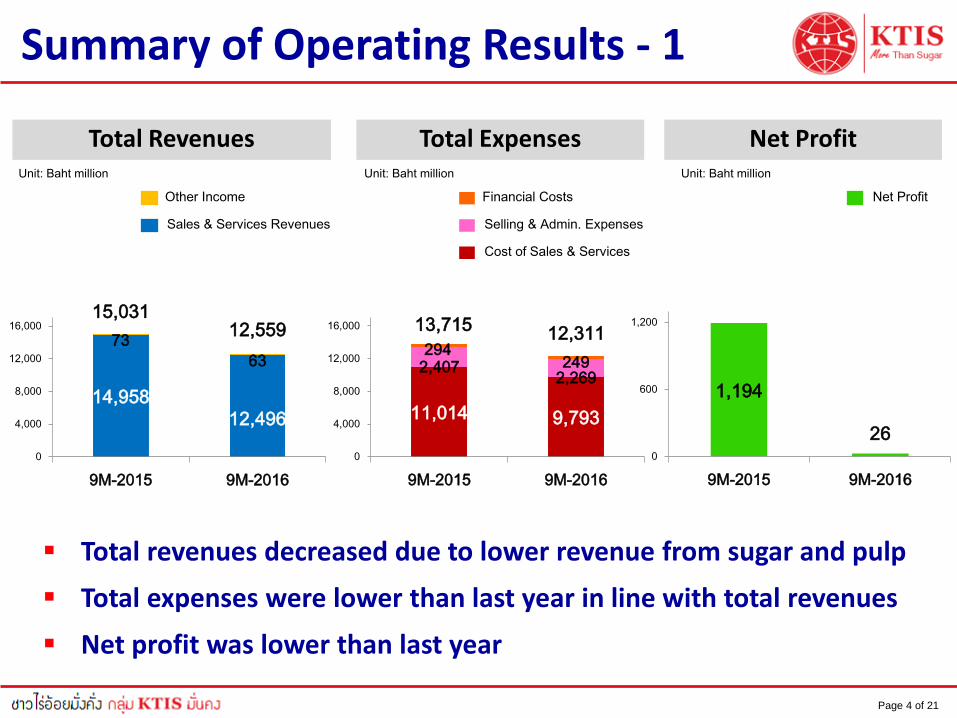

Summary of Operating Results - 1

Financial Costs

Total Revenues Total Expenses Net Profit

Total revenues decreased due to lower revenue from sugar and pulp

Total expenses were lower than last year in line with total revenues

Net profit was lower than last year

Unit: Baht million Unit: Baht million Unit: Baht million

14,958

12,496

73

63

15,03112,559

0

4,000

8,000

12,000

16,000

9M-2015 9M-2016

Other Income

Sales & Services Revenues

Net Profit

11,014 9,793

2,4072,269

294249

13,71512,311

0

4,000

8,000

12,000

16,000

9M-2015 9M-2016

Selling & Admin. Expenses

Cost of Sales & Services

1,194

260

600

1,200

9M-2015 9M-2016

Page 5 of 21

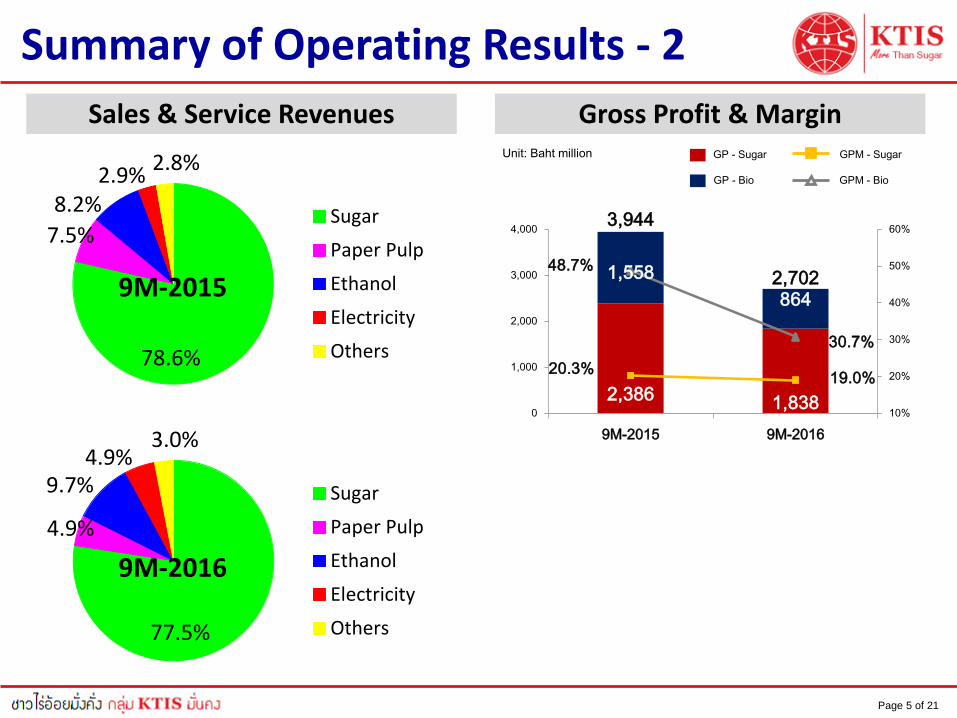

77.5%

4.9%

9.7%4.9%

3.0%

Sugar

Paper Pulp

Ethanol

Electricity

Others

Sales & Service Revenues Gross Profit & Margin

Summary of Operating Results - 2

Unit: Baht million GP - Sugar

GP - Bio

GPM - Sugar

GPM - Bio

2,386 1,838

1,558

864

3,944

2,702

20.3%19.0%

48.7%

30.7%

10%

20%

30%

40%

50%

60%

0

1,000

2,000

3,000

4,000

9M-2015 9M-2016

78.6%

7.5%

8.2%2.9%

2.8%

Sugar

Paper Pulp

Ethanol

Electricity

Others

9M-2015

9M-2016

Page 6 of 21

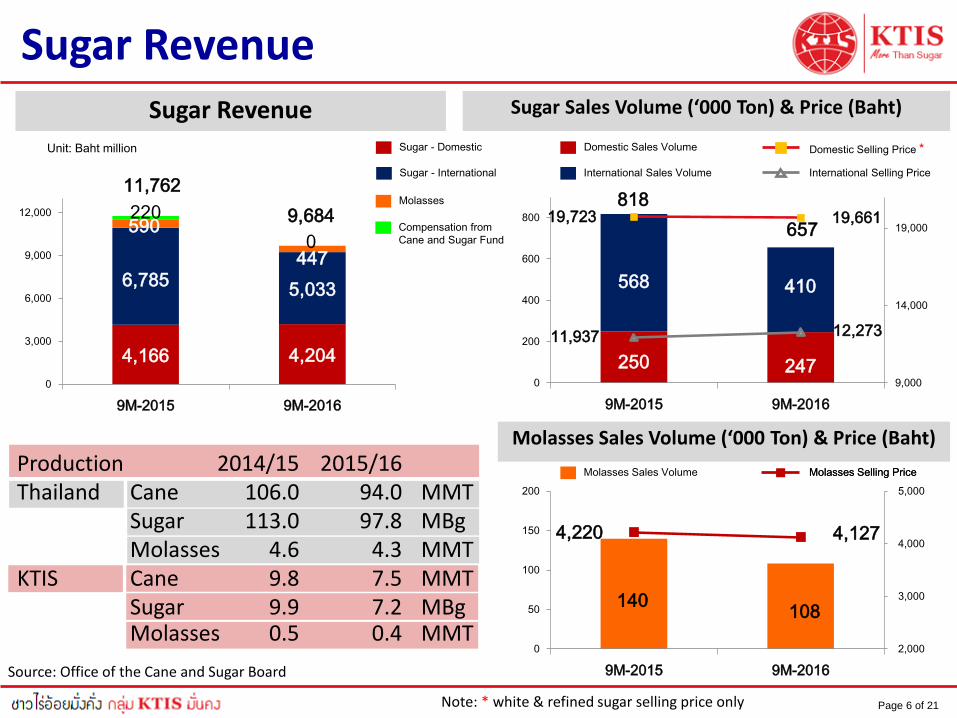

Sugar RevenueSugar Revenue Sugar Sales Volume (‘000 Ton) & Price (Baht)

250 247

568 410

818

65719,723 19,661

11,937 12,273

9,000

14,000

19,000

0

200

400

600

800

9M-2015 9M-2016

Sugar - Domestic

Sugar - International

Domestic Sales Volume

International Sales Volume

Domestic Selling Price *

International Selling Price

Molasses

140108

4,220 4,127

2,000

3,000

4,000

5,000

0

50

100

150

200

9M-2015 9M-2016

Molasses Sales Volume (‘000 Ton) & Price (Baht)

Molasses Sales Volume Molasses Selling Price

Note: * white & refined sugar selling price only

Source: Office of the Cane and Sugar Board

Production 2014/15 2015/16Thailand Cane 106.0 94.0 MMT

Sugar 113.0 97.8 MBgMolasses 4.6 4.3 MMT

KTIS Cane 9.8 7.5 MMTSugar 9.9 7.2 MBgMolasses 0.5 0.4 MMT

4,166 4,204

6,7855,033

590

447

220

0

11,762

9,684

0

3,000

6,000

9,000

12,000

9M-2015 9M-2016

Unit: Baht million

Compensation from

Cane and Sugar Fund

Molasses Selling Price

Page 7 of 21

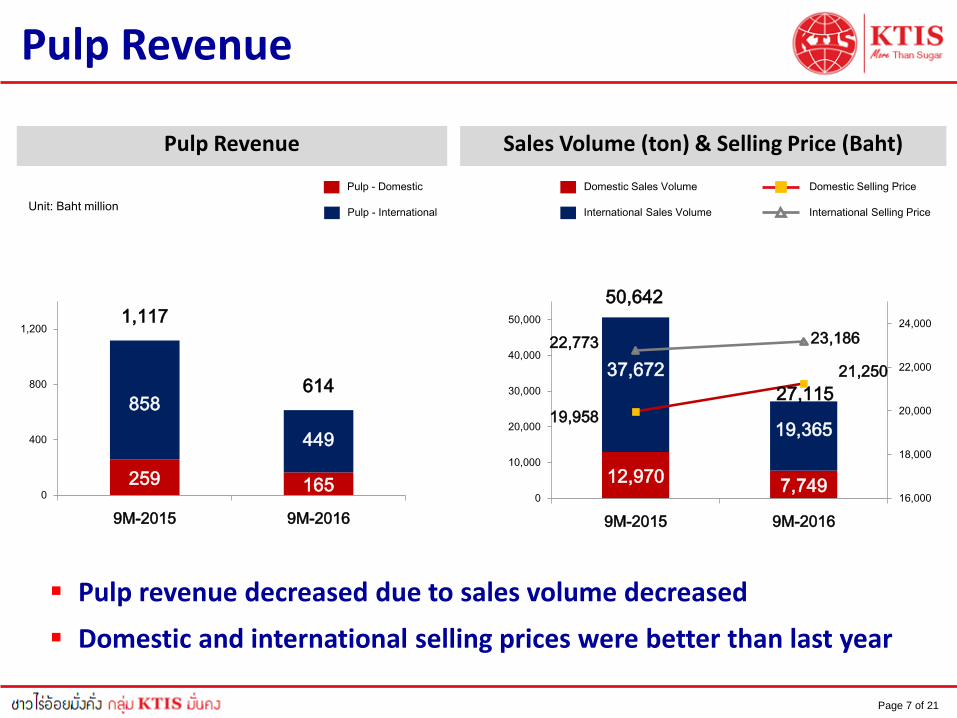

Pulp Revenue

259 165

858

449

1,117

614

0

400

800

1,200

9M-2015 9M-2016

Unit: Baht million

Pulp Revenue

12,9707,749

37,672

19,365

50,642

27,115

19,958

21,250

22,773 23,186

16,000

18,000

20,000

22,000

24,000

0

10,000

20,000

30,000

40,000

50,000

9M-2015 9M-2016

Sales Volume (ton) & Selling Price (Baht)

Pulp revenue decreased due to sales volume decreased

Domestic and international selling prices were better than last year

Pulp - Domestic

Pulp - International

Domestic Sales Volume Domestic Selling Price

International Sales Volume International Selling Price

Page 8 of 21

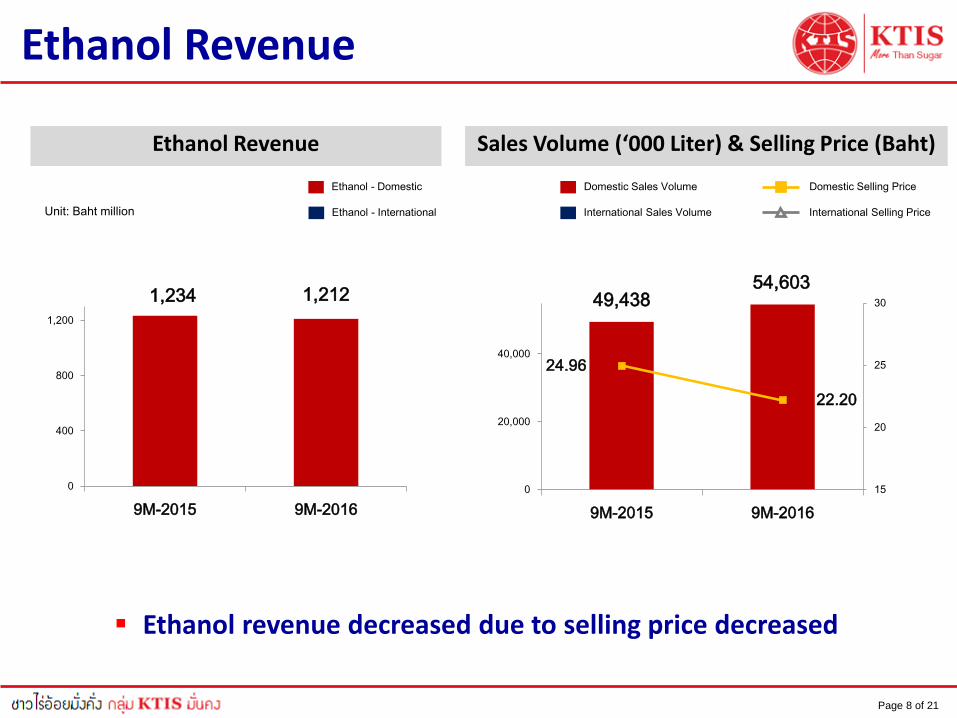

Ethanol Revenue

1,234 1,212

0

400

800

1,200

9M-2015 9M-2016

49,43854,603

24.96

22.20

15

20

25

30

0

20,000

40,000

9M-2015 9M-2016

Unit: Baht million

Ethanol Revenue Sales Volume (‘000 Liter) & Selling Price (Baht)

Ethanol revenue decreased due to selling price decreased

Ethanol - Domestic

Ethanol - International

Domestic Sales Volume Domestic Selling Price

International Sales Volume International Selling Price

Page 9 of 21

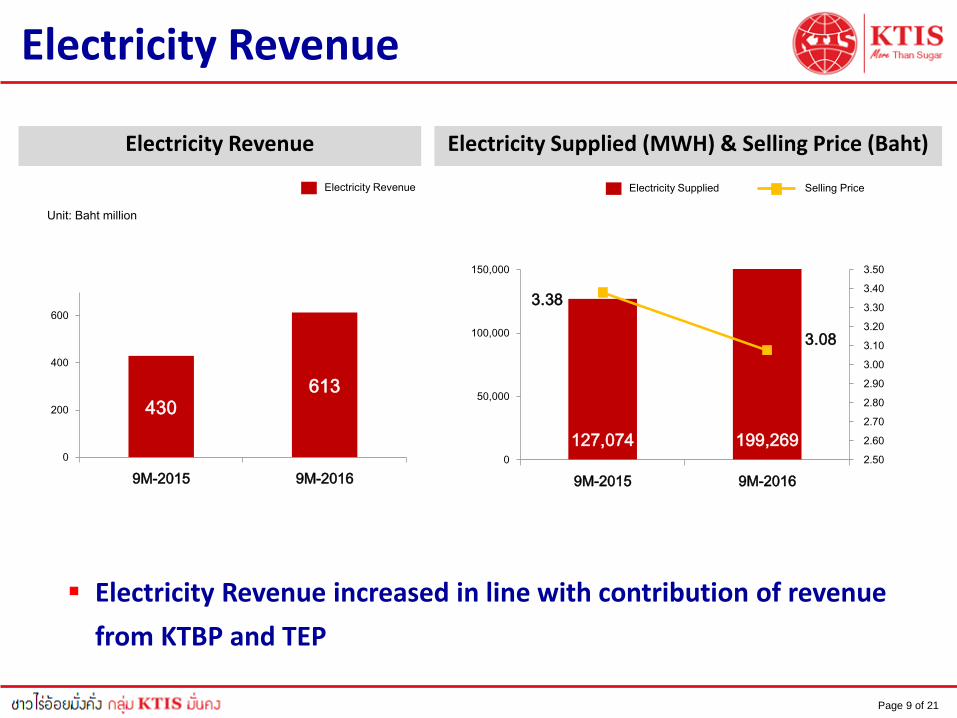

Electricity Revenue

430613

0

200

400

600

9M-2015 9M-2016

Unit: Baht million

Electricity Revenue

127,074 199,269

3.38

3.08

2.50

2.60

2.70

2.80

2.90

3.00

3.10

3.20

3.30

3.40

3.50

0

50,000

100,000

150,000

9M-2015 9M-2016

Electricity Supplied (MWH) & Selling Price (Baht)

Electricity Supplied Selling Price

Electricity Revenue increased in line with contribution of revenue

from KTBP and TEP

Electricity Revenue

Page 10 of 21

Projects in Progress

Page 11 of 21

Projects in Progress

Biomass power plants (RPBP 50MW)

Page 12 of 21

Sugar & Bio Industry Trends

Page 13 of 21

Positive Factors for Sugar

World Supply / Demand for 2016/17 are expected to be deficit

around 4 million tons.

With steady consumption growth, China, India and ASEAN region

continue to be in deficit, which leads to competitive advantages

of Thai sugar.

Although market consensus for Brazilian crop is still for 35 million

tons, mills are closing early. If production falls below this level,

trade balance deficits become bigger.

Thai regulation of the profit sharing system allows the

sustainable earning for both farmers and millers.

AFTA give better access and competitiveness to ASEAN countries.

Page 14 of 21

Negative Factors for Sugar

Global deficit forecast has been revised downwards due to

improved production prospects for EU, Mexico, and US, however

still deficit.

The fund position looks vulnerable. Later Oct saw the funds

reduce their net long position. A large scale sell-off remains a

threat to future market.

Chinese government has announced that it will release the

350,000 tons of stock. And market expects that the releasing

amount might be bigger, leading to less import demand.

Deregulation in EU sugar industry will encourage refined sugar

exports from late 2017.

Strong US dollar from US policy.

Page 15 of 21

World Sugar Price

Source: Reuters

Page 16 of 21

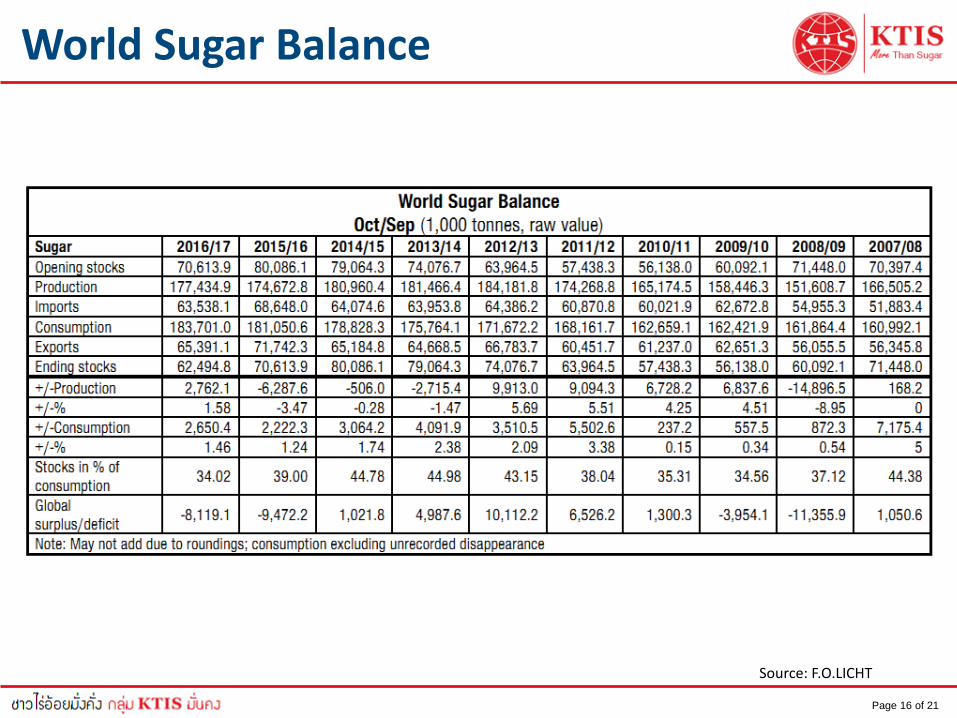

Source: F.O.LICHT

World Sugar Balance

Page 17 of 21

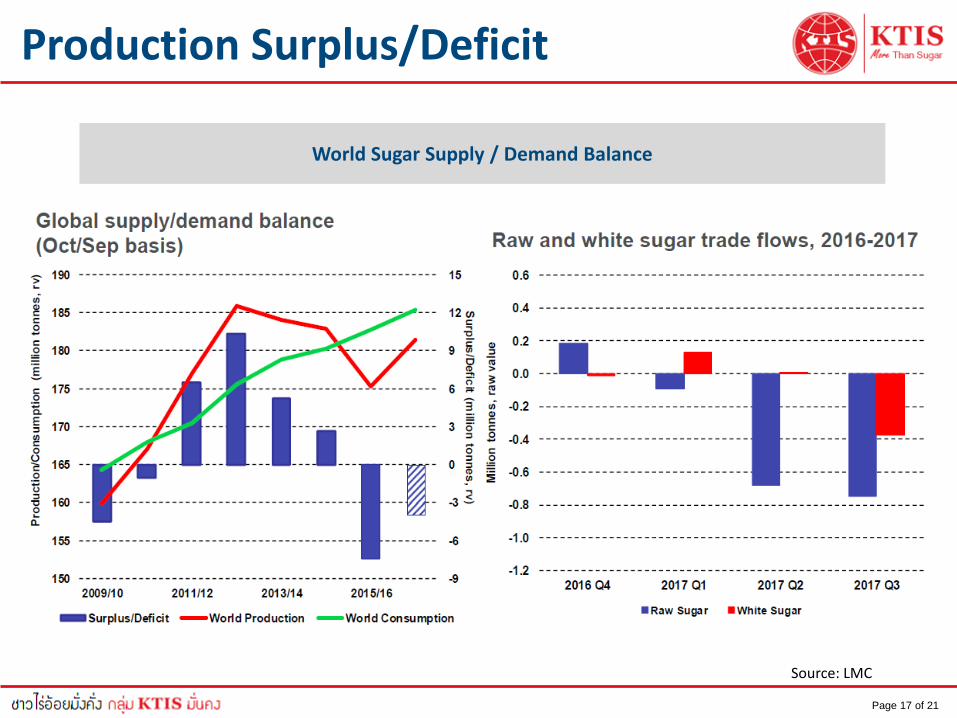

Source: LMC

Production Surplus/Deficit

World Sugar Supply / Demand Balance

Page 18 of 21

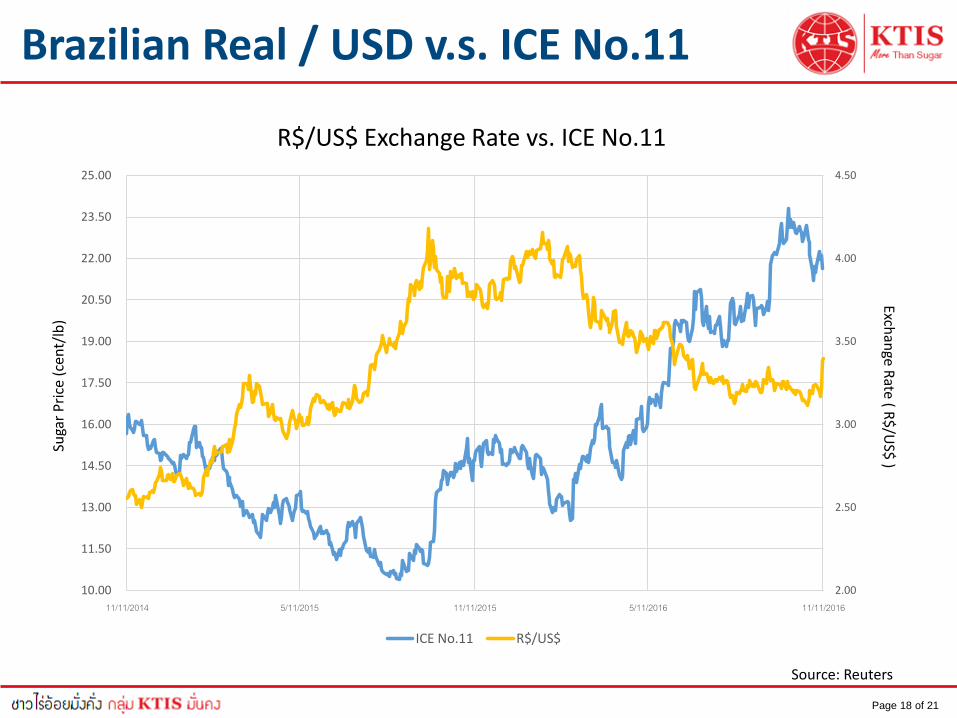

Brazilian Real / USD v.s. ICE No.11

Source: Reuters

2.00

2.50

3.00

3.50

4.00

4.50

10.00

11.50

13.00

14.50

16.00

17.50

19.00

20.50

22.00

23.50

25.00

11/11/2014 5/11/2015 11/11/2015 5/11/2016 11/11/2016

Exchan

ge Rate ( R

$/U

S$ )

Suga

r P

rice

(ce

nt/

lb)

R$/US$ Exchange Rate vs. ICE No.11

ICE No.11 R$/US$

Page 19 of 21

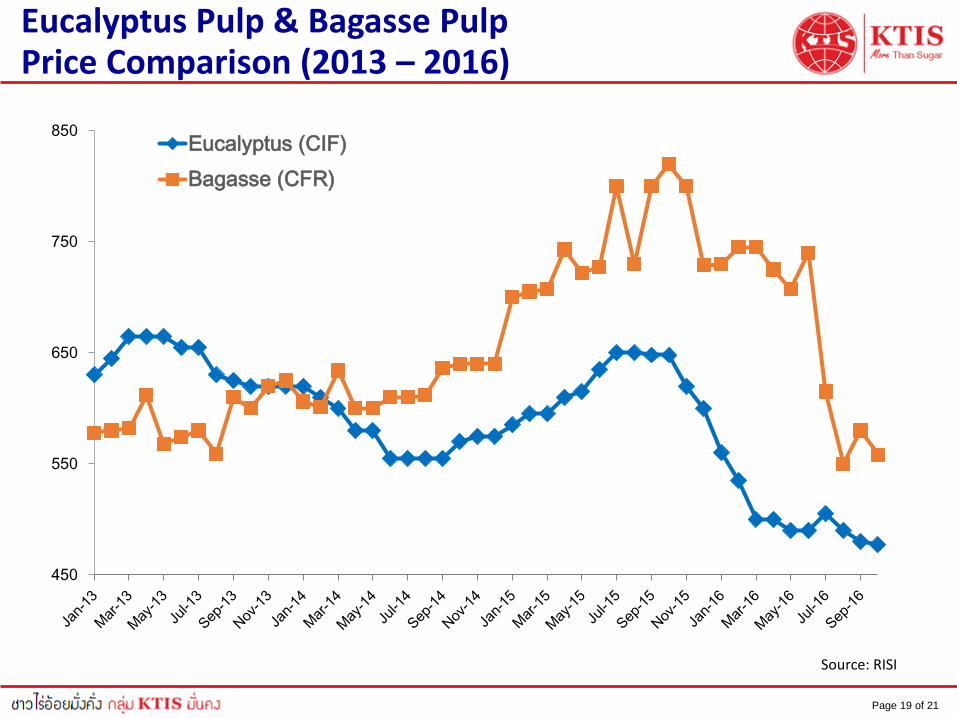

Eucalyptus Pulp & Bagasse PulpPrice Comparison (2013 – 2016)

450

550

650

750

850Eucalyptus (CIF)

Bagasse (CFR)

Source: RISI

Page 20 of 21

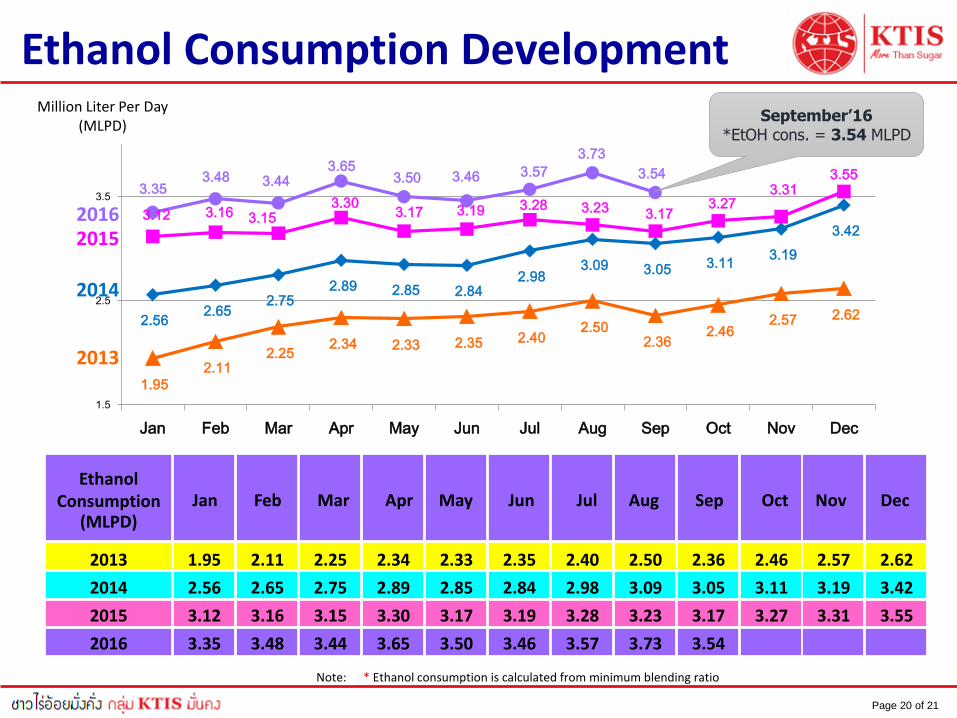

EthanolConsumption

(MLPD)Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

3.353.48 3.44

3.653.50 3.46 3.57

3.73

3.54

3.12 3.16 3.15 3.30

3.17 3.19 3.28 3.23 3.17 3.27

3.31 3.55

2.56 2.65

2.75 2.89 2.85 2.84

2.98 3.09 3.05 3.11

3.19

3.42

1.95

2.11 2.25

2.34 2.33 2.35 2.40 2.50

2.36 2.46

2.57 2.62

1.5

2.5

3.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Million Liter Per Day(MLPD)

2013

2014

2015

Ethanol Consumption Development

2013

2014

2015

2016

1.95

2.56

3.12

3.35

2.11

2.65

3.16

3.48

2.25

2.75

3.15

3.44

2.34

2.89

3.30

3.65

2.33

2.85

3.17

3.50

2.40

2.98

3.28

3.57

2.50

3.09

3.23

3.73

2.36

3.05

3.17

3.54

2.46

3.11

3.27

2.57

3.19

3.31

2.62

3.42

3.55

2.35

2.84

3.19

3.46

2016

Note: * Ethanol consumption is calculated from minimum blending ratio

September’16*EtOH cons. = 3.54 MLPD

Page 21 of 21

Important Notice

This presentation is confidential. This presentation is not a prospectus. This presentation does not constitute or form part of any offer

for sales or solicitation of any offer to buy any securities nor shall it or any part of it form the basis of or be relied on in connection

with any contract or commitment whatsoever.

This presentation has been prepared for the purpose of providing certain individuals with business, financial and other information

concerning Kaset Thai International Sugar Corporation Company Limited (“KTIS”)

The information contained in this presentation is intended solely for your personal reference only. If you are not an intended

recipient, you must not read, disclose, copy, circulate, retain, distribute or take any action in reliance upon this material. This

presentation is not intended to substitute your own analysis and investigation, and should not be considered a recommendation to

any recipient of this presentation. Some statements contained herein are forward-looking statements identified by the use of

forward- looking terminology such as “may” , “will” , “expect” , “anticipate”, “intend” , “estimate” , “continue”, “plan” or other similar

words, which are subject to various risks and uncertainties. These statements include statements with respect to KTIS’s corporate

plans, strategies and beliefs and other statements that are not historical facts. This presentation is prepared based on the

assumptions and beliefs of KTIS’s management in light of the information currently available to KTIS involving risks and uncertainties

which may cause the actual results, performance or achievements to be materially different from any future results, performance or

achievements expressed or implied by such forward-looking statements. Nothing in this presentation is, or shall be relied on as

promise or representation of KTIS as to the future.

For more information, contact : [email protected]

Related Documents