1 V. 24.11. 2016 Family Day | 2 décembre 2016 Investor Day December 1, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1V. 24.11. 2016 Family Day | 2 décembre 2016

Investor DayDecember 1, 2016

2Wendel Investor Day | December 1, 2016

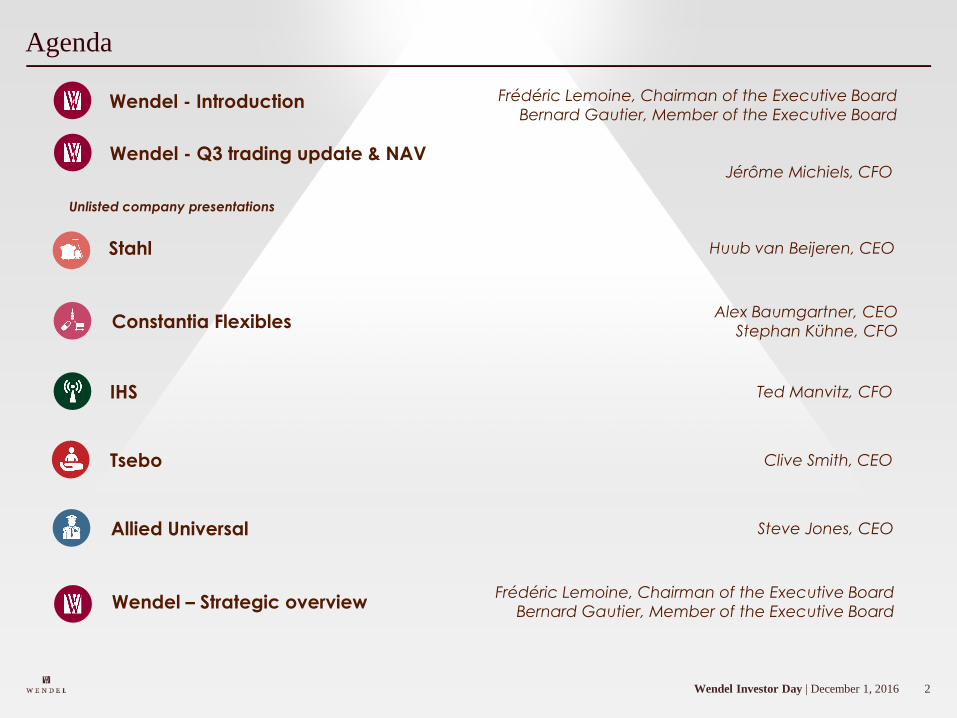

Agenda

Wendel - Q3 trading update & NAV

Stahl Huub van Beijeren, CEO

Constantia FlexiblesAlex Baumgartner, CEO

Stephan Kühne, CFO

IHS Ted Manvitz, CFO

Tsebo Clive Smith, CEO

Allied Universal Steve Jones, CEO

Wendel – Strategic overviewFrédéric Lemoine, Chairman of the Executive Board

Bernard Gautier, Member of the Executive Board

Wendel - Introduction

Jérôme Michiels, CFO

Frédéric Lemoine, Chairman of the Executive Board

Bernard Gautier, Member of the Executive Board

Unlisted company presentations

3Wendel Investor Day | December 1, 2016

Put your questions to our speakers through out the morning

OR OR

Visit app.wisembly.com

Enter keyword: wendel2016

Scan QR code

Access Wisembly directly

Send SMS to +44 1582 380 335

Type wendel2016 followed by

a space mark and your question

Q&A sessions will follow each keynote

In the room, you can ask questions orally or use our interactive tool.

From the web, you can ask questions from our interactive tool.

4Wendel Investor Day | December 1, 2016

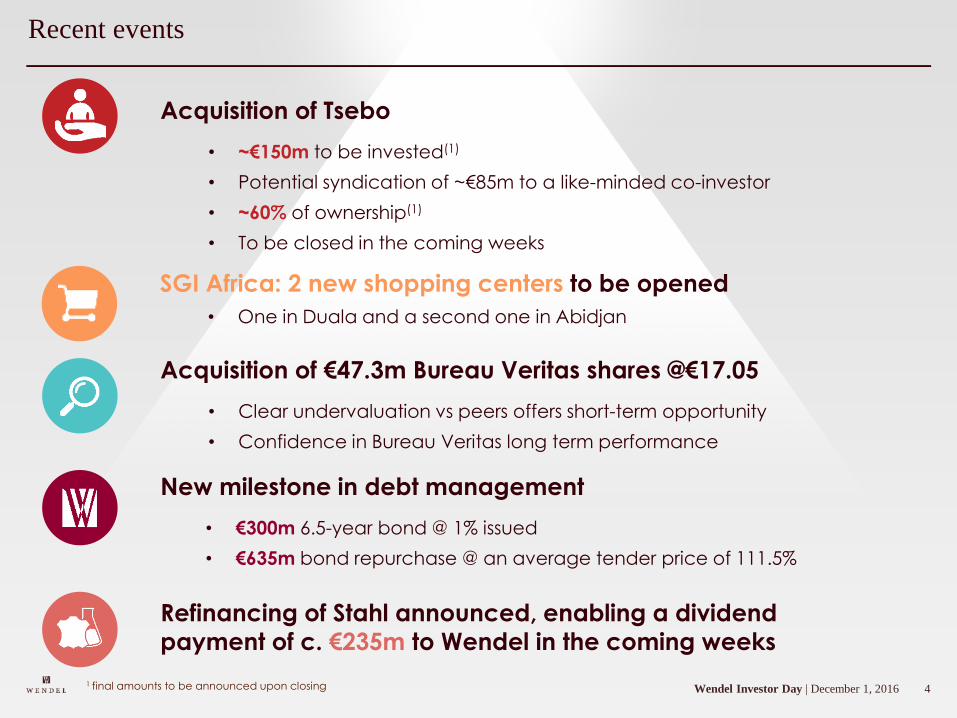

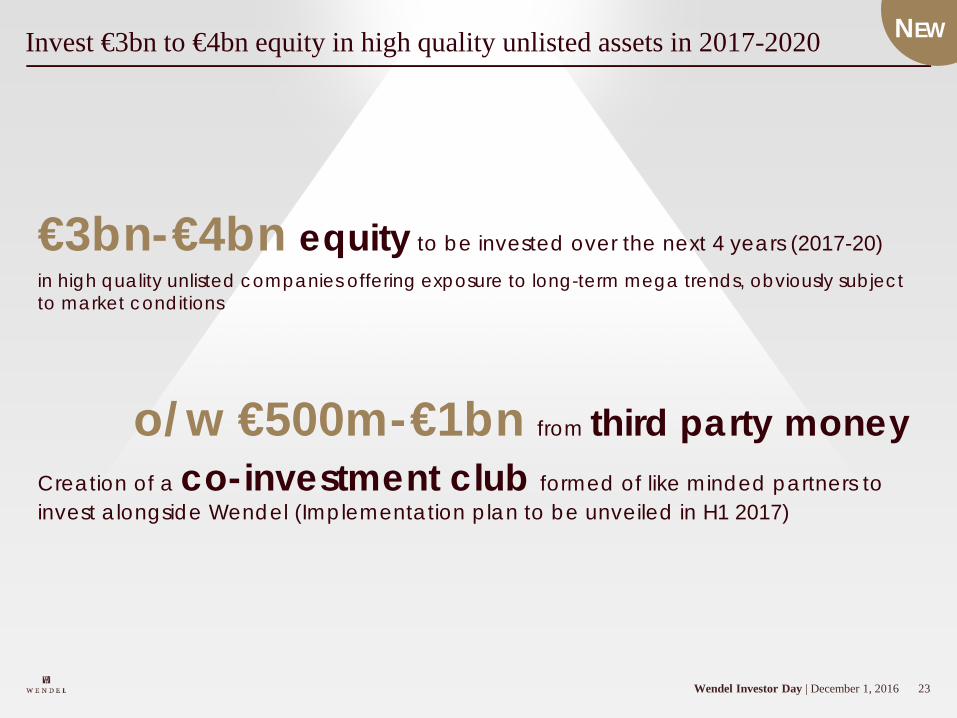

Recent events

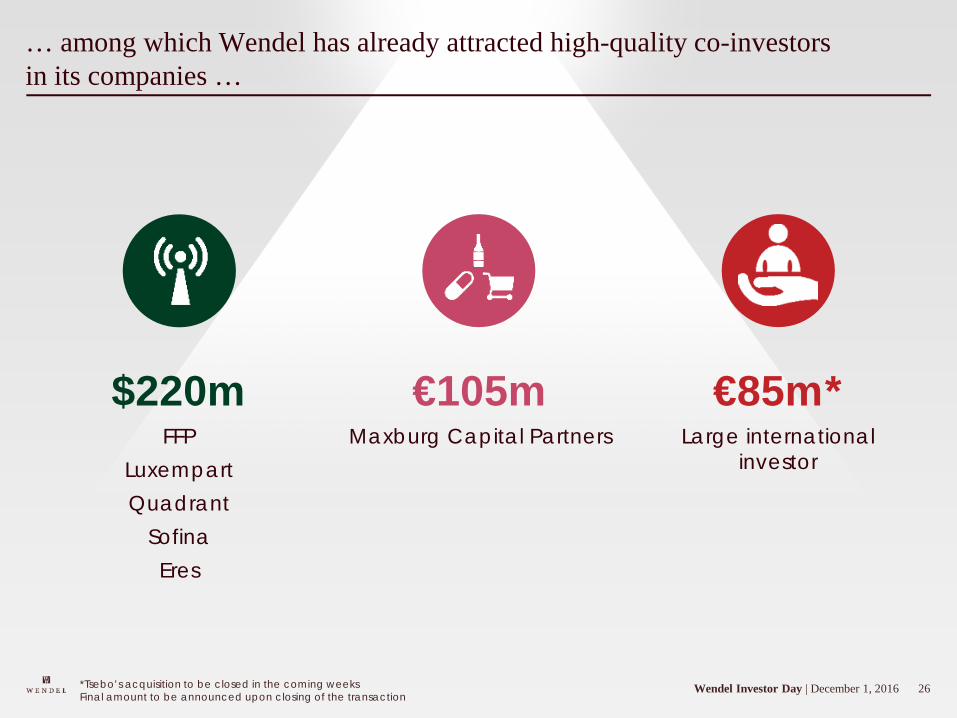

Acquisition of Tsebo

• ~€150m to be invested(1)

• Potential syndication of ~€85m to a like-minded co-investor

• ~60% of ownership(1)

• To be closed in the coming weeks

New milestone in debt management

• €300m 6.5-year bond @ 1% issued

• €635m bond repurchase @ an average tender price of 111.5%

1 final amounts to be announced upon closing

Acquisition of €47.3m Bureau Veritas shares @€17.05

• Clear undervaluation vs peers offers short-term opportunity

• Confidence in Bureau Veritas long term performance

Refinancing of Stahl announced, enabling a dividend

payment of c. €235m to Wendel in the coming weeks

SGI Africa: 2 new shopping centers to be opened

• One in Duala and a second one in Abidjan

5V. 24.11. 2016 Family Day | 2 décembre 2016

Trading updateWendel

6Wendel Investor Day | December 1, 2016

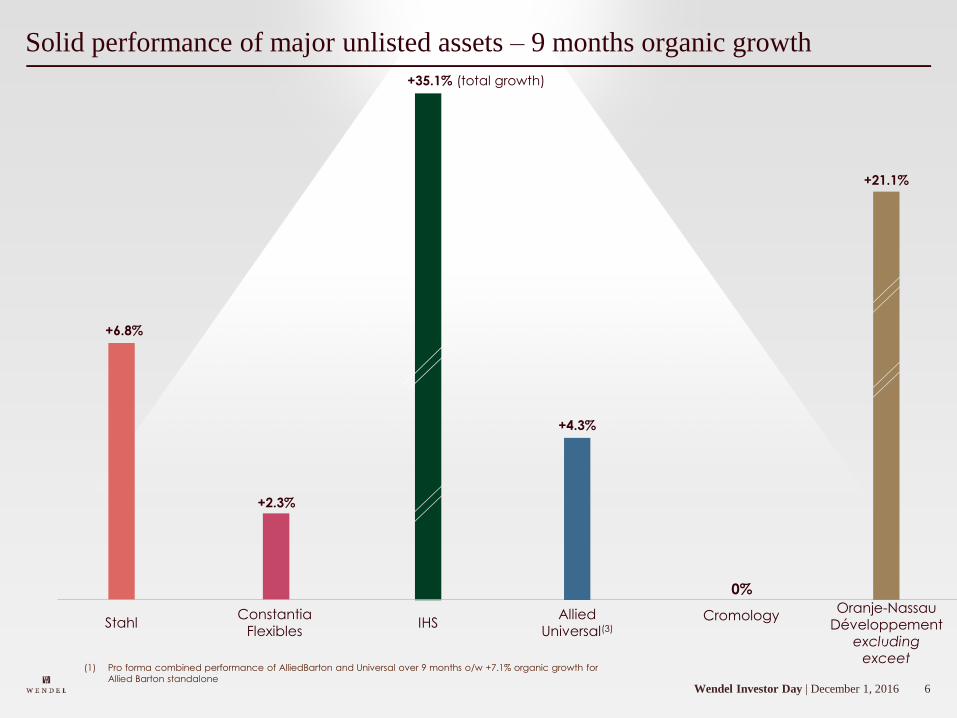

IHS

+35.1% (total growth)

Constantia Flexibles

+2.3%

Solid performance of major unlisted assets – 9 months organic growth

(1) Pro forma combined performance of AlliedBarton and Universal over 9 months o/w +7.1% organic growth for

Allied Barton standalone

StahlAllied

Universal(3)

0%

Cromology

+6.8%

+4.3%

Oranje-NassauDéveloppement

excludingexceet

+21.1%

7Wendel Investor Day | December 1, 2016

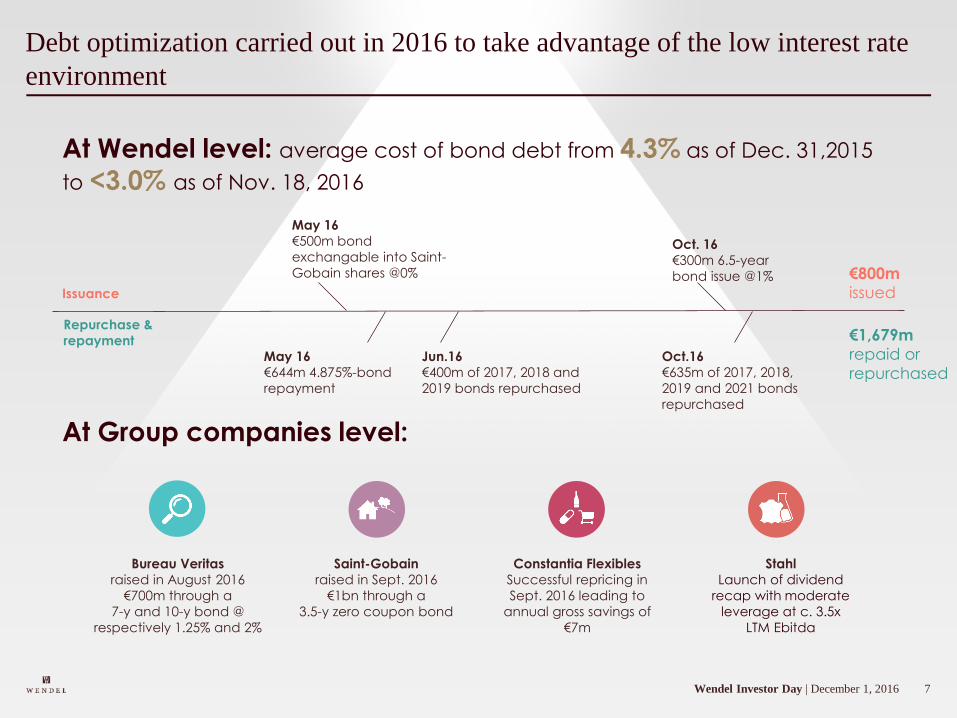

Debt optimization carried out in 2016 to take advantage of the low interest rate

environment

At Wendel level: average cost of bond debt from 4.3% as of Dec. 31,2015

to <3.0% as of Nov. 18, 2016

May 16

€500m bond

exchangable into Saint-

Gobain shares @0%

Jun.16

€400m of 2017, 2018 and

2019 bonds repurchased

Oct. 16

€300m 6.5-year

bond issue @1%

Oct.16

€635m of 2017, 2018,

2019 and 2021 bonds

repurchased

May 16

€644m 4.875%-bond

repayment

At Group companies level:

Bureau Veritas

raised in August 2016

€700m through a

7-y and 10-y bond @

respectively 1.25% and 2%

Saint-Gobain

raised in Sept. 2016

€1bn through a

3.5-y zero coupon bond

Constantia Flexibles

Successful repricing in

Sept. 2016 leading to

annual gross savings of

€7m

Stahl

Launch of dividend

recap with moderate

leverage at c. 3.5x

LTM Ebitda

Issuance

Repurchase &

repayment

€800m

issued

€1,679m

repaid or

repurchased

8Wendel Investor Day | December 1, 2016

Number

of peers9 5 6 5 7 6 9

Type of

peers

TowerCos: 2

EU, 4 emerging

markets and 3

US

3 global

packaging

groups and 2

label

companies

2 diversified

semi-

specialists

and 4 niche

specialists

Leading

global

paints and

coatings

companies

3 healthcare

packaging

manufacturers

and 4 leading

global

packaging

companies

2 generalist industrial

equipment providers,

2 foodservice

equipment

manufacturers, 1

bakery machines

manufacturer and 1

food solutions provider

Fluid equipment

manufacturers:

Europe (4),

North America

(3), Asia (2)

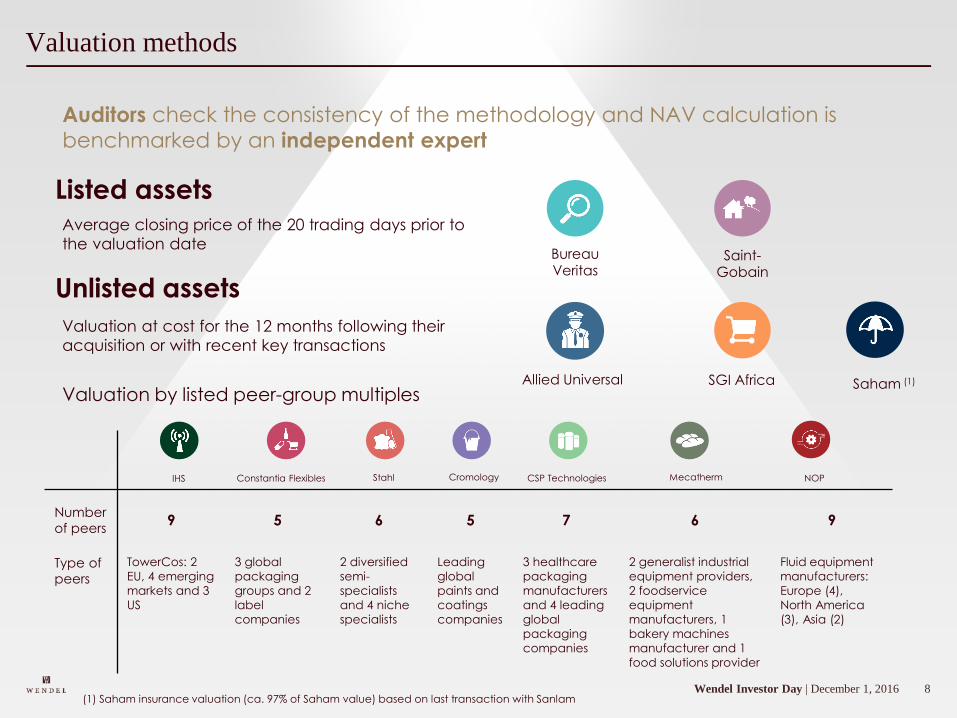

Valuation methods

Listed assetsAverage closing price of the 20 trading days prior to

the valuation date

Unlisted assets

Valuation at cost for the 12 months following their

acquisition or with recent key transactions

Valuation by listed peer-group multiples

Bureau Veritas

SGI Africa

IHS Constantia Flexibles Stahl Cromology CSP Technologies Mecatherm

Saham (1)

NOP

Allied Universal

Saint-Gobain

(1) Saham insurance valuation (ca. 97% of Saham value) based on last transaction with Sanlam

Auditors check the consistency of the methodology and NAV calculation is

benchmarked by an independent expert

9Wendel Investor Day | December 1, 2016

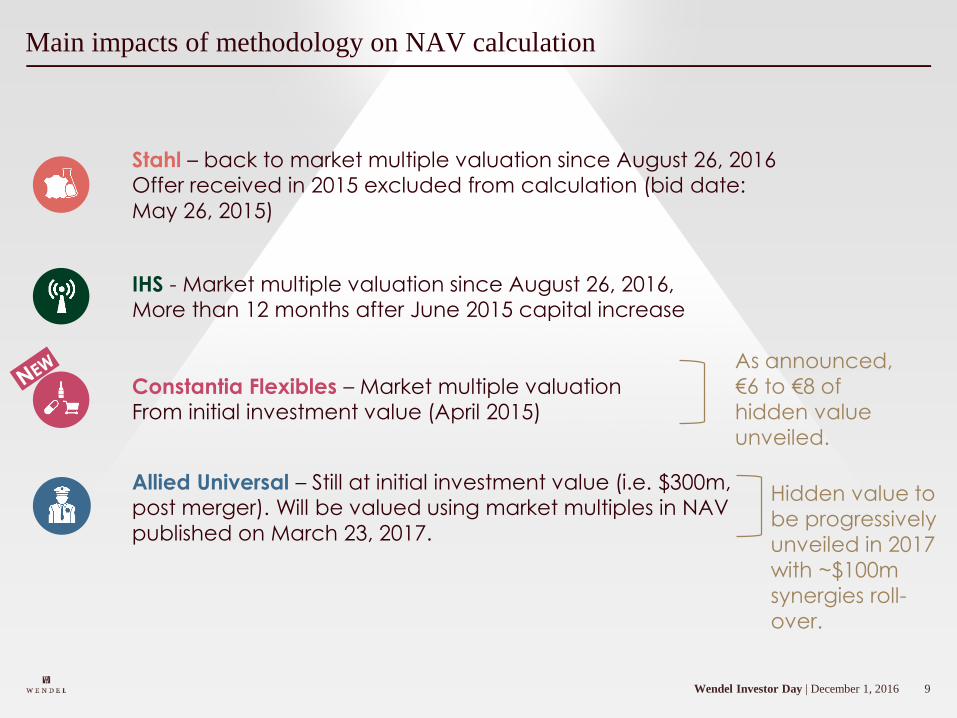

Constantia Flexibles – Market multiple valuationFrom initial investment value (April 2015)

Main impacts of methodology on NAV calculation

Stahl – back to market multiple valuation since August 26, 2016Offer received in 2015 excluded from calculation (bid date:

May 26, 2015)

IHS - Market multiple valuation since August 26, 2016,More than 12 months after June 2015 capital increase

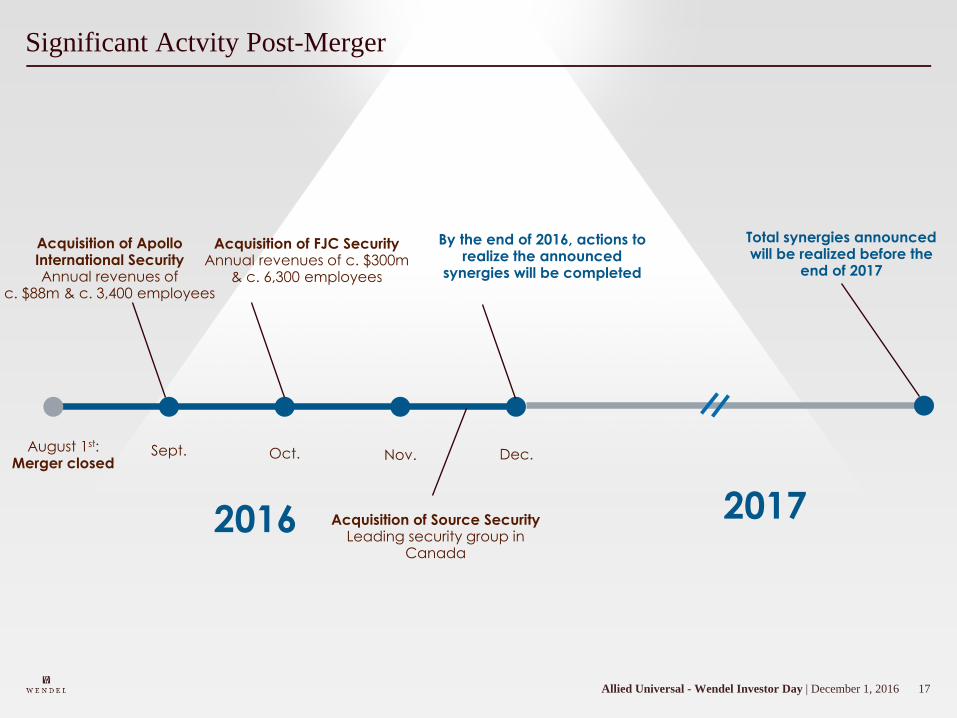

Allied Universal – Still at initial investment value (i.e. $300m, post merger). Will be valued using market multiples in NAV

published on March 23, 2017.

As announced,

€6 to €8 of

hidden value

unveiled.

Hidden value to

be progressively

unveiled in 2017

with ~$100m

synergies roll-

over.

10Wendel Investor Day | December 1, 2016

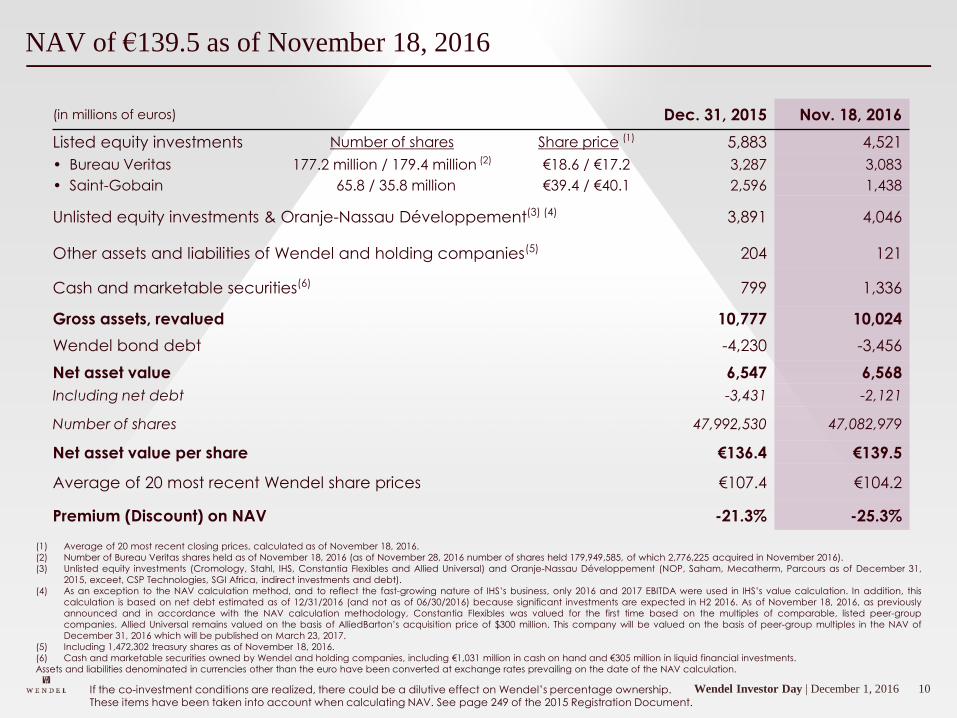

NAV of €139.5 as of November 18, 2016

(in millions of euros) Dec. 31, 2015 Nov. 18, 2016

Listed equity investments Number of shares Share price (1) 5,883 4,521

• Bureau Veritas 177.2 million / 179.4 million (2) €18.6 / €17.2 3,287 3,083

• Saint-Gobain 65.8 / 35.8 million €39.4 / €40.1 2,596 1,438

Unlisted equity investments & Oranje-Nassau Développement(3) (4) 3,891 4,046

Other assets and liabilities of Wendel and holding companies(5) 204 121

Cash and marketable securities(6) 799 1,336

Gross assets, revalued 10,777 10,024

Wendel bond debt -4,230 -3,456

Net asset value 6,547 6,568

Including net debt -3,431 -2,121

Number of shares 47,992,530 47,082,979

Net asset value per share €136.4 €139.5

Average of 20 most recent Wendel share prices €107.4 €104.2

Premium (Discount) on NAV -21.3% -25.3%

(1) Average of 20 most recent closing prices, calculated as of November 18, 2016.

(2) Number of Bureau Veritas shares held as of November 18, 2016 (as of November 28, 2016 number of shares held 179,949,585, of which 2,776,225 acquired in November 2016).

(3) Unlisted equity investments (Cromology, Stahl, IHS, Constantia Flexibles and Allied Universal) and Oranje-Nassau Développement (NOP, Saham, Mecatherm, Parcours as of December 31,

2015, exceet, CSP Technologies, SGI Africa, indirect investments and debt).

(4) As an exception to the NAV calculation method, and to reflect the fast-growing nature of IHS’s business, only 2016 and 2017 EBITDA were used in IHS’s value calculation. In addition, this

calculation is based on net debt estimated as of 12/31/2016 (and not as of 06/30/2016) because significant investments are expected in H2 2016. As of November 18, 2016, as previously

announced and in accordance with the NAV calculation methodology, Constantia Flexibles was valued for the first time based on the multiples of comparable, listed peer-group

companies. Allied Universal remains valued on the basis of AlliedBarton’s acquisition price of $300 million. This company will be valued on the basis of peer-group multiples in the NAV of

December 31, 2016 which will be published on March 23, 2017.

(5) Including 1,472,302 treasury shares as of November 18, 2016.

(6) Cash and marketable securities owned by Wendel and holding companies, including €1,031 million in cash on hand and €305 million in liquid financial investments.

Assets and liabilities denominated in currencies other than the euro have been converted at exchange rates prevailing on the date of the NAV calculation.

If the co-investment conditions are realized, there could be a dilutive effect on Wendel’s percentage ownership. These items have been taken into account when calculating NAV. See page 249 of the 2015 Registration Document.

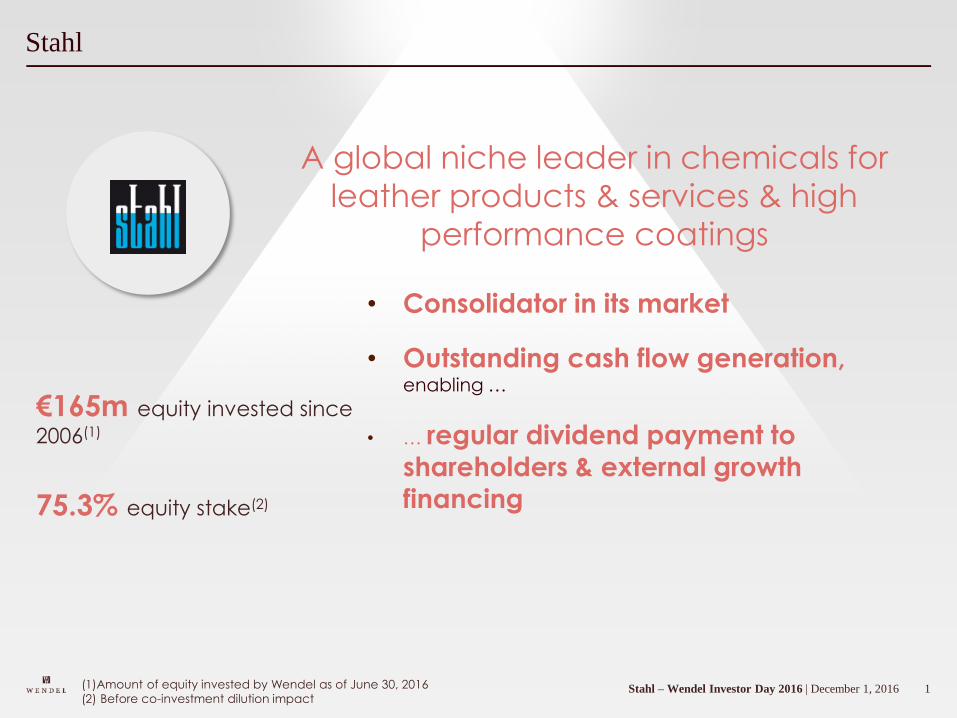

1Stahl – Wendel Investor Day 2016 | December 1, 2016

Stahl

• Consolidator in its market

• Outstanding cash flow generation, enabling …

• … regular dividend payment to shareholders & external growth

financing

A global niche leader in chemicals for

leather products & services & high

performance coatings

€165m equity invested since

2006(1)

75.3% equity stake(2)

(1)Amount of equity invested by Wendel as of June 30, 2016

(2) Before co-investment dilution impact

2Stahl – Wendel Investor Day 2016 | December 1, 2016

Huub van Beijeren–CEO of Stahl

Huub van Beijeren has been Stahl’s Chief Executive Officer since 2007.

He has led the company through the financial crisis and succeeded in making Stahl the market leader in process chemicals for leather and other substrates.

Huub has broad experience in a variety of international manufacturing industries, in public companies and in the private equity world.

Prior to Stahl, he was Director of the Paper and Packaging Industry of DS Smith plc. and at British VITA plc., a polymer manufacturer. Huub holds a Bachelor degree in Law from the University of Utrecht and a MSc in Company Law from the University of Leiden, The Netherlands.

In 2016, Huub van Beijeren received Honorary Doctorate of University of Northampton, UK.

3V. 24.11. 2016 Family Day | 2 décembre 2016

Stahl Huub van Beijeren

4Stahl – Wendel Investor Day 2016 | December 1, 2016

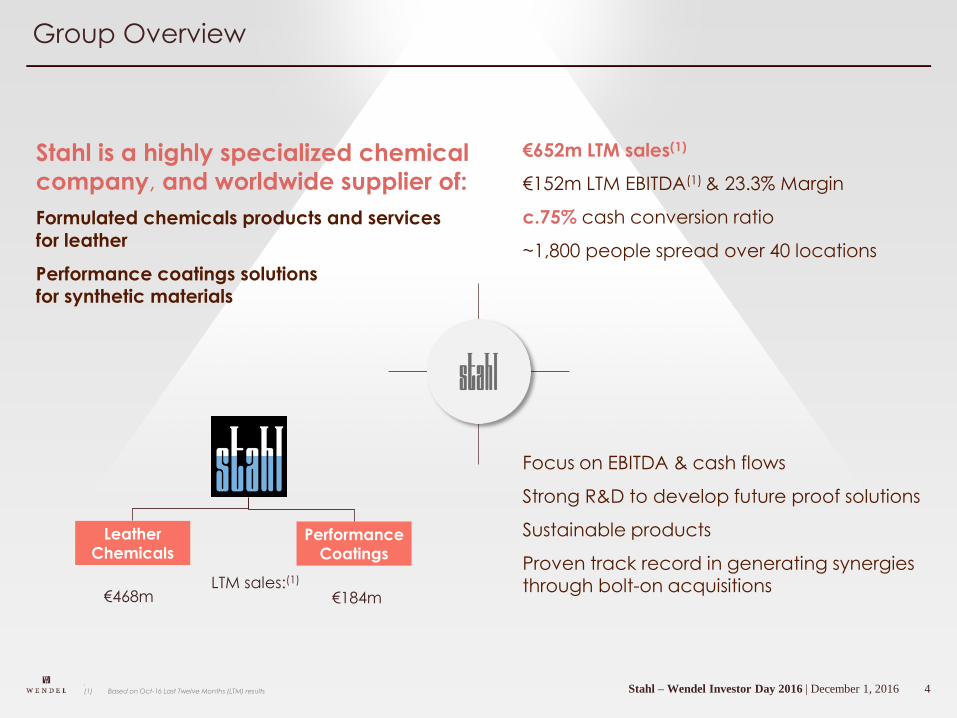

Group Overview

Stahl is a highly specialized chemical

company, and worldwide supplier of:

Formulated chemicals products and services

for leather

Performance coatings solutions for synthetic materials

€652m LTM sales(1)

€152m LTM EBITDA(1) & 23.3% Margin

c.75% cash conversion ratio

~1,800 people spread over 40 locations

Focus on EBITDA & cash flows

Strong R&D to develop future proof solutions

Sustainable products

Proven track record in generating synergies through bolt-on acquisitions

Leather

ChemicalsPerformance

Coatings

.(1) Based on Oct-16 Last Twelve Months (LTM) results

LTM sales:(1)

€184m€468m

5Stahl – Wendel Investor Day 2016 | December 1, 2016

Management Team

Bram Drexhage

Dutch

CFO - Board Member

Guido Borgart

Dutch

Group Director Operations &

Supply Line

Ralph Blach

German

Group Director R&D and

Technical Application

Uwe Siebgens

German

Group Director Performance

Coatings and Polymers

Harald BauerGermanGroup Director Wet-End, Chemicals and Dyes

Mark Chatwood

British

Group Director Automotive

Leather Chemicals

Xavier Rafols

Spanish

Group Director

Leather Finish and Pielcolor

Jacques Potier

French

Group Director Procurement

Huub van Beijeren

Dutch

CEO - Board Member

John Fletcher

American

Group Director Marketing &

Brand Services

6Stahl – Wendel Investor Day 2016 | December 1, 2016

42 Centers of Excellence, Labs & offices(1)

13 Manufacturing plants

1 Headquarters

~1,800 Employees

USA

Mexico

Brazil

Italy

Netherlands

Spain

India

China

Singapore

Argentina

Bangladesh

Colombia

Turkey

Ethiopia

Pakistan

Thailand

Taiwan

JapanKorea

France

Indonesia

Germany

Uruguay

Global Footprint

.(1) 7 Centers of Excellence, 31 application labs and 4 sales offices

7Stahl – Wendel Investor Day 2016 | December 1, 2016

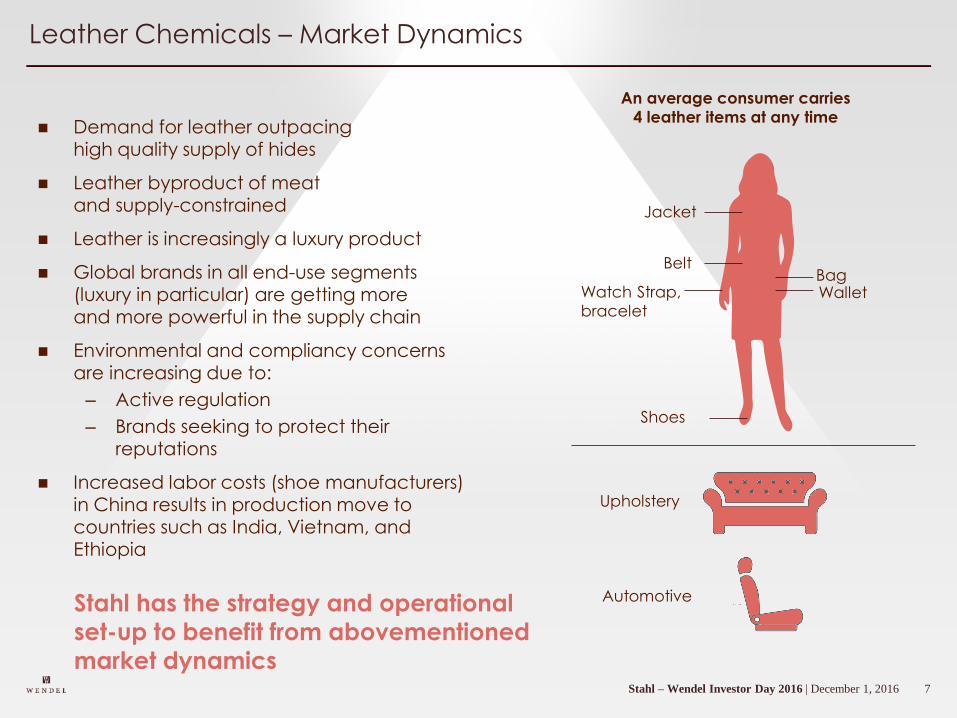

Demand for leather outpacing high quality supply of hides

Leather byproduct of meat and supply-constrained

Leather is increasingly a luxury product

Global brands in all end-use segments (luxury in particular) are getting more and more powerful in the supply chain

Environmental and compliancy concerns are increasing due to:

– Active regulation

– Brands seeking to protect their reputations

Increased labor costs (shoe manufacturers) in China results in production move to countries such as India, Vietnam, and Ethiopia

An average consumer carries 4 leather items at any time

Jacket

Belt

Watch Strap,bracelet

Shoes

BagWallet

Upholstery

Automotive

Leather Chemicals – Market Dynamics

Stahl has the strategy and operational

set-up to benefit from abovementioned

market dynamics

8Stahl – Wendel Investor Day 2016 | December 1, 2016

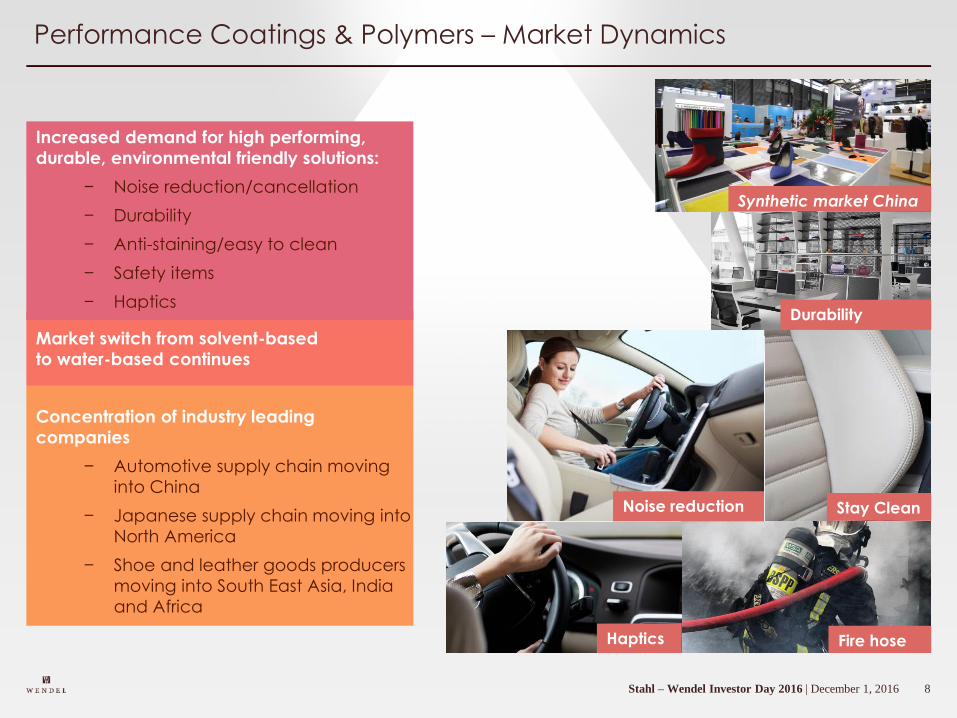

Increased demand for high performing,

durable, environmental friendly solutions:

− Noise reduction/cancellation

− Durability

− Anti-staining/easy to clean

− Safety items

− Haptics

Market switch from solvent-based

to water-based continues

Concentration of industry leading

companies

− Automotive supply chain moving

into China

− Japanese supply chain moving into

North America

− Shoe and leather goods producers

moving into South East Asia, India

and Africa

Performance Coatings & Polymers – Market Dynamics

Fire hose

Stay CleanNoise reduction

Haptics

Durability

Synthetic market China

9Stahl – Wendel Investor Day 2016 | December 1, 2016

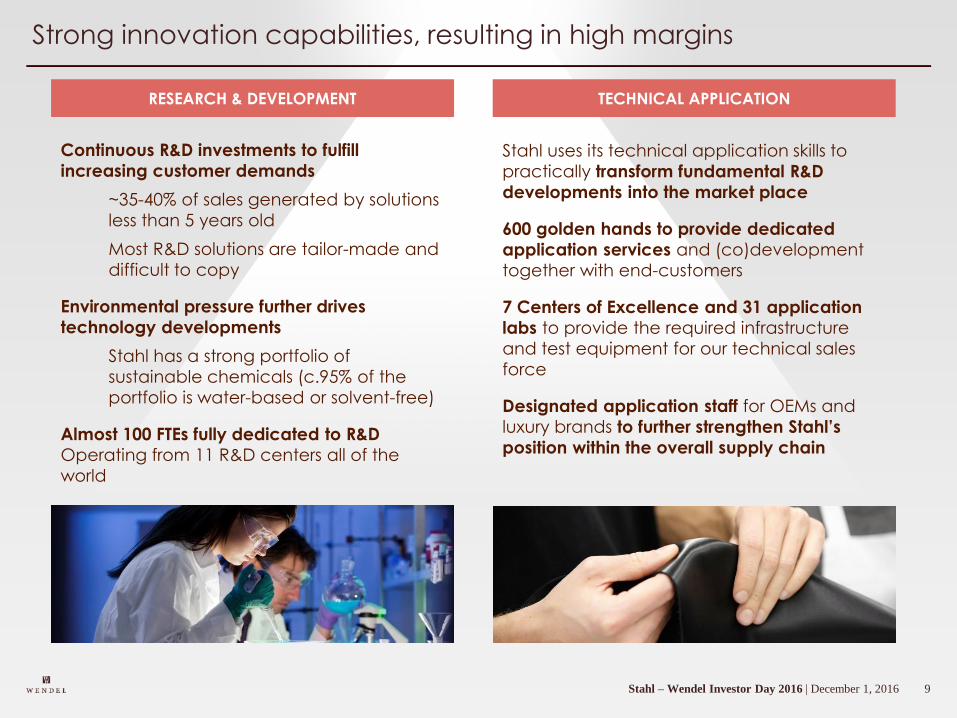

Strong innovation capabilities, resulting in high margins

Continuous R&D investments to fulfill

increasing customer demands

~35-40% of sales generated by solutions

less than 5 years old

Most R&D solutions are tailor-made and

difficult to copy

Environmental pressure further drives

technology developments

Stahl has a strong portfolio of

sustainable chemicals (c.95% of the

portfolio is water-based or solvent-free)

Almost 100 FTEs fully dedicated to R&D

Operating from 11 R&D centers all of the

world

RESEARCH & DEVELOPMENT TECHNICAL APPLICATION

Stahl uses its technical application skills to

practically transform fundamental R&D

developments into the market place

600 golden hands to provide dedicated

application services and (co)development

together with end-customers

7 Centers of Excellence and 31 application

labs to provide the required infrastructure

and test equipment for our technical sales

force

Designated application staff for OEMs and

luxury brands to further strengthen Stahl’s

position within the overall supply chain

10Stahl – Wendel Investor Day 2016 | December 1, 2016

Stahl’s transition between

2010 and 2016

11Stahl – Wendel Investor Day 2016 | December 1, 2016

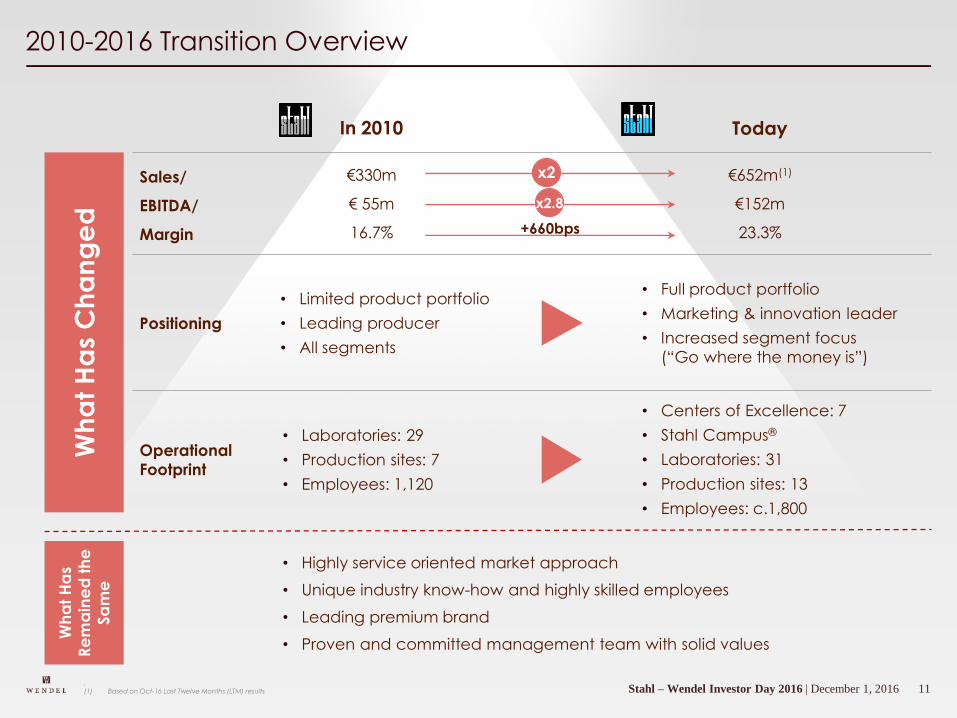

2010-2016 Transition Overview

Wh

at

Ha

s C

ha

ng

ed

Wh

at

Ha

s

Re

ma

ine

d t

he

Sa

me

• Highly service oriented market approach

• Unique industry know-how and highly skilled employees

• Leading premium brand

• Proven and committed management team with solid values

In 2010 Today

Sales/

EBITDA/

Margin

€330m

€ 55m

16.7%

€652m(1)

€152m

23.3%

.(1) Based on Oct-16 Last Twelve Months (LTM) results

Positioning

• Limited product portfolio

• Leading producer

• All segments

• Full product portfolio

• Marketing & innovation leader

• Increased segment focus

(“Go where the money is”)

Operational

Footprint

• Laboratories: 29

• Production sites: 7

• Employees: 1,120

• Centers of Excellence: 7

• Stahl Campus®

• Laboratories: 31

• Production sites: 13

• Employees: c.1,800

x2

x2.8

+660bps

12Stahl – Wendel Investor Day 2016 | December 1, 2016

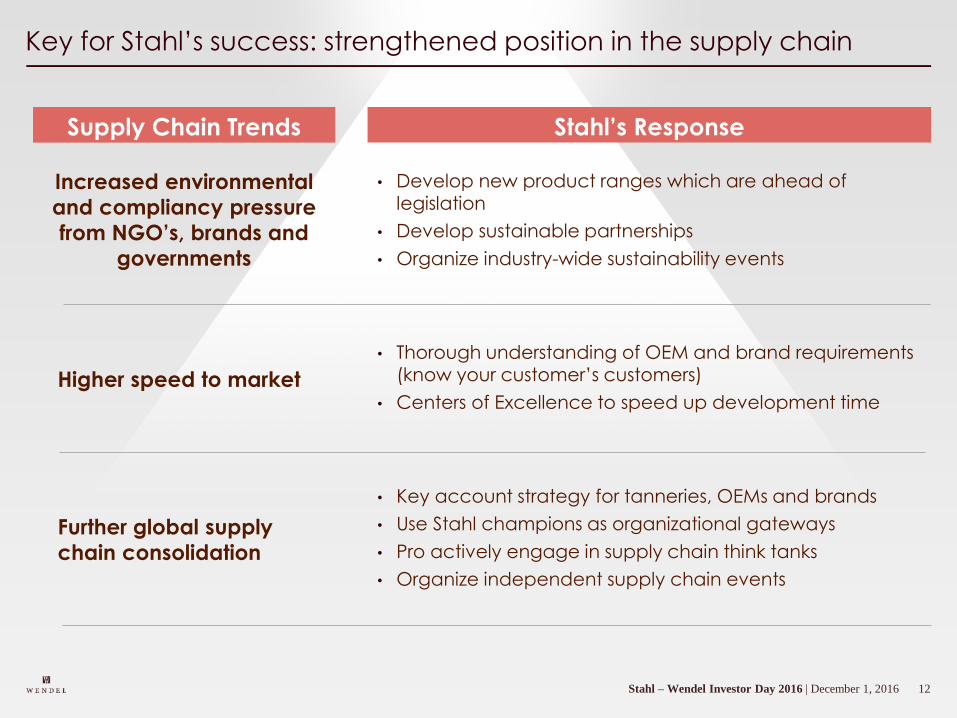

Key for Stahl’s success: strengthened position in the supply chain

Increased environmental

and compliancy pressure

from NGO’s, brands and

governments

Supply Chain Trends Stahl’s Response

• Develop new product ranges which are ahead of legislation

• Develop sustainable partnerships

• Organize industry-wide sustainability events

Higher speed to market

• Thorough understanding of OEM and brand requirements (know your customer’s customers)

• Centers of Excellence to speed up development time

Further global supply

chain consolidation

• Key account strategy for tanneries, OEMs and brands

• Use Stahl champions as organizational gateways

• Pro actively engage in supply chain think tanks

• Organize independent supply chain events

13Stahl – Wendel Investor Day 2016 | December 1, 2016

Key for Stahl Success:

Automotive Center of Excellence (CoE) in the Netherlands

The only CoE in the world to offer full testing and training facilities

for automotive interior solutions, covering:

• Leather Chemicals

• Performance Coatings

State-of-the art equipment to help OEMs design leather

and synthetic interiors for the future

Seat upholstery

Door panels

Steering wheel

Air bags

Door seals

Performance CoatingsLeather Chemicals (WE & LF)

Instrument panel

Shift boot/gear lever

Head rest

Weather strips

Sun visorPillar coverCenter

console

14Stahl – Wendel Investor Day 2016 | December 1, 2016

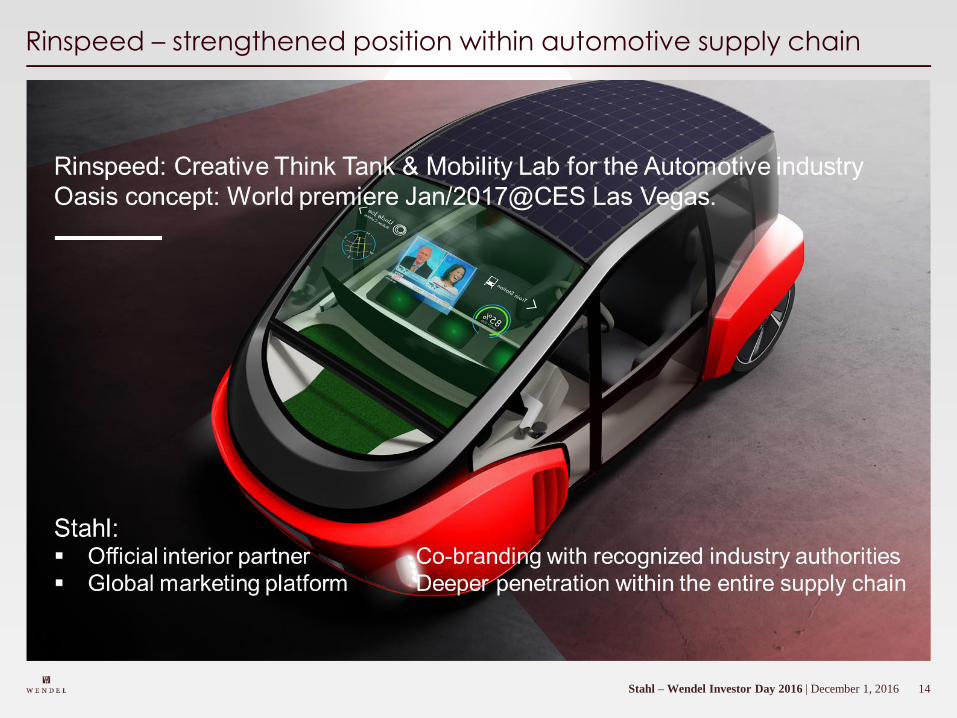

Rinspeed – strengthened position within automotive supply chain

15Stahl – Wendel Investor Day 2016 | December 1, 2016

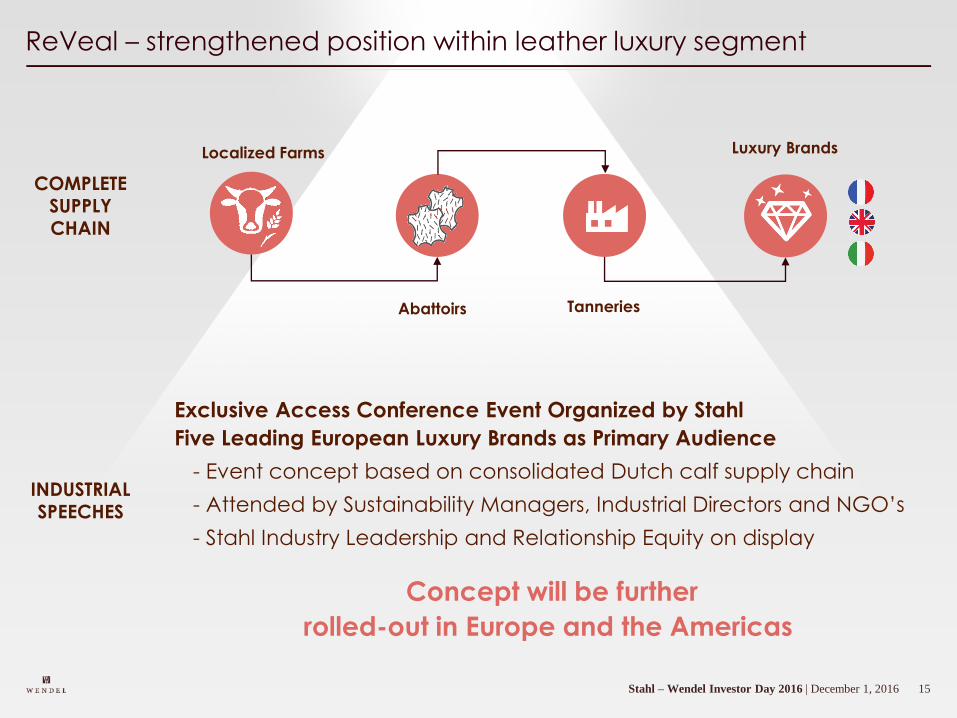

ReVeal – strengthened position within leather luxury segment

Tanneries

Localized Farms

Abattoirs

Exclusive Access Conference Event Organized by Stahl

Five Leading European Luxury Brands as Primary Audience

- Event concept based on consolidated Dutch calf supply chain

- Attended by Sustainability Managers, Industrial Directors and NGO’s

- Stahl Industry Leadership and Relationship Equity on display

Concept will be further

rolled-out in Europe and the Americas

Luxury Brands

COMPLETESUPPLYCHAIN

INDUSTRIALSPEECHES

16Stahl – Wendel Investor Day 2016 | December 1, 2016

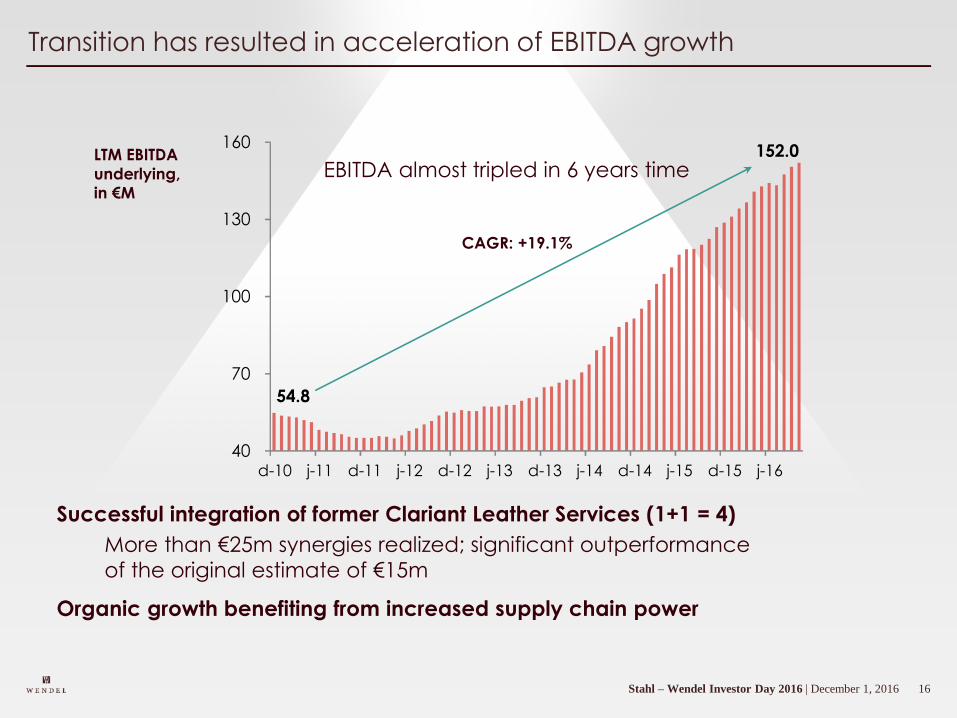

Transition has resulted in acceleration of EBITDA growth

Successful integration of former Clariant Leather Services (1+1 = 4)

More than €25m synergies realized; significant outperformance

of the original estimate of €15m

Organic growth benefiting from increased supply chain power

54.8

152.0

40

70

100

130

160

d-10 j-11 d-11 j-12 d-12 j-13 d-13 j-14 d-14 j-15 d-15 j-16

CAGR: +19.1%

LTM EBITDA

underlying, in €M

EBITDA almost tripled in 6 years time

17Stahl – Wendel Investor Day 2016 | December 1, 2016

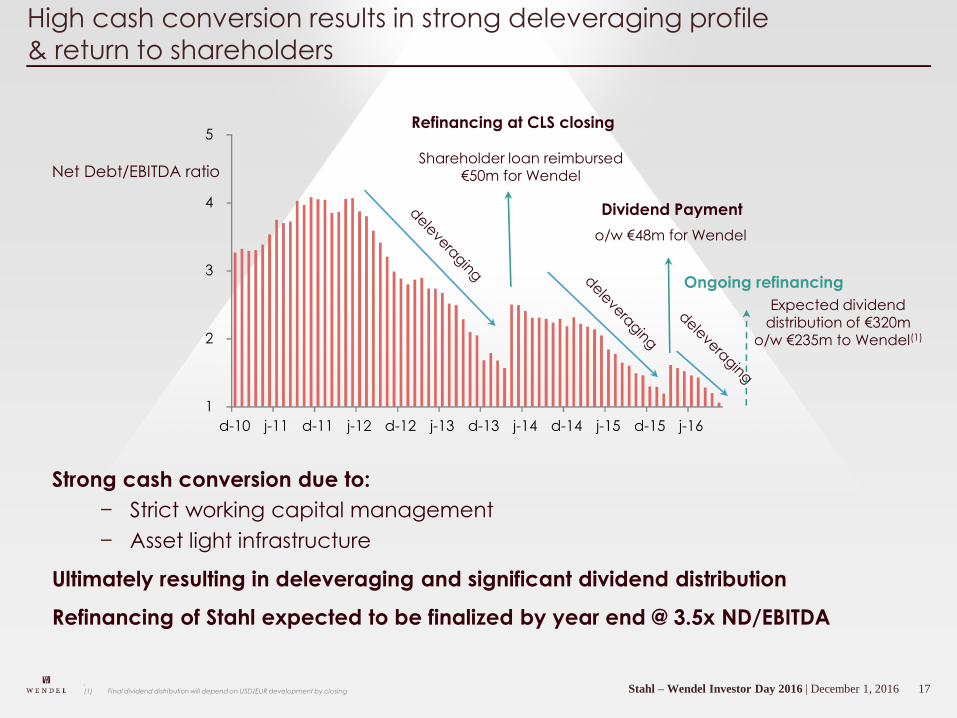

High cash conversion results in strong deleveraging profile

& return to shareholders

Strong cash conversion due to:

− Strict working capital management

− Asset light infrastructure

Ultimately resulting in deleveraging and significant dividend distribution

Refinancing of Stahl expected to be finalized by year end @ 3.5x ND/EBITDA

1

2

3

4

5

d-10 j-11 d-11 j-12 d-12 j-13 d-13 j-14 d-14 j-15 d-15 j-16

Refinancing at CLS closing

Shareholder loan reimbursed€50m for Wendel

Dividend Payment

o/w €48m for Wendel

Ongoing refinancing

Expected dividend distribution of €320m

o/w €235m to Wendel(1)

Net Debt/EBITDA ratio

.(1) Final dividend distribution will depend on USD/EUR development by closing

18Stahl – Wendel Investor Day 2016 | December 1, 2016

2010-2016 transition results

First dividends paid to our shareholders in March 2016, and more to come

Very strong operating performance & deleveraging

Materialization of value adding bolt-on acquisitions

Transformation into a €650m+ revenue companywith a more diversified business model

19Stahl – Wendel Investor Day 2016 | December 1, 2016

Key levers for future EBITDA and Cash Flow growth

ORGANICALLY

Continued focus on profitable

sales growth

Leather Chemicals : selected customer approaches/working with worldwide OEMs and brands

Performance Coatings : numerous opportunities

Leverage on green and water-

based product portfolio

(being ahead of legislation)

ACQUISITIONS

Acquisitions within Leather

Chemicals to further realize

synergies(e.g. Viswaat – April 2016

+ more to come)

Buy and build acquisitions within

Performance Coatings market

totaling more than €40 billion(e.g. Eagle – November 2016

+ more to come)

&

20Stahl – Wendel Investor Day 2016 | December 1, 2016

Eagle Acquisition

Significant cross selling opportunities for Stahl;leveraging on Stahl’s global footprint

Local footprint and set-up

FY 2015: Sales $ 19m; Underlying EBITDA $ 4m

U.S. market leader in water-based flame retardants

21Stahl – Wendel Investor Day 2016 | December 1, 2016

Digitalization is also a strong

lever for growth

22Stahl – Wendel Investor Day 2016 | December 1, 2016

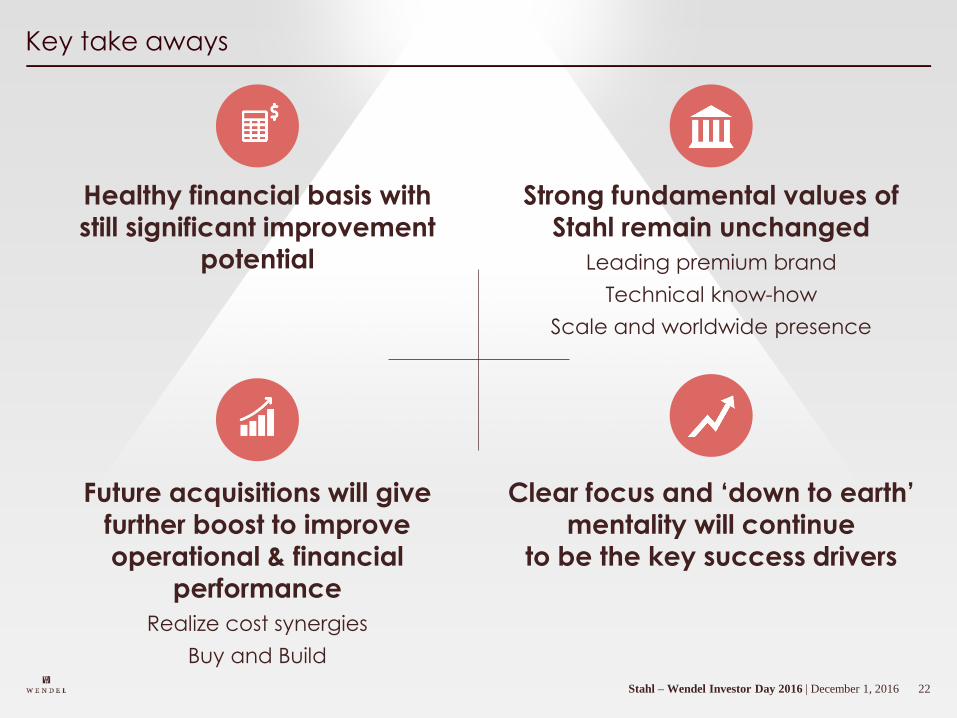

Healthy financial basis with

still significant improvement

potential

Clear focus and ‘down to earth’

mentality will continue

to be the key success drivers

Strong fundamental values of

Stahl remain unchanged

Leading premium brand

Technical know-how

Scale and worldwide presence

Future acquisitions will give

further boost to improve

operational & financial

performance

Realize cost synergies

Buy and Build

Key take aways

24Stahl – Wendel Investor Day 2016 | December 1, 2016

Appendix

25Stahl – Wendel Investor Day 2016 | December 1, 2016

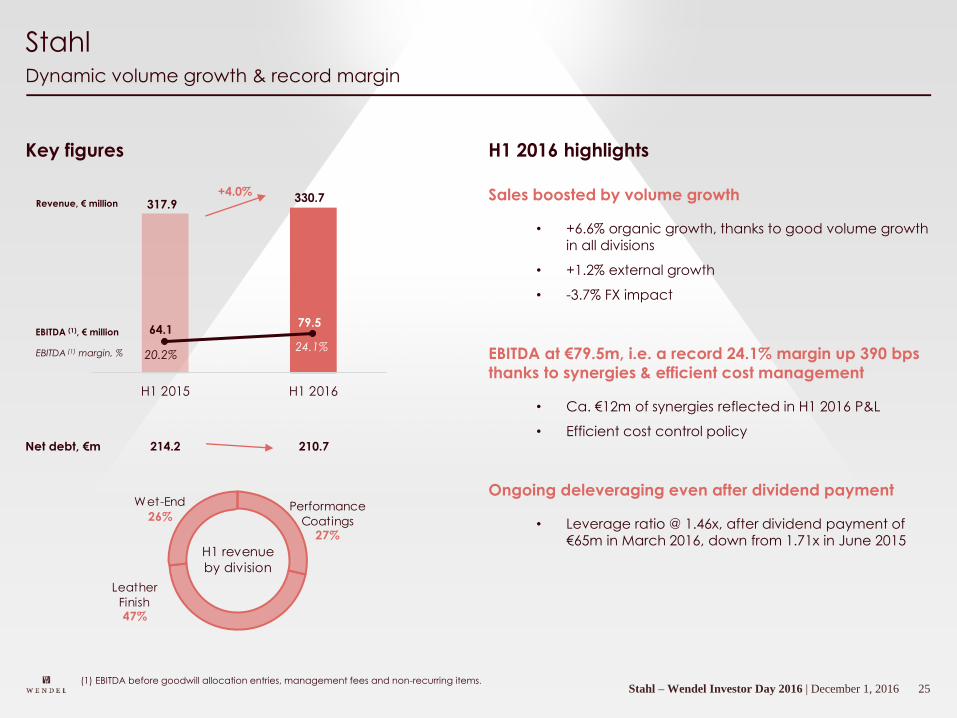

H1 2015 H1 2016

Dynamic volume growth & record margin

Stahl

(1) EBITDA before goodwill allocation entries, management fees and non-recurring items.

Key figures

330.7Revenue, € million

EBITDA (1), € million

Sales boosted by volume growth

• +6.6% organic growth, thanks to good volume growth

in all divisions

• +1.2% external growth

• -3.7% FX impact

EBITDA at €79.5m, i.e. a record 24.1% margin up 390 bps

thanks to synergies & efficient cost management

• Ca. €12m of synergies reflected in H1 2016 P&L

• Efficient cost control policy

Ongoing deleveraging even after dividend payment

• Leverage ratio @ 1.46x, after dividend payment of €65m in March 2016, down from 1.71x in June 2015

317.9

64.179.5

20.2%24.1%

Net debt, €m 214.2 210.7

+4.0%

H1 2016 highlights

EBITDA (1) margin, %

Performance

Coatings27%

Leather

Finish47%

Wet-End

26%

H1 revenue

by division

26Stahl – Wendel Investor Day 2016 | December 1, 2016

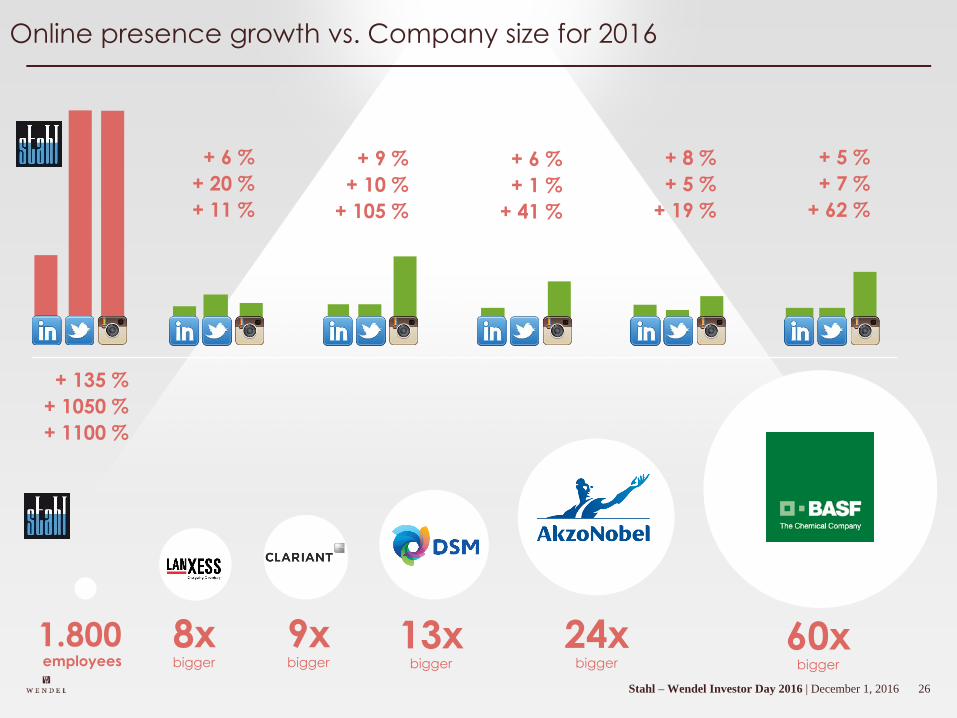

Online presence growth vs. Company size for 2016

8xbigger

9xbigger

13xbigger

24xbigger

60xbigger

1.800employees

+ 135 %

+ 1050 %

+ 1100 %

+ 6 %

+ 20 %

+ 11 %

+ 9 %

+ 10 %

+ 105 %

+ 6 %

+ 1 %

+ 41 %

+ 8 %

+ 5 %

+ 19 %

+ 5 %

+ 7 %

+ 62 %

23Stahl – Wendel Investor Day 2016 | December 1, 2016

Investor DayDecember 1, 2016

1Constantia - Wendel Investor Day | December 1, 2016

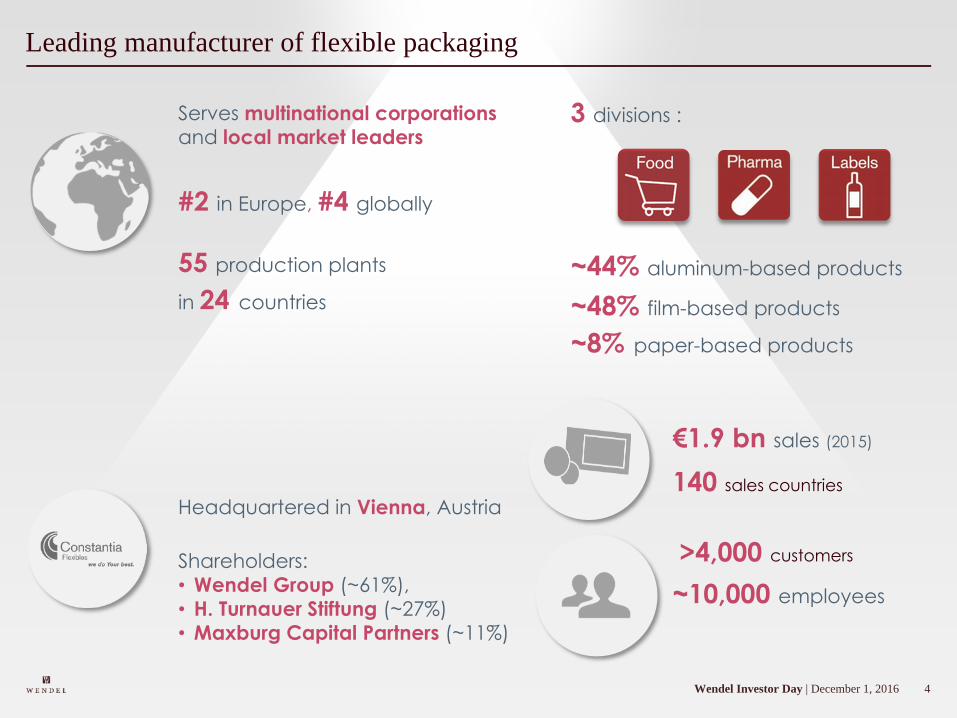

Constantia Flexibles

• International leader in flexible packaging & labels

• 55 manufacturing sites in 24 countries serving more

than 4,000 customers in 140 countries

• Resilient organic growth underpinned by …

• … long-term megatrends:Urbanization

Mobility

Middle class expansion, smaller households

Demand for individual portions, light, eco-friendly

& practical packaging

Building an alternative provider

of innovative packaging solutions

for global markets

€565m equity invested

60.5% equity stake

Partnerships with long-term

co-investors (H. Turnauer Foundation

& MCP backed by RAG

Foundation)

2Constantia - Wendel Investor Day | December 1, 2016

Alexander Baumgartner – CEO of Constantia Flexibles

• 20 years of packaging industry experience

• Extensive experience in sales & marketing activities,

plant operations, restructuring and growth strategies

• Before joining Constantia Flexibles in October 2015, he was

President for Europe of the Beauty & Home

Aptargroup division. Here he played a significant role in

leading the Beauty & Home reorganization and developing

and implementing a European manufacturing strategy.

He has previously worked for Germany’s STI Group and

Austria’s Mayr-Melnhof Group

• He is a graduate of Wirtschaftsuniversität in Vienna

and Luigi Bocconi University in Milan

3V. 24.11. 2016 Family Day | 2 décembre 2016

Constantia FlexiblesAlexander Baumgartner, CEO & Stephan Kuehne, CFO

4Wendel Investor Day | December 1, 2016

Leading manufacturer of flexible packaging

Serves multinational corporations

and local market leaders

55 production plants

in 24 countries

Headquartered in Vienna, Austria

Shareholders:

• Wendel Group (~61%),

• H. Turnauer Stiftung (~27%)

• Maxburg Capital Partners (~11%)

3 divisions :

#2 in Europe, #4 globally

~10,000 employees

~44% aluminum-based products

~48% film-based products

~8% paper-based products

€1.9 bn sales (2015)

140 sales countries

>4,000 customers

5Wendel Investor Day | December 1, 2016

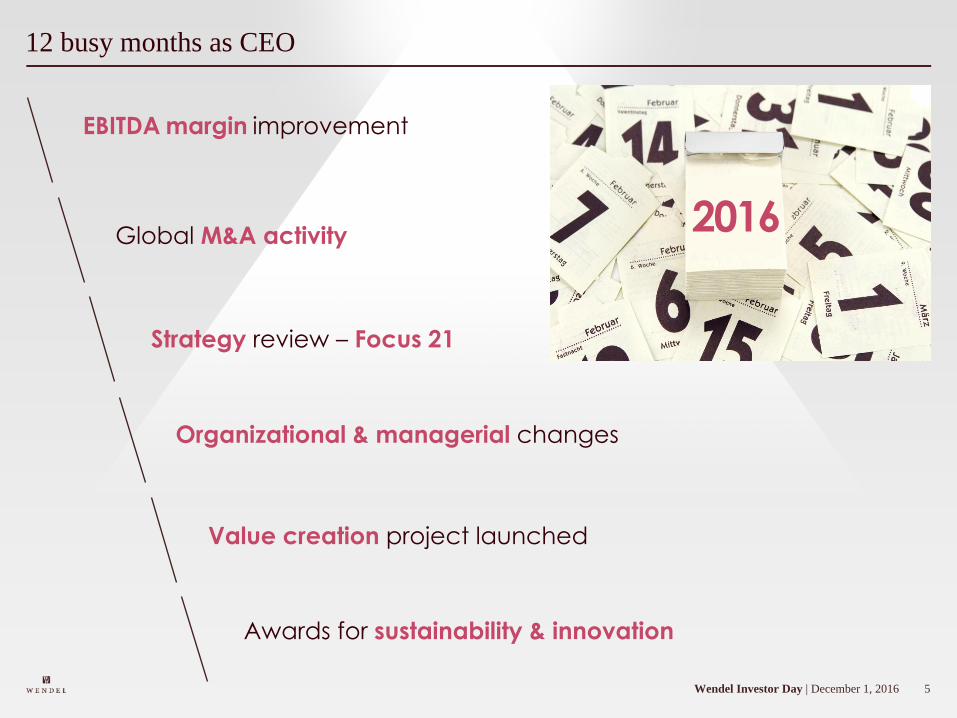

12 busy months as CEO

EBITDA margin improvement

Strategy review – Focus 21

Global M&A activity

Organizational & managerial changes

Awards for sustainability & innovation

Value creation project launched

2016

6Wendel Investor Day | December 1, 2016

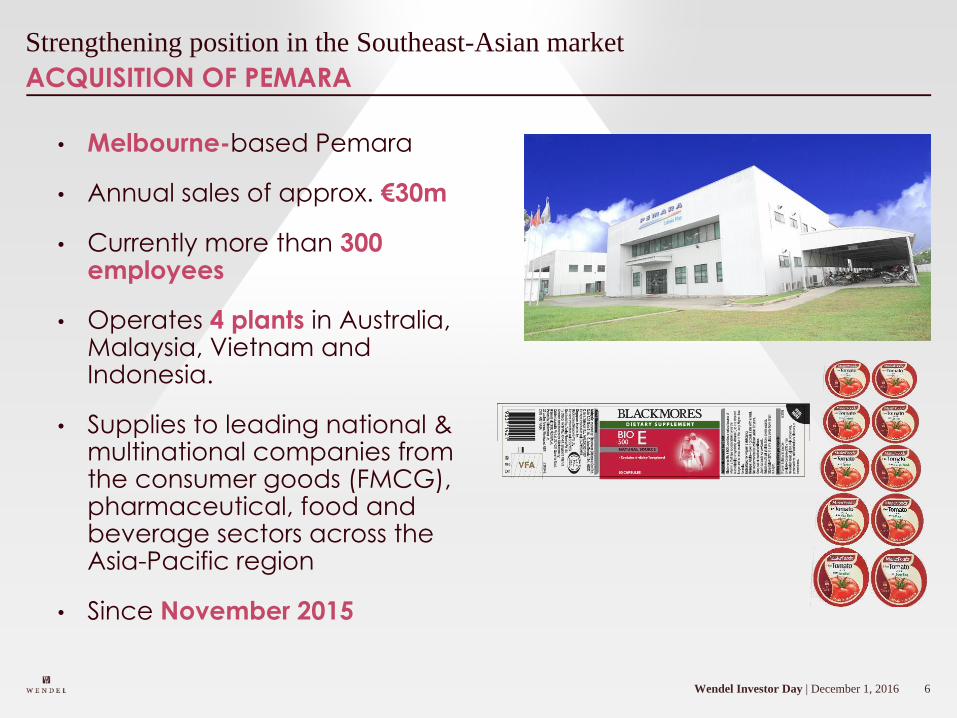

ACQUISITION OF PEMARA

Strengthening position in the Southeast-Asian market

• Melbourne-based Pemara

• Annual sales of approx. €30m

• Currently more than 300 employees

• Operates 4 plants in Australia, Malaysia, Vietnam and Indonesia.

• Supplies to leading national & multinational companies from the consumer goods (FMCG), pharmaceutical, food and beverage sectors across the Asia-Pacific region

• Since November 2015

7Wendel Investor Day | December 1, 2016

ACQUISITION OF AFRIPACK

Strengthening position in the African market

• Durban-based

• Annual ales of approx. €100m

• Currently around 1,150

employees

• Five plants in South Africa, one

in Kenya and one in Mauritius

• Second largest flexible

packaging company in South

Africa and Sub-Saharan

Africa. Also has labels

production.

• Since December 2015

8Wendel Investor Day | December 1, 2016

ACQUISITION OF OAI HUNG

Strengthening position in the Southeast-Asian market

•Headquartered in Ho Chi Minh City, Vietnam

•Annual sales of approx. €25m

•Currently 240 employees

•Main products: aluminum blister foil and rigid film for growing local pharmaceutical market

•Also active in dairy lidding sector in last two years

•State-of-the-art production site equipped with a clean room that meets high international standards

•Since July 2016

9Wendel Investor Day | December 1, 2016

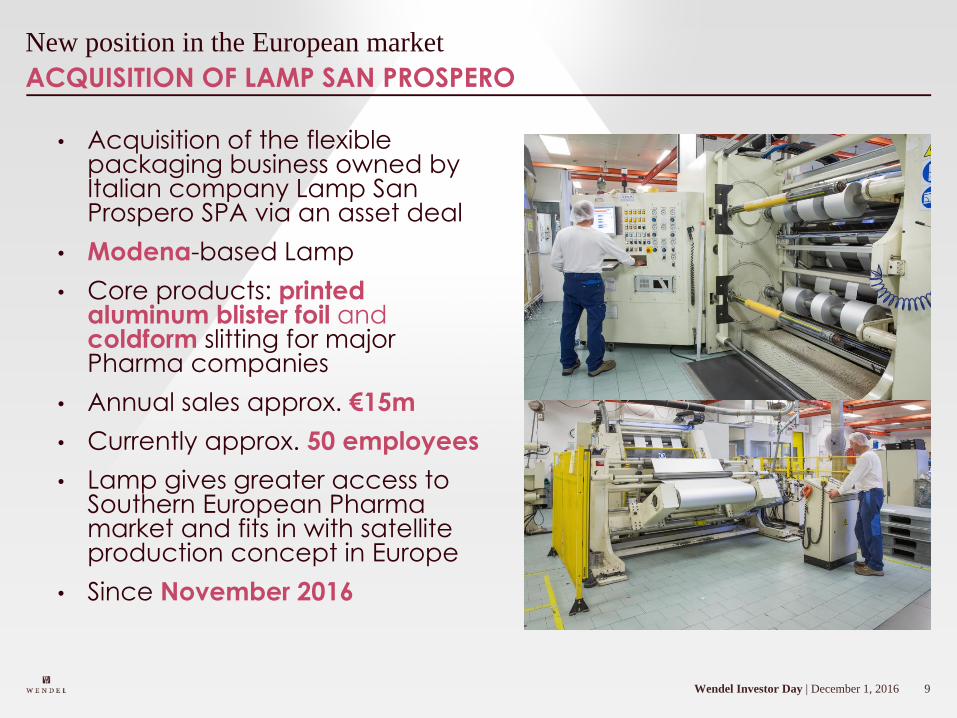

ACQUISITION OF LAMP SAN PROSPERO

New position in the European market

• Acquisition of the flexible packaging business owned by Italian company Lamp San Prospero SPA via an asset deal

• Modena-based Lamp

• Core products: printed aluminum blister foil and coldform slitting for major Pharma companies

• Annual sales approx. €15m

• Currently approx. 50 employees

• Lamp gives greater access to Southern European Pharma market and fits in with satellite production concept in Europe

• Since November 2016

10Wendel Investor Day | December 1, 2016

ALUPRINT PLEGADIZOS SOLD

Folding carton business in Mexico sold

• Constantia Flexibles acquired Aluprint

Plegadizos as part of takeover of

Globalpack in 2013

• Company located in San Luis Potosi,

Mexico

• Approximately 600 employees

• Manufactures folding cartons and

high graphics micro-corrugated boxes

for the fast moving consumer goods

industry in Mexico, the U.S., Canada,

Central America and the Caribbean

• Sold in November 2016

11Wendel Investor Day | December 1, 2016

VERSTRAETE IN-MOULD LABELS

In-mould labels investment in USA

• New site in Clarksville, Tennessee

• First international site for global IML leader

• North America is the IML market with the best growth potential

• Reduced infrastructure and overhead cost due to close collaboration with existing labels plant

• Operational Q4 2017

• 55 jobs to be created

• Total investment: €18.5m over three years, financed out of cash flow

12Wendel Investor Day | December 1, 2016

CFO since August 2016

Stephan Kuehne appointed as new CFO

Previous positions

• Managing Director & CFO of

Intersnack Group GmbH & Co. KG,

Düsseldorf (since 2011)

• European market leader for

savory snack foods

• Annual turnover of €2.3bn

• 28 manufacturing sites

• 8,500 employees

• Deutsche Messe AG in Hannover,

Germany – Member of the Executive

Board and CFO

• Kloeckner Pentaplast of America, Inc.

in Gordonsville/VA, USA – CFO

13Wendel Investor Day | December 1, 2016

Term Loan B

Successful repricing

• Repricing, amendment and upsizing of covenant-lite cross-border Term Loan B facilities

• Amendments to €1.2bn syndicated loan facilities and reduce margin on its €660m EUR Term Loan to Euribor* + 300 bps (from Euribor + 375 bps)

• US Dollar Tranche upsized to $250mm and repriced to Libor* + 300 bps (from Libor + 375 bps)

• Company is rated B+/B1 by S&P and Moody’s

• Supported by strong interest from investors, both the Euro and US Dollar tranches were substantially oversubscribed

• Annual interest savings of €7 million

*1% floor

14Wendel Investor Day | December 1, 2016

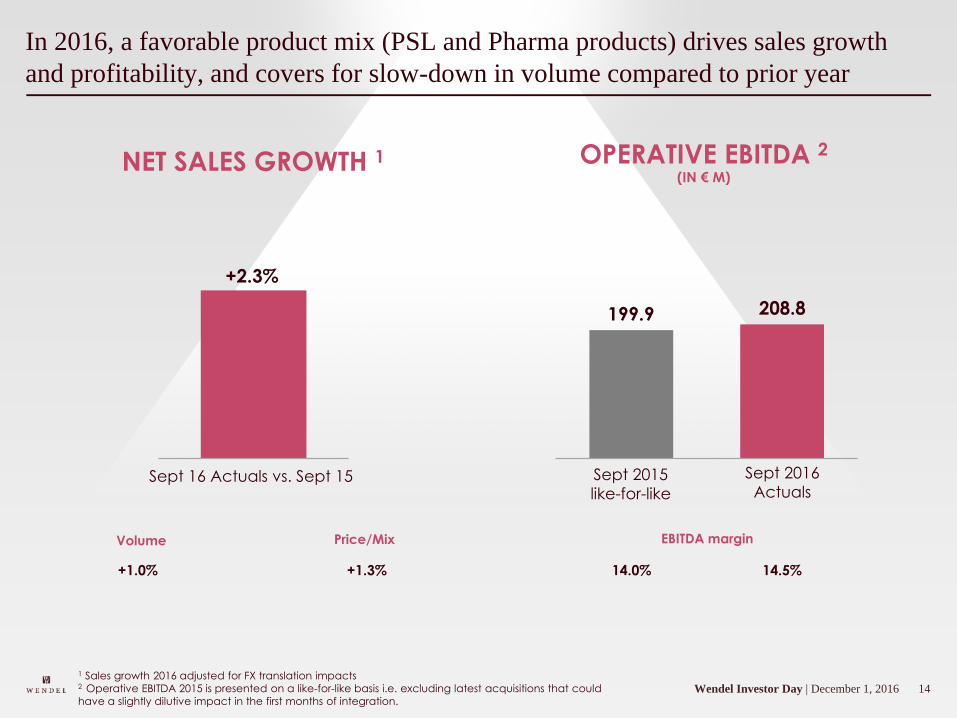

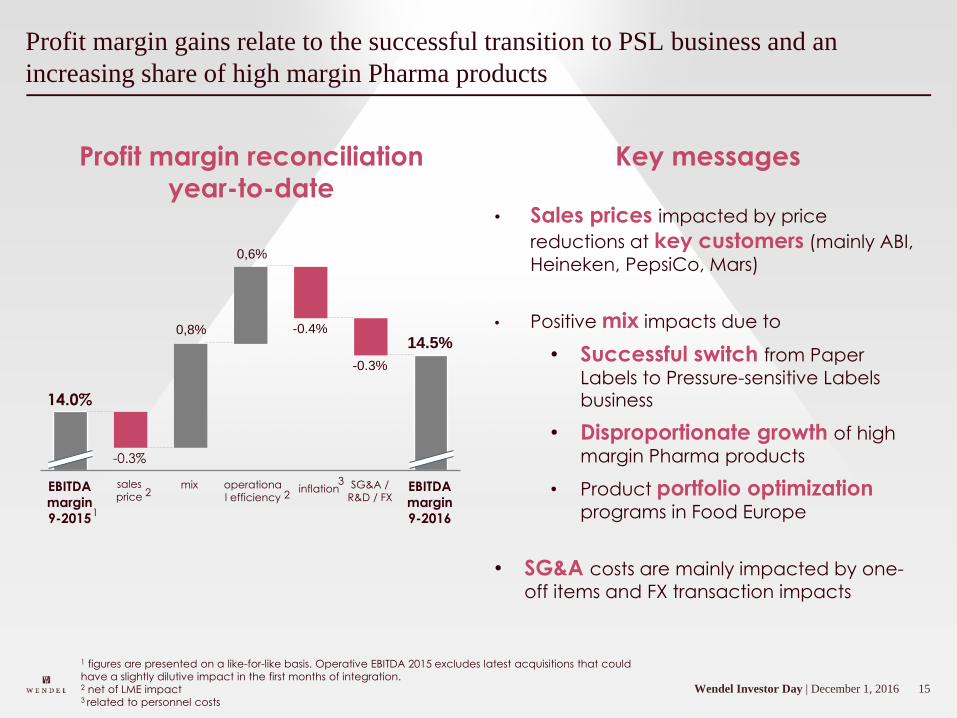

In 2016, a favorable product mix (PSL and Pharma products) drives sales growth

and profitability, and covers for slow-down in volume compared to prior year

1 Sales growth 2016 adjusted for FX translation impacts2 Operative EBITDA 2015 is presented on a like-for-like basis i.e. excluding latest acquisitions that could

have a slightly dilutive impact in the first months of integration.

NET SALES GROWTH 1 OPERATIVE EBITDA 2(IN € M)

Sept 16 Actuals vs. Sept 15

+2.3%

Volume Price/Mix

+1.0% +1.3% 14.5%

EBITDA margin

199.9 208.8

Sept 2016

ActualsSept 2015

like-for-like

14.0%

15Wendel Investor Day | December 1, 2016

0,8%

0,6%

operationa

l efficiency

Profit margin gains relate to the successful transition to PSL business and an

increasing share of high margin Pharma products

Profit margin reconciliation

year-to-date

Key messages

• Sales prices impacted by price

reductions at key customers (mainly ABI,

Heineken, PepsiCo, Mars)

• Positive mix impacts due to

• Successful switch from Paper

Labels to Pressure-sensitive Labels

business

• Disproportionate growth of high

margin Pharma products

• Product portfolio optimization programs in Food Europe

• SG&A costs are mainly impacted by one-

off items and FX transaction impacts

2 2

3inflation

-0.3%

EBITDA

margin

9-2016

SG&A /

R&D / FX

14.5%-0.4%

sales

price

-0.3%

mixEBITDA

margin

9-2015

14.0%

1

1 figures are presented on a like-for-like basis. Operative EBITDA 2015 excludes latest acquisitions that could

have a slightly dilutive impact in the first months of integration.2 net of LME impact3 related to personnel costs

16Wendel Investor Day | December 1, 2016

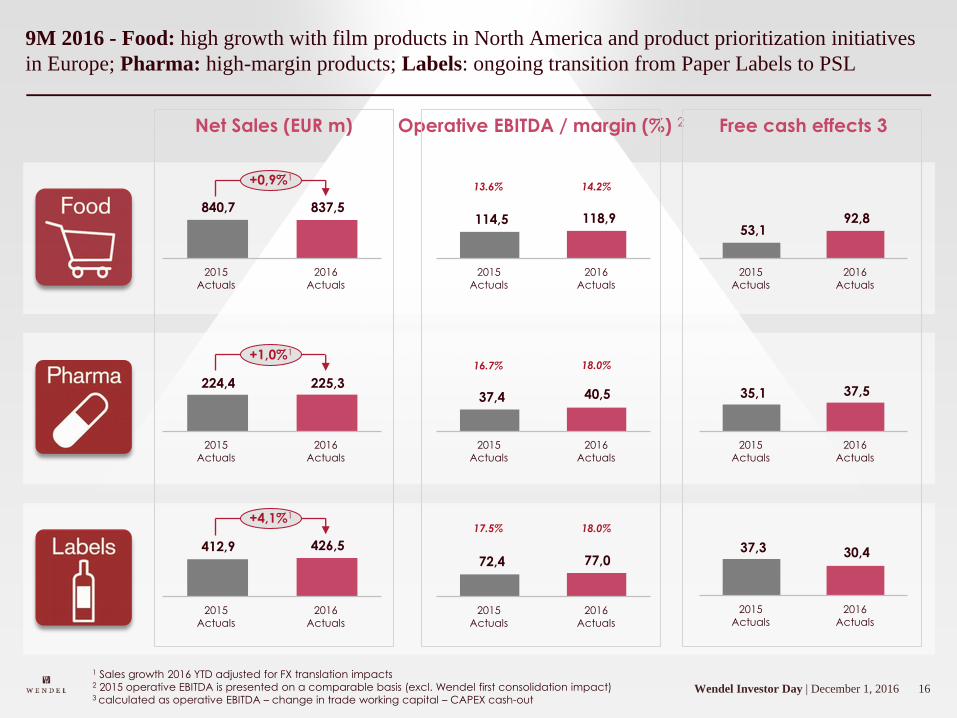

9M 2016 - Food: high growth with film products in North America and product prioritization initiatives

in Europe; Pharma: high-margin products; Labels: ongoing transition from Paper Labels to PSL

1 Sales growth 2016 YTD adjusted for FX translation impacts2 2015 operative EBITDA is presented on a comparable basis (excl. Wendel first consolidation impact)3 calculated as operative EBITDA – change in trade working capital – CAPEX cash-out

Net Sales (EUR m)

840,7 837,5

2015

Actuals

+0,9%1

2016

Actuals

224,4 225,3

+1,0%1

2016

Actuals

2015

Actuals

412,9 426,5

2015

Actuals

2016

Actuals

+4,1%1

114,5 118,9

2016

Actuals

2015

Actuals

13.6% 14.2%

Operative EBITDA / margin (%) 2

37,4 40,5

2016

Actuals

2015

Actuals

72,4 77,0

2016

Actuals

2015

Actuals

17.5% 18.0%

16.7% 18.0%

53,192,8

2016

Actuals

2015

Actuals

Free cash effects 3

35,1 37,5

2016

Actuals

2015

Actuals

37,3 30,4

2015

Actuals

2016

Actuals

17Wendel Investor Day | December 1, 2016

Digital printing is already shaping the industry

‘Print 4.0’

• Digital printing opens the doors to digitalized production with worldwide

quality standards

• Same printing result and final product

quality worldwide for global customers

• Quick turnaround saves costs and enables faster and especially more flexible production

• Cloud solutions increase flexibility

• Unlimited motives can be printed around the globe from different

operators

• Personalized and individual designs

• Trend to short production runs

18Wendel Investor Day | December 1, 2016

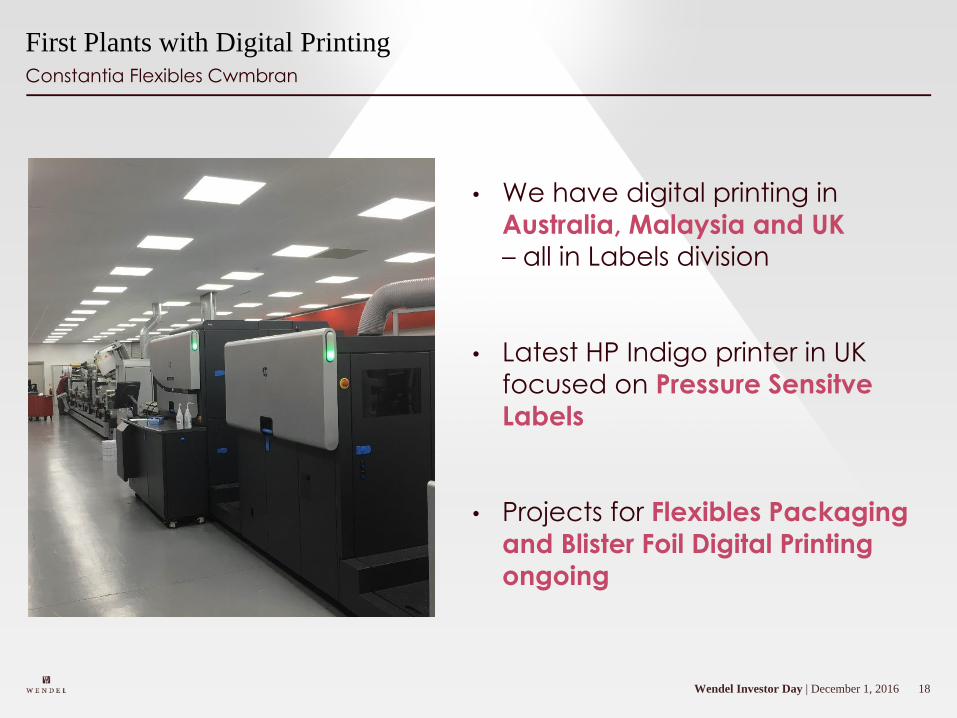

Constantia Flexibles Cwmbran

First Plants with Digital Printing

• We have digital printing in

Australia, Malaysia and UK

– all in Labels division

• Latest HP Indigo printer in UK

focused on Pressure Sensitve

Labels

• Projects for Flexibles Packaging

and Blister Foil Digital Printing

ongoing

19Wendel Investor Day | December 1, 2016

A new strategy leads our way forward

Profitable and sustainable

growth by focusing

on attractive

end-markets worldwide

We focus on selective end-markets

in attractive regions with our customers

20Wendel Investor Day | December 1, 2016

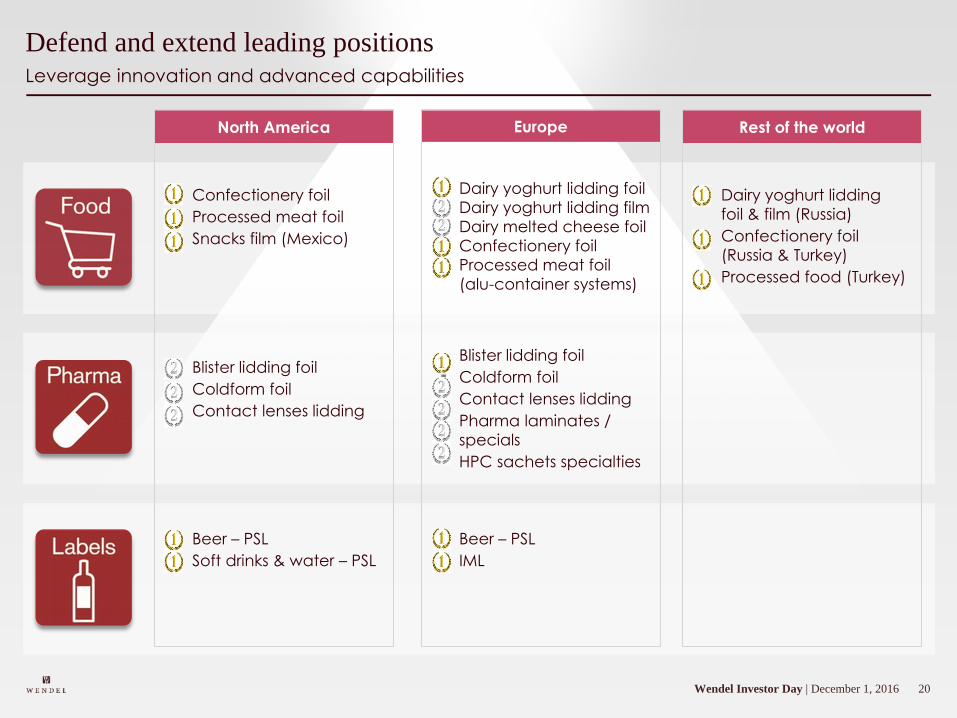

Leverage innovation and advanced capabilities

Defend and extend leading positions

Beer – PSL

Soft drinks & water – PSL

Confectionery foil

Processed meat foil

Snacks film (Mexico)

Blister lidding foil

Coldform foil

Contact lenses lidding

Beer – PSL

IML

Dairy yoghurt lidding foil

Dairy yoghurt lidding film

Dairy melted cheese foil

Confectionery foil

Processed meat foil

(alu-container systems)

Blister lidding foil

Coldform foil

Contact lenses lidding

Pharma laminates /

specials

HPC sachets specialties

North America Rest of the worldEurope

Dairy yoghurt lidding

foil & film (Russia)

Confectionery foil

(Russia & Turkey)

Processed food (Turkey)

21Wendel Investor Day | December 1, 2016

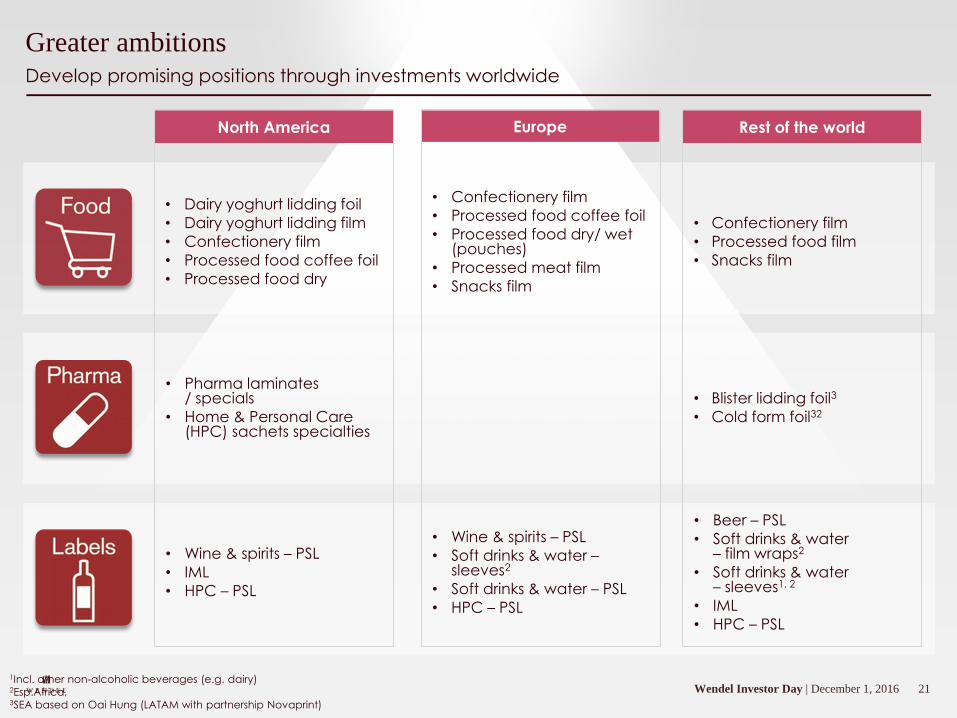

Develop promising positions through investments worldwide

Greater ambitions

1Incl. other non-alcoholic beverages (e.g. dairy)2Esp.Africa, 3SEA based on Oai Hung (LATAM with partnership Novaprint)

North America Rest of the worldEurope

• Wine & spirits – PSL

• IML

• HPC – PSL

• Dairy yoghurt lidding foil

• Dairy yoghurt lidding film

• Confectionery film

• Processed food coffee foil

• Processed food dry

• Pharma laminates / specials

• Home & Personal Care (HPC) sachets specialties

• Wine & spirits – PSL

• Soft drinks & water –sleeves2

• Soft drinks & water – PSL

• HPC – PSL

• Confectionery film

• Processed food coffee foil

• Processed food dry/ wet (pouches)

• Processed meat film

• Snacks film

• Beer – PSL

• Soft drinks & water – film wraps2

• Soft drinks & water – sleeves1, 2

• IML

• HPC – PSL

• Confectionery film

• Processed food film

• Snacks film

• Blister lidding foil3

• Cold form foil32

22Wendel Investor Day | December 1, 2016

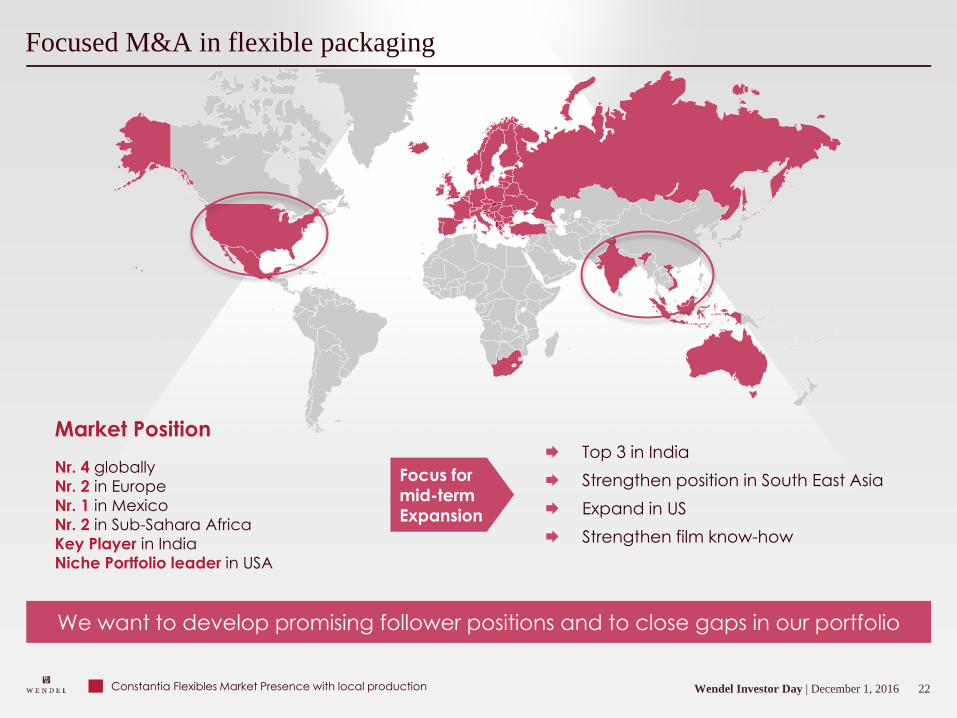

Focused M&A in flexible packaging

Top 3 in India

Strengthen position in South East Asia

Expand in US

Strengthen film know-how

Focus for

mid-term

Expansion

Constantia Flexibles Market Presence with local production

We want to develop promising follower positions and to close gaps in our portfolio

Market Position

Nr. 4 globally

Nr. 2 in Europe

Nr. 1 in Mexico

Nr. 2 in Sub-Sahara Africa

Key Player in India

Niche Portfolio leader in USA

23Wendel Investor Day | December 1, 2016

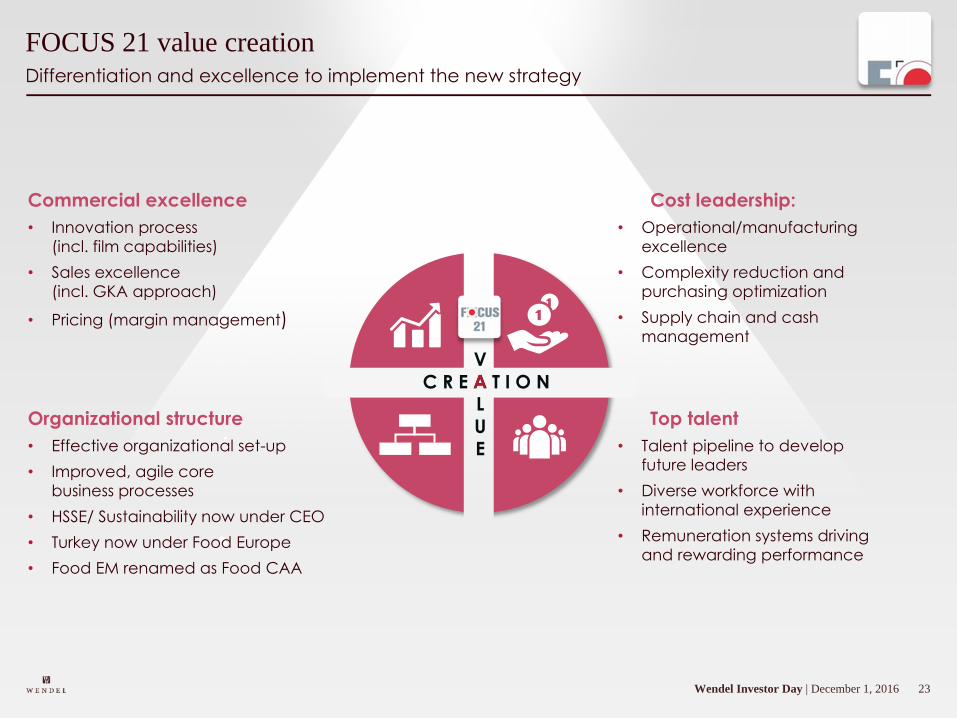

Differentiation and excellence to implement the new strategy

FOCUS 21 value creation

Top talent

• Talent pipeline to develop

future leaders

• Diverse workforce with

international experience

• Remuneration systems driving

and rewarding performance

V

A

L

U

E

C R E A T I O N

Organizational structure

• Effective organizational set-up

• Improved, agile core

business processes

• HSSE/ Sustainability now under CEO

• Turkey now under Food Europe

• Food EM renamed as Food CAA

Commercial excellence

• Innovation process

(incl. film capabilities)

• Sales excellence

(incl. GKA approach)

• Pricing (margin management)

Cost leadership:

• Operational/manufacturing

excellence

• Complexity reduction and

purchasing optimization

• Supply chain and cash

management

24Wendel Investor Day | December 1, 2016

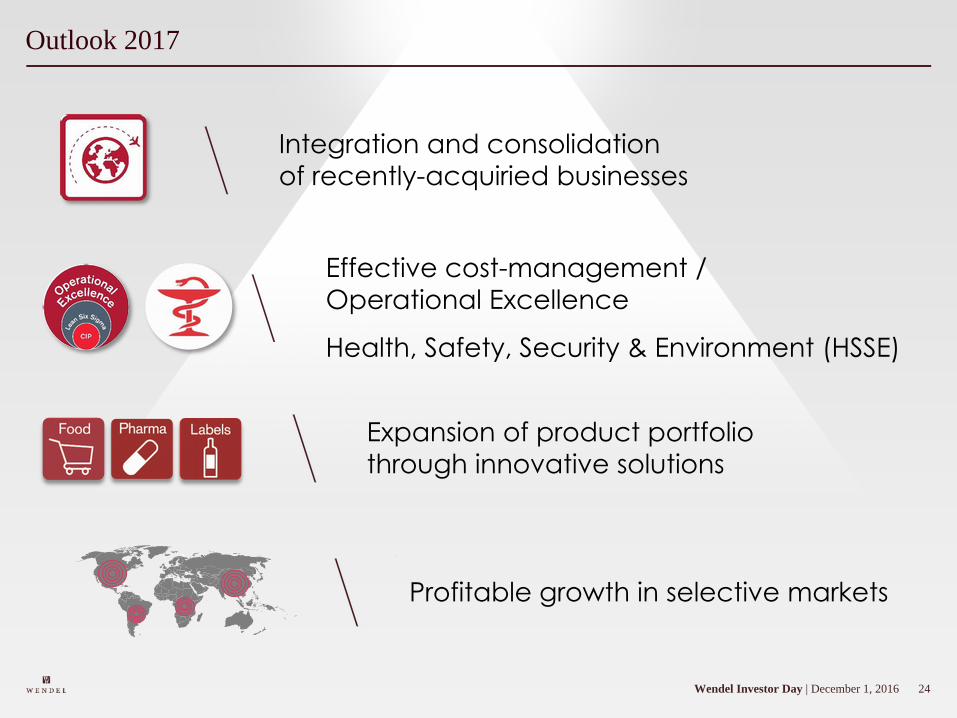

Outlook 2017

Integration and consolidation

of recently-acquiried businesses

Effective cost-management /

Operational Excellence

Health, Safety, Security & Environment (HSSE)

Expansion of product portfolio

through innovative solutions

Profitable growth in selective markets

25Wendel Investor Day | December 1, 2016

PEOPLE

PASSION

PACKAGING

Thank You!

26IHS - Wendel Investor Day | December 1, 2016

Investor DayDecember 1, 2016

1IHS - Wendel Investor Day | December 1, 2016

IHS

• Strong underlying growth in a high risk

and turbulent environmentRapid expansion of mobile phone use in Africa

Ongoing consolidation

• Undisputed African leader

• Recent volume hypergrowth leading to …

• …an already large installed base of towers

Scalable investment with high return

potential in the telecom tower business

consolidation in Africa

$825m equity invested

~26% equity stake

35% of voting rights with

co-investors

2IHS - Wendel Investor Day | December 1, 2016

Ted Manvitz–CFO of IHS

Ted joined IHS in 2009 and, as Group CFO, he is

responsible for the company’s financial management,

debt and equity funding initiatives, M&A activities and

the investor relations programme. Prior to being named

CFO, Ted served as the group’s Chief Operating Officer

and Chief Investment Officer as the company

expanded into four new countries, raised over $5.5

billion in debt and equity funding and completed 13

acquisitions.

Before joining IHS, Ted lived in Nigeria and was

managing Investment AB Kinnevik’s new investments in

Africa. Ted previously worked with JP Morgan

in London and San Francisco and started his career as

a corporate lawyer with Bryan Cave in Missouri, USA.

Ted has an MBA from the Kelly School of Business,

Indiana University; a law degree from the University of

Iowa College of Law (with distinction); and a

Bachelor’s Degree in Business Administration from Avila

University (major in Accounting cum laude).

3IHS - Wendel Investor Day | December 1, 2016

IHSTed Manvitz– Group CFO

4IHS - Wendel Investor Day | December 1, 2016

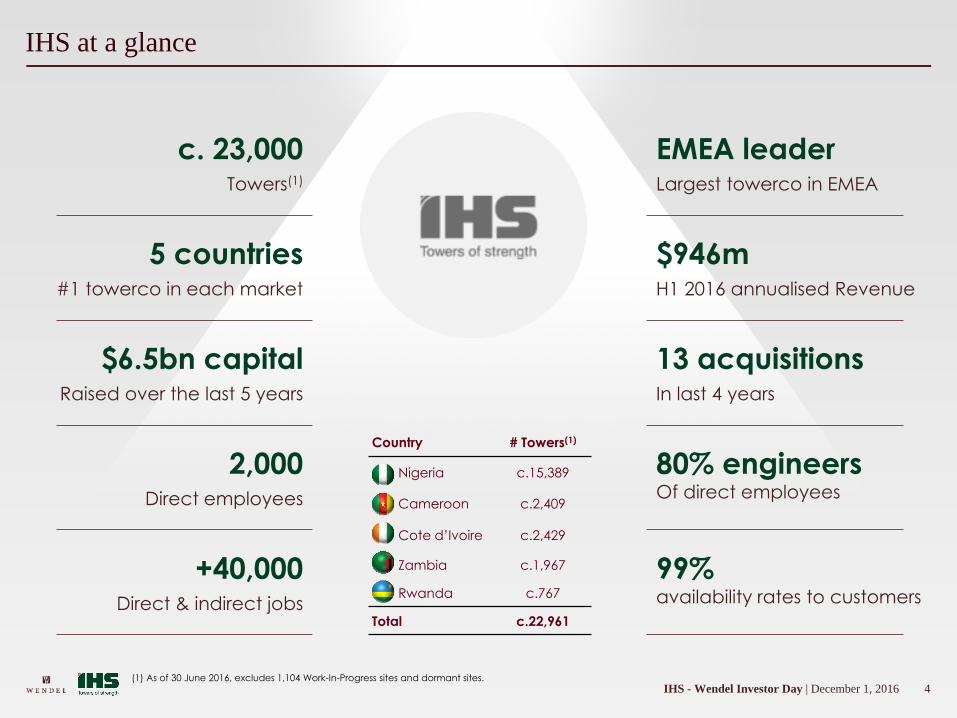

IHS at a glance

c. 23,000Towers(1)

13 acquisitionsIn last 4 years

$6.5bn capitalRaised over the last 5 years

$946m H1 2016 annualised Revenue

5 countries#1 towerco in each market

2,000Direct employees

80% engineersOf direct employees

EMEA leaderLargest towerco in EMEA

Country # Towers(1)

Nigeria c.15,389

Cameroon c.2,409

Cote d’Ivoire c.2,429

Zambia c.1,967

Rwanda c.767

Total c.22,961

+40,000 Direct & indirect jobs

99%availability rates to customers

(1) As of 30 June 2016, excludes 1,104 Work-In-Progress sites and dormant sites.

5IHS - Wendel Investor Day | December 1, 2016

IHS & The African Market

6IHS - Wendel Investor Day | December 1, 2016

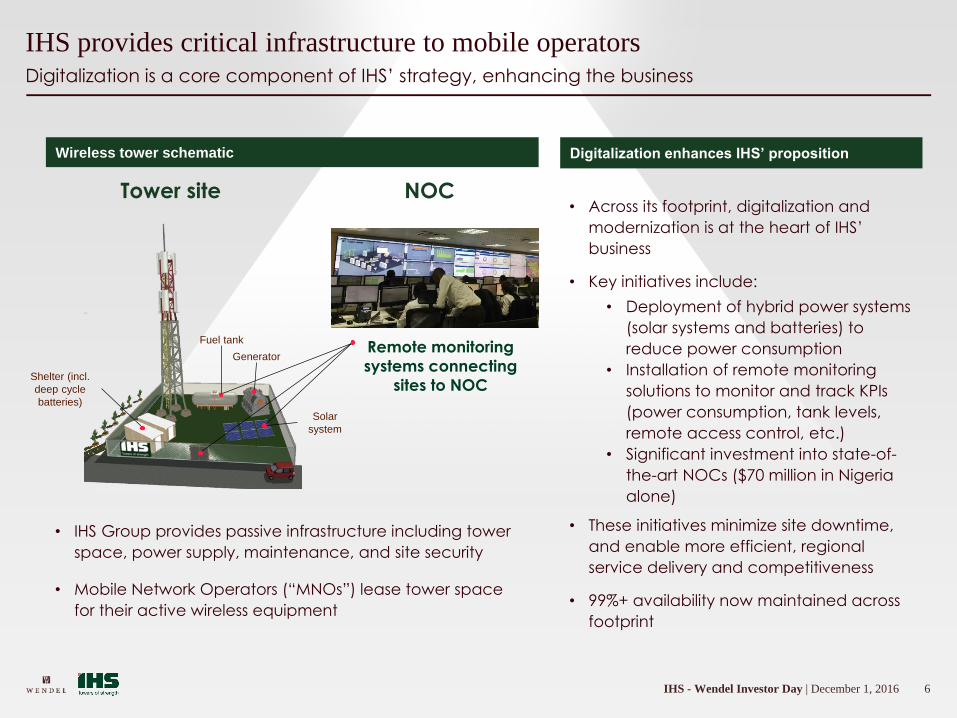

Digitalization is a core component of IHS’ strategy, enhancing the business

IHS provides critical infrastructure to mobile operators

Wireless tower schematic

• IHS Group provides passive infrastructure including tower

space, power supply, maintenance, and site security

• Mobile Network Operators (“MNOs”) lease tower space

for their active wireless equipment

Digitalization enhances IHS’ proposition

• Across its footprint, digitalization and

modernization is at the heart of IHS’

business

• Key initiatives include:

• Deployment of hybrid power systems

(solar systems and batteries) to

reduce power consumption

• Installation of remote monitoring

solutions to monitor and track KPIs

(power consumption, tank levels,

remote access control, etc.)

• Significant investment into state-of-

the-art NOCs ($70 million in Nigeria

alone)

• These initiatives minimize site downtime,

and enable more efficient, regional

service delivery and competitiveness

• 99%+ availability now maintained across

footprint

Remote monitoring

systems connecting

sites to NOC

NOCTower site

Shelter (incl.

deep cycle

batteries)

Fuel tank

Solar

system

Generator

7IHS - Wendel Investor Day | December 1, 2016

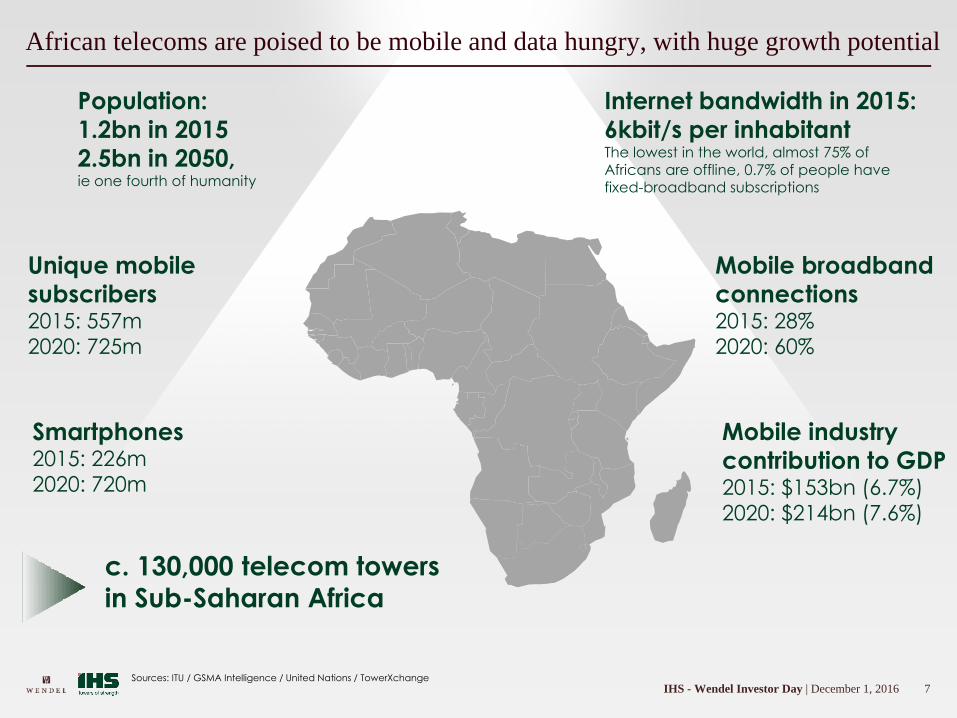

African telecoms are poised to be mobile and data hungry, with huge growth potential

Population:

1.2bn in 2015

2.5bn in 2050, ie one fourth of humanity

Internet bandwidth in 2015:

6kbit/s per inhabitantThe lowest in the world, almost 75% of

Africans are offline, 0.7% of people have fixed-broadband subscriptions

c. 130,000 telecom towers

in Sub-Saharan Africa

Unique mobile

subscribers2015: 557m

2020: 725m

Mobile industry

contribution to GDP2015: $153bn (6.7%)

2020: $214bn (7.6%)

Mobile broadband

connections2015: 28%

2020: 60%

Smartphones2015: 226m

2020: 720m

Sources: ITU / GSMA Intelligence / United Nations / TowerXchange

8IHS - Wendel Investor Day | December 1, 2016

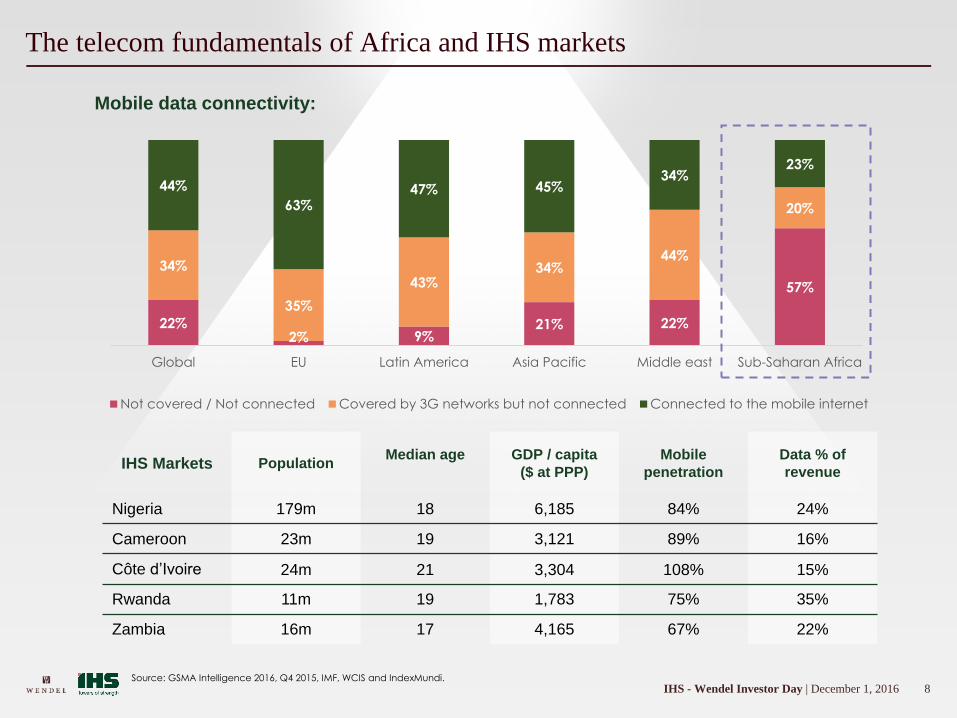

The telecom fundamentals of Africa and IHS markets

IHS Markets PopulationMedian age GDP / capita

($ at PPP)

Mobile

penetration

Data % of

revenue

Nigeria 179m 18 6,185 84% 24%

Cameroon 23m 19 3,121 89% 16%

Côte d’Ivoire 24m 21 3,304 108% 15%

Rwanda 11m 19 1,783 75% 35%

Zambia 16m 17 4,165 67% 22%

22%2% 9%

21% 22%

57%

34%

35%

43%34%

44%

20%

44%

63%47% 45%

34%23%

Global EU Latin America Asia Pacific Middle east Sub-Saharan Africa

Not covered / Not connected Covered by 3G networks but not connected Connected to the mobile internet

Source: GSMA Intelligence 2016, Q4 2015, IMF, WCIS and IndexMundi.

Mobile data connectivity:

9IHS - Wendel Investor Day | December 1, 2016

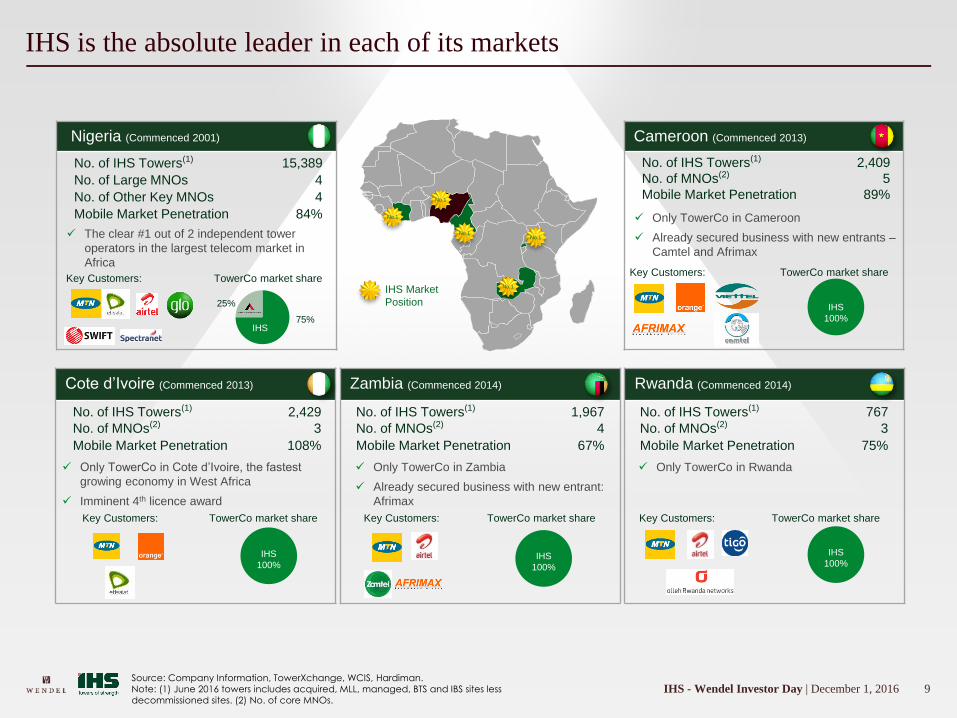

IHS is the absolute leader in each of its markets

Source: Company Information, TowerXchange, WCIS, Hardiman.Note: (1) June 2016 towers includes acquired, MLL, managed, BTS and IBS sites less decommissioned sites. (2) No. of core MNOs.

Cameroon (Commenced 2013)

IHS

100%

Nigeria (Commenced 2001)

Zambia (Commenced 2014)

No.1

No.1

No.1

No.1

No.1

IHS Market

Position

Cote d’Ivoire (Commenced 2013) Rwanda (Commenced 2014)

Only TowerCo in Cameroon

Already secured business with new entrants –

Camtel and Afrimax

The clear #1 out of 2 independent tower

operators in the largest telecom market in

Africa

No. of IHS Towers(1) 15,389

No. of Large MNOs 4

No. of Other Key MNOs 4

Mobile Market Penetration 84%

No. of IHS Towers(1) 2,429

No. of MNOs(2) 3

Mobile Market Penetration 108%

No. of IHS Towers(1) 1,967

No. of MNOs(2) 4

Mobile Market Penetration 67%

No. of IHS Towers(1) 767

No. of MNOs(2) 3

Mobile Market Penetration 75%

No. of IHS Towers(1) 2,409

No. of MNOs(2) 5

Mobile Market Penetration 89%

Only TowerCo in Rwanda Only TowerCo in Zambia

Already secured business with new entrant:

Afrimax

Only TowerCo in Cote d’Ivoire, the fastest

growing economy in West Africa

Imminent 4th licence award

Key Customers:Key Customers:

Key Customers: Key Customers: Key Customers:

TowerCo market share

IHS

TowerCo market share

75%

25%

TowerCo market share

IHS

100%

TowerCo market share

IHS

100%

TowerCo market share

IHS

100%

10IHS - Wendel Investor Day | December 1, 2016

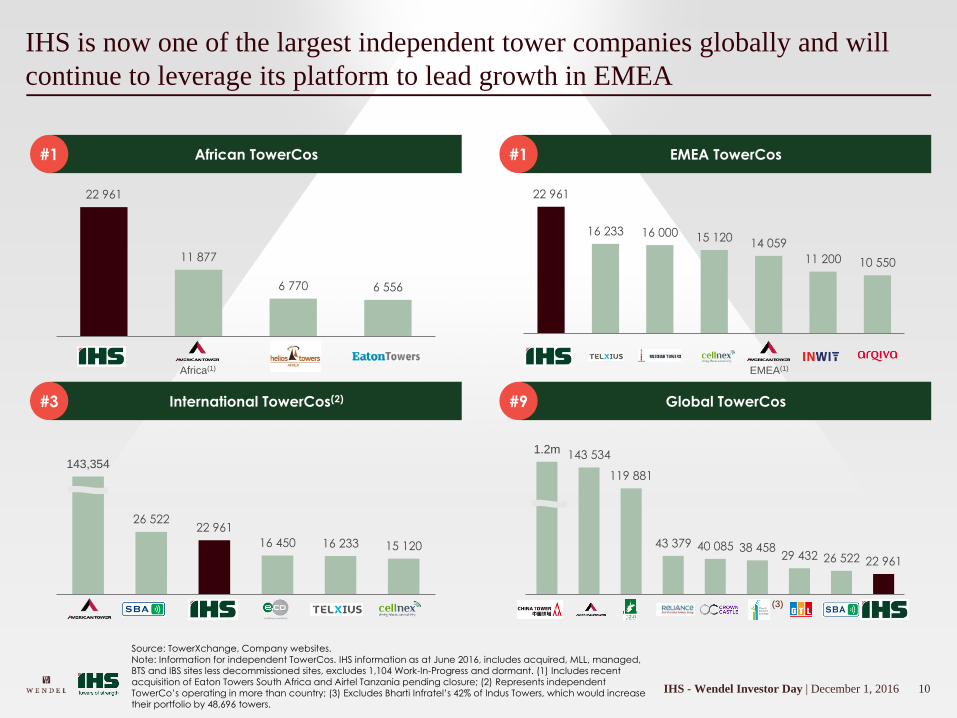

IHS is now one of the largest independent tower companies globally and will

continue to leverage its platform to lead growth in EMEA

Source: TowerXchange, Company websites.Note: Information for independent TowerCos. IHS information as at June 2016, includes acquired, MLL, managed, BTS and IBS sites less decommissioned sites, excludes 1,104 Work-In-Progress and dormant. (1) Includes recent acquisition of Eaton Towers South Africa and Airtel Tanzania pending closure; (2) Represents independent TowerCo’s operating in more than country; (3) Excludes Bharti Infratel’s 42% of Indus Towers, which would increase their portfolio by 48,696 towers.

African TowerCos#1 EMEA TowerCos#1

International TowerCos(2)#3 Global TowerCos#9

22 961

11 877

6 770 6 556

Africa(1)

143,354

26 52222 961

16 450 16 233 15 120

1.2m 143 534

119 881

43 379 40 085 38 45829 432 26 522 22 961

(3)

22 961

16 233 16 000 15 12014 059

11 200 10 550

EMEA(1)

11IHS - Wendel Investor Day | December 1, 2016

Financials & Corporate Activity

12IHS - Wendel Investor Day | December 1, 2016

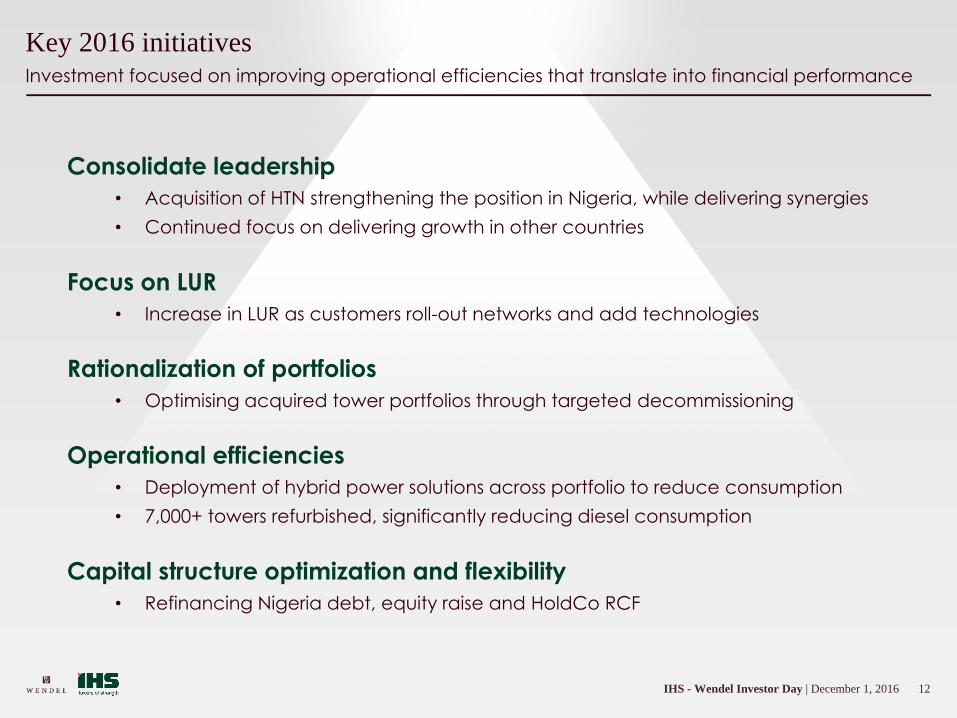

Investment focused on improving operational efficiencies that translate into financial performance

Key 2016 initiatives

Consolidate leadership

• Acquisition of HTN strengthening the position in Nigeria, while delivering synergies

• Continued focus on delivering growth in other countries

Focus on LUR

• Increase in LUR as customers roll-out networks and add technologies

Operational efficiencies

• Deployment of hybrid power solutions across portfolio to reduce consumption

• 7,000+ towers refurbished, significantly reducing diesel consumption

Capital structure optimization and flexibility

• Refinancing Nigeria debt, equity raise and HoldCo RCF

Rationalization of portfolios

• Optimising acquired tower portfolios through targeted decommissioning

13IHS - Wendel Investor Day | December 1, 2016

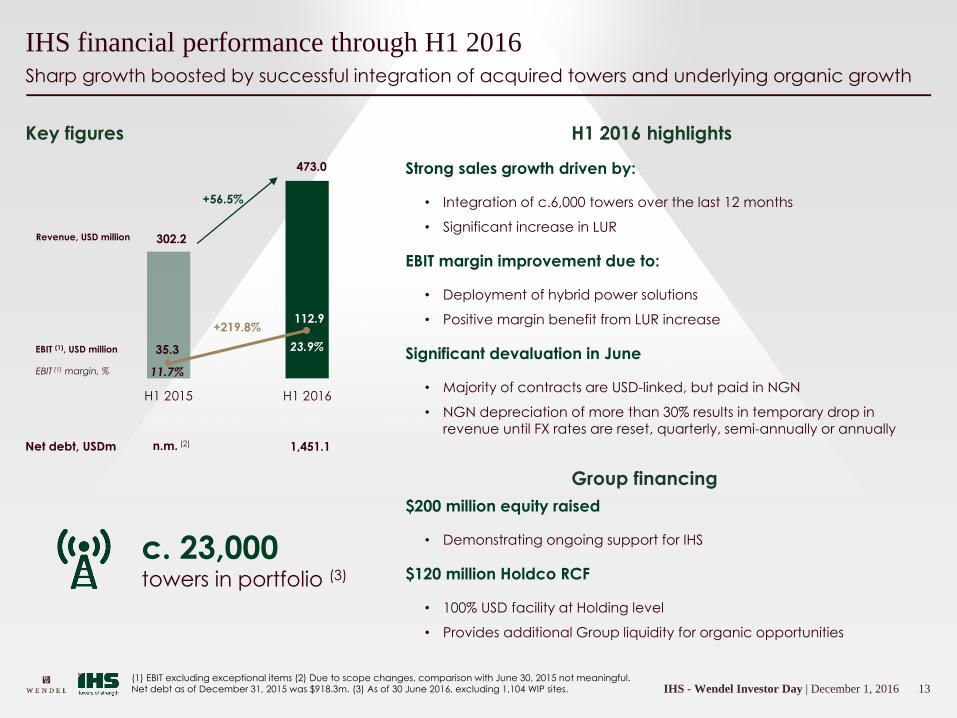

H1 2015 H1 2016

Sharp growth boosted by successful integration of acquired towers and underlying organic growth

IHS financial performance through H1 2016

Key figures

473.0

Revenue, USD million

EBIT (1), USD million

Strong sales growth driven by:

• Integration of c.6,000 towers over the last 12 months

• Significant increase in LUR

EBIT margin improvement due to:

• Deployment of hybrid power solutions

• Positive margin benefit from LUR increase

Significant devaluation in June

• Majority of contracts are USD-linked, but paid in NGN

• NGN depreciation of more than 30% results in temporary drop in

revenue until FX rates are reset, quarterly, semi-annually or annually

302.2

35.3

112.9

11.7%

Net debt, USDm 1,451.1

+56.5%

H1 2016 highlights

EBIT (1) margin, %

c. 23,000towers in portfolio (3)

23.9%

n.m. (2)

+219.8%

(1) EBIT excluding exceptional items (2) Due to scope changes, comparison with June 30, 2015 not meaningful. Net debt as of December 31, 2015 was $918.3m. (3) As of 30 June 2016, excluding 1,104 WIP sites.

Group financing

$200 million equity raised

• Demonstrating ongoing support for IHS

$120 million Holdco RCF

• 100% USD facility at Holding level

• Provides additional Group liquidity for organic opportunities

14IHS - Wendel Investor Day | December 1, 2016

Outlook & Strategy

15IHS - Wendel Investor Day | December 1, 2016

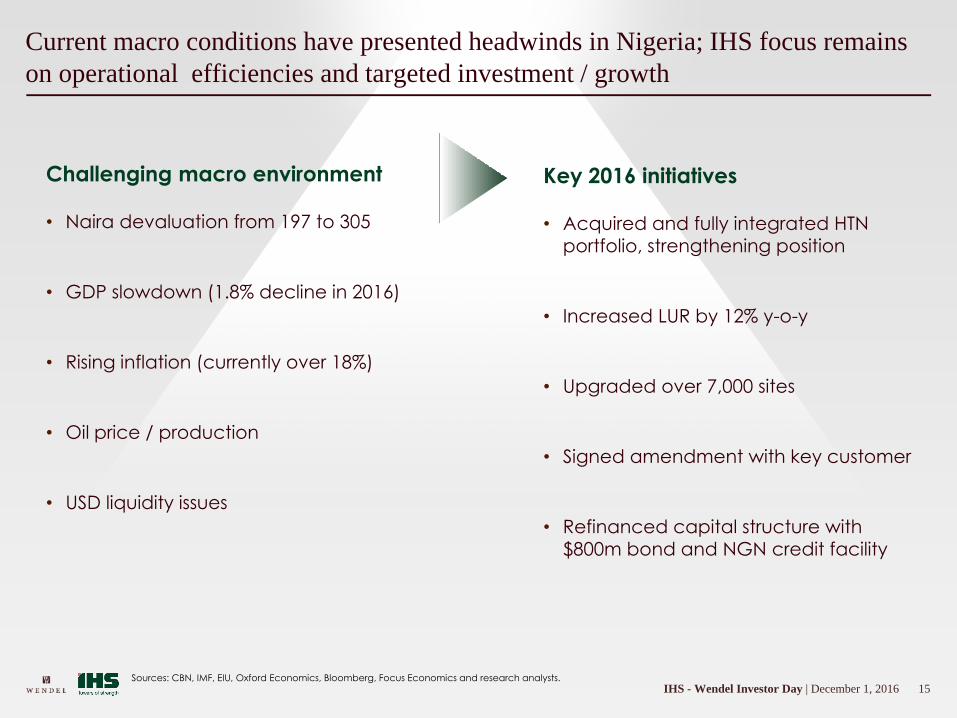

Current macro conditions have presented headwinds in Nigeria; IHS focus remains

on operational efficiencies and targeted investment / growth

Sources: CBN, IMF, EIU, Oxford Economics, Bloomberg, Focus Economics and research analysts.

Challenging macro environment

• Naira devaluation from 197 to 305

• GDP slowdown (1.8% decline in 2016)

• Rising inflation (currently over 18%)

• Oil price / production

• USD liquidity issues

Key 2016 initiatives

• Acquired and fully integrated HTN

portfolio, strengthening position

• Increased LUR by 12% y-o-y

• Upgraded over 7,000 sites

• Signed amendment with key customer

• Refinanced capital structure with

$800m bond and NGN credit facility

16IHS - Wendel Investor Day | December 1, 2016

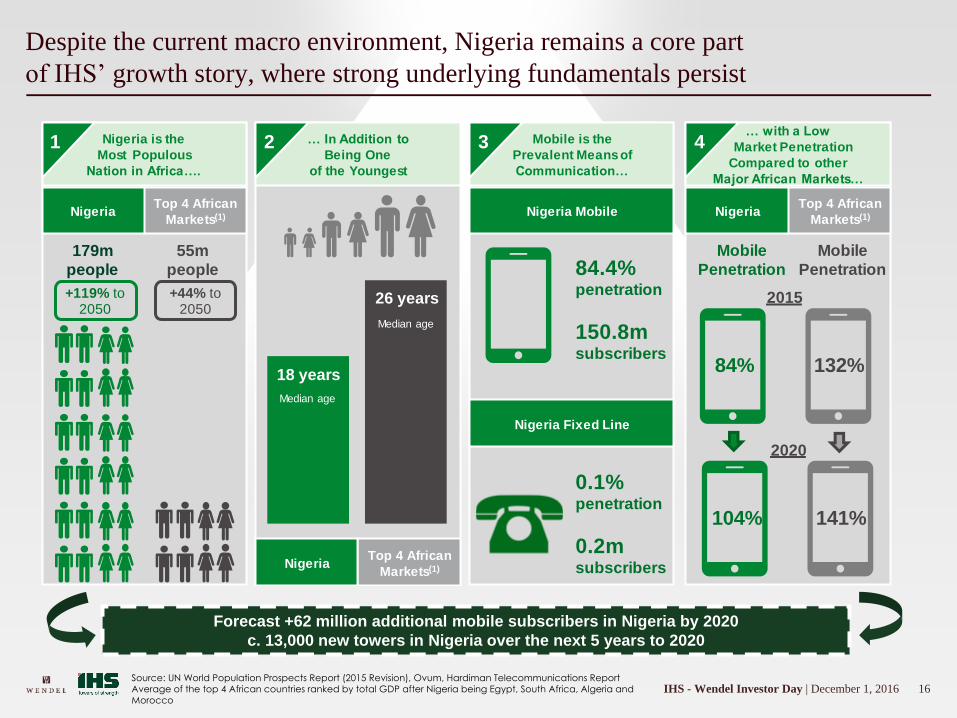

Despite the current macro environment, Nigeria remains a core part

of IHS’ growth story, where strong underlying fundamentals persist

Nigeria is the

Most Populous

Nation in Africa….

… In Addition to

Being One

of the Youngest

… with a Low

Market Penetration

Compared to other

Major African Markets…

Mobile is the

Prevalent Means of

Communication…

+119% to 2050

84.4% penetration

150.8m subscribers

1 2 3 4

Top 4 African

Markets(1)Nigeria

179m

people

+44% to 2050

55m

people

Top 4 African

Markets(1)Nigeria

18 years

26 years

Nigeria Mobile

Nigeria Fixed Line

0.1% penetration

0.2m subscribers

Top 4 African

Markets(1)Nigeria

84%

Mobile

Penetration

132%

Mobile

Penetration

2015

104% 141%

2020

Median age

Median age

Forecast +62 million additional mobile subscribers in Nigeria by 2020Forecast +62 million additional mobile subscribers in Nigeria by 2020

c. 13,000 new towers in Nigeria over the next 5 years to 2020

Source: UN World Population Prospects Report (2015 Revision), Ovum, Hardiman Telecommunications ReportAverage of the top 4 African countries ranked by total GDP after Nigeria being Egypt, South Africa, Algeria and Morocco

17IHS - Wendel Investor Day | December 1, 2016

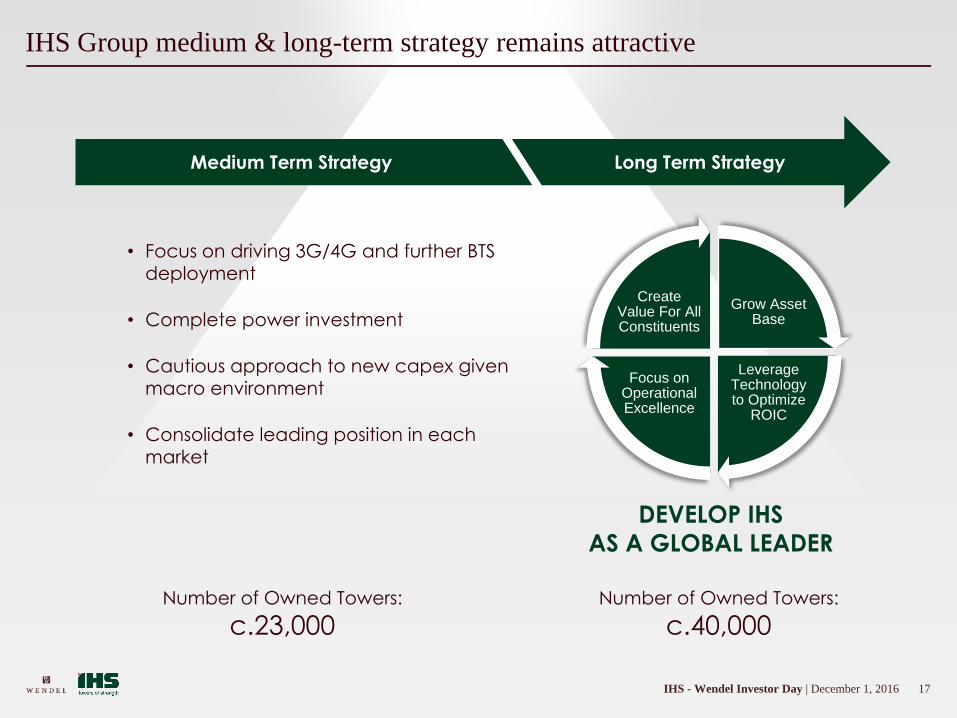

IHS Group medium & long-term strategy remains attractive

• Focus on driving 3G/4G and further BTS

deployment

• Complete power investment

• Cautious approach to new capex given

macro environment

• Consolidate leading position in each

market

Medium Term Strategy Long Term Strategy

Grow Asset Base

Leverage Technology to Optimize

ROIC

Focus on Operational Excellence

Create Value For All Constituents

DEVELOP IHS

AS A GLOBAL LEADER

Number of Owned Towers:

c.23,000Number of Owned Towers:

c.40,000

18IHS - Wendel Investor Day | December 1, 2016

Thank You

19IHS - Wendel Investor Day | December 1, 2016

Investor DayDecember 1, 2016

20IHS - Wendel Investor Day | December 1, 2016

Break

1Tsebo - Wendel Investor Day | December 1, 2016

Tsebo

Investing in the leading pan-African facilities services provider

~€150m* equity to be invested

~60%* equity stake

Transaction to be closed in the coming weeks

Unrivalled footprint in Africa,with presence in 23 countries

Attractive growth prospects organically and through acquisition

Resilient business model

Strong cash generation

* Final amounts to be announced upon closing of the transaction

2Tsebo - Wendel Investor Day | December 1, 2016

Clive Smith – CEO of Tsebo

• Clive has had leadership experience across the group Tsebo over the last 20 years, including time as CEO of Drake and Scull and as CEO of Fedics.

• He has a strong financial background, many years of experience in leading large employee groups, operating companies and driving organic and acquisitive growth strategies.Since taking up his position as Tsebo’s CEO in 2004, Tsebo has enhanced its transformation credentials and delivered consistent customer and shareholder value.

• Clive is a dynamic leader who believes in empowerment as a business strategy and not merely a compliance requirement. It is a vision that has seen Tsebo grow to unprecedented size over the last 10 years.

3V. 24.11. 2016 Family Day | 2 décembre 2016

TseboClive Smith, CEO

4Tsebo - Wendel Investor Day | December 1, 2016

Focus areas

An overview of Tsebo and its positioning

Tsebo's strategy to exploit potential growth levers and selected opportunities

Our view of the facility services market in Africa and its potential

5Tsebo - Wendel Investor Day | December 1, 2016

Tsebo at a glance

ZAR 6.33bn of sales(1)

ZAR 507m of Ebitda(1)

34,000+ staff

7,000+ client sites across a variety of industries

The leading pan-African facilities services provider(catering, cleaning, security, facilities management…)

Founded in 1971, 'homegrown' African company

(1) Period ended March 31, 2016

6Tsebo - Wendel Investor Day | December 1, 2016

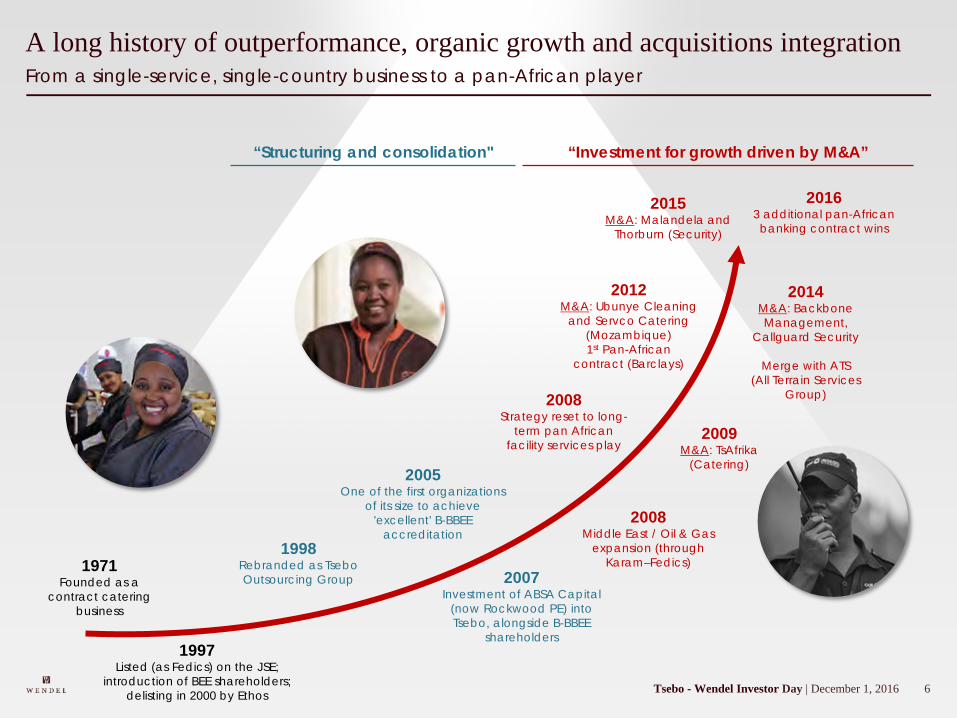

From a single-service, single-country business to a pan-African player A long history of outperformance, organic growth and acquisitions integration

1971 Founded as a

contract catering business

1997Listed (as Fedics) on the JSE;

introduction of BEE shareholders; delisting in 2000 by Ethos

1998Rebranded as TseboOutsourcing Group

2005 One of the first organizations

of its size to achieve 'excellent' B-BBEE

accreditation

2007Investment of ABSA Capital

(now Rockwood PE) into Tsebo, alongside B-BBEE

shareholders

2009M&A: TsAfrika

(Catering)

2012M&A: Ubunye Cleaning

and Servco Catering (Mozambique)1st Pan-African

contract (Barclays)

2015M&A: Malandela and

Thorburn (Security)

2014M&A: Backbone Management,

Callguard Security

Merge with ATS(All Terrain Services

Group)

“Investment for growth driven by M&A”“Structuring and consolidation"

2008Strategy reset to long-

term pan African facility services play

2016 3 additional pan-African banking contract wins

2008Middle East / Oil & Gas

expansion (through Karam–Fedics)

7Tsebo - Wendel Investor Day | December 1, 2016

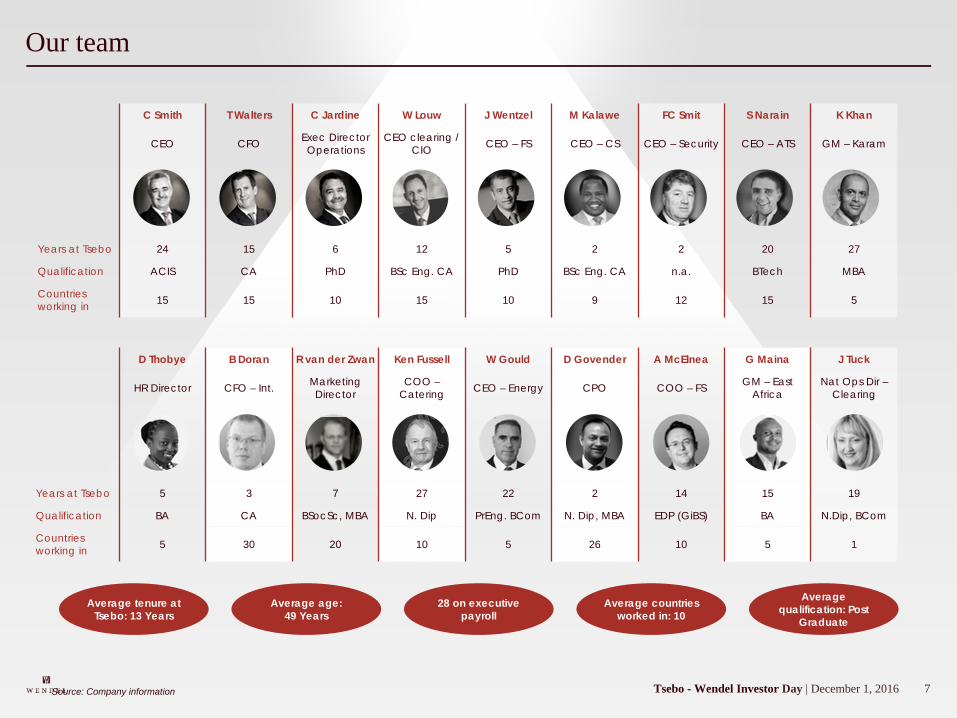

Our team

C Smith T Walters C Jardine W Louw J Wentzel M Kalawe FC Smit S Narain K Khan

CEO CFO Exec Director Operations

CEO clearing / CIO CEO – FS CEO – CS CEO – Security CEO – ATS GM – Karam

Years at Tsebo 24 15 6 12 5 2 2 20 27

Qualification ACIS CA PhD BSc Eng. CA PhD BSc Eng. CA n.a. BTech MBA

Countriesworking in 15 15 10 15 10 9 12 15 5

D Thobye B Doran R van der Zwan Ken Fussell W Gould D Govender A McElnea G Maina J Tuck

HR Director CFO – Int. MarketingDirector

COO –Catering CEO – Energy CPO COO – FS GM – East

AfricaNat Ops Dir –

Clearing

Years at Tsebo 5 3 7 27 22 2 14 15 19

Qualification BA CA BSocSc, MBA N. Dip PrEng. BCom N. Dip, MBA EDP (GiBS) BA N.Dip, BCom

Countriesworking in 5 30 20 10 5 26 10 5 1

Average tenure at Tsebo: 13 Years

Average age: 49 Years

28 on executive payroll

Average countries worked in: 10

Average qualification: Post

Graduate

Source: Company information

8Tsebo - Wendel Investor Day | December 1, 2016

A clear brand strategy, to support current positioning and enter markets

A powerful Mother BrandComplemented by a limited number of sub-brands that serve

specific markets that the Mother Brand cannot serve as effectively

Five agreed Power Brands, smaller brands to be retired

Catering Security Cleaning FM Remote sites

9Tsebo - Wendel Investor Day | December 1, 2016

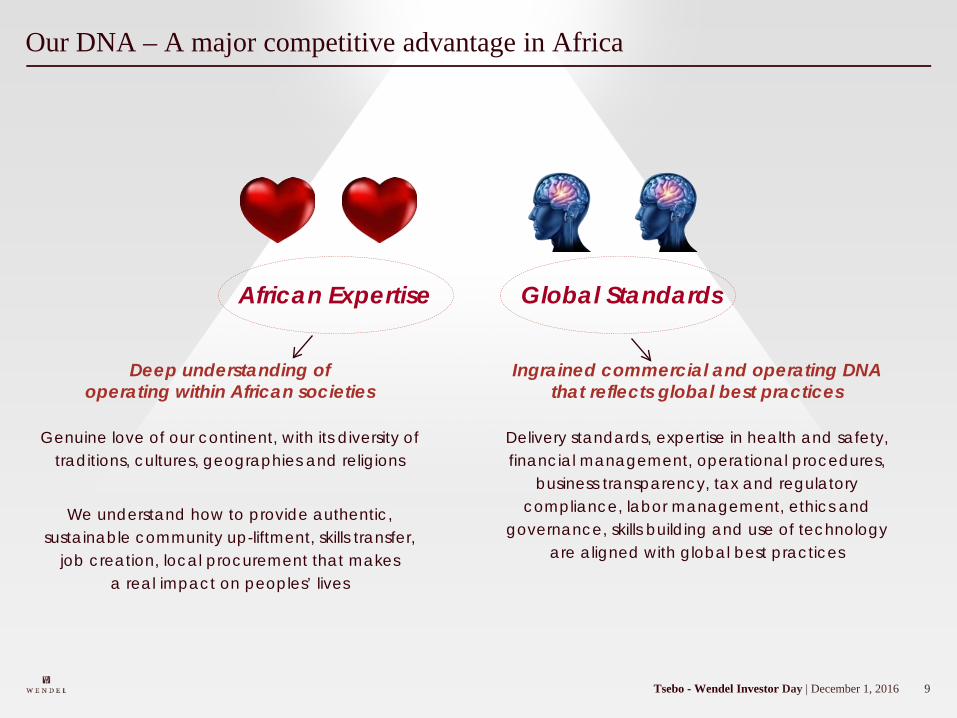

Our DNA – A major competitive advantage in Africa

Ingrained commercial and operating DNA that reflects global best practices

African Expertise Global Standards

Deep understanding of operating within African societies

Genuine love of our continent, with its diversity of traditions, cultures, geographies and religions

We understand how to provide authentic, sustainable community up-liftment, skills transfer,

job creation, local procurement that makes a real impact on peoples’ lives

Delivery standards, expertise in health and safety, financial management, operational procedures,

business transparency, tax and regulatory compliance, labor management, ethics and

governance, skills building and use of technology are aligned with global best practices

10Tsebo - Wendel Investor Day | December 1, 2016

The facility services industry covers a wide range of activitiesOur business

Activities which Tsebo can self-perform

COMMERCIAL FMFOODSERVICE RELATED OFFICE RELATED

TECHNICAL FM INFRASTRUCTURE MANAGEMENT

Procurement

Cost Planning

Insurance

Public Charges

Facility Accounting

Catering / Canteen

Vending / Beverage

Events/ Functions

Remote Mine Camps

Oil Rig Life Support

Office Cleaning

Hygiene

Access/ Security

Reception

Office Churns

Mailroom

Gardening

Archiving

Pest Control

HVAC

Health & Safety

Building Maintenance

Waste Management

Energy/ Utilities

Mechanical Services

Audio-visual

Fire Suppression

Lifts And Escalators

Self-

Perf

orm

Su

b-Co

ntra

ct

Areas of self-performance focus on site-based services, leveraging core competencies

11Tsebo - Wendel Investor Day | December 1, 2016

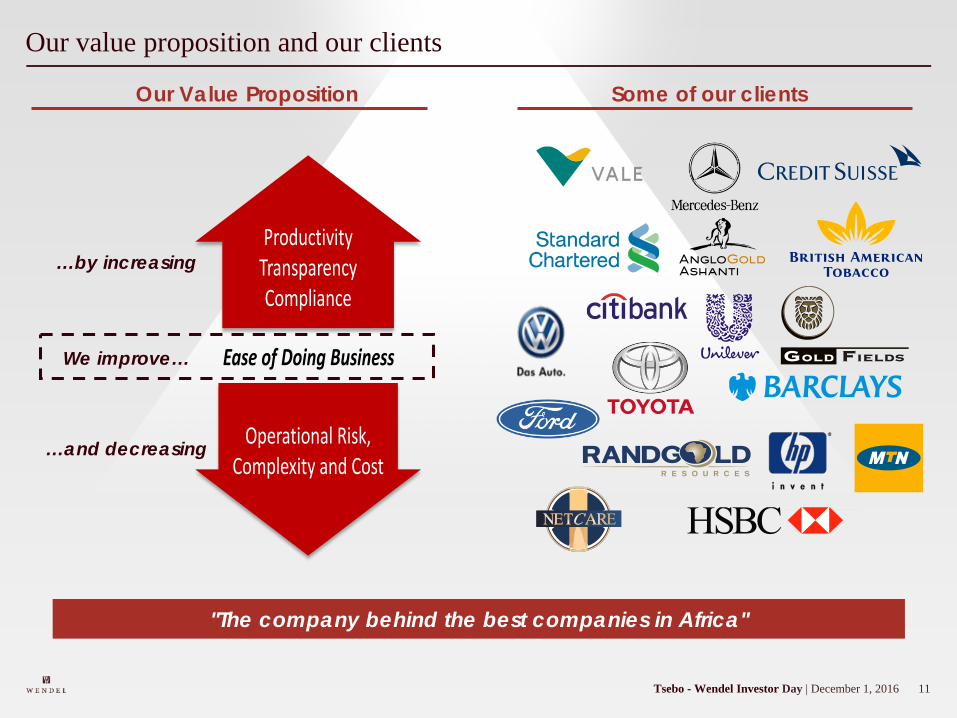

Our value proposition and our clients

Operational Risk, Complexity and Cost

ProductivityTransparencyCompliance

Ease of Doing Business

"The company behind the best companies in Africa"

Our Value Proposition

…by increasing

…and decreasing

We improve…

Some of our clients

12Tsebo - Wendel Investor Day | December 1, 2016

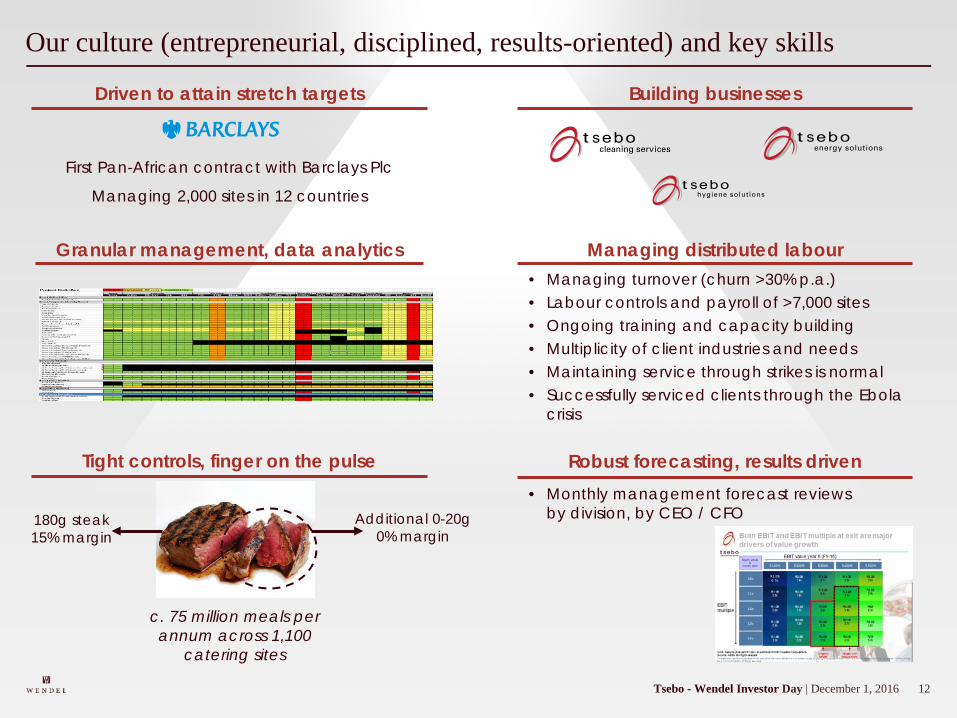

• Monthly management forecast reviews by division, by CEO / CFO

Our culture (entrepreneurial, disciplined, results-oriented) and key skills

First Pan-African contract with Barclays Plc

Managing 2,000 sites in 12 countries

Driven to attain stretch targets Building businesses

Granular management, data analytics

Tight controls, finger on the pulse

180g steak15% margin

Additional 0-20g 0% margin

Robust forecasting, results driven

Managing distributed labour• Managing turnover (churn >30% p.a.)• Labour controls and payroll of >7,000 sites• Ongoing training and capacity building• Multiplicity of client industries and needs• Maintaining service through strikes is normal• Successfully serviced clients through the Ebola

crisis

c. 75 million meals per annum across 1,100

catering sites

13Tsebo - Wendel Investor Day | December 1, 2016

Corporate Governance and risk management are an integral part of our DNA

Comprehensive risk matrix developed and managed

Corporate governance and risk management approacho Zero tolerance policyo Annual risk review

ABACo UK Bribery Acto US Foreign Corrupt Practices Acto RSA Prevention and Combating of Corrupto Practices Act – Venus modelled on UK Acto Status of ABAC strategy

Ethicso Employee accountability and tip-off hotlineo Code of ethics and good business practice

Audit Regulatory environment

14Tsebo - Wendel Investor Day | December 1, 2016

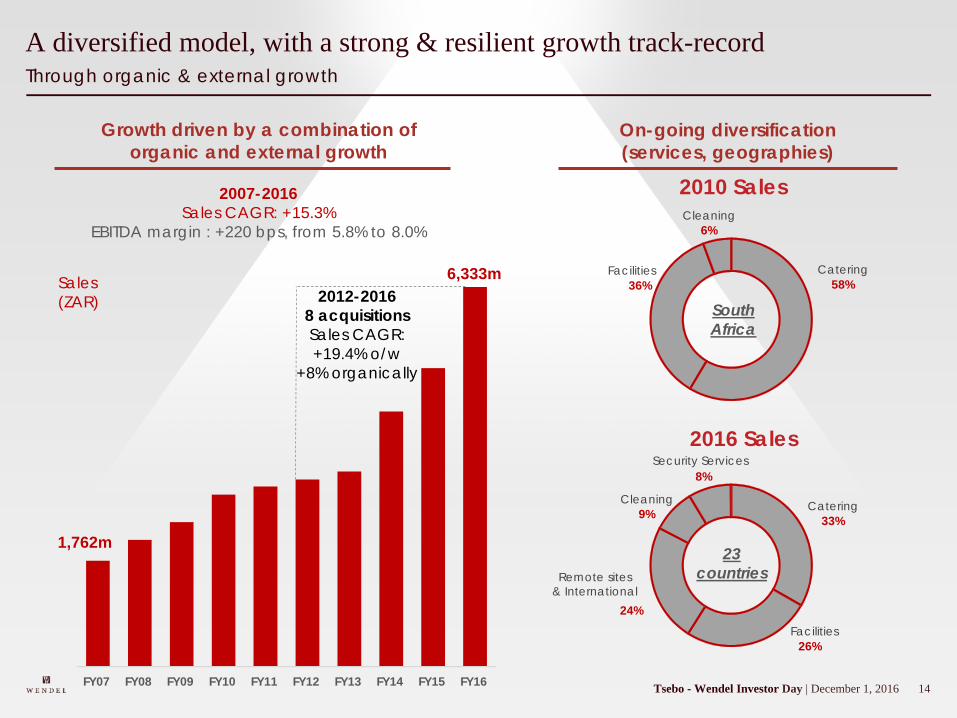

Through organic & external growthA diversified model, with a strong & resilient growth track-record

2012-20168 acquisitions Sales CAGR: +19.4% o/w

+8% organically

Growth driven by a combination of organic and external growth

2016 Sales

2010 Sales

1,762m

Sales (ZAR)

6,333m

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

2007-2016Sales CAGR: +15.3%

EBITDA margin : +220 bps, from 5.8% to 8.0%

SouthAfrica

23countries

Catering33%

Facilities26%

Remote sites & International

24%

Cleaning9%

Security Services8%

Catering58%

Facilities36%

Cleaning6%

On-going diversification(services, geographies)

15Tsebo - Wendel Investor Day | December 1, 2016

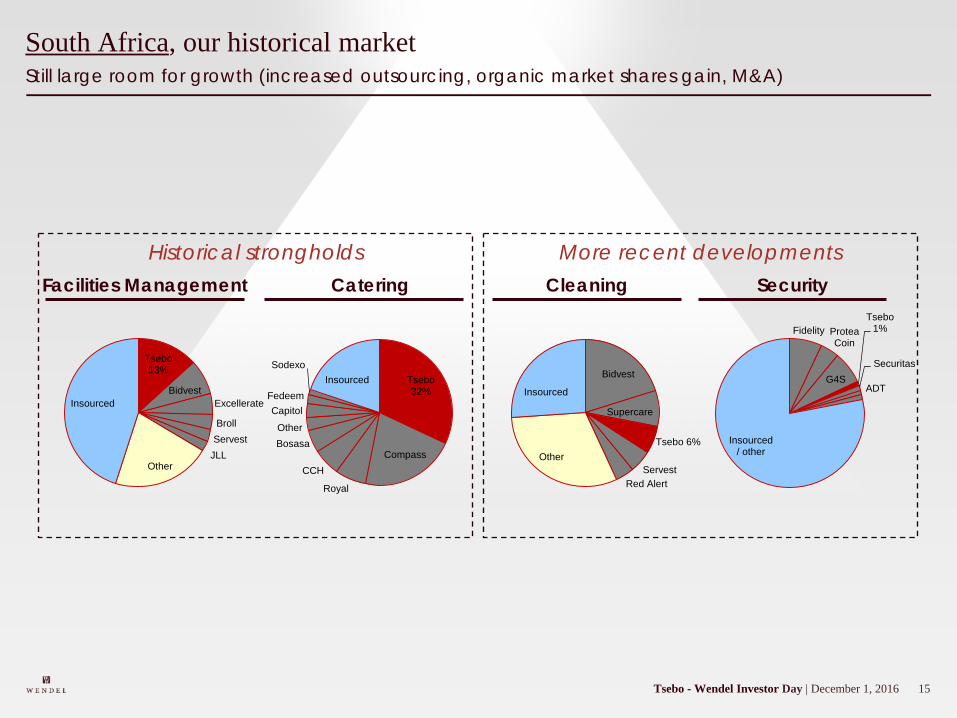

Still large room for growth (increased outsourcing, organic market shares gain, M&A)South Africa, our historical market

Catering CleaningFacilities Management Security

Tsebo13%

Bidvest

Excellerate

Broll

Servest

JLLOther

Insourced

Fidelity Protea Coin

G4S

Tsebo1%

Securitas

ADT

Insourced/ other

Bidvest

Supercare

Tsebo 6%

Servest

Red Alert

Other

Insourced

Tsebo32%

Compass

Royal

CCH

Bosasa

Other

Capitol

Fedeem

Sodexo

Insourced

Historical strongholds More recent developments

16Tsebo - Wendel Investor Day | December 1, 2016

Rest of Africa: our investment thesis

(1) Period ended March 31, 2016

Strong macro fundamentals, urbanization and increased consumer spending attracting our global customers into Africa and developing local markets

In a currently highly underpenetrated market (>2/3 insourced), Tsebo is already a leader and ideally positioned to capture the opportunity

These global customers are seeking global solutions; all are seeking less complexity, enhanced compliance and productivity

17Tsebo - Wendel Investor Day | December 1, 2016

Tsebo's African target market growth is driven by strong fundamentals

1. Excluding South AfricaSource: IMF World Economic Outlook, October 2016, Team Estimates

Economic and population growth Urbanization

• Sub-Saharan Africa1

expected (IMF) to grow 3.4% in 2017, 4.6% in 2021 (2nd fastest after Emerging and Developing Asia)

• Population to exceed China's in 20 years

• 20 SSA countries expected to grow over 5% in 2017

• 7 countries expected over 6%

• By 2025, >80 African cities will have >1m inhabitants, driving c. 60% of GDP

• They will service over 300m middle class consumers, who will require $180bn p/a of infrastructure spending to support growth

• Political stability• Governance• Infrastructure• …

Attracting our global customers into Africa, developing local markets

Improving Ease of Doing Business

18Tsebo - Wendel Investor Day | December 1, 2016

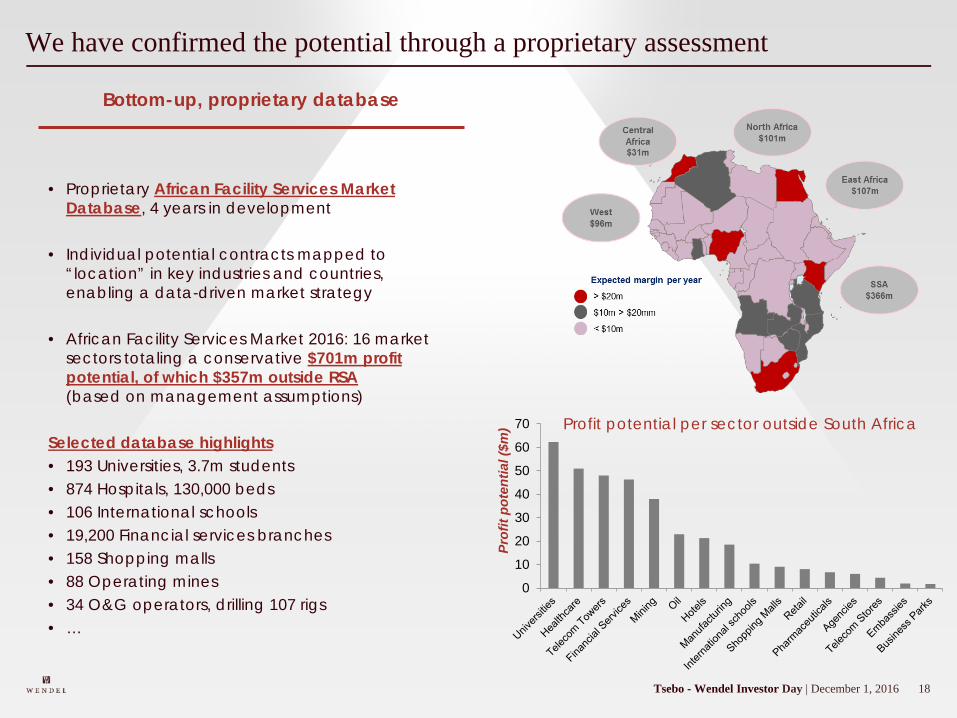

We have confirmed the potential through a proprietary assessment

Bottom-up, proprietary database

• Proprietary African Facility Services Market Database, 4 years in development

• Individual potential contracts mapped to “location” in key industries and countries, enabling a data-driven market strategy

• African Facility Services Market 2016: 16 market sectors totaling a conservative $701m profit potential, of which $357m outside RSA (based on management assumptions)

Selected database highlights • 193 Universities, 3.7m students • 874 Hospitals, 130,000 beds • 106 International schools• 19,200 Financial services branches • 158 Shopping malls • 88 Operating mines • 34 O&G operators, drilling 107 rigs • …

Profit potential per sector outside South Africa

0

10

20

30

40

50

60

70

Prof

it po

tent

ial (

$m)

19Tsebo - Wendel Investor Day | December 1, 2016

In a currently highly underpenetrated market (Rest of Africa)…

Tsebo's estimated market(across Africa)

Remote sites(across Tsebo countries excl. RSA)

InsourcedTsebo3%

Other

Tsebo15.9%

CIS

SodexoOther

Insourced

20Tsebo - Wendel Investor Day | December 1, 2016

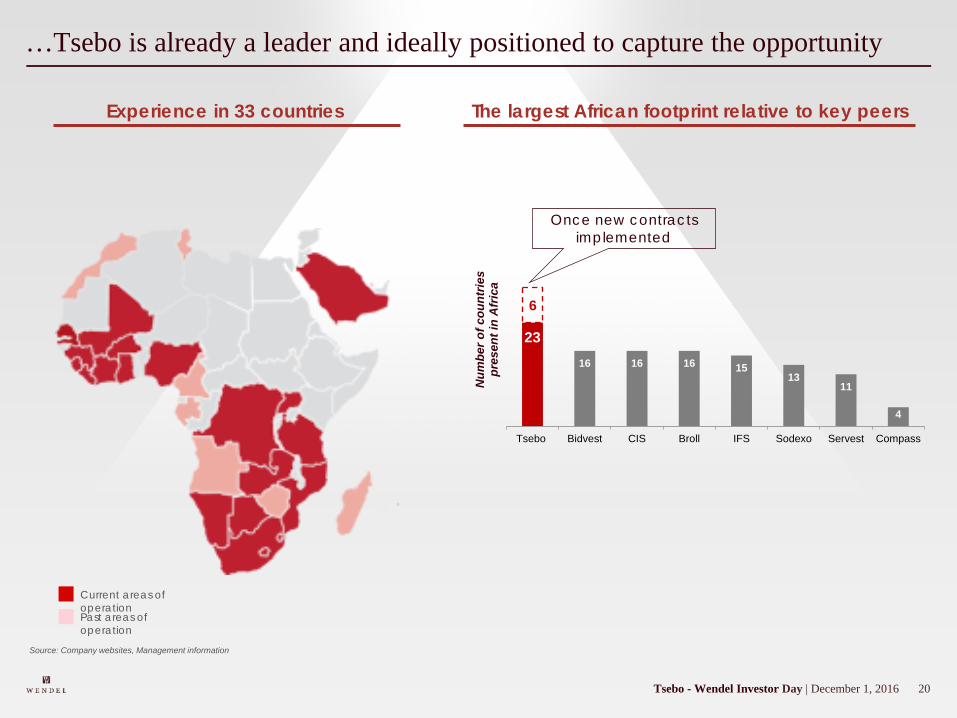

…Tsebo is already a leader and ideally positioned to capture the opportunity

Current areas of operationPast areas of operation

Source: Company websites, Management information

23

16 16 16 1513

11

4

Tsebo Bidvest CIS Broll IFS Sodexo Servest Compass

Num

ber o

f cou

ntrie

s pr

esen

t in

Afr

ica

6

Once new contracts implemented

Experience in 33 countries The largest African footprint relative to key peers

21Tsebo - Wendel Investor Day | December 1, 2016

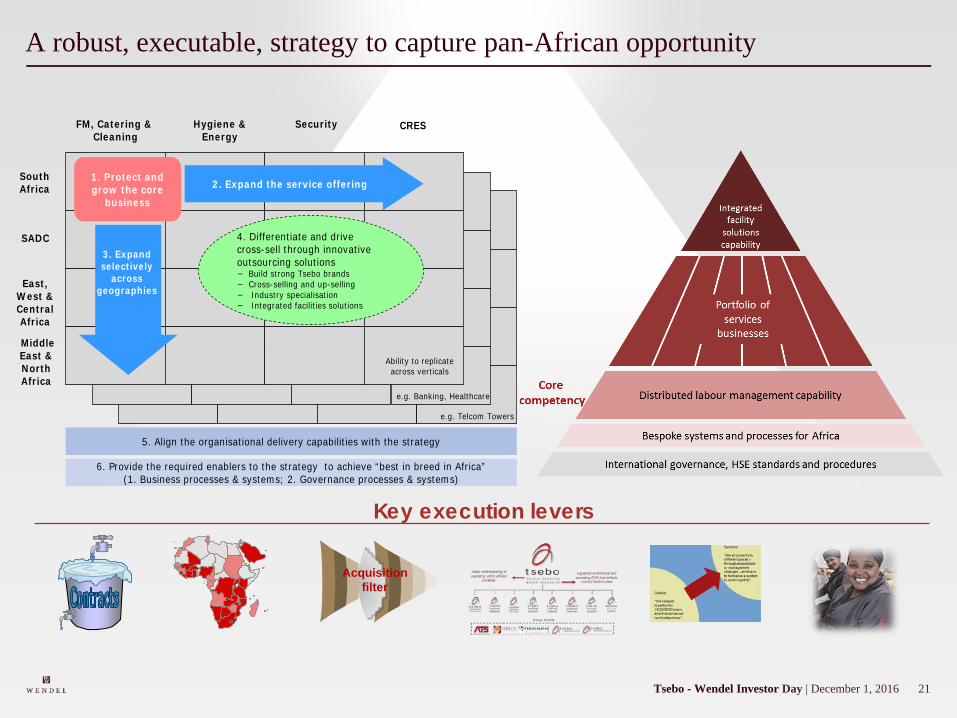

A robust, executable, strategy to capture pan-African opportunity

Key execution levers

Acquisition

filter

FM, Catering & Cleaning

South Africa

1. Protect and grow the core

business2. Expand the service offering

3. Expand selectively

across geographies

5. Align the organisational delivery capabilities with the strategy

6. Provide the required enablers to the strategy to achieve “best in breed in Africa”(1. Business processes & systems; 2. Governance processes & systems)

4. Differentiate and drive cross-sell through innovative outsourcing solutions− Build strong Tsebo brands − Cross-selling and up-selling − Industry specialisation− Integrated facilities solutions

Ability to replicate across verticals

e.g. Banking, Healthcare

e.g. Telcom Towers

Hygiene & Energy

Security CRES

SADC

East, West & Central Africa

Middle East & North Africa

22Tsebo - Wendel Investor Day | December 1, 2016

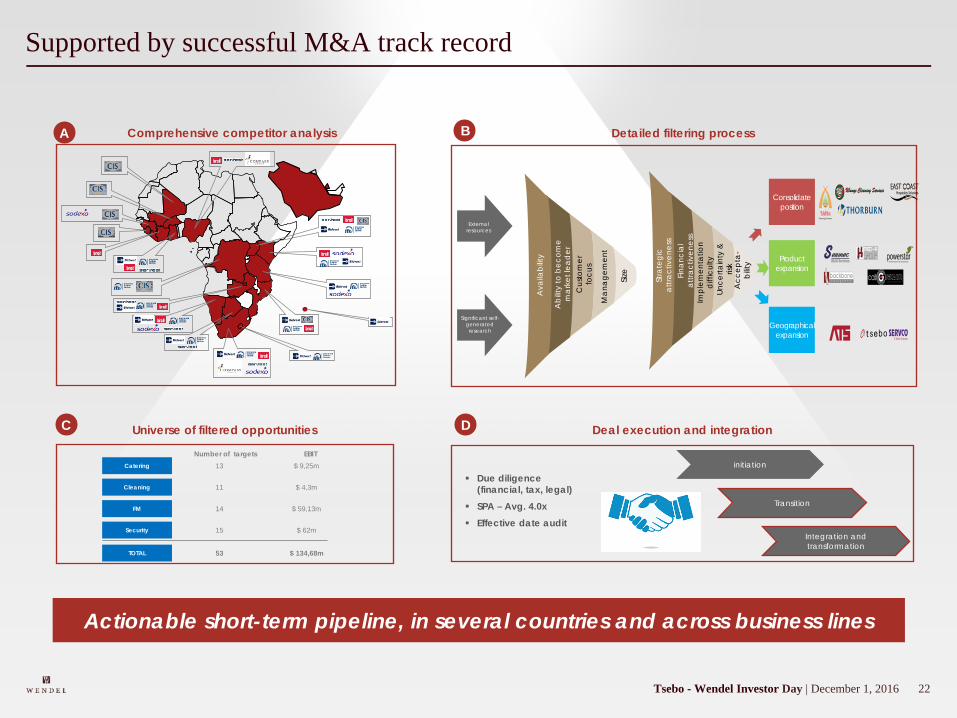

Supported by successful M&A track record

Universe of filtered opportunities

Comprehensive competitor analysis Detailed filtering process

Integration and transformation

Transition

Due diligence (financial, tax, legal)

SPA – Avg. 4.0x Effective date audit

Deal execution and integration

A B

C D

initiationCatering 13 $ 9,25m

Cleaning 11 $ 4,3m

FM 14 $ 59,13m

Security 15 $ 62m

Number of targets EBIT

TOTAL 53 $ 134,68m

External resources

Significant self-generated research

Stra

tegi

c at

tract

iven

ess

Finan

cial

at

tract

iven

ess

Impl

emen

tatio

n d

iffic

ulty

Unce

rtain

ty &

ris

kA

ccep

ta-

bilit

y

Cus

tom

er

focu

s

Abi

lity

to b

ecom

e m

arke

t lea

der

Size

Ava

ilabi

lity

Man

agem

ent

Consolidate position

Product expansion

Geographical expansion

Actionable short-term pipeline, in several countries and across business lines

23Tsebo - Wendel Investor Day | December 1, 2016

Deep-rooted Corporate Citizenship, Ethics and Localization commitment

Investment in sponsoring 150 managers on post-graduate

MBA / MAP studies

Massive community-based supplier

development programs in rural areas

Industry leader in development of disabled staff (2.3% of workforce)

Vibrant company Foundation that supports

communities

Leader in corporate SA on BEE

First large corporate to receive Level 1 on new codes Largest skills developer in the

industry (35,000 staff trained over last 3 years)

Embedded Corporate Governance

24Tsebo - Wendel Investor Day | December 1, 2016

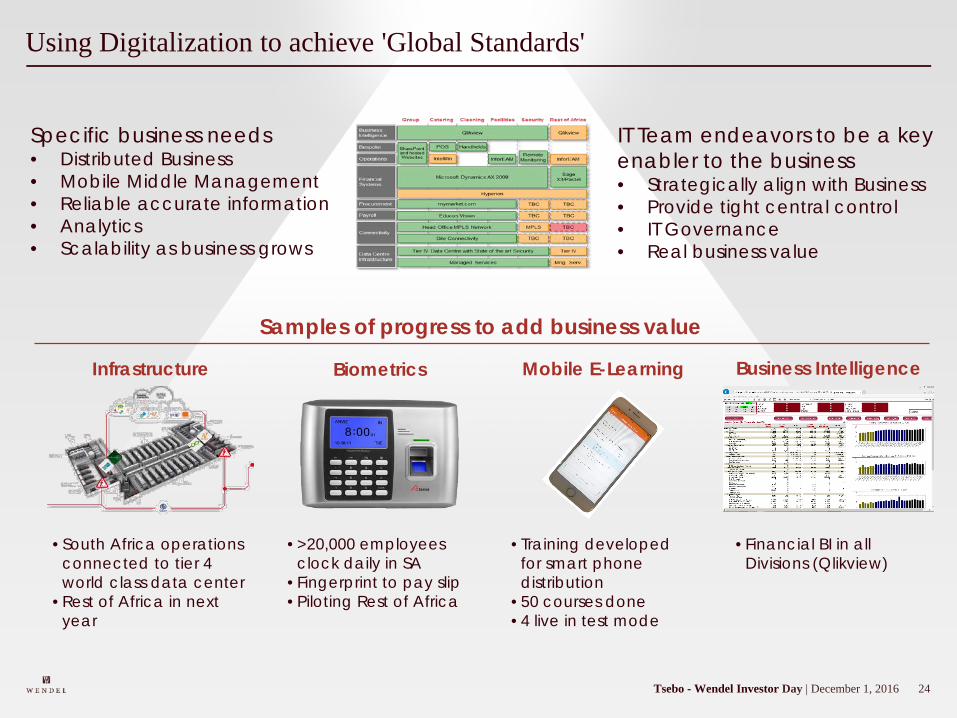

Using Digitalization to achieve 'Global Standards'

Specific business needs• Distributed Business• Mobile Middle Management• Reliable accurate information• Analytics • Scalability as business grows

IT Team endeavors to be a key enabler to the business• Strategically align with Business• Provide tight central control• IT Governance• Real business value

Samples of progress to add business value

Biometrics

• South Africa operations connected to tier 4 world class data center

• Rest of Africa in next year

Mobile E-Learning Business IntelligenceInfrastructure

• >20,000 employees clock daily in SA

• Fingerprint to pay slip• Piloting Rest of Africa

• Training developed for smart phone distribution

• 50 courses done• 4 live in test mode

Picture

• Financial BI in all Divisions (Qlikview)

25Tsebo - Wendel Investor Day | December 1, 2016

Key takeaways

African facility services market, a large, fragmented and growing market, thus we have huge potential to sell, consolidate and replicate

Tsebo is ideally positioned to capture an important share of this growth through organic and acquisitive growth

Tsebo has crafted pan-African leadership position, and built a robust platform with the largest footprint in the industry

Investment in brands, culture, systems and the consolidation engine are supported by strong cash generation and a stable, passionate team

The team is excited to continue the journey with international shareholders of reference

The key to success is the careful prioritization of limited resourcesto unlock the potential

26IHS - Wendel Investor Day | December 1, 2016

Investor DayDecember 1, 2016

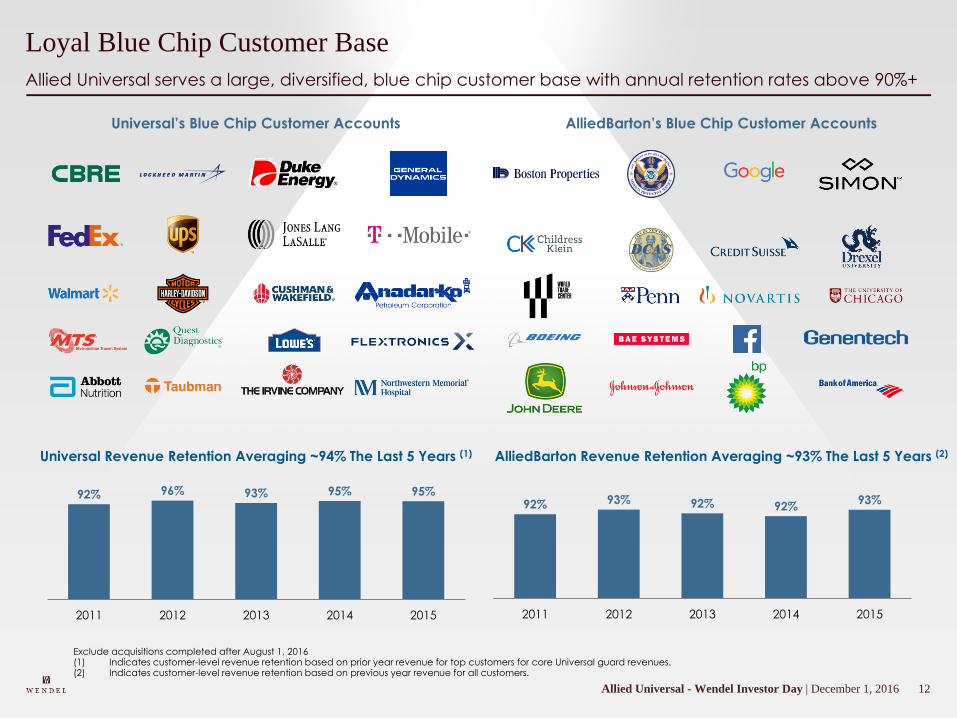

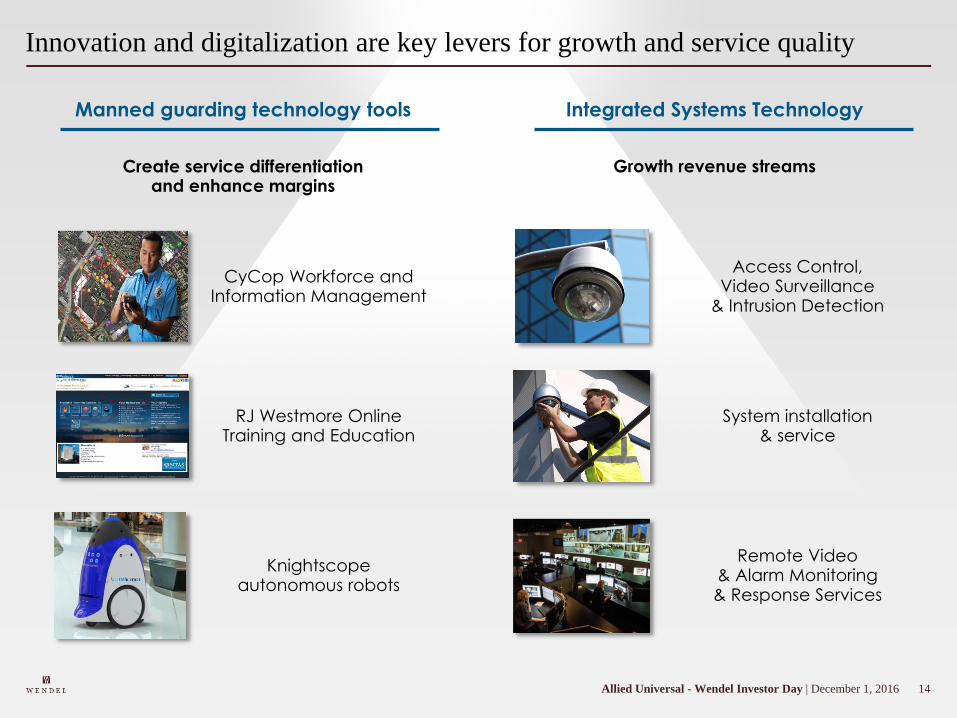

0Allied Universal - Wendel Investor Day | December 1, 2016

Allied Universal

• Well-known American player of security services with a nationwide footprint

• Outstanding platform for consolidation

• Resilient growth and high cash flows

• High quality services & strongcredibility in the market

Capitalize on a very strong megatrend in America:

organic growth & consolidationof the security services market

$300m equity invested

c. 33% equity stake

co-control with Warburg-Pincus

1Allied Universal - Wendel Investor Day | December 1, 2016

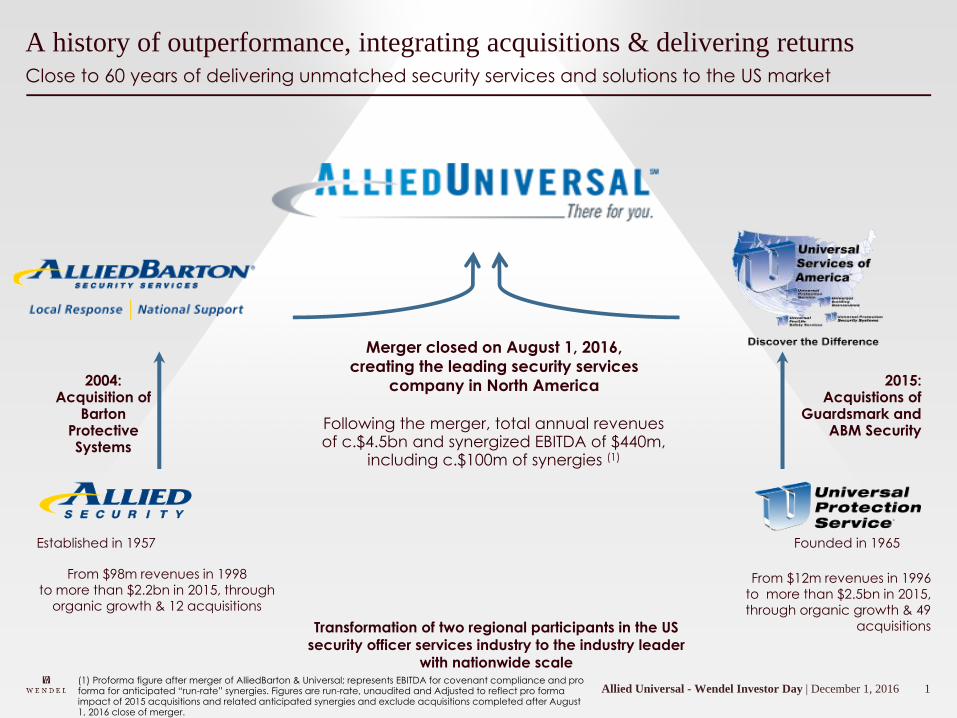

Close to 60 years of delivering unmatched security services and solutions to the US market

A history of outperformance, integrating acquisitions & delivering returns

Transformation of two regional participants in the US

security officer services industry to the industry leader

with nationwide scale

Founded in 1965

From $12m revenues in 1996

to more than $2.5bn in 2015,

through organic growth & 49

acquisitions

Established in 1957

From $98m revenues in 1998

to more than $2.2bn in 2015, through

organic growth & 12 acquisitions

Merger closed on August 1, 2016,

creating the leading security services

company in North America2004:Acquisition of

Barton Protective Systems

2015:Acquistions of

Guardsmark and ABM SecurityFollowing the merger, total annual revenues

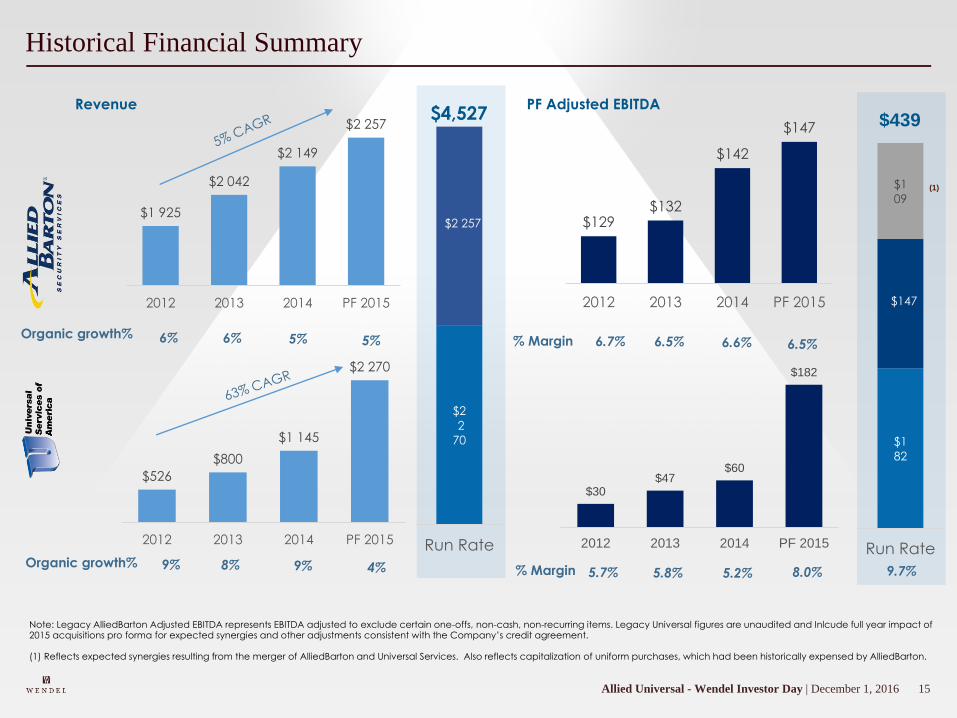

of c.$4.5bn and synergized EBITDA of $440m, including c.$100m of synergies (1)

(1) Proforma figure after merger of AlliedBarton & Universal; represents EBITDA for covenant compliance and pro forma for anticipated “run-rate” synergies. Figures are run-rate, unaudited and Adjusted to reflect pro forma impact of 2015 acquisitions and related anticipated synergies and exclude acquisitions completed after August 1, 2016 close of merger.

2Allied Universal - Wendel Investor Day | December 1, 2016

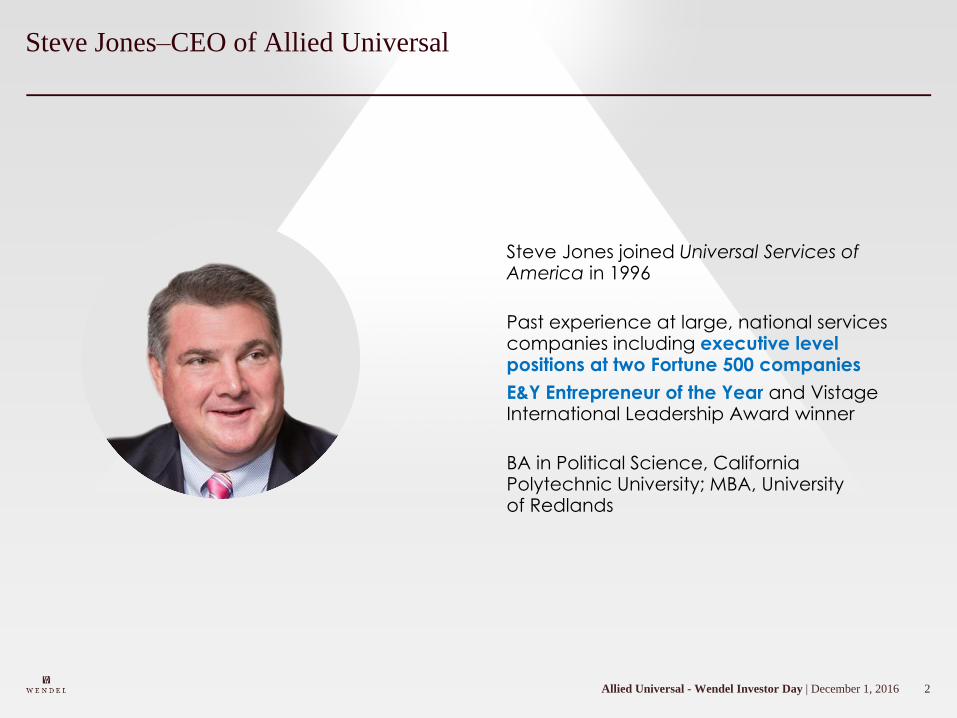

Steve Jones–CEO of Allied Universal

Steve Jones joined Universal Services of America in 1996

Past experience at large, national services companies including executive level positions at two Fortune 500 companies

E&Y Entrepreneur of the Year and Vistage International Leadership Award winner

BA in Political Science, California Polytechnic University; MBA, University of Redlands

3Allied Universal - Wendel Investor Day | December 1, 2016

Allied Universal Steve Jones - CEO

4Allied Universal - Wendel Investor Day | December 1, 2016

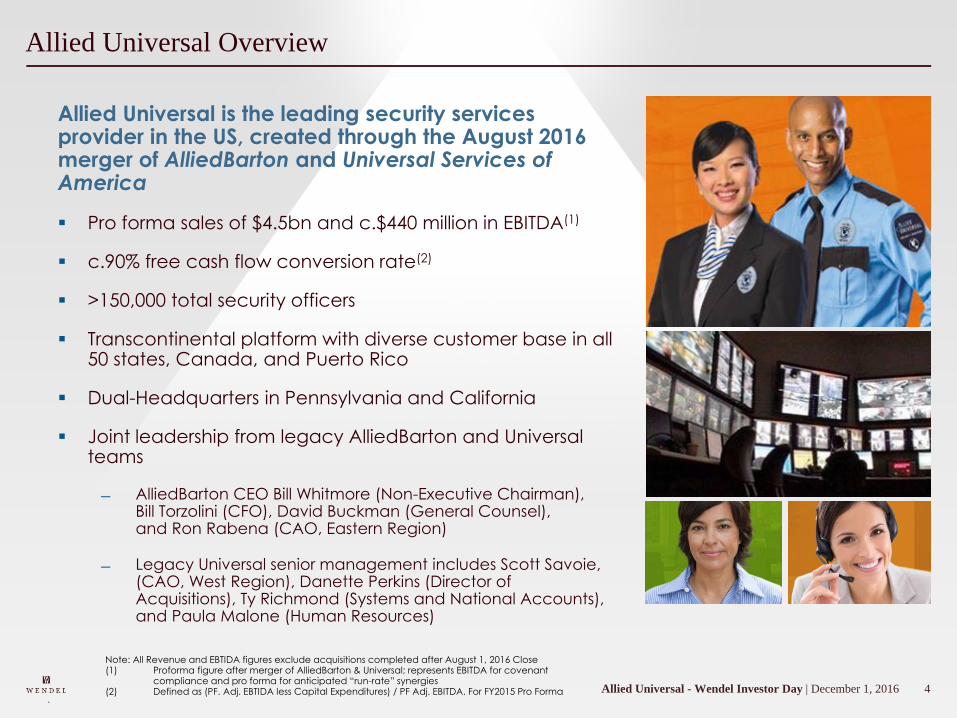

Allied Universal Overview

Allied Universal is the leading security services provider in the US, created through the August 2016 merger of AlliedBarton and Universal Services of America

Pro forma sales of $4.5bn and c.$440 million in EBITDA(1)

c.90% free cash flow conversion rate(2)

>150,000 total security officers

Transcontinental platform with diverse customer base in all 50 states, Canada, and Puerto Rico

Dual-Headquarters in Pennsylvania and California

Joint leadership from legacy AlliedBarton and Universal teams

AlliedBarton CEO Bill Whitmore (Non-Executive Chairman), Bill Torzolini (CFO), David Buckman (General Counsel), and Ron Rabena (CAO, Eastern Region)

Legacy Universal senior management includes Scott Savoie, (CAO, West Region), Danette Perkins (Director of Acquisitions), Ty Richmond (Systems and National Accounts), and Paula Malone (Human Resources)

.

Note: All Revenue and EBTIDA figures exclude acquisitions completed after August 1, 2016 Close(1) Proforma figure after merger of AlliedBarton & Universal; represents EBITDA for covenant

compliance and pro forma for anticipated “run-rate” synergies (2) Defined as (PF. Adj. EBTIDA less Capital Expenditures) / PF Adj. EBITDA. For FY2015 Pro Forma

5Allied Universal - Wendel Investor Day | December 1, 2016

Allied Universal Merger Rationale

The combination of Universal and AlliedBarton has created the industry leader with unmatched scale and expertise in providing quality security services

✔ Formation of the #1 security services provider in North America

✔ Combination of the preeminent organic and M&A growth engines

✔ Ability to capitalize on the strengths of both companies and retain best-of-breed management

✔ Unmatched service coverage, with scale on a national level and significant density in local markets

✔ Cost synergies meaningfully enhance attractive cash flow profile

✔ Increased diversification across industry verticals, geographies and customers

✔ Expertise and leadership in high growth national accounts and attractive industry verticals

6Allied Universal - Wendel Investor Day | December 1, 2016

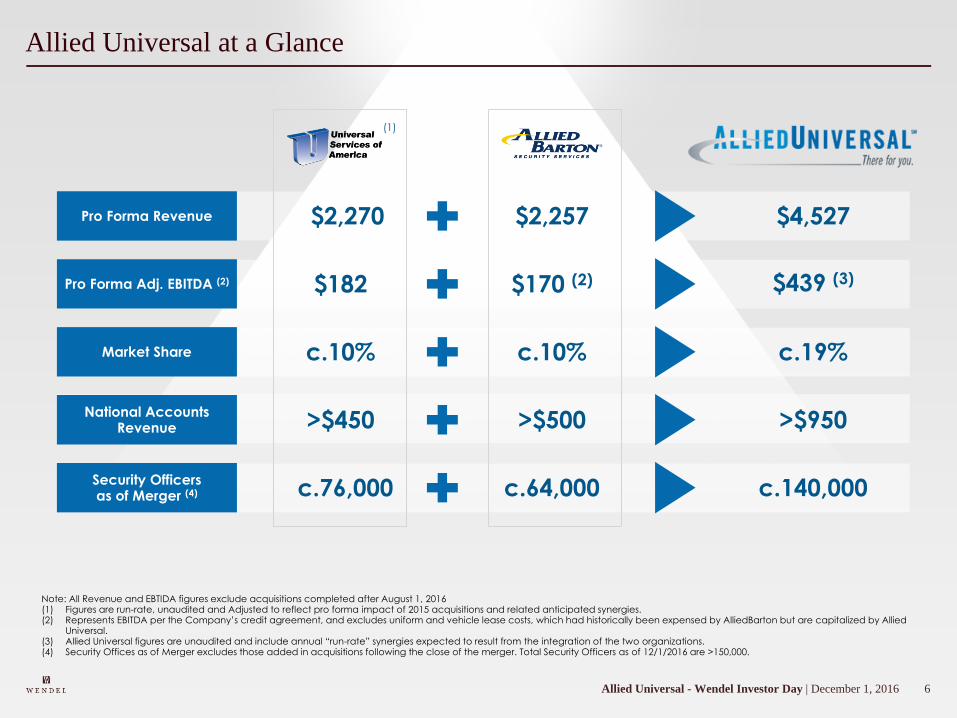

Allied Universal at a Glance

Pro Forma Revenue $2,270 $2,257 $4,527

Pro Forma Adj. EBITDA (2) $182 $170 (2) $439 (3)

Market Share c.10% c.10% c.19%

National Accounts Revenue >$450 >$500 >$950

Security Officers as of Merger (4) c.76,000 c.64,000 c.140,000