i n t e r i m r e s u l t s for the six months ended june 2005

I n t e r i m r e s u l t s for the six months ended june 2005.

Jan 02, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

i n t e r i m r e s u l t sfor the six months ended june 2005

D a v i n d e r C h u g h

c h i e f e x e c u t i v e o f f i c e r

m a r k e t & o p e r a t i o n

s

4

Overview

Record half year earnings of R3 221m

- Earnings per share of 723c up 108%

- Operating margin of 35% up 66%

- Return on equity of 37% up 61%

- High international steel prices

- Cost increases contained

Delivering on R9bn capital investment programme

Note: All comparisons against corresponding period in 2004

Maintaining strong performance

5

Key Result Drivers

8% Strengthening of Rand

11% Increase in HRC Rand cash cost per tonne

(7%)Slowdown in domestic sales volume

6% Export sales volume up

35% Increase in HRC US$ export price

1H’05 vs 1H’04

Good performance supported by cost containment

13% Increase in HRC Rand domestic price

6

Export PricesM

itta

l S

teel

In

voic

ed P

rice

s (c

&f)

US

$/t

HRC

Low Carbon Wire Rod

700

600

500

400

300

200

100

01994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Historical high prices prevailed

7

Global Market Trends

Global steel demand outstripped supply in 2004/2005

Inventory adjustments prompted recent price slide

World economic growth is expected to remain positive

Consolidation amongst steel companies globally continues

Steelmakers’ input costs will remain high

Chinese economy still growing at high rate

In 2004, China accounted for

- 30% of world steel production

- 32% of world steel consumption

Global steel demand driven by China

8

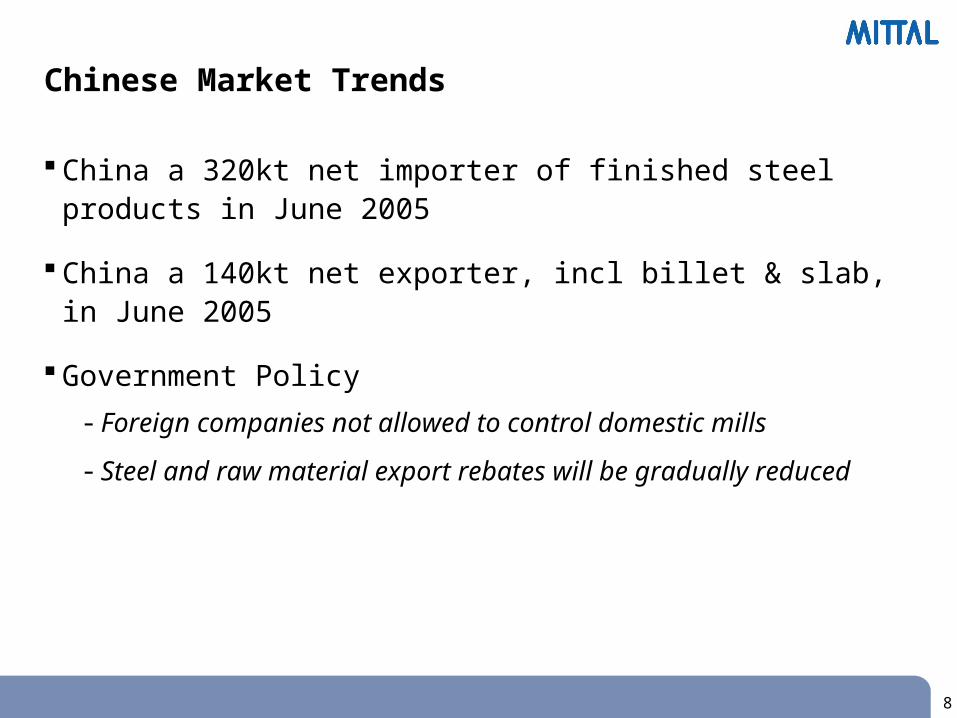

Chinese Market Trends

China a 320kt net importer of finished steel products in June 2005

China a 140kt net exporter, incl billet & slab, in June 2005

Government Policy

- Foreign companies not allowed to control domestic mills

- Steel and raw material export rebates will be gradually reduced

9

Chinese Market Trends

Domestic Industry Consolidation

- 10 largest mills will account for 50% of steel output by 2010

- Aims to create two industry giants with capacity > 30m tonnes

- Government will not ‘in principle’ grant approval for new steel plants

- Existing steel makers will be gradually reduced

Technology

- Promote production of high end, low cost steel products

- By 2010 steel mills to consume < 0.73 tpts of coal & < 8 tpts of water

China imposing internal regulations

Note: tpts = tonnes per tonne of steel

10

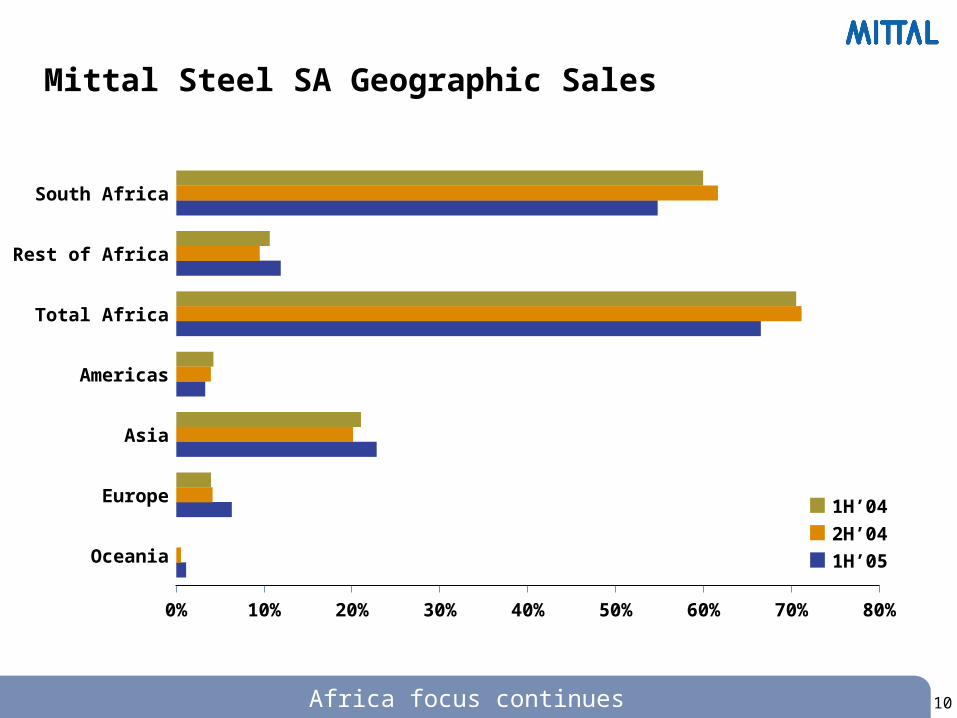

Mittal Steel SA Geographic Sales

South Africa

Rest of Africa

Total Africa

Americas

Asia

Europe

Oceania

0% 10% 20% 30% 40% 50% 60% 70% 80%

1H’05

2H’04

1H’04

Africa focus continues

11

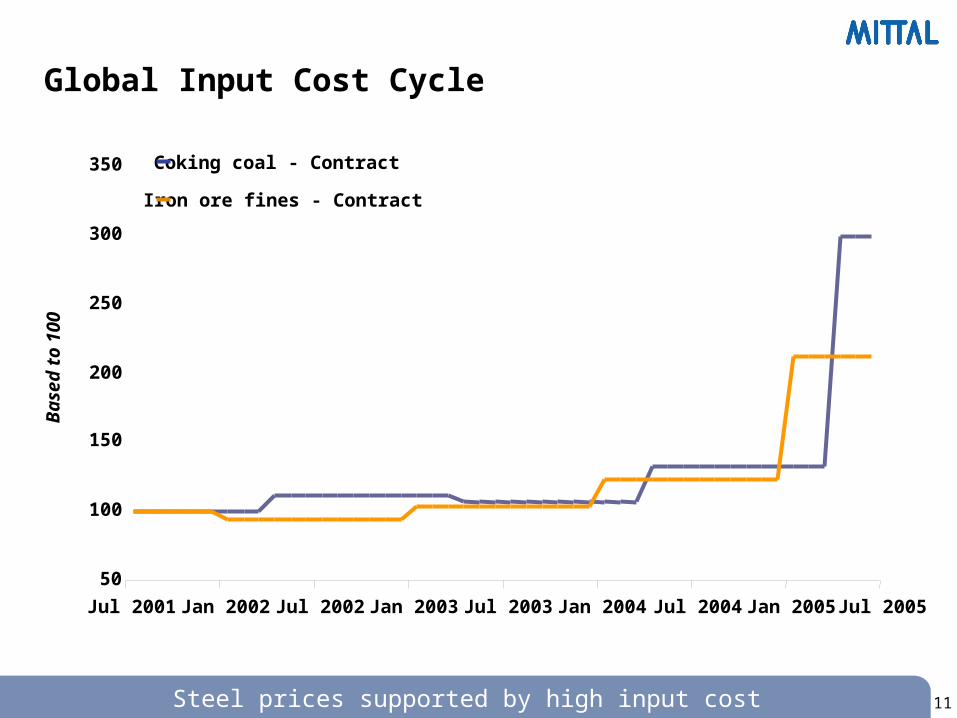

Global Input Cost CycleB

ased

to

10 0

Steel prices supported by high input cost

Coking coal - Contract

Iron ore fines - Contract

50

100

150

200

250

300

350

Jul 2001 Jan 2002 Jul 2002 Jan 2003 Jul 2003 Jan 2004 Jul 2004 Jan 2005 Jul 2005

12

Global Input Cost Cycle

600

500

400

300

200

100

0

700 Freight Rates - Spot

Coke - Spot

Scrap - Spot

New capacity taking effect

Bas

ed t

o 1

0 0

Jul 2001 Jan 2002 Jul 2002 Jan 2003 Jul 2003 Jan 2004 Jul 2004 Jan 2005 Jul 2005

13

Source: World Steel Dynamics

Global Input Cost Trends

Iron ore price increased by 71%

Metallurgical coking coal contracts settled at +120%

Freight rates slightly reduced but still at high levels

Coke prices reduced by 50% after peaking above US$400/t

Scrap prices coming down, still above long-term trend

Input material spot prices softening as new capacity starts to show

Various expansion projects to eliminate logistics chain bottlenecks

Further input costs increase expected

14

Key Performance Indicators

65 7771- long

48 4849Percentage value-add exports - flat

1 876 1 7531 686HRC cash cost - R/t

1H’05 2H’041H’04

(141)396657CI savings (Rm) - incl procurement

10 755 11 41612 072Number of full-time employees

3.4 3.73.9Man hours per ton steel

1 141 1 096874Revenue per head (R’000)

86 320519- excl procurement

303 284254- US$/t

Efficiency improvements partially countered high input costs

15

Liquid Steel Production

4 000

3 000

2 500

2 000

1 500

1 000

500

0

3 500

Vanderbijlpark Saldanha Long Products Total

1H’052H’041H’04

1829 17991986

563 664 616

1085 1093 1105

3477 35563707

Half year production record

’00 0

to

nn

es

16

Sales Volumes

ExportDomestic

470

1099

Vanderbijlpark Saldanha Long Products Total1H’04 2H’04 1H’05 1H’04 2H’04 1H’05 1H’04 2H’04 1H’05 1H’04 2H’04 1H’05

3 500

3 000

2 500

2 000

1 500

1 000

500

50

1569472

1125

1597

524

996

1520

350

198

548287

306

593

333

214

547390

594

984

353

557

910426

540

966

1210

1891

3101

1112

1988

3100

1283

1750

3033

Sales impacted by inventory adjustment

’00 0

to

nn

es

17

Environmental

Environmental projects > R1bn at different stages

Vanderbijlpark- Zero effluent discharge (MTP) 222 2H’05 - Cleaning of coke ovens gas 306 1H’06- New sinter plant off-gas system 210 2H’07- Blast Furnace D Tap floor de-dusting 40 Commissioned

Newcastle- Reverse osmosis plant 50 1H’06

Projects completed- Newcastle

• Coke oven repair project 231 2H’04

Environmental projects on track

PlannedCompletion

CostRm

18

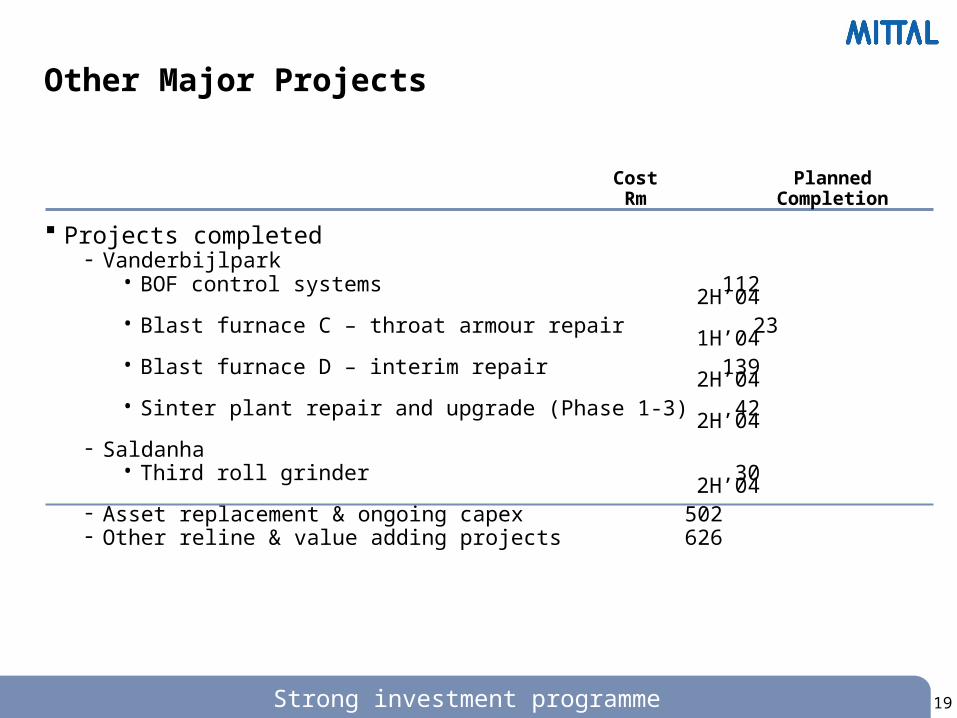

Other Major Projects

Investment plan of R8bn at different stages

Vanderbijlpark- Blast furnace C interim repair 40 2H’05- Blast furnace D reline 537 2H’06 - Blast furnace D – stoves 318 2H’06- 3rd sinter strand 288 2H’06- 2 New DRI kilns 432 2H’07

Saldanha- Corex reline 310 2H’07

Newcastle- Pulverised coal injection 211 Commissioned- Blast furnace N5 reline 590 2H’08

Mittal Coke & Chemicals- Market coke expansion 455 2H’06

Asset replacement & ongoing capex 1 280 Other downstream projects under investigation 1 300 Other reline & value adding projects 655

PlannedCompletion

CostRm

19

Other Major Projects

Projects completed- Vanderbijlpark

• BOF control systems 1122H’04

• Blast furnace C – throat armour repair 231H’04

• Blast furnace D – interim repair 1392H’04

• Sinter plant repair and upgrade (Phase 1-3) 422H’04

- Saldanha • Third roll grinder 30

2H’04- Asset replacement & ongoing capex 502- Other reline & value adding projects 626

Strong investment programme

PlannedCompletion

CostRm

f i n a n c e

21

Headline Earnings

Headline earnings

BAA remuneration*

- in US$m

Comparable earnings

Minority interest

Equity earnings*

Tax

- long-term provision top-up

Financing cost - net interest (expense)/income

Comparable operating profit

Revenue

3 221

521

3 221

(3)

153

(1 329)

(30)

83

4 347

12 264

1H’05

2 990

482

2 990

(2)

79

(1 551)

(37)

50

4 451

12 509

2H’04

1 551

(511)

311

2 062

(4)

179

(914)

(133)#

(14)

2 948

10 544

1H’04 Rm

* After tax# Lower discount rate accounts for R100m

Record earnings

22

Comparable Headline Earnings TrendR

m

1 750

1 500

1 250

1 000

750

500

250

0

657596

352

655 669

1393

1575

1415

15781643

1Q’03 2Q’03 3Q’03 4Q’03 1Q’04 2Q’04 3Q’04 4Q’04 1Q’05 2Q’05

Earnings level maintained

23

Operating Profit

4 347 4 451 2 217 Operating profit

(731)BAA remuneration

4 347 4 451 2 948 Comparable operating profit

(36)(91)(59)Corporate

12 24 18 Other

159 301 161 Coke and chemicals

1 195 1 129 640 Long products

685 799 348 Saldanha Steel

2 332 2 289 1 840 Vanderbijlpark

1H’05 2H’04 1H’04 Rm

Strong performance from all units

24

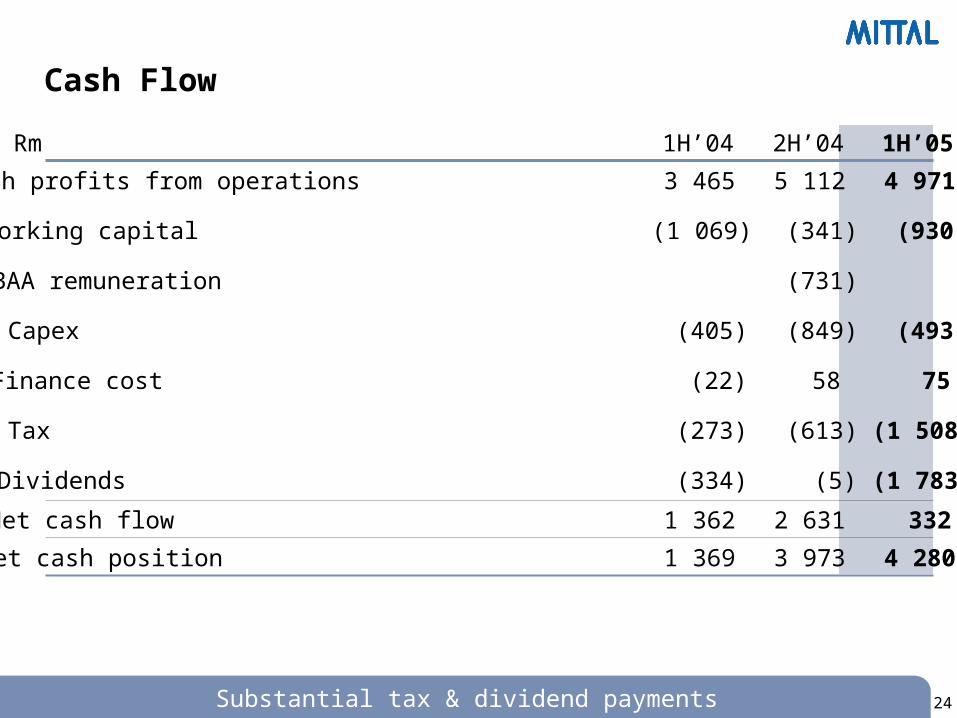

Cash Flow

4 280 3 973 1 369 Net cash position

332 2 631 1 362 Net cash flow

(1 783)(5)(334)Dividends

(1 508)(613)(273)Tax

75 58 (22)Finance cost

(493)(849)(405)Capex

(731)BAA remuneration

(930)(341)(1 069)Working capital

4 971 5 112 3 465 Cash profits from operations

1H’05 2H’04 1H’04 Rm

Substantial tax & dividend payments

25

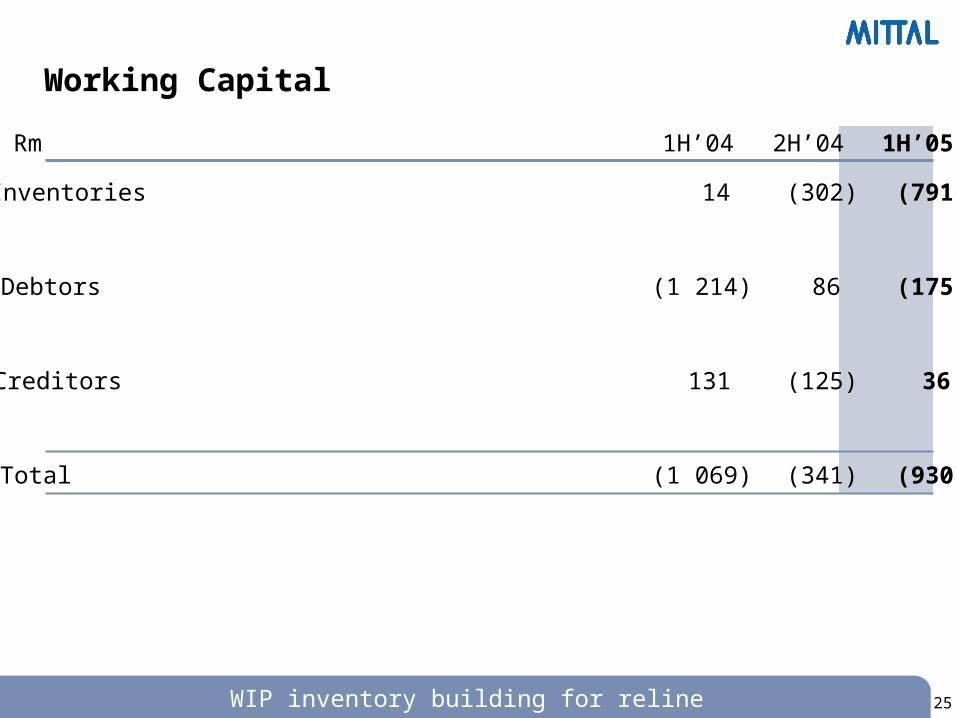

Working Capital

(930)(341)(1 069)Total

36 (125)131 Creditors

(175)86 (1 214)Debtors

(791)(302)14 Inventories

1H’05 2H’04 1H’04 Rm

WIP inventory building for reline

26

374030- on comparative basis (%)*

374023Return on equity (%)

1.51.71.4Revenue/invested capital (times)

403933- on comparative basis (%)*

403926EBITDA margin (%)

22.624.89.7Net cash/equity (%)

353628- on comparative basis (%)*

1H’052H’041H’04

353621Operating margin (%)

Financial Ratios

* Adjusted for once-off items

Sound business performance

27

Share Performance

2002 2003 2004 2005

350

300

250

200

150

100

50

0

Good investment case

Mittal Steel SA

All Share

Top 40

Bas

ed t

o 1

0 0

Source: I-Net Bridge

28

Dividend

Dividend policy

- Distributing one third of headline earnings

Dividend declared

- Interim dividend of 240 cents per share -12 September 2005

i n v e s t m e n t c a s e

30

Strategy Update

2 Mtpa throughput strategy

- Several projects at EIA stage

US$50/t Cost reduction strategy

- Newcastle PCI project exceeding expectations

Africa strategy

- 90% Africa focus inline with development plans of SA Govt & NEPAD

Strategy gaining momentum

31

Contribution to the Economy

R9bn capital investment programme

US$704m gross export revenue

Contribution to the state treasury of R1.6bn

Procurement from affirmative business enterprises of R805m

Refocused social investment on science & technology education

- Scitech exhibition (attendance 38 000 learners)

- Mittal National Science Olympiad (participation 10 000 learners)

Supporting economic growth

32

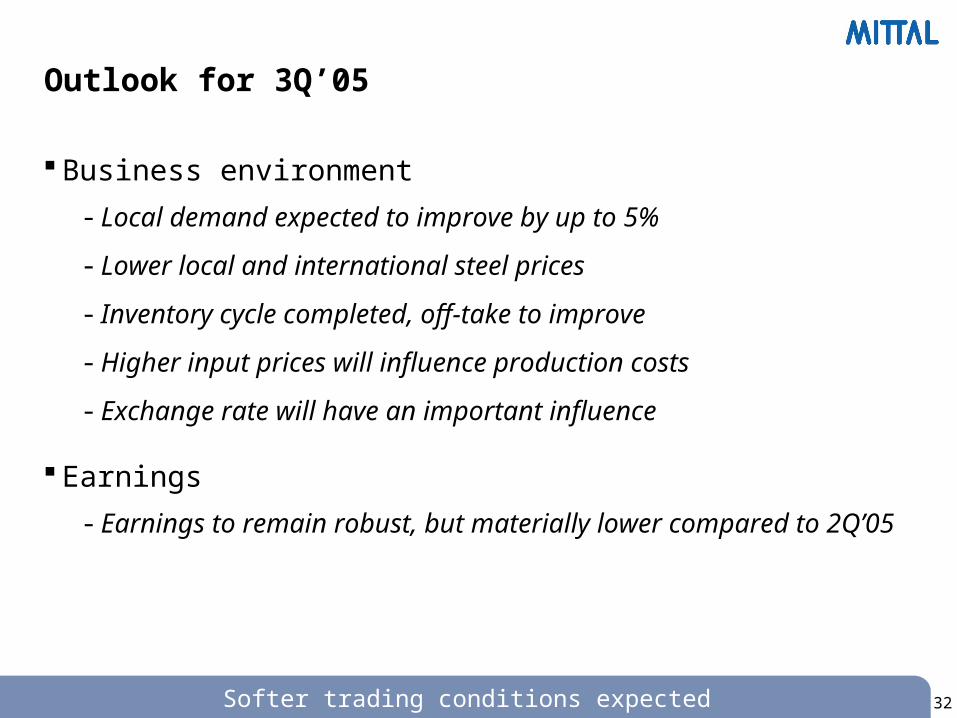

Outlook for 3Q’05

Business environment

- Local demand expected to improve by up to 5%

- Lower local and international steel prices

- Inventory cycle completed, off-take to improve

- Higher input prices will influence production costs

- Exchange rate will have an important influence

Earnings

- Earnings to remain robust, but materially lower compared to 2Q’05

Softer trading conditions expected

33

Mittal Steel Company NV

The world’s largest & most global steel producer

- Revenues of over US$32bn*

- Shipments of 69Mt*

- 14 operations on four continents

- 164 000 employees over 45 nationalities

- Major supplier to all steel consuming sectors

- Technology leadership with major R&D centres

- Significant vertical integration

- Unrivalled acquisition & turnaround experience

- Ranked 253rd ito revenues & 55th ito profits (Fortune 500)

*Pro-forma 2005

Shaping the future of steel

i n t e r i m r e s u l t sfor the six months ended june 2005

Related Documents