How Do I Stay on Track? Monitoring and Control Requires: Identifying factors critical to success Measuring performance Defining standards of expected.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

How Do I Stay on Track?

Monitoring and Control Requires:

• Identifying factors critical to success• Measuring performance• Defining standards of expected performance• Comparing actual and expected performance• Assessing need for and type of adjustment

Monitoring and Control Process

DoesPerformance Match

Standards?

DetermineWhat toMeasure

EstablishStandards

MeasurePerformance Continue

Monitoring

Yes

Devise StrategyDetermine Critical Success Factors

No

OperationsProblem?

TakeCorrective

Action

Yes

• Internal?• Financial?

• Customers?• Innovation

and Learning?

No

Identifying Critical Success Factors• The few key areas or activities where things must go

well if vision is to be achieved • Should focus on answering:– How do owners see us? (Financial perspective)– How do customers see us? (Customer perspective)– What must we excel at?(Internal perspective)– Can we continue to improve and create value? (Innovation

and learning perspective)

Determining What to Measure• What information is needed to determine how

stakeholders see us?• If the information is gathered, how will it affect

the decision-making process?– Preliminary controls– Concurrent controls– Feedback controls

• When should the measures be taken to be useful?

Controls Should. . .• Involve only the minimum amount of information

needed to give a reliable picture of events.• Monitor only meaningful activities and results,

regardless of measurement difficulty.• Be timely.• Be long-term and short-term.• Pinpoint exceptions (trigger action).• Be used to reward rather than punish.

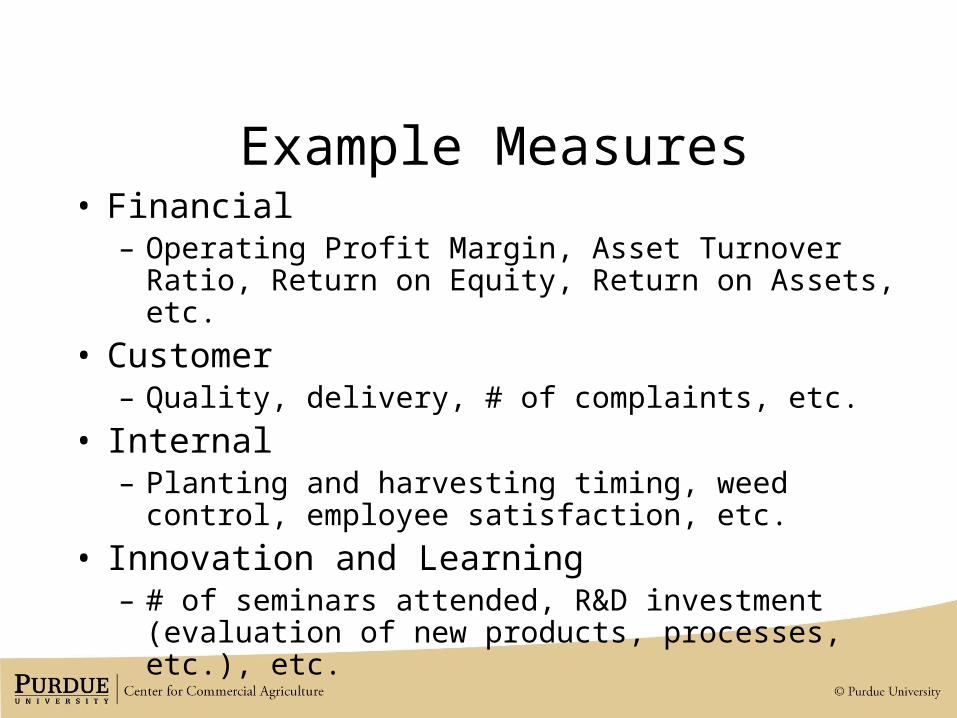

Example Measures• Financial– Operating Profit Margin, Asset Turnover Ratio, Return on

Equity, Return on Assets, etc.• Customer– Quality, delivery, # of complaints, etc.

• Internal– Planting and harvesting timing, weed control, employee

satisfaction, etc.• Innovation and Learning– # of seminars attended, R&D investment (evaluation of new

products, processes, etc.), etc.

Defining Standards of Performance

• Benchmarking– Looking for those businesses that are the best at

doing something and learning how they do it so that we might emulate their methods

Benchmarking: How?• Identify the area or process to be examined.– Should be an activity that has potential for competitive

advantage• Find behavioral and/or output measures of the are or

process to obtain measurements.• Select an accessible set of competitors and best-in-class

companies to benchmark.– Performing similar activities– Not necessarily in agriculture

Benchmarking Principles

• Be sure to understand and appreciate the differences between business environment and cultures.

• Understand how the aspect that is being studied fits with the other elements of the firm.

Monitoring and Taking Action• Are we meeting the standard?– If yes, continue to monitor or move to next level.– If no, is the performance gap due to extenuating

circumstances?• Wait and measure again, but be careful!

– If no, is the performance gap due to operational breakdowns?• Take corrective measures to fix the problem.

– If no, is the performance gap due to changes in the firm’s external or internal environment?• Assess strategic position and prepare new strategy

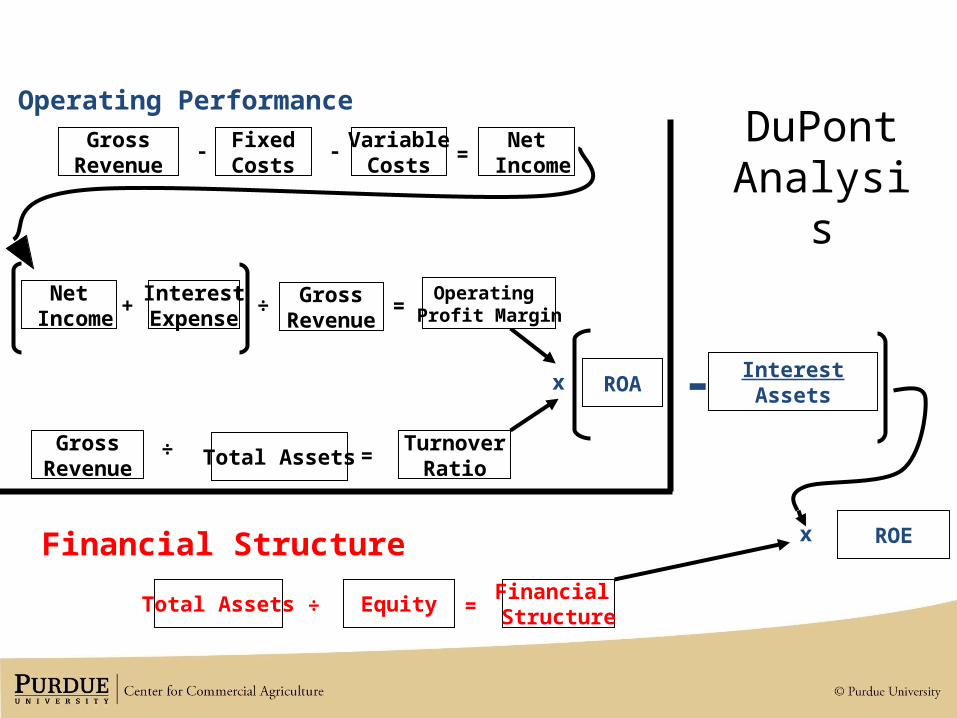

Using Dupont Analysis in Monitoring and Control

Operating PerformanceGross

RevenueFixedCosts

VariableCosts

Net Income

- - =

Total AssetsGross

RevenueTurnover

Ratio=÷

ROAx

InterestExpense

Net Income

GrossRevenue

Operating Profit Margin+ ÷ =

Total Assets EquityFinancial Structure=

Financial Structure

÷

ROE

InterestAssets-

x

DuPont Analysis

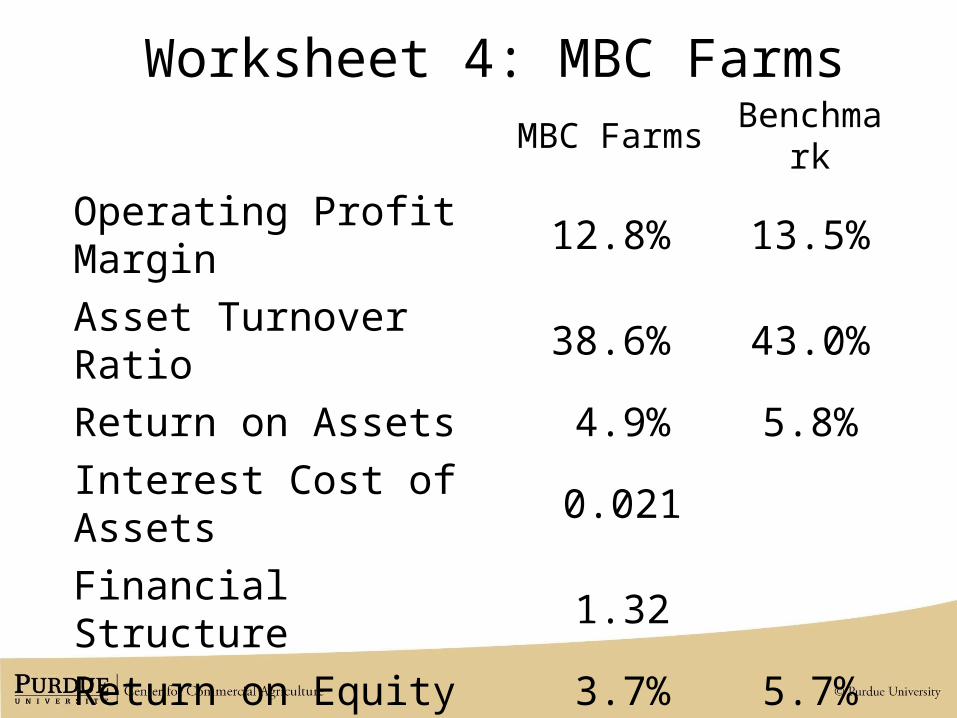

Worksheet 4: MBC FarmsFinancial Data

1. Gross Revenue

$1,796,651

2. Fixed Costs385,638

3. Variable Costs1,280,494

4. Net Income130,519

5. Total Farm Assets

4,655,476

6. Owner's Equity

3,534,037

7. Interest Expense

98,716

Worksheet 4: MBC FarmsMBC Farms

Benchmark

Operating Profit Margin

12.8% 13.5%

Asset Turnover Ratio 38.6% 43.0%Return on Assets 4.9% 5.8%Interest Cost of Assets

0.021

Financial Structure 1.32Return on Equity 3.7% 5.7%

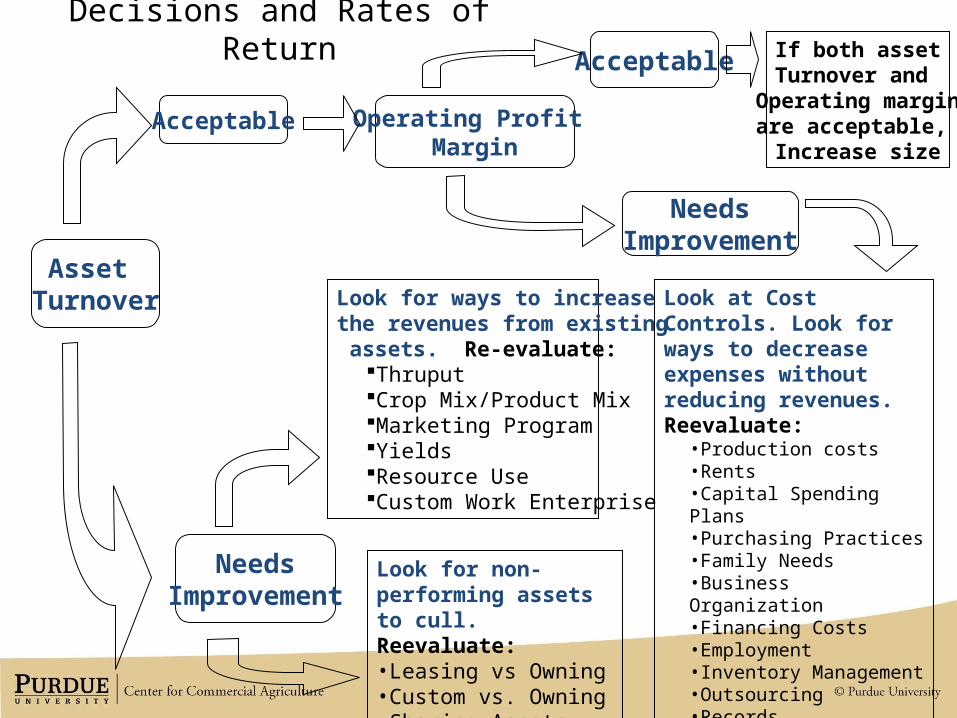

Decisions and Rates of Return

Asset Turnover

NeedsImprovement

Look for ways to increase the revenues from existing assets. Re-evaluate:

ThruputCrop Mix/Product MixMarketing ProgramYieldsResource UseCustom Work Enterprise

Look for non-performing assets to cull. Reevaluate:•Leasing vs Owning•Custom vs. Owning•Sharing Assets

Acceptable Operating Profit Margin

Acceptable

NeedsImprovement

Look at Cost Controls. Look for ways to decrease expenses without reducing revenues. Reevaluate:

•Production costs•Rents•Capital Spending Plans•Purchasing Practices•Family Needs•Business Organization•Financing Costs•Employment•Inventory Management•Outsourcing•Records•Control Procedures•Management Priorities

If both assetTurnover and

Operating marginare acceptable,

Increase size

Linking Ideas & Actions• Action Steps– Behavior Controls

• Policies, rules, and SOP’s to get an idea implemented– Output Controls

• Using objectives and performance targets to achieve an idea

• Resources– People– Financial– Equipment– Information

Linking Ideas & Actions• Responsible Individual• Performance Monitor• Time Table• Corrective Adjustments

Exercise• Work on the action plan table.• Try to identify critical actions/controls.– Include both behavioral and output actions.– Make sure to identify the resources need to

accomplish the action.– Make someone be responsible for the action.– Determine how you will measure achievement.– Think of the responsible person’s authority to take

corrective action.

Strategic Business Planning for Commercial Producers

Related Documents