International Accounting and Finance

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 1/17

International Accounting

and Finance

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 2/17

OHT 11.2

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Objective

Discuss the background to accounting and its two main divisions;

Identify the main users of accounting information and the keyfinancial statements;

Outline the differences of accounting treatment followed byvarious countries;

Assess the need for international harmonisation of accountingpractices;

Examine some key issues facing a firm in the management of international firms and when operating under different financialand fiscal regimes;

Identify some of the financial instruments used in finance of foreign trade.

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 3/17

OHT 11.3

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Background to Accounting

What is accounting?

Identifying the key financial components of anorganisation

Measuring the monetary values of the keyfinancial components

Communicating the financial information

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 4/17

OHT 11.4

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Users of accounting

information Investors

Lenders

Suppliers and other creditors

Employees

Customers

Government and its agencies The public

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 5/17

OHT 11.5

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Major Financial Accounting

Statements The profit and loss account (or Statement of

Income)

The balance sheet The cash flow statement

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 6/17

OHT 11.6

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Published Accounts

Large corporations will publish financialinformation, usually as a requirement of a specificstock exchange or due to national legislation

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 7/17

OHT 11.7

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Extract 1: Rover trouble was

unavoidable(Losses in

brackets)

Rover Net

Profit using

Br a/c rules

£m

Rover Net

Profit using

Gr a/c rules

£m

Difference £m

1994 279 Unpublished -

1995 (51) (163) -112

1996 (100) (109) -9

1997 19 (91) -72

Total 147 (363) -216

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 8/17

OHT 11.8

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

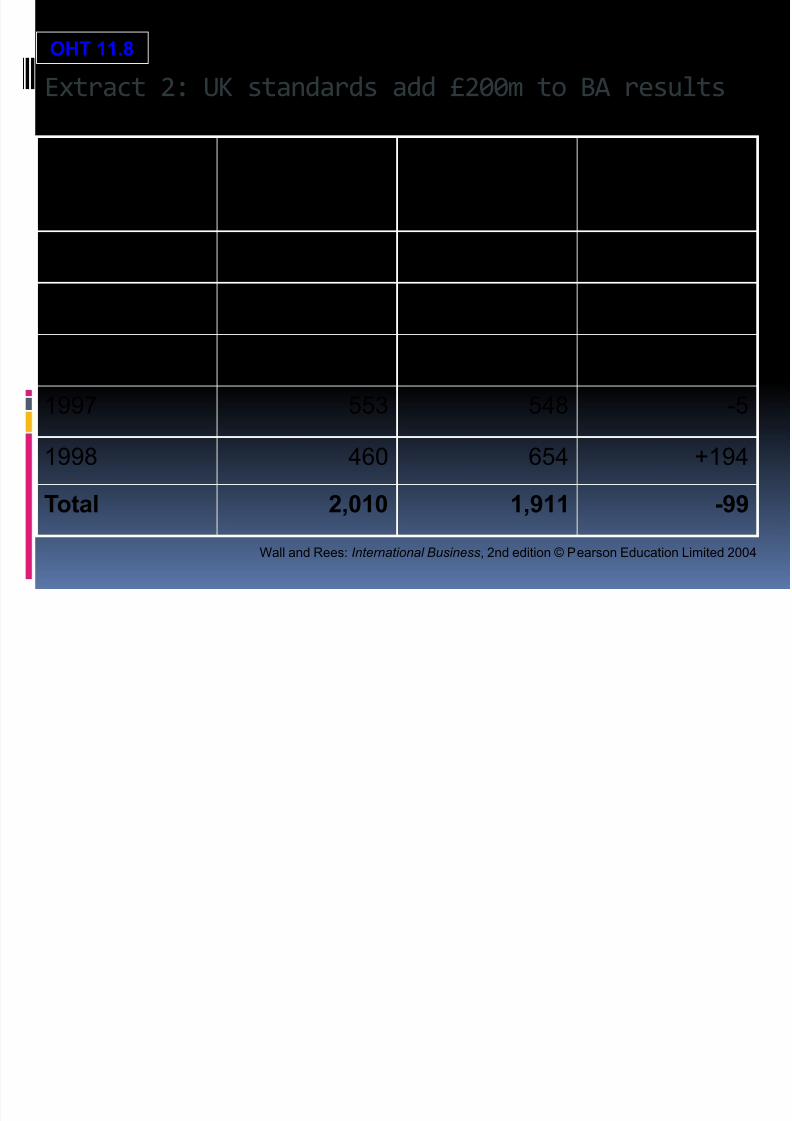

Extract 2: UK standards add £200m to BA results

(Losses in

brackets)

BA Net Profit

using Br a/c

rules £m

BA Net Profit

using Gr a/c

rules £m

Difference £m

1994 274 145 -129

1995 250 297 +47

1996 473 267 -206

1997 553 548 -5

1998 460 654 +194

Total 2,010 1,911 -99

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 9/17

OHT 11.9

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Reasons for different

accounting standards The legal system

Types of ownership patterns

The accounting profession

Conservatism

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 10/17

OHT 11.10

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Global Accounting Standards

The International Accounting Standards Board (IASB)

Sarbanes–Oxley Act 2002 in US

Which company does the act apply to?

Do chief executives have to swear the truth of theircompany accounts?

What if the accounts are later proven to be wrong?

When does the act come into force?

What will it mean for more junior executives?

What else should companies look out for?

Is there any chance UK and other businesses may escapethis provision?

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 11/17

OHT 11.11

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Higgs Committee Report

(2002)Sought to improve corporate governance in the UK byrecommending that:

At least 50% of a company’s board should consist of

independent non-executive directors Rigorous, formal and transparent procedures should

be adopted when recruiting new directors to a board

Roles of Chairman and Chief Executive of a company

should be separate No individual should be appointed to a second

chairmanship of a FTSE 100 company

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 12/17

OHT 11.12

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Integration of ways to manage risk

Source: Lisa Meulbrook, Financial Times, 9 May 2000.

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 13/17

OHT 11.13

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Strategic Risk Management

Methods of implementing such a policyinclude: Modifying the company’s operations

Adjusting the company’s capital structure

Employing targeted financial instruments

Combining the above 3 methods to minimise theaggregate net exposure to risk from all sources

Alternative risk transfer (ART)

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 14/17

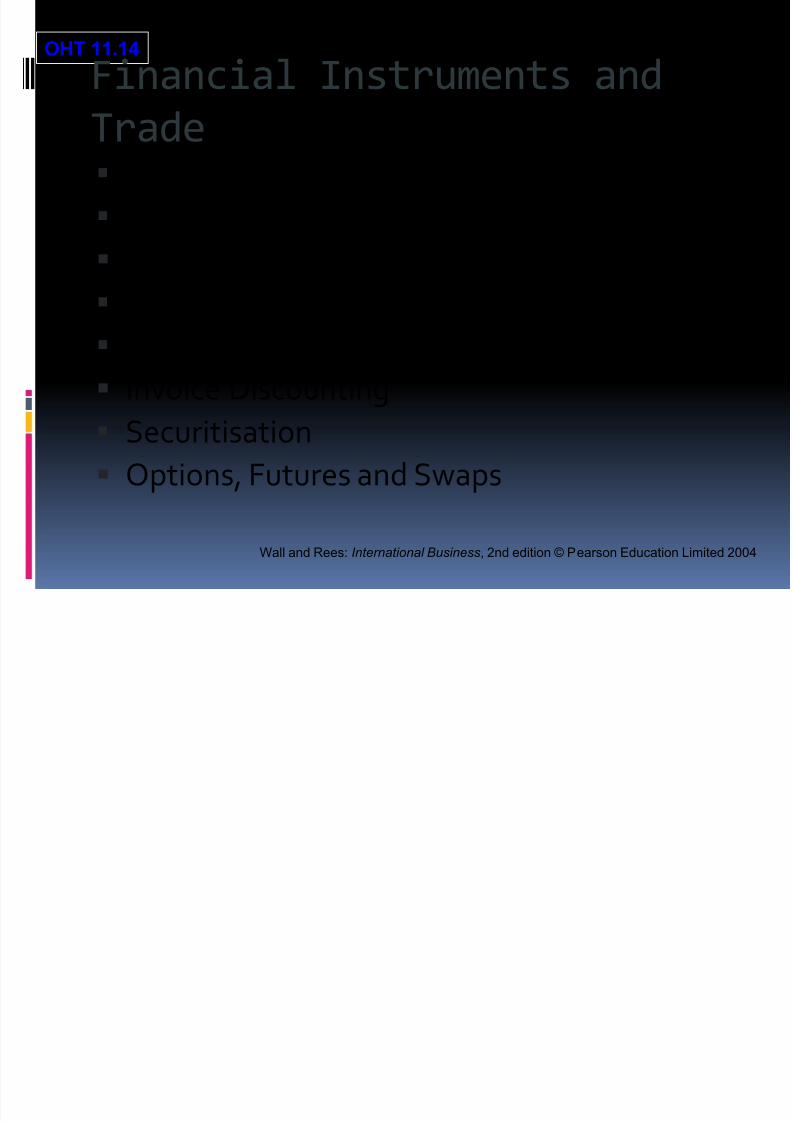

OHT 11.14

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Financial Instruments and

Trade Bills of Exchange

‘Avalised’ Bills of Exchange

Forfaiting

Letters of Credit

Factoring

Invoice Discounting

Securitisation

Options, Futures and Swaps

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 15/17

OHT 11.15

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Centralised Financial

Management Reasons in favour:

Minimising cost/maximising return

Flexibility

Scale economies

Professional expertise

Synchronisation

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 16/17

OHT 11.16

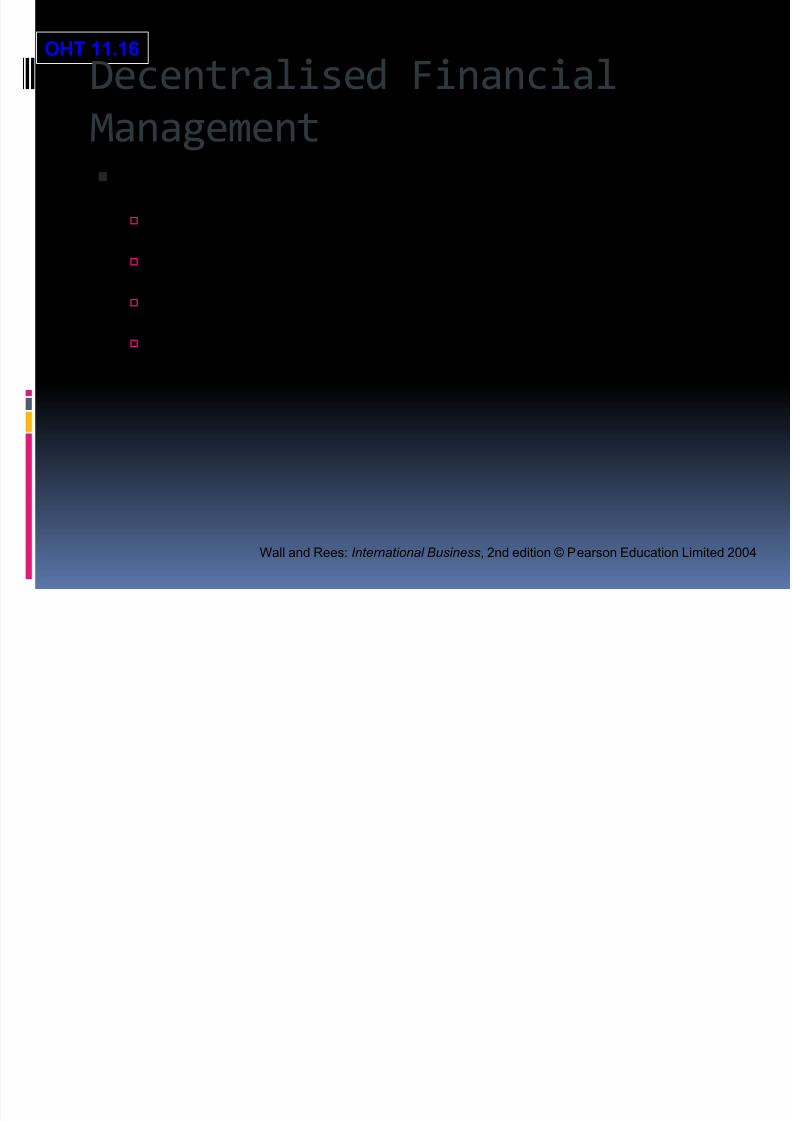

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

Decentralised Financial

Management Reasons in favour:

Generality

Motivation and morale

Conflicts

Inflexibility

7/27/2019 International Accounting and Finance.ppt

http://slidepdf.com/reader/full/international-accounting-and-financeppt 17/17

OHT 11.17

Wall and Rees: International Business, 2nd edition © Pearson Education Limited 2004

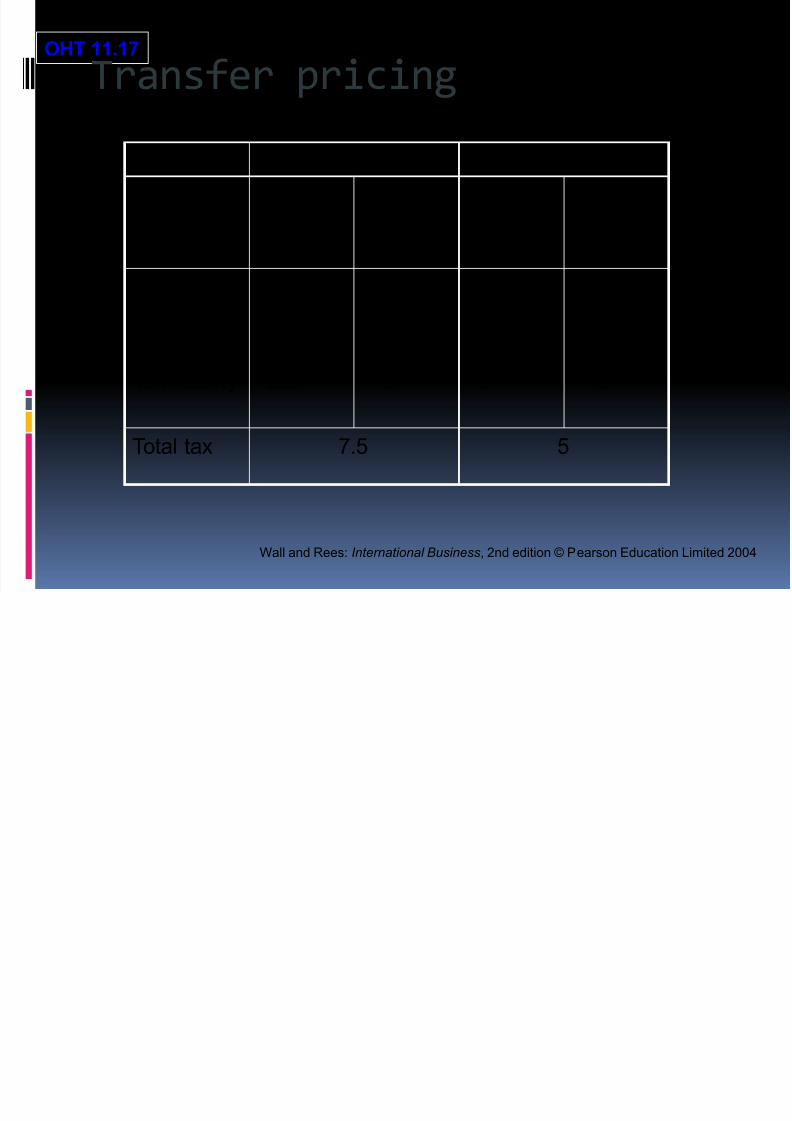

Transfer pricing

Scenario 1 Scenario 2

$m Country A

CountryB

Country A

CountryB

Costs

Sales

Profit

Tax liability

40

50

10

2.5

90

100

10

5

40

60

20

5

100

100

0

0

Total tax 7.5 5

Related Documents