Marketing Strategies HSBC Table of Contents Executive Summary.................................................... 2 INTRODUCTION......................................................... 3 Company profile...................................................... 4 1. Market Segmentations.............................................. 6 1.1. Geographic Segmentation:.......................................6 1.2. Demographic segmentation:......................................6 1.3. Psychographic Segmentation:....................................7 1.4. Behavioral Segmentation:.......................................7 2. Market Targeting.................................................. 8 2.1. Selection of Target Market.....................................8 2.2. Evaluation of Target Market...................................13 3. Positioning...................................................... 14 3.1. Value proposition.............................................15 4. Marketing Mix.................................................... 17 4.1. Product.......................................................17 4.2. Price.........................................................20 4.3. Place.........................................................22 4.4. Promotion.....................................................22 Conclusion.......................................................... 24 References.......................................................... 25 Page 1 of 34

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Marketing Strategies HSBC

Table of ContentsExecutive Summary.....................................................................................................................................2

INTRODUCTION......................................................................................................................................3

Company profile........................................................................................................................................4

1. Market Segmentations.........................................................................................................................6

1.1. Geographic Segmentation:...............................................................................................................6

1.2. Demographic segmentation:............................................................................................................6

1.3. Psychographic Segmentation:...........................................................................................................7

1.4. Behavioral Segmentation:.................................................................................................................7

2. Market Targeting.....................................................................................................................................8

2.1. Selection of Target Market...............................................................................................................8

2.2. Evaluation of Target Market...........................................................................................................13

3. Positioning.............................................................................................................................................14

3.1. Value proposition...........................................................................................................................15

4. Marketing Mix.......................................................................................................................................17

4.1. Product...........................................................................................................................................17

4.2. Price...........................................................................................................................................20

4.3. Place..........................................................................................................................................22

4.4. Promotion..................................................................................................................................22

Conclusion.................................................................................................................................................24

References.................................................................................................................................................25

Page 1 of 26

Marketing Strategies HSBC

Executive Summary

HSBC is a global banking and financial service company headquartered in London, United Kingdom. As of 2011, it was the world's second-largest banking and financial services group and second-largest public company. It has around 7500 offices in 87 countries and territories across Africa, Asia, Europe, North America and South America and around 100 million customers.

As of 30 June 2010, it had total assets of $2.418 trillion, of which roughly half were in Europe, a quarter in the Americas and a quarter in Asia.

HSBC Holdings plc was founded in London in 1991 by The Hongkong and Shanghai Banking Corporation to act as a new group holding company and to enable the acquisition of UK-based Midland Bank. The origins of the bank lie in Hong Kong and Shanghai, where branches were first opened in 1865. Today, HSBC remains the largest bank in Hong Kong, and recent expansion in mainland China, where it is now the largest international bank has returned it to that part of its roots.

This report provides the details of HSBC’s marketing strategy. HSBC divides the market into different segments, evaluates the product and uses local marketing to provide the best service to its customers.

Page 2 of 26

Marketing Strategies HSBC

HSBC Marketing Strategies

INTRODUCTIONMarketing strategy is the process that allows HSBC to concentrate its limited resources on the greatest opportunities to increase sales and achieve a sustainable competitive advantage. Marketing strategies serve as the fundamental underpinning of marketing plans designed to fill market needs and reach marketing objectives. Plans and objectives are generally tested for measurable results. Commonly, marketing strategies are developed as multi-year plans, with a tactical plan detailing specific actions to be accomplished in the current year. Time horizons covered by the marketing plan vary by company, by industry, and by nation, however, time horizons are becoming shorter as the speed of change in the environment increases. Marketing strategies are dynamic and interactive. They are partially planned and partially unplanned.

Page 3 of 26

Marketing Strategies HSBC

Company profileHSBC Holdings plc is a global banking and financial services company headquartered in Canary Wharf, London, United Kingdom. As of 2011, it was the world's second-largest banking and financial services group and second-largest public company according to a composite measure by Forbes magazine. It has around 7,500 offices in 87 countries and territories across Africa, Asia, Europe, North America and South America and around 100 million customers. As of 30 June 2010, it had total assets of $2.418 trillion, of which roughly half were in Europe, a quarter in the Americas and a quarter in Asia. The shares of this company have been taken by various shareholders all around the world. It has 220,000 shareholders in 124 countries which speaks volumes about the goodwill of the company.

HSBC Holdings plc was founded in London in 1991 by The Hongkong and Shanghai Banking Corporation to act as a new group holding company and to enable the acquisition of UK-based Midland Bank. The origins of the bank lie in Hong Kong and Shanghai, where branches were first opened in 1865. Today, HSBC remains the largest bank in Hong Kong, and recent expansion in mainland China, where it is now the largest international bank has returned it to that part of its roots.

HSBC runs a number of operative systems to assure its global successfulness. In particular, HSBCnet is the Group’s global service that coordinates local business needs and offers functional services to the operating spots worldwide. At that, both corporate and individual customers obtain access to banking transactions, trade services, exchange operations and money trading services. In addition to this, HSBCnet is widely applied as the marketing tool to promote the Bank’s e-commerce services.

At present, the HSBC group provides a comprehensive range of financial services namely:

Page 4 of 26

Marketing Strategies HSBC

Personal Financial Services: It has over 100 million personal consumers' worldwide (including Consumer Finance customers). It provides a full range of personal finance services, including current and savings accounts, mortgages, insurance, loans, credit cards, pensions, and investment services. It is one of the world's top ten issuers of credit cards.

Consumer Finance: The Company's Finance Corporation's consumer finance business ensures point of sale credit to consumers, and lends money and provides related services to meet the financial needs of everyday people. In 2004, it completed the integration of its former household businesses.

Commercial Banking: HSBC is a leading provider of financial services to small, medium-sized and middle market enterprises. The group has over two million such customers, including sole proprietors, partnerships, clubs, and associations, incorporated businesses and publicly quoted companies. In the UK, 209 Commercial Centre were launched to provide improved relationship management for higher value small-medium-sized enterprise customers, while in Hong Kong, Business Banking Centers, were expanded to provide a one-stop service.

Corporate Investment Banking and Markets: Tailored financial services are provided to corporate and financial clients. Business lines include Global Markets, Corporate and Institutional Banking, Global Transaction Banking, and Global Investment Banking. Global Markets includes foreign exchange, fixed income, derivatives, equities, metals trade, and other trading businesses. Corporate and Institutional Banking covers relationship management and lending activities. Global Transaction Banking includes payment and cash management, trade services, supply chain, securities services, and wholesale banknotes businesses. Global Investment Banking involves investment banking advisory, and investment banking financing activities.

Page 5 of 26

Marketing Strategies HSBC

Private Banking: HSBC is one of the world's top private banking businesses, providing financial services to high net worth individual and families in 70 different locations.

1. Market Segmentations

1.1. Geographic Segmentation:

Market segmentation strategy of HSBC where by the intended audience for a given service is decided according to geographic units such as countries, cities etc.

1.1.1. Country/World Region: HSBC is organized by business line (personal financial services, consumer finance, commercial banking, corporate investment banking and private banking) by geographic segments-

1. Asia Pacific2. U.K.

Page 6 of 26

Marketing Strategies HSBC

3. North America/NAFTA4. South America

1.1.2. City/Metro City: HSBC is more willing to open their branches in the big, developed and crowded cities or areas as they want to attract the higher class people. But they also have some branches in small and undeveloped cities also.

1.1.3. Density: Most of the HSBC branches are in the urban areas. They hardly open their branches in rural areas. HSBC divides the market on the basis of different geographic units such as urban market, rural market, eastern market, western market, etc.

1.2. Demographic segmentation:

The demographic segmentation of HSBC is where the services are divided into various categories based on demographic variables such as income, education, religion, politics etc. Demographic segmentation is the most popular basis for dividing groups because customers’ wants or needs usually match the demographic categories.

1.2.1. Income: Income is the most important segment for HSBC. Fixed income earners demand more services than that of variable income earners. On the basis of social class, the market is segmented into higher class and upper middle class. Higher class customers are complicated, selective but they are more profitable. On the other hand, most of the retired customers own a large sum of pension. The bank mainly focuses on the people who can earn a healthy income every month. So, their main targets are the upper middle and upper/higher class people. HSBC targets these segments as their customers and hope that they can open accounts in HSBC or make investment through them.

1.2.2. Religion: HSBC has special services for different religions. For example, HSBC has "Islamic Banking System" with their traditional banking system especially for the Muslim countries. For example, they offer Amanah, Amanah Personal and Amanah Corporate for Muslim customers.Education HSBC likes to deal with educated people, as they are easier to deal with.

1.2.3. Occupation: HSBC likes to deal with professional and technical; managers, officials and proprietors; clerical sales; craftspeople; forepersons; operatives; farmers; retired; students; homemakers

1.2.4. Family life cycle: HSBC provides different services for different stages of life cycle. HSBC follows young, single; young married, no children; young, married, youngest child under 6; young, married, youngest child 6 or over; older, married, with children; older, married, no children under 18; older, single; other

Page 7 of 26

Marketing Strategies HSBC

1.3. Psychographic Segmentation:

HSBC divides the customer market into different groups based on their social class and lifestyle.

1.3.1. Social Class: social class is one of the unique points of HSBC. Income, occupation, education, wealth these four factors determine social class. People in the same demographic group can have very different social class. HSBC segments the customer market by targeting the upper middle class, upper class people.

1.3.2. Lifestyle: HSBC segment their market by customer lifestyle and base their marketing strategies of lifestyle. Generally the bank targets the achievers, those people who have comfortable and luxurious lifestyle.

1.4. Behavioral Segmentation: HSBC divides customers into groups based of their knowledge, attitudes and responses to services. HSBC believes that behavioral variables are the best starting for market segmentation.

1.4.1. Occasion: HSBC provides various services to the customers in various occasions.

1.4.2. Benefits: HSBC divides the market into groups according to the different benefits that customers seek from the services.

1.4.3. Loyalty: HSBC segments the market by customer loyalty. Customers are divided into groups according to their loyalty. Some customers are completely loyal and so they get special services from the bank.

2. Market Targeting

2.1. Evaluation of Target Market

HSBC Bank plc is the U.K. member of the HSBC banking group. Its card services division manages the credit card products. The card services analysis unit uses SPSS software for marketing campaign evaluation and customer segmentation strategies.

About 125 million credit card transactions are made each year by HSBC Bank cardholders. Each transaction carries an income fee payable by the receiving bank to the cardholder’s bank. The rules on fee rates applied are somewhat complex. A further complicating factor is that banks processing the transactions from the retailers may use different processing systems.

Page 8 of 26

Marketing Strategies HSBC

But the challenge is the credit card market is one of the most volatile banking product markets in the U.K., due in part to an influx of new entrants over the past five years. These range from single product suppliers looking to extend their market to vertical industries diversifying their product range. Barriers to entry are relatively low, so the credit card tends to be used as a “foot-in-the-door” product. This has increased the need for traditional U.K. credit card issuers such as HSBC to develop appropriate retention and income generation strategies. Bob Howlett, manager of business analysis, card services, HSBC Bank plc, explains, “We believed that incorrect fees were being received for some transactions. Our task was to verify this and also set up a process which would ensure that the correct transaction fee was being applied on all transactions.” HSBC Bank plc decided to evaluate SPSS after internal software and basic database software had proved ineffectual.

As a result of extensive experience in handling large volumes of data, a member of the card services analysis unit was asked to help solve this challenge. A daily transaction feed was sorted using SPSS for Windows software and, within two weeks, income shortfalls had been identified. Further manipulation of the data indicated substantial variances between the income received and the income that should have been received. “We anticipate that recovery of this underpayment will generate in excess of one million pounds (~US$1.43 million) per annum,” explained Mr. Howlett.

Using SPSS software, HSBC Bank plc was able to analyze millions of bytes of data efficiently to recover lost money. The people who analyze customer-level databases are able to apply their knowledge to sort high volumes of individual transactions and deliver the required outputs with ease. As a result this marketing evaluation campaign worked out just fine for HSBC Bank.

On February 08, 2011 in London - HSBC Bank plc announced that HSBC Net, its global online banking solution, has maintained its position as one of the leading electronic banking platforms for corporate and commercial clients globally, according to results of the 2010 Greenwich Associates Online Services Benchmarking study.

The study ranks HSBC net in the top spot among global banks in the areas of Usability/Ease of Use and Integration/Organization, while demonstrating “Best of Breed” features in the areas of Look and Feel, Cross Product Integration and Transaction Search/Item Inquiry. HSBC net outperforms the peer group on more than half of the evaluation factors, with improvements noted by Greenwich Associates since 2008 in the areas of Online Help/Support, Education/Training, Security Features and User Authentication.

Page 9 of 26

Marketing Strategies HSBC

HSBC serves 16.1 million customers in the UK and employs approximately 56,000 people. In the UK, HSBC offers a complete range of personal, premier and private banking services, commercial banking for small to media businesses and corporate and institutional banking services. HSBC Bank plc is a wholly owned subsidiary of HSBC Holdings plc.

HSBC net is a global online banking platform for corporate and commercial customers, offering a comprehensive suite of cash management, trade and supply chain, securities solutions.

Client sphere is a patent pending cash management solution implementation platform developed by HSBC. The robust project management and communication platform can be used by HSBC, clients and third party vendors during an implementation project. It fosters visibility and control of implementation project progress, and alignment among all parties, regardless of their geographical and organizational boundaries. Its streamlined processes and embedded best-practice workflows enhance regional consistency and efficiency, thereby enabling swift and seamless cash management solution delivery.

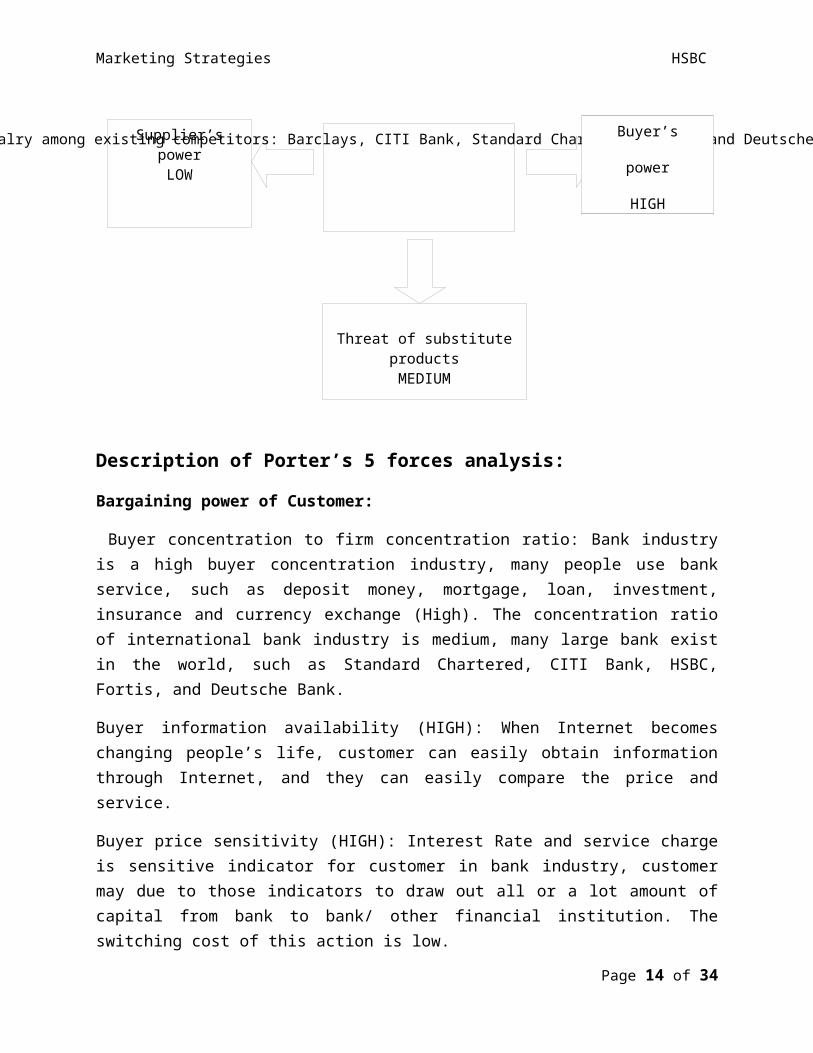

Michael Porter’s 5 forces analysis:

Page 10 of 26

Threat of new entrants

HIGH

Threat of substitute productsMEDIUM

Supplier’spowerLOW

Rivalry among existing competitors: Barclays, CITI Bank, Standard Chartered, Fortis and Deutsche Bank.

Marketing Strategies HSBC

Description of Porter’s 5 forces analysis:

Bargaining power of Customer:

Buyer concentration to firm concentration ratio: Bank industry is a high buyer concentration industry, many people use bank service, such as deposit money, mortgage, loan, investment, insurance and currency exchange (High). The concentration ratio of international bank industry is medium, many large bank exist in the world, such as Standard Chartered, CITI Bank, HSBC, Fortis, and Deutsche Bank.

Buyer information availability (HIGH): When Internet becomes changing people’s life, customer can easily obtain information through Internet, and they can easily compare the price and service.

Buyer price sensitivity (HIGH): Interest Rate and service charge is sensitive indicator for customer in bank industry, customer may due to those indicators to draw out all or a lot amount of capital from bank to bank/ other financial institution. The switching cost of this action is low.

Availability of existing substitute products (HIGH): Many substitute product or service present in recent year, such as currency exchange, insurance and loan. They mainly provided by other financial institution.

Page 11 of 26

Buyer’s

power

HIGH

Marketing Strategies HSBC

Bargaining power of Supplier (Low):

Bank capital supplier (Low): Depositor also is capital supplier of bank, they will compare with other financial product to see whether draw out capital or not.

Computer equipment supplier (Low): The concentration ratio of computer is high, many companies use IBM, but it doesn’t mean other computer companies are not good, such as Sun Microsystems, Fujitsu and Hewlett-Pack also provide similar computer equipment and solution.

Credit Card supplier (Medium):

Credit Card industry is a high concentration ratio industry, VISA, Master Card and American Express is the most popular credit card in the world. Although other organization also release credit card system, such as JCB, there market share in the world is much less than these three organizations. Moreover, these three organizations brand name is louder than other organizations, so the switching cost from these organizations to others may be too large.

Threats of new entrants (High):

When many countries and cities join WTO and the Internet effect, the barrier of bank become disappear. Many financial even non-financial organizations can easily entry to bank industry. They can use more little money to build a website; they can also integrate with other organizations. The switching cost of this behavior become smaller than before and the advantage is larger than before also.

Threats of substitute product:

Internet makes many organizations can use smaller amount of money relatively to provide similar even same service, and the service charge become smaller. Customer will due to convenience, low cost and high efficiency to change the service to other organization. Real-time money transfer (i.e. Western Union), real-time payment (i.e. Paypal), currency exchange (i.e. Xe.com) and insurance (i.e. InsWeb.com), they through Internet to provide a high quality but low service charge service.

The intensity of competitive rivalry:

Page 12 of 26

Marketing Strategies HSBC

There are many banks in the world, which are competitors of HSBC Bank, for example Barclays, CITI bank, Standard Chartered, Fortis and Deutsche Bank. The Earning Before Interest and Tax (EBIT) in 2006 of top 1000 banks in the world is 6451 billions US dollars, higher than 2005. Due to technology becomes improve; financial control become release and the change of environment in the society, competition between banks become violent and the maturity of financial market in western country is very high, so the competitiveness force bank to find other profit continuously.

2.2. Selection of Target Market

Selecting markets of HSBC has four levels: mass, segmented, niches and micro marketing. Market segments are large identifiable groups within a market. A niche is a more narrowly defined group. Marketers appeal to local markets through grassroots marketing for trading areas, neighborhoods, and even individual stores.

2.1.1. Mass marketing: The argument for mass marketing is that it creates the largest potential market, which leads, to the lowest costs that in turn can lead to lower prices or higher margins.

Page 13 of 26

Marketing Strategies HSBC

2.1.2. Segmented marketing:In segmented marketing marketers does not create the segments. The marketer’s task is to identify the segments and decide which one(s) to target.

2.1.3. Niche marketing:Niche marketers presumably understand their customers’ needs so well that the customers willingly pay a premium.Globalization facilitated niche marketing.The low of setting up shop on the internet has led to many small business start ups aimed at niches.

2.1.4. Local marketing:Local marketing reflects growing trend called grassroots marketing.Marketing activities concentrate on getting as close and personally relevant to individual customers as possible.A large part of local, grassroots marketing is experiential marketing that promotes a product or service not just by communicating its features and benefits, but by also connecting it with unique and interesting experiences.

HSBC has discontinued mass marketing and use segmented marketing a little. They use niche marketing more than segmented marketing. But their real focus is on local marketing and that is the reason HSBC is called “world’s local bank”.

The key success factors for HSBC have been advertising campaigns that illustrates HSBC’s local connection to the countries and markets that they are doing business. HSBC’s success rests on its ability to understand the local markets and niche markets in the countries that they reside. HSBC must continue to understand the local market and to continue to make the “connection” with local communities.

3. Positioning

The banking market positioning refers to the banks based on the location of capital strength and services, having regard to the existing customers demand characteristics, develop the bank’s financial products and services representing its image to show distinct personality to customers. So as to establish its place in the target market (Alessandrini, Calcagnini and Zazzaro, 2008)

Page 14 of 26

Marketing Strategies HSBC

Despite growing in almost 80 countries all over the world, HSBC has been successful in positioning itself in ‘World’s local bank’. As the bank constantly works hard to maintain a local feel and local knowledge, customers feel comfortable to bank with an international brand like HSBC. Consequently it has ensured high customer loyalty and HSBC has been able to retain its large customer pool.

HSBC is an international financial institution. It can be said that it has prominent position in the financial sector. Although it is not a major bank in other areas, however, as the group has a global management, and has strong robust strength in the banking industry, so it still plays a supporting and promoting role in financial development. Furthermore, the group itself is a large listed financial institution and has a good financial situation {Mizuno, 2004). So, it has established customer’s confidence in HSBC. Therefore, the banks use these advantages to attract high level depositors. As based Hong Kong bank, the general fees and business strategy are developed according to the living index of Hong Kong, so it may not meet the conditions of the rest of the world. (Palrnatier. 2007).

At the same time, HSBC mainly focuses on corporate clients, businesses and high level individual customers.

3.1. Value proposition

HSBC Bank follows the more for more and less for less value proposition where more benefits are provided for more prices. The customers who provide high price are valued by HSBC highly and the customer service is provided accordingly. For example, HSBC has created a high-touch customer experience for its “premier” clients in Hong Kong. These high-net-worth customers receive preferential counter service and pricing, supported by a branch upgrade that allows tellers to spend more time on service and less on routine transactions, plus a 24-hour call center and website that provide an integrated view of both local and foreign currency accounts.

Page 15 of 26

Marketing Strategies HSBC

How HSBC adds value:

HSBC adds value to the commercial-banking experience by managing a network of customers with complementary needs. At a very basic level, HSBC serves as an intermediary that links depositors with borrowers. Providing excellent customer service and leveraging its expertise in niche markets allows HSBC to differentiate itself from other Canadian banks. HSBC does not attempt to be a low-cost provider, as it does not have the economies of scale to compete against the larger Canadian banks. Rather, HSBC competes with a differentiation strategy.

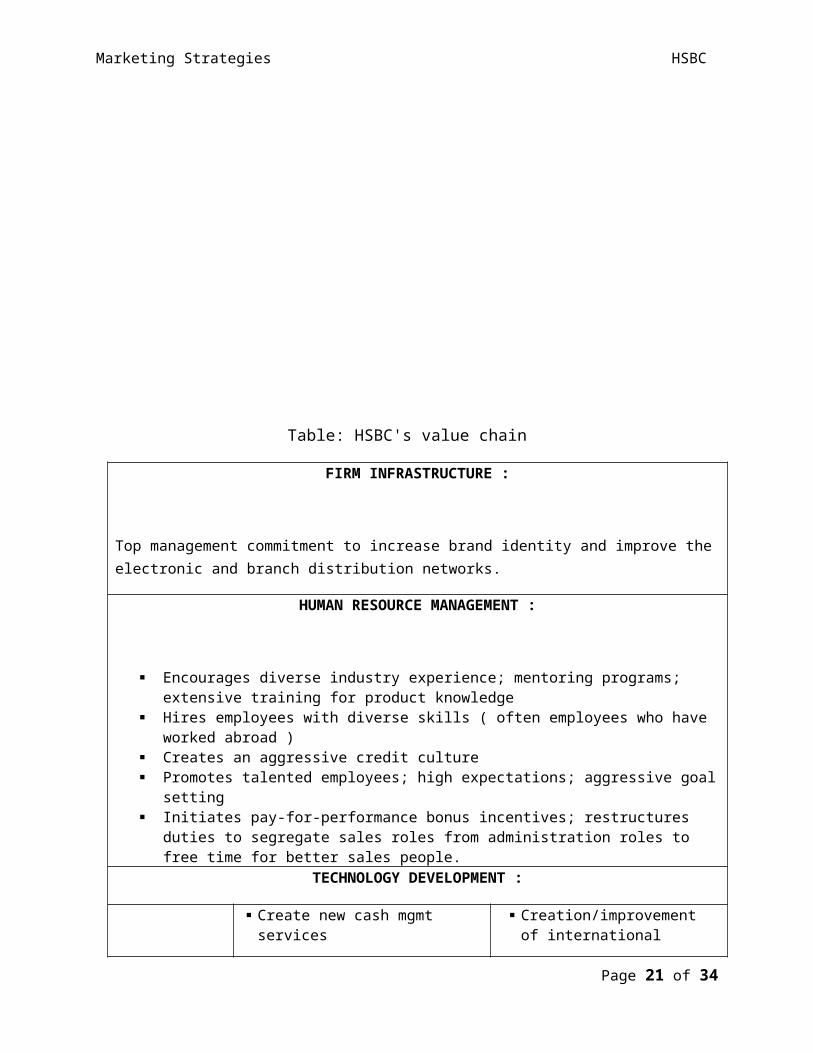

Table: HSBC's value chain

FIRM INFRASTRUCTURE :

Top management commitment to increase brand identity and improve the electronic and branch distribution networks.

Page 16 of 26

Marketing Strategies HSBC

HUMAN RESOURCE MANAGEMENT :

Encourages diverse industry experience; mentoring programs; extensive training for product knowledge

Hires employees with diverse skills ( often employees who have worked abroad )

Creates an aggressive credit culture Promotes talented employees; high expectations; aggressive goal setting Initiates pay-for-performance bonus incentives; restructures duties to

segregate sales roles from administration roles to free time for better sales people.

TECHNOLOGY DEVELOPMENT :

Create new cash mgmt services

Improve user-friendliness of website

Improve internal application processes ( reduce delivery of service time )

Creation/improvement of international technology (i.e. internet) platforms

24/7 account accessibility from around the world.

PROCUREMENT :

Network Promotion and Contract Management

Strong sponsorship of sports and recreational events

Carter to well traveled and affluent

Appeal to image conscious

Offer full service offering (i.e. include personal and investment services to complement commercial services )

Well established and secure bank (especially with regards to internet security)

Service Provisioning

High quality of advice. Superior trade finance

services. Superior cash

management services. Superior leasing

services Access to unlimited

funds. Global presence. Flexible service

offerings; ability to customize commercial services

Infrastructure Operation

Operate branch network and selectively increase # of location.

Operate internet banking. Operate phone banking. Operate ABM network. Maintain access to funds

(primarily for lending purposes)

Maintain close links between subsidiaries around the world.

4. Marketing Mix

4.1. ProductPage 17 of 26

Marketing Strategies HSBC

Usually product could be referred to the goods as well as the services that are offered to the customers. In case of goods product is tangible in nature whereas in case of service it is intangible. Elements like features, quality, services, options and brand name that are associated with the product are crucial for the success of any product or service. In case of service quality is the key element (Purdue University, n.d.).

As far as HSBC private bank is concerned, its major products include investment services, family wealth advisory, private wealth solutions and general banking services. All these services are designed considering various needs of customers. Family advisory service is developed in such a way so that it can take care of the financial prosperity of a family by helping it to attain greater tax efficiency. Private wealth solutions are nothing but wealth management plans which are developed to protect the valuable wealth of a family. Various banking services of HSBC private bank include general transaction related services, loans and mortgages, onshore and offshore deposits, foreign exchange etc. (HSBC private Bank, n.d.). So, it can be stated that services, offered by the bank, are very much customer and market oriented.

HSBC private bank needs to improve its product and service portfolio by increasing the number of offerings. The bank can enter into the insurance market (both life and general) by making an alliance with one of the insurance giant in the Chinese market.

In order to attract new customers the bank has to offer something new to them. In order to do so bank can undertake a medium size market survey in order to find out the financial needs of the HNI Chinese customers and products or services could be developed based on the findings of this survey.

The HSBC group provides a comprehensive range of financial services namely:

Personal Financial Services: It has over 100 million personal consumers’ worldwide (including Consumer Finance customers). It provides a full range of personal financial services, including current and savings accounts, mortgages, insurance, loans, credit cards, pensions, and investment services. It is one of the world’s top ten issuers of credit cards. Consumer Finance: The Company’s Finance Corporation’s consumer Finance business ensures point of sale credit to consumers, and lends money and provides related services to meet the financial needs of everyday people. In 2004, it completed the integration of its former household businesses.

Commercial Banking: HSBC is a leading provider of financial services to small, medium-sized and middle market enterprises. The group has over two million such customers, including sole proprietors, partnerships, clubs, and associations, incorporated businesses and publicly quoted companies. In the UK, 209 Commercial Centre were launched to provide improved relationship management for higher value small-medium-sized enterprise customers, while in Hong Kong, Business Banking Centers, were expanded to provide a one-stop service.

Page 18 of 26

Marketing Strategies HSBC

Corporate Investment Banking and Markets: Tailored financial services are provided to corporate and financial clients. Business lines include Global Markets, Corporate and Institutional Banking, Global Transaction Banking, and Global Investment Banking. Global Markets includes foreign exchange, fixed income, derivatives, equities, metals trade, and other trading businesses. Corporate and Institutional Banking covers relationship management and lending activities. Global Transaction Banking includes payment and cash management, trade services, supply chain, securities services, and wholesale banknotes businesses. Global Investment Banking involves investment banking advisory, and investment banking financing activities.

The product must be a means to solve a problem or satisfy a want in the market. To date, overspending is a major issue in the Western world. This is the reason why the new HSBC prepaid card is included in the new current account package as a means to ensure that customers do not overspend by ensuring prudential budgeting of financial resources.

Key business areas in Bangladesh

Key business areas:

Retail Banking and Wealth Management

Commercial Banking

Corporate and Institutional banking

Global Markets

Shariah Compliant Banking

Types of accounts provided

Personal Home Loan Personal Loan NRB Services HSBC Select Power Vantage

Corporate Export Services Import Services Electronic DC Advising Cash Management

Page 19 of 26

Marketing Strategies HSBC

Amanah Amanah Personal Amanah Corporate

Unique Features:

Prepaid Card

HSBC will launch two prepaid cards, namely, the HSBC’s Financial Manager and the HSBC’s Budget Manager prepaid card. Both prepaid cards come preloaded with £10 after the customer pays the initial card issue fee. The Financial Manager is a way to manage a monthly budget by transferring your spending money from your bank account onto the card. It has an annual load limit of £15,000. The Budget Manager on the other hand has a smaller annual load limit of £2,000.

The new HSBC prepaid cards would be fee-free while offering the same flexibility as a credit or debit card. The prepaid card however, would need to be loaded up with cash first before allowing its users to purchase products and services. The prepaid cards can also be used to withdraw money from cash machines.

Real Time Balance Alerts

Real time balance alerts will be sent to the customer’s mobile device every time a HSBC prepaid card user purchases something. This balance update will notify the prepaid card user on the amount of money spent and the amount of money left for free. HSBC may need to team up with companies like Vodafone to provide this service.

Online Banking

Another unique element of the HSBC prepaid cards are their flexibility in managing the customer’s financial resources. Bank customers can access the HSBC website and set standing orders on how much money to load onto the budget manager every month as long as the funds are available in their current account.

Optional Savings Account

Bank customers that pay more than £500 into their current account every month would qualify for the HSBC’s Current Account Advance. Regular payments can be made through the internet or by direct standing order from the customer’s current account to save a specific amount every month. This feature is ideal for customers with a fixed monthly income.

Page 20 of 26

Marketing Strategies HSBC

4.2. Price

The pricing component plays twin roles for HSBC in the sense that it must be able to first attract customers to purchase the service and also generate revenue for HSBC. According to Adrian Palmer (2008), there are five main factors that influence pricing decisions, namely, profit maximization, market-share maximization, survival, social considerations and personal objectives.

While pricing strategy is highly dynamic for other products and services, pricing for current account services have become rather static in recent years. Most banks do not require any fees to set up a current account. Banks instead rely on the money that floats in the interval when they are deposited to when they are spent in order to profit from current accounts.

It is unlikely that any increases in interest rates would be able to attract customers to open up new current accounts with HSBC. The base lending rate that is now at 0.5% provides little room to maneuver for banks and other financial institutions. Adding to that is the credit crunch and declining asset prices that makes borrowing at a higher rate unattractive at the moment. The initial prepaid card issue fee should be around £10. This is in line with what competitors are charging at the moment.

The catch with the prepaid card scheme is that it encourages bank customers to save. Any money that is saved is held within the customer’s current account and remains available for banks to provide further lending. This may prove to be highly beneficial to HSBC during times when raising new capital is extremely difficult.

The cost of using prepaid cards

Card Initial card issue fee

Monthly fee Charge for ATM

withdrawals

Charge for purchases

Cost to reload the

card

Page 21 of 26

Marketing Strategies HSBC

HSBC Prepaid Visa Card £9.99 Nil (But annual fee of

£5.00

Nil Nil Free

Virgin Prepaid Master Card

£9.95 Nil 2.95% 2.95% Free at post office or via bank

transfer

Cash plus Gold Master Card

£4.95 £4.95 99p Nil Free

Tuxedo Master Card £9.95 £4.99 50p Nil 99p at post office or free via

bank transfer

The BREAD card Maestro

£10.00 Nil £1.50 2.00% Free at post office

Optimum Master Card £9.95 £4.95 £1.50 Nil Free at post office or via bank

transfer

Splash Plastic Maestro £5.00 Nil (But £4.95 annual fee)

£1.50 (plus 2% for

withdrawals over £50

2.5% 30p per £100

loaded at post office

4.3. Place

The place element involves delivering the product element to customers through appropriate methods and delivery channels. Delivery may involve both physical and electronic channels. Failure to make a service product readily available to customers would guarantee its failure regardless of how good the service product is.

Page 22 of 26

Marketing Strategies HSBC

HSBC's international network comprises around 7,500 offices in 87 countries and territories in Europe, the Asia-Pacific region, the Americas, the Middle East and Africa.

Offices by Region

Region Number of officesAmericas 3,821Asia-Pacific 1,830Europe 2,315Middle East & Africa 302

HSBC networks in Bangladesh

13 offices,

39 ATMs,

9 Customer Service Centers,

an offshore banking unit,

Offices in 7 EPZs.

4.4. Promotion

Promotion of a particular product or service is mainly done either to push the product to the customers or pull the customers to the products or service. In case of service customers are generally pulled by the service creators to the place where it is being created and various promotional strategies are adopted for this purpose. The promotion element relies on effective communications to bring awareness in the market of the service products offered by HSBC. The three objectives of the promotion element are to gain the attention of customers, provide additional information and persuade customers to purchase the product. Advertising is mass, paid communication that is used to transmit information, develop attitudes and induce some form of response on the part of the audience (Adrian Palmer, 2008).

HSBC’s advertising certainly reflects one brand value, and very much so — the first one, “Perceptive.” All the bank’s current advertising materials illustrate how the bank celebrates diverse cultures and customs of people around the world, and that “every individual has their own priorities and values, and that these form the basis of many important decisions,” as the bank puts it.

Page 23 of 26

Marketing Strategies HSBC

“A different point of view is simply the view from a place where you’re not.”– HSBC

“Through our campaign, HSBC challenges people to address their own values and discover what drives and motivates them in their daily lives,” the bank says on its website. “And through this journey it is our belief that what we learn from one customer will help us to better serve another.”

If all the marketing goals and objectives are to achieved promotion would be the most important ‘P’ among all. One of the most important marketing objectives is to increase the number HNI client by 20% within the month of April. Three marketing communication tools, advertising, public relation and direct selling would be most effective in order to achieve the marketing goals and objectives. Advertising would mainly be done in electronic and print media. Online promotion would be an important factor as the number of internet users is increasing rapidly in the country. Advertising is likely to increase the awareness of the products and services of HSBC private bank. Direct selling is another technique that is likely to be very effective in increasing the number of high net worth customers. In direct selling target customers are directly approached by mail, phone or SMS. Efficient sales persons with excellent convincing skill are involved in the process. In order to achieve the target of increasing the number of HNI client by 20%, target could be divided among each of the three cities in the country. Since Beijing and Shanghai are the two major commercial hubs in the country, most of the HNI clients are likely to be living there. So, 80% of the target customers could be achieved from these two cities. Another major promotional activity that needs to be performed is to make a separate website of HSBC private bank China. Like any other HSBC website this site would also include all the details regarding the products, services and various terms & conditions. Website needs to be heavily promoted in order to rebuild the brand HSBC among the HNI market in China.

Several public relation and CSR activities need to be performed in order to regain customers’ trust. The bank provides educational support to the poor children; it gets involved with some of the renowned healthcare institutions with the purpose of providing financial support to all those people who can not afford the cost of their treatment.

Page 24 of 26

Marketing Strategies HSBC

Conclusion

From this report we can say that HSBC is an organization that helps its customers not only on big scale

but also on small scale. It has gone through many evaluation stages which have created more facilities

for the customers. The key of success of HSBC bank is that they use local marketing, so they must

continue to understand the local market and to continue to make connections with the local

communities. They should watch out for rapid changes to their target markets in local and national

levels. Market positioning helps create a special place in the minds of the customers. Marketing mix is

the most vital part of marketing strategies. Without a proper marketing mix, the marketing is

incomplete. HSBC is one of the leading banks which does its evaluation with the changes of the

technologies and provides local marketing as well as international marketing. HSBC brings customer

satisfaction that helps the bank to retain its customers.

Page 25 of 26

Marketing Strategies HSBC

References

http://www.spss.com.sg/data/files/pdf/stories/Financial%20Services/HSBC%20Bank%20plc.pdf

http://content.householdaccount.com/hsbc_pcm/onetime/HSBCnet_Greenwich.pdf

http://saxontse.drivehq.com/SMIS_HW.doc

http://www.ukessays.com/essays/business/marketing-strategies-hsbc.php

http://www.oup.com/uk/orc/bin/9780199290437/baines_ch06.pdf

http://www.spss.com.sg/data/files/pdf/stories/Financial%20Services/HSBC%20Bank%20plc.pdf

http://www.prenhall.com/behindthebook/0132390027/pdf/Kotler_CH07.pdf

http://en.wikipedia.org/wiki/Marketing_strategy#cite_note-0

Class Notes and Lectures

Page 26 of 26

Related Documents