IN T R O D UC T ION T O ECO NO M ICS

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 1/51

INTRODUCTION

TOECONOMICS

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 2/51

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 3/51

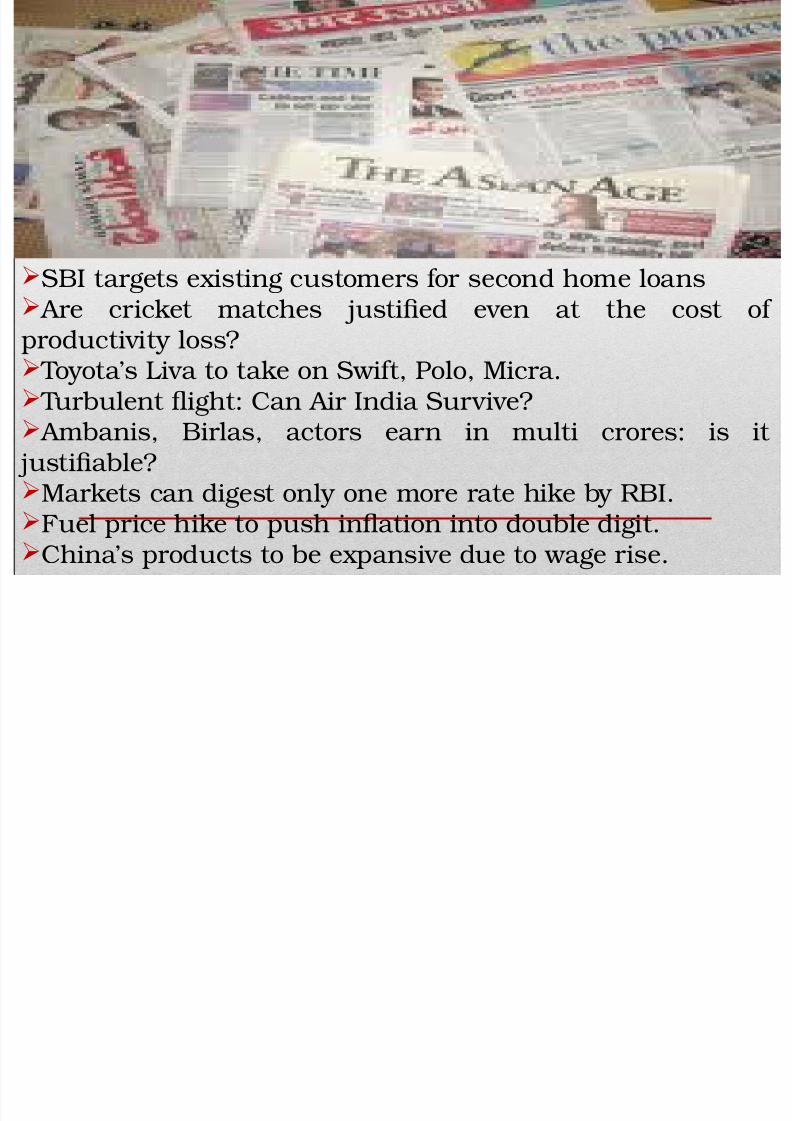

SBI targets existing customers for second home loans Are cricket matches justified even at the cost ofproductivity loss? Toyota’s Liva to take on Swift, Polo, Micra.

Turbulent flight: Can Air India Survive? Ambanis, Birlas, actors earn in multi crores: is itjustifiable?Markets can digest only one more rate hike by RBI.

Fuel price hike to push inflation into double digit.China’s products to be expansive due to wage rise.

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 4/51

Emphasis Significant Contribution

Wealth Adam Smith

Welfare Alfred Marshall

Scarcity Lionel Robbins

Growth Paul Samuelson

What is Economics?

The wordeconomy comes from a Greek word for“one who manages a household.”

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 5/51

WEALTH DEFINITION

Adam smith (1723 - 1790), Father ofEconomics

Book “An Inquiry into Nature and Causes

of Wealth of Nations” (1776)

Defined economics as the practical science

of production and distribution of wealth.

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 6/51

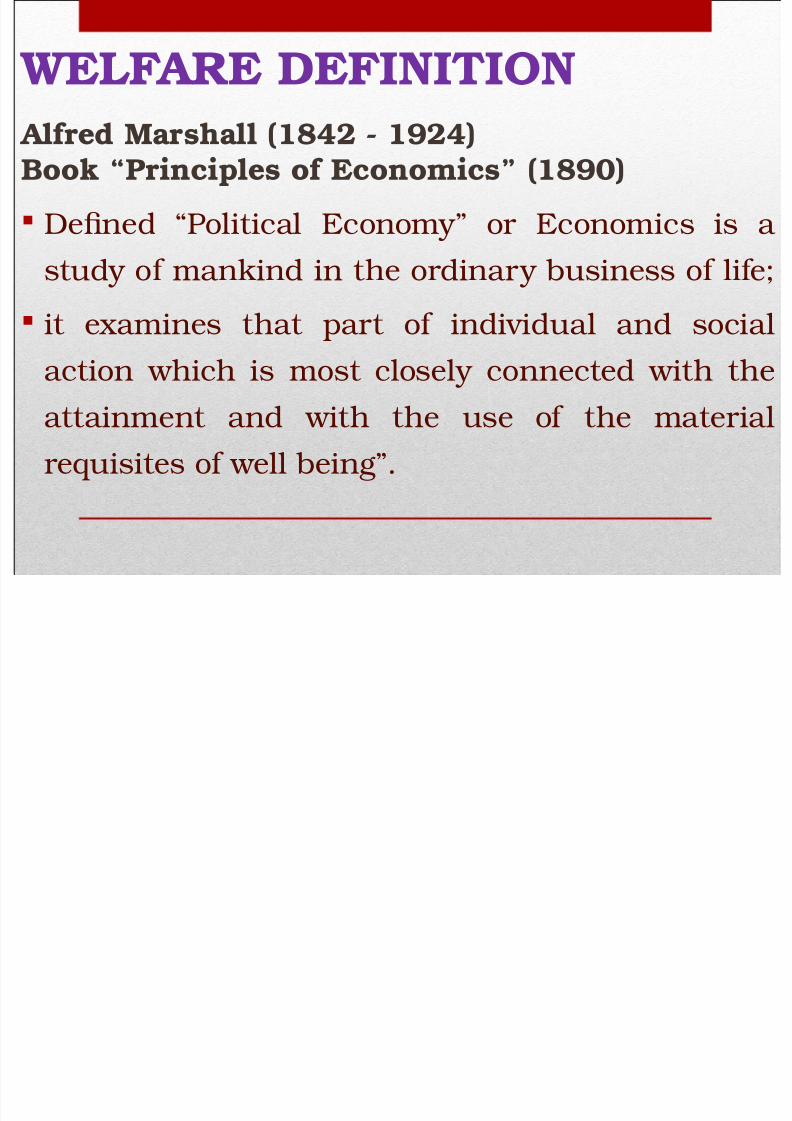

WELFARE DEFINITION

Alfred Marshall (1842 - 1924)Book “Principles of Economics” (1890)

Defined “Political Economy” or Economics is a

study of mankind in the ordinary business of life;

it examines that part of individual and social

action which is most closely connected with the

attainment and with the use of the material

requisites of well being”.

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 7/51

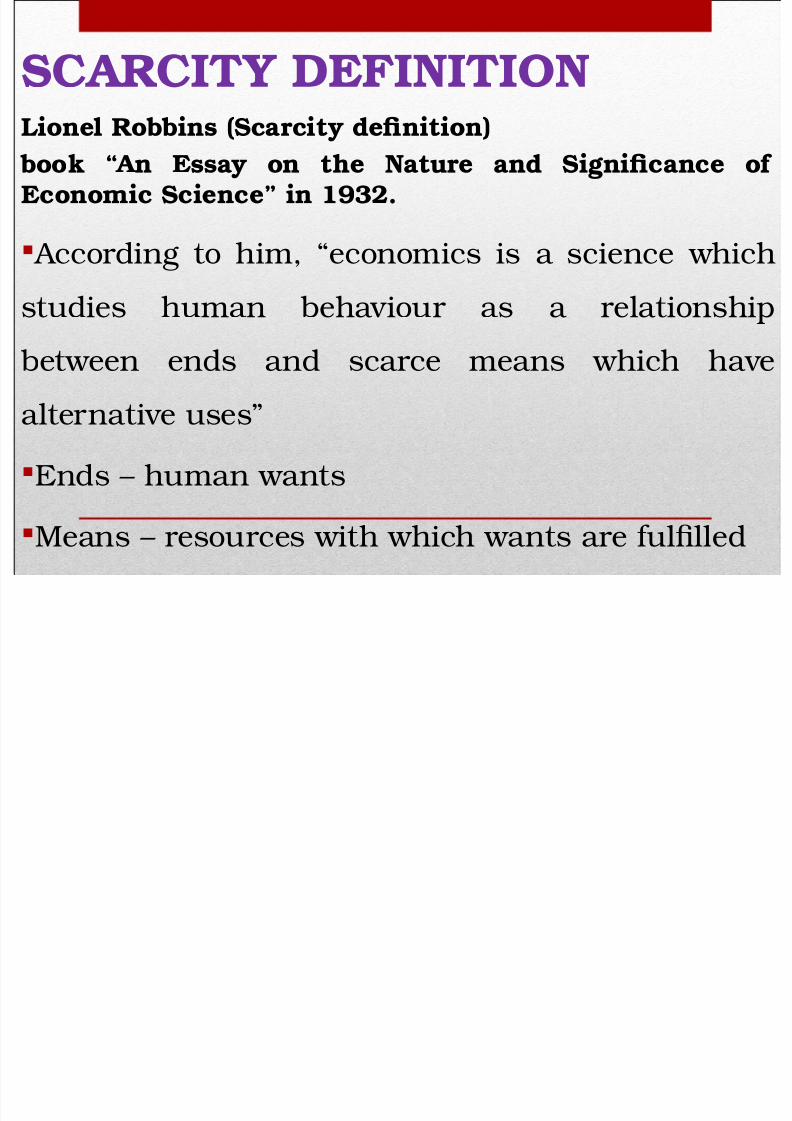

SCARCITY DEFINITION

Lionel Robbins (Scarcity definition)book “An Essay on the Nature and Significance ofEconomic Science” in 1932.

According to him, “economics is a science whichstudies human behaviour as a relationship

between ends and scarce means which have

alternative uses”

Ends – human wants

Means – resources with which wants are fulfilled

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 8/51

defined economics as “the study of how men and

society choose, with or without the use of

money, to employ scarce productive resources

which could have alternative uses, to produce

various commodities over time, and distribute

them for consumption, now and in the future

among various people and groups of society”

GROWTH DEFINITION

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 9/51

contd….. Thus economics is a social science that studies

human behaviour and institutional arrangementsin societies that influence the processes by whichrelatively scarce resources are allocated toalternative uses.

It covers the actions of individuals and groups ofindividuals in the process of producing,

exchanging and consuming of goods and servicesto achieve optimization of resource use”

social science and decision science

components of economics

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 10/51

Economics as a Social

Science

Human behavior is influenced by a matrix of

complex forcesPsychologySociology Anthropology

EconomicsPolitical ScienceReligion, ...

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 11/51

Scarcity

A situation in which the amountof something actually available

would not be sufficient to satisfythe desire for it, if it wereprovided free of charge.

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 12/51

Factors of Production

There are 4 factors that must all be

used to produce anythingNatural Resources (also referred to as“land”)

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 13/51

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 14/51

Capital – human-made resources used to

create other goods Kinds of Capital Physical Capital – Also called CapitalGoods, objects that are used to produce

other goods

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 15/51

Kinds of Capital

Human Capital – knowledge or skills workers get from education andexperience

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 16/51

There are 4 factors that must all be

used to produce anythingEntrepreneurship – person who takes arisk in combining the other 3 factors to

create a new good

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 17/51

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 18/51

Engineers need to manipulate systems toachieve a balance in attributes in both the

physical and economic environments, and within the bounds of limited resources. Following are some examples where engineeringeconomy plays a crucial role: Choosing the best design for a high-efficiency gasfurnace

Selecting the most suitable robot for a weldingoperation on an automotive assembly line

Making a recommendation about whether jetairplanes for an overnight delivery service should be purchased or leased Considering the choice between reusable anddisposable bottles for high-demand beverages

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 19/51

19

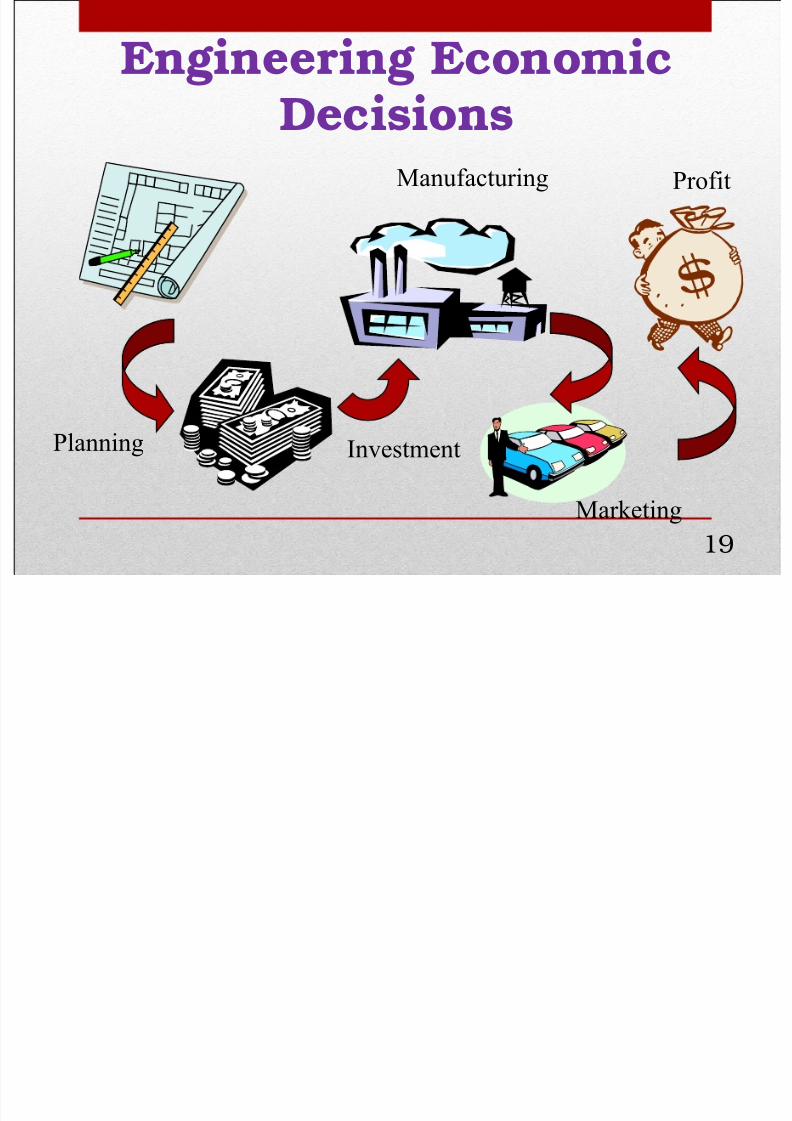

Engineering Economic

Decisions

Planning Investment

Marketing

ProfitManufacturing

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 20/51

Making Economic DecisionsEvery decision we make involvestrade-offs–alternatives that we must give up whenwe make a choice

So while making an economic decision 1st Place is what we would choose to do

2nd Place is our opportunity cost (we give it upto do option 1)

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 21/51

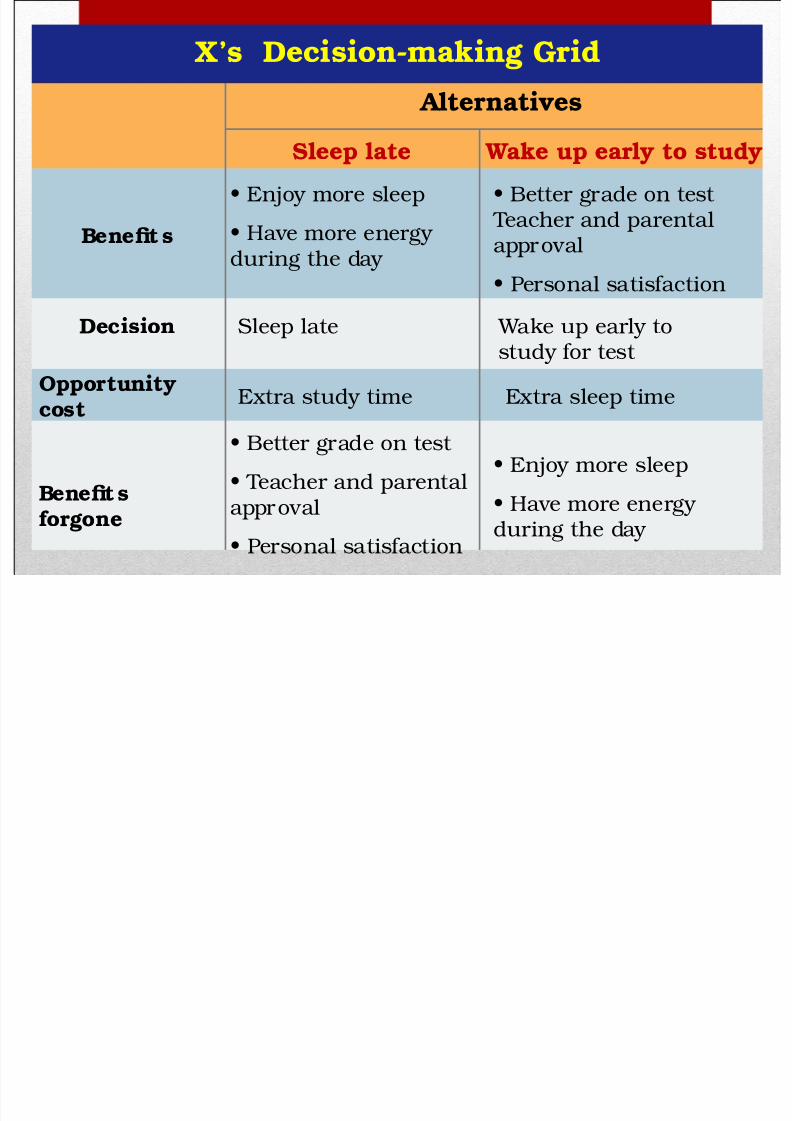

X’s Decision-making Grid

Alternatives

Sleep late Wake up early to study

Benefits

• Enjoy more sleep

• Have more energyduring the day

• Better grade on test Teacher and parentalapproval

• Personal satisfaction

Decision Sleep late Wake up early tostudy for test

Opportunity

cost Extra study time Extra sleep time

Benefitsforgone

• Better grade on test

• Teacher and parentalapproval

• Personal satisfaction

• Enjoy more sleep

• Have more energy

during the day

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 22/51

Opportunity Cost

Definition – the cost expressed in terms of thenext best alternative sacrificed

Helps us view the true cost of decision making

Implies valuing different choices

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 23/51

Few appealing VACATIONDestinations

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 24/51

Individuals may try to maximize utility giventhe constraints of income, time, prices, etc.

Firms may have objectives such as themaximization of profits, sales, market share,etc. or the minimization of costs per unit

Social objective, maximize the well being of themembers of society

Objectives

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 25/51

The Economic ProblemProduction Decisions

Exchange Decisions

Consumption Decisions

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 26/51

What goods and services should an economy

produce? – should the emphasis be onagriculture, manufacturing or services, should it be on sport and leisure or housing?

How should goods and services be produced? –labour intensive, land intensive, capital intensive?Efficiency?

Who should get the goods and servicesproduced? – even distribution? more for the

rich? for those who work hard?

contd.........

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 27/51

•Capital Goods and Consumer Goods

Consumer Goods

Goods produced for present consumption.

Investment

The process of using resources to produce newcapital.

Because resources are scarce, the opportunity costof every investment in capital is forgone presentconsumption.

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 28/51

Every resource is best suited forcertain types of goods

Farmland and cows make butter

Metals and factories make guns

Butter v/s Guns: To convert butterproduction to guns, you must sell the cowsand build new factories on the land

Production Possibility Frontiers

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 29/51

Watermelons(m.t.)

Shoes(millions of pairs)

S h o e s ( m i l l i o n s o f

p a i r s ) 25

20

15

10

5

0252015105

Production Possibilities Graph

Watermelons (millions of tons)

0

a (0,15)

15

b (8,14)

14

18

20

21

12

9

5

0

A production

possibilities frontier

c (14,12)

d (18,9)

e (20,5)

f (21,0)

8 14

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 30/51

PPF shows the different combinations of goods

and services that can be produced with a givenamount of resources

No ‘ideal’ point on the curve

Any point inside the curve – suggests resourcesare not being utilised efficiently

Any point outside the curve – not attainable withthe current level of resources

Useful to demonstrate economic growth andopportunity cost

contd.......

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 31/51

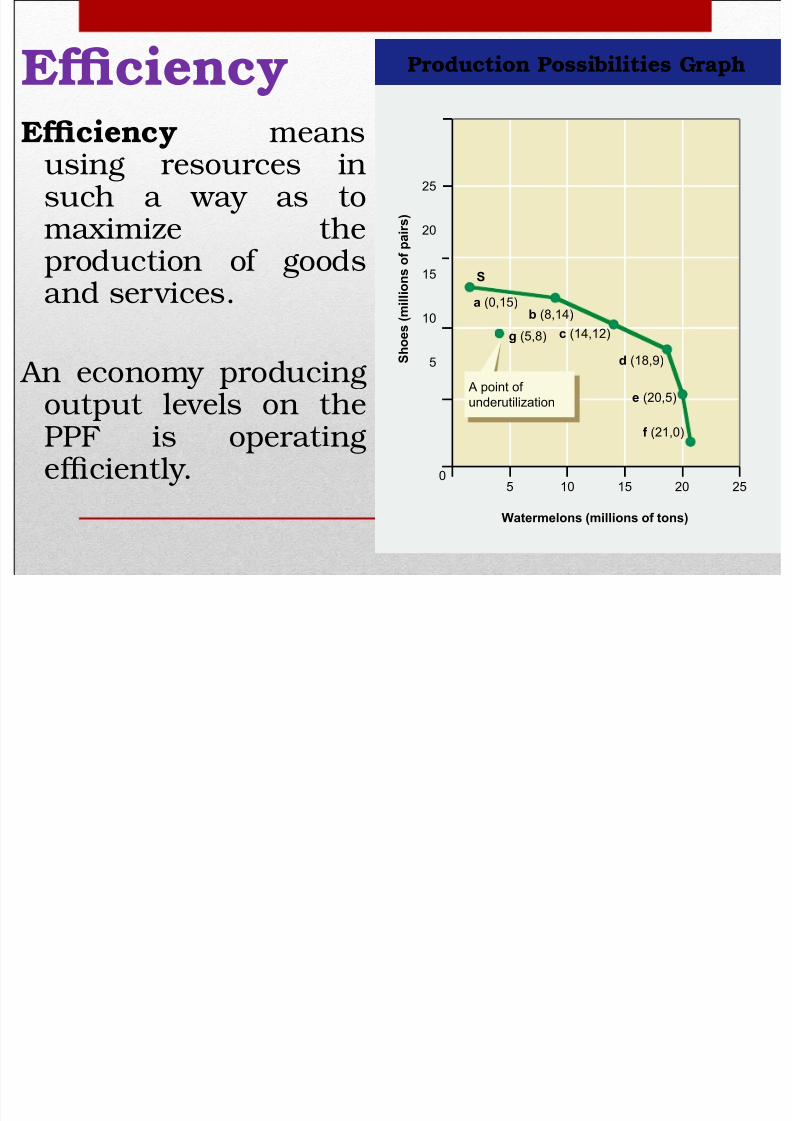

Efficiency

Efficiency meansusing resources insuch a way as tomaximize the

production of goodsand services.

An economy producing

output levels on thePPF is operatingefficiently.

S h o e s ( m i l l i o n s

o f p a i r s )

25

20

15

10

5

0252015105

Watermelons (millions of tons)

Production Possibilities Graph

g (5,8)

A point of

underutilization

c (14,12)

d (18,9)

e (20,5)

f (21,0)

a (0,15)b (8,14)

S

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 32/51

Growth

Growth If more resources become available, or if

technology improves, an

economy can increase its

level of output and grow. When this happens, the

entire production

possibilities curve “shifts

to the right.”

S h o e s ( m i l l i o n s

o f p a i r s )

25

20

15

10

5

0252015105

Watermelons (millions of tons)

Production Possibilities Graph

TFuture production

Possibilities frontier

c (14,12)

d (18,9)

e (20,5)

f (21,0)

a (0,15)b (8,14)

S

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 33/51

Positive & Normative Economics

Health care can beimproved with moretax funding

Pollution control iseffective through asystem of fines

Society ought to

provide homes for all Any strategy aimed atreducing factoryclosures in deprived

areas would be helpful

Positive Statements:Capable of being verified or refuted byresorting to fact or

further investigationNormative Statements:

Contains a value judgement which

cannot be verified byresort toinvestigation orresearch

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 34/51

Micro & Macro Economics

Microeconomics The study of howhouseholds and businesses make choices,how they interact in markets, and how thegovernment attempts to influence their

choices.

Macroeconomics The study of the

economy as a whole, including topics suchas inflation, unemployment, economicgrowth National income etc.

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 35/51

QUIZ TIME

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 36/51

Which of the following are factors of production?a. Capital and Land

b. Scarcity and shortages

c. Technology and productivityd. economics and business decisions

a. capital and land

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 37/51

Which of the following is an example of usingphysical capital to save time and money?

a. hiring more workers to do a job? b. building extra space in a factory to simplifyproduction

c. switching from oil to coal to make productioncheaper

d. lowering workers’ wages to increase profits

b. building extra space in a factory to simplifyproduction

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 38/51

To what part of an industry does a worker’seducation contribute?

a. technology

b. physical capital

c. human capital

d. scarce resources

c. human capital

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 39/51

Which of the following is an entrepreneur?

a. person who earns a lot of money as a singer

or dancer b. person who creates a game and sells it to agame manufacturer

c. person who starts an all-organic cleaning

supplies business that employs othersd. person who works as a highly paid computerprogrammer

c. person who starts an all-organic cleaningsupplies business that employs others

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 40/51

What is the difference between a shortage andscarcity?

a. A shortage can be temporary or long-term, but scarcity always exists.

b. A shortage results from rising prices; scarcityresults from falling prices.

c. A shortage is a lack of all goods and services;scarcity concerns a single item.

d. There is no real difference between a shortageand scarcity

a. A shortage can be temporary or long-term, but scarcity always exists!

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 41/51

What does an economist mean by the termLAND?

a. farmland only b. food crops grown on farmland as well as thefarmland itself

c. goods and services that are produced formthe land

d. all natural resources used to produce goodsand services

d. all natural resources used to produce goodsand services!

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 42/51

The economic concept of guns or butter meansthat …

a. a person can spend extra money either on sportsequipment or food.

b. a company must decide whether to manufactureguns or butter

c. a government must decide whether to producemore or less military or consumer goodsd. a government can buy unlimited military andcivilian goods if it is rich enough

c. a government must decide whether to producemore or less military or consumer goods …trade off …. due to scarcity!

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 43/51

If a person who wants to buy a compact disc (CD)has just enough money to buy one, and chooses

CD A instead of CD B, then CD B is the

a. trade-off

b. opportunity costc. decision at the margin

d. opportunity at the margin

b. opportunity cost

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 44/51

A decision-making grid is a visual way of:

a. examining opportunity costs

b. selling goods or services

c. making marginal decisions

d. identifying shortages

a. examining opportunity costs!

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 45/51

A decision is made at the margin when eachalternative considers

a. a different trade-off than the others

b. where the most costly alternative will be.

c. what the “all or nothing” alternative will be.

d. cost and benefit ranked in progressive units.

d. cost and benefit ranked in progressive units

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 46/51

A production possibilities curve shows the

relationship between the production of:a. farm goods and factory goods

b. two types of farm goods

c. two types of factory goodsd. any two categories of goods

d. any two categories of goods.

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 47/51

The line on a production possibilities curve

showing the relative amounts of two types ofgoods produced using all resources is called the

a. production possibilities frontier

b. opportunity cost linec. utilization of resources

d. maximum possible production line

a. production possibilities frontier

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 48/51

The law of increasing costs means that asproduction shifts from one item to another,

a.the cost of production gets cheaper and cheaper.b.the cost of producing an item stays the same nomatter how many are produced.

c.more and more resources are necessary to

increase production of the second itemd.the land costs of increasing production risemuch more steeply than do the labor costs

c. more and more resources are necessary toincrease production of the second item

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 49/51

and last question …

The curve usually seen in a productionpossibilities frontier can be explained by:

a. growth in the economy

b. underutilization of resourcesc. increasing an economy’s efficiency

d. the law of increasing costs

d. the law of increasing costs!

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 50/51

8/11/2019 Introduction to Economics - Final

http://slidepdf.com/reader/full/introduction-to-economics-final 51/51

Related Documents