How HMRC propose to verify Scotch whisky Consultation document Publication date: 12 October 2012 Closing date for comments: 07 December 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

How HMRC propose to verify Scotch whisky

Consultation document Publication date: 12 October 2012 Closing date for comments: 07 December 2012

2

Subject of this consultation:

Scotch whisky is protected under EU legislation as a product of Geographical Indication (GI). To market a GI product in the EU requires it to be verified as compliant with the technical file for that product. The EU legislation requires the cost of verification to be borne by producers. This document outlines how HM Revenue and Customs (HMRC) propose to verify the GI of Scotch whisky and recover associated costs.

Scope of this consultation:

This consultation seeks comment from Scotch whisky producers involved in any of the five identified production processes (fermentation, distillation, maturation, blending and bottling/labelling). Comments are welcome on how HMRC propose to verify the GI of brands, recover associated costs and issue Certificates of Verification, intended to replace the current Certificates of Age.

Who should read this:

HMRC welcomes input from any person, business or representative body with an interest in the verification of the Scotch whisky GI, or who is involved in any of the five production process identified above.

Duration: 12 October 2012 to 07 December 2012

Lead official: Sid Werrin, HMRC.

How to respond or enquire about this consultation:

Please respond, preferably by e-mail, to: [email protected], or by post to: Scotch Whisky Verification (Attention S Werrin), HM Revenue & Customs, Alcohol Policy (ECSM), 10th Floor, City Centre House, 30 Union Street, Birmingham, West Midlands, B2 4AD. Enquiries about the content or scope of this consultation, and requests for printed copies of the consultation document should be made using the contact details above, or by telephone to S Werrin on 0121 535 6762.

After the consultation:

HMRC will analyse and publish the results from the consultation as soon as practically possible after the consultation period, identifying any further actions planned or required as a result.

Getting to this stage:

GI verification of spirit drinks is a new initiative arising from EU legislation. Certificates of Verification are intended to replace the current Certificates of Age and Origin, which HMRC currently issue to facilitate the spirit drinks trade. Neither will be revenue raising.

3

Previous engagement:

The Department for Environment, Food and Rural Affairs (Defra) hold the policy for GIs and with HMRC have developed the verification scheme proposed here. Previous engagement has been through the industry’s principal representative body, The Scotch Whisky Association (SWA).

4

Contents

1

Introduction and Background

2

Definition of Terms and Acronyms

3

Verification Scheme

4

Certificates of Verification

5

Costs of Verification

6

Impact Assessment

7

Summary of Consultation Questions

8

The Consultation Process: How to respond

Annex A

List of stakeholders

Annex B

Relevant (current) Government Legislation

Annex C

Verification Checks

Annex D

Certificate of Verification

Annex E

Scotch whisky Technical File

Annex F

Draft Spirit Drinks (Costs of Verification) Regulations

Annex G

Indicative Postal Costs

On request this document can be produced in Welsh and alternate formats including large print, audio and Braille formats

5

1 Introduction 1.1 Scotch whisky is protected under EU legislation as a product of Geographical Indication (GI). This document outlines how HMRC propose to verify Scotch whisky. 1.2 HMRC’s role comprises two separate but inter-related services, to: verify products as compliant within the definitions of Scotch whisky

(Chapter 3); and on request, issue Certificates of Verification (Chapter 4). In all cases the costs of these services shall be borne by the Scotch whisky industry. 1.3 HMRC propose to verify Scotch whisky produced in the UK by checking that the manufacturing processes are correctly set up to create products that comply with its definitions1. The scheme will require producers in the Scotch whisky industry to apply for verification before placing their product on the market. 1.4 Scotch whisky produced (blended and bottled/labelled) in other European Union (EU) Member States, or outside the EU to be marketed in the EU, must also be verified for compliance with its definitions. In such cases producers will be required to make their own arrangements directly with an appropriate product certification body assuring their processes are to the standard established by us. HMRC will require a copy of the assurance report and the certification provided. 1.5 HMRC will publish lists of production facilities with assured processes and verified brands. Once the scheme has been implemented, only products verified by HMRC can be marketed legally in the EU as Scotch whisky. Producers who do not have their processes verified cannot legally produce and market their product as Scotch whisky. 1.6 As part of implementing this verification regime it is proposed that the current 'Certificates of Age and Origin' and ‘Certificates of Authenticity’ are withdrawn, to be replaced by a new single 'Certificate of Verification'.

1 Refer to technical file, see Annex F.

6

Background 1.7 Regulation (EC) No 110/2008 (110/2008/EC) includes a provision for Member States to introduce measures ensuring that spirit drinks marketed with a protected GI2 are produced in accordance with the specific conditions laid down in a technical file for the product. In the UK, this primarily affects Scotch whisky but also affects Irish whiskey produced in Northern Ireland and Somerset cider brandy. 1.8 For the UK, the Spirit Drinks Regulations 2008 (SDR) give effect to 110/2008/EC, which includes provisions for the production, labelling and marketing of spirit drinks. The Scotch Whisky Regulations 2009 (SWR) impose stricter rules on the production, description, presentation and labelling than those contained in 110/2008/EC. The aim of these regulations is to further enhance the protection of Scotch whisky. 1.9 Verification of compliance with the technical file is carried out by a designated authority and HMRC have been designated this role for UK spirit drinks with a protected GI and will therefore make The Spirit Drinks (Costs of Verification) Regulations 201X to legislate for the Verification scheme. A draft of these regulations is appended at Annex F. 1.10 Access to verification records by HMRC staff will be limited to the information required to support their verification activity, as indicated in Annex C outlining the verification checks intended to be undertaken. 1.11 HMRC’s role is limited to verifying that products notified to comply with the technical file and publication of details of facilities with compliant production processes and verified brands. 1.12 Where a process is found to be non-compliant, HMRC will notify the producer and require remedial action to be taken. Failure to comply will result in enforcement action, see paragraph 3.27. Enforcement of non-compliance with the verification scheme has been designated to Trading Standards and Port Health Authorities. HMRC are able to pass relevant information to these designated enforcement authorities through established legal gateways. 1.13 Circumstances under which HMRC will not verify and publish details of facilities or brands will include where: notification is not given by producers of Scotch whisky that they should be

included within the verification scheme; or an appropriate product certification body acting on a producers behalf are

unable to establish compliance with the technical file

2 Geographical indications are a type of intellectual property. They are forms of identification which identify a product as originating in a region or locality in a particular country. The product’s reputation for quality or authenticity is intimately linked to its geographical origin.

7

HMRC are requested to exclude a brand by a relevant enforcement authority, considering evidence of failure / non-compliance in an assured process.

1.14 A draft verification scheme has been developed, the full costs of which will be borne by producers in the Scotch whisky industry, as required by 110/2008/EC. Your responses to the questions, summarised at Chapter 7, are welcome. 1.15 Details of how to respond are explained in Chapter 8.

8

2 Definition of Terms 2.1 This document uses terms that can have different meanings depending on context. For clarity, the terms below should always be associated with the accompanying definitions.

Term Definition

Producer The owner of a production facility carrying out at least one stage of the production of Scotch whisky.

Operator A person responsible for the operation of a production facility. This can be a distillery manager, for example.

Facility or production facility

A facility operating one or more production processes required to create Scotch whisky.

Process or production process

One of five processes required to create Scotch whisky: fermentation: distillation; maturation; blending; and labelling of final product (bottling).

Brand The label name on a bottled product excluding ages, descriptors and regions.

Technical file

A document that specifies the requirements of Scotch whisky. This includes requirements for production, description, presentation and labelling of Scotch whisky.

Fermentation

The process of converting sugars into alcohol with the addition of yeast. This includes all stages of production up to but not including the distillation process (including mashing of cereals).

Distillation The process of acquiring spirit drinks using a fermented mixture. This includes all stages after fermentation up to the point where newly distilled spirit is obtained.

Maturation

The process of aging spirit to create Scotch whisky. This includes all processes from when newly distilled spirit is obtained up to but not including the point when casks are to be emptied for blending or vatting. This includes the filling of casks and tracking of ages.

Blending

The process of combining two or more single whiskies to create a new whisky in one of three categories: blended malt, blended grain or blended. This includes all processes from the emptying of casks to vatting, blending and diluting up to the point of bottling.

Labelling (and bottling)

Labelling means all descriptions and other references, signs, designs or trade marks which distinguish a drink and which appear on the same container. This includes its sealing device or the tag attached to the container and the sheathing covering the neck of the bottle. It also includes the process of bottling and presentation.

9

Acronyms

Acronym Definition

abv alcohol by volume CION European Commission COELA Cabinet Office European Legal Advisors

Defra Department for the Environment, Food and Rural Affairs

EC European Commission EU European Union GI Geographical Indication(s) HMRC Her Majesty’s Revenue and Customs HMT Her Majesty’s Treasury SDR Spirit Drinks Regulations 2008 SWA Scotch Whisky Association SWR Scotch Whisky Regulations 2009 UK United Kingdom

10

3 Verification Scheme 3.1 HMRC is obliged to verify Scotch whisky brands only when it can be shown that each process involved in creating that product complies with the Scotch whisky Technical file. 3.2 There are potentially two approaches that might be adopted by HMRC to conduct the necessary assurance:

i) for each brand notified, carry out full (end to end) assurance of all production process involved, or

ii) verify the compliance of all notified UK production facilities and processes periodically, and when brands are notified provide assurance that they originate from those compliant facilities and processes.

3.3 It is common for multiple brands to originate from a single production facility, and therefore a programme of assurance consistent with the latter approach is proposed. This will ensure that no single operator is visited more than once (unnecessarily) for the same purpose, and that costs to industry of operating an effective verification scheme are minimised. 3.4 HMRC will assure the 5 key processes involved in production of Scotch whisky. Each producer who conducts one of these processes will have their process checked to assure compliance with the technical file. 3.5 Subject to any transitional arrangements, once the scheme is implemented only production facilities with assured processes can be used to produce and market Scotch whisky legally in the EU. Producers who market their product as Scotch whisky but have not gained assurance of their processes will be doing so illegally and will be referred to the enforcement authorities for appropriate action. What production processes will HMRC examine to verify Scotch whisky? 3.6 The five key production processes defined in SWR which HMRC propose to check for compliance are: 1. fermentation

2. distillation

3. maturation

4. blending

5. labelling of final product

The production processes for Scotch whisky

11

3.7 HMRC may only verify a brand if all processes involved have been assured, including any non UK blending/bottling/labelling facilities. Who should apply for verification and how? 3.8 All operators of premises undertaking one or more of the key production processes (above) should apply to HMRC to have their processes verified. Operators will be required to notify HMRC using the form available through its website or through the Scotch whisky verification unit, providing sufficient information to manage the verification scheme, for example: Production Facility Name Production Facility Address Production Facility Process(es) Undertaken Correspondence Address Invoice/Billing Address Operator (Production Facility Contact) Name Operator Address Operator e-mail address Operator telephone number It is intended that operators will be able to submit this information to HMRC electronically but, alternatively the form may be posted to the Scotch whisky verification unit. 3.9 For operators in the UK the information provided will be used by HMRC to issue invoices and, within a month after payment, to make contact to arrange an appointment for the necessary process assurance visit. 3.10 For operators outside the UK the information will be used to support verification of individual products but operators will be required to directly commission, at their own cost, an appropriate product certification body to undertake the necessary process assurance visit. Assuring production processes within the UK

3.11 HMRC will assure all notified Scotch whisky production processes in the UK for compliance with the specifications, requirements and definitions, in the Scotch whisky technical file, using the checks outlined at Annex C. For example: Checking HMRC records to ensure all appropriate approvals are held; Checking purchase invoices, and delivery records, for ingredients and

equipment; Physical examination of equipment; Checking procedures, as written, observed and through interview. 3.12 It is the responsibility of operators to notify HMRC that they run production processes requiring assurance.

12

3.13 A visit will follow to the production facilities to check that their processes comply with the technical file for Scotch whisky. Where this involves documentary checks, for example purchase records of ingredients and casks etc. these must be made available to the verification team at the premises when and where the production process assurance visit takes place. 3.14 There will be a charge to the producer for the costs of this service. Assuring production processes outside the UK 3.15 Scotch whisky operators in other EU Member States, and those outside the EU who know or believe their products will be marketed in the EU, must also have their production processes assured. 3.16 It is proposed that any relevant processes outside of the UK are assured for compliance with the Scotch whisky technical file by a control body (Article 2 of Regulation 882/2204/EC) operating as a product certification body (Article 22 of Regulation 110/2008/EC). This would require operators to directly commission, at their own cost, an appropriate product certification body that meets the qualification criteria laid down in 110/2008/EC. Subsequently they would need to provide HMRC with a report of their findings, which must include all of the following: evidence that the product certification body complies and is accredited

with: - European Standard EN 45011; or - ISO/IEC Guide 65 (General requirements for bodies operating product certification systems)

adequate guarantees of their objectivity and impartiality confirmation that the assurance was undertaken by qualified staff using

appropriate resources evidence supporting their opinion of whether the overseas production

process is compliant with the Scotch whisky technical file. 3.17 If the conditions at paragraph 3.16 are met and there are no other reasonable grounds to do otherwise, HMRC will accept the decision of the product certification body as if they had undertaken the production process assurance. This will be recorded as appropriate. Details of production facilities with assured processes or verified brands will not be published or updated until a copy of the assurance report and certification is received.

13

How will HMRC assure that brands originate from compliant processes? 3.18 HMRC will require operators responsible for the final labelling of the Scotch whisky products to submit a list of all brands that they bottle and label, either on behalf of their customers or which they supply themselves. Working backwards from that point, they must also provide evidence that the brand being submitted for verification originates from assured production facilities operating compliant processes e.g. from an operator whose blending and maturation processes have been verified as compliant. That operator in turn would need to be able to evidence to HMRC that all spirits being matured as Scotch whisky were from production facilities operating assured distillation processes and so on through the 5 processes of production. HMRC, and appropriate product certification bodies outside the UK, will assure these claims to verify they are correct. 3.19 Producers are required to retain such records as may be required to verify a brand. The records should allow HMRC to trace a bottled product back though the production processes to determine where the product was bottled, blended, matured, distilled and fermented. If a non-compliant product is reported to HMRC, producers should retain sufficient information to allow their investigation into the source of non-compliance and put in place measures to remedy the situation. How will I know whether production facilities have been assured? 3.20 After the verification scheme has been introduced there are likely to be two groups of production processes in the industry, processes that are: checked by HMRC or an appropriate product certification body and

assured as compliant with the technical file either non-compliant or have not been checked by HMRC or an

appropriate product certification body because the producer has not sought assurance.

3.21 It is proposed to allow producers to check whether other production facilities in the industry have had their processes assured in order to ensure that the product remains verified. To facilitate this, HMRC will publish a list of production facilities with assured processes on its website.

14

Production facilities with assured processes The following production facilities have had their processes inspected and assured by HMRC as complying with the requirements to produce Scotch whisky. A brand of Scotch whisky can be placed on the market only if the entire production process has been assured by HMRC in the UK and an appropriate product certification body outside the UK. Production Facility Address of Facility Assured Processes

John’s Distillery Fermentation Distillation (Grain)

Jane’s Bottling Blending Labelling

Jan’s Glenwhisky Distillery

Fermentation Distillation (Malt) Maturation

| An example of how HMRC may list production facilities with assured processes on their website.

How will I know whether brands have been verified? 3.22 It is proposed to list verified brands on HMRC’s website so that customers (consumers, importers and overseas authorities) are able to check their verification status. Brands not appearing on the website will either not have been verified by or have not been notified to HMRC. In these circumstances the brand cannot be legally marketed as Scotch whisky. 3.23 HMRC propose to list brands on its website in alphabetical order. Producers may indicate how they wish their verified brands to be listed by advising the operator responsible for labelling the final product how they should record the relevant brand names when informing HMRC. The list will not list various ages of the same brand.

Verified brands Below is the complete list of brands whose production processes have been assured by HMRC as compliant with the technical file. These brands can be marketed as Scotch whisky. Brands that do not appear in the list below cannot be marketed as Scotch whisky.

Brand

(The) Andrew’s Single Malt (Isle of) Angus Single Malt Belinda’s Blended Grain

| An example of how HMRC may list verified brands on their website.

15

How frequently will HMRC assure the compliance of the industry? 3.24 A programme of visits to assure notified production processes will commence once this scheme has been finalised, and thereafter every two years to assure continued compliance with SWR and the technical file for Scotch whisky. 3.25 It is anticipated that all Scotch whisky producers and operators will wish to apply for process assurance/brand verification and it is expected that the verification of all legitimate brands will take approximately two years to complete. Operators outside the UK should ensure that their own processes are independently assured by an appropriate product certification body, and provide a copy of the report giving that independent assurance to HMRC, within that two year period, and every two years thereafter. 3.26 There will be a transitional period when there will be some Scotch whisky brands on the market which have not been verified through production process assurance visits. For Scotch whisky this may be considerable depending on the period of maturation. To enable that product to be marketed, unless there is evidence to the contrary, Scotch whisky which was distilled (i.e. sold or sent for maturation, blending or bottling/labelling) before the date of any verification visit to the facilities will be deemed compliant with the specifications of the technical file, provided that the processes are subsequently found to be compliant. What happens in the event of Non-Compliance? 3.27 In the event of non-compliance with the verification requirements, or if HMRC are not able to assure a production process, within the UK the producer or operator will be advised how they can become compliant and a reasonable period of time agreed with them to take remedial action. This will vary depending on the nature of the remedial action required. Outside the UK it will be the responsibility of the producer, seeking verification to seek and implement such advice from their product certification body. 3.28 The period of time permitted will depend on the nature of change to be implemented and will be proposed by the assurance/verification officer to be agreed with the producer. Failure to comply after this period will result in the production facility being removed from, or not included on, the list of production facilities with assured processes. HMRC will also inform the designated enforcement authorities. 3.29 Production processes that are assured and subsequently found to be non-compliant will similarly result in associated brands no longer being verified until such time that compliance is achieved.

16

3.30 Producers are required to check the list of production facilities with assured processes routinely to ensure that the inward delivery is from an assured source. Non-compliance will be detected either via routine visits or by notification from other producers. Where this is the case, any subsequent products created using non-compliant processes will no longer be verified. HMRC will assume compliance of product already produced and will only remove these from the list of verified brands if evidence of prior non-compliance is conclusive. Q1 What are your views on the proposed verification scheme, particularly: the concept of verifying brands of Scotch whisky by assuring the

processes used to create them, and the level of evidence expected of you to demonstrate compliance? Q2 What are your views on how HMRC propose to verify production processes outside the UK? Q3 What are your views on how HMRC propose to collect brand names from the final production process? Q4 How often do you think it would be necessary to refresh the list of verified brands, i.e. how often are new brands created? Q5 What are your views on the proposed verification checks included at Annex C? Q6 What are your views on the technical file (Annex E) detailing the specifications with which Scotch whisky must comply?

17

4 Certificates of Verification 4.1 HMRC currently issue certificates of age and origin or certificates of authenticity for spirit drinks. There is no legal requirement for this service but it is provided at the request of the spirit drinks industry to facilitate exports. The Scotch whisky industry is the main customer of these certificates, although a small number of certificates are issued for other spirit drinks. 4.2 There are seven certificates currently in use, some of which are generic and others are for specific markets. Some certificates are printed on watermarked paper and cost £3.80 each; others cost £3.50 each plus the cost of postage and packaging. 4.3 It is propose to cease issuing certificates of age and origin/authenticity and to replace them with a single new Certificate of Verification for Scotch whisky as a protected GI under Regulation 110/2008/EC. 4.4 Certificates of Verification for: the bulk movement of Scotch whisky by producers recorded on HMRC’s

lists of production facilities with assured processes, or each brand recorded on HMRC’s lists of verified brands will be issued only to, and on request from, producers whose production facilities have been assured by HMRC, in the UK, or by an accredited product certification body, outside the UK. Producers responsible for, or otherwise using, overseas facilities (whether in or outside the EU) who have gained assurance of the processes at those production facilities for Scotch whisky can also request Certificates of Verification for verified products. 4.5 Producers may request more than one copy of this certificate at a cost borne by them. HMRC estimate the maximum cost of a certificate at £2.00 plus postage and packaging. It is intended to use Second Class ‘Registered Signed For’ for UK postage and ‘Signed For’ Airmail for international postage. An indication of the postal charges is attached at Annex G. This cost will attract Value Added Tax (VAT) at the Standard Rate, currently 20%, and will be in addition to the proposed verification fee. 4.6 Certificates of Verification will be pre-authenticated: a producer can request certificates in advance and use them in each shipment of Scotch whisky without presenting it to HMRC. If a Certificate of Verification is used to support the bulk export of Scotch whisky there can only be confirmation that the bulk product has been verified to be Scotch whisky and that the final product has not been verified. 4.7 A producer who loses assurance of one or more processes at any of their, or sub-contracted, production facilities can no longer request certificates and will be required to return any unused certificates to HMRC.

18

4.8 Certificates will be issued on request to producers and cannot be transferred or sold to others outside the control of the producer to whom they were issued. In the event that this is found to occur subsequent requests may be refused. Handlers of Scotch whisky who are not part of the verification scheme cannot request copy certificates. 4.9 Certificates will be printed on security paper with a restricted watermark and will contain a unique reference number to allow tracking. HMRC will conduct sample compliance activity on certificates by randomly selecting certificate numbers and tracing the declared spirit back to where and when it was distilled. Should it not be possible to trace product from declared certificates back to where and when it was distilled then the declaring producer will be deemed to be non-compliant within the requirements for Scotch whisky verification. 4.10 HMRC will advise the declaring producer how they can become compliant and will issue them with a reasonable period of time to do so. Failure to comply after this time will mean that the declaring producer’s production facilities will be removed from, or not included on, the list of assured production facilities. HMRC will also inform the enforcement authorities. 4.11 In the event of non-compliance with verification requirements or if HMRC are not able to assure, or confirm assurance of a production process, Certificates of Verification will not be issued to producers. For example, during their agreed ‘period of correction’, until their compliance is (re)established. 4.12 A sample draft certificate is included with this document, at Annex D. Q7 What are your views on our proposal for a new Certificate of Verification? For example: considering cost and benefit, what level of security printing is

appropriate? will the proposed Certificate meet your needs and the needs of your

export markets?

19

5 Costs of Verification 5.1 Article 22(1) of Regulation (EC) No 110/2008 states that “notwithstanding national legislation, the costs of such verification of compliance with the specifications in the technical file shall be borne by the operators subject to those controls”. Within the UK any charges need to comply with HM Treasury guidance “Managing Public Money”, available on-line at: http://www.hm-treasury.gov.uk/psr_managingpublicmoney_publication.htm and HMRC intend to set fees with the aim of ensuring full cost recovery on a financial year basis. These will attract Value Added Tax (VAT) at the Standard Rate, currently 20%. 5.2 The payment scheme HMRC proposes to introduce is:

1. Scotch whisky production facilities in the UK will be required to pay a published standard fee, in advance, in the financial year in which their production process is assured. These fees will be reviewed biennially, to provide equity during the two year rolling programme of verification visits, to ensure that charges match the verification scheme costs to HMRC; and,

2. Scotch whisky production facilities outside the UK requiring assurance of their production processes will be required to pay the product certification body directly for the process assurance services provided, (paragraphs 3.15-3.17).

HMRC do not intend to charge a separate administration fee for listing production facilities with assured processes, or verified brands, on its website. Charges for Certificates of Verification will be calculated and invoiced separately from verification scheme fees. These will apply to all requests, as outlined in Chapter 4. 5.3 A standard fee structure is proposed in which a standard charge will be levied for each production process operating in each of the premises that is required to be verified. This reflects the costs that will be incurred by HMRC, which will be the same or similar regardless of the size of the operation or location. For example, the same checks will be conducted at a large grain distillery and a small malt distillery and the overheads of maintaining verification (e.g. IT systems, people costs) will remain the same. Calculation of fees 5.4 The fee for verification will seek to recover the full costs incurred by HMRC. It is estimated the full costs of verification for UK production and processing sites to be approximately £290,000 per year, which includes salary costs of staff carrying out the work, travel expenses, the costs of maintaining the verification scheme, computer systems and other overheads as outlined in Chapter 6.

20

5.5 These costs assume the Scotch whisky verification unit will be based in Glasgow. This may change so the additional costs of visiting remote Scotch whisky productions sites, estimated to be approximately £10,000 has been excluded from the overall costs of the verification scheme in the interests of calculating an equitable flat rate fee. 5.6 HMRC’s costs may of course increase if repeat visits are required to production facilities due to non-compliant production processes. The fee itself will also be affected by the number of producers who apply for verification. 5.7 105 Scotch whisky distilleries have been identified, each responsible for fermentation and distillation processes, and it is estimated that there are a similar number of producers involved in subsequent processes of maturation, blending and bottling/labelling. In total it is estimated that there are approximately 200 production facilities in the industry. 5.8 The five Scotch whisky production processes defined in SWR, multiplied by the105 distilleries gives an estimated maximum number of Scotch whisky processes which HMRC must assure as 105 x 5 = 525. However, processes after distillation may be operated by producers servicing more than one distillery. Assuming that the estimated 200 production facilities in the industry will each operate an average of two production processes it is estimated HMRC must assure, over an anticipated two year rolling programme of visits, 200 x 2 = 400, or 200 processes a year. 5.9 As a guide only, based on the above assumptions and charging a standard fee per process: A producer undertaking fermentation and distillation processes on a single

site might incur a fee of 2 x £1,400 = £2,800 payable every two years. That same operator, also with on-site maturation facilities would incur a

fee of 3 x £1,400 = £4,200 payable every two years. An independent operator responsible for blending and bottling/labelling the

final product will incur a fee of 2 x £1,400 = £2,800 payable every two years.

Payment and collection of fees 5.10 If a producer applies for assurance of its processes then HMRC will issue invoices to the address notified by producers on their application/registration under the verification scheme. 5.11 Following payment of the appropriate fee, HMRC will visit the premises, conduct assurance checks and, if satisfied, will include the production facility in the list of facilities with assured processes. 5.12 Fees will be invoiced approximately every two years, in time for producers to make payment facilitating their necessary process approval visit every two years.

21

5.13 Fees must be paid prior to any verification visit and will be collected by electronic payment channels only, such as Faster Payment, BACS or CHAPS. 5.14 If payment is not received then the producer will either not receive their initial process assurance visit or otherwise will be deemed non-compliant under the provisions of Article 22(1) in Regulation (EC) No110/2008 and their facilities will be removed from, or not included on, the list of production facilities with assured processes published on the HMRC website. 5.15 If a production facility fails the initial, or any subsequent, assurance checks then HMRC will provide sufficient time and opportunity to comply. This may mean that follow-up visits to assure the process(es) in question may be required. If a follow-up visit is required, HMRC will charge the producer an additional standard fee charge for the process requiring further assurance. 5.16 If a production facility becomes non-compliant, or no longer requires assurance, their processes will be removed from the list of production facilities with assured processes. Any impacted brand details will also be removed from the list of verified brands. 5.17 Fees will be set with the aim of ensuring full cost recovery on a financial year basis. The fee will be reviewed periodically (at least every two years in line with the programme of visits) and adjusted to account for deficits or surpluses. HMRC will publish details of fees and consult producers if substantial changes are required to the fee structure. 5.18 Fees will not be refunded. Alternative options considered 5.19.1 Charge producers a standard fee for each production facility. This

would impose the same financial burden on producers regardless of the number of processes they operate. This was rejected as inequitable and did not reflect the actual cost of verification that HMRC would incur and so not be compliant with “Managing Public Money” guidance.

5.19.2 Charge producers an annual standard fee for each production

process they operate in each of their production facilities. This was rejected as costs and charges would relate to different financial years, so would not comply with “Managing Public Money” guidance.

5.19.3 Charge producers a scaled fee reflecting the size of the business. This was rejected as it would create cross subsidies (i.e. larger businesses subsidising smaller ones). It would also not be proportionate to the service HMRC would provide to each producer, which will be the same or similar regardless of size. Both of the above fail to comply with Managing Public Money” guidance.

22

5.19.4 Charge producers the full costs of verification associated with each individual visit. This was rejected as inequitable and increase the overall cost of administering the scheme. It would result in higher costs to producers more remote from HMRC’s verification team in Glasgow, reflecting varying travel and subsistence costs, for the same verification service offered to each producer. Though accurate this would require post verification invoicing and payment which potentially increasing the rechargeable costs of verification from increased administration and Bad Debt recovery.

Q8 Do you consider charging a flat fee per production process an appropriate method of recovering costs of verification? Q9 Are there any alternative methods of apportioning the costs of verification that you would prefer, and why? Q10 What are your views on the draft charging regulations (Annex F) which HMRC propose to make?

23

6 Impact Assessment

Summary of Impacts Exchequer impact This is not a revenue raising initiative and no revenue will accrue to the Exchequer. The costs of the verification scheme, as detailed below, will be recovered by charging the industry. The wider costs, benefits and rationale of UK legislation to enhance the protection of Scotch Whisky were considered in the Impact Assessment that accompanied the Scotch Whisky Regulations 2009. The rest of this impact assessment considers only the specific costs related to the ‘Costs of Verification’ Regulations. Economic impact In 2010 90% of Scotch whisky (Litres of Pure Alcohol) was exported. In 2011 Export Values of Scotch whisky were £4.32 billion. Against these levels of business the recharge to the industry of Scotch whisky GI verification costs (detailed above) is extremely small. (0.0000625%) Charges for Certificates of Verification will be calculated to be self funding so charges will reflect individual demands. Impact on individuals and households In 2011 there were reportedly almost 500,000 bottles of Scotch whisky sold in the UK. If the total cost of the verification scheme were to be absorbed by the home market the increase in bottle prices would be 60 pence. Assuming this to be only 10% of the global Scotch whisky Market the increase in bottle price would be 6 pence. The cost of verification represents only 0.0000625% of industry sales. Equalities impacts None identified. Impact on businesses and Civil Society Organisations Annual HMRC Costs (calculated in March 2011):

(NB Costs are approximate and may be subject to change)VERIFICATION SCHEME Full Cost of Staff (Verification Team Salaries + Overheads) £212,367 IT Capital Investment and Cost of Capital (Estimated) Annual Average over 10 years £28,553 Administration - Stationery, Printing, Postage etc. (Estimated) £15,000 Subsistence (Estimated) £25,080 Travel (Estimated) £10,301 TOTAL (VERIFICATION SCHEME) £291,301 CERTIFICATES OF VERIFICATION Full Cost of Staff (Salaries + Overheads) £25,064IT Capital Investment and Cost of Capital (Estimated) Annual Average over 10 years £4,348 Security Printed Certificates (Estimated) £40,000 Administration - Stationery, Postage etc. (Estimated) £5,000TOTAL (CERTIFICATES OF VERIFICATION) £74,412 TOTAL (VERIFICATION SCHEME+CERTIFICATES OF VERIFICATION) £365,713 These costs will be recovered by charging the industry. There are no identified impacts on the third sector. Impact on HMRC or other public sector delivery organisations HMRC will incur nil net cost because the expense of the scheme will be recovered from the industry. Capital Costs (as identified above) will be recovered from the industry over the next ten years. Other impacts None identified.

24

Q11 Do you agree with the assessments of impacts indicated?

25

7 Summary of Consultation Questions Whilst HMRC will have worked with many stakeholders to develop this draft scheme, HMRC would be grateful for your views on how this scheme will affect you and, in particular, your responses to the questions below. Additionally we would be happy to consider any other comments or suggestions you may have.

Q1 What are your views on the proposed verification scheme, particularly: the concept of verifying brands of Scotch whisky by

assuring the processes used to create them, and the level of evidence expected of you to demonstrate

compliance?

Q2 What are your views on how HMRC propose to verify production processes outside the UK?

Q3 What are your views on how HMRC propose to collect brand names from the final production process?

Q4 How often do you think it would be necessary to refresh the list of verified brands, i.e. how often are new brands created?

Q5 What are your views on the proposed verification checks included at Annex C?

Chapter 3

Q6 What are your views on the technical file (Annex E) detailing the specifications with which Scotch whisky must comply?

Chapter 4

Q7 What are your views on our proposal for a new Certificate of Verification? For example: considering cost and benefit, what level of security

printing is appropriate? will the proposed Certificate meet the needs of industry

and export markets?

Q8 Do you consider charging a flat fee per production process an appropriate method of recovering costs of verification?

Q9 Are there any alternative methods of apportioning the costs of verification that you would prefer, and why?

Chapter 5

Q10 What are your views on the draft charging regulations (Annex F) which HMRC propose to make?

Chapter 6

Q11 Do you agree with the assessments of impacts indicated?

26

8 The Consultation Process The purpose of the consultation is to seek views on: the detailed policy design and a framework for implementation of a specific

proposal, rather than to seek views on alternative proposals the draft legislation in order to confirm, as far as possible, that it will

achieve the intended policy effect with no unintended effects How to respond A summary of the questions in this consultation is included at Chapter 7. HMRC would also welcome your views on the proposed verification scheme and charging provisions and your thoughts on the assurance checks to be carried out. Responses should be sent by 07 December 2012. by e-mail to: [email protected] or by post to: Scotch Whisky Verification (Attention S Werrin) HM Revenue & Customs Alcohol Policy (ECSM), 10th Floor, City Centre House, 30 Union Street, Birmingham, West Midlands, B2 4AD Enquiries about the content or scope of this consultation, and requests for paper copies should be made using the contact details above, or by telephone to S Werrin on 0121 535 6762. If you require more time to respond then please contact us using the above details and HMRC will try to accommodate your request. Paper copies of this document or copies in Welsh and alternative formats (large print, audio and Braille) may be obtained free of charge from the above address. This document can also be accessed from the HMRC internet site at http://www.hmrc.gov.uk/consultations/index.htm. All responses will be acknowledged, but it will not be possible to give substantive replies to individual representations. When responding please say if you are a business, individual or representative body. In the case of representative bodies please provide information on the number and nature of people you represent.

27

Confidentiality Information provided in response to this consultation, including personal information, may be published or disclosed in accordance with the access to information regimes. These are primarily the Freedom of Information Act 2000 (FOIA), the Data Protection Act 1998 (DPA) and the Environmental Information Regulations 2004. If you want the information that you provide to be treated as confidential, please be aware that, under the FOIA, there is a statutory Code of Practice with which public authorities must comply and which deals with, amongst other things, obligations of confidence. In view of this it would be helpful if you could explain to us why you regard the information you have provided as confidential. If we receive a request for disclosure of the information we will take full account of your explanation, but we cannot give an assurance that confidentially can be maintained in all circumstances. An automatic confidentiality disclaimer generated by your IT system will not, of itself, be regarded as binding on HMRC. HMRC will process your personal data in accordance with the DPA and in the majority of circumstances this will mean that your personal data will not be disclosed to third parties. Consultation Principles This consultation is being run in accordance with the Government’s Consultation Principles. The consultation is being run for 8 weeks to allow for the implementation date of early 2013 and because this is an issue specifically impacting the Scotch whisky industry whose representative body, the Scotch Whisky Association, have already been involved in discussions on behalf of those affected. To ensure that people are able to contribute as fully as possible to this consultation HMRC will be making the consultation document available in a variety of formats, if required. The Consultation Principles are available on the Cabinet Office website: http://www.cabinetoffice.gov.uk/resource-library/consultation-principles-guidance If you have any comments or complaints about the consultation process please contact: Amy Burgess, Consultation Coordinator, Budget & Finance Bill Co-ordination Group, HM Revenue & Customs, 100 Parliament Street, London, SW1A 2BQ e-mail [email protected] Please do not send responses to the consultation to this address.

28

Annex A: List of stakeholders consulted/for consultation This verification scheme is being shared with the Scotch whisky industry and its representatives only and HMRC have sought to identify operators in it. HMRC appreciate that this list may not be complete and so would welcome your assistance in identifying other operators in the industry who may be affected by this scheme. Please forward details of such operators to [email protected]. Aberfeldy Distillery Aberlour Distillery Abhainn Dearg Distillery Ailsa Bay Distillery Allt a'Bhainne Distillery Ardbeg Distillery Ardmore Distillery Arran Distillery Auchentoshan Distillery Auchroisk Distillery Aultmore Distillery Balblair Distillery Co Ltd Balmenach Distillery Balvenie Distillery Ben Nevis Distillery Benriach Distillery Benrinnes Distillery Benromach Distillery Bladnoch Distillery Blair Athol Distillery Bowmore Distillery Braeval Distillery Bruichladdich Distillery Bunnahabhain Distillery Cameron Bridge Distillery Caol Ila Distillery Cardhu Distillery Clynelish Distillery Cragganmore Distillery Craigellachie Distillery Daftmill Distillery Dailuaine Distillery Dalmore Distillery Dalwhinnie Distillery Deanston Distillery Dufftown Distillery Edradour Distillery Fettercairn Distillery Girvan Distillery Glen Elgin Distillery Glen Garioch Distillery Glen Grant Distillery Co Ltd

Glen Keith Distillery Glen Moray Distillery Glen Ord Distillery Glen Scotia Distillery Glen Spey Distillery Glenallachie Distillery Glenburgie Distillery Glencadam Distillery Glendronach Distillery Glendullan Distillery Glenfarclas Distillery Glenfiddich Distillery Glenglassaugh Distillery Company Ltd Glengoyne Distillery Glengyle Distillery Glenkinchie Distillery Glenlivet Distillery Glenlossie Distillery Glenmorangie Distillery Glenrothes Distillery Glentauchers Distillery Glenturret Distillery Highland Park Distillery Inchgower Distillery Invergordon Distillery Isle of Jura Distillery Kilchoman Distillery Co Ltd Kininvie Distillery Knockando Distillery Knockdhu Distillery Co Ltd Lagavulin Distillery Laphroaig Distillery Linkwood Distillery Loch Lomond Distillery Co Ltd Longmorn Distillery Macallan Distillery Macduff Distillery Mannochmore Distillery Miltonduff Distillery Mortlach Distillery North British Distillery Co Ltd Oban Distillery

29

Pulteney Distillery Co Ltd Roseisle Distillery Royal Brackla Distillery Royal Lochnagar Distillery Scapa Distillery Speyburn Distillery Co Ltd Speyside Distillery Springbank Distillery Strathclyde Distillery Strathisla Distillery

Strathmill Distillery Talisker Distillery Tamdhu Distillery Tamnavulin Distillery Teaninich Distillery Tobermory Distillery Tomatin Distillery Co Ltd Tomintoul Distillery Tormore Distillery Tullibardine Distillery

Bottlers Aberko Limited Aceo Limited Adelphi Distillery Alchemist Beverage Co Bennachie Whisky Co Berry Bros & Rudd Ltd Blackadder International Brands Development Worldwide Broxburn Bottlers Cabrach Whisky Company Chivas Brothers Bottling (Kilmalid) Compass Box Craigton Packaging Ltd Dewar Rattray Diageo Bottling (Kilmarnock) Diageo Bottling (Leven) Diageo Bottling (Sheildhall) Distillers.com Douglas Laing & Co Ltd Duncan Taylor & Co Glen Turner Distillery Ltd Halewood International Ltd

Hart Brothers James MacArthur & Co John G Russell (Transport) Ltd John Milroy Ladybank Company of Distillers Club Leinburn Lombard Scotch Whisky Murray McDavid MWBH Bottling Co Old St Andrews Ltd Prabàn na Linne Ltd Scotch Malt Whisky Society The Creative Whisky Co The Harris Whisky Co The Master of Malt The Premier Scotch Whisky Co The Queen of the Moorlands Whisky

Co The Vintage Malt Whisky Company Vintage Malt Whisky Company Whisky Castle Ltd Wm Cadenhead Ltd

Producers Angus Dundee Distillers Plc Beam Global Spirits & Wine Inc Blairmhor Ltd Burn Stewart Distillers Ltd Chivas Brothers Ltd Co-ordinated Development Services D Johnston & Co (Laphroaig) Ltd Diageo Distilling Ltd Drambuie Liqueur Company Ltd Edrington Group Ltd Glen Catrine Bonded Warehouse Ltd Glenmorangie Company Ltd Gordon & MacPhail

Harvies of Edinburgh International Ltd Highland Distillers Ltd Ian Macleod Distillers Ltd International Whisky Co Ltd Inver House Distillers Ltd Isle of Arran Distillers J&A Mitchell & Co Ltd J&G Grant J&W Hardie Ltd James Buchanan & Co Ltd James Catto & Co Ltd John Dewar & Sons Ltd Justerini & Brooks Ltd

Last Drop Distillers Ltd London & Scottish International Ltd Morrison Bowmore Distillers Ltd

Peter J Russell & Co Ltd Signatory Vintage Scotch Whisky Co Whyte & Mackay

30

William Grant & Sons Ltd Wm Lawson Distillers Ltd

Wm Teacher & Sons Ltd

Other Department for Environment Food and Rural Affairs (Defra) Local Government Regulation (formerly Local Authorities Co-ordinators of Regulatory

Services) Scotch Whisky Association The Wine and Spirit Trade Association

Annex B: Relevant (current) Government Legislation Regulation (EC) No 110/2008 on the definition, description, presentation, labelling and the protection of geographical indications of spirit drinks: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:32008R0110:en:NOT The Spirit Drinks Regulations 2008 http://www.legislation.gov.uk/uksi/2008/3206/made The Scotch Whisky Regulations 2009 http://www.legislation.gov.uk/uksi/2009/2890/made The Spirit Drinks (Costs of Verification) Regulations 2012 A copy is included with this document (Annex F). Main specifications of the technical file for Scotch whisky A copy is included with this document (Annex E). HM Treasury Managing Public Money 2007 Managing Public Money (MPM): Chapter 6: Fees, charges and levies

http://www.hm-treasury.gov.uk/psr_managingpublicmoney_publication.htm MPM Annex 6.2 How to calculate fees

http://www.hm-treasury.gov.uk/psr_mpm_annexes.htm Cabinet Office “The Consultation Principles” http://www.cabinetoffice.gov.uk/resource-library/consultation-principles-guidance

Annex C: Verification Checks 1. Distillery

Serial Requirement Check Comments Pass

1.

Distillers and distilleries (i) All distillers and distilleries must be licensed by HMRC to distil alcohol. (ii) All Scotch whisky distilleries must be located in Scotland. (iii) All distilleries must have an approval of plant and process from HMRC. (iv) Each distillery must submit a quarterly distillery return (W21).

(i) Check the HMRC list of licensed distillers to ensure compliance and validity and compliance with any conditions – both distiller and particular premises would need to be checked. (ii) Check address. (iii) Check HMRC records for correct approval of plant and process. (iv) Check HMRC records for regular submissions of W21. Check for abnormal fluctuations in yield which may indicate extra materials are added to the process or spirit being removed from the process.

2.

Cereals (i) Single Malt – only malted barley is used. (ii) Single Grain – malted barley to which unmalted barley and other whole grains of cereals can be added.

(i) If a malt distillery malts its own barley then check records to ensure no other cereals are received (and then added) to this. If distillery does not malt its own barley then check delivery records to ensure only malted barley is used. (ii) For grain distilleries, check delivery records to ensure that some malted barley is received (or barley malted in distillery). Check mash ingredients to ensure some malted barley is included in each batch and that only whole grains of other cereals are used. Check that no pseudo cereals3 are used (e.g. buckwheat and quinoa).

3 Pseudo cereals are cereals obtained from broadleaf plants that can be ground into flour and used as cereals. True cereals (such as wheat, maize, barley) are grasses.

33

Serial Requirement Check Comments Pass

3.

Mashing Mashing must take place at the distillery.

(i) Check that the cereals are processed into a mash at the distillery. (ii) Check mash bill to ensure that no additional enzymes or fermentable material are added. (iii) Check purchase records to ensure that pre-mashed product is not purchased. (Processors should be informed of the need to make purchase records available when booking their verification visit.)

4.

Fermentation Fermentation must take place at the distillery and only by the addition of yeast.

(i) Check that a wash-back vessel exists at the distillery and is in use. (ii) Check the process and distillery specifications to ensure that fermentation is by yeast only and no enzymes or other fermentable material are added. Grain distilleries may recycle spent wash (known as “back-set”). (iii) Check that only approved processing aids are used and no flavourings are added (e.g. anti-foams, water treatments for ph balance etc).

5.

Distillation (i) Single Malt – only distilled in pot stills from 100% malt mash. (ii) Single Grain – typically distilled in column stills. (iii) Distillation must be at an alcoholic strength by volume (abv) of less than 94.8%.

(i) Check the type of still being used. Spirits distilled in a pot still from anything other than 100% malt mash may only be used in grain whisky. (ii) Check the type of still being used. Spirits distilled in a column still (even if it is from 100% malt mash) can only be used in grain whisky. (iii) Check distillery records to confirm distillation strength and visually check procedures. (iv) Check all alcohol intended for filling as Scotch whisky has been distilled.

34

Serial Requirement Check Comments Pass

6.

Filling and maturation (i) Filling of distilled spirit into casks may take place at the distillery or the spirit may be despatched by tanker to a maturation site and filled into cask there. (ii) Where filling and/or maturation takes place at the distillery, the checks specified under “Maturation” should be carried out.

See check no. 3 under “Maturation”.

7.

Bulk exports (i) Business or individuals may export Scotch whisky in inert containers outside Scotland to be used as an ingredient in foreign whiskies. All processes up to the point of export (fermentation, distillation and maturation) must be assured by HMRC using the above checks. (ii) On or after 23 November 2012, Single Malt Scotch whisky may not be exported in bulk or moved from Scotland.

(i) Check that all production up to the point of export has been carried out by assured processes. (ii) Check to see if Single Malt is exported in bulk on or after 23 November 2012. If so, it can no longer be described as Scotch whisky.

8. Innovative practices Only HMRC approved operations should take place in warehouse.

Check to see if there are any departures from normal industry practice and seek advice from policy team, if necessary.

35

2. Maturation (including filling locations)

Serial Requirement Check Comments Pass

1.

Warehouse (i) The warehouse must be registered with HMRC as a distiller’s warehouse or a ‘permitted place’. (ii) Maturation may only take place in Scotland. (iii) The maturation facility must be able to demonstrate that spirit being matured as Scotch whisky was sourced from a distillery with HMRC-assured processes.

(i) Check HMRC records for compliance. A permitted place is any place to which spirits are moved for: - re-warehousing to another excise warehouse - temporary purposes and periods as allowed by HMRC - scientific research and testing - other premises where goods of the same class or description may be kept, under Customs and Excise Acts - other premises permitted by HMRC. (ii) Check address. (iii) Check what controls are in place to monitor inward shipments.

2.

Casks (i) Scotch whisky must be matured in oak casks. (ii) The capacity of each cask must not exceed 700 litres at any time during maturation.

(i) Check operator’s purchase records to ensure that casks are made of oak. All repairs to casks must be made with oak. Steel bungs are allowed. Traditional cooperage practices (such as charring and de-charring) are allowed. (ii) Check a sample of casks to identify their size. Check operator’s purchase records to identify sizes of casks. (iii) Seek confirmation from operator that casks they have not been rendered inert by glazing, plastic liners etc. (Processors should be informed of the need to make purchase records available when booking their verification visit.)

3.

Filling (i) Casks must be filled only with distilled spirit that will mature into Scotch whisky. No additives are allowed at this stage.

(i) Check procedures to ensure that casks are thoroughly drained of any previous contents before being filled. Check that there is an appropriate procedure in place for emptying casks. (ii) Check procedures to ensure that no substance is added to the inside of the cask before being filled e.g. paxarette, boisé, sugar, caramel, oak chips, wooden structures (whether oak or not).

36

Serial Requirement Check Comments Pass

4.

Ageing (i) Scotch whisky needs to be matured for at least three years. (ii) It can be marketed with different maturities (ages).

(i) Check the maturer’s record keeping process to understand how they log the ageing of a cask. (ii) Check that the maturer has a fit-and-proper system of tracking ages of casks. (iii) Check that the maturer has adequate measures to ensure the ageing process is not interrupted: - leaks or evaporative losses do not cause any problems for the age of the spirit left in the cask; - the contents of a cask may be re-racked into another empty cask for further ageing, but re-racking should normally take place immediately in order to ensure proper control of maturation periods; and - topping up of casks with younger spirit is not allowed – “marrying in cask” is allowed to continue.

5.

Bulk exports (i) Business or individuals may export Scotch whisky in inert containers outside Scotland to be used as an ingredient in foreign whiskies. All processes up to the point of export (fermentation, distillation and maturation) must be assured by HMRC using the above checks. (ii) On or after 23 November 2012, Single Malt Scotch whisky may not be exported in bulk or moved from Scotland.

(i) Check that all production up to the point of export has been carried out by assured processes. (ii) Check to see if Single Malt is exported in bulk on or after 23 November 2012. If so, it can no longer be described as Scotch whisky.

5. Innovative practices Only HMRC approved operations should take place in warehouse.

Check to see if there are any departures from normal industry practice and seek advice from policy team, if necessary.

37

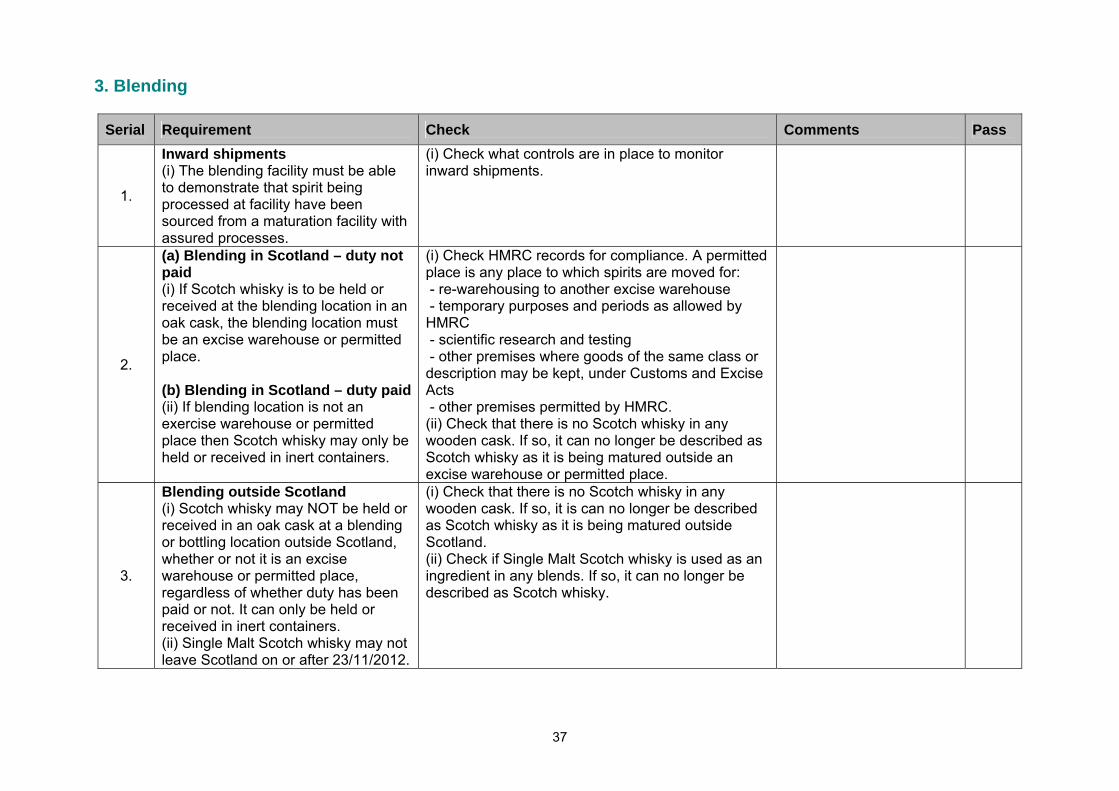

3. Blending

Serial Requirement Check Comments Pass

1.

Inward shipments (i) The blending facility must be able to demonstrate that spirit being processed at facility have been sourced from a maturation facility with assured processes.

(i) Check what controls are in place to monitor inward shipments.

2.

(a) Blending in Scotland – duty not paid (i) If Scotch whisky is to be held or received at the blending location in an oak cask, the blending location must be an excise warehouse or permitted place. (b) Blending in Scotland – duty paid(ii) If blending location is not an exercise warehouse or permitted place then Scotch whisky may only be held or received in inert containers.

(i) Check HMRC records for compliance. A permitted place is any place to which spirits are moved for: - re-warehousing to another excise warehouse - temporary purposes and periods as allowed by HMRC - scientific research and testing - other premises where goods of the same class or description may be kept, under Customs and Excise Acts - other premises permitted by HMRC. (ii) Check that there is no Scotch whisky in any wooden cask. If so, it can no longer be described as Scotch whisky as it is being matured outside an excise warehouse or permitted place.

3.

Blending outside Scotland (i) Scotch whisky may NOT be held or received in an oak cask at a blending or bottling location outside Scotland, whether or not it is an excise warehouse or permitted place, regardless of whether duty has been paid or not. It can only be held or received in inert containers. (ii) Single Malt Scotch whisky may not leave Scotland on or after 23/11/2012.

(i) Check that there is no Scotch whisky in any wooden cask. If so, it is can no longer be described as Scotch whisky as it is being matured outside Scotland. (ii) Check if Single Malt Scotch whisky is used as an ingredient in any blends. If so, it can no longer be described as Scotch whisky.

38

Serial Requirement Check Comments Pass

4.

Additions Nothing should be added during blending other than water and plain caramel colouring.

(i) Check the operators purchase records to ensure that the type of colouring is only plain caramel colouring E150A. Burnt sugar cannot be used for colouring purposes. (ii) Check procedures to ensure that no flavourings or other substances are added. Yeast cannot be added at blending stage. (Processors should be informed of the need to make purchase records available when booking their verification visit.)

5.

Types of blends There are five different categories of Scotch whisky. (i) Single Malt Scotch – must not be blended with any whisky other than Single Malt from the same distillery. (ii) Single Grain Scotch – must not be blended with any whisky other than Single Grain from the same distillery. (iii) Blended Scotch – is a blend of one or more Single Malt with one or more Single Grain Scotch whiskies. (iv) Blended Malt Scotch – is a blend of two or more Single Malt Scotch whiskies. (v) Blended Grain Scotch – is a blend of two or more Single Grain Scotch whiskies.

(i) Check and assure that the blender’s record keeping and tracking of Scotch whisky allows them to blend different whiskies that are consistent with the five definitions. (ii) Ensure that the blender has adequate control mechanisms to keep such blends separate so as not to interfere with each other. (iii) Does blender only blend own whiskies or do they buy in whiskies from other distilleries to blend? If so, check purchases of other whiskies match those used in blend recipes. (Processors should be informed of the need to make purchase records available when booking their verification visit.)

39

Serial Requirement Check Comments Pass

6.

Age of blends Within each category blenders can blend different ages of Scotch whisky. The age of the blend is that of the youngest of each constituent whisky.

(i) Check the production and record keeping process to ensure that ages of each ingredient of the blend are recorded and that only the youngest of those ages is used to describe the blend. (ii) Check the declared ages of purchased and own whiskies to ensure they match what is entered in the production records. (iii) If the age of the blend is not stated, the minimum age is 3 years. (Processors should be informed of the need to make purchase records available when booking their verification visit.)

7.

Strength The alcohol strength by volume is at least 40%.

(i) Ensure that the operator has a process of checking the alcohol strength during the blending stage to assure that the addition of water and/or plain caramel colouring does not dilute the blend to below 40% abv.

8.

Bulk exports (i) Business or individuals may export Scotch whisky in inert containers outside Scotland to be used as an ingredient in foreign whiskies. All processes up to the point of export must be assured by HMRC using the above checks. (ii) On or after 23 November 2012, Single Malt Scotch whisky may not be exported in bulk or moved from Scotland.

(i) Check that all production up to the point of export has been carried out by assured processes. (ii) Check to see if Single Malt is exported in bulk on or after 23 November 2012. If so, it can no longer be described as Scotch whisky.

40

Serial Requirement Check Comments Pass

9.

Certificates of Verification Bulk product may be exported in bulk to be bottled outside Scotland. Producers may request copy Certificates of Verification to use with each shipment. (i) Certificates may only be used by producers who have obtained verification of their processes and published as such on the HMRC website. (ii) Certificates may only be used by producers for verified brands that have been published as such on the HMRC website.

(i) Check producer’s processes to ensure that certificates are only used if all processes are verified. Check if producer has a fir-for-purpose record keeping system to allow HMRC to trace certificates on request of an overseas authority. (ii) Check a sample of issued certificates to ensure they are only issued for brands verified by HMRC.

10.

Innovative practices Only HMRC approved operations should take place in an excise warehouse.

Check to see if there are any departures from normal industry practice and seek advice from policy team, if necessary.

41

4. Labelling of final product (including bottling)

Serial Requirement Check Comments Pass

1.

Inward shipments (i) The bottling/labelling facility must be able to demonstrate that spirit being processed at facility have been sourced from a maturation facility with assured processes.

(i) Check what controls are in place to monitor inward shipments.

2.

(a) Bottling in Scotland – duty not paid (i) If Scotch whisky is to be held or received at the bottling location in an oak cask, the bottling location must be an excise warehouse or permitted place. (b) Bottling in Scotland – duty paid (ii) If bottling location is not an excise warehouse or permitted place then Scotch whisky may only be held or received in inert containers.

(i) Check HMRC records for compliance. A permitted place is any place to which spirits are moved for: - re-warehousing to another excise warehouse - temporary purposes and periods as allowed by HMRC - scientific research and testing - other premises where goods of the same class or description may be kept, under Customs and Excise Acts - other premises permitted by HMRC. (ii) Check that there is no Scotch whisky in any wooden cask. If so, it can no longer be described as Scotch whisky as it is being matured outside an excise warehouse or permitted place.

3.

Bottling outside Scotland (i) Scotch whisky may NOT be held or received in an oak cask at a blending or bottling location outside Scotland, whether or not it is an excise warehouse or permitted place, regardless of whether duty has been paid or not. It can only be held or received in inert containers. (ii) Single Malt Scotch whisky may not leave Scotland on or after 23/11/2012.

(i) Check that there is no Scotch whisky is in any wooden cask. If so, it can no longer be described as Scotch whisky as it is being matured outside Scotland. (ii) Check if Single Malt Scotch whisky is used as an ingredient in any blends or being bottled separately. If so, it can no longer be described as Scotch whisky.

42

Serial Requirement Check Comments Pass

4.

Additions (i) Scotch whisky can be transported in bulk to the place of bottling at high alcoholic strength. The bottler may only add water to dilute the product to bottling strength and plain caramel colouring (E150a) to adjust colour.

(i) Check the manufacturing process to ensure that no other additives are introduced. If water and/or plain caramel colouring is added, ensure alcoholic strength is not reduced below 40% vol. Natural water or tap water is permitted provided it meets EU standards. (iii) Check what control mechanisms exist to ensure abv ≥ 40%.

5.

Labelling – Requirements (i) All Scotch whisky must be labelled as belonging to one of five categories. (ii) The name of a distillery may be used if the whole whisky was distilled in a single distillery. (iii) The name of a locality or region may be used if the whole whisky was distilled in the region or locality named or, in the case of a blend from more than one region or locality, all the regions or localities represented in the blend are identified. Names of defined localities are: Campbeltown and Islay. Names of defined regions are: Highland, Lowland and Speyside. Other locality or region names may be used provided they are accurate, e.g. Mull, Skye,

(i) Check that the operator has reasonable control mechanisms to keep different blends of Scotch whisky separate so as not to mix and incorrectly label a batch. Five categories are: - Single Malt Scotch whisky - Single Grain Scotch whisky - Blended Malt Scotch whisky - Blended Grain Scotch whisky - Blended Scotch whisky (ii) Check that all constituent parts of a single whisky originate from a single distillery – can be verified from movement details. Single Malt Scotch whisky may only be bottled in Scotland on or after 23/11/2012. (iii) Check that all constituent parts of a whisky described as originating from a particular locality or region/localities or regions – can be verified from movement or blending records. (Speyside whiskies are a subset of Highland whiskies and may be described as Speyside or Highland).

43

Serial Requirement Check Comments Pass

6.

Labelling – Design (i) The category description must be displayed on any individual container and displayed as prominently as any other description. (ii) The category description can be preceded by the name of a locality or region but not interfered with in any other way with overlays or underlays of other words or pictures. (iii) The words pure must not be used adjectivally in connection with the word ‘malt’. (iv) The age of whisky can only be expressed in years. (v) Date of distillation can only be stated if (a) it is in the form of a calendar year; (b) the whole whisky was distilled in that year; and (c) the year of bottling or the maturation period is stated in the same field of vision. (vi) Label must not contain reference to any other number that can be misinterpreted to mean the above.

(i) Check the label template for the single and blended whiskies bottled by the operator for compliance. (ii) The word pure can be used on labels in relation to matters other than malt e.g. “pure water”. (iii) Only names which identify a specific locality or region may precede the category name. “Highland Single Malt Scotch whisky” is an acceptable category description, but “Island Single Malt Scotch whisky” or “North Highland Single Malt Scotch whisky” are not. Reference to such terms elsewhere on the label is acceptable provided they can be justified.

7.

Brand names (i) The operator responsible for labelling of the final product will submit names of verified brands to HMRC for publishing.

(i) Check that the producer has adequate record keeping systems to ensure that the product being bottled has been verified up to that point. (ii) Check that the producer has processes to notify HMRC when it identifies a brand is no longer compliant i.e. the previous production process is not assured. (iii) Check that the producer retains sufficient records to allow the product to be traced back to the previous production process.

44

Serial Requirement Check Comments Pass

8. Certificates of Verification See check No 8 under Blending

See check No 8 under Blending

9.

Innovative practices Only HMRC approved operations should take place in an excise warehouse.

Check to see if there are any departures from normal industry practice and seek advice from policy team, if necessary.

45

Annex D: Certificate of Verification Certificate of Verification for Scotch whisky

No. 123456

Notes:

1. This certificate is issued by HM Revenue & Customs (HMRC), a government department of the UK, on condition that all facilities used in the production of the under mentioned products have been inspected by HMRC and found to comply with the requirements to produce Scotch whisky.

2. This certificate is for use only by the producer to whom it has been issued and on condition that it will not be reproduced or quoted on any label or in any advertisement.

3. Column 3 is to be completed for products in final bottle state. Column 8 should only be completed where an age greater than three years is claimed. All other sections must be completed.

To whom it may concern,

I/We . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …………………………….(name and address of exporting producer/consignor)

declare that the spirits contained in the under mentioned . . . . . . . . . . . . . ... . . . .….. . . . . . (number in words)

packages which were/will be* delivered for exportation to . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …. .... .. . . . (name and address of consignee)

to be imported by . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …………………………………………………………………………………..(name and address of importer)

on . . . . . . . . . . . ……………………………………………………………………………………………... (date).

• are Single Malt / Single Grain / Blended Malt / Blended Grain / Blended* Scotch whisky • matured in oak casks in Scotland for a period of not less than three years • have been produced in compliance with UK laws regulating the production of Scotch whisky for home consumption, and • conform to the requirements of Regulation (EC) No 110/2008 for spirits produced in the EU and the related Scotch whisky Technical File.

Particulars of Scotch whisky to be exported

Number and description of packages (1)

Number of bottles (2)

Bottling date and rotation

(3)

Name of verified bottled

product or category of verified bulk product (4)

Strength of spirit (abv)

(5) Litres of spirit

(6) Litres of

alcohol (7) Period of

maturation in years (8)

I/We confirm that the aforementioned Scotch Whiskies have been verified by HMRC as compliant with UK and EU law.

Signed . . . . . . . . . . . . . . . . . . . . . . . . . ………(proprietor / partner / director / secretary / duly authorised person*)

*delete as appropriate

Date . . . . . . . . …………………………………………….. . . . . . . . . . . . . . . . . . . . . …………………….. . . .

I certify that the Scotch Whiskies described above have been verified by HMRC and the above details can be substantiated from industry production records.

Officer of HMRC

HM Revenue & Customs, Scotch Whisky Verification, Portcullis House, 21 India Street, Glasgow, G2 4PZ

www.hmrc.gov.uk/scotchwhisky