Akhil Prakash PGP 14005 Amitava Chaudhuri PGP 14006 Davinder Yadav PGP 14015 Rinesh Jain PGP 14039 Rishank Gupta PGP 14040 1 Strategy Analysis of Hindalco Industries Ltd.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Akhil Prakash PGP 14005Amitava Chaudhuri PGP

14006Davinder Yadav PGP

14015Rinesh Jain PGP 14039

Rishank Gupta PGP 14040Sudhanshu Singh PGP

14051

1

Strategy Analysis of Hindalco Industries Ltd.

HINDALCO Overview Established in 1958 as Hindustan Aluminium Corporation Limited

(HACL) The production of aluminium commenced at Renukoot, U.P. in 1962 In 1989, it was restructured and renamed HINDALCO HINDALCO went through a series of acquisitions and mergers (total

7) between 2002-2007 with Indal, Birla Copper, The Nifty, Mt. Gordon copper mines to strengthen its position as a global player

In 2007, it acquired Novelis Inc. making it the 5th largest aluminium producer worldwide

Today HINDALCO has its presence in 11 countries. Annual turnover FY’14 – USD 14.5 Billion (Rs. 876.95 crore)References: http://www.hindalco.com/about-us

2

Global Aluminium Industry Overview

Multipurpose metal industry with several key benefits Presence in Infrastructure building, heavy industry, wide variety

of consumer goods industries from kitchenware to automobiles Global aluminium consumption grew by 7% annually powered mainly

by ASIA The value chain consists of three key business areas –

1. Bauxite mining2. Aluminium production3. Manufacture of value added products

Four different business models1. Upstream companies2. Production companies3. Downstream companies4. Integrated giants 3

SWOT AnalysisStrengths

Cost and operational effectivenesshigh degree qualityExpansion capacity Integrated production facility well-established distribution network

WeaknessesProduction capacity is not adequateFace huge cash outflowTechnology up gradation up to the level of its competitors is missing

OpportunitiesRecycling should be adopted as routine productionDownstream production of value added products Increasing aluminum production

ThreatsGlobal competitors, such as TATA, POSCO, MITTAL, ESSAR Falling sales of copper in global market.Fall in price of AlInnovative revolution in plastic and steel industry

References: http://www.slideshare.net/vibhach/hindalco-industries http://hindalcoindustrieslimited.blogspot.in/2010/12/swot-analysis-of-hindalco.html.

4

Mission – Vision – Values

VISION - To be a premium metals major, global in size and reach, excelling in everything we do, and creating value for its stakeholders.

MISSION - To relentlessly pursue the creation of superior shareholder value, by exceeding customer expectation profitably, unleashing employee potential, while being a responsible corporate citizen, adhering to our values.

VALUES – 1. Integrity – Honesty in every action2. Commitment – Deliver on the promise3. Passion – Energised action4. Seamlessness – Boundary less in letter and spirit5. Speed – One step ahead always

References:http://www.hindalco.com/vision-and-values

5

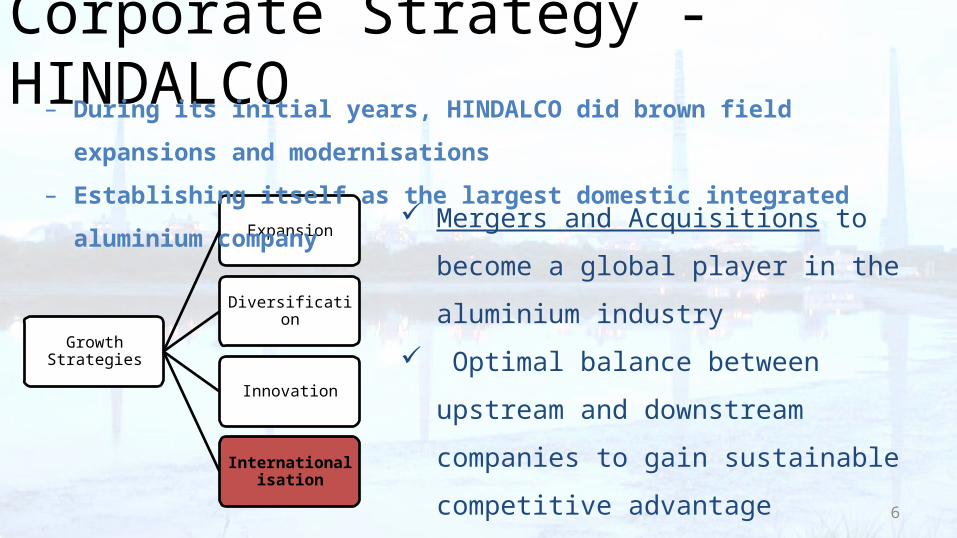

Corporate Strategy - HINDALCO

Mergers and Acquisitions to become a global player in the aluminium industry

Optimal balance between upstream and downstream companies to gain sustainable competitive advantage Upstream – Commodity markets Downstream – Manufacturing enterprises

Growth Strategies

Expansion

Diversification

Innovation

Internationalisation

– During its initial years, HINDALCO did brown field expansions and modernisations

– Establishing itself as the largest domestic integrated aluminium company

6

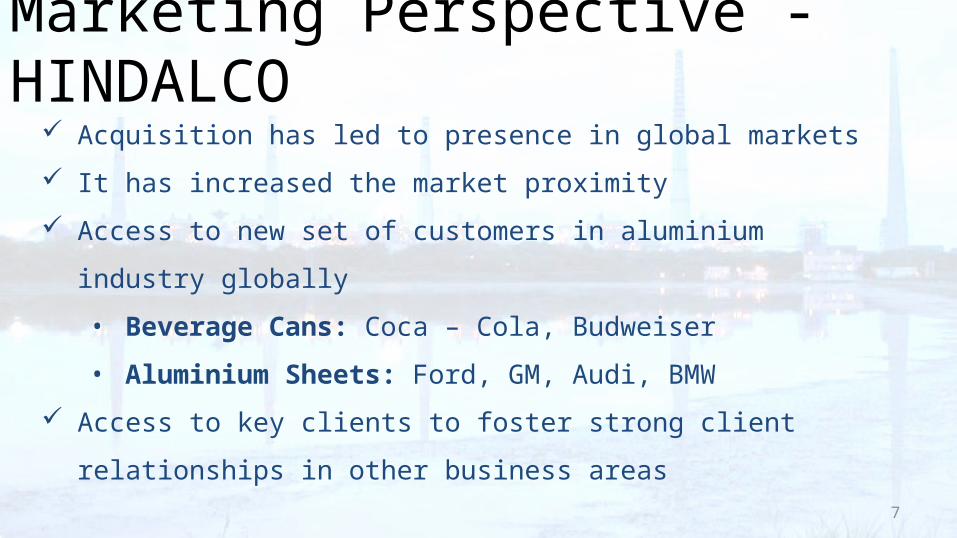

Marketing Perspective - HINDALCO

Acquisition has led to presence in global markets It has increased the market proximity Access to new set of customers in aluminium

industry globally• Beverage Cans: Coca – Cola, Budweiser• Aluminium Sheets: Ford, GM, Audi, BMW

Access to key clients to foster strong client relationships in other business areas

7

Operational Perspective - HINDALCO

Acquisition of both upstream and downstream companies to gain following operational advantages :

1. Upstream Companies Economies of size – low cost of production Economies of scale – consistent profits Access to cutting edge technologies

2. Downstream Companies Value addition by companies and conversion of

aluminium into recognizable customer products Improved quality and delivery

8

Financial Perspective - HINDALCOUpstream companies – Commodity

MarketsAdvantages

Higher profitability gains from the upstream markets

Disadvantages High Volatility in Upstream

markets Prices set on London stock

exchange

Downstream companies- Manufacturing Advantages

Manufacturing enterprises Low volatility in downstream

markets Increase profits consistently

Disadvantages Lower profit margins from

downstream markets

9

Mar '14 Mar '13 Mar '12 Mar '11 Mar '10 Mar '09 Mar '08 Mar '07 Mar '06 Mar '05

Total Debt 63,348.35

56,298.91

40,858.55

29,365.87

23,998.70

26,366.95

24,144.77

14,571.91 7,271.50 6,356.9

0 Debt Equity

Ratio 0.72 0.72 0.46 0.24 0.23 0.35 0.48 0.59 0.51 0.5

Earning Retention

Ratio88.59 84.23 85.72 87.04 82.57 88.17 89.78 93.16 86.07 84.47

Reported Net Profit 1,413.33 1,699.20 2,237.20 2,136.92 1,915.63 2,230.27 2,860.94 2,564.33 1,655.55 1,329.3

6

Market Cap 36733.15 33430.534

31491.061

29696.142

27907.843

23754.486

17296.397

12417.584

9606.2084

7666.587References:

http://www.moneycontrol.com/india/stockpricequote/aluminium/hindalcoindustries/HI

Thank You !!

10

Questions Please ??

Related Documents