Anton Löf Senior Iron Ore Analyst COO, Raw Materials Group [email protected] Global iron ore: new import areas and the Chinese slowdown? Mining on top: Stockholm

Global iron ore: new import areas and Chinese slowdown?

Aug 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Anton Löf

Senior Iron Ore Analyst COO, Raw Materials Group

Global iron ore: new import areas and the

Chinese slowdown?

Mining on top: Stockholm

• The Iron ore industry

• China

• New import areas?

• China today

• New export areas?

• Iron ore prices

• Summary

Outline

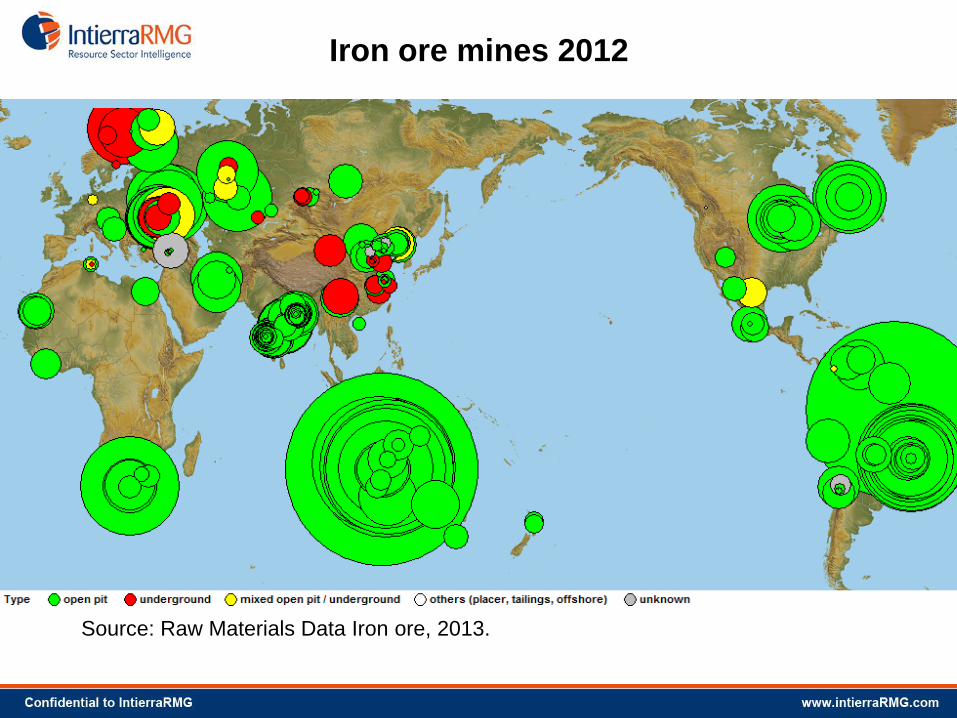

Iron ore mines 2012

Source: Raw Materials Data Iron ore, 2013.

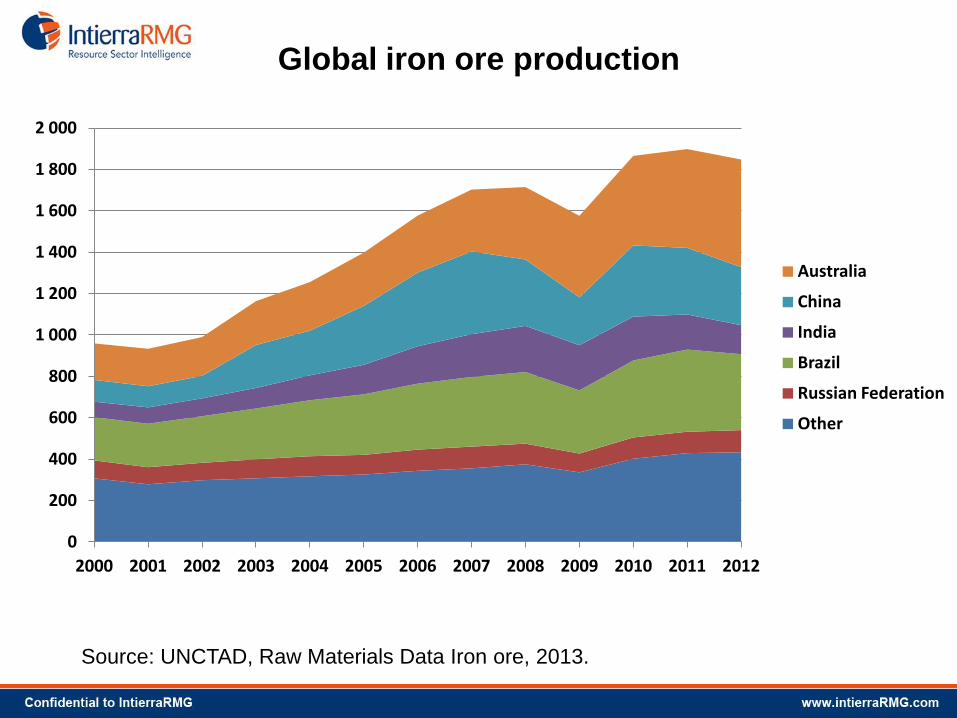

Global iron ore production

Source: UNCTAD, Raw Materials Data Iron ore, 2013.

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Australia

China

India

Brazil

Russian Federation

Other

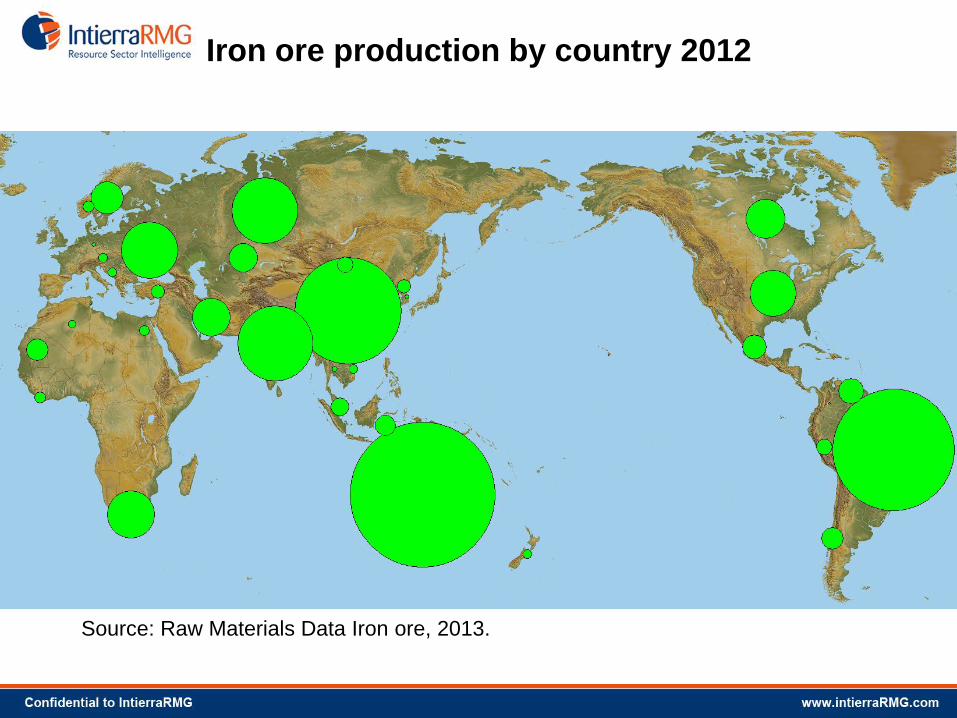

Iron ore production by country 2012

Source: Raw Materials Data Iron ore, 2013.

Crude steel production

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

1 800 000

kt

Total world crude steel production

Crude steel production

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

1 800 000

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

kt

Chinese influence on total crude steel production

China

Rest of the world

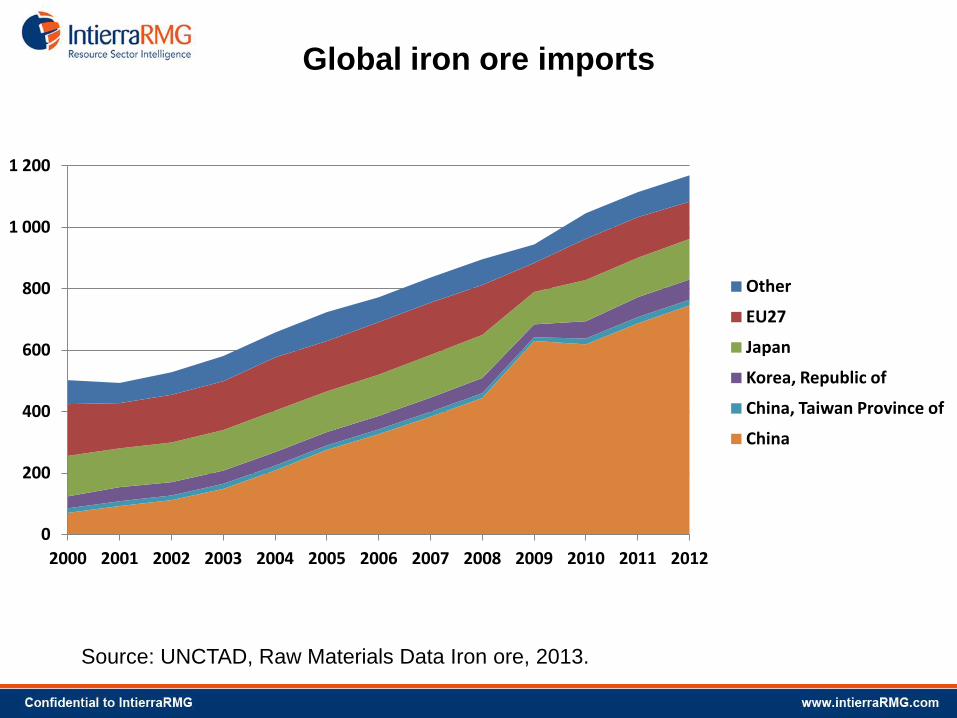

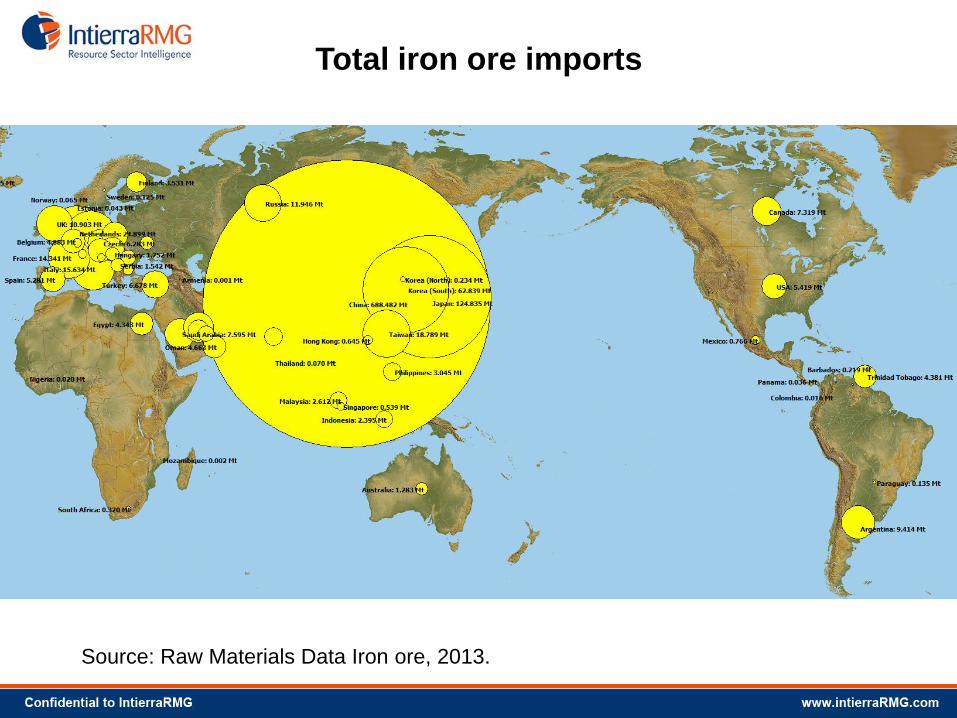

Global iron ore imports

Source: UNCTAD, Raw Materials Data Iron ore, 2013.

0

200

400

600

800

1 000

1 200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Other

EU27

Japan

Korea, Republic of

China, Taiwan Province of

China

Total iron ore imports

Source: Raw Materials Data Iron ore, 2013.

Chinese population

—

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

—

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

1990 1995 2000 2005 2010 2015 2020 2025 2030

Chinese population

China urban population

Proportion urban population

WORLD MINING to 2030

0

10

20

30

40

50

60

70

1850 1870 1890 1910 1930 1950 1970 1990 2010 2030

Europe

USA

China

USSR/CIS

Australia/Canada

6 resource rich developing

countries

Sources: Raw Materials Data, Stockholm and Sames.

% of global mining

World population

—

10.0

20.0

30.0

40.0

50.0

60.0

70.0

—

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

9 000 000

1990 1995 2000 2005 2010 2015 2020 2025 2030

Chart Title

total population

total urbanised population

proportion urban

Potential new importers, population

—

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

19

90

19

95

20

00

20

05

20

10

20

15

20

20

20

25

20

30

India

MENA

Indonesia

—

10

20

30

40

50

60

70

19

90

19

95

20

00

20

05

20

10

20

15

20

20

20

25

20

30

India

MENA

Indonesia

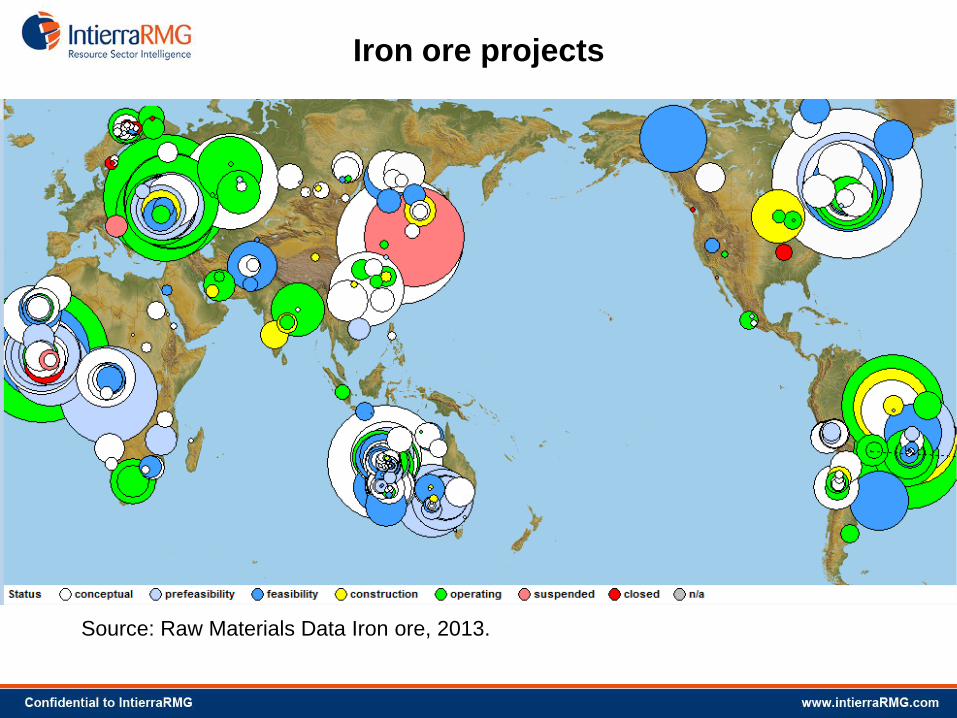

Iron ore projects

Source: Raw Materials Data Iron ore, 2013.

Chinese crude steel production

0

10000

20000

30000

40000

50000

60000

70000

80000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

kt

2009

2010

2011

2012

2013

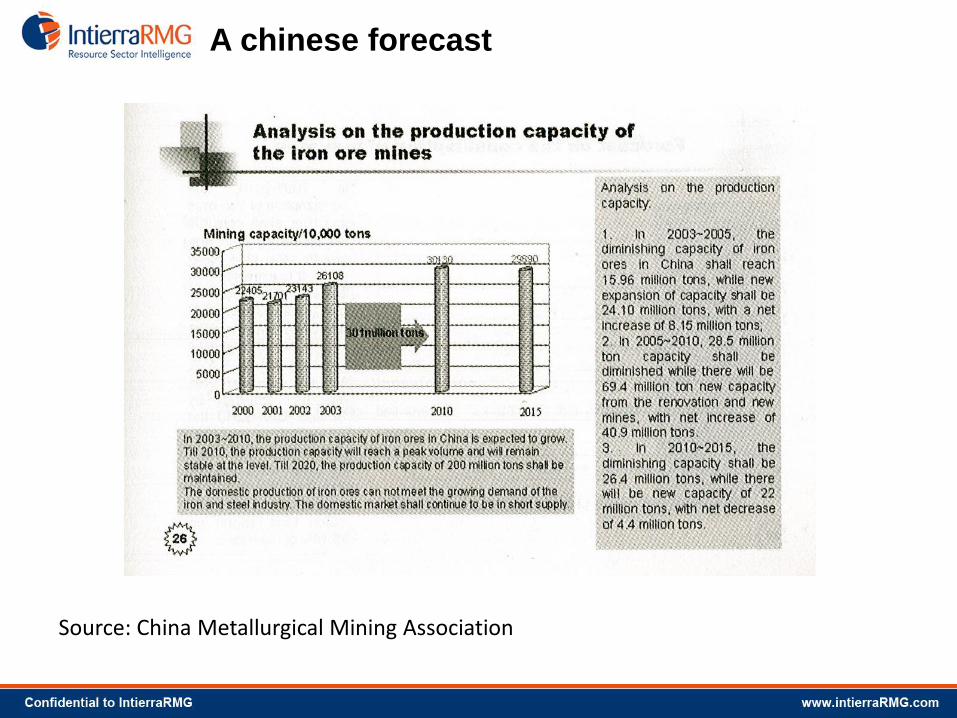

A chinese forecast

Source: China Metallurgical Mining Association

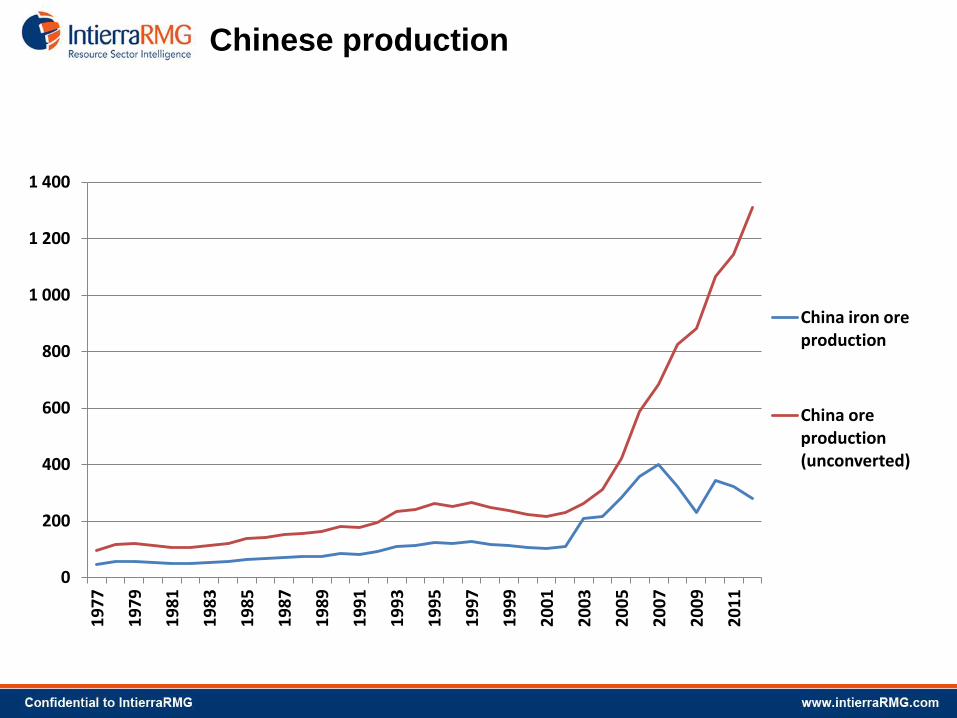

Chinese production

0

200

400

600

800

1 000

1 200

1 400

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

China iron ore production

China ore production (unconverted)

World iron ore demand

0

500

1000

1500

2000

2500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

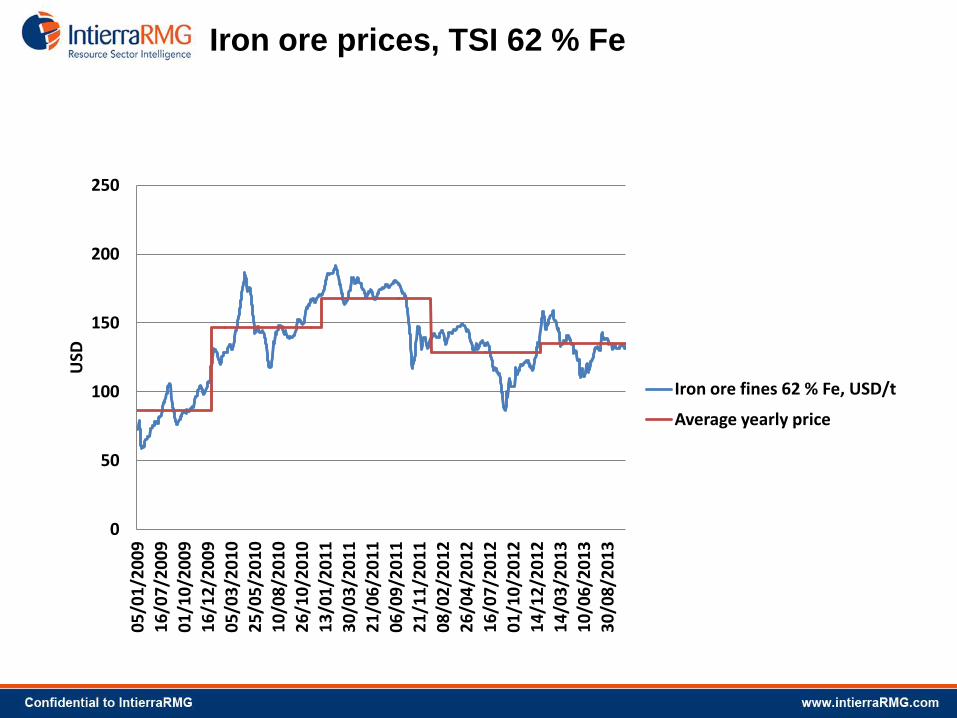

Iron ore prices, TSI 62 % Fe

0

50

100

150

200

250

05

/01

/20

09

16

/07

/20

09

01

/10

/20

09

16

/12

/20

09

05

/03

/20

10

25

/05

/20

10

10

/08

/20

10

26

/10

/20

10

13

/01

/20

11

30

/03

/20

11

21

/06

/20

11

06

/09

/20

11

21

/11

/20

11

08

/02

/20

12

26

/04

/20

12

16

/07

/20

12

01

/10

/20

12

14

/12

/20

12

14

/03

/20

13

10

/06

/20

13

30

/08

/20

13

USD

Iron ore fines 62 % Fe, USD/t

Average yearly price

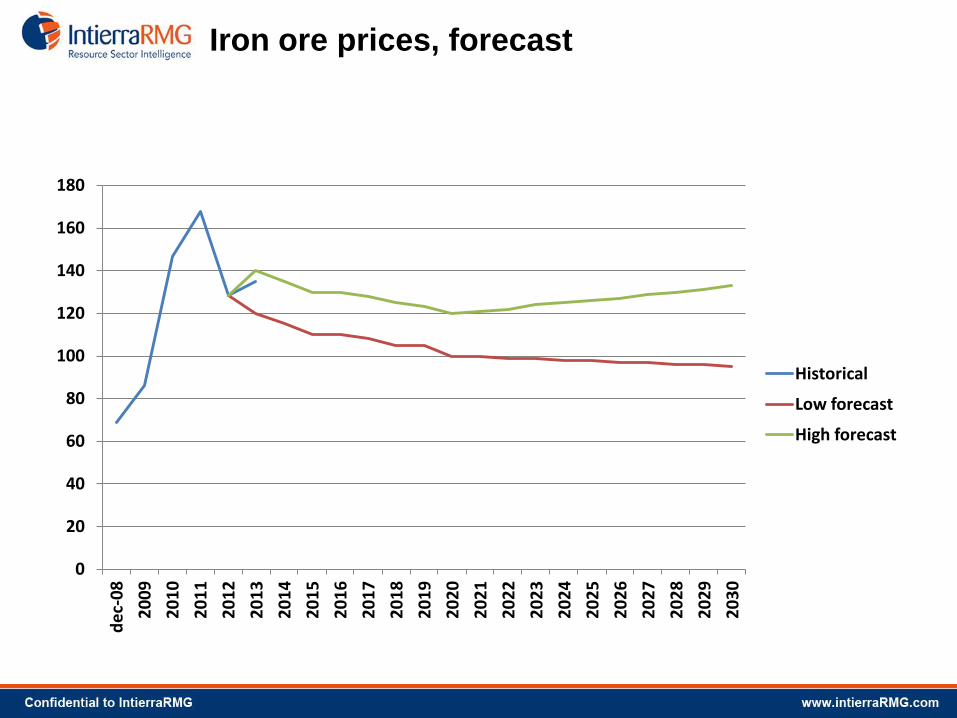

Iron ore prices, forecast

0

20

40

60

80

100

120

140

160

180

de

c-0

8

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

Historical

Low forecast

High forecast

Conclusions

Summary

Molybdenum drawing: Kaianders Sempler.

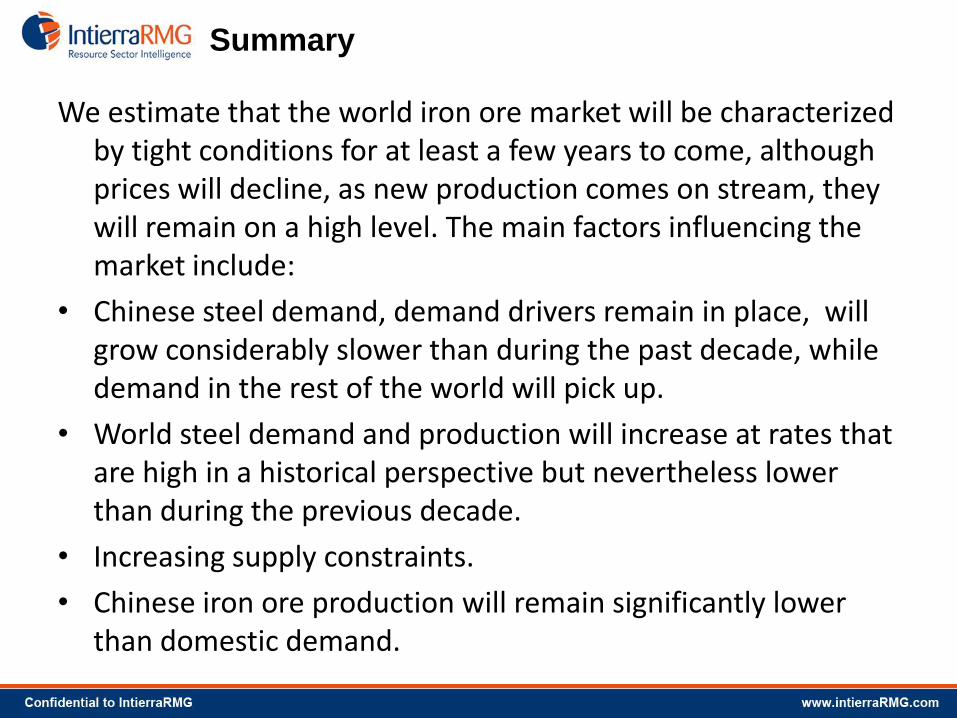

Summary

We estimate that the world iron ore market will be characterized by tight conditions for at least a few years to come, although prices will decline, as new production comes on stream, they will remain on a high level. The main factors influencing the market include:

• Chinese steel demand, demand drivers remain in place, will grow considerably slower than during the past decade, while demand in the rest of the world will pick up.

• World steel demand and production will increase at rates that are high in a historical perspective but nevertheless lower than during the previous decade.

• Increasing supply constraints.

• Chinese iron ore production will remain significantly lower than domestic demand.

Anton Löf PO Box 3127 SE-169 03 Solna, Sweden [email protected] Tel: +46-8-744 00 65 Fax: +46-8-744 0066

www.rmg.se www.intierrarmg.se

Thank you !

NIckel drawing: Kaianders Sempler.

Metals first isolated in

Sweden/Finland

Please visit www.rmg.se

Related Documents