Introduction to Accounting and Finance, Geoff Black, 2nd Ed_2009

Oct 26, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

We work with leading authors to develop the strongest

educational materials in accounting, bringing cutting-edge

thinking and best learning practice to a global market.

Under a range of well-known imprints, including

Financial Times Prentice Hall, we craft high quality print

and electronic publications which help readers to

understand and apply their content, whether studying or

at work.

To find out more about the complete range of our

publishing please visit us on the World Wide Web at:

www.pearsoned.co.uk

Geoff Black

FT Prentice Hall FINANCIAL TIMES

An imprint of Pearson Education Harlow, England. London. New York· Boston. San Francisco. Toronto. Sydney. Singapore. Hong Kong Tokyo. Seoul. Taipei. New Delhi. Cape Town. Madrid· Mexico City. Amsterdam· Munich. Paris. Milan

Pearson Education Limited

Edinburgh Gate Harlow Essex CM20 2JE England

and Associated Companies around the world

Visit us on the World Wide Web at: www.pearsoned.co.uk

First published 2005 Second edition published 2009

© Pearson Education Limited 2005, 2009

The right of Geoff Black to be identified as author of this work has been asserted by him in accordance with the Copyright, Designs, and Patents Act 1988.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted .in any form or by any means, electronic, mechanical , photocopying, recording, or otherwise, without either the prior written permission of the publisher or a licence permitting restricted copying in the United Kingdom issued by the Copyright Licensing Agency Ltd, Saffron House, 6-10 Kirby Street, London EC1N 8TS.

ISBN 978 -0-273-71162-9

British Library Cataloguing-in-Publication Data A catalogue record for this book is available from the British Library

Library of Congress Cataloging-in-Publicatlon Data Black, Geoff.

Introduction to accounting and finance / Geoff Black. -- 2nd ed. p. cm.

Includes bibliographical references and index. ISBN 978 -0-273-71162-9 (pbk. : alk. paper) 1. Accounting. 2. Managerial

accounting. 3. Business enterprises--Finance. I. Title. HF5636.B55 2009 657--dc22

10 9 8 7 6 5 4 3 2 1 13 12 11 10 09

Typeset in 9 .5/12.5pt Stone Serif by 30 Printed and bound by Graficas Estella, Navarro, Spain.

200804

The publisher's policy is to use paper manufactured from sustainable forests.

Chapter 1

Chapter 2

Preface Acknowledgements Guided tour of MyAccountingLab

The background to accounting

1.1 Introduction 1.2 What is accounting? 1_3 Who needs accounting? 1.4 Financial accounting and management accounting 1.5 Accounting assumptions and characteristics 1.6 Assets, liabilities and capital 1.7 The accounting equation

1.7.1 How does the value of capital change? 1.8 Summary 1.9 Changes in terminology 1.10 Glossary

Self-check questions Self-study questions Case study: Marvin makes a career choice References

Recording financial transactions

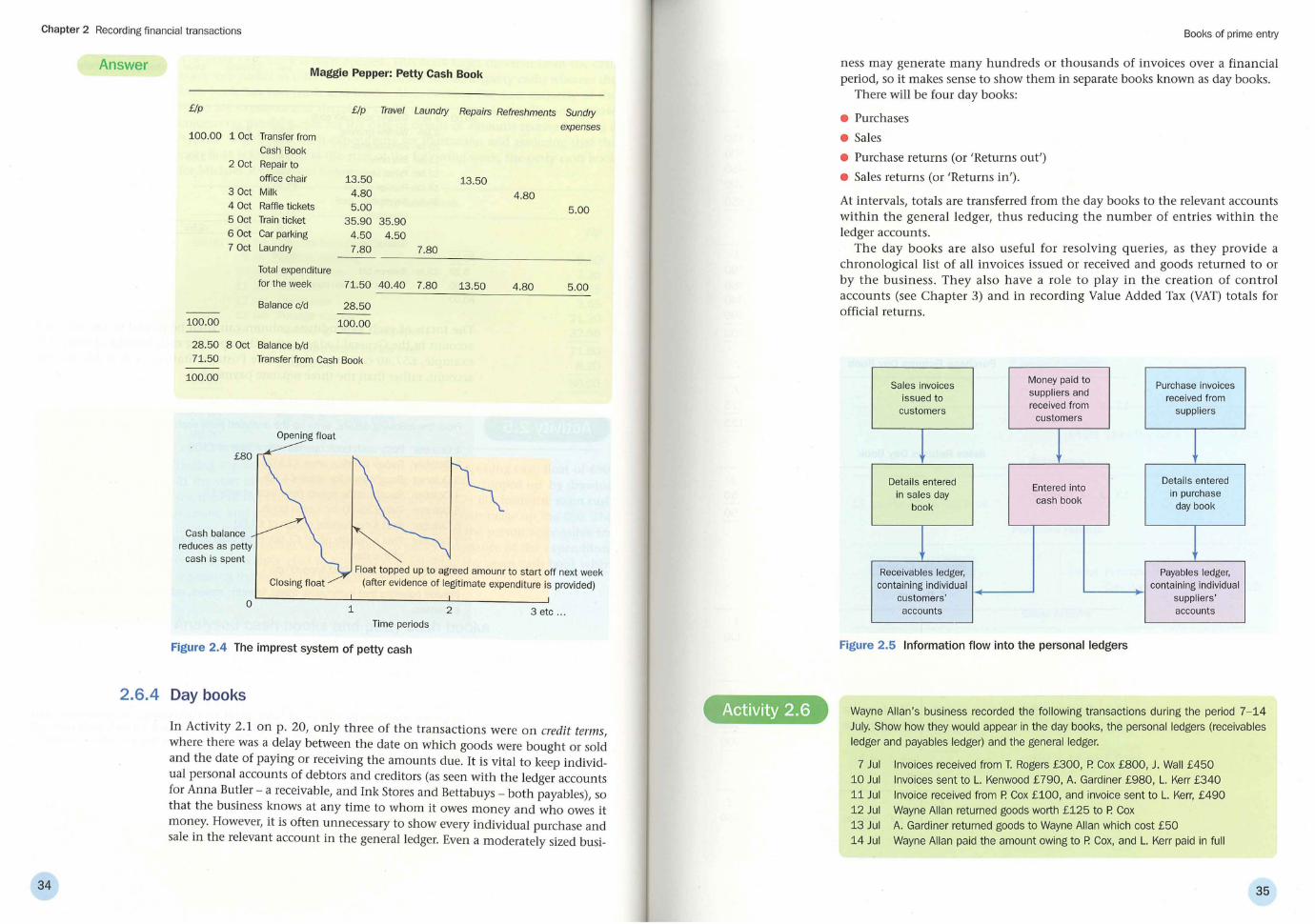

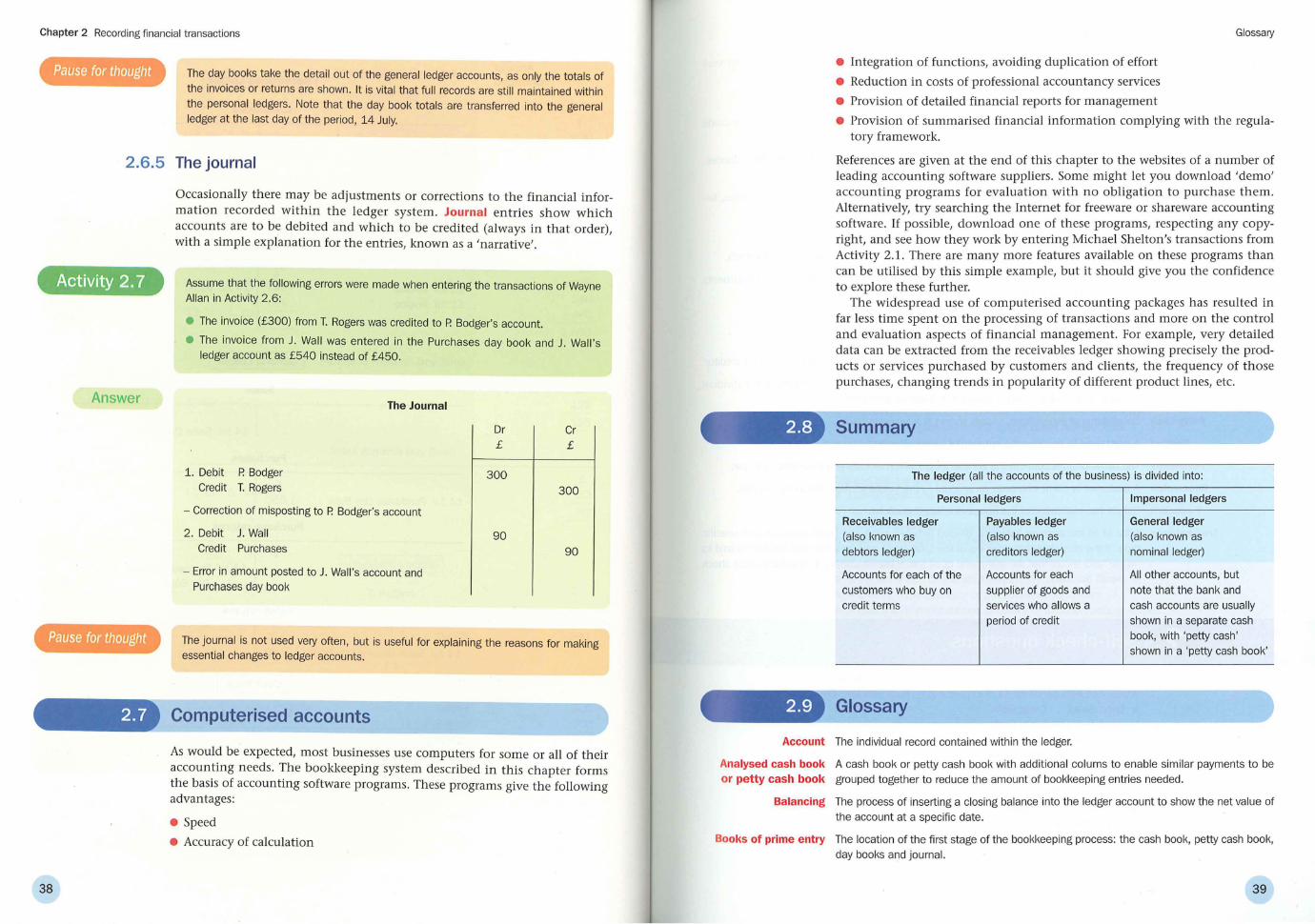

2.1 Introduction 2.2 The principles of double-entry bookkeeping 2.3 The double-entry bookkeeping system 2.4 Balancing accounts 2 .5 A simple trial balance 2.6 Books of prime entry

2.6.1 The cash book 2.6.2 The petty cash book 2.6.3 Analysed cash and petty cash books 2.6.4 Day books 2.6.5 The journal

2.7 Computerised accounts 2.8 Summary 2.9 Glossary

Self-check questions Self-study questions Case study: Marvin buys rabbits! References

xiii xvii xviii

1

1 2 2 4 4 8

10 10 13 13

.14 15 16 18 18

19

19 20 22 27 29 30 30 31 32 34 38 38 39 39 40 42 44 45

v

Contents

Chapter 3

Chapter 4

Chapter 5

vi

Applying controls and concepts to financial information

3.1 Introduction 3 .2 Cash flow statements and beyond 3.3 Bank reconciliation statements 3.4 Control accounts 3.5 Accounting adjustments

3.5.1 Unsold inventory 3.5.2 Accruals and prepayments 3.5.3 Depreciation

3.6 The financial summaries 3 .6.1 The income statement 3.6.2 The balance sheet

3.7 Summary 3.8 Glossary

Self-check questions Self-study questions Case study: Esmeralda appears, then disappears References

The income statement and balance sheet

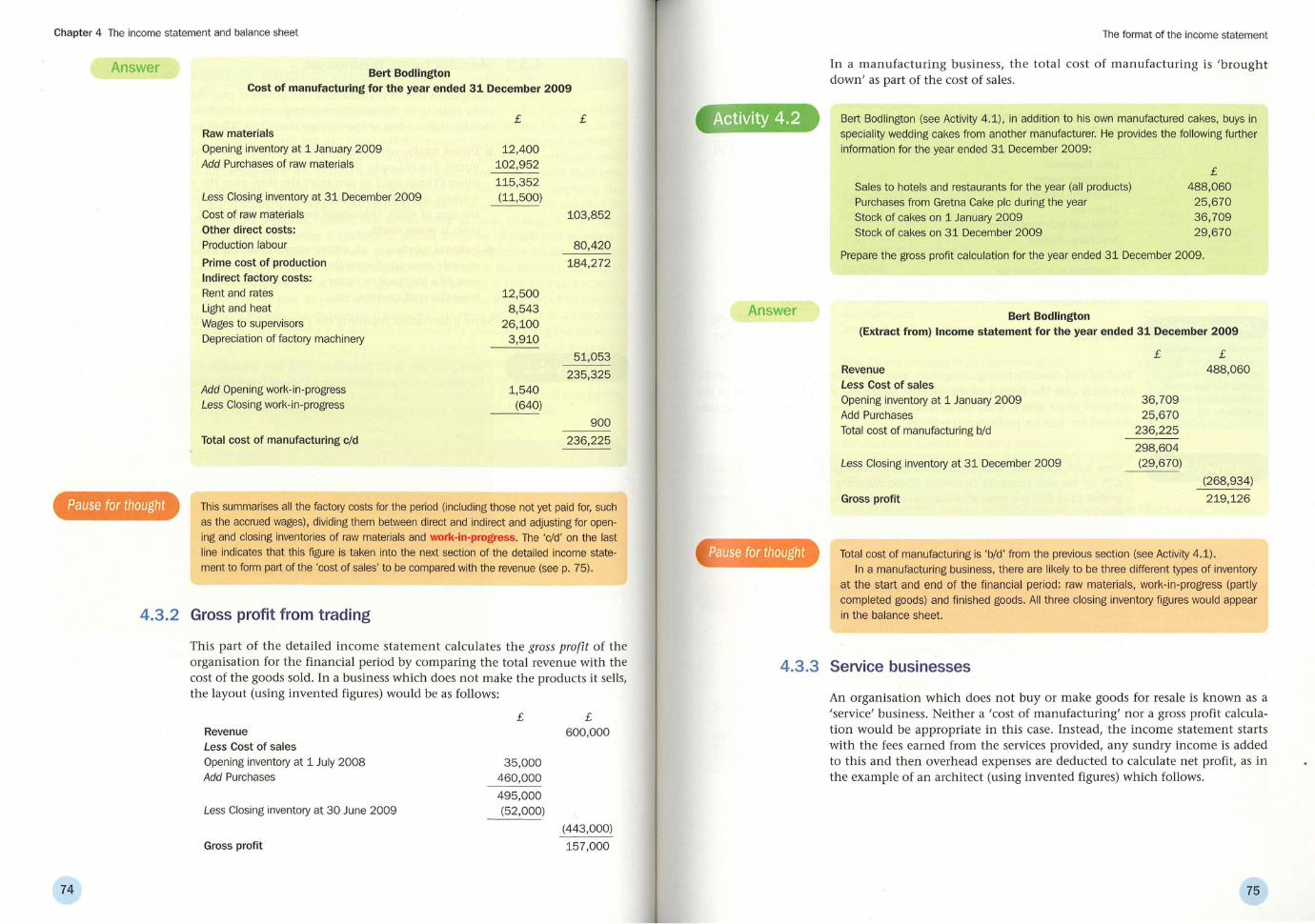

4.1 Introduction 4.2 What is 'profit'? 4.3 The format of the income statement

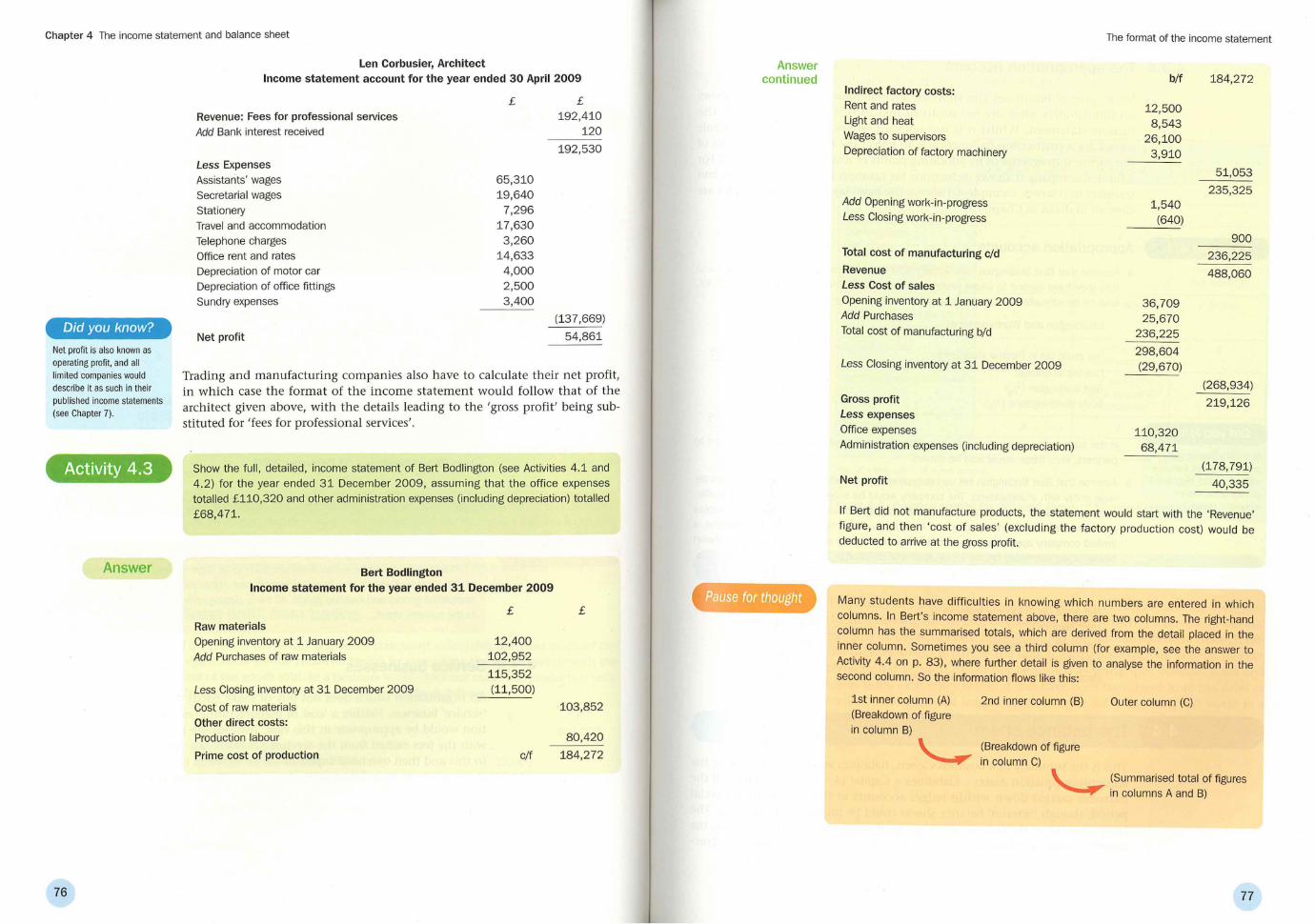

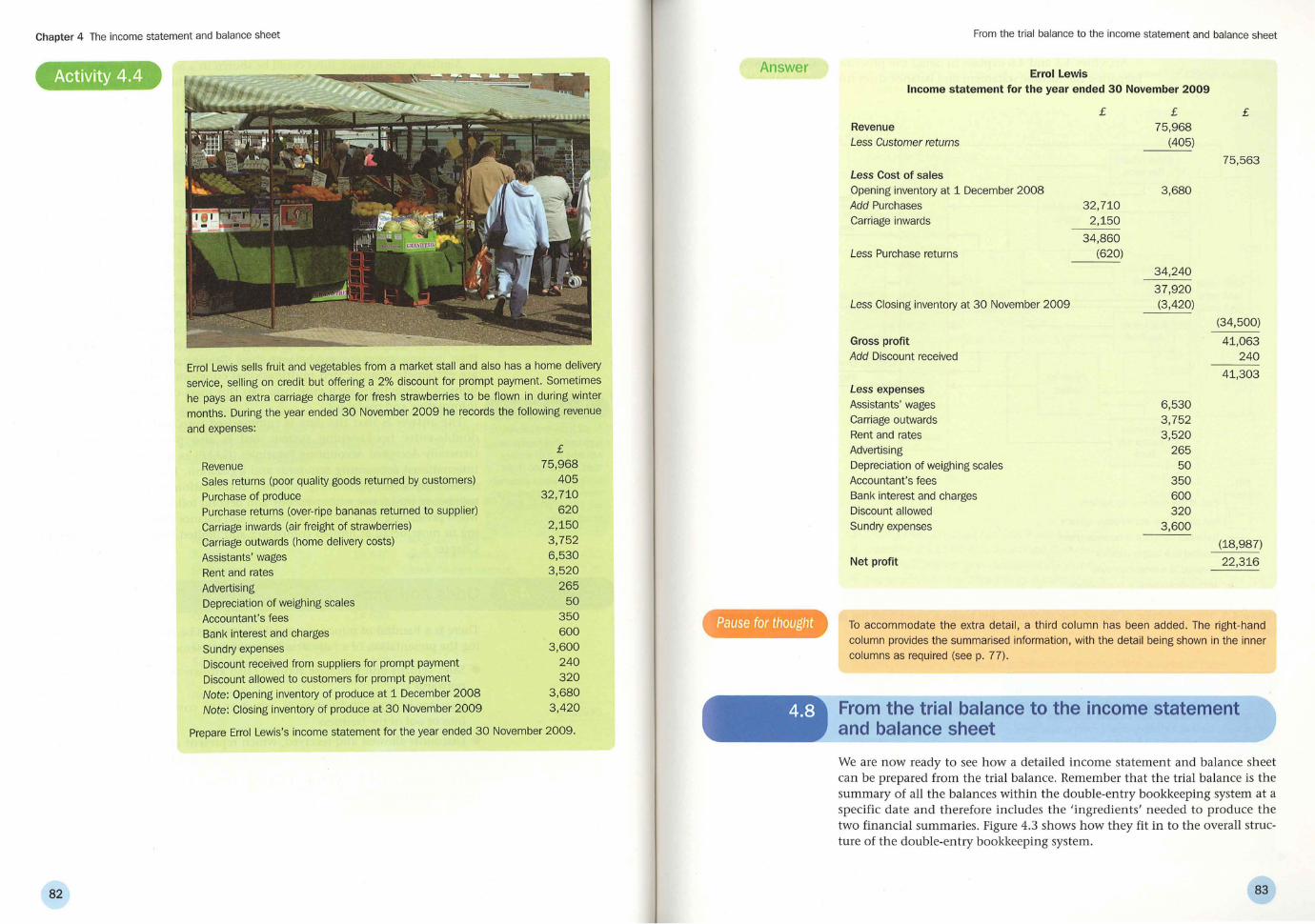

4.3.1 Manufacturing businesses 4.3.2 Gross profit from trading 4.3.3 Service businesses 4.3.4 The appropriation account

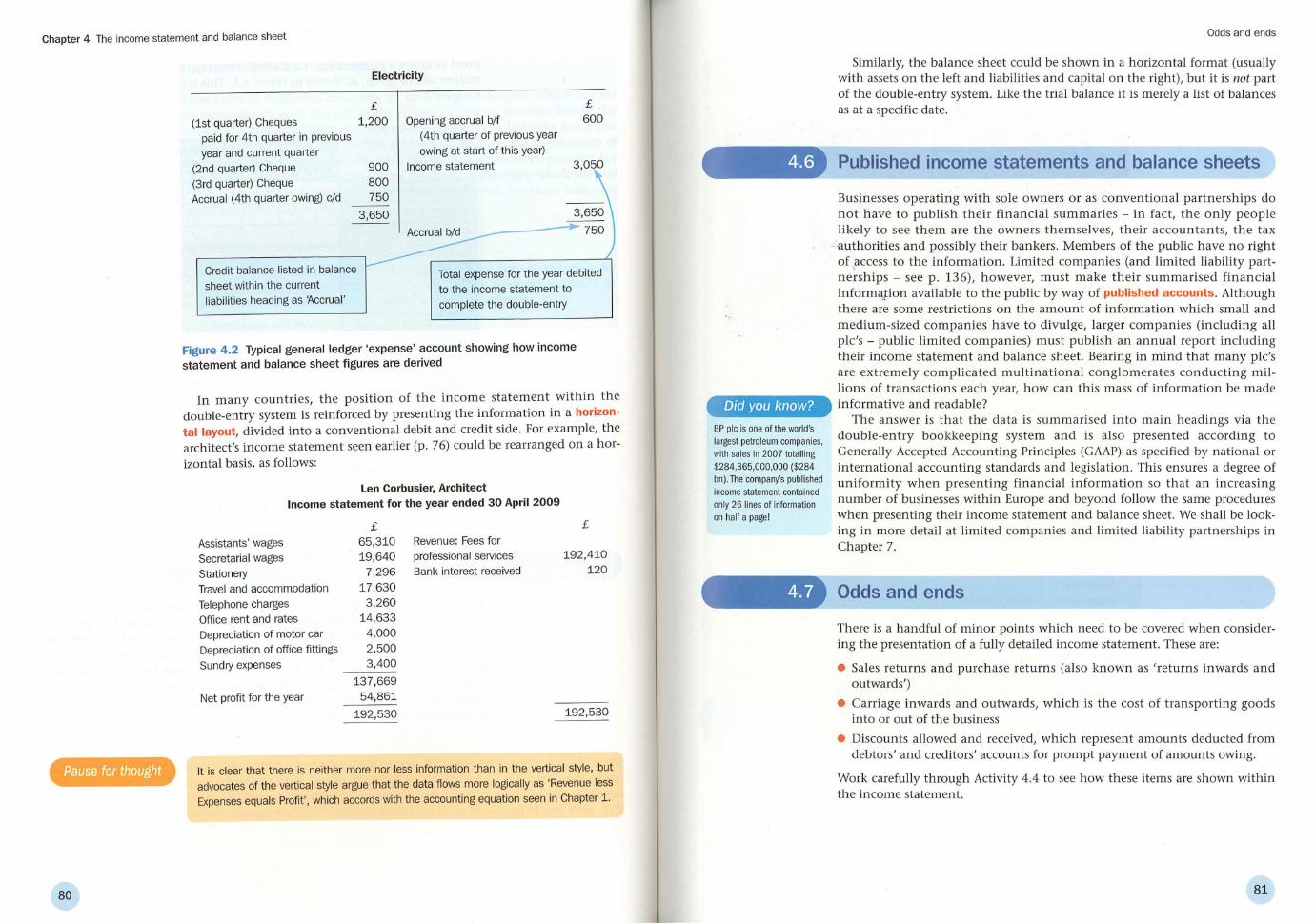

4.4 The balance sheet 4.5 Alternative formats: 'horizontal ' layout 4.6 Published income statements and balance sheets 4.7 Odds and ends 4.8 From the trial balance to the income statement and balance sheet

4.9 Summary 4.10 Glossary

Self-check questions Self-study questions Case study: Marvin makes magic References

A further look at assets and liabilities

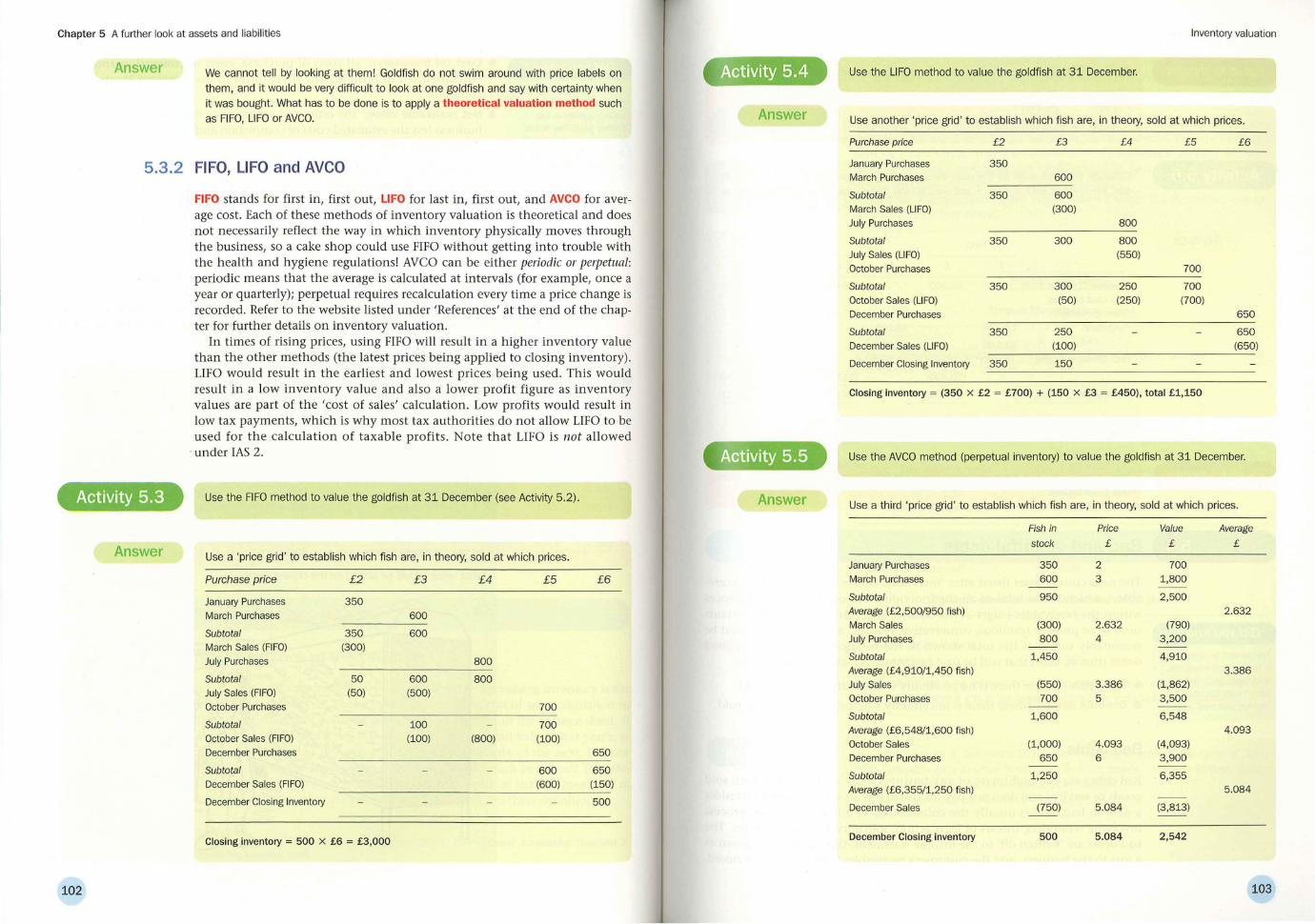

5.1 Introduction 5.2 Sales of non-current assets 5.3 Inventory valuation

5.3.1 The importance of the valuation 5.3.2 FIFO, LIFO and AVCO

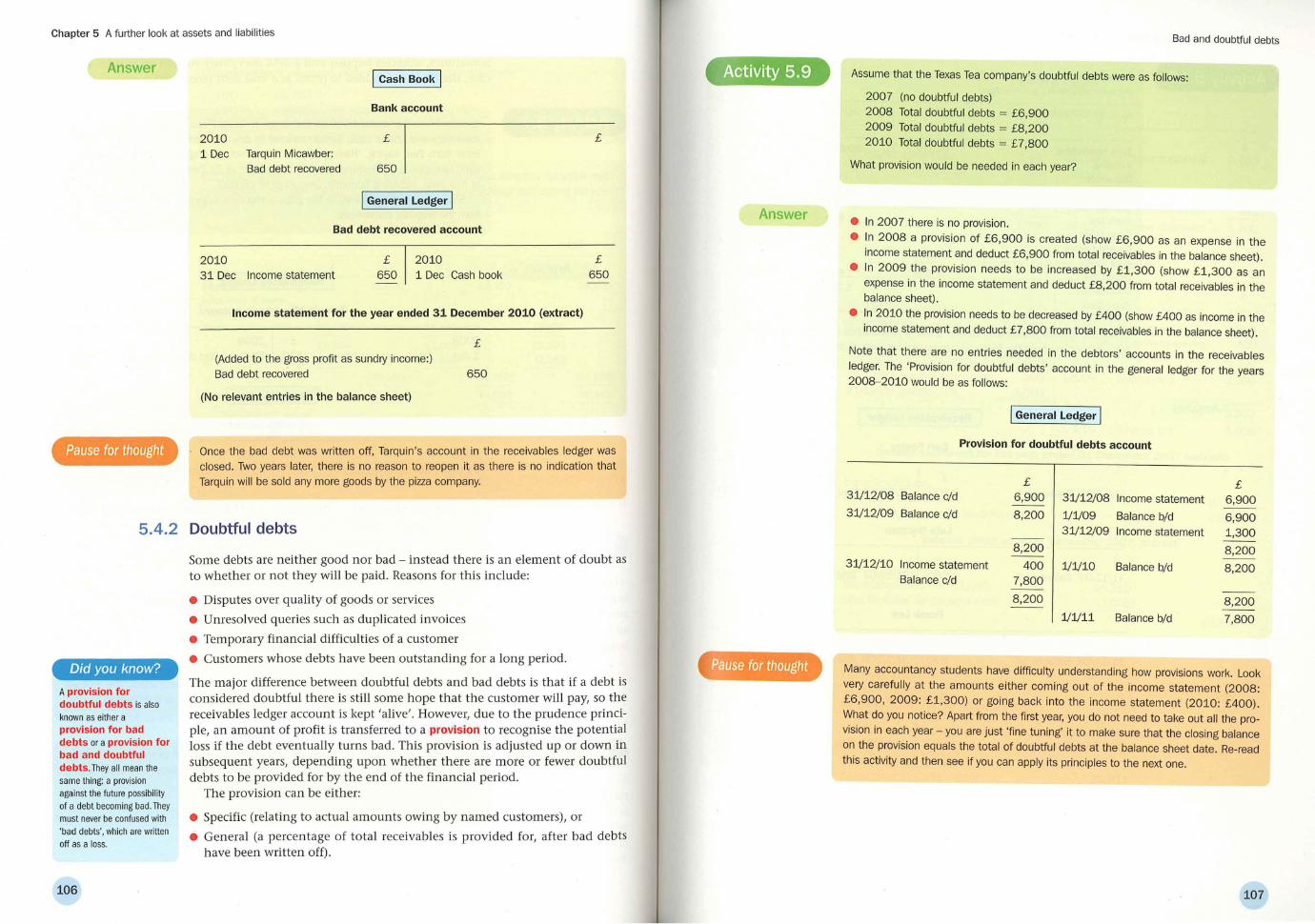

5.4 Bad and doubtful debts 5.4.1 Bad debts 5.4.2 Doubtful debts

46

46 47 47 50 53 53 54 57 61 61 62 64 64 65 67 69 70

71

71 72 72 73 74 75 78 78 79 81 81 83 88 88 89 91 93 94

95

95 95

100 100 102 104 104 106

Chapter 6

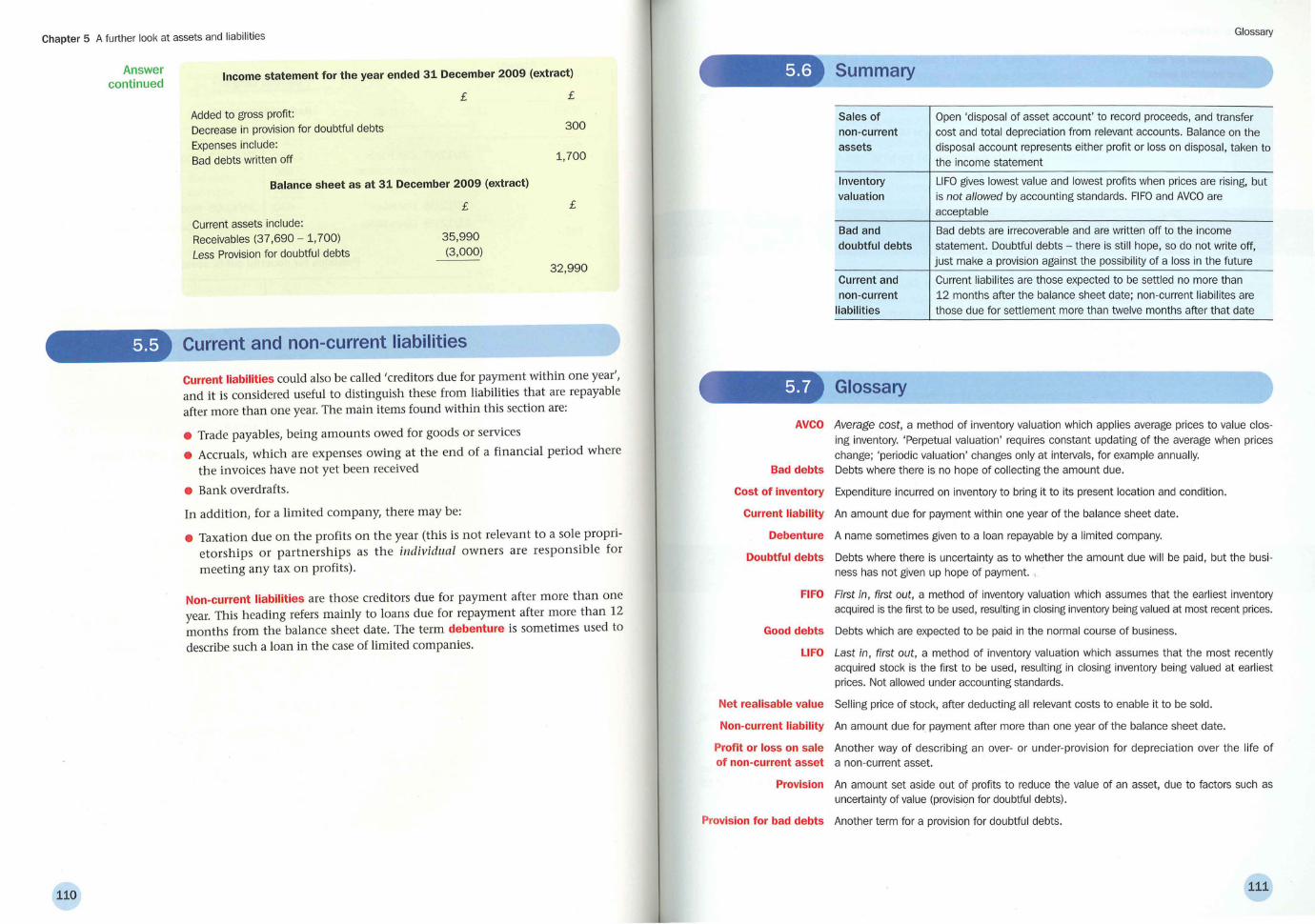

Chapter 7

5.5 Current and non-current liabilities 5.6 Summary 5.7 Glossary

Self-check questions Self-study questions Case study: Esmeralda doesn't disappear, so Chiquita appears References

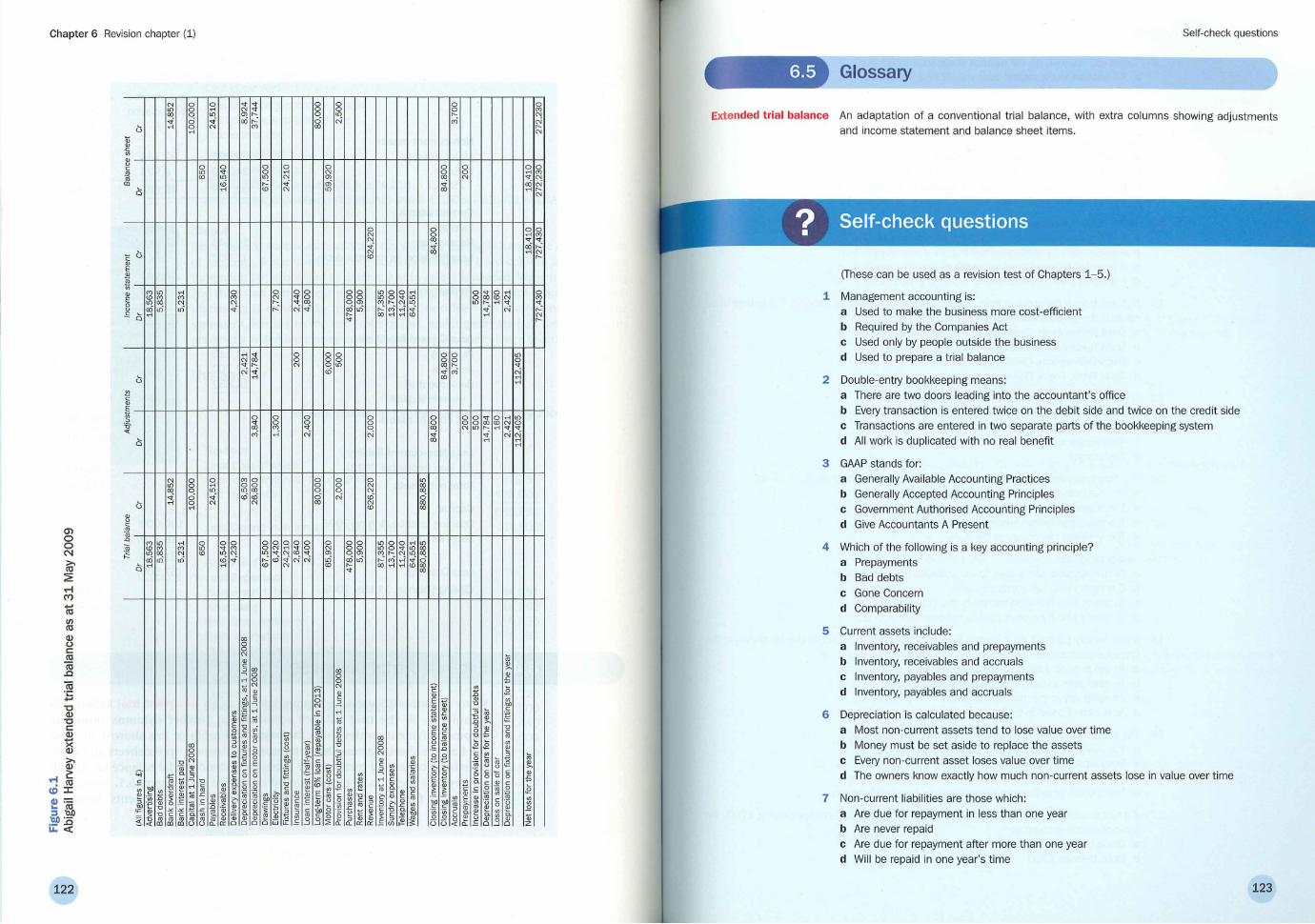

Revision chapter (1)

6.1 Introduction 6.2 Revision question 6.3 Answer to revision question 6.4 Extended trial balances 6.5 Glossary

Self-check questions Self-study questions Case study: Marvin's second birthday References

Accounting and financing of multi-owner organisations

7.1 Introduction 7.2 Sole proprietorships 7.3 Partnerships

7.3.1 Accounting requirements of partnerships 7.3.2 Capital accounts and current accounts 7.3.3 Partnership income statements 7.3.4 Partnership balance sheet 7.3.5 Limited liability partnerships

7.4 Limited companies 7.4.1 Accounting requirements of limited companies 7.4.2 Rights issues and bonus issues

7.5 Short- and long-term sources of financing 7.5.1 Long-term sources of finance: share sales 7.5.2 Long-term sources of finance: loans 7.5.3 Long-term sources of finance: finance leases 7.5.4 Short-term sources of finance: bank overdrafts 7.5.5 Short-term sources of finance: debt factoring 7.5 .6 Internal sources of finance 7.5.7 Summary of finance sources

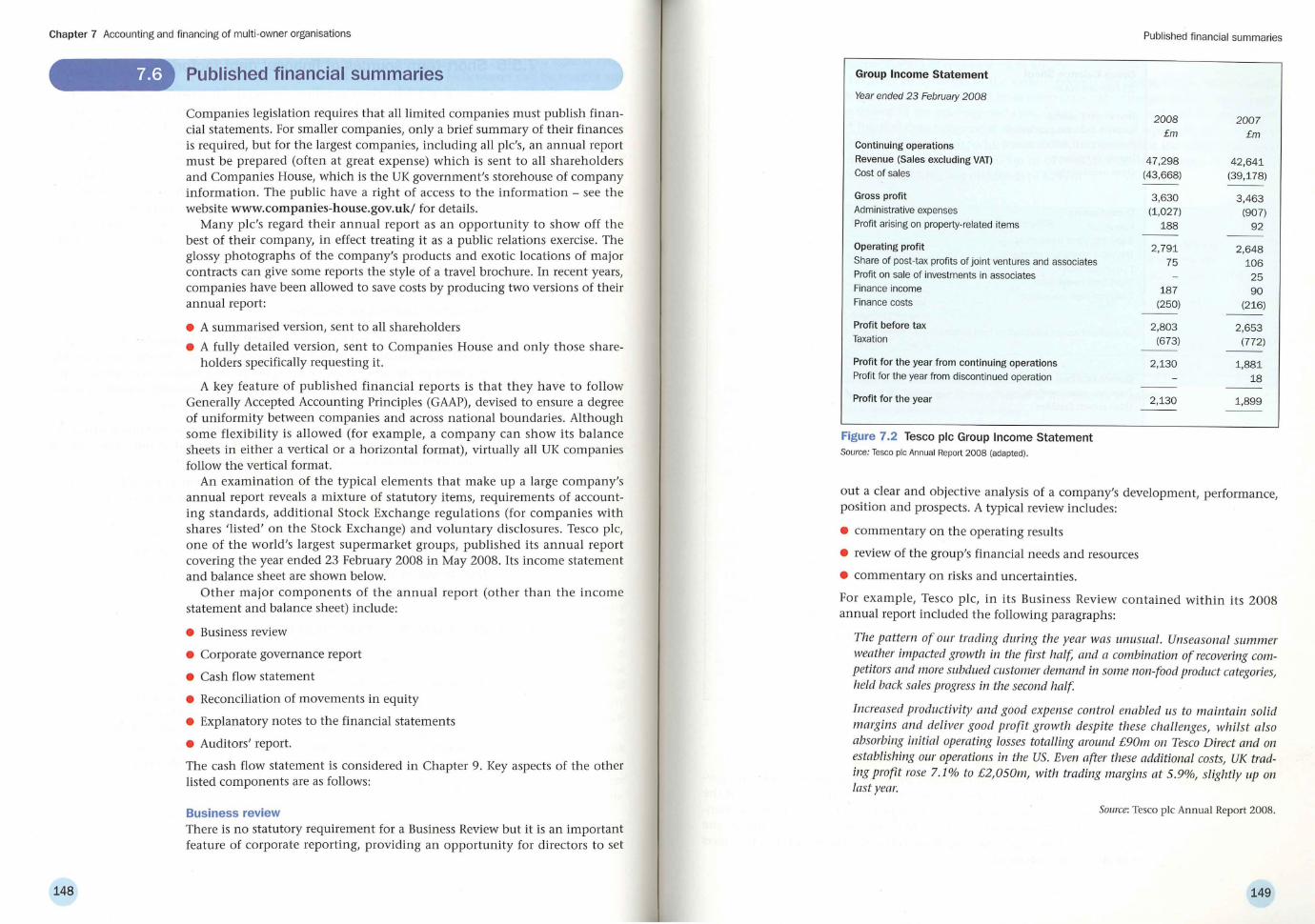

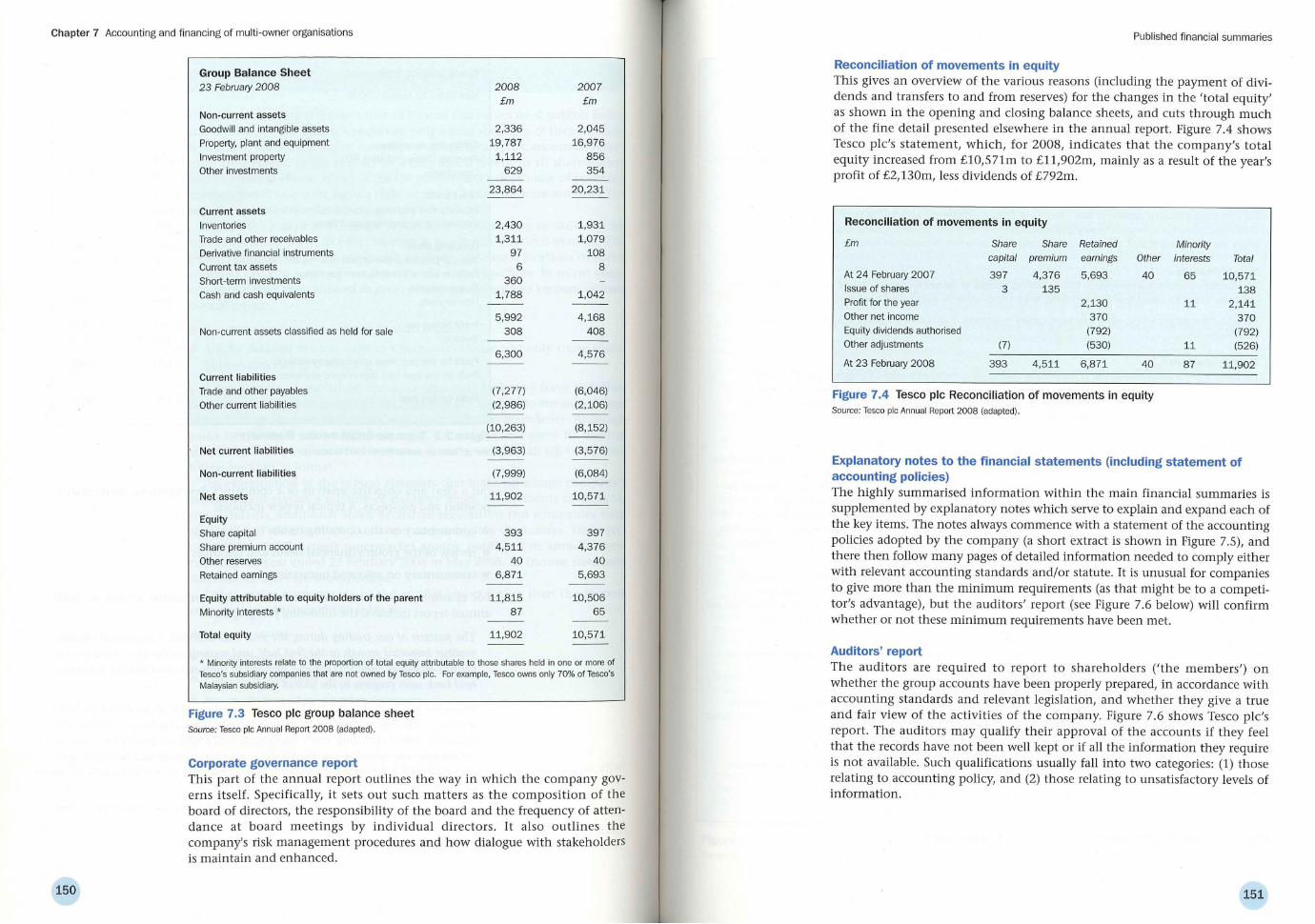

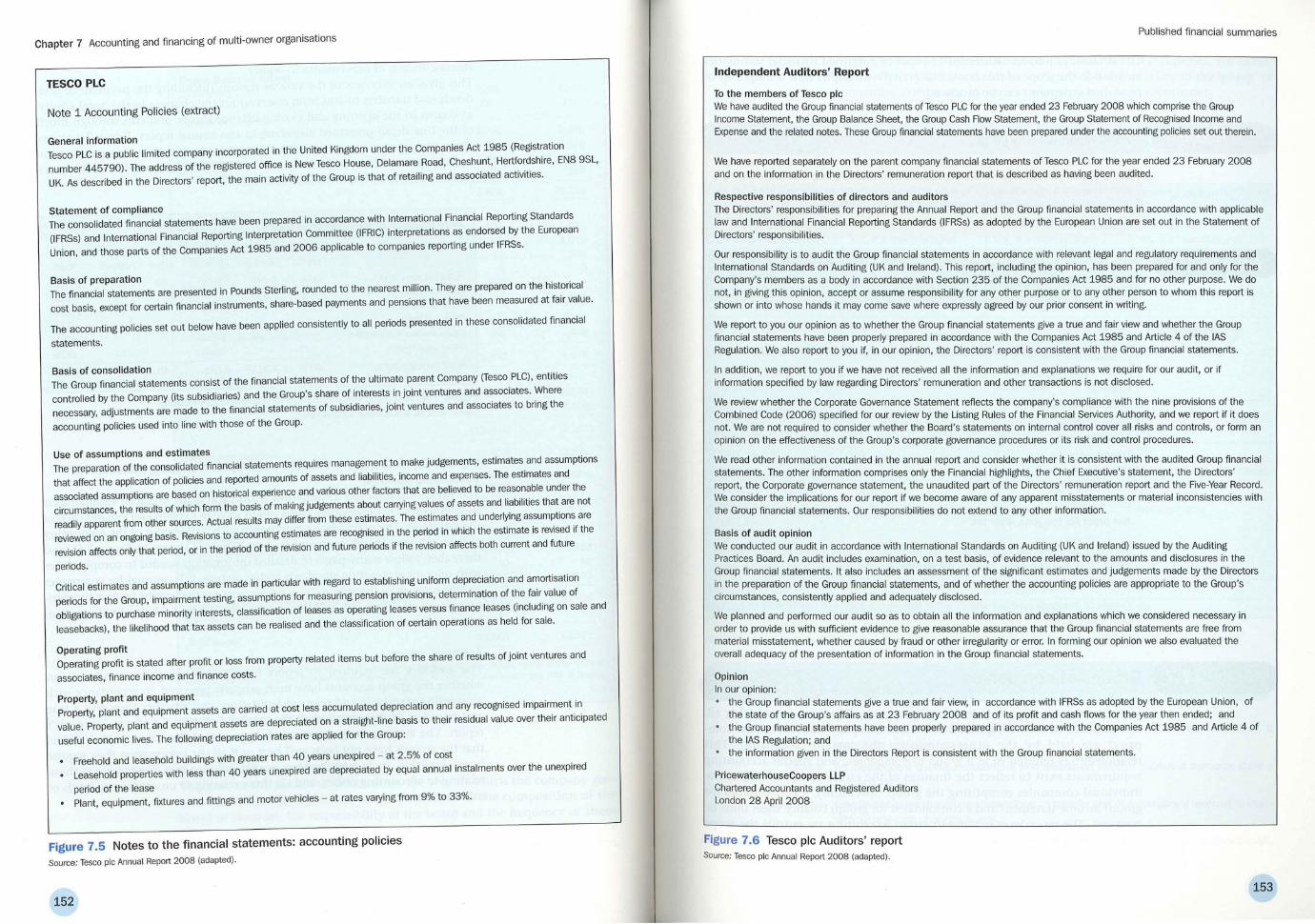

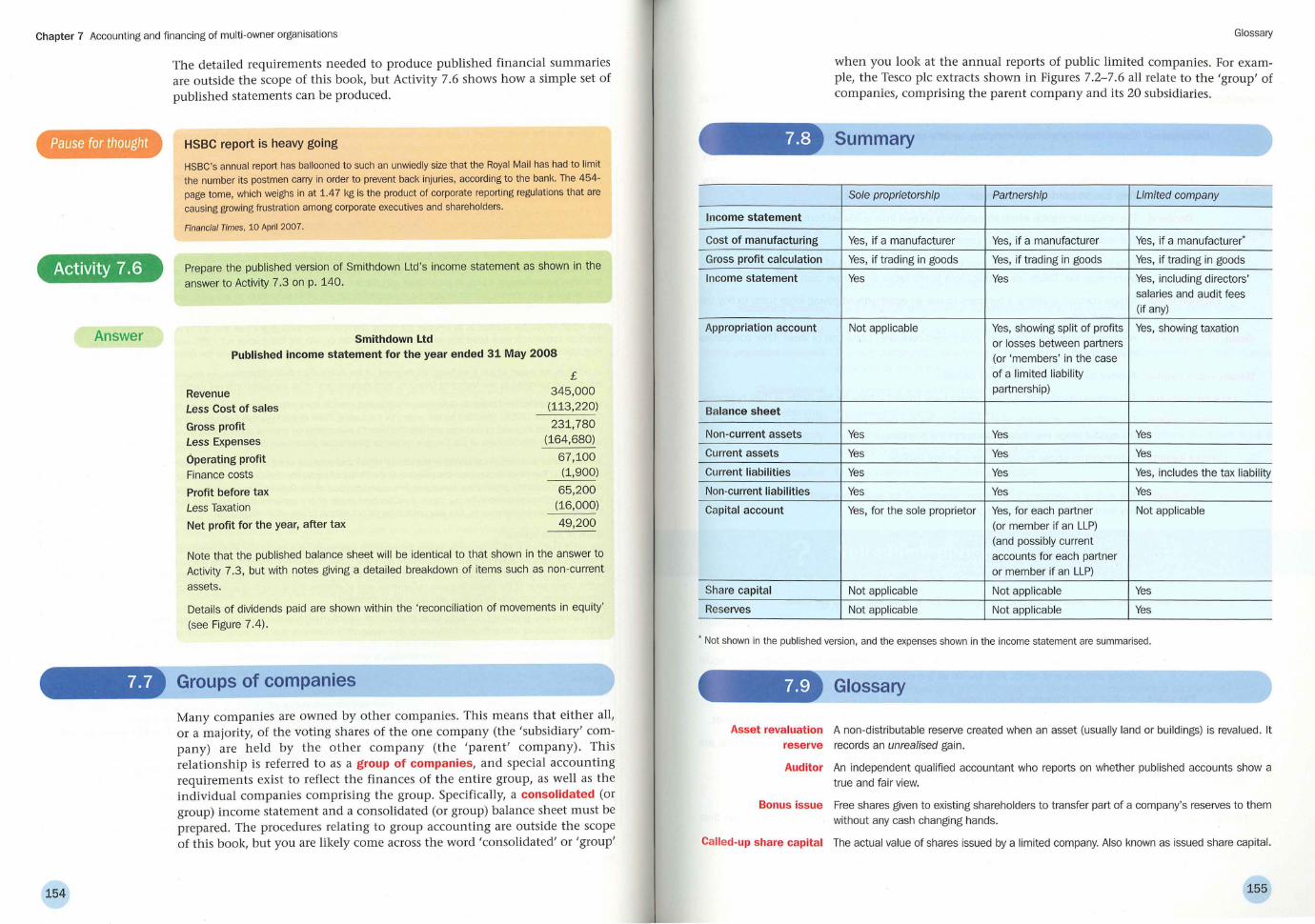

7.6 Published financial summaries 7.7 Groups of companies 7.8 Summary 7.9 Glossary

Self-check questions Self-study questions Case study: Marvin and Chiquita make Machiq, but Esmeralda makes trouble References

Contents

110 111 111 112 113 115 116

117

117 118 119 121 123 123 127 129 130

131

131 132 132 133 134 134 135 135 136 137 141 143 144 145 146 146 147 147 147 148 154 155 155 157 159

161 162

vii

Contents

Chapter 8

Chapter 9

Chapter 10

viii

Incomplete records and club accounts 163

8.1 Introduction 163 8.2 What are 'incomplete records'? 164 8.3 Statement of affairs 165 8.4 Use of control accounts to deduce information 166 8.5 Club accounts 168

8.5.1 Receipts and payments account 169 8.5.2 Income and expenditure account 170

8.6 Summary 174 8.7 Glossary 174

Self-check questions 175 Self-study questions 176 Case study: The treasurer of the Abracadabra Club does a vanishing trick 180 References 181

Cash flow: past and future 182

9.1 Introduction 182 9.2 Cash versus profit 183 9.3 The cash flow statement 185 9.4 Cash flow forecasts 191 9.5 Cash flow forecasts and business planning 9.6 Summary 9.7 Glossary

Self-check questions Self-study questions Case study: There's the profit, but where's the cash? References

Making sense of financial statements

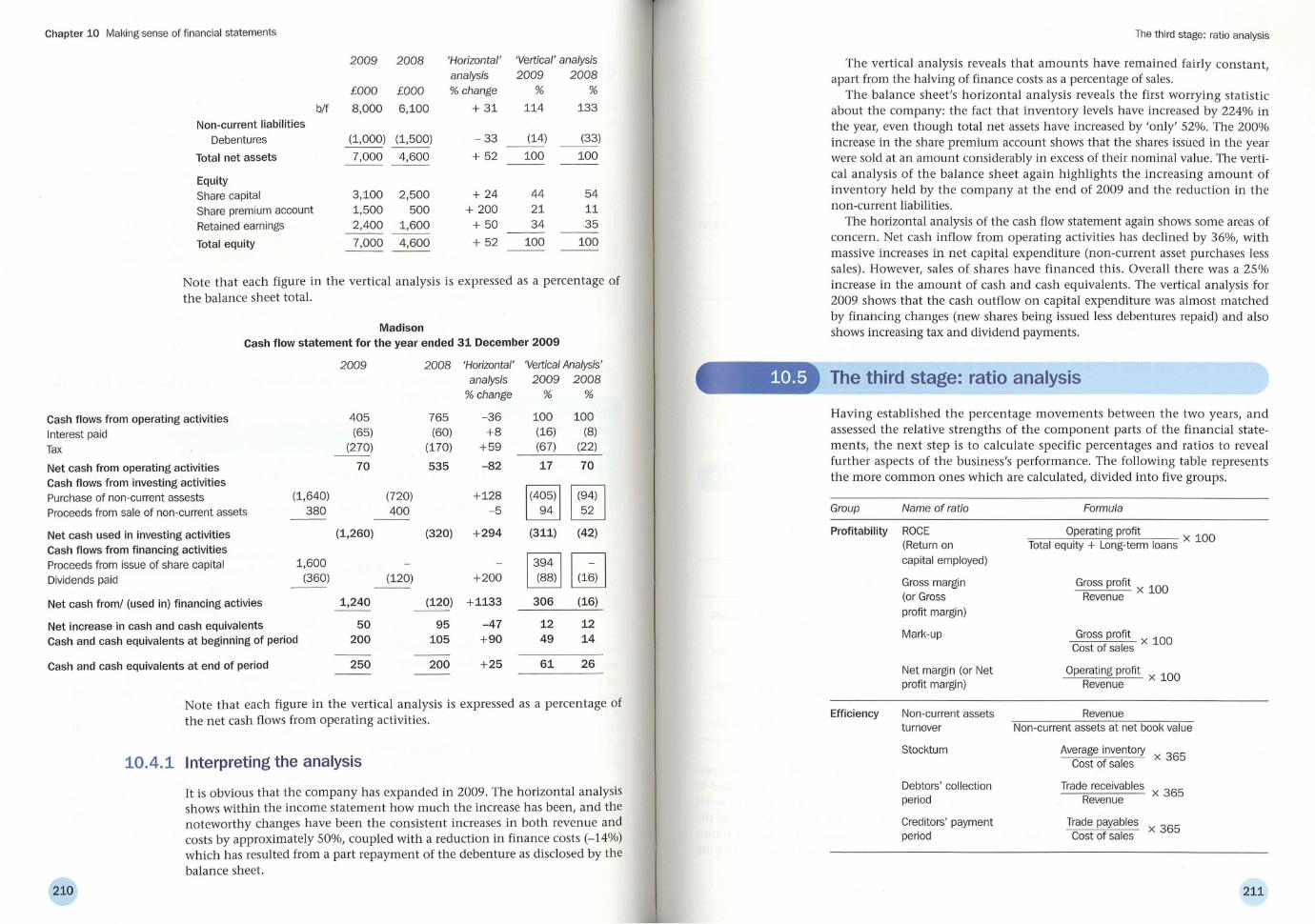

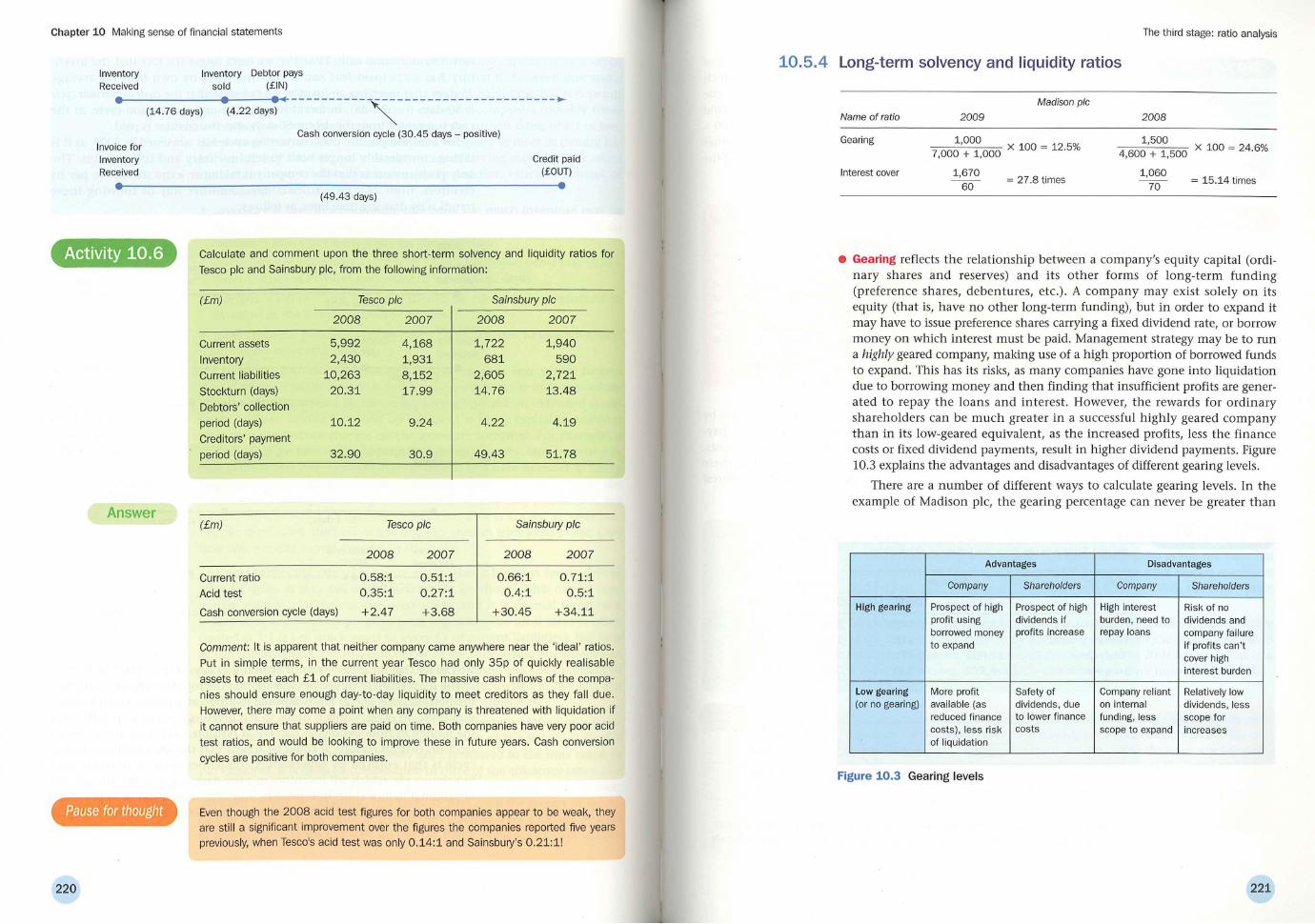

10.1 Introduction 10.2 Data for analysis 10.3 The first stage: preliminary research 10.4 The second stage: horizontal and vertical analysis

10.4.1 Interpreting the analysis 10.5 The third stage: ratio analysis

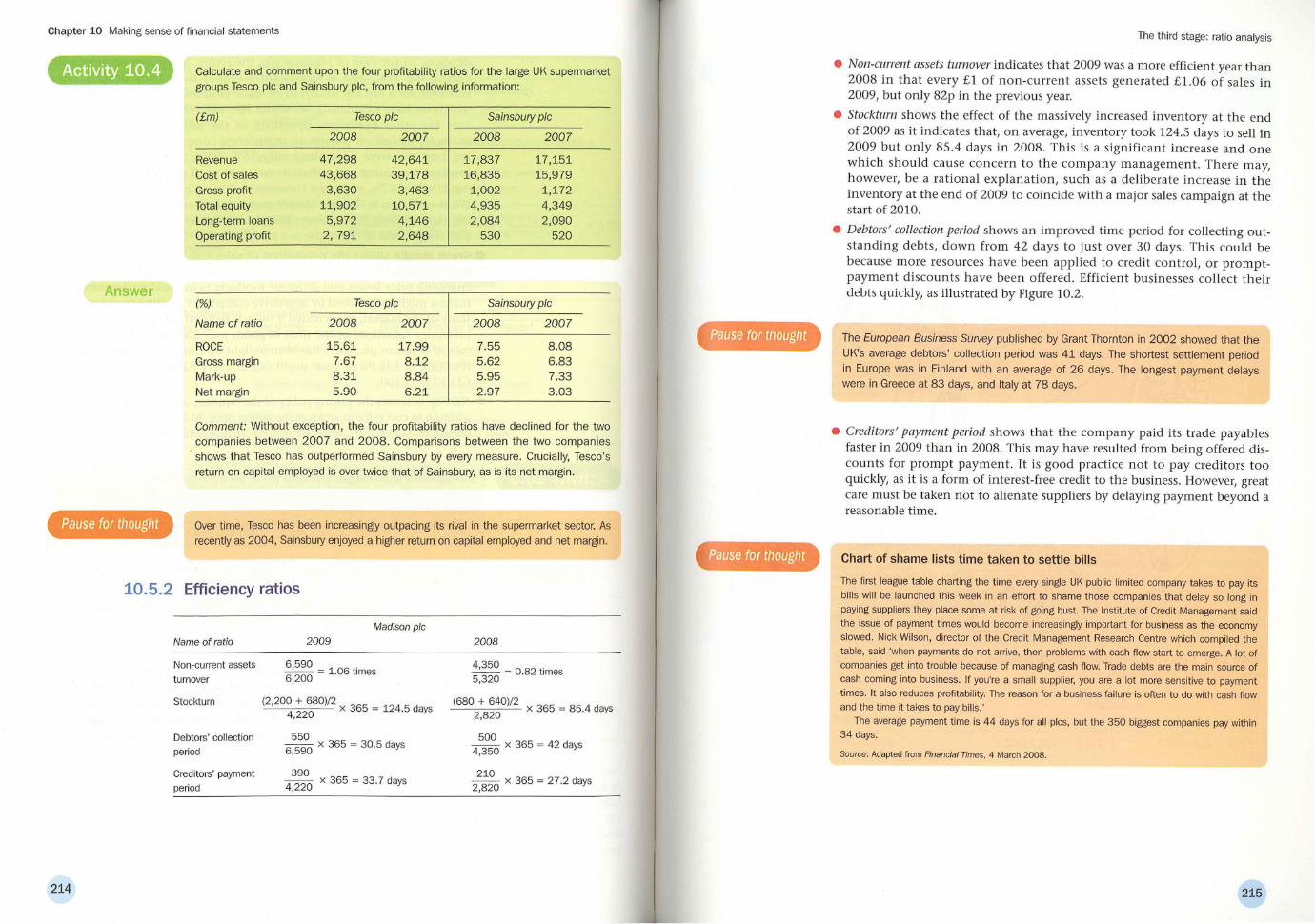

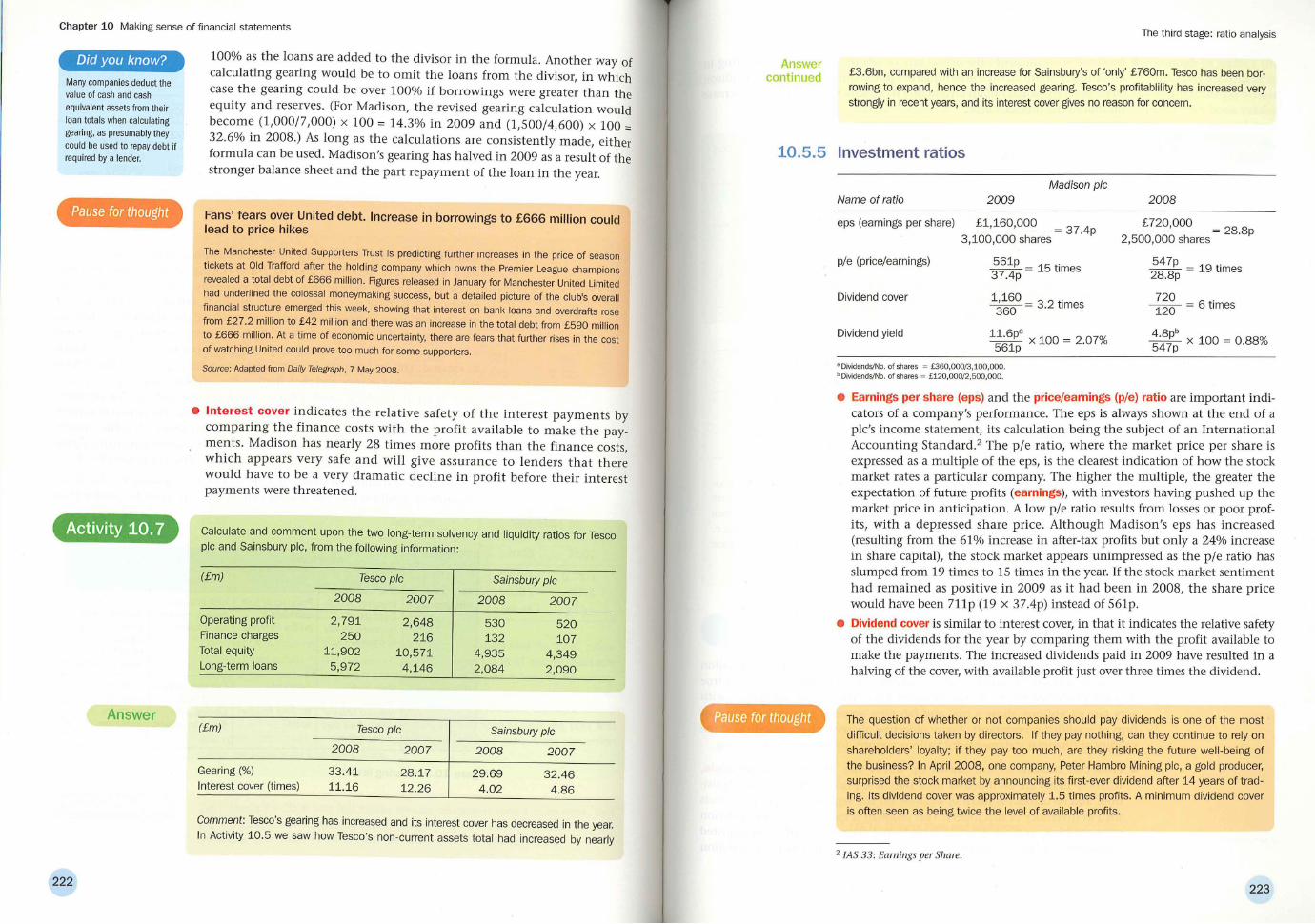

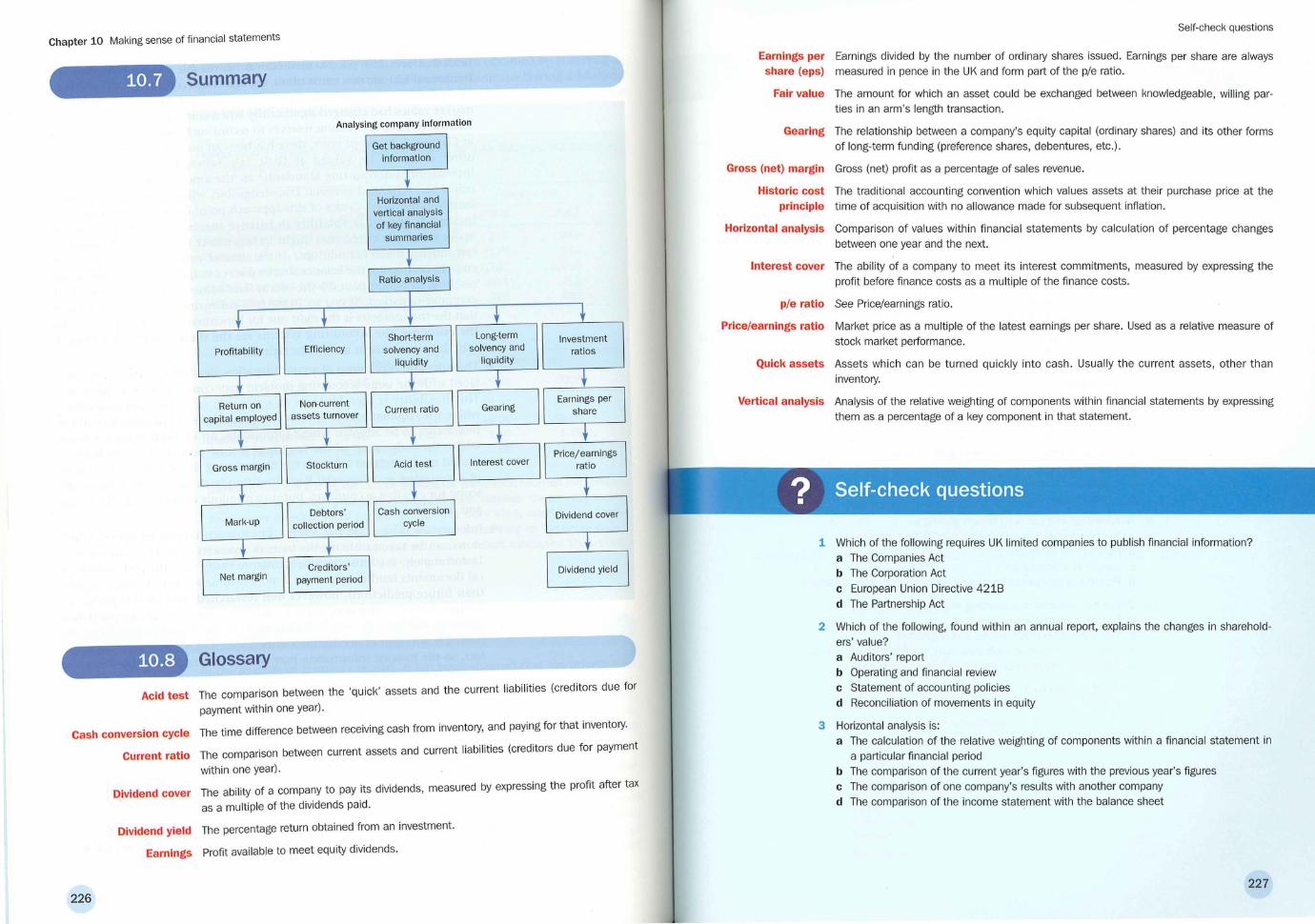

10.5.1 Profitability ratios 10.5.2 Efficiency ratios 10.5.3 Short-term solvency and liquidity ratios 10.5.4 Long-term solvency and liquidity ratios 10.5.5 Investment ratios

10.6 The validity of the financial statements 10.7 Summary 10.8 Glossary

Self-check questions Self-study questions Case study: Esmeralda springs a surprise Reference

192 195 195 196 197 200 201

202

202 203 205 208 210 211 212 214 217 221 223 224 226 226 227 229 231 233

Chapter 11

Chapter 12

Chapter 13

Chapter 14

Revision chapter (2)

11.1 Introduction 11.2 Practice examination paper 1 11.3 Practice examination paper 2

References

An introduction to management accounting

12.1 Introduction 12.2 A definition of management accounting 12.3 The classification of costs

12.3.1 Analysis by function 12.3.2 Analysis by type 12.3.3 Analysis by behaviour 12.3.4 Analysis by time

12.4 Summary 12.5 Glossary

Self-check questions Self-study questions Case study: The great disappearing profits trick References

Absorption costing and marginal costing

13.1 Introduction 13.2 Absorption costing

13.2.1 Stage 1: Allocation of costs to cost centres 13.2.2 Stage 2: Apportionment of overheads 13.2.3 Stage 3: Reapportionment of overheads 13.2.4 Stage 4: Absorption of production centre costs into products

13.3 Advantages and disadvantages of absorption costing 13.4 Activity-based costing (ABC) 13.5 Absorption costing and activity-based costing compared 13.6 Marginal costing 13.7 Using the contribution for 'what-if' calculations ' 13.8 Absorption costing and marginal costing compared 13.9 Summary 13.10 Glossary

Self-check questions Self-study questions Case study: Who is Mrs Eadale? References

Product costing

14.1 Introduction 14.2 Specific order costing

14.2.1 Job costing 14.2.2 Quotations and job cost sheets 14.2.3 Batch costing 14.2.4 Contract costing

Contents

234

234 235 240 242

243

243 244 245 245 246 247 248 249 249 250 251 252 252

253

253 254 254 254 255 257 258 259 261 262 264 265 265 266 266 267 269 269

270

270 271 271 271 272 273

ix

Contents

Chapter 15

Chapter 16

Chapter 17

x

14.3 Operation costing 14.3.1 Process costing 14.3.2 Service costing

14.4 Summary 14.5 Glossary

Self-check questions Self-study questions Case study: The antidote to the potion References

Break-even and cost- volume- profit analysis

15.1 Introduction 15.2 Break-even charts

15.2.1 A combination of graphs 15.2.2 Interpreting the chart 15.2.3 Changes in costs and revenue 15.2.4 Limitations of break-even charts

15.3 Profit/volume chart 15.4 Summary 15.5 Glossary

Self-check questions Self-study questions

Case study: Chiquita's chart References

Budgeting

16.1 Introduction 16.2 Reasons for budgeting 16.3 Long- and short-term planning 16.4 Limiting factors 16.5 The budget process 16.6 Preparing a budget 16.7 The cash budget

16.8 Master budgets

16.9 Summary 16.10 Glossary

Self-check questions Self-study questions

Case study: Reappearance, followed by glowing and floating ... References

Investment appraisal

17.1 Introduction 17.2 Present values and future values

17.2.1 From present values to future values 17.2.2 From future values to present values

273 273 275 276 276 277 278 279 279

280

280 280 281 283 286 286 287 289 290 290 291 293 293

294

294 295 295 296 296 297 299 300 301 301 301 303 304 305

306

306 307 307 308

Chapter 18

17.3 Investment appraisal using discounting techniques 17.3.1 Discounted cash flow (DCF) 17.3.2 Net present value (NPV) 17.3.3 Internal rate of return (lRR)

17.4 Investment appraisal using non-discounting techniques

17.4.1 Payback period 17.4.2 Accounting rate of return (ARR)

17.5 Summary 17.6 Glossary

Self-check questions Self-study questions Case study: Machiq Limited's bid for world domination References

Revision chapter (3)

18.1 Introduction 18.2 Practice examination paper 3

References

Appendix 1: Answers to self-check questions Appendix 2: Answers to self-study questions Appendix 3: Answers to case study questions Appendix 4: Answers to practice examination papers 1, 2 and 3

Index

Contents

309 309 311 312 313 313 315 316 316 317 319 320 321

322

322 322 325

326 327 375 393

401

xi

'Mr Anchovy, our experts desaibe you as an appallingly dull fellow, unimaginative, timid, lacking in initiative, spineless, easily dominated, no sense of 11llmow; tedious company and iITepressibly drab and awful. And, whereas in most professions these would be considerable drawbacks, in accountancy they are a positive boon.'

Monly P)'thon, 'The Lion Tamer sketch'

My aim in writing this book is to make your initial study of accounting and finance interesting and enjoyable and to help you complete your studies with a much more positive image of accountants than that of Monty Python! Who knows, you might even become an accountant one day! This is said in the knowledge that most students think that this subject requires:

• advanced mathematical skills

• an IQ of 200+ • a high boredom threshold.

In the 18 chapters of this book, I have borne in mind that most students reading it will be coming to the subject for the first time, with or without these preconceptions. Many will be on modular courses lasting one semester, with limited access to tutorial help and higher demand than supply in terms of library and other support. To make the learning process as smooth as possible, there is a logical progression in the subject matter from chapter to chapter. I have chosen the pattern of topics to reflect most closely the majority of introductory courses within universities and colleges.

Each chapter commences with a statement of objectives, indicating what you should be able to do after completing that chapter. There are three revision chapters - Chapters 6, 11 and 18 - which will help you to consolidate your knowledge. Within each chapter you will find a number of further features in addition to the textual explanation of the subject matter:

• Pause for thought. Either a thought-provoking or a humorous diversion to get you looking at the topic in a different way, or an added explanation of a difficult topic.

• Did you know? A factual item of ipformation to back up the subject text.

• Activities. Practical exercises for you to tackle to ensure that you have understood the subject matter. Answers to these follow directly, so to get the maximum benefit you should conceal the ariswers whilst attempting each activity.

• Glossary. A glossary of terms (those highlighted in red) found within the chapter.

• Self-check questions. Multiple-choice questions with answers in AppendiX 1 at the back of the book.

• Self-study questions. Longer questions with answers in Appendix 2.

• Case study. To provide a synoptic link between chapters, each chapter has a case study based on a business which starts in Chapter 1 and then devel-

xiii

Preface

xiv

ops and expands throughout subsequent chapters, to form a 'book within a book'. Each case study is self-standing but builds on the knowledge gained in the previous chapters.

• References. Most of the references given are to pages on the World Wide Web. These are to enhance research into particular areas, or else to provide further practical activities. Website references have a habit of changing over time, but with perseverance and the use of search engines such as Google, most sites can be accessed.

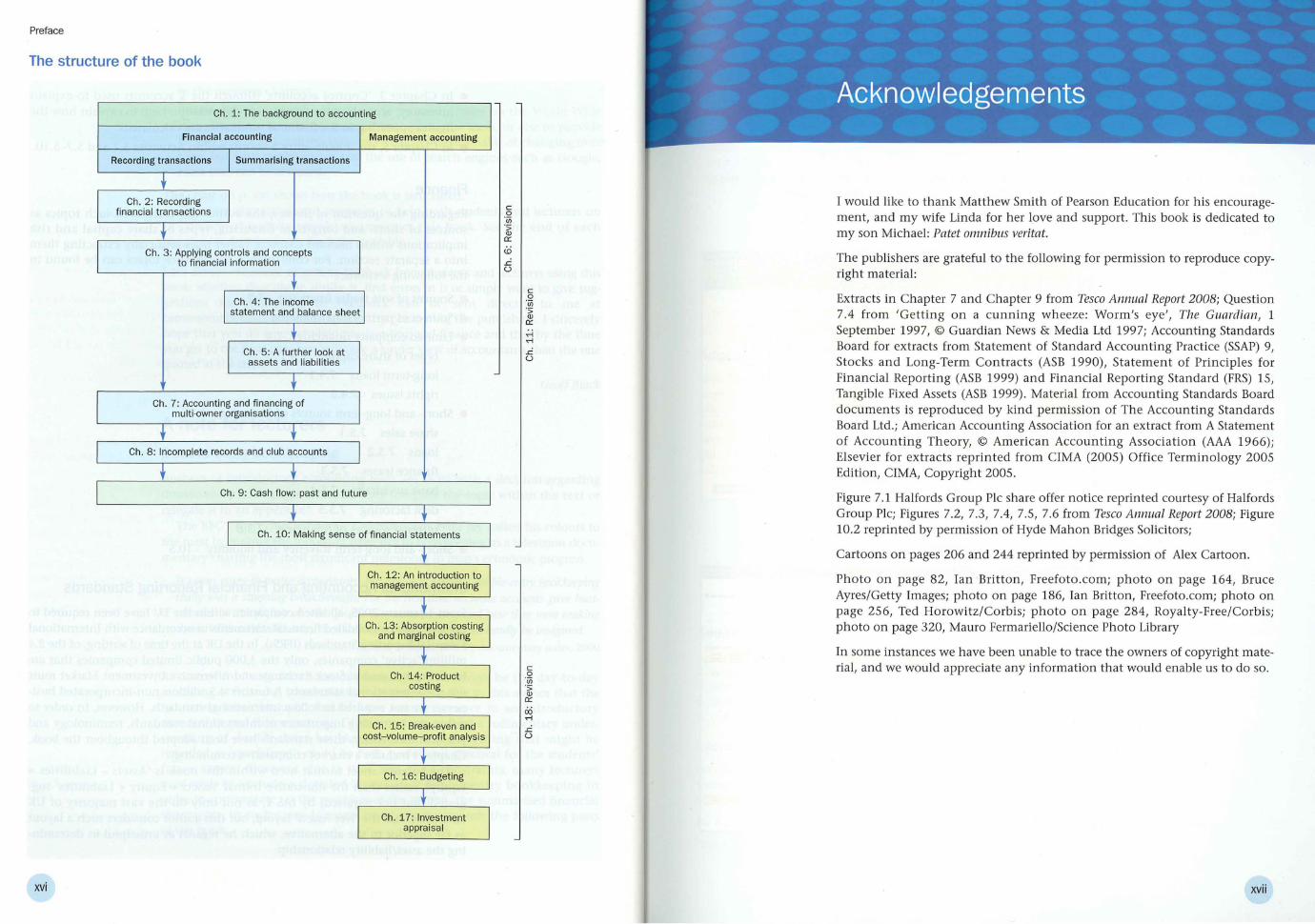

The chart on p. xvi shows how the book is structured. There are also significant resources to help both students and lecturers on

the dedicated website which accompanies this book. See the end of each chapter for details of speCific help available.

I am always interested in getting feedback from students and lecturers using this book, whether they like it, dislike it, find errors in it or simply want to give suggestions for improving it. Feedback can be sent directly to me at commentonbook@googlemai l.com.orbycontactingthepublishers.lsincerely hope that you do enjoy studying accounting and finance and that by the time you get to the final page you will take a kinder view of accountants than the one quoted at the start.

Geoff Black

A note for lecturers

Double-entry bookkeeping

Authors of introductory accounting texts are faced with a decision regarding double-entry bookkeeping. Should they integrate the topic within the text or relegate it to an appendix?

The BBe's then chief economic correspondent Peter Jay nailed his colours to the mast by making the following reference to bookkeeping in a television documentary charting the most significant milestones in man's economic progress:

It seems crazy to praise accountants; but dl)' as it sounds, double-enD), bookkeeping really was a stunning breakthrough. For the first time accurate accounts gave businessmen a Dlle picture of what profits they were making and how they were making them. Without double-enD)' bookkeeping capitalism itself can hardly be imagined.

Peter Jay, The Road to Riches, BBC TV documentary series, 2000

As one of the basic functions of accounting will always be the day-to-day recording of financial transactions, it seems reasonable to this author that the 'stunning breakthrough' should have some relevance to an introductory accounting and finance course. Giving students at least a rudimentary understanding of double-entry bookkeeping (omitting anything that might be regarded as 'specialised') could be both useful and practical for the students' future careers . However, due to time and other constraints, many lecturers may wish to exclude a detailed appraisal of double-entry bookkeeping in order to concentrate on the products of the system, the summarised financial statements. In such cases, lecturers could choose to omit the following parts of the book:

Preface

• Chapter 2 (other than pages 19-22, which can be used for a simple introduction to the topic) .

• In Chapter 3, 'Control accounts' (though the T accounts used to explain inventory, accruals, prepayments and depreciation help to explain how the figures appearing in the financial summaries are calculated) .

• In Chapter 5, the double-entry accounts within Activities 5.1 and 5.7-5.10.

Finance

Regarding the question of finance, the author has integrated such topics as sources of short- and long-term financing, types of share capital and risk implications within relevant chapters, rather than artificially extracting them into a separate section. For convenience, key finance topics can be found in the following sections:

• • •

•

Sources of sole trader financing 7.2

Sources of partnership financing 7.3

Limited company financing 7.4

types of share capital 7.4.1

long-term loans 7.4.1

rights issu,es 7.4.2

Short- and long-term sources of financing

share sales 7.5 .1

loans 7.5.2

finance leases 7.5.3

bank overdrafts 7.5.4

debt factoring 7.5.5

internal sources of financing 7.5.6

7.5

• Short- and long-term solvency and liqUidity 10.5

International Accounting and Financial Reporting Standards

From 1 January 2005, all listed companies within the EU have been required to prepare their consolidated financial statements in accordance with International Financial Reporting Standards (IFRSs). In the UK at the time of writing, of the 2.4 million 'active' companies, only the 3,000 public limited companies that are listed on the London Stock Exchange and Alternative Investment Market must use the international standards. A further 4.5 million non-incorporated businesses are not reqUired to follow international standards. However, in order to reflect the increasing importance of international standards, terminology and practices used within these standards have been adopted throughout the book. Chapter 1 includes a chart of comparative terminology.

The balance sheet format used within this book is 'Assets - Liabilities = Equity', rather than the illustrative format 'Assets::;, Equity + Liabilities' suggested (but not required) by lAS I, as not only do the vast majority of UK enterprises use the 'Net Assets' layout, but this author considers such a layout as far superior to the alternative, which he regards as unhelpful in determining the asset/liability relationship.

xv

Preface

The structure of the book

Ch . 1: The background to accounting

Financial accounting Management accounting

Recording transactions I Summarising transactions

f Ch. 2: Recording

J f inancial transactions

i Ch. 3: Applying controls and concepts

I to financial information

f I Ch. 4: The income I

statement and balance sheet

f

I Ch. 5: A further look at assets and liabil ities

f Ch. 7: Accounting and financing of

multi-owner organisations

f f Ch. 8 : Incomplete records and club accounts

f t Ch. 9 : Cash flow: past and future

xvi

c o 'iii "> Q)

0::

<0

.<: ()

c o 'iii .~

0::

00 ,-i

.<: ()

I would like to thank Matthew Smith of Pearson Education for his encouragement, and my wife Linda for her love and support. This book is dedicated to my son Michael: Patet omnibus veritat.

The publishers are grateful to the following for permission to reproduce copyright material:

Extracts in Chapter 7 and Chapter 9 from Tesco Annual Report 2008; Question 7.4 from 'Getting on a cunning wheeze: Worm's eye', The Guardian, 1 September 1997, © Guardian News & Media Ltd 1997; Accounting Standards Board for extracts from Statement of Standard Accounting Practice (SSAP) 9, Stocks and Long-Term Contracts (ASB 1990), Statement of Principles for Financial Reporting (ASB 1999) and Financial Reporting Standard (FRS) IS, Tangible Fixed Assets (ASB 1999). Material from Accounting Standards Board documents is reproduced by kind permission of The Accounting Standards Board Ltd.; American Accounting Association for an extract from A Statement of Accounting Theory, © American Accounting Association (AAA 1966); Elsevier for extracts reprinted from CrMA (2005) Office Terminology 2005 Edition, CrMA, Copyright 2005.

Figure 7.1 Halfords Group Plc share offer notice reprinted courtesy of Halfords Group Plc; Figures 7.2, 7.3, 7.4, 7.5, 7.6 from Tesco Annual Report 2008; Figure 10.2 reprinted by permission of Hyde Mahon Bridges Solicitors;

Cartoons on pages 206 and 244 reprinted by permission of Alex Cartoon.

Photo on page 82, Ian Britton, Freefoto.com; photo on page 164, Bruce Ayres/Getty Images; photo on page 186, Ian Britton, Freefoto.com; photo on page 256, Ted Horowitz/Corbis; photo on page 284, Royalty-Free/Corbis; photo on page 320, Mauro Fermariello/Science Photo Library

In some instances we have been unable to trace the owners of copyright material, and we would appreciate any information that would enable us to do so.

xvii

MyAccountinglab puts students in control of their own learning through a suite of study and practice tools tied to the online e-book and other media tools. At the core of MyAccountingLab are the following features:

Practice tests

Practice tests for each section of the textbook enable students to test their understanding and identify the areas in which they need to do further work. Lecturers can customise the practice tests or leave students to use the two pre-built tests per chapter.

Personalised study plan

Based on a student's performance on a practice test, a personal study plan is generated that shows where further study needs to focus . This study plan consists of a series of additional practice exercises.

xviii

CD o eeooooooQlc The accounl balances of Mary Bur1c:e's Music Store al Apnl ;J) , 2003 , ale presented to the right.

Req uire d

I. ~e~a:D.t~~'ance sheel oUhe business ill

2. Vlhal does lheb .. rancesheelreport~nancial position 01 operilting resulls?Whichfinancial slal ementrepOrlSlhe Olher infolmalion?

Re qll!! em' n'1 Fdlin lheheildingfor lhe balancesheel

Equipment

Irmntory(stock)

Loan payable

Renl expense

Cashal bank

13,200

5/iO

5,200

'!lJ 1.100

Sales rl!Yenue 13"..,

Accounts receivable 6,200

Accounts payable 3.700

Mary Burke's capital ?

Salary expense 1,l.5(]

Enter .. lI the assets in the first column and their amounts in the second column. Add the assels lo calculate Ihe l olal assel s.

....... , ' ~

Choose from 1m, bt or enter 4ny number en the input fields, then dick "I/e:.t Question" or 'Pre'f' ious Question: ®

<DTf\ •• ~« ... ~. ll .. ~retumtoltj,p'l e .

(%l ,roai<.iMtc-:ia , wllud lolb.ld, «O).

Q'l lO""" ..... _rto,. C'i2f),t.\.onoCt><, u.:r£.:...lW o< .... ~.

@ l bl .l1!tIt ..... 9Yrd ' PMPNrfl ...

@ lb 3·M' M ... n ll" .. • .... m"·<1· ,e ' .... ".,"mftt·"'1on 0 rb ,f'U.,rpr.l""'!lM9N!iI ... ~""Itt! ....... 01

@ l bi· ", flI:lhtt r ........ .,··n;I, ..... llu

@ 'b '·f!crt?'nnd!o"" U'

@ (b l·sen""tedeN",*"st·"'""",·pMlf_Uon.

@ (b l P·.,.H ... ' ..... e IO...."g.! . '!!I ... mh

@ rb ll 'Rc)sdm£bte'um

• $bm .. r( .. II'>,·su ... 1 1t . !!vi. si t ,

() ()

~ () ()

Tieue UllUiz tto TineUml

nmeSlle llc

"'"" ... Pt OIJU!SS

00111 01 10 questions cowplete

r'H l et IlIJl H.·sl~ 1

Wotlh1 poWJt

''''iiM'@-

" Jym. t,!!bus l e ,"' c 4'"t

...... iI."r. 1"1 ... , Q .. ~rtI.". S,cnt

Guided tour of MyAccountingLab

Additional practice exercises

Generated by the student's own performance on a practice test, addit ional practice exercises are keyed to the textbook and provide extensive practice, and link students to the e-book and to other tutorial instruction

resources.

Tutorial instruction

Launched from the additional practice exercises, tutorial instruction is provided in the form of solutions to problems, detailed differential feedback, step-by-step explanations, and other media-based explanations, including key concept animations.

Welcome Hom. Int,riofs began2llll with uphl ofE20JXI). On Juty 12, Rogel Wayn, Oh. ov.ner) irmsted 13JX1) cash in the business. On Septembfl 26, Ihe 0"1\1111 Ir~nsrelle d 10 Ihe company hnd V4th,red it E71!Ol. The income stat@mlml for Ih. yur ended December 31.2007. reponed nH profit ofE&4JX1). During this f.nilKi)! year.lhe O"I\1IerVl;thdr,. .... U,DlJ neh month for pusOAlil ua.

Reqllh emenl: Prepare the part of Welcome Home is1teriols balince i heet shOViin9 changu 10 the O'I'rTIe r's c;lp~al dUfing the year ended Decembef31,:2CO'l.

fled you can c.omple te the part oflhe balince shul ~hO'..r.ng OVIner's cap:ti1 Ohe plrt shO'Mng assets and babilAiu I!n' I~quired). ...

W,Ic.om, Hom, Int"lolS ] I 8alnnc.t.h.II

u i tOecembeI31 , 21X13

I ,

RoguWayne. Capital, 31DeCfmber. 21X13 -rt ~

OVe.t.c.nPI07!ets l

Cost

Additional MyAccountingLab tools

1. Interactive study guide 2. Electronic tutorials 3. Glossary - key terms from the textbook 4. Glossary flashcards 5. Links to the most useful accounting data and information sources on the Internet.

Lecturer training and support

~H~This) [!] KE'/tal((pts )

~U1book~

iii Ciku!a:Of

e AUI'~fIoWudOf_)

iii.~

We offer lecturers personalised training and support for MyAccountinglab. We have a dedicated team of Technology Specialists whose job it is to support lecturers in their use of our media products , Including MyAccountingLab. To make contact with your Technology Specialist please email [email protected] .

For a visual walkthrough of how to make the most of MyAccountingLab, visit www.MyAcountinglab.com.

To f ind details of your local sales representatives go to www.pearsoned.co.uk/replocater.

xix

Objectives When you have read this chapter you will be able to:

~ Explain what is meant by 'accounting'

~ Distinguish between financial accounting and management accounting

~ Identify the main users of accounting information

~ Understand the concepts and principles on which accounting is based

~ Distinguish between assets, liabilities, capital, revenue and expenses

~ Understand the 'accounting equations'

Introduction

This chapter introduces you to the whole area of accounting - what it is, who it is for, and who makes the rules and regulations that govern it. Accounting has a number of divisions, the main two being financial accounting and management accounting. The two areas are explained in this chapter, as well as the concepts and principles that underpin accounting. The chapter also introduces some key terms: assets, liabilities, capital, revenue and expenses, and how they are linked within 'accounting equations'. These equations help us to understand the logical basis of accounting and see how the financial affairs of even the most complex organisation can be summarised and analysed.

1

Chapter 1 The bacl~ground to accounting

2

What is accounting?

You may think that you know nothing at all about accounting, but consider this snippet of conversation:

'Rita wrote her car off yesterday. She'd gone into the red to pay for it, but - would you credit it - the car wasn't insured. There's no accounting for some people. The bottom line is - you need to protect your assets!'

You may be surprised that this contains six separate accounting references! Most of the terms are so familiar that they are used without thinking where they came from. The origins of accounting can in fact be traced back to ancient times, with the need for accurate records of trading transactions. A logical system of recording financial information, known as double-entry bookkeeping, was in use in medieval Italy, and the first published accounting work, Summa de Alithmetica, Geometria, Proportioni et PropOlTIonalita, was written in 1494 by a Venetian monk, Luca Pacioli. The principles of double-entry bookkeeping are still in use today, even where all financial data is processed by computers.

Accounting can be defined simply as the recording, summarising and interpretation of financial information. A more detailed definition is that offered by the American Accounting Association (1966), as follows:

The process of identifying, measuring and communicating economic infOlmation about an OIganisation or other entity, in order to permit informed judgements by users of the information.

The 'key aspects of accounting are therefore identifying, measuring and communicating:

• Identifying the key financial components of an organisation, such as assets, liabilities, capital, revenue, expenses and cash flow.

• Measuring the monetary values of the key financial components in a way which represents a true and fair view of the organisation.

• Communicating the financial information in ways that are useful to the users of that information.

Who needs accounting?

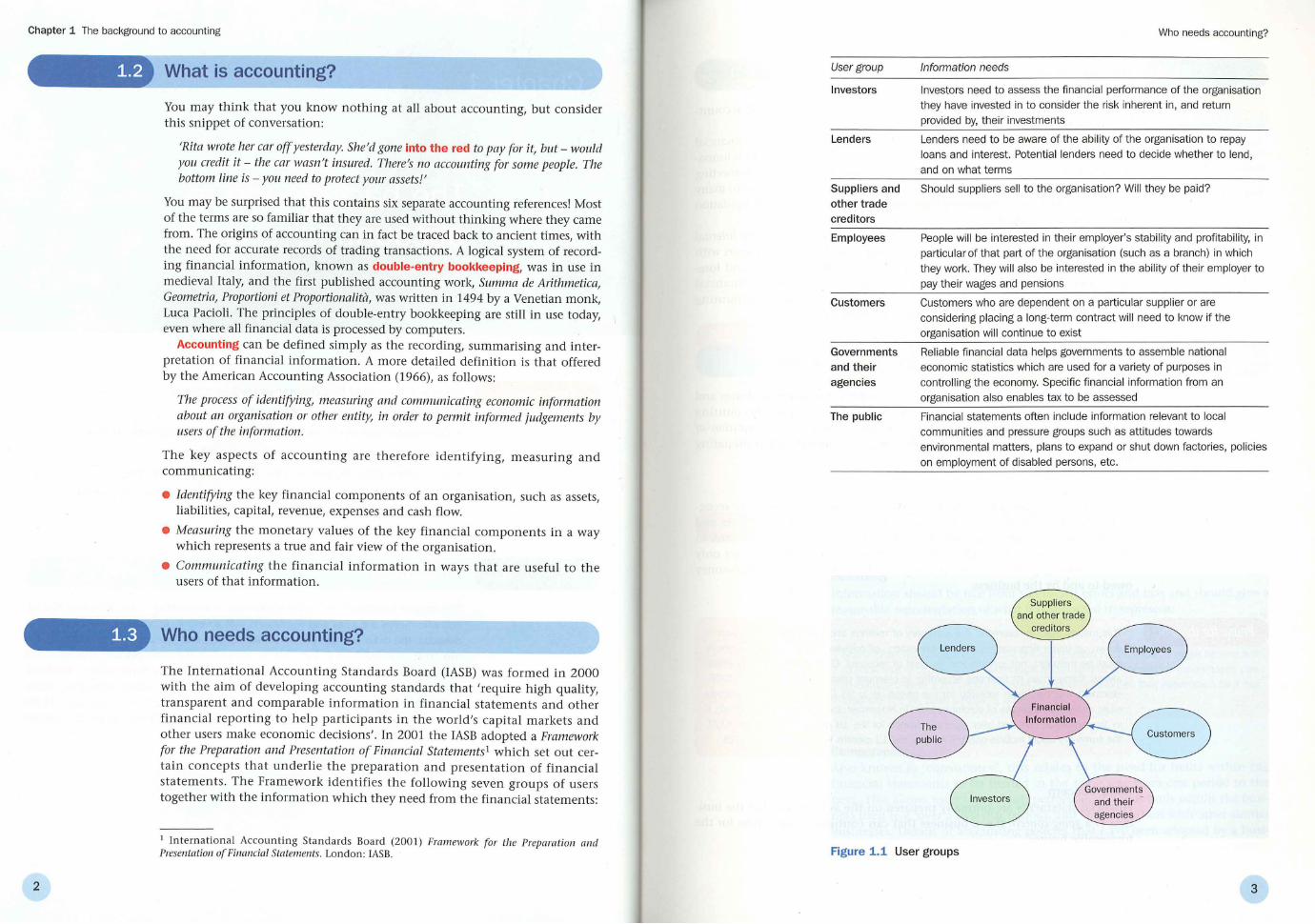

The International Accounting Standards Board (IASB) was formed in 2000 with the aim of developing accounting standards that 'require high quality, transparent and comparable information in financial statements and other financial reporting to help participants in the world's capital markets and other users make economic decisions' . In 2001 the IASB adopted a Framework for the Preparation and Presentation of Financial Statements1 which set out certain concepts that underlie the preparation and presentation of financial statements. The Framework identifies the following seven groups of users together with the information which they need from the financial statements:

1 International Accounting Standards Board (2001) Framework for the Preparation and Presentation ofFinanciai Statements. London: IASB.

User group

Investors

Lenders

Suppliers and

other trade creditors

Employees

Customers

Governments

and their

agencies

The public

Who needs accounting?

Information needs

Investors need to assess the financial performance of the organisation they have invested in to consider the risk inherent in, and retum

provided by, their investments

Lenders need to be aware of the ability of the organisation to repay

loans and interest. Potential lenders need to decide whether to lend,

and on what terms

Should suppliers sell to the organisation? Will they be paid?

People will be interested in their employer's stability and profitability, in

particular of that part of the organisation (such as a branch) in which

they work. They will also be interested in the ability of their employer to

pay their wages and pensions

Customers who are dependent on a particular supplier or are

considering placing a long-term contract will need to know if the

organisation will continue to exist

Reliable financial data helps governments to assemble national

economic statistics which are used for a variety of purposes in

controlling the economy. Specific financial information from an

organisation also enables tax to be assessed

Financial statements often include information relevant to local

communities and pressure groups such as attitudes towards

environmental matters, plans to expand or shut down factories, policies

on employment of disabled persons, etc.

The public

Suppliers and other trade

creditors

Figure 1.1 User groups

3

Chapter 1 The background to accounting

Did you know?

The Chartered Institute of Management Accountants, founded in 1919, has over 164,000 members and students in 161 countries.

Pause for thought

4

Financial accounting and management accounting

Accounting information can be classified broadly between financial accounting and management accounting.

Financial accounting is the day-to-day recording of an organisation's financial transactions and the summarising of those transactions to satisfy the information needs of the user groups listed above. It is sometimes referred to as meeting the external accounting needs of the organisation, and as such is subject to many rules and regulations (a regulatory framework) imposed by company legislation and accounting standards.

Management accounting is sometimes referred to as meeting the internal accounting needs of the organisation, as it is designed to help managers with decision making and planning. As such it often involves estimates and forecasts, and is not subject to the same regulatory framework as financial accounting. Chapters 12-17 explore some of the management accounting areas such as marginal costing and break-even analysis.

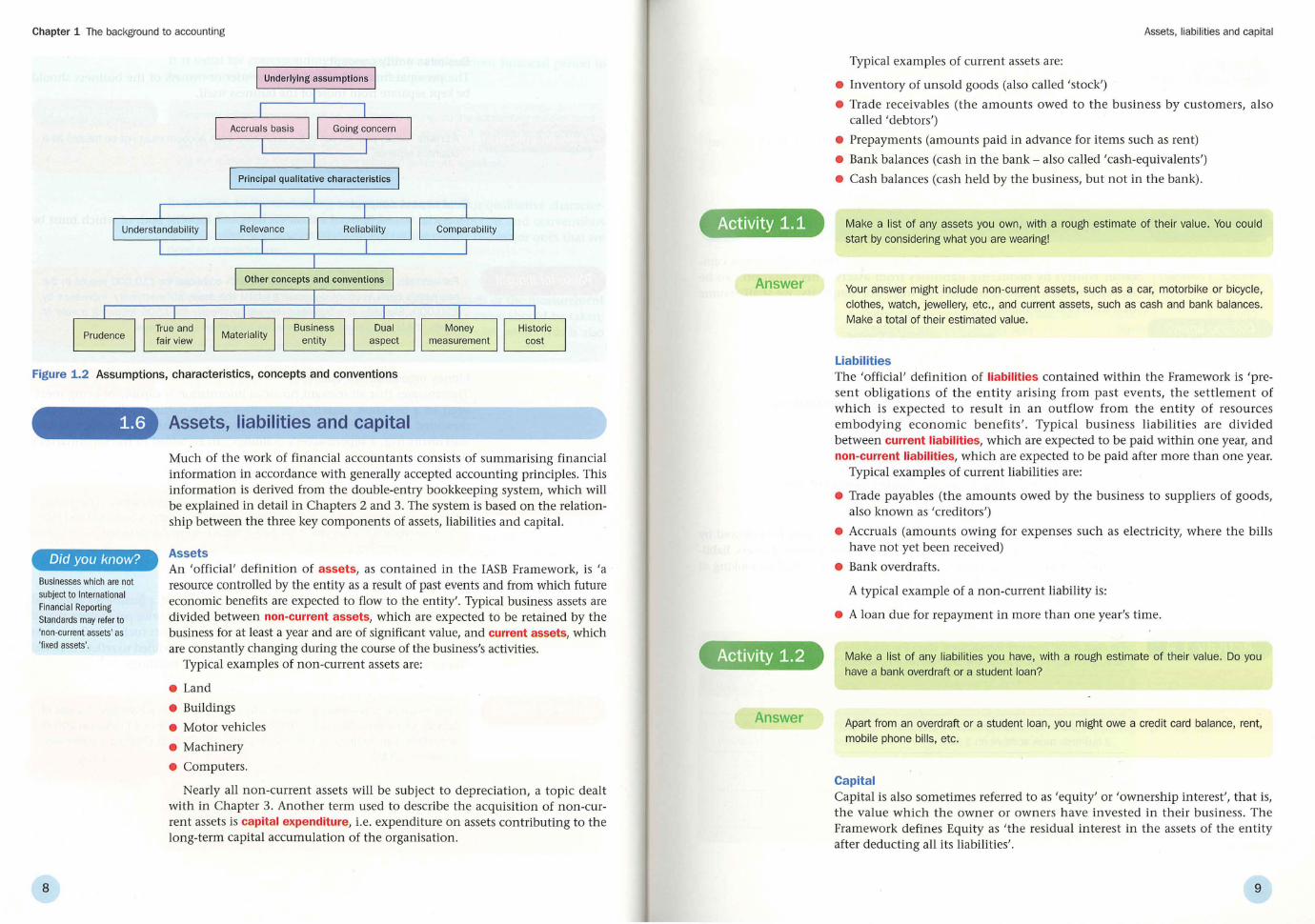

Accounting assumptions and characteristics

Accounting procedures and practices have evolved over many centuries and are now known by the acronym GAAP (Generally Accepted Accounting P~inci~les) . The lASE's Framework for the Preparation and Presentation of Fmanczal Statements refers to two underlying assumptions when preparing financial statements:

The Accruals basis ~hen preparing financial statements, the effects of transactions are recogmsed when they occur and are recorded in the accounting records and reported in the financial statements of the periods to which they relate. In practice, this means that (other than for cash flow information) we not only consider money paid and received in a particular time period, but also money owed to and by the business.

This means that, for example, if a summary of revenue and expenditure for a year is drawn up under financial accounting principles, all relevant revenues and expenses must be included, not just the money paid or received. Consider a company which always summarises its finances according to calendar years. If, by the end of 2008, electricity bills had been received for the period up to 31 October only, the summary must include an estimate of electricity used in November and December. Conversely, if in January 2008 rent had been paid in advance for the 18 months to 30 June 2009 the summary would include only the rent for the 12 months to 31 December 2008. '

Going concern Financial statements are normally prepared on the assumption that the business is a going concern (i.e. a business that can continue in operation for the foreseeable future) .

Pause for thought

Pause for thought

Pause for thought

Pause for thought

Accounting assumptions and characteristics

We would have to be told if a business is in severe financial difficulties, but under normal circumstances we do not need to assume that the business is in any immi

nent danger of failing.

In addition to the two underlying assumptions, the Framework also lists a number of qualitative characteristics of financial statements which make the information provided useful to the user groups. The four principal characteristics are understandability, relevance, reliability and comparability.

Understandability Information provided in financial statements should be readily understandable by users. However, users are assumed to have a reasonable knowledge of business and economic activities and accounting and a willingness to study the information with 'reasonable diligence'.

Particularly for large and complex businesses, very detailed explanations of financial procedures and transactions are provided which might need very specialised knOWl

edge to understand.

Relevance The financial information must be relevant to the decision-making needs of users. For example, if there have been major abnormal transactions in the current year, it would be helpful to disclose them separately, so that we can then assess year-to-year profit trends based on the 'normal' activities.

In other words, if information is irrelevant, what is the point of producing it?

Reliability Information should be free from significant errors and bias and should give a reasonable representation of what it is supposed to represent.

Some information might be relevant but not reliable. For example, it might be relevant to know that a company has taken legal action against a competitor for damages due to infringement of a copyrighted design, but how reliable can that information be if the

case has not yet been settled by a court?

Comparability Also known as 'conSistency', this relates to the need for items within the financial statements to be treated in the same way from one period to the next. This allows users to establish performance trends both within the business itself (e.g. over a five-year period), and by comparison with other similar businesses. Details of accounting policies that have been adopted by a business are disclosed when presenting financial statements. To aid compatibility,

5

Chapter 1 The background to accounting

Pause for thought

Pause for thought

Pause for thought

Pause for thought

6

it is usual for corresponding information for the previous financial period to be presented alongside that for the current period.

Financial information must not be consistently wrong, so the accounting policies used by a business can be changed if appropriate. For example, if an asset was incorrectly valued last year, a correction can be made this year provided that information regarding the reasons for the change in the valuation policy are explained.

In addition to the underlying assumptions and the four qualitative characteristics of financial statements, a number of other concepts and conventions influence the way in which information is presented. The major ones that we need to consider are:

Prudence

Accountants should be cautious in the valuation of assets or the measurement of profit. The lowest reasonable estimate of an asset's value should be taken whilst a forecast loss would be included but not a forecast profit. This is als~ known as the 'conservatism' principle.

The prudence principle is of great importance to users of the accounting information, as it ensures that the accounting summaries have not been drawn up on the basis of over-optimistic or speculative forecasts, and that foreseeable losses and expenses have been included.

True and fair view

The overall aim of the financial statements should be to present a true and fair view of the business's financial position and performance. Truth and fairness are difficult concepts to define . However, if the financial statements follow the principal qualitative characteristics described above and also follow relevant laws and accounting standards then this normally results in a 'true and fair view' .

For large businesses, an independent report from a firm of auditors will state whether in their opinion, the financial statements show a 'true and fair view'. '

Materiality concept

Materiality refers to the significance of information contained within financial statements. It is considered significant if its inclusion could influence the economic decisions of the users.

If information is immaterial, then it does not need to be disclosed separately, or in any other way that gives it undue significance. For example, if a business's communications budget consisted of £10,000 paid for mobile phone usage and £20,000 paid for other phone calls, this could be amalgamated as one total of £30,000 without any effect on the value of the information to users.

Pause for thought

Pause for thought

Pause for thought

Pause for thought

Accounting assumptions and characteristics

Business entity concept The personal financial affairs of the owner or owners of the business should be kept separate from those of the business itself.

A private holiday paid for out of the business's bank account must not be treated as a business expense.

Dual aspect concept Financial transactions of a business have two aspects, both of which must be shown within the financial recording system.

For example, a business buying a machine with a cheque for £10,000 results in the business's bank account decreasing whilst the asset of 'machinery' increases by £10,000. Similarly, if a business receives a cheque for £500 following a sale of goods, the bank account will increase but inventories will decrease.

Money measurement concept This assumes that all relevant financial information is capable of being measured in a common currency, regardless of the nature of the items being measured. This enables dissimilar items to be aggregated within the financial statements (e.g. a supermarket's buildings can be added to the supermarket's delivery lorries) .

Not everything that affects a business can be measured in money terms. For example, how do you measure the value of a dynamic managing director, a contented and productive workforce or a poor record of dealing with customers' complaints?

Historic cost concept Under this concept, when presenting a statement of a business 's financial position, the values of assets are based on the original price paid rather than a subsequent valuation which adjusts the value for factors such as inflation. As we shall see later in the book, this concept is often modified to reflect material changes in significant assets - particularly land and buildings.

What would be a true and fair view of a business's assets, if it had bought a plot of land for £1 million in 2001, and that land had a market value of £4 million in 2008? It would be hard to argue that the historic cost of £1 million reflected a reasonable valuation in 2008!

7

Chapter 1 The background to accounting

Principal qualitative characteristics

Other concepts and conventions

Figure 1.2 Assumptions, characteristics, concepts and conventions

Did you know?

Businesses which are not subject to International Financial Reporting Standards may refer to 'non-current assets' as 'fixed assets'.

8

Assets, liabilities and capital

Much of the work of financial accountants consists of summarising financial information in accordance with generally accepted accounting principles. This information is derived from the double-entry bookkeeping system, which will be explained in detail in Chapters 2 and 3. The system is based on the relationship between the three key components of assets, liabilities and capital.

Assets An 'official' definition of assets, as contained in the IASB Framework, is 'a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity' . Typical business assets are divided between non-current assets, which are expected to be retained by the business for at least a year and are of significant value, and current assets, which are constantly changing during the course of the business's activities.

Typical examples of non-current assets are:

• Land • Buildings

• Motor vehicles

• Machinery

• Computers.

Nearly all non-current assets will be subject to depreciation, a topic dealt with in Chapter 3. Another term used to describe the acquisition of non-current assets is capital expenditure, i.e. expenditure on assets contributing to the long-term capital accumulation of the organisation.

Activity 1.1

Answer

Activity 1.2

Answer

Assets, liabilities and capital

Typical examples of current assets are:

• Inventory of unsold goods (also called 'stock')

• Trade receivables (the amounts owed to the business by customers, also called 'debtors')

• Prepayments (amounts paid in advance for items such as rent)

• Bank balances (cash in the bank - also called 'cash-equivalents')

• Cash balances (cash held by the business, but not in the bank).

Make a list of any assets you own, with a rough estimate of their value. You could start by considering what you are wearing!

Your answer might include non-current assets, such as a car, motorbike or bicycle, clothes, watch, jewellery, etc., and current assets, such as cash and bank balances. Make a total of their estimated value.

Liabilities The 'official' definition of liabilities contained within the Framework is 'present obligations of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits'. Typical business liabilities are divided between current liabilities, which are expected to be paid within one year, and non-current liabilities, which are expected to be paid after more than one year.

Typical examples of current liabilities are:

• Trade payables (the amounts owed by the business to suppliers of goods, also known as 'creditors')

• Accruals (amounts owing for expenses such as electricity, where the bills have not yet been received)

• Bank overdrafts.

A typical example of a non-current liability is:

• A loan due for repayment in more than one year's time.

Make a list of any liabilities you have, with a rough estimate of their value. Do you have a bank overdraft or a student loan?

Apart from an overdraft or a student loan, you might owe a credit card balance, rent, mobile phone bil ls, etc.

Capital Capital is also sometimes referred to as 'equity' or 'ownership interest', that is, the value which the owner or owners have invested in their business. The Framework defines Equity as 'the residual interest in the assets of the entity after deducting all its liabilities' .

9

Chapter 1 The background to accounting

Activity 1.3

Answer

Did you know?

Another acceptable version of the formula followed when producing the balance sheet is:

Non-current Assets +

Current Assets

Liabilities + Capital

However, this version is not common in the UK.

Activity 1.4

10

Deduct the total of your liabilities which you found in Activity 1 .2 from the total assets

found in Activity 1.1.

If your assets exceed your liabilities, you have positive capital. If your liabilities exceed

your assets, you have negative capital.

The accounting equation

As we have seen, we find the value of the owner's interest (known as capital or equity) by deducting liabilities from assets. This equation can be represented in a number of different ways (for simplicity, we shall assume that assets exceed liabilities) :

or

or

Assets - Liabilities = Capital

Non-current Assets + (Current Assets) - (Current Liabilities

+ Non-current Liabilities) = Capital

(Non-current Assets + Current Assets - Current Liabilities) - Non-current Liabilities= Capital

This final version of the accounting equation is the one usually followed by accountants in the UK when preparing the financial summary of assets, liabilities and capital, which is known as a balance sheet. We shall be looking at balance sheets in detail in Chapter 4.

Now attempt Activity 1.4.

For each of the following transactions, show the effect (as pluses and minuses) on

assets, liabilities and capital. The first has been completed for illustration.

Assets Liabilities Capital

£ £ £

1 Owner starts business with £3,000 paid into +3,000 +3,000 a business bank account on 1 April (bank) (capita l)

2 Business buys machinery with a cheque for

£800 on 2 April

3 Business buys office computer for £800 on

credit from Lupin pic on 4 April

Answer

Pause for thought

The accounting equation

4 On 5 April, business borrows £10,000 on

loan from a bank. Money is paid into

business's bank account

5 Business pays Lupin pic £800 by cheque

on 6 April

6 Owner takes £100 from bank for personal

spending money

Summary (overall change)

Assets Liabilities Capital

£ £ £

1 Owner starts business with £3,000 paid into +3,000 +3,000 a business bank account on 1 April (bank) (capital)

2 Business buys machinery with a cheque for +800 £800 on 2 April (machinery)

-800 (bank)

3 Business buys office computer for £800 +800 +800 on credit from Lupin pic on 4 April (computer) (creditor:

Lupin pic)

4 On 5 April, business borrows £10,000 on +10,000 +10,000 loan from a bank. Money is paid into (bank) (loan)

business's bank account

5 Business pays Lupin pic £800 by cheque -800 -800 on 6 April (bank) (creditor:

Lupin pic)

6 Owner takes £100 from bank for personal - 100 - 100 spending money (bank) (capital)

Summary (overall change) +12,900 +10,000 +2,900

Applying the accounting equation, A - L = C, we see that the overall change in assets

(£12,900) less the change in liabilities (£10,000) is matched by the change in

capital (£2,900).

1.7.1 How does the value of capital change?

The owner's investment will change for a number of reasons, most obvious of which is if more capital is contributed by the owner, or capital is withdrawn by the owner. However, the other main reason is the business making either a profit or a loss. We calculate profit or loss by comparing a business's Revenue with its Expenses.

11

Chapter 1 The background to accounting

12

• If Revenue exceeds Expenses, the business makes a profit, and the owner's capital increases .

• If Expenses exceed Revenue, the business makes a loss, and the owner's capital decreases.

Revenue and Expenses are defined as follows :

• Revenue: The revenue generated by the business by selling its goods or services, plus any sundry income such as bank interest received.

• Expenses: The expenditure made by a business related to the revenue generated within the same financial period. The cost of non-current assets is /lot considered as an expense, as the assets last for several financial periods. However, an estimate is made, known as depreciation, of the proportion of the non-current asset's value used up in the specific financial period. This loss in value is then treated as an expense when calculating the profit or loss and is also deducted from the non-current assets value in the balance sheet.

Remember that the accruals basis tells us to include all the Revenue and Expenses for a period, not just cash received or paid in that period.

The comparison of Revenue and Expenses leads us to another set of equations, the first of which is:

Revenue - Expenses = Profit

(assuming that revenue exceeds expenses) . This formula is represented in another main financial summary, the income

statement, which we shall be looking at in detail in Chapter 4. If we combine the accounting equations for capital and profit, we see that

the capital figure grows over a specific period (known, in algebraic terms, as from time zero to time one) as follows:

that is, total assets minus total liabilities equal capital at time zero. If a profit is made during time one:

i.e. total assets at the end of time one minus total liabilities at the end of time one equal capital at the start (time zero) plus the profit (revenue less expenses) earned during time one.

The two financial summaries which have been referred to - the balance sheet and the income statement - reflect this formula, as shown in Figure 1.3.

Assets - Liabilities = Capital + (Revenue - Expenses) \ ) \~---,~--~

t t Balance sheet Income statement

Figure 1.3 How the accounting equation relates to the balance sheet and income statement

Did you know?

You can remember this formula with the mnemonic 'All Elephants Like Chocolate Rolls'.

Changes in terminology

When, in the next chapter, we see how financial transactions are recorded by using the double-entry bookkeeping system, we are using a rearrangement of this formula, as follows:

A+E=L+C+R

where assets and expenses are seen to equal liabilities, capital and revenue.

Summary

We have seen four equations in this chapter:

1 Balance sheet equation Assets - Liabilities = Capital

2 Profit equation Revenue - Expenses = Profit

3 1 and 2 combined Assets - Liabilities = Capital + (Revenue - Expenses)

4 Double·entry equation (same as 3 but in a different order)

Assets + Expenses = Liabilities + Capital + Revenue

Changes in terminology

In recent years, there has been a requirement for most large businesses to implement International Accounting Standards (lASs) when recording and presenting their financial information. This has resulted in many changes to once-familiar terms, which are still used by smaller enterprises and in day-today financial language. For consistency, and to reflect the increasing importance and influence of lASs, terminology used in lASs is used throughout this book where relevant. The following is a gUide to some of these changes in terminology:

Older terminology

Creditors

Debtors

Fixed assets

Long-term liabilities

Profit and loss account

Stock (of unsold goods and materials')

Newer terminology

Trade payables (or 'payables')

Trade receivables (or 'receivables')

Non-current assets

Non-current liabilities

Income Statement

Inventories

13

Chapter 1 The background to accounting

1.10 Glossary

Accounting The process of identifying, measuring and communicating economic information about an organisation or other entity, in order to permit informed judgements by users of the information.

Accounting equation The formula representing the relationship between a business's assets, liabilities and capital, usually expressed as A - L = C or, when extended to include revenue and expenses, A + E = L + C + R.

Assets A resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity.

Balance sheet A financial summary showing the assets, liabilities and capital at a specific date.

Bookkeeping The process of recording financial transactions.

Capital The value of the investment of the owner or owners in the business, found by deducting all of the organisation's liabilities from all of the organisation's assets. Also known as 'equity'.

Capital expenditure Another term for non-current assets.

Current asset An asset whose value constantly changes during the course of a business's activities.

Current liability A liability expected to be paid within one year of the date of the balance sheet.

Depreciation An estimate of the loss in value of a non-current asset.

Double-entry The system, first described by Luca Pacioli in 1494, which allows a logical record to be bookkeeping made of all the components of the accounting equation.

Equity Another term for 'capital'.

Expenses Expenditure made by a business related to the revenue generated within the same financial period. It includes goods bought for resale, and overheads such as light and heat, wages and salaries.

Financial accounting The day-to-day recording of an organisation's financial transactions and the summarising of those transactions to satisfy the information needs of various user groups in accordance with the regulatory framework.

Income statement A financial summary showing revenue and expenses for the financial period.

'In the red' In the days before computers, banks used to use red ink to show overdrawn balances, hence you were 'in the red' if you had an overdraft.

Key concepts Important principles underlying the preparation of financial summaries.

Liabilities Present obligations of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.

Management accounting The internal accounting needs of an organisation, involving planning, forecasting and budgeting for decision-making purposes.

Non-current assets Assets which are normally expected to be retained by the business for at least a year from the date of the balance sheet and are of a significant value. Most are subject to depreciation. Also referred to as 'capital expenditure' or 'fixed ' assets.

Non-current liability A liability expected to be paid more than one year after the balance sheet date.

Regulatory framework The rules and regulations followed by financial accountants, imposed mainly by company legislation and Accounting Standards Boards.

14

Self-check questions

Revenue The revenue generated by the business by selling its goods or services, plus sundry income such as interest received.

True and fair view An important accounting concept, requiring financial summaries to reflect truth and fairness in their representation of the organisation 's affairs.

1 Financial accounting is: a Mainly concerned with forecasting the future b Used only by the management of the business c Used only by people outside the business d Used by people both inside and outside the business

2 The key aspects of accounting are:

a Identifying, measuring and communicating economic information b Processing, recording and publishing financial information c SummariSing, analysing and interpreting business information d Conveying inside information about the company to the owners

3 A steward is:

a The accountant of the organisation b The owner of the organisation c A trusted person who manages an organisation for others d A security guard who patrols the organisation's premises

4 Which one of the following is an underlying accounting assumption? a Relevance b Going concern c Prudence d Reliability

5 Non-current assets are assets which are:

a Likely to last at least a year and are valuable b Not going to be depreciated c Unlikely to last a year d The unsold goods of the business

6 Current assets are assets which: a Keep their value over at least a year b Constantly change their value c Are depreciated d Sometimes change their value

7 Liabilities are usually divided between: a Urgent and non-urgent b Fixed and current c Current and non-current d Medium-term and long-term

8 A bank overdraft is usually classified as: a A current asset b A non-current liability

15

Chapter 1 The background to accounting

16

c A current liability

d Capital

9 The accounting equation can be shown as:

a Capital - Liabilities = Assets

b Capital + Assets = Liabilities

c Assets + Liabilities = Capital

d Assets - Liabilities = Capital

10 Which of the following will not result in a change in the owner's capital?

a A non-current asset bought by the business for £10,000 b A profit made by the organisation

c A loss made by the organisation d The owner withdrawing £5,000 from the organisation

(Answers in Appendix 1)

(Answers in Appendix 2)

Question 1.1 Using your knowledge of the accounting equation, fill in the white boxes in the following

table (all figures in f):

Assets Liabilities Capital

£ £ £

1 25,630 14,256

2 I 23,658 15,498

3 619,557 352,491 I I 4 69,810 14,863

5 I I 21,596 35,462

6 36,520 24,510

7 I I 65,342 86,290

8 114,785 17,853

9 212,589 146,820

10 I I 63,527 201,581

Totals I I

Self-study questions

Question 1.2 a For each of the following transactions, show the effect (as pluses and minuses) on

assets, liabilities and capital. The first has been completed for illustration.

Question 1.3

1 Owner starts business with £10,000 paid

into a business bank account on 1 May

2 Business buys furniture with a cheque for

£2,500 on 2 May

3 Business pays £600 by cheque for a photocopier on 4 May

4 Business receives an invoice on 5 May

from Chambers Ltd for £2,000 for inventory

5 Also on 5 May, the business buys inventory

with a cheque for £600

6 Owner takes £400 from banl~ for

personal spending money on 6 May

7 On 7 May, the business pays the invoice

received from Chambers Ltd on 5 May

8 On 8 May, the business receives an invoice

for £4,000 for a second-hand motor van

Summary (overall change)

Assets

£

+£10,000

Bank

b From the above table, complete the following equation:

Overall change in assets

Less overall change in liabilities

Overall change in Capital

Liabilities

£

c What is the name given to the formula Assets - Liabilities = Capital?

Capital

£

+£10,000

Capital

The annual report of a major public limited company included the following statement:

Going concern The directors consider that the group and the company have adequate resources to remain in operation for the foreseeable future and have therefore continued to adopt the going concern basis in preparing the financial statements. As with all business forecasts the directors' statement cannot guarantee that the going concern basis will remain appropriate given the inherent uncertainty about future events.

(Tesco pic Annual Report 2008)

a Explain why the going concern principle is of importance to a user of an annual report.

b Explain the meaning of I\ccruals' as an underlying assumption when preparing financial

statements, and the qualitative characteristics of 'Comparability' and 'Prudence'.

c Explain why a 'true and fair view' is of particular importance when presenting financial statements.

17

Chapter 1 The background to accounting

18

,/ Marvin makes a career choice

References

Marvin always had an ambition to be a magician. As a child he took great delight in mal(ing his younger brothers and sisters disappear and he was often in demand to perform conjuring tricl(s at birthday parties. It was a natural career choice for him when, at the age of 21, he decided to leave college on 1 July 2004 and make his fortune in the world , setting up in business as a magician. He made the following payments in his first week out of college.

On 1 July he paid £3,000 for a glittering costume with a top hat and cloak; on 2 July he paid £2,000 for a special edition of a book, 'The ancient secrets of magic'; and on 3 July he bought four packs of magicians' playing cards from Kazam Limited for £100 each. Marvin expected to use these items for many years. He paid cash from his own savings for the costume and the book, but he agreed that he would pay for the playing cards in a few weeks' time from the business bank account.

His first appearance as a magician was on 7 July at the Skittleborough Magic Show, for which he was paid a fee of £750 by cheque , with which he opened a business bank account on the same day. He incurred £20 travel expenses which he again paid from his own savings.

Required: a Prepare a summary of Marvin's income and expenses for the week ended 7 July. Ignore

any depreciation on Marvin 's assets.

b Draw up a list as at 7 July of Marvin 's non-current assets and current assets, then deduct any current liabilities from the assets. What is Marvin's capital at that date? Show how you can prove that the capital figure is correct.

(Answers in Appendix 3)

Professional accountancy bodies

International Accounting Standards Board: www.iasb.org

Institute of Chartered Accountants in England and Wales: www.icaew.com

Chartered Institute of Management Accountants: www.cimaglobal.com

Association of Chartered Certified Accountants: www.accaglobal.com

Now check your progress in your personal Study Plan

~Objectives ><L.>-. When you have read this chapter you will be able to:

>- Understand the concept of double-entry bookkeeping

>- Apply the concept of double-entry bookkeeping to the recording of financial transactions

>- Prepare a simple trial balance whilst appreciating its limitations

>- Understand the role of the books of prime entry and ledgers which comprise the double-entry bookkeeping system

Introduction

In the previous chapter, the accounting equation showed us that

Assets + Expenses = Liabilities + Capital + Revenue

Records of financial transactions of the vast majority of commercial organisations are

made according to the double-entry bookkeeping system, which is based on this equation. The system is highly structured and logical and enables even the largest organisation to keep track of its financial position over time.

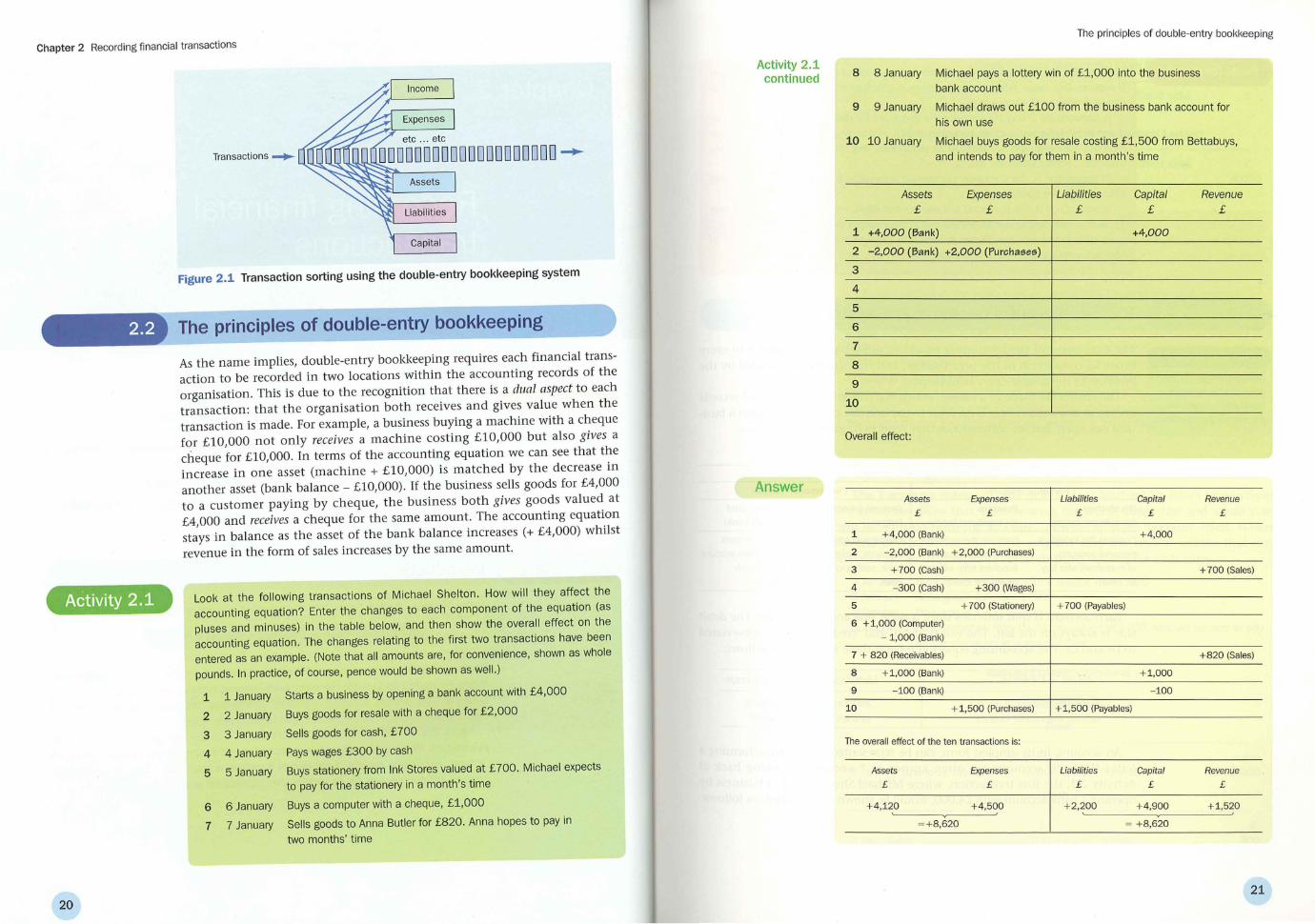

Figure 2.1 shows how transactions are sorted into the key categories of financial information. When each transaction is recorded in the system, the relevant effect on income, expenses, assets, liabilities and capital is recorded. This is an endless process which continues for as long as the organisation is in existence.

19

Chapter 2 Recording financial transactions

Activity 2.1

20

Transactions ~

Figure 2.1 Transaction sorting using the double·entry bookkeeping system

The principles of double-entry bookkeeping

As the name implies, double-entry bookkeeping requires each financial transaction to be recorded in two locations within the accounting records of the organisation. This is due to the recognition that there is a dual aspect to each transaction: that the organisation both receives and gives value wh en the transaction is made. For example, a business buying a machine with a cheque for £10,000 not only receives a machine costing £10,000 but also gives a cheque for £10,000. In terms of the accounting equation we can see that the in crease in one asset (machine + £10,000) is matched by the decrease in another asset (bank balance - £10,000). If the business sells goods for £4,000 to a customer paying by cheque, the business both gives goods valued at £4,000 and receives a cheque for the same amount. The accounting equation stays in balance as the asset of the bank balance increases (+ £4,000) whilst revenue in the form of sales increases by the same amount.

Look at the following transactions of Michael Shelton. How will they affect the accounting equation? Enter the changes to each component of the equation (as pluses and minuses) in the table below, and then show the overall effect on the accounting equation. The changes relating to the first two transactions have been entered as an example. (Note that all amounts are, for convenience, shown as whole

pounds. In practice, of course, pence would be shown as well.)

1 1 January Starts a business by opening a bank account with £4,000

2 2 January Buys goods for resale with a cheque for £2,000

3 3 January Sells goods for cash, £700

4 4 January Pays wages £300 by cash

5 5 January Buys stationery from Ink Stores valued at £700. Michael expects

to pay for the stationery in a month's time

6 6 January Buys a computer with a cheque, £1,000

7 7 January Sells goods to Anna Butler for £820. Anna hopes to pay in

two months' time

Activity 2.1 continued

Answer

The principles of double-entry bool<keeping

8 8 January Michael pays a lottery win of £1,000 into the business bank account

9 9 January Michael draws out £100 from the business bank account for his own use

10 10 January Michael buys goods for resale costing £1,500 from Bettabuys, and intends to pay for them in a month's time

Assets Expenses Liabilities Capital Revenue £ £ £ £ £

1 +4,000 (Bank) +4,000

2 2,000 (Bank) +2,000 (Purcha6e6)

3

4

5

6

7

8

9

10

Overall effect:

Assets Expenses Liabilities Capital Revenue

£ £ £ £ £

1 + 4,000 (Bank) + 4,000

2 - 2,000 (Bank) + 2,000 (Purchases)

3 +700 (Cash) + 700 (Sales)

4 300 (Cash) +300 (Wages)

5 + 700 (Stationery)

6 +1,000 (Computer)

- 1,000 (Bank)

7 + 820 (Receivables)

8 + 1,000 (Bank)

9 - 100 (Bank)

10 +1,500 (Purchases)

The overall effect of the ten transactions is:

Assets

£

Expenses

£

+ 4,120 +4,500

=+8,620

+ 700 (Payables)

+ 820 (Sales)

+1,000

100

+ 1,500 (Payables)

Liabilities Capital Revenue

£ £ £

+ 2,200 +4,900 + 1,520

= +8,620

21

Chapter 2 Recording financial transactions

Pause for thought

Did you know?

Readers whose course does not cover detailed bool(keeping can omit the rest of this chapter.

22

In transactions 1 and 8 , Michael is increasing the value of his capital , but transaction 9 reduces this value. When an owner takes out money or goods from the organisation, it is referred to as 'drawings'.

In transactions 2 and 10, because the goods are for resale, they are referred to as 'purchases'. Expenses such as stationery, petrol, and so on, which are used up in running the business, are not classed as purchases, but might be entered as 'office

expenses', 'motor expenses' etc. In transaction 5, the stationery company is a payable (or creditor), a liability, until

Michael pays the amount owing. In transaction 6, the computer is a non-current asset, not an expense (see Chapter

1), as it is expected to last for several accounting periods and is of substantial value. In transaction 7, Anna Butler is Michael's receivable (or debtor), an asset of

Michael, until she pays the amount she owes.

The double-entry bookkeeping system

The dual aspect of the accounting equation, as we have seen, applies to every financial transaction of the organisation, and this should be recorded by the business in the double-entry bookkeeping system.

The entries are made in a ledger, which is a collection of individual records known as accounts. There is no limit to the number of accounts which a business can open, but for convenience they tend to be grouped as follows:

Accounts grouped within :

('Personal' ledgers) (,Impersonal' ledger)

Receivables Payables General (or nominal) Cash book (and (or debtors) ledger (or creditors) ledger ledger petty cash book)

Contains the individual personal accounts

Contains the individual Contains all other Contains the bank

of customers who buy on credit

personal accounts of suppliers from whom we buy on credit

accounts, except account, cash account bank, cash and petty and petty cash cash account

Each account is split into two sides, a debit side and a credit side. The debit side is always on the left. The words 'debit' and 'credit' are often abbreviated to Dr and Cr. The accounting equation reflects these two sides, as follows:

Assets + Expenses

Accounts with more debit entries than credit entries

Liabilities + Capital + Revenue

Accounts with more credit entries than debit entries

An account, in its simplest form, can be represented by two lines, forming a letter 'T'. Such accounts are often known as T accounts. Looking back at

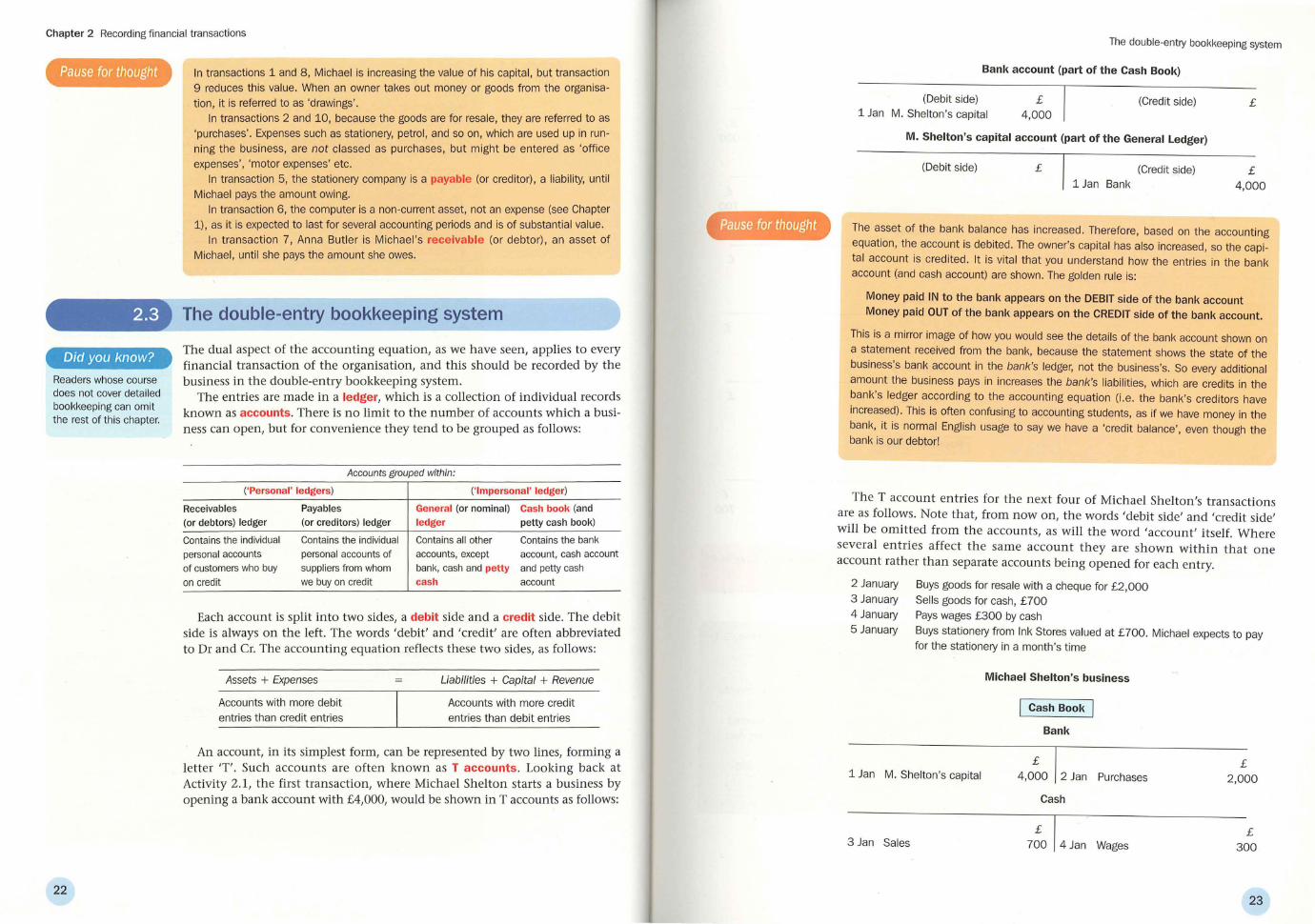

Activity 2.1, the first transaction, where Michael Shelton starts a business by opening a bank account with £4,000, would be shown in T accounts as follows:

Pause for thought

The double-entry bool(keeping system

Bank account (part of the Cash Book)

(Debit side) 1 Jan M. Shelton 's capital

£ 4,000

(Credit side)

M. Shelton's capital account (part of the General Ledger)

(Debit side) £ (Credit side) 1 Jan Bank

£

£ 4,000

The asset of the bank balance has increased. Therefore, based on the accounting equation, the account is debited. The owner's capital has also increased, so the capital account is credited . It is vital that you understand how the entries in the bank account (and cash account) are shown. The golden rule is:

Money paid IN to the bank appears on the DEBIT side of the bank account Money paid OUT of the bank appears on the CREDIT side of the bank account.

This is a mirror image of how you would see the details of the bank account shown on a statement received from the bank, because the statement shows the state of the business's bank account in the bank's ledger, not the business's. So every additional amount the business pays in increases the bank's liabilities, which are credits in the bank's ledger according to the accounting equation (i.e. the bank's creditors have

increased). This is often confusing to accounting stUdents, as if we have money in the bank, it is normal English usage to say we have a 'credit balance', even though the bank is our debtor!

The T account entries for the next four of Michael Shelton'S transactions are as follows. Note that, from now on, the words 'debit side' and 'credit side'

will be omitted from the accounts, as will the word 'account' itself. Where several entries affect the same account they are shown within that one account rather than separate accounts being opened for each entry.

2 January 3 January 4 January 5 January

Buys goods for resale with a cheque for £2,000 Sells goods for cash, £700 Pays wages £300 by cash

Buys stationery from Ink Stores valued at £700. Michael expects to pay for the stationery in a month's time

Michael Shelton's business

Cash Book

Bank

£ 1 Jan M. Shelton's capital 4,000 2 Jan Purchases

£ 2,000

Cash

3 Jan Sales 7~0 14 Jan Wages £

300

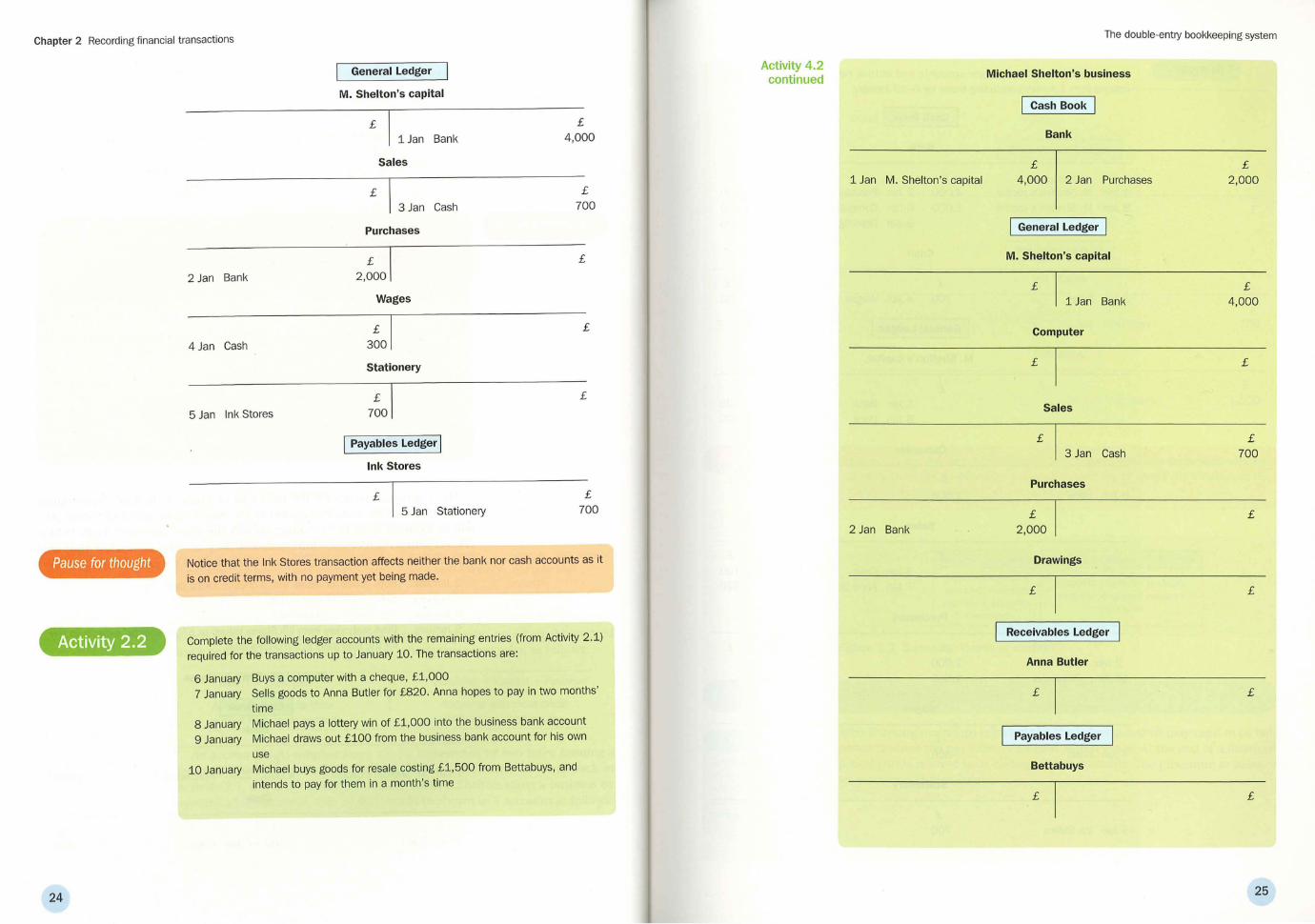

23

Chapter 2 Recording financial transactions

Pause for thought

Activity 2.2

24

2 Jan Bank

4 Jan Cash

5 Jan Ink Stores

General Ledger

M. Shelton's capital

£ 11 Jan Bank

Sales

£ 13 Jan Cash

Purchases

Wages

Stationery

I Payables Ledger I Ink Stores

£ 15 Jan Stationery

£ 4,000

£ 700

£

£

£

£ 700

Notice that the Ink Stores transaction affects neither the bank nor cash accounts as it

is on credit terms, with no payment yet being made.

Complete the following ledger accounts with the remaining entries (from Activity 2.1) required for the transactions up to January 10. The transactions are:

6 January Buys a computer with a cheque, £1,000 7 January Sells goods to Anna Butler for £820. Anna hopes to pay in two months'

time 8 January Michael pays a lottery win of £1,000 into the business bank account 9 January Michael draws out £100 from the business bank account for his own

use 10 January Michael buys goods for resale costing £1,500 from Bettabuys, and

intends to pay for them in a month 's time

Activity 4.2 continued

1 Jan M. Shelton 's capital

2 Jan Bank

The double-entry bookkeeping system

Michael Shelton's business

Cash Book

Bank

£ 4,000 2 Jan Purchases

General Ledger

M. Shelton's capital

£ 11 Jan Bank

Computer

£

Sales

£ 13 Jan Cash

Purchases

2 ,~00 1

Drawings

£

Receivables Ledger

Anna Butler

£

Payables Ledger

Bettabuys

£

£ 2,000

£ 4,000

£

£ 700

£

£

£

£

25

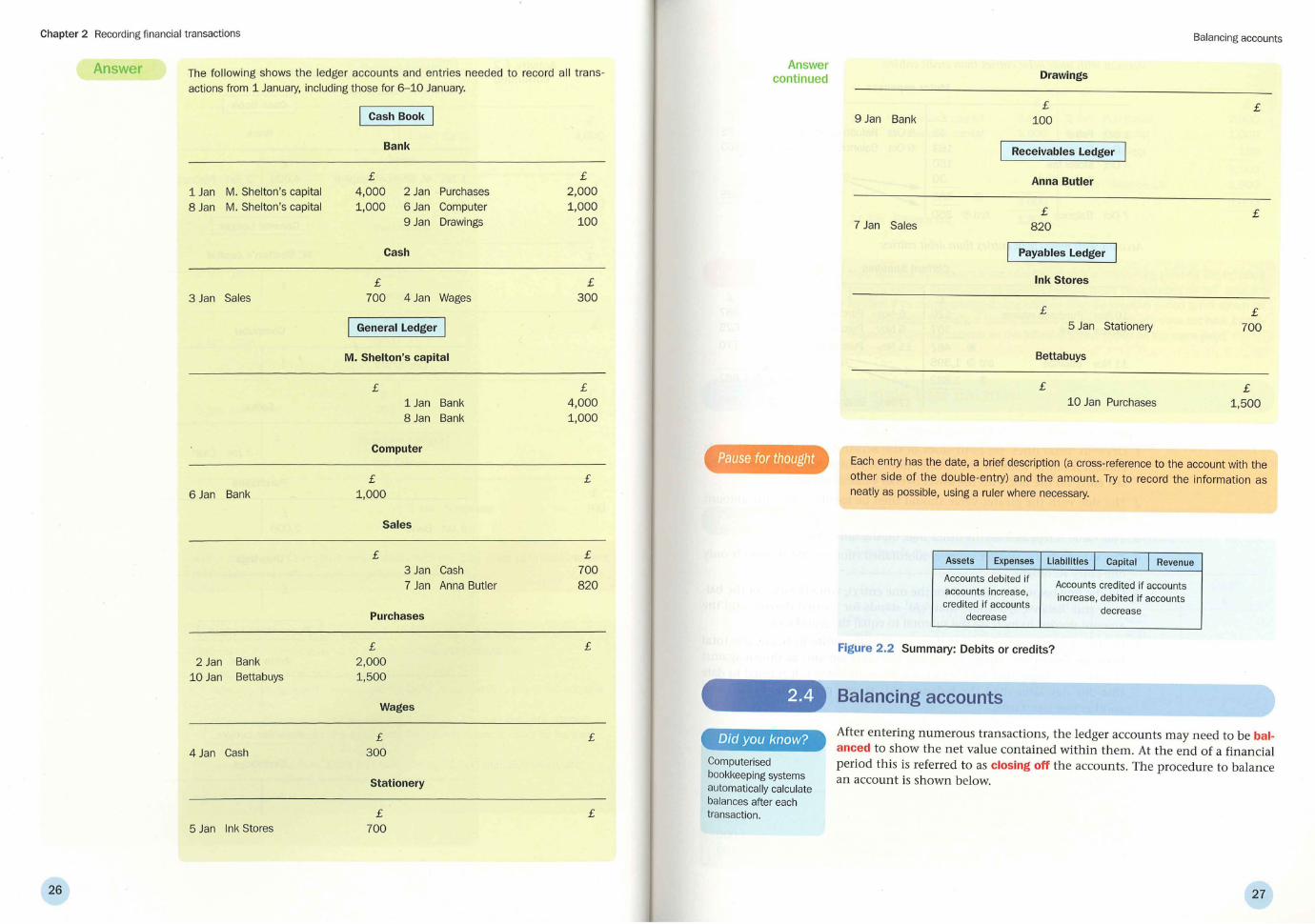

Chapter 2 Recording financial transactions

Answer

26

The following shows the ledger accounts and entries needed to record all trans

actions from 1 January, including those for 6- 10 January.

1 Jan M. Shelton's capital

8 Jan M. Shelton 's capital

3 Jan Sales

6 Jan Bank

2 Jan Bank

10 Jan Bettabuys

4 Jan Cash

5 Jan Ink Stores

Cash Book

Bank

£ 4 ,000 1,000

2 Jan Purchases 6 Jan Computer

9 Jan Drawings

Cash

£ 700 4 Jan Wages

General Ledger I

M. Shelton's capital

£ 1 Jan Bank

8 Jan Bank

Computer

£ 1,000

Sales

£ 3 Jan Cash

7 Jan Anna Butler

Purchases

£ 2,000 1,500

wages

£ 300

Stationery

£ 700

£ 2,000 1,000

100

£ 300

£ 4,000 1,000

£

£ 700 820

£

£