“International Finance and Payments” Lecture VI “International FX Markets” Lect. Cristian PĂUN Lect. Cristian PĂUN Email: Email: cpaun @ase.ro URL: URL: http://www.finint.ase.ro http://www.finint.ase.ro Academy of Economic Studies Faculty of International Business and Economics

“International Finance and Payments” Lecture VI “International FX Markets” Lect. Cristian PĂUN Email: [email protected] [email protected]@ase.ro URL: .

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

“International Finance and Payments”

Lecture VI

“International FX Markets”

Lect. Cristian PĂUNLect. Cristian PĂUN

Email: Email: [email protected]

URL: http://www.finint.ase.roURL: http://www.finint.ase.ro

Academy of Economic Studies

Faculty of International Business and Economics

Lecture 6: International FX Markets 2

Risks in international financing - review

• risks mean potential losses caused by different factors in case of a specific transaction

• in international financing we have: environmental risks, company risks and project risks;

• country risk: describe the economic and political environment of a country

• interest risk: is determined by an unfavorable evolution of interest rates on international financial markets

• currency exposure: affects financing denominated in different currencies;

• default risk: expresses the capacity of a company to pay-back its debt in terms of liquidity, solvability and profitability;

Lecture 6: International FX Markets 3

FX Markets – basic concepts

• Foreign currency: money from abroad circulated within

an economy, including coins and paper notes.

• Exchange rate: the exchange rate is the price of one

country’s currency in terms of another country’s currency

• FX Market: the place where brokerage firms and banks

are connected over an electronic network that allows

them to convert the currencies of most countries.

• Exchange rate regime: the legal environment about FX

transactions and FX market.

Lecture 6: International FX Markets 4

FX Markets – main characteristics

• The FX market is a highly active, highly decentralized market for currency conversions that operates almost 24 hours per day around the world (see the next slide).

•The vast majority of foreign exchange (FX) trading is done over-the-counter (OTC)

• Most transactions have the USD on one side (USD is a vehicle currency)

• FX Market is a Wholesale Market- Interbank Market and Retail--Client Market too;

• About 700 banks worldwide stand ready to make a market in Foreign exchange.

• Non-bank dealers account for about 20% of the market.

• The FX market is the most active market in the world ($1,210 trillion turnover per day, worldwide, in April 2001)

Lecture 6: International FX Markets 5

Around-the-clock FX trading

Average Electronic Conversions Per Hour

Greenwich Mean Time

0

5,000

10,000

15,000

20,000

25,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Tokyoopens

Asiaclosing

10 AMIn Tokyo

Afternoonin America

Londonclosing

6 pmIn NY

Americasopen

Europeopening

LunchIn Tokyo

Lecture 6: International FX Markets 6

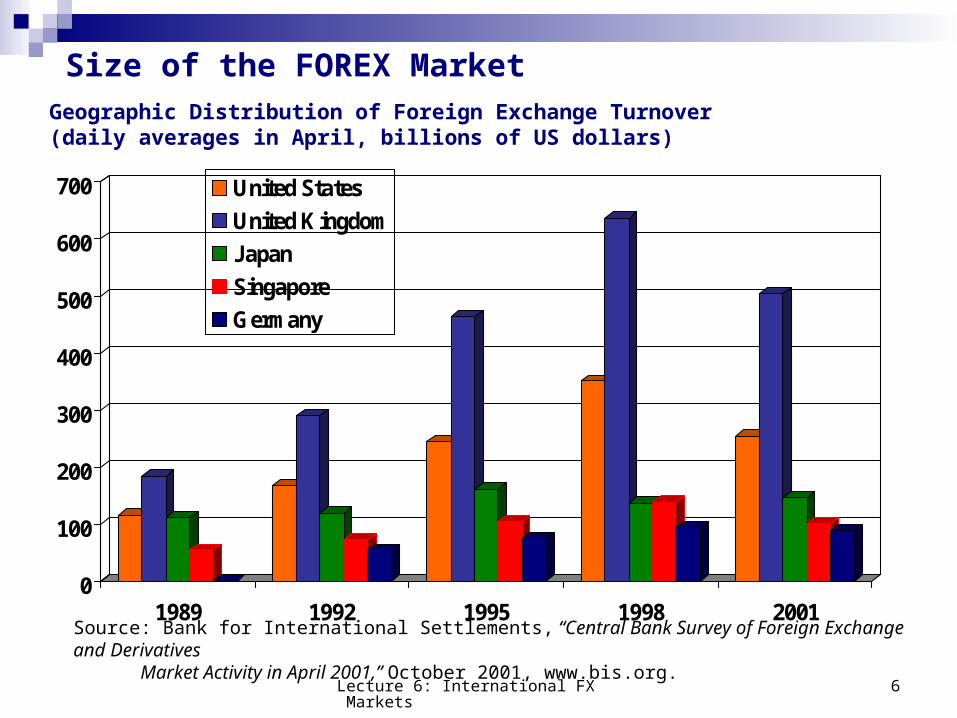

Size of the FOREX Market

0

100

200

300

400

500

600

700

1989 1992 1995 1998 2001

United States

United Kingdom

Japan

Singapore

Germany

Geographic Distribution of Foreign Exchange Turnover (daily averages in April, billions of US dollars)

Source: Bank for International Settlements, “Central Bank Survey of Foreign Exchange and Derivatives Market Activity in April 2001,” October 2001, www.bis.org.

Lecture 6: International FX Markets 7

World inter-bank FX transactions

By currency pairs -- 2001

$/euro25%

$/yen20%

$/pound10%

$/other28%

non-$17%

Lecture 6: International FX Markets 8

Forex swap53%

Forward11%

OTC Options

5%

Spot31%

World FX transactions$1.2 trillion/day (2001)

Lecture 6: International FX Markets 9

FX Markets – Direct quote vs. Indirect quote

Quoted exchange rates can be either direct or indirect, one method

is usually the convention

Direct: home currency per unit of foreign currency

Examples from US perspective:

1.676 US Dollars (USD) per British

Pound (GBP)

1.152 US Dollars (USD) per Euro

(EUR)

Indirect: foreign currency per unit of home currency

Examples from ROL perspective:

109.58 Japanese Yen (JPY) per

US Dollar (USD)

1.3664 Swiss Francs (CHF) per US

Dollar (USD)

Pound, CAD, AUD, NED - Indirect Quote

USD, Euro, ROL – Direct Quote

Lecture 6: International FX Markets 10

FX Markets – The Bid / Ask Spread

bid price--the price a dealer (NOT you) is willing to pay you for a currency.

ask price--the amount the dealer wants you to pay for a currency.

The bid-ask spread is the difference between the bid and ask prices

1 USD = 30.500 – 550 ROL

1 USD = 30.500 – 30.550 ROL

The spread = 0.050 ROL / 1 USD

Lecture 6: International FX Markets 11

Exchange rates

- Nominal Exchange Rate: the price between the local currency and a

foreign currency

- Real Exchange Rate: the nominal exchange rate adjusted with prices

differential:

RFX=NFX x (PROM-PUS)/(1+PUS)

- Effective Exchange Rate: the nominal exchange rate between a currency

basket (simple or weighted):

EFX=1/n (NFXUSD+NFXyen+NFXpound)

• Effective Exchange Rate: the effective exchange rate between a currency

basket (simple or weighted):

EFX=1/n (RFXUSD+RFXyen+NFXpound)Calculated by IMF, Morgan Guaranty Trust Company, Federal Reserve Bank

Lecture 6: International FX Markets 12

Cross exchange Rates

Suppose that S($/€) = .50 i.e. $1 = 2 €

and that S(¥/€) = 50 i.e. €1 = ¥50

What must the $/¥ cross rate be? What must the ¥/$ cross rate be?

The use of cross exchange rate:

- To determine exchange rate between two different foreign currencies;

- in arbitrage transaction (buy and sell on different FX markets)

Lecture 6: International FX Markets 13

Depreciation and Appreciation of a currency

A depreciation of the local currency means that it takes more local currency to buy a unit of foreign currency An appreciation of the local currency is the opposite

Example: If the $/€ exchange rate goes up from 1.20 to 1.30 the dollar has

depreciated against the euro but, the euro has appreciated against the dollar.

Valuation / Devaluation of a currency-When a government interviews on FX market to manage (to fix) the exchange rate at a specific level (value)

- Specific in the case of fixed exchange regimes

The relationship between depreciation of local currency and export development !!!

Lecture 6: International FX Markets 14

Currency regimes

Define the regulations related to the FX Rate mechanism (Central Bank intervention on FX Market, official exchange rate, exchange rate control)

Fixed Exchange Regime Hybrid Exchange Regimes

Dirty Float or Managed Float Fixed Band Crawling Band Fixed Peg Crawling Peg Currency Board.

Free Floating Exchange Regimes

Lecture 6: International FX Markets 15

“Dirty” or managed float

Central Bank Intervention

A

B

Exchange Rate

Central Bank Intervention

Lecture 6: International FX Markets 16

Fixed Band

Central Bank Intervention

Central Bank Intervention

Anchor

Lecture 6: International FX Markets 17

Crawling Band

T1 T2 T3

Fixed Anchor

Adjustable Margins

Fixed Margins

Adjustable Anchor

Lecture 6: International FX Markets 18

Fixed and Crawling Peg

Fixed Peg

Crawling Peg

Lecture 6: International FX Markets 19

Currency Regimes and FX Rate Control

Currency Regimes Low Medium HighFixed Exchange Rate

Currency Board

Fixed Peg

Crawling Peg

Narrow Band

Oblique Band

Wide Band

Crawling Band

Mixed Currency Regime

Managed Float

Free Floating

FX Rate C

ontrol

Lecture 6: International FX Markets 20

Convertibility of a currency

Full convertible currency: no restrictions in terms of transactions volume, capital transfers and FX Market access for residents and non-residents;

Partial convertible currency:Current Account ConvertibilityCapital Account Convertibility

No Convertibility: FX Market is very restrictive

Lecture 6: International FX Markets 21

Spot transactions

In the inter-bank market, the standard size trade for a

spot transaction is about U.S. $10 million;

Private information is an important determinant of spot

exchange rates.

Bid-Ask spreads in the spot FX market: increase with FX exchange rate volatility and

decrease with dealer competition.

The settlement or value date for a spot transaction (the

date on which the parties actually exchange assets)

occurs two business days after the deal is made ;

Lecture 6: International FX Markets 22

Forward Transactions

A forward contract is an agreement to buy or sell an asset in the future at prices agreed upon today.

Main characteristics: Usual maturity: 30, 90 and 180 days; It is not a stock exchange contract; Implies a direct negotiations with the bank It is not standardized; It has a fixed value established in the initial moment; It has not a secondary market; Can be finished only at the maturity; It is considered a money market instrument

Lecture 6: International FX Markets 23

Forward transactions

Long ForwardShort Forward

Profit

Loss

Exchange Rate at the Maturity

Initial Spot Exchange Rate

Lecture 6: International FX Markets 24

Forward Contracts and Risk Management

Position in a credit

Currency Exposure

Forward Strategy

Debtor Local currency will increase

Long Forward

Creditor Local currency will decrease

Short Forward

Lecture 6: International FX Markets 25

Forward and Spot Quotations

Spot 1,6325 - 35 ($) 2,30 - 2,30 3 / 4 (€) 263,15 - 25 ¥

Forward 1 m 0,75 - 0,73 cents 5/8 - 1/2 cents 0.15 ¥ premium0.10 ¥ discount

Forward 2 m 1,35 - 1,32 cents 1 1/8 - 1 cents 0.17 ¥ premium0.8 ¥ discount

Forward 3 m 2,03 - 2,00 cents 1 5/8 - 1 1/2 cents 0.19 ¥ premium0.6 ¥ discount

Pound against USD, Euro and Yen

Rule for pips:

- If the pip for bid is higher than pip for ask then –

- If the pip for bid is lower than pip for ask then +

Lecture 6: International FX Markets 26

FX Rate Determinants

Traditional Approach (Keynes) Purchasing Power Parity (PPP) Monetary Approach (Friedman) Interest Power Parity General Equilibrium Theory Mundell – Fleming Model Rudiger Dornbush Model

Lecture 6: International FX Markets 27

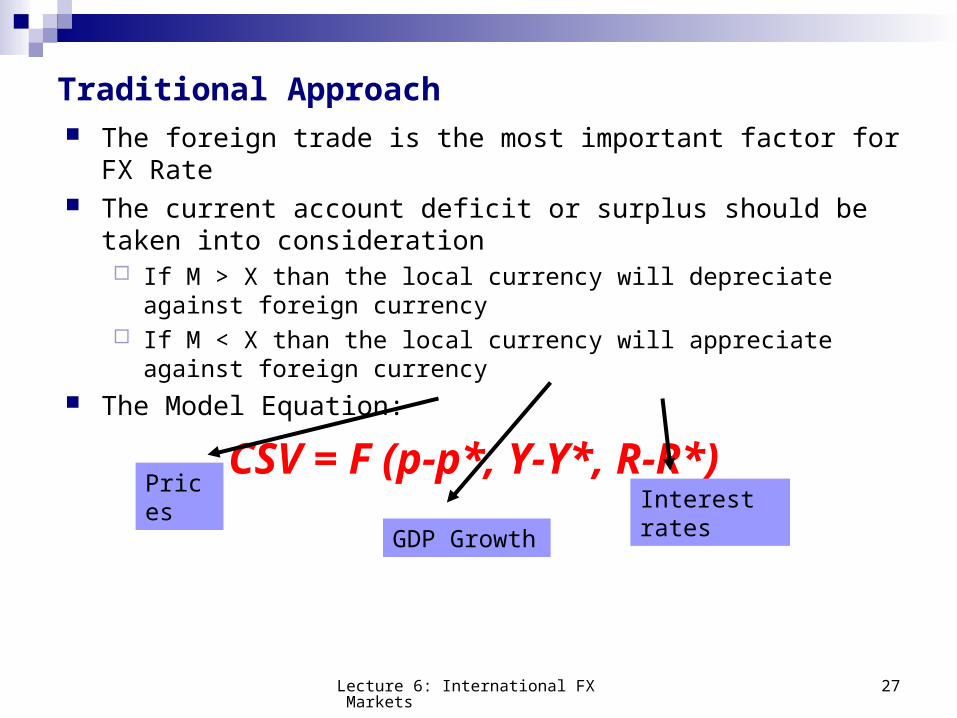

Traditional Approach The foreign trade is the most important factor for FX Rate The current account deficit or surplus should be taken into

consideration If M > X than the local currency will depreciate against foreign currency If M < X than the local currency will appreciate against foreign currency

The Model Equation:

CSV = F (p-p*, Y-Y*, R-R*)

Prices

GDP Growth

Interest rates

Lecture 6: International FX Markets 28

Purchasing Power Parity Low of one price: we can write an equation for the law of one price

as:

PiLC = Pi

FC * Ewhere

PiLC is the local currency price of good i

PiFC is the foreign currency price of good i

E is the dollar to euro exchange rate

Or we can rearrange the equation to get

E = PiLC / P

iFC

USD

lei

0 p

ps

)p (1 x p

)p(1 x ps

USDUSD

leilei_

lei

USD

USD

lei

USD

lei

0

0

_

p

p x 1

)p (1

)p(1 x

p

p

s

s s

)p (1

)p-(p

s

s s

USD

USDleu

0

0

_

Lecture 6: International FX Markets 29

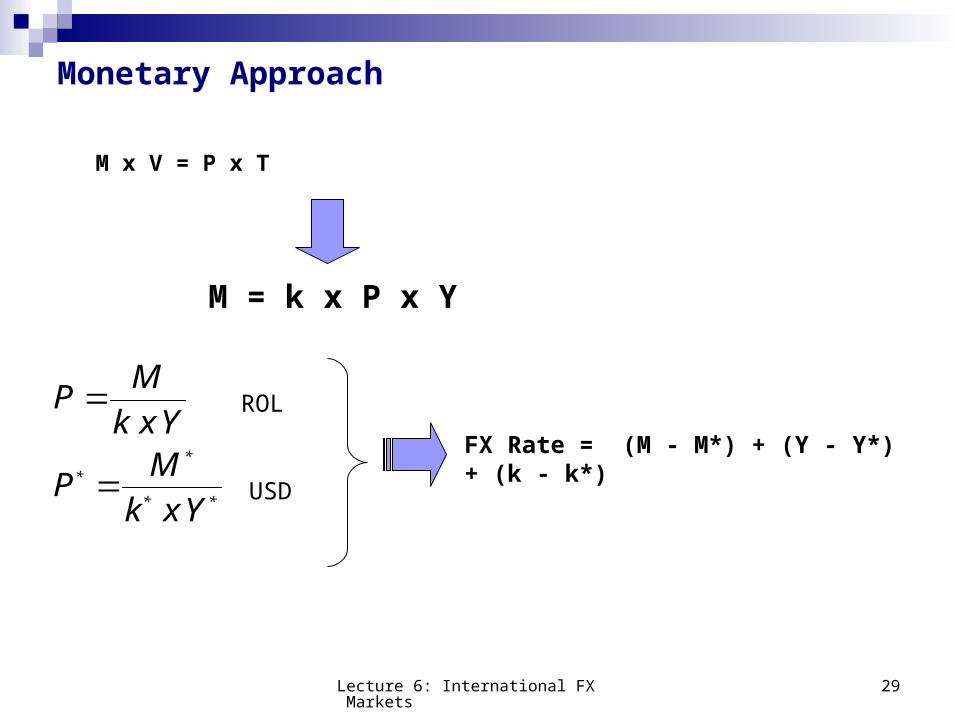

Monetary Approach

M x V = P x T

M = k x P x Y

americana piatapentru - Y x k

MP

romaneasca piatapentru Y x k

MP

**

*

*

ROL

USDFX Rate = (M - M*) + (Y - Y*) + (k - k*)

Lecture 6: International FX Markets 30

Interest Power Parity

General Equilibrium Theory

(p - p*) / (1+p*) = (d - d*)/ (1+ d*) = (f - s) / (1 + s) = (s1 – s0) / (1 + s0)

Real Market Money Market Spot and Forward FX Market

(i - i*)/ (1+ i*) = (s1 – s0) / (1 + s0)

i – interest rate (i* - interest rate from abroad)

s0 – initial spot exchange rate

s1 – predicted spot

Lecture 6: International FX Markets 31

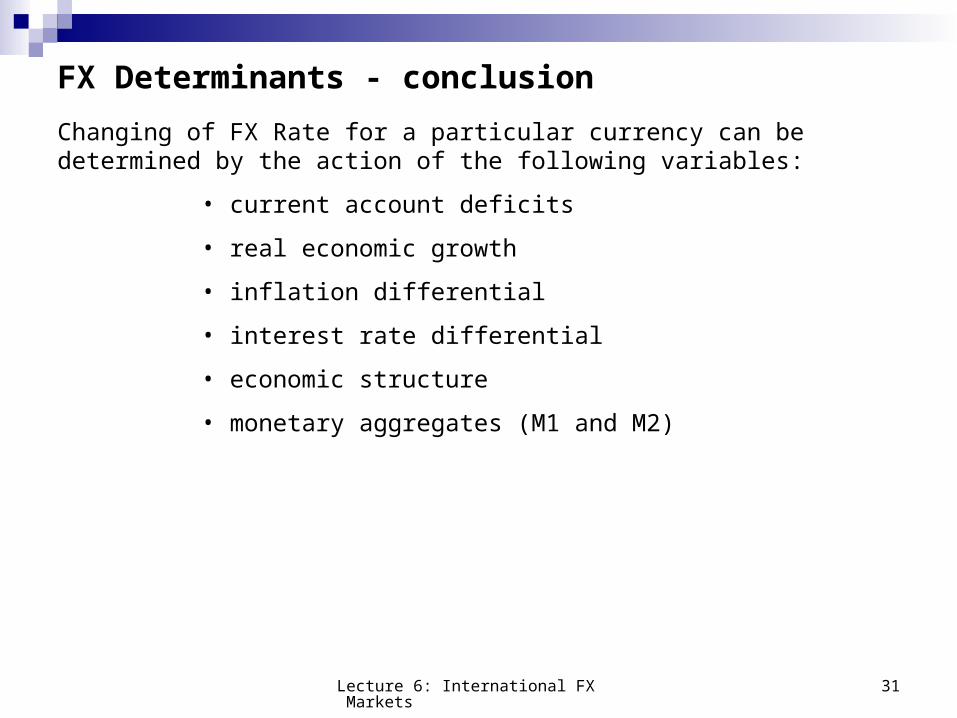

FX Determinants - conclusion

Changing of FX Rate for a particular currency can be determined by the action of the following variables:

• current account deficits

• real economic growth

• inflation differential

• interest rate differential

• economic structure

• monetary aggregates (M1 and M2)

Related Documents