Foreign Exchange

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Foreign Exchange

Case: Volkswagen Hedging StrategyJan’2004: Co’s 2003 Q4 profits dropped by 95% (€1.05bln to

€50mln.) 50% drop YOY in 2003.Main factors: unprecedented rise in value of € vs. $ in 20031 & Co’s

decision to hedge(??) only 30% foreign currency exposure, opposed to 70% it had traditionally hedged2.

Consider a Volkswagen Jetta built in Germany @ €14,000 & sold by US dealer @ $ 15,000. Considering €1=$1> profit = €1,000.

If exchange rate changes: €1=$1.25, as in 2003, then $1=€0.80… > $15,000 = €12,000…> loss= €2,000

Soln.: Hedging strategy: At end of 2002, Co could have bought forward contract (gives right to currency exchange at some future point, say 180 days, @ predetermined rate) @ an exchange rate of $1= €1, enabling Co. to protect profits irrespective of the actual exchange rate at that time.

However Hedging strategy has risk. If € had declined, Co. would have made more profit in absence of

hedging.

IB M11 Prof Purshottam Patil 2014-15

Foreign Exchange MarketForeign Exchange Market:

Market for converting the currency of one nation into the that of another nation.

Foreign Exchange Market is a place where foreign moneys are bought & sold

..Kindleberger

Foreign Exchange:

Branch of Economic Science in which we seek to determine principles on which people globally, settle their debts one to other …Thomas

Exchange Rate:

Rate at which one currency is converted into another.

E.g. Volkswagen uses forex market to convert dollars it earns from cars in US into Euros.

In absence of forex market Cos. would have to resort to barter & global trade would not have been as high as today.

IB M11 Prof Purshottam Patil 2014-15

Average daily Forex trading volume nation wise rankings in April 2013

Top 5 currency traders in May 2013

Most traded currencies by value (April 2010)

Rank Nation Share

1 UK 41%

2 US 19%

3 Singapore 5.7%

4 Japan 5.6%

5 Hong Kong 4.1%

Rank Currency Trader Market Share

1 Deutsche Bank 15.18%

2 Citi 14.90%

3 Barclays Investment Bank 10.24%

4 UBS AG 10.11%

5 HSBC 6.93%

Rank Currency Global Market Turnover Share

1 USD ($) 84.9%

2 Euro (€) 39.1%

3 Japan (¥) 19.0%

4 Pound (£) 12.9%

5 Australian Dollar AUD ($) 7.6% IB M11 Prof Purshottam Patil 2014-15

Forex Market Participants

Participants of Forex Market

Retail Clients : international

investors, MNCs, etc who need foreign

exchange currencies for business

operations. Operate by placing buy/sell

order with Commercial Banks

Commercial Banks: Most

active in Forex market. Offer

services to convert one

currency to other.

Customers : via banks, Exports & Importers need to

convert $>Rs & Rs>$ respectively, for goods/servicesCentral Banks:

as RBI, Federal Bank. Frequently intervene to buy/

sell their currencies in bid to influence rate of currency for

trade.

Foreign Exchange Brokers: Banks

buy/sell via forex brokers, as they

collect quotations for most currencies from many banks >

to obtain quick quotation.

Speculators: Major players.

Banks, Corporations & Individuals in view to profit from favorable movement in exchange rate.

IB M11 Prof Purshottam Patil 2014-15

Functions of Forex Market:

a. Currency Conversion

• Facilitate currency conversion via credit instruments as bank drafts & foreign bills

b. Credit

• Provide credit, to promote foreign trade

c. Hedge

• When conversion from one currency to other occurs, there may be gain/loss.

• Unpredicted changes in future exchanges rates will have adverse consequences on firms.

• These risks need to protected

IB M11 Prof Purshottam Patil 2014-15

Currency Conversion Within Borders of particular nation, one must use domestic currency.

Foreign Tourists are minor participants in forex markets vis-à-vis Cos engaged in IB

IBes have main uses of forex markets, viz.,

1. Receivable Payments

• As payments from exports, income from foreign investment/ licensing agreements need to be converted for use in home nation

• e.g. Volkswagen sells cars in US for $, it must be converted to € for use in Germany

2. Payments to firms located abroad.

• To pay for products/ services in its national currency

• e.g. Dell buys its components for its computers from Malaysian firms. Malaysian firms must be paid in Malaysian currency_ Ringgit.

3. Investment in foreign nation

• IBes use forex markets when they have to invest surplus cash for short term in money markets

• e.g. US Co. wants to invest $10mln. for 3 months. Interest Rates: US_ 2%, S Korea_12%. So converts its $10mln. into Korean Won to invest in S Korea.

IB M11 Prof Purshottam Patil 2014-15

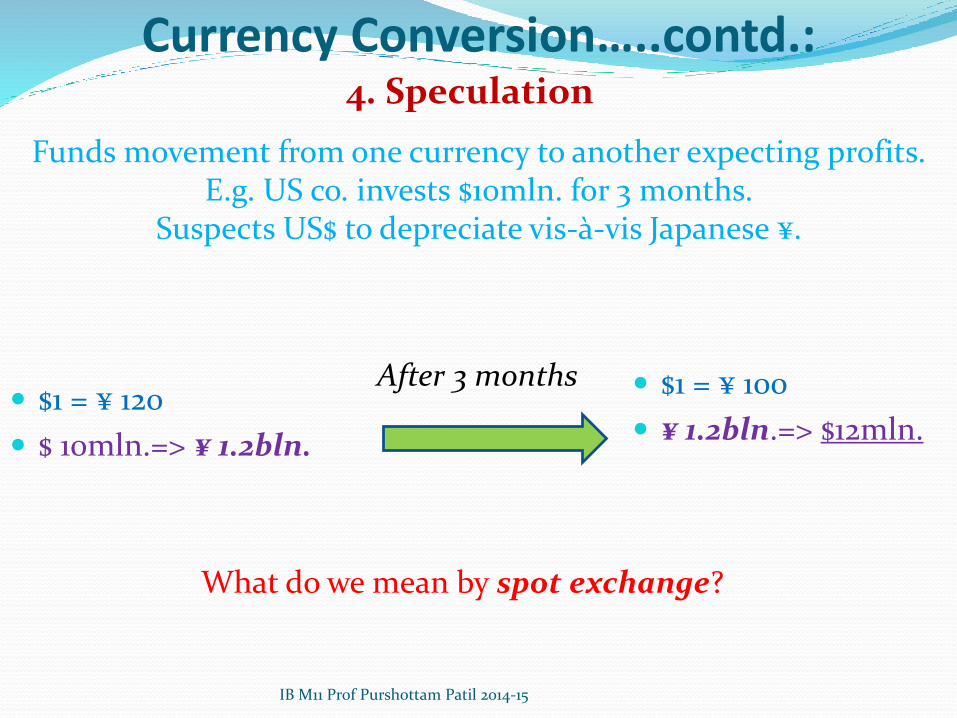

Currency Conversion…..contd.:

$1 = ¥ 120

$ 10mln.=> ¥ 1.2bln.

$1 = ¥ 100

¥ 1.2bln.=> $12mln.

IB M11 Prof Purshottam Patil 2014-15

Funds movement from one currency to another expecting profits. E.g. US co. invests $10mln. for 3 months.

Suspects US$ to depreciate vis-à-vis Japanese ¥.

After 3 months

4. Speculation

What do we mean by spot exchange?

3 Types of Major Forex Instruments

1. Spot Exchange

• 2 parties agree to exchange currency & execute deal immediately (on same day). Exchange rates on such case are spot exchange rates.

• e.g. US tourist in Mumbai goes to bank to convert $ into Rs. The exchange rate is spot exchange rate for the day. Reported daily in Financial newspapers.

• Spot exchange rate change continuously, daily, depends on demand & supply of national currency wrt other currencies.

IB M11 Prof Purshottam Patil 2014-15

Explain: forward exchange & currency swaps?

2. Forward Exchange

• E.g. Current exchange rate: $1=¥120. US Co. importing laptops from Japan, pays @ ¥2,00,000 per laptop ($1667<=2,00,000/120), within 30 days of shipment. If SP is $2000, profit is $ 333 per laptop.

• But Co. pays only after all laptops sold. Next 30 days $ depreciates, say $1=¥95, US Co. still has to pay ¥2,00,000($2105 <=2,00,000/95) to Japanese supplier per laptop, which is more than SP!

• Hence : Changes in spot exchange rates > problematic for IBes.

• Depreciating value of $ from $1=¥120 to $1=¥95, transforms seemingly profitable deal into unprofitable deal.

• Solution: US Co. avoids this risk by engaging into forward exchange.

• Assume 30 day forward exchange rate for converting $ to ¥ is $1=¥110.This guarantees that importer will pay not more than $1818 per laptop(2,00,000/110), guaranteeing profit of $182 per laptop. In e.g. above, spot exchange rate ($1=¥120) & 30 day forward rate($1=¥110) differ. Fact: $1 bought more in spot exchange than forward exchange, indicates that forex dealers expected $ to depreciate vs ¥ in next 30 days. When this occurs we say $ is selling at discount on 30 day forward market. Similarly, we say ¥ is trading at premium on 30 day forward market. This reflects forex dealers expect ¥ will appreciate vs. $ over next 30 days.

3 Types of Major Forex Instruments

IB M11 Prof Purshottam Patil 2014-15

3 Types of Major Forex Instruments

3. Currency Swaps

• 2010: Forward instruments were 65% of all forex transactions, while spot exchanges were 35%. Majority of forward exchanges were currency swaps(simultaneous purchase & sale of given amount of forex by IBes, Banks & Govts., for 2 different value dates)

• e.g. Apple assembles laptops in US, but makes screens & also sells some laptops in Japan.

• Assume: Apple converts $1Mln. to ¥ to pay its suppliers for screens, today. Also it will be paid ¥120Mln in 90 days by Japanese importer for finished laptops, which must be converted to $. Today’s spot exchange rate_$1=¥120& 90 days forward exchange rate_$1=¥110.

• Thus, Apple sells $1Mln to bank in return for ¥ 120Mln. to pay Japanese supplier.

• Also, Apple enters into 90 days forward exchange deal to convert ¥120 to $. In 90 days it will receive $1.09 Mln.(¥120Mln./110)

• Swap deal enables Apple: to insure itself against forex risk1, also it knows today that ¥120Mln. payment it will receive in 90 days will yield $1.092

IB M11 Prof Purshottam Patil 2014-15

Nature of Forex Market

Rank: Trading Center (2010) Forex Trading Activity

London 31%

N. York 19%

Tokyo 8%

Singapore 5%

London> Earlier Capital of world’s first major industrial trading nation. Retained position as largest international banking center.> Centrally located between Tokyo & Singapore on east & N. York at west, linking Asia & US.> Due to time zone differences, London opens soon after Tokyo closes at night & still open for first few hours of trading in N. York

IB M11 Prof Purshottam Patil 2014-15

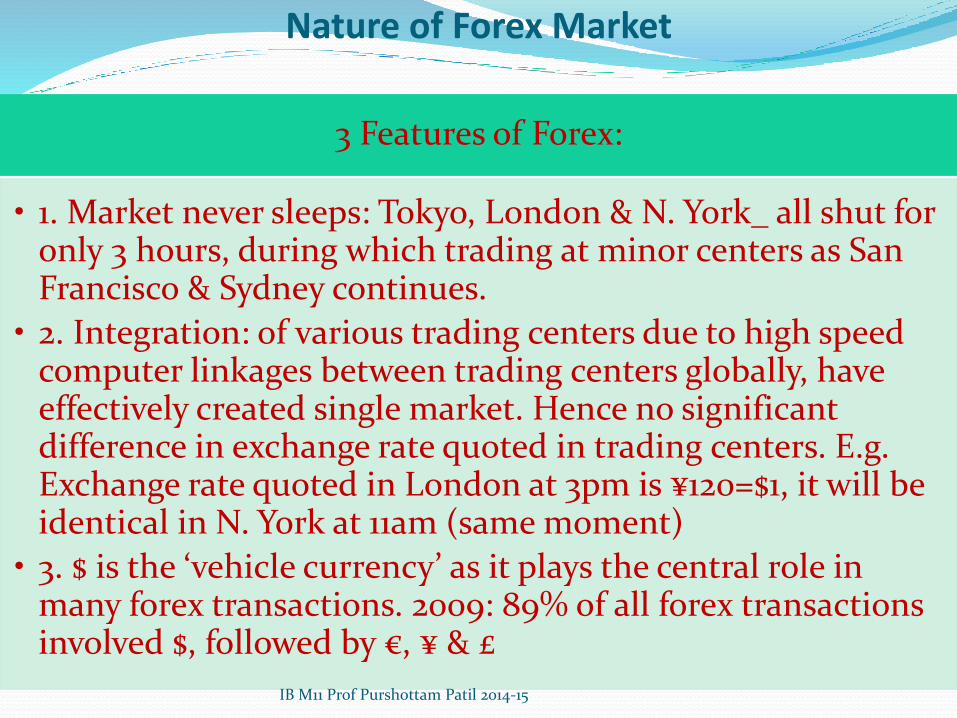

3 Features of Forex:

• 1. Market never sleeps: Tokyo, London & N. York_ all shut for only 3 hours, during which trading at minor centers as San Francisco & Sydney continues.

• 2. Integration: of various trading centers due to high speed computer linkages between trading centers globally, have effectively created single market. Hence no significant difference in exchange rate quoted in trading centers. E.g. Exchange rate quoted in London at 3pm is ¥120=$1, it will be identical in N. York at 11am (same moment)

• 3. $ is the ‘vehicle currency’ as it plays the central role in many forex transactions. 2009: 89% of all forex transactions involved $, followed by €, ¥ & £

Nature of Forex Market

IB M11 Prof Purshottam Patil 2014-15

Economic Theories of Exchange Rate Determination

Economic theories of exchange rates state that 3 factors impact future exchange rate movements in nation’s price inflation:

1. Nation’s Price Inflation

2. Interest Rate

3. Market Psychology

IB M11 Prof Purshottam Patil 2014-15

Law of One Price“Competitive markets (free of transportation costs & barriers to trade, as tariffs), identical products sold in different nations must sell for same price when expressed in same currency.”

E.g. if £1=$1.50, a jacket price @ $75 in New York should sell @ £50 in London ($75/1.50).

What if Jacket costs £40 in London ($60 in US currency)?

A trader would buy jackets in London & sell them in N. York (arbitrage). Co. profit=$15 on each jacket by purchasing it for £40 ($60) in London & selling it for $75 in N. York.

However, increased demand in London would raise price in London & increased supply in N York would lower their price there.

This would continue until prices equalized (£44($66) in London & $66 in N York).

IB M11 Prof Purshottam Patil 2014-15

Purchasing Power ParityA less extreme version PPP theory states that given relatively efficient markets (has no impediments to free flow of goods & services, as trade barriers), the price of basket of goods should be roughly equivalent in each nation.

Let P$ =price of basket of specific goods in $. P¥ = Price of same basket of specific goods in ¥. The PPP theory predicts that $ vs. ¥ exchange rate,

E$/¥ =P$/P¥

E.g. basket of goods costs $200 in US & ¥20,000 in Japan, PPP theory predicts that $/¥ exchange rate should be $200/ ¥ 20,000 or $0.01 per Japanese ¥(i.e. $1= ¥ 100)

Assume no inflation in US, while prices in Japan are increasing by 10% p.a.

Start of Year : basket of goods costs $200 in US & ¥ 20,000 in Japan.

As per PPP theory, $/ ¥ Exchange rate should be $1= ¥ 100.

End of Year: basket of goods still costs $200 in US, but ¥ 22,000 in Japan. PPP theory predicts exchange rate should change accordingly.

Hence: E$/¥ =$200/ ¥ 22,000= 0.0091 ($1= ¥ 110).

Due to 10% inflation, ¥ depreciated by 10% vs. $ IB M11 Prof Purshottam Patil 2014-15

Money Supply & Price InflationNation having high price inflation should expect its currency to depreciate vis-à-vis those with lower inflation rates.

Predicting nation’s future inflation will help predicting of its currency values vis-à-vis other currencies.

Growth rate of a nation’s money supply determines its likely future inflation rates.

Inflation: Monetary phenomenon. Occurs when quantity of money in circulation rises faster than stock of goods & services. i.e. money supply increases faster than output increases. (e.g. Rs 10,00,000 suddenly given to everyone by Govt.)

Increase in money supply by govt. makes it easier for banks to borrow from govt. & for individuals & Cos. to borrow from banks, resulting in increase in demand for goods & services.

Unless, output of goods & services grows at similar rate as money supply, result will be inflation.

Imp.: PPP theory illustrates that: Nation with high inflation rate will see depreciation in its currency exchange rate. IB M11 Prof Purshottam Patil 2014-15

PPP Theory: Bolivia Case

Month MoneySupply(Bln.)(Peso)

Price Level Relative to 1982

Exchange Rate (Pesos per dollar)

1984: June 440 32 3,342

Sept 889 54 13,685

Dec 3,296 181 24,515

1985: Apr 12,885 1,206 1,67,428

July 47,341 4,855 8,85,476

Oct 1,32,550 12,412 11,20,210

Bolivia experienced hyperinflation in mid 1980s. Money supply growth, price inflation rate & depreciation in Peso vs. $: moved up together. June’84-July’85: Bolivia’s Money Supply & Prices increased by 17,433 % & 22,908 %respectively. Value of Peso vs. $ fell by 24,662%.

In Oct’85: Bolivian govt. instituted stabilization plan_ including tight control of money supply. Result: by 1987, Bolivia’s annual inflation was down to 16%

IB M11 Prof Purshottam Patil 2014-15

Money Supply, Govt.’s Policy, Inflation & Currency Exchange Rate

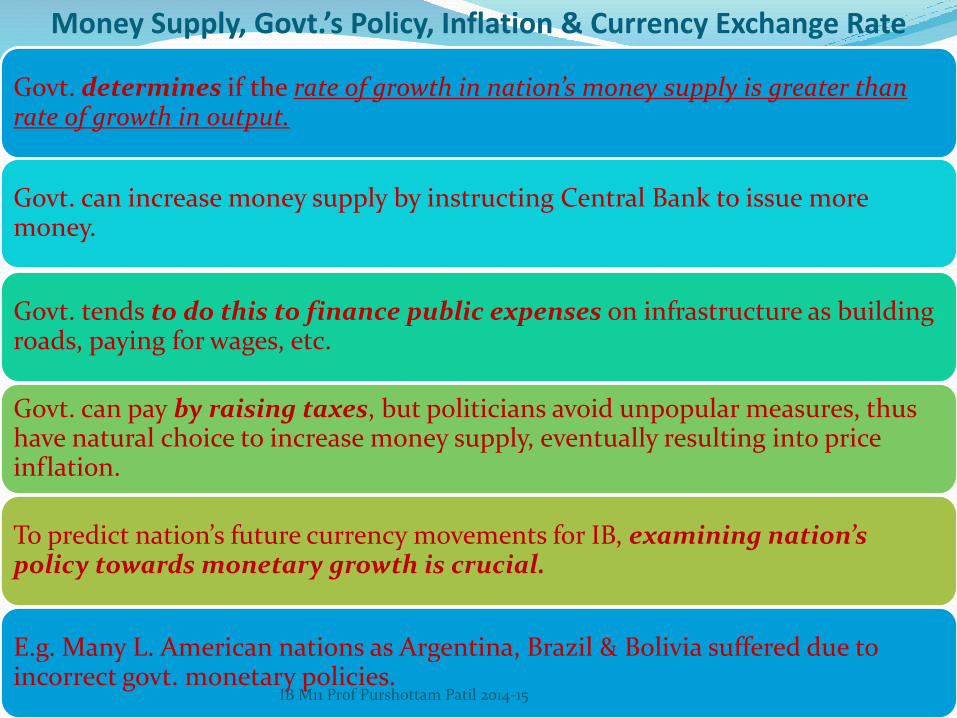

Govt. determines if the rate of growth in nation’s money supply is greater than rate of growth in output.

Govt. can increase money supply by instructing Central Bank to issue more money.

Govt. tends to do this to finance public expenses on infrastructure as building roads, paying for wages, etc.

Govt. can pay by raising taxes, but politicians avoid unpopular measures, thus have natural choice to increase money supply, eventually resulting into price inflation.

To predict nation’s future currency movements for IB, examining nation’s policy towards monetary growth is crucial.

E.g. Many L. American nations as Argentina, Brazil & Bolivia suffered due to incorrect govt. monetary policies.

IB M11 Prof Purshottam Patil 2014-15

Interest Rates & Exchange Rates: Fisher Effect

“Nations expected to have high inflation rates, will also have high interest rates, as investors want compensation for decline in value of money.”

This relationship was first formulated by economist Irvin Fisher, known as Fisher Effect.

Fisher Effect: states that ‘nation’s “nominal” interest rate(i) is sum of required “real” rate of interest(r) & expected inflation rate over period for which funds are to lent(l). i.e.

i=r+l

E.g. if l= 10%, r=5% then, nominal interest rate(i)=15%

IB M11 Prof Purshottam Patil 2014-15

Application of Fisher Effect:

• Globally, when investors freely transfer capital between nations, real interest rate will be same in every nation. If differences in real interest rates emerge between nations, arbitrage would soon equalize them. e.g. real interest rate in Japan & US were 10% & 6% respectively. Investors would borrow money in US & invest in Japan.

• This would continue until 2 sets of real interest rates are equalized.

• It follows from Fisher Effect, that if real interest rate is same worldwide, any difference in interest rates between nations reflects differing expectations about inflation rates.

• Hence “if expected rate of inflation in US is greater than that in Japan, US nominal interest rates will be greater than Japanese nominal interest rates.”

• IFE: PPP Theory states that there is link between inflation & exchange rates…1

• Interest rates reflect expectations about inflation, hence there must be a link between interest rates & exchange rates…2

• This link is known as IFE(International Fisher Effect)

Interest Rates & Exchange Rates: Fisher Effect

IB M11 Prof Purshottam Patil 2014-15

Investor Psychology & Bandwagon Effect

Evidence suggests that neither PPP theory nor IFE are precise at explaining short-term movements in exchange rates.

One reason maybe investor psychology.

Sept’1992 : Famous international Financer George Soros borrowed Billions of £, using assets of his investment funds& immediately sold them for German Deutschmarks (before advent of Euro).

This short selling by Soros pushed down value of £ in forex market as many forex traders did likewise, triggering a classic ‘Bandwagon Effect’.

Massive selling pushed down value of £ vs. Deutschmarks, not due to any macroeconomic fundamentals, but due to momentum started by George Soros.

IB M11 Prof Purshottam Patil 2014-15

Factors Influencing Exchange Rate Fluctuations:

1. State of International Trade: of a nation or changes in volume of imports & exports will also affect the rate of exchange. Deficit in trade will adversely affect the rate & vice versa.

2. Monetary Policy: regulation of money supply & frequent changes in money supply will affect fluctuation on rate of exchange

3. Industrial Factors: in case of industrial development, there is more investment of foreign capital & rate will be favorably affected & vice versa.

4. Political Conditions: Political stability favorable for forex.

5. National Income: Increase will lead to increase in investment, production & consumption, effecting exchange rates.

IB M11 Prof Purshottam Patil 2014-15

Related Documents