Confidential. © 2017 IHS Markit TM . All Rights Reserved. Presentation Indiana Economic Forecast Update December 18, 2017 Tom Jackson, Principal Economist, +1 215 789 7432 [email protected] IHS Markit Economics

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Presentation

Indiana Economic Forecast UpdateDecember 18, 2017

Tom Jackson, Principal Economist, +1 215 789 7432 [email protected]

IHS Markit Economics

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

The US economy will sustain above-trend growth

Indiana Economic Forecast Update / December 2017

• The US economy began 2017 on a weak note – since then growth has averaged nearly 3.0%.

• With the strong momentum at the end of the year, IHS Markit expects growth in calendar year 2018 to be 2.6%, above the 2.3% in 2017 and well above the 1.5% in 2016.

• Strong economic fundamentals will sustain this above-trend growth.

• Financial conditions remain supportive, household balance sheets are improving, the US dollar is off its peak, and capacity utilization rates are high.

• Moreover, there are no obvious imbalances that could threaten the expansion.

• With trend growth estimated to be around 2.0%, this means the unemployment rate will be pushed below 4.0%.

• If the Republican Tax Cuts and Jobs Act is passed by the full Congress, it would raise growth 0.3 percentage points per year from 2018 to 2020, push down the unemployment rate even lower, and push up interest rates and the dollar even more.

2

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Changes to forecast since April update

Indiana Economic Forecast Update / December 2017

• Higher manufacturing employment, production• State-level employment data revised higher for Indiana

• National outlook has improved

• Demand for durables is improving, especially from fixed business investment

• Global economy has been much better than expected, from the European Union to emerging markets; this has lowered the dollar, increased exports

• Wage levels for Indiana and the US were revised down for 2016, which lowered the baseline moving forward

• Overall employment growth rate slightly higher, as national economy better than expected

3

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Indiana’s real GSP growth outpaces payroll growth, indicating higher productivity

4

-6

-3

0

3

6

9

12

15

18

2010 2012 2014 2016 2018 2020

Real GSP Employment

Indiana real GSP and payroll employment

Perc

ent c

hang

e, a

nnua

l rat

e

Source: IHS Markit © 2017 IHS

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

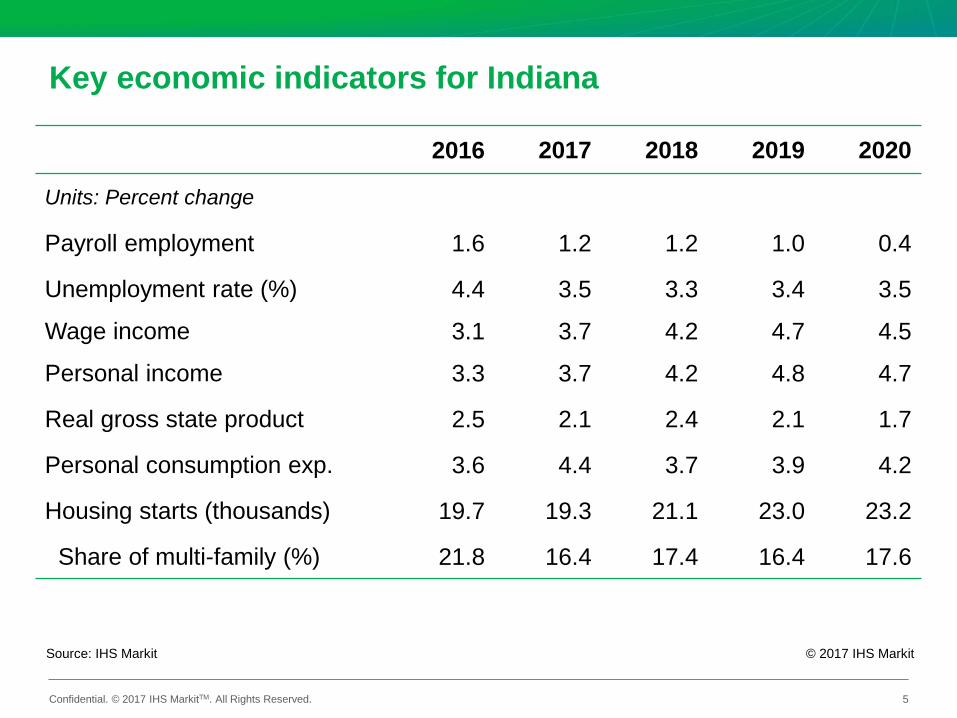

Key economic indicators for Indiana

5

2016 2017 2018 2019 2020

Units: Percent change

Payroll employment 1.6 1.2 1.2 1.0 0.4

Unemployment rate (%) 4.4 3.5 3.3 3.4 3.5

Wage income 3.1 3.7 4.2 4.7 4.5

Personal income 3.3 3.7 4.2 4.8 4.7

Real gross state product 2.5 2.1 2.4 2.1 1.7

Personal consumption exp. 3.6 4.4 3.7 3.9 4.2

Housing starts (thousands) 19.7 19.3 21.1 23.0 23.2

Share of multi-family (%) 21.8 16.4 17.4 16.4 17.6

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

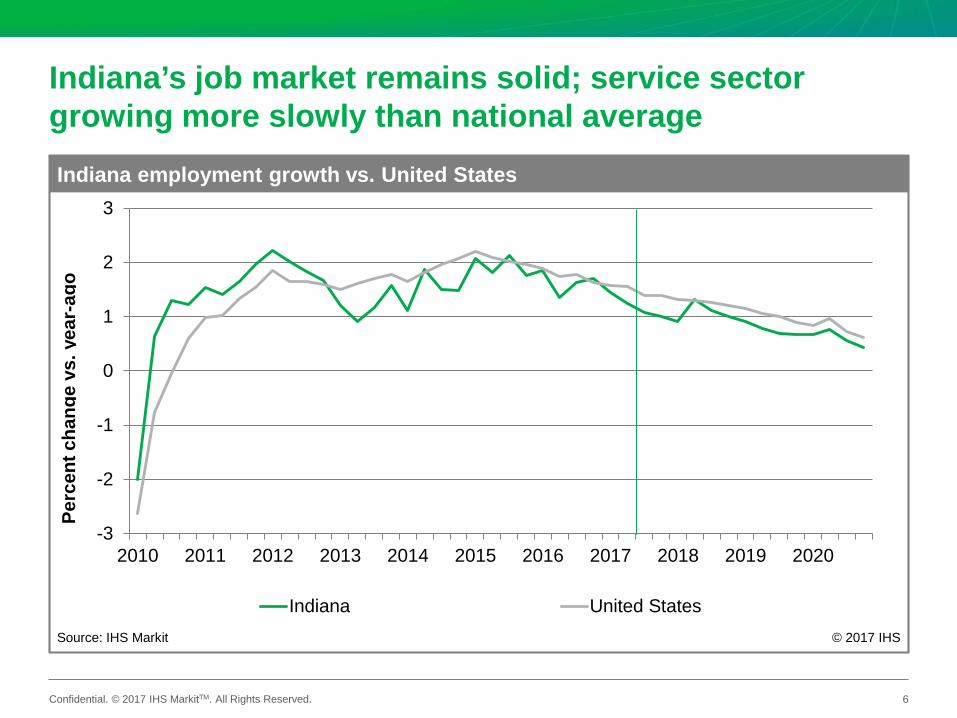

Indiana’s job market remains solid; service sector growing more slowly than national average

6

-3

-2

-1

0

1

2

3

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Indiana United States

Indiana employment growth vs. United States

Perc

ent c

hang

e vs

. yea

r-ag

o

Source: IHS Markit © 2017 IHS

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

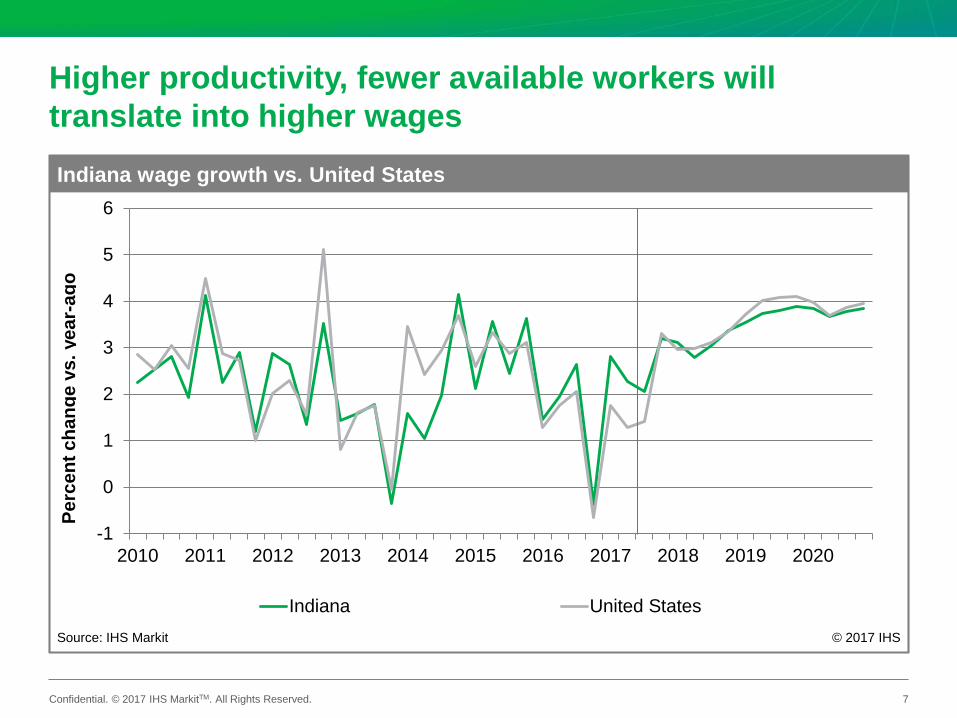

Higher productivity, fewer available workers will translate into higher wages

7

-1

0

1

2

3

4

5

6

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Indiana United States

Indiana wage growth vs. United States

Perc

ent c

hang

e vs

. yea

r-ag

o

Source: IHS Markit © 2017 IHS

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Manufacturing sector remains the leader in state job growth

8

-4 -2 0 2 4 6 8 10

Transport & warehousingEducation

InformationProf. & business services

Federal governmentRetail trade

Utilities & miningLeisure & hospitality

Wholesale tradeOther services

ConstructionFinancial servicesState & local govt.

Health & social servicesManufacturing

Change in Indiana payroll employment, Oct 2016 - Oct 2017

ThousandsSource: IHS Markit © 2017 IHS

Job change = 29,400

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

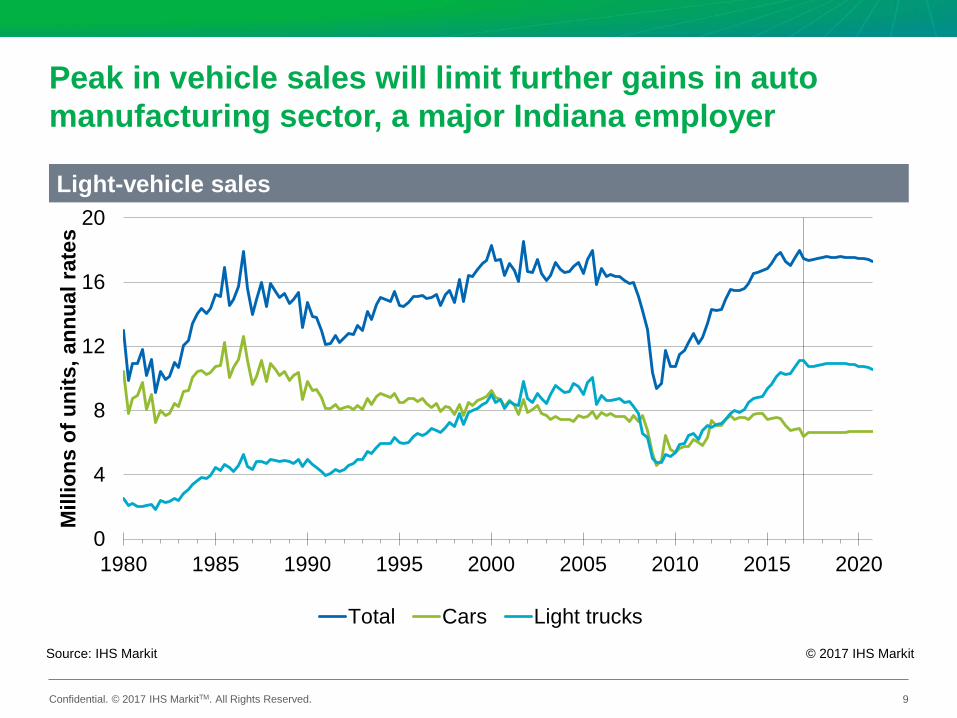

Peak in vehicle sales will limit further gains in auto manufacturing sector, a major Indiana employer

9

Source: IHS Markit © 2017 IHS Markit

Light-vehicle sales

0

4

8

12

16

20

1980 1985 1990 1995 2000 2005 2010 2015 2020

Mill

ions

of u

nits

, ann

ual r

ates

Total Cars Light trucks

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

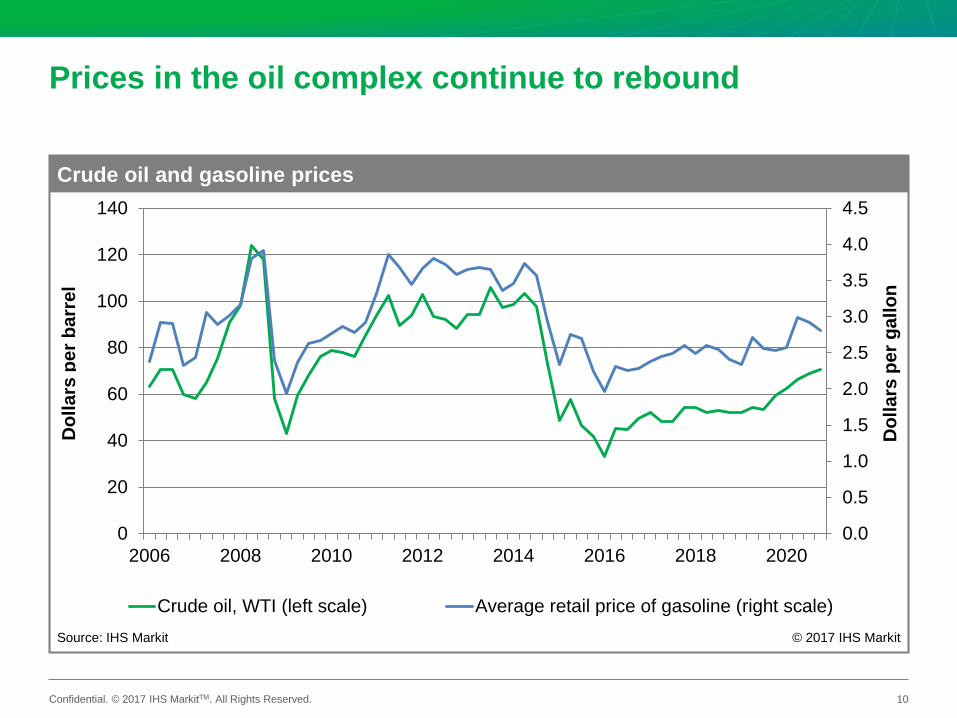

Prices in the oil complex continue to rebound

10

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0

20

40

60

80

100

120

140

2006 2008 2010 2012 2014 2016 2018 2020

Crude oil, WTI (left scale) Average retail price of gasoline (right scale)

Crude oil and gasoline prices

Dol

lars

per

bar

rel

Dol

lars

per g

allo

n

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

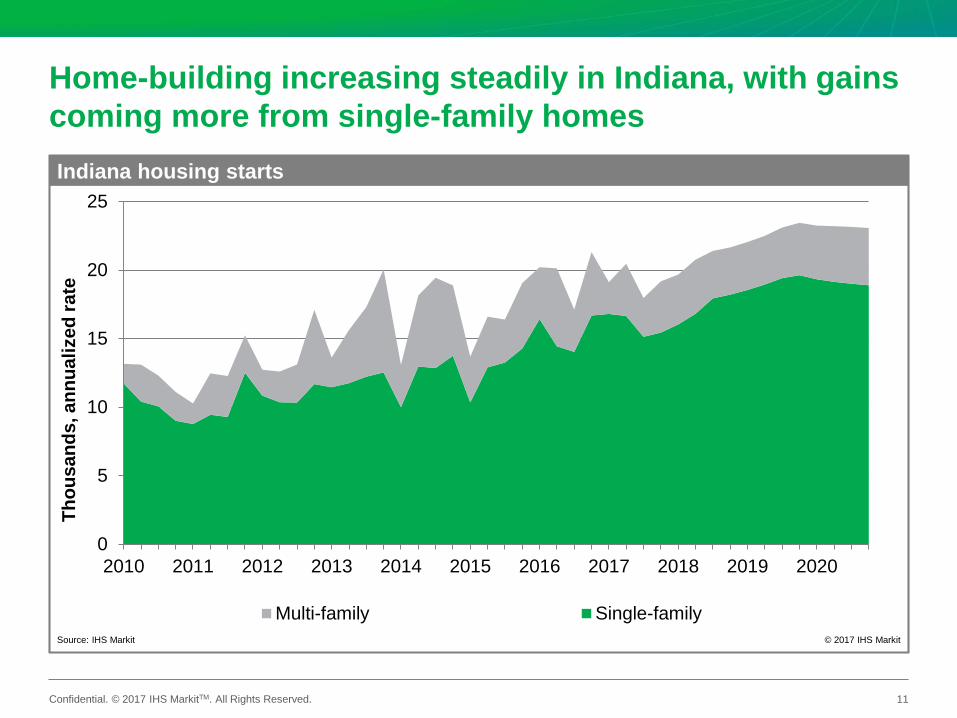

Home-building increasing steadily in Indiana, with gains coming more from single-family homes

11

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Multi-family Single-family

Indiana housing starts

Thou

sand

s,an

nual

ized

rate

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

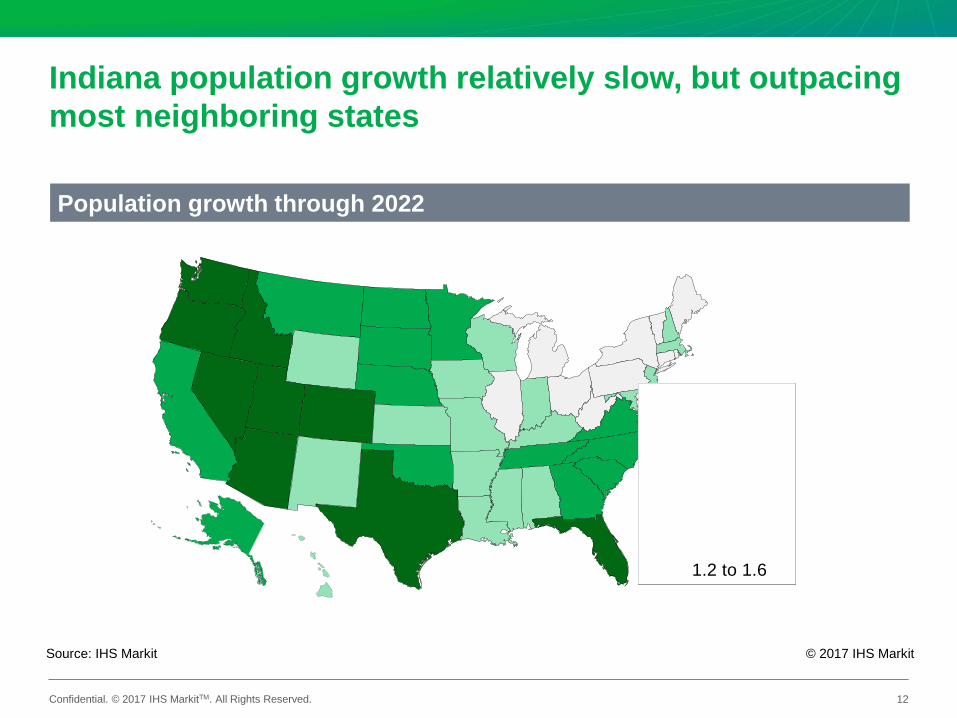

Indiana population growth relatively slow, but outpacing most neighboring states

12

Source: IHS Markit © 2017 IHS Markit

Population growth through 2022

Percent-0.1 to 0.2 0.3 to 0.6 0.7 to 1.1 1.2 to 1.6

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

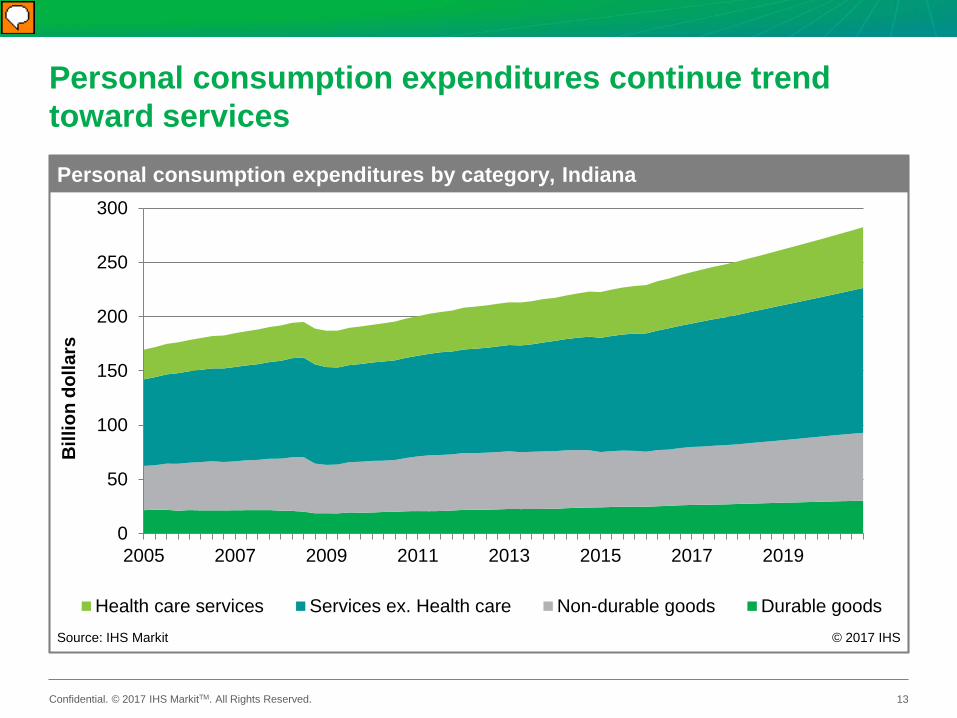

Personal consumption expenditures continue trend toward services

13

0

50

100

150

200

250

300

2005 2007 2009 2011 2013 2015 2017 2019

Health care services Services ex. Health care Non-durable goods Durable goods

Personal consumption expenditures by category, Indiana

Bill

ion

dolla

rs

Source: IHS Markit © 2017 IHS

Presenter

Presentation Notes

Average annual growth rates from 2005-2020: Health care: 4.8% Other services: 3.2% Non-durables: 2.5% Durables: 1.8%

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Bottom line for Indiana• Wage and salary income continues steady growth, even with downward

revision in 2016• Gains will need to come from wage rates more than payroll growth as state

approaches full employment• Manufacturing still has some room to grow, even as auto sales level off

• Out-migration of jobs is an ongoing risks factor, while automation looms• Continued increase in labor force is key to attracting and retaining employers

and sustaining state economic growth• This is difficult for states with low population growth• Achieved through in-migration and increased participation

• Service sector can be supported by strong education system, attractive business environment• High-tech sectors a bright spot in diversifying state’s economic base• Some sectors are dependent on local population growth as demand base

14

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

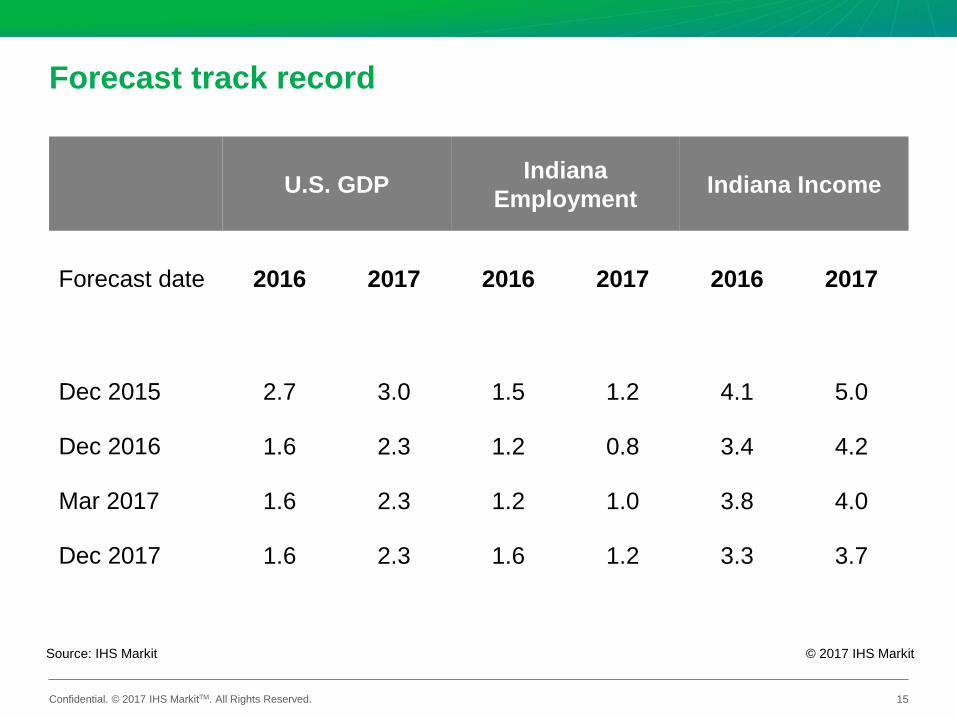

Forecast track record

U.S. GDP Indiana Employment Indiana Income

Forecast date 2016 2017 2016 2017 2016 2017

Dec 2015 2.7 3.0 1.5 1.2 4.1 5.0

Dec 2016 1.6 2.3 1.2 0.8 3.4 4.2

Mar 2017 1.6 2.3 1.2 1.0 3.8 4.0

Dec 2017 1.6 2.3 1.6 1.2 3.3 3.7

15

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

US Economy Appendix

Indiana Economic Forecast Update / December 2017

16

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

The US economy on a solid growth path

Indiana Economic Forecast Update / December 2017

• The US economy has solid momentum after 3.3% annualized real GDP growth in the third quarter. Fourth-quarter growth is estimated at 2.6%.

• Consumer spending continues to drive US economic growth, supported by rising employment, real incomes, and household wealth.

• Business fixed investment will benefit from expanding global markets and an easing of regulatory policies, although commercial building is slowing.

• Increasing household formation by young adults, low supplies of homes for sale, and rising prices will encourage more homebuilding.

• The baseline forecast assumes no significant changes in US tax, infrastructure, healthcare, or international trade policies.

• The Federal Reserve is expected to gradually raise the federal funds rate to a high of 3.2% in 2021, overshooting its long-run equilibrium of 2.75%.

17

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

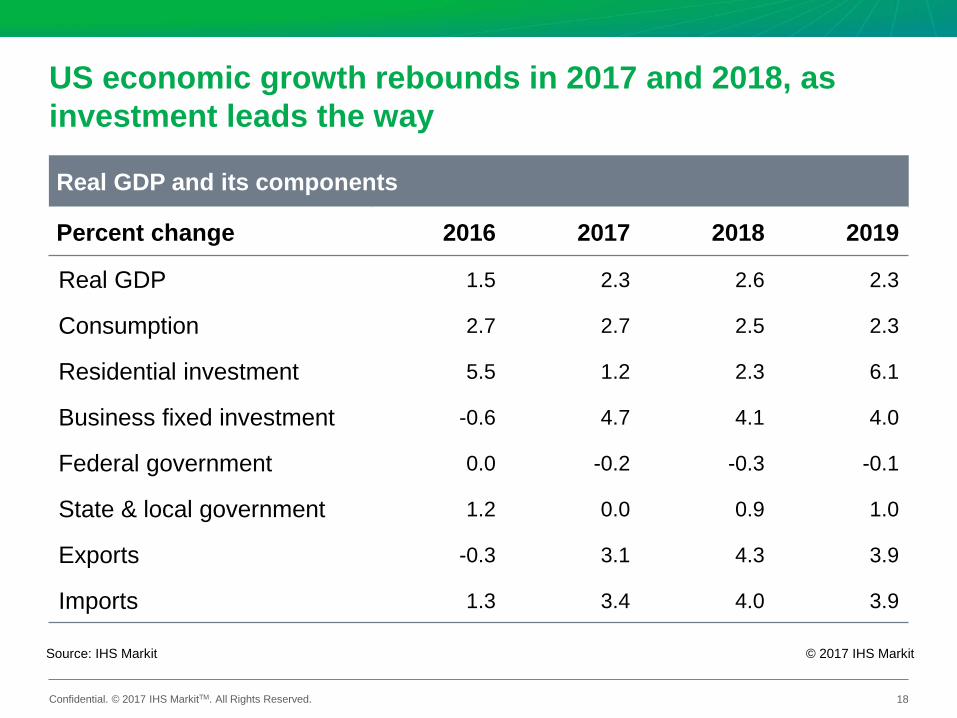

US economic growth rebounds in 2017 and 2018, as investment leads the way

18

Source: IHS Markit © 2017 IHS Markit

Real GDP and its components

Percent change 2016 2017 2018 2019

Real GDP 1.5 2.3 2.6 2.3

Consumption 2.7 2.7 2.5 2.3

Residential investment 5.5 1.2 2.3 6.1

Business fixed investment -0.6 4.7 4.1 4.0

Federal government 0.0 -0.2 -0.3 -0.1

State & local government 1.2 0.0 0.9 1.0

Exports -0.3 3.1 4.3 3.9

Imports 1.3 3.4 4.0 3.9

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

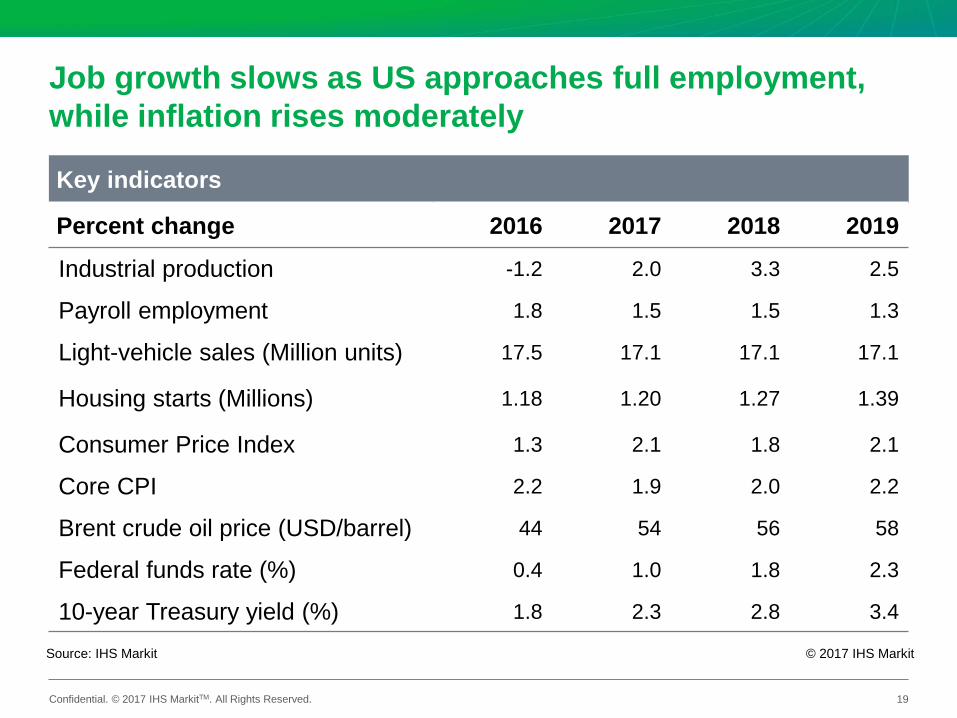

Job growth slows as US approaches full employment, while inflation rises moderately

19

Source: IHS Markit © 2017 IHS Markit

Key indicators

Percent change 2016 2017 2018 2019

Industrial production -1.2 2.0 3.3 2.5

Payroll employment 1.8 1.5 1.5 1.3

Light-vehicle sales (Million units) 17.5 17.1 17.1 17.1

Housing starts (Millions) 1.18 1.20 1.27 1.39

Consumer Price Index 1.3 2.1 1.8 2.1

Core CPI 2.2 1.9 2.0 2.2

Brent crude oil price (USD/barrel) 44 54 56 58

Federal funds rate (%) 0.4 1.0 1.8 2.3

10-year Treasury yield (%) 1.8 2.3 2.8 3.4

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

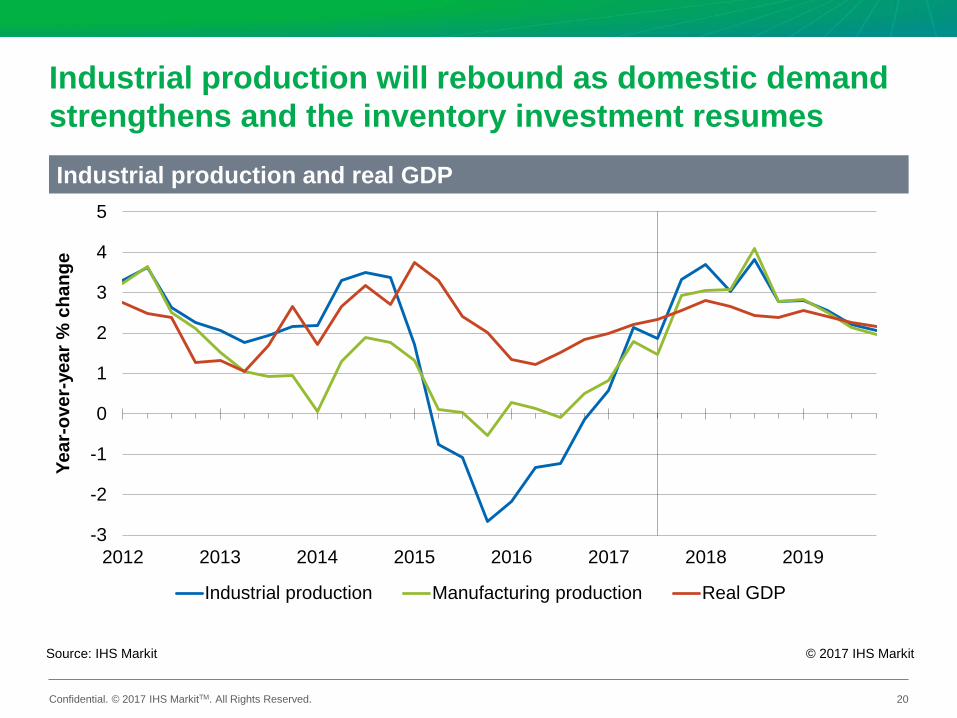

Industrial production will rebound as domestic demand strengthens and the inventory investment resumes

20

Source: IHS Markit © 2017 IHS Markit

Industrial production and real GDP

-3

-2

-1

0

1

2

3

4

5

2012 2013 2014 2015 2016 2017 2018 2019

Year

-ove

r-ye

ar %

cha

nge

Industrial production Manufacturing production Real GDP

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

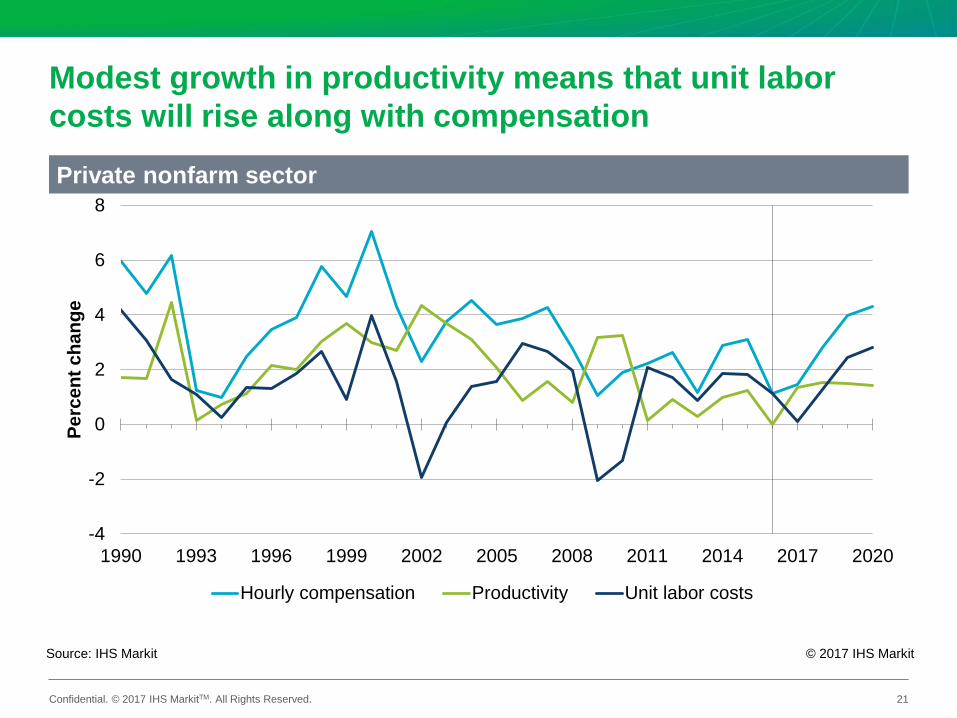

Modest growth in productivity means that unit labor costs will rise along with compensation

21

Source: IHS Markit © 2017 IHS Markit

Private nonfarm sector

-4

-2

0

2

4

6

8

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

Perc

ent c

hang

e

Hourly compensation Productivity Unit labor costs

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

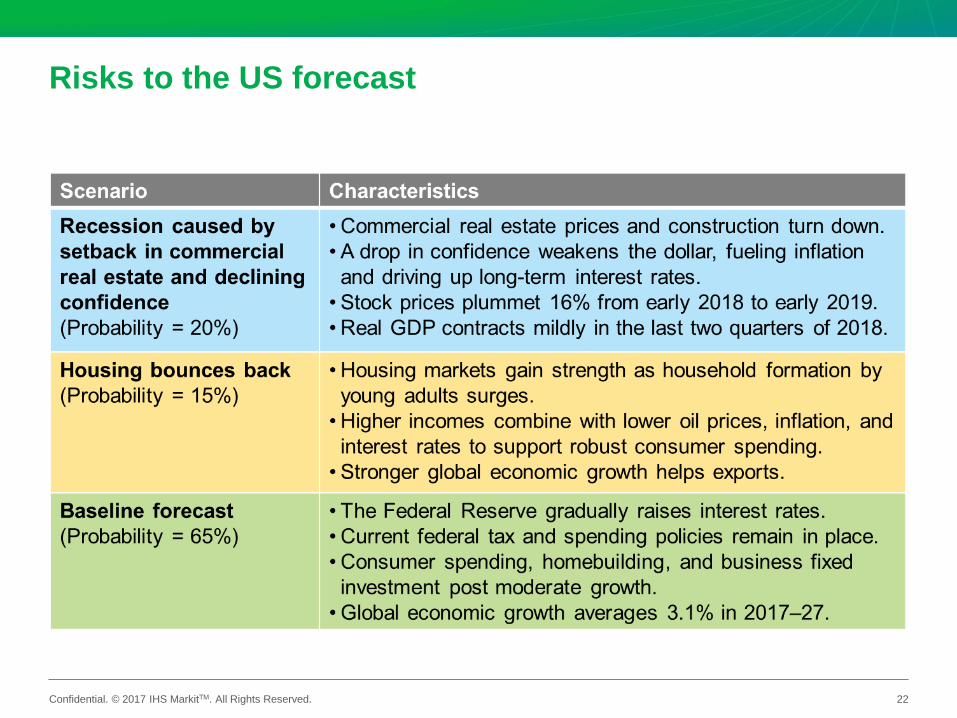

Risks to the US forecast

22

Related Documents

![10 5 09 Forecast Results Update[1]](https://static.cupdf.com/doc/110x72/54974103b47959143a8b4574/10-5-09-forecast-results-update1.jpg)