www.ubs.com/investmentresearch This report has been prepared by UBS Securities LLC. ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 40. UBS does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Global Research 15 August 2018 Is Tesla Revolutionary or Evolutionary? Lap 1: Powertrain – An Engineer's Dream, But An Accountant's Nightmare What's better than tearing down a Tesla Model 3? Tesla is now ramping production of the Model 3, the highest-profile car launch in the past decade. Last year, UBS Evidence Lab tore down an electric car to understand the progress of EV powertrains. This time, UBS Evidence Lab did not only tear down the new Tesla Model 3, we also tore down a 2014 BMW i3, and a 2017 Chevy Bolt to find out if Tesla deserves its reputation as the leader in electric powertrain and technology. This report focuses on EV powertrain, while subsequent reports will look at the electronics and fit & finish of all three vehicles. Surprise #1: Amazing powertrain tech falls short on cost Who won Lap 1 for EV powertrain? Tesla! All in, Tesla delivered the best powertrain at the lowest cost. Tesla's battery cost was $178/kWh vs. $205/kWh for the Chevy Bolt. TSLA's powertrain had the best power, torque and acceleration. The teardown engineers were crazy about the powertrain, highlighting next-gen, military-grade tech years ahead of peers. However, the excitement did not translate into large cost savings. TSLA indicated in 2016 that the Model S battery was already <$190/kWh; therefore, $178/kWh reflects <6% improvement. The powertrain cost was $950 higher than we forecast. With these economics, we expect the $35k base Model 3 to lose ~$6k/car. Surprise #2: Semi content rises 10%, while high voltage wiring falls 48% The Tesla Model 3 shifted to silicon carbide in the inverter, which offers major system benefits through higher efficiency, extending range and providing more heat tolerance. This resulted in a 10% increase in semi content in the powertrain. On the other hand, the more efficient design of the powertrain resulted in a 48% reduction in HV cabling. Surprise #3: Powertrain vertical integration significantly higher Almost all the design recommendations from our Chevy Bolt teardown were already incorporated into the Model 3. Our experts attribute much of the Model 3 engineering leadership to higher vertical integration. Outside of Panasonic battery cells, the entire EV powertrain was done in-house at TSLA. In contrast, LG alone supplied ~90% of the Chevy Bolt's powertrain content. Traditional automakers may need to bring more in- house, or more likely, leverage suppliers with broad EV capabilities. Equities Global Automobiles Colin Langan, CFA Analyst [email protected] +1-212-713 9949 Gene Vladimirov, CFA Associate Analyst [email protected] +1-212-713-1091 Patrick Hummel, CFA Analyst [email protected] +41-44-239 79 23 David Lesne Analyst [email protected] +44-20-7567 5815 Julian Radlinger, CFA Analyst [email protected] +44-20-7568 1171 Kohei Takahashi Analyst [email protected] +81-3-5208 6172 Paul Gong Analyst [email protected] +852-2971 7868 Eugene Jung Analyst [email protected] +82 2 3702 8801 David Mulholland, CFA Analyst [email protected] +44-20-7568 4069 Kenji Yasui Analyst [email protected] +81-3-5208 6211 Timothy Arcuri Analyst [email protected] +1-415-352 5676 Nicolas Gaudois Analyst [email protected] +852-2971 5681

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.ubs.com/investmentresearch

This report has been prepared by UBS Securities LLC. ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 40. UBS does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Global Research 15 August 2018

Is Tesla Revolutionary or Evolutionary? Lap 1: Powertrain – An Engineer's Dream, But An Accountant's Nightmare

What's better than tearing down a Tesla Model 3? Tesla is now ramping production of the Model 3, the highest-profile car launch in the past decade. Last year, UBS Evidence Lab tore down an electric car to understand the progress of EV powertrains. This time, UBS Evidence Lab did not only tear down the new Tesla Model 3, we also tore down a 2014 BMW i3, and a 2017 Chevy Bolt to find out if Tesla deserves its reputation as the leader in electric powertrain and technology. This report focuses on EV powertrain, while subsequent reports will look at the electronics and fit & finish of all three vehicles.

Surprise #1: Amazing powertrain tech falls short on cost Who won Lap 1 for EV powertrain? Tesla! All in, Tesla delivered the best powertrain at the lowest cost. Tesla's battery cost was $178/kWh vs. $205/kWh for the Chevy Bolt. TSLA's powertrain had the best power, torque and acceleration. The teardown engineers were crazy about the powertrain, highlighting next-gen, military-grade tech years ahead of peers. However, the excitement did not translate into large cost savings. TSLA indicated in 2016 that the Model S battery was already <$190/kWh; therefore, $178/kWh reflects <6% improvement. The powertrain cost was $950 higher than we forecast. With these economics, we expect the $35k base Model 3 to lose ~$6k/car.

Surprise #2: Semi content rises 10%, while high voltage wiring falls 48% The Tesla Model 3 shifted to silicon carbide in the inverter, which offers major system benefits through higher efficiency, extending range and providing more heat tolerance. This resulted in a 10% increase in semi content in the powertrain. On the other hand, the more efficient design of the powertrain resulted in a 48% reduction in HV cabling.

Surprise #3: Powertrain vertical integration significantly higher Almost all the design recommendations from our Chevy Bolt teardown were already incorporated into the Model 3. Our experts attribute much of the Model 3 engineering leadership to higher vertical integration. Outside of Panasonic battery cells, the entire EV powertrain was done in-house at TSLA. In contrast, LG alone supplied ~90% of the Chevy Bolt's powertrain content. Traditional automakers may need to bring more in-house, or more likely, leverage suppliers with broad EV capabilities.

Equities

Global

Automobiles

Colin Langan, CFA Analyst

[email protected] +1-212-713 9949

Gene Vladimirov, CFA Associate Analyst

[email protected] +1-212-713-1091

Patrick Hummel, CFA Analyst

[email protected] +41-44-239 79 23

David Lesne Analyst

[email protected] +44-20-7567 5815

Julian Radlinger, CFA Analyst

[email protected] +44-20-7568 1171

Kohei Takahashi Analyst

[email protected] +81-3-5208 6172

Paul Gong Analyst

[email protected] +852-2971 7868

Eugene Jung Analyst

[email protected] +82 2 3702 8801

David Mulholland, CFA Analyst

[email protected] +44-20-7568 4069

Kenji Yasui Analyst

[email protected] +81-3-5208 6211

Timothy Arcuri Analyst

[email protected] +1-415-352 5676

Nicolas Gaudois Analyst

[email protected] +852-2971 5681

Is Tesla Revolutionary or Evolutionary? 15 August 2018

2

Contents

Summary ........................................................................................... 3

Surprise #1: Tesla's powertrain not as cheap as expected ............................ 3

Surprise #2: More Semis Content, Less HV Wiring ....................................... 4

Surprise #3: More Vertically Integrated ........................................................ 4

Surprise #4: Battery Pack Cost ..................................................................... 7

Surprise #5: Base Model Unprofitable .......................................................... 8

Surprise #6: EV Pack Cost on Trend ............................................................. 9

Q: Who is Best & Worst Positioned? ............................................. 10

Sector Summaries........................................................................... 11

Global Autos.............................................................................................. 12

Global Auto Suppliers ................................................................................ 13

Global Batteries ......................................................................................... 14

Global Semis .............................................................................................. 14

Let the Race Begin! ........................................................................ 16

Q: Who Won Lap 1: Powertrain & Battery? ................................................ 17

The First Turn: The Battery ............................................................ 19

Straightaway: Battery Management & Charging ........................ 24

Final Turn: E-Motor & Inverter ...................................................... 28

Home Stretch: Cooling & Wiring ................................................... 33

Other Indirect EV Costs .............................................................................. 35

Appendix ........................................................................................ 36

Battery Background ................................................................................... 36

Colin Langan, CFA Analyst

[email protected] +1-212-713 9949

Gene Vladimirov, CFA Associate Analyst

[email protected] +1-212-713-1091

Patrick Hummel, CFA Analyst

[email protected] +41-44-239 79 23

David Lesne Analyst

[email protected] +44-20-7567 5815

Julian Radlinger, CFA Analyst

[email protected] +44-20-7568 1171

Kohei Takahashi Analyst

[email protected] +81-3-5208 6172

Paul Gong Analyst

[email protected] +852-2971 7868

Eugene Jung Analyst

[email protected] +82 2 3702 8801

David Mulholland, CFA Analyst

[email protected] +44-20-7568 4069

Kenji Yasui Analyst

[email protected] +81-3-5208 6211

Timothy Arcuri Analyst

[email protected] +1-415-352 5676

Nicolas Gaudois Analyst

[email protected] +852-2971 5681

Is Tesla Revolutionary or Evolutionary? 15 August 2018

3

Summary The UBS Evidence Lab hired engineers to tear down the 2017 Tesla Model 3, 2014 BMW i3 and 2017 Chevy Bolt. The UBS teardown experts provided a full breakdown of the vehicle of the major vehicle components including the Powertrain & Battery, the Controlling Electronics, the Body & Chassis, and the Interior & Safety. Each component was removed, studied, and scrutinized for a full view of the pros and cons of the design, functionality, the ease of manufacturing, and the cost of production. Lap 1 of our Teardown series will focus on the BEV (battery electric vehicle) powertrain. We discuss the top six surprising finding from our teardowns below.

Surprise #1: Tesla's powertrain not as cheap as expected While Tesla's powertrain was better than peers in terms of cost per kWh and performance, their lead was not as large as we would have expected. The overall cost at $178/kWh is only ~6% better than their <$190/kWh estimate for the Model S/X provided in 2016. Moreover, the cell cost at $148/kWh is well above Tesla's guidance of below $100/kWh ending 2018. We note that this cost estimate is based on our engineering partners' expertise and channel checks at the time the teardown was performed. We look forward to doing more detailed work with our partners in UBS Evidence Lab to better understand the breakdown of these costs. That said, Tesla's powertrain was $178/kWh vs. $205/kWh on the Chevy Bolt and $442/kWh on the 2014 BMW i3 (est. now at ~$300-320/kWh now). We'd expect future EVs from traditional automakers to have similar cost.

Figure 1: TSLA Model 3 Actual vs. Estimated Cost Figure 2: Tesla Model 3 vs. Chevy Bolt & BMW i3

Source: UBS Source: UBS

$16,900 $17,800

Model 3 Estimate Model 3 Actual

Interior & Safety Body & ChassisControlling Electronics Powertrain & Battery

+$950 higher

than our estimate

Lap 3

Lap 2

Tesla Model 3 2017 Chevy Bolt 2014 BMW i3Battery E Motor Power Distrib. Inverter Other

$178/kWh $205/kWh $442/kWh

(Gen 2 est. ~$300-320/kWh)

The UBS Evidence Lab tore down a Tesla Model 3, BMW i3, and Chevy Bolt to understand if Tesla is an EV and electronics leader.

At $148/kWh, Tesla's battery cell cost was well above its guidance for <$100/kWh by the end of 2018.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

4

Surprise #2: More Semis Content, Less HV Wiring Overall, the semi content in the Model 3 was 10% (~$60) higher than the Chevy Bolt. However, the high voltage (HV) wiring content was about $160 lower than the Bolt. Despite the fact the Model 3 is more powerful and larger, it actually is slightly more than half of the cost of the Bolt's HV wiring. The key suppliers for semi content on the Model 3 are ST Micro & Texas Instruments. However, the significant decline in high voltage wiring is an incremental negative for suppliers like Aptiv, Leoni & Lear.

Figure 3: Powertrain Semiconductor Content Figure 4: HV Wiring & Harnessing Content

Source: UBS Source: UBS

Surprise #3: More Vertically Integrated While the cost of the Tesla powertrain was higher than expected, the teardown engineers are crazy for the powertrain, highlighting next-gen, military-grade tech that's years ahead of peers. The Model 3 appears to have been built with a goal of simplifying the engineering, removing components, and building things as modularly as possible. The inverter was embedded into the e-motor and gearbox. More impressively, the battery management and charging electronics merged the DC/DC converter, on board charger, and power distribution module into one simple unit (see basic illustration below). We see this as driving two possible shifts: 1) Suppliers needed a wider range of EV capabilities, or 2) automakers bringing these capabilities in-house.

$0

$100

$200

$300

$400

$500

$600

$700

Tesla Model 3 Chevy Bolt

OtherBattery ManagementOn-Board Charger & DC-DC ConverterHigh Voltage System ControllerInverted Module & Control

0

50

100

150

200

250

300

350

400

HV Charger Other HV Wiring/Harnessing

Chevy Bolt BMW i3 Tesla Model 3

The Model 3 had 10% higher semi content than the Chevy Bolt, but the HV wiring is almost 50% lower.

Tesla's vertical integration appears to be a crucial advantage allowing revolutionary designs

Is Tesla Revolutionary or Evolutionary? 15 August 2018

5

Figure 5: Battery Management & Charging Electronics Bolt vs. Model 3

Source: UBS

Broader is better on EV. If this is indeed the way of the future, an OEM shift to larger and integrated components would mean Tier 1 suppliers need to have a diversified expertise in electronics and potentially a larger piece of each vehicle. Overall, this would likely drive a separation of suppliers into winners and losers with electrical powertrain leaders becoming a larger part of vehicles and ancillary component makers losing content share. This shift may also drive incremental power to the suppliers as they become more crucial to an OEM.

This likely explains why BorgWarner acquired Sevon as it provides inverter capabilities and why Valeo formed a JV with Siemens at the end of 2016 which can supply the full system. It has already developed modules which are merging most of the moving parts. After 1.5 years, the JV has gained almost €11bn worth of orders. We estimate this should translate into a global market share for key EV components of 25% for EV powertrain related parts. Another example of increasing electrical capabilities among suppliers is the recent Toyota sale of an electric component factory to Denso. Nissan has also recently decided to sell key subsidiaries Calsonic Kansei (inverter) and AESC (battery).

If size matters most in electric components, we believe both Japanese suppliers and companies which deal with Japanese HEVs like Denso will be winners in the early phase of the electrification. Toyota, which sold 1.5m HEVs last year, will share key electric components such as the motor, inverter, converter, and others among its full HEVs, PHEVs, BEVs, and FVCs. The new FCV model “Mirai” actually shares the majority of its power electric components and modules with the “Prius”, which is a HEV. We see the Japanese, US and Korean OEMs as aggressively expanding full HEVs in the next 3-5 years. We note that 48V "mild" hybrid systems are too small to share electric components with BEVs, so suppliers with full HEV technology and components will enjoy the benefit of early adoption in our opinion.

Among the major auto suppliers, Conti, Denso, and Valeo appear to the most capable providers of BEV components. Each has electric motor and inverter capabilities, among the most important and expensive (outside the battery) components in an EV.

On-Board Charger DC-DC ConverterPower Distribution

ModuleBattery Mangagment

Module

Is Tesla Revolutionary or Evolutionary? 15 August 2018

6

Figure 6: Chevy Bolt EV Powertrain

Source: UBS

Figure 7: Model 3 Battery Mang. & Charging Electronics Figure 8: 3D Rendering of Model 3 Motor & Inverter

Source: UBS Source: UBS

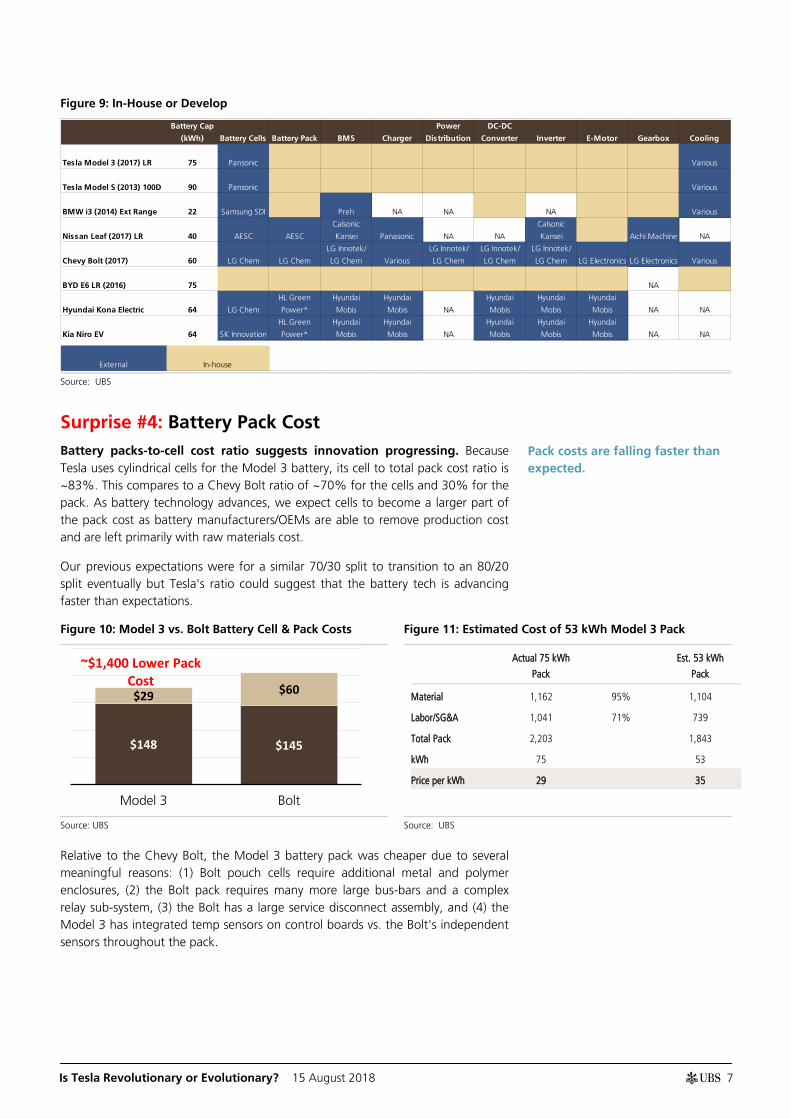

OEMs bringing in-housing? The opposite case, however, would see much of the tech developed and kept in-house. Tesla's strides forward seem to be in large part due to its development of technologies in-house. As expected, the more complex and unique the technology, the more likely OEMs will develop it in house. A specific example of technology different that OEMs have mostly kept in house is the e-motor. E-motors have numerous designs which can help differentiate the EVs performance from competitors and thus far some OEMs seem dedicated to keeping the tech in-house.

DC-DC ConverterOn Board ChargerPower DistributionInverterE-Motor

Is Tesla Revolutionary or Evolutionary? 15 August 2018

7

Figure 9: In-House or Develop

Source: UBS

Surprise #4: Battery Pack Cost Battery packs-to-cell cost ratio suggests innovation progressing. Because Tesla uses cylindrical cells for the Model 3 battery, its cell to total pack cost ratio is ~83%. This compares to a Chevy Bolt ratio of ~70% for the cells and 30% for the pack. As battery technology advances, we expect cells to become a larger part of the pack cost as battery manufacturers/OEMs are able to remove production cost and are left primarily with raw materials cost.

Our previous expectations were for a similar 70/30 split to transition to an 80/20 split eventually but Tesla's ratio could suggest that the battery tech is advancing faster than expectations.

Figure 10: Model 3 vs. Bolt Battery Cell & Pack Costs Figure 11: Estimated Cost of 53 kWh Model 3 Pack

Actual 75 kWh

Pack

Est. 53 kWh

Pack

Material 1,162 95% 1,104

Labor/SG&A 1,041 71% 739

Total Pack 2,203

1,843

kWh 75

53

Price per kWh 29

35

Source: UBS Source: UBS

Relative to the Chevy Bolt, the Model 3 battery pack was cheaper due to several meaningful reasons: (1) Bolt pouch cells require additional metal and polymer enclosures, (2) the Bolt pack requires many more large bus-bars and a complex relay sub-system, (3) the Bolt has a large service disconnect assembly, and (4) the Model 3 has integrated temp sensors on control boards vs. the Bolt's independent sensors throughout the pack.

Battery Cap

(kWh) Battery Cells Battery Pack BMS Charger

Power

Distribution

DC-DC

Converter Inverter E-Motor Gearbox Cooling

Tesla Model 3 (2017) LR 75 Pansonic Various

Tesla Model S (2013) 100D 90 Pansonic Various

BMW i3 (2014) Ext Range 22 Samsung SDI Preh NA NA NA Various

Nissan Leaf (2017) LR 40 AESC AESC

Calsonic

Kansei Panasonic NA NA

Calsonic

Kansei Aichi Machine NA

Chevy Bolt (2017) 60 LG Chem LG Chem

LG Innotek/

LG Chem Various

LG Innotek/

LG Chem

LG Innotek/

LG Chem

LG Innotek/

LG Chem LG Electronics LG Electronics Various

BYD E6 LR (2016) 75 NA

Hyundai Kona Electric 64 LG Chem

HL Green

Power*

Hyundai

Mobis

Hyundai

Mobis NA

Hyundai

Mobis

Hyundai

Mobis

Hyundai

Mobis NA NA

Kia Niro EV 64 SK Innovation

HL Green

Power*

Hyundai

Mobis

Hyundai

Mobis NA

Hyundai

Mobis

Hyundai

Mobis

Hyundai

Mobis NA NA

External In-house

$148 $145

$29 $60

Model 3 Bolt

~$1,400 Lower Pack Cost

Pack costs are falling faster than expected.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

8

Figure 12: Model 3 Pack Cost Split Figure 13: Model 3 Pack Cost Split

Source: UBS Source: UBS

Most expensive Battery Management. The battery management and charging electronics were extremely well engineered and enabled $160 in savings around high voltage wiring. However, it did not result in overall cost savings. The system was actually $350 more expensive than the combined Bolt systems (DC/DC converter, power distribution module, and on board charger), more than offsetting the cost savings on wiring.

Surprise #5: Base Model Unprofitable The Model 3 we disassembled was $49,000 which included the 75 kWh battery (+$9,000) and the high end trim (+$5,000). We estimate this model has a factory variable margin of ~29%, a gross margin of ~18%, and an operating margin of ~7%. However, the incremental margins on the options are high. We assume the base version at $35,000 would lose about $5,900 per car.

Figure 14: Tesla Profit Analysis

Source: UBS

Material 53%

Process & Labor 47%

Housing 20%

Cooling 11%

Battery Monitor

10% Sensor Stips 10%

Pack Cover 4%

Other 45%

14,280

3,630

-5,900

FactoryVariable

Profit

D&A,Warranty &

Freight

R&D SG&A OperatingProfit

53 kWhBattery

Lower Trim OperatingProfit Base

Based on the teardown, we believe the base Tesla Model 3 will lose $5.9k per car.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

9

Surprise #6: EV Pack Cost on Trend We are forecasting ~6% annual reduction in cell & pack costs through 2025. At $178/kWh, this would be ~2 years ahead of our forecast. However, Tesla uses NCA batteries, which have been used in consumer applications for longer than NMC, and therefore we expected these costs to be lower today. Moreover, we estimate that cost of the 53 kWh pack will be slightly higher than the 75 kWh. This would offer comparable range to the Chevy Bolt today. The cell cost of $148/kWh should be unchanged; however the pack costs we estimate increases from $29/kWh to ~$35/kWh. This implies that a luxury ICE is about $5,700 cheaper up front than an EV today.

Figure 15: EV Battery Cost Projections Figure 16: Updated EV vs. ICE Upfront Cost Comparison

Source: UBS Source: UBS

For additional color, please see our companion notes:

Tesla – Teardown Gives Us a View on Model 3 P&L

Semis: Who's powering Tesla's Model 3?

$205 $183 $178

$130

2017 2018 2019 2020 2021 2022 2023 2024 2025

$14,200

$8,500

$6,500

TSLA Powertrain (53kWh)

Luxury ICE Mass Market ICE

Battery (53 kWh) EV Powertrain ICE

Tesla's use of non-standard NCA battery chem allows a cheaper battery; b/c of this, we can't extrapolate overall EV battery costs for the industry.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

10

Q: Who is Best & Worst Positioned?

Is Tesla Revolutionary or Evolutionary? 15 August 2018

11

Sector Summaries In Figure 17 below, we recap the best and worst positioned based on the teardown.

Figure 17: Who are the best and worst positioned?

Sector Best Positioned Worst Positioned Sector Comments

Auto OEMs Daimler FCA The Model 3 teardown showed continued declines in EV costs, consistent with our prior

outlook. Earlier cost parity implies sooner and higher returns on EVs, in particular in the

premium segment and, regionally, speaking, in Europe. European OEMs can also benefit from a

strong tailwind to CO2 fleet targets post 2020. The flipside of the accelerated shift is the

residual value to fincos and lower contribution from highly profitable aftermarket long-term.

Volkswagen PSA

Renault Subaru

GM

Toyota

Auto Suppliers Valeo Schaeffler Suppliers with strong exposure to EV/hybrid and other megatrends (AV, connectivity, LED, etc)

will likely outperform industry growth, while those with big ICE exposure are likely to

underperform. Incrementally the EV wiring opportunity is shrinking fast which implies the EV

upside for suppliers like APTV, LEA, and Leoni is more limited. While in our Bolt teardown we

saw risk from competition from non-traditional suppliers (LG), the Model 3 teardown highlights

in-sourcing risks at the OEMs and/or the need for suppliers with broad EV capabilities.

Conti Faurecia

Delphi Tenneco

Hyundai Mobis

Denso

Batteries LG Chem While the Model 3 used NCA chemistry, we continued to believe NMC will be the long term

winner having better safety characteristics today and potentially lower cost over time. The

battery suppliers with NMC scale like LG Chem and Samsung SDI look best positioned long

term. Panasonic’s issue today is its single biggest customer: TSLA. If & when the company is

able to make a deal with an OEM such as Toyota, it would likely stabilize its business.

Samsung SDI

Panasonic

Chemicals Sumitomo Chem Johnson Matthey The Model 3 teardown did not drive any material changes vs. our previous view on the impact

from the shift to EVs. The most negative impacts should be to the autocatalysts producers. The

risks to consider are hydrogen growth and process catalyst companies. Hitachi Chem EMS Chemie

Umicore

Albermarle

Semiconductors Infineon Melexis Tesla's approach to in-housing its modules does not appear to be lowering the semi content –

but is changing the mix (less MCU content than Bolt). Its adoption of Silicon Carbide (SiC) in

the inverter could help to accelerate that shift. Overall, it reinforces our view that EVs provide a

significant content opportunity to semis – especially power semi suppliers.

Source: UBS

Is Tesla Revolutionary or Evolutionary? 15 August 2018

12

Figure 18: Global Team Analysts

Sector Region Analyst Email

Autos & Auto Parts Americas Colin Langan [email protected]

Autos & Auto Parts Americas Gene Vladimirov [email protected]

Autos & Auto Parts EMEA Patrick Hummel [email protected]

Autos & Auto Parts EMEA Julian Radlinger [email protected]

Autos & Auto Parts EMEA David Lesne [email protected]

Autos & Auto Parts EMEA Benedikt Baumann [email protected]

Autos & Auto Parts APAC Kohei Takahashi [email protected]

Autos & Auto Parts APAC Paul Gong [email protected]

Autos & Auto Parts APAC Eugene Jung [email protected]

Autos & Auto Parts APAC Sonal Gupta [email protected]

Autos & Auto Parts Americas Rogerio Araujo [email protected]

Batteries APAC Tim Bush [email protected]

Batteries APAC Kenji Yasui [email protected]

Chemicals Americas John Roberts [email protected]

Chemicals Americas Josh Spector [email protected]

Chemicals APAC Go Miyamoto [email protected]

Chemicals EMEA Andrew Stott [email protected]

Chemicals EMEA Geoff Haire [email protected]

Semis Americas Tim Arcuri [email protected]

Semis Americas John Ahn [email protected]

Semis EMEA David Mulholland [email protected]

Semis EMEA Francois-Xavier Bouvignies [email protected]

Semis APAC Nicolas Gaudois [email protected]

Semis APAC Bill Lu [email protected]

Semis APAC Taewoo Lee [email protected]

Source: UBS

Global Autos In the US, GM remains well positioned for the transition to EVs. While the Bolt's engineering was not as advanced as the Model 3, the overall package relative to the cost of the system was still impressive. Recently, GM said it would increase production of its Chevy Bolt by 20% in Q4 2018 due to increasing demand for the model. It noted that sales increased by over 40% in H1 2018. In 2017, the company sold ~28.5k Chevy Bolts.

In the European space, we see Daimler, Volkswagen and Renault best positioned for the transition to EVs. All three OEMs will launch dedicated EV platforms within 1-2 years and have aggressive model launch targets. Moreover, all three OEMs guide for at least a breakeven EBIT margin for their BEVs by 2020 or shortly thereafter. Daimler is the best-positioned premium OEM in our view: Daimler will launch 8 BEV models by 2022 and has already managed EBIT margin expectations by guiding for 8-10% during the transition phase (instead of 10%). The first of these models, the EQC SUV, will launch in early 2019. Volkswagen has the advantage of utilizing its dedicated platform(s) across brands and segments, which should reduce costs and group margin dilution. It will launch the first Audi BEV before year-end, followed by Porsche's first BEV and multiple mass-market BEVs amongst the VW, Skoda and Seat brands in quick succession starting in early 2020. Renault's advantage is that it invested in electrification earlier than most other OEMs and already has a strong sales track-record with the Renault Zoe and Nissan Leaf. Sharing a dedicated EV platform within its alliance should give it a similar edge on costs as Volkswagen. BMW has little to offer near-term, with only electrified versions of two ICE models (the Mini in 2019 and the X3 in 2020). The

Is Tesla Revolutionary or Evolutionary? 15 August 2018

13

next dedicated volume BEV won't be launched until 2021. BMW is working on a platform that fits all powertrains. This might sacrifice range and interior space of the EVs compared to a dedicated BEV architecture, we think.

Toyota is also well positioned for the transition to EVs. It is currently a leader in electrification as it sold 1.5 million HEVs/PHEVs last year. As the company is able to share key electric components across its lines of HEVs/PHEVs, it should be able to keep the cost of key electric components lower than competitors, even over the next five years. We estimate current average operating margins on HEVs of about 8-10% not including any subsidies. With its tie-up with Panasonic and aggressive development of solid state batteries, we believe it will keep the leading position within battery tech. The company has also formed an alliance to develop EVs with Suzuki, Mazda, Subaru, and Isuzu. Total sales volume from the alliance was ~17 million last year.

Global Auto Suppliers We recap the relative ICE vs. BEV content exposure for the global suppliers below.

Figure 19: ICE Specific Content vs. BEV Specific Content Figure 20: BEV Specific Content Less ICE Specific Content

Source: UBS Source: UBS

-5,000-4,000-3,000-2,000-1,000 0 1,000 2,000 3,000

Aisin SeikiSchaeffler

TennecoFaurecia

DanaAptivLeoniHella

ValeoBWA

MagnaConti

DensoDelphi

Lear

ICE -4,000 -3,000 -2,000 -1,000 0 1,000 2,000 3,000

Aisin SeikiSchaeffler

TennecoFaurecia

DanaAptivLeoniHella

ValeoBWA

MagnaConti

DensoDelphi

Lear

Is Tesla Revolutionary or Evolutionary? 15 August 2018

14

Figure 21: Who Supplies What?

Source: UBS

Global Batteries While NCA battery packs provides higher energy density with lower cost vs NMC (according to our teardown), we don't think we can conclude a winner on battery cell chemistry just based on this. We have been seeing most major OEMs turning towards NMC and not NCA, despite the latter having been around and available for a much longer time.

An important aspect to consider other than cost and performance is safety. Our understanding is that OEMs' priorities in battery cell qualification in order of importance are 1) safety, 2) cost, 3) reliability, 4) durability and 5) performance (Battery Expert call: Focus on Technology).

Concerns on safety has been the main drawback for NCA batteries, as they are known to be less stable given the higher nickel content and having to work with significantly higher number of cells. Tesla seems to be managing this better with a more precise battery management system, but this could be one of the main reasons why we have not seen NCA being adopted by others.

Global Semis Tesla's approach to in-housing its modules does not appear to be lowering the semi content – but is changing the mix (less MCU content than Bolt). Its adoption of Silicon Carbide (SiC) in the inverter could help to accelerate that shift. Overall, it reinforces our view that EVs provide a significant content opportunity to semis – especially power semi suppliers.

Overall we estimate a semis bill of materials for the powertrain of $640, 10% higher than the $580 we found in the Bolt. While the Model 3 is a key success story for STMicro's SiC products, this was already known and we believe is coming

Components / partsAverage pricing

($)Aisin Seiki Aptiv BWA Conti Delphi Dana Denso Faurecia Hella

Hyundai Mobis

Lear Leoni Magna Schaeffler TennecoToyota

IndustriesValeo

Battery - main 13,330

Battery cell 11,100 Developing

BMS 230 Developing

Battery pack 2,000 Developing

Wiring 390

High voltage cables 240

Charging cord 150

Propulsion 2,140

Electric motor 750 Developing

Gearbox 410

Inverter 800 Developing

Half Shafts 180

Power electronics 1,300

Power distribution module 375

DC/DC converter 275

On board charger 650 Developing

Cooling 280 Developing

Electric compressor 250

Total 17,440 1,960 390 2,240 3,360 1,955 460 3,360 280 785 4,705 2,490 390 2,240 410 0 14655 3,165

Engine 5,130

Internal combustion engine (ICE) 3,760

Fuel injection system 250

Fuel Storage 150

Starter + alternator / starter-generator 250

Engine actuators 200

Engine sensors / electronics 520

Transmission 1,200

Clutch system (incl. torque converter) 350

Multi-speed gearbox (incl. control valve) 700

Prop / drive shaft 50

Differential 100

AWD Content 325

Exhaust system 700

Exhaust gas recirculation / heat recovery 150

SCR system 300

Patriculate filter 150

Manifolds 50

Muffler 50

Total * 7,030 5,410 100 1,480 2,510 770 475 2,918 700 388 2,150 100 100 1,475 1,542 700 3,760 2,742

BEV powertrain

ICE powertrain

Is Tesla Revolutionary or Evolutionary? 15 August 2018

15

at low margins today given limited premium vs. silicon being charged. We also found much TI content for many small components but totaling to a small overall amount making it the second largest supplier we identified.

The teardown affirms our positive view on the content opportunity for semis in the shift to electric vehicles. Despite its limited presence in the Model 3, we continue to see Infineon (Buy, €28 PT) as the best positioned play on the shift to electric vehicles in semis and is continuing to win key design wins for mass-market European EV ramps in 2020. We are cautious to read too much into Tesla's approach to manufacturing and whether other OEMs will follow immediately. For more details, please see the global semis team companion piece: Semis: Who's Powering Tesla's Model 3?

Is Tesla Revolutionary or Evolutionary? 15 August 2018

16

Let the Race Begin!

Is Tesla Revolutionary or Evolutionary? 15 August 2018

17

Q: Who Won Lap 1: Powertrain & Battery? The EV powertrain is divided into several components. Outside the battery, there are five key parts of the powertrain (see below). This section will compare the batteries & electric drivetrain: the design, technology, integration and cost of each.

Figure 22: EV Powertrain Overview

Source: UBS

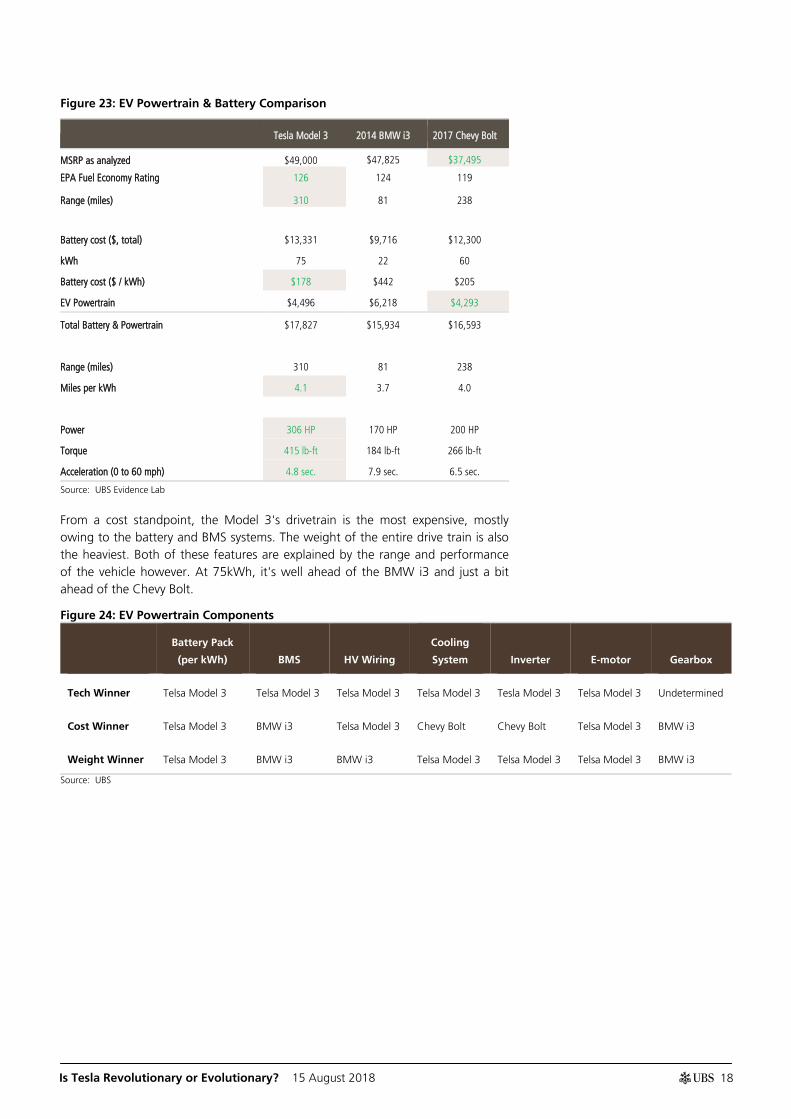

Lap 1 goes to Tesla! All-in, the Tesla Model 3 is the Lap 1 Battery & Powertrain winner among these vehicles. Through the teardown of the battery and drivetrain, we saw numerous advancements and innovations within the Model 3. The technology in the battery pack appears to be ahead of all current production EVs and the BMS operates within tolerances not seen in others. The focus on modularity and compact design also suggests potential for automated production.

Compared to the i3 and Bolt, the Tesla Model 3 long-range has a larger battery capacity and as such is both more powerful and has a longer range. It is the first Tesla car aimed at the mass-market as TSLA aims to become more than a niche EV player. Although the company is aiming to sell a base version for $35k (for a 210 mile range version), at the time of this writing, the cheapest available version sells for $49k and some were actually selling for $80.5k. This puts it well above both the $37.5k Chevy Bolt and the 2014 BMW i3 we used for compare. Currently, the 2019 Chevy Bolt's base MSRP is ~$36.5k and the 2018 BMW i3's (94Ah) is ~$44.5. With a range extender, the i3 gets up to ~$51.5k as a starting price. The 75 kWh Tesla powertrain is more expensive; however per kWh cost is the lowest. Moreover, miles per kWh are also slightly higher. More importantly, the overall performance is superior with much better power, torque, and acceleration.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

18

Figure 23: EV Powertrain & Battery Comparison

Tesla Model 3 2014 BMW i3 2017 Chevy Bolt

MSRP as analyzed $49,000 $47,825 $37,495

EPA Fuel Economy Rating 126 124 119

Range (miles) 310 81 238

Battery cost ($, total) $13,331 $9,716 $12,300

kWh 75 22 60

Battery cost ($ / kWh) $178 $442 $205

EV Powertrain $4,496 $6,218 $4,293

Total Battery & Powertrain $17,827 $15,934 $16,593

Range (miles) 310 81 238

Miles per kWh 4.1 3.7 4.0

Power 306 HP 170 HP 200 HP

Torque 415 lb-ft 184 lb-ft 266 lb-ft

Acceleration (0 to 60 mph) 4.8 sec. 7.9 sec. 6.5 sec.

Source: UBS Evidence Lab

From a cost standpoint, the Model 3's drivetrain is the most expensive, mostly owing to the battery and BMS systems. The weight of the entire drive train is also the heaviest. Both of these features are explained by the range and performance of the vehicle however. At 75kWh, it's well ahead of the BMW i3 and just a bit ahead of the Chevy Bolt.

Figure 24: EV Powertrain Components

Battery Pack

(per kWh) BMS HV Wiring

Cooling

System Inverter E-motor Gearbox

Tech Winner Telsa Model 3 Telsa Model 3 Telsa Model 3 Telsa Model 3 Tesla Model 3 Telsa Model 3 Undetermined

Cost Winner Telsa Model 3 BMW i3 Telsa Model 3 Chevy Bolt Chevy Bolt Telsa Model 3 BMW i3

Weight Winner Telsa Model 3 BMW i3 BMW i3 Telsa Model 3 Telsa Model 3 Telsa Model 3 BMW i3

Source: UBS

Is Tesla Revolutionary or Evolutionary? 15 August 2018

19

The First Turn: The Battery What does it do?

The battery contains the following two basic components:

Cells: This is the main power source for the vehicle.

Pack: The pack ensures the battery cells are properly cooled and monitored for safety. The pack includes a strong outer case to ensure the cells can't be punctured, a battery management system that ensure the cells do not have a thermal runaway event (catch fire), and a cooling system to make sure the cells remain at the optimal temperature to ensure safety and long life.

Who makes it?

Cells: Panasonic, LG, Samsung SDI, and CATL are the top four cell suppliers globally.

Packs: This is typically performed in-house by the automaker.

Who is the winner?

TSLA has the advantage in terms of timing and we would expect them to lead the field in battery tech. Our teardown confirmed this hypothesis and to a larger degree than expected. The Model 3 battery is more power dense, cheaper to manufacture and has an overall larger range (and would even at similar battery pack sizes). Although the longevity and safety are still in the process of being determined, there is not much data to suggest that currently any of these vehicles are better than the others in that sense. Battery winner: Tesla Model 3.

Figure 25: Battery Cell Comparison

2017 Model 3 (LR, RWD) 2017 Chevy Bolt 2014 BMW i3 (LR)

Chemistry NCA NMC LMO

Supplier Panasonic LG Chem Samsung SDI

Format Cylindrical Pouch Prismatic

# Cells 4416 288 96

Easily Swappable? No Yes Yes

Battery Pack

Cost as analyzed $13,331 $12,300 $9,716

Power Capacity (kWh) 75 60 22

Weight (kgs) 442 428 230

Pack Power:Weight Ratio (Wh/kg) 170 140 96

Charge Times

Leve 1: Basic - 120V residential ~55 hours ~60 hours ~20 hours

Level 2: Fast - 240V fast-charging ~9 hours ~9.5 hours ~3.5 hours

Super-fast - public DC fast-charging ~1.25 hours ~1.5 hours ~0.5 hours

Source: UBS

Is Tesla Revolutionary or Evolutionary? 15 August 2018

20

Figure 26: Summary of EV Battery Cells

2017 Model 3 2017 Chevy Bolt 2014 BMW i3

The battery cells used in the Tesla model 3 are

a newly developed 2170 NCA cell developed

with Panasonic, which, per Tesla, are the

"highest energy density cells used in any

electric vehicle". Although the chemical

makeup for the 2170s is proprietary, TSLA has

hinted that the chemistry is different from the

18650s and as such has driven increased

energy density. It has also claimed that the

NCA cells have a lower Cobalt content than the

upcoming 8:1:1 NMC batteries.

The 2170 is 21mm in diameter and 70mm in

length and replaces the previously used 18650

(18mm diameter, 65mm long). In essence, the

2170 is ~50% larger in volume and has a

capacity of ~5750-6000 mAh, or ~100% larger

than the 3000 mAh of the 18650. Also

according to TSLA, the size is the optimal size

for energy density.

The cells above are put together in "bricks"

which each contain 46 cells. Within the Model

3, there are four modules – two modules hold

23 bricks each and the other two hold 25

bricks. There are seven cooling channels within

each brick and six spacers, designed in such a

way that each cell is in contact with a cooling

channel. This ensures thermal stability. The

overall pack weighs 442kgs.

Our Bolt Teardown last year walked through

the details of the battery. As a reminder: the

Bolt's battery pack is supplied by LG Chem and

is a NMC (Nickel Manganese Cobalt) battery

with a usable capacity of 60kWh, which

provides an EPA-rated range of 238 miles / 384

km. It uses a pouch format, with 96 cells

connected in series (adding up to a voltage of

365V) and three strings of cells in parallel.

The i3's battery is supplied by Samsung SDI and

like the Chevy Bolt, used LMO technology.

BWA has since moved to its 2nd gen battery

which uses NMC 111 with an estimated cell

cost of ~$200/kWh (pack ~$300-320/kWh).

The battery pack includes 8 "bricks" with 12

prismatic cells per block. The 2014 model used

for our compare had a 60Ah/22kWh battery

but BMW introduced a 94Ah/33kWh version

that extended the range of the car from

81miles to 114 miles. However, the "fuel

efficiency" also dropped to 118 mpg vs 124

previously. In addition, the media has reported

that a 120Ah/43kWh battery is on the horizon

for late 2018, which should increase the range

to 150-155 miles.

Source: UBS, GM, RudolfSimon

How is the chemical composition different?

Thus far, most BEV development has used NMC chemistries with NMC 622 as the latest production generation and NMC 811 on the horizon. TSLA, however, has used NCA chemistries and the Model 3 is no different. Generally speaking, NCA batteries have a shorter life cycle and higher energy density. Additionally, they are less stable than NMC batteries. Both the longevity and stability of the new 2170 cells are still in the process of being determined.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

21

In the case of these three vehicles, from a performance and cost standpoint, Tesla's NCA chemistry appears to be advantageous to the NMC 622 chemistry used in the Bolt. As our teardown shows, the pack has a higher power to weight ratio and a lower cost to kWh ratio. Although this may change with the introduction of NMC 811 chemistries, Tesla/Panasonic's batteries appear to be leading.

How is the form factor different?

In terms of total material distribution within the three vehicles, battery cells make up ~40% of the Chevy Bolt's total, ~30% of the Model 3's and ~15% of the i3's. This is driven by the combination of form factor used, desired power capacity and overall vehicle size.

Tesla's use of cylindrical cells appears at least partially a function of its partnership with Panasonic who has long been a leader in cylindrical cells. Use of the cylindrical cells make for an easier automated production process as well as easier pack design. Given the steel case for each cell, it also helps the long-term stability of the cells. One concern with using this design is that it requires many more cells, 4416 in the Model 3's case vs. the 288 and 96 in the Chevy Bolt and i3, respectively. Ensuring steady connection and battery power load becomes more challenging. Tesla has overcome this problem by wire bonding the conductors to the batteries and gluing the entire pack shut. In addition, the BMS within the Model 3 appears to be far ahead of competition: our teardown measured the variation of voltage between different bricks was 2-3 mV, a miniscule amount given the possible range.

The Chevy Bolt and i3, however, use pouch and prismatic cells, respectively. One advantage of this form factor is the weight to power profile as well as the design flexibility offered by rectangular boxes. One of the things we've learned in the teardown of the Model 3 is how the design of the car from the ground up has allowed it more freedom to be developed as a pure electric vehicle. Traditional OEM's have strong incentives to use components across different platforms, often limiting design elements within their electric cars. Therefore, the use of rectangular pouch/prismatic cells allows for design flexibility.

Tesla's use of the cylindrical form factor doesn’t necessarily seem to give an advantage over the Bolt or i3 from a performance standpoint. However, the combination of using the NCA chemistry as well as advanced BMS appears to work in conjunction with the cylindrical form factor to help drive lower cost and better performance. With that in mind, we'll call the form factor competition to be undetermined for now.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

22

Figure 27: Summary of EV Battery Packs

2017 Model 3 2017 Chevy Bolt 2014 BMW i3

'The TLSA pack is complicated by the volume of

cells which requires advanced battery

management software. However, it also enables

a simpler cooling system.

Within the pack, each 2170 cell is welded to the

current collectors in such a way that a short

circuit causes the connecting wire to burn out.

This wire bonding process is just one of multiple

safety disconnects built into the Model 3 pack.

Furthermore, due to the volume of individual

cells, an individual cell should not cause any

meaningful impact on total capacity or power.

The cells are housed in 10 module cases. It

weighs 436 kg, out of which 300 kg relate to

the battery cells. Of the total weight, 26% is

contributed by the packaging and cooling (steel,

aluminum and iron), and about 68% by the

"active" materials in the battery cells.

The pack has fewer, but larger cells. The larger

cell format requires a more robust cooling

system as the risk of a thermal event in once cell

is more severe.

The pack used in our analysis weighs

~230kgs/500lbs and translates to 96Wh/Kg, well

below the 140 & 170 values for the Chevy Bolt

and Tesla Model 3, respectively.

In terms of swap ability, the i3's pack is actually a

structural part of the chassis but relatively easy to

remove and replace. Individual "bricks" are

replaceable and given the importance of each to

the overall power, this makes sense. On a limited

basis, owners of older 22kWh battery packs have

been able to get 33kWh battery packs installed.

The modularity and usability of the BMW

developed packs is such that their use has

extended to non-automotive applications: from

electric boats to electric delivery vehicles. This

widespread usage should help Samsung

SDI/BMW to scale production, discover long-term

issues, and feed aftermarket sales.

Source: UBS

How do the costs compare?

Battery costs are typically compared relative to cost per kWh as the higher kWh the longer the vehicle range. Companies often quote just a cell cost vs. the cell and pack cost, which clear makes a difference. Beyond these differences, there can also be difference in what is included in the cost (supplier profit margin or allocations for D&A & R&D). Below are the relative costs.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

23

Figure 28: Battery Pack Cost per kWh Figure 29: Model 3 vs. Bolt Cell and Pack Costs

Source: UBS Source: UBS

Our Model 3 teardown puts the cost of the full battery pack at $13,331. At 75kWh, this translates to a rate of $178 per kWh. Tesla itself has stated the cost is <$190 per kWh. Although slightly dated, this compares to $209 per kWh for the 2017 Chevy Bolt and $441 per kWh for the 2014 BMW i3 (est. 2nd gen NMC 111 battery is closer to $300-320/kWh).

For the Model 3, the cost of the cells breaks down to $148 per kWh, which is actually slightly more than the $145/kWh we calculate for the Chevy Bolt. Despite the fact that the Model 3 pack has more components (4416 vs 288 cells), each of which is welded to the conductors, the pack itself ends up costing less than the Bolt. This is likely due to a combination of Tesla's well engineered cooling system as well as the complexity of working with Prismatic cells in the i3.

Once again, Tesla appears to be ahead of the competition as it has leveraged its battery tech and developed battery packs that are ~15% cheaper than the competition. As the Model 3 is designed to be a longer range vehicle than the others, on an absolute basis, the battery pack is actually more expensive. Although the company's engineering makes the pack cheaper on a per kWh basis, when considering overall cost, consumers may lean towards cheaper vehicles with enough range to cover their needs.

$178 $209

$441

2017 Model 3 (LR,RWD)

2017 Chevy Bolt 2014 BMW i3 (LR)

Tesla Model 3 2017 Chevy BoltCell Pack

Is Tesla Revolutionary or Evolutionary? 15 August 2018

24

Straightaway: Battery Management & Charging What does it do?

One of the hardest parts of developing and manufacturing BEV's is the ability to design and integrate a robust battery management system (BMS) and associated components. There are typically three main components:

Power Distribution Module: The "brains" of the power operation which monitors and directs power to where it is needed safely and efficiently.

DC-DC Converter Module: Converts high-voltage DC from the battery management system to low voltage for the non-propulsion electricity users such as car electronics or power windows. Before "arriving" in the DC/DC converter, the current is routed through the HV system controller from the battery management module.

On-Board Charger: For safely and efficiently directing charging input to the battery pack. Converts AC power to DC for battery charging. Also responsible for AC filtering, rectification, power factor correction and DC conditioning.

Battery Management System: Electronics that manage the state of charge of the batteries to ensure safety and battery life.

Who makes it?

Power Distribution Module: Bosch, Conti, Delphi, Denso, & LG Electronics

DC-DC Converter: Bosch, Conti, Delphi, Denso, Hyundai Mobis, LG Electronics, Valeo, & ZF

On-Board Charger: Conti, Delphi, Denso, Hyundai Mobis, Lear, LG Electronics, & Valeo

Battery Management System: Preh, Calsonic Kansei, LG Electronics, Hyundai Mobis

Who is the winner?

Overall, despite its all-in-one modular design for the power management system, the Model 3 has significantly more components and weight in the BMS and charging electronics systems than the BMW i3 and the Chevy Bolt. However, the weight and cost distributions are in line with the mileage range and battery capacity of each vehicle.

The level of engineering within the BMS of the Model 3, however, appears to be multiple technological steps ahead of the Chevy Bolt or i3. Once again, Tesla's later entry into the market, as well as its pure focus on electric vehicles gives it an advantage here. Battery Management winner: Tesla Model 3.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

25

Figure 30: Summary of EV Battery Management & Charging

2017 Model 3 2017 Chevy Bolt 2014 BMW i3

One the most impressive aspects of the Model

3 is the modularity of the battery management

module. The module houses most of the power

electronics in one spot and is radically different

from most competing designs. The Module

contains the high-voltage controller, the power

conversion unit (the DC to DC converter),

multiple sensors and connectors, fuses and, the

pyro-technic fuse. Tesla has also combined the

on-board charger (OBC) and DC-DC converter

into one unit which is unlike any other EV BMS.

This design appears to be new for Tesla as well

and being able to squeeze 10kW of charger

into a small and cool component is viewed as

quite remarkable.

The module is mounted at on top of and at the

back of the battery pack and right near the

rear-wheel drive motor. Given the proximity to

each of the components and the drivetrain,

through the overall design of the vehicle, Tesla

was able to reduce the required HV wiring,

ultimately reducing the total weight. The only

long-run HV wiring the Model 3 requires are

the cables that power the AC compressor and

heater. In contrast to the Model S/X, the Model

3 has the e-motor in front of the rear wheel

half-shafts, reducing the HV wiring even

further. Otherwise, all the HV wiring is localized

around the battery management module.

Given the design of the battery management

module, the company likely assembles the pack

and module at the Gigafactory and then puts it

all together at the Fremont plant.

Within the Chevy Bolt, the BMS is responsible

for monitoring the voltage from each Li-ion cell

group and temperature. Each subsystem has a

LG Chem ASIC and a Freescale 8-bit MCU. The

inverter/converter assembly houses a main logic

board, a gate driver board, a large DC-link

capacitor array and power module for motor

control. The whole assembly is liquid cooled.

The Chevy Bolt features a current sensor for

monitoring DC levels, a 40AMP fuse for

incoming OBCM voltage and multiple relays.

Charging requires an on-board charger

module, a communication controller and a

charging cord. The charger module is

responsible for charging the battery pack by

converting AC to DC with high efficiency.

Various high-voltage cables are required to

connect the modules with each other and with

the battery.

Within BMW's battery pack, each of the 12

bricks has its own BMS board which flows into

a main controller. In addition to the battery,

BMW also developed numerous battery

monitoring components including ones which

ensure the interconnection of the cells

themselves as well as the connection between

the battery system and the vehicle. Given the

importance of each cell and brick within the

system (only 96 cells in 8 bricks), this is likely a

necessity for overall range and performance.

The design of the system is integrated into a

central control unit and the electronic

components are in proximity of the cells,

including battery management sensors. In

order to maintain output and capacity over

time, the BMS controls both the charging and

the discharging processes, as well as the

operating temperature of the cells. Similar to

the Tesla Model 3, the direct connection

between the electronics and electric motor in

the rear of the BMW i3 reduces the length of

HV wiring required.

Source: UBS

Is Tesla Revolutionary or Evolutionary? 15 August 2018

26

Overall Battery Management: Tesla's battery management begins with a control board mounted directly to each of the four battery modules. This local control of the battery module reduces the amount of wiring required to perform the overall battery management process vs a centrally located board monitoring the full pack. The PC board monitors the SOC (state of charge) for each of the individual “Bricks” in the modules.

The Model 3 BMS controls the voltage of the 23 to 25 individual brick sections to within 2 to 3 millivolts. This precise level of voltage variance demonstrates an improved methodology for balancing batteries and is much better than what is typically achieved in an EV battery pack.

Figure 31: Tesla Model 3 Battery Management Module

Source: UBS

How do the costs compare?

Tesla's Model 3 BMS and charging components come in at $1.7k and weigh 28.5kg. This covers the entire battery management module noted above. Key components include the HV OBC/DC-DC converter, estimated at $1,065 and the HV system controller assembly at $207.

The Chevy Bolt BMS components in this sub-group cost $1.3k with a total weight of 21.1kg. Within that, the DC-DC converter costs $179 and the high-power distribution module costs $328 with any future cost reduction potential mainly seen through economies of scale.

The BMW i3 BMS and charging electronics come in at a similar $1.3k price but weigh 16.5kg. Given the lower capacity of the i3, the weight drop is expected.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

27

Figure 32: Battery Management & Charging Electronics Figure 33: Model 3 vs. Bolt Battery Mang. Breakout

Source: UBS Source: UBS

$1,700

$1,300 $1,300

Model 3 Chevy Bolt BMW i3

$1,700

Model 3 Chevy Bolt

Battery ManagementSystem

Power DistributionModule

On Board Charger

DC-DC Converter

Is Tesla Revolutionary or Evolutionary? 15 August 2018

28

Final Turn: E-Motor & Inverter What does it do?

There are three main components to the overall motor – the inverter, the electric motor, and the gearbox.

Inverter: To drive the e-motor and wheels, power from the battery pack flows through the HV controller/power distribution module to an inverter. The inverter takes DC supplied from the power distribution and converts it to 3-phase AC for synchronous motor control. This also works in the reverse to take AC power from regenerative braking and charge the DC battery pack.

E Motor & Gearbox: Once the inverter has converted the power flow to an AC current, the e-motor converts the current to a rotational motion. This motion feeds through the gearbox to turn the half-shafts to drive the wheels. There are different e-motor designs in the market, and each one has pros and cons. Generally speaking, permanent-magnet (PM) motors are more efficient while induction motors allow for higher performance. Thus far, most OEMs have used PM motors while Tesla has used induction motors in the Roadster, Model S and Model X.

Who makes it?

Inverter: Aisen Seiki, Bosch, Conti, Delphi, Denso, Hitachi, Hyundai Mobis, LG Electronics, Valeo, Toyota industries, BorgWarner (with Sevon acquisition) and ZF

E Motor: LG Electronics, Bosch, Conti, Denso, Valeo, Hitachi, Hyundai Mobis, BorgWarner, Magna, Nidec, Aisin Seiki, and Mahle

Gearbox: Aisin Seiki, BorgWaner, Magna, Schaeffler, and Valeo.

Who is the winner?

Of the three vehicles, the Tesla Model 3 has the lightest motor that's able to deliver the most power. Together with the gearbox and other components, its cost falls between that of the cheaper BMW i3 and the more expensive Chevy Bolt. Although a new technology for Tesla, the e-motor appears to be another step forward for EVs. The compact and modular design of the drive unit should help keep weights down and manufacturing cost low. Although the i3 and Chevy Bolt motors were steps forward when they were introduced, the Model 3 once again appears to have the benefit of time on its side and appears to be the tech leader. E-Motor winner: Tesla Model 3.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

29

Figure 34: Summary of Inverter

2017 Model 3 2017 Chevy Bolt 2014 BMW i3

The Tesla Model 3 has made technological

strides in the build and design of the

inverter/converter. The Model 3 Power Inverter

Module (PIM) is a compact unit with provisions

for controlling, distributing, and filtering the

high voltage power to drive and brake the

motor. Part of the inverter actually includes a

Silicon Carbide (SiC) power module – one of

the 1st. A SiC inverter involves using a different

material – Silicon Carbide over traditional

Silicon. SiC is a much harder material and in

operation enables the device to switch the

electricity faster, with greater efficiency

(extending the range of the battery) with the

added benefit of the material being more heat

tolerant and requiring less cooling. Despite the

semi components costing more – because the

system requires less passive components and

cooling it can potentially be cheaper at the

system level to standard silicon. In other words,

they are able to do similar work in a much

more efficient way. Additional liquid cooling

for the 24 power MOSFETs is built into the

housing.

The inverter on the Bolt is a separate unit

connected to the e-motor and power

distribution module with high voltage cables.

The system is liquid cooled.

The inverter/converter on the BLW i3 also

includes a PDC module which may partially

explain the higher costs vs. peers.

Source: UBS

Is Tesla Revolutionary or Evolutionary? 15 August 2018

30

Figure 35: Summary of Electric Motor & Gearbox

2017 Model 3 2017 Chevy Bolt 2014 BMW i3

The Model 3 gearbox houses the motor and

the gear train and several direct mounted

components in a compact configuration: oil

pump, oil filter, resolver, Power Inverter

Module, cooling lines, heat exchanger &

mounts. The gearbox is divided into 3 sections:

1: the rotor, stator, resolver, and thermistor; 2:

the drivetrain, oil filer, oil pump, and heat

exchanger and 3: dry PIM and housing. This

assembly continues the design theme we've

seen with the rest of the Model 3 components:

modular and compact.

In contrast to previous Tesla models which used

induction motors, Model 3 uses a permanent

magnet Motor. Most all other EVs have

traditionally used PM motors as they are more

efficient. Tesla's choice to switch to a PM

version is likely driven by a desire to increase

the range, especially in city driving conditions.

This efficiency comes at a price however, as

performance is impacted. In the AWD version,

the FWD motor is an induction motor while the

rear remains the PM motor – this allows for a

balance of both performance and efficiency.

The Drive unit including both the gearbox and

the rotor, are cooled using Automatic

Transmission Fluid (ATF). ATF is pumped

through an externally mounted plate style

cooler. Ethylene glycol also passes through the

external cooler in a separate cell, dissipating

the heat of the ATF through convection. The

motor sits inside of the gearbox housing which

allows coolant to flow around the outside of

the motor with no cooling jacket. Rather the

gearbox housing has cast-in inlets and outlets

to allow the trans oil to move around the

motor. Elimination of the cooling jacket is not

only a cost savings; it also reduces the size of

the gearbox housing.

The Chevy Bolt uses a permanent-magnet

synchronous motor supplied by LG Electronics

and engineered by GM. The one-speed

transmission (7.05:1 final drive ratio) houses in

the same module, also known as drive unit.

The regenerative braking function is

accomplished via the e-motor being utilized as

a generator and the inverter/converter

converting the generated AC in to DC for the

battery, i.e. no additional mechanical

equipment is required.

The one-speed transmission is directly attached

to the e-motor and sits in the same housing.

We counted only four gear wheels. A fixed

transmission ratio (to reduce the rpm of the

engine while increasing the torque) is sufficient

due to the constant torque across the entire

usable rpm range of the motor.

The BMW i3 has a hybrid synchronous electric

motor developed and produced by BMW. The

motor generates a max 125kW with peak

torque of 250 lb-ft. The motor utilizes an

arrangement of components which generates a

self-magnetizing effect helping to keep the

magnetic field stable, even at higher RPMs. This

also allows the e-motor to operate with higher

power output in an efficient size. This

translates to a better vehicle range. The 9.70:1

gear ratio is the highest among the three

vehicles, suggesting that the i3 was tuned

more for acceleration than top speed. Indeed,

the car is limited to a top speed of 93mph.

Like the Model 3 and Chevy Bolt, the i3 has

single-pedal control which allows regeneration

to recharge the battery. According to BMW, its

speed-sensitive speed control allows a driver to

perform 75% of braking maneuvers without

touching the brake pedal.

Among the three vehicles, the i3 is also the

only one that offers a range extender, the REx.

The REx is powered by a 650cc two-cylinder

34hp engine borrowed from a BMW scooter. If

equipped, the REx is mounted adjacent to the

electric motor and provides another 50-60

miles of range.

Source: UBS

Is Tesla Revolutionary or Evolutionary? 15 August 2018

31

E-motors are either manufactured by the automakers or by suppliers, the latter of which can be split into "traditional" tier-1 suppliers and new players from the electronics industry, including LG Electronics. As OEMs need to focus their investments in a rapidly changing industry, there is a case for outsourcing to prevail longer-term. For the next five years, however, some OEMs (including Tesla, Toyota, Nissan and BMW) will likely hold on to in-house manufacturing in order to better understand the technology and also the levers of cost reduction. In-house manufacturing at some OEMs (such as Volkswagen) is also likely driven by job considerations. Finally, as there is still potential for innovation in e-motor technology, some OEMs might be able to create a competitive advantage with in-house produced motors. However, as the mechanical complexity of e-motors is much lower compared to combustion engines, the number of plant workers should be dramatically lower in any case.

Figure 36: E-Motor Overview

2017 Model 3 (LR, RWD) 2017 Chevy Bolt 2014 BMW i3 (LR)

Type

3-Phase 6-Pole Permanent

magnet Motor

Permanent magnet synchronous

motor (PMSM)

Hybrid synchronous motor

(HSM)

Peak Power (HP) 306 200 170

Peak Torque (lb-ft) 307 265 250

Max RPM 18,000 8,810 11,400

Acceleration (0-60 mph in seconds) 5.1 6.9 7.3

Top Speed (mph) 140 90 93 (limited)

Cost Today $1,351 $1,436 $1,272

…E-motor $754 $836 $842

…Gearbox, housing, rest $597 $599 $430

Weight (kgs) 95.6 97.8 83.6

…E-motor (kgs) 46.1 51.5 48.4

…Gearbox, housing, rest (kgs) 49.5 46.3 35.2

Gearbox final drive ratio 9.03:1 7.05:1 9.70:1

Source: UBS

A "Revolutionary" Motor. CEO Musk has teased the fact that the rear motor in the Model 3 is a Permanent Magnet Switched Reluctance Motor. Although many other EVs use a version of a permanent magnet motor, TSLA appears to have advanced the design using technology to limit issues regarding "torque ripple" (inconsistent torque on the rotor causing power fluctuation) and rotor positioning. Without getting too into the technical details on how TSLA was able to make this advance, we do note that it allows the company a more compact motor that is actually more efficient than the company's previous versions.

How do the cost compare?

All-in the Model 3 e-motor and inverter were about $90 lower than the Chevy Bolt.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

32

Figure 37: E-Motor & Inverter Cost Comparison Figure 38: E-Motor & Inverter Cost Split

Source: UBS Source: UBS

$1,960

$2,050

$2,240

Model 3 Chevy Bolt BMW i3

$750 $840 $840

$410 $460 $290

$800 $750 $1,110

Model 3 Chevy Bolt BMW i3

Inverter Gearbox E-Motor

Is Tesla Revolutionary or Evolutionary? 15 August 2018

33

Home Stretch: Cooling & Wiring What does it do?

There are four main systems left on the EV – the cooling, the high voltage cables, the half shaft, and the range-extender (REx).

Cooling / Thermal Management: There four main components that require thermal management in a vehicle – the battery, the motor, the power electronics, and the passenger. The large battery packs which draw lots of energy as they charge and expel lots of energy as they power the car require cooling systems to function correctly and efficiently. Li-ion cells last longer and perform better when kept within the ideal temperature range. The cooling and heating systems within EVs are designed to keep the cells within this temperature range. The heating and cooling systems within these vehicles also focus on parts of the drive unit. Finally, the HVAC in an ICE leverages the heat from the engine; therefore a new solution is needed for an EV which typically requires separate heaters to accomplish the task.

High Voltage Cables: These are the thick cables that connect the major EV systems. This cost also includes $150-200 related to the charging cord.

Half Shaft: The shaft that transmits the torque from the e-motor to the wheels. There does not appear to be anything unique about this product for EVs.

REx: This is a range extender and is only offered on the BMW i3.

Who makes it?

Cooling / Thermal Management: BorgWarner, Conti, Dana, Denso, Hella, Magna, and Valeo.

Wiring: Aptiv, Lear, Leoni, Yazaki, and Sumitomo.

Half Shaft: traditional drivetrain suppliers.

How do the cost compare?

The cooling pack and lines for all three vehicles are in the $250-$300 range and weigh between 12-16kgs. Despite Tesla's more advanced design, the car is larger/more powerful which adds to the overall cost and weight. However, on this metric, we would say that Tesla is the winner.

Who is the winner?

The Tesla Model 3 had some very innovative engineering solutions, though at a similar cost to the Bolt. More importantly, the Model 3 was able to reduce the use and cost of high voltage cables by consolidating systems in the powertrain. Cooling & wiring winner: Tesla Model 3.

Is Tesla Revolutionary or Evolutionary? 15 August 2018

34

Figure 39: Summary of Cooling

2017 Model 3 2017 Chevy Bolt 2014 BMW i3

One of the notable design features of both the

past and current Tesla models is the unique

battery cooling feature. Tesla's patented system

consists of coated aluminum serpentine micro

extrusion cooling channels running lengthwise

between the cells to transport the ethylene-

glycol through the battery pack. Although the

cells themselves have been updated from the

18650 to the 2170s, the cooling system

appears to be based on the company's previous

designs.

The Model 3 uses a horizontally mounted

cooling pack as opposed to a conventional

vertically mounted cooling pack. Air enters

through the Active Grille Shutters (AGS) of the

lower grille and is pulled downward through

the cooling pack. The horizontal packaging

allows Tesla to lower the front of the hood

which helps with styling and reduces

aerodynamic drag. The cooling fan itself is

located on the bottom of the vehicle and pulls

air down to prevent ingesting road debris into

the cooling pack.

In contrast to other EVs, the Model 3 uses a

centralized coolant reservoir with integrated

chiller and pumps. As seen in the Figure below,

it uses a rotating valve in the coolant reservoir

to distribute the fluid flow in five directions.

Tesla’s coolant bottle is strategically placed to

also minimize hose lengths. The integration of

components eliminates additional brackets and

labor and simplifies the entire cooling system.

This system is also capable of providing both

cooling and heating for the battery pack, in

contrast to other EVs that use multiple systems.

Once again, the efficient layout of the battery

components minimizes the number and length

of coolant hoses and high voltage cables.

The rotating cooling valve is another innovative

advancement within the Model 3 that seems to

improve on previous tech. Its ability to direct

fluid in multiple directions allows for less

components and a more centrally managed

cooling distribution.

The Chevy Bolt has three separate thermal

management circuits: for the battery, for the e-

motor and power electronics and for the cabin.

This means it has three different coolant bottles

and the corresponding requisite pumps, valves,

etc. Battery heating/cooling as well as cooling

of power electronics is performed by liquid

circuits, in the battery pack through aluminum

plates and in the e-motor and electronics

through built-in passages in the module

housing.

Once again, as a vehicle designed from the

ground up to be an EV, the Tesla seems to

have simplified complications that seem to be

legacy for ICE OEMs. Tesla has reduced the

cooling to its bare minimum requirements and

removed components in the process. This saves

both cost and manufacturing time.

For the three vehicles used in our comparison,

the Tesla Model 3 and Chevy Bolt both use

glycol for cooling the battery, while the BMW

i3 uses AC refrigerant. The BMW i3 requires

the AC refrigerant as it needs a higher cooling

capacity for the range extender (REx) engine (if

equipped). The Model 3 and BMW i3 run

coolant lines from the front to the rear of the

vehicle. The Bolt has multiple coolant loops in

the front and does not run any coolant lines to

the rear of the vehicle.

Source: UBS

Is Tesla Revolutionary or Evolutionary? 15 August 2018

35

Figure 40: Tesla Battery Pack Cross-Sectional View Figure 41: Tesla Model 3 Rotating Cooling Valve

Source: UBS Source: UBS

How do the cost compare?

All-in the Model 3 high voltage cables were about $160 lower than the Bolt. The cooling was about in-line, and the half shaft was about $40 more costly than the Bolt.

Figure 42: Cooling, Wiring, & Other Comparison Figure 43: E-Cooling, Wiring, and Half Shaft Costs

Source: UBS Source: UBS

Other Indirect EV Costs There many systems that are powered by the engine. For example, the heating in an ICE leverages heat from the engine. In addition, certain systems need to be electrified like the steering and braking.

$850 $920

$2,670

Model 3 Chevy Bolt BMW i3

$280 $290 $290

$390 $490 $460

$180 $140 $140

Model 3 Chevy Bolt BMW i3 (exRex)

Half Shaft

High VoltageCables

Cooling

Is Tesla Revolutionary or Evolutionary? 15 August 2018

36

Appendix

Battery Background Below we revisit our overall views on batteries: raw materials, global capacity, battery tech, and cost.

Battery Raw Materials