Higher Education: Improved Tax Information Could Help Families Pay for College (GAO-12-560) Presentation at the 30 th Annual SFARN Conference June 21, 2013 Page 1

Higher Education: Improved Tax Information Could Help Families Pay for College (GAO-12-560) Presentation at the 30 th Annual SFARN Conference June 21,

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Higher Education: Improved Tax Information Could Help Families Pay

for College (GAO-12-560)

Presentation at the 30th Annual

SFARN Conference

June 21, 2013

Page 1

Research Objectives

1) Assess the extent to which tax filers select higher education provisions that maximize their tax benefit.

2) Describe the size and distribution of Title IV student aid and tax expenditures available to assist students and their families with higher education expenses.

3) Summarize what is known about the effect of student aid and tax expenditures on student outcomes.

Page 2

Scope and Methodology

• Analyzed data from the Department of Education, the Internal Revenue Service (IRS), and the Board of Governors of the Federal Reserve.

• Conducted a literature review for original empirical research.

Page 3

Background• The federal government

provides billions of dollars in assistance each year to help millions of students and families meet the costs of higher education.

• We reviewed a variety of Title IV programs and tax expenditures administered by the Department of Education and the Department of Treasury.

Page 4

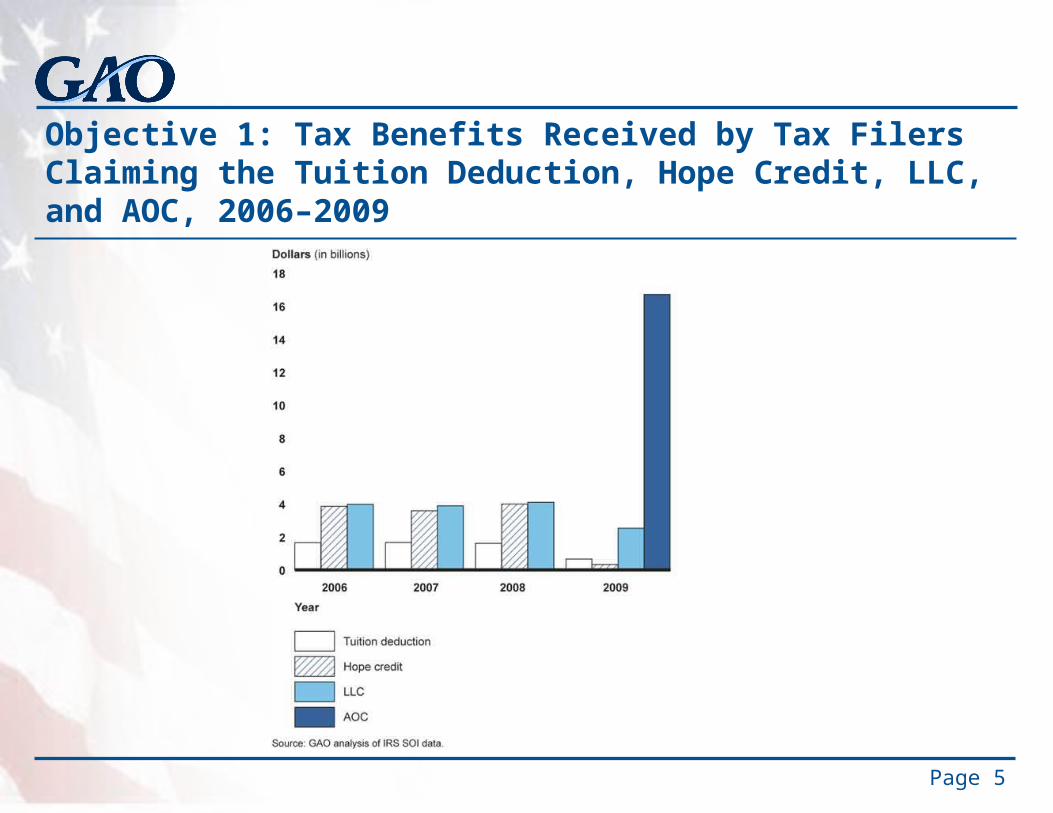

Amount of Benefits from Selected Title IV Programs and Tax Expenditures That Pay for Current Expenses, 2006 – 2009

Objective 1: Tax Benefits Received by Tax Filers Claiming the Tuition Deduction, Hope Credit, LLC, and AOC, 2006–2009

Page 5

Objective 1: Suboptimal Choice Analysis

• Some taxpayers may not maximize benefits• Failure to claim any credit or deduction• Choosing a credit or deduction that yields less of a tax

benefit than another provision would• Included calculation of impact on state tax liability

Page 6

Objective 1: Limitations

• Couldn’t analyze all returns• tax filers who appeared eligible for the LLC or tuition

deduction in 2009• had a 1098-T with information on the student’s education

expenses• had a tax liability after claiming other tax benefits.

• Couldn’t analyze American Opportunity Credit because of lack of information

Page 7

Objective 1: Limitations (2)

• Assumption of accurate information on the 1098-T.

• Some students may not have been eligible to claim credits because expenses were covered by other sources (529 distribution, employers, outside scholarships)

Page 8

Objective 1: Federal Tax Benefit

Claiming no credit or deduction Claimed the LLC instead of the tuition deduction Claimed the tuition deduction instead of the LLC0

5

10

15

20

25

30

35

40

45

Percent of eligible taxpayers making a suboptimal choice at the federal level

Percent of eligible taxpayers making a suboptimal choice at the federal level

Page 9

Objective 1: Federal Tax Benefit (2)

Page 10

Claim

ing n

o cr

edit

or d

educ

tion

Claim

ed th

e LL

C inst

ead

of th

e tu

ition

dedu

ction

*

Claim

ed th

e tu

ition

dedu

ction

inst

ead

of th

e LL

C

$- $50

$100 $150 $200 $250 $300 $350 $400 $450 $500

Average amount tax filer failed to increase their federal tax benefit

*Sample size is too small to estimate the average amount the tax filers failed to increase their tax benefit.

Objective 1: State Tax Benefit

• Choosing deduction lowers AGI, which can reduce state income tax liability enough to compensate for higher federal income tax paid.

• About one third of those that made a suboptimal federal choice by choosing a deduction actually maximized their combined federal and state tax benefit.

Page 11

Objective 1: Factors Contributing to Suboptimal Decisions

• Unaware of tax provisions or misunderstanding eligibility rules.

• Number of provisions.

• Similarity of provisions.

• Differences in key definitions.

• Coordination with other tax provisions.

Page 12

Objective 1: Reducing Suboptimal Choices

• Educating tax filers

• Educating tax preparers

• Developing tools to help tax filers make better choices

• Improving tax preparation software

Page 13

Objective 2: Substantial Aid to Populations Across Income Levels

• In 2009, 12.8 million students received Title IV aid and approximately 18 million tax filers claimed a higher education tax benefit for current expenses.

• Title IV grants tend to benefit students and families with incomes below the national median, while loans and work-study also benefit those with income above the median.

• The tuition and fees deduction and parental exemption mostly benefit households with incomes above $60,000, whereas the majority of benefits from other tax expenditures went to households with lower incomes.

Page 14

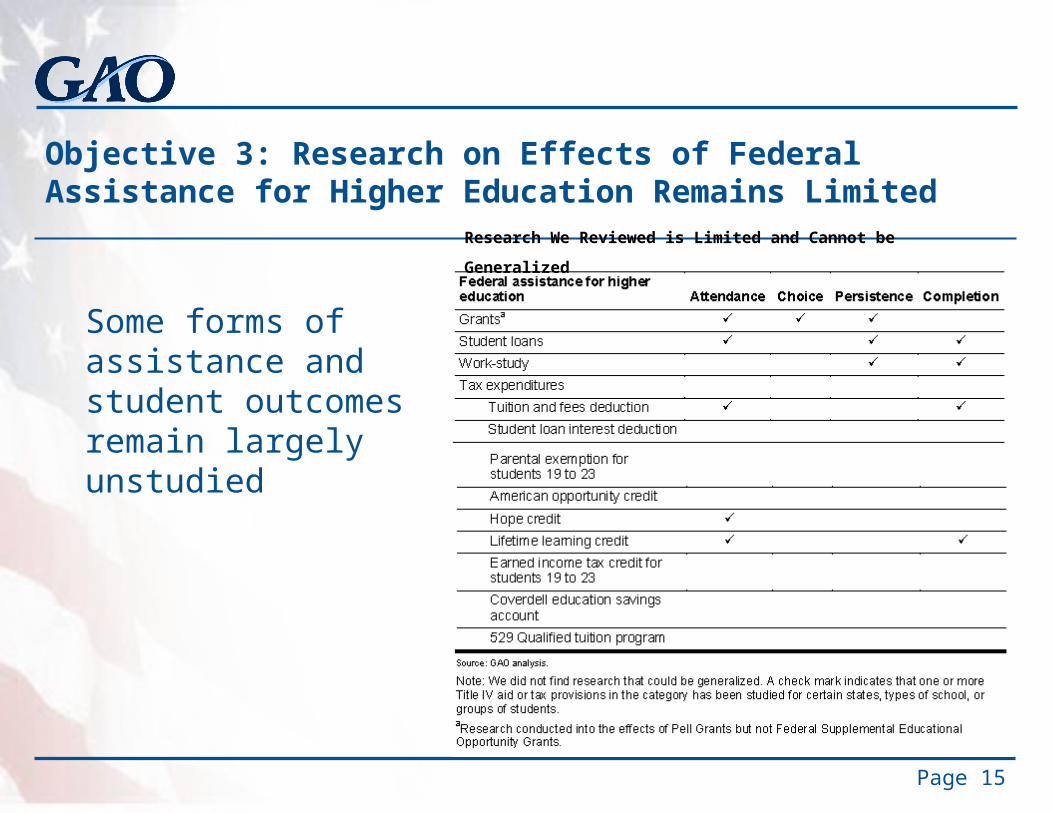

Objective 3: Research on Effects of Federal Assistance for Higher Education Remains Limited

Some forms of assistance and student outcomes remain largely unstudied

Page 15

Research We Reviewed is Limited and Cannot be Generalized

Objective 3: Data and Methodological Challenges Remain Persistent Obstacles to Research

• Data on Title IV programs are fragmented and not routinely available; data on tax expenditures are subject to privacy restrictions or are not collected by IRS.

• Opportunities to measure the effects of federal assistance are limited.

Page 16

Recommendations

1) GAO recommends that IRS and the Department of Education work together to develop a strategy to improve information provided to tax filers who appear eligible to claim a tax provision but do not.

2) GAO recommends that the Department of Education take advantage of recent and anticipated program changes to sponsor and conduct evaluative research into the effects of Title IV programs and higher education tax expenditures at improving student outcomes.

Page 17

Page 18

Related work:2013 Annual Report: Actions Needed to Reduce Fragmentation, Overlap, and Duplication and Achieve Other Financial Benefits. GAO-13-279SP. Washington, D.C., April 9, 2013.

Higher Education: Improved Tax Information Could Help Pay for College. GAO-12-863T. Washington, D.C.: July 25, 2012.

Higher Education: Multiple Higher Education Tax Incentives Create Opportunities for Taxpayers to Make Costly Mistakes. GAO-08-717T. Washington, D.C., May 1, 2008.

Postsecondary Education: Multiple Tax Preferences and Title IV Student Aid Programs Create a Complex Education Financing Environment. GAO-07-262T. Washington, D.C., December 5, 2006.

Student Aid and Postsecondary Tax Preferences: Limited Research Exists on Effectiveness of Tools to Assist Students and Families through Title IV Student Aid and Tax Preferences. GAO-05-684. Washington, D.C.: July 29, 2005.

GAO on the WebWeb site: http://www.gao.gov/

CopyrightThis is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

Page 19

Related Documents