Panel on Delinquency and Default Measures Student Financial Aid Research Network (SFARN) Portland, OR June 20-21, 2013

Panel on Delinquency and Default Measures Student Financial Aid Research Network (SFARN) Portland, OR June 20-21, 2013.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Panel onDelinquency and Default Measures

Student Financial Aid Research Network (SFARN)Portland, ORJune 20-21, 2013

Panelists

Sean Simone (Panel Chair)

Statistician & Associate Project Officer, National Postsecondary Student Aid Study

National Center for Education Statistics, U.S. Department of Education

Alisa CunninghamSenior AssociateInstitute for Higher Education Policy

Jeff WebsterAssistant Vice President, Research and Analytical ServicesTexas Guaranteed Student Loan Corporation

Jennie WooSenior Research AssociateRTI International

Agenda

• 3 Propositions on Delinquency/Default Measures

• Panelist Responses• Open Discussion

Proposition #1

Challenges remain in measuring delinquency and/or default due to specialized business practices for student loans.

• Default– To fail to fulfill a contract, agreement, or

duty.– Examples include:

• To fail to meet a financial obligation and

• To fail to do something required by law.

• Delinquency– A debt on which payment is due.

Proposition #1Definitions

• In practice there are business practices and legal requirements for administering FFEL and Direct Loans:– Delinquency is identified after 60 days of

nonpayment, but this may be difficult to measure.

– Default is identified after 270 days of nonpayment.

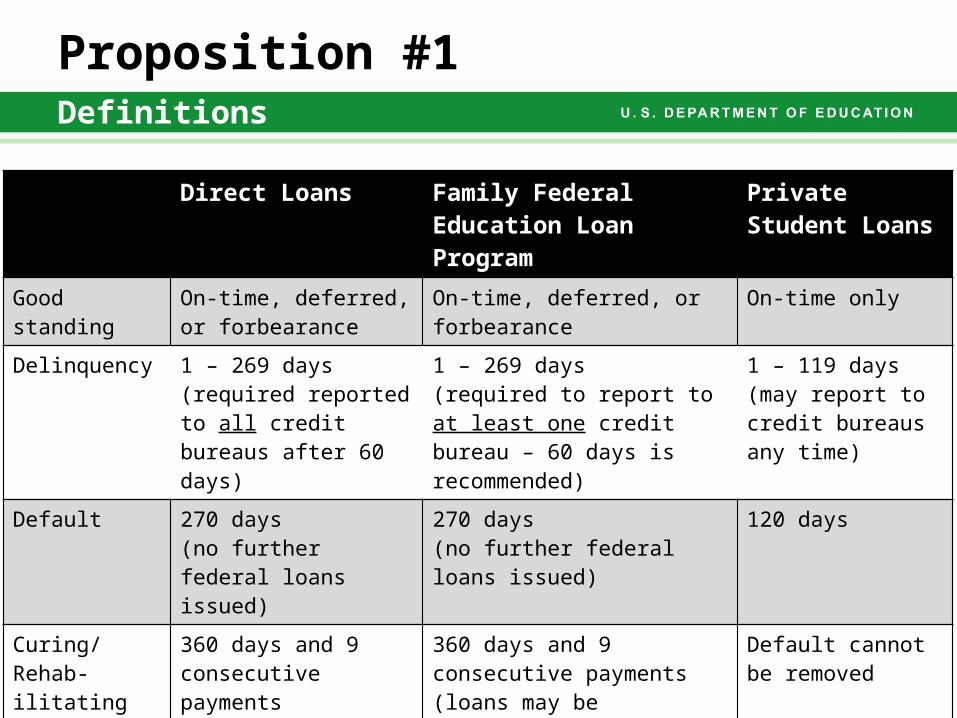

Proposition #1Definitions

Direct Loans Family Federal Education Loan Program

Private Student Loans

Good standing On-time, deferred, or forbearance

On-time, deferred, or forbearance

On-time only

Delinquency 1 – 269 days (required reported to all credit bureaus after 60 days)

1 – 269 days (required to report to at least one credit bureau – 60 days is recommended)

1 – 119 days(may report to credit bureaus any time)

Default 270 days(no further federal loans issued)

270 days(no further federal loans issued)

120 days

Curing/Rehab-ilitating Loans

360 days and 9 consecutive payments

360 days and 9 consecutive payments (loans may be repurchased by servicer)

Default cannot be removed

Debt collection 361 days – sent to Debt Management and Collections contractor (DMCS)

Guarantee agency serves as the debt collection agency.

Proposition #1Definitions

Proposition #2

Not all delinquencies and defaults are equal and we should not measure them as if they are the same.

Scenario #1 – Multiple Loan MonaMona attended two institutions for a total of 6 years and has 11 student loans valued at $25,000. The loans are held by three servicers as a result of lenders transferring/selling loans. She has lost track of one $500 loan from 4 years ago. When she moved out of her parent’s house, she didn’t know about the third lender and made no payments after the grace period expired and is 280 days overdue.

Proposition #2Differing Scenarios of Delinquency

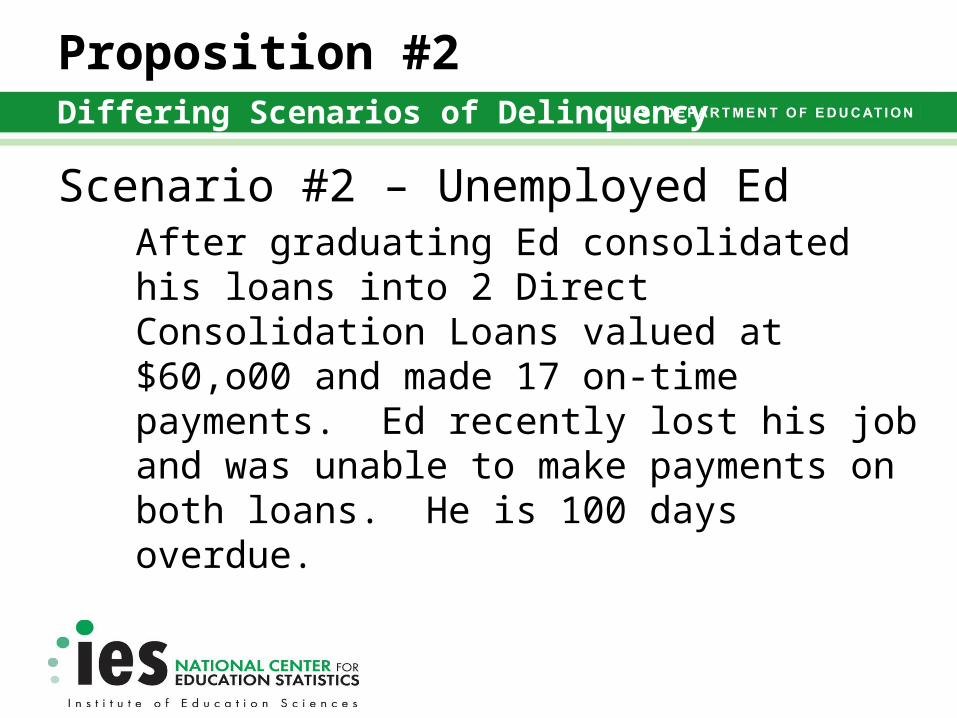

Scenario #2 – Unemployed EdAfter graduating Ed consolidated his loans into 2 Direct Consolidation Loans valued at $60,o00 and made 17 on-time payments. Ed recently lost his job and was unable to make payments on both loans. He is 100 days overdue.

Proposition #2Differing Scenarios of Delinquency

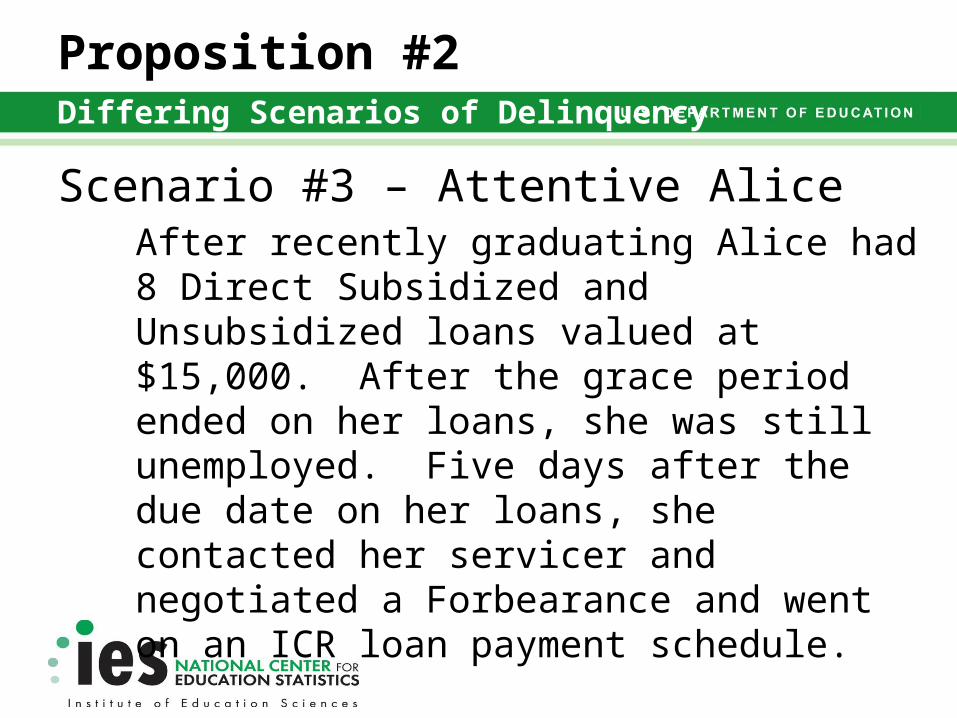

Scenario #3 – Attentive AliceAfter recently graduating Alice had 8 Direct Subsidized and Unsubsidized loans valued at $15,000. After the grace period ended on her loans, she was still unemployed. Five days after the due date on her loans, she contacted her servicer and negotiated a Forbearance and went on an ICR loan payment schedule.

Proposition #2Differing Scenarios of Delinquency

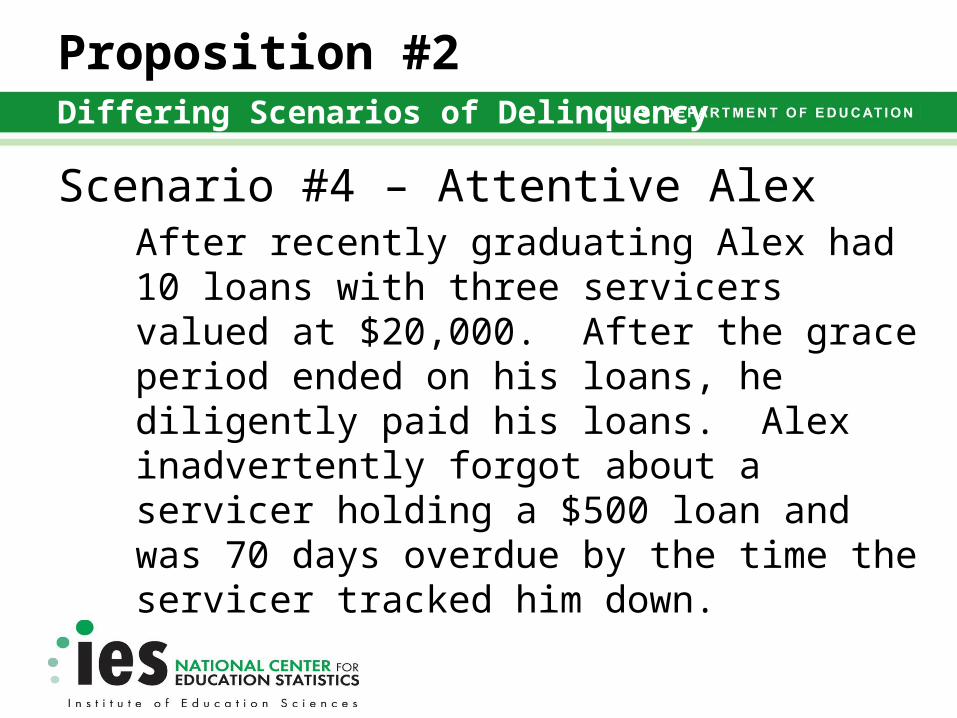

Scenario #4 – Attentive AlexAfter recently graduating Alex had 10 loans with three servicers valued at $20,000. After the grace period ended on his loans, he diligently paid his loans. Alex inadvertently forgot about a servicer holding a $500 loan and was 70 days overdue by the time the servicer tracked him down.

Proposition #2Differing Scenarios of Delinquency

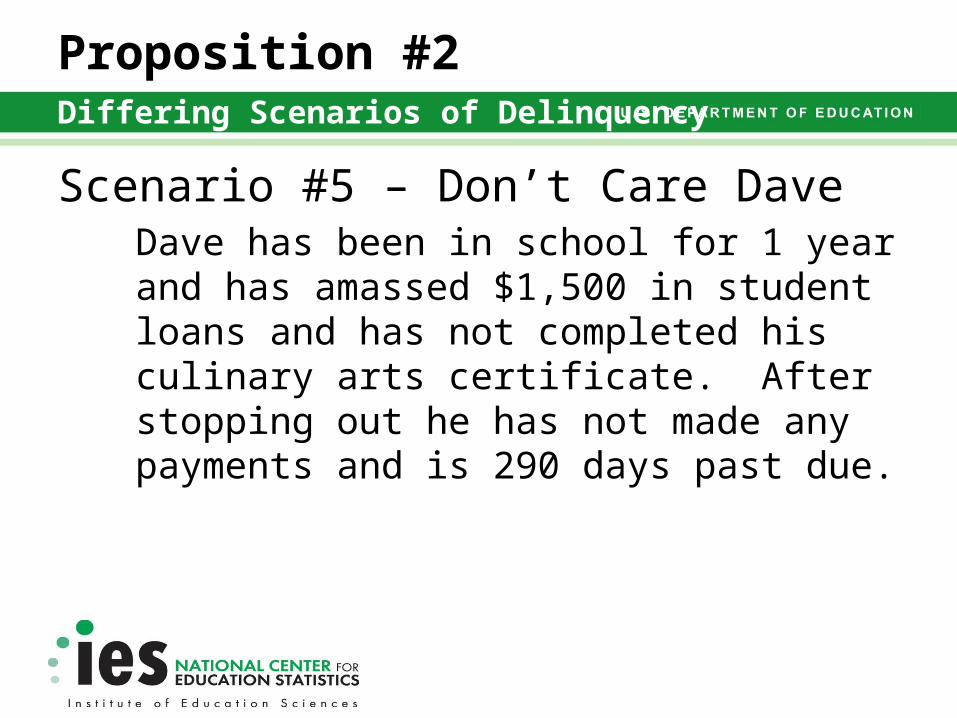

Scenario #5 – Don’t Care DaveDave has been in school for 1 year and has amassed $1,500 in student loans and has not completed his culinary arts certificate. After stopping out he has not made any payments and is 290 days past due.

Proposition #2Differing Scenarios of Delinquency

Proposition #3

It is unclear what current student loan default and delinquency measures mean.

– Is there an agreement on an acceptable percent of students that default?

– At what point do policymakers, university/institution staff/financial aid administrators need to make an intervention?

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20100

5

10

15

20

25

17.6%

17.2%

21.4%

22.4%

17.8% 15.0%

11.6%

10.7% 10.4%

9.6%

8.8%

6.9%

5.6% 5.9%

5.4%5.2%4.5%

5.1%4.6%

5.2%

6.7% 7.0%

8.8%9.1%

Cohort Years

Coh

ort D

efau

lt R

ate

FY 2010 2-Year Official National Student Loan Default Rates 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

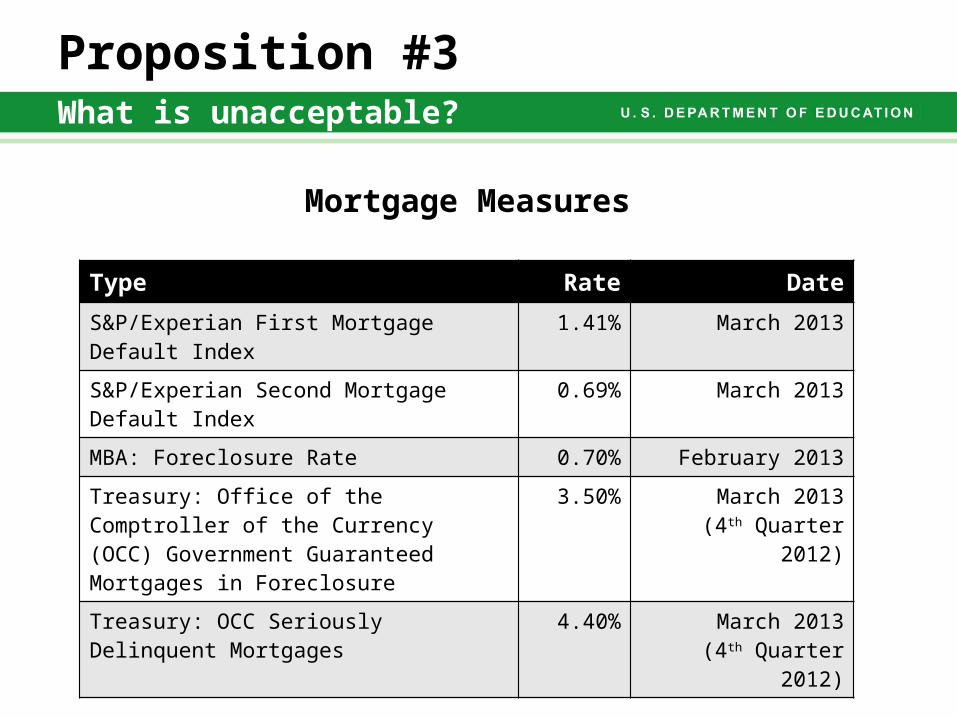

Proposition #3What is unacceptable?

• It is difficult to evaluate student loan delinquency or default measures because:– Student loans can be rehabilitated removing the

default from the student record.– There are no other measures (aside from past

history) available to evaluate if students are defaulting at “high” levels.

• Comparable measures for other financial products suffer from survivorship bias.

Proposition #3What is unacceptable?

Type Rate Date

S&P/Experian First Mortgage Default Index 1.41% March 2013

S&P/Experian Second Mortgage Default Index

0.69% March 2013

MBA: Foreclosure Rate 0.70% February 2013

Treasury: Office of the Comptroller of the Currency (OCC) Government Guaranteed Mortgages in Foreclosure

3.50% March 2013(4th Quarter 2012)

Treasury: OCC Seriously Delinquent Mortgages

4.40% March 2013(4th Quarter 2012)

Mortgage Measures

Panelist Response

Alisa CunninghamSenior AssociateInstitute for Higher Education Policy

Jeff WebsterAssistant Vice President, Research and Analytical ServicesTexas Guaranteed Student Loan Corporation

Jennie WooSenior Research AssociateRTI International

Open Discussion

Related Documents