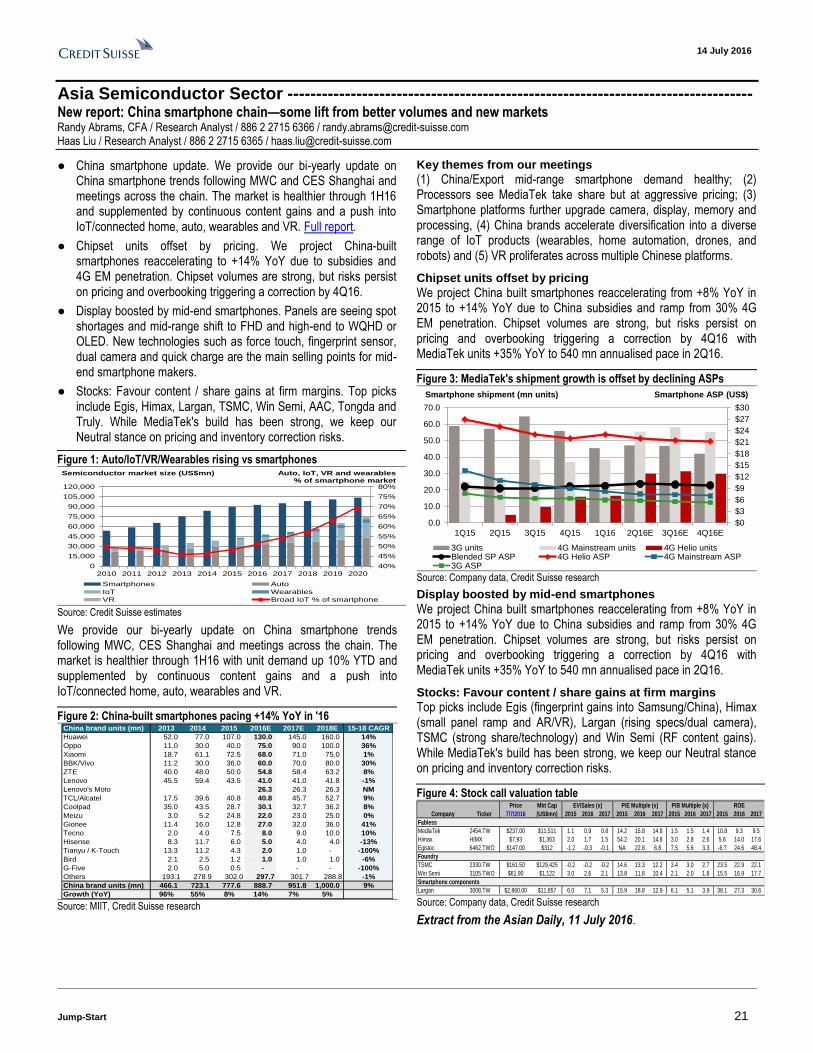

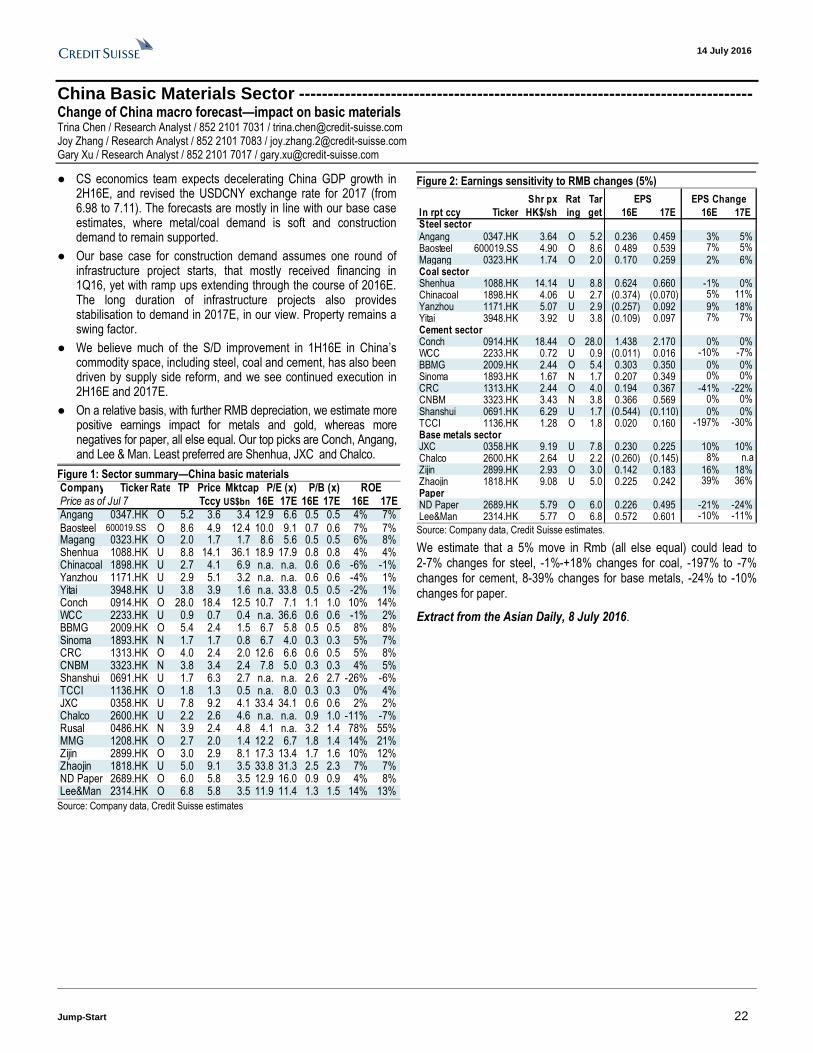

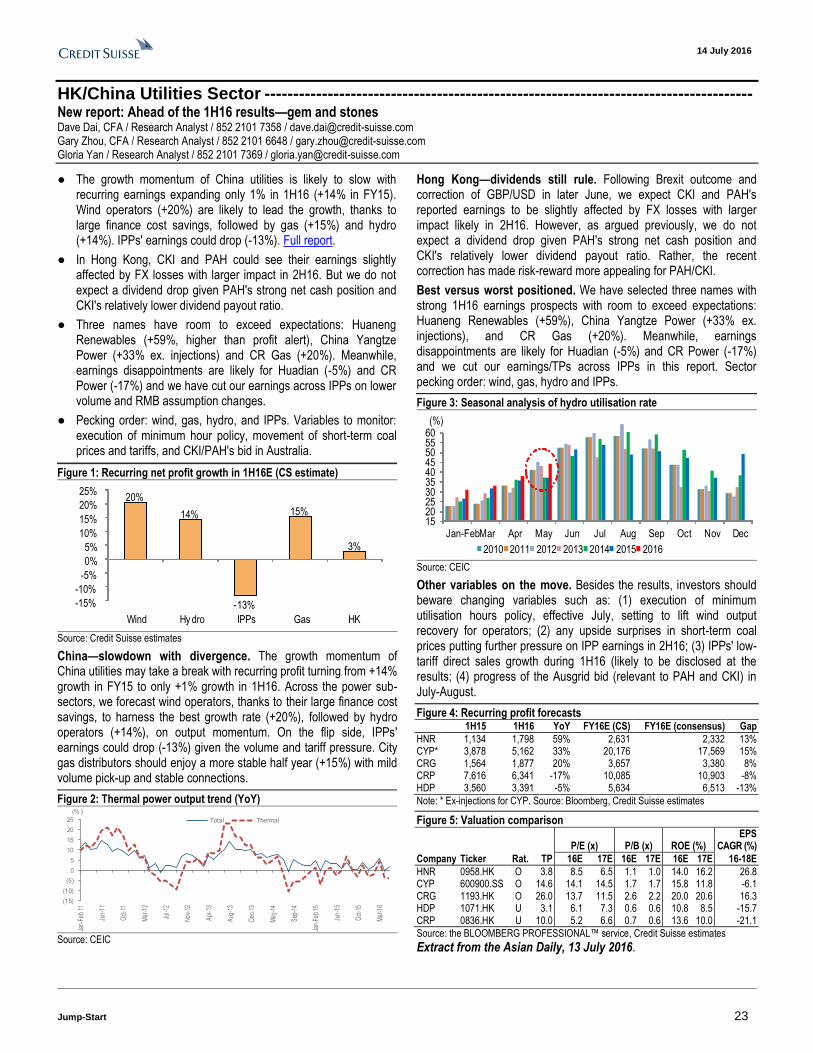

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 14 July 2016 Asia Pacific Equity Research Investment Strategy Jump-Start STRATEGY Jump-Start aims to provide you with a summary of the week that was and helps you prepare for the week ahead with a results calendar, economic forecasts and valuation summaries. China Property Sector: A new chapter—Go for quality. We assume coverage of China Property Sector (6 initiations and 16 assumptions) with MARKETWEIGHT and expect the overall sector to be range-bound amid stable sales outlook in 2H16-17E. In our view, the policy direction is no longer sufficient to drive sector performance and we therefore adopt a bottom-up approach to search for "quality" developers. We have non-consensus UNDERPERFORM calls on Vanke-H and Wanda. Our preferred names include COLI, CRL, Longfor, R&F, CIFI and Yuzhou. (Link) India Automobiles Sector: Mind the (regulatory) gap. India is going on a path of unprecedented tightening of its emissions and safety standards. We believe the market has re- rated auto stocks on possible GST implementation but it is not focusing on the regulatory headwinds ahead. GST implementation would result in a ~5-7% benefit for almost all segments within autos and should help offset some of the negative impact. Overall, gasoline PVs are best positioned as they will have the least price increases over the next four years. We still prefer Maruti as our top pick. (Link) China Internet Sector: Express Delivery—"Served in China". Express delivery service is riding the wave of e-commerce and O2O services boom, and has become an integral part of China's service infrastructure that has enhanced people's everyday life. Third-party express delivery companies such as STO, ZTO and SF Express are the largest beneficiaries of the boom. Our express company performance matrix and comparison analysis on various express delivery players show unit economic efficiency is the key driver for profitability. (Link) Must-read recently published reports 1) India Market Strategy– Agriculture: The problem is plenty (18/5) Neelkanth Mishra Volumes slowed in the past two years to 45-year lows, but the surprise has been price weakness. As India's per capita calorie consumption continues to fall and food habits change, cereal demand has peaked. Where demand is growing supply has grown with improving infrastructure and six years of elevated prices. 2) Research Institute— Emerging Consumer Survey 2016 (31/3) Richard Kersley Weak markets and currencies, and downgraded growth expectations have provided the backdrop to this year’s Emerging Consumer Survey. Negative cyclical influences underscore replies from our consumers, which are generally weaker than a year ago, if differing by country. 3) Asia Tobacco Sector— Emerging Asia Tobacco: Time to switch? (31/5) Arnab Mitra India is the world's most dominated cigarette market (outside China), with ITC having ~77%/96% volume/profit share. ITC's margins are the highest in the world. With FDI in cigarettes being banned, ITC's dominance remains unchallenged. 4) China Internet Sector – Express Delivery: "Served in China (11/7) Evan Zhou Express delivery service is riding the wave of e- commerce and O2O services boom, and has become an integral part of China's service infrastructure that has enhanced people's everyday life. 5) Asia Technology Strategy—Automotive- tech: Asian supply chain (29/6) Manish Nigam Tech products' sales into auto industry (we refer to it as 'automotive-tech') is set to grow rapidly over the coming decade. While the theme by itself isn't new, investors have been looking for Asian tech cos best exposed to this theme. Research Analyst Manish Nigam 852 2101 7067 [email protected] Credit Suisse forthcoming events Thematic Trip China Healthcare Tour Date 18-19 July, Zhengzhou and Beijing Analyst Iris Wang Shenzhen Auto Dealer Visit (Mandarin Speaker Only) Date 19 July, Shenzhen Analyst Bin Wang India Macro Tour – Reforms & Reforms Date 01-03 August, Mumbai, New Delhi Analyst Neelkanth Mishra Indonesia Conference Site Trip – Surabaya; Taking the pulse of Infrastructure, Property and Consumption Date 17-18 August, Surabaya, Indonesia Analyst Jahanzeb Naseer ASEAN Banks Tour – trough valuations? Date 22-26 August, Jakarta, Bangkok, Manila Analyst Sanjay Jain Corporate Days / Conferences 2016 Indonesia Conference Date 15-16 August, Singapore Analyst Jahanzeb Naseer 4th Asia Internet C-Level Conference Date 24-25 August, HK / 26 August, Singapore 17th Annual Asian Technology Conference Date 07-09 September, Taipei Analyst Manish Nigam Macau Gaming Corporate Day Date 13 September, Hong Kong Analyst Kenneth Fong Hong Kong / China (Non-deal roadshow) Vinda International Holdings Ltd (3331.HK) Post results Date 22 July, Hong Kong Analyst Raymond Ching Cheung Kong Infrastructure (1038.HK), Power Assets Holdings Limited (0006.HK) Post results Date 29 July, Hong Kong Analyst Dave Dai Hang Lung Properties (0101.HK) Date 29 July, Hong Kong Analyst Susanna Leung Singapore (Non-deal roadshow) Egis Technology Inc.(6462.TWO) Date 18-19 July, Singapore 20-22 July, Hong Kong Analyst Jerry Su China Gas Holdings Ltd (0384.HK) Post results Date 25-26 July, Singapore Analyst Dave Dai Contact [email protected] or your usual sales representative

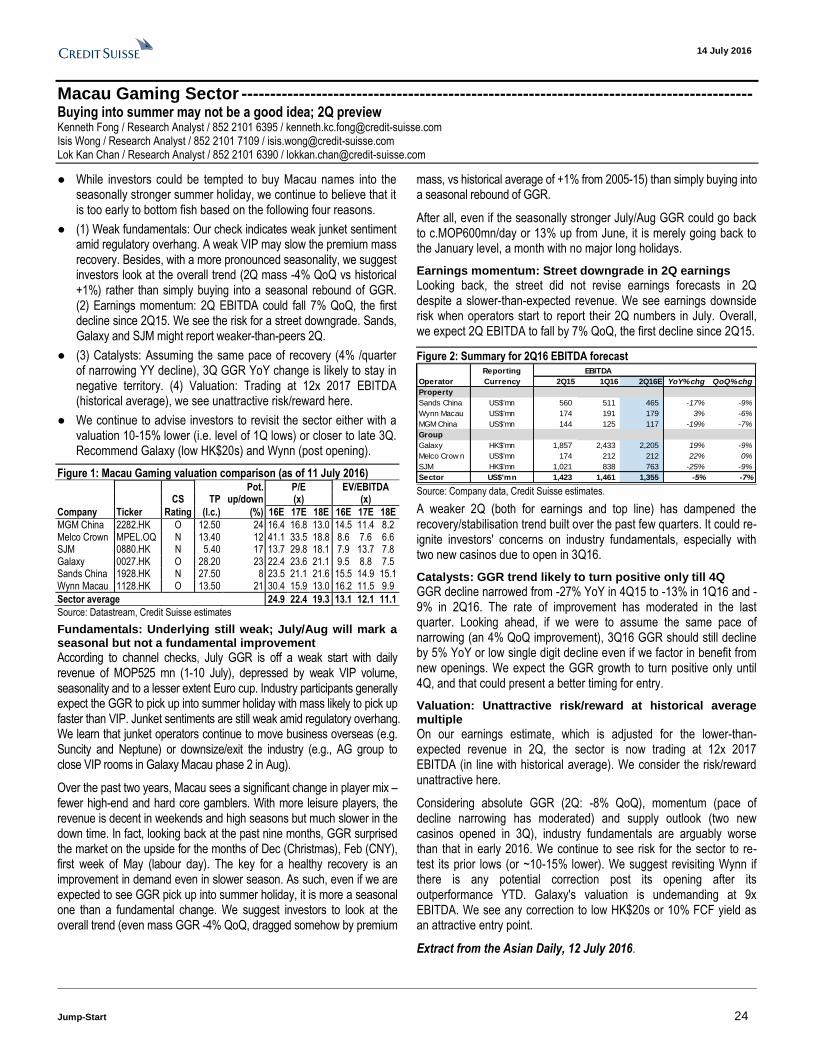

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

14 July 2016

Asia Pacific

Equity Research

Investment Strategy

Jump-Start STRATEGY

Jump-Start aims to provide you with a summary of the week that was and helps you prepare

for the week ahead with a results calendar, economic forecasts and valuation summaries.

China Property Sector: A new chapter—Go for quality. We assume coverage of China

Property Sector (6 initiations and 16 assumptions) with MARKETWEIGHT and expect the overall

sector to be range-bound amid stable sales outlook in 2H16-17E. In our view, the policy direction is

no longer sufficient to drive sector performance and we therefore adopt a bottom-up approach to

search for "quality" developers. We have non-consensus UNDERPERFORM calls on Vanke-H

and Wanda. Our preferred names include COLI, CRL, Longfor, R&F, CIFI and Yuzhou. (Link)

India Automobiles Sector: Mind the (regulatory) gap. India is going on a path of

unprecedented tightening of its emissions and safety standards. We believe the market has re-

rated auto stocks on possible GST implementation but it is not focusing on the regulatory

headwinds ahead. GST implementation would result in a ~5-7% benefit for almost all

segments within autos and should help offset some of the negative impact. Overall, gasoline

PVs are best positioned as they will have the least price increases over the next four years.

We still prefer Maruti as our top pick. (Link)

China Internet Sector: Express Delivery—"Served in China". Express delivery service is

riding the wave of e-commerce and O2O services boom, and has become an integral part of

China's service infrastructure that has enhanced people's everyday life. Third-party express

delivery companies such as STO, ZTO and SF Express are the largest beneficiaries of the

boom. Our express company performance matrix and comparison analysis on various express

delivery players show unit economic efficiency is the key driver for profitability. (Link)

Must-read recently published reports

1) India Market Strategy– Agriculture: The problem is plenty (18/5)

Neelkanth Mishra

Volumes slowed in the past two years to 45-year lows, but the surprise has been price weakness. As India's per capita calorie consumption continues to fall and food habits change, cereal demand has peaked. Where demand is growing supply has grown with improving infrastructure and six years of elevated prices.

2) Research Institute—Emerging Consumer Survey 2016 (31/3)

Richard Kersley Weak markets and currencies, and downgraded growth expectations have provided the backdrop to this year’s Emerging Consumer Survey. Negative cyclical influences underscore replies from our consumers, which are generally weaker than a year ago, if differing by country.

3) Asia Tobacco Sector— Emerging Asia Tobacco: Time to switch? (31/5)

Arnab Mitra India is the world's most dominated cigarette market (outside China), with ITC having ~77%/96% volume/profit share. ITC's margins are the highest in the world. With FDI in cigarettes being banned, ITC's dominance remains unchallenged.

4) China Internet Sector – Express Delivery: "Served in China (11/7)

Evan Zhou Express delivery service is riding the wave of e-commerce and O2O services boom, and has become an integral part of China's service infrastructure that has enhanced people's everyday life.

5) Asia Technology Strategy—Automotive-tech: Asian supply chain (29/6)

Manish Nigam Tech products' sales into auto industry (we refer to it as 'automotive-tech') is set to grow rapidly over the coming decade. While the theme by itself isn't new, investors have been looking for Asian tech cos best exposed to this theme.

Research Analyst

Manish Nigam

852 2101 7067

Credit Suisse forthcoming events

Thematic Trip

China Healthcare Tour

Date 18-19 July, Zhengzhou and Beijing

Analyst Iris Wang

Shenzhen Auto Dealer Visit (Mandarin Speaker Only)

Date 19 July, Shenzhen

Analyst Bin Wang

India Macro Tour – Reforms & Reforms

Date 01-03 August, Mumbai, New Delhi

Analyst Neelkanth Mishra

Indonesia Conference Site Trip – Surabaya; Taking the pulse of Infrastructure, Property and Consumption

Date 17-18 August, Surabaya, Indonesia

Analyst Jahanzeb Naseer

ASEAN Banks Tour – trough valuations?

Date 22-26 August, Jakarta, Bangkok, Manila

Analyst Sanjay Jain

Corporate Days / Conferences

2016 Indonesia Conference

Date 15-16 August, Singapore

Analyst Jahanzeb Naseer

4th Asia Internet C-Level Conference

Date 24-25 August, HK / 26 August, Singapore

17th Annual Asian Technology Conference

Date 07-09 September, Taipei

Analyst Manish Nigam

Macau Gaming Corporate Day

Date 13 September, Hong Kong

Analyst Kenneth Fong

Hong Kong / China (Non-deal roadshow)

Vinda International Holdings Ltd (3331.HK) Post results

Date 22 July, Hong Kong

Analyst Raymond Ching

Cheung Kong Infrastructure (1038.HK), Power Assets Holdings Limited (0006.HK) Post results

Date 29 July, Hong Kong

Analyst Dave Dai

Hang Lung Properties (0101.HK)

Date 29 July, Hong Kong

Analyst Susanna Leung

Singapore (Non-deal roadshow)

Egis Technology Inc.(6462.TWO)

Date 18-19 July, Singapore 20-22 July, Hong Kong

Analyst Jerry Su

China Gas Holdings Ltd (0384.HK) Post results

Date 25-26 July, Singapore

Analyst Dave Dai

Contact [email protected] or your usual sales representative

14 J

uly

201

6

Ju

mp

-Sta

rt 2

Weekly revision review

Company rating/earnings/target price changes

New EPS Old EPS

Last New Old forecasts forecasts % change

New Old closing target target % Curr Curr Curr Curr Curr Curr

Country Date RIC Company rating rating price price price change year yr + 1 year yr + 1 year yr + 1 Analyst

Upgrade

China 11 Jul 3383.HK Agile N U HK$ 3.869 HK$ 4.8 HK$ 2.4 100.0 Rmb 0.6383 Rmb 0.6886 Rmb 0.6681 Rmb 0.7669 -4.46 -10.21 Alvin Wong

China 11 Jul 1109.HK CRL O N HK$ 19.2 HK$ 24.4 HK$ 20.3 20.2 HK$ 2.4071 HK$ 2.884 HK$ 2.4862 HK$ 2.6439 -3.18 9.08 Alvin Wong

China 11 Jul 1813.HK KWG O N HK$ 3.921 HK$ 5.4 HK$ 5 8.0 Rmb 0.9588 Rmb 1.0494 Rmb 0.944 Rmb 1.009 1.57 4.01 Alvin Wong

China 11 Jul 2777.HK R&F O U HK$ 9.549 HK$ 13.2 HK$ 7.7 71.4 Rmb 2.2123 Rmb 2.488 Rmb 2.0607 Rmb 2.2881 7.36 8.74 Alvin Wong

China 11 Jul 2382.HK Sunny Optical O N HK$ 25.078 HK$ 32.5 HK$ 23.3 39.5 Rmb 1.0056 Rmb 1.3235 Rmb 1.0327 Rmb 1.3154 -2.62 0.62 Sam Li

Taiwan 12 Jul 1326.TW FCFC O N NT$ 82.2 NT$ 96 NT$ 78 23.1 NT$ 5.7789 NT$ 5.9793 NT$ 4.4924 NT$ 4.5443 28.64 31.58 Jeremy Chen

Taiwan 13 Jul 6239.TW PTI O N NT$ 73.9 NT$ 85.8 NT$ 78 10.0 NT$ 5.2018 NT$ 6.0018 NT$ 5.2018 NT$ 6.0032 0.00 -0.02 Randy Abrams

Upward revision

China 06 Jul 0291.HK China Res Beer N N HK$ 17.36 HK$ 17.5 HK$ 14.5 20.7 HK$ 0.5611 HK$ 0.6251 HK$ 0.3775 HK$ 0.4355 48.64 43.52 Simon Sun

China 07 Jul 0285.HK BYDE N N HK$ 4.645 HK$ 5.1 HK$ 4.7 8.5 Rmb 0.5279 Rmb 0.5098 Rmb 0.446 Rmb 0.4699 18.37 8.50 Sam Li

China 07 Jul 601238.SS Guangzhou Auto (A) U U Rmb 21.62 Rmb 10.02 Rmb 9.686 3.4 Rmb 1.0014 Rmb 1.1059 Rmb 0.9631 Rmb 1.0543 3.98 4.90 Bin Wang

China 07 Jul 2238.HK Guangzhou Auto (H) O O HK$ 8.601 HK$ 12 HK$ 11.6 3.4 Rmb 1.0014 Rmb 1.1059 Rmb 0.9631 Rmb 1.0543 3.98 4.90 Bin Wang

China 11 Jul 600519.SS Kweichow Moutai O O Rmb 324.73 Rmb 380 Rmb 310 22.6 Rmb 13.9329 Rmb 16.1894 Rmb 13.719 Rmb 15.1506 1.56 6.86 Simon Sun

China 11 Jul 000858.SZ Wuliangye O O Rmb 37.42 Rmb 45 Rmb 36 25.0 Rmb 1.9095 Rmb 2.2648 Rmb 1.8805 Rmb 2.1822 1.54 3.78 Simon Sun

China 11 Jul 002304.SZ Yanghe Brewery O O Rmb 76.12 Rmb 90 Rmb 85 5.9 Rmb 4.0736 Rmb 4.8513 Rmb 4.0417 Rmb 4.8129 0.79 0.80 Simon Sun

China 13 Jul 1347.HK Huahong Semi O O HK$ 0.922 HK$ 11 HK$ 11 0.0 US$ 0.1086 US$ 0.097 US$ 0.1086 US$ 0.0908 0.00 6.79 Randy Abrams

China 13 Jul 0981.HK SMIC O O HK$ 0.083 HK$ 0.93 HK$ 0.93 0.0 US$ 0.0066 US$ 0.0063 US$ 0.0066 US$ 0.0057 0.00 11.30 Randy Abrams

India 06 Jul NTPC.BO NTPC O O Rs 158 Rs 180 Rs 165 9.1 Rs 11.4053 Rs 13.5734 Rs 11.7494 Rs 13.1083 -2.93 3.55 Lokesh Garg

India 07 Jul PGRD.BO PGCIL O O Rs 166.55 Rs 200 Rs 200 0.0 Rs 14.5179 Rs 16.7885 Rs 14.3087 Rs 16.3171 1.46 2.89 Lokesh Garg

India 11 Jul BJFN.BO Bajaj Finance U U Rs 8625.35 Rs 5500 Rs 5500 0.0 Rs 327.9876 Rs 406.0609 Rs 326.0243 Rs 403.7172 0.60 0.58 Sunil Tirumalai

India 11 Jul BHAF.BO Bharat Financial N N Rs 778.65 Rs 660 Rs 660 0.0 Rs 56.3324 Rs 64.2231 Rs 54.7593 Rs 62.5485 2.87 2.68 Sunil Tirumalai

India 11 Jul SRTR.BO Shriram Transport O O Rs 1299.4 Rs 1500 Rs 1200 25.0 Rs 74.7443 Rs 114.2373 Rs 74.7462 Rs 110.719 0.00 3.18 Sunil Tirumalai

India 12 Jul LICH.BO LIC Housing Finance O O Rs 520.85 Rs 625 Rs 590 5.9 Rs 46.0053 Rs 58.7808 Rs 46.1671 Rs 59.0641 -0.35 -0.48 Sunil Tirumalai

Philippines 06 Jul RRHI.PS Robinsons Retail N N P 86.6 P 80.1 P 74.4 7.7 P 3.4809 P 4.034 P 3.5447 P 4.0444 -1.80 -0.26 Sofia Cabral

Singapore 06 Jul MONE.SI M1 U U S$ 2.87 S$ 2.05 S$ 2.05 0.0 S$ 0.1867 S$ 0.1575 S$ 0.184 S$ 0.1564 1.47 0.68 Varun Ahuja

Singapore 06 Jul MACT.SI MCT O O S$ 1.535 S$ 1.64 S$ 1.62 1.2 S$ 0.0675 S$ 0.0815 S$ 0.0784 S$ 0.0798 -13.96 2.13 Nicholas Teh

Singapore 06 Jul STAR.SI StarHub U U S$ 3.91 S$ 3 S$ 3 0.0 S$ 0.218 S$ 0.1892 S$ 0.2157 S$ 0.1889 1.09 0.13 Varun Ahuja

South Korea 06 Jul 005490.KS POSCO O O W 227000 W 280000 W 280000 0.0 W 16060 W 22416 W 14176 W 20508 13.29 9.30 Minseok Sinn

South Korea 08 Jul 130960.KQ CJ E&M O O W 73200 W 91000 W 91000 0.0 W 2530 W 3709 W 2505 W 3678 0.99 0.85 Ray Kim

South Korea 13 Jul 036570.KS NC Soft U U W 255500 W 199000 W 186000 7.0 W 10102 W 10955 W 10132 W 10414 -0.29 5.19 Eric Cha

Taiwan 06 Jul 2324.TW Compal N N NT$ 21.2 NT$ 20 NT$ 19 5.3 NT$ 2.1023 NT$ 2.3722 NT$ 2.033 NT$ 2.3216 3.41 2.18 Thompson Wu

Taiwan 06 Jul 2880.TW Hua Nan Financial N N NT$ 17.05 NT$ 16 NT$ 15.9 0.6 NT$ 1.4156 NT$ 1.4342 NT$ 1.3522 NT$ 1.4297 4.69 0.32 Chung Hsu

Taiwan 06 Jul 2887.TW Taishin Financial N N NT$ 12.75 NT$ 14 NT$ 12.8 9.4 NT$ 1.5824 NT$ 1.5014 NT$ 1.5778 NT$ 1.5319 0.29 -1.99 Chung Hsu

Taiwan 08 Jul 2360.TW Chroma O O NT$ 79.5 NT$ 88 NT$ 84 4.8 NT$ 4.4122 NT$ 4.9565 NT$ 4.4146 NT$ 4.9511 -0.05 0.11 Jerry Su

Taiwan 12 Jul 6505.TW FPCC O O NT$ 88 NT$ 105 NT$ 102 2.9 NT$ 5.933 NT$ 6.21 NT$ 4.8603 NT$ 5.0118 22.07 23.91 Jeremy Chen

Taiwan 12 Jul 1303.TW NYPC N N NT$ 62.5 NT$ 68 NT$ 64 6.3 NT$ 3.8341 NT$ 3.8414 NT$ 4.138 NT$ 4.2728 -7.34 -10.10 Jeremy Chen

Taiwan 13 Jul 2330.TW TSMC O O NT$ 168.5 NT$ 185 NT$ 177 4.5 NT$ 12.1465 NT$ 13.1998 NT$ 12.15 NT$ 13.2001 -0.03 0.00 Randy Abrams

Taiwan 13 Jul 3702.TW WPG N N NT$ 39.3 NT$ 40.2 NT$ 38 5.8 NT$ 3.2738 NT$ 3.8509 NT$ 3.2738 NT$ 3.8001 0.00 1.34 Randy Abrams

14 J

uly

201

6

Ju

mp

-Sta

rt 3

Company rating/earnings/target price changes (continued)

New EPS Old EPS

Last New Old forecasts forecasts % change

New Old closing target target % Curr Curr Curr Curr Curr Curr

Country Date RIC Company rating rating price price price change year yr + 1 year yr + 1 year yr + 1 Analyst

Downgrade

China 11 Jul 0081.HK COGO U O HK$ 2.33 HK$ 1.9 HK$ 3.7 -48.6 HK$ 0.3576 HK$ 0.3545 HK$ 0.7283 HK$ 0.8604 -50.90 -58.79 Alvin Wong

China 11 Jul 3333.HK Evergrande U N HK$ 4.188 HK$ 3.9 HK$ 4.8 -18.8 Rmb 0.0867 Rmb 0.1035 Rmb 0.5575 Rmb 0.6049 -84.44 -82.88 Alvin Wong

China 11 Jul 0817.HK Jinmao N O HK$ 2.26 HK$ 2.2 HK$ 2.7 -18.5 HK$ 0.2608 HK$ 0.305 HK$ 0.2608 HK$ 0.3981 0.03 -23.40 Kelvin Tam

China 11 Jul 0119.HK Poly Prop U O HK$ 2.01 HK$ 1.8 HK$ 2.9 -37.9 HK$ -0.1375 HK$ 0.0112 HK$ 0.0926 HK$ 0.0658 n.m. -82.98 Alvin Wong

China 11 Jul 0813.HK Shimao N O HK$ 8.652 HK$ 10.6 HK$ 14.5 -26.9 Rmb 1.3572 Rmb 1.4168 Rmb 1.9637 Rmb 2.1802 -30.89 -35.01 Kelvin Tam

China 11 Jul 0410.HK SOHO N O HK$ 3.344 HK$ 3.8 HK$ 5.1 -25.5 Rmb 0.0693 Rmb 0.071 Rmb 0.0734 Rmb 0.0789 -5.53 -9.98 Kelvin Tam

China 11 Jul 000002.SZ Vanke-A U O Rmb 18.32 Rmb 10.1 Rmb 20.8 -51.4 Rmb 1.8378 Rmb 2.0055 Rmb 2.0004 Rmb 2.1624 -8.13 -7.26 Alvin Wong

China 11 Jul 2202.HK Vanke-H U O HK$ 13.823 HK$ 12.1 HK$ 25.4 -52.4 Rmb 1.8361 Rmb 2.0037 Rmb 2.046 Rmb 2.4384 -10.26 -17.83 Alvin Wong

China 11 Jul 3699.HK Wanda U O HK$ 41.108 HK$ 35.4 HK$ 60 -41.0 Rmb 3.2751 Rmb 3.4809 Rmb 4.3079 Rmb 4.8702 -23.97 -28.53 Alvin Wong

Hong Kong 11 Jul 1426.HK Spring REIT N O HK$ 0.436 HK$ 3.6 HK$ 3.82 -5.8 US$ 0.0304 US$ 0.0302 US$ 0.034 US$ 0.0336 -10.61 -10.10 Kelvin Tam

Malaysia 11 Jul ALFG.KL Alliance Financial Group N O RM 4.06 RM 4 RM 3.97 0.8 RM 0.3464 RM 0.3815 RM 0.3561 RM 0.385 -2.73 -0.91 Danny Goh

Philippines 12 Jul MCP.PS Melco Crown (Phils) U O P 4.18 P 3.28 P 3.2 2.5 P -0.6582 P -0.3721 P -0.7061 P -0.3784 n.m. n.m. Patricia Palanca

Taiwan 06 Jul 2801.TW Chang Hwa Bank U N NT$ 16.65 NT$ 15 NT$ 16.5 -9.1 NT$ 1.3565 NT$ 1.2535 NT$ 1.3565 NT$ 1.3786 0.00 -9.08 Chung Hsu

Taiwan 06 Jul 2884.TW E. Sun Financial N O NT$ 19.1 NT$ 19.8 NT$ 22.4 -11.6 NT$ 1.8135 NT$ 1.8055 NT$ 1.8138 NT$ 2.0035 -0.02 -9.89 Chung Hsu

Taiwan 06 Jul 2886.TW Mega Financial N O NT$ 24.5 NT$ 25 NT$ 25.5 -2.0 NT$ 2.1194 NT$ 2.171 NT$ 2.2562 NT$ 2.3032 -6.06 -5.74 Chung Hsu

Taiwan 06 Jul 2888.TW Shin Kong FHC U N NT$ 6.4 NT$ 5.4 NT$ 7 -22.9 NT$ 0.509 NT$ 0.518 NT$ 0.509 NT$ 0.5271 0.00 -1.72 Chung Hsu

Taiwan 12 Jul 1301.TW Formosa Plastics N O NT$ 78 NT$ 86 NT$ 90 -4.4 NT$ 4.8076 NT$ 5.0724 NT$ 4.7695 NT$ 5.018 0.80 1.08 Jeremy Chen

Downward revision

China 11 Jul 2007.HK CG U U HK$ 2.818 HK$ 2.6 HK$ 2.6 0.0 Rmb 0.3578 Rmb 0.4176 Rmb 0.458 Rmb 0.4864 -21.88 -14.14 Alvin Wong

China 11 Jul 0941.HK China Mobile O O HK$ 78.509 HK$ 123.5 HK$ 125.17 -1.3 Rmb 5.7039 Rmb 6.1502 Rmb 5.7029 Rmb 6.1503 0.02 0.00 Colin McCallum

China 11 Jul 0728.HK China Telecom O O HK$ 3.12 HK$ 6.85 HK$ 7.55 -9.3 Rmb 0.2491 Rmb 0.3079 Rmb 0.2491 Rmb 0.3078 0.01 0.03 Colin McCallum

China 11 Jul 0762.HK China Unicom O O HK$ 6.86 HK$ 16 HK$ 18 -11.1 Rmb 0.3262 Rmb 0.5255 Rmb 0.3255 Rmb 0.5252 0.22 0.05 Colin McCallum

China 11 Jul 0688.HK COLI O O HK$ 25.6 HK$ 30 HK$ 30.5 -1.6 HK$ 3.0988 HK$ 3.5617 HK$ 3.4523 HK$ 3.9935 -10.24 -10.81 Alvin Wong

China 11 Jul 2369.HK Coolpad U U HK$ 1.32 HK$ 1.15 HK$ 1.2 -4.2 HK$ -0.0305 HK$ 0.0698 HK$ 0.0198 HK$ 0.0705 n.m. -1.10 Kyna Wong

China 11 Jul 3900.HK Greentown O O HK$ 5.093 HK$ 6.7 HK$ 8 -16.3 Rmb 0.4789 Rmb 0.562 Rmb 0.5173 Rmb 0.8423 -7.41 -33.28 Kelvin Tam

China 11 Jul 002475.SZ Luxshare O O Rmb 17.83 Rmb 26 Rmb 29.4 -11.6 Rmb 0.6395 Rmb 0.9109 Rmb 0.7201 Rmb 0.9531 -11.19 -4.43 Sam Li

China 11 Jul 3377.HK Sino-Ocean N N HK$ 2.887 HK$ 3.5 HK$ 4.2 -16.7 Rmb 0.3342 Rmb 0.3944 Rmb 0.4282 Rmb 0.5189 -21.95 -23.99 Alvin Wong

China 11 Jul 1918.HK Sunac U U HK$ 4.43 HK$ 4.1 HK$ 4.5 -8.9 Rmb 0.3433 Rmb 0.3508 Rmb 0.7051 Rmb 0.8437 -51.31 -58.42 Kelvin Tam

China 11 Jul 600050.SS Unicom (A) O O Rmb 4.05 Rmb 5 Rmb 5.6 -10.7 Rmb 0.1282 Rmb 0.1946 Rmb 0.1278 Rmb 0.1945 0.28 0.10 Colin McCallum

China 12 Jul 600871.SS Sinopec SSC (A) U U Rmb 4.25 Rmb 0.9 Rmb 1 -10.0 Rmb -0.2035 Rmb -0.1562 Rmb -0.0509 Rmb 0.0213 n.m. n.m. Horace Tse

China 12 Jul 1033.HK Sinopec SSC (H) U U HK$ 1.396 HK$ 1.1 HK$ 1.2 -8.3 Rmb -0.2035 Rmb -0.1562 Rmb -0.0509 Rmb 0.0213 n.m. n.m. Horace Tse

China 13 Jul 0836.HK CR Power U U HK$ 11.2 HK$ 10 HK$ 11 -9.1 HK$ 2.0978 HK$ 1.6482 HK$ 2.155 HK$ 1.7065 -2.65 -3.42 Dave Dai

China 13 Jul 601991.SS Datang (A) U U Rmb 4.05 Rmb 1.84 Rmb 1.9 -3.2 Rmb 0.2769 Rmb 0.2439 Rmb 0.285 Rmb 0.2511 -2.83 -2.86 Dave Dai

China 13 Jul 0991.HK Datang (H) N N HK$ 1.68 HK$ 2.1 HK$ 2.2 -4.5 Rmb 0.2769 Rmb 0.2439 Rmb 0.285 Rmb 0.2511 -2.83 -2.86 Dave Dai

China 13 Jul 600027.SS HDP (A) U U Rmb 5.12 Rmb 2.8 Rmb 2.9 -3.4 Rmb 0.4931 Rmb 0.4131 Rmb 0.5112 Rmb 0.4274 -3.55 -3.35 Dave Dai

China 13 Jul 1071.HK HDP (H) U U HK$ 3.059 HK$ 3.1 HK$ 3.4 -8.8 Rmb 0.4931 Rmb 0.4131 Rmb 0.5112 Rmb 0.4274 -3.55 -3.35 Dave Dai

China 13 Jul 600011.SS Huaneng (A) U U Rmb 7.2 Rmb 3.7 Rmb 3.8 -2.6 Rmb 0.6806 Rmb 0.5676 Rmb 0.7065 Rmb 0.5863 -3.67 -3.19 Dave Dai

China 13 Jul 0902.HK Huaneng (H) U U HK$ 3.947 HK$ 4 HK$ 4.3 -7.0 Rmb 0.6806 Rmb 0.5676 Rmb 0.7065 Rmb 0.5863 -3.67 -3.19 Dave Dai

Hong Kong 11 Jul 3311.HK CSCI O O HK$ 10.5 HK$ 13.6 HK$ 14.3 -4.9 HK$ 1.1803 HK$ 1.2919 HK$ 1.2332 HK$ 1.3955 -4.29 -7.42 Edmond Huang

India 06 Jul BHEL.BO BHEL U U Rs 138.3 Rs 100 Rs 100 0.0 Rs 4.5689 Rs 5.6068 Rs 4.7163 Rs 6.2112 -3.13 -9.73 Lokesh Garg

India 08 Jul SADE.BO Sadbhav Engg. O O Rs 286.85 Rs 340 Rs 350 -2.9 Rs 7.2501 Rs 8.6992 Rs 7.2501 Rs 8.7011 0.00 -0.02 Lokesh Garg

India 11 Jul INBF.BO Indiabulls Housing O O Rs 743.35 Rs 800 Rs 800 0.0 Rs 73.5807 Rs 91.3765 Rs 76.0698 Rs 94.4555 -3.27 -3.26 Sunil Tirumalai

India 11 Jul INBK.BO IndusInd Bank O O Rs 1124.4 Rs 1301 Rs 1301 0.0 Rs 49.7183 Rs 62.599 Rs 51.4128 Rs 64.656 -3.30 -3.18 Ashish Gupta

India 11 Jul MMFS.BO MMFSL O O Rs 356.75 Rs 410 Rs 410 0.0 Rs 22.9605 Rs 31.2345 Rs 23.5632 Rs 31.9317 -2.56 -2.18 Sunil Tirumalai

India 11 Jul SHCU.BO Shriram City O O Rs 1792.05 Rs 1880 Rs 1880 0.0 Rs 120.0518 Rs 157.0608 Rs 124.5171 Rs 163.9206 -3.59 -4.18 Sunil Tirumalai

India 12 Jul CADI.BO Cadila O O Rs 371.25 Rs 405 Rs 405 0.0 Rs 15.3906 Rs 20.3906 Rs 15.3907 Rs 20.3908 0.00 0.00 Anubhav Aggarwal

India 12 Jul COAL.BO Coal India O O Rs 316.85 Rs 400 Rs 400 0.0 Rs 22.5333 Rs 21.5088 Rs 22.5333 Rs 21.5089 0.00 0.00 Ravi Shankar

14 J

uly

201

6

Ju

mp

-Sta

rt 4

Company rating/earnings/target price changes (continued)

New EPS Old EPS

Last New Old forecasts forecasts % change

New Old closing target target % Curr Curr Curr Curr Curr Curr

Country Date RIC Company rating rating price price price change year yr + 1 year yr + 1 year yr + 1 Analyst

Downward revision

Malaysia 11 Jul RHBC.KL RHB Capital O O RM 5.15 RM 5.69 RM 7.4 -23.1 RM 0.5021 RM 0.5883 RM 0.6538 RM 0.767 -23.21 -23.29 Danny Goh

Malaysia 12 Jul SKPE.KL SapuraKencana N N RM 1.43 RM 1.4 RM 1.4 0.0 RM 0.0646 RM 0.0502 RM 0.0675 RM 0.0725 -4.27 -30.75 Muzhafar Mukhtar

Pakistan 11 Jul EGCH.KA Engro Corp O O PRs 339.11 PRs 375 PRs 410 -8.5 PRs 88.9975 PRs 27.4644 PRs 40.537 PRs 48.2456 119.55 -43.07 Farhan Rizvi

Philippines 07 Jul EMP.PS Emperador N N P 7.33 P 7.6 P 9.9 -23.2 P 0.4201 P 0.4565 P 0.4519 P 0.4956 -7.04 -7.89 Kathi Go

Singapore 06 Jul STEL.SI SingTel O O S$ 4.31 S$ 4.45 S$ 4.45 0.0 S$ 0.2357 S$ 0.25 S$ 0.2376 S$ 0.2503 -0.80 -0.09 Varun Ahuja

South Korea 06 Jul 000270.KS Kia O O W 41850 W 50000 W 61000 -18.0 W 6411 W 7800 W 7500 W 8007 -14.52 -2.59 Michael Sohn

South Korea 11 Jul 018880.KS HanOn U U W 10700 W 8000 W 8000 0.0 W 520 W 574 W 550 W 578 -5.56 -0.64 Michael Sohn

Taiwan 06 Jul 2882.TW Cathay FHC N N NT$ 35.1 NT$ 36 NT$ 40 -10.0 NT$ 3.0556 NT$ 2.927 NT$ 3.0526 NT$ 3.0285 0.10 -3.35 Chung Hsu

Taiwan 06 Jul 2883.TW CDF N N NT$ 7.71 NT$ 8.5 NT$ 8.5 0.0 NT$ 0.4183 NT$ 0.5364 NT$ 0.4566 NT$ 0.5744 -8.38 -6.61 Chung Hsu

Taiwan 06 Jul 2891.TW CTBC Holding O O NT$ 17.65 NT$ 20 NT$ 20 0.0 NT$ 1.5132 NT$ 1.8693 NT$ 1.7313 NT$ 1.9822 -12.60 -5.70 Chung Hsu

Taiwan 06 Jul 2881.TW Fubon FHC N N NT$ 37.9 NT$ 38 NT$ 40.8 -6.9 NT$ 4.0421 NT$ 3.9188 NT$ 4.0422 NT$ 3.9862 0.00 -1.69 Chung Hsu

Taiwan 06 Jul 2498.TW HTC U U NT$ 100 NT$ 57 NT$ 57 0.0 NT$ -3.4786 NT$ 0.5602 NT$ -3.4744 NT$ 0.7411 n.m. -24.41 Pauline Chen

Taiwan 06 Jul 1477.TW Makalot O O NT$ 163 NT$ 180 NT$ 209 -13.9 NT$ 9.9056 NT$ 12.0097 NT$ 11.5703 NT$ 13.8677 -14.39 -13.40 Jeremy Chen

Taiwan 06 Jul 3034.TW Novatek O O NT$ 112.5 NT$ 135 NT$ 140 -3.6 NT$ 9.1667 NT$ 10.2883 NT$ 9.9954 NT$ 11.1579 -8.29 -7.79 Jerry Su

Taiwan 06 Jul 4966.TWO Parade O O NT$ 303 NT$ 375 NT$ 380 -1.3 NT$ 18.5142 NT$ 20.9709 NT$ 18.8343 NT$ 20.9664 -1.70 0.02 Derrick Yang

Taiwan 11 Jul 2890.TW SinoPac Financial O O NT$ 9.85 NT$ 11 NT$ 11.5 -4.3 NT$ 0.9719 NT$ 1.1804 NT$ 1.0352 NT$ 1.0885 -6.12 8.44 Chung Hsu

Thailand 12 Jul DTAC.BK DTAC O O Bt 31.75 Bt 66 Bt 70 -5.7 Bt 1.5941 Bt 1.6978 Bt 2.0802 Bt 2.2579 -23.37 -24.80 Colin McCallum

Initiation

China 11 Jul 0884.HK CIFI O - HK$ 1.68 HK$ 2.5 - n.a. Rmb 0.3793 Rmb 0.4687 - - n.a. n.a. Alvin Wong

China 11 Jul 0207.HK Joy City O - HK$ 1.017 HK$ 1.4 - n.a. Rmb 0.0741 Rmb 0.1103 - - n.a. n.a. Alvin Wong

China 11 Jul 0960.HK Longfor O - HK$ 9.135 HK$ 12.4 - n.a. Rmb 1.3297 Rmb 1.5086 - - n.a. n.a. Alvin Wong

China 11 Jul 0123.HK Yuexiu Prop N - HK$ 0.836 HK$ 1 - n.a. Rmb 0.0989 Rmb 0.1084 - - n.a. n.a. Kelvin Tam

China 11 Jul 0405.HK Yuexiu REIT O - HK$ 3.844 HK$ 5.5 - n.a. Rmb 0.0946 Rmb 0.1036 - - n.a. n.a. Kelvin Tam

China 11 Jul 1628.HK Yuzhou O - HK$ 1.87 HK$ 2.8 - n.a. Rmb 0.4503 Rmb 0.5217 - - n.a. n.a. Alvin Wong

Malaysia 11 Jul WPHB.KL Westports U - RM 4.26 RM 3.7 - n.a. RM 0.1785 RM 0.1839 - - n.a. n.a. Muzhafar Mukhtar

Others

China 11 Jul 0272.HK SOL O O HK$ 1.749 HK$ 2.5 HK$ 2.5 0.0 Rmb 0.2612 Rmb 0.3359 Rmb 0.354 Rmb 0.2668 -26.21 25.93 Kelvin Tam

India 11 Jul GAIL.BO GAIL U U Rs 378.45 Rs 295 Rs 295 0.0 Rs 17.6095 Rs 22.7107 Rs 16.061 Rs 22.7108 9.64 0.00 Badrinath Srinivasan

India 12 Jul CUMM.BO Cummins India N N Rs 816.05 Rs 875 Rs 875 0.0 Rs 27.654 Rs 29.6948 Rs 27.123 Rs 29.7603 1.96 -0.22 Lokesh Garg

South Korea 07 Jul 105560.KS KB Financial O O W 33400 W 46000 W 46000 0.0 W 4669 W 5252 W 4652 W 5272 0.37 -0.39 Gil Kim

Taiwan 06 Jul 2892.TW First FHC N N NT$ 17.15 NT$ 17 NT$ 17 0.0 NT$ 1.381 NT$ 1.3851 NT$ 1.3537 NT$ 1.4073 2.02 -1.57 Chung Hsu

Taiwan 11 Jul 2823.TW China Life Taiwan O O NT$ 26.2 NT$ 30 NT$ 30 0.0 NT$ 2.802 NT$ 2.1314 NT$ 2.121 NT$ 2.1315 32.11 0.00 Chung Hsu

Taiwan 13 Jul 2454.TW MediaTek N N NT$ 247 NT$ 225 NT$ 225 0.0 NT$ 15.4961 NT$ 16.0032 NT$ 15.003 NT$ 16.0043 3.29 -0.01 Randy Abrams

Note: Prices are as of 13 Jul 2016, US$. Entries are organised by changes in rating first, followed by that in target price and earnings. Source: Credit Suisse estimates

14 July 2016

Jump-Start 5

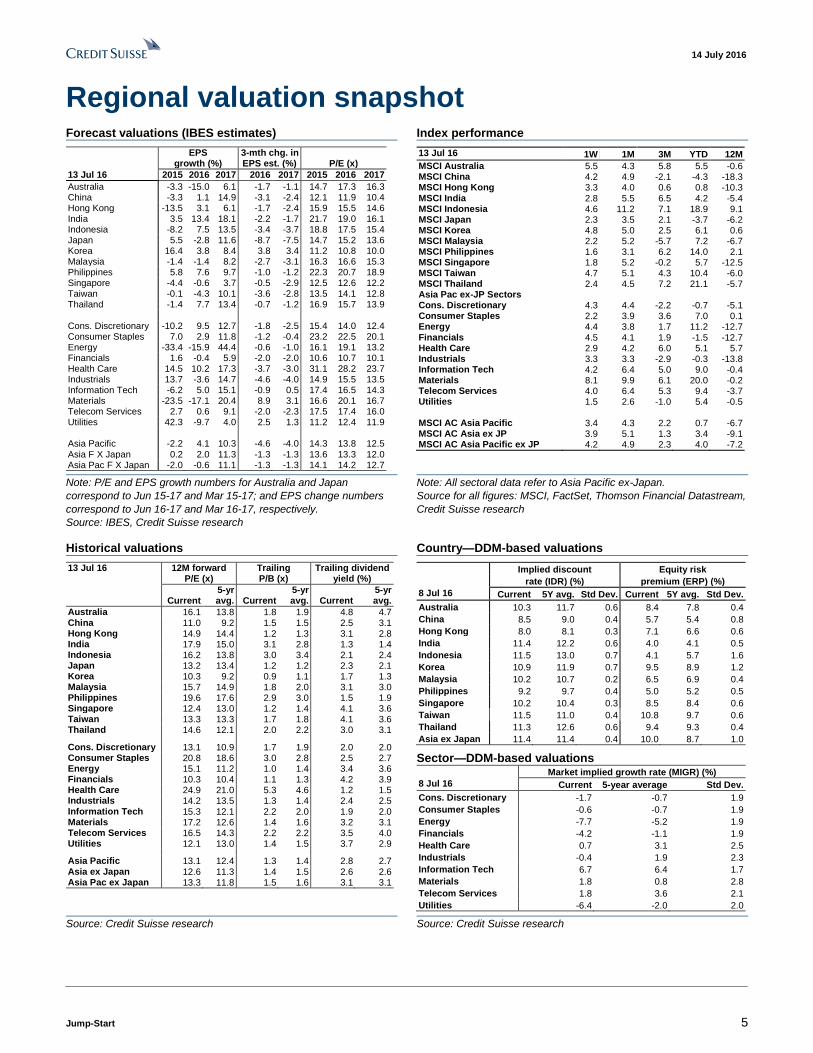

Regional valuation snapshot Forecast valuations (IBES estimates) Index performance

EPS 3-mth chg. in growth (%) EPS est. (%) P/E (x)

13 Jul 16 2015 2016 2017 2016 2017 2015 2016 2017

Australia -3.3 -15.0 6.1 -1.7 -1.1 14.7 17.3 16.3 China -3.3 1.1 14.9 -3.1 -2.4 12.1 11.9 10.4 Hong Kong -13.5 3.1 6.1 -1.7 -2.4 15.9 15.5 14.6 India 3.5 13.4 18.1 -2.2 -1.7 21.7 19.0 16.1 Indonesia -8.2 7.5 13.5 -3.4 -3.7 18.8 17.5 15.4 Japan 5.5 -2.8 11.6 -8.7 -7.5 14.7 15.2 13.6 Korea 16.4 3.8 8.4 3.8 3.4 11.2 10.8 10.0 Malaysia -1.4 -1.4 8.2 -2.7 -3.1 16.3 16.6 15.3 Philippines 5.8 7.6 9.7 -1.0 -1.2 22.3 20.7 18.9 Singapore -4.4 -0.6 3.7 -0.5 -2.9 12.5 12.6 12.2 Taiwan -0.1 -4.3 10.1 -3.6 -2.8 13.5 14.1 12.8 Thailand -1.4 7.7 13.4 -0.7 -1.2 16.9 15.7 13.9 Cons. Discretionary -10.2 9.5 12.7 -1.8 -2.5 15.4 14.0 12.4 Consumer Staples 7.0 2.9 11.8 -1.2 -0.4 23.2 22.5 20.1 Energy -33.4 -15.9 44.4 -0.6 -1.0 16.1 19.1 13.2 Financials 1.6 -0.4 5.9 -2.0 -2.0 10.6 10.7 10.1 Health Care 14.5 10.2 17.3 -3.7 -3.0 31.1 28.2 23.7 Industrials 13.7 -3.6 14.7 -4.6 -4.0 14.9 15.5 13.5 Information Tech -6.2 5.0 15.1 -0.9 0.5 17.4 16.5 14.3 Materials -23.5 -17.1 20.4 8.9 3.1 16.6 20.1 16.7 Telecom Services 2.7 0.6 9.1 -2.0 -2.3 17.5 17.4 16.0 Utilities 42.3 -9.7 4.0 2.5 1.3 11.2 12.4 11.9 Asia Pacific -2.2 4.1 10.3 -4.6 -4.0 14.3 13.8 12.5 Asia F X Japan 0.2 2.0 11.3 -1.3 -1.3 13.6 13.3 12.0 Asia Pac F X Japan -2.0 -0.6 11.1 -1.3 -1.3 14.1 14.2 12.7

13 Jul 16 1W 1M 3M YTD 12M

MSCI Australia 5.5 4.3 5.8 5.5 -0.6 MSCI China 4.2 4.9 -2.1 -4.3 -18.3 MSCI Hong Kong 3.3 4.0 0.6 0.8 -10.3 MSCI India 2.8 5.5 6.5 4.2 -5.4 MSCI Indonesia 4.6 11.2 7.1 18.9 9.1 MSCI Japan 2.3 3.5 2.1 -3.7 -6.2 MSCI Korea 4.8 5.0 2.5 6.1 0.6 MSCI Malaysia 2.2 5.2 -5.7 7.2 -6.7 MSCI Philippines 1.6 3.1 6.2 14.0 2.1 MSCI Singapore 1.8 5.2 -0.2 5.7 -12.5 MSCI Taiwan 4.7 5.1 4.3 10.4 -6.0 MSCI Thailand 2.4 4.5 7.2 21.1 -5.7 Asia Pac ex-JP Sectors Cons. Discretionary 4.3 4.4 -2.2 -0.7 -5.1 Consumer Staples 2.2 3.9 3.6 7.0 0.1 Energy 4.4 3.8 1.7 11.2 -12.7 Financials 4.5 4.1 1.9 -1.5 -12.7 Health Care 2.9 4.2 6.0 5.1 5.7 Industrials 3.3 3.3 -2.9 -0.3 -13.8 Information Tech 4.2 6.4 5.0 9.0 -0.4 Materials 8.1 9.9 6.1 20.0 -0.2 Telecom Services 4.0 6.4 5.3 9.4 -3.7 Utilities 1.5 2.6 -1.0 5.4 -0.5 MSCI AC Asia Pacific 3.4 4.3 2.2 0.7 -6.7 MSCI AC Asia ex JP 3.9 5.1 1.3 3.4 -9.1 MSCI AC Asia Pacific ex JP 4.2 4.9 2.3 4.0 -7.2

Note: P/E and EPS growth numbers for Australia and Japan

correspond to Jun 15-17 and Mar 15-17; and EPS change numbers

correspond to Jun 16-17 and Mar 16-17, respectively.

Source: IBES, Credit Suisse research

Note: All sectoral data refer to Asia Pacific ex-Japan.

Source for all figures: MSCI, FactSet, Thomson Financial Datastream,

Credit Suisse research

Historical valuations Country—DDM-based valuations

13 Jul 16 12M forward P/E (x)

Trailing P/B (x)

Trailing dividend yield (%)

Current 5-yr avg. Current

5-yr avg. Current

5-yr avg.

Australia 16.1 13.8 1.8 1.9 4.8 4.7 China 11.0 9.2 1.5 1.5 2.5 3.1 Hong Kong 14.9 14.4 1.2 1.3 3.1 2.8 India 17.9 15.0 3.1 2.8 1.3 1.4 Indonesia 16.2 13.8 3.0 3.4 2.1 2.4 Japan 13.2 13.4 1.2 1.2 2.3 2.1 Korea 10.3 9.2 0.9 1.1 1.7 1.3 Malaysia 15.7 14.9 1.8 2.0 3.1 3.0 Philippines 19.6 17.6 2.9 3.0 1.5 1.9 Singapore 12.4 13.0 1.2 1.4 4.1 3.6 Taiwan 13.3 13.3 1.7 1.8 4.1 3.6 Thailand 14.6 12.1 2.0 2.2 3.0 3.1 Cons. Discretionary 13.1 10.9 1.7 1.9 2.0 2.0 Consumer Staples 20.8 18.6 3.0 2.8 2.5 2.7 Energy 15.1 11.2 1.0 1.4 3.4 3.6 Financials 10.3 10.4 1.1 1.3 4.2 3.9 Health Care 24.9 21.0 5.3 4.6 1.2 1.5 Industrials 14.2 13.5 1.3 1.4 2.4 2.5 Information Tech 15.3 12.1 2.2 2.0 1.9 2.0 Materials 17.2 12.6 1.4 1.6 3.2 3.1 Telecom Services 16.5 14.3 2.2 2.2 3.5 4.0 Utilities 12.1 13.0 1.4 1.5 3.7 2.9 Asia Pacific 13.1 12.4 1.3 1.4 2.8 2.7 Asia ex Japan 12.6 11.3 1.4 1.5 2.6 2.6 Asia Pac ex Japan 13.3 11.8 1.5 1.6 3.1 3.1

Implied discount Equity risk

rate (IDR) (%) premium (ERP) (%)

8 Jul 16 Current 5Y avg. Std Dev. Current 5Y avg. Std Dev.

Australia 10.3 11.7 0.6 8.4 7.8 0.4

China 8.5 9.0 0.4 5.7 5.4 0.8

Hong Kong 8.0 8.1 0.3 7.1 6.6 0.6

India 11.4 12.2 0.6 4.0 4.1 0.5

Indonesia 11.5 13.0 0.7 4.1 5.7 1.6

Korea 10.9 11.9 0.7 9.5 8.9 1.2

Malaysia 10.2 10.7 0.2 6.5 6.9 0.4

Philippines 9.2 9.7 0.4 5.0 5.2 0.5

Singapore 10.2 10.4 0.3 8.5 8.4 0.6

Taiwan 11.5 11.0 0.4 10.8 9.7 0.6

Thailand 11.3 12.6 0.6 9.4 9.3 0.4

Asia ex Japan 11.4 11.4 0.4 10.0 8.7 1.0

Sector—DDM-based valuations Market implied growth rate (MIGR) (%)

8 Jul 16 Current 5-year average Std Dev.

Cons. Discretionary -1.7 -0.7 1.9

Consumer Staples -0.6 -0.7 1.9

Energy -7.7 -5.2 1.9

Financials -4.2 -1.1 1.9

Health Care 0.7 3.1 2.5

Industrials -0.4 1.9 2.3

Information Tech 6.7 6.4 1.7

Materials 1.8 0.8 2.8

Telecom Services 1.8 3.6 2.1

Utilities -6.4 -2.0 2.0

Source: Credit Suisse research

Source: Credit Suisse research

14 July 2016

Jump-Start 6

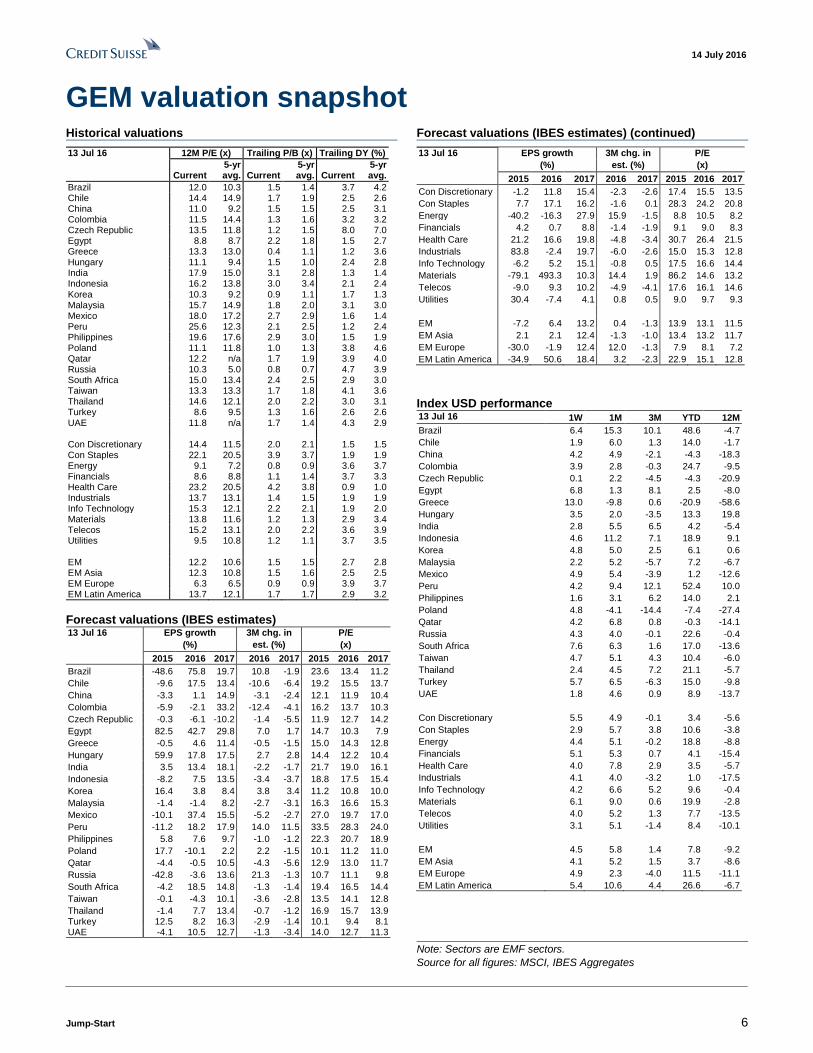

GEM valuation snapshot Historical valuations Forecast valuations (IBES estimates) (continued)

13 Jul 16 12M P/E (x) Trailing P/B (x) Trailing DY (%)

Current 5-yr

avg. Current 5-yr avg. Current

5-yr avg.

Brazil 12.0 10.3 1.5 1.4 3.7 4.2 Chile 14.4 14.9 1.7 1.9 2.5 2.6 China 11.0 9.2 1.5 1.5 2.5 3.1 Colombia 11.5 14.4 1.3 1.6 3.2 3.2 Czech Republic 13.5 11.8 1.2 1.5 8.0 7.0 Egypt 8.8 8.7 2.2 1.8 1.5 2.7 Greece 13.3 13.0 0.4 1.1 1.2 3.6 Hungary 11.1 9.4 1.5 1.0 2.4 2.8 India 17.9 15.0 3.1 2.8 1.3 1.4 Indonesia 16.2 13.8 3.0 3.4 2.1 2.4

Korea 10.3 9.2 0.9 1.1 1.7 1.3 Malaysia 15.7 14.9 1.8 2.0 3.1 3.0 Mexico 18.0 17.2 2.7 2.9 1.6 1.4 Peru 25.6 12.3 2.1 2.5 1.2 2.4 Philippines 19.6 17.6 2.9 3.0 1.5 1.9 Poland 11.1 11.8 1.0 1.3 3.8 4.6 Qatar 12.2 n/a 1.7 1.9 3.9 4.0 Russia 10.3 5.0 0.8 0.7 4.7 3.9 South Africa 15.0 13.4 2.4 2.5 2.9 3.0 Taiwan 13.3 13.3 1.7 1.8 4.1 3.6 Thailand 14.6 12.1 2.0 2.2 3.0 3.1 Turkey 8.6 9.5 1.3 1.6 2.6 2.6 UAE 11.8 n/a 1.7 1.4 4.3 2.9 Con Discretionary 14.4 11.5 2.0 2.1 1.5 1.5 Con Staples 22.1 20.5 3.9 3.7 1.9 1.9 Energy 9.1 7.2 0.8 0.9 3.6 3.7 Financials 8.6 8.8 1.1 1.4 3.7 3.3 Health Care 23.2 20.5 4.2 3.8 0.9 1.0 Industrials 13.7 13.1 1.4 1.5 1.9 1.9 Info Technology 15.3 12.1 2.2 2.1 1.9 2.0 Materials 13.8 11.6 1.2 1.3 2.9 3.4 Telecos 15.2 13.1 2.0 2.2 3.6 3.9 Utilities 9.5 10.8 1.2 1.1 3.7 3.5 EM 12.2 10.6 1.5 1.5 2.7 2.8 EM Asia 12.3 10.8 1.5 1.6 2.5 2.5 EM Europe 6.3 6.5 0.9 0.9 3.9 3.7 EM Latin America 13.7 12.1 1.7 1.7 2.9 3.2

Forecast valuations (IBES estimates) 13 Jul 16 EPS growth 3M chg. in P/E

(%) est. (%) (x)

2015 2016 2017 2016 2017 2015 2016 2017

Brazil -48.6 75.8 19.7 10.8 -1.9 23.6 13.4 11.2

Chile -9.6 17.5 13.4 -10.6 -6.4 19.2 15.5 13.7

China -3.3 1.1 14.9 -3.1 -2.4 12.1 11.9 10.4

Colombia -5.9 -2.1 33.2 -12.4 -4.1 16.2 13.7 10.3

Czech Republic -0.3 -6.1 -10.2 -1.4 -5.5 11.9 12.7 14.2

Egypt 82.5 42.7 29.8 7.0 1.7 14.7 10.3 7.9

Greece -0.5 4.6 11.4 -0.5 -1.5 15.0 14.3 12.8

Hungary 59.9 17.8 17.5 2.7 2.8 14.4 12.2 10.4

India 3.5 13.4 18.1 -2.2 -1.7 21.7 19.0 16.1

Indonesia -8.2 7.5 13.5 -3.4 -3.7 18.8 17.5 15.4

Korea 16.4 3.8 8.4 3.8 3.4 11.2 10.8 10.0

Malaysia -1.4 -1.4 8.2 -2.7 -3.1 16.3 16.6 15.3

Mexico -10.1 37.4 15.5 -5.2 -2.7 27.0 19.7 17.0

Peru -11.2 18.2 17.9 14.0 11.5 33.5 28.3 24.0

Philippines 5.8 7.6 9.7 -1.0 -1.2 22.3 20.7 18.9

Poland 17.7 -10.1 2.2 2.2 -1.5 10.1 11.2 11.0

Qatar -4.4 -0.5 10.5 -4.3 -5.6 12.9 13.0 11.7

Russia -42.8 -3.6 13.6 21.3 -1.3 10.7 11.1 9.8

South Africa -4.2 18.5 14.8 -1.3 -1.4 19.4 16.5 14.4

Taiwan -0.1 -4.3 10.1 -3.6 -2.8 13.5 14.1 12.8

Thailand -1.4 7.7 13.4 -0.7 -1.2 16.9 15.7 13.9 Turkey 12.5 8.2 16.3 -2.9 -1.4 10.1 9.4 8.1 UAE -4.1 10.5 12.7 -1.3 -3.4 14.0 12.7 11.3

13 Jul 16 EPS growth 3M chg. in P/E

(%) est. (%) (x)

2015 2016 2017 2016 2017 2015 2016 2017

Con Discretionary -1.2 11.8 15.4 -2.3 -2.6 17.4 15.5 13.5

Con Staples 7.7 17.1 16.2 -1.6 0.1 28.3 24.2 20.8

Energy -40.2 -16.3 27.9 15.9 -1.5 8.8 10.5 8.2

Financials 4.2 0.7 8.8 -1.4 -1.9 9.1 9.0 8.3

Health Care 21.2 16.6 19.8 -4.8 -3.4 30.7 26.4 21.5

Industrials 83.8 -2.4 19.7 -6.0 -2.6 15.0 15.3 12.8

Info Technology -6.2 5.2 15.1 -0.8 0.5 17.5 16.6 14.4

Materials -79.1 493.3 10.3 14.4 1.9 86.2 14.6 13.2

Telecos -9.0 9.3 10.2 -4.9 -4.1 17.6 16.1 14.6

Utilities 30.4 -7.4 4.1 0.8 0.5 9.0 9.7 9.3

EM -7.2 6.4 13.2 0.4 -1.3 13.9 13.1 11.5

EM Asia 2.1 2.1 12.4 -1.3 -1.0 13.4 13.2 11.7

EM Europe -30.0 -1.9 12.4 12.0 -1.3 7.9 8.1 7.2

EM Latin America -34.9 50.6 18.4 3.2 -2.3 22.9 15.1 12.8

Index USD performance 13 Jul 16 1W 1M 3M YTD 12M

Brazil 6.4 15.3 10.1 48.6 -4.7

Chile 1.9 6.0 1.3 14.0 -1.7

China 4.2 4.9 -2.1 -4.3 -18.3

Colombia 3.9 2.8 -0.3 24.7 -9.5

Czech Republic 0.1 2.2 -4.5 -4.3 -20.9

Egypt 6.8 1.3 8.1 2.5 -8.0

Greece 13.0 -9.8 0.6 -20.9 -58.6

Hungary 3.5 2.0 -3.5 13.3 19.8

India 2.8 5.5 6.5 4.2 -5.4

Indonesia 4.6 11.2 7.1 18.9 9.1

Korea 4.8 5.0 2.5 6.1 0.6

Malaysia 2.2 5.2 -5.7 7.2 -6.7

Mexico 4.9 5.4 -3.9 1.2 -12.6

Peru 4.2 9.4 12.1 52.4 10.0

Philippines 1.6 3.1 6.2 14.0 2.1

Poland 4.8 -4.1 -14.4 -7.4 -27.4

Qatar 4.2 6.8 0.8 -0.3 -14.1

Russia 4.3 4.0 -0.1 22.6 -0.4

South Africa 7.6 6.3 1.6 17.0 -13.6

Taiwan 4.7 5.1 4.3 10.4 -6.0

Thailand 2.4 4.5 7.2 21.1 -5.7

Turkey 5.7 6.5 -6.3 15.0 -9.8

UAE 1.8 4.6 0.9 8.9 -13.7

Con Discretionary 5.5 4.9 -0.1 3.4 -5.6

Con Staples 2.9 5.7 3.8 10.6 -3.8

Energy 4.4 5.1 -0.2 18.8 -8.8

Financials 5.1 5.3 0.7 4.1 -15.4

Health Care 4.0 7.8 2.9 3.5 -5.7

Industrials 4.1 4.0 -3.2 1.0 -17.5

Info Technology 4.2 6.6 5.2 9.6 -0.4

Materials 6.1 9.0 0.6 19.9 -2.8

Telecos 4.0 5.2 1.3 7.7 -13.5

Utilities 3.1 5.1 -1.4 8.4 -10.1

EM 4.5 5.8 1.4 7.8 -9.2

EM Asia 4.1 5.2 1.5 3.7 -8.6

EM Europe 4.9 2.3 -4.0 11.5 -11.1

EM Latin America 5.4 10.6 4.4 26.6 -6.7

Note: Sectors are EMF sectors.

Source for all figures: MSCI, IBES Aggregates

14 July 2016

Jump-Start 7

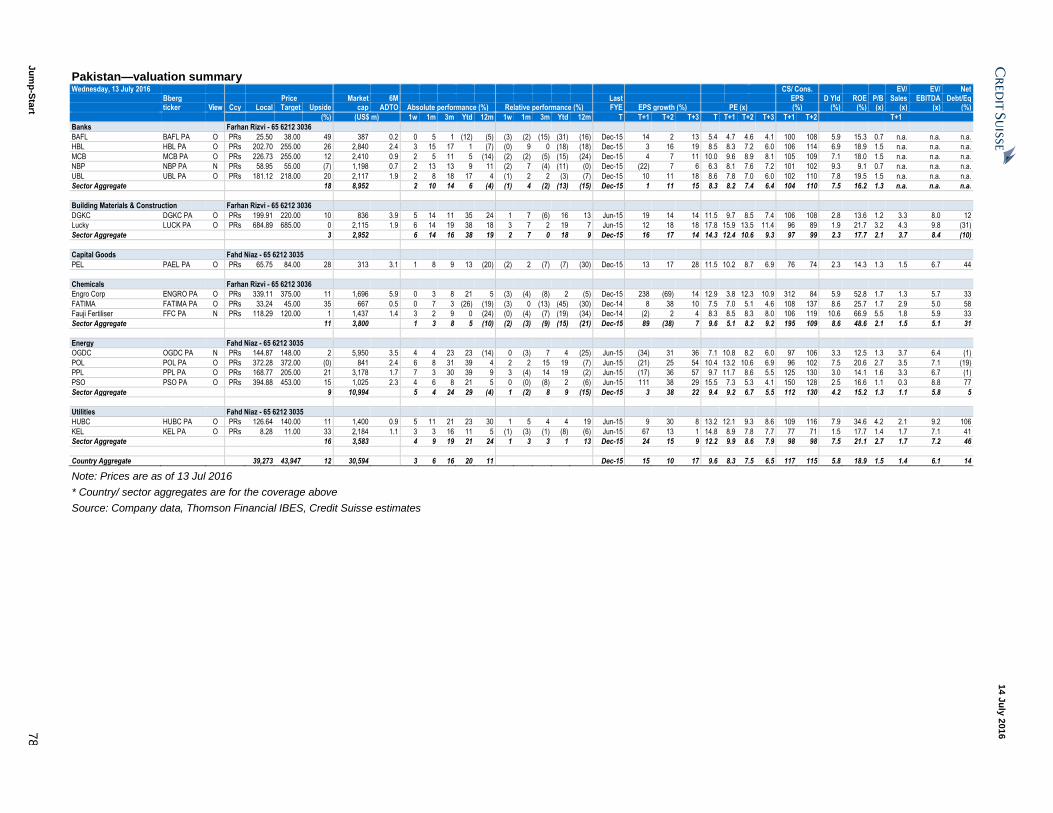

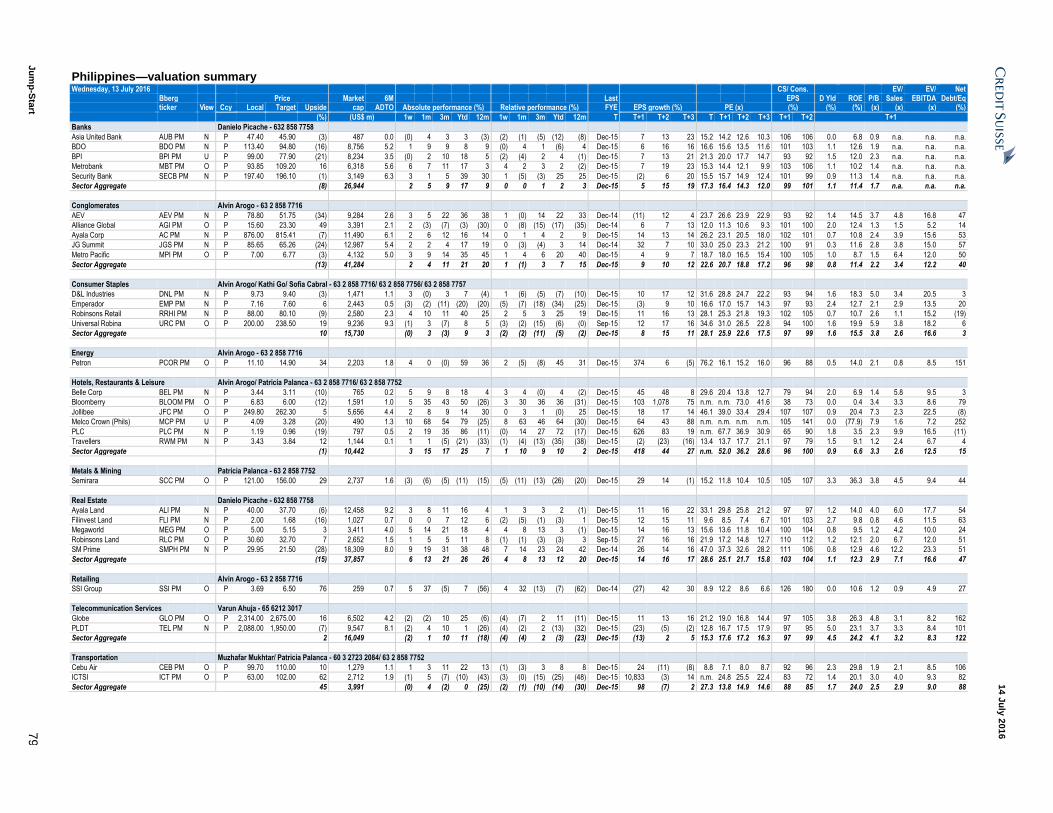

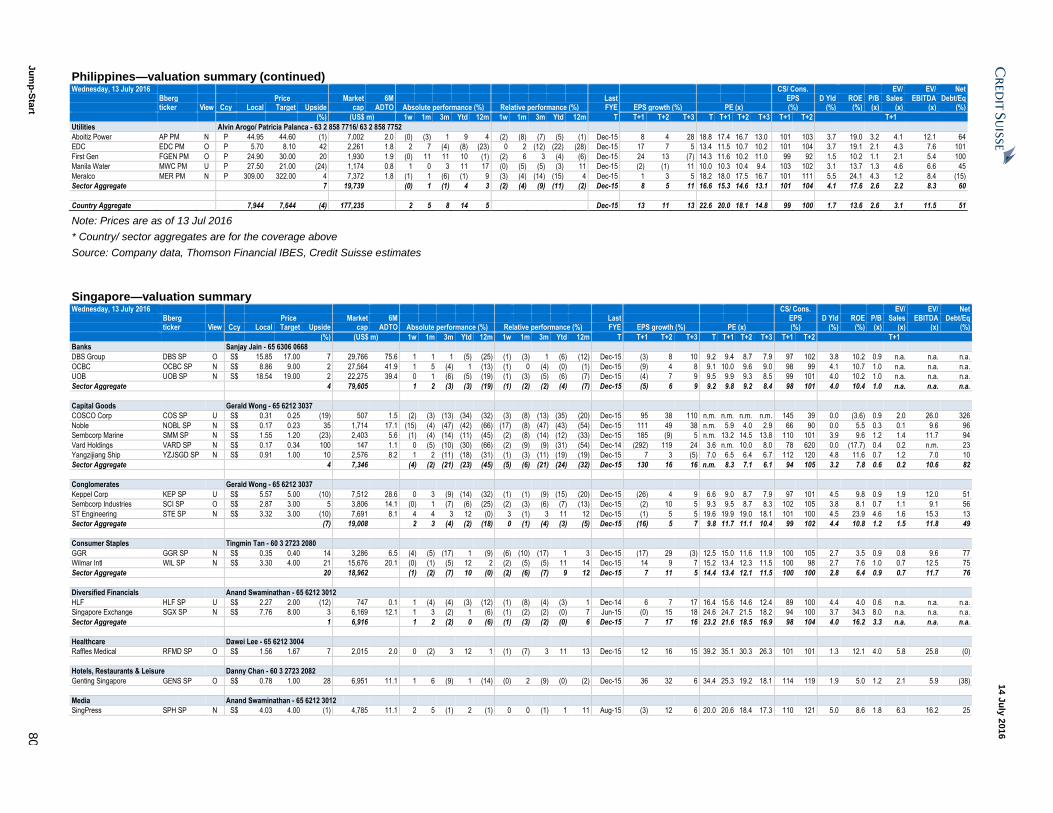

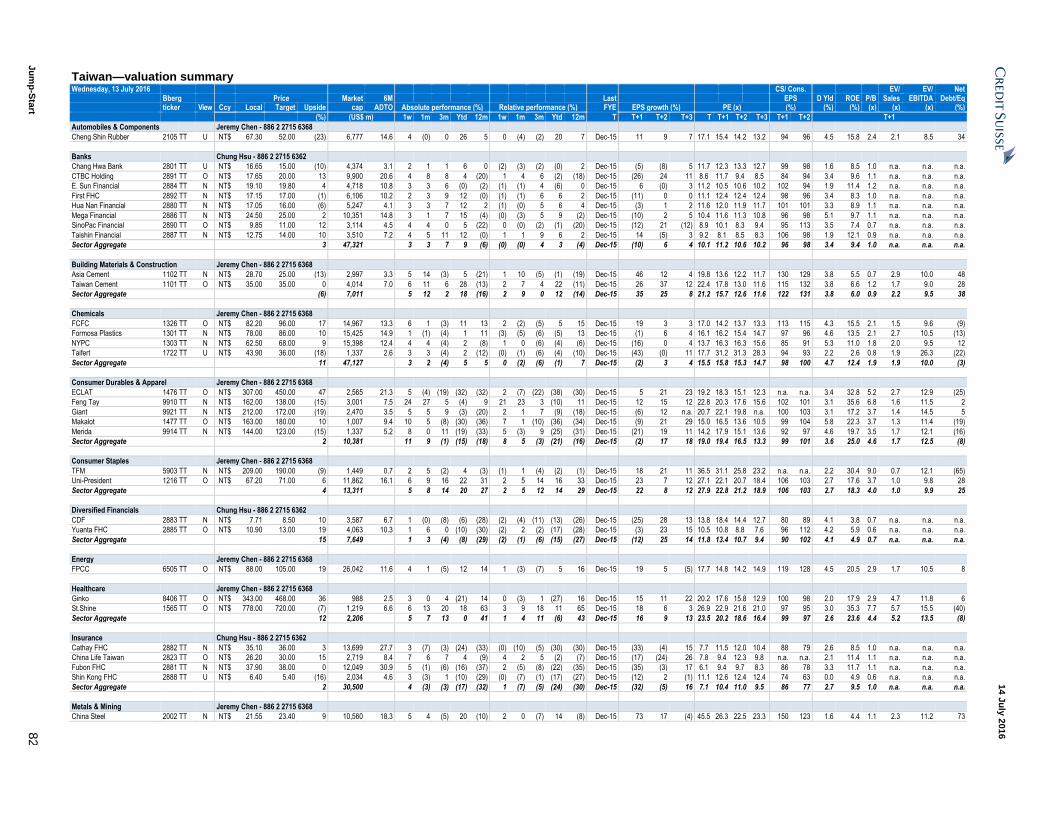

Operational and valuation data showing top ten VALUATION

Top 10 P/E (x) Top 10 P/B (x) Top 10 dividend yield (%)

FY1 FY1 FY1

1 6138.HK Harbin Bank 3.8 1 0119.HK Poly Prop 0.29 1 2455.TW VPEC 11.6

2 EGCH.KA Engro Corp 3.8 2 0845.HK Glorious 0.29 2 FAUF.KA Fauji Fertiliser 10.8

3 1685.HK Boer Power 3.9 3 086790.KS HFG 0.30 3 FATF.KA FATIMA 10.7

4 1055.HK CSA (H) 4.0 4 1133.HK Harbin Electric 0.30 4 5371.TWO Coretronic 10.3

5 1813.HK KWG 4.1 5 3323.HK CNBM 0.31 5 BJBR.JK Bank Jabar Banten 9.5

6 3618.HK CRCB 4.1 6 NOBG.SI Noble 0.32 6 NBPK.KA NBP 9.3

7 1628.HK Yuzhou 4.2 7 IOBK.BO IOB 0.32 7 2777.HK R&F 9.3

8 0486.HK Rusal 4.2 8 1136.HK TCC International 0.33 8 2548.TW Huaku 9.0

9 2777.HK R&F 4.3 9 0683.HK Kerry Prop 0.34 9 6176.TW Radiant 9.0

10 0884.HK CIFI 4.4 10 0123.HK Yuexiu Prop 0.34 10 8086.TWO AWSC 8.7

Top 10 sales growth (%) Top 10 gross margin (%) Top 10 EPS growth (%)

FY1 FY1 FY1

1 6462.TWO Egis Technology 289 1 0323.HK Maanshan (H) 822 1 0853.HK Microport 892

2 COE.N 51Talk 175 2 NOBG.SI Noble 766 2 IFAR.SI Indofood Agri 815

3 IDFB.BO IDFC Bank 155 3 SCMN.SI Sembcorp Marine 291 3 600019.SS Baosteel 696

4 PLC.PS PLC 145 4 COSC.SI COSCO Corp 231 4 PLC.PS PLC 626

5 0272.HK SOL 125 5 3673.TW TPK 222 5 HALC.BO Hindalco 614

6 034730.KS SK Holdings 120 6 010140.KS Samsung Heavy 151 6 005490.KS POSCO 611

7 002074.SZ Guoxuan High-Tech 119 7 0054.HK Hopewell 144 7 ITD.BK ITD 579

8 600900.SS Yangtze Power 111 8 0347.HK Angang Steel (H) 138 8 2331.HK Li Ning 579

9 0570.HK China TCM 106 9 009540.KS Hyundai Heavy 136 9 JKLC.BO JK Lakshmi 571

10 FGVH.KL FGV 94 10 042660.KS DSME 135 10 2686.HK AAG 558

Top 10 ROE (%) Top 10 Free Cashflow Yield (%) Top 10 Net cash/ equity (%)

FY1 FY1 FY1

1 EGCH.KA Engro Corp 52.8 1 COSC.SI COSCO Corp 146 1 DL.N CDEL 164

2 FATF.KA FATIMA 30.7 2 0884.HK CIFI 116 2 ZPIN.N Zhaopin 145

3 HALC.SI Halcyon Agri 30.6 3 0267.HK CITIC 115 3 8044.TWO PChome online 137

4 000625.SZ Changan Auto 30.5 4 0493.HK Gome 96 4 WB.OQ Weibo 136

5 CEB.PS Cebu Air 29.8 5 NOBG.SI Noble 69 5 MRTI.BO Maruti Suzuki 125

6 DIFu.BK DIF 24.4 6 1133.HK Harbin Electric 61 6 JD.OQ JD.com 125

7 LPN.BK L.P.N. 24.4 7 6176.TW Radiant 60 7 JUST.BO Just Dial 124

8 1055.HK CSA (H) 23.8 8 011210.KS Wia 55 8 COAL.BO Coal India 117

9 600674.SS Chuantou 23.5 9 0272.HK SOL 54 9 0493.HK Gome 117

10 AIRX.KL AirAsia X 22.7 10 0123.HK Yuexiu Prop 50 10 600835.SS SMEIC 116

RELATIVE PERFORMANCE

Top 10 performers Bottom 10 performers

1M% 1M%

1 MCP.PS Melco Crown (Phils) 61.6 1 300433.SZ LensTech -68.0

2 PNBK.BO PNB 46.0 2 2233.HK WCC -57.3

3 600188.SS Yanzhou Coal (A) 41.7 3 1836.HK Stella -31.3

4 VDAN.BO Vedanta 32.3 4 000002.SZ Vanke-A -29.3

5 1818.HK Zhaojin 30.5 5 2455.TW VPEC -22.4

6 SSI.PS SSI Group 30.4 6 8086.TWO AWSC -22.3

7 1898.HK CN Coal Energy (H) 30.4 7 1117.HK China Modern Dairy -22.0

8 2899.HK Zijin (H) 28.7 8 VNET.OQ 21 Vianet -19.3

9 2618.HK TCLC 26.7 9 DTAC.BK DTAC -18.5

10 1171.HK Yanzhou Coal (H) 26.7 10 2369.HK Coolpad -18.0

Note: Ratios based on Credit Suisse FY1 estimates. Source: Credit Suisse estimates

14 July 2016

Jump-Start 8

Credit Suisse macroeconomic forecasts

14 July 2016

Jump-Start 9

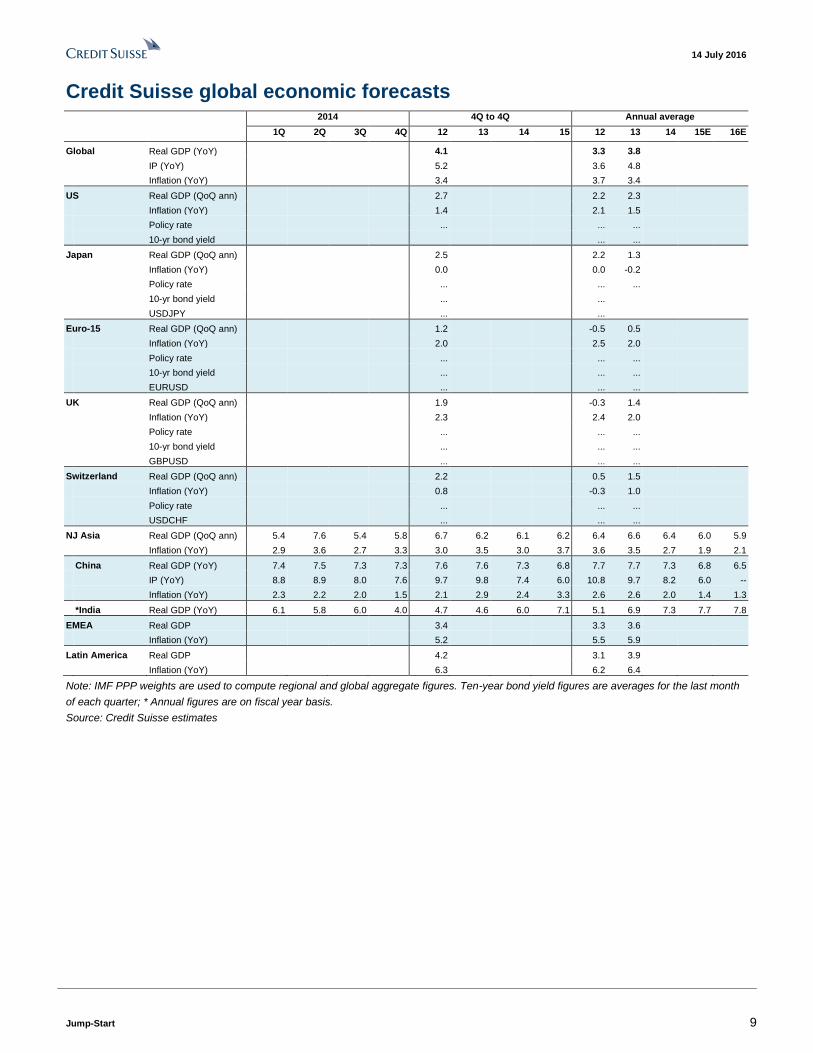

Credit Suisse global economic forecasts

2014 4Q to 4Q Annual average

1Q 2Q 3Q 4Q 12 13 14 15 12 13 14 15E 16E

Global Real GDP (YoY) 4.1 3.3 3.8 IP (YoY) 5.2 3.6 4.8 Inflation (YoY) 3.4 3.7 3.4

US Real GDP (QoQ ann) 2.7 2.2 2.3 Inflation (YoY) 1.4 2.1 1.5 Policy rate ... ... ... 10-yr bond yield ... ...

Japan Real GDP (QoQ ann) 2.5 2.2 1.3 Inflation (YoY) 0.0 0.0 -0.2 Policy rate ... ... ... 10-yr bond yield ... ... USDJPY ... ...

Euro-15 Real GDP (QoQ ann) 1.2 -0.5 0.5 Inflation (YoY) 2.0 2.5 2.0 Policy rate ... ... ... 10-yr bond yield ... ... ... EURUSD ... ... ...

UK Real GDP (QoQ ann) 1.9 -0.3 1.4 Inflation (YoY) 2.3 2.4 2.0 Policy rate ... ... ... 10-yr bond yield ... ... ... GBPUSD ... ... ...

Switzerland Real GDP (QoQ ann) 2.2 0.5 1.5 Inflation (YoY) 0.8 -0.3 1.0 Policy rate ... ... ... USDCHF ... ... ...

NJ Asia Real GDP (QoQ ann) 5.4 7.6 5.4 5.8 6.7 6.2 6.1 6.2 6.4 6.6 6.4 6.0 5.9

Inflation (YoY) 2.9 3.6 2.7 3.3 3.0 3.5 3.0 3.7 3.6 3.5 2.7 1.9 2.1

China Real GDP (YoY) 7.4 7.5 7.3 7.3 7.6 7.6 7.3 6.8 7.7 7.7 7.3 6.8 6.5 IP (YoY) 8.8 8.9 8.0 7.6 9.7 9.8 7.4 6.0 10.8 9.7 8.2 6.0 -- Inflation (YoY) 2.3 2.2 2.0 1.5 2.1 2.9 2.4 3.3 2.6 2.6 2.0 1.4 1.3

*India Real GDP (YoY) 6.1 5.8 6.0 4.0 4.7 4.6 6.0 7.1 5.1 6.9 7.3 7.7 7.8

EMEA Real GDP 3.4 3.3 3.6 Inflation (YoY) 5.2 5.5 5.9

Latin America Real GDP 4.2 3.1 3.9 Inflation (YoY) 6.3 6.2 6.4

Note: IMF PPP weights are used to compute regional and global aggregate figures. Ten-year bond yield figures are averages for the last month

of each quarter; * Annual figures are on fiscal year basis.

Source: Credit Suisse estimates

14 July 2016

Jump-Start 10

Credit Suisse Asian economic forecasts

Consensus

2013 2014 2015 2016E 2015 2016E 2017E

China Real GDP 7.7 7.3 6.9 6.5 6.9 6.5 6.3

Inflation 2.6 2.0 1.4 2.0 1.4 1.9 1.8

3-month interbank rate (year-end) 5.6 4.7 3.1 3.0 … … …

12m

Currency, per USD 6.78 6.20 6.43 6.84 … … …

Hong Kong Real GDP 3.1 2.5 2.4 1.3 2.4 1.7 1.9

Inflation 4.3 4.4 3.0 2.9 3.0 2.4 1.9

3-month HIBOR (year-end) 0.4 0.4 0.6 1.0 … … …

12m

Currency, per USD 7.80 7.76 7.75 7.80 … … …

India Real GDP 6.6 7.2 7.6 7.8 7.4 7.6 7.7

Inflation 9.5 9.9 4.9 5.2 5.0 5.1 5.1

Repo rate (year-end) 8.00 7.50 6.75 6.25 … … …

12m

Currency, per USD 71.00 62.50 66.30 70.00 … … …

Indonesia Real GDP 5.6 5.0 4.8 5.2 4.8 5.0 5.3

Inflation 6.4 6.4 6.4 4.0 6.4 4.3 4.9

Overnight SBI yield (year-end) 7.50 7.75 7.50 6.00 … … …

12m

Currency, per USD 14,200 12,440 13,795 13,800 … … …

Korea Real GDP 3.0 3.3 2.5 2.4 2.6 2.6 2.8

Inflation 1.3 1.3 0.7 1.0 0.7 1.2 1.8

Overnight call rate (year-end) 2.50 2.00 1.50 1.00 … … …

12m

Currency, per USD 1,245 1,100 1,170 1,210 … … …

Malaysia Real GDP 4.7 6.0 5.0 4.1 4.8 4.2 4.4

Inflation 2.1 3.1 2.1 2.2 2.1 2.5 2.7

Overnight Policy rate (year-end) 3.00 3.25 3.25 3.00 … … …

12m

Currency, per USD 4.25 3.50 4.29 4.23 … … …

Philippines Real GDP 7.1 6.2 5.9 6.2 5.8 5.9 5.9

Inflation 2.9 4.2 1.4 1.9 1.4 1.8 2.8

Overnight borrowing rate (year-end) 3.50 4.00 4.00 3.00 … … …

12m

Currency, per USD 47.50 44.62 47.17 47.00 … … …

Singapore Real GDP 4.7 3.3 2.0 1.3 2.0 1.7 2.2

Inflation 2.4 1.0 -0.5 -0.9 -0.5 -0.3 1.0

3m SIBOR (year-end) 0.4 0.5 1.2 1.3 … … …

12m

Currency, per USD 1.50 1.32 1.41 1.41 … … …

Taiwan Real GDP 2.2 3.9 0.7 1.2 0.9 1.3 2.1

Inflation 1.0 1.2 -0.3 0.4 -0.3 1.0 1.2

Overnight call rate (year-end) 0.4 0.4 0.3 0.2 … … …

12m

Currency, per USD 34.40 31.45 32.80 33.80 … … …

Thailand Real GDP 2.7 0.8 2.8 2.7 2.7 2.9 3.3

Inflation 2.2 1.9 -0.9 0.6 -0.9 0.4 1.9

Overnight Repo rate (year-end) 2.3 2.0 1.5 1.3 … … …

12m

Currency, per USD 36.50 32.90 35.99 36.20 … … …

* Through 2006, Thailand's policy rate was the 14-day repo rate

Source: CEIC, Asia Pacific Consensus Forecasts, Credit Suisse estimates

14 July 2016

Jump-Start 11

Real interest rates Real policy rates

1

Annual forecast

Current 2015 2016(F) 2017(F)

China 2.45 1.60 1.13 1.13

Hong Kong -2.05 -1.83 -0.79 -0.01

India 0.73 1.65 1.05 1.05

Indonesia 3.05 2.69 2.13 1.49

Korea 0.45 0.44 -0.27 -0.52

Malaysia 1.00 0.65 1.10 0.50

Philippines 1.10 3.01 0.50 0.10

Singapore 1.73 1.91 2.25 1.85

Taiwan 0.48 -0.08 -0.53 -1.32

Thailand 1.12 2.37 -0.35 -0.56

1 NJA Policy Rates: China=End Year Lending Rate, Hong kong-3 month interbank rate, India- Repo rate,

Indonesia-Overnight Rate, Korea- Base rate, Malaysia-overnight Rate, Philippines-Reverse repo rate,

Singapore-3 month interbank rate, Taiwan: Discount rate, Thailand- Overnight repo rate

2 NJA stands for Non-Japan Asia

Source: Central banks, CEIC, Statistical agencies, Credit Suisse

14 July 2016

Jump-Start 12

Top stories from Credit Suisse research last week

14 July 2016

Jump-Start 13

China Property Sector -------------------------- Assuming Coverage with MARKET WEIGHT New report: A new chapter—Go for quality Alvin Wong / Research Analyst / 852 2101 6486 / [email protected] Kelvin Tam, CFA / Research Analyst / 852 2101 6582 / [email protected] Jizhou Dong / Research Analyst / 852 2101 6538 / [email protected]

● We assume coverage of the China Property Sector (6 initiations and 16 assumptions) with a MARKET WEIGHT view and expect the overall sector to be range-bound amid a stable sales outlook in 2H16-17E. In our view, the policy direction itself is no longer sufficient to drive sector performance and we therefore adopt a bottom-up approach to search for "quality" developers. Full report.

● Sustainable sector rally existed only when developers generated positive FCF on aggregate. Bankruptcy is always a major concern. With this, developers have to show their sincerity to strengthen their balance sheets by improving their cashflow positions.

● The strategy of aiming for market-share gain (by contracted sales) but neglecting the profitability is not an ideal business model. We prefer developers to consistently report above sector-average earnings growth so as to gain the "earnings" share.

● We have non-consensus UNDERPERFORM calls on Vanke-H (management overhang) and Wanda (risk of privatisation failure). Our preferred names include COLI, CRL, Longfor, R&F, CIFI and Yuzhou.

Figure 1: We expect a range-bound market over 2H16-17

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Yoy change in commodity property GFA sold (LHS) NAV discount (RHS)

1 2 3 4 5 1 2 3 4 5 1 2

Source: CEIC, the BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates

Strength to rise above policy

We forecast commodity property sales growth of 10.4% and 1% YoY in 2016E and 2017E, respectively. This leads us to the midway between moderation and stabilisation phase of a property cycle where we see low chance of a sustainable sector rally. Looking forward, the overall policy stance should remain supportive amid a slowing economy, yet we have been seeing rising policy risks across first-tier cities and some second-tier cities. In our view, the policy direction itself is no longer sufficient to drive the sector performance and this requires a bottom-up investment approach for stock selection.

Positive free cashflow is the real key

Two sustainable sector rallies appeared in Aug-08–Jul-09 and Feb-12–Feb-13 only when developers generated positive FCF on aggregate by slowing down both new-starts and land purchases. Looking into 2H16E, most developers should focus on destocking, yet the overall sector's FCF will be dragged by several aggressive developers like Evergrande, CG and Sunac. Bankruptcy is always a major investment concern. Developers have to show their sincerity to strengthen their B/S by improving their cashflow positions.

Figure 2: Positive FCF is the key driver of sector outperformance

-50

0

50

100

150

200

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

60%

70% 3%

CS China Property H Shares Index ––– (tightening) ––– (easing) ––– (tightening/easing)+ / - indicate sector's FCF, which we expect to be negative in 2016E

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research

Earnings share gain is a new theme

Rather than simply looking at developers' top-line numbers (i.e., contracted sales), it is even more important to focus on their bottom-line figures (i.e., profitability). We have been seeing many volume-driven developers such as Evergrande and Sunac gaining market share (by contracted sales) at the expense of declining profits and deteriorating balance sheets; while balanced-growth developers such as COLI and CRL have consistently gained market share (by core profits) with stable margins and healthy net gearings.

Figure 3: China property—2016E market-share gain

16.2%1.0%

6.4%21.2%

11.1%11.8%

0.9%3.7%

6.2%0.8%

5.7%2.0%2.0%2.0%2.1%

0.0%1.0%

2.3%1.4%

0.5%1.7%

Market share by core profit 2016E

17.2%12.8%

10.1%9.9%

6.1%6.1%

4.8%4.1%4.0%3.9%3.6%

2.8%2.7%2.6%

1.8%1.7%1.5%1.3%1.1%1.1%0.8%

Vanke-H

Evergrande

CG

COLI

CRL

Wanda

Sunac

Shimao

Longfor

Greentown

R&F

Agile

Sino-Ocean

CIFI

Jinmao

Poly Prop

Yuexiu Prop

KWG

Yuzhou

COGO

SOL

Market share by presales 2016E

Note: We expect Poly Prop to report core profit loss in FY16E. Source: Company data, Credit Suisse research

Non-consensus Underperforms: Vanke-H and Wanda

Unless there is any significant change in either GDP or policy direction, we believe the current sector NAV discount of 34% suggests limited upside potential, compared to an average NAV discount of 29% over the last moderation/stabilisation period (i.e., Mar-13–Dec-13). In our view, developers' share price performance will be differentiated from their individual business and operating performance. In addition to the above-mentioned key investment themes (i.e., positive cashflow and earnings share gain), we also study developers' land bank exposure which is a traditional way to gauge their quality. Our non-consensus UNDERPERFORM calls include Vanke-H (management overhang) and Wanda (risk of privatisation failure) while our preferred names include COLI, CRL, Longfor, R&F, CIFI and Yuzhou.

Extract from the Asian Daily, 12 July 2016.

14 July 2016

Jump-Start 14

India Automobiles Sector ------------------------------------------------------------------------------------ New report: Mind the (regulatory) gap Jatin Chawla / Research Analyst / 91 22 6777 3719 / [email protected] Akshay Saxena / Research Analyst / 91 22 6777 3825 / [email protected]

● India is going on a path of unprecedented tightening of its emissions and safety standards. We believe the market has re-rated auto stocks on possible GST implementation but it is not focusing on the regulatory headwinds ahead. Full report

● In order to assess the impact, we focus on (1) cost increases, and (2) the ability to pass them on. 2Ws will face cost increases of ~12-15%, in our view; given the competitive intensity, they also have the least ability to pass them on fully. Given the significant reduction required in emissions of diesel vehicles, CVs (~20% increase) and diesel PVs (~15%) have to incur sizeable cost of compliance.

● GST implementation would result in a ~5-7% benefit for almost all segments within autos and should help offset some of the negative impact. Overall, gasoline PVs are best positioned as they will have the least price increases over the next four years.

● We still prefer Maruti as our top pick and raise TP to Rs4,810 (from Rs4,540); downgrade Hero Motocorp to UNDERPERFORM (~15% downside); and stay UNDERPERFORM on TVS, as it will be difficult for it to show margin improvement amid such cost increases.

Figure 1: Gasoline PVs to see the least adverse impact from regulations

-1%

2% 2%

-2% -2%

5%

8%

12%

0%

8%

-4%

0%

4%

8%

12%

2W's (<125cc) 2W (>125 cc) CV's PV's (Gasoline) PV's (diesel)

Price increase needed by 2019 (BS-IV + Safety net of GST benefit)

Total by 2020 (BS-VI additional) Source: Company data, ICCT, Credit Suisse estimates

2Ws: Compliance costs much higher than GST benefit. For 2Ws, we expect the regulatory cost increases to offset the entire 6% price reduction that can happen from the GST. Movement to BS-IV emission standards from Apr-2017 should result in a ~2% price increase. 2Ws have generally had lenient emission standards when compared to cars but with BS-VI being implemented from Apr-2020, 2Ws also have very tough standards to meet. This would entail a further ~6% increase in prices. Similarly, on the safety side too, India

is taking a big lead when compared to ASEAN nations by making ABS (Anti-lock braking system) compulsory for >125cc vehicles and CBS (Combined braking system) compulsory for <125cc vehicles, which would mean a further 6%/3% price increase.

CVs: Highest cost impact from regulations. Commercial vehicles face the biggest cost increase going forward, primarily on higher emission compliance costs. BS-IV implementation from Apr-2017 will result in a ~7% price increase. Further going forward with BS-VI implementation in Apr-2020; CVs would need a further ~10% price increase. The safety compliance has already happened with the ABS implementation in Oct-2015. For CVs, price increases don’t tend to impact demand very significantly as that is more linked to freight demand. However, GST implementation can lead to an increase in the freight carrying capacity as truck travel becomes more efficient and hence could negatively impact demand. If the proposed voluntary scrappage plan were to be implemented it could take out some truck capacity from the system, but it has implementation challenges.

PVs: Gasoline vehicles are best placed. PVs by and large are already compliant with BS-IV emission norms and hence emission-related cost increases will happen only with BS-VI in Apr-2020. Even then, the price increase on gasoline vehicles will not be very significant. However, diesel vehicles will need a ~10% increase. On the safety side too, the implementation in cars is later than that in 2Ws and CVs. While new vehicles need to comply with both the frontal and lateral crash norms by Oct-2017, existing vehicles need to do so only by Oct-2018 for lateral collisions and Oct-2019 for frontal collisions.

Figure 2: Timeline for the implementation of emission norms in the country Norm Deadline Segment Technology and required price increase

BS-IV Apr-17 2W Improving oxidation catalyst (~2% increase) BS-IV Apr-17 CV Common rail fuel injection (~7% increase) BS-IV Apr-17 PV Already Compliant BS-VI Apr-20 2W Fuel injection technology (~6% increase) BS-VI Apr-20 CV After-treatment system (~10% increase) BS-VI Apr-20 PV Small change in gasoline, big in diesel

Source: MORTH, company data, ICCT, Credit Suisse

Figure 3: Timeline for the implementation of safety norms in the country Segment Deadline Regulation and required price increase

New 2W models Apr-18 ABS for >125cc (~6%), CBS for <125cc (~3%) All 2Ws Apr-19 ABS for >125cc, CBS for <125cc CVs Oct-15 ABS implementation already done New PV models Oct-17 Crash norms complaint (4-5% price increase in total) All PVs Oct-18 Lateral collision crash norm All PVs Oct-19 Fully complaint with crash norm (Frontal collision also)

Source: MORTH, company data, Credit Suisse

Valuation metrics

Rating TP Up/dn Div. yld ROE P/B Company Ticker (prev. Price chg to TP Year EPS chg (%) EPS EPS grth (%) P/E (x) (%) (%) (x)

rating) Local Target (%) (%) T T+1 T+2 T+1 T+2 T+1 T+2 T+1 T+2 T+1 T+1 T+1

Maruti Suzuki MRTI.BO O (O) 4,370 4,810 (4,540) 5.9 10 03/15 0 0 152 205 23 35 28.8 21.3 0.9 18.1 4.9 Hero Motocorp HROM.BO U (N) 3,244 2,750 (2,590) 6.2 (15) 03/15 0 0 157 170 23 8 20.7 19.1 2.3 43.2 8.1

Source: Company data, Credit Suisse estimates

Extract from the Asian Daily, 14 July 2016.

14 July 2016

Jump-Start 15

China Internet Sector ------------------------------------------------------------------------------------------ New report: Express Delivery—"Served in China"

Evan Zhou / Research Analyst / 852 2101 6745 / [email protected] Monica Chen / Research Analyst / 852 2101 7150 / [email protected]

● Express delivery service is riding the wave of e-commerce and O2O services boom, and has become an integral part of China's service infrastructure that has enhanced people's everyday life. Full report.

● Profitable growth. Third-party express delivery companies such as STO, ZTO and S.F. Express are the largest beneficiaries of the boom. Our express company performance matrix and comparison analysis on various express delivery players show unit economic efficiency is the key driver for profitability.

● From days to minutes. The emergence of high-frequency delivery is taking the infrastructure capability to the next level – i.e., to enable delivery of time-sensitive merchandises and services in minutes. Efficiency level for current high-frequency players still needs time to reach the ideal level.

● We see third-party express companies improvement to eclipse the speed and quality advantage of in-house delivery of VIPS (N, TP $12.5) and JD (N, TP $20.8). Incremental operating leverage from fulfilment expense will be more limited, and higher fulfilment cost due to BABA's Tmall Supermarket will drag near-term profitability.

Figure 1: Highlights of leading express delivery players SF STO YTO Yunda EMS

Revenue (Rmb mn) 48,101 7,711 11,747 5,053 25,885 GPM% 19.8% 16.6% 13.4% 31.1% 19.0% NPM% 2.3% 9.9% 6.1% 10.6% 3.5% Delivery volume (bn) 1.70 2.6 3.03 2.17 n.a. Growth CAGR (10-15) 32% 40% 61% 63% n.a. Mkt share % 8.3% 13.6% 14.6% 10.7% n.a. # of networks 45,000 10,000 24,000 20,000 45,000 # of vehicles 15,000 n.a. 32,000 28,400 10,000 # of employees 120,000 200,000 220,000 100,000 100,000 County coverage 88% 90% 94% 95% 100%

Source: Company data. Note: All metrics as of end-2015, except those for EMS which are as of end-2011.

China express delivery service is riding the wave of e-commerce and O2O services boom: The growth of China's overall logistics growth will continue to slow down due to macro headwinds, in our view. But the highway delivery segment – as one of its main sub-sectors, is expanding with decent growth, driven by the boom of e-commerce business. Among that, express and LTL are the growth layers, which accounted for 5%/40% of the highway delivery market, respectively. We expected continuing consolidation and mutual penetration of express and LTL players.

The LTL market is fragmented in China, with 90% occupied by self-employed vehicles. We expect to see an "Uber-style" business model emerging among LTL players and market consolidation should drive up efficiency and improve standardisation of service quality.

Express delivery – profitable growth. Driven by increasing penetration of online shopping, China's express delivery volume recorded more than 50% CAGR in the past five years, with aggregate volume at ~21 billion orders in 2015, within which at least 60% are the e-commerce related parcels. We expect the volume to reach 50 billion by 2020 and third-party express delivery companies such as STO, ZTO and S.F. Express can benefit the most from the e-commerce

boom. We analysed the performance of various express companies based on comparison of five metrics: network coverage, service quality, delivery speed, price attractiveness and value-added service and showed that unit economic efficiency is the key driver for profitability.

Meanwhile, e-commerce retailers are increasingly adopting in-house logistics capacity and delivery teams. We foresee both in-house and third-party logistics providers will continue to invest in the last mile infrastructure and resources, and to explore more innovative and efficient options to improve efficiency and service experience.

High-frequency delivery – from days to minutes. Apart from purchasing goods from e-commerce retailers, consumers also increasingly use O2O services that require on-demand intra-city delivery within hours. In-house delivery capacities are a competitive edge for most major O2O food take-out platforms. Meanwhile, crowdsourcing delivery service, a more cost-effective and flexible approach to address the long-tail demand, has also gained traction in volume ramp-up. The recent merger of Dada and JD Daojia, the two frontrunners in this sector, is expected to increase cost synergies and create another major player in this segment.

Figure 2: Comps for e-commerce in-house delivery peers Close Target Mkt cap PE

Company Ticker Ccy price Rating price (US$ mn) 2015 2016 2017

Alibaba BABA.N USD 79.35 O 100.0 199,361 38.0x 31.7x 24.9x JD.com JD.OQ USD 20.57 N 20.8 29,959 N/A N/A N/A Vipshop VIPS.N USD 11.81 N 12.5 6,742 22.7x 17.8x 13.9x Suning 002024.SZ CNY 10.88 O 22.5 15,119 N/A N/A N/A

Average 30.3x 24.7x 19.4x

Note: * Price as of 7 July, 2016; Source: Company data, Reuters, Credit Suisse estimates.

For listed B2C e-commerce players with in-house delivery teams, we see the network expansion/service quality improvement of third-party express delivery companies gradually eclipsing the advantage of speed and quality of in-house delivery teams of JD (N, TP $20.8) and VIPS (N, TP $12.5).

Fulfilment expense is the biggest and the most crucial cost item for all B2C e-commerce players. Efficiency improvement in fulfilment has been driving the profitability of e-commerce players such as JD, VIPS and BZUN in the past years. But incremental help on overall margin improvement will be more limited down the road. We estimate a 20 bp/30 bp improvement in fulfilment as a percentage of revenue for JD/VIPS in 2017E.

The ramp-up of food and grocery categories from Alibaba's Tmall Supermarket is likely to drive higher fulfilment cost and drag profitability incrementally in the coming quarters.

The author of this report wishes to acknowledge the contributions made by Dan Zhao, an employee of Evalueserve Research Hong Kong Ltd, a third-party provider to Credit Suisse of research support services.

Extract from the Asian Daily, 11 July 2016.

14 July 2016

Jump-Start 16

APAC Equity Strategy ----------------------------------------------------------------------------------------- New report: Is MSCI China's ROE bottoming? Sakthi Siva / Research Analyst / 65 6212 3027 / [email protected] Kin Nang Chik / Research Analyst / 852 2101 7482 / [email protected]

● After five years during which MSCI Asia ex-Japan (MXASJ) went nowhere (amid trading rallies) as MSCI China's ROE slowed from a peak of 17.2% in November 2011 to 12.4% currently, we highlight that MSCI China ROE has been flat at 12.4% for the last three months. The key question for investors is whether these are the first signs that MSCI China ROE is finally bottoming.

● As discussed in our report of 12 April China PPI leads ROE?, we believe the recent uptick in the China PPI (from -5.9% YoY in December 2015 to -2.6% in June 2016) acts as a proxy for commodity prices and leads China's ROE.

● Figure 2 highlights that MSCI China ROE ex Financials and Energy bottomed at 11.8% in November 2015 and has since risen to 13%. Figure 3 highlights that MSCI China ROE ex Financials (given rising NPLs) has risen from a low of 10.1% to 10.8% currently.

● While our biggest Overweight markets are Korea (the only market with rising ROE in the Asia Pacific) and Taiwan (the only market sitting on net cash), we reiterate our modest 1% Overweight on MSCI China given these early signs of ROE bottoming. Full report.

Figure 1: MSCI China ROE

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

MSCI China - ROE

12.4% now

High 17.2% Nov 2011

Source: MSCI

MSCI China ROE flat at 12.4% for three consecutive months

After five years during which MSCI Asia ex-Japan (MXASJ) went nowhere (amidst trading rallies) as MSCI China's ROE slowed from a peak of 17.2% in November 2011 to 12.4% currently, we highlight that MSCI China ROE has been flat at 12.4% for the last three months. The key question for investors is whether these are the first signs that MSCI China ROE is finally bottoming.

We believe Yes

As discussed in our report of 12 April China PPI leads ROE?, we believe the recent uptick in the China PPI (from -5.9% year-on-year in December 2015 to -2.6% in June 2016) acts as a proxy for commodity prices and leads China's ROE. Figure 2 highlights that MSCI China ROE ex Financials and Energy bottomed at 11.8% in November 2015 and has since risen to 13%. Figure 3 highlights that MSCI China ROE ex Financials (given rising NPLs) has risen from a low of 10.1% to 10.8% currently.

Reiterate our modest 1% Overweight on MSCI China

While our biggest Overweight markets are Korea (the only market with rising ROE in the Asia Pacific) and Taiwan (the only market sitting on net cash), we reiterate our modest 1% Overweight on MSCI China given these early signs of ROE bottoming.

Figure 2: MSCI China ex Financials ex Energy ROE

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

MSCI China ex Financials & Energy - ROE

13.0% now

Low 11.8%

Source: MSCI

Figure 3: MSCI China ex Financials ROE

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

MSCI China ex Financials - ROE

10.8% now

Low 10.1%

Source: IBES

Extract from the Asian Daily, 12 July 2016.

14 July 2016

Jump-Start 17

China Economics ----------------------------------------------------------------------------------------------- Assessing the impact of floods Ray Farris / Fixed Income Research Analyst / 65 6212 3412 / [email protected] Weishen Deng / Economist / 852 2101 7162 / [email protected]

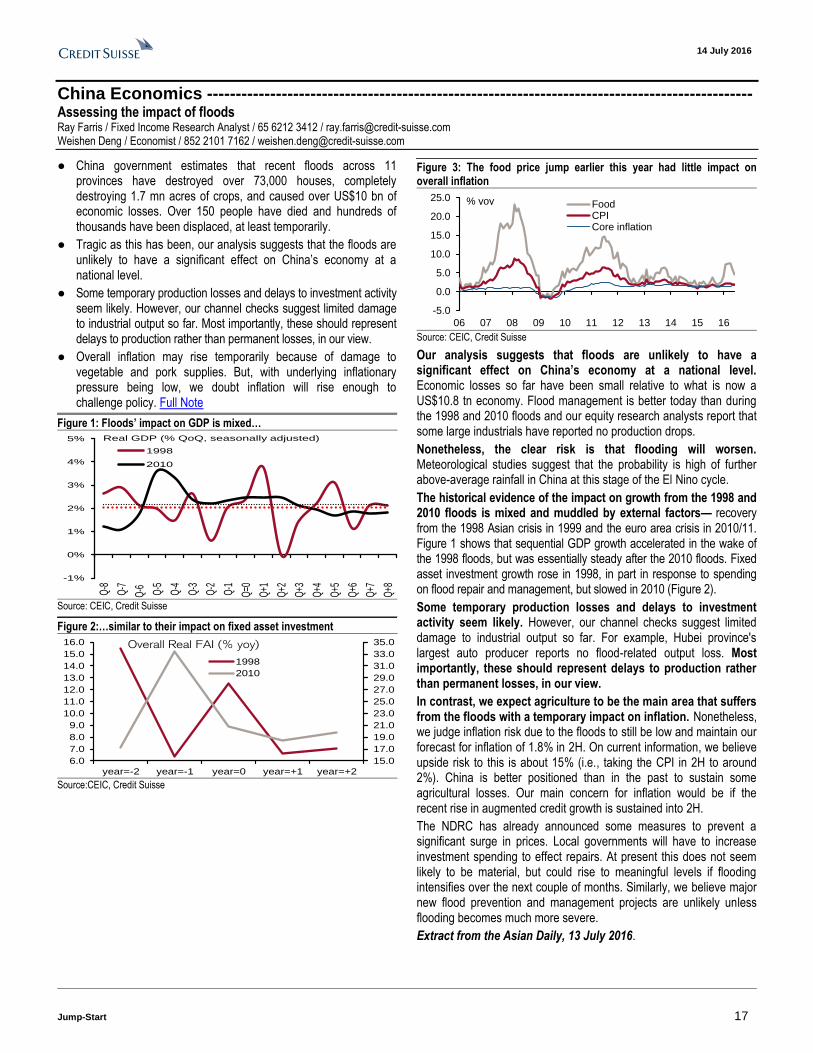

● China government estimates that recent floods across 11 provinces have destroyed over 73,000 houses, completely destroying 1.7 mn acres of crops, and caused over US$10 bn of economic losses. Over 150 people have died and hundreds of thousands have been displaced, at least temporarily.

● Tragic as this has been, our analysis suggests that the floods are unlikely to have a significant effect on China’s economy at a national level.

● Some temporary production losses and delays to investment activity seem likely. However, our channel checks suggest limited damage to industrial output so far. Most importantly, these should represent delays to production rather than permanent losses, in our view.

● Overall inflation may rise temporarily because of damage to vegetable and pork supplies. But, with underlying inflationary pressure being low, we doubt inflation will rise enough to challenge policy. Full Note

Figure 1: Floods’ impact on GDP is mixed…

-1%

0%

1%

2%

3%

4%

5%

Q-8

Q-7

Q-6 Q-5

Q-4

Q-3

Q-2

Q-1

Q=0

Q+1

Q+2

Q+3

Q+4

Q+5

Q+6

Q+7

Q+8

1998

2010

Real GDP (% QoQ, seasonally adjusted)

Source: CEIC, Credit Suisse

Figure 2:…similar to their impact on fixed asset investment

15.0

17.0

19.0

21.0

23.0

25.0

27.0

29.0

31.0

33.0

35.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

year=-2 year=-1 year=0 year=+1 year=+2

1998

2010

Overall Real FAI (% yoy)

Source:CEIC, Credit Suisse

Figure 3: The food price jump earlier this year had little impact on overall inflation

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

06 07 08 09 10 11 12 13 14 15 16

FoodCPICore inflation

% yoy

Source: CEIC, Credit Suisse

Our analysis suggests that floods are unlikely to have a significant effect on China’s economy at a national level. Economic losses so far have been small relative to what is now a US$10.8 tn economy. Flood management is better today than during the 1998 and 2010 floods and our equity research analysts report that some large industrials have reported no production drops.

Nonetheless, the clear risk is that flooding will worsen. Meteorological studies suggest that the probability is high of further above-average rainfall in China at this stage of the El Nino cycle.

The historical evidence of the impact on growth from the 1998 and 2010 floods is mixed and muddled by external factors— recovery from the 1998 Asian crisis in 1999 and the euro area crisis in 2010/11. Figure 1 shows that sequential GDP growth accelerated in the wake of the 1998 floods, but was essentially steady after the 2010 floods. Fixed asset investment growth rose in 1998, in part in response to spending on flood repair and management, but slowed in 2010 (Figure 2).

Some temporary production losses and delays to investment activity seem likely. However, our channel checks suggest limited damage to industrial output so far. For example, Hubei province's largest auto producer reports no flood-related output loss. Most importantly, these should represent delays to production rather than permanent losses, in our view.

In contrast, we expect agriculture to be the main area that suffers from the floods with a temporary impact on inflation. Nonetheless, we judge inflation risk due to the floods to still be low and maintain our forecast for inflation of 1.8% in 2H. On current information, we believe upside risk to this is about 15% (i.e., taking the CPI in 2H to around 2%). China is better positioned than in the past to sustain some agricultural losses. Our main concern for inflation would be if the recent rise in augmented credit growth is sustained into 2H.

The NDRC has already announced some measures to prevent a significant surge in prices. Local governments will have to increase investment spending to effect repairs. At present this does not seem likely to be material, but could rise to meaningful levels if flooding intensifies over the next couple of months. Similarly, we believe major new flood prevention and management projects are unlikely unless flooding becomes much more severe.

Extract from the Asian Daily, 13 July 2016.

14 July 2016

Jump-Start 18

China Economics ----------------------------------------------------------------------------------------------- Downhill from here Ray Farris / Fixed Income Research Analyst / 65 6212 3412 / [email protected] Weishen Deng / Economist / 852 2101 7162 / [email protected] Dong Tao / Economist / 852 2101 7469 / [email protected]

● We revise down our 2016 GDP growth forecast to 6.5% from previous forecast of 6.6%. We forecast that China's GDP growth will slow from about 6.6% (saar) in 2Q to 6.2% in 4Q before new stimulus drives a bounceback to 6.5% in 2017.

● Private investment growth, ex-real estate, has fallen sharply, government spending is set to slow sharply absent new fiscal stimulus, and the export outlook has deteriorated.

● The government is likely to continue to allow some of the balance of payments pressure to clear through CNY depreciation. We forecast USDCNY to rise to about 6.84 by end-2016 and 7.11 by end-2017.

● Monetary policy is likely to play only a passive role in any stimulus. We expect China’s reserve requirement ratios (RRR) to be cut by 100 bp. However, we believe continuing pressure on the CNY greatly limits the scope for lower interest rates. Full report.

Figure 1: Summary of forecasts Current Previous

14 15E 16F 17F 16F 17F

GDP 7.3 6.9 6.5 6.5 6.6 6.5 CPI inflation (yav) 2.0 1.4 2.0 1.7 2.0 1.7 One-year lending rate (%, ye) 5.60 4.35 4.35 4.35 3.60 3.60 M2 money supply (ye) 12.2 13.3 12.0 12.5 13.0 12.5 Exports (% YoY) 6.0 -2.9 -5.5 2.0 4.5 5.0 Imports (% YoY ) 0.5 -14.2 -10.0 0.0 -5.0 1.5 Trade balance (US$ bn) 383 593 636 679 780 875 Current account (as a % of GDP) 2.7 3.1 2.7 2.6 3.2 2.7 USDCNY exchange rate (ye) 6.20 6.43 6.84 7.11 6.72 6.98

Source: CEIC, Credit Suisse

We revise down our 2016 GDP growth forecast to 6.5% from previous forecast of 6.6%. We forecast that China's GDP growth will slow from about 6.6% (saar) in 2Q to 6.2% in 4Q before new stimulus drives a bounceback to 6.5% in 2017. Private investment growth, ex-real estate, has fallen sharply, government spending is set to slow sharply absent new fiscal stimulus, and the export outlook has deteriorated.

Growth momentum has clearly weakened and become more dependent on SOEs and government spending. This reflects the continuing deterioration in investment growth, despite government stimulus. In contrast, real estate investment is likely to rise through 3Q, supporting growth, but even this sector should taper into 4Q. Stronger infrastructure investment supported 1Q growth, but will likely slow in 2H. To be sure, fiscal policy is programmed to tighten in 2H. Official budget spending is planned to rise 2.8% this year, but grew 13.8% in the first five months as the government front-loaded spending. Stronger-than-expected government revenues and land sale revenues so far provide capacity to spend more, but no indications of changes to the official budgets yet exist.

Credit growth is also likely to continue moderating. Growth in total social financing, ex-equity financing, slowed to 12.4% YoY in May from 13.1% in March. Nonetheless, financial sector risk is likely to continue to rise rapidly. Even the official target for total social financing growth of 13% for 2015 implies that debt/GDP will rise, but

we estimate that it is more realistic to think of credit growing about 18% YoY this year. This would push credit/GDP (excluding government and financial bonds) to roughly 235%. Crucially, more of this credit this year is going to the real estate sector, which is dominated by smaller private developers, and takes the form of shadow activity funded by interbank borrowing. It is impossible to forecast when this could result in a problem that requires PBoC support, but we believe the risk is rising. As long as inflation remains low, the government’s capacity to contain the impact on the financial sector of unexpected defaults will remain high, in our view. To be sure, we forecast CPI inflation will remain low at 2% this year and 1.7% in 2017. The stabilisation of commodity prices and demand for basic materials lead us to expect PPI deflation to diminish to -1.5% to -2.0% by the end of 2016.