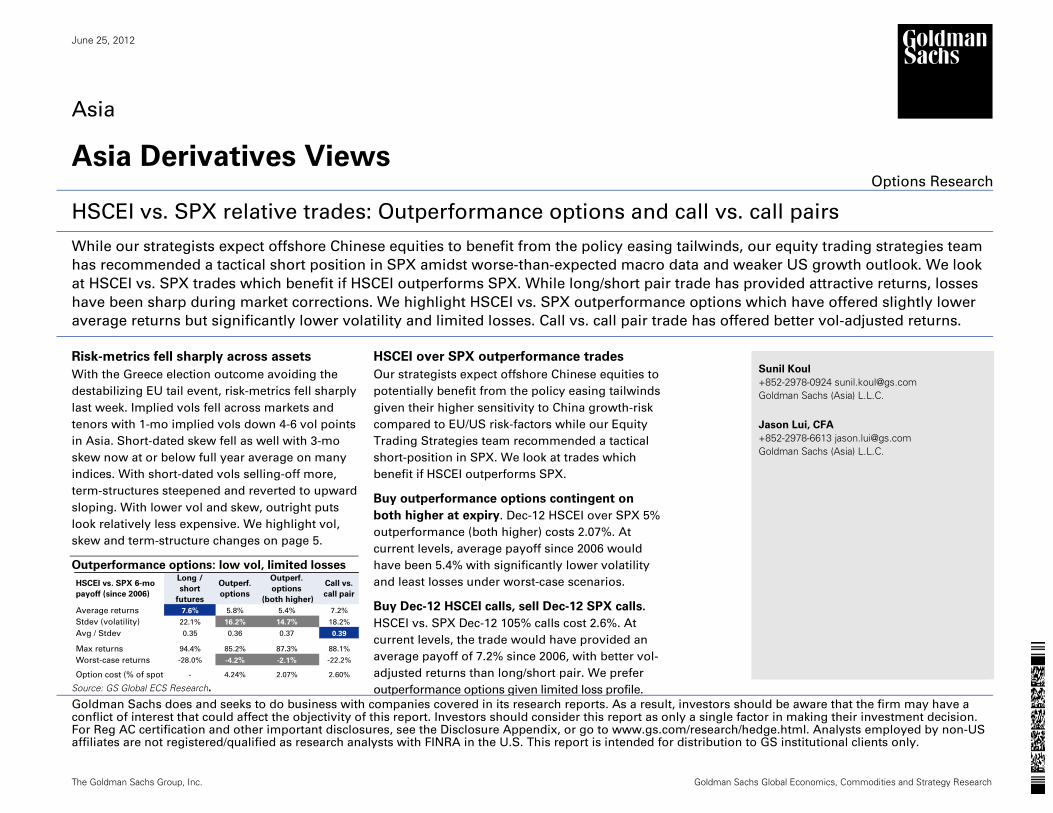

June 25, 2012 Asia Asia Derivatives Views Options Research HSCEI vs. SPX relative trades: Outperformance options and call vs. call pairs While our strategists expect offshore Chinese equities to benefit from the policy easing tailwinds, our equity trading strategies team has recommended a tactical short position in SPX amidst worse-than-expected macro data and weaker US growth outlook. We look at HSCEI vs. SPX trades which benefit if HSCEI outperforms SPX. While long/short pair trade has provided attractive returns, losses have been sharp during market corrections. We highlight HSCEI vs. SPX outperformance options which have offered slightly lower average returns but significantly lower volatility and limited losses. Call vs. call pair trade has offered better vol-adjusted returns. Risk-metrics fell sharply across assets With the Greece election outcome avoiding the destabilizing EU tail event, risk-metrics fell sharply last week. Implied vols fell across markets and tenors with 1-mo implied vols down 4-6 vol points in Asia. Short-dated skew fell as well with 3-mo skew now at or below full year average on many indices. With short-dated vols selling-off more, term-structures steepened and reverted to upward sloping. With lower vol and skew, outright puts look relatively less expensive. We highlight vol, skew and term-structure changes on page 5. Outperformance options: low vol, limited losses Source: GS Global ECS Research. HSCEI over SPX outperformance trades Our strategists expect offshore Chinese equities to potentially benefit from the policy easing tailwinds given their higher sensitivity to China growth-risk compared to EU/US risk-factors while our Equity Trading Strategies team recommended a tactical short-position in SPX. We look at trades which benefit if HSCEI outperforms SPX. Buy outperformance options contingent on both higher at expiry. Dec-12 HSCEI over SPX 5% outperformance (both higher) costs 2.07%. At current levels, average payoff since 2006 would have been 5.4% with significantly lower volatility and least losses under worst-case scenarios. Buy Dec-12 HSCEI calls, sell Dec-12 SPX calls. HSCEI vs. SPX Dec-12 105% calls cost 2.6%. At current levels, the trade would have provided an average payoff of 7.2% since 2006, with better vol- adjusted returns than long/short pair. We prefer outperformance options given limited loss profile. Sunil Koul +852-2978-0924 [email protected] Goldman Sachs (Asia) L.L.C. Jason Lui, CFA +852-2978-6613 [email protected] Goldman Sachs (Asia) L.L.C. Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. This report is intended for distribution to GS institutional clients only. The Goldman Sachs Group, Inc. Goldman Sachs Global Economics, Commodities and Strategy Research HSCEI vs. SPX 6-mo payoff (since 2006) Long / short futures Outperf. options Outperf. options (both higher) Call vs. call pair Average returns 7.6% 5.8% 5.4% 7.2% Stdev (volatility) 22.1% 16.2% 14.7% 18.2% Avg / Stdev 0.35 0.36 0.37 0.39 Max returns 94.4% 85.2% 87.3% 88.1% Worst-case returns -28.0% -4.2% -2.1% -22.2% Option cost (% of spot - 4.24% 2.07% 2.60%

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

June 25, 2012

Asia

Asia Derivatives Views Options Research

HSCEI vs. SPX relative trades: Outperformance options and call vs. call pairs

While our strategists expect offshore Chinese equities to benefit from the policy easing tailwinds, our equity trading strategies team

has recommended a tactical short position in SPX amidst worse-than-expected macro data and weaker US growth outlook. We look

at HSCEI vs. SPX trades which benefit if HSCEI outperforms SPX. While long/short pair trade has provided attractive returns, losses

have been sharp during market corrections. We highlight HSCEI vs. SPX outperformance options which have offered slightly lower

average returns but significantly lower volatility and limited losses. Call vs. call pair trade has offered better vol-adjusted returns.

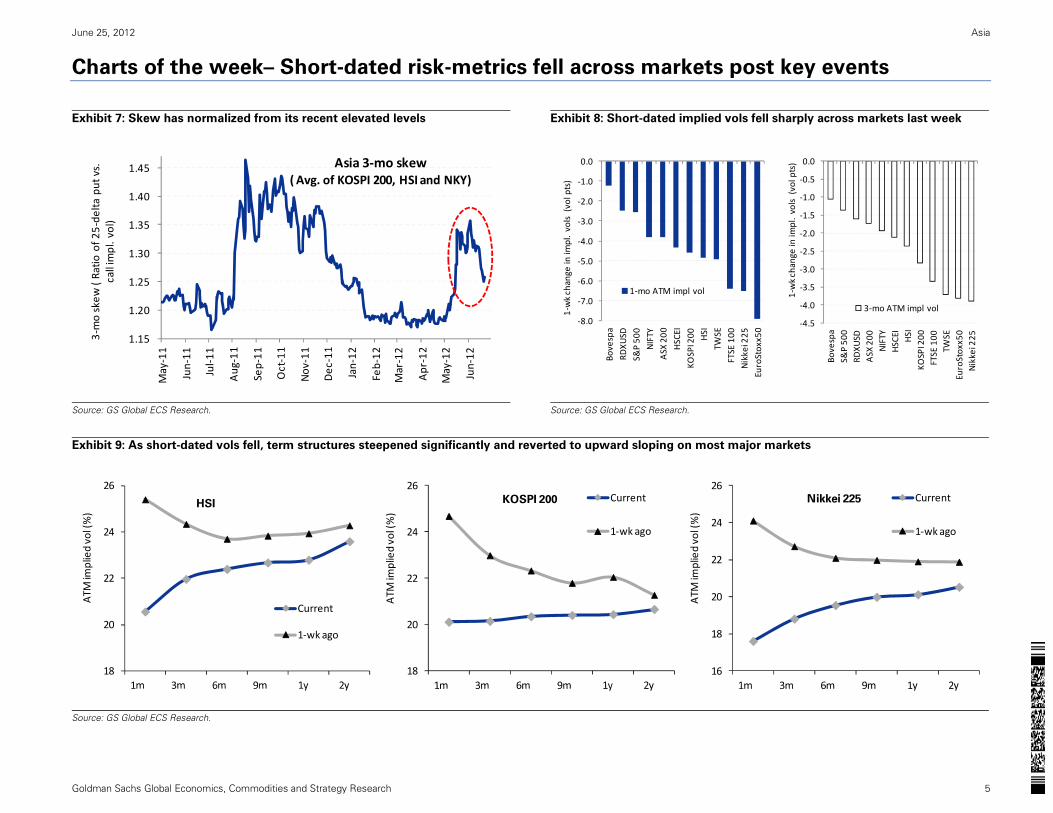

Risk-metrics fell sharply across assets

With the Greece election outcome avoiding the

destabilizing EU tail event, risk-metrics fell sharply

last week. Implied vols fell across markets and

tenors with 1-mo implied vols down 4-6 vol points

in Asia. Short-dated skew fell as well with 3-mo

skew now at or below full year average on many

indices. With short-dated vols selling-off more,

term-structures steepened and reverted to upward

sloping. With lower vol and skew, outright puts

look relatively less expensive. We highlight vol,

skew and term-structure changes on page 5.

Outperformance options: low vol, limited losses

Source: GS Global ECS Research.

HSCEI over SPX outperformance trades

Our strategists expect offshore Chinese equities to

potentially benefit from the policy easing tailwinds

given their higher sensitivity to China growth-risk

compared to EU/US risk-factors while our Equity

Trading Strategies team recommended a tactical

short-position in SPX. We look at trades which

benefit if HSCEI outperforms SPX.

Buy outperformance options contingent on

both higher at expiry. Dec-12 HSCEI over SPX 5%

outperformance (both higher) costs 2.07%. At

current levels, average payoff since 2006 would

have been 5.4% with significantly lower volatility

and least losses under worst-case scenarios.

Buy Dec-12 HSCEI calls, sell Dec-12 SPX calls.

HSCEI vs. SPX Dec-12 105% calls cost 2.6%. At

current levels, the trade would have provided an

average payoff of 7.2% since 2006, with better vol-

adjusted returns than long/short pair. We prefer

outperformance options given limited loss profile.

Sunil Koul

+852-2978-0924 [email protected] Goldman Sachs (Asia) L.L.C.

Jason Lui, CFA

+852-2978-6613 [email protected] Goldman Sachs (Asia) L.L.C.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. This report is intended for distribution to GS institutional clients only.

The Goldman Sachs Group, Inc. Goldman Sachs Global Economics, Commodities and Strategy Research

HSCEI vs. SPX 6-mo

payoff (since 2006)

Long /

short

futures

Outperf.

options

Outperf.

options

(both higher)

Call vs.

call pair

Average returns 7.6% 5.8% 5.4% 7.2%

Stdev (volatility) 22.1% 16.2% 14.7% 18.2%

Avg / Stdev 0.35 0.36 0.37 0.39

Max returns 94.4% 85.2% 87.3% 88.1%

Worst-case returns -28.0% -4.2% -2.1% -22.2%

Option cost (% of spot - 4.24% 2.07% 2.60%

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 2

HSCEI vs. SPX relative trades: Outperformance options and call vs. call pairs

Our strategists expect offshore Chinese equities to benefit from the policy easing tailwinds. As highlighted in our latest

Growth Markets Perspective: Strategies for a China loosening cycle (June 21), offshore Chinese equities have a higher risk-

sensitivity to China growth risk compared to EU/US risk-factors and could potentially benefit from the ongoing and further policy

easing. While HSCEI sold off 11% amidst EU sovereign concerns in May, onshore China equities (CSI 300) ended the month

essentially flat suggesting offshore equities could close the gap relative to A-shares, should global macro risks normalize. Easier

financial conditions, coupled with inexpensive valuations and light positioning drives our positive strategic stance for Chinese

equities.

On the other hand, our Equity Trading Strategies team recommended a tactical short position in S&P 500. Our Equity Trading

Strategists in their recent report (Trade Update: Recommending short position in the S&P 500, June 21) recommend a tactical short

position in SPX with a near-term downside target of 1285, on the back of worse-than-expected macro data and weaker US-growth

outlook while our US strategist expects SPX to trade at 1250 by year-end (6.5% downside from current levels).

We look at relative option trades to express our preference for HSCEI over SPX. An easier China policy with deteriorating US

growth outlook could cause HSCEI to outperform SPX during 2H12, in our view. We look at HSCEI vs. SPX trades which could benefit if

HSCEI outperforms SPX. We compare HSCEI vs. SPX outperformance options and call vs. call pair trades to a long-short futures

pair trade as shown below:

(1) Long Dec-12 HSCEI over SPX 105% outperformance options, contingent on both indices higher, for 2.07%.

Outperformance options contingent on both indices higher has a bullish bias to equities and provides positive returns only if SPX

and HSCEI are both higher at expiration by year-end. The advantage of contingent options is a lower upfront premium. Currently

Dec-12 (28-Dec-12 expiry) HSCEI over SPX 5% strike outperformance, contingent on both indices higher, costs 2.07%, at more than

50% discount to vanilla 5% strike outperformance options (4.24%). HSCEI has historically made larger directional moves compared

to SPX, both on the up-side and down-side (Exhibit 1 in p.3). So the risk-reward on outperformance options contingent on both

indices higher looks better compared to vanilla outperformance options. The disadvantage however is that the trade provides no

return if HSCEI rallies while SPX falls. As shown in exhibit 2 and 3, we look at the historical profitability of a 6-mo HSCEI over SPX

5% outperformance options when entered at current levels. Since 2006, the average payoff for the outperformance option

contingent on both indices higher, has been 5.4%, less than long/short or call vs. call pair trade but with significantly lower

volatility and limited losses. Risk is loss of upfront premium.

(2) Long HSCEI Dec-12 105% calls vs. short SPX Dec-12 105% calls. Pay 2.6% in upfront premium.

Compared to a long/short futures trade, call vs. call pair trade isolates returns to the case where either of the markets is higher at

expiration. While HSCEI/SPX long-short pair has had sharp negative returns during market corrections, the call vs. call pair trade will

have a maximum loss of 2.6% upfront premium if SPX is lower at expiry. As shown in Exhibit 4 on p.4, we look at historical payoff of

buying 6-mo HSCEI 105% calls vs. selling 6-mo SPX 105% calls. At current levels, the trade would have provided an average return

of 7.2% since 2006 (vs. 7.6% for long/short pair) but with lower volatility and thus better vol-adjusted returns. Risks: Buyers of HSCEI

vs. SPX call vs. call pair trade risk unlimited loss if SPX rallies significantly more than HSCEI by expiry.

We prefer outperformance options to long/short futures or call vs. call pair trade given limited loss profile of the trade.

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 3

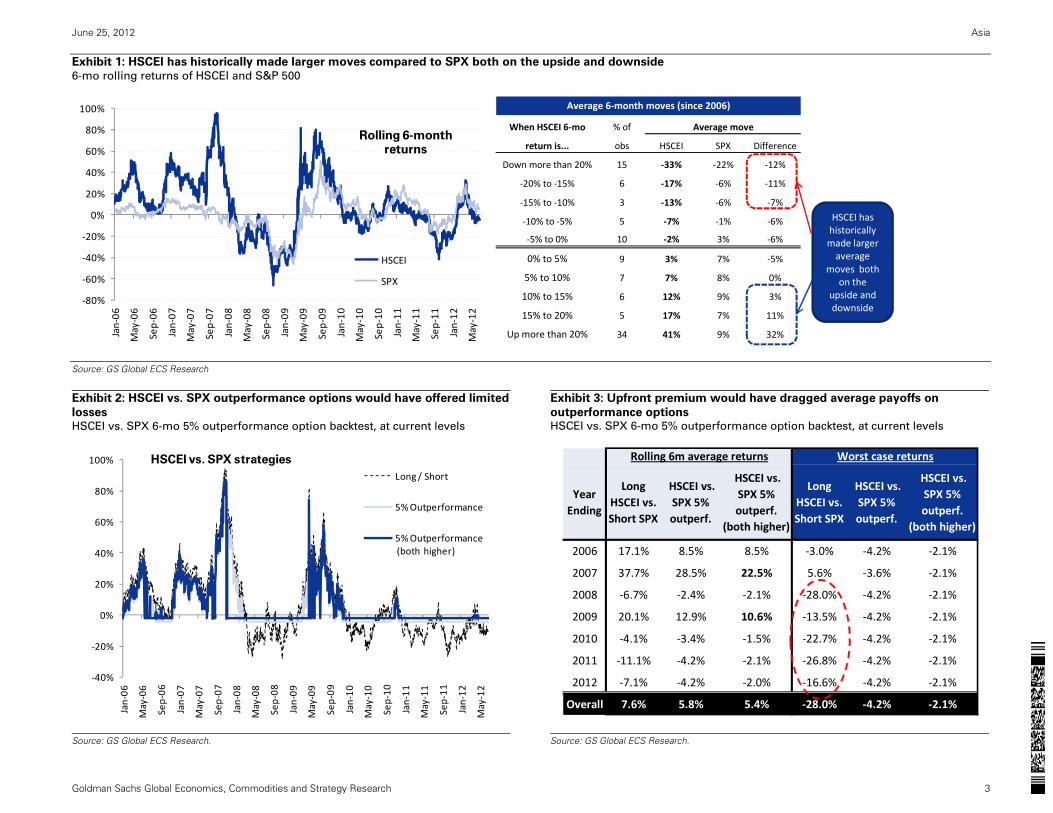

Exhibit 1: HSCEI has historically made larger moves compared to SPX both on the upside and downside

6-mo rolling returns of HSCEI and S&P 500

Source: GS Global ECS Research

Exhibit 2: HSCEI vs. SPX outperformance options would have offered limited

losses HSCEI vs. SPX 6-mo 5% outperformance option backtest, at current levels

Exhibit 3: Upfront premium would have dragged average payoffs on

outperformance options HSCEI vs. SPX 6-mo 5% outperformance option backtest, at current levels

Source: GS Global ECS Research.

Source: GS Global ECS Research.

‐80%

‐60%

‐40%

‐20%

0%

20%

40%

60%

80%

100%Jan‐06

May‐06

Sep‐06

Jan‐07

May‐07

Sep‐07

Jan‐08

May‐08

Sep‐08

Jan‐09

May‐09

Sep‐09

Jan‐10

May‐10

Sep‐10

Jan‐11

May‐11

Sep‐11

Jan‐12

May‐12

HSCEI

SPX

Rolling 6-month returns

Average 6‐month moves (since 2006)

When HSCEI 6‐mo % of Average move

return is... obs HSCEI SPX Difference

Down more than 20% 15 ‐33% ‐22% ‐12%

‐20% to ‐15% 6 ‐17% ‐6% ‐11%

‐15% to ‐10% 3 ‐13% ‐6% ‐7%

‐10% to ‐5% 5 ‐7% ‐1% ‐6%

‐5% to 0% 10 ‐2% 3% ‐6%

0% to 5% 9 3% 7% ‐5%

5% to 10% 7 7% 8% 0%

10% to 15% 6 12% 9% 3%

15% to 20% 5 17% 7% 11%

Up more than 20% 34 41% 9% 32%

HSCEI has historically made larger average

moves both on the

upside anddownside

‐40%

‐20%

0%

20%

40%

60%

80%

100%

Jan‐06

May‐06

Sep‐06

Jan‐07

May‐07

Sep‐07

Jan‐08

May‐08

Sep‐08

Jan‐09

May‐09

Sep‐09

Jan‐10

May‐10

Sep‐10

Jan‐11

May‐11

Sep‐11

Jan‐12

May‐12

Long / Short

5% Outperformance

5% Outperformance(both higher)

HSCEI vs. SPX strategies

Year Ending

Long HSCEI vs. Short SPX

HSCEI vs. SPX 5% outperf.

HSCEI vs. SPX 5% outperf.

(both higher)

Long HSCEI vs. Short SPX

HSCEI vs. SPX 5% outperf.

HSCEI vs. SPX 5% outperf.

(both higher)

2006 17.1% 8.5% 8.5% ‐3.0% ‐4.2% ‐2.1%

2007 37.7% 28.5% 22.5% 5.6% ‐3.6% ‐2.1%

2008 ‐6.7% ‐2.4% ‐2.1% ‐28.0% ‐4.2% ‐2.1%

2009 20.1% 12.9% 10.6% ‐13.5% ‐4.2% ‐2.1%

2010 ‐4.1% ‐3.4% ‐1.5% ‐22.7% ‐4.2% ‐2.1%

2011 ‐11.1% ‐4.2% ‐2.1% ‐26.8% ‐4.2% ‐2.1%

2012 ‐7.1% ‐4.2% ‐2.0% ‐16.6% ‐4.2% ‐2.1%

Overall 7.6% 5.8% 5.4% ‐28.0% ‐4.2% ‐2.1%

Rolling 6m average returns Worst case returns

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 4

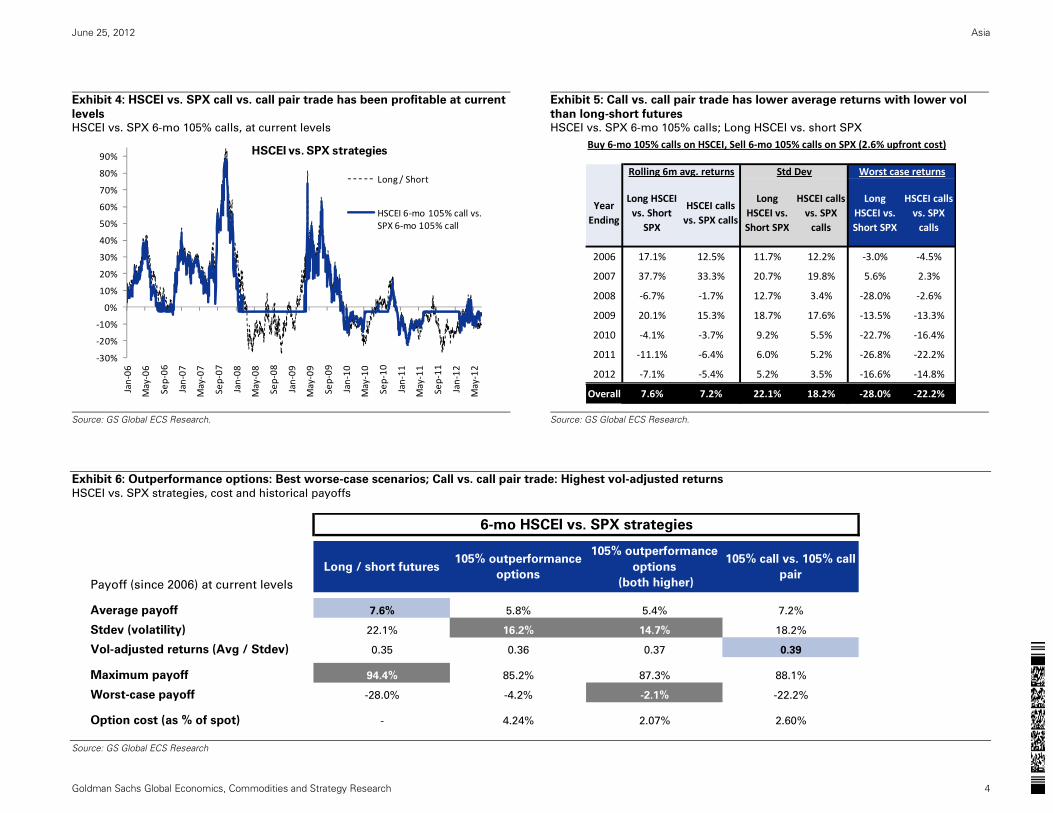

Exhibit 4: HSCEI vs. SPX call vs. call pair trade has been profitable at current

levels HSCEI vs. SPX 6-mo 105% calls, at current levels

Exhibit 5: Call vs. call pair trade has lower average returns with lower vol

than long-short futures HSCEI vs. SPX 6-mo 105% calls; Long HSCEI vs. short SPX

Source: GS Global ECS Research.

Source: GS Global ECS Research.

Exhibit 6: Outperformance options: Best worse-case scenarios; Call vs. call pair trade: Highest vol-adjusted returns

HSCEI vs. SPX strategies, cost and historical payoffs

Source: GS Global ECS Research

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Jan‐06

May‐06

Sep‐06

Jan‐07

May‐07

Sep‐07

Jan‐08

May‐08

Sep‐08

Jan‐09

May‐09

Sep‐09

Jan‐10

May‐10

Sep‐10

Jan‐11

May‐11

Sep‐11

Jan‐12

May‐12

Long / Short

HSCEI 6‐mo 105% call vs. SPX 6‐mo 105% call

HSCEI vs. SPX strategiesBuy 6‐mo 105% calls on HSCEI, Sell 6‐mo 105% calls on SPX (2.6% upfront cost)

Year Ending

Long HSCEI vs. Short

SPX

HSCEI calls vs. SPX calls

Long HSCEI vs. Short SPX

HSCEI calls vs. SPX calls

Long HSCEI vs. Short SPX

HSCEI calls vs. SPX calls

2006 17.1% 12.5% 11.7% 12.2% ‐3.0% ‐4.5%

2007 37.7% 33.3% 20.7% 19.8% 5.6% 2.3%

2008 ‐6.7% ‐1.7% 12.7% 3.4% ‐28.0% ‐2.6%

2009 20.1% 15.3% 18.7% 17.6% ‐13.5% ‐13.3%

2010 ‐4.1% ‐3.7% 9.2% 5.5% ‐22.7% ‐16.4%

2011 ‐11.1% ‐6.4% 6.0% 5.2% ‐26.8% ‐22.2%

2012 ‐7.1% ‐5.4% 5.2% 3.5% ‐16.6% ‐14.8%

Overall 7.6% 7.2% 22.1% 18.2% ‐28.0% ‐22.2%

Rolling 6m avg. returns Std Dev Worst case returns

Payoff (since 2006) at current levels

Long / short futures105% outperformance

options

105% outperformance

options

(both higher)

105% call vs. 105% call

pair

Average payoff 7.6% 5.8% 5.4% 7.2%

Stdev (volatility) 22.1% 16.2% 14.7% 18.2%

Vol-adjusted returns (Avg / Stdev) 0.35 0.36 0.37 0.39

Maximum payoff 94.4% 85.2% 87.3% 88.1%

Worst-case payoff -28.0% -4.2% -2.1% -22.2%

Option cost (as % of spot) - 4.24% 2.07% 2.60%

6-mo HSCEI vs. SPX strategies

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 5

Charts of the week– Short-dated risk-metrics fell across markets post key events

Exhibit 7: Skew has normalized from its recent elevated levels

Exhibit 8: Short-dated implied vols fell sharply across markets last week

Source: GS Global ECS Research.

Source: GS Global ECS Research.

Exhibit 9: As short-dated vols fell, term structures steepened significantly and reverted to upward sloping on most major markets

Source: GS Global ECS Research.

1.15

1.20

1.25

1.30

1.35

1.40

1.45May‐11

Jun‐11

Jul‐1

1

Aug

‐11

Sep‐11

Oct‐11

Nov

‐11

Dec

‐11

Jan‐12

Feb‐12

Mar‐12

Apr‐12

May‐12

Jun‐12

3‐mo skew

( Ratio

of 2

5‐de

lta put vs.

call impl. vol)

Asia 3‐mo skew ( Avg. of KOSPI 200, HSI and NKY)

‐8.0

‐7.0

‐6.0

‐5.0

‐4.0

‐3.0

‐2.0

‐1.0

0.0

Bovespa

RDXU

SDS&

P 50

0NIFTY

ASX

200

HSCEI

KOSPI 200 HSI

TWSE

FTSE 100

Nikkei 225

EuroStoxx50

1‐wk change

in im

pl. vols (vol pts)

1‐mo ATM impl vol

‐4.5

‐4.0

‐3.5

‐3.0

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

Bovespa

S&P 50

0RD

XUSD

ASX

200

NIFTY

HSCEI HSI

KOSPI 200

FTSE 100

TWSE

EuroStoxx50

Nikkei 225

1‐wk change

in im

pl. vols (vol pts)

3‐mo ATM impl vol

18

20

22

24

26

ATM

implied vol (%)

Current

1‐wk ago

HSI

18

20

22

24

26

ATM

implied vol (%)

Current

1‐wk ago

KOSPI 200

16

18

20

22

24

26

ATM

implied vol (%)

Current

1‐wk ago

Nikkei 225

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 6

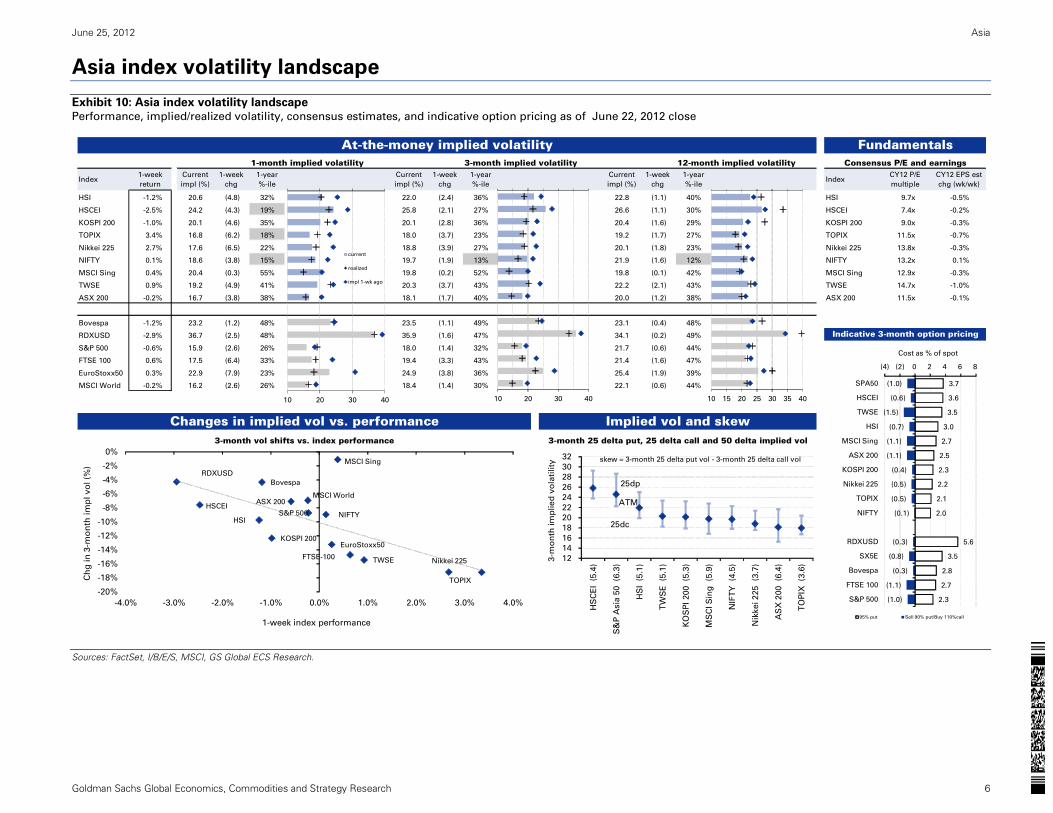

Asia index volatility landscape

Exhibit 10: Asia index volatility landscape

Performance, implied/realized volatility, consensus estimates, and indicative option pricing as of June 22, 2012 close

Sources: FactSet, I/B/E/S, MSCI, GS Global ECS Research.

1-month implied volatility 3-month implied volatility 12-month implied volatility

Index1-week

return

Current

impl (%)

1-week

chg

1-year

%-ile

Current

impl (%)

1-week

chg

1-year

%-ile

Current

impl (%)

1-week

chg

1-year

%-ileIndex

CY12 P/E

multiple

CY12 EPS est

chg (wk/wk)

HSI -1.2% 20.6 (4.8) 32% 22.0 (2.4) 36% 22.8 (1.1) 40% HSI 9.7x -0.5%

HSCEI -2.5% 24.2 (4.3) 19% 25.8 (2.1) 27% 26.6 (1.1) 30% HSCEI 7.4x -0.2%

KOSPI 200 -1.0% 20.1 (4.6) 35% 20.1 (2.8) 36% 20.4 (1.6) 29% KOSPI 200 9.0x -0.3%

TOPIX 3.4% 16.8 (6.2) 18% 18.0 (3.7) 23% 19.2 (1.7) 27% TOPIX 11.5x -0.7%

Nikkei 225 2.7% 17.6 (6.5) 22% 18.8 (3.9) 27% 20.1 (1.8) 23% Nikkei 225 13.8x -0.3%

NIFTY 0.1% 18.6 (3.8) 15% 19.7 (1.9) 13% 21.9 (1.6) 12% NIFTY 13.2x 0.1%

MSCI Sing 0.4% 20.4 (0.3) 55% 19.8 (0.2) 52% 19.8 (0.1) 42% MSCI Sing 12.9x -0.3%

TWSE 0.9% 19.2 (4.9) 41% 20.3 (3.7) 43% 22.2 (2.1) 43% TWSE 14.7x -1.0%

ASX 200 -0.2% 16.7 (3.8) 38% 18.1 (1.7) 40% 20.0 (1.2) 38% ASX 200 11.5x -0.1%

Bovespa -1.2% 23.2 (1.2) 48% 23.5 (1.1) 49% 23.1 (0.4) 48%

RDXUSD -2.9% 36.7 (2.5) 48% 35.9 (1.6) 47% 34.1 (0.2) 49%

S&P 500 -0.6% 15.9 (2.6) 26% 18.0 (1.4) 32% 21.7 (0.6) 44%

FTSE 100 0.6% 17.5 (6.4) 33% 19.4 (3.3) 43% 21.4 (1.6) 47%

EuroStoxx50 0.3% 22.9 (7.9) 23% 24.9 (3.8) 36% 25.4 (1.9) 39%

MSCI World -0.2% 16.2 (2.6) 26% 18.4 (1.4) 30% 22.1 (0.6) 44%

3-month 25 delta put, 25 delta call and 50 delta implied vol3-month vol shifts vs. index performance

FundamentalsConsensus P/E and earnings

Changes in implied vol vs. performance

At-the-money implied volatility

Implied vol and skew

Indicative 3-month option pricing

12

14

16

18

20

22

24

26

28

30

32

HS

CE

I (

5.4

)

S&

P A

sia

50

(6

.3)

HS

I (

5.1

)

TW

SE

(5

.1)

KO

SP

I 200

(5

.3)

MS

CI S

ing

(5

.9)

NIF

TY

(4

.5)

Nik

kei 2

25

(3.7

)

AS

X 2

00

(6.4

)

TO

PIX

(3

.6)

3-m

on

th im

plie

d v

ola

tility

ATM

25dc

skew = 3-month 25 delta put vol - 3-month 25 delta call vol

25dp

3.7

3.6

3.5

3.0

2.7

2.5

2.3

2.2

2.1

2.0

5.6

3.5

2.8

2.7

2.3

(1.0)

(0.6)

(1.5)

(0.7)

(1.1)

(1.1)

(0.4)

(0.5)

(0.5)

(0.1)

(0.3)

(0.8)

(0.3)

(1.1)

(1.0)

(4) (2) 0 2 4 6 8

SPA50

HSCEI

TWSE

HSI

MSCI Sing

ASX 200

KOSPI 200

Nikkei 225

TOPIX

NIFTY

RDXUSD

SX5E

Bovespa

FTSE 100

S&P 500

Cost as % of spot

95% put Sell 90% put/Buy 110%call

10 20 30 40

current

realized

impl 1-wk ago

10 20 30 40 10 15 20 25 30 35 40

HSI

HSCEI

KOSPI 200

TOPIX

Nikkei 225

NIFTY

MSCI Sing

TWSE

ASX 200

Bovespa

S&P 500

FTSE-100

EuroStoxx50

RDXUSD

MSCI World

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

-4.0% -3.0% -2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0%

Ch

g i

n 3

-mo

nth

im

pl

vo

l (%

)

1-week index performance

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 7

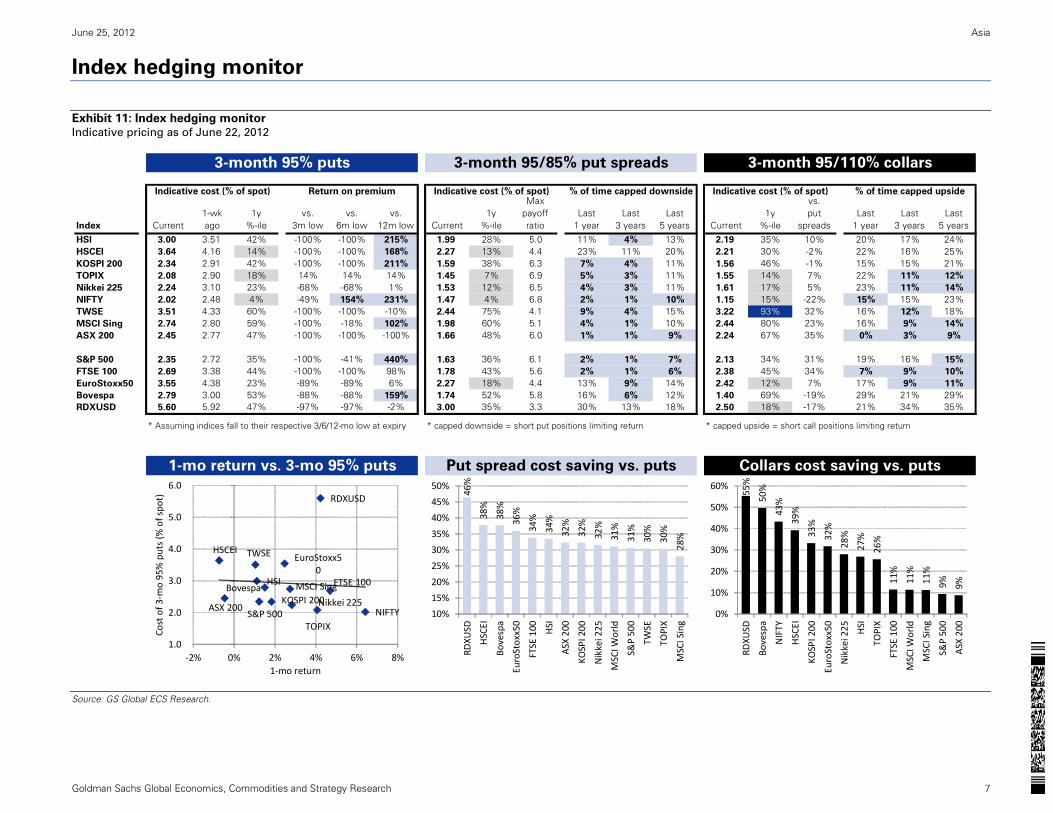

Index hedging monitor

Exhibit 11: Index hedging monitor

Indicative pricing as of June 22, 2012

Source: GS Global ECS Research.

3-month 95% puts 3-month 95/85% put spreads 3-month 95/110% collars

Indicative cost (% of spot) Return on premium Indicative cost (% of spot) % of time capped downside Indicative cost (% of spot) % of time capped upside

Index Current1-wk ago

1y %-ile

vs. 3m low

vs. 6m low

vs. 12m low Current

1y %-ile

Max payoff ratio

Last 1 year

Last 3 years

Last 5 years Current

1y %-ile

vs. put

spreadsLast

1 yearLast

3 yearsLast

5 years

HSI 3.00 3.51 42% -100% -100% 215% 1.99 28% 5.0 11% 4% 13% 2.19 35% 10% 20% 17% 24%HSCEI 3.64 4.16 14% -100% -100% 168% 2.27 13% 4.4 23% 11% 20% 2.21 30% -2% 22% 16% 25%KOSPI 200 2.34 2.91 42% -100% -100% 211% 1.59 38% 6.3 7% 4% 11% 1.56 46% -1% 15% 15% 21%TOPIX 2.08 2.90 18% 14% 14% 14% 1.45 7% 6.9 5% 3% 11% 1.55 14% 7% 22% 11% 12%

Nikkei 225 2.24 3.10 23% -68% -68% 1% 1.53 12% 6.5 4% 3% 11% 1.61 17% 5% 23% 11% 14%

NIFTY 2.02 2.48 4% -49% 154% 231% 1.47 4% 6.8 2% 1% 10% 1.15 15% -22% 15% 15% 23%TWSE 3.51 4.33 60% -100% -100% -10% 2.44 75% 4.1 9% 4% 15% 3.22 93% 32% 16% 12% 18%MSCI Sing 2.74 2.80 59% -100% -18% 102% 1.98 60% 5.1 4% 1% 10% 2.44 80% 23% 16% 9% 14%

ASX 200 2.45 2.77 47% -100% -100% -100% 1.66 48% 6.0 1% 1% 9% 2.24 67% 35% 0% 3% 9%

S&P 500 2.35 2.72 35% -100% -41% 440% 1.63 36% 6.1 2% 1% 7% 2.13 34% 31% 19% 16% 15%

FTSE 100 2.69 3.38 44% -100% -100% 98% 1.78 43% 5.6 2% 1% 6% 2.38 45% 34% 7% 9% 10%

EuroStoxx50 3.55 4.38 23% -89% -89% 6% 2.27 18% 4.4 13% 9% 14% 2.42 12% 7% 17% 9% 11%

Bovespa 2.79 3.00 53% -88% -88% 159% 1.74 52% 5.8 16% 6% 12% 1.40 69% -19% 29% 21% 29%RDXUSD 5.60 5.92 47% -97% -97% -2% 3.00 35% 3.3 30% 13% 18% 2.50 18% -17% 21% 34% 35%

* Assuming indices fall to their respective 3/6/12-mo low at expiry * capped downside = short put positions limiting return * capped upside = short call positions limiting return

1-mo return vs. 3-mo 95% puts Put spread cost saving vs. puts Collars cost saving vs. puts

HSI

HSCEI

KOSPI 200

TOPIX

Nikkei 225NIFTY

TWSE

MSCI Sing

ASX 200S&P 500

FTSE 100

EuroStoxx50

Bovespa

RDXUSD

1.0

2.0

3.0

4.0

5.0

6.0

‐2% 0% 2% 4% 6% 8%

Cost of 3

‐mo 95% puts (%

of spo

t)

1‐mo return

46%

38%

38%

36%

34%

34%

32%

32%

32%

31%

31%

30%

30%

28%

10%

15%

20%

25%

30%

35%

40%

45%

50%

RDXU

SD

HSCEI

Bovespa

EuroStoxx50

FTSE 100 HSI

ASX 200

KOSPI 200

Nikkei 225

MSCI W

orld

S&P 500

TWSE

TOPIX

MSCI Sing

55%

50%

43%

39%

33%

32%

28%

27%

26%

11%

11%

11%

9% 9%

0%

10%

20%

30%

40%

50%

60%

RDXU

SD

Bovespa

NIFTY

HSCEI

KOSPI 200

EuroStoxx50

Nikkei 225 HSI

TOPIX

FTSE 100

MSCI W

orld

MSCI Sing

S&P 500

ASX 200

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 8

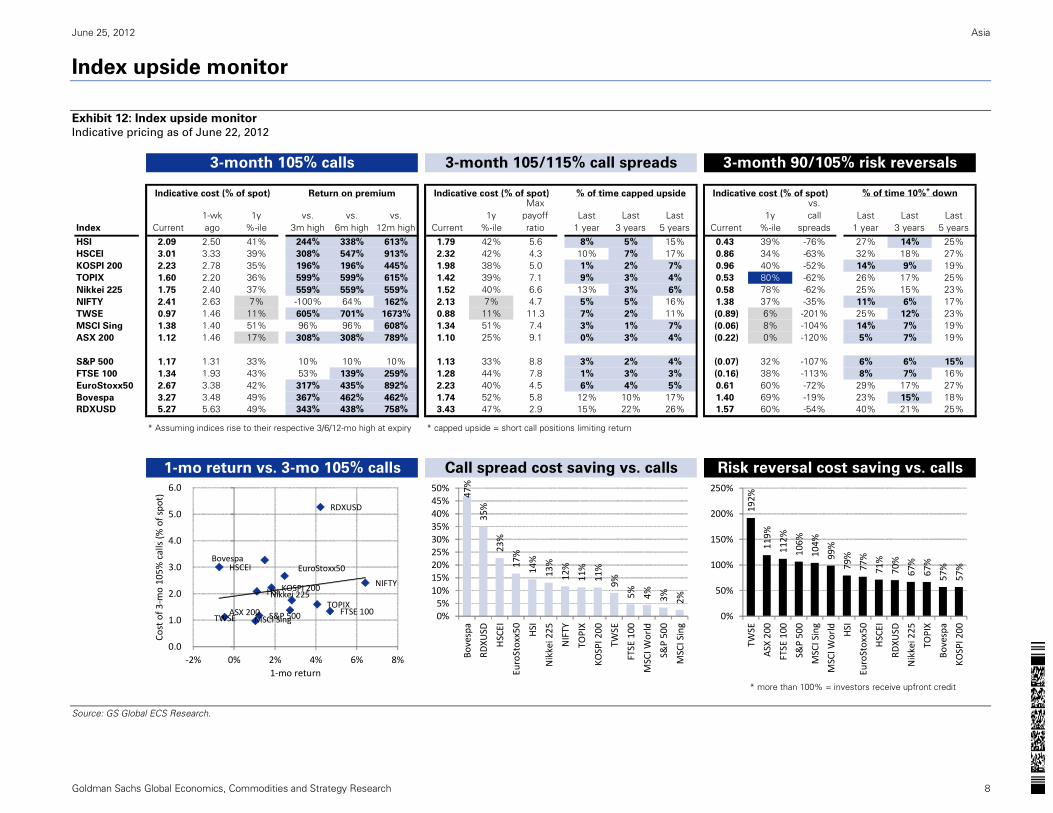

Index upside monitor

Exhibit 12: Index upside monitor

Indicative pricing as of June 22, 2012

Source: GS Global ECS Research.

3-month 105% calls 3-month 105/115% call spreads 3-month 90/105% risk reversals

Indicative cost (% of spot) Return on premium Indicative cost (% of spot) % of time capped upside Indicative cost (% of spot) % of time 10%+ down

Index Current1-wk ago

1y %-ile

vs. 3m high

vs. 6m high

vs. 12m high Current

1y %-ile

Max payoff ratio

Last 1 year

Last 3 years

Last 5 years Current

1y %-ile

vs. call

spreadsLast

1 yearLast

3 yearsLast

5 years

HSI 2.09 2.50 41% 244% 338% 613% 1.79 42% 5.6 8% 5% 15% 0.43 39% -76% 27% 14% 25%HSCEI 3.01 3.33 39% 308% 547% 913% 2.32 42% 4.3 10% 7% 17% 0.86 34% -63% 32% 18% 27%KOSPI 200 2.23 2.78 35% 196% 196% 445% 1.98 38% 5.0 1% 2% 7% 0.96 40% -52% 14% 9% 19%TOPIX 1.60 2.20 36% 599% 599% 615% 1.42 39% 7.1 9% 3% 4% 0.53 80% -62% 26% 17% 25%Nikkei 225 1.75 2.40 37% 559% 559% 559% 1.52 40% 6.6 13% 3% 6% 0.58 78% -62% 25% 15% 23%NIFTY 2.41 2.63 7% -100% 64% 162% 2.13 7% 4.7 5% 5% 16% 1.38 37% -35% 11% 6% 17%TWSE 0.97 1.46 11% 605% 701% 1673% 0.88 11% 11.3 7% 2% 11% (0.89) 6% -201% 25% 12% 23%MSCI Sing 1.38 1.40 51% 96% 96% 608% 1.34 51% 7.4 3% 1% 7% (0.06) 8% -104% 14% 7% 19%ASX 200 1.12 1.46 17% 308% 308% 789% 1.10 25% 9.1 0% 3% 4% (0.22) 0% -120% 5% 7% 19%

S&P 500 1.17 1.31 33% 10% 10% 10% 1.13 33% 8.8 3% 2% 4% (0.07) 32% -107% 6% 6% 15%

FTSE 100 1.34 1.93 43% 53% 139% 259% 1.28 44% 7.8 1% 3% 3% (0.16) 38% -113% 8% 7% 16%EuroStoxx50 2.67 3.38 42% 317% 435% 892% 2.23 40% 4.5 6% 4% 5% 0.61 60% -72% 29% 17% 27%Bovespa 3.27 3.48 49% 367% 462% 462% 1.74 52% 5.8 12% 10% 17% 1.40 69% -19% 23% 15% 18%RDXUSD 5.27 5.63 49% 343% 438% 758% 3.43 47% 2.9 15% 22% 26% 1.57 60% -54% 40% 21% 25%

* Assuming indices rise to their respective 3/6/12-mo high at expiry * capped upside = short call positions limiting return

1-mo return vs. 3-mo 105% calls Call spread cost saving vs. calls Risk reversal cost saving vs. calls

* more than 100% = investors receive upfront credit

HSI

HSCEI

KOSPI 200

TOPIXNikkei 225

NIFTY

TWSE MSCI SingASX 200 S&P 500 FTSE 100

EuroStoxx50Bovespa

RDXUSD

0.0

1.0

2.0

3.0

4.0

5.0

6.0

‐2% 0% 2% 4% 6% 8%

Cost of 3

‐mo 105%

calls (%

of spo

t)

1‐mo return

47%

35%

23%

17%

14%

13%

12%

11%

11%

9%

5% 4% 3% 2%

0%5%

10%15%20%25%30%35%40%45%50%

Bovespa

RDXU

SD

HSCEI

EuroStoxx50

HSI

Nikkei 225

NIFTY

TOPIX

KOSPI 200

TWSE

FTSE 100

MSCI W

orld

S&P 500

MSCI Sing

192%

119%

112%

106%

104%

99%

79%

77%

71%

70%

67%

67%

57%

57%

0%

50%

100%

150%

200%

250%

TWSE

ASX

200

FTSE 100

S&P 500

MSCI Sing

MSCI W

orld

HSI

EuroStoxx50

HSCEI

RDXU

SD

Nikkei 225

TOPIX

Bovespa

KOSPI 200

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 9

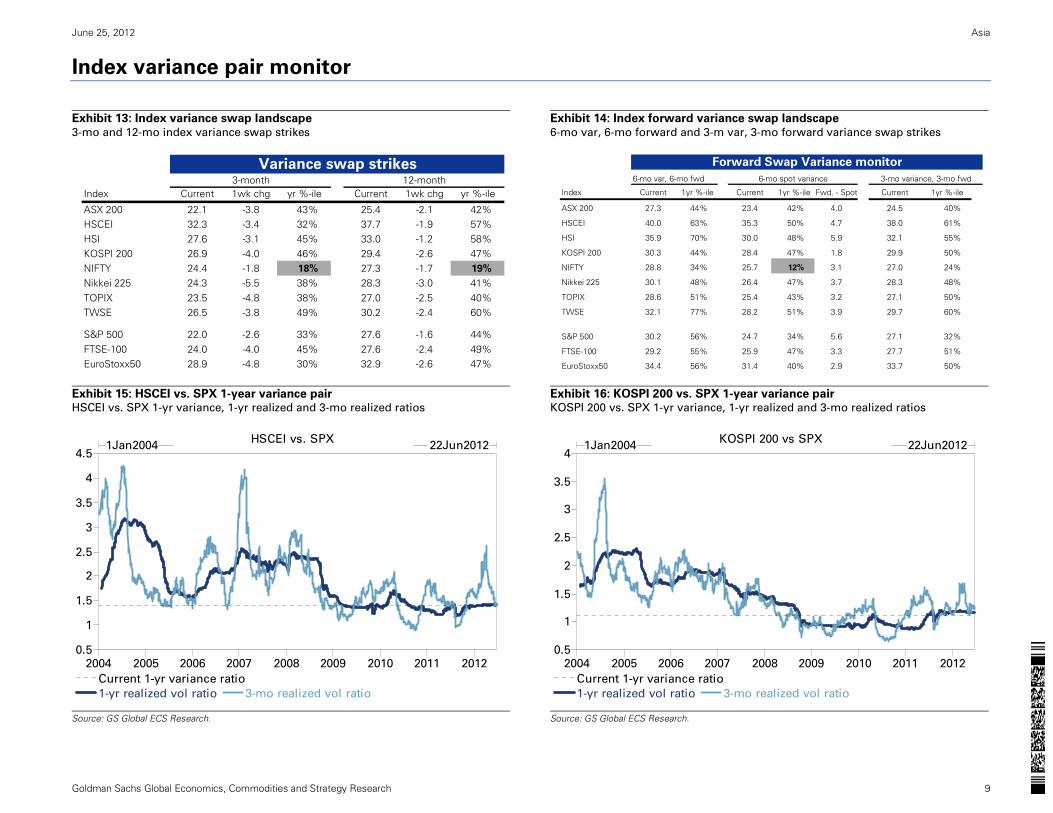

Index variance pair monitor

Exhibit 13: Index variance swap landscape

3-mo and 12-mo index variance swap strikes

Exhibit 14: Index forward variance swap landscape

6-mo var, 6-mo forward and 3-m var, 3-mo forward variance swap strikes

Exhibit 15: HSCEI vs. SPX 1-year variance pair HSCEI vs. SPX 1-yr variance, 1-yr realized and 3-mo realized ratios

Exhibit 16: KOSPI 200 vs. SPX 1-year variance pair KOSPI 200 vs. SPX 1-yr variance, 1-yr realized and 3-mo realized ratios

Source: GS Global ECS Research.

Source: GS Global ECS Research.

3-month 12-monthIndex Current 1wk chg yr %-ile Current 1wk chg yr %-ile

ASX 200 22.1 -3.8 43% 25.4 -2.1 42%HSCEI 32.3 -3.4 32% 37.7 -1.9 57%HSI 27.6 -3.1 45% 33.0 -1.2 58%KOSPI 200 26.9 -4.0 46% 29.4 -2.6 47%NIFTY 24.4 -1.8 18% 27.3 -1.7 19%

Nikkei 225 24.3 -5.5 38% 28.3 -3.0 41%TOPIX 23.5 -4.8 38% 27.0 -2.5 40%TWSE 26.5 -3.8 49% 30.2 -2.4 60%

S&P 500 22.0 -2.6 33% 27.6 -1.6 44%FTSE-100 24.0 -4.0 45% 27.6 -2.4 49%EuroStoxx50 28.9 -4.8 30% 32.9 -2.6 47%

Variance swap strikes6-mo var, 6-mo fwd 6-mo spot variance 3-mo variance, 3-mo fwd

Index Current 1yr %-ile Current 1yr %-ile Fwd. - Spot Current 1yr %-ile

ASX 200 27.3 44% 23.4 42% 4.0 24.5 40%

HSCEI 40.0 63% 35.3 50% 4.7 38.0 61%

HSI 35.9 70% 30.0 48% 5.9 32.1 55%

KOSPI 200 30.3 44% 28.4 47% 1.8 29.9 50%

NIFTY 28.8 34% 25.7 12% 3.1 27.0 24%

Nikkei 225 30.1 48% 26.4 47% 3.7 28.3 48%

TOPIX 28.6 51% 25.4 43% 3.2 27.1 50%

TWSE 32.1 77% 28.2 51% 3.9 29.7 60%

S&P 500 30.2 56% 24.7 34% 5.6 27.1 32%

FTSE-100 29.2 55% 25.9 47% 3.3 27.7 51%

EuroStoxx50 34.4 56% 31.4 40% 2.9 33.7 50%

Forward Swap Variance monitor

1-yr realized vol ratio 3-mo realized vol ratio

Current 1-yr variance ratio

HSCEI vs. SPX

0.5

1

1.5

2

2.5

3

3.5

4

4.5

2004 2005 2006 2007 2008 2009 2010 2011 2012

1Jan2004 22Jun2012

1-yr realized vol ratio 3-mo realized vol ratio

Current 1-yr variance ratio

KOSPI 200 vs SPX

0.5

1

1.5

2

2.5

3

3.5

4

2004 2005 2006 2007 2008 2009 2010 2011 2012

1Jan2004 22Jun2012

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 10

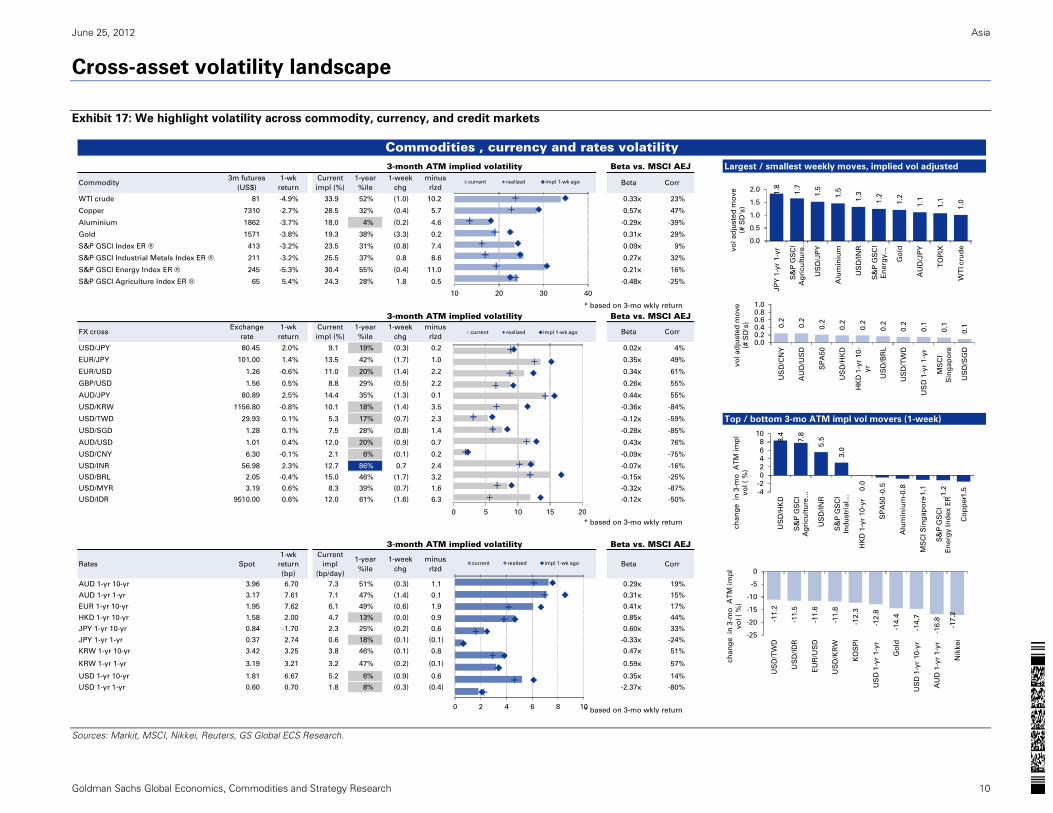

Cross-asset volatility landscape

Exhibit 17: We highlight volatility across commodity, currency, and credit markets

Sources: Markit, MSCI, Nikkei, Reuters, GS Global ECS Research.

Largest / smallest weekly moves, implied vol adjusted

Commodity3m futures

(US$)

1-wk

return

Current

impl (%)

1-year

%ile

1-week

chg

minus

rlzdBeta Corr

WTI crude 81 -4.9% 33.9 52% (1.0) 10.2 0.33x 23%

Copper 7310 -2.7% 28.5 32% (0.4) 5.7 0.57x 47%

Aluminium 1862 -3.7% 18.0 4% (0.2) 4.6 -0.29x -39%

Gold 1571 -3.8% 19.3 38% (3.3) 0.2 0.31x 29%

S&P GSCI Index ER ® 413 -3.2% 23.5 31% (0.8) 7.4 0.09x 9%

S&P GSCI Industrial Metals Index ER ® 211 -3.2% 25.5 37% 0.8 8.6 0.27x 32%

S&P GSCI Energy Index ER ® 245 -5.3% 30.4 55% (0.4) 11.0 0.21x 16%

S&P GSCI Agriculture Index ER ® 65 5.4% 24.3 28% 1.8 0.5 -0.48x -25%

* based on 3-mo wkly return

FX crossExchange

rate

1-wk

return

Current

impl (%)

1-year

%ile

1-week

chg

minus

rlzdBeta Corr

USD/JPY 80.45 2.0% 9.1 19% (0.3) 0.2 0.02x 4%

EUR/JPY 101.00 1.4% 13.5 42% (1.7) 1.0 0.35x 49%

EUR/USD 1.26 -0.6% 11.0 20% (1.4) 2.2 0.34x 61%

GBP/USD 1.56 0.5% 8.8 29% (0.5) 2.2 0.26x 55%

AUD/JPY 80.89 2.5% 14.4 35% (1.3) 0.1 0.44x 55%

USD/KRW 1156.80 -0.8% 10.1 18% (1.4) 3.5 -0.36x -84%

USD/TWD 29.93 0.1% 5.3 17% (0.7) 2.3 -0.12x -59% Top / bottom 3-mo ATM impl vol movers (1-week)

USD/SGD 1.28 0.1% 7.5 28% (0.8) 1.4 -0.28x -85%

AUD/USD 1.01 0.4% 12.0 20% (0.9) 0.7 0.43x 76%

USD/CNY 6.30 -0.1% 2.1 6% (0.1) 0.2 -0.09x -75%

USD/INR 56.98 2.3% 12.7 86% 0.7 2.4 -0.07x -16%

USD/BRL 2.05 -0.4% 15.0 46% (1.7) 3.2 -0.15x -25%

USD/MYR 3.19 0.6% 8.3 39% (0.7) 1.6 -0.32x -87%

USD/IDR 9510.00 0.6% 12.0 61% (1.6) 6.3 -0.12x -50%

* based on 3-mo wkly return

Rates Spot

1-wk

return

(bp)

Current

impl

(bp/day)

1-year

%ile

1-week

chg

minus

rlzdBeta Corr

AUD 1-yr 10-yr 3.96 6.70 7.3 51% (0.3) 1.1 0.29x 19%

AUD 1-yr 1-yr 3.17 7.61 7.1 47% (1.4) 0.1 0.31x 15%

EUR 1-yr 10-yr 1.95 7.62 6.1 49% (0.6) 1.9 0.41x 17%

HKD 1-yr 10-yr 1.58 2.00 4.7 13% (0.0) 0.9 0.85x 44%

JPY 1-yr 10-yr 0.84 -1.70 2.3 25% (0.2) 0.6 0.60x 33%

JPY 1-yr 1-yr 0.37 2.74 0.6 18% (0.1) (0.1) -0.33x -24%

KRW 1-yr 10-yr 3.42 3.25 3.8 46% (0.1) 0.8 0.47x 51%

KRW 1-yr 1-yr 3.19 3.21 3.2 47% (0.2) (0.1) 0.59x 57%

USD 1-yr 10-yr 1.81 6.67 5.2 6% (0.9) 0.6 0.35x 14%

USD 1-yr 1-yr 0.60 0.70 1.8 8% (0.3) (0.4) -2.37x -80%

* based on 3-mo wkly return

3-month ATM implied volatility Beta vs. MSCI AEJ

Commodities , currency and rates volatility3-month ATM implied volatility Beta vs. MSCI AEJ

3-month ATM implied volatility Beta vs. MSCI AEJ

0 5 10 15 20

current realized impl 1-wk ago

10 20 30 40

current realized impl 1-wk ago

0 2 4 6 8 10

current realized impl 1-wk ago

1.8

1.7

1.5

1.5

1.3

1.2

1.2

1.1

1.1

1.0

0.0

0.5

1.0

1.5

2.0

JP

Y 1

-yr

1-y

r

S&

P G

SC

I

Ag

ricu

ltu

re …

US

D/J

PY

Alu

min

ium

US

D/I

NR

S&

P G

SC

I

En

erg

y …

Go

ld

AU

D/J

PY

TO

PIX

WT

I cru

devo

l ad

juste

d m

ove

(# S

D's

)

0.2

0.2

0.2

0.2

0.2

0.2

0.2

0.1

0.1

0.1

0.00.20.40.60.81.0

US

D/C

NY

AU

D/U

SD

SP

A50

US

D/H

KD

HK

D 1

-yr

10-

yr

US

D/B

RL

US

D/T

WD

US

D 1

-yr

1-y

r

MS

CI

Sin

gap

ore

US

D/S

GD

vo

l ad

juste

d m

ove

(# S

D's

)

8.4

7.8

5.5

3.0

0.0

-0.5

-0.8

-1.1

-1.2

-1.5-4

-2

0246

810

US

D/H

KD

S&

P G

SC

I

Ag

ricu

ltu

re …

US

D/IN

R

S&

P G

SC

I

Ind

ustr

ial …

HK

D 1

-yr

10-y

r

SP

A50

Alu

min

ium

MS

CI S

ing

ap

ore

S&

P G

SC

I

En

erg

y In

dex E

R

Co

pp

er

ch

an

ge in

3-m

o A

TM

im

pl

vo

l (

%)

-11.2

-11.5

-11.6

-11.8

-12.3

-12.8

-14.4

-14.7

-16

.8

-17.2

-25

-20

-15

-10

-5

0

US

D/T

WD

US

D/I

DR

EU

R/U

SD

US

D/K

RW

KO

SP

I

US

D 1

-yr

1-y

r

Go

ld

US

D 1

-yr

10-y

r

AU

D 1

-yr

1-y

r

Nik

kei

ch

an

ge in

3-m

o A

TM

im

pl

vo

l (

%)

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 11

Asia index skew and term structure

Exhibit 18: Asia index skew and term structure

Performance, implied/realized volatility, consensus estimates, and indicative option pricing as of June 22, 2012 close

Source: GS Global ECS Research.

1-month / 3-month 3-month / 12-monthIndex Current 1wk chg yr ago yr %-ile Current 1wk chg yr ago yr %-ile

ASX 200 0.92 -0.11 0.95 28% 0.91 -0.03 0.94 37%HSCEI 0.94 -0.08 0.98 9% 0.97 -0.04 0.97 26%HSI 0.94 -0.11 0.97 23% 0.96 -0.05 0.93 35%KOSPI 200 1.00 -0.08 1.04 41% 0.99 -0.06 1.00 38%MSCI Singapore 1.03 -0.00 0.91 66% 1.00 -0.01 0.90 55%NIFTY 0.94 -0.09 0.96 16% 0.90 -0.02 0.88 24%Nikkei 225 0.94 -0.13 0.99 25% 0.94 -0.10 0.98 29%TOPIX 0.94 -0.13 0.99 22% 0.93 -0.10 0.98 24%TWSE 0.95 -0.06 0.94 28% 0.91 -0.08 0.91 36%

S&P 500 0.88 -0.07 0.94 21% 0.83 -0.04 0.88 9%

FTSE-100 0.90 -0.15 0.94 19% 0.91 -0.08 0.88 31%EuroStoxx50 0.92 -0.15 1.01 16% 0.98 -0.07 0.95 26%MSCI World 0.88 -0.07 0.95 19% 0.83 -0.04 0.90 7%

3-month 12-monthIndex Current 1wk chg yr ago yr %-ile Current 1wk chg yr ago yr %-ile

ASX 200 1.42 +0.03 1.34 92% 1.46 +0.01 1.35 100%

HSCEI 1.23 -0.04 1.14 53% 1.27 -0.02 1.16 50%HSI 1.26 -0.03 1.15 52% 1.32 +0.01 1.19 59%KOSPI 200 1.30 -0.02 1.22 58% 1.24 -0.02 1.23 36%MSCI Singapore 1.36 -0.00 1.20 90% 1.35 +0.00 1.21 90%

NIFTY 1.25 -0.03 1.26 35% 1.30 +0.00 1.32 75%Nikkei 225 1.22 -0.09 1.24 35% 1.26 -0.04 1.29 31%TOPIX 1.22 -0.09 1.22 37% 1.27 -0.04 1.27 40%TWSE 1.28 -0.03 1.14 74% 1.31 -0.01 1.14 96%

S&P 500 1.48 -0.13 1.43 43% 1.65 -0.04 1.50 89%

FTSE-100 1.46 -0.02 1.42 55% 1.57 -0.01 1.52 78%EuroStoxx50 1.29 -0.04 1.40 0% 1.40 -0.01 1.47 2%

MSCI World 1.48 -0.12 1.43 43% 1.64 -0.04 1.50 89%

Term structure history

3-mo skew historySkew ( 25-delta put / 25-delta call implied vol )

Ratio of ATM implied vol ATM impl vol across terms

Skew term structure

1.0

1.1

1.2

1.3

1.4

1.5

Jun-11 Sep-11 Dec-11 Mar-12

HSI

Nikkei

KOSPI

1.10

1.15

1.20

1.25

1.30

1.35

1M 3M 6M 12M

Rat

io o

f 3m

25-

delta

put

/3m

25-

delta

ca

ll

HSI Nikkei KOSPI

21

22

2223 23

24

18

19

2020 20

21

2020 20 20

2021

17

18

19

20

21

22

23

24

ATM

impl

ied

vol (

%)

HSI Nikkei KOSPI0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

Jun-11 Sep-11 Dec-11 Mar-12

HSI

Nikkei 225

KOSPI 200

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 12

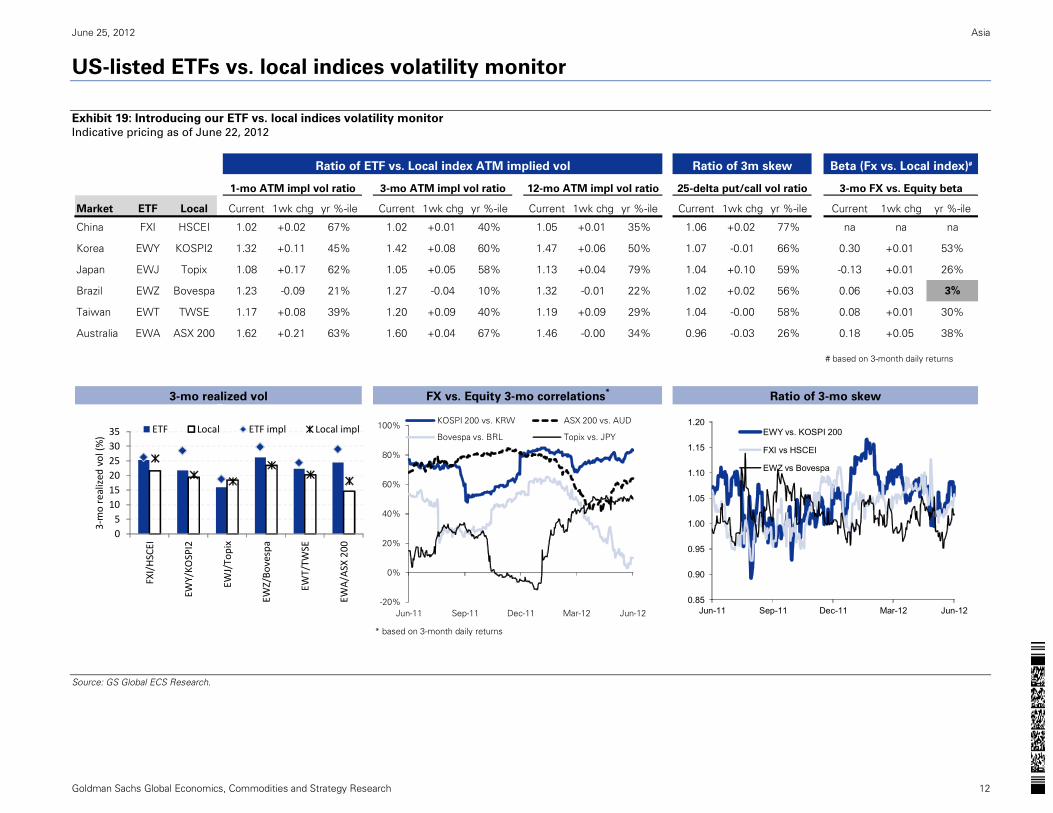

US-listed ETFs vs. local indices volatility monitor

Exhibit 19: Introducing our ETF vs. local indices volatility monitor

Indicative pricing as of June 22, 2012

Source: GS Global ECS Research.

Market ETF Local Current 1wk chg yr %-ile Current 1wk chg yr %-ile Current 1wk chg yr %-ile Current 1wk chg yr %-ile Current 1wk chg yr %-ile

China FXI HSCEI 1.02 +0.02 67% 1.02 +0.01 40% 1.05 +0.01 35% 1.06 +0.02 77% na na na

Korea EWY KOSPI2 1.32 +0.11 45% 1.42 +0.08 60% 1.47 +0.06 50% 1.07 -0.01 66% 0.30 +0.01 53%

Japan EWJ Topix 1.08 +0.17 62% 1.05 +0.05 58% 1.13 +0.04 79% 1.04 +0.10 59% -0.13 +0.01 26%

Brazil EWZ Bovespa 1.23 -0.09 21% 1.27 -0.04 10% 1.32 -0.01 22% 1.02 +0.02 56% 0.06 +0.03 3%

Taiwan EWT TWSE 1.17 +0.08 39% 1.20 +0.09 40% 1.19 +0.09 29% 1.04 -0.00 58% 0.08 +0.01 30%

Australia EWA ASX 200 1.62 +0.21 63% 1.60 +0.04 67% 1.46 -0.00 34% 0.96 -0.03 26% 0.18 +0.05 38%

# based on 3-month daily returns

* based on 3-month daily returns

Beta (Fx vs. Local index)#

3-mo FX vs. Equity beta

FX vs. Equity 3-mo correlations*

Ratio of 3-mo skew

Ratio of 3m skew

3-mo ATM impl vol ratio 12-mo ATM impl vol ratio

Ratio of ETF vs. Local index ATM implied vol

3-mo realized vol

25-delta put/call vol ratio1-mo ATM impl vol ratio

05

101520253035

FXI/HSCEI

EWY/KO

SPI2

EWJ/Topix

EWZ/Bo

vespa

EWT/TW

SE

EWA/ASX

200

3‐mo realized

vol (%

)

ETF Local ETF impl Local impl

-20%

0%

20%

40%

60%

80%

100%

Jun-11 Sep-11 Dec-11 Mar-12 Jun-12

KOSPI 200 vs. KRW ASX 200 vs. AUD

Bovespa vs. BRL Topix vs. JPY

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

Jun-11 Sep-11 Dec-11 Mar-12 Jun-12

EWY vs. KOSPI 200

FXI vs HSCEI

EWZ vs Bovespa

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 13

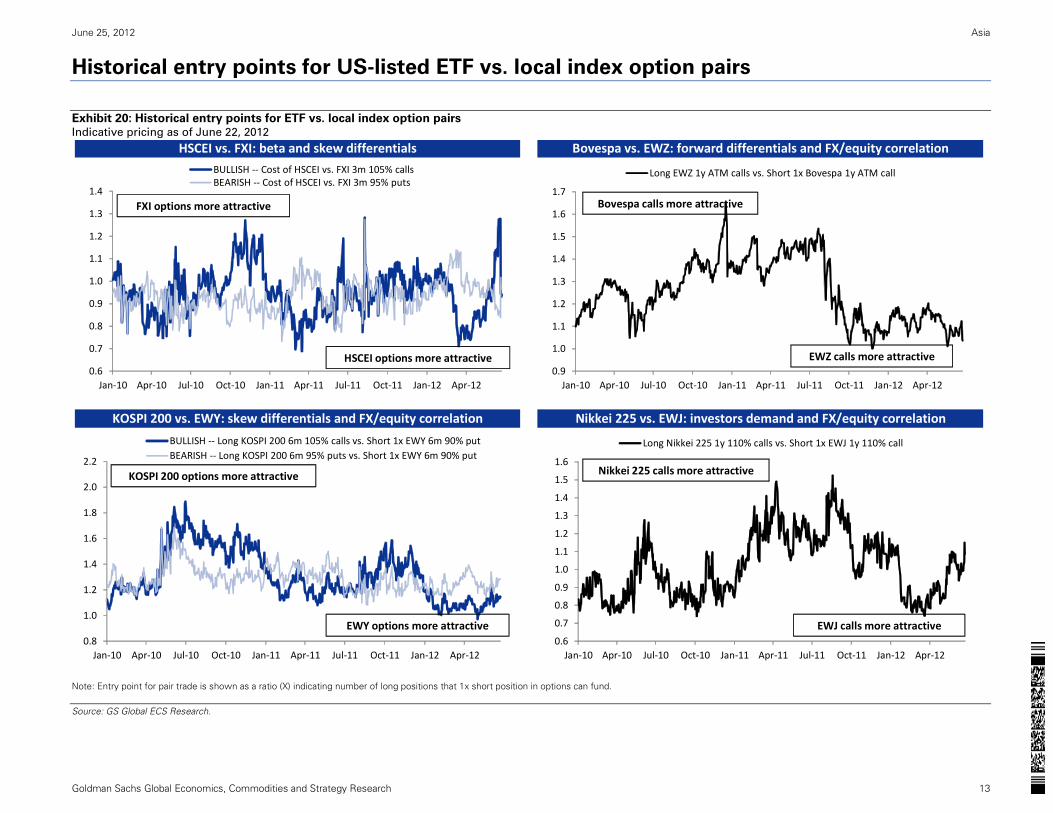

Historical entry points for US-listed ETF vs. local index option pairs

Exhibit 20: Historical entry points for ETF vs. local index option pairs Indicative pricing as of June 22, 2012

Note: Entry point for pair trade is shown as a ratio (X) indicating number of long positions that 1x short position in options can fund.

Source: GS Global ECS Research.

HSCEI vs. FXI: beta and skew differentials Bovespa vs. EWZ: forward differentials and FX/equity correlation

Nikkei 225 vs. EWJ: investors demand and FX/equity correlationKOSPI 200 vs. EWY: skew differentials and FX/equity correlation

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

Jan‐10 Apr‐10 Jul‐10 Oct‐10 Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12

BULLISH ‐‐ Cost of HSCEI vs. FXI 3m 105% callsBEARISH ‐‐ Cost of HSCEI vs. FXI 3m 95% puts

FXI options more attractive

HSCEI options more attractive0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

Jan‐10 Apr‐10 Jul‐10 Oct‐10 Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12

Long EWZ 1y ATM calls vs. Short 1x Bovespa 1y ATM call

Bovespa calls more attractive

EWZ calls more attractive

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Jan‐10 Apr‐10 Jul‐10 Oct‐10 Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12

BULLISH ‐‐ Long KOSPI 200 6m 105% calls vs. Short 1x EWY 6m 90% putBEARISH ‐‐ Long KOSPI 200 6m 95% puts vs. Short 1x EWY 6m 90% put

KOSPI 200 options more attractive

EWY options more attractive0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

Jan‐10 Apr‐10 Jul‐10 Oct‐10 Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12

Long Nikkei 225 1y 110% calls vs. Short 1x EWJ 1y 110% call

Nikkei 225 calls more attractive

EWJ calls more attractive

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 14

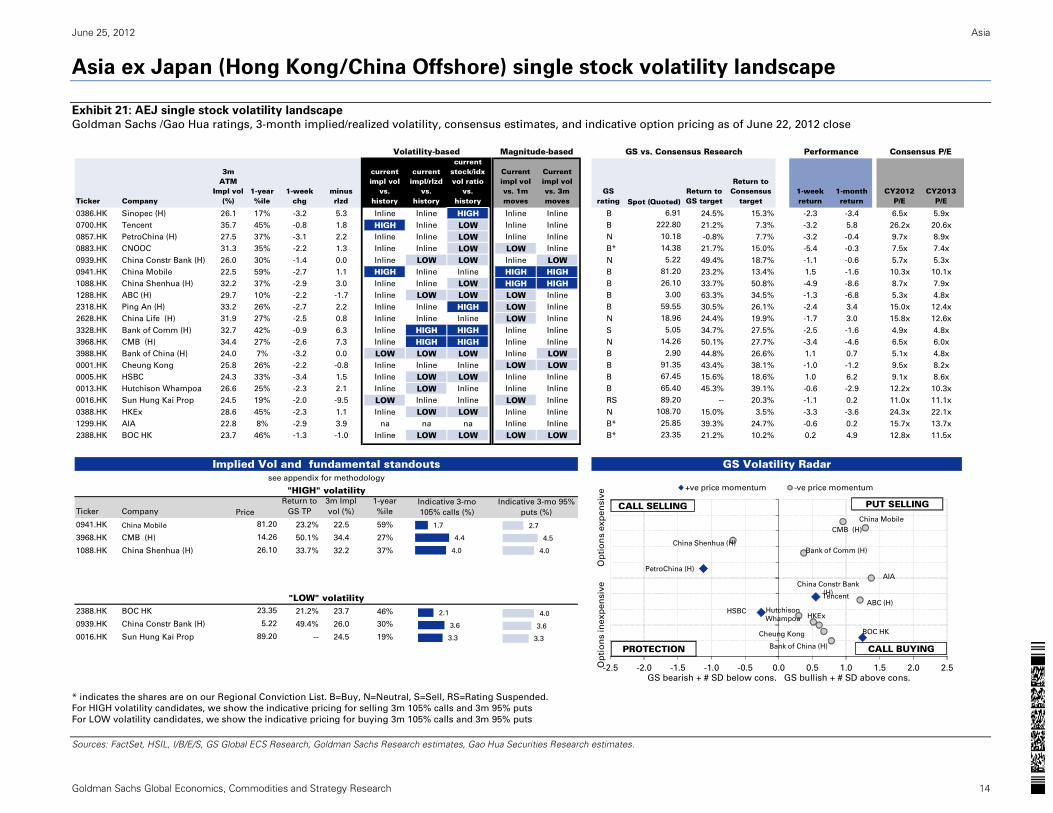

Asia ex Japan (Hong Kong/China Offshore) single stock volatility landscape

Exhibit 21: AEJ single stock volatility landscape

Goldman Sachs /Gao Hua ratings, 3-month implied/realized volatility, consensus estimates, and indicative option pricing as of June 22, 2012 close

* indicates the shares are on our Regional Conviction List. B=Buy, N=Neutral, S=Sell, RS=Rating Suspended.

For HIGH volatility candidates, we show the indicative pricing for selling 3m 105% calls and 3m 95% puts

For LOW volatility candidates, we show the indicative pricing for buying 3m 105% calls and 3m 95% puts

Sources: FactSet, HSIL, I/B/E/S, GS Global ECS Research, Goldman Sachs Research estimates, Gao Hua Securities Research estimates.

Ticker Company

3m ATM

Impl vol (%)

1-year %ile

1-week chg

minus rlzd

current impl vol

vs. history

current impl/rlzd

vs. history

current stock/idx vol ratio

vs. history

Current impl vol vs. 1m moves

Current impl vol vs. 3m moves

GS rating

Return to GS target

Return to Consensus

target1-week return

1-month return

CY2012 P/E

CY2013 P/E

0386.HK Sinopec (H) 26.1 17% -3.2 5.3 Inline Inline HIGH Inline Inline B 24.5% 15.3% -2.3 -3.4 6.5x 5.9x

0700.HK Tencent 35.7 45% -0.8 1.8 HIGH Inline LOW Inline Inline B 21.2% 7.3% -3.2 5.8 26.2x 20.6x

0857.HK PetroChina (H) 27.5 37% -3.1 2.2 Inline Inline LOW Inline Inline N -0.8% 7.7% -3.2 -0.4 9.7x 8.9x

0883.HK CNOOC 31.3 35% -2.2 1.3 Inline Inline LOW LOW Inline B* 21.7% 15.0% -5.4 -0.3 7.5x 7.4x

0939.HK China Constr Bank (H) 26.0 30% -1.4 0.0 Inline LOW LOW Inline LOW N 49.4% 18.7% -1.1 -0.6 5.7x 5.3x

0941.HK China Mobile 22.5 59% -2.7 1.1 HIGH Inline Inline HIGH HIGH B 23.2% 13.4% 1.5 -1.6 10.3x 10.1x

1088.HK China Shenhua (H) 32.2 37% -2.9 3.0 Inline Inline LOW HIGH HIGH B 33.7% 50.8% -4.9 -8.6 8.7x 7.9x

1288.HK ABC (H) 29.7 10% -2.2 -1.7 Inline LOW LOW LOW Inline B 63.3% 34.5% -1.3 -6.8 5.3x 4.8x

2318.HK Ping An (H) 33.2 26% -2.7 2.2 Inline Inline HIGH LOW Inline B 30.5% 26.1% -2.4 3.4 15.0x 12.4x

2628.HK China Life (H) 31.9 27% -2.5 0.8 Inline Inline Inline LOW Inline N 24.4% 19.9% -1.7 3.0 15.8x 12.6x

3328.HK Bank of Comm (H) 32.7 42% -0.9 6.3 Inline HIGH HIGH Inline Inline S 34.7% 27.5% -2.5 -1.6 4.9x 4.8x

3968.HK CMB (H) 34.4 27% -2.6 7.3 Inline HIGH HIGH Inline Inline N 50.1% 27.7% -3.4 -4.6 6.5x 6.0x

3988.HK Bank of China (H) 24.0 7% -3.2 0.0 LOW LOW LOW Inline LOW B 44.8% 26.6% 1.1 0.7 5.1x 4.8x

0001.HK Cheung Kong 25.8 26% -2.2 -0.8 Inline Inline Inline LOW LOW B 43.4% 38.1% -1.0 -1.2 9.5x 8.2x

0005.HK HSBC 24.3 33% -3.4 1.5 Inline LOW LOW Inline Inline B 15.6% 18.6% 1.0 6.2 9.1x 8.6x

0013.HK Hutchison Whampoa 26.6 25% -2.3 2.1 Inline LOW Inline Inline Inline B 45.3% 39.1% -0.6 -2.9 12.2x 10.3x

0016.HK Sun Hung Kai Prop 24.5 19% -2.0 -9.5 LOW Inline Inline LOW Inline RS -- 20.3% -1.1 0.2 11.0x 11.1x

0388.HK HKEx 28.6 45% -2.3 1.1 Inline LOW LOW Inline Inline N 15.0% 3.5% -3.3 -3.6 24.3x 22.1x

1299.HK AIA 22.8 8% -2.9 3.9 na na na Inline Inline B* 39.3% 24.7% -0.6 0.2 15.7x 13.7x

2388.HK BOC HK 23.7 46% -1.3 -1.0 Inline LOW LOW LOW LOW B* 21.2% 10.2% 0.2 4.9 12.8x 11.5x

Implied Vol and fundamental standouts GS Volatility Radar

Ticker Company

Return to

GS TP

3m Impl

vol (%)

1-year

%ile

0941.HK China Mobile 23.2% 22.5 59%

3968.HK CMB (H) 50.1% 34.4 27%

1088.HK China Shenhua (H) 33.7% 32.2 37%

2388.HK BOC HK 21.2% 23.7 46%

0939.HK China Constr Bank (H) 49.4% 26.0 30%

0016.HK Sun Hung Kai Prop -- 24.5 19%

Volatility-based Magnitude-based

25.85

23.35

PerformanceGS vs. Consensus Research

108.70

Spot (Quoted)

222.80

10.18

Consensus P/E

91.35

67.45

65.40

89.20

59.55

18.96

5.05

14.26

2.90

14.38

5.22

81.20

26.10

3.00

6.91

see appendix for methodology

26.10

14.26

81.20

Price

Indicative 3-mo

105% calls (%)

"HIGH" volatilityIndicative 3-mo 95%

puts (%)

"LOW" volatility

89.20

5.22

23.35

1.7

4.4

4.0

2.1

3.6

3.3

2.7

4.5

4.0

4.0

3.6

3.3

Tencent

PetroChina (H)

HSBC

BOC HK

China Constr Bank

(H)

China Mobile

China Shenhua (H)

ABC (H)

Bank of Comm (H)

CMB (H)

Bank of China (H)

Cheung Kong

Hutchison

Whampoa HKEx

AIA

-2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5GS bearish + # SD below cons. GS bullish + # SD above cons.

+ve price momentum -ve price momentum

CALL SELLING

CALL BUYING

PUT SELLING

PROTECTION

Op

tio

ns in

ex

pe

nsiv

e

Op

tio

ns e

xp

en

siv

e

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 15

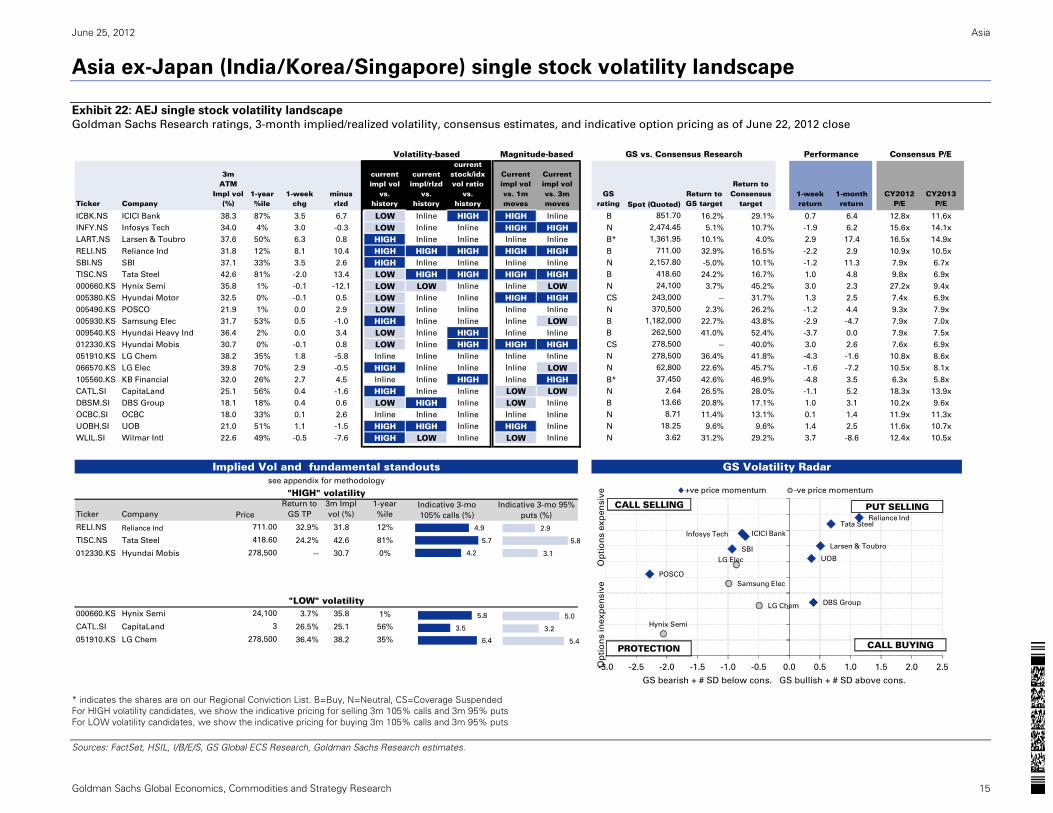

Asia ex-Japan (India/Korea/Singapore) single stock volatility landscape

Exhibit 22: AEJ single stock volatility landscape

Goldman Sachs Research ratings, 3-month implied/realized volatility, consensus estimates, and indicative option pricing as of June 22, 2012 close

* indicates the shares are on our Regional Conviction List. B=Buy, N=Neutral, CS=Coverage Suspended For HIGH volatility candidates, we show the indicative pricing for selling 3m 105% calls and 3m 95% puts For LOW volatility candidates, we show the indicative pricing for buying 3m 105% calls and 3m 95% puts

Sources: FactSet, HSIL, I/B/E/S, GS Global ECS Research, Goldman Sachs Research estimates.

Ticker Company

3m ATM

Impl vol (%)

1-year %ile

1-week chg

minus rlzd

current impl vol

vs. history

current impl/rlzd

vs. history

current stock/idx vol ratio

vs. history

Current impl vol vs. 1m moves

Current impl vol vs. 3m moves

GS rating

Return to GS target

Return to Consensus

target1-week return

1-month return

CY2012 P/E

CY2013 P/E

ICBK.NS ICICI Bank 38.3 87% 3.5 6.7 LOW Inline HIGH HIGH Inline B 16.2% 29.1% 0.7 6.4 12.8x 11.6x

INFY.NS Infosys Tech 34.0 4% 3.0 -0.3 LOW Inline Inline HIGH HIGH N 5.1% 10.7% -1.9 6.2 15.6x 14.1x

LART.NS Larsen & Toubro 37.6 50% 6.3 0.8 HIGH Inline Inline Inline Inline B* 10.1% 4.0% 2.9 17.4 16.5x 14.9x

RELI.NS Reliance Ind 31.8 12% 8.1 10.4 HIGH HIGH HIGH HIGH HIGH B 32.9% 16.5% -2.2 2.9 10.9x 10.5x

SBI.NS SBI 37.1 33% 3.5 2.6 HIGH Inline Inline Inline Inline N -5.0% 10.1% -1.2 11.3 7.9x 6.7x

TISC.NS Tata Steel 42.6 81% -2.0 13.4 LOW HIGH HIGH HIGH HIGH B 24.2% 16.7% 1.0 4.8 9.8x 6.9x

000660.KS Hynix Semi 35.8 1% -0.1 -12.1 LOW LOW Inline Inline LOW N 3.7% 45.2% 3.0 2.3 27.2x 9.4x

005380.KS Hyundai Motor 32.5 0% -0.1 0.5 LOW Inline Inline HIGH HIGH CS -- 31.7% 1.3 2.5 7.4x 6.9x

005490.KS POSCO 21.9 1% 0.0 2.9 LOW Inline Inline Inline Inline N 2.3% 26.2% -1.2 4.4 9.3x 7.9x

005930.KS Samsung Elec 31.7 53% 0.5 -1.0 HIGH Inline Inline Inline LOW B 22.7% 43.8% -2.9 -4.7 7.9x 7.0x

009540.KS Hyundai Heavy Ind 36.4 2% 0.0 3.4 LOW Inline HIGH Inline Inline B 41.0% 52.4% -3.7 0.0 7.9x 7.5x

012330.KS Hyundai Mobis 30.7 0% -0.1 0.8 LOW Inline HIGH HIGH HIGH CS -- 40.0% 3.0 2.6 7.6x 6.9x

051910.KS LG Chem 38.2 35% 1.8 -5.8 Inline Inline Inline Inline Inline N 36.4% 41.8% -4.3 -1.6 10.8x 8.6x

066570.KS LG Elec 39.8 70% 2.9 -0.5 HIGH Inline Inline Inline LOW N 22.6% 45.7% -1.6 -7.2 10.5x 8.1x

105560.KS KB Financial 32.0 26% 2.7 4.5 Inline Inline HIGH Inline HIGH B* 42.6% 46.9% -4.8 3.5 6.3x 5.8x

CATL.SI CapitaLand 25.1 56% 0.4 -1.6 HIGH Inline Inline LOW LOW N 26.5% 28.0% -1.1 5.2 18.3x 13.9x

DBSM.SI DBS Group 18.1 18% 0.4 0.6 LOW HIGH Inline LOW Inline B 20.8% 17.1% 1.0 3.1 10.2x 9.6x

OCBC.SI OCBC 18.0 33% 0.1 2.6 Inline Inline Inline Inline Inline N 11.4% 13.1% 0.1 1.4 11.9x 11.3x

UOBH.SI UOB 21.0 51% 1.1 -1.5 HIGH HIGH Inline HIGH Inline N 9.6% 9.6% 1.4 2.5 11.6x 10.7x

WLIL.SI Wilmar Intl 22.6 49% -0.5 -7.6 HIGH LOW Inline LOW Inline N 31.2% 29.2% 3.7 -8.6 12.4x 10.5x

Implied Vol and fundamental standouts GS Volatility Radar

Ticker Company

Return to

GS TP

3m Impl

vol (%)

1-year

%ile

RELI.NS Reliance Ind 32.9% 31.8 12%

TISC.NS Tata Steel 24.2% 42.6 81%

012330.KS Hyundai Mobis -- 30.7 0%

000660.KS Hynix Semi 3.7% 35.8 1%

CATL.SI CapitaLand 26.5% 25.1 56%

051910.KS LG Chem 36.4% 38.2 35%

711.00

418.60

278,500

"LOW" volatility24,100

3

278,500

18.25

3.62

see appendix for methodology

"HIGH" volatility

Price

Indicative 3-mo

105% calls (%)

Indicative 3-mo 95%

puts (%)

8.71

24,100

243,000

370,500

1,182,000

262,500

278,500

278,500

62,800

37,450

2.64

13.66

Consensus P/E

Spot (Quoted)

418.60

Volatility-based Magnitude-based GS vs. Consensus Research Performance

851.70

2,474.45

1,361.95

711.00

2,157.80

4.9

5.7

4.2

5.8

3.5

6.4

2.9

5.8

3.1

5.0

3.2

5.4

ICICI BankInfosys Tech

Larsen & Toubro

Reliance Ind

SBI

Tata Steel

POSCO

DBS Group

UOB

Hynix Semi

Samsung Elec

LG Chem

LG Elec

-3.0 -2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

GS bearish + # SD below cons. GS bullish + # SD above cons.

+ve price momentum -ve price momentum

CALL SELLING

CALL BUYING

PUT SELLING

PROTECTION

Op

tio

ns in

ex

pe

nsiv

e

Op

tio

ns e

xp

en

siv

e

June 25, 2012 Asia

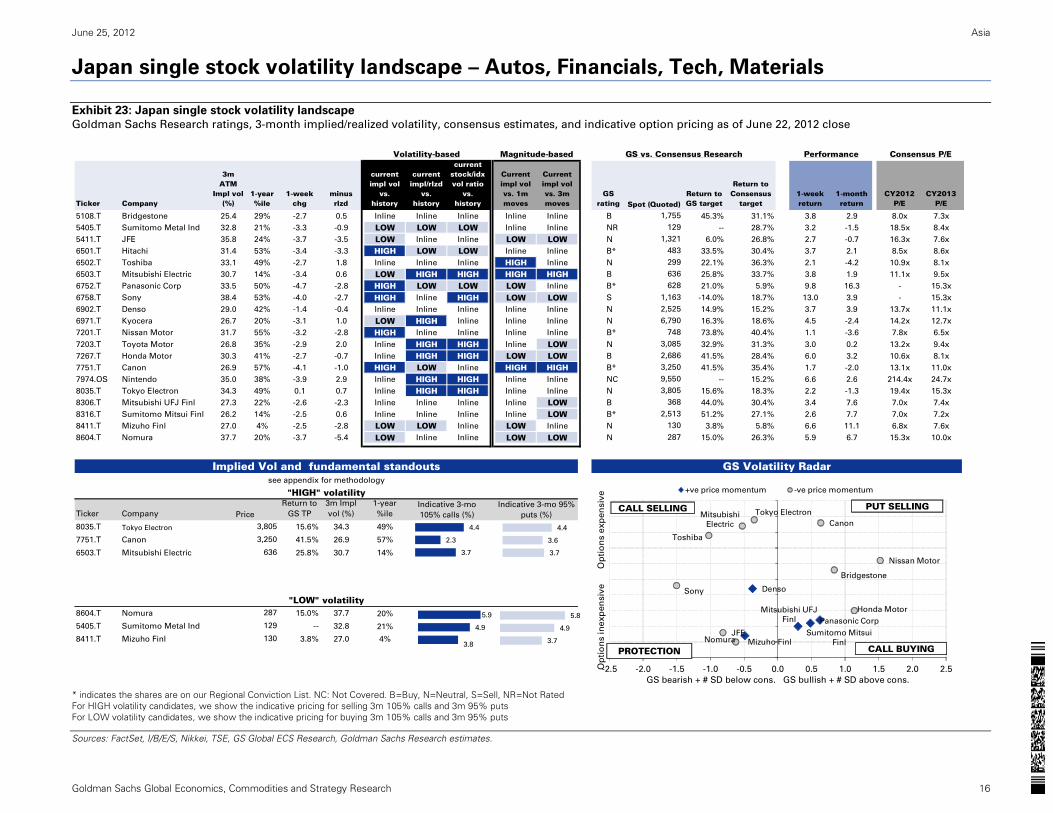

Goldman Sachs Global Economics, Commodities and Strategy Research 16

Japan single stock volatility landscape – Autos, Financials, Tech, Materials

Exhibit 23: Japan single stock volatility landscape

Goldman Sachs Research ratings, 3-month implied/realized volatility, consensus estimates, and indicative option pricing as of June 22, 2012 close

* indicates the shares are on our Regional Conviction List. NC: Not Covered. B=Buy, N=Neutral, S=Sell, NR=Not Rated For HIGH volatility candidates, we show the indicative pricing for selling 3m 105% calls and 3m 95% puts For LOW volatility candidates, we show the indicative pricing for buying 3m 105% calls and 3m 95% puts

Sources: FactSet, I/B/E/S, Nikkei, TSE, GS Global ECS Research, Goldman Sachs Research estimates.

Ticker Company

3m ATM

Impl vol (%)

1-year %ile

1-week chg

minus rlzd

current impl vol

vs. history

current impl/rlzd

vs. history

current stock/idx vol ratio

vs. history

Current impl vol vs. 1m moves

Current impl vol vs. 3m moves

GS rating

Return to GS target

Return to Consensus

target1-week return

1-month return

CY2012 P/E

CY2013 P/E

5108.T Bridgestone 25.4 29% -2.7 0.5 Inline Inline Inline Inline Inline B 45.3% 31.1% 3.8 2.9 8.0x 7.3x

5405.T Sumitomo Metal Ind 32.8 21% -3.3 -0.9 LOW LOW LOW Inline Inline NR -- 28.7% 3.2 -1.5 18.5x 8.4x

5411.T JFE 35.8 24% -3.7 -3.5 LOW Inline Inline LOW LOW N 6.0% 26.8% 2.7 -0.7 16.3x 7.6x

6501.T Hitachi 31.4 53% -3.4 -3.3 HIGH LOW LOW Inline Inline B* 33.5% 30.4% 3.7 2.1 8.5x 8.6x

6502.T Toshiba 33.1 49% -2.7 1.8 Inline Inline Inline HIGH Inline N 22.1% 36.3% 2.1 -4.2 10.9x 8.1x

6503.T Mitsubishi Electric 30.7 14% -3.4 0.6 LOW HIGH HIGH HIGH HIGH B 25.8% 33.7% 3.8 1.9 11.1x 9.5x

6752.T Panasonic Corp 33.5 50% -4.7 -2.8 HIGH LOW LOW LOW Inline B* 21.0% 5.9% 9.8 16.3 - 15.3x

6758.T Sony 38.4 53% -4.0 -2.7 HIGH Inline HIGH LOW LOW S -14.0% 18.7% 13.0 3.9 - 15.3x

6902.T Denso 29.0 42% -1.4 -0.4 Inline Inline Inline Inline Inline N 14.9% 15.2% 3.7 3.9 13.7x 11.1x

6971.T Kyocera 26.7 20% -3.1 1.0 LOW HIGH Inline Inline Inline N 16.3% 18.6% 4.5 -2.4 14.2x 12.7x

7201.T Nissan Motor 31.7 55% -3.2 -2.8 HIGH Inline Inline Inline Inline B* 73.8% 40.4% 1.1 -3.6 7.8x 6.5x

7203.T Toyota Motor 26.8 35% -2.9 2.0 Inline HIGH HIGH Inline LOW N 32.9% 31.3% 3.0 0.2 13.2x 9.4x

7267.T Honda Motor 30.3 41% -2.7 -0.7 Inline HIGH HIGH LOW LOW B 41.5% 28.4% 6.0 3.2 10.6x 8.1x

7751.T Canon 26.9 57% -4.1 -1.0 HIGH LOW Inline HIGH HIGH B* 41.5% 35.4% 1.7 -2.0 13.1x 11.0x

7974.OS Nintendo 35.0 38% -3.9 2.9 Inline HIGH HIGH Inline Inline NC -- 15.2% 6.6 2.6 214.4x 24.7x

8035.T Tokyo Electron 34.3 49% 0.1 0.7 Inline HIGH HIGH Inline Inline N 15.6% 18.3% 2.2 -1.3 19.4x 15.3x

8306.T Mitsubishi UFJ Finl 27.3 22% -2.6 -2.3 Inline Inline Inline Inline LOW B 44.0% 30.4% 3.4 7.6 7.0x 7.4x

8316.T Sumitomo Mitsui Finl 26.2 14% -2.5 0.6 Inline Inline Inline Inline LOW B* 51.2% 27.1% 2.6 7.7 7.0x 7.2x

8411.T Mizuho Finl 27.0 4% -2.5 -2.8 LOW LOW Inline LOW Inline N 3.8% 5.8% 6.6 11.1 6.8x 7.6x

8604.T Nomura 37.7 20% -3.7 -5.4 LOW Inline Inline LOW LOW N 15.0% 26.3% 5.9 6.7 15.3x 10.0x

Implied Vol and fundamental standouts GS Volatility Radar

Ticker Company

Return to

GS TP

3m Impl

vol (%)

1-year

%ile

8035.T Tokyo Electron 15.6% 34.3 49%

7751.T Canon 41.5% 26.9 57%

6503.T Mitsubishi Electric 25.8% 30.7 14%

8604.T Nomura 15.0% 37.7 20%

5405.T Sumitomo Metal Ind -- 32.8 21%

8411.T Mizuho Finl 3.8% 27.0 4%

Indicative 3-mo

105% calls (%)

"HIGH" volatilityIndicative 3-mo 95%

puts (%)

"LOW" volatility

130

129

287

see appendix for methodology

636

3,250

3,805

Price

Consensus P/E

3,250

9,550

3,805

368

2,525

6,790

748

3,085

2,686

483

299

636

628

1,163

1,755

Volatility-based Magnitude-based

130

287

PerformanceGS vs. Consensus Research

2,513

Spot (Quoted)

129

1,321

4.4

2.3

3.7

5.9

4.9

3.8

4.4

3.6

3.7

5.8

4.9

3.7

Panasonic Corp

Denso

Mitsubishi UFJ

Finl

Sumitomo Mitsui

FinlMizuho Finl

Bridgestone

JFE

Toshiba

Mitsubishi

Electric

Sony

Nissan Motor

Honda Motor

Canon

Tokyo Electron

Nomura

-2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

GS bearish + # SD below cons. GS bullish + # SD above cons.

+ve price momentum -ve price momentum

CALL SELLING

CALL BUYING

PUT SELLING

PROTECTION

Op

tio

ns in

exp

en

siv

e

Op

tio

ns e

xp

en

siv

e

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 17

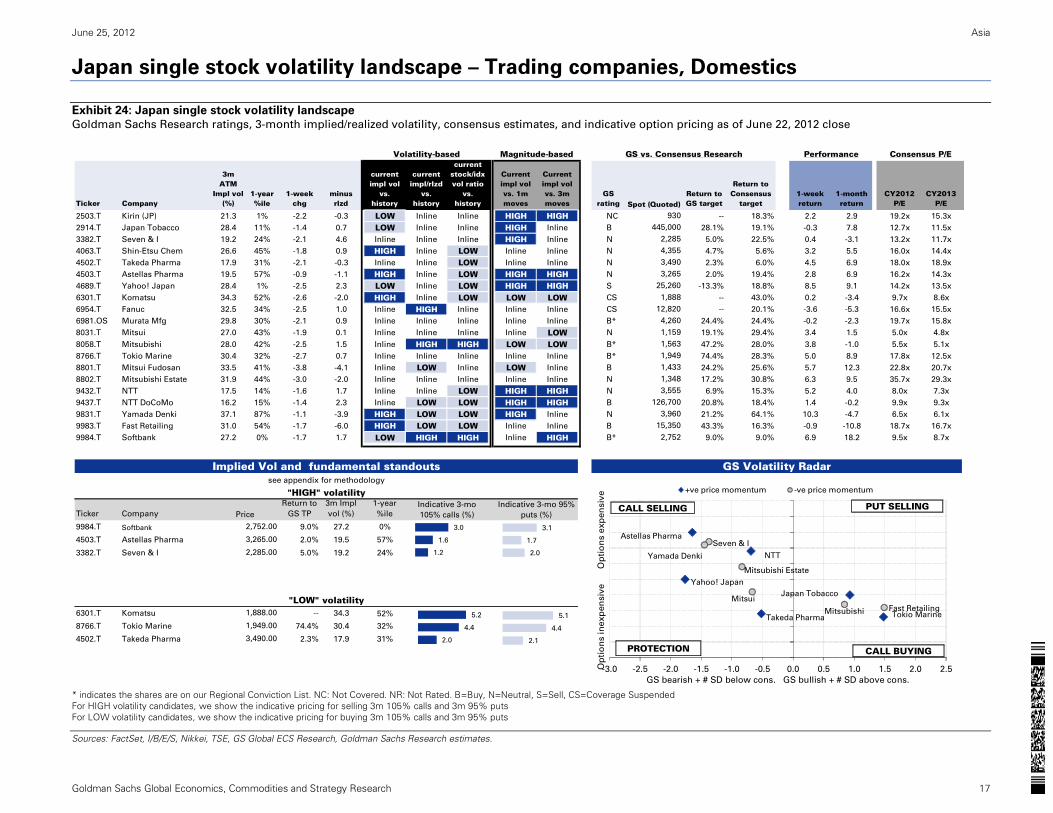

Japan single stock volatility landscape – Trading companies, Domestics

Exhibit 24: Japan single stock volatility landscape

Goldman Sachs Research ratings, 3-month implied/realized volatility, consensus estimates, and indicative option pricing as of June 22, 2012 close

* indicates the shares are on our Regional Conviction List. NC: Not Covered. NR: Not Rated. B=Buy, N=Neutral, S=Sell, CS=Coverage Suspended For HIGH volatility candidates, we show the indicative pricing for selling 3m 105% calls and 3m 95% puts For LOW volatility candidates, we show the indicative pricing for buying 3m 105% calls and 3m 95% puts

Sources: FactSet, I/B/E/S, Nikkei, TSE, GS Global ECS Research, Goldman Sachs Research estimates.

Ticker Company

3m ATM

Impl vol (%)

1-year %ile

1-week chg

minus rlzd

current impl vol

vs. history

current impl/rlzd

vs. history

current stock/idx vol ratio

vs. history

Current impl vol vs. 1m moves

Current impl vol vs. 3m moves

GS rating

Return to GS target

Return to Consensus

target1-week return

1-month return

CY2012 P/E

CY2013 P/E

2503.T Kirin (JP) 21.3 1% -2.2 -0.3 LOW Inline Inline HIGH HIGH NC -- 18.3% 2.2 2.9 19.2x 15.3x

2914.T Japan Tobacco 28.4 11% -1.4 0.7 LOW Inline Inline HIGH Inline B 28.1% 19.1% -0.3 7.8 12.7x 11.5x

3382.T Seven & I 19.2 24% -2.1 4.6 Inline Inline Inline HIGH Inline N 5.0% 22.5% 0.4 -3.1 13.2x 11.7x

4063.T Shin-Etsu Chem 26.6 45% -1.8 0.9 HIGH Inline LOW Inline Inline N 4.7% 5.6% 3.2 5.5 16.0x 14.4x

4502.T Takeda Pharma 17.9 31% -2.1 -0.3 Inline Inline LOW Inline Inline N 2.3% 6.0% 4.5 6.9 18.0x 18.9x

4503.T Astellas Pharma 19.5 57% -0.9 -1.1 HIGH Inline LOW HIGH HIGH N 2.0% 19.4% 2.8 6.9 16.2x 14.3x

4689.T Yahoo! Japan 28.4 1% -2.5 2.3 LOW Inline LOW HIGH HIGH S -13.3% 18.8% 8.5 9.1 14.2x 13.5x

6301.T Komatsu 34.3 52% -2.6 -2.0 HIGH Inline LOW LOW LOW CS -- 43.0% 0.2 -3.4 9.7x 8.6x

6954.T Fanuc 32.5 34% -2.5 1.0 Inline HIGH Inline Inline Inline CS -- 20.1% -3.6 -5.3 16.6x 15.5x

6981.OS Murata Mfg 29.8 30% -2.1 0.9 Inline Inline Inline Inline Inline B* 24.4% 24.4% -0.2 -2.3 19.7x 15.8x

8031.T Mitsui 27.0 43% -1.9 0.1 Inline Inline Inline Inline LOW N 19.1% 29.4% 3.4 1.5 5.0x 4.8x

8058.T Mitsubishi 28.0 42% -2.5 1.5 Inline HIGH HIGH LOW LOW B* 47.2% 28.0% 3.8 -1.0 5.5x 5.1x

8766.T Tokio Marine 30.4 32% -2.7 0.7 Inline Inline Inline Inline Inline B* 74.4% 28.3% 5.0 8.9 17.8x 12.5x

8801.T Mitsui Fudosan 33.5 41% -3.8 -4.1 Inline LOW Inline LOW Inline B 24.2% 25.6% 5.7 12.3 22.8x 20.7x

8802.T Mitsubishi Estate 31.9 44% -3.0 -2.0 Inline Inline Inline Inline Inline N 17.2% 30.8% 6.3 9.5 35.7x 29.3x

9432.T NTT 17.5 14% -1.6 1.7 Inline Inline LOW HIGH HIGH N 6.9% 15.3% 5.2 4.0 8.0x 7.3x

9437.T NTT DoCoMo 16.2 15% -1.4 2.3 Inline LOW LOW HIGH HIGH B 20.8% 18.4% 1.4 -0.2 9.9x 9.3x

9831.T Yamada Denki 37.1 87% -1.1 -3.9 HIGH LOW LOW HIGH Inline N 21.2% 64.1% 10.3 -4.7 6.5x 6.1x

9983.T Fast Retailing 31.0 54% -1.7 -6.0 HIGH LOW LOW Inline Inline B 43.3% 16.3% -0.9 -10.8 18.7x 16.7x

9984.T Softbank 27.2 0% -1.7 1.7 LOW HIGH HIGH Inline HIGH B* 9.0% 9.0% 6.9 18.2 9.5x 8.7x

Implied Vol and fundamental standouts GS Volatility Radar

Ticker Company

Return to

GS TP

3m Impl

vol (%)

1-year

%ile

9984.T Softbank 9.0% 27.2 0%

4503.T Astellas Pharma 2.0% 19.5 57%

3382.T Seven & I 5.0% 19.2 24%

6301.T Komatsu -- 34.3 52%

8766.T Tokio Marine 74.4% 30.4 32%

4502.T Takeda Pharma 2.3% 17.9 31%

Consensus P/E

Spot (Quoted)

3,265

Volatility-based Magnitude-based GS vs. Consensus Research Performance

930

445,000

2,285

4,355

3,490

3,960

25,260

1,888

12,820

4,260

1,159

1,563

1,949

1,433

1,348

3,555

126,700

15,350

2,752

see appendix for methodology

"HIGH" volatility

Price

Indicative 3-mo

105% calls (%)

Indicative 3-mo 95%

puts (%)

2,752.00

3,265.00

2,285.00

"LOW" volatility1,888.00

1,949.00

3,490.00

3.0

1.6

1.2

5.2

4.4

2.0

3.1

1.7

2.0

5.1

4.4

2.1

Japan Tobacco

Takeda Pharma

Astellas Pharma

Yahoo! Japan

Tokio Marine

Mitsubishi Estate

Seven & I

Mitsui

Mitsubishi

NTTYamada Denki

Fast Retailing

-3.0 -2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

GS bearish + # SD below cons. GS bullish + # SD above cons.

+ve price momentum -ve price momentum

CALL SELLING

CALL BUYING

PUT SELLING

PROTECTION

Op

tio

ns in

exp

en

siv

e

Op

tio

ns e

xp

en

siv

e

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 18

MSCI disclosure

All MSCI data used in this report is the exclusive property of MSCI, Inc. (MSCI). Without prior written permission of MSCI, this

information and any other MSCI intellectual property may not be reproduced or redisseminated in any form and may not be used to

create any financial instruments or products or any indices. This information is provided on an “as is” basis, and the user of this

information assumes the entire risk of any use made of this information. Neither MSCI, any of its affiliates nor any third party

involved in, or related to, computing or compiling the data makes any express or implied warranties or representations with respect

to this information (or the results to be obtained by the use thereof), and MSCI, its affiliates and any such third party hereby

expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with

respect to any of this information. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third

party involved in, or related to, computing or compiling the data have any liability for any direct, indirect, special, punitive,

consequential or any other damages (including lost profits) even if notified of the possibility of such damages. MSCI and the MSCI

indexes are service marks of MSCI and its affiliates. The Global Industry Classification Standard (GICS) were developed by and is the

exclusive property of MSCI and Standard & Poor’s. GICS is a service mark of MSCI and S&P and has been licensed for use by The

Goldman Sachs Group, Inc.

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 19

Disclosure Appendix

Reg AC

We, Sunil Koul and Jason Lui, CFA, hereby certify that all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities.

We also certify that no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Disclosures

Option Specific Disclosures

Price target methodology: Please refer to the analyst’s previously published research for methodology and risks associated with equity price targets.

Pricing Disclosure: Option prices and volatility levels in this note are indicative only, and are based on our estimates of recent mid-market levels(unless otherwise noted). All prices and levels

exclude transaction costs unless otherwise stated.

General Options Risks – The risks below and any other options risks mentioned in this research report pertain both to specific derivative trade recommendations mentioned and to discussion of

general opportunities and advantages of derivative strategies. Unless otherwise noted, options strategies mentioned in this report may be a combination of the strategies below and therefore carry

with them the risks of those strategies.

Buying Options - Investors who buy call (put) options risk loss of the entire premium paid if the underlying security finishes below (above) the strike price at expiration. Investors who buy call or put

spreads also risk a maximum loss of the premium paid. The maximum gain on a long call or put spread is the difference between the strike prices, less the premium paid.

Selling Options - Investors who sell calls on securities they do not own risk unlimited loss of the security price less the strike price. Investors who sell covered calls (sell calls while owning the

underlying security) risk having to deliver the underlying security or pay the difference between the security price and the strike price, depending on whether the option is settled by physical delivery or

cash-settled. Investors who sell puts risk loss of the strike price less the premium received for selling the put. Investors who sell put or call spreads risk a maximum loss of the difference between the

strikes less the premium received, while their maximum gain is the premium received.

For options settled by physical delivery, the above risks assume the options buyer or seller, buys or sells the resulting securities at the settlement price on expiry.

Distribution of ratings/investment banking relationships

Goldman Sachs Investment Research global coverage universe

Rating Distribution Investment Banking Relationships

Buy Hold Sell Buy Hold Sell

Global 31% 54% 15% 48% 41% 36%

As of April 1, 2012, Goldman Sachs Global Investment Research had investment ratings on 3,507 equity securities. Goldman Sachs assigns stocks as Buys and Sells on various regional Investment

Lists; stocks not so assigned are deemed Neutral. Such assignments equate to Buy, Hold and Sell for the purposes of the above disclosure required by NASD/NYSE rules. See 'Ratings, Coverage

groups and views and related definitions' below.

Disclosures required by United States laws and regulations

See company-specific regulatory disclosures above for any of the following disclosures required as to companies referred to in this report: manager or co-manager in a pending transaction; 1% or

other ownership; compensation for certain services; types of client relationships; managed/co-managed public offerings in prior periods; directorships; for equity securities, market making and/or

specialist role. Goldman Sachs usually makes a market in fixed income securities of issuers discussed in this report and usually deals as a principal in these securities.

The following are additional required disclosures: Ownership and material conflicts of interest: Goldman Sachs policy prohibits its analysts, professionals reporting to analysts and members of their

households from owning securities of any company in the analyst's area of coverage. Analyst compensation: Analysts are paid in part based on the profitability of Goldman Sachs, which includes

investment banking revenues. Analyst as officer or director: Goldman Sachs policy prohibits its analysts, persons reporting to analysts or members of their households from serving as an officer,

June 25, 2012 Asia

Goldman Sachs Global Economics, Commodities and Strategy Research 20

director, advisory board member or employee of any company in the analyst's area of coverage. Non-U.S. Analysts: Non-U.S. analysts may not be associated persons of Goldman, Sachs & Co. and

therefore may not be subject to NASD Rule 2711/NYSE Rules 472 restrictions on communications with subject company, public appearances and trading securities held by the analysts.

Additional disclosures required under the laws and regulations of jurisdictions other than the United States

The following disclosures are those required by the jurisdiction indicated, except to the extent already made above pursuant to United States laws and regulations. Australia: Goldman Sachs Australia

Pty Ltd and its affiliates are not authorised deposit-taking institutions (as that term is defined in the Banking Act 1959 (Cth)) in Australia and do not provide banking services, nor carry on a banking

business, in Australia. This research, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act, unless otherwise agreed by Goldman

Sachs. Brazil: Disclosure information in relation to CVM Instruction 483 is available at http://www.gs.com/worldwide/brazil/area/gir/index.html. Where applicable, the Brazil-registered analyst primarily

responsible for the content of this research report, as defined in Article 16 of CVM Instruction 483, is the first author named at the beginning of this report, unless indicated otherwise at the end of the

text. Canada: Goldman, Sachs & Co. has approved of, and agreed to take responsibility for, this research in Canada if and to the extent it relates to equity securities of Canadian issuers. Analysts may

conduct site visits but are prohibited from accepting payment or reimbursement by the company of travel expenses for such visits. Hong Kong: Further information on the securities of covered

companies referred to in this research may be obtained on request from Goldman Sachs (Asia) L.L.C. India: Further information on the subject company or companies referred to in this research may

be obtained from Goldman Sachs (India) Securities Private Limited; Japan: See below. Korea: Further information on the subject company or companies referred to in this research may be obtained

from Goldman Sachs (Asia) L.L.C., Seoul Branch. New Zealand: Goldman Sachs New Zealand Limited and its affiliates are neither "registered banks" nor "deposit takers" (as defined in the Reserve

Bank of New Zealand Act 1989) in New Zealand. This research, and any access to it, is intended for "wholesale clients" (as defined in the Financial Advisers Act 2008) unless otherwise agreed by

Goldman Sachs. Russia: Research reports distributed in the Russian Federation are not advertising as defined in the Russian legislation, but are information and analysis not having product

promotion as their main purpose and do not provide appraisal within the meaning of the Russian legislation on appraisal activity. Singapore: Further information on the covered companies referred

to in this research may be obtained from Goldman Sachs (Singapore) Pte. (Company Number: 198602165W). Taiwan: This material is for reference only and must not be reprinted without permission.

Investors should carefully consider their own investment risk. Investment results are the responsibility of the individual investor. United Kingdom: Persons who would be categorized as retail clients

in the United Kingdom, as such term is defined in the rules of the Financial Services Authority, should read this research in conjunction with prior Goldman Sachs research on the covered companies

referred to herein and should refer to the risk warnings that have been sent to them by Goldman Sachs International. A copy of these risks warnings, and a glossary of certain financial terms used in

this report, are available from Goldman Sachs International on request.

European Union: Disclosure information in relation to Article 4 (1) (d) and Article 6 (2) of the European Commission Directive 2003/126/EC is available at

http://www.gs.com/disclosures/europeanpolicy.html which states the European Policy for Managing Conflicts of Interest in Connection with Investment Research.

Japan: Goldman Sachs Japan Co., Ltd. is a Financial Instrument Dealer under the Financial Instrument and Exchange Law, registered with the Kanto Financial Bureau (Registration No. 69), and is a

member of Japan Securities Dealers Association (JSDA) and Financial Futures Association of Japan (FFAJ). Sales and purchase of equities are subject to commission pre-determined with clients plus

consumption tax. See company-specific disclosures as to any applicable disclosures required by Japanese stock exchanges, the Japanese Securities Dealers Association or the Japanese Securities

Finance Company.

Ratings, coverage groups and views and related definitions

Buy (B), Neutral (N), Sell (S) -Analysts recommend stocks as Buys or Sells for inclusion on various regional Investment Lists. Being assigned a Buy or Sell on an Investment List is determined by a

stock's return potential relative to its coverage group as described below. Any stock not assigned as a Buy or a Sell on an Investment List is deemed Neutral. Each regional Investment Review

Committee manages various regional Investment Lists to a global guideline of 25%-35% of stocks as Buy and 10%-15% of stocks as Sell; however, the distribution of Buys and Sells in any particular

coverage group may vary as determined by the regional Investment Review Committee. Regional Conviction Buy and Sell lists represent investment recommendations focused on either the size of the

potential return or the likelihood of the realization of the return.