University of Mississippi University of Mississippi eGrove eGrove Haskins and Sells Publications Deloitte Collection 1-1-1903 How to keep household accounts, A manual of family finance How to keep household accounts, A manual of family finance Charles Waldo Haskins Follow this and additional works at: https://egrove.olemiss.edu/dl_hs Part of the Accounting Commons, and the Taxation Commons Recommended Citation Recommended Citation Haskins, Charles Waldo, "How to keep household accounts, A manual of family finance" (1903). Haskins and Sells Publications. 1693. https://egrove.olemiss.edu/dl_hs/1693 This Article is brought to you for free and open access by the Deloitte Collection at eGrove. It has been accepted for inclusion in Haskins and Sells Publications by an authorized administrator of eGrove. For more information, please contact [email protected].

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

University of Mississippi University of Mississippi

eGrove eGrove

Haskins and Sells Publications Deloitte Collection

1-1-1903

How to keep household accounts, A manual of family finance How to keep household accounts, A manual of family finance

Charles Waldo Haskins

Follow this and additional works at: https://egrove.olemiss.edu/dl_hs

Part of the Accounting Commons, and the Taxation Commons

Recommended Citation Recommended Citation Haskins, Charles Waldo, "How to keep household accounts, A manual of family finance" (1903). Haskins and Sells Publications. 1693. https://egrove.olemiss.edu/dl_hs/1693

This Article is brought to you for free and open access by the Deloitte Collection at eGrove. It has been accepted for inclusion in Haskins and Sells Publications by an authorized administrator of eGrove. For more information, please contact [email protected].

H O W T O K E E P H O U S E H O L D A C C O U N T S A MANUAL OF FAMILY FINANCE

BY

C. W. HASKINS, L.H.M., C.P.A. Late Dean of the New York University School of

Commerce, Accounts, and Finance

NEW YORK AND LONDON HARPER & BROTHERS PUBLISHERS

1903

Copyright, 1903, by HARPER & BROTHERS. All rights reserved.

Published April, 1903.

TO MY DAUGHTER

R U T H I DEDICATE THIS LITTLE BOOK

PREFACE

T H I S little book is not a treatise on book-keeping. It is less, and it is

more. Far less, because it treats of but one of many thousand applications of that useful art; and more, because, beginning with the very simplest exposition of general principles, i t endeavors to unfold, as pleasantly as may be, a science of accountancy, and to indicate its relations, in the sphere of domestic economy, to finance, administration, and the other sciences of social life.

In view of the present unsatisfactory condition of instruction i n domestic accountancy, i t has been thought well to

v

PREFACE

employ, as far as possible, the historical method of teaching. The story form, i t is hoped, wi l l lend interest to the exploration of the field and to the laying down of the bases upon which the accountancy of the house is built.

Very little has been as yet written upon this important subject of household accounting. Especially is this true of books in our own language. To a few Italian, German, and French writers, however, a general acknowledgment is here due for material assistance in the effort to produce a manual of domestic money matters which may prove of practical uti l i ty in the administration of the modern home.

C O N T E N T S

CHAPTER PAGE

I. DOMESTIC ECONOMY 1

II. HOUSEHOLD ACCOUNTS 9

III. THE HOME ACCOUNT-BOOK. 34

IV. THE BALANCE-SHEET 57

V. BUDGET, VOUCHERS, AND INVENTORY . 66

VI. THE BANK ACCOUNT 91

HOW TO K E E P

H O U S E H O L D A C C O U N T S

THE oldest existing literary work on household management is the Eco

nomics of Xenophon. From this charming Greek classic—of which there are many good translations—we have our very words economy and economics; and for twenty-three hundred years it has held its own as the code, the breviary, the book of books, of all thrift. Aristotle adopted its title for one of his own treatises; Cicero made a Lat in rendering of i t

I

1

DOMESTIC ECONOMY

HOW TO KEEP HOUSEHOLD ACCOUNTS

in his youth; and the only other really great book on the same subject, the Italian Della Famiglia, was written i n imitation of it.

The Italian work, founded upon that of Xenophon, is variously ascribed to the celebrated architect Alberti, whose name is closely associated with that of Leonardo da Vinci , and to Pandolfini, another Florentine of the early Renaissance. It very closely follows its original, even to the incidents of the introductory prayer and the later advice to forego the use of face powders. It takes the young bride over the house; gives her the keys; teaches her the oversight of servants and the right ordering of all her affairs; makes honesty her chief virtue; inducts her into the science of family finance; i n a word, develops her from a shy girl, brought up i n careful seclusion, to the

2

DOMESTIC ECONOMY

perfect mistress of the household, and sets before us, in a well-drawn picture, one of the ideal characters of early Italian literature.

The Florentines became noted for their orderliness in the affairs of domestic economy; and when modern book-keeping, invented by a monk, was introduced into their household matters, the women we are told "are supposed to have been in this respect model helpmates to their husbands."

About twenty-five hundred books, in the English language alone, have been classed in one way or another under the general head of domestic economy. A very great number of them are handy collections of recipes of various kinds; many are books of practical advice to the members of the household; some are special discussions of the application of

3

HOW TO KEEP HOUSEHOLD ACCOUNTS

particular departments of human knowledge to family life; and others are commendable and often successful attempts to develop or elucidate one or more of the administrative functions of the housewife. A limited number of these books are of scientific aspect, and of the highest value within their sphere; and all, no doubt, would be of use in a scientific treatment of the whole subject. Were some genius, however, to erect, out of the mass of their material, a science of domestic economy having its own identity and its own broad comprehensiveness, a few staring gaps, it is feared, would be left in the superstructure. On the financial front, certainly, the absence of accountancy would be noticeable. To supply this lack is the object of the present volume.

Educational leaders and reformers in

4

DOMESTIC ECONOMY

various countries have endeavored, not wholly without encouragement and success, to introduce domestic economy into their national systems of instruction. As in the case of our literature of the subject, their actual teaching, thus far, has been largely confined to particular branches of housekeeping. Their profession, however, has induced a careful study of profound works on female education; has led them to a lively interchange of ideas; and has kept alive their scientific aspirations. Thus, aggressively, they have pushed on, enlarging and unifying their courses of study, until a few of them have gained for domestic economy a sort of permissive foothold on the lecture platforms of certain universities. Their programmes, if combined, - would suggest a consideration of the household, its moral, intellectual, social, and economic welfare,

5

HOW TO KEEP HOUSEHOLD ACCOUNTS

and its organization and general administration; woman, her sphere, her need of directive intelligence, and the education of girls; the house, its location with reference to business, health, economy, and general convenience, and its interior arrangement; heat, light, and ventilation; furniture, from the point of view of hygiene, art, and practical use, its disposition about the house, its freedom from dirt, and its repair and maintenance; carpets, draperies, and the like; clothing and toilet articles, their choice, cost, and care; foods, their varieties, succession by seasons, cost, use according to one's age, occupation, and condition of health, with rules for the detection of adulteration; care of the sick; and the advantages of keeping down expenses.

The high school for young women at Geneva teaches, both in its literary

6

DOMESTIC ECONOMY

department and in its pedagogical section, the principles of domestic economy, the rôle of the mistress, the need of professional teaching, care of furniture, clothing, linen, washing, light, heat, alimentation, provisions, accounts, budget of receipts and expenses, savings, and insurance.

A programme of domestic economy laid before a congress of educators at Brussels is of value for the prominence it gives to a suggested course of family finance, and is interesting for the place upon the faculty accorded to " L e Bon-homme Richard." Its concluding head is:

"Money and work. Receipts and expenses. How to make the most of one's knowledge and talents. Gaining and keeping, a double profit; temperance in the number of articles desired; how to buy; knowledge of the price of pro-

7

HOW TO KEEP HOUSEHOLD ACCOUNTS

visions, of cloth, of linen, of calico, of utensils, and the like. Avarice and prodigality. Accounts of the household. The memorandum-book and the monthly examination. The superfluous and the necessary. Buying on credit; danger of debt; honesty. Promptness in repairing or replacing articles broken, deteriorated, or worn out. The toilet. Luxury, good taste, and simplicity. The maxims of Benjamin Franklin, 'Poor Richard': wise employment of time. The habit of taking notes."

II

HOUSEHOLD ACCOUNTS

IT is clearly evident that domestic economy, or household manage

ment, is very largely a matter of money and money's worth, and that it marks out an important field of financial accountancy.

Nor is this financial aspect of the subject in any wise confined, as we are too apt to imagine, to that "exterior" department of administration which is today included under the head of political economy, or economics. All who have ever treated this phase of the subject have contended that finance and accountancy sustain important relations to wel-

9

HOW TO KEEP HOUSEHOLD ACCOUNTS

fare in the " interior" management, to which we now more particularly apply the term domestic economy, and which lies within the special province of the woman.

The story told by Josephus, and less fully by Esdras, of the Jewish captive who argued, in a prize essay read before Darius and his princes and grandees, that the care and preservation of all household business is dependent upon woman's administration, shows that such an argument could be understood and appreciated throughout the whole Persian empire, from India to the Danube.

To the Greek, as may be seen in X e n -ophon, the home interior was a department of economic administration, demanding of woman a very fair measure of business ability. Aristophanes, in his comic argument that women should be

10

HOUSEHOLD ACCOUNTS

also at the head of all outside affairs, says that they are already taking care of everything within, as, from the days of old, they have been always doing, and adds that for ways and means there's nothing cleverer than a woman; that as for negotiation, she's hard indeed to beat or cheat. A n d Aristotle, borrowing the time-worn figure of the Danaïdes, says that a domestic economy which does not join to the exterior talent for acquisition the interior one of managing and uti lizing, and especially of calculating expenses so that they shall not exceed the receipts, is like the sieve, or the bucket pierced with holes, with which one tries to carry water.

The Latins were a calculating, administrative people; and the matron of Rome, freer than her sister of Athens, and bearing undisputed sway in her household,

11

HOW TO KEEP HOUSEHOLD ACCOUNTS

guided her affairs frugally and with taste, and enriched the family treasury by her business-like activity and exactness.

The woman of the Middle Ages, whether lady of the manor, mistress of the city residence, or guardian of the humble cottage of the peasant, was remarkable for business ability. The Florentine imitation of the Economics of Xenophon, already referred to, was one of the most popular books of the Renaissance. A hundred years later, Olivier de Serres, a French writer on rural and household affairs, could still describe the mistress of the mansion as Xenophon had described her; and Montaigne, avowing that he had no concern with business, and was glad that "women do find delight in managing affairs," could safely relinquish to his wife the planting and reaping of his crops, the oversight of

12

HOUSEHOLD ACCOUNTS

his masons, the negotiating of bargains for him, the collection of debts due him, and the keeping of his accounts, while he, as one of his countrymen has said, "dawdled through Italy at his leisure."

Writing of woman's administration as understood in the sixteenth century, Montaigne says: " T h e most useful and honorable science and occupation for the mother of a family is that of domestic economy. I see many who are avaricious, but of real economists I find but few. This, indeed, is the mistress quality—the one that should be sought above all others, the dowry that wil l either ruin or save our establishments."

Sti l l later, two women, allied by marriage to the family of L a Rochefoucauld, gave to the seventeenth and eighteenth centuries examples of the wisest administration of extensive country and

13

HOW TO KEEP HOUSEHOLD ACCOUNTS

city establishments. The former, Jeanne de Schomberg, Duchess of Liancourt, drew up a scheme of administration in which we discover a broad conception of family finance; and the latter, Augustine de Montmirail, Duchess of Doudeauville, not only administered her own estate, but brought the large hereditary property of her exiled husband through the Reign of Terror, and "left the family of L a Rochefoucauld in the unusual position of landed proprietors when nearly all the French nobility were irretrievably ruined."

A close view of early domestic accounting may be had in many of the old "household books" of the women of England. " W e read," says an English writer, "of the abundant hospitality of the great houses of past days; but reference to books like those which record the

14

HOUSEHOLD ACCOUNTS

household expenses of Northumberland or the Countess of Hardwick show how carefully every expense was regulated by the heads of the family. The famous 'Bess of Hardwicke' was a careful housekeeper. 'Avoiding superfluities or waste of anything' is to be the rule of her establishment, as laid down in the household books which have come down to us; and it is curious, in perusing documents like these, to observe how careful our ancestors were to look into every trifle of their domestic expenditure."

What is still more curious, however, and worthy of all admiration, is the surprising perfection of result obtained with the very primitive appliances at their disposal. The books were hardly more than diaries; the entries were mere memorandums, and were written, for a long time, in a crabbed L a t i n ; and the

15

HOW TO KEEP HOUSEHOLD ACCOUNTS

amounts were expressed, up to a late period, in the old Roman numerals, sometimes in columns, oftener run in with the text, and almost impossible of addition except by a roundabout method of figuring or with the aid of the abacus, a device somewhat similar to the counting-frame of our kindergartens. So utterly unscientific, indeed, was the whole scheme, and so dependent upon contrivance for the accomplishment of any general result, that men of great reputation—as in the Rules of Saint Robert, " that the good Bishop of Lincoln, Saint Robert the Greathead, made for the Countess of Lincoln"—gave themselves up to the writing of chapters on " H o w you may know to compare the accounts."

The household book of the ducal family of Buckingham is written in the abbreviated Latin of the year 1507, the

16

HOUSEHOLD ACCOUNTS

numbers being expressed in Roman letters incorporated with the reading-matter. The following is one of the shorter paragraphs; it records the expenditure at Newbury for "the dinner of the Lord with his household; dined, gentry, twenty; valets, fourteen; garçons, twenty-nine":

Die D'nica XXXmo. die Janu. ib'm. Panet. ex it'm ex empcon. xxxiij pan. p'c.

xvjd. ob. Cellar. expend, it'm ex empcon. ij pich. vini

gasc. p'c. xvjd. Buttill. exp. it'm ex empcon. xv lag. cervis.

p'cii iijs. ixd. Coquin. exp. it'm ex empc. j qrt. carn. boum

p'cij iiijs. iiijd. vitul. p'c. ijs. viijd. Achates ex in ijb porcellis xijd. ij capon xiiijd.

ij cunictis xvjd. j curlew. vd. ix redshankes vjd. v disc. butir vd. ovis gallin. iiijd. herbis et farin. aven. ijd.

Aul. & Camer. ex. de fagottes xxviij. p'cij ijs. iiijd

a 17

HOW TO KEEP HOUSEHOLD ACCOUNTS

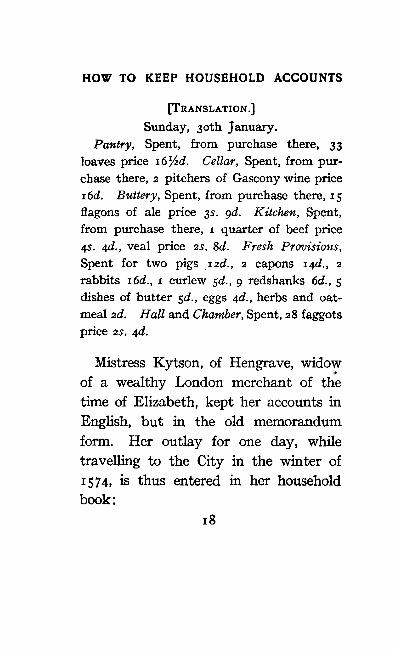

[ T R A N S L A T I O N . ]

Sunday, 30th January. Pantry, Spent, from purchase there, 33

loaves price 16½d. Cellar, Spent, from purchase there, 2 pitchers of Gascony wine price 16d. Buttery, Spent, from purchase there, 15 flagons of ale price 3s. 9d. Kitchen, Spent, from purchase there, 1 quarter of beef price 4s. 4d., veal price 2s. 8d. Fresh Provisions,

Spent for two pigs 12d., 2 capons 14d., 2 rabbits 16d., 1 curlew 5d., 9 redshanks 6d., 5 dishes of butter 5d., eggs 4d., herbs and oatmeal 2d. Hall and Chamber, Spent, 28 faggots price 2s. 4d.

Mistress Kytson, of Hengrave, widow of a wealthy London merchant of the time of Elizabeth, kept her accounts in English, but in the old memorandum form. Her outlay for one day, while travelling to the City in the winter of 1574, is thus entered in her household book:

18

HOUSEHOLD ACCOUNTS

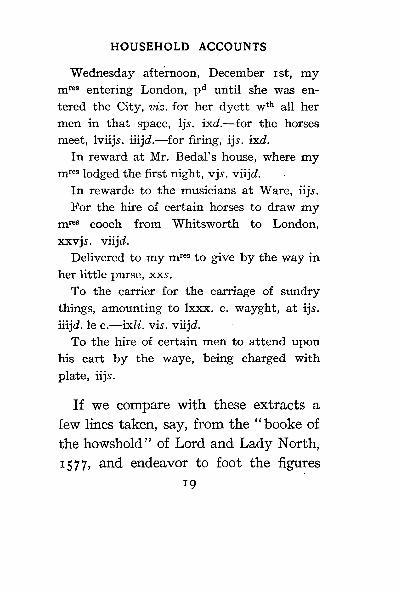

Wednesday afternoon, December 1st, my m r e s entering London, p d until she was entered the City, viz. for her dyett wth all her men in that space, ljs. ixd.—for the horses meet, lviijs. iiijd.—for firing, ijs. ixd.

In reward at Mr. Bedal's house, where my m r e s lodged the first night, vjs. viijd.

In rewarde to the musicians at Ware, iijs.

For the hire of certain horses to draw my m r e s cooch from Whitsworth to London, xxvjs. viijd.

Delivered to my m r e s to give by the way in her little purse, xxs.

To the carrier for the carriage of sundry things, amounting to lxxx. c. wayght, at ijs. iiijd. le c.—ixli. vis. viijd.

To the hire of certain men to attend upon his cart by the waye, being charged with plate, iijs.

If we compare with these extracts a few lines taken, say, from the "booke of the howshold" of Lord and Lady North, 1577, and endeavor to foot the figures

19

HOW TO KEEP HOUSEHOLD ACCOUNTS

up, we shall wonder why, unless in blind imitation of the new "Ital ian method," columns have been introduced at a l l ; and we shall admire the administrative mind that could base a budget upon a book containing " A " cartload, " 2 " horse-loads, and " v " livres in a single line:

Gammonds of bacon viij xxxs.

Larde xiij lbs viijs. viijd. Neats tongs,

feet, and uddrs xi**. i liijs. iiijd/.

Butter iiijC xxx lb vjli. vijs. vjd. Eggs ijM vC. xxij iijli. Hp.

Sturgeons iij caggs xlvjs. viijd. Craye fyshes viij doos xiijs. iiijd. Turbutts viij liijs. iiijd. Oysters A cartload and 2 horseloads. vli.

These were the accounts of the titled and the wealthy. The woman of hum-

20

HOUSEHOLD ACCOUNTS

bler condition, whose affairs were less complicated, had simpler methods.

A story is told of an old lady who kept her accounts in chalk on the back of her shop door, in a system known only to herself. She fell i l l , and her son came home to manage the shop until his mother recovered; but he did not understand her method of "booking." The result was that every time a customer came to settle up the son was compelled to unhinge the door and carry it up to his mother's bedroom, so that she might calculate the amount of the debt. He endured this for a day or two, and then gave the door a coat of paint, thus finally settling the accounts. The old lady declared, when she came down again, that by this action she lost nearly five hundred dollars.

But now comes an unexplained wonder; and it is partly on account of the exist-

21

HOW TO KEEP HOUSEHOLD ACCOUNTS

ence of this unique riddle of economic history that the narrative form has been thus far followed i n our attempt to instil into the mind of the reader the general principles of household accountancy. It must have been evident that we are dealing with a branch of human knowledge once and for long ages recognized and fully accepted as an important part of woman's education, but now, unfortunately, almost extinct. It creates, indeed, less surprise to-day to read that a woman of Babylon was a principal member of the great banking firm of that ancient city than it would to be told that a thoroughly modern lady of the United States had incorporated into her domestic administration a fairly comprehensive system of financial accounting. We have seen that accounting is an essential feature of domestic economy, that its func-

22

HOUSEHOLD ACCOUNTS

tions are embraced in the sphere of the woman, that her administrative ability requires it, and that for a long time she was identified with its application. Why, then, we are compelled to ask, and at what point in the world's history, did the woman of the household begin to lose interest in the science and practice of accounts? As early, at least, as the sixteenth century this falling away had become noticeable, and from that time on there is a general tone of regretful argument, instead of the old Xenophontean praise, in approaching the subject of household accounting.

While women of the type of Madame de Maintenon were looking after their home accounts, others, more susceptible of extraneous influences, were drawn into the swirl of a less practical life; and we read that the Précieuses— a nickname bestowed upon the somewhat finical la-

23

HOW TO KEEP HOUSEHOLD ACCOUNTS

dies of the early part of the seventeenth century—"left their servants' accounts unaudited that they might preach the doctrines of grace."

Sir Matthew Hale complains that in his time "the young gentlewomen think it disparagement for them to know what belongs to good housewifery or to practise it. They know," he says, "the ready way to consume an estate and to ruin a family quickly, but neither know nor can endure to learn or practise the ways and methods to save it or increase i t ; and it is no wonder that great portions are expected with them, for their portions are commonly al l their value."

It had become a maxim of the Dutch, however, that "no one is ever ruined who keeps good accounts"; and Mary Astell, an English reformer of the seventeenth century, could still recommend to her

24

HOUSEHOLD ACCOUNTS

countrywomen the example of the housewives of Holland, who, she writes, "keep the books, balance the accounts, and do all the business with as much dexterity and exactness as their own or our men can do."

To the amiable Fénelon, however, we must look for a picture of the real condition of things, as well as for an indication of the true line of reform. He and Madame de Maintenon complained that in their day few girls could cast up the simplest household accounts without falling into confusion; and while the prelate, in his classical work on female education, developed his theories, the court lady endeavored to apply them and to promulgate them by the example of her famous school of Saint-Cyr.

Fénelon thought that besides Latin, history, biography, travels, poetry, music,

25

HOW TO KEEP HOUSEHOLD ACCOUNTS

and art, a young woman should know something of law, trade, and manufacture, and should be taught the "minutest details of domestic economy." He prescribed for her a knowledge of the four rules of arithmetic, not that she might become a second Hypatia, but in order that she might keep the accounts of the household.

Miss Edgeworth, a century later, writing of economy as a domestic virtue, says that children must have the management of money, and that girls ought to keep the family accounts; and Mrs. Ellis, in one of her remarkable works on English women, dedicated to Queen Victoria, says that "married women who love justice to themselves as well as to others should always keep strict accounts."

Anne Cobbett, in her once popular work for English housekeepers, seems to

26

HOUSEHOLD ACCOUNTS

have in mind the comprehensive accountancy of the chatelaine. After referring favorably to her father's writings on cottage economy, she says: "One branch of domestic economy which devolves upon the mistress of a house is to keep an account of the expenditure of her family. She ought to make this as simple an affair as possible, by ascertaining, first, how much the housekeeping is to cost—that is to say, how much she can afford to expend in i t ; then, by keeping a very strict account of every article for the first two months, and making a little allowance for casualties, she may be able to form an estimate for the year; and if she finds that she has exceeded in these two months the allotted sum, she must examine each article, and determine in which she can best diminish the expense; and then, having the average of

27

HOW TO KEEP HOUSEHOLD ACCOUNTS

two months to go by, she may calculate how much she is to allow each month for meat, bread, groceries, washing, and the like. Having laid down her plan, whatever excess she may be compelled to allow in one month she must make up for in the next month.

" I should not advise the paying for everything at the moment," she writes, "but rather once a week; for if a tradesman omit to keep an account of the money received for a particular article, he may, by mistake, make a charge as for something had extra and upon trust. A weekly account has every advantage of ready money, and it saves trouble. I should recommend that all tradespeople be paid on a Monday morning, the bills receipted, . . . and put by in a portfolio or case where they may be easily referred to as vouchers, or to refresh the memory

28

HOUSEHOLD ACCOUNTS

as to the price of any particular article. It is a satisfaction, independent of the pecuniary benefit, for the head of a family to be able at the end of the year to account to herself for what she has done with the money."

The same attitude of entreaty is seen in the writings of the Americans. Our best-known work on domestic economy, for many years, was a treatise by Miss Catherine Beecher. " H o w few," she says, "keep any account at al l of their current expenses! If a woman," she again says, arguing for benevolence, "has never kept any accounts, nor attempted to regulate her expenditures by the right rule, nor used her influence with those that control her plans, she has no right to say how much she can or cannot do. Let a woman keep an account of all she spends for herself and her family for

29

HOW TO KEEP HOUSEHOLD ACCOUNTS

a year, arranging the items under three general heads. Under the first put all articles for food, raiment, rent, wages, and all conveniences. Under the second place all sums paid in securing an education, and books, and other intellectual advantages. Under the third head place all that is spent for benevolence and religion.

" A t the end of the year the first and largest account wil l show the mixed items of necessaries and superfluities, which can be arranged so as to gain some sort of idea how much has been spent for superfluities and how much for necessaries. Then, by comparing what is spent for superfluities with what is spent for intellectual and moral advantages, data wil l be gained for judging of the past and regulating the future."

A n d again, arguing on purely economic

30

HOUSEHOLD ACCOUNTS

grounds, Miss Beecher continues: "There are certain general principles which all unite in sanctioning. The first is that care be taken to know the amount of income and of current expenses, so that the proper relative proportion be preserved and the expenditures never exceed the means. Few women can do this thoroughly without keeping regular accounts. A great deal of uneasiness is caused to both husband and wife, in many cases, by an entire want of system and forethought in arranging expenses. Both keep buying what they think they need, without any calculation as to how matters are coming out, and with a sort of dread of running in debt all the time harassing them. Such never know the comfort of independence. But if a man and woman wil l only calculate what their income is, and then plan so as to know

31

HOW TO KEEP HOUSEHOLD ACCOUNTS

that they are all the time living within it, they secure one of the greatest comforts which wealth ever bestows, and what many of the rich who live in a loose and careless way never enjoy. It is not so much the amount of income as the regular and correct apportionment of expenses that makes a family truly comfortable.

" Y o u n g ladies also," she adds, "should learn systematic economy in expenses; and it wil l be a great benefit for every young girl to begin at twelve or thirteen years of age to make her own purchases and keep her accounts, under the guidance of her mother or some other friend. How strange it appears," she concludes, " that so many young ladies take charge of a husband's establishment without having had either instruction or experience in one of the most important duties of their station."

32

HOUSEHOLD ACCOUNTS

Thus we have shown that fireside accountancy rests upon moral as well as economic bases, and have indicated the character of these bases as viewed by those who have made domestic administration their study.

3

III

A C C O U N T I N G is commercial or noncommercial. Non - commercial ac

counting applies to the finances of those who do not make commerce, or buying and selling for profit, their habitual profession. Under this head are included the capitalist and all those who live on the labor of their brain and of their muscles. Household accounting is practically identical with that of the brain-worker and laborer. It is simple and elementary, and is properly introductory, in an educational sense, to capitalistic and commercial accounting and to all the higher developments of scientific ac-

34

THE HOME ACCOUNT-BOOK

THE HOME ACCOUNT-BOOK

countancy. B y a very pretty fiction of accountancy, the lady of the house may lead a son or daughter through all the experiences of an industrious and economical young man or woman who, from a wage-earner, becomes an investor and a leader of commerce and industry; and thus this domestic education wi l l lay the foundation for actual business life. This method is followed in several educational institutions in Europe.

For instance, the class is given the case of a poor young man who, having saved a little money, goes to town and finds employment as a laborer in the establishment of a merchant. His good conduct and intelligence are noted by his employer, who makes him his bookkeeper and salesman. His continued activity advances him in favor, and the merchant gives him his niece in marriage.

35

HOW TO KEEP HOUSEHOLD ACCOUNTS

Then, with his savings augmented with the dowry of his bride and the facilities of credit gained by his character, the young man enters mercantile life on his own account. Thus the student, accompanying a single individual through various conditions in life, sees how the simple accountancy of the laborer is transformed into that of the small capitalist; how, alongside of the latter, the accountancy of the merchant is constituted; and how both of these systems of accountancy, working side by side, establish the situation of the same individual as viewed in the double character of capitalist and merchant. Meanwhile, upon the simple accountancy of the young employe and that of his bride is formed the accountancy of the new domestic establishment.

The matron wi l l see, also, by this 36

THE HOME ACCOUNT-BOOK

illustration, that her own household accounting wi l l afford her an easy introduction to the care of money in bank or invested in securities, and that if thrown upon her own resources she wil l be able the more readily to adapt her methods to the administration of exterior business affairs.

We labor to satisfy our needs and to increase our hoard. Our labor is productive of these results, however, in proportion as it is well ordered; and it is by noting and writing down our dealings as regularly and methodically as possible that we are able, whether we belong to the commercial or the non-commercial community, to keep in touch with the progress and outcome of our affairs and to modify their direction to the best advantage.

Accountancy, which consists of a state-

37

HOW TO KEEP HOUSEHOLD ACCOUNTS

ment of receipts and expenses, is therefore the controlling record of exchanges; and the matron of the household, though not engaged i n the pursuit of commerce, is none the less continually effecting exchanges. She buys the goods or services of which her household is in need, and she settles with her dealers and her servants, on the spot or on time, in coin or bills. The family accounts may include the purchase of a piece of real or personal property, or a paper security, and the sale of i t at a loss or profit. A n d in all this buying and selling the economic aim of the household, as that of the business establishment, is to amass, year by year, a new capital—to save, to make, to become possessed of a part of the mass of social wealth.

In thus producing, exchanging, consuming, and saving, the household es-

38

THE HOME ACCOUNT-BOOK

tablishment, as well as a business concern, must call to its aid the science of accounts, in order, first, to follow the movements of its receipts and expenses; second, to keep track of its investments; and third, to determine, at the end of the year or other set period, the results of its operations and the exact situation of its capital.

Now, it is well known that any blank-book, ruled for dates, details, and dollars and cents, and exhibiting receipts on the left-hand page and disbursements on the right, is far better than nothing at all as a help to the memory. Indeed, the income and outgo of money are often thus inscribed on the back and front of the stubs of a check-book; so that, if al l receipts have been deposited in the bank and all expenses have been taken therefrom, the stub-book is left

39

HOW TO KEEP HOUSEHOLD ACCOUNTS

as a chronological record of cash movements.

A series of ordinary expense books, though cumbersome, are of some assistance in keeping control of the cost of conducting the different departments of the home establishment; and the passbooks of the grocer and other dealers, and miscellaneous receipted bills, are not wholly useless as accounting appliances even in the most hand-to-mouth administration. A miniature set of commercial books, consisting of ledger, cash-book, and journal, is now and then seen in the home, and would seem to have been heretofore needed wherever credit transactions have occurred.

A convenient form for a very simple household cash-book, in which entries, both of receipt and expense, are confined to one page, is shown in example A :

40

T H E HOME ACCOUNT-BOOK

1903

Jan.1 " 2

" 3

" 5 " 7

" 8

P A R T I C U L A R S

Cash in hand Wood and oil Bread Ribbon Bread Potatoes Provisions Dry-goods Washing Mending Bread Salary Cloak Underwear Rent Paid grocer Paid butcher Fares and sundries..

(Balance $39.15)--

5 0 . 0 0

40.00

$120.00

EXAMPLE A 41

D A T E S R E C E I V E D P A I D

$1.20

.80

.90

.80

2.00

.65

3.50

2.00

.75

.95

8.00

3.50

40.00

10.80

3.50

1.50

$80.85

HOW TO KEEP HOUSEHOLD ACCOUNTS

In example B it wil l be noticed that the simple plan is carried a step further, making it even more convenient.

But what is really needed, and the want of which has been a source of increasing discouragement in home management during the centuries in which modern accountancy has been industriously fitted to the varying forms of counting-house administration, is a system of household accounting that shall be at once comprehensive in scope and aim, and easy to work and to interpret. A n d to meet these requirements a single register, scientifically arranged as wil l be described, is sufficient.

The method recommended wil l be understood from the following model and a few words of explanation. It meets the requirements already specified, establishes the balance-sheet of the family and

42

DATES OF RECEIPTS

AND E X P E N D I

T U R E S

RECEIPTS

N A T U R E OF CASH E X P E N S E S

CASH E X P E N S E S DATES OF RECEIPTS

AND E X P E N D I

T U R E S SOURCES OF INCOME SUMS

N A T U R E OF CASH E X P E N S E S

SUMS DAILY TOTALS

1903 Jan. 1

2

Cash in hand $80.00 1903

Jan. 1 2

$80.00 Wood and oil Bread

$1.20 .80

$2.00

" 3 Ribbon Bread Potatoes Provisions

.90

.80 2.00

.65 4.35

" 5 Dry-goods 3.50 3.50

" 7 Washing Mending Bread

2.00 .75 .95 3.70

" 8 Salary. . . . . . . . 40.00 Cloak. 8.00 40.00 Underwear Rent Paid grocer Paid butcher Car-fare and sundries .

3.50 40.00 10.80

3.50 1.50 67.30

Total $120.00 (Balance $39.15) . . . $80.85

EXAMPLE B

THE HOME ACCOUNT-BOOK

constitutes, as it were, the financial history of the household. It enables the matron to keep a complete and exact account of her domestic operations.

Household receipts, independently of gifts and inheritances, consist of wages, salaries, allowances, fees, profits, rents, dividends, interest, and the like, and may be entered in the register merely as items of cash brought in by this or that member of the family.

Household expenses are composed of purchases of articles for consumption— such as food, raiment, fuel, and amusements; or of remuneration, as for service, instruction, rent, insurance, transportation; or of purchases of durable utilities, such as tools, pictures, books, furniture, real estate; or of investments of money in enterprises or in securities.

The receipts and expenses do not al-

43

HOW TO KEEP HOUSEHOLD ACCOUNTS

ways, however, exhibit this variety. In the larger number of households a saving —that is, an excess of receipts over expenses— is obtained only by a careful cutting off of the superfluous, by a wise employment of the necessary, and by the utmost order and economy in the domestic management. Those who impose this line of conduct upon themselves, and follow it persistently, create a capital which, in time, adds an interesting column to their scheme of accounts.

Receipts represent a simple account. Expenses represent another simple account. These together form a true accountancy, as has been stated, which, however rudimentary, may register three kinds of result. First, if the expenses are more than the receipts, either by the insufficiency of the latter or because the household has been improvident and

44

THE HOME ACCOUNT-BOOK

prodigal, not only is there nothing left at the end of the period, but, having lived upon credit—that is, upon the capital of others—the household has contracted debts, and this wi l l be expressed by the debit balance upon closing the annual account. Second, if the expenses exactly balance the receipts, the money has merely passed through the establishment; nothing remains at the end of the year; and this fact wi l l be shown upon closing the annual account. Third, if the receipts exceed the expenses, a surplus has been created, a capital remains in the possession of the household; and this is expressed by the credit balance appearing upon closing the annual account.

The books necessary for household accounts, as well as for business accounts, are the journal and ledger, and, in addition, the balance-sheet. But as the

45

HOW TO KEEP HOUSEHOLD ACCOUNTS

household journal is a mere record of movements of cash, it is practically reduced to a simple original cash-book. As for the ledger, it is limited to the credit accounts of a few dealers, together with a classified statistical display of expenses, which display, after a time, wi l l furnish the means of comparison by which to regulate future expenses. Thus the cash journal records the dates and amounts of all moneys received or paid out; the ledger records the same transactions, which have been transferred to it from the cash journal, each item being placed under its proper account whether of a person or thing. A n d still further to simplify this rudimentary accountancy, the two books may be fused into a single journal-ledger, in which the receipts and expenses day by day are seen at a glance. This view indicates

46

THE HOME ACCOUNT-BOOK

by dates, throughout the period, all receipts and their sources; al l cash and credit purchases; detailed sums of all cash expenses; daily totals of cash expenses; al l credit transactions with dealers; statistics, according to kind, of all articles bought on time and for cash, and daily totals of entire outlay; so that the whole financial situation of the household may be definitely determined at the end of a set period or at any other time.

A view of the accompanying model wil l show the use to which the various divisions of the journal-ledger are devoted. The left-hand page of the book is the journal, which, in the accountancy of the household, as we have seen, is reduced to little more than a cash-book. The right-hand page is the ledger, carrying the accounts of persons and of things.

Beginning on the left of the left-hand

47

HOW TO KEEP HOUSEHOLD ACCOUNTS

page, the first column is reserved for the dates of the entire record on both pages.

The second column indicates the sources of the receipts. Whether receipts shall be traced to their outside sources, as wages, fees, and other specified earnings, or merely recorded as coming from the different members of the household into the hands of the matron, wil l depend upon the stand-point she may choose to occupy as keeper of the accounts.

In the third column are inscribed the sums of the receipts and the cash in hand at the beginning of the period. This column should be totalled up at least once a week.

The fourth column is devoted to a chronological record of the nature of all purchases. It is essential that this indication of kinds of goods bought should

48

1903 Jan. 1

2

RECEIPTS

Cash in Hand.

Salary

Total

SUMS

$8o.oo

40.00

$120.00

N A T U R E OP CASH AND CREDIT E X P E N S E S

Meat Wood and oil. Bread Groceries

Ribbon . . . Bread.... Beef Potatoes . . Provisions

Dry-goods

Groceries.

Washing Mending Mutton . Bread.. .

Cloak Underwear

Sugar Rent Paid grocer Paid butcher Car-fare and sundries.

(Balance $39.15) . . .

CASH E X P E N S E S

$1.20 .80

.90

.80

2.00

.65

3.50

2.00

•75

.95

8.00

3.50

40.00 10.80

3.50 1.50

DAILY TOTALS

$2.00

4.35

3.50

3.70

67.30

$80.85

CREDIT E X P E N S E S

$10.80

$10.80

$6.50

3.50

.80

$10.80

$3.50

$3.50

$ 1 . 0 0

$3.50

$1.00

.80 6.50

.80

1.35 2.00

.65

3.50

1.15 .95

.80

$19.50

$ .90

3.50

8.00

3.50

$15.90

LIG

HT

, H

EA

T,

WA

SH

ING

, M

EN

DIN

G

$1.20

2.00 •75

$40.00

$1.50

$3.95 $40.00

MODEL OF THE HOME ACCOUNT-BOOK

DA

TE

S

OF

R

E

CE

IPT

S

AN

D

EX

PE

ND

ITU

RE

S

" 3

" 5 " 6

" 7

" 8

SOURCES SUMS

GROCER

DR. CR.

B U T C H E R

DR. CR.

FO

OD

CL

OT

HIN

G

PL

EA

SU

RE

A

ND

M

ISC

EL

LA

NE

OU

S

RE

NT

, T

AX

ES

DA

ILY

T

OT

AL

S

OF

E

NT

IRE

E

X

PE

ND

ITU

RE

$9.50

5.70

3.50

3.50

4.85

53.80

$80.85

1.35

THE HOME ACCOUNT-BOOK

be explicit, so as to furnish the information required for the statistical columns which follow on the ledger side; but to avoid the multiplication of detail, the entries here may be under somewhat general heads, and the particulars may be kept in the butcher's and grocer's passbooks or in a rough memorandum-book of daily expenses. The two following columns carry, i n the one the detailed figures of the cash expenses, and i n the other the daily totals of the same expenses. A t least once a week the cash outlay should be totalled up and compared with the total receipts, and the balance, as found by the book and verified by actual count of money in hand, may be set down within brackets in the fourth column, as shown in the model. It wi l l be better still if this balance in hand be figured up and verified daily.

4 49

HOW TO KEEP HOUSEHOLD ACCOUNTS

Credit purchases as well as cash purchases are described in the fourth column, but their figures are carried forward to the credit columns of the dealers— that is to say, to the columns in which are placed all amounts due the dealers; and thus the housewife has, day by day, a view of her entire cash and credit expenses. The number of credit accounts, of course, is optional. Each dealer has a debit and a credit column. When the payment, or a part payment, is made, it is described in the fourth and the amount is entered in the fifth column as a cash expense, and the amount of payment is also entered in the debit column of the dealer—that is to say, in the column which records the amounts paid the dealer. When the columns of the dealers are footed up, if a debit column does not amount to as much as the adjoining

50

THE HOME ACCOUNT-BOOK

credit column, the difference is the amount due the dealer.

Following the accounts of the dealers on the ledger page are several columns exhibiting together a daily statistical abstract of al l expenses. This abstract is merely a classified repetition of the entries already made, and must agree in its collective total with the combined totals of the cash and credit expense columns on the journal, or left-hand, page. It must be remembered, however, that as credit expenses have been carried into these statistical columns from the credit columns of the dealers, they must not be again brought forward from the debit columns of the dealers, or from the cash column on the journal page, when the payments are made.

The statistical columns enable the

housewife to make constant comparison

51

HOW TO KEEP HOUSEHOLD ACCOUNTS

of the cost of the living departments with one another and with her income; to make necessary modifications; and to regulate, at the end of any period, her budget for the ensuing period. The number of these columns is optional, depending upon the variety of statistical information desired.

Mrs. Ellen Richards, an American authority on the cost of living, has suggested a number of budgets under the following five general heads: first, food; second, rent; third, operating expenses, wages, fuel, light, and so on; fourth, clothes; fifth, higher life, books, travel, church, charity, savings, insurance. On the other hand, in a table of actual family expenses, the same lady uses twenty-eight general heads of outlay. The simple distribution adopted in the model wil l be sufficiently elaborate for a modest be-

52

THE HOME ACCOUNT-BOOK

ginning; and the housewife may set off other columns, as desired, at the beginning of any new period.

When, by industry and economy, and by order therein, a capital shall have been saved that may be invested in anything of permanent value, such as furniture, pictures, books, etc., a column may be set apart from the miscellaneous column for the record of such transactions. This wil l lead, by an easy gradation, to the establishment of a capitalistic accountancy; an accountancy of the second degree, whose twofold mission is, first, to render account of current receipts and expenses; and, second, of a capital amassed and successively modified. A t first, however, it wil l be well to become thoroughly familiar with the simpler form by carrying all unusual items into the miscellaneous column.

53

HOW TO KEEP HOUSEHOLD ACCOUNTS

The final column receives the entire daily total of cash and credit expenses. It should be footed up weekly. It must always agree with the sums shown by the statistical columns. It must also agree with the combined sums of the credit columns of the dealers and the cash column of expenses, minus the payments to dealers, as already explained. It wil l agree with the cash expense column alone, if the dealers have been fully paid; if not, the difference will show the entire amount remaining unpaid.

Thus we see that the administrator of the household affairs, by means of this simple series of concurrent columns, may know from day to day: first, from the cash balance, her pecuniary situation with reference to herself; second, from the accounts of the dealers, her pecuniary situation with reference to her creditors;

54

THE HOME ACCOUNT-BOOK

third, her daily cash expense; fourth, her total current cash and credit expense; fifth, from the statistical columns, the current cost of each department. The columns should be totalled each week.

The entries for each week follow without break the totals as shown under the preceding week, so as not to interrupt the addition of the columns. On the last day of December the total of the cash expense column indicates the annual cash outlay; the columns of the dealers show the full yearly amount of debt incurred and the full amount paid in settlement; and the final column presents the grand total of the cost of the household, cash and credit, for the year. On the first of January, or the day following the close of the old period, the journal-ledger is again opened, for the ensuing period, with the cash in hand entered as before,

55

HOW TO KEEP HOUSEHOLD ACCOUNTS

and with any balance that may still be due to a dealer entered in his credit column.

All these financial details the housewife must know, in order that she may regulate her administration intelligently, that she may economize methodically, and that she may constitute a savings fund and direct that fund in the way of increase.

IV

THE BALANCE-SHEET

IT is at this point, when the accounts of a period are closed and those of

the following period are opened, that the financial condition of the household is recorded on the balance-sheet. This closing and opening of the accounts in no wise interferes with the movement of affairs; and the balance-sheet is but a kind of instantaneous photograph of the status of the business at the chosen moment, showing how the situation compares, on the one hand, with a former condition, and, on the other, with the ideal in the mind of the administrator.

In form, a balance-sheet, as its name 57

HOW TO KEEP HOUSEHOLD ACCOUNTS

implies, is a sheet of balances. In the complicated accountancy of modern commerce and finance, it is the result of much labor expended in centralizing the figures of a more or less extensive system of books of account. Its appearance is often awaited with anxiety, and its contents are studied with care by the stockholder, the bondholder, the manager, the competitor, and the political economist.

In the accountancy of the household, however, the balance-sheet is a much simpler affair. The journal-ledger here recommended affords a ready view of the situation from day to day; while the weekly or monthly balancings, appearing at a glance in one short, horizontal row of figures, are a kind of periodical review; and thus, in this progression of the whole record together, the housewife has a complete history of her conduct of

58

THE BALANCE-SHEET

affairs. But for permanent comparison of the results of her administration, it is convenient to make a division of time into periods of uniform length and character, and to sum up the results of each period and record them by themselves. The natural uniform period is the year; and the form in which the results of the period are brought together for convenient reference and comparison is the balance-sheet.

Three kinds of result, as already noted, are possible: the income may have been insufficient, or just enough, or more than enough, to meet the expense. We may apply these three results to the accountancy of a young couple who, let us say, open their book of financial record on January 1, 1902, with $80 cash in hand. The first year, besides the $80 entered on the 1st of January, there is

59

HOW TO KEEP HOUSEHOLD ACCOUNTS

an income of $40 a week for fifty weeks— two weeks having been lost in one way and another—being a total of receipts of $2,000 + $80 = $2,080. Their expenses, by reason of their want of experience in the practice of economy, and because of their early need of household effects, have reached the sum of $2,300, leaving a deficit of $220, of which $70 are due to the butcher and $150 to the grocer. To express, at the close of the year, this result in a methodical manner, they prepare their simple household balance-sheet, dated December 31, 1902, based upon the following facts as shown by their journal-ledger:

Their cash income, including the cash in hand at the beginning of the period, has given them $2,080, and the grocer has loaned them $150 and the butcher $70 worth of goods, making in all $2,300

60

THE BALANCE-SHEET

to meet a total expense of $2,300, $220 of which is an indebtedness which they will carry over to the credit of the grocer and butcher when the accounts are reopened. This situation is expressed in tabular form as follows:

DECEMBER 31, 1002 DR. CR.

Cash resources $2,080

150 70

Balance due on credit purchases:

Grocer

$2,080

150 70 Butcher

$2,080

150 70

Expenses for the year Totals

$2,300

$2,080

150 70

Expenses for the year Totals $2,300 $2,300 $2,300 $2,300

HOUSEHOLD BALANCE-SHEET EXPRESSING A DEFICIT.

The table given above may be inscribed in any convenient place, say near the end of the journal-ledger; and on the first day of January, 1903, the

61

HOW TO KEEP HOUSEHOLD ACCOUNTS

journal-ledger is reopened with the $70 carried to the credit of the butcher and the $150 carried to the credit of the grocer.

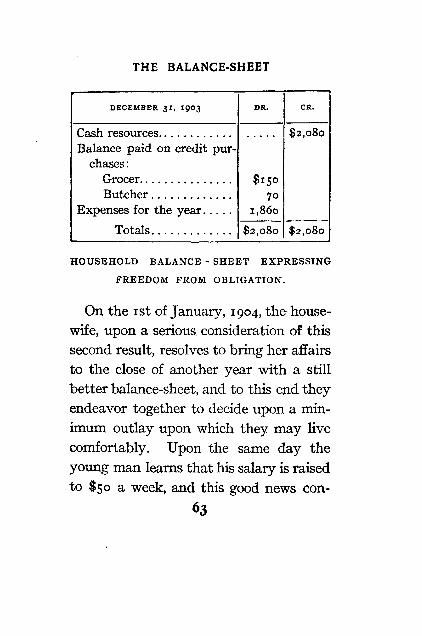

The second year a total of $2,080, being $40 a week for the full fifty-two weeks, is earned and entered in the cash receipts. An examination of the statistical columns has shown the young housewife that money has been spent in one or two of the departments which might have been saved; and this second year she has not only paid off the debt of $220 to the butcher and grocer, but has kept her running expenses down to the $1,860 remaining of the $2,080, thus equalizing the receipts and expenses. At the close of the second year, therefore, she is in a position to prepare a balance-sheet expressive of freedom from obligation:

62

THE BALANCE-SHEET

DECEMBER 31, 1903 DR. CR.

Cash resources $2,080

Balance paid on credit purchases:

Grocer $150

70

1,860

$2,080

Butcher Expenses for the year

Totals

$150

70

1,860

$2,080

Butcher Expenses for the year

Totals $2,080 $2,080

HOUSEHOLD BALANCE - SHEET EXPRESSING

FREEDOM FROM OBLIGATION.

On the 1st of January, 1904, the housewife, upon a serious consideration of this second result, resolves to bring her affairs to the close of another year with a still better balance-sheet, and to this end they endeavor together to decide upon a minimum outlay upon which they may live comfortably. Upon the same day the young man learns that his salary is raised to $50 a week, and this good news con-

63

HOW TO KEEP HOUSEHOLD ACCOUNTS

firms them in their projects of economy. The income during this third year is $50 x 52 = $2,600, while the expenses are $2,025. Thus there is a cash balance at the end of the year of $575, and the new balance-sheet shows the young domestic economist is now prepared to add to her household accountancy the further feature of capitalistic accountancy:

DECEMBER 31, 1904 DR. CR.

Cash resources $2,600

Totals

$575 2,025

$2,600

Totals $2,600 $2,600 $2,600 $2,600

HOUSEHOLD BALANCE - SHEET EXPRESSING

POSSESSION OF CAPITAL.

It ought here to be again noted that the simple journal-ledger contains in itself all the accounts of the household.

64

THE BALANCE-SHEET

The balance-sheet, valuable for purposes of administration and the full expression of the financial situation, can be made up at any time for any past period or series of periods, and need not give the housewife any concern for at least a year after the first opening of her journal-ledger.

This journal-ledger may be any wide-paged blank-book, in which she may rule off her columns a couple of pages at a time as wanted; and the ruling, it need hardly be said, may be with pencil or with pen and ink, and with or without all the captions fully expressed as in the model.

It cannot be too strongly emphasized that the entire value of the book rests upon a recognition of the absolute need of order and method in the financial administration of the modern household; that is, that the whole question is first and last a matter of business,

5 65

V

BUDGET, VOUCHERS, AND INVENTORY

THE budget, though one of the most important features of the matron's

administration, and the twin-sister, we may say, of her accountancy, is not to be considered as in any way affecting the completeness of the subject as already viewed. And so with the voucher; and so, also, with the inventory. All these are of greater or less importance; but, with or without them, the journal-ledger embraces the entire movement, the balance-sheet records the exact situation, and whatever is more is, at most, only of correlative value to accountancy.

66

BUDGET, VOUCHERS, AND INVENTORY

THE BUDGET

The budget has been often called "the prospective balance-sheet." We have seen that the statistical columns of the journal-ledger are for the purpose of distributing or classifying the household purchases according to the nature of the articles bought, and that the number and headings of these columns are dependent upon the variety of information the matron may desire thus to preserve. She may have a special reason for wishing to know just how much money she is spending on some particular object in which another household might not be interested, and to this end she can mark off a column in which to carry the cost of each purchase of this article; and so on.

But the principal use of this information is to furnish a basis for estimating

67

HOW TO KEEP HOUSEHOLD ACCOUNTS

the cost of maintaining the household in the immediate future. This estimate is known as the budget, so called from the bag or budget of financial estimates laid before the British House of Commons by the Chancellor of the Exchequer.

"And let us not deceive ourselves," says Louise d'Alq, in La Maîtresse de Maison; "many a household has quite as much trouble as certain ministers, and much more, to attain this object of establishing its budget of receipts and expenses; for it cannot have recourse, as they can, to forced loans and other arbitrary sources of income."

The household budget, or statement of the probable revenue and expenditure of the establishment for the ensuing period, is the result of a careful comparison of what is wanted or desired with what can be attained. "The budget is born," said

68

BUDGET, VOUCHERS, AND INVENTORY

a noted French journalist, "of the imperious necessity for an equilibrium of receipts and expenses." There must be, first of all, an approximately correct notion of the amount of income from which the expenditure may be drawn; and within this limit—by reason, indeed, of the limitation itself—there is ample room for the fullest exercise of woman's ingenuity and judgment in arriving at a well-proportioned estimate of expenses. In this work, the one indispensable ally of the matron will be the statistical department of her journal-ledger. Her accountancy will unite the past to the future of her finances, and her household budget will be the connecting link between this accountancy and her active administration.

A few general considerations, founded upon a study of many budgets, will not,

69

HOW TO KEEP HOUSEHOLD ACCOUNTS

it is hoped, be out of place. This study, it must be admitted, like that of the more elementary household accounting upon which it is founded, has not, in our modern civilization, gone very deep or very far. The commissioner of labor of the United States has tabulated the average percentages of various expenses to income of a number of families engaged in the iron, coal, glass, cotton, and woollen industries. Dr. Engels, head of the Prussian royal bureau of statistics, has published a series of studies on family budgets; Ellen Richards, to whom reference has already been made, has instituted inquiry in the same line of research; and a number of valuable articles have been contributed to various periodicals on the same subject. And thus it will be seen that a beginning has been made, and that "it is for those educated

70

BUDGET, VOUCHERS, AND INVENTORY

persons with one thousand to three thousand dollars annual income to lead the way in the studies necessary to be undertaken before any authoritative statements can be made."

The Bulletin of the International Institute of Statistics has printed a formulation of four laws by Dr. Engels, which have been pronounced by other statisticians to be "absolutely exact." These laws, the result of observation, are expressed in the language of mathematics; the drift of them is: first, that as income increases, the smaller is the relative percentage of outlay for food; second, that the outlay for clothing maintains a constant proportion to the whole; third, that the percentage of the outlay for shelter, and for heat and light, is the same, whatever the income; and fourth, that the percentage of outlay for sun-

71

HOW TO KEEP HOUSEHOLD ACCOUNTS

dries (expressing the degree of prosperity) increases as income advances. A concluding observation is, that the less a household earns the greater is the proportion expended for nutriment, whatever else may have to be renounced.

The Prussian statistician estimates that, taking one country with another, a poor family, with an income of a dollar a day for the working year of three hundred days, will expend on an average $186 for food, $36 for rent, $15 for light and heat, $48 for raiment, and $15 on the higher life. A modest household, dependent upon one of the industries selected by the commissioner of labor for comparison, and having a total of receipts of $1,000 a year, lays out $343.40 for food, $149.60 for rent, $40 for fuel, $7.40 for light, $168.40 for clothing, and $291.20 for all other purposes.

72

BUDGET, VOUCHERS, AND INVENTORY

A very common American budget is that of a household of four adults and two children, who, with an income of $2,000, spend $726 for nutriment, $484 for shelter and car-fares to and from place of business, $418 for light, heat, service, and other operating items, and $372 for clothing, education, amusements, benevolence, savings, and the higher life generally; in contrast with which Mrs. Richards has suggested, for the same income, a distribution of $500 for food, about $400 for rent, about $300 for service, light, fuel, and other operating expenses, about $400 for raiment, and $400 for the higher life, books, travel, church, charity, savings, and insurance; while Miss Florence Stacpoole, an English lecturer and writer on domestic economy, recommends to her countrywomen, for the same total outlay, $300 for rent, $835 for housekeeping,

73

HOW TO KEEP HOUSEHOLD ACCOUNTS

$200 for service, $80 for heat and light, $225 for dress, and $360 for education, amusements, sickness, and incidentals. It will be remarked that if these amounts are reduced to percentages, a very wide latitude is seen in the proportioning of expenses; food, for example, ranging all the way from 62 down to 25 per cent. This may be partially attributed to economic differences between Great Britain and America.

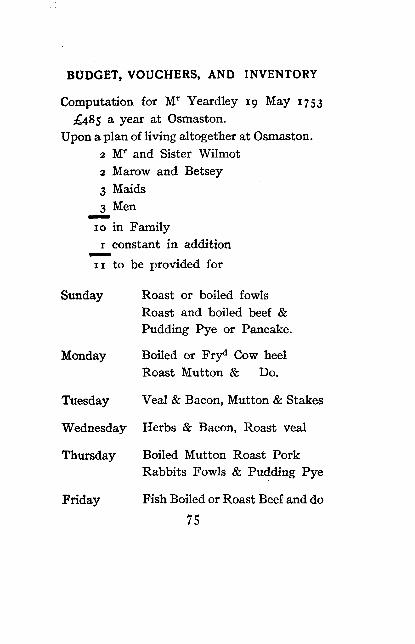

The following interesting budget, the original of which is preserved at Osmas-ton Hall, Derbyshire, England, will show that the latter percentage for food was considered fair in the middle of the eighteenth century; though to produce this proportion we must leave out of the 25 per cent. the beer and liquors, the cows, and the board of the boys at school:

74

BUDGET, VOUCHERS, AND INVENTORY

Computation for M r Yeardley 19 May 1753 £485 a year at Osmaston.

Upon a plan of living altogether at Osmaston. 2 M r and Sister Wilmot 2 Marow and Betsey 3 Maids 3 Men

10 in Family 1 constant in addition

11 to be provided for

Sunday Roast or boiled fowls Roast and boiled beef & Pudding Pye or Pancake.

Monday Boiled or Fryd Cow heel Roast Mutton & Do.

Tuesday Veal & Bacon, Mutton & Stakes

Wednesday Herbs & Bacon, Roast veal

Thursday Boiled Mutton Roast Pork Rabbits Fowls & Pudding Pye

Friday Fish Boiled or Roast Beef and do

75

HOW TO KEEP HOUSEHOLD ACCOUNTS

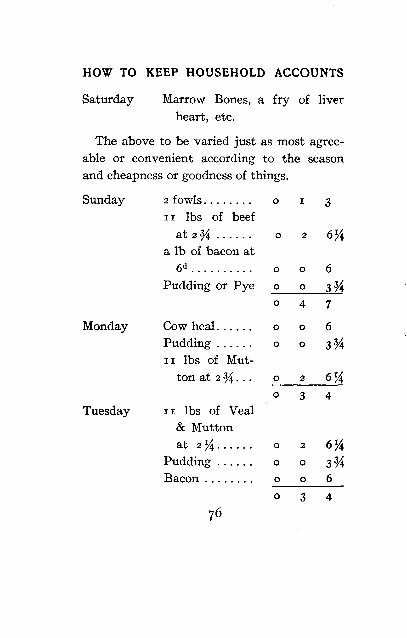

Saturday Marrow Bones, a fry of liver heart, etc.

The above to be varied just as most agreeable or convenient according to the season and cheapness or goodness of things.

Sunday 2 fowls 11 lbs of beef

at 2 ¾

a lb of bacon at 6 d

Pudding or Pye

0 I 3

0 2 6¼

0 0 6 0 0 3¾ 0 4 7

0 0 6 0 0 3¾

0 2 6¼ 0 3 4

0 2 6¼ 0 0 3¾ 0 0 6 0 3 4

Monday Cow heal Pudding 1 lbs of Mut

ton at 2 ¾ . . .

Tuesday 11 lbs of Veal & Mutton at 2 ¼

Pudding Bacon

76

BUDGET, VOUCHERS, AND INVENTORY

77

Wednesday

Thursday

Friday

Saturday

Bacon 11 lbs of Veal Pudding

11 lbs of mutton or pork

Pudding Rabbits

Fish removed with chickens

11 lbs of Beef Pudding

Marrow Bones. Fry Pudding

11 lbs of butter a week at 6 d

Bread and Muffins Salt Vinegar & pepper oyl ... Cheese

0 0 6 0 2 6¼ 0 0 3¾ 0 3 4

0 2 6¼

0 0 3¾ 0 I o

0 3 10

0 2 6 0 2 6¼ 0 0 3¾ 0 5 4

0 0 6 0 1 6 0 0 6 0 2 6 I 6 3 0 5 6 0 7 0 0 2 3 0 I 0 2 2 0

HOW TO KEEP HOUSEHOLD ACCOUNTS

78

Two guineas a week amount to

Strong beer, small beer, or ale.. Wine Spirits Coals Soap, candles, blacking Tea, chocolate, coffee, rice Sugar for tea and house 3 maids wages 3 mens wages and liveries Sister Wilmots Cloathes and pin

money Marow Do Betty Gardeners [2] 3 Boys at School £30 M r Yeardley 4 horses £40 coach tax and re

pairs 2 Cows etc

109 4 0

3 ° 0 0

15 0 0

10 0 0

12 0 0

12 0 0

6 0 0

7 0 0

10 0 0

25 0 0

20 0 0

10 0 0

10 0 0

13 0 0

90 0 0

50 0 0

10 0 0

5 16 0

£ 4 4 5 0 0

Balance over £40.

BUDGET, VOUCHERS, AND INVENTORY

These budgets emphasize the permanence of certain wants, and indicate the few statistical columns to which the inexperienced housewife may confine her distribution of expenses. A matron who should begin with a record of outlay for shelter, for general operation of the house, for nourishment, for dress, and for sundries, might have occasion, in the course of years, to set off particular columns for board, meat, groceries, medicine, the doctor, the lawyer, servants, "travelling, local car-fares, amusements, books, periodicals, papers, furniture, taxes, interest, insurance, stable, charity, education, laundry, music, water, repairs, milk, ice, and the private expenses of the sons, of the daughters, and of monsieur and madame.

But, in the main, the reasoning of the domestic economist will be that we must

79

HOW TO KEEP HOUSEHOLD ACCOUNTS

eat and drink, wear clothes, have a roof over our heads, pay for service, educate the young, look after the general comfort and well-being of the household, and save what we may, conveniently, out of our income. And nothing, it may be said, will require more careful consideration—will more clearly reveal the character of the mistress of the home, or repay her with greater results—than the production of a well-balanced and economical budget founded upon well-kept accounts.

THE VOUCHER

The voucher is a written evidence of payment, and, as we have seen in the administration of the chatelaine and the recommendation of modern writers, it ought as such to be preserved.

The voucher is of threefold value—ac-80

BUDGET, VOUCHERS, AND INVENTORY

counting, administrative, and legal. A complete series of vouchers would alone constitute a reliable though clumsy record of expenses. But, as in the case of the check-book used for a cash-book, this is not the primary object of the voucher; nor does accountancy depend upon any such secondary employment of borrowed appliances.

In the organization of extensive enterprises, the idea of the voucher includes all kinds of interior documentary authority for payment, as well as exterior evidence of it; and as labor is more and more divided in these vast concerns, the voucher becomes of greater importance and variety. But, as Eugène Léautey, author of La Science des Comptes, has said, "we must admit that in the accountancy of simple individuals the need of classifying all vouchers as

6 81

HOW TO KEEP HOUSEHOLD ACCOUNTS

supports for the movements of money is much less rigorous than in mercantile and industrial accounting." The matron of the household will find her receipts, receipted bills, dealers' passbooks, letters of acknowledgment, and the like, useful as memoranda when making up her accounts, and legally valuable as vouchers in case of dispute, and may be content merely to keep them for a reasonable while in some handy way of reference, and then either to get rid of them or store them away in packages.

THE INVENTORY

The inventory, if kept at all, will take form according to its intended use. It may be a simple list of household goods, made up either with or without order; it may be either without valuation, or priced according to cost, or according to

82

BUDGET, VOUCHERS, AND INVENTORY

some notion of present worth; and it may be kept entirely apart by itself, or the money value may be entered, either as a total or as several sub - totals, in the accounts. Such entry, to keep the accounts in balance, can be made, with accompanying explanation, as cash received and cash expended for the goods, and thus the household effects will obtain representation.

But as no practical purpose is served by the introduction of this element into the book, and as all articles bought since the opening of the book are already accounted for, the inventory will better be kept out of the account-book until the housewife shall have studied the mysteries of fluctuating values in connection with capitalistic accountancy.

Small articles of value, if not kept in a safe-deposit vault or under lock and key,

83

HOW TO KEEP HOUSEHOLD ACCOUNTS

especially silverware, ought to be carefully noted in such a list and compared with the list frequently, as one of the principal uses of a methodically arranged and conservatively priced inventory of household effects is as an insurance record in case of loss by fire.

How a catalogue of household goods appeared in the olden time may be seen from a few conservative lines in a long "Inventory of the Goodes belongyng to the Kynges Grace by the forfettoure of the Lady Hungerford," who was attainted in the fourteenth year of the reign of Henry VIII.:

Item, a flowre of golde, fulle of sparkes of dyamondes set abowte with perles, and the Holy Gost in the mydste of yt.

Item, a table of golde with the pyktor of Seynt Cristofer in hym.

84

BUDGET, VOUCHERS, AND INVENTORY

Item, a harte of golde inhand with a wyd chene, inameled with white and blewe.

Item, a gret broiche of golde with a man and a woman in hym, the valure iiij pounde iiij l i.

Item, ij broches of golde with the pykter of Seynt Kateren in them, the value of them v marcs v marc.

Item, xxxv payre of aglettes of golde, which coste iiijli xiijs iiijd.

The following inventory of the household effects of a young couple living in comfort in one of the suburbs of New York is fairly representative. The furnace and ranges are fixtures; therefore no account is taken of heating apparatus. Wearing apparel, books, pictures, a sewing-machine, and the parlor organ are also excluded, in order that the list may be suggestive merely of what is usually required for the furnishing of the house:

85

HOW TO KEEP HOUSEHOLD ACCOUNTS

Sitting - room or parlor. — Carpet, ingrain, thirty yards, say $45; two roller shades, $4; two cornices, $8; lace curtains for two windows, $30; rep-covered sofa and two chairs, $80; two reception-chairs, $8; fancy chair, $10; sewing-chair, $4; marble-top table, $15. Total, $204.

Dining-room.—Carpet, ingrain, thirty yards, say $30; two roller shades, $3; cornices, $5; curtains, $7; extension-table, $12; six cane-bottom chairs, $15; sideboard, $30; cooler, $2.50; two trays, $2; coffee-pot, $2.50; egg-boiler, 50c; three dozen spoons, three sizes, $20; two dozen forks, two sizes, $15; dinner caster, $8; one dozen knives, $5; carving-knife, with steel sharpener, $3; mats; $1; two bells, $1.50; dinner-set, china, 134 pieces, $27; tea-set, china, forty-four pieces, $7; one dozen cut-glass goblets, $3; one dozen tumblers, $1; two cut-glass pre-

86

BUDGET, VOUCHERS, AND INVENTORY

serve-dishes, $3; china fruit-basket, $1; glass, $1; celery-glass, 50c.; pitcher, 50c.; molasses-jug, 50c.; one dozen salts, 50c. Total, $208.

Bedroom.—Carpet, thirty yards, say $30; two shades, cornice, and curtains, $12; furniture, ten pieces, $55; springs, $5; mattress, hair, $26; pillows and bolster, $12; pair blankets, $12; two spreads, $6; sheets and pillow-cases, three sets, $10; china toilet-set, $7. Total, $175.

Bedroom, or servant's room. — Carpet twenty-five yards, $25; window - shade, $1; table, $1.50; bureau and glass, $8; wash-stand, $2; two chairs and rocker, $4; bedstead and springs, $9; mattress, $15; pair blankets, $6; spread and comfortable, $4; pillows and bolster, $8; sheets and pillow-cases, three sets, $6; toilet-set, $4. Total, $93.50.

87

HOW TO KEEP HOUSEHOLD ACCOUNTS

Hall and stairs.— Hall carpet, $12; stair carpet, $10; padding, $3.50; eighteen rods, $6; hat - stand and umbrella - rack, $9. Total, $40.50.

Linen. — Table - cloths, eight yards damask, $5; five yards fine damask, bordered, $7.50; two plain table-cloths, $2; three dozen napkins, two qualities, $7.50; three dozen common towels, $1.50; one dozen dish-towels, $1. Total, $32.50.

Kitchen.—Large and small table, $7; five chairs, $2.50; refrigerator, $12; clock, $2.50; ladder, $2; hammer and tack-hammer, 50c; scales, $1.25; clothes-basket and market-basket, $2; scuttle, $1; covered slop-pail, $1; hatchet and screw-driver, $1; knife-board, knife-box, spoon-basket, and can-opener, $2; pint and quart measure, 25c; canisters for tea, coffee, and sugar, $1; nest of boxes, 75c.; bread and cake boxes, $2.50; funnel,

88

BUDGET, VOUCHERS, AND INVENTORY

15c.; wash-tubs, $3; ironing-boards, $1.25; wash-board, 25c.; clothes-pins, 25c.; boiler, $2; clothes-line, 50c.; six irons and two stands, $3.25; brooms and brushes, $2; dust-pan, 25c.; tea-kettle, $1; two iron pots, $3; preserve - kettle, $1.50; saucepans, $2; frying-pans, $1; dish-pans, $2; tin pans, various sizes, $3; earthen pans, $1; bowls, $1; pudding-dishes, 50c.; griddle, soapstone, $1.50; chopping-knife and board and bowl, $1.50; rolling-pin and kneading board and bowl, $1.25; cutters, 25c.; coffee-pot, 75c.; dipper and skimmer, 4 0 c ; two pails, 50c.; three sieves, $1.25; masher, 10c.; dredgers, 40c.; egg-beater, and cake-turner, 30c.; pie-plates, 50c.; patty-pans, 50c.; lemon-squeezer, 20c.; graters, 50c.; gridiron, 50c.; colander, 50c.; jelly - mould, 50c.; salt-box, 30c.; feather duster, $1. Total, $82.95.

89

HOW TO KEEP HOUSEHOLD ACCOUNTS

Recapitulation.— Sitting - room, $204; dining-room, $208; bedroom, $175; bedroom or servant's room, $93.50; hall and stairs, $40.50; linen, $32.50; kitchen, $82.95. Total, $836.45.

VI

THE BANK ACCOUNT

IT has been already remarked that if all the household money were passed

through the bank, the bank check-book might be used as a cash-book; but such a proceeding is neither desirable nor necessary in view of the simple accountancy of the journal-ledger, in which the cash-book is a component part of a tabular system fully controlling all the finances of the matron.

To say that accountancy is able, upon occasion, to adapt itself to all the circumstances and exigencies of place and time; that it can utilize, and has utilized, for its own scientific ends, the check - book,

91