Introduction to Financial Engineering Aashish Dhakal Week 6: Convertible Bonds

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Introduction to Financial Engineering

Aashish Dhakal

Week 6: Convertible Bonds

Convertible Bonds:Convertible Bonds are those Bonds that give holder the right (but not obligation) to convert the bonds into equity shares (normally) of the issuing company, under specified terms and conditions.

A convertible bond is an Hybrid instrument that has both the option Fixed Income (Bond) and equity (Common Share) characteristic.

It has set maturity date.

Just like any regular bond it has set coupon rate and Pay the holder an annual interest income.

Typically, the bond is convertible into common shares of the issuing corporation, but some may offer an option of converting it into other securities issued by the corporation.

Thus the convertible bond will pay regular income through the bond coupon payment PLUS they offer the ability to participate in capital appreciation through the potential conversion into common shares.

HOW Converted? Conversion Formula

Lets look at some features with example.

When a convertible bond is issued, in addition to the Maturity Date , Coupon Rate, and other bond features, IT WILL HAVE A STATED CONVERSION FORMULA.

This Formulae will typically stipulate the number of common shares the bond can be converted into and the ending date for the conversion privilege.

For ex: a conversion formulae may be written as, “Convertible until April 15, 2015 into 81 share per Rs 10000 of bond face value, being conversion price per share Rs 123.45 per share.” This conversion price is also sometimes referred as the strike price.

CR

CP

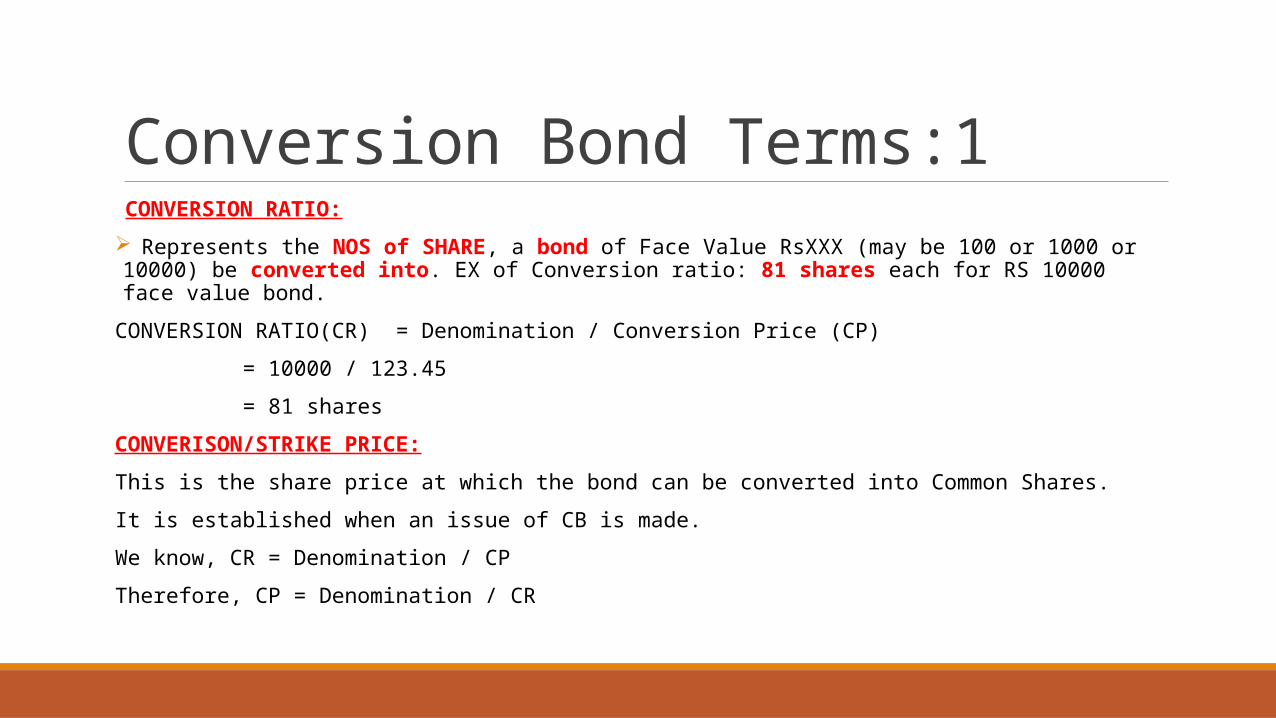

Conversion Bond Terms:1 CONVERSION RATIO:

Represents the NOS of SHARE, a bond of Face Value RsXXX (may be 100 or 1000 or 10000) be converted into. EX of Conversion ratio: 81 shares each for RS 10000 face value bond.

CONVERSION RATIO(CR) = Denomination / Conversion Price (CP)

= 10000 / 123.45

= 81 shares

CONVERISON/STRIKE PRICE:

This is the share price at which the bond can be converted into Common Shares.

It is established when an issue of CB is made.

We know, CR = Denomination / CP

Therefore, CP = Denomination / CR

When an Investor start an incentive to adopt the conversion option?SIMPLE : When the Market Rate of Common Share is GREATER THAN Conversion Price.

If the company shares are currently trading at or below conversion price, there is no incentive for the bond holder to convert the bond into shares. As a result the bond holder will trade the bond just like any other bond and will hang onto the bond and collect the interest payment.

As soon as the Common shares begin to trade above the conversion price, then the bondholder will have an increasing incentive to convert their bond into shares.

Situation Incentive Action

MP < CP NIL Go as Normal Bond

MP = CP NIL Go as Normal Bond

MP > CP High Convert

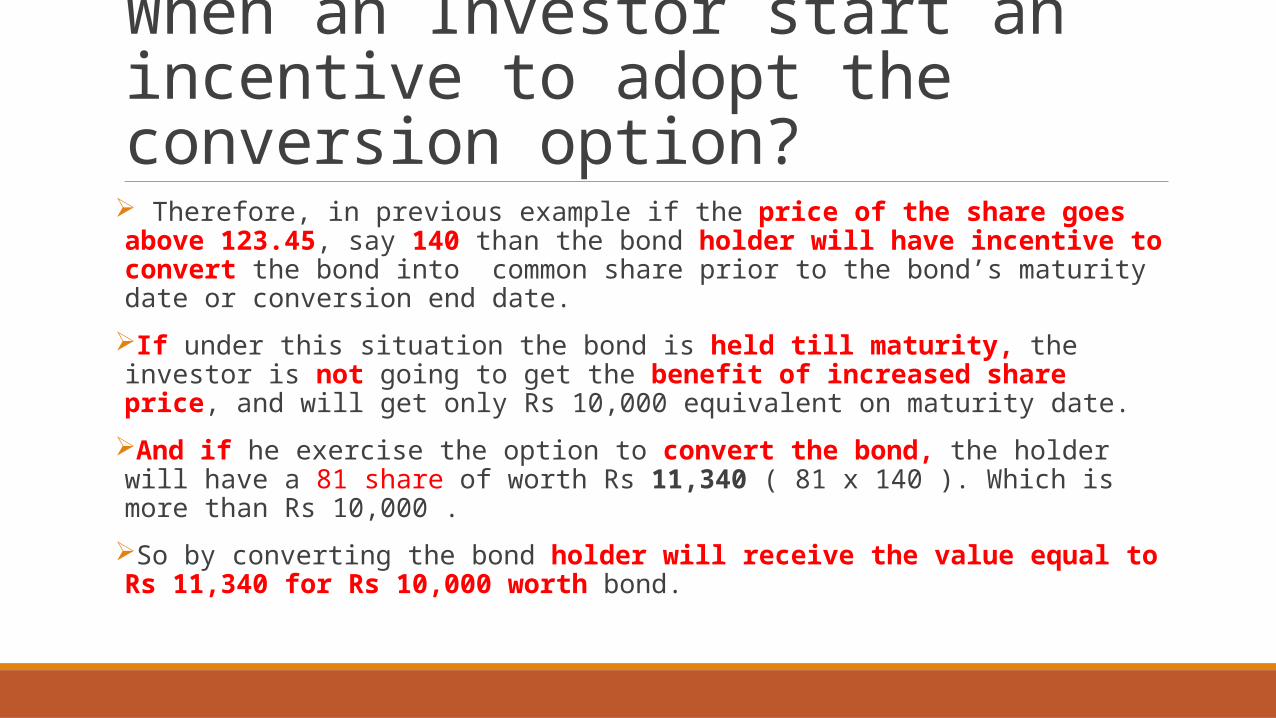

When an Investor start an incentive to adopt the conversion option? Therefore, in previous example if the price of the share goes above 123.45, say 140 than the bond holder will have incentive to convert the bond into common share prior to the bond’s maturity date or conversion end date.

If under this situation the bond is held till maturity, the investor is not going to get the benefit of increased share price, and will get only Rs 10,000 equivalent on maturity date.

And if he exercise the option to convert the bond, the holder will have a 81 share of worth Rs 11,340 ( 81 x 140 ). Which is more than Rs 10,000 .

So by converting the bond holder will receive the value equal to Rs 11,340 for Rs 10,000 worth bond.

CB Trading In The Money:When the common share market price trades above the conversion price, I.E. MP > CP

the bond market price will be priced as if it is to be converted into common shares.

At This Point, the Bond is said to be Trading In The Money.

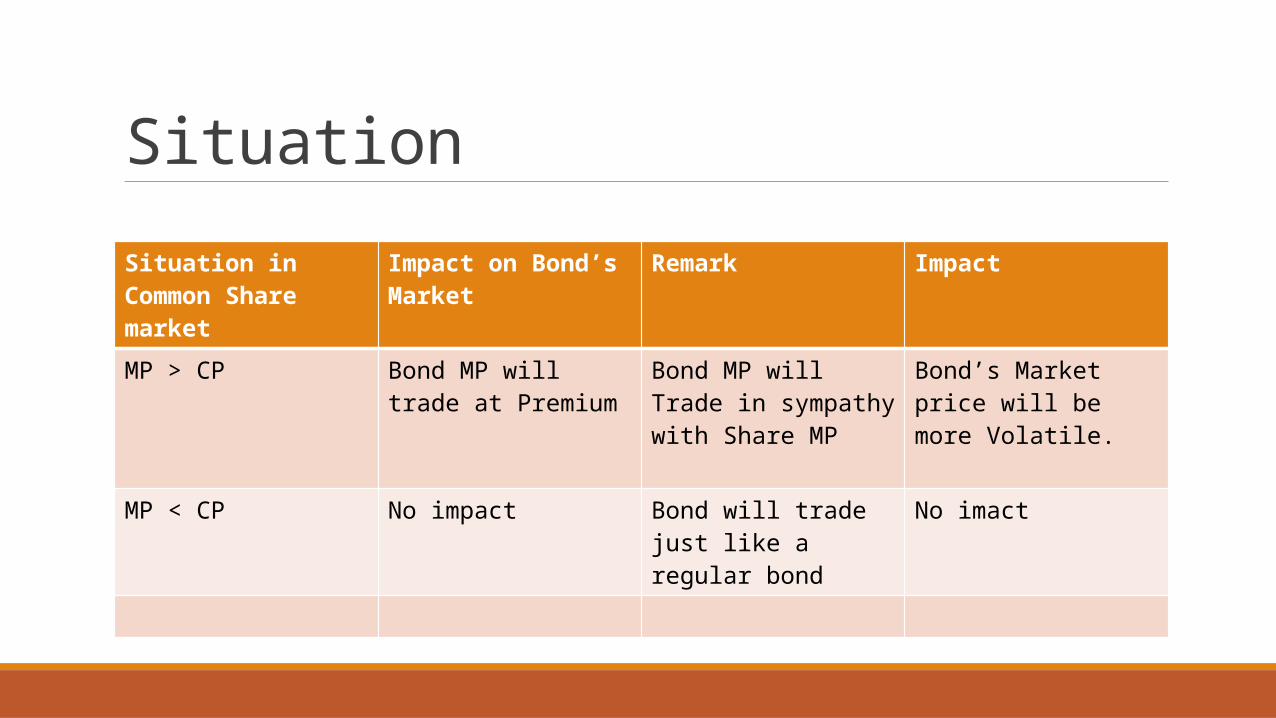

Situation

Situation in Common Share market

Impact on Bond’s Market

Remark Impact

MP > CP Bond MP will trade at Premium

Bond MP will Trade in sympathy with Share MP

Bond’s Market price will be more Volatile.

MP < CP No impact Bond will trade just like a regular bond

No imact

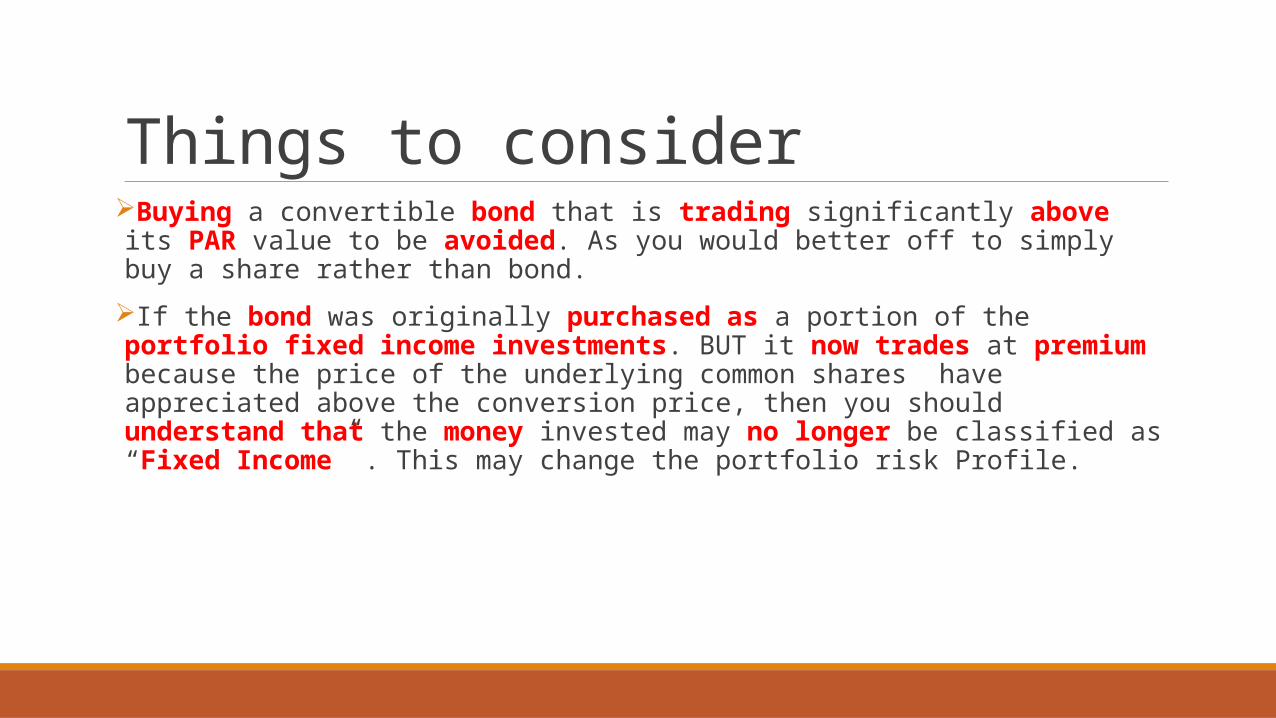

Things to considerBuying a convertible bond that is trading significantly above its PAR value to be avoided. As you would better off to simply buy a share rather than bond.

If the bond was originally purchased as a portion of the portfolio fixed income investments. BUT it now trades at premium because the price of the underlying common shares have appreciated above the conversion price, then you should understand that the money invested may no longer be classified as “Fixed Income” . This may change the portfolio risk Profile.

Conversion Bond Terms:TRADING IN THE MONEY:

A Convertible is said to be Trading In The Money, IF the MP of the common share is GREATER THAN Conversion Price.

CONVERSION PREMIUM

When convertibles are issued, the conversion price is higher (CP) than the current market value (Current MP) of the shares into which they can be converted.

CP of Share > Current MP of Share This Difference = Conversion Premium

The difference between the price of the convertible bonds (CP) and the market value of the shares into which they can be converted is called the conversion premium.

It Keeps on changing over the time, with the change in the market price of the Underlying Share.

MP of Share Increases Conversion Premium also Increases

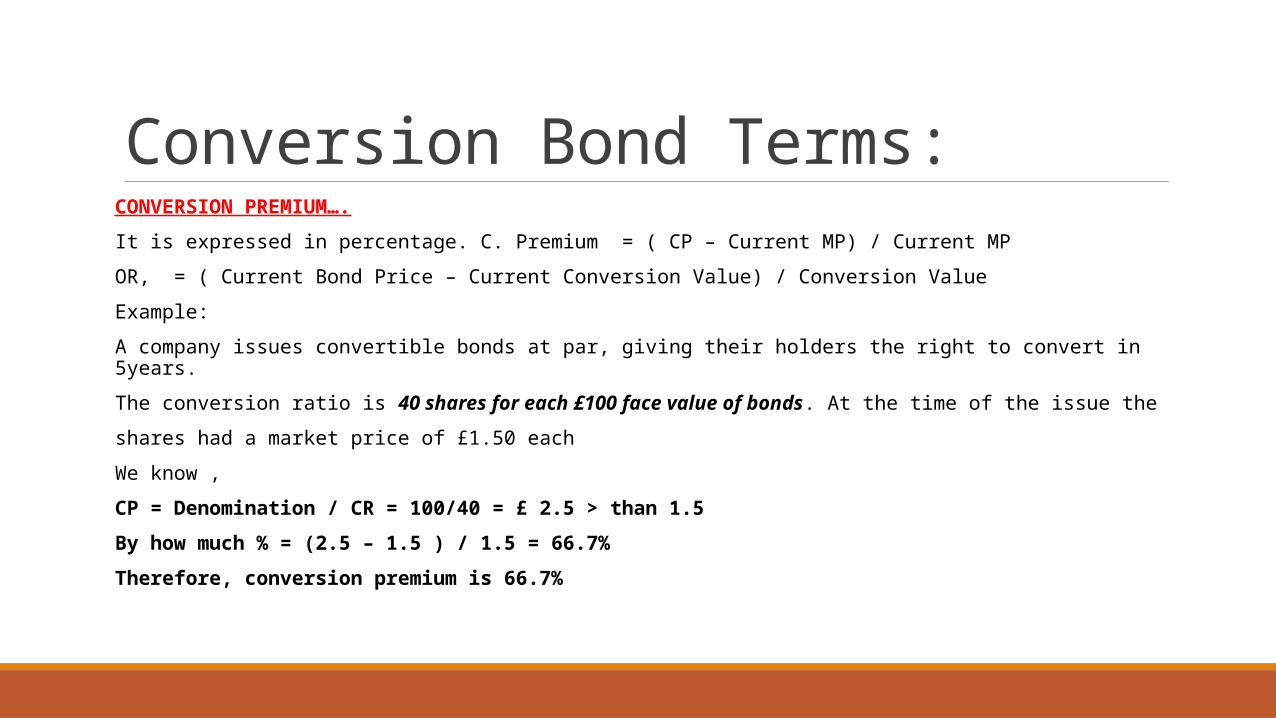

Conversion Bond Terms:CONVERSION PREMIUM….

It is expressed in percentage. C. Premium = ( CP – Current MP) / Current MP

OR, = ( Current Bond Price – Current Conversion Value) / Conversion Value

Example:

A company issues convertible bonds at par, giving their holders the right to convert in 5years.

The conversion ratio is 40 shares for each £100 face value of bonds. At the time of the issue the

shares had a market price of £1.50 each

We know ,

CP = Denomination / CR = 100/40 = £ 2.5 > than 1.5

By how much % = (2.5 – 1.5 ) / 1.5 = 66.7%

Therefore, conversion premium is 66.7%

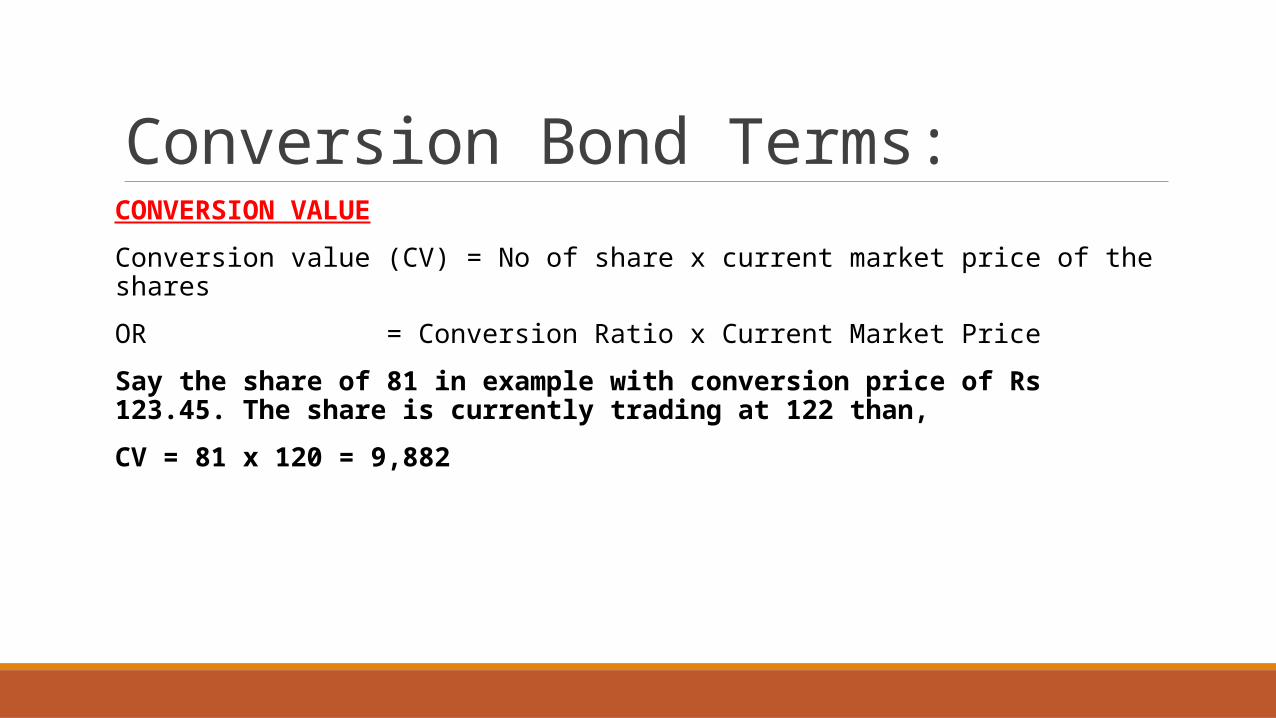

Conversion Bond Terms:CONVERSION VALUE

Conversion value (CV) = No of share x current market price of the shares

OR = Conversion Ratio x Current Market Price

Say the share of 81 in example with conversion price of Rs 123.45. The share is currently trading at 122 than,

CV = 81 x 120 = 9,882

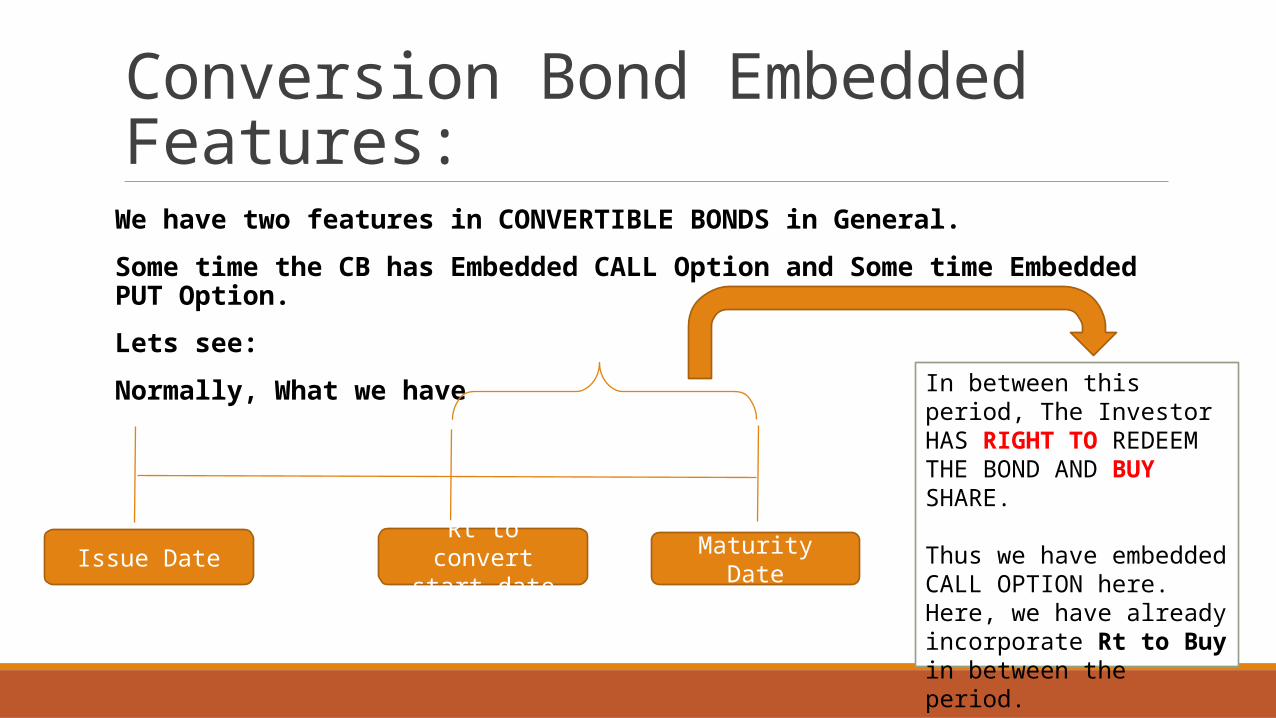

Conversion Bond Embedded Features:

We have two features in CONVERTIBLE BONDS in General.

Some time the CB has Embedded CALL Option and Some time Embedded PUT Option.

Lets see:

Normally, What we have

Issue DateRt to convert start

date Maturity Date

In between this period, The Investor HAS RIGHT TO REDEEM THE BOND AND BUY SHARE.

Thus we have embedded CALL OPTION here.Here, we have already incorporate Rt to Buy in between the period.

Conversion Bond Embedded Features:

Some time the CB has Embedded PUT Option:

Lets see:

In this case, What we have

Issue Date Maturity Date

In between this period, The Investor CAN DEMAND FOR EARLY REDEEMPTION OF THE BOND AND BUY SHARE.

Thus we have embedded PUT OPTION here WHERE BY WE HOLD RT FOR REDEMPTION ANYTIME WE LIKE.

Pricing the CBsPricing can be performed in several frameworks:

• Black & Scholes

• Binomial

• Trinomial

• Simulation

• Synthetic replication

InvestorsConventional CBs offer the same profile as a call option but they offer more as a financial instrument and this feature appeals to a wide range of potential investors:

• Some investors are interested only in bond part

• Some in equity part

• CBs can be bond one day and equity another day

The key feature of a CB that makes it a mixture of bond and equity is that the individual holding the instrument has

an option:

• To turn it into equity at any time

• Or just let it run to expiry and take the

cash

Why Corporations issue CBsBenefits in general:

If converted – issuing shares at a premium

If redeemed – issuing debt at discount

Coupons are tax deductible, dividends not

Coupons are fixed, dividends not

But what corporations are really doing using CBs is…

Raising cash on a virtual asset

Selling future volatility on their shares

Related Documents