Pets at Home Investor & Analyst Capital Markets Presentation September 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Pets at Home Investor & Analyst Capital Markets Presentation

September 2017

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Introduction

Ian Kellett Group CEO

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Today: a focus on the Group’s strategic and competitive position and our medium term outlook in the sector

2

Growing our overall share in the pet products and services market

1

Bringing convenience to our customers through omnichannel

investment

2

Growing the market and our share in Advanced Nutrition food

3

Giving more service and advice to customers, online and in-store

4

Rolling out new practices and growing ahead of market in our

veterinary business

5

Pursuing bolt-on growth opportunities, particularly in the

veterinary market

6

Group strategic focus and achievements

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Afternoon timetable

14.00 – 15.00

Ian Kellett Introduction

Pet market insights and our competitive position

Andrei Balta Vet Group business

Q&A

15.00 – 15.25 Break and networking with Pets at Home colleagues

15.30 – 16.25

Peter Pritchard Retail business

Mike Iddon and Ian Kellett Integrated product and services economics Conclusions

Q&A

16.30 Finish 0

3

Presenter

Presentation Notes

Flag that we will take a break after the Seamless shopping section

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

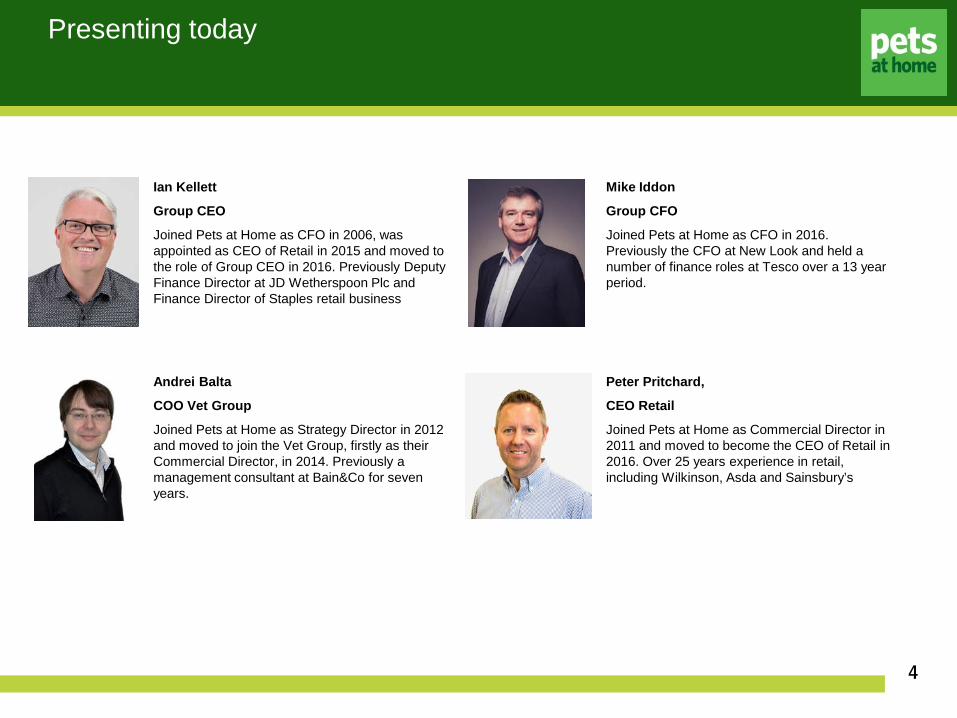

Ian Kellett

Group CEO

Joined Pets at Home as CFO in 2006, was appointed as CEO of Retail in 2015 and moved to the role of Group CEO in 2016. Previously Deputy Finance Director at JD Wetherspoon Plc and Finance Director of Staples retail business

Mike Iddon

Group CFO

Joined Pets at Home as CFO in 2016. Previously the CFO at New Look and held a number of finance roles at Tesco over a 13 year period.

Andrei Balta

COO Vet Group

Joined Pets at Home as Strategy Director in 2012 and moved to join the Vet Group, firstly as their Commercial Director, in 2014. Previously a management consultant at Bain&Co for seven years.

Peter Pritchard,

CEO Retail

Joined Pets at Home as Commercial Director in 2011 and moved to become the CEO of Retail in 2016. Over 25 years experience in retail, including Wilkinson, Asda and Sainsbury’s

Presenting today

4

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Pet market insights

Ian Kellett Group CEO

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

There are multiple factors driving growth in the UK pet market

Vet Group Retail

6

Humanisation of pets

Stable pet numbers

Focus on health &

wellbeing

Expanding vet

procedures

Increasing insurance coverage

Advanced Nutrition

Expected annual growth in UK pet

products and services market 5%

(2016-21)1

1 Source: OC&C

Omnichannel sales

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

UK pet market growth has been boosted by services and has been more resilient than the general retail market

Vet Group Retail

7

100

102

104

106

108

110

112

114

116

118

120

2012 2013 2014 2015 2016

Mar

ket g

row

th (r

ebas

ed)

UK General Retail Pet Products Pet Market including Services

Source: UK General Retail data: ONS Value Seasonally Adjusted: All Retailers excluding fuel. Pet products and market data: OC&C 2017.

UK general retail market vs. pet retail market growth

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

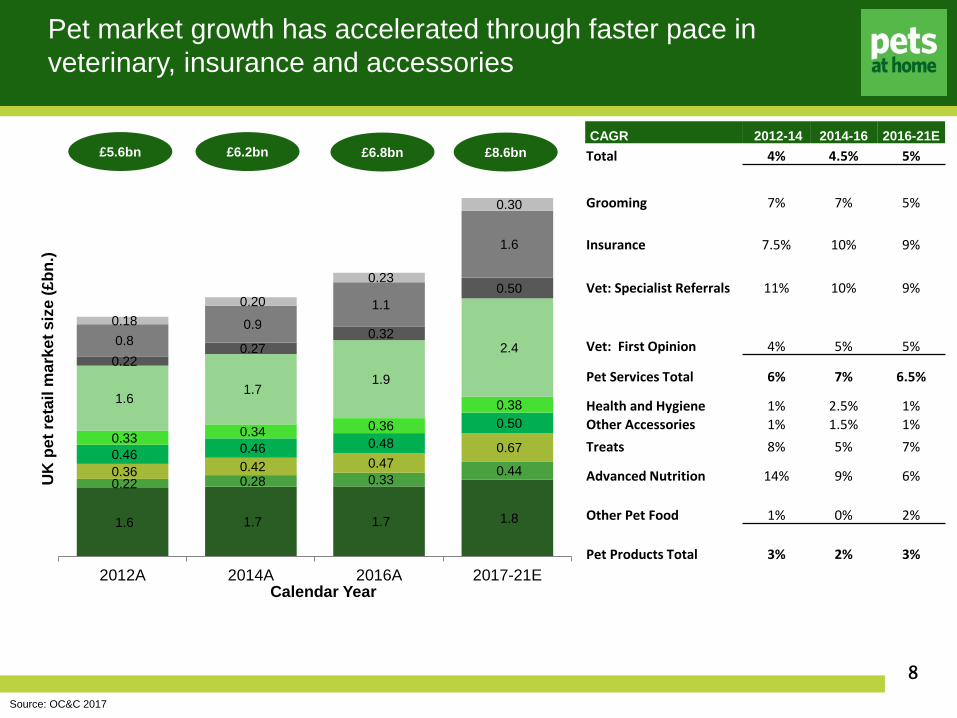

Pet market growth has accelerated through faster pace in veterinary, insurance and accessories

Vet Group

8

1.6 1.7 1.7 1.8

0.22 0.28 0.33 0.44 0.36 0.42 0.47 0.67 0.46 0.46 0.48 0.50

0.33 0.34 0.36 0.38 1.6

1.7 1.9

2.4 0.22

0.27 0.32

0.50

0.8 0.9

1.1

1.6

0.18 0.20

0.23

0.30

2012A 2014A 2016A 2017-21E

UK

pet

reta

il m

arke

t siz

e (£

bn.)

Calendar Year

£5.6bn £6.2bn £8.6bn £6.8bn

Source: OC&C 2017

CAGR 2012-14 2014-16 2016-21E Total 4% 4.5% 5%

Grooming 7% 7% 5%

Insurance 7.5% 10% 9%

Vet: Specialist Referrals 11% 10% 9%

Vet: First Opinion 4% 5% 5%

Pet Services Total 6% 7% 6.5%

Health and Hygiene 1% 2.5% 1% Other Accessories 1% 1.5% 1% Treats 8% 5% 7%

Advanced Nutrition 14% 9% 6%

Other Pet Food 1% 0% 2%

Pet Products Total 3% 2% 3%

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

We remain the UK’s largest pet business

Retail

9

0

100

200

300

400

500

600

700

800

900

FY17

Num

ber o

f Sto

res

Financial Year

Pets at Home Pets Corner Pet HutJolleyes Just For Pets KennelGate

0

200

400

600

800

1000

1200

1400

FY17

Num

ber o

f Pra

ctic

es

Financial Year

Pets at Home CVS IVC Medivet Vet Partners

Source: Annual report and financial statements and company websites.

Vet first opinion practice numbers by competitor Pet store numbers by competitor

Total UK small animal vet

practices c5000

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our total pet product market share has grown from 19% to 20% through 2014-2016

Vet Group Retail

10 Source: OC&C 2017

53%

21%

5% 13%

36%

36% 73% 64%

6%

14% 13%

17%

19%

15%

19%

7%

8%

13%

16%

12%

8% 9% 3%

21%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Advanced Nutrition Bridging Grocery Treats Accessories

Mar

ket S

hare

Pets at Home Grocers Discounters Vets Pet Specialists Online (Specialists and Non-Specialists) Other

Pets at Home Share Change 2014-2016

+2%

Pet product market share by player, 2016

+3% 0% +1% +2%

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Stores are an important part of future market growth. Bricks and mortar sales along with C&C expected to grow at 2.7% per annum

Vet Group Retail

11

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2016A 2021E

Expe

cted

UK

Pet

Pro

duct

Mar

ket

Valu

e (£

bn.)

Bricks and Mortar Online Click and Collect Online Deliver to Home

Source: OC&C 2017. Data refers to calendar years.

c15% c11% Online participation

0f pet market

Pet Products Market CAGR

2016-21

Total 3.0%

Online Deliver to Home 5.3%

Online Click and Collect 30.0%

Bricks and Mortar 2.1%

2.7%

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

The vet market continues to consolidate and we are one of three major players with leading market share

Vet Group Retail

12

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2014 2016

Mar

ket S

hare

PAH JV CVS Medivet IVC Other

Source: OC&C 2017 and Pets at Home estimates

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Actual Estimated Mature

Mar

ket S

hare

PAH JV CVS Medivet IVC Other

Note: Data refers to calendar years, by estimated revenue per practice.

If all our existing practices were mature, estimated PAH share would be 18%

PAH Vet Group has a 12% market share with a young practice estate

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Unique competitive position

Ian Kellett Group CEO

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Unique integrated product and service offering

Vet Group Retail

14

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

And a differentiated competitive position in the pet market

15

Grocers/discounters

Online specialists

Online generalists

Vet groups

Product range

Vet or groom services

Online platform

Omnichannel capabilities

Expertise & advice

Value & price

Convenience

Customer pet data

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

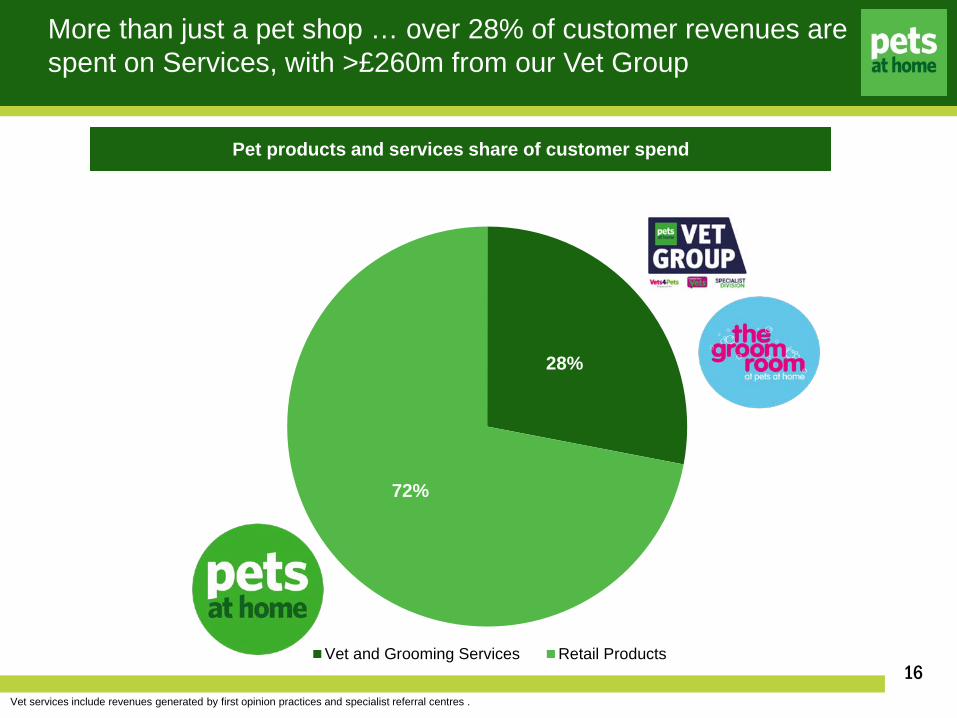

More than just a pet shop … over 28% of customer revenues are spent on Services, with >£260m from our Vet Group

Vet Group Retail

16

28%

72%

Vet and Grooming Services Retail Products

Pet products and services share of customer spend

Vet services include revenues generated by first opinion practices and specialist referral centres .

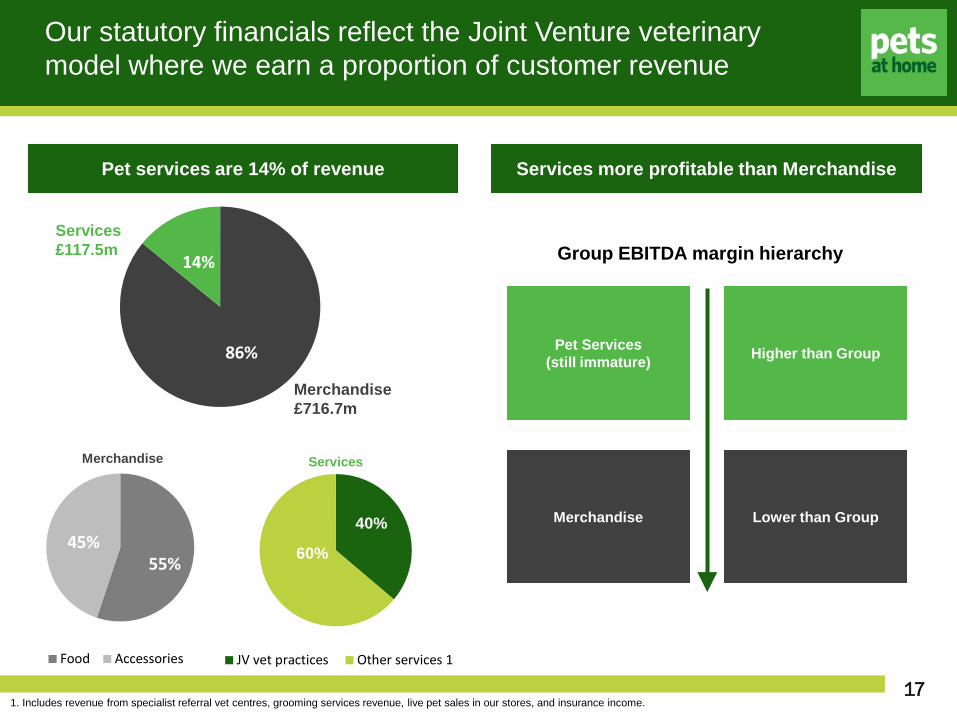

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

JV vet practices Other services 1

55% 45%

Food Accessories

86%

14%

Pet Services (still immature)

Merchandise

Higher than Group

Lower than Group

Group EBITDA margin hierarchy

Merchandise £716.7m

Services £117.5m

Our statutory financials reflect the Joint Venture veterinary model where we earn a proportion of customer revenue

17 1. Includes revenue from specialist referral vet centres, grooming services revenue, live pet sales in our stores, and insurance income.

Services more profitable than Merchandise Pet services are 14% of revenue

40%

60%

Merchandise Services

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Having an integrated product and services offering drives overall customer spend and frequency

Vet Group

18

Store Only Store and Web Store & Web &Groomer

Store & Vet & Web Store & Vet & Web &Groomer

Spen

d pe

r ann

um (£

)

Customer type

Store Vet Online Groom

£490 £339 £76 £- £-

£396 £245 £295 £195 £125

VIP loyalty card data: average yearly spend of product and services customers

34 22 19 11 6 Customer

Transactions per annum

Services spend

Store spend

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Rollout of vet practices and grooming salons, along with marketing, is encouraging more VIPs to purchase product & services

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

FY15 FY16 FY17

+36%

+14%

19

Number of VIP loyalty card members who purchase both products and a service

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our strategy is designed to maximise our competitive position and market opportunity

Price, innovation, services & advice

Vet practice maturity

Optimised Store & Services Rollout

Key Growth Drivers

Driv

ers

of C

ore

Gro

wth

Like For Like

Space

Margin

VIP club members

Omnichannel

Vet Group

Private label mix

20

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Vet Group

Andrei Balta Vet Group COO

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

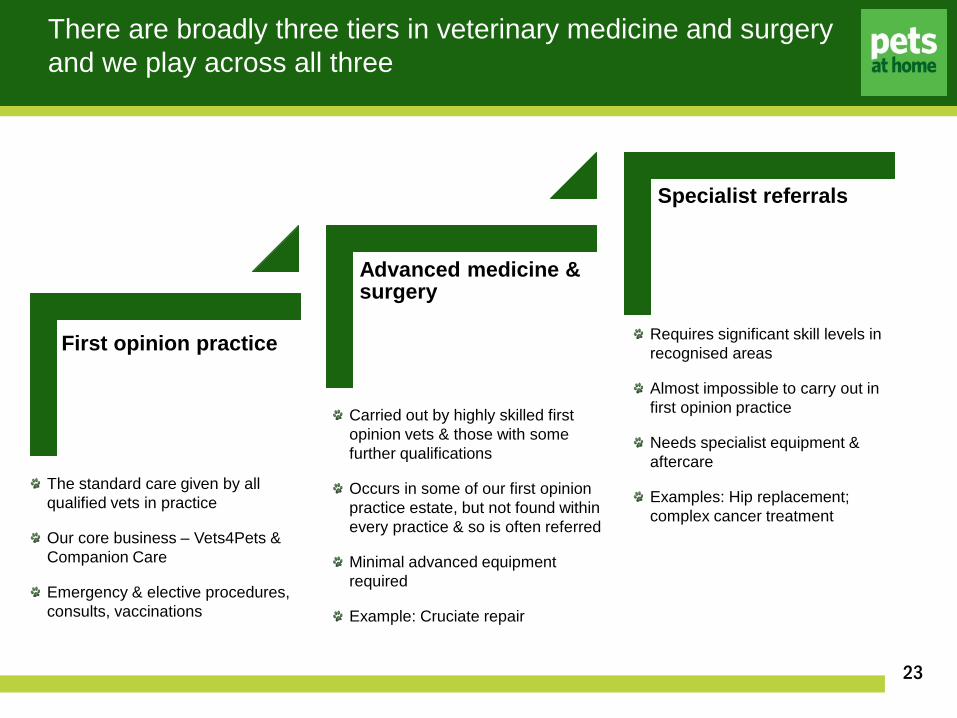

Our core business is first opinion small animal veterinary practices, with recent extension into specialist referral care

22

Vet Group Retail

438 practices at end FY17 289 in-store 149 standalone

Covers all aspects of general small animal veterinary work: preventative care, emergency care, sick pet work Health plans 24/7 out of hours care Extended hours Own brand nutraceuticals

Internal medicine Oncology Orthopaedic surgery Soft tissue surgery Neurology and neurosurgery Diagnostic imaging

First opinion practices Referral centres

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

23

First opinion practice

Advanced medicine & surgery

Specialist referrals

The standard care given by all qualified vets in practice

Our core business – Vets4Pets & Companion Care

Emergency & elective procedures, consults, vaccinations

Carried out by highly skilled first opinion vets & those with some further qualifications

Occurs in some of our first opinion practice estate, but not found within every practice & so is often referred

Minimal advanced equipment required

Example: Cruciate repair

Requires significant skill levels in recognised areas

Almost impossible to carry out in first opinion practice

Needs specialist equipment & aftercare

Examples: Hip replacement; complex cancer treatment

There are broadly three tiers in veterinary medicine and surgery and we play across all three

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

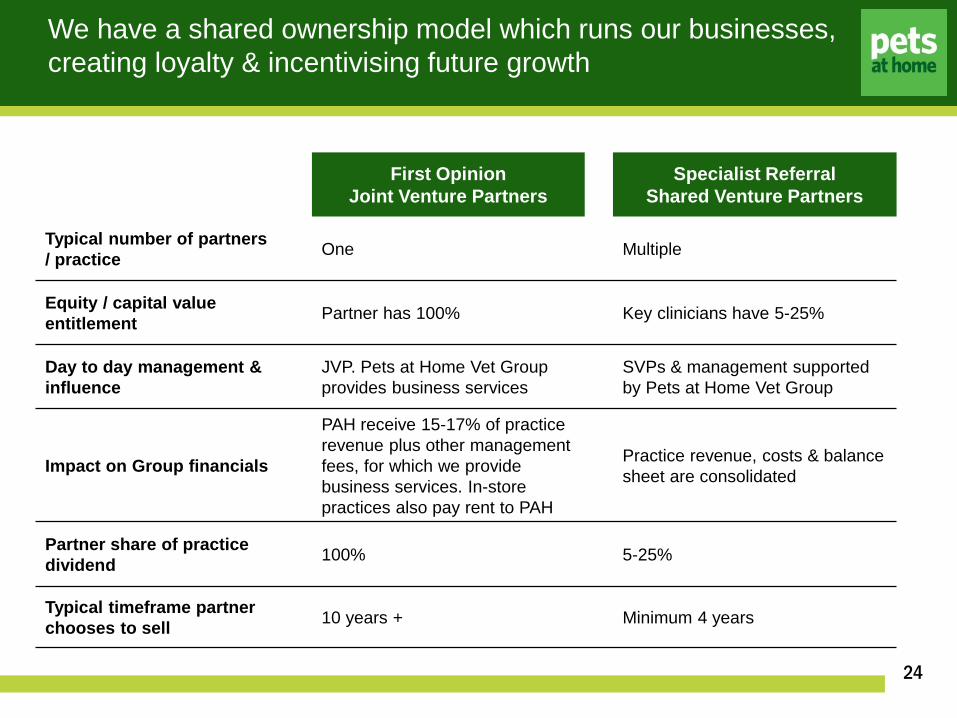

We have a shared ownership model which runs our businesses, creating loyalty & incentivising future growth

24

First Opinion Joint Venture Partners

Specialist Referral Shared Venture Partners

Typical number of partners / practice One Multiple

Equity / capital value entitlement Partner has 100% Key clinicians have 5-25%

Day to day management & influence

JVP. Pets at Home Vet Group provides business services

SVPs & management supported by Pets at Home Vet Group

Impact on Group financials

PAH receive 15-17% of practice revenue plus other management fees, for which we provide business services. In-store practices also pay rent to PAH

Practice revenue, costs & balance sheet are consolidated

Partner share of practice dividend 100% 5-25%

Typical timeframe partner chooses to sell 10 years + Minimum 4 years

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

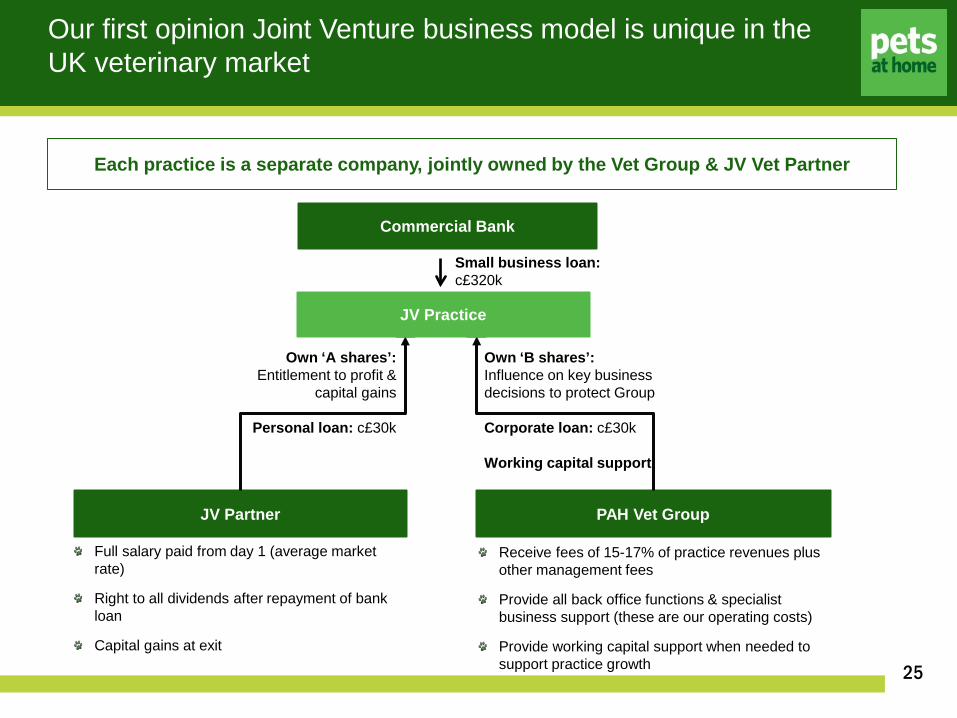

Our first opinion Joint Venture business model is unique in the UK veterinary market

25

JV Partner PAH Vet Group

Own ‘A shares’: Entitlement to profit &

capital gains

Personal loan: c£30k

Own ‘B shares’: Influence on key business decisions to protect Group Corporate loan: c£30k Working capital support

Full salary paid from day 1 (average market rate)

Right to all dividends after repayment of bank loan

Capital gains at exit

Receive fees of 15-17% of practice revenues plus other management fees

Provide all back office functions & specialist business support (these are our operating costs)

Provide working capital support when needed to support practice growth

JV Practice

Commercial Bank

Small business loan: c£320k

Each practice is a separate company, jointly owned by the Vet Group & JV Vet Partner

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our Joint Venture partnership model provides a number of important advantages

26

Vet Group Our competitive advantage Vs corporate

competitors Vs independents

JV Partner highly motivated to drive business: sense of ownership and potential for high returns

Employed colleagues lack incentive to drive business to full potential

Independent ownership creates motivation but responsibility daunting to many vets

Business support from Vet Group provides expert support in non-clinical areas, leveraging our scale and expertise

Business support provided centrally

Vets responsible for clinical and non-clinical issues, often lacking core business capabilities. Minimal benefits of scale

National Brand provides opportunity to reach customers at scale

Closest competitors have no national branding

Can build local reputation, but not national

Association with Pets at Home provides access to highly engaged VIP members and PAH colleague advocates

No association with national retailer to leverage

Local relationships cannot replicate VIP or PAH opportunity

Growth plans focused on highly repeatable new opening model

Minimal number of new openings. Growth dependent on acquisitions

New opening challenging due to funding constraints and risk of new entity

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

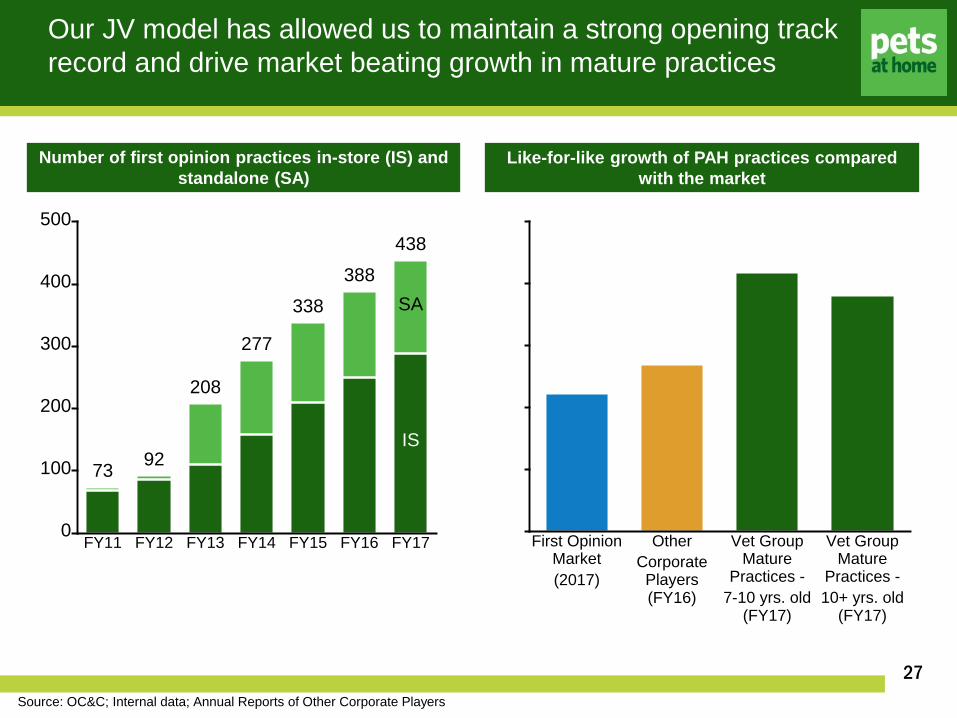

Our JV model has allowed us to maintain a strong opening track record and drive market beating growth in mature practices

27

0

100

200

300

400

500

Pets at Home Vet Group Practices

FY11

73

FY12

92

FY13

208

FY14

277

FY15

338

FY16

388

FY17

IS

SA

438

Like-for-like growth

First Opinion

Market

(2017)

Other

Corporate

Players

(FY16)

Vet Group

Mature

Practices -

7-10 yrs. old

(FY17)

Vet Group

Mature

Practices -

10+ yrs. old

(FY17)

Source: OC&C; Internal data; Annual Reports of Other Corporate Players

Number of first opinion practices in-store (IS) and standalone (SA)

Like-for-like growth of PAH practices compared with the market

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our First Opinion strategy is built around four pillars and underpinned by preparing for future scale

28

Vet Group

Build our brand

Be the best place to work

Put our clients first

Deliver world class support

Prepare for future scale

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

0

20

40

60

80

Feb-16 Jul-16 Oct-16 Feb-17

Advocacy

Building our brand: We have the most recognised brand in the UK vet market and it is well perceived

29

Vet Group

0

20

40

60%

Vets4P

ets

Medive

t

Compa

nion

CareIV

C

Best F

riend

sCVS

Godda

rd

Prompted awareness of UK veterinary

groups among regular vet users

Source: PAH Annual Survey 2017; Millward Brown metrics Advocacy measured as % of people who would recommend this brand to a friend or colleague

Advocacy – measured as the percentage of people who would recommend the brand

Prompted awareness of UK veterinary groups amongst regular vet users

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Build our brand: Our strong brand allows us to achieve national, regional and local visibility

30

Vet Group

Our TV campaigns had an annual reach of 46m in the last 12 months

We’ve built unique relationships with national charities to help

attract rehoming clients

We’re creating regional partnerships and educating pet

owners alongside building awareness of our brand

We can build strong local messages, reinforcing the local nature alongside our national

brand

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Be the best place to work: We’re focused on being the employer of choice for clinical and non-clinical colleagues

31

Vet Group

Graduate programme refreshed & extended

International Intern programme

Everywoman Programme

Nursing Academy

Nurse & VCA Apprenticeships

Nurse Conference & Continuing Professional Development (CPD)

Reception Academy

Healthcare Plan modules

JVP Development Journey

Our focus on colleague engagement and wellbeing differentiates us from our competitors

Vets Nurses Non-clinical

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Put our clients first: We perform well on the key indicators most important to clients and significant progress has been achieved

32

Vet Group

Source: PAH Vets Group Customer Insights 2017

All Respondents: Key Purchase Criteria Im

port

ance

Great cu

stomer

serv

ice

Conv

enien

t loc

ation

Been

trea

ting my p

ets f

or ye

ars

Prem

ises h

ave n

ice lo

ok an

d fee

l

I can

alway

s see

the s

ame v

et

Reco

mmen

ded by

frien

d/oll

eagu

e

Lowes

t pric

e

Reco

mmen

ded by

staff

in pe

t sho

p

Vet a

nd nur

ses a

re w

ell

traine

d &

profes

siona

l

All s

ervic

es m

y pet nee

ds

Conv

enien

t ope

ning ho

urs

Open for e

mer

genc

ies

at nigh

ts an

d at w

eeke

nds

Spec

ialist

vets

at th

e pra

ctice

Good va

lue fo

r mon

ey

Reco

mmen

ded on

line

Reco

mmen

ded by

my b

reed

er

V4P 2017V4P 2014

Local

independents

Key purchase criteria and ratings of our practices compared with independents

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Deliver world class Partner support: Strong support system in place around Partners that we are constantly investing in

33

Vet Group

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Deliver world class Partner support: Helping JVPs develop their mature businesses is an important part of our support

34

Vet Group Expand mature practice Acquire multiple sites Sell their ownership

Developing “super surgeries” and 24/7 – space and time expansion of existing mature practices

Example Mature practice opened in 1998

FY 15/16: Customer revenue £2.0M

Dec. 2015: added 3 consults and 1 theatre

Dec. 2016: launched 24/7

Customer revenue LfL growth FY18 YTD; 28%

Practice EBITDA LFL growth 48%

JVPs can acquire a stake in multiple practices

Example

JVP opened first in-store practice July 2010

Opened 2nd site with 2nd JVP in 2011

JVP now holds stake in 5 practices, already drawing dividends from 2010 opening

Mentors younger vets to become Co-Partners

Opportunity to work together across cluster i.e. 24/7, CT scanner facilities

JVPs exit their practice by selling A shares to another vet (approved by PAH). All profits belong to the JVP

Example Practice opened July 2010. Partner decided to exit September 2016 to allow change in lifestyle

Sold for £0.6m

Practice LfL growth post sale 13% vs 9% pre sale Uptick in growth expected post sale: “JVP effect”

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

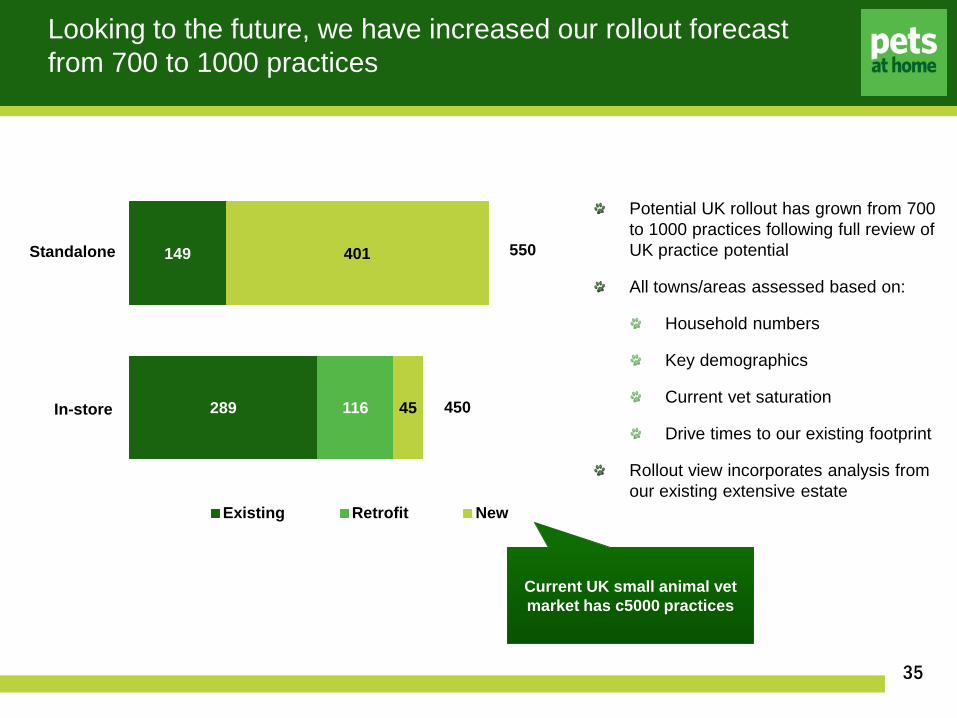

Looking to the future, we have increased our rollout forecast from 700 to 1000 practices

35

Vet Group

Potential UK rollout has grown from 700 to 1000 practices following full review of UK practice potential

All towns/areas assessed based on:

Household numbers

Key demographics

Current vet saturation

Drive times to our existing footprint

Rollout view incorporates analysis from our existing extensive estate

Current UK small animal vet market has c5000 practices

289

149

116 45

401

Existing Retrofit New

550

450 In-store

Standalone

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Entering the specialist market brings financial & reputational benefits to the Group

36

A natural adjacency in the veterinary market where we have core competency

Incremental market spend & share of wallet opportunity with existing clients

Enhances our reputation with clients, potential Joint Venture vet partners & employed vets / nurses

Offers world class CPD to our first opinion vets & nurses

Internal Medicine

Oncology

Ophthalmology

Cardiology

Neurology

Orthopeadics

Spinal Surgery

Diagnostic Imaging

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our specialist division is performing well and growing ahead of the market rate

Market

PAH Vet Group

Specialist

Division

Specialist Like for Like growth

122.9

Source: Market data based on FY17 to FY18 full year, OC&C; PAH VG based on YTD

Like-for-like growth in our referral centres is 12 percentage points ahead of the overall market

37

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

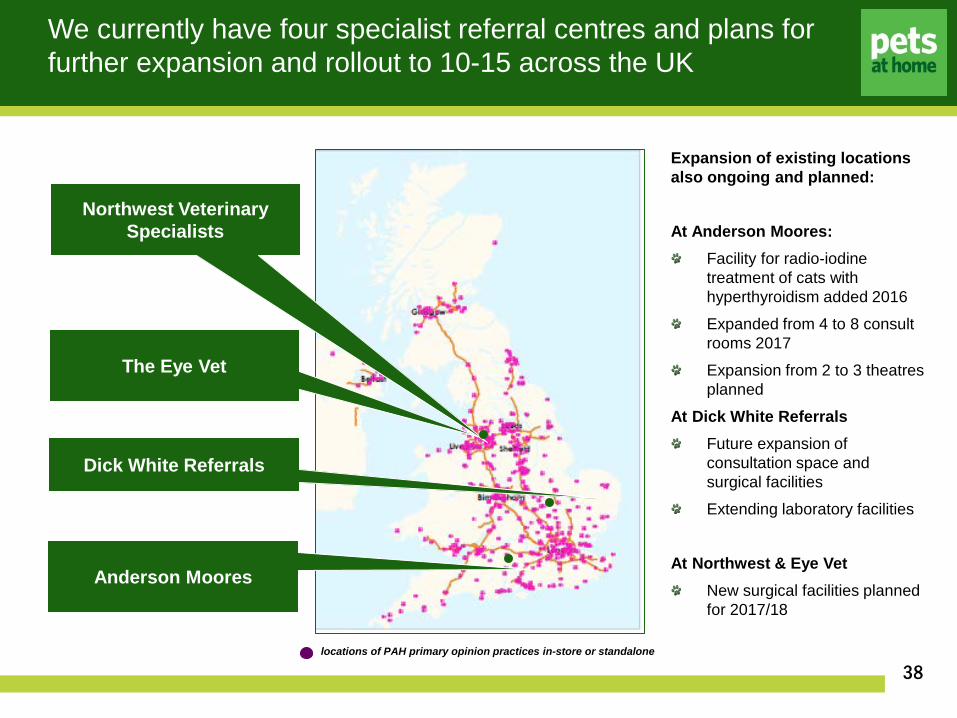

We currently have four specialist referral centres and plans for further expansion and rollout to 10-15 across the UK

38 locations of PAH primary opinion practices in-store or standalone

Northwest Veterinary Specialists

Dick White Referrals

Anderson Moores

The Eye Vet

Expansion of existing locations also ongoing and planned:

At Anderson Moores: Facility for radio-iodine treatment of cats with hyperthyroidism added 2016

Expanded from 4 to 8 consult rooms 2017

Expansion from 2 to 3 theatres planned

At Dick White Referrals Future expansion of consultation space and surgical facilities

Extending laboratory facilities

At Northwest & Eye Vet New surgical facilities planned for 2017/18

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

<1 Year 1-2 Years 3- 4 Years 5-6 Years 7-10Years

10+ Years

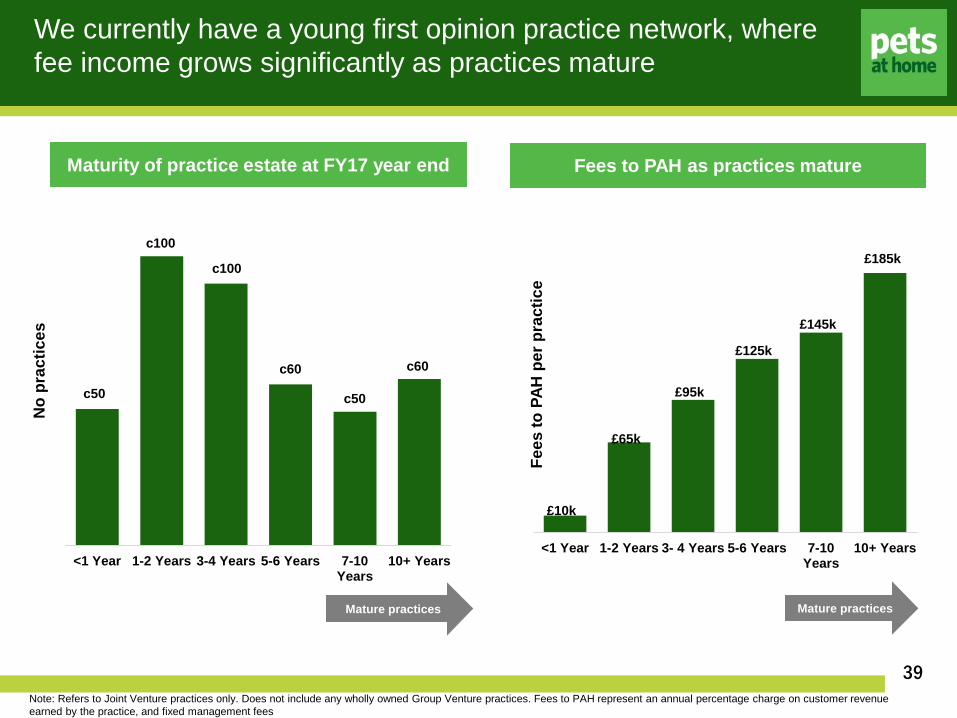

We currently have a young first opinion practice network, where fee income grows significantly as practices mature

39

Maturity of practice estate at FY17 year end

No

prac

tices

Fees to PAH as practices mature

Mature practices

Fees

to P

AH p

er p

ract

ice

<1 Year 1-2 Years 3-4 Years 5-6 Years 7-10

Years10+ Years

Mature practices

c100

c60

c50

c60

c100

c50

Note: Refers to Joint Venture practices only. Does not include any wholly owned Group Venture practices. Fees to PAH represent an annual percentage charge on customer revenue earned by the practice, and fixed management fees

£10k

£95k

£125k

£145k

£185k

£65k

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

FY17a FY20e FY23e

The number of mature practices is expected to almost double by FY20 and more than triple by FY23

40

Number of mature practices aged 7 years and older

Almost double the number of mature practices vs FY17

c110

>200

>350

Note: Mature practices refers to Joint Venture practices aged 7+ years. The generation of mature practices to FY23 does not require any further new practice openings

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

£0m

£25m

£50m

£75m

£100m

FY17a FY20e FY23e

Fees from new openings & immature practices Fees from Mature Practices

As we roll out towards reaching 1000 practices, our fee income is expected to double

41

Tota

l fee

inco

me

to P

AH

c50% expected increase from current fees

Expected doubling of current fees

Note: Future rollout estimated at 40 practices per annum. Fee income forecasts are based upon the FY17 average fee income for practice cohorts as they age, shown on slide 20 and inflated at c1% per annum. Fees from mature practices includes those aged 7+ years

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

£0

£40,000

£80,000

£120,000

£160,000

£200,000

<1 Year 1-2 Years 3- 4 Years 5-6 Years 7-10 Years 10+ Years

Fees to PAH Incremental PAH costs per new practice opening

The mainly fixed Support Office costs mean that margin leverage is delivered as our first opinion practices mature

42

Incremental costs are additional Support Office colleagues when the practice opens. Colleague costs will then grow at c5% per

annum

Tota

l fee

inco

me

and

cost

s to

PAH

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Overall Vet Group economics: there is an opportunity to significantly increase EBITDA both through maturation and rollout

43

FY17a Current Vet Group (438practices, 4 referral centres)

MATURE Current Vet Group(438 practices, 4 referral

centres)

MATURE Full UK rollout VetGroup (700 practices, 4 referral

centres)

MATURE Full UK rollout VetGroup (1000 practices, 4

referral centres)

FY17a Current Vet Group

438 practices, 4 referral centres

Mature Current Vet Group2

438 practices, 4 referral centres

Mature 700 rollout Vet Group,3

700 practices, 4 referral centres

Mature 1000 rollout Vet Group3

1000 practices, 4 referral centres

1. Mature fee income forecasts for first opinion practices are based upon those for FY17 cohorts aged 10+years – with c1% inflation per annum. EBITDA does not include any central cost allocation for the Executive Management team or Pets at Home Group Head Office support. Referral centre revenue and EBITDA is assumed to remain flat from FY17 actuals

2. EBITDA to PAH assumes no additional colleagues required at Vet Group Support Office to support the existing practice base. Colleague costs are inflated at c5% per annum 3. EBITDA to PAH assumes additional colleagues are required at Vet Group Support Office to support new practice openings. New and existing colleague costs are inflated at c5% per

annum

EBITDA1 to Pets at Home from the Vet Group

c2x Today

Today

>3x Today

c5x Today

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Future plans … our Vet Group strategy is focused on accelerating growth opportunities

44

Build our brand

Be the best place to work

Put our clients first

Deliver world class support

Build scale and grow share across the veterinary market

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Retail business

Peter Pritchard Retail CEO

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

We hold a position of significant share and strength within the pet products market

46

Share of total pet product market

Supermarkets

Online specialists and generalists

Store specialists

Vet practices

Share of pet product market excluding grocery food & treats

20%

46%

8%

7%

6%

13%

40%

7%

16%

12%

13%

11%

Pets at Home

Pets at Home

Supermarkets

Vet practices

Online specialists and generalists

Store specialists

Discounters

Discounters

Note: 2016 estimated market shares Source: OC&C 2016 and PAH pet owner survey 2017

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our points of difference lie in our ability to deliver on all aspects of the market as the only omnichannel products and services provider

47

Omnichannel

Owner and pet data

Colleague advice and expertise

Private label

Subscription platform

Services Strategic

differentiators

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

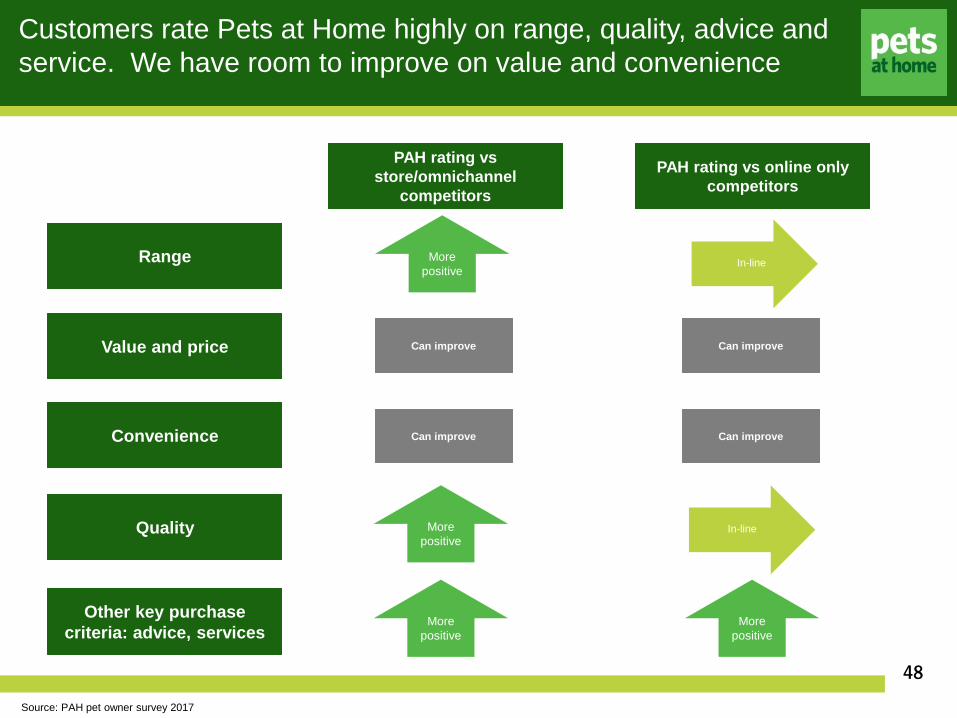

Customers rate Pets at Home highly on range, quality, advice and service. We have room to improve on value and convenience

48

Range

Value and price

Convenience

Quality

PAH rating vs store/omnichannel

competitors

PAH rating vs online only competitors

More positive

More positive

In-line

In-line

Can improve Can improve

Can improve Can improve

Other key purchase criteria: advice, services

More positive

More positive

In-line

Source: PAH pet owner survey 2017

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our immediate strategic focus in retail is based around three key themes: value, competitive advantage and operational leverage

49

Value Competitive Advantage

Operational Leverage

Leveraging the value and quality of our private label

premium foods

Leveraging our points of difference

Driving cost efficiencies

Repositioning prices in branded economy and

Advanced Nutrition foods

Repositioning prices in everyday pet essentials

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

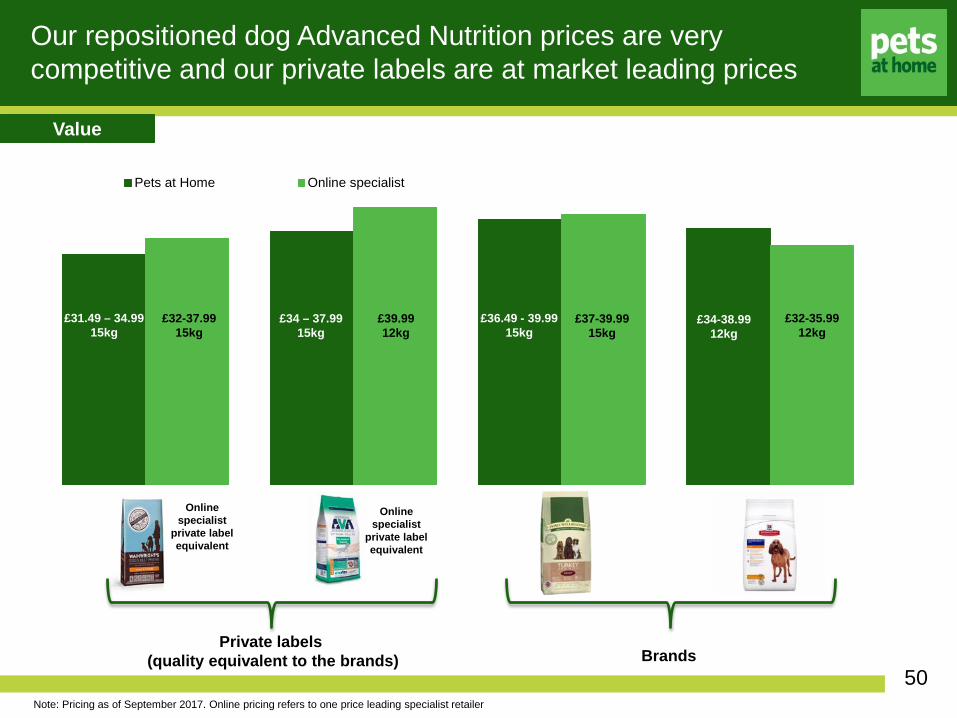

Pets at Home Online specialist

Our repositioned dog Advanced Nutrition prices are very competitive and our private labels are at market leading prices

Online specialist

private label equivalent

Online specialist

private label equivalent

£31.49 – 34.99 15kg

£32-37.99 15kg

Private labels (quality equivalent to the brands) Brands

£39.99 12kg

£37-39.99 15kg

£36.49 - 39.99 15kg

£34-38.99 12kg

£32-35.99 12kg

Note: Pricing as of September 2017. Online pricing refers to one price leading specialist retailer

£34 – 37.99 15kg

Value

50

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Note: Charts show relative pricing index vs Pets at Home. Source: Brandview lowest available price compared for LFL products

-20%

0%

20%

40%

60%

80%

100%

120%

140%

Pre Launch�Post launch

Cat Dog

Pet essentials pricing is now on par with the discounters post repositioning

Value

51

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

100

120

140

160

180

200

220

Jan 17 Feb 17 Mar 17 Apr 17 May 17 Jun 17 Jul 17 Aug 17

We have seen a good response in demand elasticity since repositioning selected dog Advanced Nutrition prices

52

Private label AN volume uplifts are exceeding the deflationary effect

Average price cut c20-30%

And whilst early days we are seeing the same in a branded AN line that we have repositioned

Note: Volumes compare the average uplift since price repositioning with a defined time period before repositioning

Average volume up

>40%

Value

Inde

xed

volu

mes

of d

og A

N p

rivat

e la

bel s

ince

pric

es re

posi

tione

d

Average price cut

c30%

Average volume up

>70%

100

120

140

160

180

200

220

240

260

Apr 17 May 17 Jun 17 Jul 17 Aug 17

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Primarily achieved through reactivating old customers and driving brand switching

53

VIPs who have purchased our private label dog Advanced Nutrition products that have had prices repositioned

Of all VIPs who have purchased,

13% were reactivated customers

Value

New to dry food

Switch from another AN

brand

Switched from grocery dog food

Other

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our Autumn marketing campaign will be the first major opportunity to advertise our pricing message to potential new customers

54

Dog food Advanced Nutrition Day to day pet essentials

Grocery food lines

Value

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our next step in Food will be a marketing campaign to highlight our specialists credentials and educate dog owners on diet quality

55

Value Competitive advantage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Order in-store is a differentiator that demonstrates the importance of stores and service from colleagues

• Colleagues have direct access to our full online range through their PetPads

• Customer order can be completed in under two minutes

• With the option to collect the product back in-store or be delivered to home

We estimate c70% of Order in-store revenues are incremental

Driven by sales of product lines from the extended online range

Competitive advantage

56

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

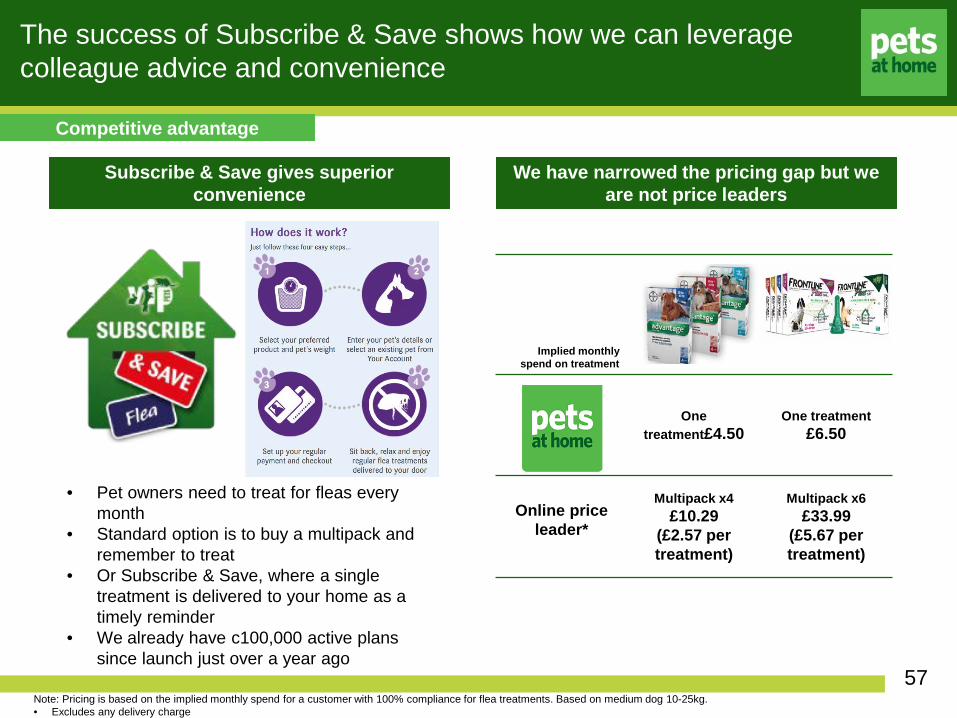

Implied monthly spend on treatment

One treatment£4.50

One treatment £6.50

Online price leader*

Multipack x4 £10.29

(£2.57 per treatment)

Multipack x6 £33.99

(£5.67 per treatment)

Note: Pricing is based on the implied monthly spend for a customer with 100% compliance for flea treatments. Based on medium dog 10-25kg. • Excludes any delivery charge

Subscribe & Save gives superior convenience

The success of Subscribe & Save shows how we can leverage colleague advice and convenience

We have narrowed the pricing gap but we are not price leaders

• Pet owners need to treat for fleas every month

• Standard option is to buy a multipack and remember to treat

• Or Subscribe & Save, where a single treatment is delivered to your home as a timely reminder

• We already have c100,000 active plans since launch just over a year ago

Competitive advantage

57

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our website developments are focused on a faster and simpler checkout process to improve conversion

58

Competitive advantage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

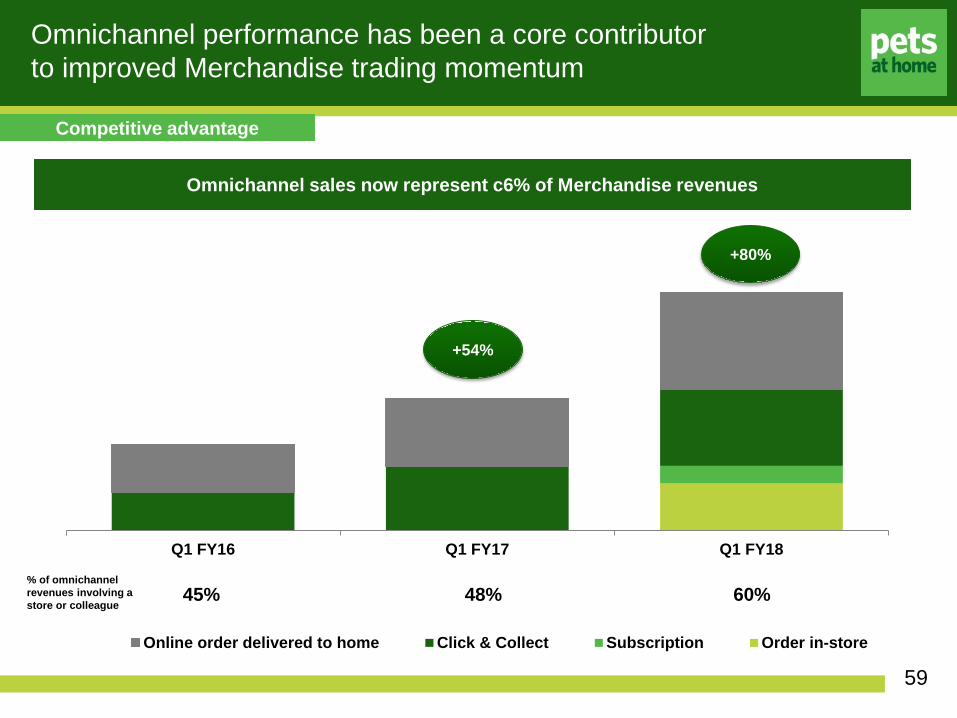

Omnichannel performance has been a core contributor to improved Merchandise trading momentum

Omnichannel sales now represent c6% of Merchandise revenues

Q1 FY16 Q1 FY17 Q1 FY18

Online order delivered to home Click & Collect Subscription Order in-store

+54%

+80%

45% 48% 60% % of omnichannel revenues involving a store or colleague

Competitive advantage

59

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

We need to capture more of the lifetime value of dog and cat owners

60

We have a significant share of the puppy and kitten market, which erodes over their lifetime

Puppy share Adult dog share Kitten share Adult cat share

Pets

at H

ome

shar

e of

pro

duct

s m

arke

t

Competitive advantage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Pet partner for product & services Lifetime loyalty Build trust & love

And have recently launched a Golden Paws initiative aimed at building a long term relationship with new puppy owners

61

Welcome

Average basket value for Golden Paws customers is >30% higher than other puppy customers

The free Advanced Nutrition consultation drives AN participation for Golden Paws customers to double that of other puppy customers

VIP data insights

Competitive advantage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Range change and innovation in accessories has also contributed to our improved trading performance

62

Competitive advantage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

At the same time as innovating – we are driving a number of simplicity initiatives through the retail business to manage costs

63

Targeting c£5m of cost savings in FY18

Reduction in store hours Energy cost management Simpler distribution

Fewer promotional & ticket changes

Simpler & improved pet care routines

Move manual processes to digital

Customer facing time not impacted

LED lights

Smart energy management systems

Reduce SKU count & promo stocking cycles

Fewer small item goods-out deliveries

Reduce goods-in deliveries

Operational leverage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

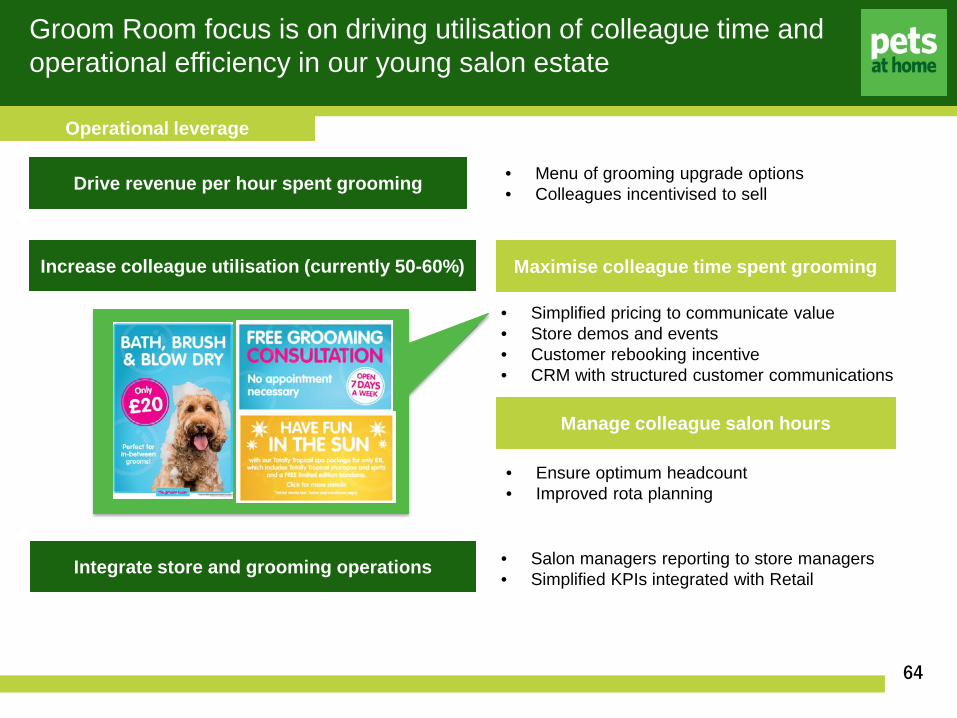

Groom Room focus is on driving utilisation of colleague time and operational efficiency in our young salon estate

64

Drive revenue per hour spent grooming

Increase colleague utilisation (currently 50-60%)

• Menu of grooming upgrade options • Colleagues incentivised to sell

Maximise colleague time spent grooming

Manage colleague salon hours

• Simplified pricing to communicate value • Store demos and events • Customer rebooking incentive • CRM with structured customer communications

Integrate store and grooming operations • Salon managers reporting to store managers • Simplified KPIs integrated with Retail

• Ensure optimum headcount • Improved rota planning

Operational leverage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Proven model will deliver 20-30 new Groom Rooms per year We are also trialling a number of new formats

65

Groom Room in new store

Retrofit in existing store alongside a vet practice

Retrofit in existing store without a vet practice

Groom Room in a standalone vet practice

Grooming salon in Barkers / High Street

Grooming salon standalone pod in other locations

• Proven models with payback <3 years • Will track new store vet refit numbers,

totalling 20-30 per year

More recent formats, where model delivering required return is yet to be proven

Operational leverage

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Future strategic focus … neutralising competitive barriers and leveraging our differentiators

66

Further strengthen price position Take Subscribe & Save to more product categories

Provide more services in-store Give colleagues more knowledge and hours to share with customers

Provide more services online Give customers more convenient shopping locations and platforms

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Integrated store economics and capital investment Mike Iddon Group CFO

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Why we are better together

Vet Group Retail

68

A mature store with integrated services delivers an EBITDA uplift of 24% per square foot compared to a

mature store without services

Annual EBITDA £0.3m Annual EBITDA £0.5m

Note: Includes central cost allocation.

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

We have invested to integrate services into over 54% of our stores. Few are mature, with significant profit maturity to come.

Retail

69

FY17A FY18E FY19E FY20E FY21E FY22E FY23E

200

15

Note: An integrated store unit is defined as a store which incorporates a first opinion veterinary practice and a groom room

Number of mature integrated store units

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our capital expenditure supports growth opportunities

Vet Group Retail

70

4.8 4.4 7.1 14.1 5.3 4.9

10.0

7.2 9.0 13.6

12.9

16.8

10.9 10.3

11.5

6.4

0

5

10

15

20

25

30

35

40

45

50

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21

Cap

ital S

pend

(£m

)

Other including distribution, energy saving and specialist referral vets Business systems and omnichannel Refurbishment and retrofit New stores

£30m

£33m

£42m

£45m £38-40m

Expected run rate

e e e e

£40-42m

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

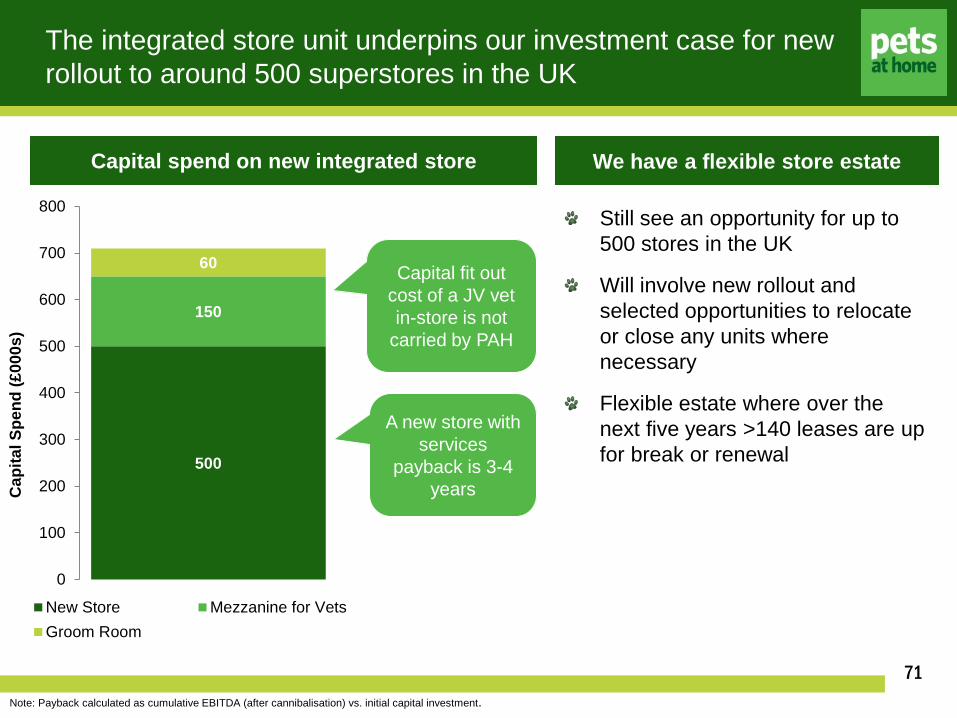

The integrated store unit underpins our investment case for new rollout to around 500 superstores in the UK

Retail

71

Capital fit out cost of a JV vet in-store is not

carried by PAH

A new store with services

payback is 3-4 years

500

150

60

0

100

200

300

400

500

600

700

800

Cap

ital S

pend

(£00

0s)

New Store Mezzanine for VetsGroom Room

Note: Payback calculated as cumulative EBITDA (after cannibalisation) vs. initial capital investment.

Capital spend on new integrated store We have a flexible store estate

Still see an opportunity for up to 500 stores in the UK

Will involve new rollout and selected opportunities to relocate or close any units where necessary

Flexible estate where over the next five years >140 leases are up for break or renewal

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

New integrated store and services rollout meets strict criteria A case study: Prestwich

72

Store Prestwich

Opened February 2016

Catchment 30,000 (Prestwich); 190,000 (Bury); 2,800,000 (Greater Manchester)

Store Size 8,000 square feet (gross) of which 2,000 of services on mezzanine & 5,000 square feet of retail

Cannibalisation Average 6% impact on 2 surrounding stores

Estimated payback period 4 years (but trading ahead)

Services Vets, Groomer, and more

Omnichannel sales participation 4%

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

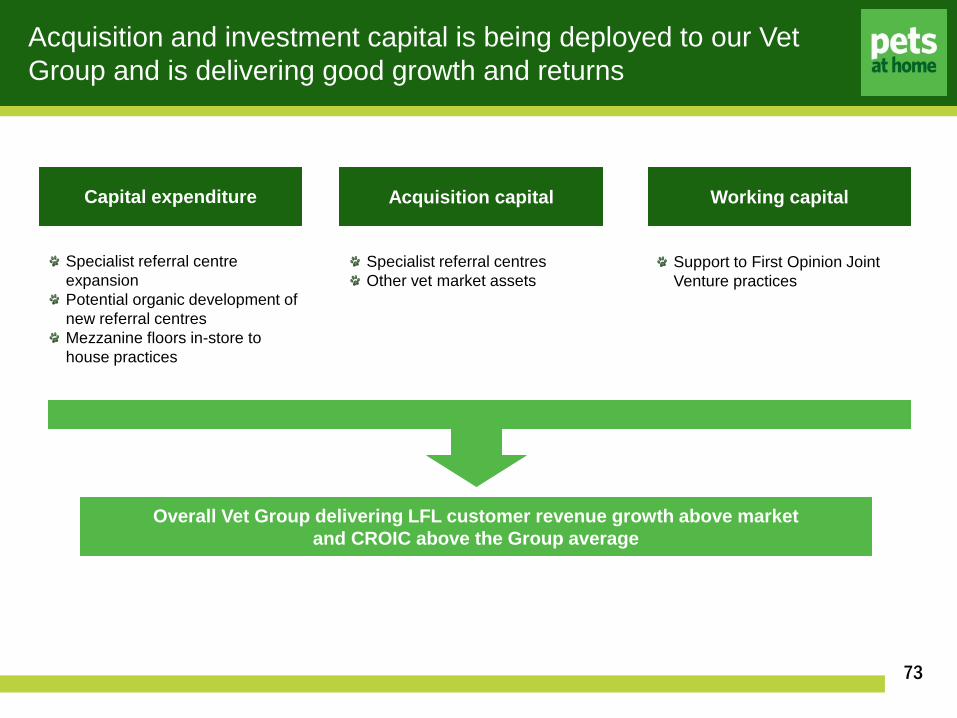

Acquisition and investment capital is being deployed to our Vet Group and is delivering good growth and returns

73

Capital expenditure Acquisition capital Working capital

Overall Vet Group delivering LFL customer revenue growth above market and CROIC above the Group average

Specialist referral centre expansion Potential organic development of new referral centres Mezzanine floors in-store to house practices

Specialist referral centres Other vet market assets

Support to First Opinion Joint Venture practices

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our priorities for use of cash remain focused on growth opportunities

Strong balance sheet Leverage policy up to 1.5x ND:EBITDA, extending up to c1.75x for appropriate acquisitions

Organic investment Ongoing programme currently focused on rollout & omnichannel strategies

Progressive dividend Ordinary dividend policy around 50% of earnings

Invest for growth Disciplined bolt-ons or investment in-line with strategy, aim to deliver returns ahead of our WACC1

Further shareholder returns Surplus FCF returned

74 1. Weighted Average Cost of Capital

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Summary and outlook

Ian Kellett Group CEO

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our focus: neutralising competitors and leveraging the unique attributes of Pets at Home to retain long term customer loyalty

76

Our strategic priorities

Become our customers’ lifetime pet partner - not just a pet shop

Deliver better value – remove price as a barrier to visit

Develop our omnichannel capabilities further and deliver the type of convenience that customers want

Maximise the Vet Group growth opportunities

Where we can still get better

Leveraging our integrated offer of product and services to customers

Using our pet and customer data to its full advantage

Giving our customers access to more advice and services, both offline and online

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

FY20 onwards Services maturity benefits evident

FY19 Transition to positive Group profit growth

Financial outlook: a three year transition to lay the foundations for future growth and realise Services maturity benefits

77

FY18 Reposition the Merchandise

business

All financial guidance reconfirmed

Price investment on track

Operational cost savings delivery H2 weighted

Increased working capital support for vet practice growth vs FY17 – overall Group working capital guidance for FY18 remains c£5m outflow

Lower rollout of grooming salons expected at 20-30 practices

On track to deliver FY in line with market expectations

Through the majority of price repositioning

Annualisation of FY18 investment

Potential for further investment in selected areas

Targeting Merchandise LFL above market levels and taking share

Vet Group delivering ongoing high profit growth

Continued operational cost savings action

Continued above market growth in Merchandise

Group operating margin expansion evident and supported by Vet Group maturation

Group profit growth at high single digit levels

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Questions?

78

Attractive long term growth market

1

Strong position as market leader in key growth segments

2

Only integrated omnichannel & services provider

3

Structural and embedded growth in vet business

4

Cash generative with clear capital allocation framework

5

Longstanding and committed management team

6

Pets at Home Investment Case

Related Documents

![Interim Results FY18 28th - Pets at Home Group plc · [xxx] nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx 161 [xxx]](https://static.cupdf.com/doc/110x72/5ecedd60c06374728112dfa4/interim-results-fy18-28th-pets-at-home-group-plc-xxx-nemo2014presentationsanalyst.jpg)

![Pets At Home Vets Group - Pets at Home Group plc...[xxx] nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx 161 [xxx] [xxx]](https://static.cupdf.com/doc/110x72/5f0ca92f7e708231d43682a7/pets-at-home-vets-group-pets-at-home-group-plc-xxx-nemo2014presentationsanalyst.jpg)