A PROJECT REPORT On “ANALYSIS OF HDFC LOANS IN BAREILLY “ For HDFC BANK Ltd. SUMMER TRAINING PROJECT UNDER THE GUIDANCE OF Akrash Mehrotra Dr. Sankalp Srivastava (Relationship Manager) (Assistant Director) HDFC BANK LTD., BAREILLY INSTITUTE OF PRODUCTIVITY & MANAGENMENT, Lucknow SUBMITTED IN PARTIAL FULFILLMENT FOR THE AWARD OF POST GRADUATION DIPLOMA IN MANAGEMENT BY KANIKA TANDON PGDM (F/T) L209021 INSTITUTE OF PRODUCTIVITY & MANAGEMENT LUCKNOW 1 Institute of Productivity and Management

Kanika tandon hdfc_bank_ltd._summer_internship_project...

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A

PROJECT REPORT

On

“ANALYSIS OF HDFC LOANS IN BAREILLY “

For

HDFC BANK Ltd.

SUMMER TRAINING PROJECT

UNDER THE GUIDANCE OF

Akrash Mehrotra Dr. Sankalp Srivastava

(Relationship Manager) (Assistant Director)

HDFC BANK LTD., BAREILLY INSTITUTE OF PRODUCTIVITY

& MANAGENMENT, Lucknow

SUBMITTED IN PARTIAL FULFILLMENT FOR THE AWARD OF POST GRADUATION DIPLOMA IN MANAGEMENT

BY

KANIKA TANDON

PGDM (F/T)

L209021

INSTITUTE OF PRODUCTIVITY & MANAGEMENT

LUCKNOW

1Institute of Productivity and Management

2009-2011

ACKNOWLEDGEMENT

At the successful completion of summer internship program, I wish to express my true regards

to individuals who supported and directed me throughout this internship.

First of all I would like to give my gratitude and sincere regards and a note of thank to Akarsh

Mehrotra (Relationship Manager, HDFC Bank Ltd., Bareilly) for giving me this

opportunity and selecting me as summer trainee in this esteemed organization.

I would like to express my deep gratitude and regards for his valuable guidance and support

without which completion of this report would not be possible.

I would also like to give special thanks to Mr. Mukul Saxena, Mrs. Shweta Arora, (HDFC

Bank Ltd., Bareilly) for giving me their valuable time, support and inputs that helped me at

every step in this project.

I take the opportunity to acknowledge and express sincere thanks to Dr. Sankalp Srivastava

(Assistant Director, IPM Lucknow) for being constant source of inspiration to me, showing all

the patience and abundant encouragement throughout the project duration.

Lastly, I would like to thank all my friends for their support and help.

Kanika Tandon

2Institute of Productivity and Management

Declaration

I hereby declare that this Project Report entitled “ANALYSIS OF HDFC LOANS IN

BAREILLY “in HDFC BANK LTD., BAREILLY submitted in the partial fulfillment of the

requirement of Post Graduate Diploma In Management (PGDM) of INSTITUTE OF

PRODUCTIVITY & MANAGEMET, LUCKNOW is based on primary & secondary data

found by me in various departments, books, magazines and websites & collected by me in under

guidance of Akarsh Mehrotra.

DATE: KANIKATANDON

PGDM (Finance)

3Institute of Productivity and Management

SECTION A

4Institute of Productivity and Management

List of Contents

Section A

Industry and Company

Profile………………………………................2

Industry Background…………………………………..

……………...18

Competitive Situation……………………………………..….............23

Company

background……………………………………...................25

Organizational

Chart………………………………………………….30

Product range…………………………………………………………

31

Financial position of the company……………………………...........59

Section B

The project Profile……………………………………………………….62

Why this project was undertaken/problem environment/the problem being

faced…………………………………………………………………..........6

3

What does company expect to do by solving the problem? ........................64

5Institute of Productivity and Management

Section C

The project – background and

methodology……………………………….67

Research problem…………………………………………………………67

Research objective and related sub

objectives……………………..............67

Information requirements – in detail and source of

information…………...68

Choice of research design…………………………………………………68

Research instrument used- details. Why?

………………………….............69

Sampling techniques used and sample size. Why?

………………………..72

Field work – method used for data collection

……………………………..73

Analytical tool

used………………………………………………………...74

Limitations……………………………………………………….

…...........74

Section D

Analysis & Interpretations …………………………….………..………76

Conclusions……………………………………………………………….10

1

Suggestions………………………………………………………………..10

2

6Institute of Productivity and Management

• Questionnaire

• Annexure

• Bibliography

Industry and Company Profile

Industry Profile

Introduction on Bank

Origin of the word

7Institute of Productivity and Management

The name bank derives from the Italian word banco "desk/bench", used during the Renaissance

by Jewish Florentine bankers, who used to make their transactions above a desk covered by a

green tablecloth. However, there are traces of banking activity even in times ancient , which

indicates that the word 'bank' might not necessarily come from the word 'banco'.

Banks date back to ancient times. During the 3rd century AD, banks in Persia and other

territories in the Persian Sassanid Empire issued letters of credit known as Ṣakks. Muslim

traders are known to have used the cheque or Sakks system since the time of Harun al-Rashid

(9th century) of the Abbasid Caliphate. In the 9th century, a Muslim businessman could cash an

early form of the cheque in China drawn on sources in Baghdad a tradition that was

significantly strengthened in the 13th and 14th centuries, during the Mongol Empire. Indeed,

fragments found in the Cairo Geniza indicate that in the 12th century cheques remarkably

similar to our own were in use, only smaller to save costs on the paper. They contain a sum to

be paid and then the order "May so and so pay the bearer such and such an amount". The date

and name of the issuer are also apparent. The earliest known state deposit bank, Banco di San

Giorgio (Bank of St. George), was founded in 1407 at Genoa, Italy. Banking in the modern

sense of the word can be traced to medieval and early Renaissance Italy, to the rich cities in the

north like Florence, Venice and Genoa. The Bardi and Peruzzi families were dominated banking

in 14th century Florence, establishing branches in many other parts of Europe. Perhaps the most

famous Italian bank was the Medici bank, set up by Giovanni Medici in 1397.

Meaning of bank

A bank is a financial intermediary that accepts deposits and channels those deposits into

lending activities. Banks are a fundamental component of the financial system, and are also

active players in financial markets. The essential role of a bank is to connect those who have

capital (such as investors or depositors), with those who seek capital (such as individuals

wanting a loan, or businesses wanting to grow).

8Institute of Productivity and Management

Banking is generally a highly regulated industry, and government restrictions on financial

activities by banks have varied over time and location. The current set of global standards is

called Basel II. In some countries such as Germany, banks have historically owned major stakes

in industrial corporations while in other countries such as the United States banks are prohibited

from owning non-financial companies. In Japan, banks are usually the nexus of a cross-share

holding entity known as the keiretsu. In France, banc assurance is prevalent, as most banks offer

insurance services (and now real estate services) to their clients. The most recent trend has been

the advance of universal banks, which attempt to offer their customers the full spectrum of

financial services under the one roof.

The oldest bank still in existence is Monte dei Paschi di Siena, headquartered in Siena, Italy,

which has been operating continuously since 1472.

Definition

The definition of a bank varies from country to country.

Under English common law, a banker is defined as a person who carries on the business of

banking, which is specified as:

• conducting current accounts for his customers

• paying cheques drawn on him, and

• Collecting cheques for his customers.

In most English common law jurisdictions there is a Bills of Exchange Act that codifies the law

in relation to negotiable instruments, including cheques, and this Act contains a statutory

definition of the term banker: banker includes a body of persons, whether incorporated or not,

who carry on the business of banking' (Section 2, Interpretation). Although this definition seems

circular, it is actually functional, because it ensures that the legal basis for bank transactions

such as cheques does not depend on how the bank is organized or regulated.

The business of banking is in many English common law countries not defined by statute but by

common law, the definition above. In other English common law jurisdictions there are

9Institute of Productivity and Management

statutory definitions of the business of banking or banking business. When looking at these

definitions it is important to keep in minds that they are defining the business of banking for the

purposes of the legislation, and not necessarily in general. In particular, most of the definitions

are from legislation that has the purposes of entry regulating and supervising banks rather than

regulating the actual business of banking. However, in many cases the statutory definition

closely mirrors the common law one. Examples of statutory definitions:

• "banking business" means the business of receiving money on current or deposit

account, paying and collecting cheques drawn by or paid in by customers, the making of

advances to customers, and includes such other business as the Authority may prescribe

for the purposes of this Act; (Banking Act (Singapore), Section 2, Interpretation).

• "banking business" means the business of either or both of the following:

1. receiving from the general public money on current, deposit, savings or other similar

account repayable on demand or within less than [3 months] ... or with a period of call or

notice of less than that period;

2. Paying or collecting cheques drawn by or paid in by customers.

Since the advent of EFTPOS (Electronic Funds Transfer at Point Of Sale), direct credit, direct

debit and internet banking, the cheque has lost its primacy in most banking systems as a

payment instrument. This has led legal theorists to suggest that the cheque based definition

should be broadened to include financial institutions that conduct current accounts for customers

and enable customers to pay and be paid by third parties, even if they do not pay and collect

cheques.

Standard activities

Banks act as payment agents by conducting checking or current accounts for customers, paying

cheques drawn by customers on the bank, and collecting cheques deposited to customers'

current accounts. Banks also enable customer payments via other payment methods such as

telegraphic transfer, EFTPOS, and ATM.

10Institute of Productivity and Management

Banks borrow money by accepting funds deposited on current accounts, by accepting term

deposits, and by issuing debt securities such as banknotes and bonds. Banks lend money by

making advances to customers on current accounts, by making installment loans, and by

investing in marketable debt securities and other forms of money lending.

Banks borrow most funds from households and non-financial businesses, and lend most funds to

households and non-financial businesses, but non-bank lenders provide a significant and in

many cases adequate substitute for bank loans, and money market funds, cash management

trusts and other non-bank financial institutions in many cases provide an adequate substitute to

banks for lending savings to.

Wider commercial role

The commercial role of banks is not limited to banking, and includes:

• issue of banknotes (promissory notes issued by a banker and payable to bearer on

demand)

• processing of payments by way of telegraphic transfer, EFTPOS, internet banking or

other means

• issuing bank drafts and bank cheques

• accepting money on term deposit

• lending money by way of overdraft, installment loan or otherwise

• providing documentary and standby letters of credit (trade finance), guarantees,

performance bonds, securities underwriting commitments and other forms of off-balance

sheet exposures

• safekeeping of documents and other items in safe deposit boxes

• currency exchange

• acting as a 'financial supermarket' for the sale, distribution or brokerage, with or without

advice, of insurance, unit trusts and similar financial product

11Institute of Productivity and Management

Channels

Banks offer many different channels to access their banking and other services:

• A branch, banking centre or financial centre is a retail location where a bank or financial

institution offers a wide array of face-to-face service to its customers.

• ATM is a computerized telecommunications device that provides a financial institution's

customers a method of financial transactions in a public space without the need for a

human clerk or bank teller. Most banks now have more ATMs than branches, and ATMs

are providing a wider range of services to a wider range of users. For example in Hong

Kong, most ATMs enable anyone to deposit cash to any customer of the bank's account

by feeding in the notes and entering the account number to be credited. Also, most

ATMs enable card holders from other banks to get their account balance and withdraw

cash, even if the card is issued by a foreign bank.

• Mail is part of the postal system which itself is a system wherein written documents

typically enclosed in envelopes, and also small packages containing other matter, are

delivered to destinations around the world. This can be used to deposit cheques and to

send orders to the bank to pay money to third parties. Banks also normally use mail to

deliver periodic account statements to customers.

• Telephone banking is a service provided by a financial institution which allows its

customers to perform transactions over the telephone. This normally includes bill

payments for bills from major billers (e.g. for electricity).

• Online banking is a term used for performing transactions, payments etc. over the

Internet through a bank, credit union or building society's secure website.

• Mobile banking is a method of using one's mobile phone to conduct simple banking

transactions by remotely linking into a banking network.

Products:-

12Institute of Productivity and Management

Retail

• Savings account

• Cheque account

• Credit card

• Home loan

• Personal loan

• Business loan

• Insurance advisor

• Mutual fund

Wholesale

• Project finance

• Capital raising (Equity / Debt / Hybrids)

• Risk management (FX, interest rates, commodities)

Banks in the economy

Economic functions

The economic functions of banks include:

1. Issue of money, in the form of banknotes and current accounts subject to cheque or

payment at the customer's order. These claims on banks can act as money because they

are negotiable and/or repayable on demand, and hence valued at par. They are

effectively transferable by mere delivery, in the case of banknotes, or by drawing a

cheque that the payee may bank or cash.

13Institute of Productivity and Management

2. Netting and settlement of payments – banks act as both collection and paying agents for

customers, participating in interbank clearing and settlement systems to collect, present,

be presented with, and pay payment instruments. This enables banks to economies on

reserves held for settlement of payments, since inward and outward payments offset each

other. It also enables the offsetting of payment flows between geographical areas,

reducing the cost of settlement between them.

3. Credit intermediation – banks borrow and lend back-to-back on their own account as

middle men.

4. Credit quality improvement – banks lend money to ordinary commercial and personal

borrowers (ordinary credit quality), but are high quality borrowers. The improvement

comes from diversification of the bank's assets and capital which provides a buffer to

absorb losses without defaulting on its obligations. However, banknotes and deposits are

generally unsecured; if the bank gets into difficulty and pledges assets as security, to rise

the funding it needs to continue to operate, this puts the note holders and depositors in an

economically subordinated position.

5. Maturity transformation – banks borrow more on demand debt and short term debt, but

provide more long term loans. In other words, they borrow short and lend long. With a

stronger credit quality than most other borrowers, banks can do this by aggregating

issues (e.g. accepting deposits and issuing banknotes) and redemptions (e.g. withdrawals

and redemptions of banknotes), maintaining reserves of cash, investing in marketable

securities that can be readily converted to cash if needed, and raising replacement

funding as needed from various sources (e.g. wholesale cash markets and securities

markets)

Types of retail banks

• Commercial bank : the term used for a normal bank to distinguish it from an investment

bank. After the Great Depression, the U.S. Congress required that banks only engage in

banking activities, whereas investment banks were limited to capital market activities.

Since the two no longer have to be under separate ownership, some use the term

14Institute of Productivity and Management

"commercial bank" to refer to a bank or a division of a bank that mostly deals with

deposits and loans from corporations or large businesses.

• Community banks : locally operated financial institutions that empower employees to

make local decisions to serve their customers and the partners.

• Community development banks : regulated banks that provide financial services and

credit to under-served markets or populations.

• Postal savings banks : savings banks associated with national postal systems.

• Private Banks : banks that manage the assets of high net worth individuals.

• Offshore banks : banks located in jurisdictions with low taxation and regulation. Many

offshore banks are essentially private banks.

• Savings bank : in Europe, savings banks take their roots in the 19th or sometimes even

18th century. Their original objective was to provide easily accessible savings products

to all strata of the population. In some countries, savings banks were created on public

initiative; in others, socially committed individuals created foundations to put in place

the necessary infrastructure. Nowadays, European savings banks have kept their focus

on retail banking: payments, savings products, credits and insurances for individuals or

small and medium-sized enterprises. Apart from this retail focus, they also differ from

commercial banks by their broadly decentralized distribution network, providing local

and regional outreach—and by their socially responsible approach to business and

society.

• Building societies and Landesbanks: institutions that conduct retail banking.

• Ethical banks : banks that prioritize the transparency of all operations and make only

what they consider to be socially-responsible investments.

Types of investment banks

15Institute of Productivity and Management

• Investment banks "underwrite" (guarantee the sale of) stock and bond issues, trade for

their own accounts, make markets, and advise corporations on capital market activities

such as mergers and acquisitions.

• Merchant banks were traditionally banks which engaged in trade finance. The modern

definition, however, refers to banks which provide capital to firms in the form of shares

rather than loans. Unlike venture capital firms, they tend not to invest in new companies.

Both combined

• Universal banks , more commonly known as financial services companies, engage in

several of these activities. These big banks are much diversified groups that, among

other services, also distribute insurance— hence the term banc assurance, a portmanteau

word combining "banque or bank" and "assurance", signifying that both banking and

insurance are provided by the same corporate entity.

Other types of banks

• Central banks are normally government-owned and charged with quasi-regulatory

responsibilities, such as supervising commercial banks, or controlling the cash interest

rate. They generally provide liquidity to the banking system and act as the lender of last

resort in event of a crisis.

• Islamic banks adhere to the concepts of Islamic law. This form of banking revolves

around several well-established principles based on Islamic canons. All banking

activities must avoid interest, a concept that is forbidden in Islam. Instead, the bank

earns profit (markup) and fees on the financing facilities that it extends to customers.

Retail Banking Products

1. Savings account

Savings accounts are accounts maintained by retail financial institutions that pay interest but

can not be used directly as money ( for example, by writing a cheque). These accounts let

customers set aside a portion of their liquid assets while earning a monetary return.

16Institute of Productivity and Management

2. Current account

Current account or cheque account is a deposit account held at a bank or other financial

institution, for the purpose of securely and quickly providing frequent access to funds on

demand, through a variety of different channels. Because money is available on demand these

accounts are also referred to as demand accounts or demand deposit accounts. Transactional

accounts are meant neither for the purpose of earning interest nor for the purpose of savings, but

for convenience of the business or personal client; hence do they tend not to bear interest.

Instead, a customer can deposit or withdraw any amount of money any number of times, subject

to availability of funds.

3. Credit card

A credit card is part of a system of payments named after the small plastic card issued to users

of the system. It is a card entitling its holder to buy goods and services based on the holder's

promise to pay for these goods and services. The issuer of the card grants a line of credit to the

consumer (or the user) from which the user can borrow money for payment to a merchant or as

a cash advance to the user. Usage of the term "credit card" to imply a credit card account is a

metonym. A credit card is different from a charge card, where a charge card requires the balance

to be paid in full each month. In contrast, credit cards allow the consumers to 'revolve' their

balance, at the cost of having interest charged. Most credit cards are issued by local banks or

credit unions, and are the shape and size specified by the ISO/IEC 7810 standard as ID-1. This

is defined as 85.60 × 53.98 mm (33/8 × 21/8 in) in size

Fees charged to customers

The major fees are for:

• Late payments or overdue payments

• Charges that result in exceeding the credit limit on the card (whether done deliberately or

by mistake), called over limit fees

17Institute of Productivity and Management

• Returned cheque fees or payment processing fees (e.g. phone payment fee)

• Cash advances and convenience cheques (often 3% of the amount)

• Transactions in a foreign currency (as much as 3% of the amount). A few financial

institutions do not charge a fee for this.

• Membership fees (annual or monthly), sometimes a percentage of the credit limit.

• Exchange rate loading fees (these may sometimes not be reported on the customer's

statement, even when they are applied).

4. Mortgage

A mortgage is a security interest in real property held by a lender as a security for a debt,

usually a loan of money. While a mortgage in itself is not a debt, it is the lender's security for a

debt. It is a transfer of an interest in land (or the equivalent) from the owner to the mortgage

lender, on the condition that this interest will be returned to the owner when the terms of the

mortgage have been satisfied or performed. In other words, the mortgage is a security for the

loan that the lender makes to the borrower. The word comes from the Old French word for

"dead pledge," apparently meaning that the pledge ends (dies) either when the obligation is

fulfilled or the property is taken through foreclosure. In most jurisdictions mortgages are

strongly associated with loans secured on real estate rather than on other property (such as

ships) and in some jurisdictions only land may be mortgaged. A mortgage is the standard

method by which individuals and businesses can purchase real estate without the need to pay the

full value immediately from their own resources. See mortgage loan for residential mortgage

lending, and commercial mortgage for lending against commercial property.

• Participants and variant terminology

Legal systems in different countries, while having some concepts in common, employ different

terminology. However, in general, a mortgage of property involves the following parties.

Mortgage lender-

18Institute of Productivity and Management

A mortgage lender is an investor that lends money secured by a mortgage on real estate. In

today's world, most lenders sell the loans they write on the secondary mortgage market. When

they sell the mortgage, they earn revenue called Service Release Premium. Typically, the

purpose of the loan is for the borrower to purchase that same real estate. The borrower, known

as the mortgagor, gives the mortgage to the lender, known as the mortgagee. As the mortgagee,

the lender has the right to sell the property to pay off the loan if the borrower fails to pay.

5. Unsecured Loan

An unsecured loan is a loan that is not backed by collateral. Also known as a signature loan or

personal loan. Unsecured loans are based solely upon the borrower's credit rating. As a result,

they are often much more difficult to get than a secured loan, which also factors in the

borrower's income. An unsecured loan is considered much cheaper and carries less risk to the

borrower. However, when an unsecured loan is granted, it does not necessarily have to be

based on a credit score. For example, if your friend lends you money without any collateral,

meaning something of worth that can be repossessed if the loan isn't repaid, then your credit

score has zero to do with it, but rather the value of your friendship is at stake. Therefore the real

meaning of an unsecured loan is that it is not backed by any object of value and is lent to you

based on your good name. For financial institutional purposes, they may want to look at your

credit score because they are not your friend and it is strictly a business transaction, therefore

your good name may be associated with your historical payment history on prior debt, reflecting

in your credit score.

• Types of unsecured loans

There are three types of unsecured loans.

• First there is a personal unsecured loan, meaning a loan that you individually are

responsible for the repayment of.

• Second is an unsecured business loan which leaves the business responsible for the

repayment.

19Institute of Productivity and Management

• Finally there is an unsecured business loan with a personal guarantee. With the latter,

although the borrower is the business, you as an individual will be the payer of last resort

if the business defaults on the loan

6. Mutual Fund

A Mutual Fund is a trust that pools the savings of a number of investors who share a

common financial goal. The money thus collected is then invested in capital market

instruments such as shares, debentures and other securities. The income earned through

these investments and the capital appreciation realized is shared by its unit holders in

proportion to the number of units owned by them. Thus a Mutual Fund is the most suitable

investment for the common man as it offers an opportunity to invest in a diversified,

professionally managed basket of securities at a relatively low-cost. The flow chart below

describes broadly the working of a mutual fund:

Mutual fund is a trust that pools money from a group of investors (sharing common financial

goals) and invests the money thus collected into asset classes that match the stated

investment objectives of the scheme. Since the stated investment objectives of a mutual fund

scheme generally form the basis for an investor's decision to contribute money to the pool, a

mutual fund can not deviate from its stated objectives at any point of time.

Wholesale Banking Products

I. Project financing

20Institute of Productivity and Management

Project finance is the long term financing of infrastructure and industrial projects based upon the

projected cash flows of the project rather than the balance sheets of the project sponsors.

Usually, a project financing structure involves a number of equity investors, known as sponsors,

as well as a syndicate of banks that provide loans to the operation. The loans are most

commonly non-recourse loans, which are secured by the project assets and paid entirely from

project cash flow, rather than from the general assets or creditworthiness of the project sponsors,

a decision in part supported by financial modeling. The financing is typically secured by all of

the project assets, including the revenue-producing contracts. Project lenders are given a lien on

all of these assets, and are able to assume control of a project if the project company has

difficulties complying with the loan terms. Generally, a special purpose entity is created for

each project, thereby shielding other assets owned by a project sponsor from the detrimental

effects of a project failure. As a special purpose entity, the project company has no assets other

than the project. Capital contribution commitments by the owners of the project company are

sometimes necessary to ensure that the project is financially sound.

II. Risk management

In ideal risk management, a prioritization process is followed whereby the risks with the greatest

loss and the greatest probability of occurring are handled first, and risks with lower probability

of occurrence and lower loss are handled in descending order. In practice the process can be

very difficult, and balancing between risks with a high probability of occurrence but lower loss

versus a risk with high loss but lower probability of occurrence can often be mishandled.

Intangible risk management identifies a new type of a risk that has a 100% probability of

occurring but is ignored by the organization due to a lack of identification ability. For example,

when deficient knowledge is applied to a situation, a knowledge risk materializes. Relationship

risk appears when ineffective collaboration occurs. Process-engagement risk may be an issue

when ineffective operational procedures are applied. These risks directly reduce the productivity

of knowledge workers, decrease cost effectiveness, profitability, service, quality, reputation,

brand value, and earnings quality. Intangible risk management allows risk management to create

immediate value from the identification and reduction of risks that reduce productivity.

21Institute of Productivity and Management

Risk management also faces difficulties in allocating resources. This is the idea of opportunity

cost. Resources spent on risk management could have been spent on more profitable activities.

Again, ideal risk management minimizes spending and minimizes the negative effects of risks.

Company Profile

HDFC Bank Ltd. is a major Indian financial services company based in Mumbai, incorporated

in August 1994, after the Reserve Bank of India allowed establishing private sector banks. The

Bank was promoted by the Housing Development Finance Corporation, a premier housing

finance company (set up in 1977) of India. HDFC Bank has 1,412 branches and over 3,295

ATMs, in 528 cities in India, and all branches of the bank are linked on an online real-time

basis. As of September 30, 2008 the bank had total assets of INR 1006.82 billion. For the fiscal

year 2008-09, the bank has reported net profit of Rs.2,244.9 crore, up 41% from the previous

fiscal. Total annual earnings of the bank increased by 58% reaching at Rs.19,622.8 crore in

2008-09.

Board of Director

Managing Director

• Mr. Aditya Puri

Executive Director

• Mr. Harish Engineer

22Institute of Productivity and Management

• Mr. Paresh Sukthankar

Group Head - Equities, Private Banking, Third Party Products, NRI & International

Consumer Business

• Mr. Abhay Aima

Treasurer

• Mr. Ashish Pathasarthy

Group Head – Properties

• Mr. Bharat Shah

Country Head - Internal Controls & Compliance Risk

• Mr. G. Subramanian

Country Head - Branch Banking

• Mr. Navin Puri

Head – Finance

• Mr. Sashi Jagdishan

23Institute of Productivity and Management

Industry Background

Banking system in India

Currently, India has 96 scheduled commercial banks (SCBs) - 27 public sector banks (that is

with the Government of India holding a stake), 31 private banks (these do not have government

stake; they may be publicly listed and traded on stock exchanges) and 38 foreign banks. They

have a combined network of over 53,000 branches and 49,000 ATMs. According to a report by

ICRA Limited, a rating agency, the public sector banks hold over 75 percent of total assets of

the banking industry, with the private and foreign banks holding 18.2% and 6.5% respectively.

24Institute of Productivity and Management

Early history

Banking in India originated in the last decades of the 18th century. The first banks were The

General Bank of India which started in 1786, and the Bank of Hindustan, both of which are now

defunct. The oldest bank in existence in India is the State Bank of India, which originated in the

Bank of Calcutta in June 1806, which almost immediately became the Bank of Bengal. This was

one of the three presidency banks, the other two being the Bank of Bombay and the Bank of

Madras, all three of which were established under charters from the British East India Company.

For many years the Presidency banks acted as quasi-central banks, as did their successors. The

three banks merged in 1921 to form the Imperial Bank of India, which, upon India's

independence, became the State Bank of India.

25Institute of Productivity and Management

Indian merchants in Calcutta established the Union Bank in 1839, but it failed in 1848 as a

consequence of the economic crisis of 1848-49. The Allahabad Bank, established in 1865 and

still functioning today, is the oldest Joint Stock bank in India. It was not the first though. That

honor belongs to the Bank of Upper India, which was established in 1863, and which survived

until 1913, when it failed, with some of its assets and liabilities being transferred to the Alliance

Bank of Shimla.

When the American Civil War stopped the supply of cotton to Lancashire from the Confederate

States, promoters opened banks to finance trading in Indian cotton. With large exposure to

speculative ventures, most of the banks opened in India during that period failed. The depositors

lost money and lost interest in keeping deposits with banks. Subsequently, banking in India

remained the exclusive domain of Europeans for next several decades until the beginning of the

20th century.

Foreign banks too started to arrive, particularly in Calcutta, in the 1860s. The Comptoire

d'Escompte de Paris opened a branch in Calcutta in 1860, and another in Bombay in 1862;

branches in Madras and Pondicherry, then a French colony, followed. HSBC established itself

in Bengal in 1869. Calcutta was the most active trading port in India, mainly due to the trade of

the British Empire, and so became a banking center.

The first entirely Indian joint stock bank was the Oudh Commercial Bank, established in 1881

in Faizabad. It failed in 1958. The next was the Punjab National Bank, established in Lahore in

1895, which has survived to the present and is now one of the largest banks in India.

Around the turn of the 20th Century, the Indian economy was passing through a relative period

of stability. Around five decades had elapsed since the Indian Mutiny, and the social, industrial

and other infrastructure had improved. Indians had established small banks, most of which

served particular ethnic and religious communities.

The presidency banks dominated banking in India but there were also some exchange banks and

a number of Indian joint stock banks. All these banks operated in different segments of the

economy. The exchange banks, mostly owned by Europeans, concentrated on financing foreign

trade. Indian joint stock banks were generally under capitalized and lacked the experience and

26Institute of Productivity and Management

maturity to compete with the presidency and exchange banks. This segmentation let Lord

Curzon to observe, "In respect of banking it seems we are behind the times. We are like some

old fashioned sailing ship, divided by solid wooden bulkheads into separate and cumbersome

compartments."

The period between 1906 and 1911, saw the establishment of banks inspired by the Swadeshi

movement. The Swadeshi movement inspired local businessmen and political figures to found

banks of and for the Indian community. A number of banks established then have survived to

the present such as Bank of India, Corporation Bank, Indian Bank, Bank of Baroda, Canara

Bank and Central Bank of India.

The fervour of Swadeshi movement lead to establishing of many private banks in Dakshina

Kannada and Udupi district which were unified earlier and known by the name South Canara

( South Kanara ) district. Four nationalised banks started in this district and also a leading

private sector bank. Hence undivided Dakshina Kannada district is known as "Cradle of Indian

Banking".

List of banks in India:-

Public Sector Banks

There are total 26 public sector banks in India (As on 26-09-2009). Of these 19 are nationalised

banks, 6(STATE BANK OF INDORE ALSO MERGED RECENTLY) belong to SBI &

associates group and 1 bank (IDBI Bank) is classified as other public sector bank.

Nationalized Banks

• Bank of Baroda

• Dena Bank

27Institute of Productivity and Management

• Indian Bank

• Indian Overseas Bank

• Oriental Bank of Commerce

• Punjab National Bank

• Punjab and Sind Bank

• Syndicate Bank

• UCO Bank

• Union Bank of India

• United Bank of India

• Vijaya Bank

• Repco bank

• Allahabad bank

SBI & associates

• State Bank of India

• State Bank of Bikaner and Jaipur

• State Bank of Indore

• State Bank of Travancore

• State Bank of Patiala

• State Bank of Hyderabad

• State Bank of Mysore

Private Banks

28Institute of Productivity and Management

• Axis Bank

• Bank of Rajasthan

• Catholic Syrian Bank

• City Union Bank

• Development Credit Bank

• Dhanalakshmi Bank

• Federal Bank

• HDFC Bank

• ICICI Bank

• ING Vysya Bank

• Jammu & Kashmir Bank

• Karnataka Bank

• Kotak Mahindra Bank

• Laxmi Vilas Bank

• Yes Bank

29Institute of Productivity and Management

Competitive Situation

ICICI Bank (formerly Industrial Credit and Investment Corporation of

India) is a major banking and financial services organization in India. It is

the 4th largest bank in India and the largest private sector bank in India by

market capitalization. The bank also has a network of 1,700+ branches (as on 31 March 2010)

and about 4,721 ATMs in India and presence in 19 countries, as well as some 24 million

customers (at the end of July 2007). ICICI Bank offers a wide range of banking products and

financial services to corporate and retail customers through a variety of delivery channels and

specialization subsidiaries and affiliates in the areas of investment banking, life and non-life

insurance, venture capital and asset management. (These data are dynamic.) ICICI Bank is also

the largest issuer of credit cards in India. The Bank is expanding in overseas markets and has the

largest international balance sheet among Indian banks. ICICI Bank now has wholly-owned

subsidiaries, branches and representatives offices in 19 countries, including an offshore unit in

Mumbai.

Axis Bank, formally UTI Bank, is a financial services firm that had begun

operations in 1994, after the Government of India allowed new private

banks to be established. The Bank was promoted jointly by the Administrator of the Specified

Undertaking of the Unit Trust of India (UTI-I), Life Insurance Corporation of India (LIC),

General Insurance Corporation Ltd., National Insurance Company Ltd., The New India

Assurance Company, The Oriental Insurance Corporation and United India Insurance Company

UTI-I holds a special position in the Indian capital markets and has promoted many leading

financial institutions in the country. The bank changed its name to Axis Bank in April 2007 to

avoid confusion with other unrelated entities with similar name..As on the year ended March 31,

2009 the Bank had a total income of Rs 13,745.04 crore (US$ 2.93 billion) and a net profit of

Rs. 1,812.93 crore (US$ 386.15 million).On February 24, 2010, Axis Bank announced the

launch of 'AXIS CALL & PAY on atom', a unique mobile payments solution using Axis Bank

30Institute of Productivity and Management

debit cards. Axis Bank is the first bank in the country to provide a secure debit card-based

payment service over IVR.

State Bank of India is the largest state-owned banking and

financial services company in India, by almost every parameter -

revenues, profits, assets, market capitalization, etc. The bank traces its ancestry to British India,

through the Imperial Bank of India, to the founding in 1806 of the Bank of Calcutta, making it

the oldest commercial bank in the Indian Subcontinent. The Government of India nationalized

the Imperial Bank of India in 1955, with the Reserve Bank of India taking a 60% stake, and

renamed it the State Bank of India. In 2008, the Government took over the stake held by the

Reserve Bank of India.SBI provides a range of banking products through its vast network of

branches in India and overseas, including products aimed at NRIs. The State Bank Group, with

over 16,000 branches, has the largest banking branch network in India. With an asset base of

$260 billion and $195 billion in deposits, it is a regional banking behemoth. It has a market

share among Indian commercial banks of about 20% in deposits and advances, and SBI

accounts for almost one-fifth of the nation's loans.

Bank of Baroda is the third largest bank in India, after the State

Bank of India and the Punjab National Bank and ahead of ICICI

Bank. BOB has total assets in excess of Rs. 2.27 lakh crores, or

Rs. 2,274 billion, a network of over 3,000 branches and offices, and about 1,100 ATMs. It offers

a wide range of banking products and financial services to corporate and retail customers

through a variety of delivery channels and through its specialized subsidiaries and affiliates in

the areas of investment banking, credit cards and asset management. As of August 2010, the

bank has 78 branches abroad and by the end of FY11 this number should climb to 90. In 2010,

BOB opened a branch in Auckland, New Zealand, and its tenth branch in the United Kingdom.

The bank also plans to open five branches in Africa.

31Institute of Productivity and Management

Company Background

History of HDFC Bank Ltd.

HDFC Bank Ltd. is a commercial bank of India, incorporated in August 1994, after

the Reserve Bank of India allowed establishing private sector banks. The Bank was promoted by

the Housing Development Finance Corporation, a premier housing finance company (set up in

1977) of India. HDFC Bank has 1,412 branches and over 3,295 ATMs, in 528 cities in India,

and all branches of the bank are linked on an online real-time basis. As of September 30, 2008

the bank had total assets of INR 1006.82 billion. For the fiscal year 2008-09, the bank has

reported net profit of Rs.2,244.9 crore, up 41% from the previous fiscal. Total annual earnings

of the bank increased by 58% reaching at Rs.19,622.8 crore in 2008-09.

HDFC Bank was incorporated in the year of 1994 by Housing Development Finance

Corporation Limited (HDFC), India's premier housing finance company. It was among the first

companies to receive an 'in principle' approval from the Reserve Bank of India (RBI) to set up a

bank in the private sector. The Bank commenced its operations as a Scheduled Commercial

Bank in January 1995 with the help of RBI's liberalization policies.

In 2008 HDFC Bank acquired Centurion Bank of Punjab taking its total branches to more than

1,000. The amalgamated bank emerged with a strong deposit base of around Rs. 1,22,000 crore

and net advances of around Rs. 89,000 crore. The balance sheet size of the combined entity is

over Rs. 1,63,000 crore. The amalgamation added significant value to HDFC Bank in terms of

increased branch network, geographic reach, and customer base, and a bigger pool of skilled

manpower.

Business Focus

HDFC Bank deals with three key business segments – Wholesale Banking Services, Retail

Banking Services, Treasury. It has entered the banking consortia of over 50 corporates for

providing working capital finance, tradeservices, corporate finance and merchant banking. It is

also providing sophisticated product structures in areas of foreign exchange and derivatives,

money markets and debt trading and equity research.

32Institute of Productivity and Management

Wholesale Banking Services

The Bank's target market ranges from large, blue-chip manufacturing companies in the Indian

corp to small & mid-sized corporates and agri-based businesses. For these customers, the Bank

provides a wide range of commercial and transactional banking services, including working

capital finance, trade services, transactional services, cash management, etc. The bank is also a

leading provider of structured solutions, which combine cash management services with vendor

and distributor finance for facilitating superior supply chain management for its corporate

customers. HDFC Bank has made significant inroads into the banking consortia of a number of

leading Indian corporate including multinationals, companies from the domestic business houses

and prime public sector companies. It is recognized as a leading provider of cash management

and transactional banking solutions to corporate customers, mutual funds, stock exchange

members and banks.

Retail Banking Services

The objective of the Retail Bank is to provide its target market customers a full range of

financial products and banking services, giving the customer a one-stop window for all his/her

banking requirements. The products are backed by world-class service and delivered to

customers through the growing branch network, as well as through alternative delivery channels

like ATMs, Phone Banking, NetBanking and Mobile Banking.

HDFC Bank was the first bank in India to launch an International Debit Card in association with

VISA (VISA Electron) and issues the Mastercard Maestro debit card as well. The Bank

launched its credit card business in late 2001. By March 2009, the bank had a total card base

(debit and credit cards) of over 13 million. The Bank is also one of the leading players in the

“merchant acquiring” business with over 70,000 Point-of-sale (POS) terminals for debit / credit

cards acceptance at merchant establishments. The Bank is well positioned as a leader in various

net based B2C opportunities including a wide range of internet banking services for Fixed

Deposits, Loans, Bill Payments, etc.

Treasury

33Institute of Productivity and Management

Within this business, the bank has three main product areas - Foreign Exchange and Derivatives,

Local Currency Money Market & Debt Securities, and Equities. These services are provided

through the bank's Treasury team. To comply with statutory reserve requirements, the bank is

required to hold 25% of its deposits in government securities. The Treasury business is

responsible for managing the returns and market risk on this investment portfolio.

Distribution network:

HDFC Bank is headquartered in Mumbai. The Bank has an network of 1,725 branches spread in

771 cities across India. All branches are linked on an online real-time basis. Customers in over

500 locations are also serviced through Telephone Banking. The Bank has a presence in all

major industrial and commercial centres across the country. Being a clearing/settlement bank to

various leading stock exchanges, the Bank has branches in the centres where the NSE/BSE have

a strong and active member base.

The Bank also has 3,898 networked ATMs across these cities. Moreover, HDFC Bank's ATM

network can be accessed by all domestic and international Visa/MasterCard, Visa

Electron/Maestro, Plus/Cirrus and American Express Credit/Charge cardholders.

In 2008 HDFC Bank acquired Centurion Bank of Punjab taking its total branches to more

than 1,000. Though, the official license was given to Centurion Bank of Punjab branches,

to continue working as HDFC Bank branches, on May 23, 2008

Housing Development Finance Corporation Limited, more popularly known as HDFC Bank

Ltd, was established in the year 1994, as a part of the liberalization of the Indian Banking

Industry by Reserve Bank of India (RBI). It was one of the first banks to receive an 'in principle'

approval from RBI, for setting up a bank in the private sector. The bank was incorporated with

the name 'HDFC Bank Limited', with its registered office in Mumbai. The following year, it

started its operations as a Scheduled Commercial Bank. Today, the bank boasts of as many as

1412 branches and over 3275 ATMs across India.

Amalgamations

In 2002, HDFC Bank witnessed its merger with Times Bank Limited (a private sector bank

34Institute of Productivity and Management

promoted by Bennett, Coleman & Co. / Times Group). With this, HDFC and Times became the

first two private banks in the New Generation Private Sector Banks to have gone through a

merger. In 2008, RBI approved the amalgamation of Centurion Bank of Punjab with HDFC

Bank. With this, the Deposits of the merged entity became Rs. 1,22,000 crore, while the

Advances were Rs. 89,000 crore and Balance Sheet size was Rs. 1,63,000 crore.

Tech-Savvy

HDFC Bank has always prided itself on a highly automated environment, be it in terms of

information technology or communication systems. All the braches of the bank boast of online

connectivity with the other, ensuring speedy funds transfer for the clients. At the same time, the

bank's branch network and Automated Teller Machines (ATMs) allow multi-branch access to

retail clients. The bank makes use of its up-to-date technology, along with market position and

expertise, to create a competitive advantage and build market share.

Capital Structure

At present, HDFC Bank boasts of an authorized capital of Rs 550 crore (Rs5.5 billion), of this

the paid-up amount is Rs 424.6 crore (Rs.4.2 billion). In terms of equity share, the HDFC Group

holds 19.4%. Foreign Institutional Investors (FIIs) have around 28% of the equity and about

17.6% is held by the ADS Depository (in respect of the bank's American Depository Shares

(ADS) Issue). The bank has about 570,000 shareholders. Its shares find a listing on the Stock

Exchange, Mumbai and National Stock Exchange, while its American Depository Shares are

listed on the New York Stock Exchange (NYSE), under the symbol 'HDB'.

Housing Finance Sector

Against the milieu of rapid urbanization and a changing socio-economic scenario, the demand

for housing has grown explosively. The importance of the housing sector in the economy can be

illustrated by a few key statistics. According to the National Building Organization (NBO), the

total demand for housing is estimated at 2 million units per year and the total housing shortfall is

estimated to be 19.4 million units, of which 12.76 million units is from rural areas and 6.64

million units from urban areas. The housing industry is the second largest employment

generator in the country. It is estimated that the budgeted 2 million units would lead to the

35Institute of Productivity and Management

creation of an additional 10 million man-years of direct employment and another 15 million

man-years of indirect employment.

Having identified housing as a priority area in the Ninth Five Year Plan (1997-2002), the

National Housing Policy has envisaged an investment target of Rs. 1,500 billion for this sector.

In order to achieve this investment target, the Government needs to make low cost funds easily

available and enforce legal and regulatory reforms.

Background

HDFC was incorporated in 1977 with the primary objective of meeting a social need - that of

promoting home ownership by providing long-term finance to households for their housing

needs. HDFC was promoted with an initial share capital of Rs. 100 million.

Business Objectives

The primary objective of HDFC is to enhance residential housing stock in the country through

the provision of housing finance in a systematic and professional manner, and to promote home

ownership. Another objective is to increase the flow of resources to the housing sector by

integrating the housing finance sector with the overall domestic financial markets.

Organizational Goals

o HDFC's main goals are to a) develop close relationships with individual households, b)

maintain its position as the premier housing finance institution in the country, c)

transform ideas into viable and creative solutions, d) provide consistently high returns to

shareholders, and e) to grow through diversification by leveraging off the existing client

base.

o HDFC is a professionally managed organization with a board of directors consisting of

eminent persons who represent various fields including finance, taxation, construction

36Institute of Productivity and Management

and urban policy & development. The board primarily focuses on strategy formulation,

policy and control, designed to deliver increasing value to shareholders.

Organizational Chart

37Institute of Productivity and Management

Products at glance

Accounts & Deposits Loans Investments & Insurance

Savings Accounts:

• Regular Savings Account• Savings Plus Account

• Savings Max Account

• Senior citizen Account

• No Frills Account

• Institutional Savings Account

• Salary Accounts:

• Payroll

• Classic

• Regular

• Premium

• Defence

• No Frills Salary Account

• Reimbursement Current Account

• Kid’s Advantage Account

• Personal Loan

• Smart Draft

• Home Loan

• Two wheeler Loan

• New Car Loan

• Used Car Loan

• Gold Loan

• Educational Loan

• Loan against Securities

• Loan against Property

• Health Care Finance

• Commercial Vehicle Finance

• Loan Against Rental Receivables

• Retail Agri Loan

• Tractor Loan

• Working Capital Finance

• Mutual Funds

• Tax Planning

• Insurance

• General & Health Insurance

• Bonds

• Knowledge centre

• Equities & Derivatives

• Mudra Gold Bar

Forex Services• Products &

Services

• Trade services

• Forex Services Branch Locator

• RBI Guidelines

• Forex Limits

Payment Services• Net Safe

• Merchant Services

38Institute of Productivity and Management

• Pension Saving Bank Account

• Family Saving Group

• Kisan No Frill Saving

• Kisan Club Services

Current Accounts:

• Plus Current Account• Regular Current Account

• Trade Current Account

• Premium Current Account

• RFC-Domestic Account

• Flexi Current Account

• Apex Current Account

• Max Current Account

Fixed Deposits:

• Regular Fixed Account• 5 Year Tax Saving Fixed

Account

• Super saver facility

• Sweep-in facility

Recurring Deposits

Demat Account

• Construction Equipment Finance

• Warehouse receipt Loan

• Prepaid Refills

• Bill Pay

• Visa Bill Pay

• Pay Now

• Register & Pay

• Insta Pay

• Direct Pay

• M Chek

• Visa Money Transfer

• RTGS Funds Transfer

• e-monies Electronic Fund Transfer

• Donate to Charity

• Religious offerings

• Online payment of DVAT

• Online payment of Gujarat VAT

• Online payment of Direct Tax

• Excise & Service Tax Payment

CardsCredit Cards:

• Silver Credit Card • Gold Credit Card

• Titanium Credit Card

• Woman’s Gold Credit card

• Platinum Gold Credit card

• Visa Signature Credit card

• World Master CardCredit Card

• Corporate Platinum credit Card

• Corporate Credit card

• Business Platinum Credit Card

• Business Gold Credit card

• Purchase card

• Distributor card Access Your Bank

39Institute of Productivity and Management

Safe deposits Lockers Debit Cards:

• Easy Shop International Debit Card

• Easy Shop Gold Debit Card

• Easy Shop International Business Debit Card

• Easy Shop Woman’s Advantage Debit card

• Easy Shop Titanium Debit Card

• Easy Shop NRO Debit Card

Prepaid Cards:

• Forex Plus card• Gift Plus Card

• Food Plus Card

• Money Plus Card

• Forex Plus Chip Card

• Net Banking

• Credit Card Online

• One View

• Insta Alerts

• Mobile Banking

• ATM

• Phone Banking

• Email Statements

• Branch Networks

HDFC Bank Imperia/Preferred/Classic Banking

• Imperia Premium Banking

• Preferred Banking

• Classic Banking

Private Banking

LOANS

• Personal Loans :

40Institute of Productivity and Management

HDFC Personal Loans have been designed by HDFC Bank to suit personal requirements of

individuals like marriage, holiday, and education, purchase of any expensive commodity or any

such anticipated or unanticipated monetary involvement.

Features & benefits:

• Borrow up to Rs 15, 00,000 for any purpose depending on your requirements

• Flexible Repayment options, ranging from 12 to 60 months.

• Repay with easy EMIs.

• One of the lowest interest rates.

• Hassle free loans - No guarantor/security/collateral required.

• Speedy loan approval.

• Convenience of service at your doorstep.

• Further, there are additional privileges for HDFC Bank account holders like:

o Special rates of interest.

o For existing Auto Loan customers with a clear repayment of 12

months or more from even any of the approved financiers of

HDFC Bank, a hassle free personal loan without income

documentation can be obtained.

o For existing HDFC Bank Personal Loan customer with a clear

repayment of 12 months or more, personal loan can be

enhanced.

Credit Shield

In case of death or total permanent disability of the loaner, the loaner/nominee can avail of the

Payment Protection Insurance (Credit Shield) which insures the principle outstanding on the

loan up to a maximum of the loan amount. Principle outstanding is defined as the amount of

loan outstanding (not including any arrears in payment or interest thereon) at the Date of Loss,

having accounted for payments made and interest accruing as determined in the Policy.

41Institute of Productivity and Management

Hence,the amount covered does not include any principal added because of non - payment of

EMI and also will not include interest/ accrued charges.*

Personal Accident Cover

In order to ensure that your family is taken care of we also offer a Personal Accident cover of

Rs.2,00,000 at a nominal premium.*

* Premium will be charged for both these products which will be deducted from the loan

amount at the time of disbursal .A transaction fee of Rs.750 will also be deducted at the time of

disbursal. Please note that service tax @ 10% and Education cess of 3% will also be charged.

Eligibility and Documentation:-

Salaried Individuals

Self Employed (Professional)

Self Employed (Individuals)

Self Employed(Private companies and Partnership Firms)

1. Salaried Individuals:

Salaried Individuals include Salaried Doctors, CAs, employees of select Public and Private

limited companies, Government Sector employees including public sector undertakings and

central, state and local bodies:

Eligibility Criteria

Minimum age of Applicant: 21 years

Maximum age of Applicant at loan maturity: 60 years

Minimum employment: Minimum 2 years in employment and minimum 1 year in the

current organization

Minimum Net Monthly Income: Rs. 10,000 per month (Rs. 15,000 in Mumbai, Delhi,

Bangalore, Chennai and Hyderabad & Rs. 12,000 in Calcutta, Ahmedabad and Cochin)

42Institute of Productivity and Management

Documents required:

Proof of Identity (Passport Copy/ Voters ID card/ Driving Licence)

Address Proof (Ration card Tel/Elect. Bill/ Rental agr. / Passport copy/Trade licence

/Est./Sales Tax certificate)

Bank Statements (latest 3 months bank statement / 6 months bank passbook)

Latest salary slip or current dated salary certificate with latest Form 16.

2. Self Employed (Professional):

Self employed (Professionals) include self - employed Doctors, Chartered Accountants,

Architects, and Company Secretaries.

Eligibility Criteria

• Minimum age of Applicant: 25 years

• Maximum age of Applicant at loan maturity: 65 years

• Years in business: 4 to 7 years depending on profession

• Minimum Annual Income: Rs. 100000 p.a.

Documents required:

Proof of Identity (Passport Copy/ Voters ID card/ Driving Licence).

Address Proof (Ration card Tel/elect. Bill/ Rental agr. / Passport copy/Trade licence

/Est./Sales Tax certificate).

Bank Statements(latest 6 months bank statement /passbook)

Latest ITR along with computation of income, B/S & P&L a/c for the last 2 yrs. certified

by a CA

Qualification proof of the highest professional degree.

3. Self Employed (Individuals):

43Institute of Productivity and Management

Self Employed (Pvt. Cos and Partnership Firms) include Private Companies and Partnership

firms in the Business of Manufacturing, Trading or Services

Eligibility Criteria

Years in business: Minimum of 3 years in current business and 5 years total business

experience

Business must be profit making for the last 2 years

Minimum Annual Income: Rs 100000 p.a.

Documents required:

Address Proof (Ration card Tel/elect. Bill/ Rental agr. / Passport copy/Trade licence

/Est./Sales Tax certificate)

Bank Statements(latest 6 months bank statement /passbook)

Latest ITR along with computation of income, B/S & P&L a/c for the last 2 yrs. certified

by a CA

Proof of continuation (Trade license /Establishment /Sales Tax certificate)

Fees & Charges for Personal Loan:

Description of Charges Personal Loan

Loan Processing Charges Upto 2.50% of the loan amount

Prepayment Salaried - No pre-payment permitted until repayment of

12 EMIs

Self-employed - No pre-payment permitted until

repayment of 6 EMIs

Pre-payment charges Salaried - 4% of the Principal Outstanding after

repayment of 12 EMIs

Self-employed - 4% of the Principal Outstanding after

44Institute of Productivity and Management

repayment of 6 EMIs

No Due Certificate / No Objection Certificate (NOC) NIL

Duplicate no due certificate / NOC Rs 250/-

Solvency Certificate Not applicable

Charges for late payment of EMI @ 24 % p.a on amount outstanding from date of default

Charges for changing from fixed to floating rate of

interest

Not applicable

Charges for changing from floating to fixed rate of

interest

Not applicable

Stamp Duty & other statutory charges As per applicable laws of the state

Credit assessment charges Not applicable

Non standard repayment charges Not applicable

Cheque swapping charges Rs 500/- per event

Loan Re-booking charges / Re-scheduling charges Rs 1000/-

Loan cancellation charges Rs. 1000/-

Cheque Bounce Charges Rs 450/- per cheque bounce

Legal / incidental charges At actual

• Business Loan:

Small & Medium Enterprises

At HDFC Bank we understand how much of hard work goes into establishing a successful

SME. We also understand that your business is anything but "small" and as demanding as ever.

And as your business expands and enters new territories and markets, you need to keep pace

with the growing requests that come in, which may lead to purchasing new, or updating existing

plant and equipment, or employing new staff to cope with the demand. That´s why we at HDFC

Bank have assembled products, services, resources and expert advice to help ensure that your

business excels.

45Institute of Productivity and Management

Our solutions are designed to meet your varying needs. The following links will help you

identify your individual needs.

Funded Services

Funded Services from HDFC Bank are meant to directly bolster the day-to-day working of a

small and a medium business enterprise. From working capital finance to credit substitutes;

from export credit to construction equipment loan - we cater to virtually every business

requirement of an SME. Click on the services below that best define your needs.

• Working Capital Finance

• Commercial Vehicle finance

• Construction Equipment Loan

• Short Term Finance

• Bill Discounting

• Credit Substitutes

• Export Credit

• Structured Cash Flow Financing

• Real Estate Initiatives

• Non-Funded Services

Under Non-Funded services HDFC Bank offers solutions that act as a catalyst to propel your

business. Imagine a situation where you have a letter of credit and need finance against the same

or you have a tender and you need to equip yourself with a guarantee in order to go ahead. This

is exactly where we can help you so that you don't face any roadblocks when it comes to your

business.

• Home Loan:

46Institute of Productivity and Management

Home Loans offered by HDFC Bank encompasses a wide range of loan options which are

subject to various parameters like term of loan, financial status of the individual seeking loan

and the purpose of loan. Owing to these diversifications, HDFC Home Loans have grown in

popularity over the years.

The primary subdivision of HDFC Home Loans is loans for:

• Resident Indian

• Non Resident Indian

Loans for Resident Indians:

With an HDFC Home Loan, one can buy a self-contained flat in an existing or proposed co-

operative society, in an apartment owner's association or even an independent single-family or

multi-family bungalow anywhere in India.

HDFC Home Loans are easy to arrange and can be customized according to the individual's

needs and repayment capabilities.

This category can be further into subdivided into:

• Home Loans: Home loans for individuals to purchase (fresh / resale) or construct

houses. Application can be made individually or jointly. HDFC finances up to 85%

maximum of the cost of the property (Agreement value + Stamp duty + Registration

charges) based on the repayment capacity of the customer.

• Home Improvement Loan - HIL facilitates internal and external repairs and other

structural improvements like painting, waterproofing, plumbing and electric works,

tiling and flooring, grills and aluminum windows. HDFC finances up to 85% of the cost

of renovation (100% for existing customers) subject to market value of the property.

• Home Extension Loan - HEL facilitates the extension of an existing dwelling unit. All

the terms are the same as applicable to Home Loan.

• Land Purchase Loan - Be it land for a dream house, or just an investment for the

future, HDFC Land Purchase Loan is a convenient loan facility to purchase land. HDFC

47Institute of Productivity and Management

finances up to 85% of the cost of the land (Conditions Apply). Repayment of the loan

can be done over a maximum period of 15 years

• Short Term Bridging Loans

• Professional Loan or Loan for Non-residential Premises

• Home Equity Loan

Loans for Non Resident Indians:

Like Resident Indians, HDFC Home Loans feature similar categories of loans for Non Resident

Indians as well. They include:

• Home Loan

• Home Improvement Loan

• Home Extension Loan

• Land Purchase Loan

Features & Benefits:

o Choose from Fixed Rate or Floating Rate with options to structure your loan as Partly

Fixed or Partly Floating.

o Flexible repayment options to suit your individual needs.

o Loan cover Term Assurance Plan - HDFC Standard Life Insurance Company Ltd.

offers an insurance plan*, which is designed to ensure that life's uncertainties do not

affect your family's interests and your precious home. LCTAP provides a lump-sum

payment on the unfortunate demise of the life assured. This pure risk plan is designed in

a way that the cover decreases as you repay your home loan making it a low cost

premium insurance plan.

*Insurance is the subject matter of solicitation.

o Automated Repayment of Home loan EMI - You can give us standing instructions to

repay your Home Loan EMIs directly from your HDFC Bank Savings Account, thus,

saving you the trouble of procuring, signing and tracking post-dated cheques.

48Institute of Productivity and Management

o HDFC also offers In-house scrutiny of Property documents for your complete peace

of mind.

o Customer privileges - If you are an existing HDFC Home Loan customer, you can

avail of other loans (such as Personal Loans , Car Loans , Two-wheeler Loans and Loan

against securities ) at lower interest rates.

o Applicant and Co - Applicant to the loan:

Loans can be applied for either individually or jointly. Proposed owners of the property

will have to be co-applicants. However, the co-applicants need not be co-owners.

o Hassle Free Documentation - no security/guarantor is required.

o Loan Amount: Customers are eligible to get upto 85% of the amount of the property.

o Tenure: 1-20Years

o Adjustable Rate Home Loan

Loan under Adjustable Rate is linked to HDFC's Retail Prime Lending Rate (RPLR).

The rate on your loan will be revised every three months from the date of first

disbursement, if there is a change in RPLR, the interest rate on your loan may change.

However, the EMI on the loan disbursed will not change*. If the interest rate increases,

the interest component in an EMI will increase and the principal component will reduce

resulting in an extension of term of the loan, and vice versa when the interest rate

decreases.

*Conditions Apply

Documents:

• Application Form and submit along with the following documents for an approval of

loan.

• Application form with photograph

• Identity and Residence Proof

• Education Qualifications Certificate and Proof of business existence

• Last 3 years Income Tax returns (self and business)

49Institute of Productivity and Management

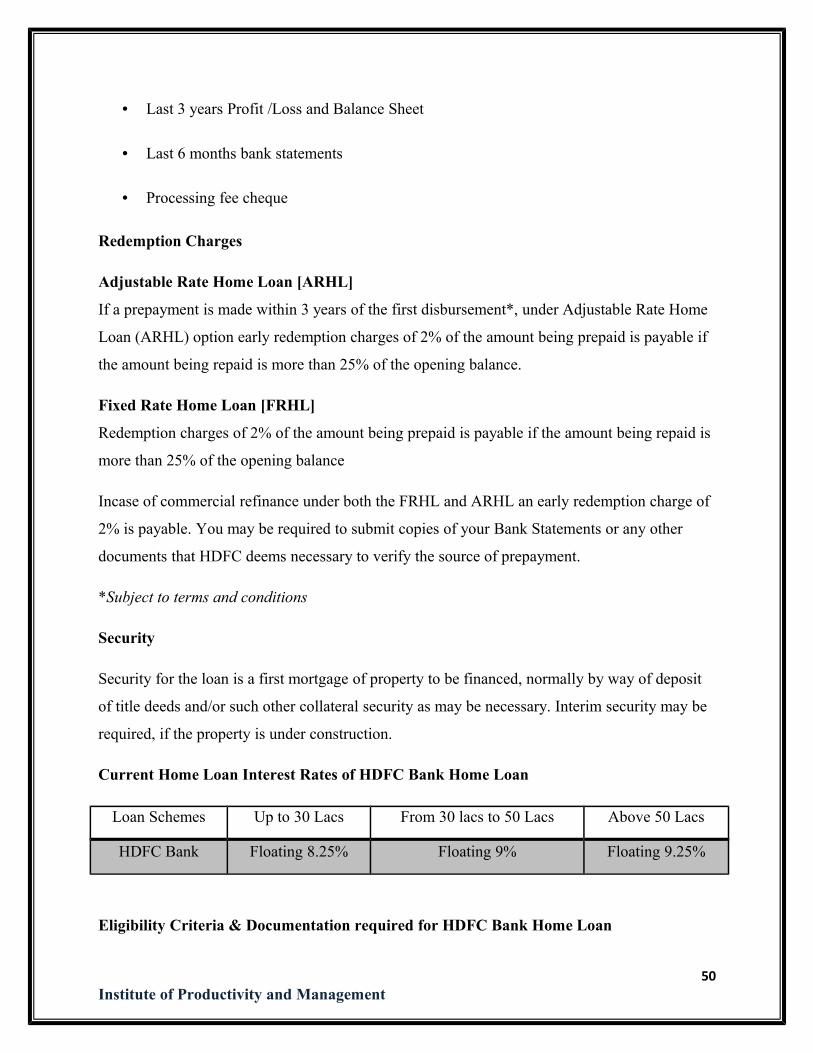

• Last 3 years Profit /Loss and Balance Sheet

• Last 6 months bank statements

• Processing fee cheque

Redemption Charges

Adjustable Rate Home Loan [ARHL]

If a prepayment is made within 3 years of the first disbursement*, under Adjustable Rate Home

Loan (ARHL) option early redemption charges of 2% of the amount being prepaid is payable if

the amount being repaid is more than 25% of the opening balance.

Fixed Rate Home Loan [FRHL]

Redemption charges of 2% of the amount being prepaid is payable if the amount being repaid is

more than 25% of the opening balance

Incase of commercial refinance under both the FRHL and ARHL an early redemption charge of

2% is payable. You may be required to submit copies of your Bank Statements or any other

documents that HDFC deems necessary to verify the source of prepayment.

*Subject to terms and conditions

Security

Security for the loan is a first mortgage of property to be financed, normally by way of deposit

of title deeds and/or such other collateral security as may be necessary. Interim security may be

required, if the property is under construction.

Current Home Loan Interest Rates of HDFC Bank Home Loan

Loan Schemes Up to 30 Lacs From 30 lacs to 50 Lacs Above 50 Lacs

HDFC Bank Floating 8.25% Floating 9% Floating 9.25%

Eligibility Criteria & Documentation required for HDFC Bank Home Loan

50Institute of Productivity and Management

Salaried Self employed

AGE 21years to 58years 21years to 65years

Income Rs.1,20,000 (p.a) Rs.1,50,000 (p.a)

Loan Amount

Offered

2,00,000 - 1,00,00000 2,00,000 - 2,00,00000

Tenure 5years-20years 5years-20years

Current Experience 3years 2years

Processing Fee 11000/- or 0.5% 11000/- or 0.5%

Documentation 1) Application form with

photograph

2) Identity & residence proof

3) Latest salary slip,

4) Form 16

5) Last 6 months bank

statements

6) Processing fee cheque

1) Application form with photograph

2) Identity & residence proof

3) Education qualifications certificate & proof of business

existence

4) Business profile, Last 3 years profit/loss & balance

sheet

5) Last 6 months bank statements

6) Processing fee cheque

Home Loan Fees & Charges:

Description of Charges Ecbop Home Loan

Foreclosure charges No prepayments allowed in first 6 months

6 months - 5 years - 1.5% of original loan amount

5 years -10 years - 0.75% of original loan amount

> 10 years - No closure fee

For Gold Category

6 months - 5 years - 2% of original loan amount

> 5 years - No closure fee

eBOP customers :

Loan repaid from own sources - no FC charges

Loan repaid from other sources - regular FC charges.

Charges for late payment of EMI 2% per month

Cheque swapping charges Rs 500/-

51Institute of Productivity and Management

Bounce Cheque Charges Rs. 500/-

Duplicate Statement Charges (per

statement)

Rs 100/- per page, Maximum Rs 300/-

Issue of Duplicate Provisional