Investment Basics Clench Fraud Trust Investment Workshop October 24, 2011 Jeff Frketich, CFA

Investment Basics Clench Fraud Trust Investment Workshop October 24, 2011 Jeff Frketich, CFA.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Investment Basics

Clench Fraud Trust

Investment WorkshopOctober 24, 2011

Jeff Frketich, CFA

2

Topics

Risk and Return Fixed income (bonds) Equities (stocks) Asset Mix (how you combine stocks and bonds) Diversification

3

Risk and Return

4

Risk And Return In financial markets you get paid a Return for taking a Risk, and every

investment contains some risk The two most common definitions or risk are

the potential of permanent loss risk of borrower not paying back interest or principal risk of company not paying dividends or the value of company’s

shares declining

the volatility of day to day changes in the market value of investments

how much and how often does the value of our investment change, for better or worse

Fixed income (bonds and short-term money market investments) are typically less risky than equities

5

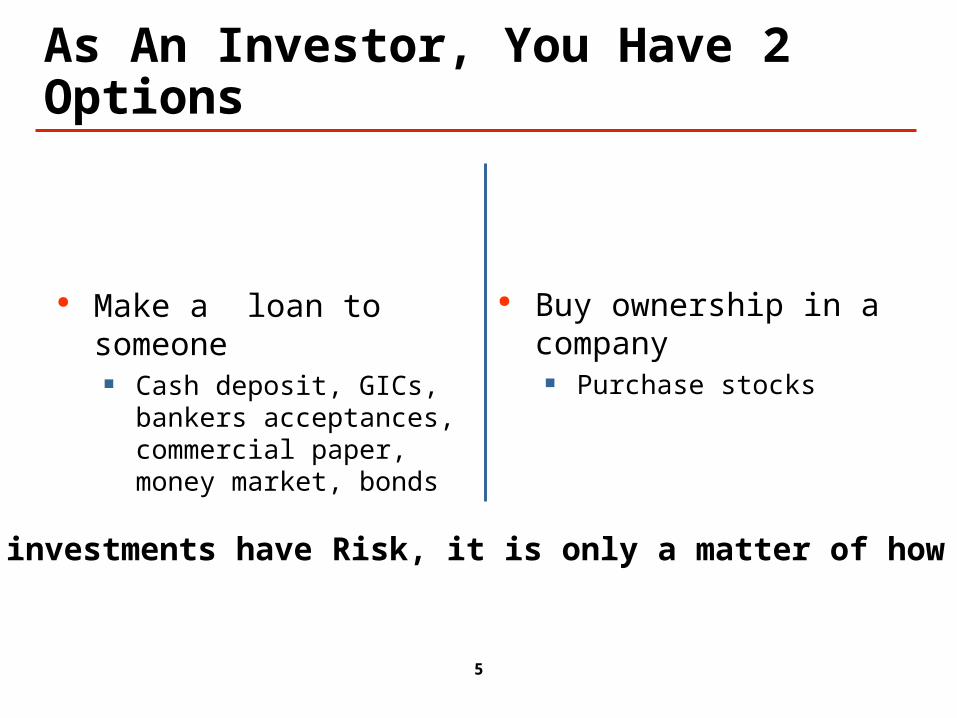

As An Investor, You Have 2 Options

Make a loan to someone Cash deposit, GICs,

bankers acceptances, commercial paper, money market, bonds

Buy ownership in a company

Purchase stocks

All investments have Risk, it is only a matter of how much

6

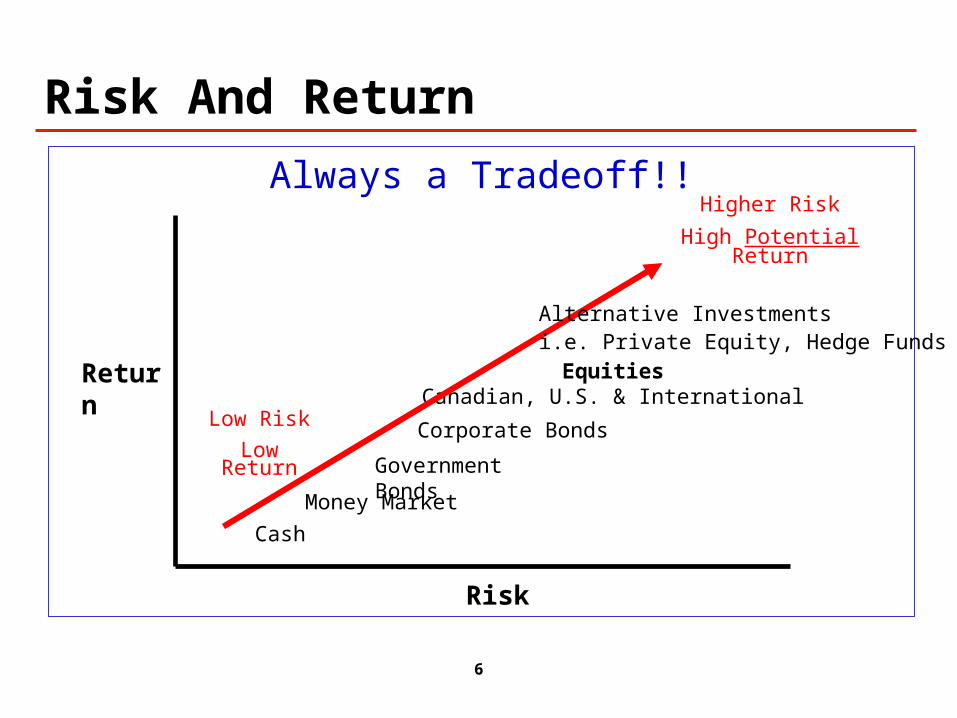

Risk And Return

Always a Tradeoff!!

Risk

Return

Low Risk

Low Return

Higher Risk

High Potential Return

Cash

Money Market

Government Bonds

Corporate Bonds

EquitiesCanadian, U.S. & International

Alternative Investmentsi.e. Private Equity, Hedge Funds

7

Fixed Income Securities (Bonds)

8

What Are Fixed Income Securities?

They pay a fixed amount of income to the owner produce a steady income stream that you can use to budget

Fixed income securities have a limited life at some point the security matures and the borrower pays back

your principal

Stocks do not ‘mature’

they exist as long as the company exists

9

Short Term Fixed Income Securities

Examples of short-term (usually less than one year) fixed income include: GICs

short-term borrowing by banks Treasury Bills

short-term borrowing by Federal and Provincial Governments

Bankers Acceptances and Commercial Paper short-term borrowing by corporations

10

Short Term Fixed Income Securities

Examples of short-term (usually less than one year) fixed income include: Money Market

a pool of treasury bills, bankers acceptances, commercial paper, short term bonds, all with a very short term to maturity

11

Long-Term Fixed Income Securities

Examples of long-term fixed income include:

Bonds long-term borrowing by governments (federal, provincial and

municipal) and corporations Mortgage and Asset Backed Securities

pools of mortgages that are packaged together and sold just like bonds

12

Bonds

When talking about fixed income securities, we are usually talking about bonds

Bonds are a contract that entitle the owner to regular interest payments and the return of their principal (original amount of the loan) when the bond matures

Bonds are bought and sold in the open market, like stocks

13

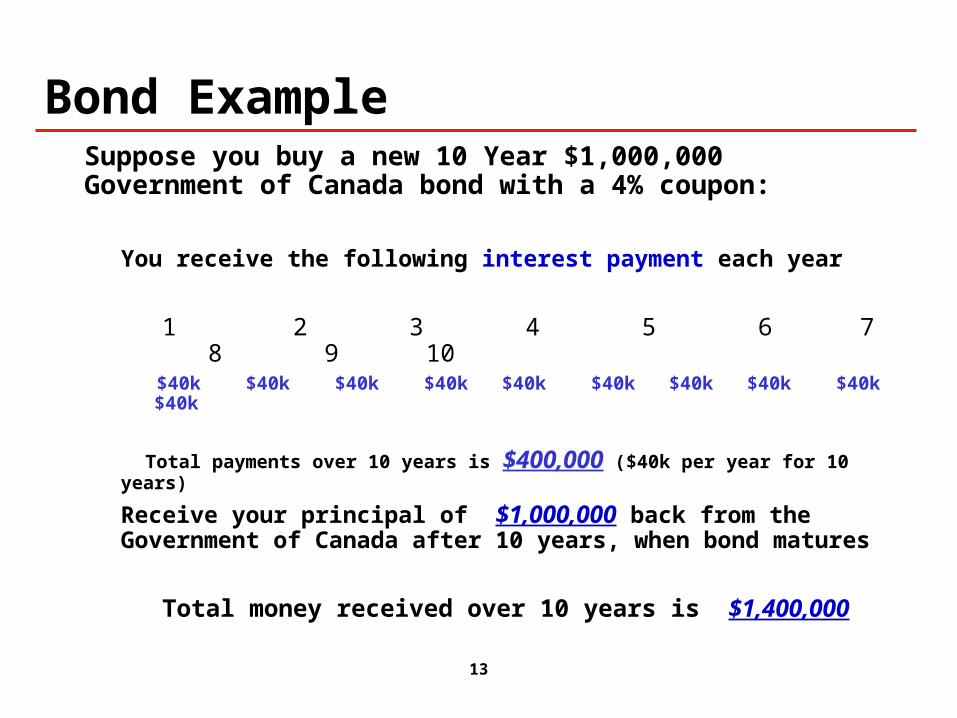

Bond Example

You receive the following interest payment each year

1 2 3 4 5 6 7 8 9 10 $40k $40k $40k $40k $40k $40k $40k $40k $40k $40k

Total payments over 10 years is $400,000 ($40k per year for 10 years)

Receive your principal of $1,000,000 back from the Government of Canada after 10 years, when bond matures

Total money received over 10 years is $1,400,000

Suppose you buy a new 10 Year $1,000,000 Government of Canada bond with a 4% coupon:

14

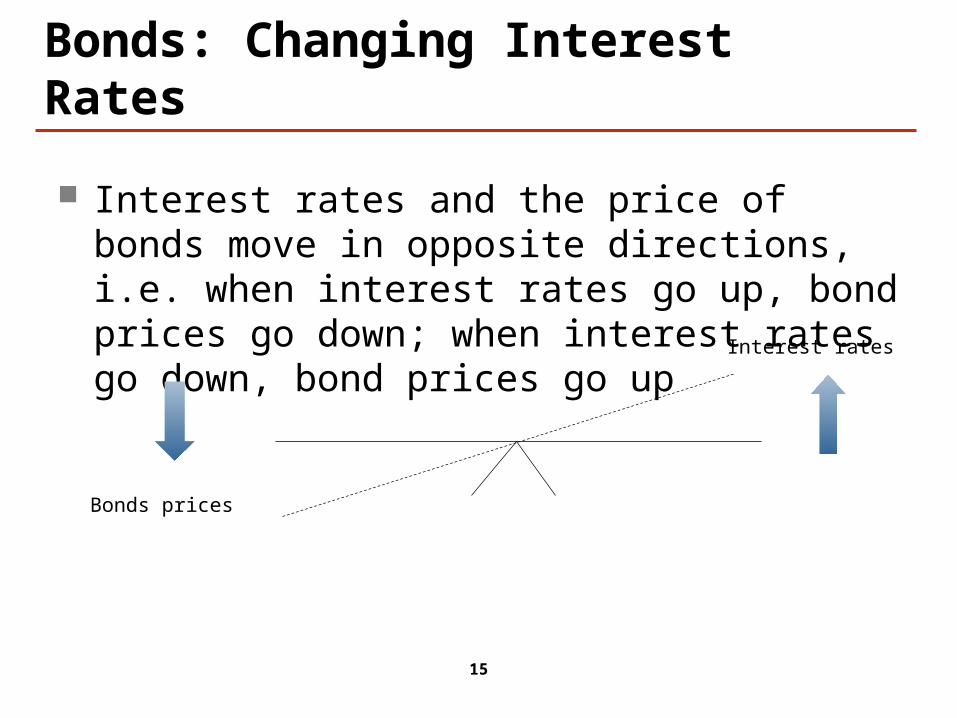

Bonds: Changing Interest Rates Interest rates affect the price of most fixed

income securities, especially bonds

Interest rates (yields) go up and down, depending on what is happening in the economy; generally the better the economy, the higher the interest rate

15

Bonds: Changing Interest Rates

Interest rates and the price of bonds move in opposite directions, i.e. when interest rates go up, bond prices go down; when interest rates go down, bond prices go up Interest rates

Bonds prices

16

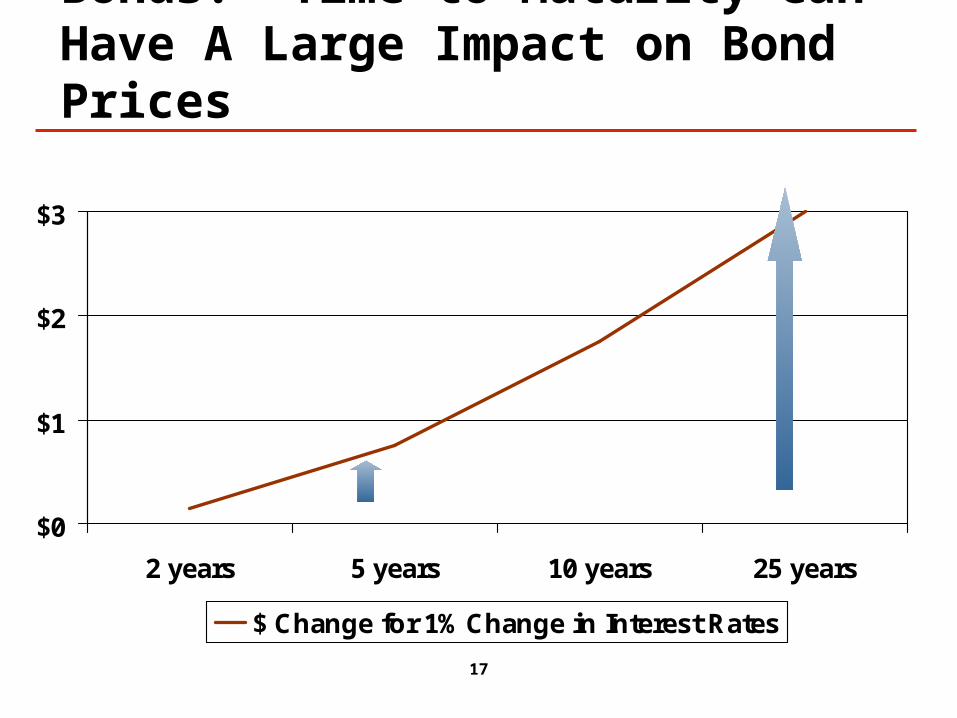

Bonds: Time to Maturity Can Have A Large Impact on Bond Prices

The longer the time to maturity, the more volatile the bond price for a given change in interest rates

a change in interest rates of 1% will not affect the price of a bond that matures tomorrow.

however, a 1% change in interest rates will have a much larger effect on a bond that matures in 10 years

17

Bonds: Time to Maturity Can Have A Large Impact on Bond Prices

$0

$1

$2

$3

2 years 5 years 10 years 25 years

$ Change for 1% Change in Interest Rates

18

Credit Rating Agencies How do you know which bonds to buy and which to

avoid?

Your investment counsellor starts the process by reviewing what independent credit rating agencies say about the bond

Two examples of credit rating agencies are Dominion Bond Rating Service and Standard & Poors

19

Credit Rating Agencies DBRS and S&P look at things like cash flows, earnings

growth, the firm’s competitive position and future capital expenditures.

The agencies come up with a grade representing the credit quality of the borrower.

The better the credit quality, the higher the credit rating; the higher the rating, the lower the interest rate the borrower must pay on the debt.

20

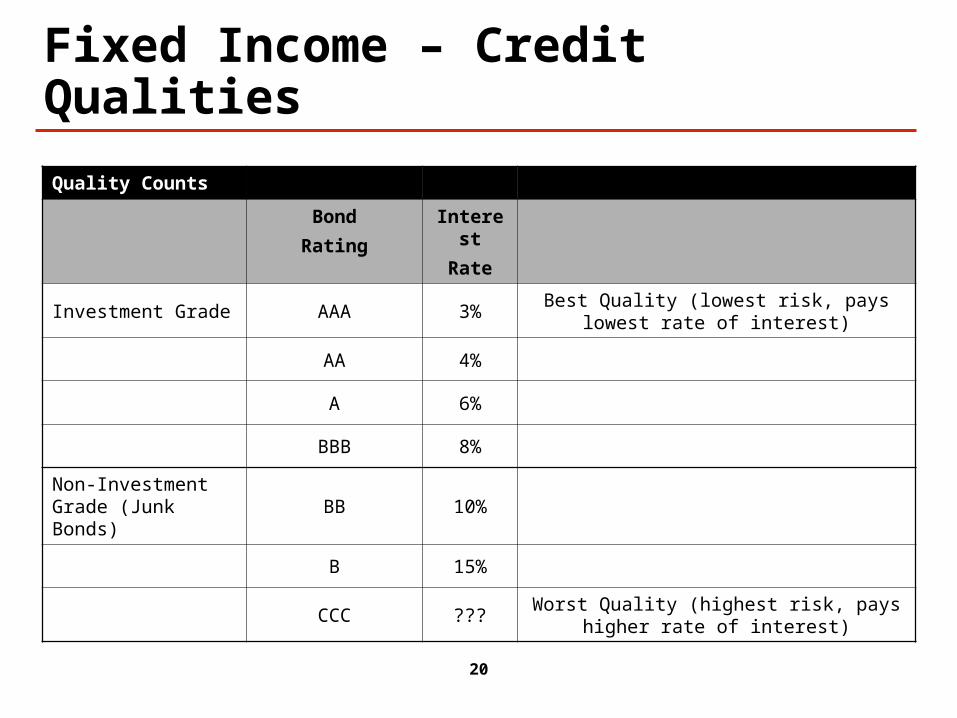

Fixed Income – Credit Qualities

Quality Counts

Bond

Rating

Interest

Rate

Investment Grade AAA 3%Best Quality (lowest risk, pays lowest rate of

interest)

AA 4%

A 6%

BBB 8%

Non-Investment Grade (Junk Bonds)

BB 10%

B 15%

CCC ???Worst Quality (highest risk, pays higher rate

of interest)

21

Equities

(Stocks)

(Shares of Companies)

22

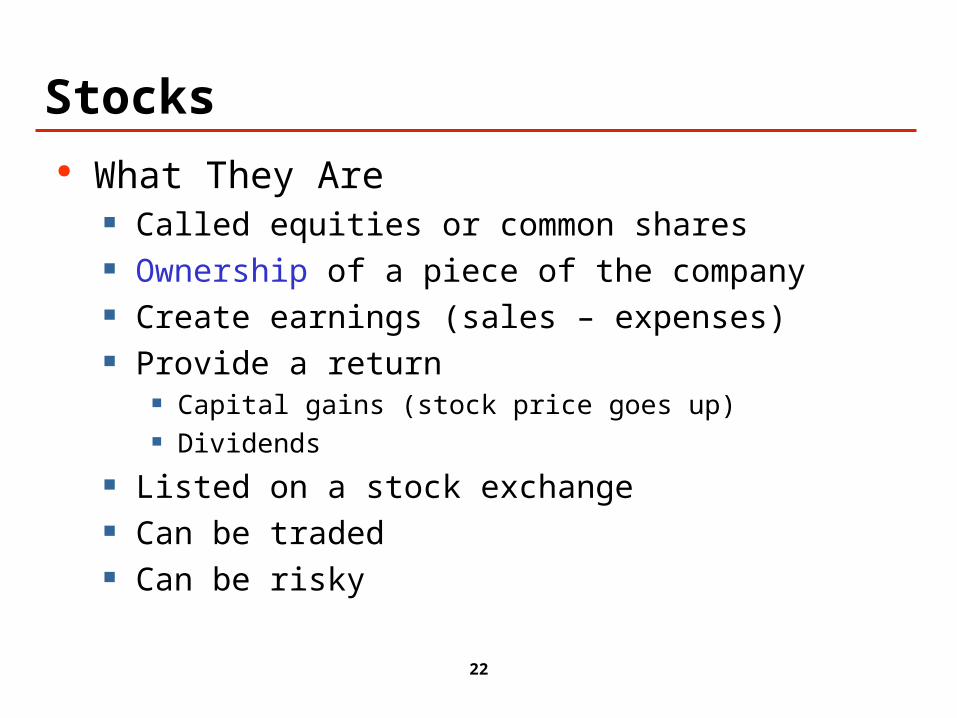

Stocks What They Are

Called equities or common shares Ownership of a piece of the company Create earnings (sales – expenses) Provide a return

Capital gains (stock price goes up) Dividends

Listed on a stock exchange Can be traded Can be risky

23

Stocks

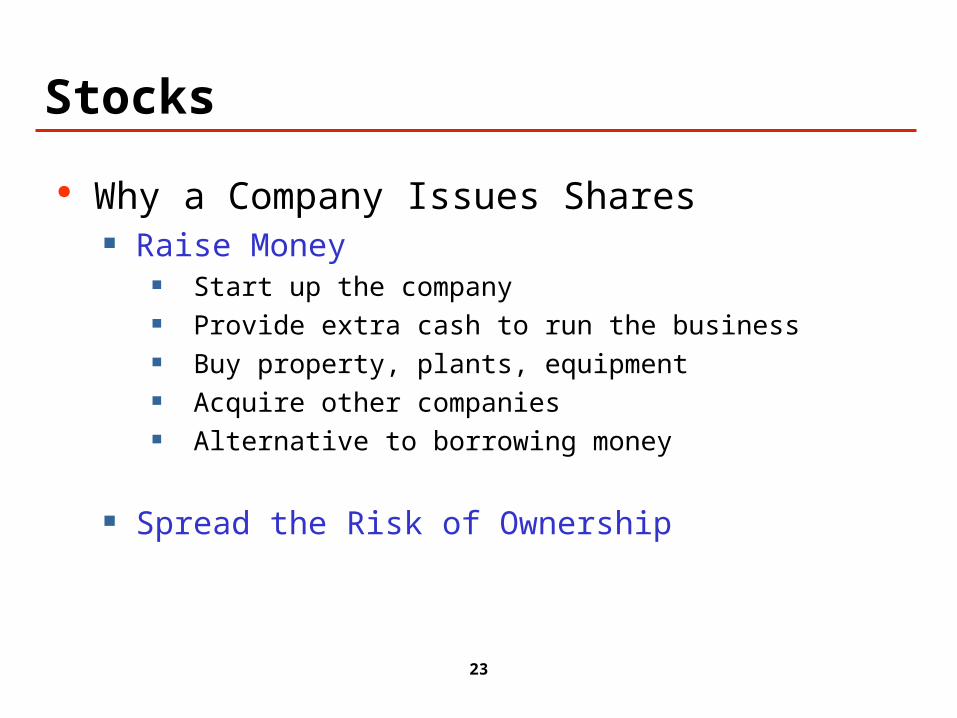

Why a Company Issues Shares Raise Money

Start up the company Provide extra cash to run the business Buy property, plants, equipment Acquire other companies Alternative to borrowing money

Spread the Risk of Ownership

24

Stocks

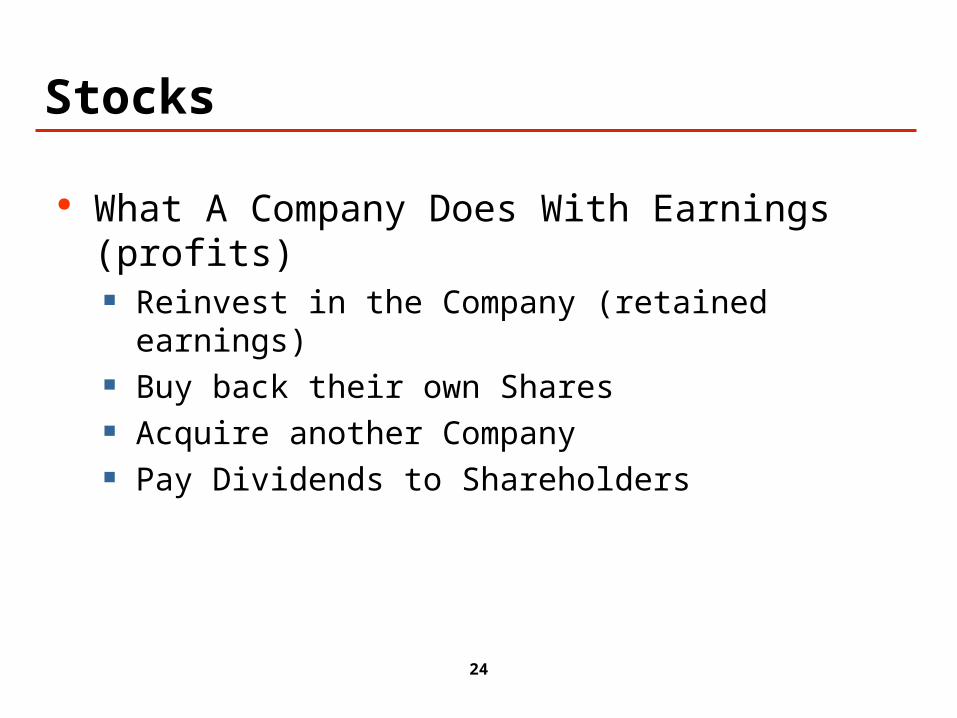

What A Company Does With Earnings (profits) Reinvest in the Company (retained earnings) Buy back their own Shares Acquire another Company Pay Dividends to Shareholders

25

Stocks

Why Investors Buy Them Investors – First Nations

Provide long term Growth to a Portfolio Typically buy to hold for longer periods than

traders/speculators For Total Return

Capital gains Dividend income

Traders/Speculators – NOT First Nations Make quick profits from an increase in price Capital Gains

26

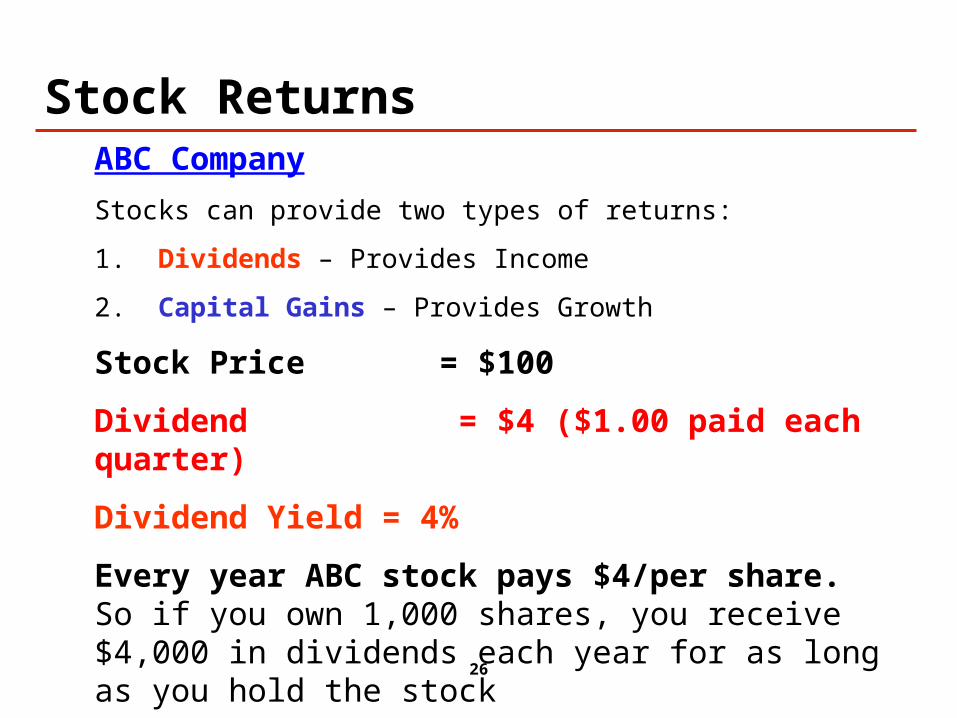

ABC Company

Stocks can provide two types of returns:

1. Dividends – Provides Income

2. Capital Gains – Provides Growth

Stock Price = $100

Dividend = $4 ($1.00 paid each quarter)

Dividend Yield = 4%

Every year ABC stock pays $4/per share. So if you own 1,000 shares, you receive $4,000 in dividends each year for as long as you hold the stock

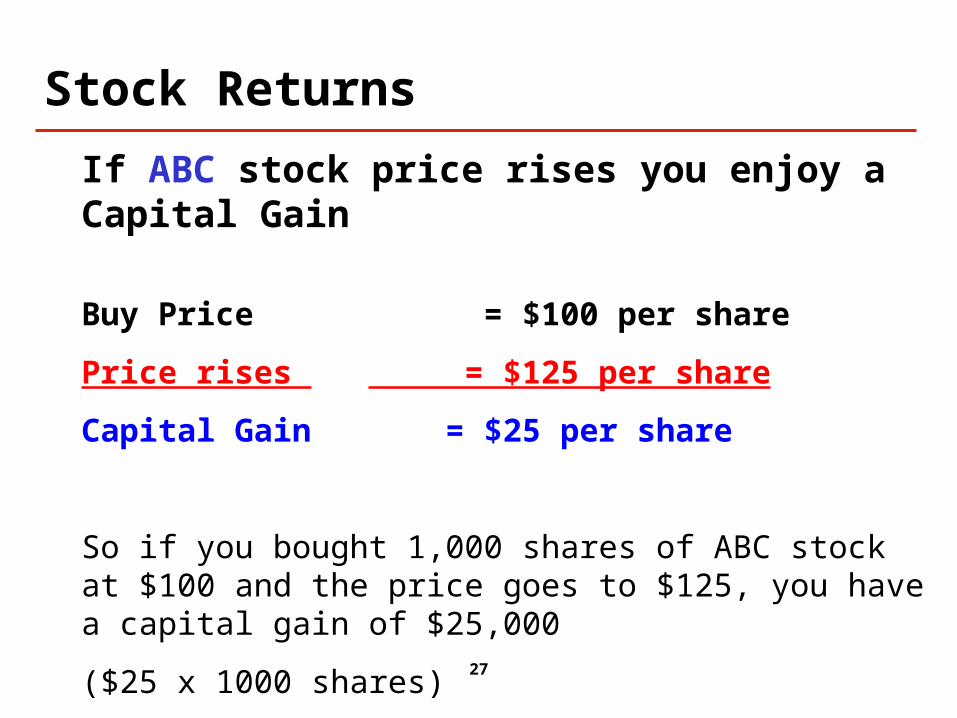

Stock Returns

27

If ABC stock price rises you enjoy a Capital Gain

Buy Price = $100 per share

Price rises = $125 per share

Capital Gain = $25 per share

So if you bought 1,000 shares of ABC stock at $100 and the price goes to $125, you have a capital gain of $25,000

($25 x 1000 shares)

Stock Returns

28

Stocks What Makes Them Change In Price

Earnings or Expected Earnings Company

Business model Competitive position Revenues and Expenses

Industry Anything affecting the particular industry or business of the

company Economy

Affects people’s ability to by Company’s products Consumer and Business spending Employment / Unemployment Interest Rates

29

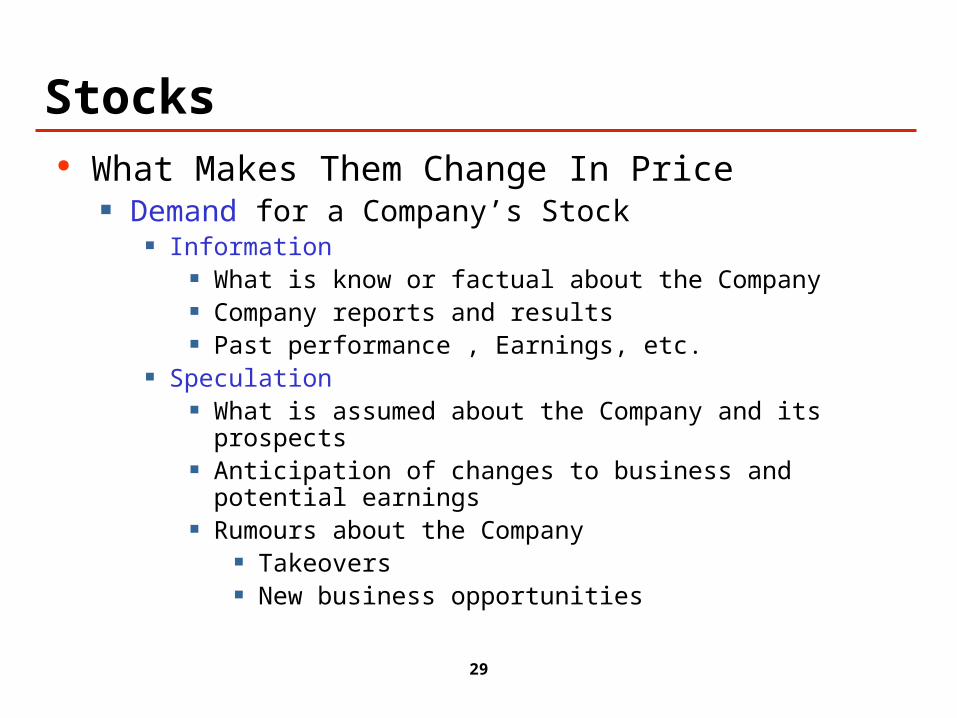

Stocks What Makes Them Change In Price

Demand for a Company’s Stock Information

What is know or factual about the Company Company reports and results Past performance , Earnings, etc.

Speculation What is assumed about the Company and its prospects Anticipation of changes to business and potential

earnings Rumours about the Company

Takeovers New business opportunities

30

Asset Mix: Combining Stocks and Bonds

31

Asset Mix

Asset mix is another way of saying how much do you have in stocks and how much do you have in bonds

Each Trust has its own unique return requirements and risk tolerance

Asset mix will determine the risk/return levels in your trust portfolio

generally, the more stocks you have the more risk you take

32

Asset Mix

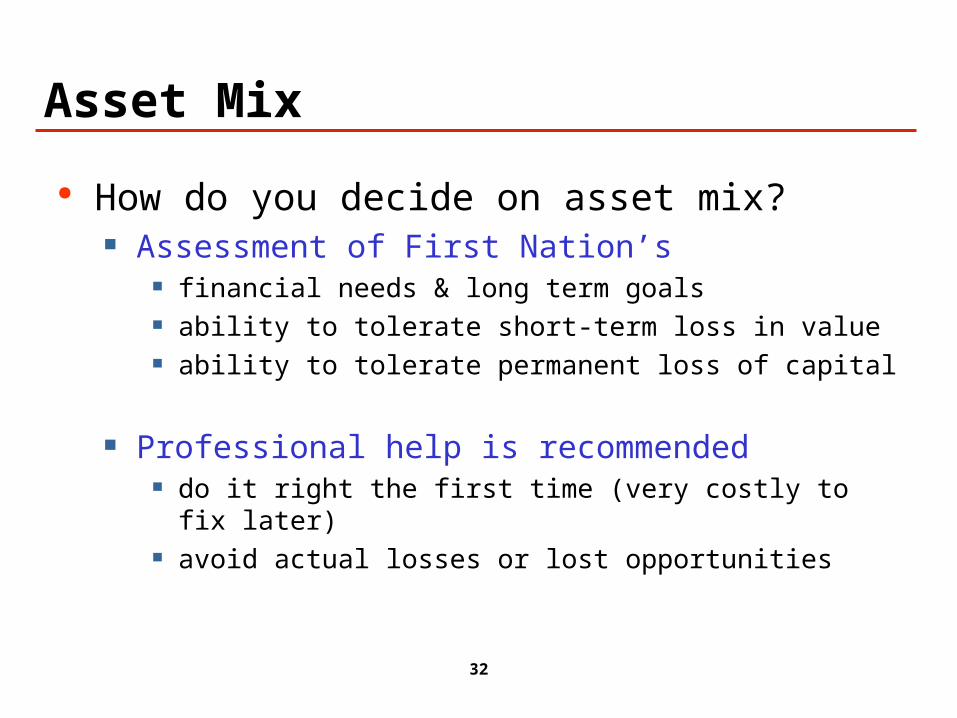

How do you decide on asset mix? Assessment of First Nation’s

financial needs & long term goals ability to tolerate short-term loss in value ability to tolerate permanent loss of capital

Professional help is recommended do it right the first time (very costly to fix later) avoid actual losses or lost opportunities

33

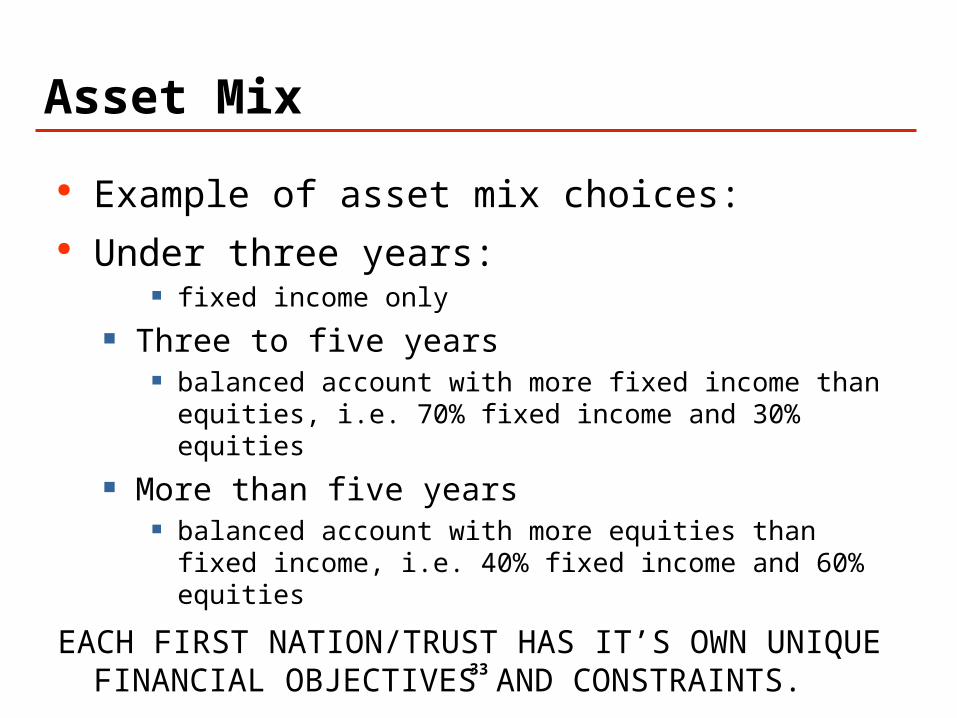

Asset Mix

Example of asset mix choices: Under three years:

fixed income only Three to five years

balanced account with more fixed income than equities, i.e. 70% fixed income and 30% equities

More than five years balanced account with more equities than fixed income, i.e.

40% fixed income and 60% equities

EACH FIRST NATION/TRUST HAS IT’S OWN UNIQUE FINANCIAL OBJECTIVES AND CONSTRAINTS.

34

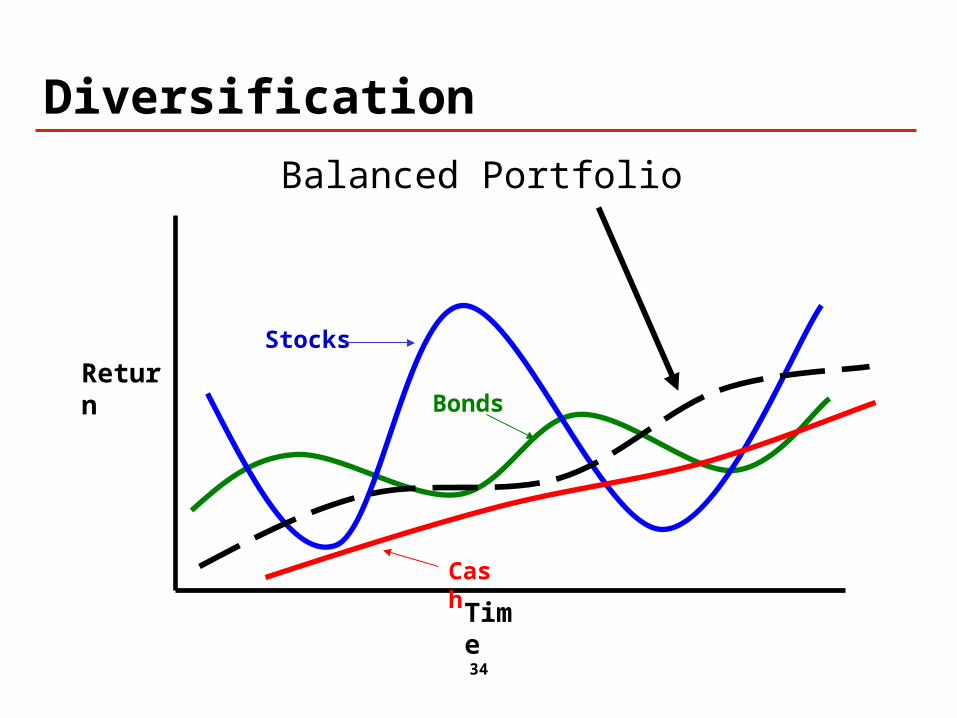

Diversification

Balanced Portfolio

Time

ReturnStocks

Bonds

Cash

Related Documents