1 GOVERNMENTAL FINANCIAL ANALYSIS: TEN QUESTIONS AND SOME ANSWERS James L. Chan ABSTRACT Key questions in municipal credit analysis are identified and suggestions are provided as follows. (1) The analyst should make sure that the reporting entity includes the bond issuer and financially interdependent units. (2) Current operating funds, capita! improvement funds, and other funds should be distinguished in analysis. (3) Debt proceeds and operating transfers are to be distinguished from revenues and expenditures, resulting in multiple “bottom lines” for governmental units. (4) The analyst should not uncritically use the “tolal” columns in combined financial statements, as interfunds transfers have not been eliminated in arriving at these totals. (5) Internal service earnings and expenditures should be eliminated, to avoid double counting. (6) Revenues and expenditures are reported in current dollars and should be adjusted for price-level changes in inflationary periods. (7) when accounting policy changes result in material changes in reported numbers, retrospective restatements should be made, or a new benchmark year adopted. Governmental financial statements are a fundamental data source for municipal credit analysis. < 1 > This paper identifies ten questions encountered in using the statements for municipal analysis and attempts to answer some of them: 1. How many governmental units to include in analysis? 2. Which fund types to group together? 3. Which “bottom line” to use? 4. How to handle interfund transfers? 5. How to handle Internal Service Funds? 6. How to gain a complete picture of capital improvements? 7. How to gain a complete picture of long-term liabilities? 8. How to deal with non-informative financial reporting? 9. How to deal with effects of inflation? 10. How to deal with accounting policy changes? The term “governmental financial statements” in this paper refers to the statements contained in the Financial Section of a governmental unit’s Comprehensive Annual Financial Report (CAFR) The financial statements are presented at two levels of aggregation. The combining statements aggregate data of individual funds to the level of a fund type, e.g. all the special revenue funds together form a “fund type” called the “Special Revenue Funds.” The financial affairs of a governmental unit are conducted through a series of fund types identified in Exhibit 1.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

GOVERNMENTAL FINANCIAL ANALYSIS: TEN QUESTIONS AND SOME ANSWERS James L. Chan ABSTRACT Key questions in municipal credit analysis are identified and suggestions are provided as follows. (1) The analyst should make sure that the reporting entity includes the bond issuer and financially interdependent units. (2) Current operating funds, capita! improvement funds, and other funds should be distinguished in analysis. (3) Debt proceeds and operating transfers are to be distinguished from revenues and expenditures, resulting in multiple “bottom lines” for governmental units. (4) The analyst should not uncritically use the “tolal” columns in combined financial statements, as interfunds transfers have not been eliminated in arriving at these totals. (5) Internal service earnings and expenditures should be eliminated, to avoid double counting. (6) Revenues and expenditures are reported in current dollars and should be adjusted for price-level changes in inflationary periods. (7) when accounting policy changes result in material changes in reported numbers, retrospective restatements should be made, or a new benchmark year adopted.

Governmental financial statements are a fundamental data source for municipal credit analysis. < 1 > This paper identifies ten questions encountered in using the statements for municipal analysis and attempts to answer some of them:

1. How many governmental units to include in analysis? 2. Which fund types to group together? 3. Which “bottom line” to use? 4. How to handle interfund transfers? 5. How to handle Internal Service Funds? 6. How to gain a complete picture of capital improvements? 7. How to gain a complete picture of long-term liabilities? 8. How to deal with non-informative financial reporting? 9. How to deal with effects of inflation? 10. How to deal with accounting policy changes?

The term “governmental financial statements” in this paper refers to the statements contained in the Financial Section of a governmental unit’s Comprehensive Annual Financial Report (CAFR) The financial statements are presented at two levels of aggregation. The combining statements aggregate data of individual funds to the level of a fund type, e.g. all the special revenue funds together form a “fund type” called the “Special Revenue Funds.” The financial affairs of a governmental unit are conducted through a series of fund types identified in Exhibit 1.

2

EXHIBIT 1 “FUND ORGANIZATIONAL CHART”

Source: Glick (1986), p. 6

3

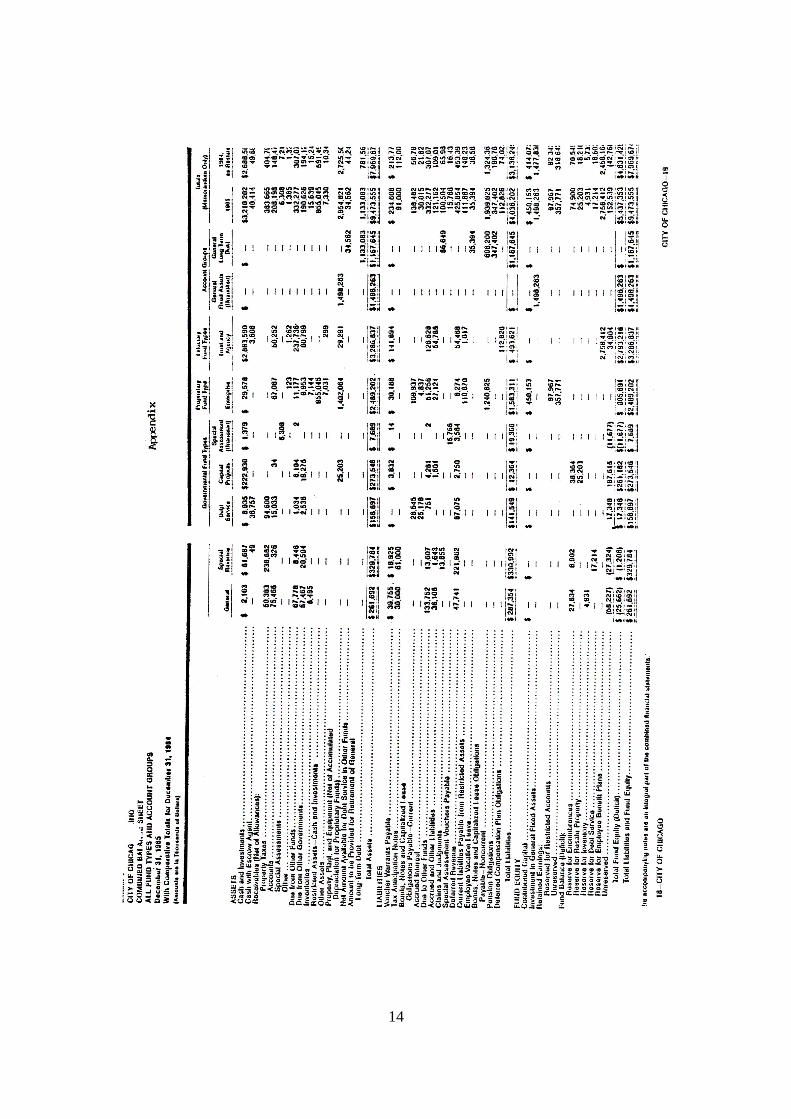

Financial statements prepared at the fund type level are characterized as combined, and are also called “general purpose financial statements” (GPFS) or basic financial statements. An example is included as an appendix to the paper.

Financial statements are designed to communicate information about both “stocks” and “flows” of resources. The former is presented in statements of financial position (commonly called balance sheets), and the latter in operating statements (or statements of revenues and expenditures/expenses). From these are derived the statement of changes in financial position, and the budget vs. actual comparisons for revenues and expenditures, where appropriate. <2>

In order to reduce information overload and to discern relationships among the various dimensions of the fiscal health of a governmental unit, indicators are constructed by using data from financial statements. A number of cities, such as Chicago, New York and Seattle, have published reports of fiscal indicators. This paper is based on the author’s experience in preparing the City of Chicago Fiscal Indicators Report, 1981-1985, and in analyzing the financial reports of six cities for a major institutional investor. < 3 >

The paper highlights the problems of financial statement analysis for credit evaluation, but not problems of government financial analysis in general. The latter should use all possible information sources, including but not limited to financial statements, such as budgets, Bureau of Census data, official statements. It is assumed that the reader has some fundamental knowledge of municipal credit analysis and governmental financial reporting. <4>

The subtitle of the paper indicates that not all the questions have been answered; the “answers” are really only proposed approaches to solving the problems encountered in attempting to make financial statements more useful than they are currently. It should be noted that the accounting profession, particularly through the Governmental Accounting Standards Board (GASB), has devoted considerable resources to improve the contents and formats of governmental financial reports. Some problems may be “solved” this way; some require greater compliance with generally accepted accounting principles (GAAP); and still others necessitate reconsideration of the existing governmental accounting model. In the short-run, the analyst uses what is available, and that is the situation being dealt with in this paper. TEN QUESTIONS AND SOME ANSWERS Ql: How many governmental units to include in analysis?

The financial viability of the bond issuer itself is likely to be the point of departure of a general obligation credit analysis. The issuer, however, may not be identical with the “reporting entity.” The reporting entity can be only one governmental unit, or the governmental unit with one or more governmental units (called “component units”) over which it exercises oversight responsibilities, and with which it is financially interdependent.

< 5 > Of Particular interest from a credit standpoint will be the government’s risk exposure due to the responsibility to fund deficits and service debts in case of a component unit’s default.

4

From the notes to financial statements, the analyst will be able to know the government units which are included or excluded from the reporting entity and the justification therefore. The analyst should seek to know the financial impacts of including the component units. He/she may also want to ask a further question: “Should any of the excluded ones be included?” This is a fair question because the credit analyst may attach different weights to the financial and legal criteria used to make the include/exclude decision.

Another reason for credit analysts to be concerned with this question is that local governments vary in terms of the scope of services they perform. A “per capita expenditure” figure is not meaningful without knowing what public services are provided with the expenditure. For example, prior to FY 1982, the school district in the City of Buffalo was not included in the financial report of the City of Buffalo. But since 1982 it has been, resulting in incomparable financial data. The problem is even more severe in cross-sectional analysis of municipal expenditures. For this reason, Clark, Ferguson and Shapiro (1982) proposed a method to arrive at an adjusted and thus comparable set of expenditures.

Q2: Which fund types to group together?

A fund type is a group of funds with similar purposes. Currently, the basic financial

statements are presented at this level of aggregation. Currently up to eight fund types are used by state and local governments (see Exhibit I). Even as the proposal of consolidated financial statements for state and local government (e.g. Davidson, 1977) has not won wide acceptance, its rationale seems compelling: aggregate the funds to the maximum extent possible to reduce information overload. This approach has been adopted as the fund types are grouped into three categories: governmental fund types, fiduciary fund types and proprietary fund types. The intent of this classification seems to distinguish between those funds associated with “governmental functions” (Gl) from the peripheral ones (G2). It is proposed that Gl be broken down further into two subgroups: Gl.a for those supporting current operations, and Gl.b supporting capital improvements.

Specifically, Gl.a would usually include the General Fund, Special Revenue Funds, Debt Service Funds, and other funds having the objective of supporting current operations, such as certain intergovernmental grants accounted for as “trust funds”.

Gl.b would essentially be Capital Project Funds and other funds that support capital improvements, such as capital grants. <6>

The rationale for this recommended approach is that the fiscal year is a natural operating cycle and revenues minus expenditures is an appropriate measure of periodic financial performance for Gl.a funds, but for Gl.b funds a different approach is necessary. Gl.b funds are on a project-cycle basis and are often financed by debt proceeds. Therefore, revenues minus expenditures could lead to misleading “artificial deficits” as the expenditures are not intended to be covered by revenues alone, but by a combination of revenues and other financing sources, primarily bond proceeds.

In summary, credit analysis should begin with, but not end at, the general fund. Nor should the analyst use the “total” columns in the combined financial statements, because these totals are virtually meaningless and potentially misleading. After clarifying the

5

purpose of analysis, the analyst should select the fund types to be encompassed in the analysis and classify them appropriately in accordance with their characteristics. Q3. Which “bottom-line” measures to use?

It has often been said that, unlike business enterprises, governments do not have

“bottom lines.” On the contrary, governments have more than one bottom line of financial performance, and it is important to recognize their meaning and significance. They are identified below.

Bottom Line #1 = Budgeted revenues - appropriations #2 = Revenues - expenditures #3 = (Revenues + transfers in) - (expenditures + transfers out) #4 = (Revenues + other financing sources) - (expenditures + other financing uses) #5 = Revenues - (expenditures + encumbrances) For the funds in Gl explained in the previous section, according to generally accepted

accounting principles, revenues are recognized in the period in which they are measurable and available to finance the expenditures of the period, i.e. on the modified accrual basis of accounting. Expenditures are recognized as cash outlays occur and when current liabilities arise. In short, this may be called the “GAAP basis” and is used in determining Bottom Line #2.

Bottom Line #1 tells whether the legally adopted budget is balanced or not. The “budgetary basis” used in measuring anticipated revenues and appropriations may or may not be identical with the GAAP-basis. The analyst should ascertain the situation, and locate information in the financial statements or notes that attempts to reconciled discrepancies.

Bottom Line #3 takes into account interfund transfers — a complex topic that deserves further explanation in the next section.

Bottom Lines #1-3 are appropriate for current operating funds (Gl.a) when capital improvements (Gl.b) are financed by debt proceeds - which are termed “other financing sources” and not revenues - Bottom Line #4 is applicable. Bottom Line #4 is not appropriate for current operating funds because it has the potential of allowing debt proceeds be interpreted (erroneously) as a revenue source.

Bottom Line #5 is influenced by budgetary practices. Encumbrances are commitments and purchase orders. They are not a liabilities or expenditures according to GAAP. However, from the point of view of Bottom Line #1, encumbrances are in substance expenditures “in process.” Again, information reconciling the budgetary and GAAP bases are available and should be examined.

All these “bottom lines” are legitimate in that each informs the reader about a different aspect of a governmental unit’s summary financial performance, while one should not give up looking for the “true” bottom line, a challenge to the analyst is to determine which one or ones of these bottom lines are most appropriate for the purpose at hand.

6

Q4: How to handle interfund transfers?

Interfund transfers refer to the movements of resources from one fund to another

within the governmental unit. Operating transfers are a major type of transfer of a regular recurring nature. Two types of operating transfers should be distinguished. One type may be called transfers in form, that is, it is the result of creating funds for specific purposes. For example, debt service payments could very well have been paid out of the General Fund; since Debt Service Funds are used, a transfer has to be made from the General Fund to the Debt Service Fund. Another type may be characterized as transfers in substance. This type of transfers amounts to subsidies, for example, by the General Fund to Capital Project Funds or Enterprise Funds.

The primary concern of the analyst would be the ability to identify the nature and extent of operating transfers in (out) between the Gl, i.e., governmental functions, funds and the G2, i.e. other, funds, and also operating transfers in (out) between one Gl fund and another Gl fund. This would enable the analyst to identify the subsidization of Gl fund operations by a G2 fund operation, and determine the related effect on fund balances associated with operating transfers in (out).

In accordance with GAAP, transfers are reported as “other financing sources (uses)” separately from revenues and expenditures/expenses. This is a good start. Unfortunately, the transfers are often reported as net amounts, i.e., the transfers in and out having offset each other. Even if both transfers in and out are stated separately, rarely are the sources and destinations of the transfers identified. The analyst would need access to alternative sources of financial information, e.g. internal accounting records, budget documents, in order to determine the nature and extent of operating transfers between funds.

The procedure of grouping the funds into Gl and G2 was intended to (1) eliminate the effect on fund balance of transfers among the Gl funds and (2) to point out the transfers between Gl funds and G2 funds. For example the operating transfer between the Debt Service Fund and the General Fund would be recorded as a transfer-in the former and a transfer-out in the latter. When the operations of these two Gl funds are aggregated, the transfer-in and transfer-out would cancel each other and would have no effect on the aggregated fund balance.

In addition, although the analyst may not be able to determine the specific nature of operating transfers between Gl and G2 funds, the extent to which Gl funds subsidized

the operations of G2 funds, or vice versa, can be determined by computing the difference between aggregated transfers-in and aggregated transfers-out for both the Gl funds and G2 funds.

In short, the problem faced by the analyst with respect to interfund transfers is primarily due to inadequate disclosures of the sources and destinations of transfers in financial statements. This information should be available from the governmental unit’s accounting records, but the additional costs should be weighed against incremental benefits. Q5: How to handle Internal Service Funds?

7

A technical problem that has attracted little attention pertains to Internal Service Funds, which are used to account for services rendered by one agency for another agency within the same governmental unit, usually on a cost-reimbursement basis. This kind of intragovernmental transactions should not result in revenues or expenditures for the governmental unit considered as a whole. A source of potentially misleading inference is that GAAP term such transactions “quasi-external” and allow the recognition of expenditures (by the service-recipient agencies) and revenues (by the Internal Service Funds). Adjustments by the analyst may therefore be necessary to eliminate any double counting. Adjustment procedures depend on how internal service functions are accounted for and reported.

Situation A: A governmental unit maintains Internal Service Funds and reports them as a proprietary fund type in the financial statements.

In the normal circumstances, the revenues and expenses of the Internal Service Funds (not of the governmental unit) should approximately equal. Since the payments to Internal Service Funds are already accounted for as expenditures of the service-recipient funds, the exclusion of Internal Service Funds from both Gl and G2 is sufficient to ensure the proper result.

Situation B. Instead of separate Internal Service Funds, the governmental unit uses the General Fund to account for internal service activities.

Suppose the General Fund provided goods costing $100 to a Special Revenue Fund and received $100. The General Fund would record revenues and expenditures of $100. (The cash received was used to pay external vendor.) The service recipient fund would record an expenditure of $100 and a cash payment of the same amount. Simply adding up the two funds would result in $200 in expenditures, $100 in revenues, and $100 in cash outflows. Considering the governmental unit as a whole, the net result should be: $100 in expenditures, and $100 in cash outflows.

Consequently in Situation B, the appropriate adjustment procedure is to eliminate “internal service earnings” - as a revenue source from the General Fund ($100 in the above illustration), and deduct the same amount from the aggregate expenditures of Gl. <7> This procedure would ensure that the total revenues and total expenditures are correctly stated. However, it would be very difficult, or almost impossible, to restate the various functional expenditures.

Q6: How to gain a complete picture of capital improvements?

In attempting to gain a more complete picture of the capital improvements from the

financial statements, the credit analyst is advised to: 1. Make a separate analysis of the funds involved in financing capital improvements

(Gl.b) from those for current operations. In addition to the reasons indicated in an earlier section, the fund balance in Capital Project Funds includes unspent bond proceeds, and should be clearly distinguished from the fund balance of current operating funds. The latter is available for future appropriation.

2. Consider comprehensively all the funding sources which may be accounted for in several funds. The logical place to start is the Capital Project Funds, which account for

8

bond proceeds in addition to revenues. But capital improvements could also be financed out of current appropriations, interfund transfers and intergovernmental capital grants.

3. Supplement financial statements with capital budgets and capital improvement plans for more detailed information about the types of project undertaken, for example, community development, environmental protection, transportation. Financial statements often disclose very little information in this regard.

4. Use a period of several years instead of one fiscal year in analyzing a government’s capital improvement efforts, preferably the same period as an official capital improvement plan. The reason is that a fiscal year is not a natural operating cycle for capital projects. Q7: How to gain a complete picture of long-term liabilities?

What Leonard (1986) calls “the quiet side of public spending” has received extensive

attention from the accounting profession in recent years. In addition to bonded debt, which has traditionally received adequate documentation, more rigorous disclosure is now required for compensated absences, claims and judgments, and unfunded pension liabilities. With respect to pensions, it is crucial to make a distinction between deficiency in annual funding, i.e. failure to make actuarial required annual contributions, and the unfunded actuarial present value of credited projected benefits. The latter is total actuarial present value of credited projected benefits minus net assets available for benefits, and can be thought of as cumulative funding deficiency. This information is usually available only in the footnote disclosures, while the annual funding deficiencies are reported in the General Long-term Debt Account Group.

The analyst should be aware that the increases in long-term liabilities could in part be attributed to better disclosure. Consequently, one should either begin a time series with the 1983-84 period when many of these requirements went into effect, or search through the footnotes or inquire with finance staffs to reconstruct a more complete picture of prior periods’ less obvious long-term liabilities.

Q8: How to deal with non-informative financial reporting?

A set of financial statements could comply with generally accepted accounting

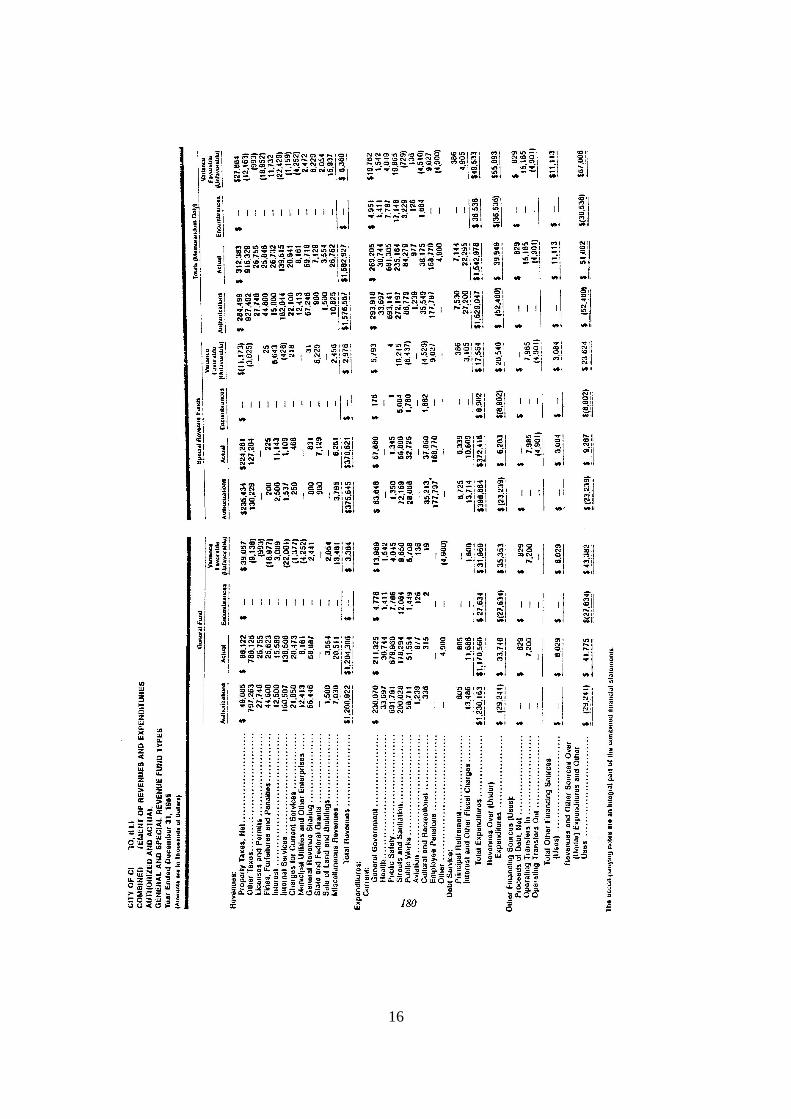

principles, and yet not be informative. Of particular concern to credit analysts would be the revenue or expenditure items labeled as “other” or “miscellaneous.” To reduce excessive details, these residual categories should not be excessive. As a case in point, for FY 1985, the City of Chicago reported almost $918 millions of “other taxes” for the General Fund, Special Revenue Funds and Debt Service Funds, or 44% of the revenues of these funds (Exhibit 1). Extensive research using the combining statements, budgets and other information sources reduced the amount down to $7 million or 3% of total revenues of these funds. The remainder was explicitly accounted for and a new revenue classification system was recommended to the city.

The example cited above illustrates the point that combined financial statements can often be too condensed for the analyst. In making the financial statements more informative, financial analysis resembles financial “archaeology” — the deeper you get, the more you may find.

9

Q9: How to deal with effects of inflation?

The numbers in governmental financial statements are stated in current dollars. In a

period of appreciable inflation, it is advisable to restate the revenue and expenditures in terms of constant dollars. One approach is to deflate the current dollars numbers by the Gross National Product Implicit Price Deflator. This was done with the City of Chicago data for the 1981-85 period, during which inflation rose by approximately 19% in terms of the GNP Implicit Price Deflator. The modest growth of revenues and expenditures, when restated in constant dollar terms, turned into steady decline. (Exhibits 2, 3).

10

11

EXHIBIT 3 “PRICE-LEVEL ADJUSTED EXPENDITURES, CITY OF CHICAGO”

12

Q10. How to deal with accounting policy changes? The last question discussed in this paper is also probably the most difficult problem.

Over the past decade, many state and local government accounting policies changed, all intended to improve the usefulness of their financial reports. And as the Governmental Accounting Standards Board becomes increasingly productive, even more changes are likely. One consequence of these changes is to make more recent financial statements less consistent with past ones. With adequate skills and data, one could analyze the effect of each standard for a governmental unit, as has been done in Wallace (1985). The effects of changes are often described in the notes, but reconciliations are often done for one or two years at the most.

Credit analysts should be concerned with this question because accounting rule changes could result in material changes in the values of financial indicators, which, if unexplained, could result in erroneous interpretation. For example, the City of Chicago’s implementation of GAAP requirement to defer property tax recognition beginning in FY 1983 meant that total fund balance for the operating fund dropped from $73 at the end of FY 1982 to a negative $107 million at the end of FY 1983, and unreserved fund balance from $21 to -$136 (see reported columns in the following chart).

Total FB Unreserved FB Restated Reported Restated Reported 1981 1982 1983 1984 1985

-126 - 93 -107 - 50 - 7

92 73 -107 - 50 - 7

-148 -145 -136 - 89 - 65

70 21 -136 - 89 - 65

The analyst is faced with unappealing alternatives. One possibility is to adopt a new

benchmark year, in this case, FY 1983. The advantage of this approach is that it is less costly than retrospective restatement, and the new standards will probably be maintained for a few years. A disadvantage is that the time series will get shorter and shorter as more accounting policy changes are introduced.

Alternatively, one could attempt retrospective restatements - restating prior years’ data to be consistent with the new benchmark year (see the restated column in the above chart). The consistency in the data, however, could be obtained with considerable time and resources.

The choice of strategy in a particular situation should be dictated by cost and benefit considerations. Governmental units could reduce the analyst’s costs by providing adequate data in the notes to facilitate restatement, if desired. Otherwise, external users would find it exceedingly difficult to do retrospective restatements. SUMMARY

This paper identifies questions that have been encountered in using governmental

financial statements to construct financial indicators for municipal credit analysis. The following key suggestions are made.

13

1. The analyst should make sure that the reporting entity includes the bond issuer and

financially interdependent units that could increase risk exposure. 2. Three groups of funds are distinguished: current operating funds (Gl.a) , capital

improvement funds (Gl.b) , and other funds (G2). 3. There exist multiple “bottom-lines” to summarize the periodic financial

performance of a governmental unit. Debt proceeds and operating transfers are to be clearly distinguished from revenues and expenditures.

4. The analyst should not uncritically use the “total” columns in combined financial statements, as interfund transfers have not been eliminated in arriving at those totals. When the current operating funds are aggregated to form Gl.a, operating transfers among them are netted out. Current financial reporting practices do not allow for detailed tracing of the sources and destinations of operating transfers.

5. Internal Service Funds should not be included in order to avoid double counting. When internal service functions are accounted for through the General Fund, internal service earnings and related expenditures should be eliminated.

6. Revenues and expenditures reported in financial statements are stated in current dollars and should be adjusted for price-level changes in periods of appreciable inflation.

7. When accounting policy changes result in material changes in reported numbers, retrospective restatements should be made, or a new benchmark year be adopted.

14

15

16

17

18

19

FOOTNOTES 1. I gratefully acknowledge the continued collaboration of Terry Nichols Clark and

research assistance of Thomas L. Malone. I am responsible for remaining shortcomings. 2. For more detailed explanation of governmental accounting and financial reporting,

refer to Chan (1988). 3. A limited number of copies of the City of Chicago Fiscal Indicators Report, 1981-

1985, are available upon request from the author at the Office for Governmental Accounting Research and Education (m/c 006), College of Business Administration, The University of Illinois at Chicago, P.O. Box 4348, Chicago, IL 60680.

4. For background information, the reader may wish to refer to other papers in this volume, and to Click (1986), and Berne and Schramm (1986) for the basics of governmental financial reporting.

5. Manifestations of these responsibilities include: financial interdependency, responsibility for financing deficits, entitlement to surplus, and guarantee of or moral responsibility for debt; selection of governing authority or designation of management; ability to significantly influence operations, and accountability for fiscal matters. See Patton (1985) for a review of the issues.

6. GASB Statement 6 recommends the elimination of Special Assessment Funds as a fund type in financial reports, by disbursing them into Capital Project Funds and Special Revenue Funds as appropriate.

7. What might seem to be a minor technical matter could involve rather significant amounts. For FY 1985, the City of Chicago reported $138.5 million of “internal services” as a revenue of the General Fund. REFERENCES Berne, Robert and Richard Schramm, The Financial Analysis of Government (Englewood Cliffs, NJ: Prentice-Hall, 1986). Chan, James L., “Governmental Accounting Principles” in Handbook of Governmental Accounting and Auditing, edited by Mortimer A. Dittenhofer (NY: Matthew Bender, 1988). Clark, Terry Nichols, Lorna Crowley Ferguson, and Robert Y. Shapiro, “Functional Performance Analysis: A New Approach to the Study of Municipal Expenditures,” Political Methodology (Fall, 1982), pp. 187-223. Davidson, Sidney, et. al., Financial Reporting State and Local Governmental Units (Universityof Chicago, Graduate School of Business, Center for Management of Public and Nonprofit Enterprises, 1977). Glick, Paul E., How to Understand Local Government Financial Statements: A Users’ Guide, Financial Report Series #6 (Chicago: Government Finance Officers Association, 1986).

20

Leonard, Herman B., Checks Unbalanced: me bet Side of Public Spending (Basic Books, 1986). Patton, James M., “The Governmental Financial Reporting Entity: A Review and Analysis,” Research in Governmental and Nonprofit Accounting, Vol. 1 (JAI Press, 1985), pp. 85-116. Wallace, Wanda A., “Accounting Policies and the Measurement of Urban Fiscal Strain,” Research in Governmental and Nonprofit Accounting, Vol. 1 (JAI Press, 1985), pp. 181-212.

Related Documents